Internship Report

On

Financial Performance Analysis of

Janata Bank Limited (PLC)

Internship Report

On

Financial Performance Analysis of

Janata Bank Limited (PLC)

Submitted to

Controller of Examinations

National University

Gazipur-1704

Supervised by

Sanjida Islam

Senior Lecturer

Department of Business Administration

Daffodil Institute of IT (DIIT)

Submitted by

Tangila Akter Bithi

Roll No: 2020477

Reg. No: 19601000603

Session: 2019-2020

Major: Finance & Banking

Program: MBA

Daffodil Institute of IT (DIIT)

(Under National University)

Submission Date: November 14, 2023

I

LETTER OF TRANSMITTAL

Date: 14 November, 2023

Controller of Examinations

National University

Gazipur - 1704

Subject: Submission of Internship Report “Financial Performance Analysis of Janata

Bank PLC.

Dear Sir,

With utmost respect I would like to present this Internship Report on “Financial

Performance Analysis of Janata Bank plc, Khilgaon Branch, Dhaka, as a requirement

for completing my Master of Business Administration. I enjoyed preparing the report

though it was challenging to finish within the given time. This report provides me an

insight on the customer service department of Janata Bank. In this report I have tried

to find out some problem areas related to customer satisfaction of Janata Bank plc.

and tried to find out some possible solutions to those particular problems.

I have a strong belief that the report will fulfill your expectation and I have tried to

give my best effort so that I can prepare a solid report as per your instruction. I would

be very grateful if you accept my report. Your kind consideration and cooperation will

be highly appreciated.

Yours Obediently,

……………………………

Tangila Akter Bithi

Roll No: 2020477

Reg. No: 19601000603

Session: 2019-2020

Major: Finance & Banking

Program: MBA

Daffodil Institute of IT (DIIT)

II

SUPERVISORS ‘APPROVAL

This is to certify that, Tangila Akter Bithi, Reg: 19601000603 , Roll No : 2020477,

Session: 2019-2020, Major: Finance & Banking, MBA Program (Professional) is a

regular student of Final Semester of MBA program, Department of Business

Administration, She has Successfully completed internship report title on “Financial

Performance Analysis of Janata Bank plc, Khilgaon Branch, under my supervision

and monitoring. I wish her success at every sphere of life. To the best of my

knowledge, no part of this report has submitted for any degree or certificate.

Internship Supervisor

………………….........

Sanjida Islam

Senior Lecturer

Department of Business Administration

Daffodil Institute of IT (DIIT)

III

STUDENT DECLARATION

I do hereby declare that the report titled “Financial Performance Analysis of Janata

Bank plc, Khilgaon Branch, It is an original work done by me under the supervision

of Sanjida Islam, Senior Lecturer, Department of Business Administration, Daffodil

Institute of IT No part of this report has been previously submitted to any other

University/ College/ Institution/ Organization for any academic certificate/ degree/

diploma/ qualification.

The work that I have presented does not breach any existing copyright.

I further undertake to indemnify the department against any loss or damage arising

from breach of the foregoing obligation, if any.

Yours Obediently,

……………………………

Tangila Akter Bithi

Roll No: 2020477

Reg. No: 19601000603

Session: 2019-2020

Major: Finance & Banking

Program: MBA

Daffodil Institute of IT (DIIT)

iv

ACKNOWLEDGEMENT

This internship report has prepared through continuous study during my internship

period for three months. This work would not be possible without the cooperation and

assistance of some generous hands. Without which this would have not been possible.

Firstly, I would like to express my heartfelt gratitude to honorable Controller of

Examinations, authority of National University and to our honorable Principal for

providing me such an opportunity. Without their effort it would be impossible to bring

this report to the light. I specially want to acknowledge Md Sham Miah, Assistant

Manager of Khilgaon Branch, and Madhuri Rani Gosh, Principal Officer, for their

tremendous support, guidance and patience. Without their kind supervision, preparing

this report would have been very difficult. They provide me the guidance and

counseling during my entire internship program. Their continuous and well-thought

feedback enabled me to make this report a comprehensive one.I also would like thank

Oaj Uddin Ahmed, Senior Officer of Khilgaon Branch, Janata Bank plc.

I would like to express my sincere gratitude to my academic supervisor Sanjida Islam,

Senior Lecturer, Daffodil Institute of IT, for her constant guidance, supervision and

feedbacks which enabled me to prepare a well-executed report.

Above all, I want to acknowledge and most grateful almighty Allah, the most merciful

blessing me with patience and tenacity of mind to complete the requirements for the

degree successfully.

v

EXECUTIVE SUMMARY

At first, it reflects the core of the report. To fulfill the partial requirement of MBA

degree under National University of this report is to remarking the Financial

Performance Analysis to deal with business and so on. Where it uses some data that

get from personal observation, face to face conversation with bank officials and

Financial Performance Analysis as well as annual report, Financial Performance

Analysis related books, information from web to make these report perfect. Though

its face limitation such as short time to make these report. Janata bank ltd. is a state-

owned commercial bank of Bangladesh established in 1972. Its headquarters is

situated at Motijheel in Dhaka, the capital city of Bangladesh. The Bank emerged as ‘

Janata Bank’ by combining the erstwhile United Bank Limited and

Union Bank Limited under the Banks Nationalization Order (

President’s order – 26) of 1972 and was restructured as a limited company in

November, 2007.Janata Bank Limited, a corporate body trusted over the years, the

2nd largest (in respect of Deposits/Assets) commercial bank in Bangladesh, has been

playing pivotal role in overall financial activities of the country and is possessing a

long heritage of discharging laudable services to the society since its embankment

immediately after the emergence of this verdant rich alluvial soil as a sovereign,

independent state.

It has a well decorated product and service mix (saving bank account, current deposit

account, fixed term deposit, short term deposit, cash credit, long and short term

financing, house building loan etc.) for the customer for feeling comfortable towards

them. Quality service consider as their strength where lack of motivation considered

as their weakness. As the place is too much comparative busy place so they have

chance to improve but their banking rules and regulation may be threats for them.

Then,

vi

Table of Contents

CHAPTERS

Particulars

Page No.

Prefatory

Part

Letter of Transmittal

i

Supervisors ‘Approval

ii

Student Declaration

iii

Acknowledgement

iv

Executive Summary

v

Acronyms

List of Tables

List of Figures

Chapter - 1

Introduction

1.1 Origin of the Report

1

1.2 Objectives of the Report

1

1.3 Methodology of the Report

2

1.4 Scope of the Report

3

1.5 Limitations of the Report

3

Chapter- 2

Organizational Overview

2.1 Historical review

4

2.2 Vision

5

2.3 Mission

5

2.4 Main Objectives of Janata Bank Limited

5

2.5 Business Philosophy of Janata Bank Limited

5

2.6 Corporate Profile of Janata Bank Limited

6

2.7 Award & recognition of Janata Bank Limited

7

2.8 Successes of Janata Bank Limited

7

2.9 Product & Services of Janata Bank Limited

8-13

2.10 Green Banking

14

2.11 Key Milestones of Janata Bank Limited

14-16

vii

2.12 Organizational Structure of Janata Bank Limited

17

2.13 Future outlook of Janata Bank Limited

18

2.14 Corporate Social Responsibility of JBL

18

2.15 SWOT analysis of Janata Bank Limited

19-20

Chapter -3

Theoretical Framework

3.1 Theoretical Framework

21

3.2 Ratios analysis

21

3.3 Types of ratio analysis

21

3.4 Financial Analysis Tools

22

3.5 Horizontal Analysis

22

3.6 Horizontal/ Trend Analysis of Janata Bank PLC

23

3.7 Vertical Analysis:

24-28

Chapter-4

Analysis & Evaluation

4.1 Ratio Analysis of Janata Bank PLC

29

4.2 Current Ratio

29

4.3 Quick or Acid Test Ratio

31

4.4 Cash Reserve Ratio

32

4.5 Analyzing Activity

33

4.5.1 Cost to Income Ratio

33

4.5.2 Fixed Asset Turnover

35

4.5.3 Investment to Deposit Ratio

35

4.5.4 Cost of Deposit

37

4.5.5 Net Working Capital

38

4.6 Debt Ratio

40

4.6.1 Debt Equity Ratio

41

4.6.2 Equity Capital Ratio

42

4.6.3 Time Interest Earned Ratio

43

4.7 Analyzing Profitability

44

4.7.1 Operating Profit Margin

44

4.7.2 Net Profit Margin

46

4.7.3 Return on Asset

48

viii

4.7.4 Return on Equity

50

4.7.5 Earnings per Share

52

Chapter- 5

Findings, Recommendations & Conclusion

5.1 Findings of the report

53

5.2 Recommendations

54

5.3 Conclusion

56

Bibliography

57

ix

ACRONYMS

Acronyms

Elaborations

ADP

Annual Development Program

ATM

Automated Teller Machine

CSR

Corporate Social Responsibility

EPS

Earning Per Share

EM

Equity Multiplier

ETD

Equity to Deposit

ICMAB

Institute of Cost & Management Accountants of Bangladesh

IME

International Money Exchange

ICT

Information & Computer Technology

JBL

Janata Bank Limited

LC

Letter of Credit

LR

Loan Ratio

LTD

Loan to Deposit

NCB

National Commercial Bank

NAVPS

Net Assets Value Per Share

NGO

Non Govt. Organization

NRB

Non Resident Bangladeshi

OER

Operating Expenses to Revenue

ROA

Return on Assets

ROE

Return on Equity

ROI

Return on Investment

TLSC

Total Liabilities to Shareholders Capital

x

List of Table

Serial No.

Particulars

Page No.

1

2.1 Corporate Profile for JBL

6

2

2.2 Key Milestones of Janata Bank Limited

16-17

3

3.1 Horizontal/Trend Analysis of JBL

25

4

3.2 Common Size Balance Sheet

28-29

5

3.3 Common Size Analysis of JBL

29

6

4.1 Current Ratio of JBL

29

7

4. 2 Acid Ratio of JBL

31

8

4.3: Cash Reserve Ratio of JBL

32

9

4.4 Cost to Income

33

10

4.5 Investment to Deposit Ratio of JBL

33

11

4.6 Cost of Deposit of JBL

35

12

4.7 Net Working Capital of JBL

35

13

4.8 Debt Ratio of JBL

37

14

4.9 Debt Ratio of JBL

38

15

4.10 Time Interest Earned Ratio

40

16

4.11 Operating Profit Ratio of JBL

41

17

4.12 Net Profit Margin Ratio of JBL

42

xi

List of Figures

Serial No.

