D

D

e

e

p

p

r

r

e

e

c

c

i

i

a

a

t

t

i

i

o

o

n

n

Frequently Asked Questions

[1]

Can I deduct the cost of the equipment that I buy to use in my business?

[2]

Are there any other capital assets besides equipment that can be depreciated?

[3]

Can I depreciate the cost of land?

[4]

How do I depreciate a capital asset (like a car) that I use for both business and personal?

[5]

If I owe money on an asset, can I still depreciate it?

[6]

Can I claim depreciation on equipment that I rent or lease for my business?

[7]

I have owned a building for several years and made major improvements to it this year. Can I deduct

the cost of those improvements?

[8]

What information do I need to compute depreciation on my capital assets?

[9]

What is basis?

[10]

What is class life?

[11]

Why is the term "placed in service" important?

[12]

What method of depreciation should I use?

[13]

How does the month I place my equipment in service affect my depreciation computation?

[14]

Does the month I place my building in service affect my depreciation computation?

[15]

Is there any exception to the general rule that costs of property must be depreciated?

[16]

Are there any limitations on the amount of depreciation I can claim in one year?

[17]

Can I claim depreciation on my business vehicle if I use the standard mileage rate?

[18]

How do I claim depreciation on my tax return?

[1] Can I deduct the cost of the equipment that I buy to use in my business?

Equipment is considered a capital asset. You can deduct the cost of a capital asset, but not all at once. The general

rule is that you depreciate the asset by deducting a portion of the cost on your tax return over several years. See

Question 15 for an exception to this general rule.

Return to top

[2] Are there any other capital assets besides equipment that can be depreciated?

There are several types of capital assets that can be depreciated when you use them in your business. For example:

•

Real Property-

buildings or anything else built on or attached to land

•

Personal Property –

cars, trucks, equipment, furniture, or almost anything that isn't "real

property"

Return to top

[3] Can I depreciate the cost of land?

Land can never be depreciated. Since land cannot be depreciated, you need to allocate the original purchase

price between land and building. You can use the property tax assessor's values to compute a ratio of the

value of the land to the building.

Example:

Ryan bought an office building for $100,000. The property tax statement shows:

Improvements $60,000 75%

Land $20,000 25%

Total Value $80,000 100%

Multiply the purchase price ($100,000) by 25% to get a land value of $25,000. You can depreciate your $75,000

basis in the building using the mid-month MACRS tables.

Return to top

[4] How do I depreciate a capital asset (like a car) that I use for both business and personal?

Only the business portion of the asset can be depreciated on your tax return. For example, if you use your car

60% for business use, depreciation can be claimed on 60% of the cost.

Return to top

[5] If I owe money on an asset, can I still depreciate it?

Yes, as long as you are responsible for making payments on the asset, you can take a depreciation deduction.

Return to top

[6] Can I claim depreciation on equipment that I rent or lease for my business?

If you are renting or leasing an asset, you can deduct your monthly rent/lease costs as an expense. Usually

only the owner can depreciate a capital asset.

Return to top

[7] I have owned a building for several years and made major improvements to it this year. Can I

deduct the cost of those improvements?

The cost of major improvements is not deductible all in one year. They must be capitalized and depreciated.

The total improvements you made this year are handled as though you purchased a new building. You would

recover the cost of the improvement using the depreciation methods in effect for the tax year you made them.

Return to top

[8] What information do I need to compute depreciation on my capital assets?

You need the following information to compute depreciation:

•Basis

•Class Life

• Placed in Service

• Method of Depreciation

Return to top

[9] What is basis?

Basis is your original cost in the asset, including sales tax, freight and installation. The cost of the property

includes:

•Cash

• The amount of money borrowed to purchase the asset

• The value of any items you traded for the new asset

• The value of bartered services

Your basis will increase by the amount of major improvements you make to the property and will decrease by

the amount of depreciation deductions you take on your tax return. This adjusted basis is used to measure

your gain or loss when you sell the property.

Example:

Adam bought a bulldozer from a local contractor for $6,000. He paid $2,000 in cash, borrowed $3,000 from the

bank, and agreed to dig the foundation for the seller’s lake cabin. Adam’s basis is $6,000. Note: Adam will also

include $1,000 in income in the year he digs the foundation.

Cash $2,000

Loan $3,000

Services $1,000

Total $6,000

Return to top

[10] What is class life?

Class life is the number of years over which an asset can be depreciated. The tax law has defined a specific

class life for each type of asset. Real Property is 39 year property, office furniture is 7 year property and

autos and trucks are 5 year property. See Publication 946, How to Depreciate Property.

Return to top

[11] Why is the term "placed in service" important?

Property is placed in service when it is ready and available for use in your business even if you have not

begun using it. This date determines when you can begin to depreciate the asset.

Return to top

[12] What method of depreciation should I use?

