YBL/CS/2023-24/039

Date: June 11, 2023

National Stock Exchange of India

Limited Exchange Plaza, Plot no. C/1, G

Block, Bandra - Kurla Complex Bandra

(E), Mumbai - 400 051 Tel.: 2659 8235/36

8458

NSE Symbol: YESBANK

BSE Limited

Corporate Relations Department

P.J. Towers, Dalal Street

Mumbai – 400 001

Tel.: 2272 8013/15/58/8307

BSE Scrip Code: 532648

Dear Sir / Madam,

Sub.: Submission of Investor Presentation

Ref.: Reg. 30 and other applicable provisions of SEBI (Listing Obligations and Disclosure

Requirements) Regulations, 2015

Please find attached the copy of Investor Presentation.

We request you to take above on your record and disseminate to all concerned.

Thanking you,

Yours faithfully

For YES BANK LIMITED

Shivanand R. Shettigar

Company Secretary

Encl: A/a

SHIVANAND

RAMA

SHETTIGAR

Digitally signed by

SHIVANAND RAMA

SHETTIGAR

Date: 2023.06.11

20:25:36 +05'30'

YES BANK – Investor Presentation

June 2023

Contents

YES BANK of Today 3-6

YES BANK Franchise 8-28

ESG Led Responsible Banking

New Age Digital Platform

Universal Bank – One Bank For All Needs

Governance and Senior Management Team

Shareholding

Financials 30-43

New Generation, Professionally Run, Private Sector

Bank with a Scalable Platform

4

Seasoned Human

Capital

▪ Run by a professional, seasoned, and stable management team; average vintage of YES BANK Top and Senior Management Team

of 8.5 Years; Duly supported by 27,000+ YES BANKers

▪ Fostering diversity, learning, inclusion and growth - certified as Top 50 Great Place To Work (2023) in BFSI Category

3

Geared for Scale

with Profitability

▪ Strong Foundation; Key levers, now in place, for scale-up and material improvement in profitability

• Retail Advances at INR 90,000 Crs (~45% of Net Advances) – focus shifting towards further improving the profitability

• A ‘Preferred Retail Franchise’ with strong Customer Acquisition run-rate of more than a 1.3 million new CASA customers per annum

• Fortified Balance Sheet - Holistically addressed Legacy Asset Quality Issues; Portfolio Asset Quality at its best since reconstruction

o Mar’23 NNPA at 0.8%,

o Collective NNPA & Net Carrying Value of SR at 2.4%

• Sufficiency in Liquidity (LCR at 118.5%

1

) and Capital Adequacy (CET I% at 13.3%)

2

Robust Risk,

Governance and

Compliance Culture

▪ Eminent 13-member Board of Directors comprising 7 independent directors, 3 women directors – domain specialists with extensive

strategic, operational and leadership experience

▪ Comprehensive and Robust Risk Management Framework; De-Centralization of Credit Approval Process

▪ ‘Compliance First’ Culture

1

New Generation

Private Sector Bank

▪ 6th Largest Private Sector, Universal Bank offering comprehensive suite of product and services via its pan India network of 1,192

branches, 150 BCBO and 1,300+ ATMs in over 300 districts of India

▪ Accelerating as a granular retail franchise with leadership in digital payments and strong focus on transaction banking

▪ Preferred Banker to Digital India with best-in-class technology / API stack

▪ ESG Led Franchise - reflected in the highest rankings by S&P Global, CDP ratings and Moody’s ESG and sustainability ratings

Total Assets:

INR 3,54,786 Crs

Total Deposits:

INR 2,17,502 Crs

Total Advances:

INR 2,03,269 Crs

Advances Split:

Retail – 45% | SME – 14%

Medium Ent. – 14% | Corporate – 27%

5

Major Shareholders

• SBI, the largest schedule commercial bank of India, 7 leading private sector banks and a leading NBFC

• Two global, marquee, private equity investors viz. Carlyle and Advent International

• Largest retail shareholder base in Indian Capital markets, with more than 50 lakh shareholders

1. Average for the quarter- Q4FY23

3

Senior Rating - At A-

Short Term Rating – Highest at A1+

24%

30%

36%

45%

13%

12%

13%

14%

8%

9%

11%

14%

56%

49%

40%

27%

03/20 03/21 03/22 03/23

Retail SME Mid Corporate Corporate

17.5%

14.2%

12.0%

FY21 FY22 FY23

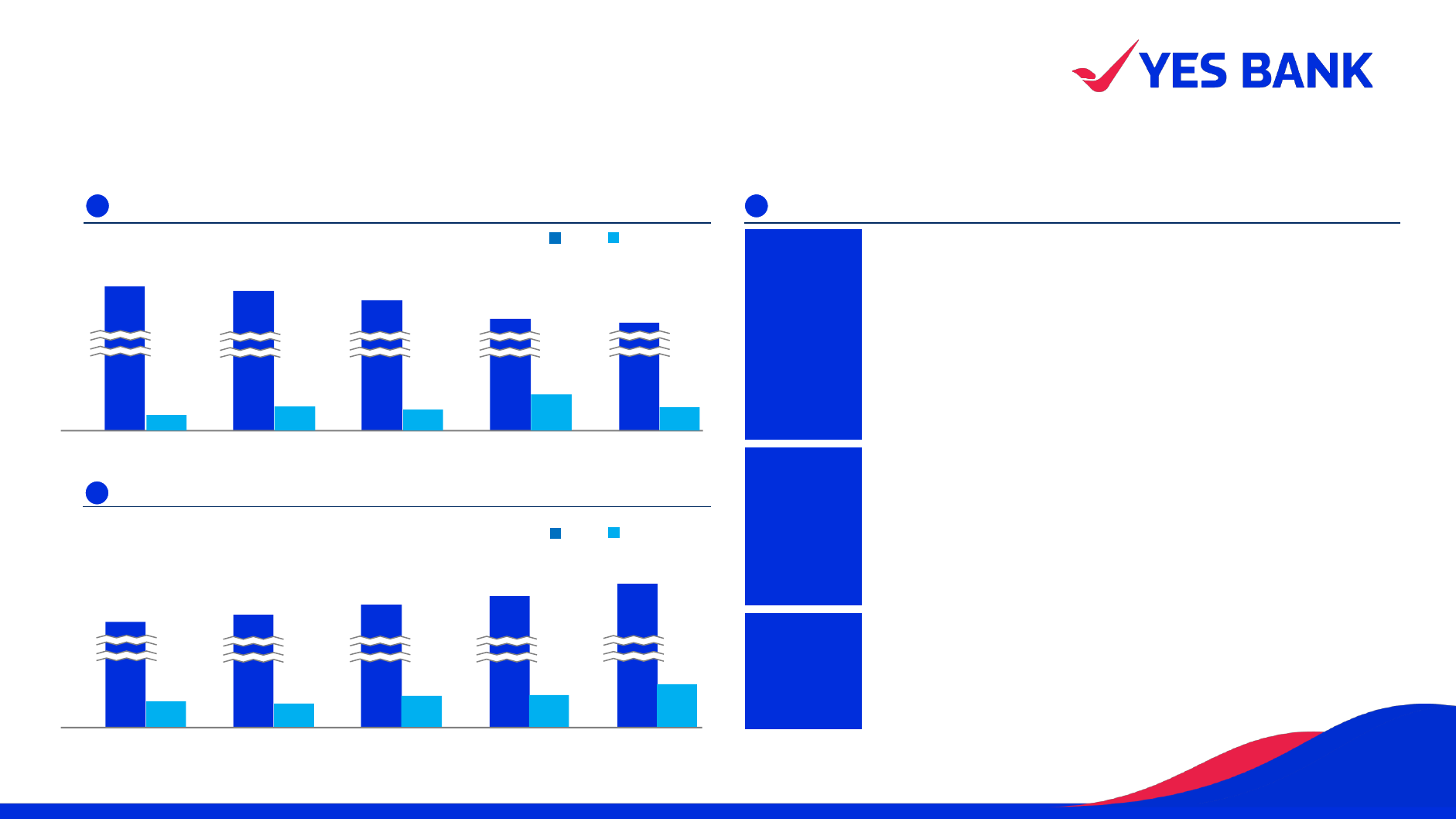

Strategic Shift towards a Granular Franchise

Strong 2.2x growth in Retail Advances between Mar’20 to Mar’23 I Retail, SME and Mid-Corporate Segment Advances at ~INR 146,215 Crore and at ~73% of Net Advances

1

171,443 200,201

INR Crores Mar’20 Mar’23 Growth

Retail Advances 40,755 90,477 2.2X

Share in Total Advances 24% 45% 1.9X

Retail Advances - Growth and Change in Mix

Strong Growth

Engines

Growth

(Mar’23 /

Mar’20)

Mix

(Mar’23)

1

Avg. ticket

size

Mortgage Loan 2.1x 33% 0.35-0.40

Auto Loan 1.7x 18% 0.09-0.10

Consumer Loan 2.8x 23% 0.05-0.06

Commercial Loans 1.7x 23% 0.25-0.30

Diversified Retail Advances BookNet Advances Growth Led by Retail Advances

Steady Granular Deposit Accretion – Higher Focus on CA and Improving SA Granularity I Reducing Share of Top 20 Depositors

2

34,971

35,558

34,673

34,878

33,300

64%

63%

65%

68%

72%

69%

68%

71%

75%

78%

35%

40%

45%

50%

55%

60%

65%

70%

75%

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q4FY22 Q1 FY 23 Q2 FY 23 Q3 FY 23 Q4 FY 23

Total SA (INR Crore) SA - Up to INR 2 Crores SA - Up to INR 5 Crores

Strong Accretion in Lower Value Buckets in SADeposits Grew ~2.1x Since Reconstruction Amidst Difficult Backdrop

Focus on Growing CA

Share of Top 20 Depositors

9,499

18,997

26,389

33,603

Mar'20 Mar'21 Mar'22 Mar'23

1

Residual consists of Inorganic

105,364

162,947

197,192

217,502

26.6%

26.1%

31.1%

30.8%

9.0%

11.7%

13.4%

15.4%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

Mar'20 Mar'21 Mar'22 Mar'23

Total Deposits CASA Ratio (RHS) CA Ratio (RHS)

All figures in INR Crs

4

5,782

7,290

6,120

Mar'21 Mar'22 Mar'23

Recoveries and Upgrades

13,703

5,747

4,792

8.2%

3.2%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,00 0

16,000

FY21 FY22 FY23

31-90 Days Overdue % of Net Advances (RHS)

Fortified Balance Sheet - Marked Improvement in Asset

Quality

0.9%

0.9%

0.3%

1.6%

5.0%

5.9%

4.5%

0.8%

5.9%

6.8%

4.8%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Mar'20 Mar'21 Mar'22 Mar'23

Net Carrying Value of SRs Net NPA Ratio

Both i) Net NPA and ii) Net NPA + Net carrying Value of SRs,

consistently trending lower

1

Strong Past Trend of Recoveries & Upgrades of INR ~20,000 Crores

since Reconstruction (INR Crores)

2

Significant Improvement in all 31-90 Days Overdue Loans (INR Crores)

3

12,035 5,795 4,775

7.1%

3.3%

2.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY21 FY22 FY23

Gross Slippages % of Avg. Advances

Gross Slippages continues to trend lower

4

All figures in INR Crs

Pro-forma Incremental

Ageing Related

Provisioning

1

In FY24E ~0.8%

In FY25E ~1.0%

In FY26E ~0.4%

1. Any recoveries / upgrades in the interim will lower the aforesaid ageing related impact on credit cost; balance ageing provisions spill over beyond FY26

5

Protected PPOP/ Assets during the strategic shift

towards Granular Franchise through Efficiency Gains

1.0%

0.9%

0.9%

FY21 FY22 FY23

PPOP/ Assets

2

50

167

77

163

65

181

95

197

90

201

115

218

Retail Advances Bank Advances Retail Deposits Bank Deposits

FY21 FY22 FY23

All figures in INR ‘000 Crs

1

Based on Internal Business Segmentation and may not match with regulatory definitions

2

Normalised PPOP excluding Interest Recoveries from NPA in NII and realised/ unrealised gain on Investments in Non-Interest Income; for FY21 PPOP incorporates accounting changes

made in Q2 FY22 to align with the RBI Circular dated August 30, 2021 and other one-offs during the year

Significant investments into the Retail franchise over past few years in order

to organically build a sustainable franchise that delivers profitable growth

1

1

Efficiency gains in the Retail franchise has aided this strategic shift in mix- resulting

in stable PPOP/ Assets

2

Strategic levers to further improve core Operating Profitability through disciplined execution

Enhanced focus on

growth in CA and

granularity in SA

Further increase in

Retail Mix with

calibrated Yield

Enhancement

Stronger Fee

growth through

Cross sell and

Transaction

banking

Addressing RIDF/

PSL drag through

organic and

inorganic solutions

Operating Leverage

+ Productivity

Improvement via

Digitization

6

Contents

YES BANK of Today 3-6

YES BANK Franchise 8-28

ESG Led Responsible Banking

New Age Digital Platform

Universal Bank – One Bank For All Needs

Governance and Senior Management Team

Shareholding

Financials 30-43

s

Balance:

Sustainability

& Profitability

Balance:

Sustainability

& Profitability

Building

Resilience

against ESG risk

Capitalizing on

Sustainable Finance

opportunities

Key Highlights

First Bank globally with an ISO 14001:2015

certified Environmental Management System

covering 832 facilities

First Indian Bank to measure and report

financed emissions of its electricity

generation loan exposure and develop targets

to align with SBTi well-below 2°C scenario

Mobilized green and social finance towards

renewable energy, electric vehicles, SMEs,

rural farmers and women entrepreneurs

First Indian Bank to be a Founding

Signatory to UNEP FI Principles for

Responsible Banking and to sign the

Commitment to Climate Action, striving to

align its business strategy with the Paris

Climate Agreement

8

S&P Global

Highest ESG score

amongst Indian banks in

the S&P Global Corporate

Sustainability Assessment

(CSA) 2022

CDP

Rated ‘A-’ for its 2022

Climate Change

disclosures - highest

rated Indian Bank. Only

Bank amongst 16 Indian

companies in Leadership

band (A and A-)

Moody’s ESG

Solutions

Ranked 5th in ESG,

amongst 90 Retail &

Specialized Banks in

Emerging Markets

Launched India’s first Green Bond and first Green Fixed Deposit

5

Promoting sustainable finance

Associated with the Task Force on Sustainable Finance (constituted by

the Department of Economic Affairs, Ministry of Finance, Government of

India) as a co-lead of the work stream ‘Building Resilience in the Financial

Sector’