Particulars

Page No.

1

4.1 Current Ratio of JBL

29

2

4. 2 Acid Ratio of JBL

29

3

4.3: Cash Reserve Ratio of JBL

31

4

4.4 Cost to Income

32

5

4.5 Investment to Deposit Ratio of JBL

33

6

4.6 Cost of Deposit of JBL

33

7

4.7 Net Working Capital of JBL

35

8

4.8 Debt Ratio of JBL

35

9

4.9 Debt Ratio of JBL

37

10

4.10 Time Interest Earned Ratio

38

11

4.11 Operating Profit Ratio of JBL

40

12

4.12 Net Profit Margin Ratio of JBL

41

1

1.1 Origin of the report:

Although total MBA program combines an excellent blend of theoretical and

classroom knowledge but aside this Project program facilitates a student to bring light

on their theoretical knowledge to apply this in practical background. This report is

originated as fulfillment of the partial requirement for obtaining MBA degree from

Daffodil Institute of IT under the curriculum of National University, Bangladesh. This

report is titled as “Financial Performance Analysis of Janata Bank PLC” A Project

program at Janata Bank PLC to gather theoretical knowledge about banking activities.

I have worked at the Financing & Banking Department of the Janata Bank Ltd.

1.2 Objectives of the report:

I have some objectives behind the preparation of the report. The objective are

mentioned below-

Broad Objective:

The broad and overall objective of preparing this report is To observe and

evaluate overall financial performance of the Janata Bank PLC.

Specific Objectives:

To fulfill the partial requirement for obtaining MBA degree from Daffodil

Institute of IT under the curriculum of National University of Bangladesh.

To identify the financial situation of Janata Bank PLC.

To understand and analyze the financial strength of Janata Bank PLC.

To understand the analyzing and interpreting of financial ratios.

To recommend for improving the financial conditions of Janata Bank PLC.

2

1.3 Methodologies of the report:

All information included in this report has been collected from different sources. To

understand different conceptual matters I took help from the websites & different

published articles in the journals & records. The sources of information are divided

into two main ways which are mentioned below-

Primary sources:

Face- to- face conversation with the respective officers.

Conversation with the Deputy General Manager of Janata Bank PLC.

Relevant file study provided by the concerned officers.

Secondary sources:

Annual Report of Janata Bank PLC.

Official website of Janata Bank PLC.

Different manuals of Janata Bank PLC.

Record from Bangladesh Bureau of Statistics.

Data processing & Analysis:

Collected information have been processed & complied with the aid of MS Word,

Excel & other related computer software. Necessary tables have been prepared on the

basis of collected data and various statistical techniques have been applied to analyses

on the basis of classified information. Detail explanation and analysis have also been

incorporated in the report.

3

1.4 Scope of the report:

This report is based on my personal observation during my internship period at august

2023 to October 2023. Here, I tried to gather knowledge on the analytical aspects of

financial performance of Janata Bank PLC. This report would also focus on overall

financial performance & financial situation of Janata Bank PLC. Lastly, all the parts

of the report have been critically analyzes under the guidelines of Bank Companies

Act 1991 and a discussion on major findings and recommendations.

1.5 Limitations:

Limitation means the barriers which create problems in the track of completing any

activities. To prepare report in a short duration is not an easy task. In the time of

preparing the report some problems have been arise, which are:

The main problem of the study was inadequate information, which was

required for the study.

There are various information that the bank employee can’t provide due to

security and other corporate obligations.

Unavailable information in website.

Some of the information needed to explore the current market scenario of the

bank, was not disclosed.

During my Project period, I was assigned for a selected branch, which was .

So, it was tough to collect information from several branch.

Lack of adequate knowledge and analytical ability for preparing such report.

4

2.1 Historical review:

Janata Bank Plc is the second largest commercial bank in terms of net worth with 872

branches and fully owned by Government of Bangladesh. The mission of the bank is

to actively participate in the socio-economic development of the nation by operating a

commercially sound banking organization.

Immediately after the independence of Bangladesh in 1971, the Erstwhile United

Bank PLC and Union Bank PLC were nationalized and renamed as Janata Bank.

Janata Bank is a state owned commercial bank which was incorporated as a Public

PLC Company on 21 May 2008 as per Companies Act 1994 and took over the

business of the then Janata Bank with all of its assets, liabilities, right, power,

privilege and obligation on a going concern basis through a vendor agreement signed

between the People’s Republic of Bangladesh and Janata Bank PLC on 15 November

2008 with a retrospective effect from 1 July 2008. All of its operational activities are

governed by the Bank Companies Act 1991.

The Bank provides all kinds of commercial banking services to its customers

including accepting deposits, extending loan & advances, discounting & purchasing

bills, remittance, money transfer, foreign exchange transaction, guarantee,

commitments etc. The principal activities of its subsidiary are to carry on the

remittance of hard-earned foreign currency to Bangladesh. Janata Bank Ltd. has a

plan to switch over to a multi- disciplinary financial institution by conducting

Merchant Banking business and Islamic Banking operation. The Bank is not

depending only on interest earnings; rather it strives hard to go for fee-based income

from non fund activities of the bank. This type of business include capital market

operations like underwriting, portfolio management, mutual fund management,

investors' account as well as commission based business like Letter Of Guarantee,

Inland remittance, Foreign remittance etc. These businesses usually do not involve

Bank's fund, but on the contrary, offer immense opportunity and scope to expand

bank services to the members of public at large.

5

2.2 Vision:

To become the effective largest commercial bank in Bangladesh to support socio-

economic development of the country and to be leading bank in south Asia.

2.3 Mission:

Janata Bank PLC will be the effective commercial bank by maintaining a stable

growth strategy, delivering high quality financial products, providing excellent

customer service through an experienced management team and ensuring good

corporate governance in every step of banking network.

2.4 Main Objectives of Janata Bank PLC:

The main objective of JBL is to provide all types of banking services at doorsteps of

the people. The bank participates in various social and development programs and

also takes part in the implementation of various policies and promises made by the

government.

2.5 Business Philosophy of Janata Bank PLC:

Janata bank PLC a full service commercial bank with local & international

institutional shareholding is primarily driven by creating opportunities and pursuing

market niches not traditionally made by support the planned growth of its distribution

network and for its various segments.

The reason Janata bank is in business is to build a profitable and socially responsible

financial institution focused on market and business with growth potential thereby

assisting JANATA shareholders build a “just, enlightened, health, democratic and

poverty free Bangladesh”. That means to help make communities and economy of the

country stronger and to help people achieve their dreams as well. They fulfill the

purpose by reaching for high standards in everything we do. For their customers, for

their shareholders, their associates and their communities upon which the future

prosperity of their company rests.

6

2.6 Corporate Profile:

Name of Company

Janata Bank PLC

Registered Office

JanataBhaban 110, Motijheel C/A

Dhaka-

1000

Legal Status

Public PLC Company

Authorized Capital

Tk. 30,000 Million

Paid up Capital

Tk. 19,140 Million

Face value per share

Tk. 100 per share

Shareholding Pattern

100% Share owned by the Government of

the

Peoples Republic of Bangladesh

Tax Identification No.

001-200-2732

Vat Registration No.

9011050160

Chairman

Luna Shamsuddoha

CEO & Managing Director

Md. Abdus Salam Azad FF

Corporate Rating Status: Entity

Rating

As govt. owned Bank

A + in the long term ST-2 in the short term

AAA in the long term

ST-1 in the short term

Telex

675840JBDBJ, 671288 JBHOBJ

Phone P ABX

9560000, 9566020, 9556245-49,

9565041-

45, 9560027-30

Fax

88-02-9564644, 9560869

E-mail

Website

Www. janatabank-bd.com, jb.com.bd

Swift Code

JANBBDDH

Table: 2.1: Corporate Profile for JBL

Source: Website (https://www.janatabank-bd.com)

7

2.7 Award and Recognition:

Since its commencement back in 1972 Janata bank has earned plaudits time and again

from the global society. As a token of its acclamation the bank has been adorned with

a number of lofty awards and Recognition by esteemed organization of home and

abroad which testify the bank’s dedication towards professionalism, customer services

and success as well. The supercilious performance of the Bank translated into its

claiming laudation through appreciable contribution to the spurring economic

development of the country. Any recognition is enthralling as well as encouraging to

us that make us more pledge-bound towards delivering up-marked services to our

customers and thus to the society. These accolades will be our force in setting

milestones in days to come.

Janata bank awarded best tax payer award 2017-2018.CEO&MD of the bank

MD.Abdus Salam receives certificate from honorable Finance Minister Abul Mal

Abdul Muhit.

2.8 Successes of JBL in 2019:

Sustainable growth of Janata Bank Ltd. lies in the growth in loan & advances against

the growth in total assets and deposit. Some successes of JBL in 2019 are highlighted

below:

All Branches have gone to live Operation into online banking.

JBL crossed BDT 649,441 million in deposit.

JBL crossed BDT 459,580 million in loans & advances.

Received “ICAB Best Presented Annual Report Award” (1st position) from

The Institute of Chartered Accountants of Bangladesh (ICAB).

Received “ICMAB Best Corporate Award” from Institute of Cost and

Management Accountants of Bangladesh (ICMAB).

Received Best presented Annual Report & SAARC anniversary award from

The South Asian Federation of Accountants (SAFA).

Received “Citizen Service Innovation Award” from Ministry of Finance.

8

2.9 Product & Services of Janata Bank PLC:

Janata Bank PLC is always committed to serve the clients with the best values and

innovative products and services to enrich its portfolio.