The method used by most taxpayers is the Modified Accelerated Cost Recovery System (MACRS). MACRS

provides a uniform method for all taxpayers to compute the depreciation. Using the basis, class life, and the

MACRS tables, you can compute the deduction for each asset in the year it is placed in service and each

subsequent year of its class life. See Publication 946, How to Depreciate Property.

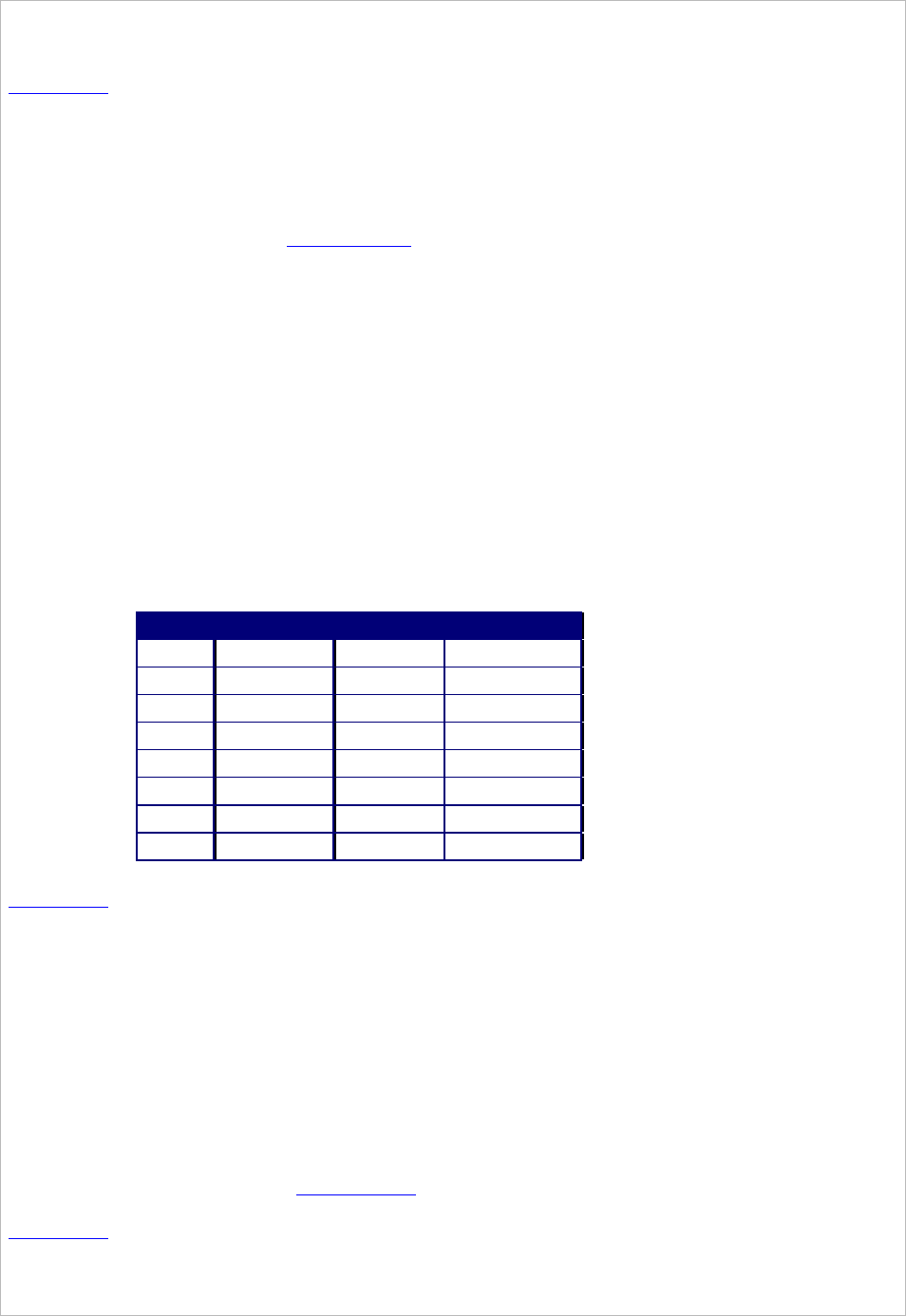

Example:

Shawn bought and placed in service a used pickup for $15,000 on March 5, 1998. The pickup has a 5 year class

life. His depreciation deduction for each year is computed in the following table.

Year Cost x MACRS % Depreciation

1998 $15,000 x 20.00% $3,000

1999 $15,000 x 32.00% $4,800

2000 $15,000 x 19.20% $2,880

2001 $15,000 x 11.52% $2,880

2002 $15,000 x 11.52% $2,880

2003 $15,000 x 5.76% $ 864

Total $15,000

MACRS Percentage Table

Year 3 Year 5 Year 7 Year

1 33.33% 20.00% 14.29%

2 44.45% 32.00% 24.49%

3 14.81% 19.20% 17.49%

4 7.41% 11.52% 12.49%

5 11.52% 8.93%

6 5.76% 8.92%

7 8.93%

8 4.46%

Return to top

[13] How does the month I place my equipment in service affect my depreciation computation?