4

Engaging stakeholders

Instituted an Environment and Social Risk Management System (ESMS)

to integrate E&S risks into overall credit risk assessment framework

1

Addressing Climate & ESG Risk

Committed to reduce greenhouse gas (GHG) emissions from operations

to net zero by 2030. Switched to renewable energy at the Bank’s

headquarters, YES BANK House

2

Net zero by 2030

Board – level CSR and ESG committee; Executive – level Sustainability

Council led by MD &CEO

ESG-linked KPIs for Top Management

Enhanced sustainability disclosures aligned to GRI and Taskforce on

Climate-related Financial Disclosures (TCFD) recommendations

3

Enhancing governance & disclosures

Responsible franchise committed to a purposeful ESG

agenda

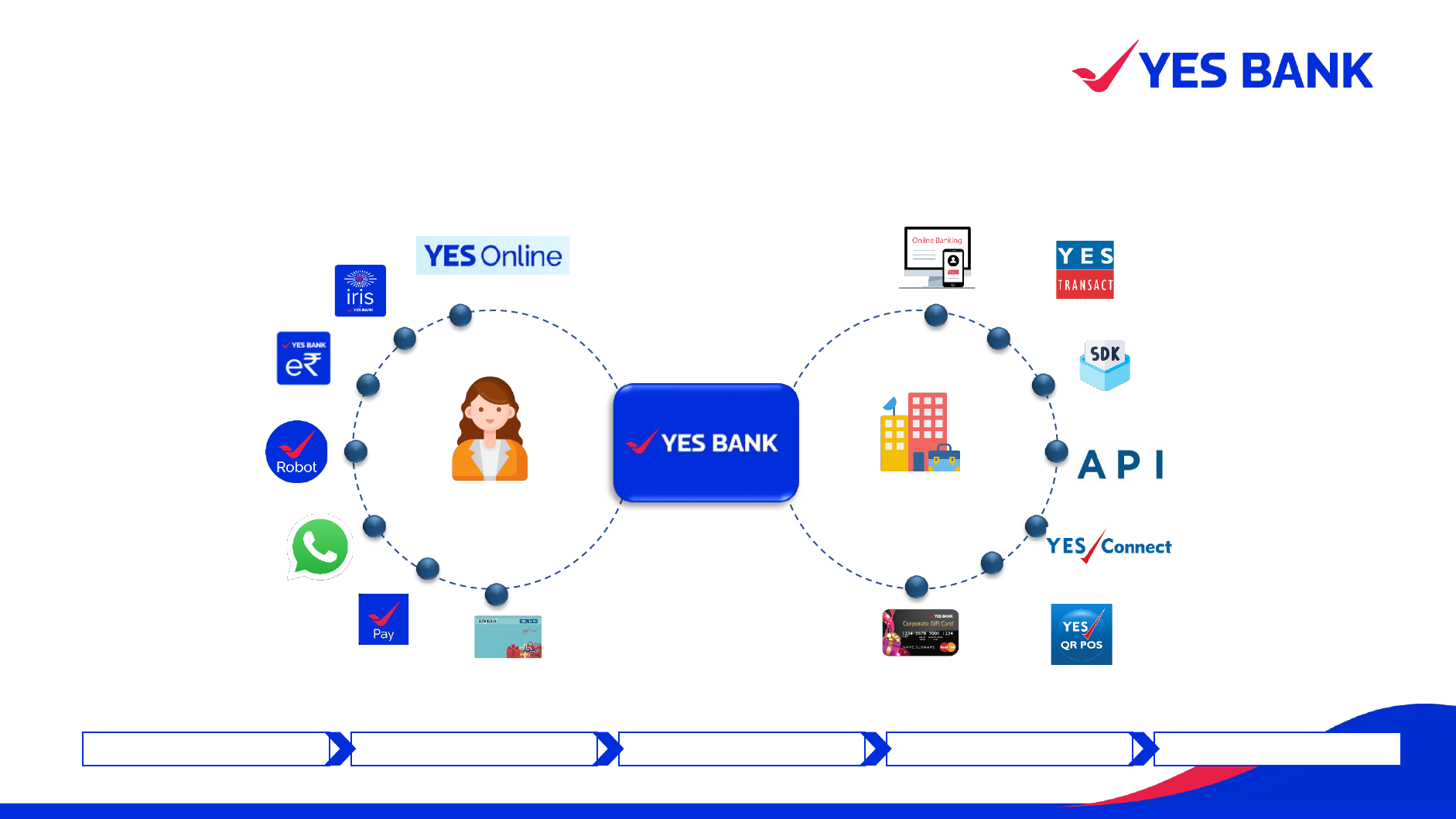

Digital & Transaction Banking:

Sustainable & Granular Revenues through Digital Payments, Trade Finance & Cash

Management

PPI @ Product Penetration Index, FB @ Fund Book, NFB @ Non-Fund Book, EXIM @ Export & Import, TBG @ Transaction Banking Group, DB @ Digital Banking

Superior

Service

90% of our Corporate CASA clients is covered by dedicated

Service Team, with query resolution at 93% First Time Right with

92% TAT adherence

~100,000 client queries addressed

successfully by our Corporate Client

Management team

TBG -Corporate Client Mgmt.

(CCM) unit is now ISO 9001: 2015

Certified

Digital Payments | Trade Finance | Cash Management | Capital Markets | Custody | Bullion & Currency | Remittances | Supply Chain

Product

Leadership

Market Leadership – YBL processes 1 in 3 Digital Payment transaction in India

UPI - 40% Rank #1 | NEFT - 18% Rank #1 | IMPS -11% | NACH – 6% | AePS – 21%

28x in YesMoney, 3x in YesOnline and 4x in IRIS –YesMobile growth in

Transaction Value in last 3 years

Corporate Cash Management Thruput has grown by 3x in last 3 years

98% of our Cash Management thruput comes from Digital modes

Digital Smart Trade Platform platform saw 20% YoY growth by volume

Corporate Trade Non-Fund & Fund Book has increased by 27% and

Supply Chain Book increased by 54% in last 3 years

Strengthenin

g Franchise

2+ PPI* in Corporates covers 82% CA, 97% CMS Thruput, 95% Trade

FB*, 88% Trade NFB* & 96% EXIM* flows

95% of our Corporate CASA is embedded with Digital & Transaction

Banking Product & Solutions

70% of all Lending Clients have 2+ TBG & DB Product Embedment

TBG led FX income has increased by 75% in last 3 years

9x growth in UPI, 8X growth in IMPS, 2.5x growth in AePS, 16x growth in

BBPS in last 3 years

93% growth in TBG* Managed CA, 22% growth in Trade NFB and 63%

growth in Digital & Transaction Banking Fees in last 3 years

9

Curated & Expansive Digital Offerings

Enriched customer experience across all customer segments

10

Source Digital Onboard Digital Transact Digital Service Digital Monitor Digital

Prepaid Instruments (PPI)

Corporate PPI Cards to Manage

Expenses

Prepaid Instruments (PPI)

Wallets /Travel / GIFT / Expense

Cards

Retail

Individuals

Corporate

and SMEs

Yes Robot –

24x7 personalized AI

powered Chatbot

Digital Rupee

CBDC Wallet for Individual

Customers

Yes Online -

Revamped, Simplified and Futuristic

Net Banking Service

IRIS – (Mobile Platform)

Revamped, Intuitive, Futuristic Super

APP in making

Whatsapp Banking –

Convenient, secure inquiry &

transacting Banking Channel

Yes Pay (BaaP) –

Digital Payment Super APP

Corporate & MSME Banking

Revamped, Simplified and Futuristic

Net Banking Service

API Banking (BaaS)

Expansive and growing API Banking

Services for New Age Businesses

Embeded Banking (BaaS)

SDKs to provide seamless Digital

experience for SuperApps /

NeoBanks and Fintechs.

Smart Trade

Digital Online Trade Platform for

Corporate and SMEs

Yes Connect (BaaP)

Corporate Super APP with Yes Bank

and partner Services

Merchant Collection

POS, QR Code (UPI / CBDC), Cash &

Cheque Solutions for Merchants and

Retailers for Digital Collections

Enriched customer experience – IRIS

SuperAPP for Retail Customers

11

▪ IRIS is a cloud native API-led mobile platform offering banking on fingertips across customer lifecycle

▪ Leveraging 30% mobile native consumers + Digital India stack to build a highly scalable and low C2I digital business model

Key Differentiators

▪ India’s first banking app

built on co-creation

▪ Simple & intuitive design

▪ Significantly enhanced

and superior banking

experience with

acquisition & onboarding

journeys

▪ Complete customer

lifecycle with hyper-

personalized financial

experiences

Products & Features Snapshot

Live on IRIS

Customer Lifecycle

NTB

Acquisition

Onboarding Cross-sell Services Transactions Value added

experiences

Credit Cards

Wealth &

Protection

Financial Planner Insurance

Personal Loans

Growth

Mutual Fund Auto Loans

UPI/ Fund

transfer

Payments

Remittances Bill Payments

Savings account

Savings

Deposits Spend Analyzer

ONDC

Experiences

IRIS gold club Service Bot

Promising green shoots in CUG

– To be launched soon

1.2 lac active users within 4 few months of CUG launch

(78% of required base)

Targeting 30% of new digital acquisition of the

bank

Exchange Houses

Manufacturers

MSME

FinTechs

Pharma

NBFCs

Co-operative

Banks

Hospitality

Others..

Traders

Hospital

Education

Solutions

Public Digital Infra -

ONDC, CBDC, ULIP etc

Cardless cash

withdrawal

Payments (FT2/IMPS)

Prepaid issuance &

Management

Card Solution Mgmt.

Smart

Collections

Trade Finance

Services

Supply Chain Business

Merchant acquiring

YES Bank &

Partner

Stack

Digital KYC

Payment Aggregator

Services

Digital Loan Mgmt.

Expense Mgmt.

E-Invoicing

Remittances

Neo Bank services

ERP Integration

Statutory Payments

Digital KYC &

Due-diligence

& Many Others

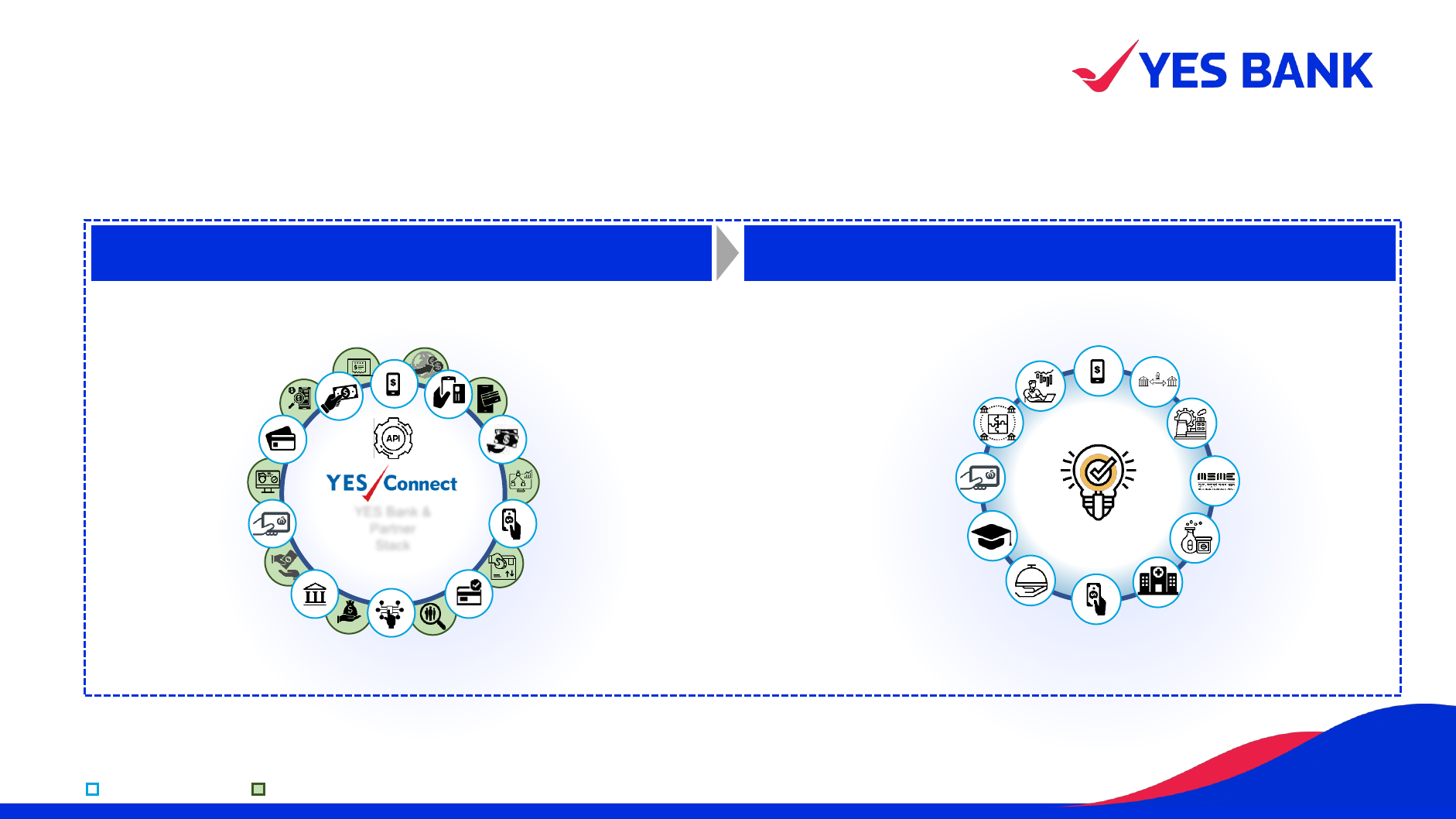

Enriched customer experience – YES Connect

Super App for Businesses

12

API’fication of our Marketplace model

(YES Bank + Partner Offerings)

Sachetization of Solutions across Industry Segments

YES Bank Services Partner Services

Embedded (Connected) Banking

Digitizing client journeys and creating inorganic client acquisition funnel thru

Fintech partnerships

13

Partnership roadmap of Digital & Transaction Banking

Source Digital Onboard Digital Transact Digital Service Digital Monitor Digital

▪ Digital Acquisition at Scale

thru Partnerships – CA-SA

accounts, Supply Chain,

Cards, Retail Assets, etc

▪ Digital Client Onboarding &

Product Setups

▪ Digital a/c Opening

▪ with Instant a/c Operations

▪ API’fication of all Bank Products

▪ Create STP journeys for Liability

& Asset products

▪ FinTech Partnership &

integration

▪ Digital tools for FTR query

resolution at low cost model

▪ Data led Service resolution

▪ Digitalized reporting & MIS

▪ End-to-end digital Sales force

▪ Digitalized Compliance, FRM,

AML

FY'21 FY'22 FY'23 YTD

450+

API Stack

30+

FinTech Partnerships

Future ready for both

BaaS & BaaP Models

New To Bank Clients Thruput in Cr

Connected Banking creating a Digital Acquisition funnel

85%

Yearly Run-rate Yearly Run-rate

200%

50+ Large Strategic

Partnerships in Pipeline

FY'21 FY'22 FY'23 YTD

FY’23FY’22FY’21 FY’23FY’22FY’21

Current

Account

X-border

remittance

Investment

Credit

Cards

FX Cards

Commercial

Card

Deposits

Personal

Loan

Saving

Account

Business

Loan

Working

Capital Loan

Supply Chain

Loan against

Securities

Quantum Force Multiplier for Inorganic Client Acquisition across…

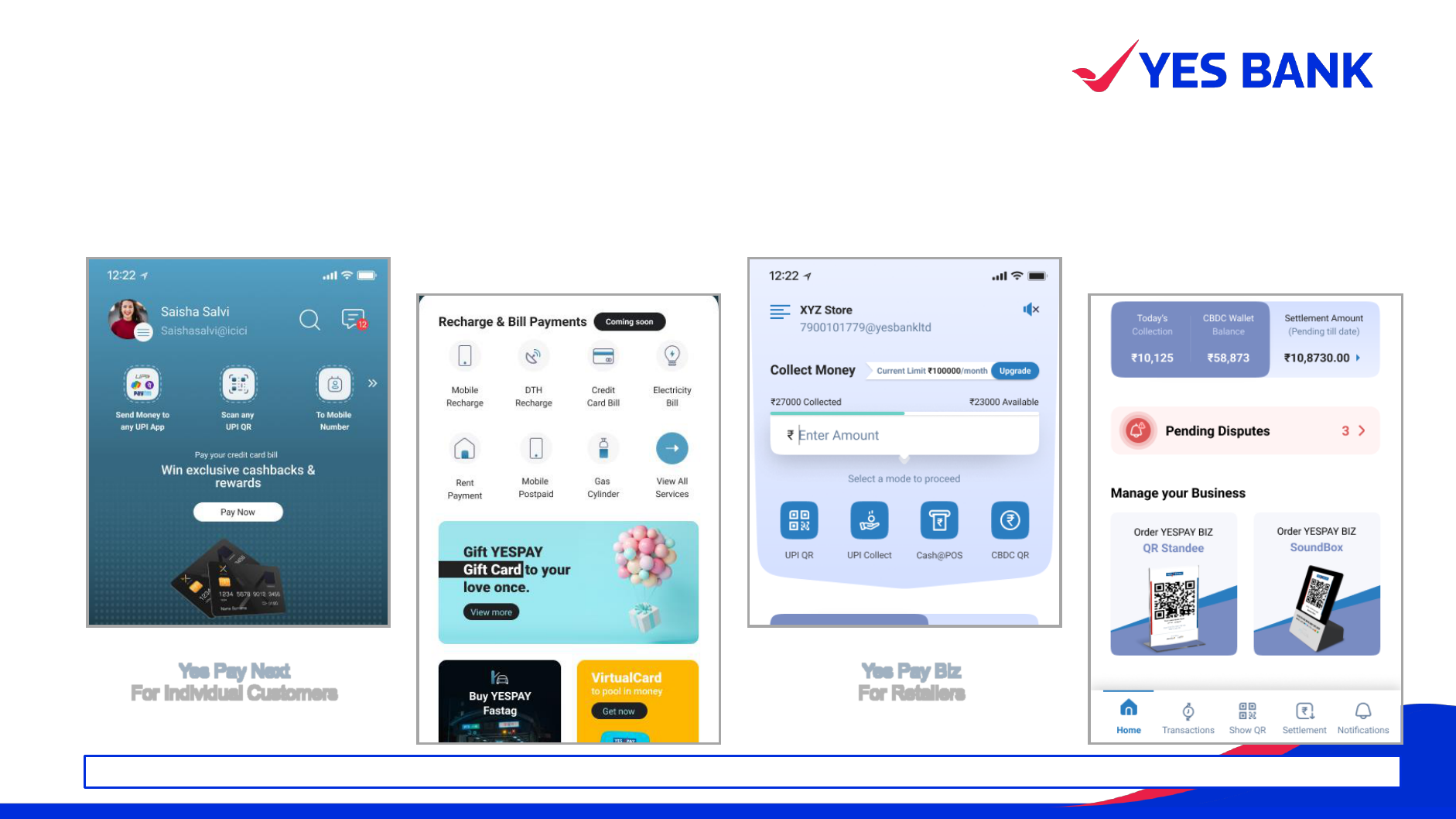

Yes Pay

Open Market “Payments Super App” for Retail individual & merchants

14

One-stop mobile applications to seamlessly manage all domestic payment (Wallets, UPI, Bills, Digital Card & POS, Transit