1. Deposits:

a) Current & Call Deposits:

Current Deposit

Call Deposit

Deposit in Foreign Currency

Resident Foreign Currency Deposit

Deposits in FC (WES)

Convertible Taka A/C (D)

b) Savings Bank Deposits:

Savings Bank Deposit

Savings Deposit from foreign remittance

Q-Cash Deposit

NRB FC Deposit

School Banking Deposit

c) Monthly Scheme Deposits:

Deposit Pension Scheme

JB Savings Pension Scheme

Medical Deposit Scheme

Education Deposit Scheme

GhoreGhoreSanchay

JB Special Deposit Scheme

JB Monthly AmanatProkalpa

Janata Hajj Deposit Scheme

Janata Deposit Scheme

9

d) Term Deposits:

Fixed Deposit

JB Double Benefit Scheme

JB Monthly Benefit Scheme

Retirement Savings Scheme

JBL Retirement Savings Scheme

Continuous Benefit Account

e) Special Notice Deposit:

Special Notice Deposit

Convertible Taka A/C (SND

2. Loans & Advances:

a) Term Loan:

Industrial Credit (IC)

Housing Building Loan (General & Commercial)

Agro based Industry/Project Loan

Shipyard loan

Loan for Overseas Employment

Consumer Credit

b) Small and Medium Enterprise Loan:

Service Sector Loan

Trading Sector Loan

Manufacturing Sector Loan

c) Continuous Loan:

Cash Credit (Hypo)

Cash Credit (Pledge)

Export Cash Credit

Secured Overdraft (SOD)

10

d) Rural & Agro Credit:

Crop Loan

Fishery Loan

Animal Husbandry Loan

Agricultural Machineries Loan

Rural Transport Loan

Flower cultivation

e) Poverty Alleviation Program:

Supervised Credit Program

Small Farmers & Landless Laborers

Self-employment Scheme

GhoroaProkalpa/Family Based Micro Credit

f) Specialized Loan Program:

Cyber Café

Service holders Loan

Doctor's Loan Scheme

Special Credit Program for Women Entrepreneurs

g) Micro & Cottage industries loan:

Dairy/Poultry/Fish Culture

Loan for Handicrafts/Disabled People

NGO linkage loan

Weavers’ Credit

Swanirvar Loan

11

h) Import & Export Finance:

Loan Against Imported Merchandise (LIM)

Inland Bill Purchase (IBP)

Loan Against Trust Receipt (LTR)

Payment Against Document (PAD)

Packing Credit (PC)

Local/Foreign Bills Purchased (FBP)

Loan Against Export Development Fund (EDF)

Advance Against Cash Incentive (Subsidy, Assistance)

i) Letter of Credit:

Letter of Credit - at Sight

Letter of Credit – Usance

Back to Back L/C

3. Services:

a) Financial Services (Inland Remittance):

Demand Draft (DD)

Telephonic Transfer (TT)

Mail Transfer (MT)

JB remittance payment system (Deposit/withdrawal from any branch)

JB PIN cash System

b) Financial Services (Foreign Remittance):

Online Speedy Remittance

Maintaining NRT Account

Foreign MT

Foreign Remittance

Foreign Demand Draft

Collection of Draft, Cheque, TC

Foreign Currency Endorsement

12

c) Other Financial Services:

Pay Order

Pay Slip

Security Deposit Receipt (SDR)

d) Utility Services:

Gas Bills Collection

Electricity Bills Collection

Telephone Bills Collection

Water/Sewerage Bills Collection

Municipal Holding Tax Collection

Port Bill Collection

Land Rent Collection

e) ATM Service:

Cash withdrawal

Balance inquiry

Mini statement of accounts

Point of Sale (POS)

Mobile recharge

Tax payment

f) Welfare Service:

Payment of Non- Govt. Teachers’ Salaries

Payment of Primary and Secondary Girl Students Stipend

Payment of Army Pension/Civil Pension

Payment of Widows, Divorcees and Destitute Women Allowances

Payment of Old-age/Disabled Allowances

Food procurement bills

Issuance of Television License

Payment of Sanchayapatra

13

g) Service to the Government:

Sale of Prize Bond

Sale of Wage Earner Bond (WEB)

Sale of Sanchay Patra (SP)

VAT collection

Tax collection

Excise duty collection

h) Other Service:

Locker Service

SMS banking

Sale of Lottery Ticket

Foreign Currency Buying and Selling

Bangladesh Electronic Fund Transfer Network(BEFTN)

Bangladesh Automated Clearing House (BACH)

Debit Card Service

Credit Card Service

i) Customer Care:

Help/Information Desk

Inquiry Desk

Counseling

14

2.10 Green Banking:

Industrialization is one of the main causes of environment pollution. By investing in

various industry banks indirectly, accelerate pollution. To protect environment

pollution, JBL has taken prompt initiatives for environment friendly financing along

with in house measurement to protecting environment, conserving natural resources

and combating climatic changes. The bank practices curtailing paper-work and using

online/electronic transactions and financing to bio-gas plant, solar panel, renewable

energy plant, and tree plantation etc. It may be noted that JBL has allotted BDT 4,300

million in the bank’s overall annual credit budget for financing green banking

projects.

2.11 Key Milestones of Janata Bank PLC:

Key Milestones of JBL

2019

All Branches have gone to live Operation into online banking.

JBL crossed BDT 649,441 million in deposit.

JBL crossed BDT 459,580 million in loans & advances.

Received “ICAB Best Presented Annual Report Award” (1st position)

from

The Institute of Chartered Accountants of Bangladesh (ICAB).

2019 Received “ICMAB Best Corporate Award” from Institute of Cost

and

Management Accountants of Bangladesh (ICMAB).

Received Best presented Annual Report & SAARC anniversary award

from

The South Asian Federation of Accountants (SAFA).

Received “Citizen Service Innovation Award” from Ministry of Finance.

Received “ICMAB Best Corporate

Award” from

Institute of

Cost and

Management Accountants of Bangladesh (ICMAB).

15

2018

Launching of JB PIN Cash service.

Highest tax payer among the State Owned Commercial Banks.

Received “ICMAB Best Corporate Award” (1st position) from The

Institute of

Cost and Management Accountants of Bangladesh

2017

JBL Rewarded “Wholesale Banking Awards 2017” &“Retail Banking

Awards 2017”.

2016

Received “ICAB Corporate Governance Award” from The Institute of

Chartered Accountants of Bangladesh (ICAB).

Received “Asian Banking and Finance Awards 2016” from The Asian

Banking and Finance Magazine (ABF).

Incorporation of Janata Exchange Company, USA.

JBL crossed 900 Branches all over the country.

2015

Full automation of JBL branches. Enhancement of paid up capital to

BDT 19,140 million

2014 &

2015

JBL Rewarded “Wholesale B anking Awards” &“Retail Banking

Awards”&“Bank of the year Award” by Asian Banking and Finance

(CMG) Singapore.

2014

JBL at the top in CSR activities among the SCBs.

Landmark of BDT 400,000 million deposit.

2013 &

2015

JBL achieved highest operating profit among SCBs

2013

Launching of JBL CIB online system.

Launching BEFTN & EFT operation.

Inauguration of online banking.

2013 &

2014

Received “ICMAB Best Corporate Award” from

Institute of Cost and Management Accountants of Bangladesh

(ICMAB).

2011

Incorporation & commencement of Janata Capital & Investment Ltd.

Launching of BACH operation.

2010

Launching of speedy remittance service.

Issuance of 1st bonus share in JBL.

16

2009

Commencement of NRB branch.

2008

Incorporation and commencement of business as JBL.

2007 &

2010

Received “World Best Bank Award” from New York based financial

magazine global finance.

2005

Received “Asian Banking Awards” on credit scheme for handicapped

people from

Asian Bankers.

Association (ABA) & Bank Marketing Association of the Philippines

(BMAP).

2004

Received “Asian Banking Award” on Financing

program for

Association of the Philippines (BMAP).

2003

JBL crossed BDT 100,000 million of loans & advances.

2002

Incorporate of ATM service.

2001,

2005

JBL awarded “The bank of the year in Bangladesh” by London based

financial times group.

2000

Deposit crossed BDT 100,000 million.

1999

1st cash dividend paid.

1990

Launching 1st computer in JBL.

Table 2.2: Key Milestones of Janata Bank PLC Source: Website

(https://www.janatabank-bd.com)

17

Managing Director

Chairman

Assistant General Manager

Manager

Senior Executive Officer

Executive Officer

2.12 Organizational Structure of Janata Bank PLC:

Figure 2.1: Organizational Structure of Janata Bank PLC

Source: Website (https://www.janatabank-bd.com)

Support Staff

Assistant Executive Officer

General Manager

Deputy Managing Direct or

18

2.13 Future Outlook of Janata Bank PLC:

In this era of globalization, the business world is continuously changing and to keep

pace with the changes every organization needs to ensure continuous development to

achieve better competitive advantage and superior service quality over the

competitors. JBL is well positioned to meet the challenges of 2019 and will continue

to strive to innovate and capture opportunity for growth and value creation. The key

concentration areas of our management will be:

1. More focus on local business.

2. Retain market leadership.

3. Product Diversification with increased sales effort.

4. Exploring new client segments.

5. Capitalizing on the brand value.

6. Investing in Technology for Better Data Management & Improved Trade

Management

7. Implementing Planned Structural Changes.

8. Investing in our Human capital. We believe that our team work shall play a

vital role in reaching our target and achieve the corporate mission to be the

market leader by increasing market share.

2.14 CSR of Janata Bank PLC:

Janata bank has actively & fully adhered to the principles of sound corporate

governance. Fairness, transparency, accountability and responsibility are the

minimum standard of acceptable corporate behavior. Janata bank PLC continuous to

ensure the compliance of corporate governance as Securities and Exchange

Commission rules ®ulations. Janata bank considers socially responsible activities

an important part of its culture, identity and business practice. It has deep

commitment, loyalty & high sense of responsibility to our nation and its people. It

conforms to all of the stringent regulations issued by the government &Bangladesh

Bank. Some points are given bellow:

Post disaster assistance.

Sponsorship in sports.

Sponsorship in cultural activities.

Commercial loan to small and medium entrepreneurs.

19

Financing in poverty alleviation sector

Women entrepreneurs’ development scheme under SME.

Beautification of Dhaka city.