MACRS assumes all

personal property

is purchased and placed in service in the middle of the year. This is

called the half-year convention. The example in Question 12 and the MACRS percentage table above show

how to compute depreciation using the half-year convention.

There is an exception to the half-year convention. If more than 40% of your newly purchased

personal

property

is placed in service during the last 3 months of a year, then you should use the mid-quarter

convention. The mid-quarter convention tables start your depreciation in the quarter that you placed the asset

in service. The mid-quarter convention reduces the amount of the depreciation for the year because you are

only using the property for a short period of time. If you are required to use the mid-quarter convention,

those MACRS tables can be found in Publication 946, How to Depreciate Property.

Return to top

[14] Does the month I place my building in service affect my depreciation computation?

Depreciation on

real property,

like an office building, begins in the month the building is placed in service.

This is called the mid-month convention. In most cases, when you buy a building, the purchase price

includes the cost of both the land and the building. Since land cannot be depreciated, you need to identify the

portion of the original purchase price that relates to land. You can use the property tax assessor's values to

compute a ratio of the value of the land to the building. The MACRS tables for mid-month convention are in

Publication 946, How to Depreciate Property.

Example:

Ryan bought an office building for $100,000. The property tax statement shows :

Improvements $60,000 75%

Land $20,000 25%

Total Value $80,000 100%

Multiply the purchase price ($100,000) by 25% to get a land value of $25,000. You can depreciate your $75,000

basis in the building using the mid-month MACRS tables.

Return to top

[15] Is there any exception to the general rule that costs of property must be depreciated?

This exception is called

Section 179 Deduction.

You can choose to take an immediate deduction for some

personal property that you would otherwise depreciate over several years. You must make this election in the

year that you placed the property in service using Form 4562, Depreciation and Amortization. You cannot

take this special deduction on property you've previously used personally and then converted to business use.

This deduction is limited to your wages and net business income. There is also a maximum dollar limit,

which changes from year to year. The maximum dollar limitation is printed on Form 4562 every year. If you

can't use all of the

Section 179 Deduction

because of the income limit, you can carry the unused deduction

over to the next tax year.

Example:

Mark purchased a piece of equipment for $30,000 in 1998. On his 1998 tax return he could choose to take an

additional

depreciation deduction up to $17,500. Mark’s total business net profit for 1998 was $12,000. His

additional

first year deduction would be limited to $12,000. If he elects the full $17,500, the unused $5,500

($17,500-$12,000) will be carried over to 1999.

Return to top

[16] Are there any limitations on the amount of depreciation I can claim in one year?

There are not any overall limitations on yearly depreciation. However, if an asset is considered

Listed

Property

, your annual deduction is limited. Listed property is a term for business assets that are often used

for personal purposes. Under the MACRS rules, depreciation is limited for listed property, such as:

• Vehicles that weigh 6,000 or less

• Other property used for transportation (pick-ups, airplanes, buses, boats, motorcycles, etc.)

• Property used for entertainment, recreation, or amusement (video recorders, stereo equipment,

photographic equipment, etc.)

• Computer and related equipment unless used at a regular place of business

• Cellular telephones

Return to top

[17] Can I claim depreciation on my business vehicle if I use the standard mileage rate?

The standard mileage rate covers all the expenses of operating your vehicle. Therefore you do not claim

depreciation seperately. However, if you use the actual expense method (see the Travel and Entertainment

FAQ's) to compute your vehicle expenses, you will be allowed to claim depreciation.

Example:

Dianne uses her Corvette in her business. She took odometer reading at the beginning and end of the year. The total

miles for the year were 12,000. She kept a log to record her business miles. The car cost $64,000.

Business Miles 7,000

Total Miles 12,000

Business Percentage (7000/12000) 58%

Original Cost $64,000

Business Use Percentage 58%

Basis to be Depreciated $37,334

MACRS percentage 20%

Maximum MACRS Depreciation $ 7,467

Maximum Vehicle Depreciation (see Publication

946)

$ 3,160

Business Use Percentage 58%

Limited Vehicle Depreciation $1,843

Dianne compares the maximum MACRS depreciation with the limited vehicle depreciation. She can deduct the

smaller of the two which is $1,843.

Return to top

[18] How do I claim depreciation on my tax return?

You must complete and attach Form 4562 to your tax return if you are claiming any of the following:

• A Section 179 deduction for the current year or a Section 179 carryover deduction from a prior

year

• Depreciation for property placed in service during the current year

• Depreciaiton on any vehicle or other listed property, regardless of when it was placed in service

Return to top