Yes Pay Biz | Yes Pay Lite | Yes Pay Next

Creating a curated database & funnel for targeted NTB client acquisition

Yes Pay Next

For Individual Customers

Yes Pay Biz

For Retailers

Pioneer in leveraging Public Digital Infrastructure

Contributing to building new-age India through collaboration on Key Digital Initiatives

Government

Digital

Ecosystem

Open Network for Digital

Network (ONDC)

Open Credit Enablement

Network (OCEN)

Account Aggregator (AA)

Unified Logistics Interface

Platform(ULIP)

Regulatory Sandbox

Central Bank Digital

Currency (CBDC)

Digital Initiatives

YES Differentiators

Enables Digital Onboarding

Digital Cash flow financing

Leverage Market Ecosystem

Efficient Cash Management

Data Driven Solutioning

Enabling Cross-Boarder Payments

Principle Objectives

Consent Layer for Data sharing system making

lending and wealth management faster

An initiative of the government to democratize

digital commerce built on Beckon protocol

Creating a common language for collaboration

and partnership with lending service providers

(LSPs)

Continuous innovation and engagement for

the evolving BFSI sector

Democratizing logistical information to

augment supply chain

Sovereign digital Currency

CBDC W- Pilot G-Sec,

CBDC R- eRupee wallet

YES BANK Joins ONDC Pilot

Transaction at VARAHI Limited, with

Seller APP

YES BANK - 1st Bank to partner with

GOI for development of different uses

cases, at Launch of ULIP, New Delhi

YES BANK launches 1

st

CBDC Pilot

Transaction at Reliance Retail Outlet,

Mumbai

15

Retail Bank:

Full spectrum retail bank growing with strong momentum

572

490

586

675

838

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

65,250

71,506

78,400

83,769

90,447

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

121,535

119,960

124,346

127,134

128,948

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

Pan-India

presence via 1,192

branches, 150 BC

banking outlets

and 1,301 ATMs,

CRM’s & BNA’s

Leadership /

significant share

in payment and

digital

businesses

(UPI, AEPS, DMT)

Cater to all

customer

segments (HNI,

affluent, NRIs,

mass, rural and

inclusive banking)

with full product

suite

Advanced score-

cards and analytics

being leveraged

across underwriting

and engagement

~90% of

transactions via

digital channels

56% of branches in

Top 200 deposit

centers

+39% p.a.

+6% Y-o-Y

Strong growth in Retail Advances

…along with growth in CASA and Retail Term Deposits

In addition, continued momentum within Retail Fee Income

45%

36% 38% 41%

As % of total

advances

60%

62% 62%

As % of total

deposits

All figures in INR Crs

Highest Ever

44%

62%

Highest Ever

59%

16

96.7%

96.9%

97.2% 97.2%

97.5%

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

16%

16%

16%

15%

12%

7%

4%

4%

2%

2%

6%

Secured Business Loans

Auto Loans

Personal Loans

Home Loans

Commercial Vehicle Loans

Construction Equipment Loans

Credit Cards

Rural Banking

Business Loans

10,201

11,863

12,563

12,667

12,705

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

Highest Ever

17

1

Split basis gross retail advances

1

Retail asset disbursements momentum continues Diversified retail book

1

3

Preferred financier status

with leading Auto OEMs

On the back of purposeful digital investments

2

▪ Expanded Product offerings through launch of

Education Loan

▪ Loan in seconds (LIS) platform and front-end

automation initiatives (Yes Robot) have resulted in

lower TAT along with higher productivity

▪ Adopted the account aggregator ecosystem as FIU

/ FIP to capitalize on consent layer of India stack

▪ Sales Force implementation helping in process

improvement and customer delight

▪ Pre-qualified Gold Loan OD for existing customers

24x7 digital process

Strong focus on book quality & collections

4

▪ High share of secured loans in Retail Assets book - 80%, with healthy LTV ratios:

– Avg. LTV for Affordable Home Loan ~67%

– Avg. LTV for LAP ~56%

All figures in INR Crs

Retail Assets:

Fast growing diversified book

857

535

736

806

443

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

Rural Assets:

Deepen the penetration in emerging rural markets & generate Agri PSL

18

1

Business originations Robust Farmer financing book & improved collections in JLG book

3

Capturing Rural value chain with geographic diversification

2

Analytics for expansion towards paperless processing

4

▪ 100% book qualifies under granular PSL lending

▪ Product suite to cater to all segments of semi urban/ rural ecosystem

▪ Parameterized lending in the granular book for faster disbursements

Book size : INR 4,836 Cr

▪ Diversified portfolio across

~225 districts in 15 states

▪ Rich pedigree of working

with credible BC partners

▪ Grid based framework for

MFI lending (Parameters

include AUM size, capital

adequacy, external rating,

delinquency, diversification

etc.)

Book Split (value) by segments

▪ High quality farmer financing book with NPA of 1%

▪ NPA <2% in the JLG book generated post–COVID (disbursements on or after April 1,

2020; constitute ~96% of total book) inline with the microfinance industry standards

▪ Collection efficiency in JLG book improved significantly

▪ On ground portfolio monitoring/ trigger-based monitoring by an independent risk

monitoring team

▪ Digital & Analytics to enhance customer experience / reduce TAT

• Digital on-boarding, dedicated LMS for rule based sanctions & disbursements and

geo-tagged based monitoring

• Usage of Bureau data up to PIN code level for geographical expansions & periodic

portfolio scrub to monitor portfolio health

• Leveraging Fintech/ digitechs for underwriting and risk management

30%

10%

56%

4%

JLG financing

Institutional MFI

financing

Farmer financing

(KCC + Farm

Mechanization)

MSME financing

All figures in INR Crs

SME Banking:

Granular book creation with a solution led approach

5,089

5,001

6,008

6,104

7,389

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

11,731

11,714

12,127

13,282

14,321

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

1

Steady momentum in disbursements

1

Strengthening Relationship Management

3

High quality & well diversified granular book

2

Digital and Analytics at fulcrum of the franchise

4

Book Split by Ticket Size

▪ Dedicated teams for shaper focus in business originations & portfolio management

▪ 100% business originations from internal channels

▪ Digital enabled parameterized lending leading to faster credit decisioning

▪ Distributed portfolio leading to

reduced concentration risk

▪ Portfolio secured by collateral

in addition to primary security of

stock & book debts

▪ Customer churning and

portfolio utilization at pre-covid

level - reflecting portfolio

strength.

Liability Book

▪ One stop solution approach for all needs of entity and promoters

▪ Dedicated Physical RMs for relationship deepening across trade, retail, API banking, etc.

▪ Virtual RMs support to enable customers for engagement, services, enhancements & cross sell

▪ Digital & Analytics to enhance customer experience / reduce friction

• Analytics driven prospective client identification

• Digital Lending Platform - Seamless customer approval experience

• Self-assist digital tools - MSME App, Trade-On-Net, FX Online, etc.

• Robust EWS framework - early identification of incipient sickness & support frontline in

remedial management

• Digital documentation – E-Sign / E-Stamp launched for SME banking

1

Includes Limit Setups

Highest Ever

41%

17%

15%

16%

6%

4%

Upto 0-0.5 cr

0.5-1 cr

1-2 cr

2-5 cr

5-10 Cr

>10 cr

All figures in INR Crs

19

Credit Cards:

Strong business growth and enhanced customer experience

Growth in Acquisition and Cross sell

3

Distribution Outreach and Digitization

4

▪ Steady growth in new card acquisition leading to 20% YoY growth in customer base

to reach ~1.4 million base.

▪ Highest ever new card acquisition of 64000+ cards and Spends of 1715 Cr in

Mar’23

▪ Book size of INR 3,500 Cr+ at end of FY23. 63% YoY growth over Q4 FY22.

▪ Improvement in Revenue per customer through Cross-sell: 34% growth in term

book YoY

▪ Digital acquisition contribution is at 81% leading to seamless customer onboarding

experience ( ETB& NTB) and reduced cost

• Equipped with Video KYC and Biometric for a fully digital ‘paperless’ customer

onboarding

• Enhanced Distribution outreach through Partnerships with Fin-techs and affiliates

▪ Digitization of value-added offerings to enhance customer experience-

• Launched ‘Smart IVR’ for self-service: Key information like Outstanding,

Available credit limit, Statement & Due Payment & Rewards points.

New Product Launches

2

Book Size in Cr

Spends in Cr

1

Sustained Strong Growth in Cards, Book Size & Card Spends

No of Cards In (000s)

1,451

2,162

3,525

2,288

2,676

4,673

Q4FY21 Q4FY22 Q4FY23

49.0%

Y-o-Y

63.0%

Y-o-Y

16.9%

Y-o-Y

74.6%

Y-o-Y

946

1,184

1,419

▪ Launched in Jan’23

▪ Industry first – completely customizable Card

▪ Select Card image & Card material (Normal / Metal / Eco –friendly)

of choice

▪ Customized perks and offers

▪ 7000 ~ Cards Sourced

Build Your Own Card

Subscription Plan

Get better benefits for an upfront subscription fee

Value Added Service

~3000 subscriptions sourced

20

19,910

21,220

23,121

24,730

27,045

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

72,413

69,948

65,372

55,828

53,986

Q4FY22 Q1FY23 Q2FY23 Q3FY23 Q4FY23

2,837

4,390

3,703

6,569

4,153

Wholesale Banking:

Granularization of incremental lending book

1

Corporate Book & Disbursements – Debulking Continues Providing tailored solutions to clients across business segments

3

Large

Corporates

▪ Team of 195 Relationship Bankers spread across 10 locations servicing 950 +

corporates and a team of 26 Product Specialists across Renewables / Infra /

Port / Road sectors / Loan syndication

▪ Focus on Trade borrowers : Letter Of Credits and Bank Guarantee of ~ INR

45,176 Cr

▪ Focus on deposit mobilization from top corporates with average deposit (AMB)

of ~ INR 37,000 Cr

▪ Continued de-risking of stressed exposure with reduction of ~INR 9,000 Cr

achieved in FY23

▪ New Credit Limits of INR 10,000 Cr sanctioned during Q4FY23, and 29 new

corporate relationships added.

Institutional

& Govt

Banking

▪ Team of 205 Relationship Bankers covering Financial Institutions and financial

sector entities, Government entities and Multinationals

▪ Market leading position in cross border remittances

▪ Solutioning led wholesale liabilities franchise across Government entities, Co-

operative sector, BFSI and Fintech

▪ Tailored custody services

▪ Granular advances growth with capital light fee driven business model

Mid

Corporates

▪ Team of 305 members with a strong coverage with presence in 37 key

locations

▪ Granular portfolio with a focus on knowledge banking

▪ Deeply entrenched in new-age entrepreneurship ecosystem by providing

bespoke digital solutions, incubation and networking platforms

Mid Corporate Break up – Granularity improving

2

Book

Disbursements

1

Book

Disbursements

1

1

Excludes movement of CC/OD

939

847

1,139

1,166

1,573

All figures in INR Crs

21

Large Corporates

Products

▪ Higher the proportion of well rated corporates in

Advances

▪ Continued reduction in stressed book &

improvement in portfolio rating

▪ Growth in Working Capital, Trade Flow business

▪ Focus on granularizing the portfolio.

▪ Average limit of new sanctions in Q4: Rs 140 Cr

▪ ECLGS exposure is 1.5% of total LC exposure &

92% of LC borrowers haven't availed ECLGS.

Portfolio Quality and Risk

▪ Proactive EWS mechanism

▪ Detailed screening of new names prior to on-

boarding

▪ Focus on Trade Corridors for imports and exports

business

Analytics

▪ Auto

▪ Cement

▪ Chemicals

▪ Engineering

▪ Fertilizers

▪ FMCG

▪ Food & Agri

Focus Sectors

▪ Metals

▪ IT / ITES

▪ Logistics &

Warehousing

▪ Oil & Gas

▪ Healthcare & Pharma

▪ Renewables

▪ Steel

Presence in 10 major locations

▪ Delhi

▪ Kolkata

▪ Mumbai

▪ Pune

▪ Ahmedabad

Pan India Presence

▪ Bengaluru

▪ Chennai

▪ Hyderabad

▪ Coimbatore

▪ Kochi

▪ Working capital Finance, Project Finance,

Supply Chain Finance , FX and Derivatives.

▪ Growing non-fund book - Letters of Credit, Bank

Guarantees (~INR 45K crores) from high quality

Large Corporates

▪ 130 New Corporates onboarded in FY’23

▪ Digital, Collection & Payments, Liquidity

Management Solutions for large corporates

▪ Major contributor to Bank’s Liabilities business

▪ Onboarding new clients via Debt Capital

Markets solutions

▪ Cross-sell via corporate salary accounts

origination by Consumer Bank & Credit Cards

from LC client base

22

Institutional & Government Banking

Anchoring the Wholesale liabilities franchise

YES BANK’s Institutional & Government Banking Group is divided into 7

segments

Cooperative banks, Scheduled

commercial banks & DFIs, NBFCs,

Insurance, Mutual Funds, Stock

brokers and payment operators

International

Banking

Indian Financial

Institutions

Banking

Corporate &

Government

Advisory

FASAR

Government

Banking

Multinational

Corporate

Banking

Institutional &

Government

Banking

IFSC Unit

Bank’s only Offshore branch at

GIFT City, Gandhinagar

Central and State

Government/ public sector

undertakings

Multinational

Corporate Clients

International banks, Global

DFIs and Cross border

money transfer operators

CGA advises emerging sectors

of Electric Mobility & Urban Infra

FASAR provides project advisory

services in the Food & Agri space

23

Mid Corporates

Growth led by NTB and X-sell -

higher wallet share and

productivity

Strong coverage – presence in

37 key locations

Sustainable growth in fund

based book - Increase Term

Loan share

ECOM Team

Unicorn and Soonicorn Focus

Knowledge Sectors – Media &

Entertainment, Gems & Jewellery,

Food & Agri, Pharma, Chemicals,

Auto ancillary, Logistics, Metals

Laser Sharp focus on portfolio

quality

Customers provide a multiplier

effect for Branch Banking

offerings - YCOPS, Wealth, TASC,

Credit Cards

Initiatives to maintain Bank’s

Leadership Position in startup

ecosystem through engagements like

API banking, Customized Digital

Solutions/UPI/PPI, Digital Escrow and

Advisory Services (accelerator

programs)

Increase Fee contribution through

Augmenting credit & non-credit Trade/CMS

income. Focus on digital channels like

Trade On Net, digital banking, API

integration.