2.15 SWOT analysis of Janata Bank PLC:

SWOT analysis involves an examination of a firm’s strengths, weakness,

opportunities and threats. It should help to evaluate firm’s strategies to exploit its

competitive advantages or defend against its weakness. Strengths and weakness

involve identifying the firm’s internal abilities or lack thereof. Opportunities and

threats include external situation.

a) Strengths of Janata Bank Ltd:

Top management consisting efficient management group.

Company reputation with positive image in the banking industry.

Many branches to satisfy customer needs.

Various products and services for clients.

Corporate culture.

b) Weakness of Janata Bank Ltd:

Heavily depended on head office for decision making.

Absence of upgraded package.

Low remuneration package.

Not fully computerized.

Low promotional campaign.

20

c) Opportunities of Janata Bank Ltd:

Product line proliferation for introducing more branches.

Introducing special corporate scheme.

Developing new products and services.

d) Threats of Janata Bank Ltd:

The default risks of all terms of loan have to be minimizing in order to sustain in the

financial market. Because default risk leads the organization towards to bankrupt.

The low compensation package of the employees from mid-level to lower

level position threats the employee motivation.

Some commercial/ foreign as well as private banks.

Customer awareness of pricing & services.

21

3.1 Theoretical Framework

Theories are formulated to explain, predict, and understand phenomena and, in many cases, to

challenge and extend existing knowledge, within the limits of the critical bounding

assumptions. The theoretical framework is the structure that can hold or support a theory of a

research study. The theoretical framework introduces and describes the theory which explains

why the research problem under study exists.

3.2 Ratios analysis

Activity Ratio highlights the activity and the operational efficiency of the business concern.

The better managements of asserts the larger the amount of sales. Activity ratio measures the

relationship between the sales and the assets. Turnover ratios are employed to evaluate the

efficiency with which the firm manages and utilize s its assets. Their ratio indicates the speed

with which assets are brought converted as turn over into sales.

3.3 Types of ratio analysis

As an accountant, you can perform several ratio analyses. Each one assesses a

different aspect of a firm's finances. This allows you to establish a more

comprehensive picture of its financial wellbeing. The section below outlines five

types of ratio analysis:

Although there are many financial ratios businesses can use to measure their

performance, they can be divided into four basic categories.

Liquidity ratios.

Activity ratios (also called efficiency ratios)

Profitability ratios.

Leverage ratios.

22

3.4 Financial Analysis Tools:

Financial analysis tools are one of the most efficient ways that can be used for

ensuring good profit from investment. These financial analysis tools are highly

helpful in evaluating the market and investing in a way so as to maximize the profit

from the investments made. These financial analysis tools are useful for deciphering

both internal and external information related to a specific business organization. The

analysis and interpretation of financial statement is used to determine the financial

position and result of operation as well. The following are tools that are used for

analyzing the financial position of the company:

Horizontal Analysis

Vertical Analysis

Ratio Analysis

Economic value added (EVA) Analysis

Market Value Analysis

3.5 Horizontal Analysis:

Horizontal analysis involves calculating the percentage change of the categories of

financial statement overtime. For example, one may be interested in the trend of a

company’s operating expenses, By examining the percentage change from year one to

year two in operating expense, he/she can determine whether costs are shrinking or

growing. However, horizontal analysis has its drawbacks. This technique does not

take into account the changing size of business. Going back to the expense example, a

manager may be concerned that the company’s expenses are growing every year, but

if the business is growing, there is no cause for concern.

23

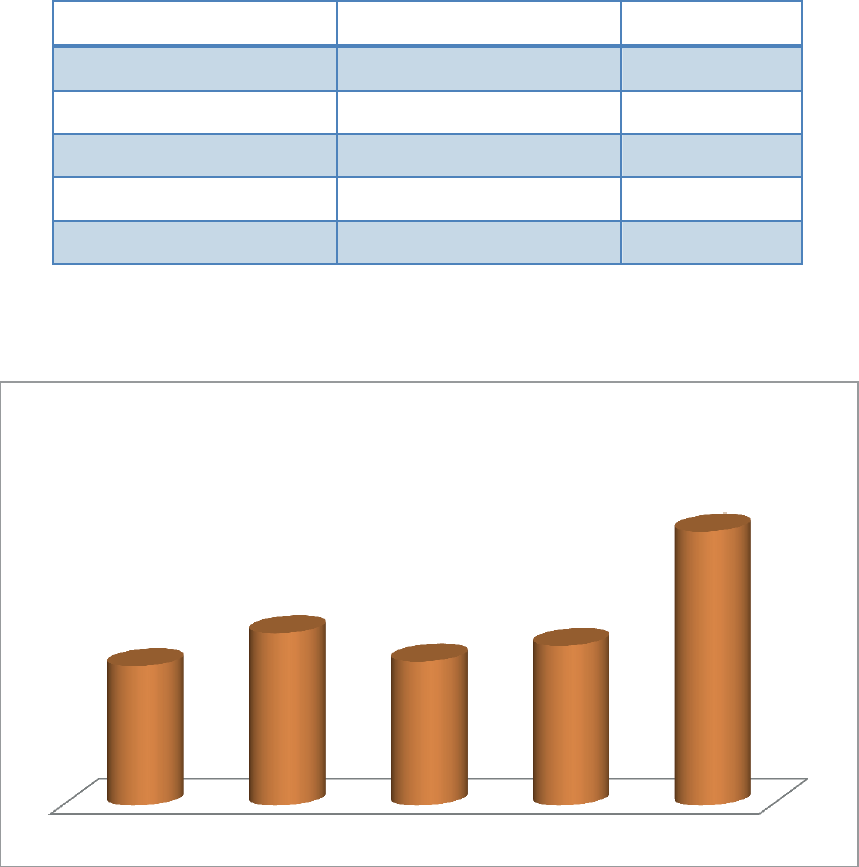

3.6 Horizontal/ Trend Analysis of Janata Bank PLC:

It is conducted by setting consecutive balance sheet, income statement or statement or

statement of cash flow side-by-side and reviewing changes in individual categories on

a year-to-year or multi year basis. The most important item revealed by comparative

financial statement analysis is trend.

Percentage change= (recent year – previous year)/ Previous year

Table: 3.1: Horizontal/Trend Analysis of JBL Source: JBL Annual Report

Item (Figure In

Millions)

2020

%

2019

%

2018

Paid up

Capital

19,140.00

0

19140.00

0

19140.00

Shareholders’

Equity

51,363.33

2.95%

49889.66

.69%

49547.44

Total assets

805,988.41

3.52%

778603.91

12.73%

690667.66

Total deposits

649,440.78

1.19%

641819.15

12.82%

568911.14

Total Loans &

Advances

459,580.05

14.03%

403037.42

15.20%

349861.30

Total

Investment

177,342.15

-2.40%

233274.87

6.45%

219150.10

Operating

Income

11,369.48

13.26%

10038.28

-6.36%

10720.50

Total

Expenditure

54364.25

2.22%

44489.80

-1.04%

44958.32

Profit Before

Provision &

Tax

11,369.48

1.32%

10038.28

-6.36%

10720.50

Profit Before

Tax

4,210.05

15.34%

3650.16

-44.36%

6560.05

Net Profit

After Tax

2,686.50

.31%

2605.48

-45.81%

4807.88

24

A comparison of statements over several years reveals direction, speed and extent of a

trend(s). The horizontal financial statements analysis is done by restating amount of

each item or group of items as a percentage. Such percentage are calculated by

selecting a base year and assign a weight of 100 to the amount of each item in the

base year statement. Thereafter, the amounts of similar items or groups of items in

prior or subsequent financial statements are expressed as percentage of the base year

amount. The resulting figures are called index numbers or trend ratios. The above

analysis shows that JBL performance trend is quite better in 2018 than 2019. Their

capital was same in 2018& 2019 but the stockholders equity has increased in 2018

compared to 2019.

3.7 Vertical Analysis:

Vertical analysis is the process of reporting each item on a set of financial statements

as a percentage of a large item. On the income statement, items are usually reported as

percentage of sales, and on the balance sheet items are usually reported as a

percentage of total assets. A single vertical analysis is not very useful to most

managers, but using the result of a vertical analysis to compare ratios across time or to

see how a company measures up to industry benchmarks can help a management team

determine areas of strength and weakness.

3.7.1Vertical/Common Size Analysis of Janata Bank PLC:

Vertical/Common size statement came from the problems in comparing the financial

statements of firms that differ in size. In the balance sheet, for example, the assets as

well as the liabilities and equity are each expressed as 100% and each item in these

categories is expressed as a percentage of the respective totals. In the common size

income statement, turnover is expressed as 100% and every item in the income

statement is expressed as a percentage of turnover (sales). Here bank has no sales so

that I have consider the operating income as 100%.

25

Balance Sheet As on December 31, 2020 & 2019

Common size Balance sheet

As on December 31, 2020

& 2019

Particular

2020 (In

Millions)

2019 (In

Millions)

2020 (%)

2019 (%)

Property and Assets:

46629.25

42546.86

5.99%

6.16%

Cash in Hand

4465.97

4588.33

.57%

.66%

Balance with

Bangladesh Bank &

Agent Bank

42163.28

37958.53

5.42%

5.50%

Balance with

other Banks and

Financial Institutions

24379.16

14295.23

3.13%

2.07%

Money at call & short

notice

2024.35

1728.36

.26%

.25%

Investment

233274.87

224273.17

29.96%

32.47%

Loans and Advances

403037.42

349861.30

51.76%

50.66%

Fixed Assets

10573.26

10033.61

1.36%

1.45%

Non-banking other

Assets

58685.60

47929.13

7.54%

6.94%

Total Property

and

Assets

778603.91

690667.67

100%

100%

Liabilities and

Shareholders’

Equity: Capital

borrowing from other

banks

7432.05

4628.68

.95%

.67%

Deposits and

other accounts

6418119.15

568911.14

82.43%

82.37%

Other Liabilities

79463.04

67580.41

10.21%

9.78%

Total Liabilities

728714.25

641120.22

93.59%

92.83%

26

Capital/Shareholders’

Equity

49889.66

49547.44

6.41%

7.17%

Total Liabilities and

Shareholders’ Equity

778603.91

690667.67

100%

100%

Table: 3.2: Common Size Balance Sheet Source: JBL Annual Report

From the vertical analysis above, we can compare the percentage mark-up of asset

item and how they have been financed. The strategies may includes increase/decrease

the holding of certain assets. The analyst may as well observe the trend of the increase

in the assets and liabilities over several years. It can be observed that there is an

increase in the holding of the current assets of the company. The management can

seek the reasons of why the holding of these assets is continuously increasing. Though

both the assets and liabilities are increasing but proportionately liabilities were a little

higher than total assets, which may make some ratio lower. The above analysis also

shows that’s total liabilities has increased so as stock holder’s equity, which indicated

that JBL has more debt financing than equity.

Common Size profit and Loss Account For the year ended December 31, 2020 & 2019

Particulars

2020

Taka

2019

Taka

Operating Income Interest

Income

Interest Paid on Deposits and

31,145,611,896

31,897,904,514

Borrowings etc.

27,093,672,662

31,331,304,819

Net Interest Income

Investment Income

4,051,939,234

566,599,695

Commission, Exchange and

14,414,821,862

16,416,874,024

Brokerage

4,910,829,124

4,204,025,685

Other Operating Income

Total Operating Income (A)

2,000,706,200

1,828,263,232

27

25,378,296,420

23,015,762,636

Operating Expenses

Salary and Allowances

Rent, Taxes, Insurance,

Electricity etc.

10,003,832,785

9,523,977,793

Legal Expenses

1,186,583,912

948,388,647

Postage, Stamp,

Telecommunication etc.

27,346,213

39,374,927

Stationery, Printings,

256,649,643

114,781,413

Advertisements etc.

Chief Executive's Salary and

237,765,433

240,740,609

Fees

Directors' Fees

4,296,774

4,800,000

Auditors' Fees

Depreciation, Repair and

4,344,000

3,800,000

Maintenance

8,673,652

9,458,346

Other Operating Expenses

843,255,279

750,517,858

Total Operating Expenses (B)

1,436,070,814

1,341,637,639

Profit/(Loss) before Provision

14,008,818,505

12,977,477,232

& Tax (C) = (A-B)

Provision for Loans and Advances

11,369,477,915

10,038,285,404

Provision for Off-balance

Sheet Exposures

4,059,525,949

3,696,393,387

Provision for Other Assets

Provision for Employee

293,600,00

(163,600,983)

Benefits

Provision for Diminution in

850,000,000

1,041,302,742

28

Value of Investments

2,081,618,836

1,760,000,000

Other Provisions Total Provisions (D)

(250,000,000)

124,680,316

-

54,025,

183

Net Profit/(Loss) before Taxes

7,159,425,101

6,388,120,329

(E) = (C-D)

Provision For Taxation

4,210,052,814

3,650,165,075

(including Ruler Tax) (F)

Current Tax

1,523,553,732

1,044,689,061

Deferred Tax

1,676,093,445

2,046,795,333

(152,539,713)

(1,002,106,272)

Net Profit/(Loss) after

Taxation (G) = (E-F)

2,686,499,082

2,605,476,014

Table: 3.3: Common Size Analysis of JBL Source: Annual Report of JBL

29

4.1 Ratio Analysis of Janata Bank PLC:

Ratio analysis is a family of techniques that involves computing common ratios of

different balance sheet and income statement categories and compeering these ratios

to those of other companies of widely established benchmark. Some ratios, such as

profit margin or return on assets, are so common that they are part of the business

vernacular. Others, such as days sales outstanding or collection cycle, may be initially

unfamiliar but quite useful. A ratio exists for nearly every business metric, so learning

these tools can be daunting; however, the ability to precisely gauge performance is

useful when investigating specific concerns about a firm.

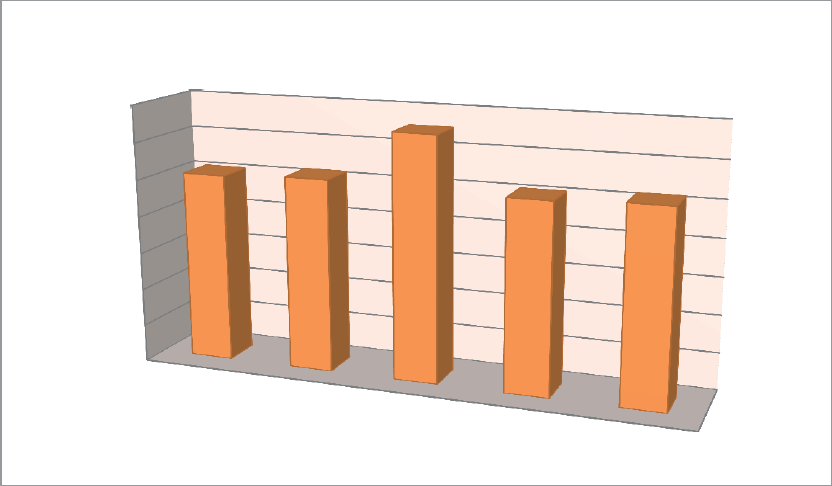

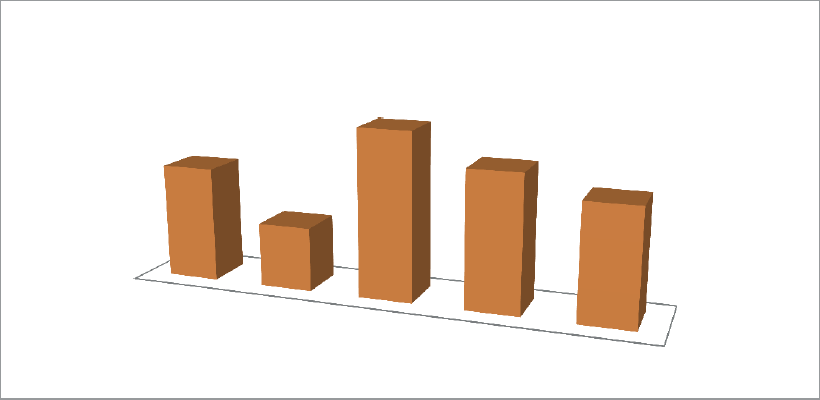

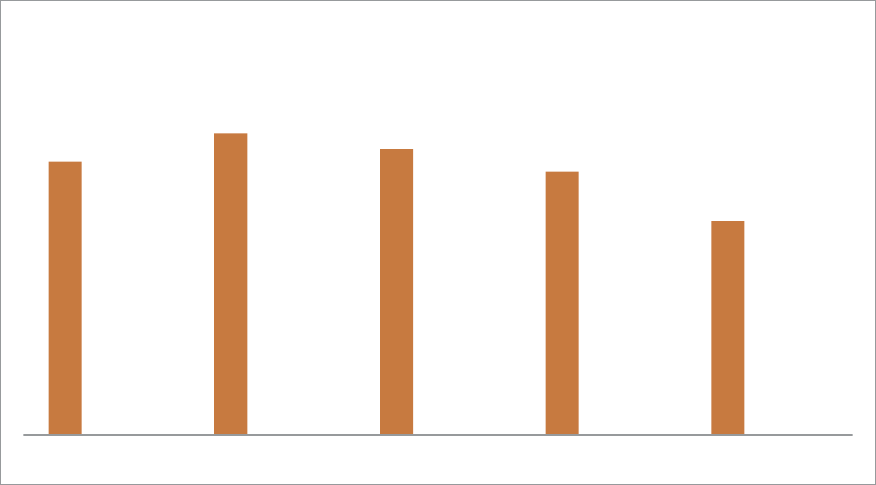

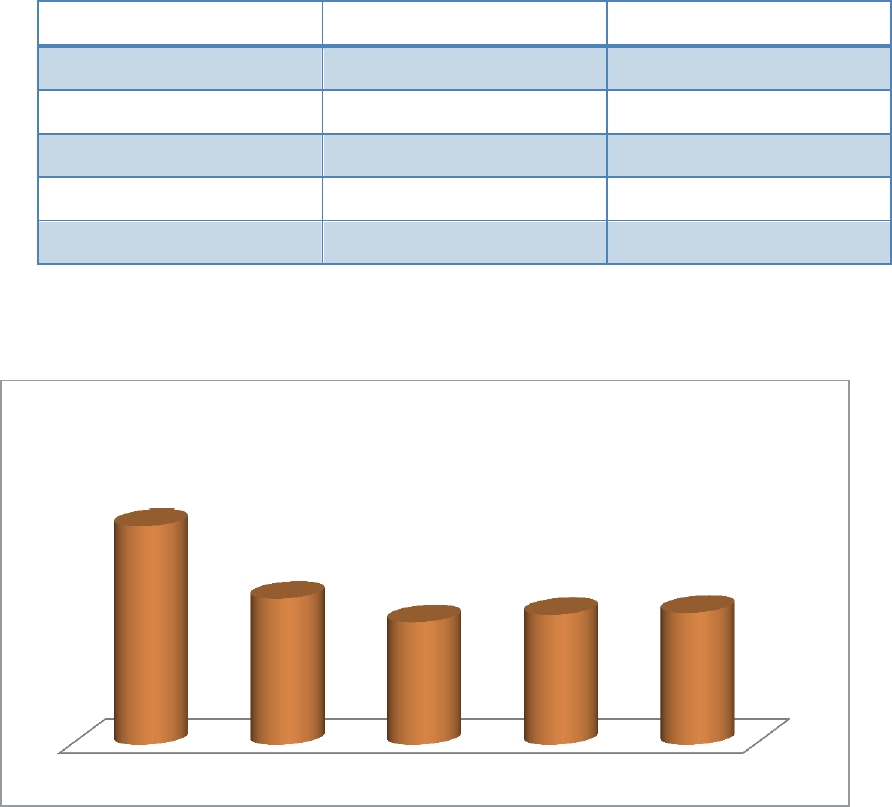

4.2 Current Ratio:

The current ratio, one of the most commonly cited financial ratios, measures the

bank’s ability to meet its short term obligations. The higher the current ratio, the

better the liquidity position of the bank. It expressed as:

Current Ratio = Current Assets / Current Liabilities

Table: 4. 1: Current Ratio of JBL Source: Annual Report of JBL

Year

Calculations

Ratio(Times)

2022

426636.64/410503.03

1.04

2021

345385.82/335978.66

1.02

2020

314186.75/305702.73

1.31

2019

285730.53/275583.75

1.04

2018

227309.99/219102.72

1.02

30

Current Ratio

1.4

1.2

1

0.8

0.6

0.4

0.2

0

2018

2019

2020

2021

2022

Graphical Presentation

Figure: 4.1: Current Ratio of JBL

Source: Annual Report of JBL

The higher the current ratio; the more liquid the firm is considered to be. But JBL,

current ratio is good because it maintains higher current assets against current

liabilities whereas normally banking industry maintain 2:1 current ratio. This Graph

shows that, the current ratio is increased in year 2019 and decreased the following

year.