Synergies with YSL, FASAR & Treasury

24

Financial Markets –

Customised solutions for clients

25

60+ Member experienced

professionals

32%

36%

32%

>15 yrs

5-15 yrs

<5 yrs

Full

Product

Suite

Remittances

Currenc

y Notes

Imports

Forward

s

FX

Options

FX and

Interest

Rates

Swaps

Exotics

Active FX trading desk

for market making

providing best in class

pricing for customer

transactions and

Propriety trading

FX All

FX GO

YesFX

CCIL FX Retail

Platform

YesFX Online

Available across digital

platforms for Rate booking

Retail Contributes 45% of

overall income

FX Sales

Debt Capital

Markets

Our Experience

1000+

Transactions originated

since inception

100+

Years of collective

Team experience

50+

First-time issuers

introduced to Debt

Capital Markets

Numerous maiden issuances & multiple repeat

mandates

Gsec/ SDLs/ IRS Vanilla

Bonds / Commercial

Paper

Securitization / Credit

Enhanced Structures

Hedging Products like

IRF and OIS

High Yield Credits

InvITs &

Project Bonds

Bank / NBFC

Debt

Comprehensive Product Suite

▪ Mutual Funds

▪ Banks

▪ Insurance Companies

▪ NBFCs

▪ Private Wealth Management

▪ Retiral Funds

▪ Corporate Treasuries

▪ Alternate investment Funds

▪ FPIs

▪ UCBs & RRBs

Diversified Investor Connect

Corporates

NBFCs & FIs

Banks

InvITs

Connect with a wide range

of Large/Mid-Size Issuers

2

nd

Largest Bank for

Bullion in India

Bullion Desk

Gold

Metal

Loan

SilverGold

Consignment import

Outright domestic and Export

Sales

Customer Types

Bullion Traders

Jewellery Mftg

Jewellery Exporters

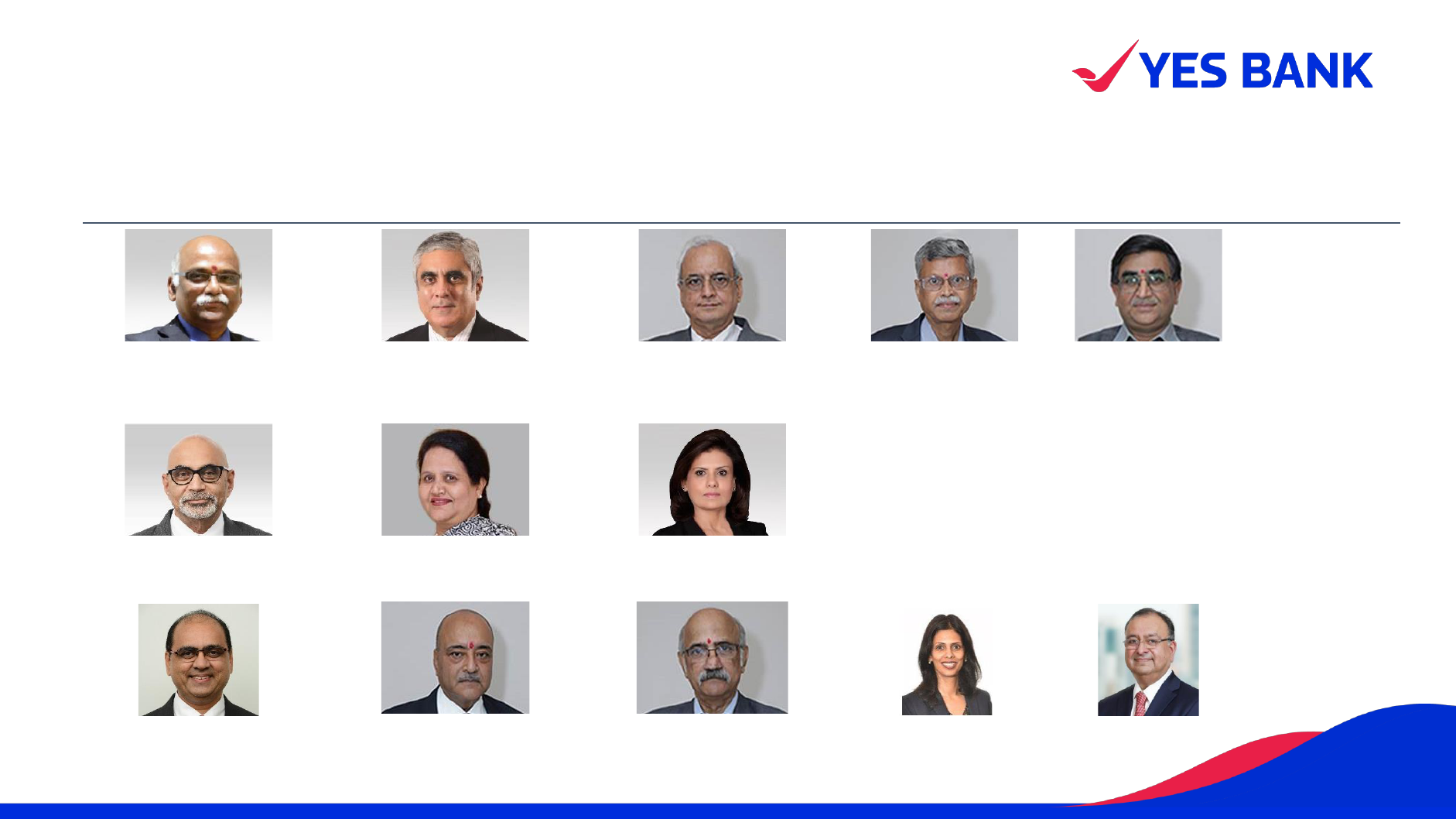

Robust Governance Structure – Board Members

26

Eminent and Experienced Board

1

Nominee of Verventa Holdings Limited

2

Nominee of CA Basque Investments

Sadashiv Srinivas Rao

Independent Director

Shweta Jalan

1

Non-Executive Director

Sharad Sharma

Independent Director

Rekha Murthy

Independent Director

Thekepat Keshav Kumar

Nominee Director appointed by SBI

Atul Malik

Independent Director

Nandita Gurjar

Independent Director

Sandeep Tewari

Nominee Director appointed by SBI

Sanjay Kumar Khemani

Independent Director

Sunil Kaul

2

Non-Executive Director

Rama Subramaniam Gandhi

Non-Executive, Part time Chairman,

Independent Director

Prashant Kumar

Managing Director & CEO

Rajan Pental

Executive Director

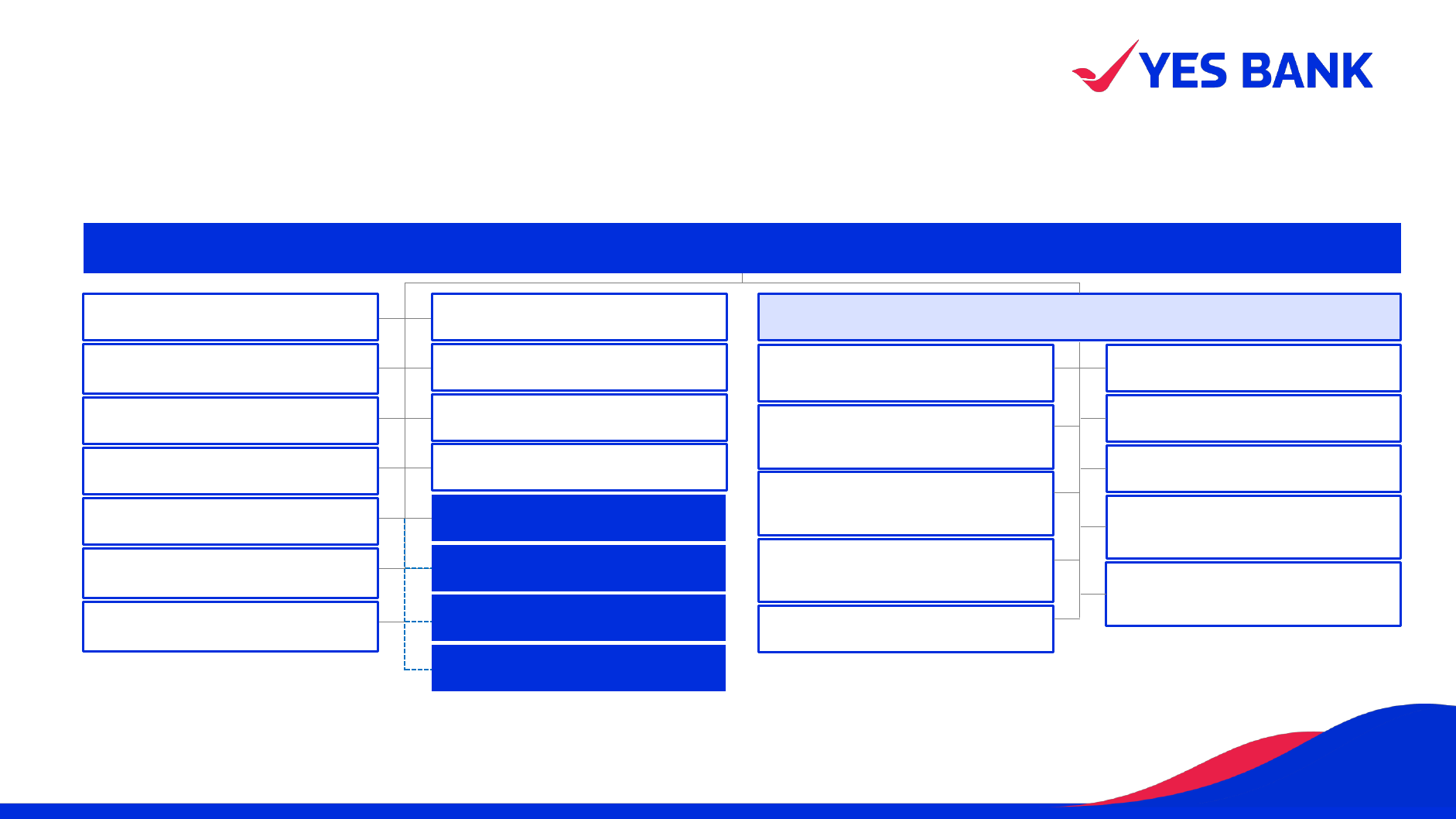

Professional and Seasoned Management team

27

Prashant Kumar

Managing Director & CEO, YES Bank

Niranjan Banodkar

Chief Financial Officer

Archana Shiroor

Chief Human Resources Officer

Rakesh Arya

Chief Credit Risk Officer

Sandeep Mehra

Chief Vigilance Officer

Shivanand R. Shettigar

1

Company Secretary

Kapil Juneja

3

Chief Internal Auditor

Sumit Gupta

2

Chief Risk Officer

Ashish Chandak

3

Chief Compliance Officer

Ravi Thota

Country Head, Large Corporates (LCs)