31

Acid Test

Ratio

1.31

1.04

1.04

1.02

1.04

2018

2019

2020

2021

2022

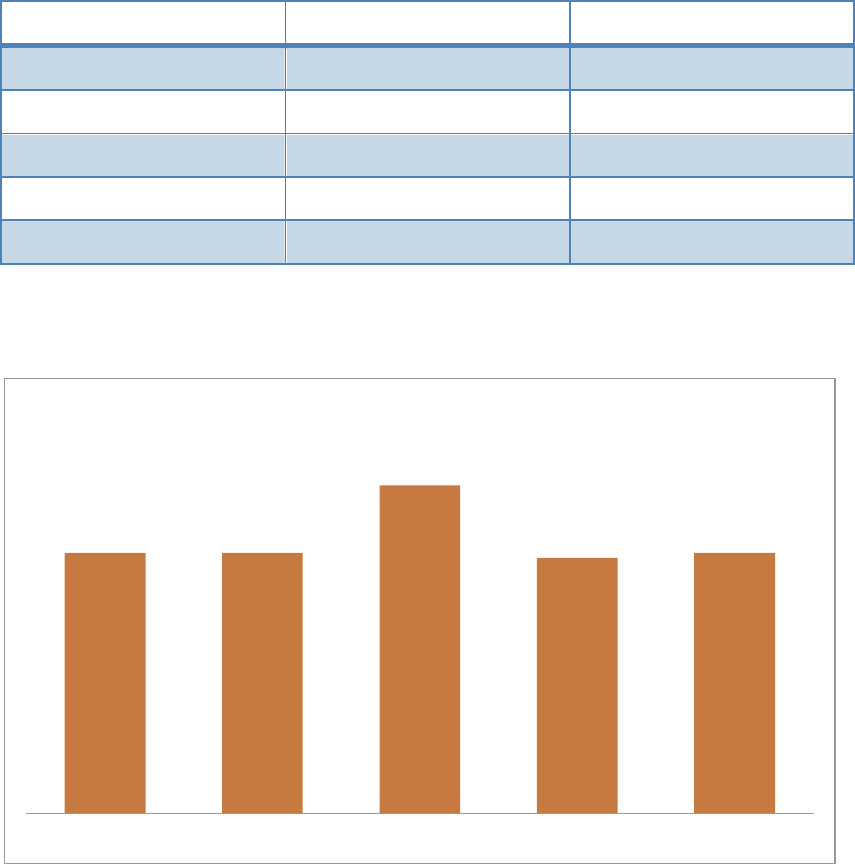

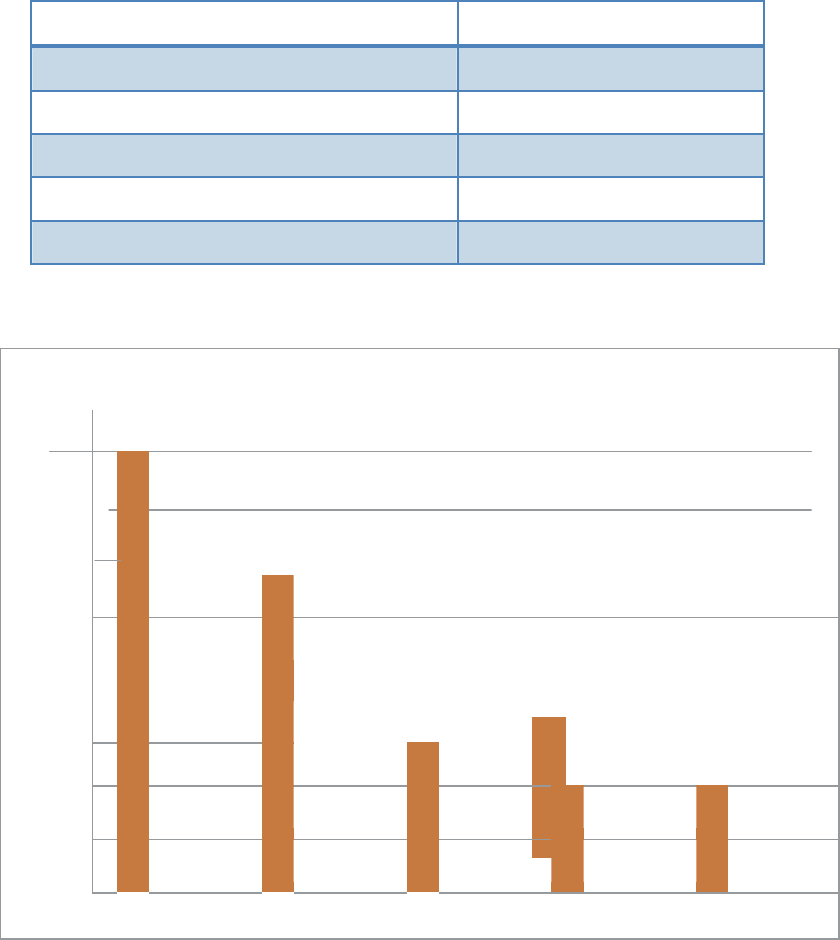

4.3 Quick or Acid Test Ratio:

A stringent indicator that determines whether a bank has enough short-term assets to

cover its immediate liabilities without selling inventory. The acid-test ratio is far more

strenuous than the working capital ratio, primarily because the working capital ratio

allows for the inclusion of inventory assets. It is expressed as:

Quick or Acid Test Ratio: (Current Assets – Inventory – Prepaid Expenses) / Current

Liabilities

Table: 4. 2: Acid Ratio of JBL Source: Annual Report of JBL

Year

Calculations

Ratio

2022

426636.64/410503.03

1.04

2021

345385.82/335978.66

1.02

2020

314186.75/305702.73

1.31

2019

285730.53/275583.75

1.04

2018

227309.99/219102.72

1.02

Graphical Presentation

Figure: 4.2: Acid Test Ratio of JBL Source: Annual Report of JBL

32

Banks with ratios of less than 1 cannot pay their current liabilities and should be

looked at with extreme caution. Furthermore, if acid-test ratio is much lower than the

working capital ratio, it means current assets are highly dependent on inventory. The

standard ratio is 1:1. But the Acid test ratio of JBL is poor than standard. To improve

this ratio, the JBL has to increased the cash, short-term investment & receivable and

reduce the current liability.

4.4 Cash Reserve Ratio:

The Cash Reserve Ratio is the amount of funds that the banks are bound to keep with

Bangladesh Bank as a portion of their Net Demand and Time Liabilities (NDTL). The

objective of CRR is to ensure the liquidity and solvency of the Banks. The CRR is

maintained fortnightly average basis.

Under CRR a certain Percentage of the total bank deposits has to be kept in the

current account with RBI which means banks do not have access to that much amount

for any economic activity or commercial activity.

Cash Reserve Ratio = Cash and Marketable Securities / Total Current Liabilities

Table: 4.3: Cash Reserve Ratio of JBL Source: Annual Report of JBL

Year

Ratio

2022

6.74%

2021

6.49%

2020

6.83%

2019

5.70%

2018

6.26%

33

Cash

Reserve Ratio

6.83%

6.26%

6.49%

6.26%

5.70%

2018

2019

2020

2021

2022

Graphical Presentation

Figure: 4.3: Cash Reserve Ratio of JBL Source: Annual Report of JBL

The higher the cash reserve ratio the better the bank’s overall financial performance.

Here the CRR was low in 2019 than 2018. Then it began to be the highest in 2019 and

lowering in the following years. It should be maintain according to the demand of the

people of the country.

4.5 Analyzing Activity:

Activity ratios measure the speed with which accounts are converted into sale or cash.

With regard to current accounts measures of liquidity are generally inadequate

because difference in the composition of a firm’s current accounts can significantly

affects its true liquidity. A number of ratios are available for measuring the activity of

the important current accounts, which includes inventory, accounts receivable, and

account payable. The activity (efficiency of utilization) of total assets can also be

assessed.

4.5.1 Cost to Income Ratio:

It measures a particular Bank’s operating efficiency by measuring the percent of the

total operating income that the Bank spends to operate its daily activities. It is

calculated as follows:

Cost to Income Ratio = Total Operating Expenses / Total Operating Income Cost to

34

Cost to Income Ratio

Income Ratio (CIR) of Janata Bank PLC:

A ratio that shows the efficiency of a company’s management by comparing operating

expenses to net sales or operating incomes. It can be calculated as:

Cost to Income = Total Operating Expenses / Total Operating Income (Revenue)

Table: 4.4: Cost to Income Source: Annual Report of JBL

Year

Ratio

2022

70.65%

2021

77.98%

2020

81.06%

2019

80.75%

2018

81.59%

Graphical Presentation

82.00%

80.00%

78.00%

76.00%

74.00%

72.00%

70.00%

68.00%

66.00%

64.00%

2019

2018

2020

2021

2022

Figure: 4.4: Cost to Income Ratio Source: Annual Report of JBL

35

We know that this ratio measures the operating efficiency of the bank by measuring

the portion if the total operating costs relative to the total operating income of that

bank and the higher the ratio, the lower the operating efficiency. In 2018 the operating

cost of JBL is low but after that is increasing is recent year. So it can be said that the

operating efficiency of the JBL is in good position compared to the past years that is

they are not in good position to minimize their operating cost.