Amit Sureka

Country Head, Financial Markets

Harsh Gupta

Country Head, Stress Asset Management

Arun Agrawal

Country Head, Institutional & Govt Banking

Ajay Rajan

Country Head, Transaction Banking

Indranil Pan

Chief Economist

Gaurav Goel

Country Head, Emerging Local Corporates

Rajan Pental

Executive Director

Dhavan Shah

Country Head, Small Medium Enterprises Banking

Dheeraj Sanghi

Country Head, Branch Banking Affluent Banking &

- Retail Banking

Akshay Sapru

Country Head, Liabilities Product and Retail

Wealth

Lavesh Sardana

Country Head, Retail Assets and Debt

Management, Retail Assets

Sanjiv Roy

Country Head, Fee Based product & Service

Experience

Sachin Raut

Chief Operating Officer

Karthikeyan J

Chief Data and Analytics Officer

Mahesh Ramamoorthy

Chief Information Officer

Nipun Kaushal

Chief Marketing Officer and Head CSR - Marketing

and Corporate Communication

Anil Singh

Country Head, Credit Cards and Merchant

Acquiring - Credit Cards

1

Reports directly to the Chairman of Board

2

Reports directly to the Risk Management Committee of the Board

3

Reports directly to the Audit Committee of the Board

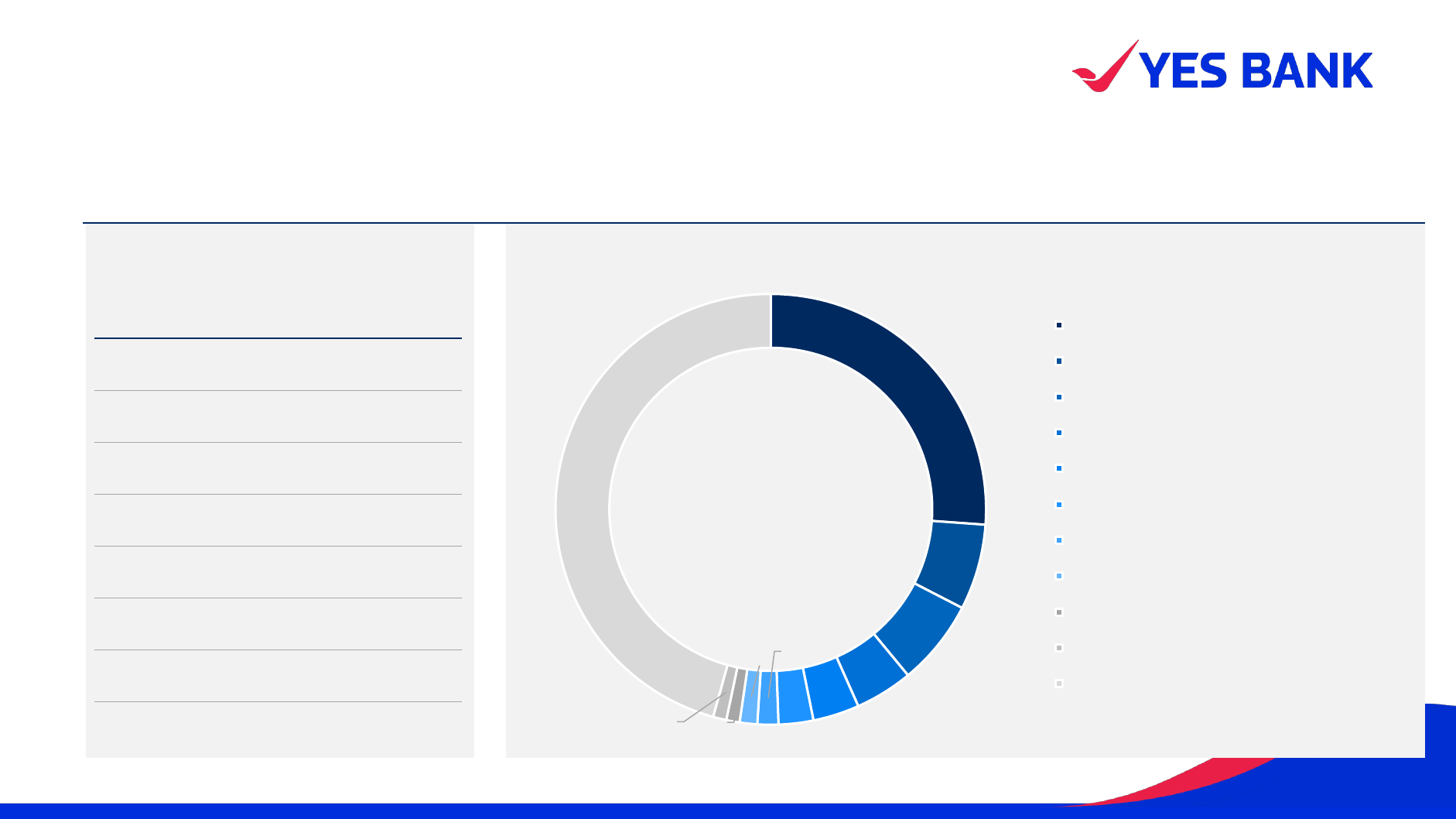

Strong Investor base

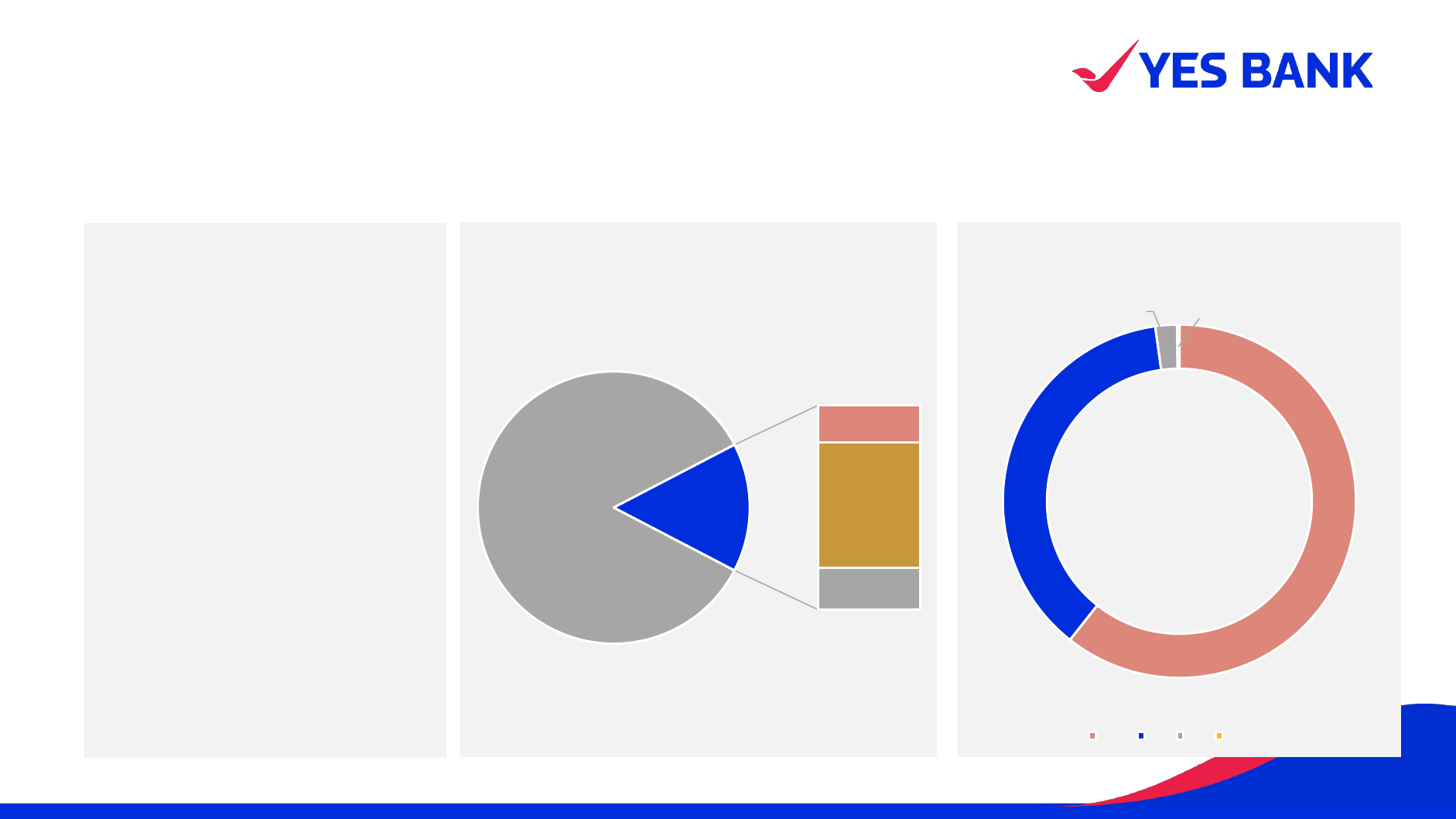

28

Well diversified Investor base:

Shareholding Pattern as on March 31, 2023

1

LIC along with its various schemes

26.1%

6.4%

6.4%

4.3%

3.5%

2.6%

1.6%

1.3%

1.0%

1.0%

45.7%

STATE BANK OF INDIA

CA BASQUE INVESTMENTS

VERVENTA HOLDINGS

LIFE INSURANCE CORPORATION OF INDIA

HOUSING DEVELOPMENT FINANCE

CORPORATION LIMITED

ICICI BANK LIMITED

AXIS BANK LIMITED

KOTAK MAHINDRA BANK LTD

AMANSA HOLDINGS PRIVATE LIMITED

IDFC FIRST BANK LIMITED

Others

1

Category %

Banks 33.0%

FDI 12.9%

Resident Individuals 29.9%

FPI’s 10.3%

Body Corporates 6.8%

Insurance Companies 4.6%

Others 2.5%

TOTAL 100.0%

YES BANK of Today 3-6

YES BANK Franchise 8-28

ESG Led Responsible Banking

New Age Digital Platform

Universal Bank – One Bank For All Needs

Governance and Senior Management Team

Shareholding

Financials 30-43

Contents

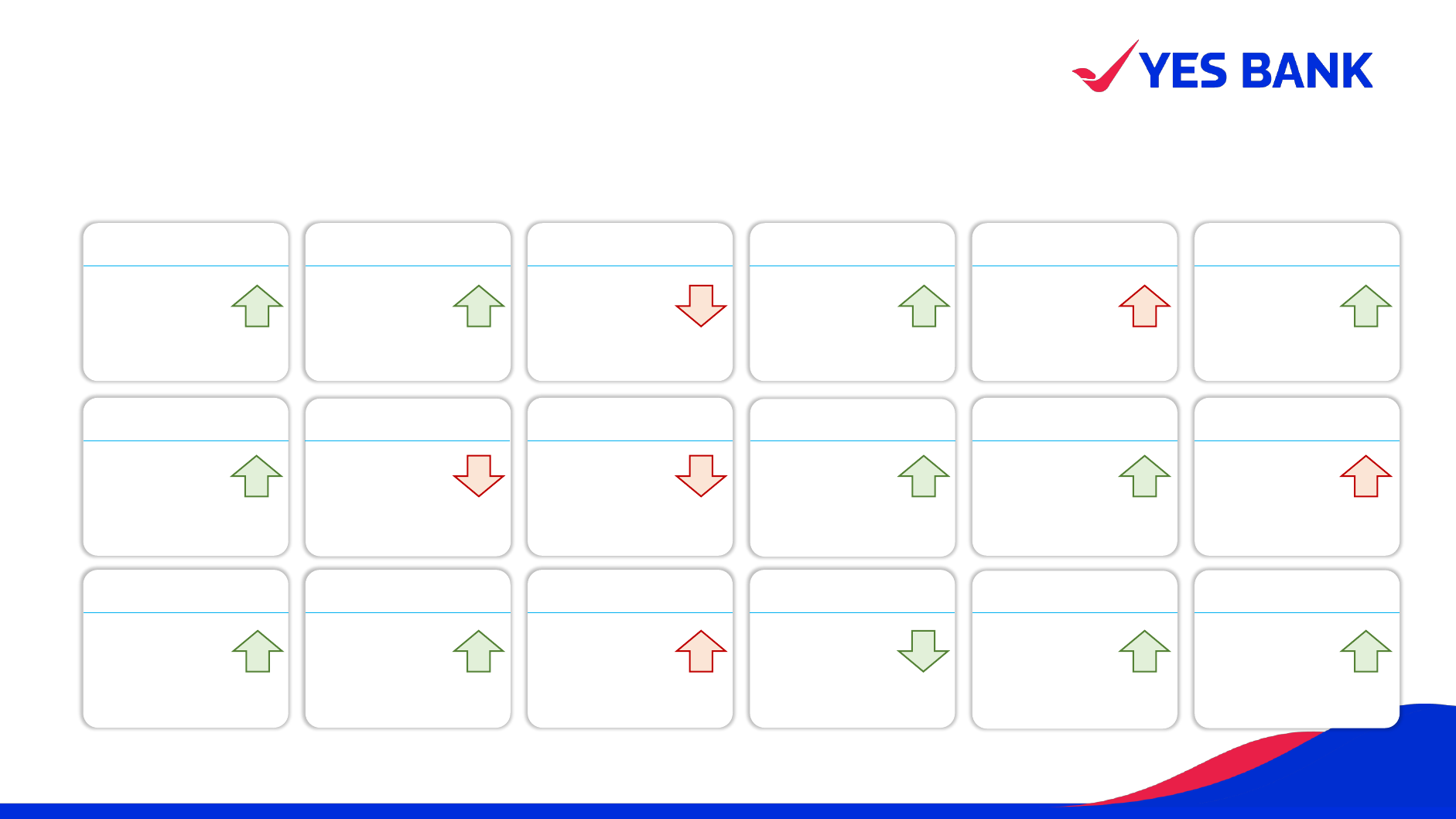

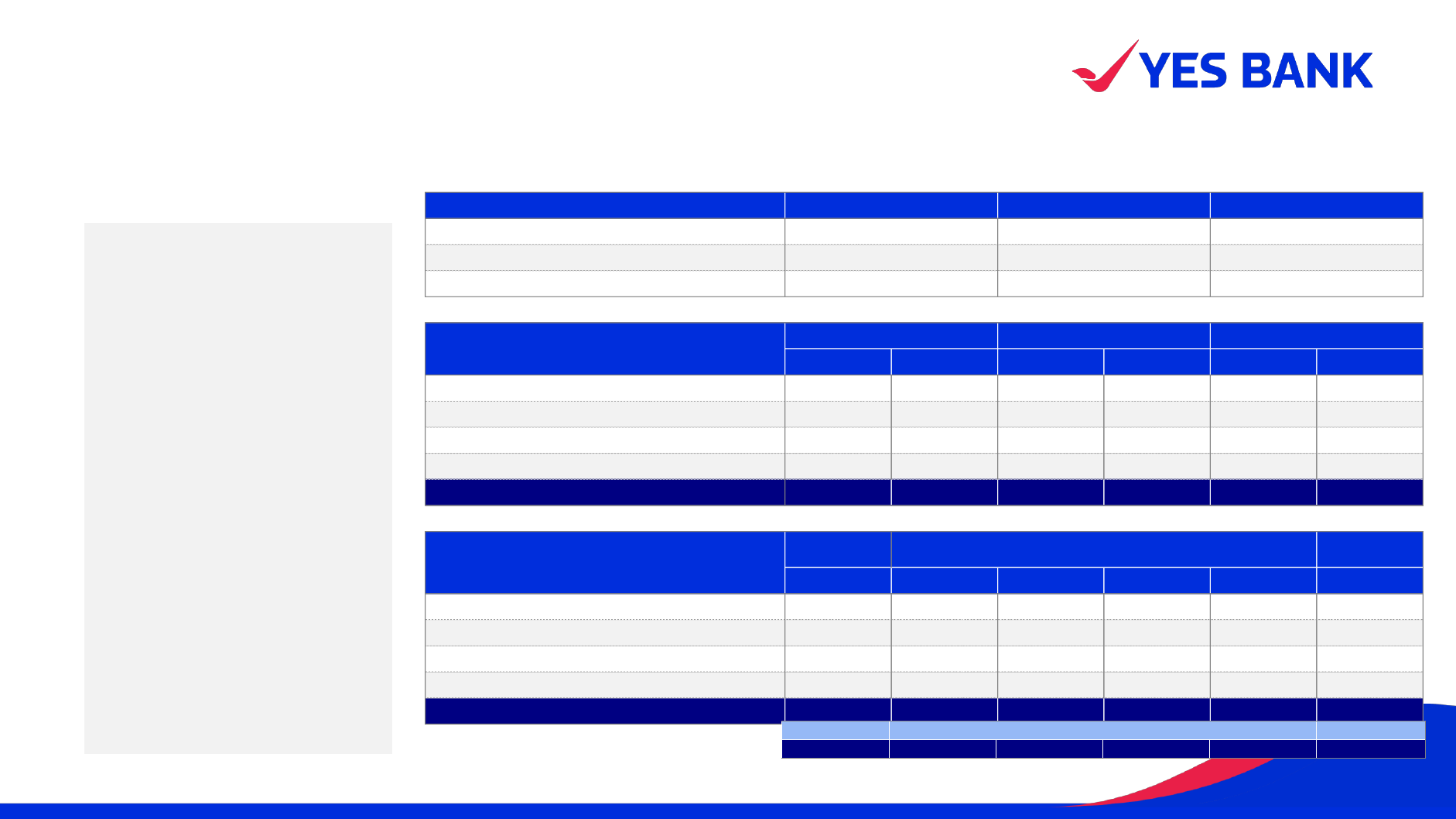

Results At a Glance – Q4FY23

All figures in INR Crs

1

Includes Limit Setup & New Sanctions

2

Excluding INR 3,069 Crs in Q4FY23 and 3,031 Crs in Q3FY23 of Interbank Reverse Repo classified as Advances as per RBI Master Circular No

DOR.ACC.REC.NO.37/21.04.018/2022-23

3

Q-o-Q and Y-o-Y trends not strictly comparable on account of full impact of ARC transaction in Q4FY23

4

Average for the quarter

Arrows indicative of Q-o-Q comparison

CD Ratio

2

92.0%

89.7% Q3FY23

91.8% Q4FY22

Advances Mix

2

59%:14%:27%

58% : 13% : 29% in Q3FY23

49% : 11% : 40% in Q4FY22

CASA Ratio

30.8%

29.9% Q3FY23

31.1% Q4FY22

NIM%

3

2.8%

2.5% Q3FY23

2.5% Q4FY22

C/I Ratio

72.1%

70.7% Q3FY23

71.3% Q4FY22

Total Assets

354,786

3.2%: Q-o-Q

11.5%: Y-o-Y

Advances

203,269

4.5%: Q-o-Q

12.3%: Y-o-Y

Total Disbursements

1,2

26,317

27,311 Q3FY23

19,923 Q4FY22

Deposits

217,502

1.8%: Q-o-Q

10.3%: Y-o-Y

Operating Profit

889

-2.7%: Q-o-Q

14.8%: Y-o-Y

YES Bankers

27,517

25,883 in Q3FY23

24,346 in Q4FY22

CET 1 Ratio

13.3%

GNPA

2.2%

NNPA

0.8%

Non-Interest Income

1,082

-5.3% Q-o-Q

22.8% Y-o-Y

LCR

4

13.0% Q3FY23

11.6% Q4FY22

2.0% Q3FY23

13.9% Q4FY22

1.0% Q3FY23

4.5% Q4FY22

Profit After Tax

202

292.8% Q3FY23

-44.9% Q4FY22

118.5%

113.3% Q3FY23

114.6% Q4FY22

v/s.

v/s.

v/s.

v/s.

v/s.

v/s.

v/s.

v/s.

v/s.

Retail & SME: Mid Corp: Corporate

v/s.

Net Interest Income

2,105

6.8% : Q-o-Q

15.7% : Y-o-Y

30

Highlights for Q4FY23 and FY23

▪ Net Profit at INR 202 Crs for Q4FY23 despite accelerated provisioning during the quarter

▪ Net Profit for FY23 at INR 717 Crs- second straight year of full year profitability

▪ Core Operating Performance sustains momentum:

• NII at INR 2,105 Crs for Q4FY23 up 15.7% Y-o-Y and 6.8% Q-o-Q; NII at INR 7,918 Crs for FY23 up

21.8% Y-o-Y; NIMs at 2.8% for Q4FY23 vs. 2.5% last year and last quarter

• Non-Interest Income at INR 1,082 Crs, up 22.8% Y-o-Y; Non-Interest Income for FY23 at INR

3,927 Crs, up 20.4% Y-o-Y. Ex- Realised/ unrealised gain on sale of Investments, Non-Interest

Income for FY23 up 31.1% Y-o-Y

• Operating Profit for Q4FY23 at INR 889 Crs; Operating Profit for FY23 at INR 3,183 Crs up 9.2% Y-o-

Y; Normalised Operating Profit

1

for FY23 up 22.6% Y-o-Y

Sustained Earnings: Second straight year of full year profitability

▪ (NNPA + net carrying value of SR) as % of Advances at 2.4% in Q4FY23 vs. 3.0% last quarter

• GNPA ratio at 2.2% as of Mar 31, 2023, v/s 2.0% last quarter and 13.9% last year; NNPA ratio improved

to at 0.8% v/s. 1.0% last quarter and 4.5% last year

• Significant step-up in Provision Coverage Ratio

2

of NPA to 62.3% v/s 49.4% last quarter

▪ Robust Recoveries and Upgrades continue to outpace Gross Slippages

• Strong Resolution momentum with recoveries and resolutions at INR 6,120 Crs

3

in FY23 vs. target of INR

5,000 Crs; total Recoveries and Resolutions at INR 1,733 Crs

3

in Q4FY23

• Gross Slippages at INR 4,775 Crs for FY23, lower by 17.6% Y-o-Y. Gross Slippages at 1,196 Crs for

Q4FY23 lower by 25.7% Q-o-Q

Marked improvement in Asset Quality: ~60 bps Q-o-Q reduction in (NNPA + net

carrying value of SR) %

▪ Sustained improvement in quality, granularity and capital efficiency

• Balance Sheet grew 11.5% Y-o-Y and 3.2% Q-o-Q; Advances up 12.3% Y-o-Y and 4.5% Q-o-Q,

and Deposit grew 10.3% Y-o-Y and 1.8% Q-o-Q - average deposit balance for the year and

quarter grew ~16% Y-o-Y

• Organically unlocked Capital: CET 1 at 13.3% v/s 11.6% last year and 13.0% last quarter; Total CRAR

at 18.0%; RWA to Total Assets improved to 69.1% from 72.8% last year and 70.9% last quarter

• Strong momentum in new business generation with Gross disbursements at ~INR 1 Lac Crs for

FY23 and INR 26,317 Crs for Q4FY23. Retail & SME : Mid Corporate : Corporate Mix further

improved to 59:14:27

3

v/s 58:13:29 last quarter

• CASA ratio improved ~90 bps Q-o-Q to 30.8% v/s 29.9% Q3FY23. Average CASA balance for

FY23 grew 26.3% Y-o-Y

▪ Added 83 new branches during FY23; branch count now at 1,192 v/s. 1,122 last year

▪ Issued the first Electronic Bank Guarantee (e-BG), in partnership with National E-Governance Services

Limited (NeSL)

▪ Partnered with Aadhar Housing Finance, one of India’s largest affordable housing finance companies to

provide convenient home finance solutions

▪ The first bank in Asia Pacific to bring forth a debit card on Mastercard’s premium World Elite Platform – a

signature global program catering to Ultra High Net Worth individual (UHNI) customers

▪ YES BANK has been certified as Great Place to Work by Great Place to Work (GPTW) Institute, India and is

ranked among the top 50 in ‘India's Best Workplaces in BFSI 2023’

1

NII normalised for Interest Income from NPA/ NPI; Non- Interest Income normalised for realised/ unrealised gain on sale of Investments;

2

Excluding Technical Write-offs. Historical disclosures were inclusive of

technical write-offs

3

Including redemption of SRs, net off the 15% Cash component paid upfront at time of transaction

4

Excluding INR 3,069 Crs in Q4FY23 and INR 3,031 Crs in Q3FY23 of Interbank Reverse Repo

classified as Advances as per RBI Master Circular No DOR.ACC.REC.NO.37/21.04.018/2022-23

Granular Growth & organic unlocking of Capital: CET 1 % up 30bps Q-o-Q Key initiatives

31

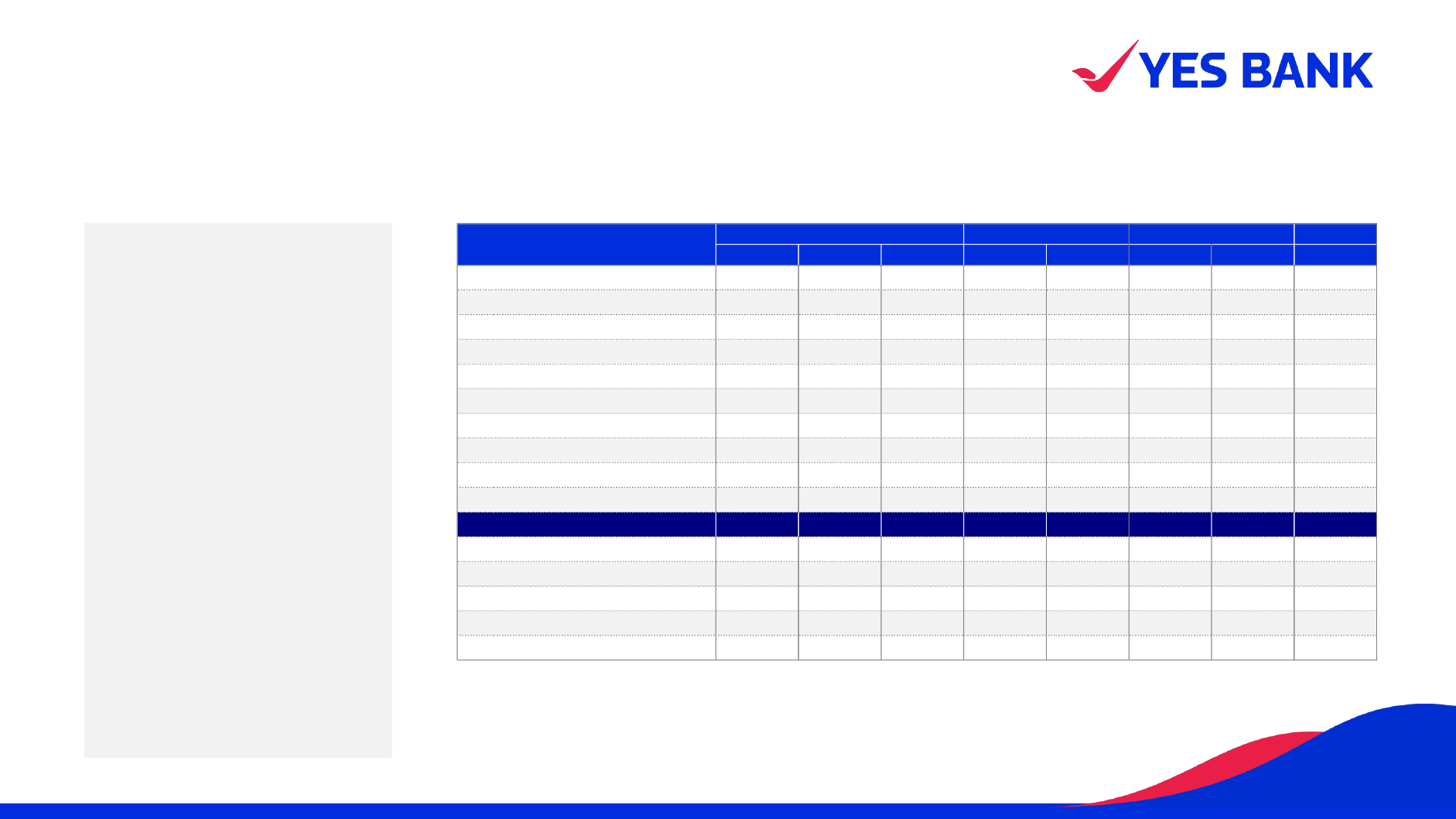

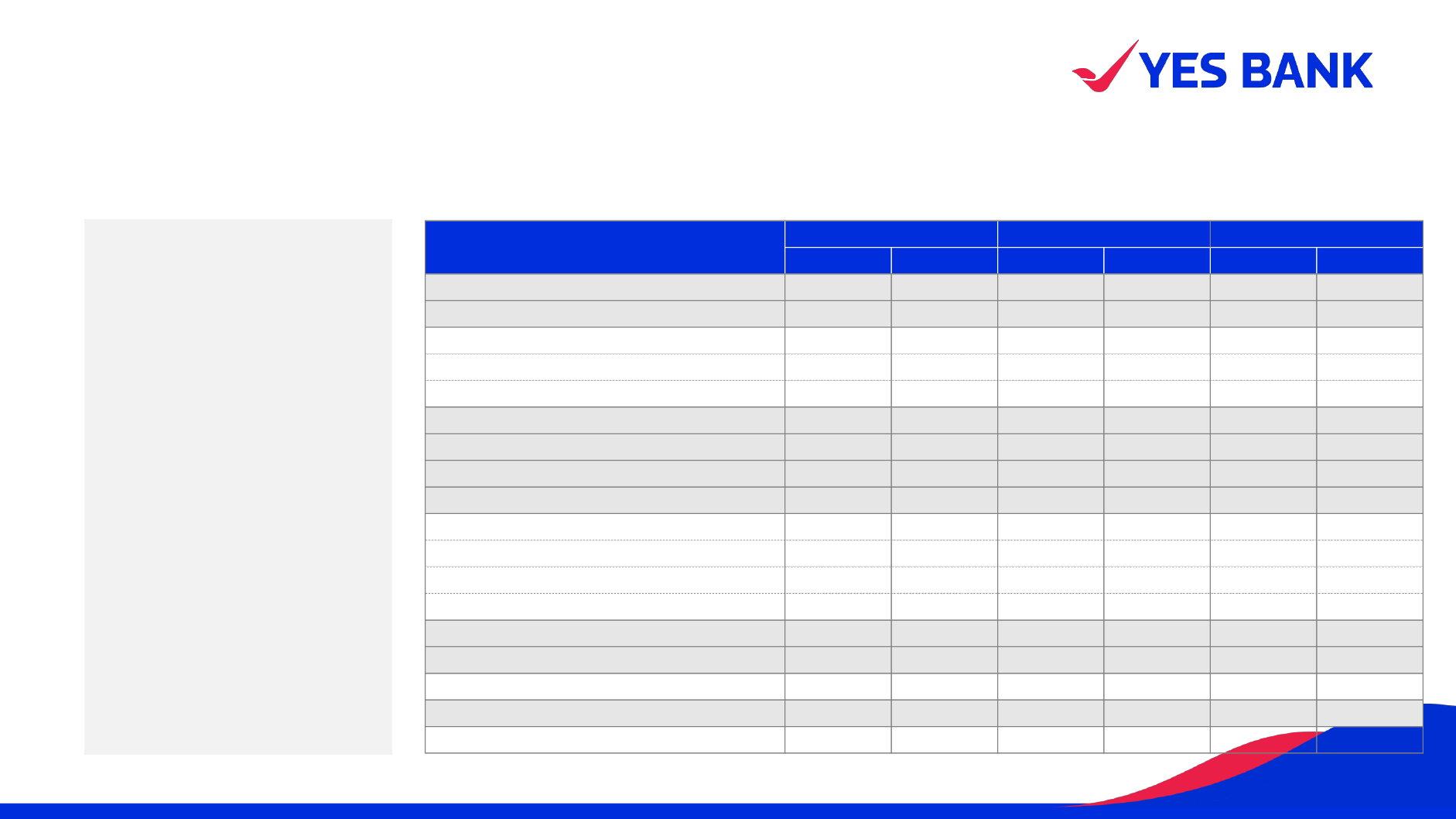

Profit and Loss Statement

32

▪ Net Profit at INR 202 Crs despite

accelerated provisioning during the

quarter

▪ Core Operating Performance sustains

momentum

– NII at INR 2,105 Crs for Q4FY23 up

6.8% Q-o-Q and 15.7% Y-o-Y

– NIM at 2.8% up 30 bps Q-o-Q

– Non-Interest Income at INR 1,082

Crs, up 22.7% Y-o-Y

▪ Net Profit for FY23 at INR 717 Crs lower

by 32.7% Y-o-Y largely on account of

step up in PCR through accelerated

provisioning

– NII at INR 7,918 Crs for FY23 up

21.8% Y-o-Y

– NIM at 2.6% for FY23 up 30 bps Y-

o-Y

– Non-Interest Income for FY23 at INR

3,927 Crs, up 20.4% Y-o-Y

▪ Normalised C/I

1

for FY23 broadly flattish

despite significant change in business

mix towards Retail Segment

Growth

Q4FY23 Q3FY23 Q4FY22 Q-o-Q Y-o-Y FY23 FY22 Y-o-Y

Net Interest Income 2,105 1,971 1,819 6.8% 15.7% 7,918 6,498 21.8%

Non Interest Income 1,082 1,143 882 -5.3% 22.8% 3,927 3,262 20.4%

Total Income 3,188 3,114 2,701 2.4% 18.0% 11,844 9,760 21.4%

Operating Expenses 2,299 2,200 1,927 4.5% 19.3% 8,661 6,844 26.5%

Human Resource Cost 854 857 772 -0.4% 10.6% 3,363 2,856 17.8%

Other Operating Expenses 1,445 1,343 1,155 7.6% 25.1% 5,299 3,989 32.8%

Operating Profit/(Loss) 889 914 774 -2.7% 14.8% 3,183 2,916 9.2%

Provisions 618 845 271 -26.9% 127.8% 2,220 1,480 50.0%

Profit Before Tax 271 69 503 293.9% -46.1% 963 1,436 -32.9%

Tax Expense 69 17 136 297.1% -49.2% 246 370 -33.6%

Net Profit / (Loss) 202 52 367 292.8% -44.9% 717 1,066 -32.7%

Yield on Advances 10.2% 9.0% 8.2% 8.9% 8.1%

Cost of Funds 5.9% 5.7% 5.1% 5.5% 5.3%

Cost of Deposits 5.6% 5.3% 4.8% 5.2% 5.0%

NIM 2.8% 2.5% 2.5% 2.6% 2.3%

Cost to income 72.1% 70.7% 71.3% 73.1% 70.1%

Profit and Loss Statement

Quarter Ended

Growth

Year Ended

1

NII normalised for Interest Income from NPA/ NPI; Non- Interest Income normalised for realised/ unrealised gain on sale of Investments