4.5.2 Fixed Asset Turnover:

A Financial ratio of net sales to fixed assets. The fixed-asset turnover ratio measures a

company’s ability to generate net sales from fixe-dasset investments – specifically

property, plant and equipment- net of depreciation. A higher fixed-asset turnover ratio

shows that the company has been more effective in using the investment in fixed

assets to generate revenues. The fixed-asset turnover ratio is calculated as:

Fixed Asset Turnover = Gross Turnover / Net fixed asset

4.5.3 Investment to Deposit Ratio:

Investment to Deposit ratio shows the operating efficiency of a particular Bank in

promoting its investment product by measuring the percentage of the total deposit

disbursed by the Bank as long and advance or as investment.

The ratio is calculated as follows:

Investment to Deposit Ratio = Total Investment / Total Deposits

Investment to Deposit Ratio of Janata Bank PLC:

It is expressed as:

36

Investment to Deposit Ratio

Investment to Deposit Ratio = Total Investment / Total Deposit

Table: 4.5: Investment to Deposit Ratio of JBL Source: Annual Report of JBL

Year

Calculation

Ratio

2022

233274.87/641819.15

0.3635

2021

219150.10/568911.14

0.3852

2020

196713.53/516010.74

0.3812

2019

193279.63/478535.57

0.4039

2018

108342.04/409767.01

0.2644

Graphical Presentation:

0.5

0.4

0.3

0.2

0.1

0

2018

2019

2020

2021

2022

Figure: 4.5: Investment to Deposit Ratio of JBL Source: Annual Report of JBL

Investment to Deposit Ratio shows that amount of deposit which is used to as

investment. JBL’s investment to deposit ratio is fluctuating year by year. That means

Bank is not properly utilization their deposit.

37

4.5.4 Cost of Deposit:

The Cost of Deposit is one of several ways to set the changing interest rates on

adjustable-rate mortgages, or ARMs in conjunction with Treasury bills, prime rates,

and the Bangladesh Bank offered Rate. This percent is calculated using the average of

the last 12 monthly average yields of CDs that have been traded for at least three

consecutive months, based on the reports of the Bangladesh Bank Reserve Board.

Cost of Deposits = Interest paid on Deposit / Total Deposits Cost of Deposit of Janata

Bank PLC:

It is a combination of a number of components.

The rate paid out to the depositor

The Central Cash and Reserve Liquidity Requirement

The compensation paid to the branch or the sales team that booked the deposit

Any additional tangible or non-tangible incentives offered or paid to the depositor or

sales team when you combine these factors across all products and depositors across

the bank you get the cost of deposit for the bank.

Cost of Deposits = Interest paid on Deposit / Total Deposits

Table: 4.6: Cost of Deposit of JBL Source: Annual Report of JBL

Year

Ratio

2022

7.02%

2021

7.75%

2020

7.34%

2019

6.76%

2018

5.49%

38

Cost of Deposit

7.75%

7.02%

7.34%

6.76%

5.49%

2018

2019

2020

2021

2022

Graphical Presentation:

Figure: 4.6: Cost of Deposit of JBL Source: Annual Report of JBL

Cost of deposit is considered as the profit on every deposit that is earned by the bank.

The above ratio shows that cost of deposit is going to be decreased in following years

from 2017 to 2019 which shows the decreasing income of JBL. JBL should increase

its cost of deposit.

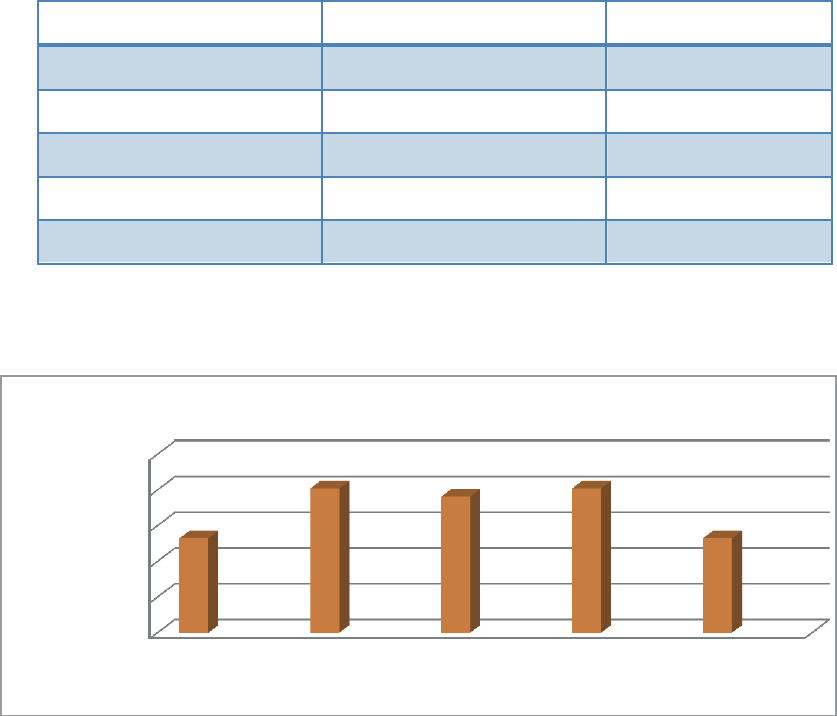

4.5.5 Net Working Capital:

Net working Capital, although not actually a ratio is a common measure of a firm’s

overall liquidity. A measure of liquidity is calculated by subtracting total current

liabilities from total current assets.

Net Working Capital = Total Current Assets – Total Current Liabilities Net

Working Capital of Janata Bank PLC:

Net working capital, although not actually a ratio is a common measure of a firm’s

overall Liquidity as a measure of liquidity ratio calculated by.

39

Net Working Capital

16133.61

10146.74

9407.16

8207.27

8484.02

2018

2019

2020

2021

2022

Net Working Capital = Current Asset – Current Liabilities

Table: 4.7: Net Working Capital of JBL Source: Annual Report of JBL

Year

Calculation

Ratio

2022

426636.64-410503.03

16133.61

2021

345385.82-335978.66

9407.16

2020

314186.75-305702.73

8484.02

2019

285730.53-275583.75

10146.74

2018

227309.99-219102.72

8207.27

Graphical Presentation

Figure: 4.7: Net Working Capital of JBL Source: Annual Report of JBL

Net working capital of JBL is slightly increased during the last two year. However,

the bank faced problems to meet up its current obligations. So the Bank should

increase its current asset more and more.

40

4.6 Debt Ratio:

The debt ratio measures the proportion of total assets provided by the firm’s creditors.

Debt Ratio = Total Liabilities / Total Assets Debt Ratio of Janata Bank:

The debt ratio measures the preparation of total assets provided by the firm’s

creditors.

Debt ratio = Total Liabilities/Total Assets

Table: 4.8: Debt Ratio of JBL Source: Annual Report of JBL

Year

Calculation

Ratio

2022

728714.25/778603.91

.936

2021

641120.23/683157.58

.939

2020

589992.60/629454.14

.937

2019

548966.78/586082.99

.937

2018

493923.73/511129.41

.966

Graphical Presentation

Figure: 4.8: Debt Ratio of JBL

Source: Annual Report of JBL

Debt Ratio

0.97

0.965

0.96

0.955

0.95

0.945

0.94

0.935

0.93

0.925

0.92

2018

2019

2020

2021

2022

41

The higher the ratio, the greater risk will be associated with the firms operations. In

addition, high debt to asset ratio indicates low borrowing capacity of a firm, which in

turn will lower firm’s financial flexibility. This graph shows that, the debt ratio was

decreasing year by year. The Debt ratio measures the proportion of total assets

provides by the firm’s creditors. Their debt ratio was mostly decreasing trend that

indicates positive sign.

4.6.1 Debt Equity Ratio:

The debt-equity ratio (D/E) is a financial ratio indicating the relative proportion of

shareholders’ equity and debt used to finance a company’s assets. Closely related to

leverage, the ratio is also known as risk, gearing or leverage. The two components are

often taken from the firm’s balance sheet or statement of financial positi,obnut the

ratio may also be calculated using market values for both, if the company’s debt and

equity are publicly traded, or using a combination of book value for debt and market

value for equity financially. The formula for calculating D/E ratios is:

Debt / Equity Ratio = Total Liabilities / Shareholders’ Equity Debt Equity Ratio

of Janata Bank PLC:

The debt-to-equity ratio is a measure of the relationship between the capital

contributed by creditors and the capital contributed by shareholders. It also shows the

extent to which shareholders’ equity can fulfill a company’s obligations to creditors in

the event of liquidation.

Debt/Equity Ratio = Total Liabilities / Shareholders’ Equity

Table:4.9: Debt Ratio of JBL Source: Annual Report of JBL

Year

Ratio (Times)

2022

11.86

2021

10.48

2020

12.08

2019

13.13

2018

24.09

42

Debt/Equity Ratio

Series 1 Series 2 Series 3

24.09

13.13

12.8

10.48

11.86

2018

2019

2020

2021

2022

Graphical Presentation:

Figure: 4.9: Debt / Equity Ratio of JBL Source: Annual Report of JBL

Debt/Equity (D/E) Ratio, calculated by dividing a company’s total liabilities by its

stockholders’ equity, is a debt ratio used to measure a company’s financial leverage.

The above D/E ratio indicates how much debt a company is using to finance its assets

relative to value of shareholders’ equity which is decreasing from 2015 to 2018. Buitt

quietly increase in 2021 which shows the incapability of JBL.

4.6.2 Equity Capital Ratio:

The ratio shows the position of Bank’s owner’s equity by measuring the portion of

total asset financed by the shareholders invested funds it is calculated as follows:

Equity Capital Ratio = Total Shareholder’s Equity / Total Assets The Ability to

Service Debt:

It refers the ability of a firm to meet the contractual payments required on a scheduled

basis over the life of a debt. The firm’s ability to meet certain fixed charges is

measured using coverage ratios.