All figures in INR Crs

Break Up of Non-Interest Income

33

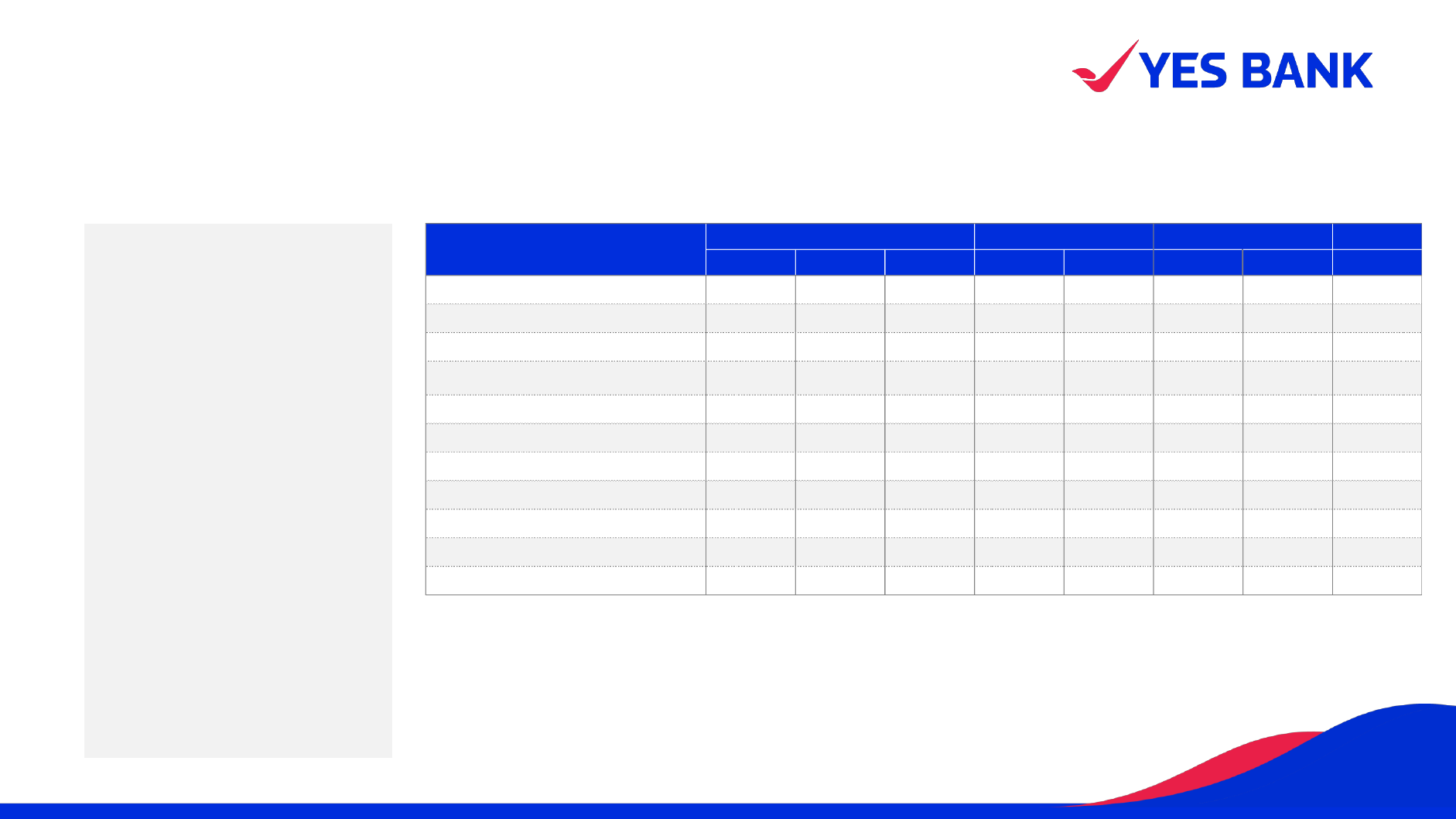

▪ Non-Interest Income at INR 1,082 Crs for

Q4FY23, up 22.8% Y-o-Y, down 5.3% Q-o-

Q

▪ Ex- realised/ unrealised gain on

Investments, Non-Interest Income

1

for

Q4FY23 up 16.3% Y-o-Y and 4.9% Q-o-Q

– Sustained Momentum in Retail

Banking Fees up 24.1% Q-o-Q &

46.4% Y-o-Y at INR 838 Crs

– Corporate Trade & Cash

Management fees grew 11.0% Q-o-

Q and 13.8% Y-o-Y

▪ Non-Interest Income for FY23 at INR

3,927 Crs, up 20.4% Y-o-Y. Normalised

Non-Interest Income

1

for FY23 up 31.1%

Y-o-Y

1

Normalised for realised/ unrealised gain on sale of Investments

Growth

Q4FY23 Q3FY23 Q4FY22 Q-o-Q Y-o-Y FY23 FY22 Y-o-Y

Non Interest Income 1,082 1,143 882 -5.3% 22.8% 3,927 3,262 20.4%

Corporate Trade & Cash Management 197 177 173 11.0% 13.8% 681 619 10.0%

Forex, Debt Capital Markets & Securities (4) 244 113 NM NM 503 749 -32.9%

Of which realised/ unrealised gain on

Investments

(73) 137 (26) NM 182.7% 31 290 -89.3%

Corporate Banking Fees 52 46 24 11.8% 116.4% 154 100 53.8%

Retail Banking Fees 838 675 572 24.1% 46.4% 2,589 1,806 43.4%

Trade & Remittance 92 88 69 4.2% 33.3% 333 236 40.9%

Facility/Processing Fee 126 108 81 16.7% 55.3% 400 292 37.1%

Third Party Sales 96 65 84 48.2% 14.4% 267 191 39.7%

Interchange Income 340 232 200 46.3% 69.8% 920 596 54.3%

General Banking Fees 184 182 138 1.2% 33.0% 669 490 36.5%

Year Ended

Break up of Non Interest Income

Quarter Ended

Growth

All figures in INR Crs

Break up of Operating Expenses

34

▪ Opex for Q4FY23 grew 4.5% Q-o-Q and

19.3% Y-o-Y

▪ Opex for FY23 grew 26.5% Y-o-Y v/s.

normalised Total Income growth of 25.6%

leading to flattish normalised C/I

▪ IT spends higher driven by AMC

escalation, depreciation related to

investments, support resources and

business SMS charges

Q4FY23 Q3FY23 Q4FY22 Q-o-Q Y-o-Y FY23 FY22 Y-o-Y

Staff 854 857 772 -0.4% 10.6% 3,363 2,856 17.8%

Business Volume linked 574 578 447 -0.8% 28.4% 2,111 1,464 44.2%

IT 245 224 179 9.4% 37.0% 900 689 30.6%

Premises 194 195 172 -0.5% 12.5% 753 693 8.7%

Professional Fees 128 109 108 17.9% 19.0% 451 291 55.0%

Others 304 237 250 28.2% 21.8% 1,085 852 27.3%

Total 2,299 2,200 1,927 4.5% 19.3% 8,661 6,844 26.5%

Cost Head

Quarter Ended

Growth

Year Ended

Professional Fees primarily comprise of Bureau costs and vendor fees related to Collections, Contact Centre and other consulting and legal costs

For reference: Breakup of Operating Expenses over last 8 quarters provided in Appendix

All figures in INR Crs

Provisions and P&L

35

NM = Not Measurable

▪ Provision costs for Q4FY23 declined

20.4% Q-o-Q, led by

– Security Receipts Redemptions of INR

1,178 Crs accrued to the Bank from JC

Flowers ARC accounts leading to INR

987 Crs of Provision write-back

▪ Provision Costs for FY23 grew 33.3% Y-o-

Y led by accelerated provisioning

▪ Gross Slippages for FY23 at INR 4,775

Crs (2.5% of avg. Advances) declined

17.6% Y-o-Y

– Retail Slippages for FY23 lower by

11.4% Y-o-Y despite strong growth in

Advances

▪ NNPA + net carrying value of SR as %

of Advances further decreased to 2.4%

v/s 3.0% last quarter

▪ Significant step up in PCR on NPA to

62.3% from 49.4% last quarter

Growth

Q4FY23 Q3FY23 Q4FY22 Q-o-Q Y-o-Y FY23 FY22 Y-o-Y

Operating Profit/(Loss) 889 914 774 -2.7% 14.8% 3,183 2,916 9.2%

Provision for Taxation 69 17 136 297.1% -49.2% 246 370 -33.6%

Provision for Investments (651) 2,902 530 NM NM 2,409 790 204.8%

Provision for Standard Advances (72) (107) (475) -32.5% -84.8% (150) (25) 494.8%

Provision for Non Performing Advances 1,311 (2,001) 227 NM 476.4% (17) 719 NM

Other Provisions 29 50 (12) NM NM (22) (4) 509.3%

Total Provisions 686 862 407 -20.4% 68.8% 2,465 1,850 33.3%

Net Profit / (Loss) 202 52 367 292.8% -44.9% 717 1,066 -32.7%

Return on Assets (annualized) 0.2% 0.1% 0.5% 0.2% 0.4%

Return on Equity (annualized) 2.0% 0.6% 4.3% 1.9% 3.2%

EPS-basic (non-annualized) 0.07 0.02 0.15 0.27 0.43

Break up of Provisions

Quarter Ended

Growth

Year Ended

All figures in INR Crs

Balance Sheet

36

▪ Balance Sheet grew 11.5% Y-o-Y

– C/D ratio at 92.0%

1

v/s. 91.8%

last fiscal and 89.7% in Q3FY23

▪ Advances growth at 12.3% Y-o-Y.

Normalized for ARC sale and

Reverse Repo, Advances Growth at

13.2% Y-o-Y

▪ ~1 Lac Crs of New Sanctions /

Disbursements in FY23

Balance Sheet 31-Mar-23 31-Dec-22 31-Mar-22

Growth %

(Q-o-Q)

Growth %

(Y-o-Y)

Assets 354,786 343,778 318,220 3.2% 11.5%

Advances 203,269 194,573 181,052 4.5% 12.3%

Investments 76,888 68,382 51,896 12.4% 48.2%

Liabilities 354,786 343,778 318,220 3.2% 11.5%

Shareholders Funds 40,742 40,154 33,742 1.5% 20.7%

Total Capital Funds 43,923 44,339 40,397 -0.9% 8.7%

Deposits 217,502 213,608 197,192 1.8% 10.3%

Borrowings 77,452 68,928 72,205 12.4% 7.3%

1

Excludes Reverse- repo classification

Disbursements

Q4FY23 FY23

Retail Assets

12,705

49,798

Rural Assets

498

2,572

SME

7,389

24,502

Mid Corporate

1,573

4,724

All figures in INR Crs

Break up of Advances 31-Mar-23 31-Dec-22 31-Mar-22

QoQ

Growth (%)

YoY

Growth (%)

Retail 90,447 83,769 65,250 8.0% 38.6%

SME 28,724 27,215 23,479 5.5% 22.3%

Mid corporate 27,045 24,730 19,910 9.4% 35.8%

Corporate 53,986 55,828 72,413 -3.3% -25.4%

Others (Reverse Repo) 3,069 3,031

Total Net Advances 203,269 194,573 181,052 4.5% 12.3%

▪ Sustained Granularization of

Balance Sheet:

– Retail Advances mix at 45.2%

v/s. 43.7% in Q3FY23(ex-

Reverse Repo adj.)

– CASA + Retail TDs

1

at 59%

– Average daily CA for FY23

grew by 30.4% Y-o-Y

– Average daily SA for FY23

grew by 23.7% Y-o-Y

– ~372K Retail CASA Accounts

opened in Q4FY23

Break up of Advances & Deposits

37

1

Based on Balances </= INR 2 Crs on an Account Level

Break up of Deposits 31-Mar-23 31-Dec-22 31-Mar-22

QoQ

Growth (%)

YoY

Growth (%)

CASA 66,903 63,927 61,360 4.7% 9.0%

Current Account 33,603 29,049 26,389 15.7% 27.3%

Savings Account 33,300 34,878 34,970 -4.5% -4.8%

CASA Ratio 30.8% 29.9% 31.1%

Term Deposits 150,599 149,681 135,832 0.6% 10.9%

Certificate of Deposits 291 3,236 4,264 -91.0% -93.2%

Total Deposits 217,502 213,608 197,192 1.8% 10.3%

All figures in INR Crs

61%

37%

2%

0.2%

Rating wise break up of Standard

Performing NSLR Investments

AAA AA BB Unrated

SLR 85%

HTM 3%

AFS 9%

HFT 3%

NSLR 15%

Investments breakup

Break up of Investments

38

▪ Total Net Investments at INR 76,888 Crs

▪ SLR – INR 65,158 Crs

▪ NSLR – INR 11,730 Crs

• Standard Performing – INR 6,497

Crs

• Others

1

– INR 5,233 Crs

1

Includes Equity Preference, CDR, US Treasury Bills, Security Receipts, NPI & Others

All figures in INR Crs

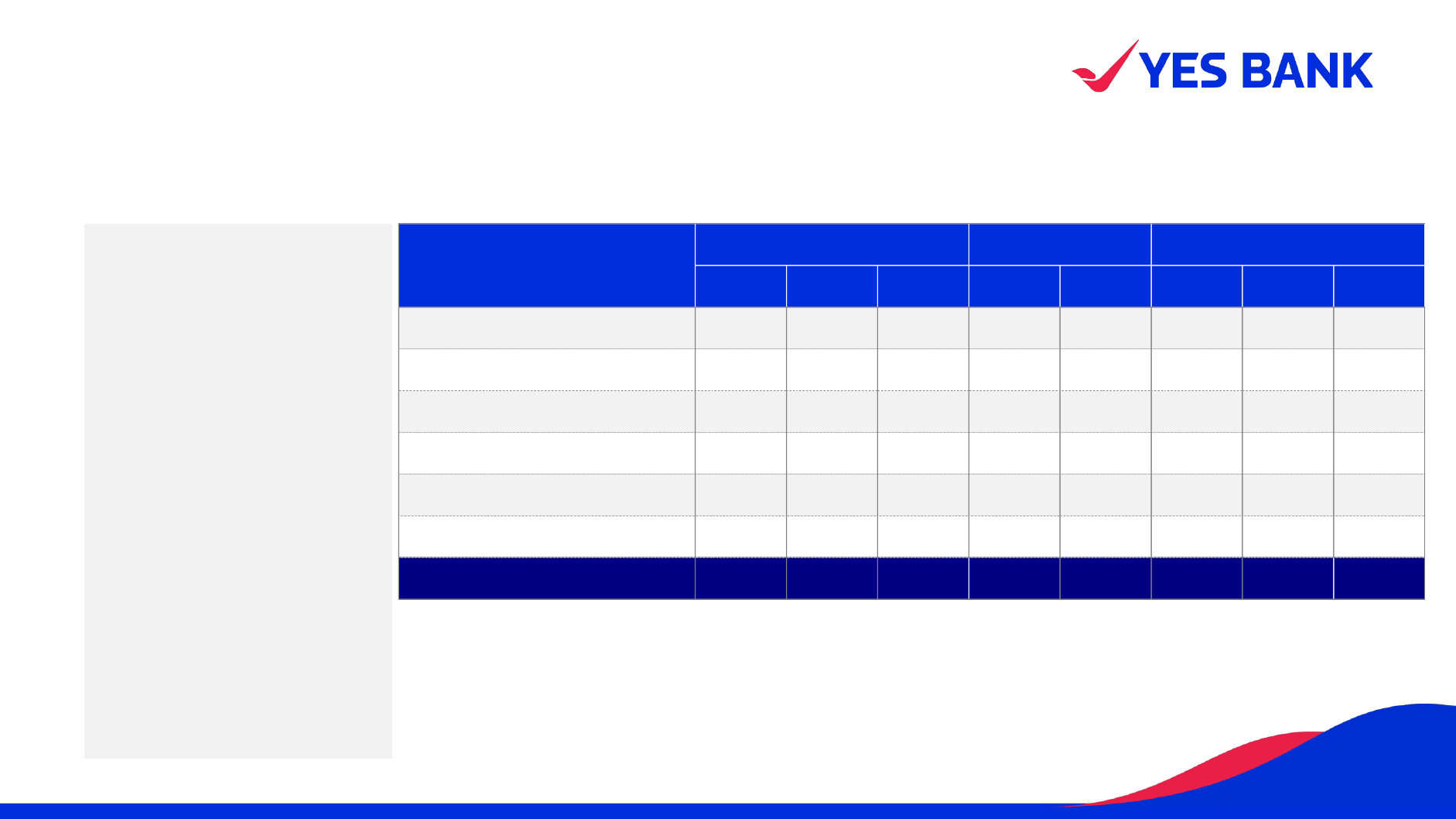

NPA Highlights

39

1

Excluding INR 3,069 Crs in Q4FY23 and INR 3,031 Crs in Q3FY23 of Interbank Reverse Repo classified as Advances as per RBI Master Circular No DOR.ACC.REC.NO.37/21.04.018/2022-23

2

Excluding technical write-offs

▪ Gross NPA Ratio at 2.2% vs 2.0%

in Q3FY23

▪ Slippages at INR 1,196 Crs for

Q4FY23 vs. INR 1,610 Crs in

Q3FY23.