43

Time Interest Ratio

0.529

0.354

0.297

0.315

0.32

2018

2019

2020

2021

2022

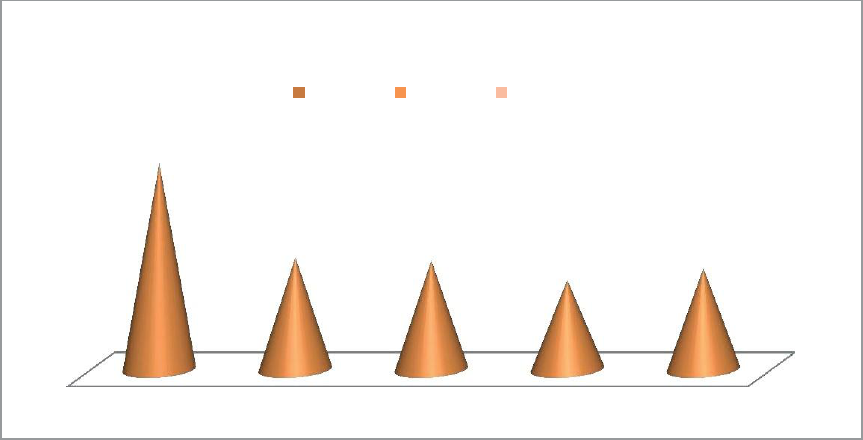

4.6.3 Time Interest Earned Ratio:

This ratio measures the ability to meet contractual interest payment that means how

much the company able to pay interest from their income.

Time Interest Earned Ratio of Janata Bank PLC:

The times interest earned ratio, sometimes called the interest coverage ratio, measures

the firm’s ability to make contractual interest payments.

Time Interest Earned Ratio = Earnings before Interest and Taxes / Interest Expense

Table: 4.10: Time Interest Earned Ratio Source: Annual Report of JBL

Year

Calculation

Ratio

2022

10038.28/31331.30

.320

2021

10720.50/33982.70

.315

2020

10683.34/35984.27

.297

2019

12127.10/34212.83

.354

2018

14533.79/27499.16

.529

Graphical Presentation:

Figure: 4.10: Time Interest Earned Ratio of JBL Source: Annual Report of JBL

44

Time Interest earned ratio on JBL’s is satisfying in 2018 but in last four years it was

slightly decreasing. So JBL should maintain highly ratio by minimizing its operating

costs in order to get adequate earnings to satisfying interest obligations. A highly ratio

can indicate that a company has an unwanted lack of debt or is paying down too much

debt with earning that could be used for other projects. It measures the ability to meet

interest payments as they come due.

4.7 Analyzing Profitability:

These measured evaluate the bank’s earnings with respect to a given level of sales, a

certain level of assets, the owner’s investment, or share value. Without profits, a firm

could not attract outside capital. Moreover, present owners and creditors would

become concerned about the company’s future and attempt to recover their funds.

Owners, creditors, and management pay close attention to boosting profits due to the

great impotence placed on earning in the marketplace.

4.7.1 Operating Profit Margin:

The operating profit margin represents what are often are often called the pure profits

earned on each sales dollar. A high operating profit margin is preferred. The operating

profit margin is calculated as follows:

Operating profit Margin = Operating Profit / Sales

Operating Profit Ratio of Janata Bank PLC:

The operating profit margin ratio indicates how much profit a company makes after

paying for variable costs of production such as wages, raw materials, etc. It is also

expressed as percentage of sales and then shows the efficiency of company

controlling the costs and expenses associated with business operation.

45

Operating Profit Ratio = Operating Profit / Operating Income

Table: 4.11: Operating Profit Ratio of JBL Source: Annual Report of JBL

Year

Ratio

2022

20.19%

2021

24.09%

2020

27.90%

2019

44.43%

2018

56.39%

Graphical Presentation:

Operating Profit Ratio

60.00%

50.00%

40.00%

30.00%

20.00%

10.00%

0.00%

2018

2019

2020

2021

20

22

Figure: 4.11: Operating Profit Ratio of JBL Source: Annual Report of JBL

A bank’s operating profit margin ratiotells you how well a bank’s operations

contribute to its profitability. For instance, a bank with a substantial profit margin

ratio makes more money on each deposit than a bank with a barrow profit margin.

The Bank operating profit margin in 2018 to 2022 indicates that operating profit

margin is decreasing day by day and it’s not good situation. JBL’s operating profit

margin is decreasing which that the banks profit is decreasing.

46

4.7.2 Net Profit Margin:

The net profit margin measures the percentage of each sales dollar remaining after all

expenses, including taxes, have deducted. The higher the net profit margin is better.

The net profit margin is calculated as follows: Net Profit Margin = Net Profit

after Taxes / Sales

Net Profit Margin of Janata Bank PLC:

The net profit margin measures the percentage of each sales dollar remaining after all

expenses, including taxes, have deducted. The higher the firm’s net profit margin is

better. The profit margin is a commonly cited measure of the company’s succeswsith

respect to earning on sales.

Net Profit Margin = Net Profit After Tax / Operating Income

Table: 4.12: Net Profit Margin Ratio of JBL Source: Annual Report of JBL

Year

Calculation

Ratio

2022

2605.48/23196.79

0.1123

2021

4807.88/21696.12

0.2216

2020

3813.15/20408.73

0.1868

2019

9551.39/20859.02

0.4579

2018

(16280.34)/22018.47

(-0.7395)

47

Net Profit Margin

-0.7395

5

4.4

4.5

3.5

3

2.8

2.4

2.5

2 2

1.8

Category 1

Category 2

Category 3

Category 4

Graphical Presentation:

Figure: 4.12: Profit Margin Ratio of JBL Source: Annual Report of JBL

The Bank net profit margin in 2018 that is (-0.7395) which indicates that profit

margin was negative. In following years this ratio is decreasing day by day and it’s

not good situation. JBL’s net profit margin is decreasing which indicates that the

banks profit is decreasing. The standard of profit margin ratio is 0.075, from the

above graph we see that the JBL profit margin ratio is higher than the standard but it

is decreasing in nature.

48

4.7.3 Return on Asset (ROA):

Return on asset (ROA), which is often called the firms return on total assets, measures

the overall effectiveness of management in generating profits with its available assets.

The higher ratio is better. An indicator of how profitable a company is relative to its

total assets. ROA gives an idea as to how efficient management is at using its assets to

generate earnings.It is calculated by dividing a company’s annual earning by its total

assets, ROA is displayed as a percentage. Sometimes this is referred to as “return on

investment”.

Return on Asset (ROA) = Net profit after Taxes / Total Assets.

Return on Asset (ROA) of Janata Bank PLC:

The return on asset (ROA), which is often called the firm’s return on total assets,

measures the overall effectiveness of management in generating profits with its

available assets. The higher ratio is better.

Return on Asset (ROA) = Net Profit after Tax/Total Asset

Table: 4.13: Rate of Return on Assets of JBL Source: Annual Report of JBL

Year

Ratio

2022

0.33%

2021

0.70%

2020

0.61%

2019

1.42%

2018

(3.50%)

49

ROA of JBL

Graphical Presentation:

Figure: 4.13: Rate of Return on Assets of JBL Source: Annual Report of JBL

Return on asset (ROA) as an indicator of managerial efficiency, indicates the

capability

of management in converting the institution’s assets into net earnings. The banks

return on asset fluctuating from 2018 to 2022 in the preceding 5 years. So the JBL

earn less profit from the assets. This is not good for the bank. But in 2019 ROA is

goes up than 2018, it’s a good condition for the bank. To improve the ratio, The JBL

has to increase the net income and control average total asset.

1.50%

1.00%

0.50%

0.00%

-0.50%

2018

2019

2020

2021

2022

-1.00%

-1.50%

-2.00%

-2.50%

-3.00%

-3.50%

50

4.7.4 Return on Equity (ROE):

The Return on Equity (ROE) measures the return earned on the owners (both

preferred and common stockholders) investment. Generally, the higher this return, the

better off the owners. The amount of net income returned as a percentage of

shareholders equity. Return on equity measures a corporation’s profitability by

revealing how much profit a company generates with the money shareholders have

invested.

Returned on Equity (ROE) = Net Profit after Tax / Shareholder’s Equi ty

Return on Equity (ROE) of Janata Bank PLC:

The return on equity measures the return earned on the owner’s (both preferred and

common stockholders’) investment. Generally higher the return indicates the better

condition of owner’s.

Return on Equity = Net profit after Tax / Shareholders’ Equity

Table: 4.14: Return on Equity of JBL Source: Annual Report of JBL

Year

Ratio

2022

5.22%

2021

9.70%

2020

9.66%

2019

30.09%

2018

(49.74%)

51

ROE of JBL

40.00%

30.00%

20.00%

10.00%

0.00%

-10.00%

-20.00%

-30.00%

2018

2019

2020

2021

2022

-40.00%

-50.00%

Graphical Presentation:

Figure: 4.14: Return on Equity of JBL Source: Annual Report of JBL

ROE is the measurement of rate of return flowing to the bank’s shareholders. It

measures the net benefit that the stockholders have receiver from investing their

capital in the bank. Higher ROE indicates the favorable position that the bank is

efficient in generating income on new investment. The banks return on equity

deviates from 2015 to 2019 in the preceding 5 years and the highest value can be

observed in 2016 and lowest value can be observed during the 2015, which is not

desirable. So the management should work hard to increase the return associated with

equity.

Earning per Share (EPS):

Earnings per share (EPS) are the earning returned on the initial investment amount.

EPS = Net income / No. of shares outstanding

52

EPS

86.31

19.92

25.12

13.61

2018

2019

2020

2021

2022

-138.91

4.7.5 Earnings per share of Janata Bank PLC:

The firm’s Earnings per share (EPS) are generally of interest to present or prospective

stockholders and management. The Earnings per share represent the number of dollars

earned on behalf of each outstanding share of common stock. The earnings per share

is calculated as follows-

Earnings per share = Earnings Available for Common stock Holder/ No. of share of

Common Stock Outstanding

Table: 4.15: EPS of JBL Source: Annual Report of JBL

Year

EPS

2022

13.61

2021

25.12

2020

19.92

2019

86.31

2018

(138.91)

Graphical Presentation:

Figure: 4.15 EPS of the JBL Source: Annual Report of JBL

EPS represents that it is earned on behalf of each outstanding shares of common stock

equity. EPS is closely watched by investors because it is an important indicator of

corporate success. The graph shows that, in 2016 Earnings per share of JBL’s are

higher than following four years. EPS is decreasing that means bank’s operating result