Asset Quality Parameters

Gross NPA (%)

Net NPA (%)

Provision Coverage Ratio (%)

GNPA (%) GNPA (%) GNPA (%)

Retail 1,146 1.3% 960 1.1% 1,093 1.7%

SME 285 1.0% 232 0.9% 739 3.1%

Mid corporate 208 0.8% 143 0.6% 401 2.0%

Corporate Banking 2,755 4.9% 2,568 4.5% 25,743 28.4%

Total 4,395 2.2% 3,904 2.0% 27,976 13.9%

31-Dec-22 31-Mar-23

Opening Additions Upgrades Recoveries Write Offs Closing

Retail 960 697 149 115 247 1,146

SME 232 74 15 5 1 285

Mid corporate 143 72 0 6 1 208

Corporate 2,568 352 110 55 0 2,755

Total 3,904 1,196 275 182 249 4,395

31-Mar-22

13.9%

4.5%

70.7%

31-Mar-23

31-Dec-22

2.2%

0.8%

62.3%

2.0%

1.0%

49.4%

31-Mar-22

Segmental GNPA

31-Mar-23

31-Dec-22

Movement

Movement of GNPA

1

1

31-Mar-22 Movement 31-Mar-23

27,976 4,775 820 9,423 18,114 4,395

2

All figures in INR Crs

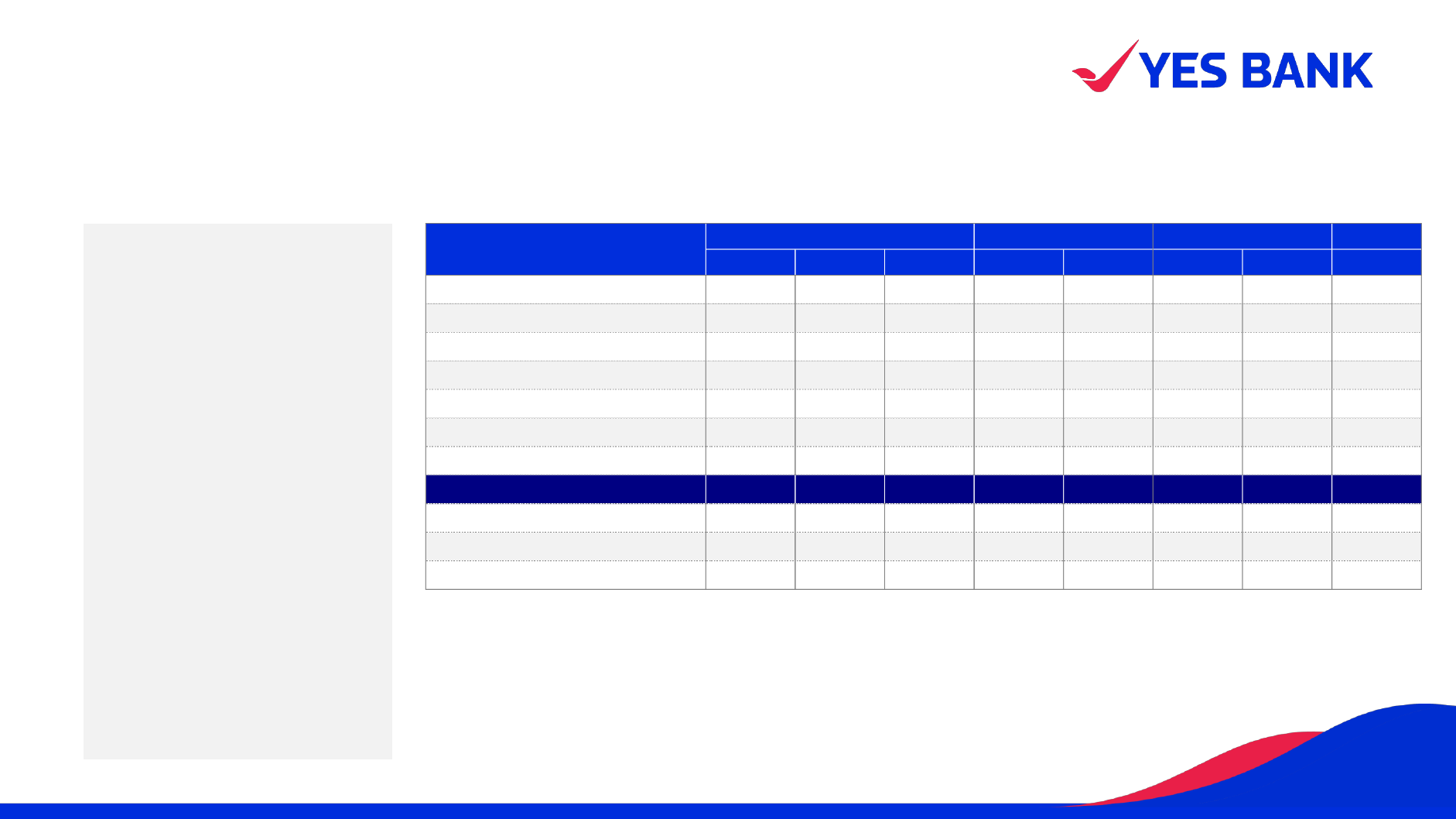

Summary of Labelled & Overdue Exposures

40

1.

Already Implemented as of respective date; Erstwhile category represents Standard Restructured accounts and does not include withdrawn categories such as SDR, S4A etc.

2.

Where provisioning has been made as per requirement of RBI circular on Prudential Framework for Resolution of Stressed Assets dated June 7, 2019

▪ Slippage of ~INR 283 Crs from

Standard Restructured Advances

pool of Q3FY23

▪ Overdue book of 31-90 days flattish

Q-o-Q at INR 4,792 Crs vs. INR

4,752 Crs in Q3FY23

Gross Provisions Gross Provisions Gross Provisions

NPA 4,395 2,736 3,904 1,930 27,976 19,771

Other Non Performing Exposures 9,128 4,742 10,221 5,392 8,503 6,647

NFB of NPA accounts 1,289 237 1,183 237 1,097 206

NPI 172 76 185 75 5,268 5,021

Security Reciepts 7,666 4,430 8,853 5,080 2,138 1,420

Total Non Performing Exposures 13,522 7,479 14,125 7,323 36,479 26,419

Technical Write-Off 0 0 16,302

Provision Coverage excl. Technical W/O 55.3% 51.8% 80.9%

Std. Restructured Advances

1

4,705 454 5,860 581 6,752 760

Erstwhile 4 4 3 3 26 1

DCCO related 1,558 78 1,718 86 1,744 87

MSME 644 66 732 75 1,016 98

Covid 2,499 306 3,407 418 3,966 573

Other Std. exposures

2

359 123 222 75 98 34

61-90 days overdue loans 1,165 2,834 1,264

Of which Retail 629 549 227

31-60 days overdue loans 3,621 1,918 4,483

Of which Retail 1,097 865 815

31-Dec-22

31-Mar-22

31-Mar-23

In INR Cr

All figures in INR Crs

11.6%

13.0%

13.3%

5.8%

5.1%

4.7%

31-Mar-22 31-Dec-22 31-Mar-23

TIER II

CET 1

Organic accretion in CET

1% during the quarter

Discounting as per Basel III

regulations of Tier II

Instruments worth INR 1,186

Crs were triggered during

the quarter

0.64%

0.09%

0.34%

72.8%

70.9%

69.1%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

67.0%

68.0%

69.0%

70.0%

71.0%

72.0%

73.0%

74.0%

31-Mar-22 31-Dec-22 31-Mar-23

RoRWA

RWA / TA

Organic accretion of Capital:

CET 1 ratio at 13.3%

41

Bank’s Capital Adequacy Ratio

1

RWA to Total Assets trending lower and Risk Adjusted Returns

1

2

CET 1 Ratio at 13.3%

▪ Post full warrant conversion ~150 bps

to further accrue to CET I ratio

▪ Warrants Application / Subscription

money amounting to INR 948 Crs (38

bps) already received in cash, not

considered for CET 1 computation

▪ RWAs lower owing to

▪ Collateral and Rated Book

Improvements

▪ Repayments in loans attracting

higher risk weights

▪ Reduction in market risk capital

charge owing to higher provisioning

for SRs

17.9%

18.2%

17.4%

CRAR

1

Includes Profits

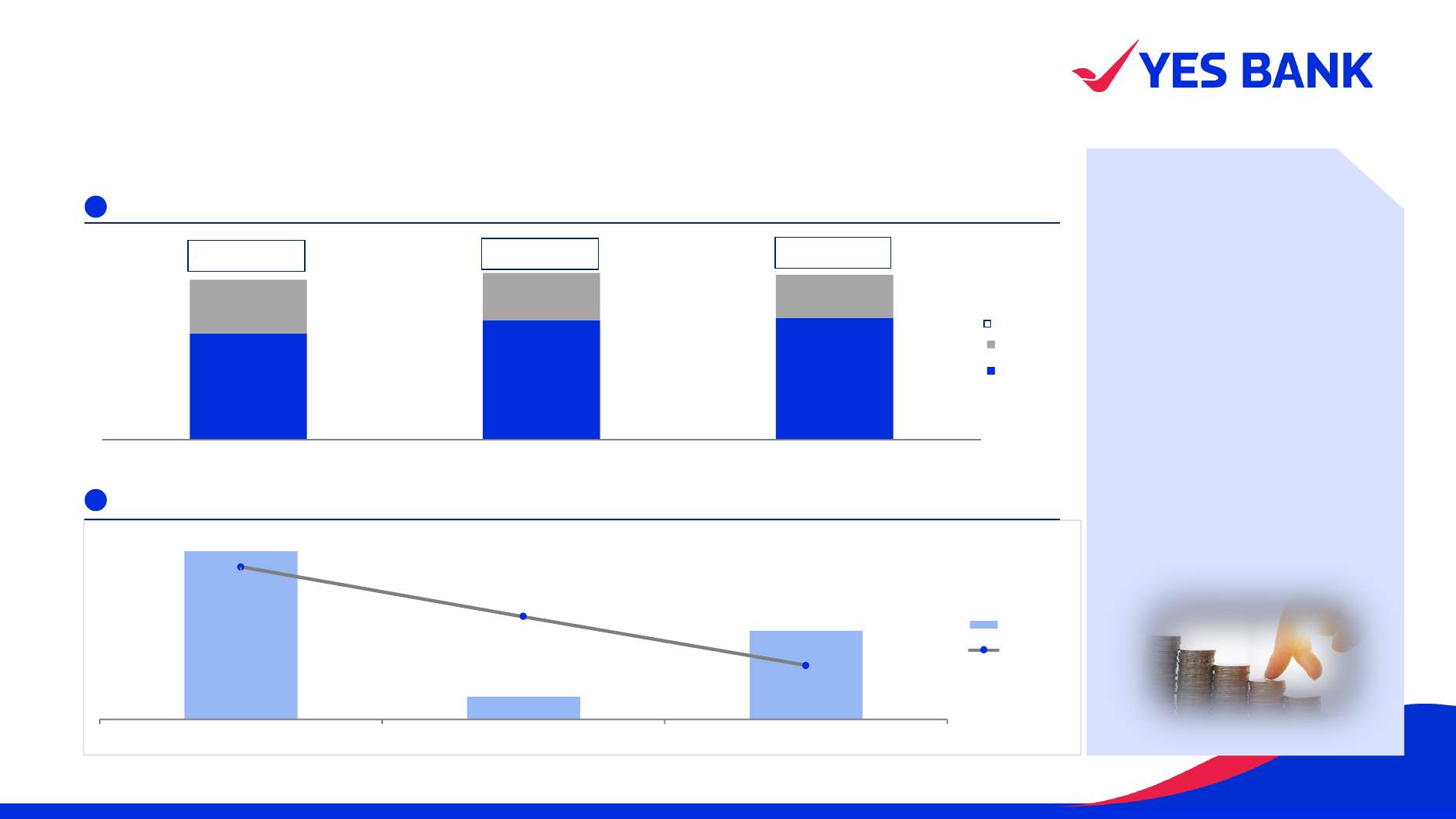

Strong people focus: Stable leadership with focus on up-skilling talent, objective

performance management & enabling employee flexibility

42

1

Data as on March 31, 2023

Net addition of 3,171 staff over the headcount of March 31, 2022

Average

Vintage

(in years)

27,517

2

5

8

Total

Band

Junior

Management

Middle

Management

Senior

Management

Top

Management

9

23,141

4,003

285

88

Q4FY23

1

Knowledge

Management

▪ YES School of Banking focusses on role and skill-specific trainings and certifications. Total 1,61,597

training days were clocked in FY23 with an average of 5.87 training days per employee.

▪ Over 75 team members from Anti-Money Laundering Team completed the CAMI Certification (Certified

Anti Money-laundering Investigator) and gained a thorough understanding of the pragmatic implications of

becoming an AML investigator when doing transaction analysis.

▪ The Bank has created an ‘Ideation Workflow’ which will facilitate employees to add their ideas (around

Transformation, Cost, Quality, Delivery, Speed and Behavioural) in a structured format.

Employee

Engagement

▪ The Bank has also been recognized among the TOP 50 in ‘India's Best Workplaces in BFSI 2023’

rankings by the Great Place to Work ® (GPTW) Institute.

▪ To engage with ex-YES BANKers and keep them updated with latest development in the BANK, an

Alumni Portal has been launched. The portal additionally provides ex-YES BANKers, access to certain of

their documents and offers an opportunity to refer friends/relatives who may want to explore career

opportunities at the Bank.

▪ The employees celebrated 3rd Foundation Day to commemorate the day when the Bank’s moratorium

was lifted i.e., 18

th

March.

▪ To celebrate and honor the women at YES Bank, sessions on ‘I am Enough’, ‘Breaking the Glass

Ceiling’ and ‘Holistic Living’ were conducted for employees on International Women’s Day. Additionally,

activities like Decoupage, Block printing on tote bag, Stained glass, Nail Art, Sound Healing, Skincare

Inside Out and Zumba sessions were arranged at various YES Bank locations.

▪ To create and nurture an inclusive culture, LGBTQ Awareness Webinar on breaking the stereotypes

was conducted by a TEDx speaker who is an activist in LGBTQ community.

D & I

Initiatives

Leadership

Development

▪ Top and Senior Management with average vintage of around 8.5 years within the Bank combined with

new talent from the industry.

▪ ‘Advanced Leadership Program’ (ALP), a three-day structured intervention was concluded for identified

Top & Senior Management executives. The program helped to further strengthen the leadership

capabilities and competencies and enhance the quality and depth of our internal leadership pool.

▪ Select Emerging Leaders from businesses participated in the ‘Emerging Leaders program’. This

program focused on Leading Self, Leading Others and Managing Business Competencies.

43

International Rating Long-term Outlook Short-term

Moody's Investors Service Ba3 Stable Not Prime

Domestic Rating Long-term Outlook Short-term

Basel III Basel II

Infra Bonds

AT I Tier II T I UT II LT II

CRISIL A- A- Positive A1+

ICRA BB A- BBB+ BBB+ A- A- Positive

India Ratings BBB+ A- Stable

CARE A- BBB A- A- Positive

Ratings across all

agencies at all time

lows:

March 2020

Moody’s

Upgrades

issuer rating to

Caa1 from Caa3

with a positive

outlook

March 16, 2020

Senior Rating & Outlook Upgrade:

ICRA: A-; Positive

India Ratings: A-; Stable

CRISIL: A-; A1+ short term; Positive

Moody’s : Ba3; Stable

INDIA Ratings

Outlook-keeps

Ratings Watch

Evolving (RWE)

March 18, 2020

ICRA Upgrades:

BASEL III Tier II to BB

BASEL II Upper Tier II to BB from D

BASEL II Lower Tier II to BB+ from D

Infrastructure Bonds to BB+ from D

Short Term FD/CD Programme to A4+

from D

March 24, 2020

ICRA Downgrades

Basel II Upper Tier II to D from BB

CARE Downgrades

Basel II Upper Tier II to D from C

Outlook-Credit Watch with

Developing Implications

June 23, 2020

August 3, 2020

Moody’s Upgrades

issuer rating to B3

from Caa1 with a

stable outlook

August 27, 2020

INDIA Ratings Upgrades

BASEL III Tier II to BBB- from B+

Infrastructure Bonds to BBB from BB –

Long Term Issuer Rating to BBB from BB-

ICRA Upgrades

BASEL III AT 1 to C from D

BASEL III Tier II to BBB- from BB

BASEL II Tier I to BB+ from D

BASEL II Upper Tier II BB+ from D

BASEL II Lower Tier II BBB from BB+

Infrastructure Bonds to BBB from BB+

September 11, 2020

CARE Upgrades:

BASEL III Tier II to BBB from C

BASEL II Tier I to BB+ from D

BASEL II Upper Tier II to BB+ from D

BASEL II Lower Tier II to BBB from B

Infrastructure Bonds to BBB from B

Outlook-Stable

November 9, 2020

November 10, 2021

Moody’s Upgrades

issuer rating to B2

from B3 with a

Positive outlook

October 12, 2022

CARE Upgrades

issuer rating to A-

from BBB+ with a

Positive outlook

August 2022

Credit Rating

Thank You

No representation or warranty, express or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of information or opinions contained herein. The information contained in this presentation is only current as of its date.

Certain statements made in this presentation may not be based on historical information or facts and may be “forward looking statements”, including those relating to YES Bank’s general business plans and strategy, its future financial condition and growth prospects, and future

developments in its industry and its competitive and regulatory environment. There is no assurance that such forward looking statements will prove to be accurate, as actual results may differ materially from these forward-looking statements due to a number of factors, including

but not limited to future changes or developments in the Bank’s business, its competitive environment and political, economic, legal and social conditions in India and other parts of the world. The forward-looking statements in this presentation are based on numerous

assumptions and these statements are not guarantees of future performance and undue reliance should not be placed on them. The Bank expressly disclaims any obligation to disseminate any update or revision of any information whatsoever contained herein to reflect any

change in such information or any events, conditions or circumstances on which any such information is based. This communication is for general information purpose only, without regard to specific objectives, financial situations and needs of any particular person. This

presentation does not contain all the information that is or may be material to investors or potential investors and does not constitute an offer or invitation or recommendation to purchase or subscribe for any shares/ securities in the Company and neither any part of it shall form

the basis of or be relied upon in connection with any contract or commitment whatsoever. The Bank may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such revision or changes. The communication of

this presentation may be restricted by law; it is not intended for distribution to, or use by any person in, any jurisdiction where such distribution or use would be contrary to local law, or regulation, or which would require any registration or licensing within such jurisdiction. If this

presentation has been received in error, it must be returned immediately to the Bank.

Disclaimer: