Financial Conduct Authority

Asset Management Market Study

Interim Report

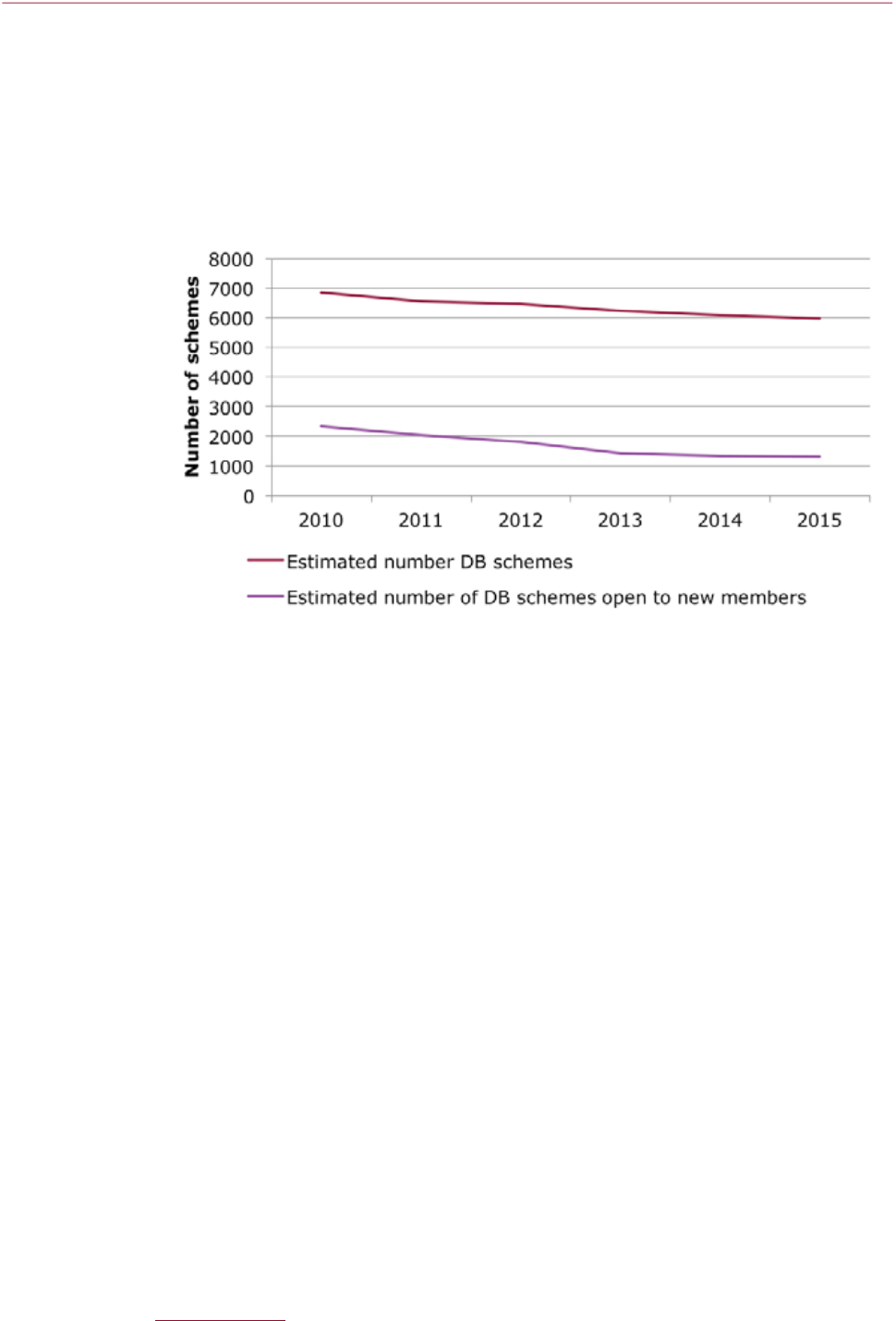

MS15/2.2

Market Study

November 2016

Financial Conduct Authority 1November 2016

MS15/2.2

Asset Management Market Study – Interim Report

Contents

Abbreviations used in this document 4

1 Executive summary 7

Overview of the asset management sector 10

Our findings in summary 11

Conclusion 20

Interim proposals on remedies 21

Next steps 22

2 Our approach 23

Why did we decide to look into the asset management market? 23

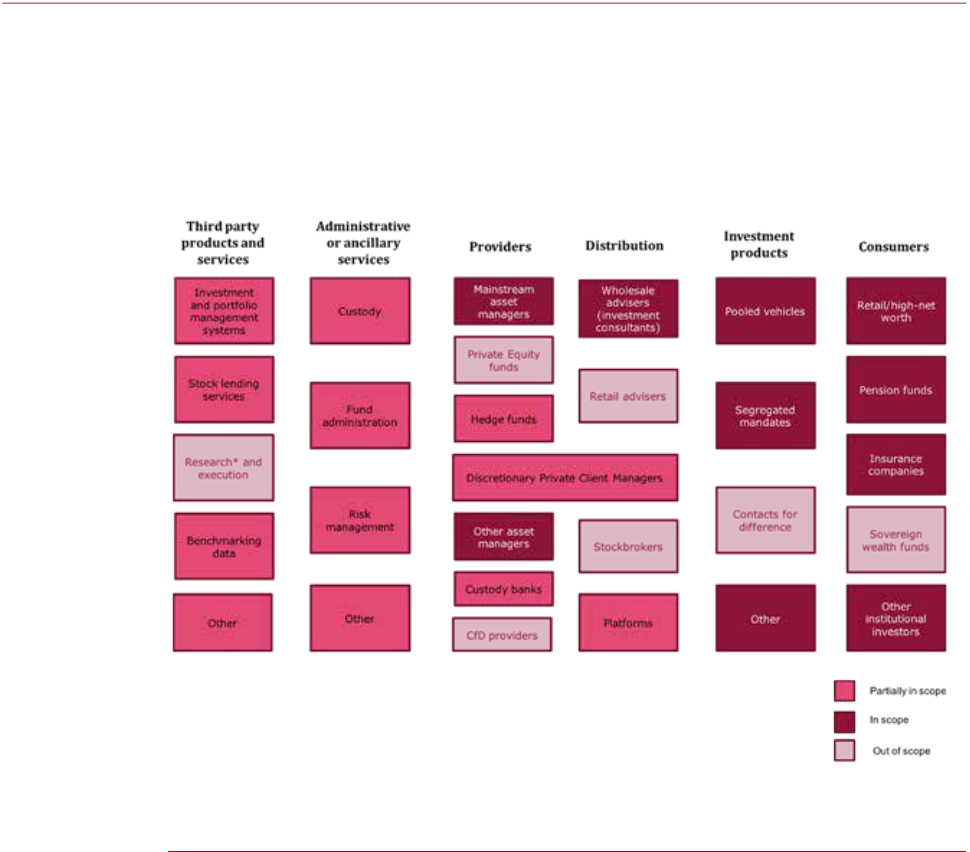

Scope of the study 24

The evidence gathered to support our analysis 25

Why are we publishing an interim report? 27

Structure of this interim report 27

3 Overview of the asset management sector 29

Background 29

Clients/investors 31

Asset management firms 32

Products and investments 36

Ancillary and third party services 40

Investment consultants and other institutional advisers 40

Platforms 41

4 How do investors choose between asset managers? 44

Introduction 44

What do retail and institutional investors perceive as value for money for asset management products? 45

How are passive funds presented to investors? 46

What factors do investors focus on when choosing and evaluating asset management products and/or

providers? 48

Are investors able to assess when to switch product and provider? 62

What impact do oversight committees have on investors’ ability to get value for money? 67

Questions for discussion and next steps 72

5 How do intermediaries and fund governance bodies affect competition between asset

managers? 73

Introduction 73

What impact do platforms have on fund charges? 75

What impact do platforms have on the total cost of investment? 78

Do platforms create barriers to asset managers gaining routes to market? 82

What impact does the financial advice market have on competition between asset managers? 85

Do fund governance bodies consider value for money on behalf of investors? 88

Other areas considered 89

Questions for discussion and next steps 90

2 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

6 What do prices, performance and profitability tell us about how competition is working? 91

Introduction 92

How are asset management firms and employees incentivised? 93

What outcomes are achieved by investors seeking to beat the benchmark? 95

What outcomes are achieved by investors that aim to achieve market returns? 107

What outcomes are achieved by investors seeking to manage returns and downsiderisk? 109

What do pricing patterns and trends and the relationship between prices and net returns tell us about

how competition is working? 110

What does the profitability of asset management firms tell us about how competition is working? 116

Questions for discussion and next steps 120

7 Are asset managers willing and able to control costs along the value chain? 122

Introduction 122

How much do investors pay for asset management and other services that support the fund? 124

Can investors monitor the costs and quality of services paid for out of the fund? 128

Can asset managers control costs and quality along the value chain? 130

8 The role of investment consultants 140

Introduction 140

Sector overview 141

How does advice given by investment consultants affect competition for assetmanagement? 147

How are conflicts within the business model of investment consultants managed? 154

Can clients monitor the services provided by investment consultants? 162

Questions for discussion and next steps 170

9 Are there barriers to entry, innovation and technological advances? 171

Introduction 171

How has innovation occurred in the asset management sector? 172

Are there barriers to entry, expansion and innovation in the asset management sector? 177

Are there features of the market or the behaviour of other parts of the value chain which inhibit

innovation? 180

Questions for discussion and next steps 180

10 Proposed remedies 181

Introduction 182

Key principles when considering remedies 183

Potential remedies 183

11 Next Steps 200

Glossary of terms used in this document 201

Annex

1 Views from stakeholders on the Terms of Reference

2 Recent Regulatory Developments

3 Consumer Research

4 Econometric Analysis – Retail

5 Institutional Demand Side

6 Econometric Analysis – Institutional

7 Fund Charges Analysis

8 Profitability Analysis

9 International Comparisons

Also to be published alongside the interim report:

MIR MS15/2.2a – Provisional decision to make a market investigation reference on investment

consultancyservices

Appendix 1 Consumer Survey Technical Report

Tilba, Baddeley & Liao (2016) research report on the effectiveness of oversight committees

Financial Conduct Authority 3November 2016

MS15/2.2

Asset Management Market Study – Interim Report

We are asking for comments on this report by 20/02/2017

You can send them to:

Becky Young

Competition Division

Financial Conduct Authority

25 The North Colonnade

Canary Wharf

London E14 5HS

Telephone: 020 7066 6894

Email: assetmanagementmarketstudy@fca.org.uk

We have carried out this work in the context of the existing UK and EU regulatory framework. We will

keep it under review to assess whether any amendments may be required in the event of changes in

the UK regulatory framework, including as a result of any negotiations following the UK’s vote to leave

the EU.

We make all responses to consultation available for public inspection unless the respondent requests

otherwise. We will not regard a standard confidentiality statement in an email message as a request for

non-disclosure.

Despite this, we may be asked to disclose a confidential response under the Freedom of Information

Act 2000. We may consult you if we receive such a request. Any decision we make not to disclose the

response is reviewable by the Information Commissioner and the Information Rights Tribunal.

All our publications are available to download from www.fca.org.uk. If you would like to receive this

paper in an alternative format, please call 020 7066 0790 or email publications_graphics @fca.org.uk or

write to Editorial and Digital Department, Financial Conduct Authority, 25 The North Colonnade, Canary

Wharf, London E14 5HS.

4 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

Abbreviations used in this document

ACD Authorised Corporate Director

AFM Authorised Fund Manager

AIF Alternative Investment Fund

AIFM Alternative Investment Fund Manager

AIFMD Alternative Investment Fund Managers Directive

AMC Annual Management Charge

ARF Absolute Return Funds

AUA Assets Under Administration

AUC Assets Under Custody

AUM Assets Under Management

B2B Business to Business

bps Basis points (equal to one hundredth of one percentage point)

CMA Competition and Markets Authority

COBS Conduct of Business Sourcebook

COLL Collective Investment Schemes

D2C Direct to Consumer

DB Defined Benefit (pension)

DC Defined Contribution (pension)

EBC Employee Benefit Consultant

ESG Environmental, Social and Governance

Financial Conduct Authority 5November 2016

MS15/2.2

Asset Management Market Study – Interim Report

ETF Exchange Traded Fund

EU European Union

FAMR Financial Advice Market Review

FUND Investment Funds Sourcebook

GIPS Global Investment Performance Standards

GSB Gold Silver Bronze Morningstar Analyst Rating

HHI Herfindahl-Hirschman Index

IA The Investment Association

IGC Independent Governance Committee

IMA Investment Management Agreement

ISA Individual Savings Account

IT Investment Trust

KIID Key Investor Information Document

LCIV London Collective Investment Vehicle

LDI Liability Driven Investment

MiFID Markets in Financial Instruments Directive

MiFID II Markets in Financial Instruments Directive II

MIR Market Investigation Reference

NURS Non-UCITs Retail Schemes

OCF Ongoing Charges Figure

OEIC Open-Ended Investment Company

OTC Over the Counter

PRIIPS Packaged Retail and Insurance-based Investment Products

6 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

PRIIPS KID Packaged Retail and Insurance-based Investment Products Key Investor Document

PRIN Principles for Business

RDR Retail Distribution Review

RFI Request for Information

RFP Request for Proposal

ROCE Return on Capital Employed

SIPP Self-Invested Personal Pensions

SMCR Senior Managers and Certification Regime

TER Targeted Expense Ratio

TPR The Pensions Regulator

UCITS Undertakings for Collective Investment in Transferable Securities

Financial Conduct Authority 7November 2016

MS15/2.2

Asset Management Market Study – Interim Report

1.

Executive summary

1.1 The asset management industry plays a vital role in the UK’s economy. Asset managers manage

the savings and pensions of millions of people, making decisions for them that will affect

their financial well-being. Asset managers generate returns for their clients by investing clients’

money in a wide variety of enterprises, both in the UK and internationally. More broadly, by

directing funding to firms they think are most likely to grow, asset managers support businesses

that provide jobs and drive economic growth. Asset managers have an important role in the

corporate governance of the businesses they fund.

1.2 The UK’s asset management industry is the second largest in the world, managing £6.9trillion

of assets. Over £1 trillion is managed for UK retail (individual) investors and £3 trillion on

behalf of UK pension funds and other institutional investors. The industry also manages around

£2.7trillion on behalf of overseas clients.

1.3 The service offered to investors comprises a search for return, risk management and

administration. The investor bears virtually all the risk. Over three quarters of UK households

with occupational or personal pensions

1

use these services, including over 9 million

2

individuals

saving for their retirement through defined contribution (DC) pension schemes and over

1.2 million savers currently saving in defined benefit (DB) pension schemes.

3

There are also

around 11 million savers with investment products such as stocks and shares ISAs. These

investors are willing to put their money at risk to generate greater returns than they can get

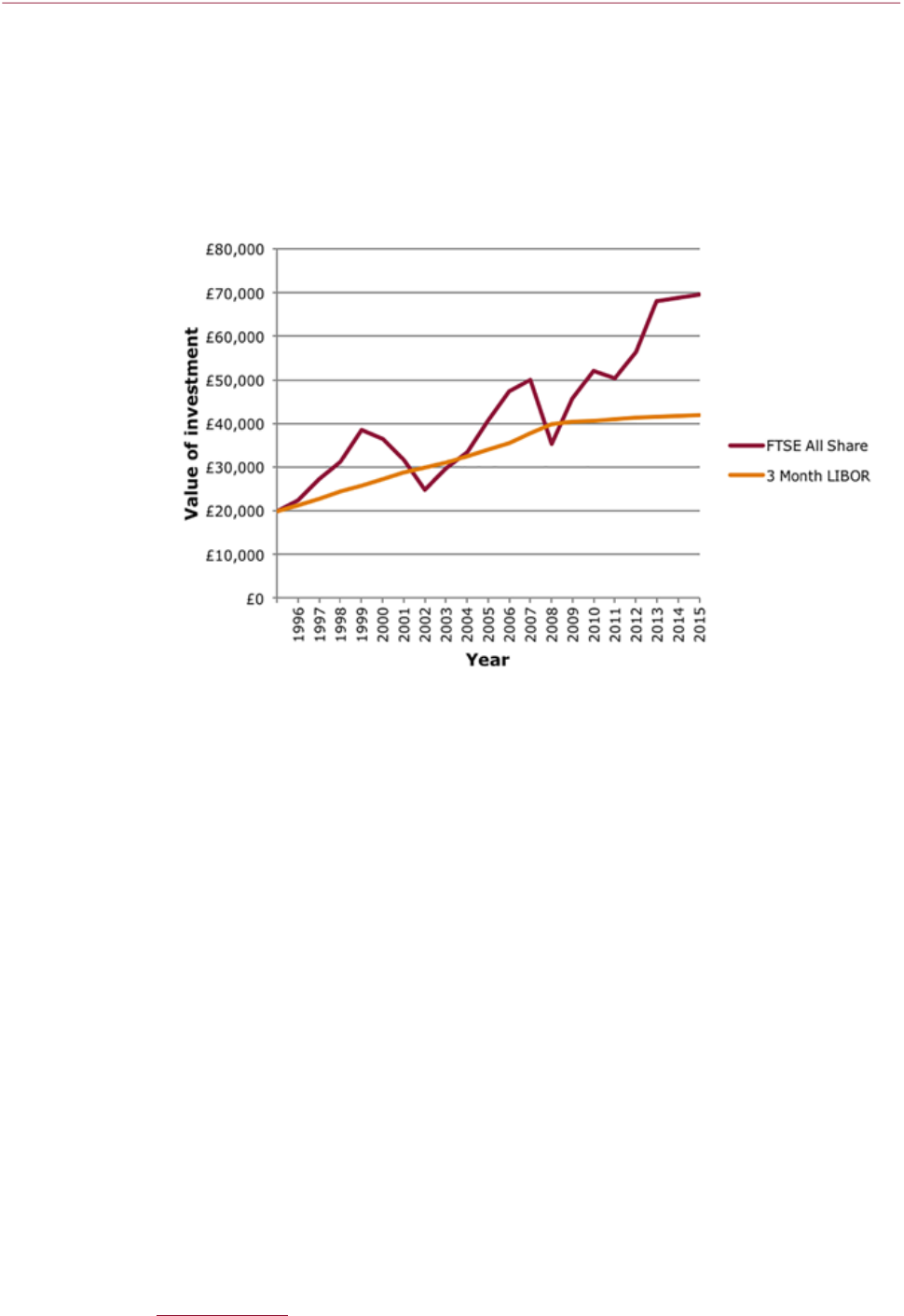

through cash savings, as illustrated in Figure 1.1.

1 The contribution of asset management to the UK economy Oxera (July 2016) www.theinvestmentassociation.org/assets/files/

press/2016/The%20contribution%20of%20asset%20management%20to%20the%20UK%20economy.pdf

2 The Pensions Regulator data based on scheme returns (1 Jan 2016) (excludes hybrid DB and DC pension schemes)

3 The Pensions Regulator data based on scheme returns (1 Jan 2016)

8 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

Figure 1.1: Value of a £20,000 investment in the FTSE all share versus cash

1996‑2015

4

1.4 The FCA has looked at this sector because we want to ensure that the market works well and

the investment products consumers use offer value for money. Improvements in value for

money could have a significant impact on pension and saving pots. Even small differences in

charges can have a significant impact over time.

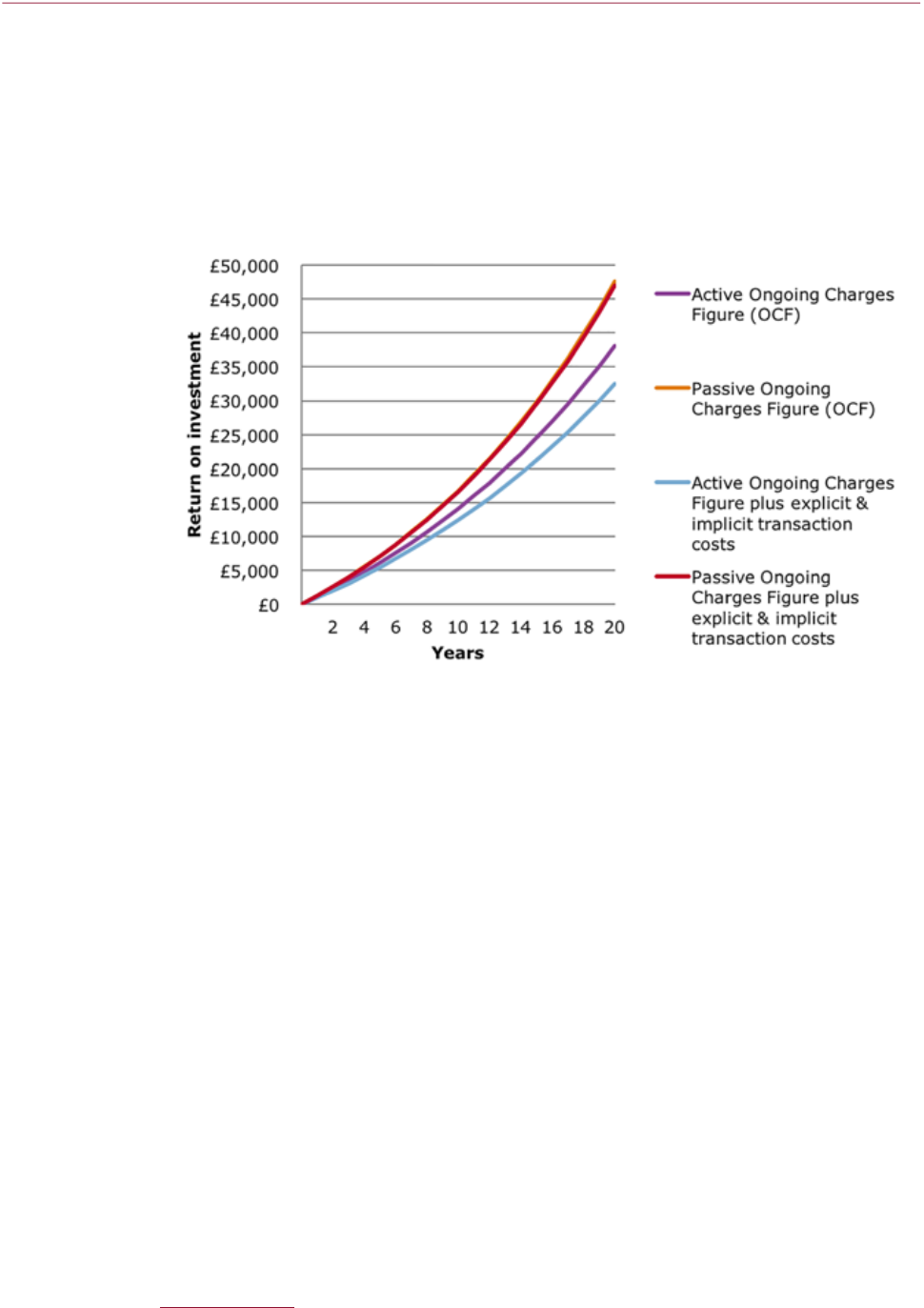

1.5 Figure 1.2 compares the net return on a £20,000 investment over 20 years to show the impact

of charges. Assuming, for illustrative purposes, that both funds earn the same return before

charges (the average FTSE all share growth), an investor in a typical low cost passive fund

would earn £9,455 (24.8%) more on a £20,000 investment than an investor in a typical active

fund, and this number could rise to £14,439 (44.4%) once transaction costs have been taken

into account. We recognise that some investors in actively managed funds are likely to expect

higher returns in exchange for the greater risk they are taking on.

4 The 3 month LIBOR is the average interbank interest rate at which banks are prepared to lend one another unsecured funds

denominated in British pounds. We consider LIBOR to be a proxy for a low risk rate of return available to retail consumers, either

directly or through banking saving rates. Equity returns are based on the FTSE all share index inclusive of dividends.

Financial Conduct Authority 9November 2016

MS15/2.2

Asset Management Market Study – Interim Report

Figure 1.2 – returns on a £20,000 equity fund over 20 years assuming average FTSE

all share growth

5

1.6 We launched this market study in November 2015 after stakeholders raised a number of

concerns which we also identified in other FCA work.

6

In order to assess how asset managers

compete to deliver value for money, we asked the following questions:

• How do investors choose between asset managers? We outline our ndings in Chapter 4

• How do intermediaries and fund governance bodies affect competition between asset

managers? We outline our ndings in Chapter 5

• What do prices, prots and performance tell us about how competition is working?

Weoutline our ndings in Chapter 6

• Are asset managers willing and able to control costs and quality along the value chain?

Weoutline our ndings in Chapter 7

• How do investment consultants affect competition for institutional asset management?

Weoutline our ndings in Chapter 8

• Are there barriers to innovation and technological advances? We outline our ndings in

Chapter 9

1.7 This report presents our interim findings. In it we set out our views on how well competition

is working and the resulting outcomes for investors. We also outline some proposed remedies.

We are keen to hear what stakeholders think about the issues we have identified.

5 These charge figures represent industry average charges for active and passive equity funds in 2015. Along with average brokerage

costs based on 16 firm responses and implicit charges as estimated by ITG and based on 100% portfolio turnover per annum for

active and 10% portfolio turnover per annum for passive funds. These charges are for illustrative purposes.

6 FS15/2 Wholesale sector competition review 2014-15

www.fca.org.uk/publications/feedback-statements/fs15-2-wholesale-sector-competition-review-2014-15

10 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

1.8 Our interim findings are drawn from multiple pieces of analysis including a profitability analysis

which assessed operating margins of asset management firms, an analysis of the charges

which are taken out of funds and mandates by asset managers, and econometric analysis to

understand the drivers of net flows of funds between asset managers. We also commissioned

research into retail and institutional investor decision making and choices.

1.9 Other countries are looking at similar issues.

7

For example, the European Commission is expected

to recommend that EU regulators investigate asset management performance andfees.

8

1.10 This market study complements other FCA work in the asset management sector. In October

2016 we published a consultation paper on transaction cost disclosure

9

in workplace pensions.

This is an important step in giving the governance bodies of pension schemes the right

information to assess whether scheme members get value for money. The market study

has been developed bearing in mind the proposed requirements in the Packaged Retail and

Insurance-based Investment Products regulation (PRIIPs).

10

We have previously examined the

way the dealing commission regime works, including how asset managers buy research with

dealing commissions

11

and we use some of that information in this report. Our interim findings

and proposed remedies sit alongside other developments to create a coherent policy package.

Overview of the asset management sector

1.11 Investors have many options when choosing how to invest their money. There are 1,840 asset

management firms authorised in the UK.

12

A wide range of asset management products offer

investors different combinations of risk and potential rewards. These products can be actively

managed, can offer small positions either side of a market benchmark, or can passively track

an index by holding securities in proportion to the market. In addition, funds can aim to deliver

a better return than conventional passive funds by using alternative weightings (so called

‘smartbeta’).

1.12 Passive funds offer investors similar levels of risk and return as the market. Actively managed

funds often offer investors the chance to ‘beat the market’, albeit with a corresponding risk of

underperformance. The difference between an active manager’s and market performance (before

fees) depends on how far the active asset manager invests differently from the composition of

stocks in a market. They can do this by, for example, investing in smaller companies or making

larger investments in firms which the manager considers to be undervalued. Since 2005 passive

funds have experienced nearly fivefold growth and now represent around 23% of the assets

under management in the UK.

13

1.13 Actively managed funds typically charge higher fees than passive funds, reflecting the higher

costs of managing an actively managed fund. The annual average disclosed fee for actively

7 Please see Annex 9: International Comparisons for our assessment of what other countries have done to improve value for money

for retail and institutional investors.

8 www.ft.com/content/a9060f50-870e-11e6-bbbe-2a4dcea95797

9 CP16/30, Transaction cost disclosure in workplace pensions (October 2016) www.fca.org.uk/publication/consultation/cp16-30.pdf

10 The European Union (EU) has passed a Regulation on key information documents for packaged retail and insurance-based

investment products (PRIIPs). This establishes standard disclosure obligations, including a requirement to disclose transaction costs for

those products in its scope. Information about the FCA’s understanding of the scope of PRIIPs is set out on the following web page:

www.fca.org.uk/firms/priips-disclosure-key-information-documents.

11 DP14/3 Discussion paper in the use of dealing commission regime www.fca.org.uk/publication/discussion/dp14-03.pdf

12 FCA internal data

13 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

Financial Conduct Authority 11November 2016

MS15/2.2

Asset Management Market Study – Interim Report

managed equity funds available to UK investors is 0.90% of the assets under management

(AUM)

14

and the average passive fee is 0.15%.

15

Furthermore, transaction costs (charged when

asset managers trade on investors’ behalf) are normally higher for active funds (as illustrated

in Figure1.2).

1.14 Both retail and institutional investors can invest through a range of different investment

vehicles managed by an asset manager. Institutional investors and wealthy individuals can set

up a ‘segregated mandate’ which means their money will be managed independently of other

investors. Alternatively, institutional and retail investors can invest in funds, combining their

money with other investors’ to increase scale and reduce costs.

1.15 Retail and institutional investors can make their investment decisions with the help of advisers.

Investment consultants advise institutional investors on their investment strategy, including

how to allocate their money between different types of investment, and help them choose the

most appropriate asset manager or fund. Retail investors can pay for financial advice to help

make investments or invest directly with an asset manager or through a platform (a ‘one stop

shop’ for those who want to compare different funds).

Our ndings in summary

1.16 The evidence suggests there is weak price competition in a number of areas of the

asset management industry. This has a material impact on the investment returns of

investors through their payments for asset management services.

1.17 There is a range of evidence underpinning this finding, relating to how asset managers compete,

investor behaviour and the role of intermediaries in helping investors choose products.

How asset managers compete

Price trends, charging practices and profitability

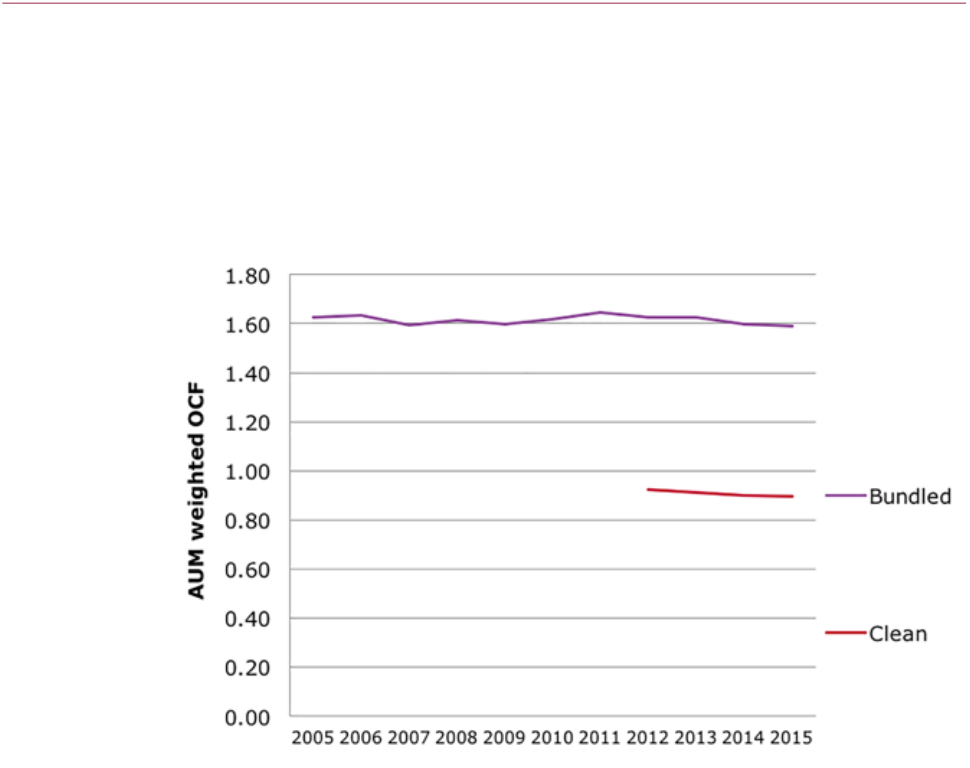

1.18 Our analysis shows mainstream actively managed fund charges have stayed broadly the same

for the last 10 years.

16

Very few asset management firms told us they lower charges to attract

investment, particularly for retail investors – most believe this would not win them new business.

14 Asset-weighted average Ongoing Charges Figure for clean share classes of active equity funds

15 Asset-weighted average Ongoing Charges Figure for clean share classes of passive equity funds

16 After taking account of the effect of the Retail Distribution Review. The Retail Distribution Review aimed to realigned adviser and

platform incentives with those of consumers’ by removing the commission they received from providers. This has resulted in the

‘unbundling’ of prices to remove the commission payments to advisers and intermediaries.

12 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

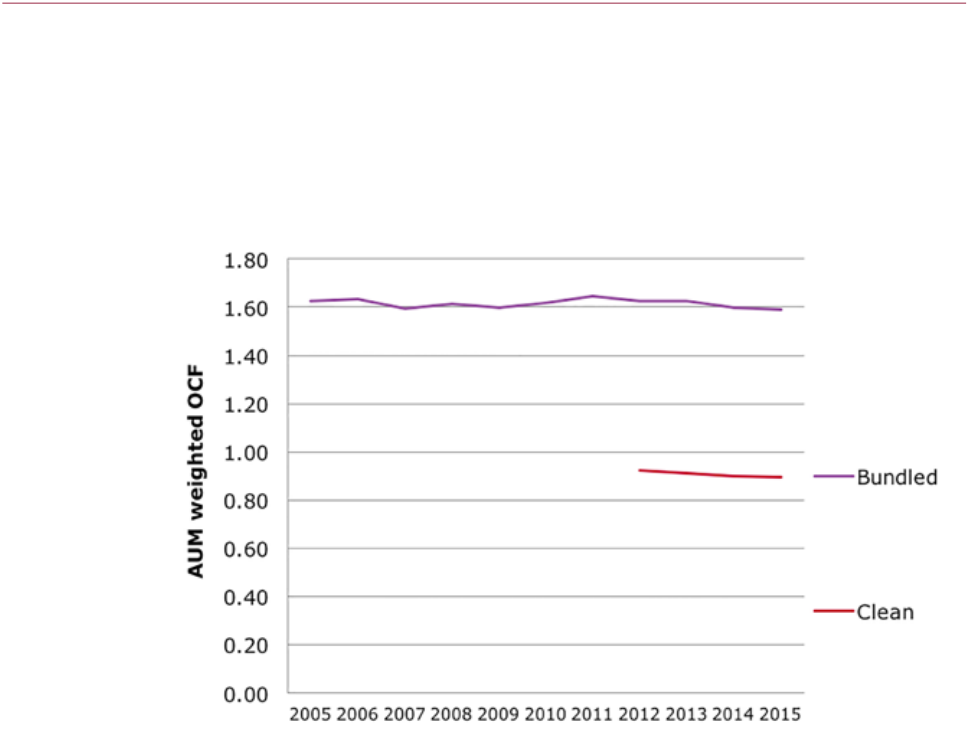

Figure 1.3: Trends in the asset‑weighted OCF for active share classes over time

Source: OCF data and information about the fee structure of share classes from a sample of asset managers enriched with

information from Morningstar Direct. AUM data from Morningstar Direct.

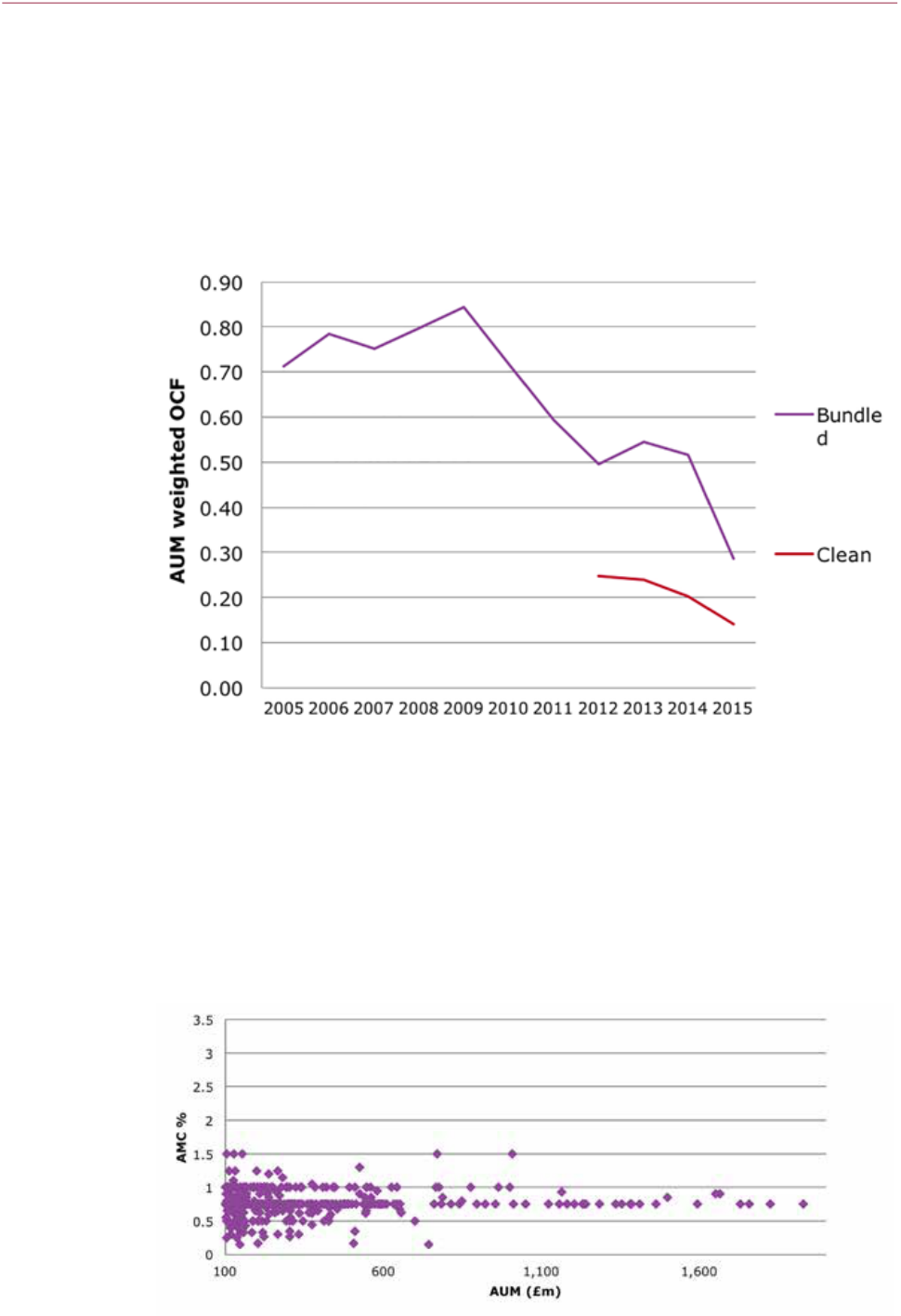

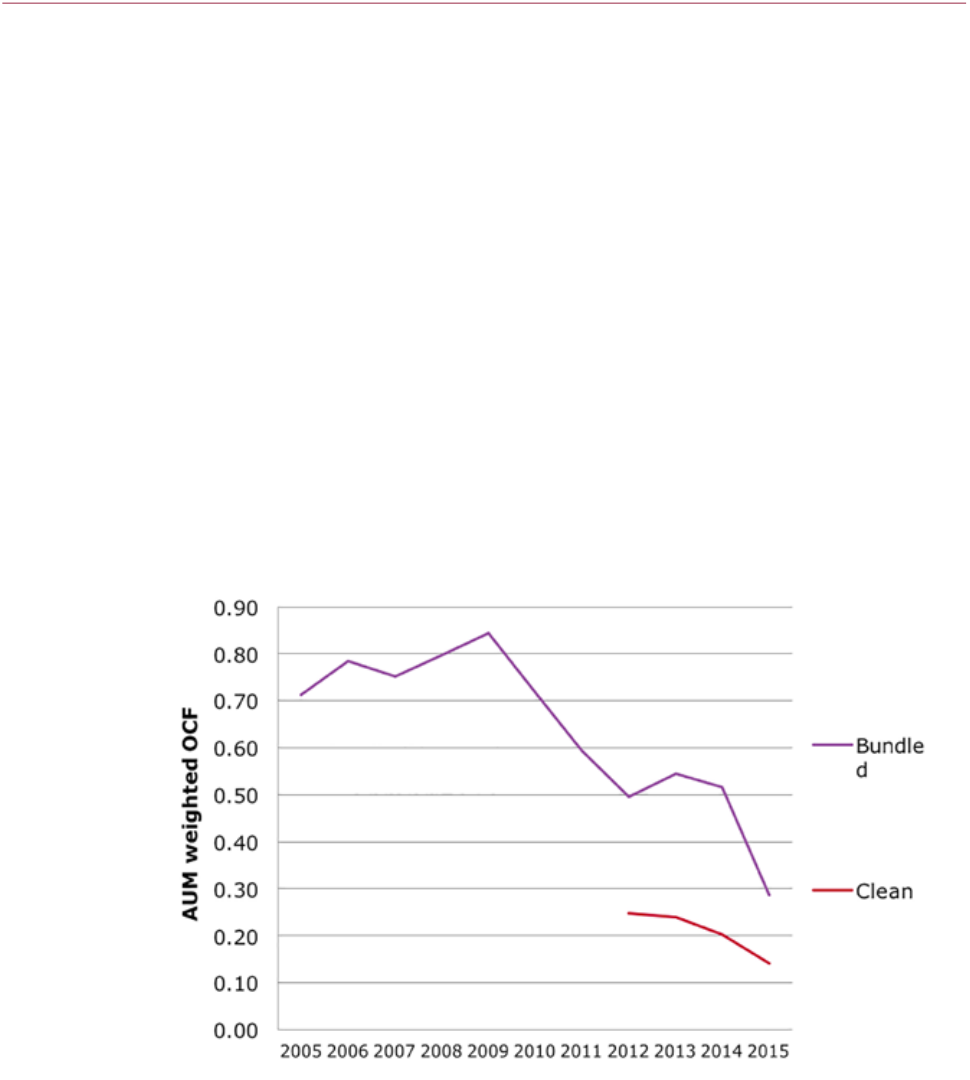

1.19 In contrast, we found that charges for passive funds have fallen over the last five years. This,

combined with the growth of passive investing, suggests that price awareness and competitive

pressure on price is building among certain groups of investors.

Financial Conduct Authority 13November 2016

MS15/2.2

Asset Management Market Study – Interim Report

Figure 1.4: Trends in the asset‑weighted OCF for index‑tracking share classes

overtime

Source: OCF data and information about the fee structure of share classes from a sample of asset managers enriched with

information from Morningstar Direct. AUM data from Morningstar direct.

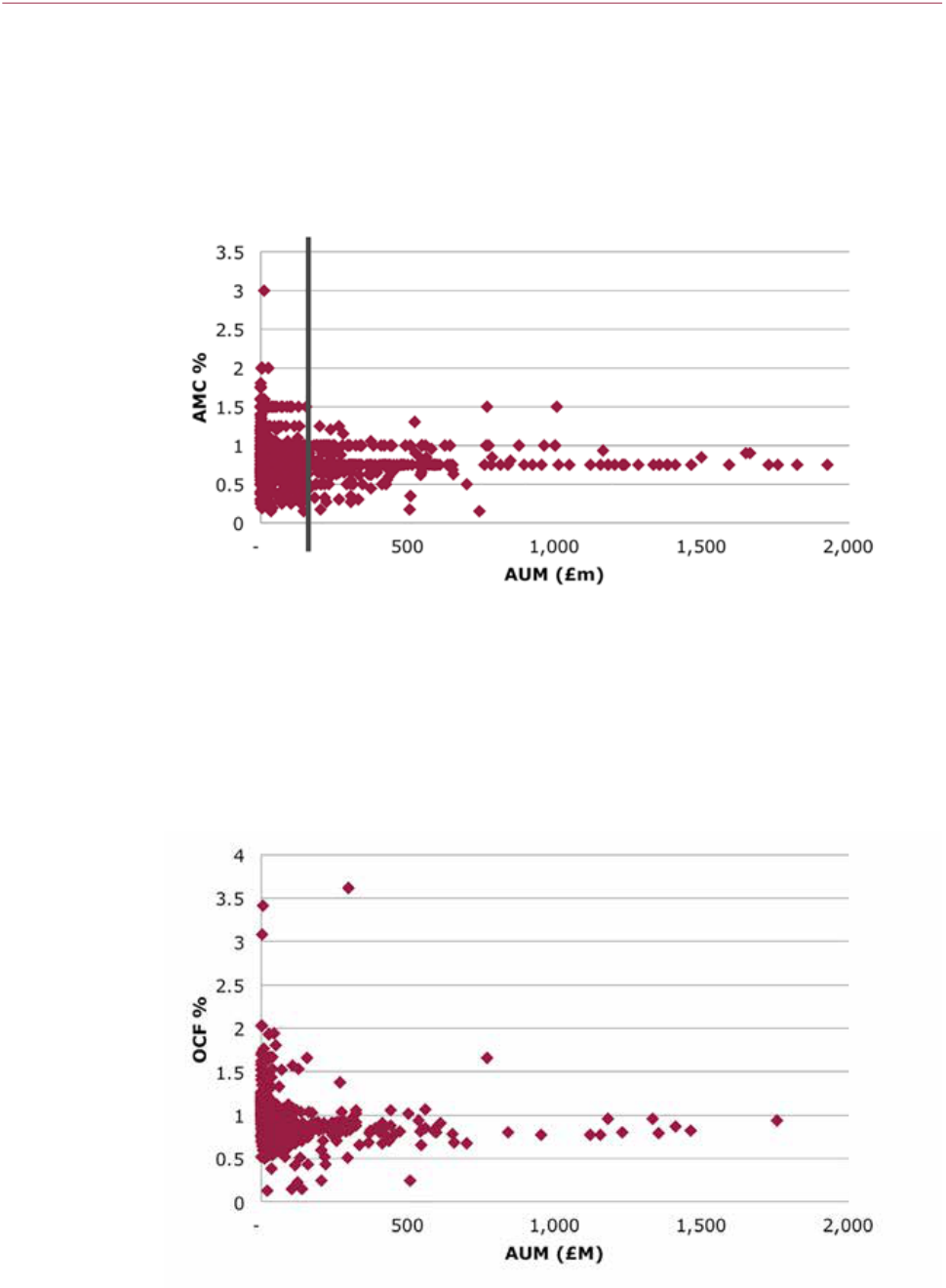

1.20 We have found considerable price clustering for active equity funds, with many fund priced at

1% and 0.75%, particularly once assets under management are greater than around £100m

(see Figure1.5). This is consistent with firms’ reluctance to undercut each other by offering

lower charges. We also note that as fund size increases, price does not fall, suggesting the

economies of scale are captured by the fund manager rather than being passed onto investors

in these funds.

Figure 1.5: The distribution of AMC against AUM for equity share classes

Source: AMC data from a sample of asset managers enriched with information from Morningstar Direct. AUM data from

Morningstar Direct. Data for clean equity share classes in December 2015.

14 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

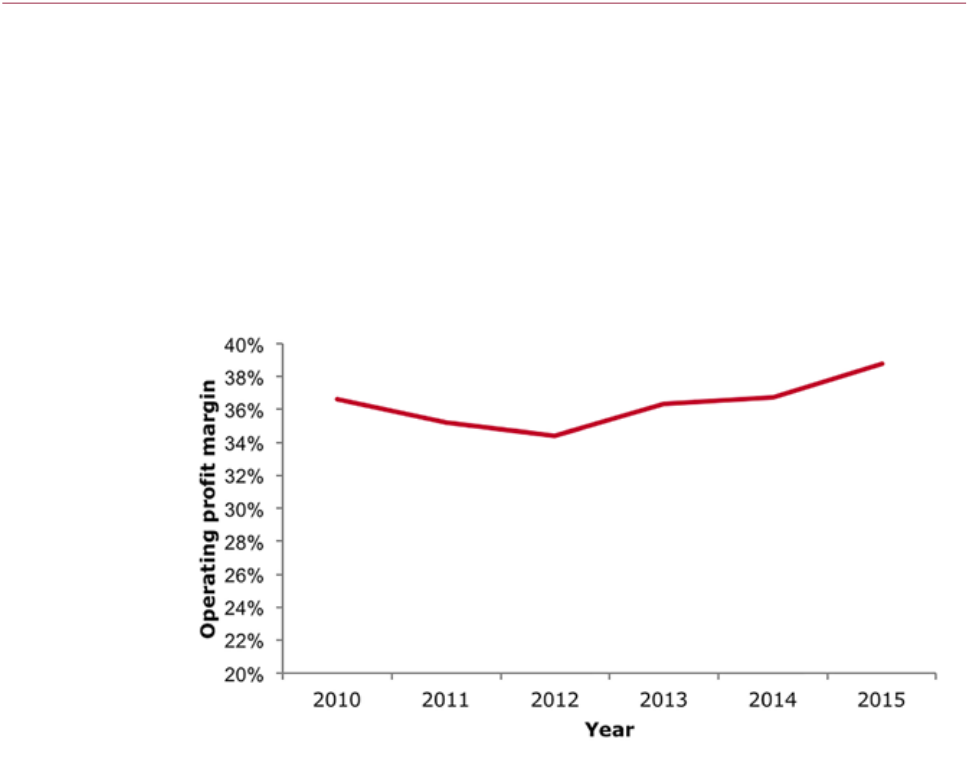

1.21 Asset management firms have consistently earned substantial profits across our six year sample,

with an average profit margin of 36%. These margins are even higher if the profit sharing

element of staff remuneration is included.

Figure 1.6: Average operating profit margin

Source: FCA analysis based on financial data submitted to the FCA from 16 firms.

1.22 In many markets, weak pressure on price is associated with weak cost control. We found the

evidence on cost control in this market to be mixed. Asset managers tend to be good at managing

charges which are straightforward and inexpensive to control, for example, negotiating fees

down for services such as safekeeping of assets and many other ancillary services. However,

they are less good at controlling costs for services where it is more expensive to monitor value

for money, such as how well executed trades and foreign exchange transactions are. Fund

governance bodies also do not exert significant pricing pressure by scrutinising asset managers’

own costs.

1.23 We would expect the costs of active asset management to be higher than the cost of managing

a passive fund. Comparing the total charges made on the fund for actively managed and

passive funds, we see that on average both costs and profits are higher in absolute terms for

actively managed products.

Financial Conduct Authority 15November 2016

MS15/2.2

Asset Management Market Study – Interim Report

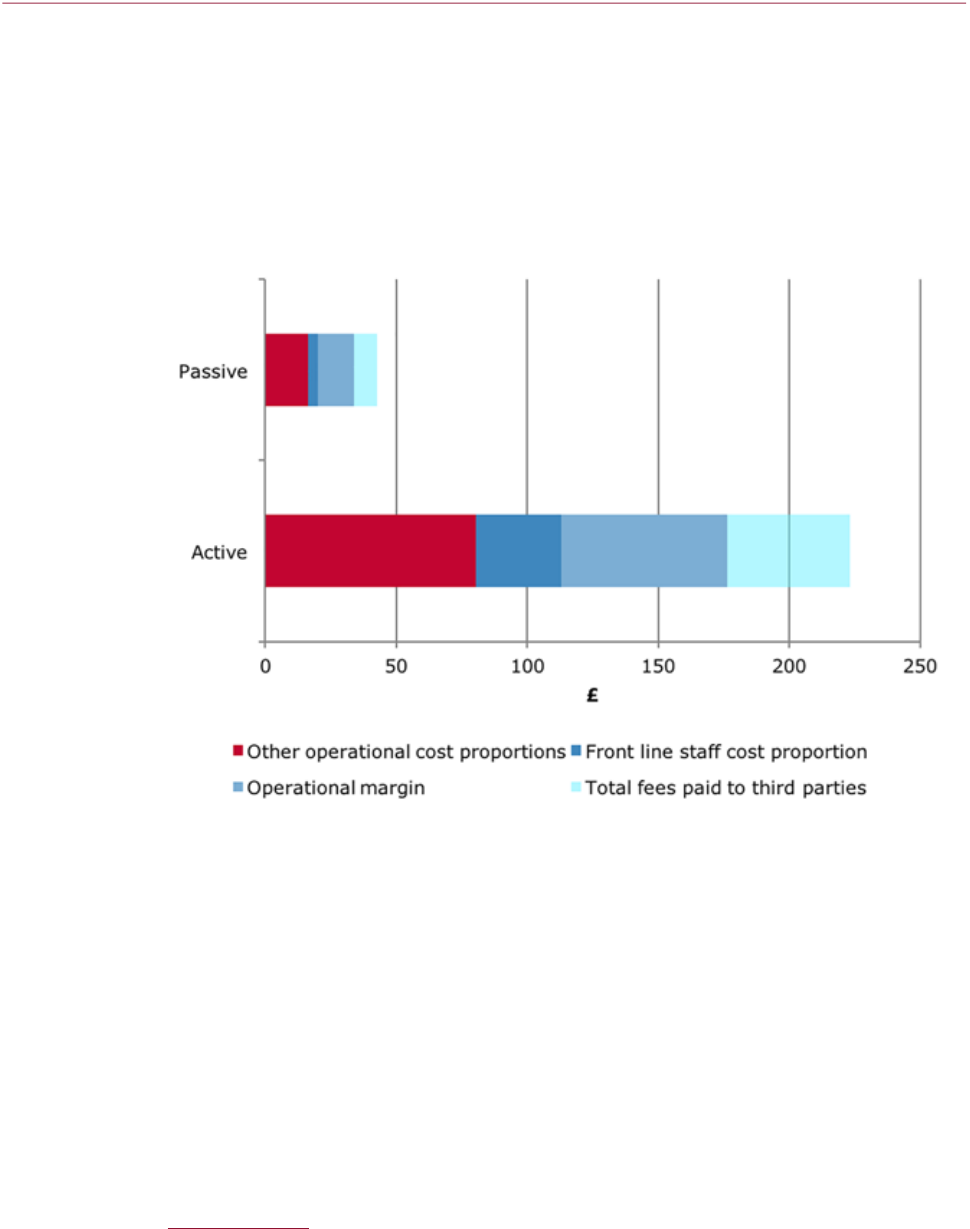

Figure 1.7 – Average fund charges for 1 year for a £20,000 FTSE all share

equityinvestment

17

Investor outcomes

1.24 We looked at the relationship between price, performance and how actively the fund

is managed.

1.25 Overall, our evidence suggests that actively managed investments do not outperform their

benchmark after costs. Funds which are available to retail investors underperform their

benchmarks after costs – while products available to pension schemes and other institutional

investors achieve returns that are not significantly above the benchmark.

18

1.26 Investors may choose to invest in funds with higher charges in the expectation of achieving

higher future returns. However, we find that there is no clear relationship between price and

performance – the most expensive funds do not appear to perform better than other funds

before or after costs.

17 Note that this only covers explicit charges. The total charges in Figure 1.7 are higher than the average OCF for actively managed

equity funds (0.90 %) and the average OCF for passively managed equity funds (0.15%). This is because the total charge in

Figure1.7 is a money weighted average across the firms in our sample, includes some costs not disclosed in the OCF (such as

brokerage costs), and includes asset classes such as fixed income and property funds which are not included in the average

OCFequity figures. We assume average returns of 6.43% on active products and passive products, which is calculated as the

compound annual growth rate of the FTSE All Share, from 1996-2015. Equity returns are calculated inclusive of dividends where

data is available (19 out of 20 years). Dividends are assumed to be reinvested in the index. Charges are based on average active and

passive outflows from all pooled funds domiciled or managed and sold within the UK by the 16 firms in our sample. Chargeswere

calculated by applying the annualised average of the FTSE All share index to an investment of £10,000 and then deducting the

money weighted average fee of an active and a passive fund based on our sample of 16 firms

18 Our analysis of returns for institutional funds and segregated mandates used ‘manager specified benchmarks’, which is the

benchmark chosen by the asset manager to represent the market in which they are investing. Our analysis of fund returns used the

Morningstar Category benchmark, which is the benchmark assigned by Morningstar to represent the relevant investment category.

16 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

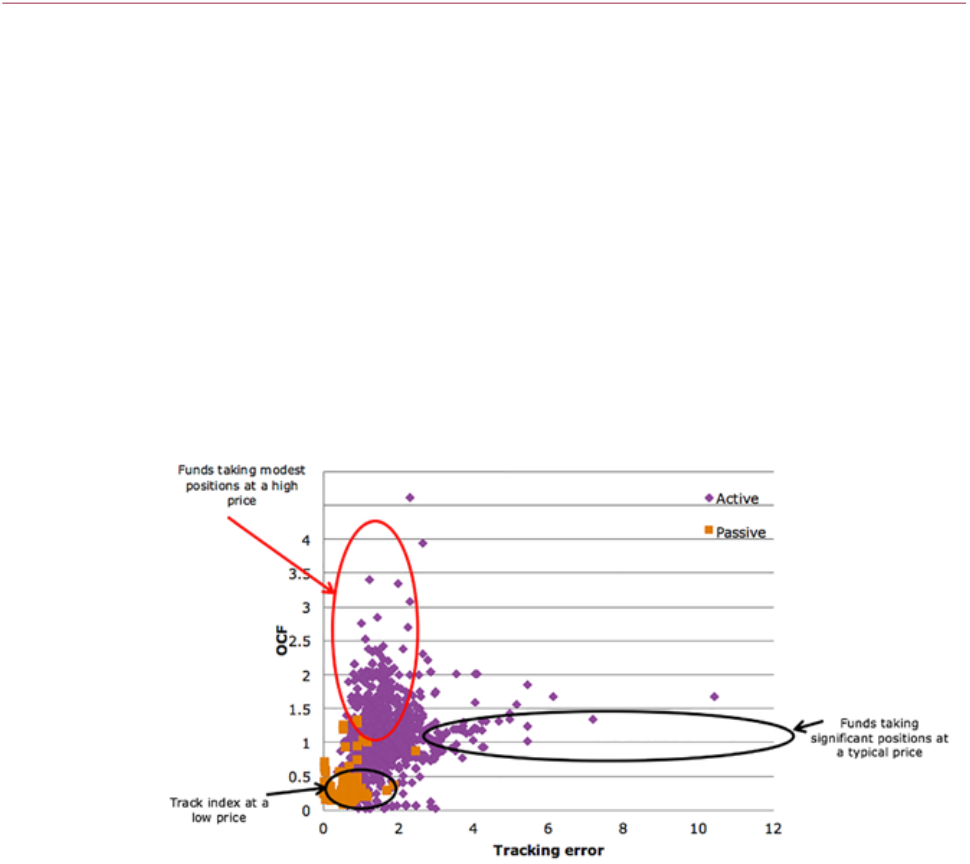

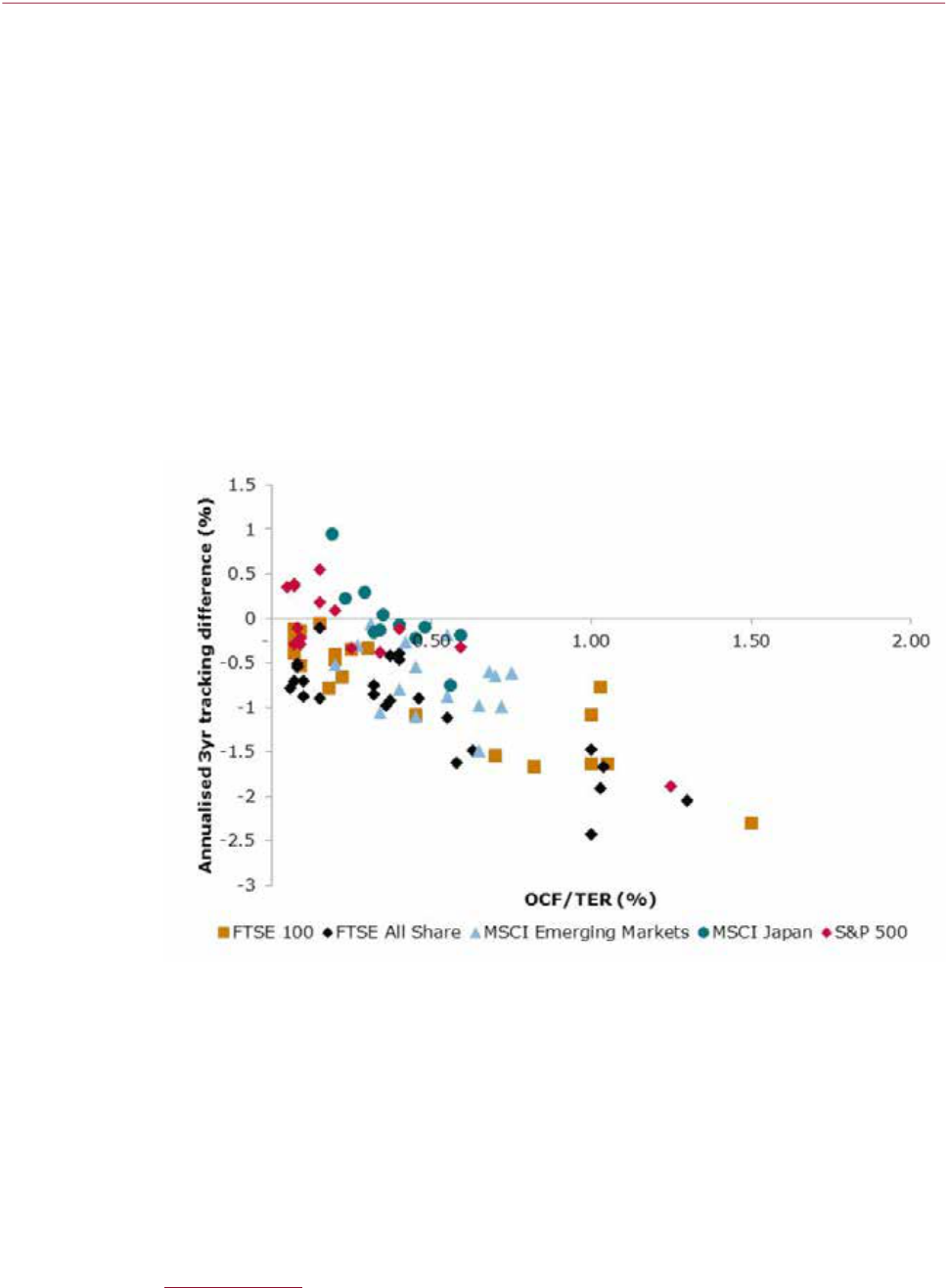

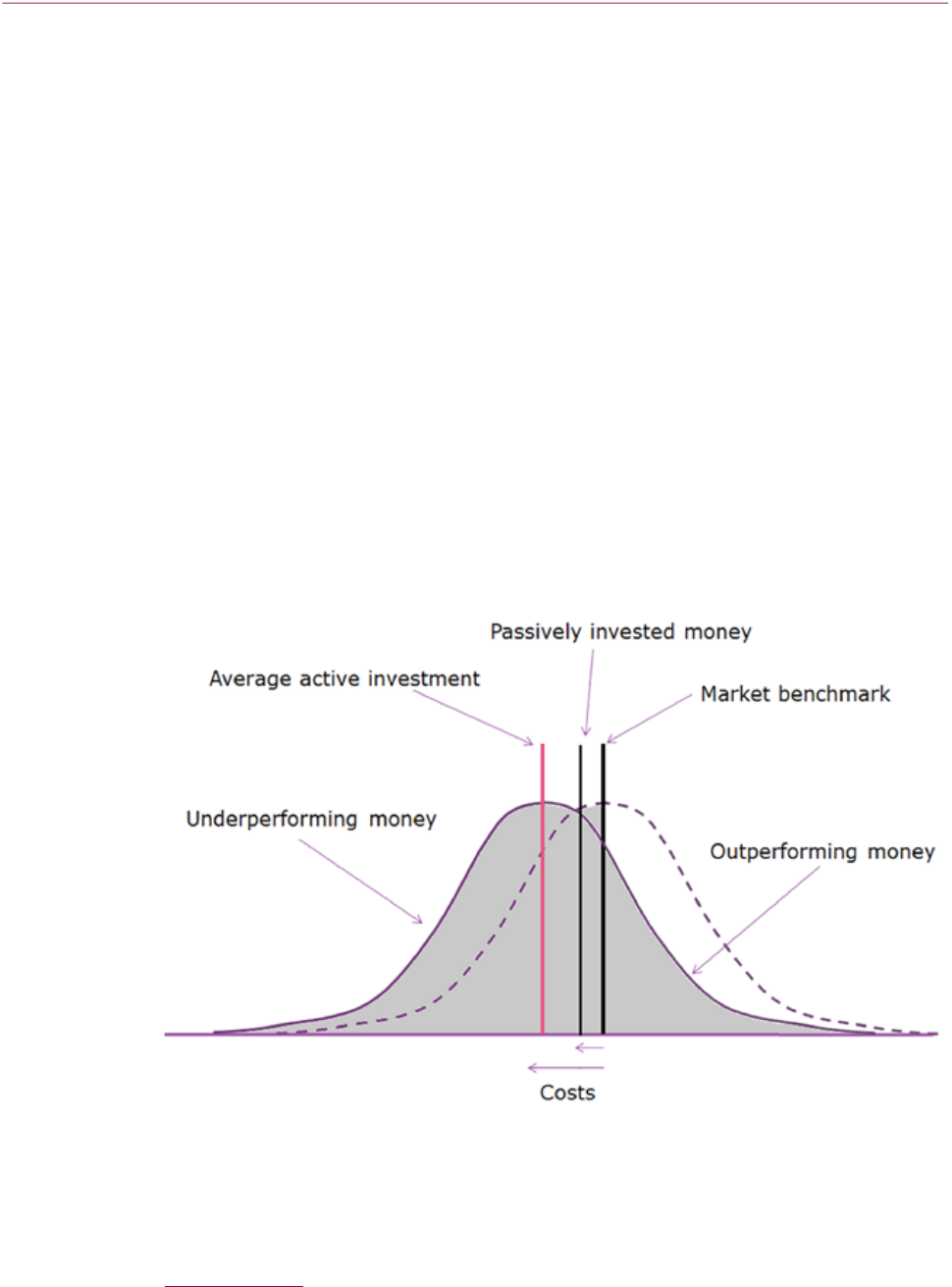

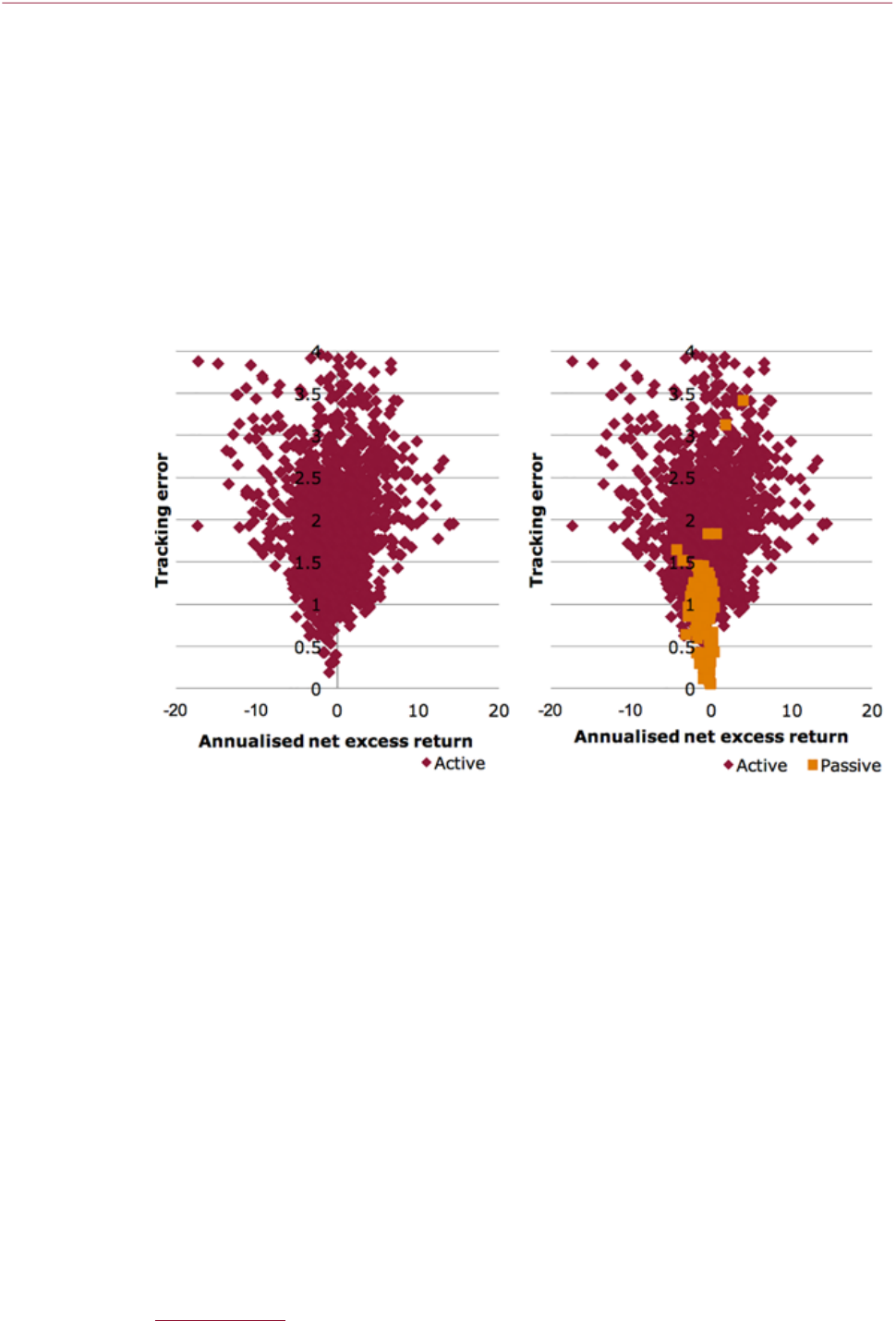

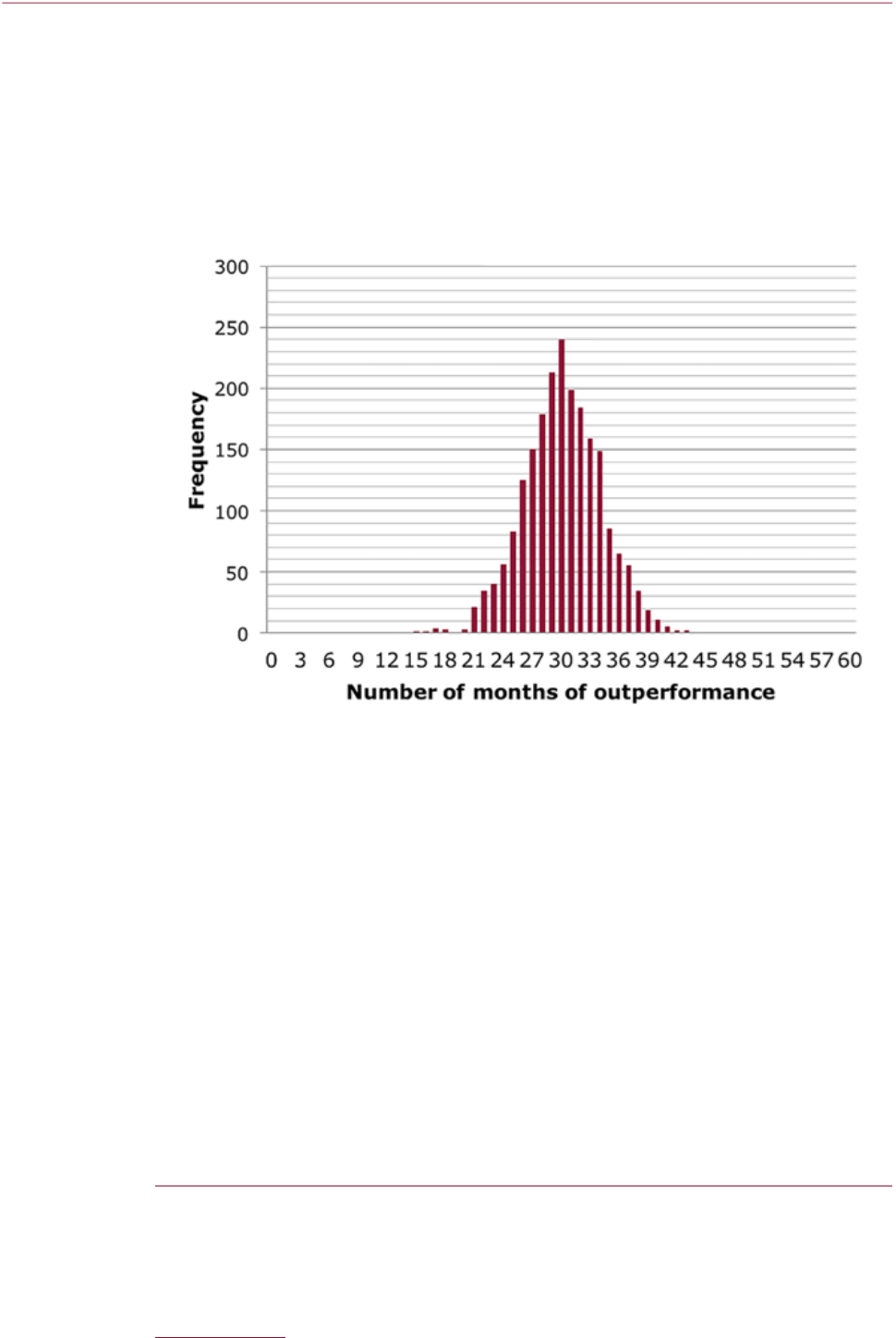

1.27 Many active funds offer similar exposure to passive funds, but some charge significantly more.

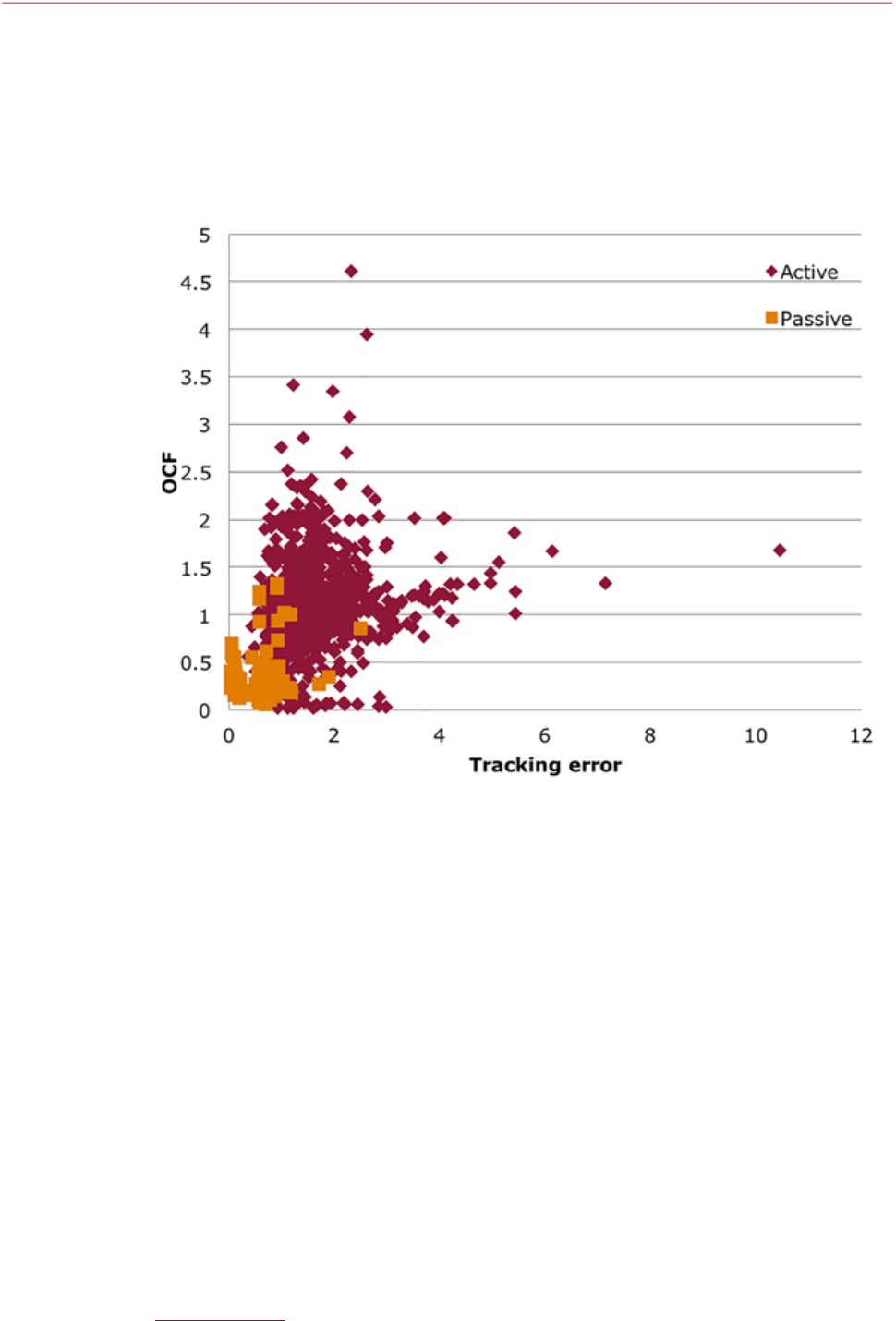

Figure 1.8 shows the charges (the Ongoing Charges Figure) for active equity funds compared

against the ‘tracking error’. The tracking error shows the variation of the difference in the returns

of the fund against the underlying benchmark. A low tracking error generally indicates that the

fund is closely replicating the benchmark, although it may be seeking a small outperformance

against this or trying to limit underperformance. There is around £109bn in expensive funds

that closely mirror the performance of the market (they have a tracking error below 1.5) and

are considerably more expensive than passive funds.

Figure 1.8: Tracking error against OCF for clean equity share classes over 2013‑15

Source: Returns and benchmark data provided by Morningstar Direct. OCF data from a sample of asset managers, enriched with

information on charges from Morningstar Direct.

Transparency and clarity of objectives and investment outcomes

1.28 The transparency of charges has been under scrutiny and debate for some time. Some progress

has been made in this area, including the introduction of the Ongoing Charges Figure, the

current FCA consultation to introduce a standardised methodology to calculate transaction

cost for defined contribution workplace pensions and work to unbundle research and dealing

commission. Industry and investor groups continue to advocate greater transparency from

asset managers.

1.29 We found the prices for ancillary services – such as administration, record keeping and services

to safeguard the assets – bought by asset managers are usually clear to investors. This is because

they are included in the ongoing charges figure for investors using funds, or the investment

management agreement for investors using segregated mandates. However, investors are not

given information on transaction costs in advance, meaning that investors cannot take the

full cost of investing into account when they make their initial investment decision. These

costs can be high and add around 50bps on average to the cost of active management for

equityinvestments.

1.30 In addition, we have concerns about how asset managers communicate their objectives and

outcomes to investors. Investors may continue to invest in expensive actively managed funds

which mirror the performance of the market because fund managers do not adequately explain

the fund’s investment strategy and charges.

Financial Conduct Authority 17November 2016

MS15/2.2

Asset Management Market Study – Interim Report

1.31 Absolute return funds are funds that aim to deliver a positive return, whatever the market

conditions. We have two concerns with absolute return funds. First, many absolute return

funds do not report their performance against the relevant returns target. For example, an

absolute return fund may be failing to achieve its performance objective of beating a cash

benchmark by 2%. But these funds show their performance against a cash benchmark only,

giving the impression that they have outperformed. Second, we have concerns about absolute

return funds that charge a performance fee when returns are lower than the performance

objective the fund is aiming to achieve. The manager is rewarded despite not achieving what

the investor considers to be target performance.

Investor behaviour

1.32 We looked at the factors that drive retail and institutional investors’ choice of asset manager

(both when making initial investment decisions and when deciding whether to switch between

providers). We also examined their ability to negotiate with asset managers.

Factors that drive investor choice

1.33 The investor community is a diverse mix of individuals and institutions. However, we found

broad agreement that value for money for asset management products is seen as a combination

of the:

• return achieved

• price paid

• risk taken

• quality of any additional services provided by the asset manager

1.34 This means that most investors generally think of value for money as risk-adjusted net returns.

1.35 We found that a key focus for retail investors and, to some extent, institutional investors when

choosing between asset managers is past performance. However, past performance is not a

good indicator of future risk-adjusted net returns for two main reasons.

1.36 First, it can be difficult to interpret and compare past performance information. Funds set

up at different times will measure performance over different time periods, which can make

comparison difficult. The performance of one fund might be measured more frequently than

another,

19

which can affect the perceived volatility of the fund’s performance, especially over

periods of volatility in the relevant market. Funds that perform poorly are often liquidated

or merged into another fund, giving investors the false impression that there are few poorly

performing funds on the market.

1.37 Second, even if past performance were easier to interpret and compare, past performance has

limited value as an indicator of future performance. The academic literature shows little evidence

of persistence in outperformance. In other words, managers that outperform in one year do

not reliably outperform in future years. Previous UK analysis has found that the majority of

funds with historical outperformance do not continue to outperform the relevant market index

or peer group for more than a few years. The evidence on persistence in underperformance is

less clear, partly because of the impact of fund mergers and closures as discussed below.

19 While the KIID requires fund managers to display performance yearly, other sources of information can measure performance

morefrequently

18 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

1.38 The evidence on investor focus on charges is mixed. There is increasing attention among

institutional investors to the level of charges that they pay, as reflected in the demand for

greater transparency around costs as discussed in paragraph 1.30. On the retail side however,

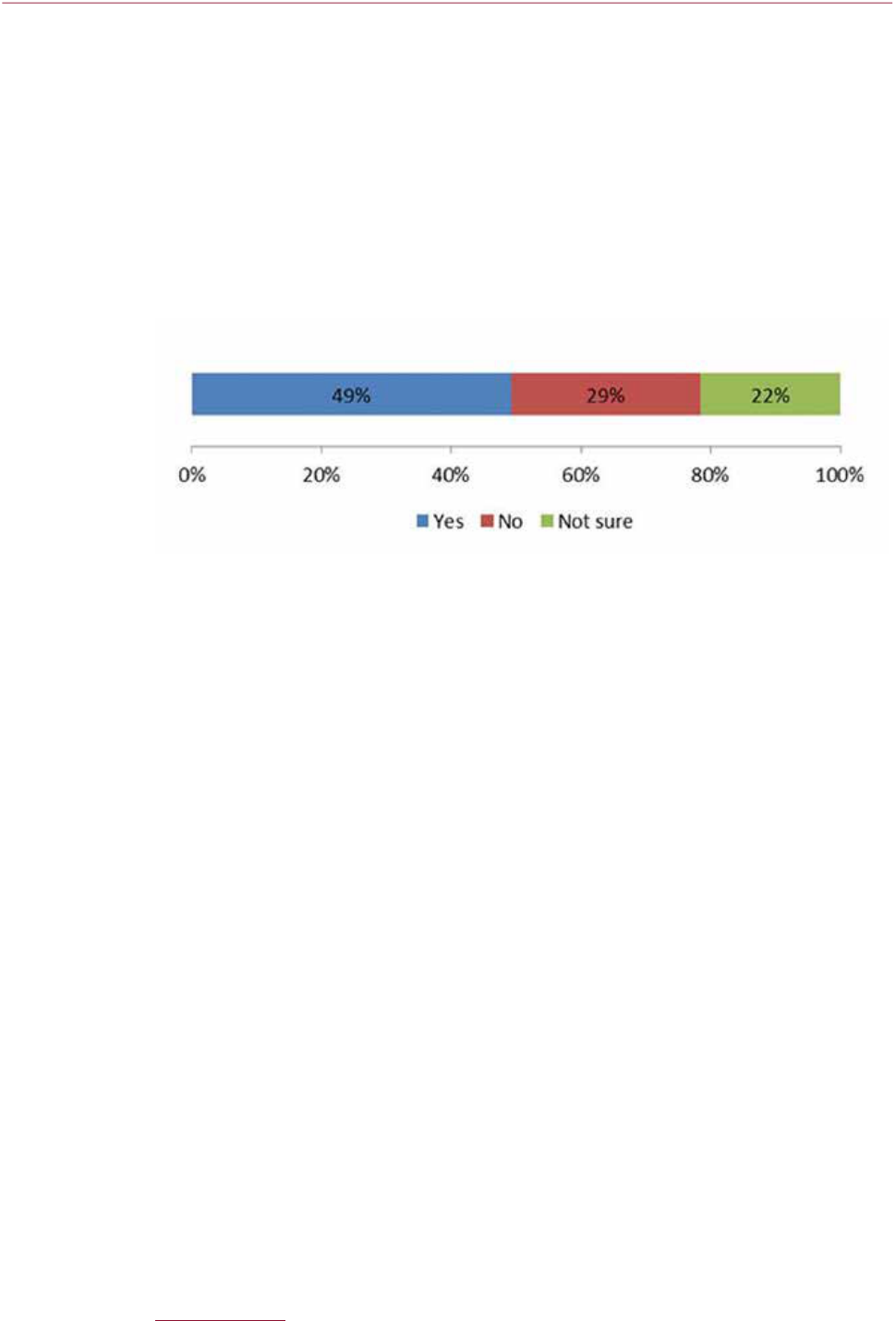

around half of the investors in our survey were not aware they were paying fund charges.

Figure 1.9 – Do you pay fund charges on your most recent investment product?

Source: NMG Consumer Research (2016)

Switching

1.39 For competition to work effectively, investors need to be able to assess whether their products

have delivered value for money and switch if alternative products are likely to better meet

theirneeds.

1.40 Investors can incur a range of costs if they switch between funds and asset managers.

Thecosts include explicit charges, tax and the time and effort it takes to switch between funds.

Investors may also be reluctant to switch if it would involve crystallising a loss or cutting short

a recommended holding period. Moreover, it is often difficult for investors to know whether

they would be better off switching providers. In some cases we have found retail investors

remaining in persistently poor performing funds.

1.41 Studies based on US and UK data suggest that there are more funds that persistently

underperform their market benchmark than would be expected in a competitive market.

Our initial analysis of equity funds available for sale in the UK shows some persistent poor

performance. These data also showed that 35% of equity funds which performed poorly

over 2005-2010 subsequently closed or merged over 2011-2015. We are undertaking further

analysis to understand the implications of fund closures and mergers on the outcomes for

investors. We welcome views from stakeholders on this.

1.42 Asset management firms told us that where they create new share classes (typically in response

to the Retail Distribution Review

20

), they find it difficult to switch investors to these new,

cheaper share classes even if this would be in the best interests of existing investors. This is

because they currently need the investors’ consent to transfer them to alternative share classes

and many investors do not respond to communications.

Ability to negotiate

1.43 Retail investors do not usually negotiate directly with asset managers and our evidence suggests

that fund governance bodies acting on their behalf do not typically focus on value for money.

On the institutional side, there are a large number of small pension schemes and trustees which

vary in how effective they are at negotiating price.

20 The Retail Distribution Review required firms to move to stop paying commission to distributors, resulting in firms moving to

‘unbundled’ shareclasses whereby commission payments are stripped from headline fees.

Financial Conduct Authority 19November 2016

MS15/2.2

Asset Management Market Study – Interim Report

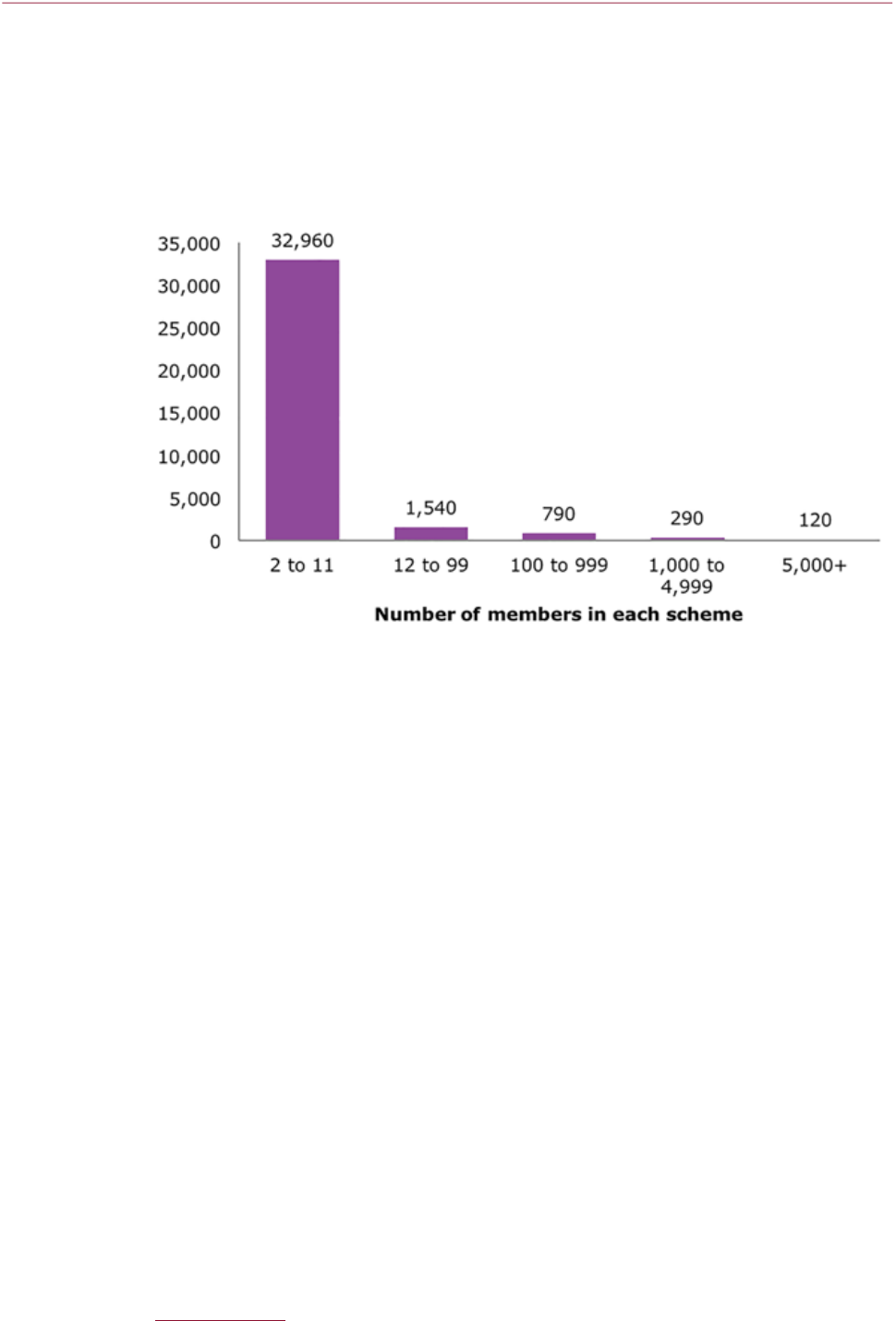

Figure 1.10: Number of defined contribution trust‑based pension schemes

21

1.44 Trustees of pension schemes, and other types of oversight committees that oversee institutional

investments, face a range of challenges in their role and their dealings with asset managers.

These include low and variable levels of investment experience on the committees and

resourceconstraints.

1.45 We found that there is a relationship between some of the challenges facing oversight

committees and their size, with smaller schemes (in terms of assets under administration and

the number of trustees), generally being less well-resourced and knowledgeable. The amount

of assets also affects oversight committees’ bargaining position, with smaller schemes being

less able to secure discounts from asset managers. It is likely that smaller pension schemes

could achieve significant cost savings from consolidating their assets.

1.46 However, there are challenges and incentives that work against consolidation. Even within

a single employer, amalgamating schemes with different objectives and funding levels is

challenging and can be costly in the short term.

The role of intermediaries

1.47 We looked at whether intermediaries help investors identify good asset managers and the

impact intermediaries have on competition between asset managers.

Retail intermediaries

1.48 There are tools available to retail investors – such as best buy lists and fund ratings – which

aim to help investors identify the best funds. Best buy lists in general use a mix of quantitative

and qualitative factors, including an assessment of the fund’s research practices, investment

processes and performance track record. In recent years, the best buy lists for retail investors

who invest through a platform have helped investors find funds that perform better than funds

21 The Pensions Regulator DC trust: a presentation of scheme return data 2015-2016

www.thepensionsregulator.gov.uk/doc-library/dc-trust-a-presentation-of-scheme-return-data-2016.aspx#s21422

20 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

not on the list. However, we note that after costs even these funds have not outperformed

their benchmarks.

1.49 Retail investors do not appear to benefit from economies of scale by pooling their money

together through direct to consumer platforms. We also have concerns about the value

provided by platforms and advisers and are proposing further FCA work in this area.

Investment consultants

1.50 Investment consultants rate asset managers and we found their ratings do influence which asset

managers institutional investors choose. While investment consultants’ due diligence means

that institutional asset managers are likely to meet minimum quality and operational standards,

we have found that these ratings do not appear to help institutional investors identify better

performing managers or funds.

1.51 In addition, whilst larger institutional investors are able to negotiate effectively with asset

managers, investment consultants do not appear to help smaller institutional investors negotiate

or otherwise drive significant price competition between asset managers.

1.52 The investment consultancy market is relatively concentrated, with the top three firms

accounting for around 60% of the market. Levels of switching in the market are low – 90%

of the investors in our survey had not switched consultant in the last 5 years. Moreover, many

institutional investors struggle to monitor and assess the performance of the advice they receive

and whether investment consultants are acting in their best interests.

1.53 We have concerns about whether the interests of investment consultants are in line with

investors’ interests. Investment consultants are expanding into fiduciary management.

22

Fiduciary management is a combination of advice, governance and carrying out investor

instructions. This means these consultants are both distributors for – and competitors to – asset

managers. We also found that investment consultants accept hospitality from asset managers,

such as concerts and sporting events. We consider that this poses a further conflict of interest

and could result in poor outcomes for end investors.

1.54 We think further investigation is therefore needed which is why we are consulting on making a

market investigation reference to the CMA on the investment consultancy market.

Conclusion

1.55 Together, these interim findings raise a series of concerns about how effectively competition

drives value for investors in the asset management sector. We believe there is room for improved

outcomes in both the institutional and retail parts of the market. However, our evidence also

suggests that competitive pressures are building in some parts of the market and stakeholders

and commentators suggest this is likely to continue.

1.56 With more effective competition, we would expect to see investors being better able to find

the best investment product for them at a reasonable price. Actively managed funds may be a

good investment for investors who prefer the associated risk exposure and, where relevant, the

chance to outperform the market. They may also be a good option for investors who want to

invest in markets where there is no passive alternative. We want these investors to be aware of

22 The exact terms of the fiduciary management agreement will be mandate specific but typically the fiduciary manager may accept

responsibility for the selection of underlying asset managers and may have discretion to deviate from the original asset allocation

decision specified by the client.

Financial Conduct Authority 21November 2016

MS15/2.2

Asset Management Market Study – Interim Report

the risks they are taking on and to pay a competitive price. For those investors seeking market

exposure we want them to invest in an appropriate fund at a competitive price.

1.57 Therefore, we propose a package of remedies to boost competitive pressure for both retail and

institutional investors and ensure a minimum level of protection for investors. This should also

increase the efficiency of the asset management industry and its attractiveness to international

and domestic investors.

Interim proposals on remedies

1.58 We have identified several ways in which asset management products and services could work

better for retail and institutional investors. We are now keen to hear from stakeholders as

we develop a package of remedies to address the issues we have found. In particular, we are

provisionally proposing:

• a strengthened duty on asset managers to act in the best interests of investors,

including reforms that will hold asset managers accountable for how they deliver value for

money, and introduce independence on fund oversight committees

• introducing an all-in fee approach to quoting charges so that investors in funds can easily

see what is being taken from the fund

• helping retail investors identify the best fund for them by:

–

requiring asset managers to be clear about the objectives of the fund and report

against these on an ongoing basis

–

clarifying and strengthening the appropriate use of benchmarks

–

providing tools for investors to identify persistent underperformance.

• making it easier for retail investors to move into better value share classes.

• requiring clearer communication of fund charges and their impact at the point of sale

and in communication to retail investors.

• requiring increased transparency and standardisation of costs and charges

information for institutional investors.

• exploring with government the potential benets of greater pooling of pension

scheme assets.

• requiring greater and clearer disclosure of duciary management fees and

performance.

• consulting on whether to make a market investigation reference to the CMA on the

institutional investment advice market.

• recommending that HM Treasury also considers bringing the provision of institutional

investment advice within the FCA’s regulatory perimeter.

22 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

1.59 We also propose further FCA work on the retail distribution of funds, particularly on the impact

that financial advisers and platforms have on value for money.

1.60 Our overall policy package will bring together a consistent and coherent framework of

interventions which will increase the transparency of costs so that those seeking information

can get it. It will also provide greater clarity of fund objectives and performance reporting and

protections for investors. When we develop this package, we will take account of the outcomes

of our consultation on transaction cost disclosure to pension schemes and Independent

Governance Committees.

Next steps

1.61 We are publishing this interim report to give all interested parties an opportunity to comment

on our emerging thinking and analysis. We appreciate the time and effort which stakeholders

have put into this study so far. We hope that this constructive engagement with stakeholders

will continue through the next phase.

1.62 We welcome your views on our findings about how competition works for asset management

products and services. We also welcome views on our emerging thinking on potential remedies.

Please send your comments to assetmanagementmarketstudy@fca.org.uk by 20 February 2017.

Financial Conduct Authority 23November 2016

MS15/2.2

Asset Management Market Study – Interim Report

2.

Our approach

We launched our market study into asset management in November 2015. Weexplained

that we want to understand how competition is working for retail and institutional

investors using asset management products and services. Since launch we have:

• issued information requests and received responses from over 50 firms including

asset managers, platform providers and investment consultants.

• conducted analysis covering over 20,000 share classes and 30,000

investmentstrategies.

• met with over 130 stakeholders in a series of round-tables and bilateral meetings.

• gathered views from over 2,500 retail investors and over 100 institutional investors

using online surveys and in-depth interviews.

Why did we decide to look into the asset management market?

2.1 We launched our market study into asset management in November 2015, with the publication

of the Terms of Reference.

23

This followed feedback from the wholesale sector competition

review, which identified areas within the asset management value chain where competition

may not be working effectively.

24

2.2 As part of that work, we identified some potential areas for consideration, based on the

feedback received about institutional asset management. These included:

• whether investors nd it difcult to monitor asset managers and ensure they are getting

value for money

• whether asset managers have the incentive and ability to effectively control costs incurred

on behalf of investors, and

• the role of investment consultants and whether there are potential conicts of interest in

the provision of both advice and asset management services.

23 FCA MS 15/2.1 Asset management market study: Terms of Reference www.fca.org.uk/publication/market-studies/ms15-02-1.pdf

24 FCA FS 15/2 Wholesale sector competition review 2014/15 at page 27.

www.fca.org.uk/publications/feedback-statements/fs15-2-wholesale-sector-competition-review-2014-15

24 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

2.3 Although these issues arose as part of our review of the wholesale sector, we considered that

retail customers were also likely to be affected by some of the competition questions raised.

2.4 Given the size of the asset management market, and the long-term nature of investments, even

a small improvement in the effectiveness of competition could substantially benefit investors.

With the growing shift from defined benefit to defined contribution schemes, the introduction

of automatic enrolment and the recently introduced pension freedoms, there are an increasing

number of end investors taking responsibility for their own pensions and savings. The choices

made by – and on behalf of – these investors can have a significant impact on the future

of their investments. So we want to understand how they make these choices and whether

competition is working effectively to drive good outcomes for them.

Scope of the study

2.5 The main focus of the market study is on how competition between asset managers is working

for retail and institutional investors that use funds and segregated mandates managed in the

UK and/or provided and marketed to UK investors.

2.6 We sought views on our Terms of Reference following its publication in November 2015 and

respondents were broadly supportive of our intended scope. We summarise the feedback we

received in Annex1.

2.7 To understand how competition works for asset management services, we have looked

at related services which affect competition for asset management. For example, we have

explored how platform providers and investment consultants affect competition between asset

managers, although our in-depth analysis has focused on the role of asset managers. Financial

advisers were largely excluded from the scope of this study since the Financial Advice Market

Review (FAMR) was ongoing at the time of launch.

2.8 Ancillary service providers are partially in scope of the study. We are interested in understanding

how asset managers buy products from these providers particularly where they pay for them

out of the investors’ money. However, as noted in the Terms of Reference, we did not carry out

an in-depth analysis into competition within these areas.

Financial Conduct Authority 25November 2016

MS15/2.2

Asset Management Market Study – Interim Report

The evidence gathered to support our analysis

2.9 We gathered data from a range of sources. We sent information requests to:

• 37 asset managers, which we selected to ensure a mix of size, businesses models,

customer types and strategies. 16 of these rms also received a more detailed nancial

information request.

• 13 investment consultants.

• 8 platforms.

2.10 We held discussions with over 20 asset management firms, 13 providers of ancillary services,

8 investment consultants, 8 advisers and adviser networks, over 20 other stakeholders and

3industry groups. We also hosted four roundtables attended by 60 industry participants under

Chatham House rule to discuss how competition was working in the retail and institutional

markets and whether regulation was creating barriers to competition. We also attended two

industry-led roundtables to discuss aspects of the market study.

2.11 We used this along with other information sources, to conduct the following pieces of analysis:

• Protability – We assessed operating margins of asset management rms in our sample

at a rm level and split by strategy, client type and asset class. We also estimated the

returns on capital employed for the rms. We analysed the relationship between assets

under management and costs to determine if the asset management rms beneted from

economies of scale. The results of this analysis are in Annex8.

26 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

• Charges along the value chain – We calculated the asset management charges for funds

and mandates. We estimated the proportion of these charges which is kept by the asset

manager and the proportion paid to third parties for services to investors. We analysed

this data at a rm level and split by strategy, client type and asset class. We also combined

the estimated charges with performance data to see how these charges affect investor

outcomes. The results of this analysis are in Chapters 6 and 7.

• Drivers of fund ows – We have performed an econometric analysis (using statistical

analysis techniques to assess economic issues) to understand what drives net ows of

funds between asset managers. We have conducted this analysis to understand which

factors investors respond to when making investment decisions. We think these are the

factors which asset managers compete with each other to attract investors. This analysis

complements the retail and institutional surveys. The results of this analysis can be found

in Annexes4 and 6.

• Ratings and recommendations value added – We conducted an econometric analysis to

assess whether ratings and recommendations used by investors add value in the investment

process. Specically, we assessed if ratings and recommendations (such as platform best

buy lists and ratings given by investment consultants) can identify superior-performing asset

managers. The results of this analysis are in Chapter4 and Annex6.

• Adviser incentives – We analysed if revenue received from asset managers has affected

how investment consultants have constructed their ratings and the implications of this.

Theresults of this analysis are discussed in Chapter8 and Annex6.

• Pricing analysis – We assessed pricing data from a sample of asset managers to understand

pricing trends over time, differences in prices between sellers ‘price dispersion’, and

differences in pricing between investor groups. The results of this analysis are in Chapter6.

• Investor returns – We analysed gross and net returns to both retail and institutional

investors to understand whether there are systematic differences in the results for different

investor groups, and if so, why. The results of this analysis are in Chapter6.

• Barriers to effective decision-making by oversight committees of pension funds.

We commissioned academic work to help us understand the dynamics of, and obstacles

to, effective investment decision-making by oversight committees. This included a review

of economic, behavioural and corporate governance literature. The academic work also

involved analysis of an online survey of pension fund trustees and in-depth interviews with

market participants. The results of this analysis are in Annex5.

• Supervision work on fund governance and dealing commission: We have used the

results of our supervisory work where it provides insights into the questions addressed in

this market study.

2.12 We also commissioned 40 in-depth interviews and a survey of 2,500 non-advised retail investors.

We wanted to understand how retail investors make choices and review their investment over

time (see Annex3). To understand how institutional investors make their choices, we ran our

own online survey with 89 respondents and had one-to-one discussions with 30 institutional

investor groups (see Annex5).

Financial Conduct Authority 27November 2016

MS15/2.2

Asset Management Market Study – Interim Report

2.13 Our engagement process has indicated a possible lack of awareness of competition law in

some areas of the sector, in particular as to how the law applies to commercial relationships

and interactions with one another.As an example, information exchange between competitors

may be prohibited under competition law if it makes firms aware of their competitors’ market

strategies.We intend to keep this issue under review as the market study progresses.

Why are we publishing an interim report?

2.14 We want this interim report to give all interested parties an opportunity to comment on

our emerging thinking and analysis. We hope this will encourage continued constructive

engagement between the FCA and firms, trade associations, consumer bodies, institutional

investor representatives and other interested parties.

2.15 Having gathered comments and observations, we expect to publish a final report along with

any proposed amendments to our rules by Q2 2017.

2.16 In this report, we set out our initial observations on how competition works for both retail

and institutional asset management, highlighting areas where we think that it can work more

effectively. We also set out our initial thinking on potential remedies in light of these findings.

Structure of this interim report

2.17 In order to understand how asset managers compete to deliver value, our analysis focused on

six core questions:

• How do investors choose between asset managers? We analysed how investors

choose between asset managers and the implications for how asset managers compete to

win business from retail and institutional investors. See Chapter4.

• How do intermediaries and fund governance bodies affect competition between

asset managers? We explored the impact investment consultants and platforms have on

competition between asset managers and whether fund governance bodies scrutinise value

for money on behalf of investors. See Chapters 5 and 8.

• What do prices, prots and performance tell us about how competition is working?

We explored what prices, prots and performance imply for the way in which competition

is working and what the implications are for different investor groups. See Chapter6.

• Are asset managers willing and able to control costs and quality along the value

chain? The returns investors receive are affected by the costs and quality of the services

that asset managers use. We looked at whether investors can monitor the costs and quality

of services they pay for, if these services add sufcient value for end investors and whether

asset managers are able and willing to control the costs and quality of the services they buy

on behalf of their funds. See Chapter7.

• How do investment consultants affect competition for institutional asset

management? Investment consultants play a pivotal role in advising institutional investors

on how to allocate their assets and which managers to select. We have looked at how

the advice given by investment consultants affects competition between asset managers

28 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

and what impact it has on the returns for institutional investors. We have examined how

investment consultants manage conicts within their business model and whether clients

can monitor the services provided. See Chapter8.

• Are there barriers to innovation and technological advances? We have explored

whether there are factors, including regulatory barriers, which prevent asset managers from

innovating and improving their technology. See Chapter9.

Financial Conduct Authority 29November 2016

MS15/2.2

Asset Management Market Study – Interim Report

3.

Overview of the asset management sector

Around £6.9 trillion of assets are managed in the UK. Of this, over £1tn is on

behalf of UK retail investors and around £3tn is on behalf of UK pension funds

and other institutional investors. Around £2.7tn is managed in the UK on behalf of

overseasclients.

The majority of UK households use asset management services. Approximately three

quarters of UK households have occupational or personal pensions and 14% of adults

hold stocks and shares ISAs.

Most assets are under active management, with 23% of assets invested passively;

but, the proportion which are passively managed has been growing gradually.

The industry is not particularly concentrated, with the largest ten asset management

firms operating in the UK accounting for around 55% of total assets under

management.

The asset management industry is heavily intermediated. Retail investors are

increasingly using platforms to access services. Pension schemes, which represent

£2.1tn or 38% of managed assets, need to get advice related to investment matters

from qualified advisers with appropriate knowledge and skills. To fulfil this requirement

pension scheme trustees tend to seek investment consultant advice on what they

should invest in and which asset managers to choose.

Background

3.1 In this section we provide some detail about the asset management industry and its participants,

to provide context for the market study.

3.2 Asset managers (also known as investment managers – we use the term asset manager

throughout this document) provide an important economic function in bringing together those

with money to invest with governments and companies who need capital. Asset managers also

act as the representatives of those who own capital and, in this role, can provide oversight and

stewardship of the investments they make.

30 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

3.3 Asset managers are agents who perform investment management services on behalf of others.

This involves two activities:

• making investment decisions on behalf of others

• operating the investment schemes which pool investors’ assets and placing them under the

control of those who make investment decisions

3.4 In terms of assets under management, the UK asset management industry is the largest in

Europe and second only to the US globally.

25

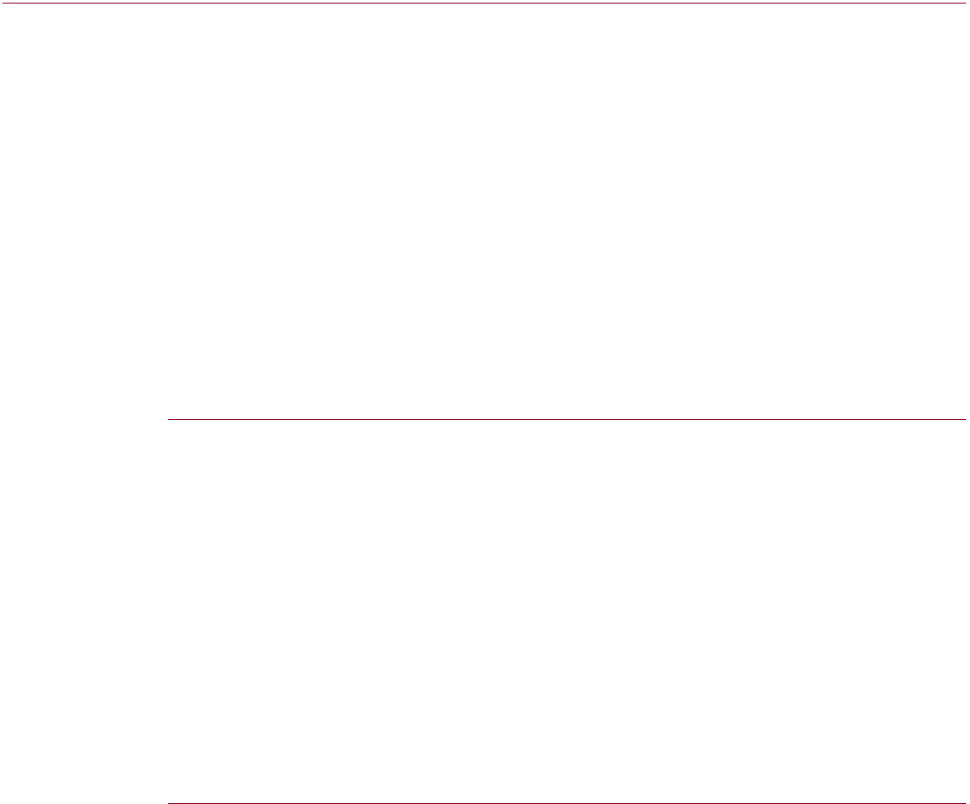

As Figure3.1 shows, assets being managed by

The Investment Association (IA) members have increased year on year since 2008.

3.5 The IA estimates that nearly 40% of assets managed in the UK are for overseas clients.

26

The asset management sector contributes significantly to the UK economy, both in terms of

employment and tax revenue. In 2015 the UK asset management industry earned around

£17billion in revenue and generated about 1% of UK GDP.

27

Figure3.1: Assets under management in the UK (managed by IA members)

Source – IA figures

There is an estimated further £1tn managed by firms which would not be included in the

above data.

28

25 £6.9trillion – 2015 figure, Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf, £6.8trillion – 2014 figure, The City UK

www.thecityuk.com/assets/2015/Reports-PDF/UK-Fund-Management-An-attractive-proposition-for-international-funds.pdf.

26 Asset Management in the UK 2015-2016. A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

27 Total average industry revenue, which is equivalent to a 6% increase in nominal terms. Asset Management in the UK 2015-2016,

A summary of the IA Annual Survey (September 2016) www.theinvestmentassociation.org//assets/files/research/2016/20160929-

amsfullreport.pdf 1% contribution to GDP is an estimate The contribution of asset management to the UK economy Oxera

(July2016) www.theinvestmentassociation.org/assets/files/press/2016/The%20contribution%20of%20asset%20management%20

to%20the%20UK%20economy.pdf

28 Based on estimates of the proportion of the part of the total UK market accounted for by non-IA members.

Financial Conduct Authority 31November 2016

MS15/2.2

Asset Management Market Study – Interim Report

Clients/investors

3.6 As illustrated in Figure3.2, institutional investors are the largest client type, accounting for

nearly 80% of AUM in the UK compared to retail investors who account for less than20%.

29

Pension funds are the largest single institutional client type with £2.1 trillion of assets

under management.

30

The distinction between client types is important as the behaviours,

relationships and governance may be different for institutional and retail investors (or within

those client types). Institutional investors are more likely to have an individual investment

portfolio (segregated mandate) at least for part of their investments, while retail investors

are more likely to be invested in pooled funds (where their money is managed alongside

otherinvestors’).

Figure3.2: Assets managed in the UK by client type as at end 2015

Source – IA data

3.7 Even though they are labelled as institutional (including in Figure3.2), the end-beneficiaries

of many institutional investments are individual investors. 75% of UK households have

occupational or personal pension wealth

31

and defined benefit (DB) schemes still make up

the greatest share of pension scheme assets.

32

IA member firms manage £1.5trillion of DB

assets.

33

However, only 13% of schemes were still open to new entrants and future accrual as

at December 2015.

34

29 Asset Management in the UK 2015-2016. , A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

30 Estimate based on IA and FCA figures. Asset Management in the UK 2014–2015, The Investment Association Annual Survey

(September 2015) www.theinvestmentassociation.org/assets/files/research/2015/20150914-ams2014-2015-fullsurvey.pdf

This figure includes defined benefit (DB) and some defined contribution (DC) schemes, DC pension assets that are operated via an

intermediary platform are reflected in the insurance client data.

31 The contribution of asset management to the UK economy Oxera (July 2016)

www.theinvestmentassociation.org/assets/files/press/2016/The%20contribution%20of%20asset%20management%20to%20

the%20UK%20economy.pdf

32 Defined benefit schemes remove much of the decision-making and risk from the individual investor.

33 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

34 The Purple Book (2015) www.pensionprotectionfund.org.uk/DocumentLibrary/Documents/purple_book_2015.pdf

32 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

3.8 Defined contribution (DC) schemes, however, continue to grow – partly due to the introduction

of automatic enrolment.

35

The shift from DB pension schemes to DC schemes means that

individuals bear more risk and employers bear less. The risk and reward sits firmly with the

individual investor in DC schemes. To some extent so does the choice of fund, although

support is provided by DC scheme trustees or the employer, for example in selecting the default

fund option.

3.9 Retail investors may invest in asset management services through product ‘wrappers’

(including pension and ISA wrappers). In 2015 14% of the UK adult population held stocks and

shares ISAs

36

, and during the past eight years the average yearly subscription per account has

been higher for stocks and shares ISAs than for cash accounts.

37

In 2015 69% of total stocks

and shares ISA value was held in funds

38

and in 2016 the fund and trust holdings in stocks and

shares ISA accounts was approximately £172bn.

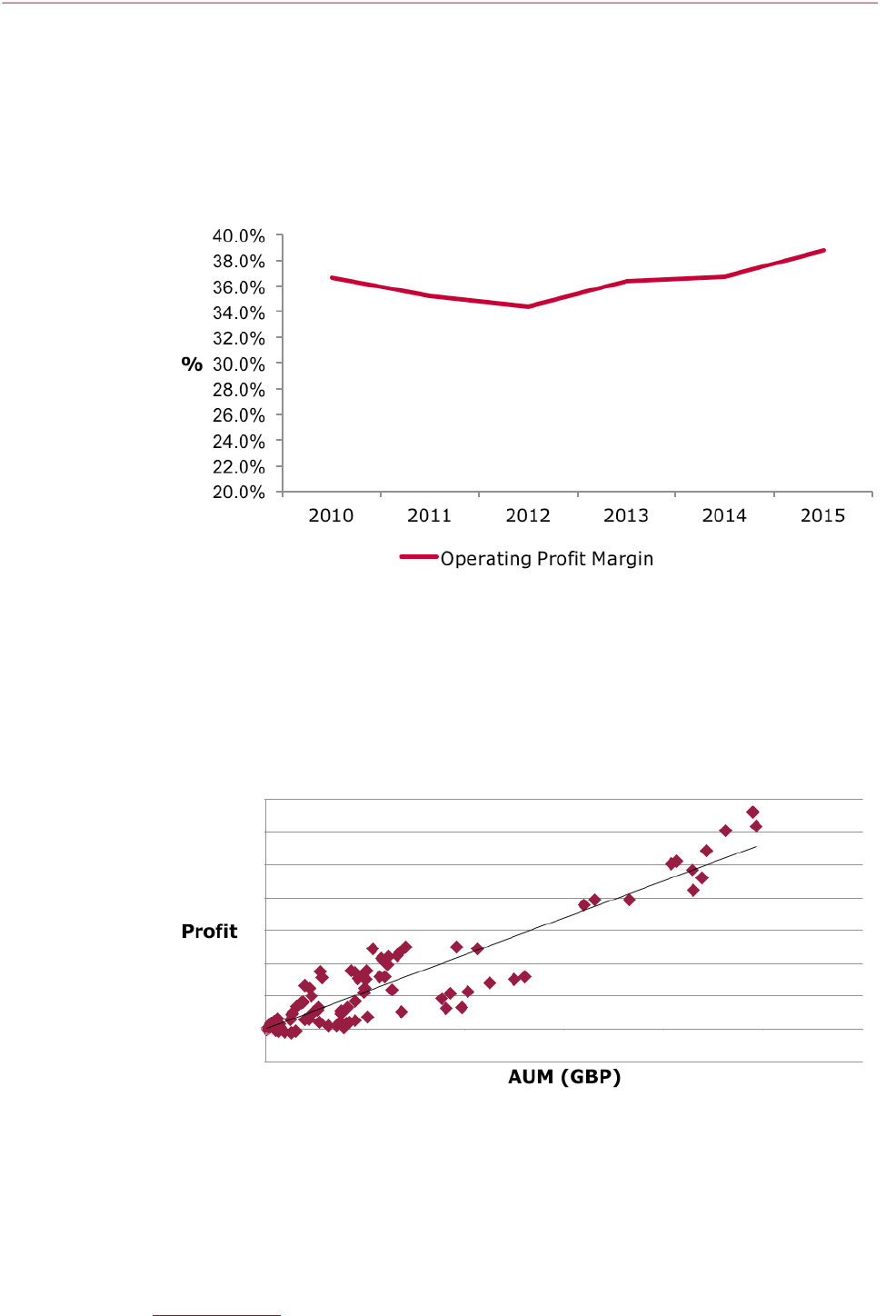

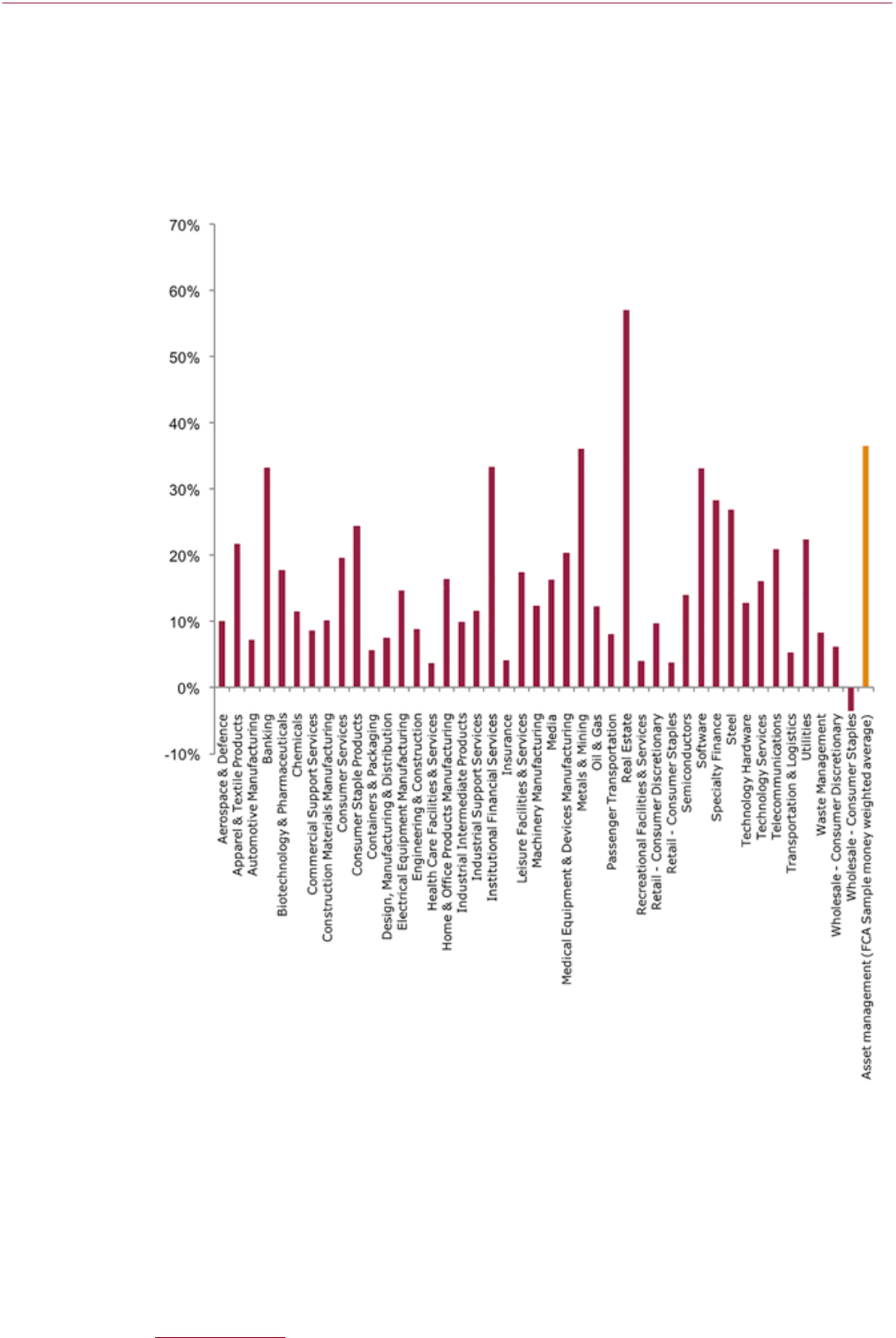

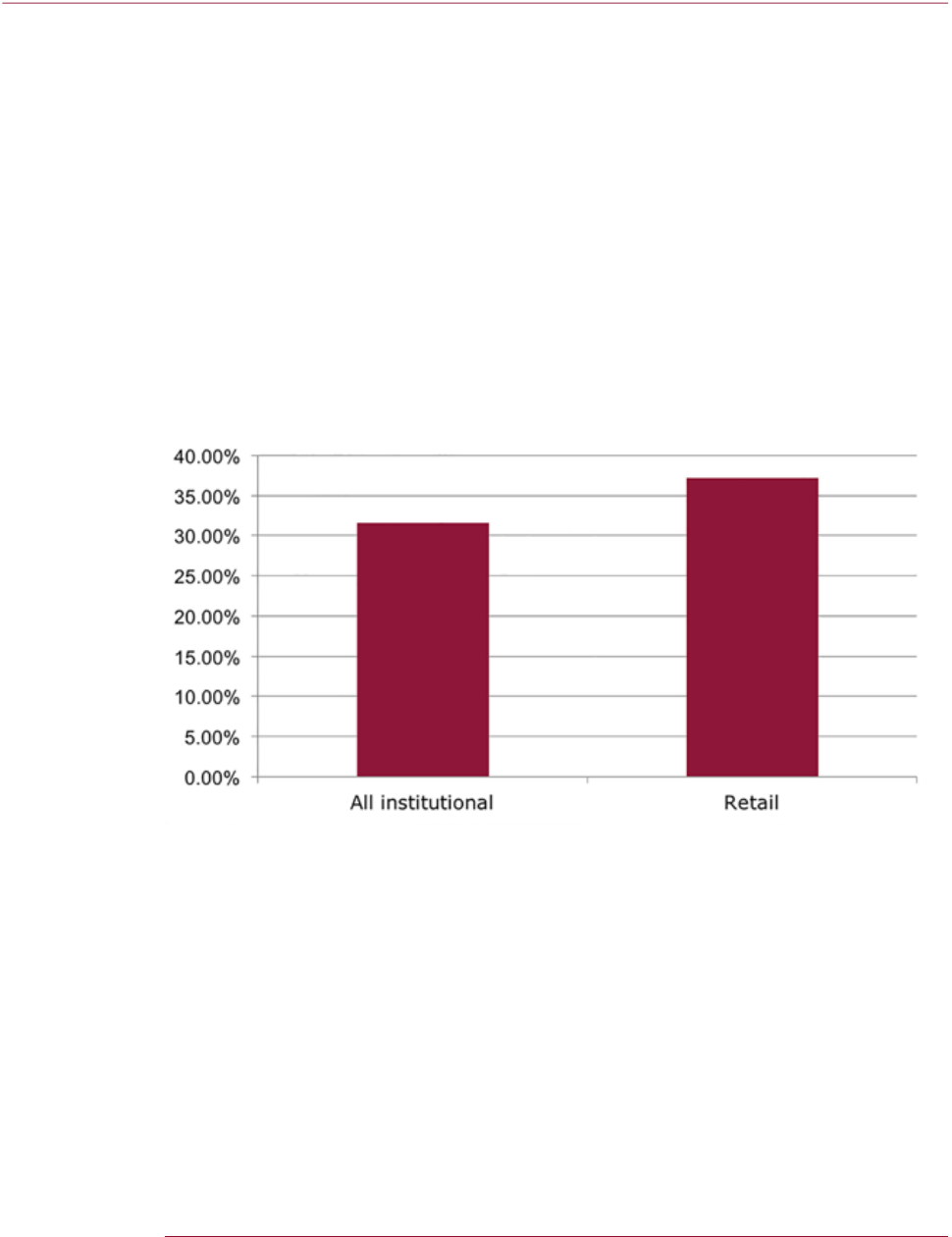

39

3.10 Significant numbers of retail investors also access asset management services through personal

pensions. There were nearly 15million policyholders with individual personal pensions at life

insurers in 2015.

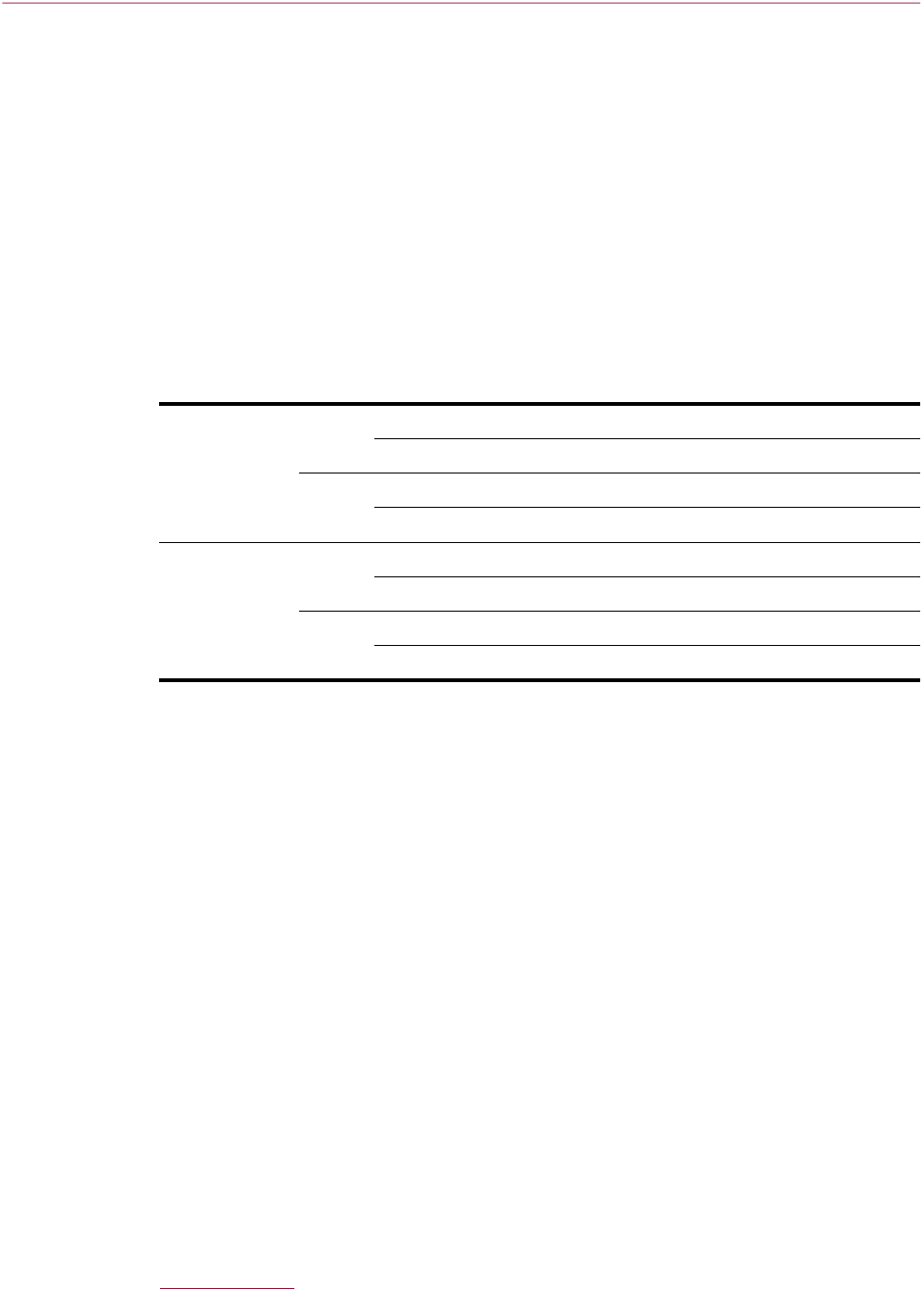

40

3.11 Investors may also access products and funds outside a wrapper, either directly or through a

platform. In 2015, 5% of households had money held in unit trusts or investment trusts outside

of wrappers; totalling an estimated £30bn.

41

3.12 Retail investors can also get financial advice from advisers who can play a role in both designing

and implementing investment decisions.

Asset management rms

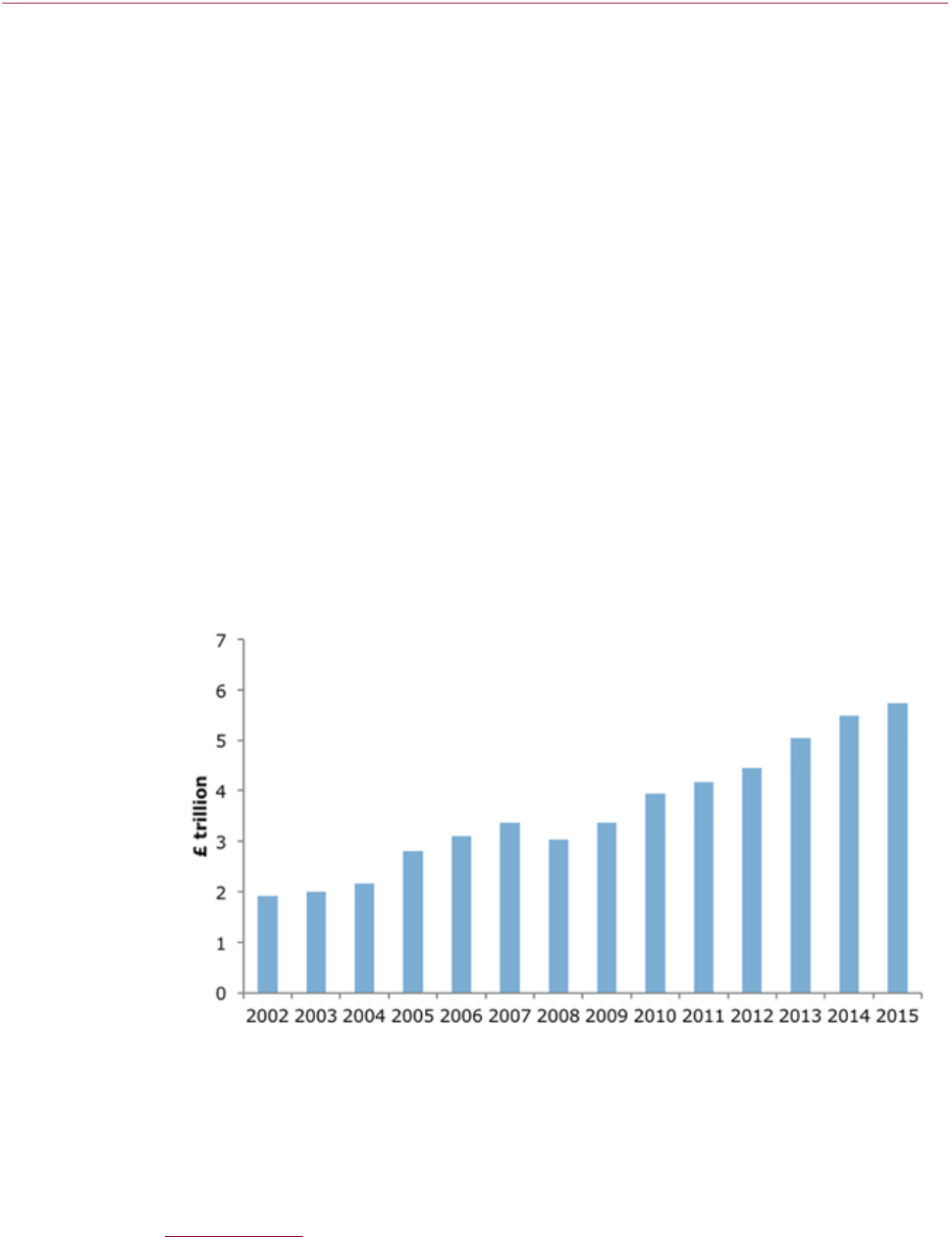

3.13 The number of asset management firms currently authorised in the UK stands at 1,840, a 2%

increase since 2014.

42

Between 2011 and 2015, at least 750 new asset management firms were

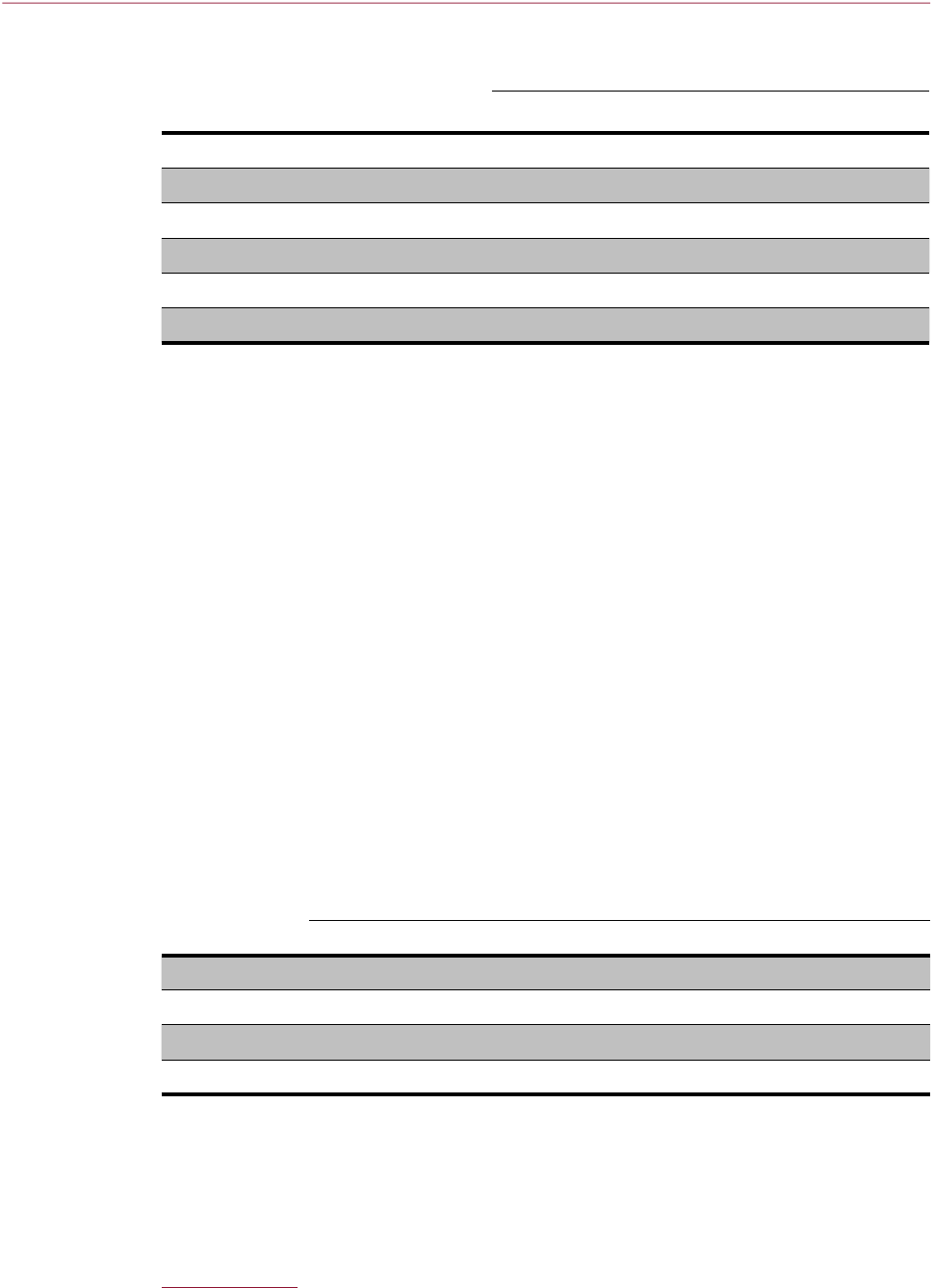

authorised that currently remain authorised and active.

43

35 NAPF Annual Survey (2014) revealed that active membership of DC schemes now outnumbers that of DB schemes for the first time:

www.napf.co.uk/PolicyandResearch/Research/Annual-Survey.aspx

36 Based on ONS population statistics and ISA subscription statistics – Population statistics:

www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates ISA statistics:

www.gov.uk/government/uploads/system/uploads/attachment_data/file/547217/Full_Statistics_Release_August_2016.pdf

37 For example, in the 2015-2016 subscription year the average subscription per stocks and shares account was £8,443 compared with

£5,810 in cash ISA accounts. Individual Savings Account (ISA) Statistics HM Revenue & Customs data (August 2016)

www.gov.uk/government/uploads/system/uploads/attachment_data/file/547217/Full_Statistics_Release_August_2016.pdf

38 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

39 Market value of holdings as of 5April 2016, based on HM Revenue & Customs and ONS data

40 Based on annual insurance returns submitted to the Prudential Regulation Authority and FCA. This understates the true number

of policyholders as it doesn’t include non-insurance company personal pension providers e.g. standalone SIPP Operators, asset

managers or Banks with a personal pension scheme.

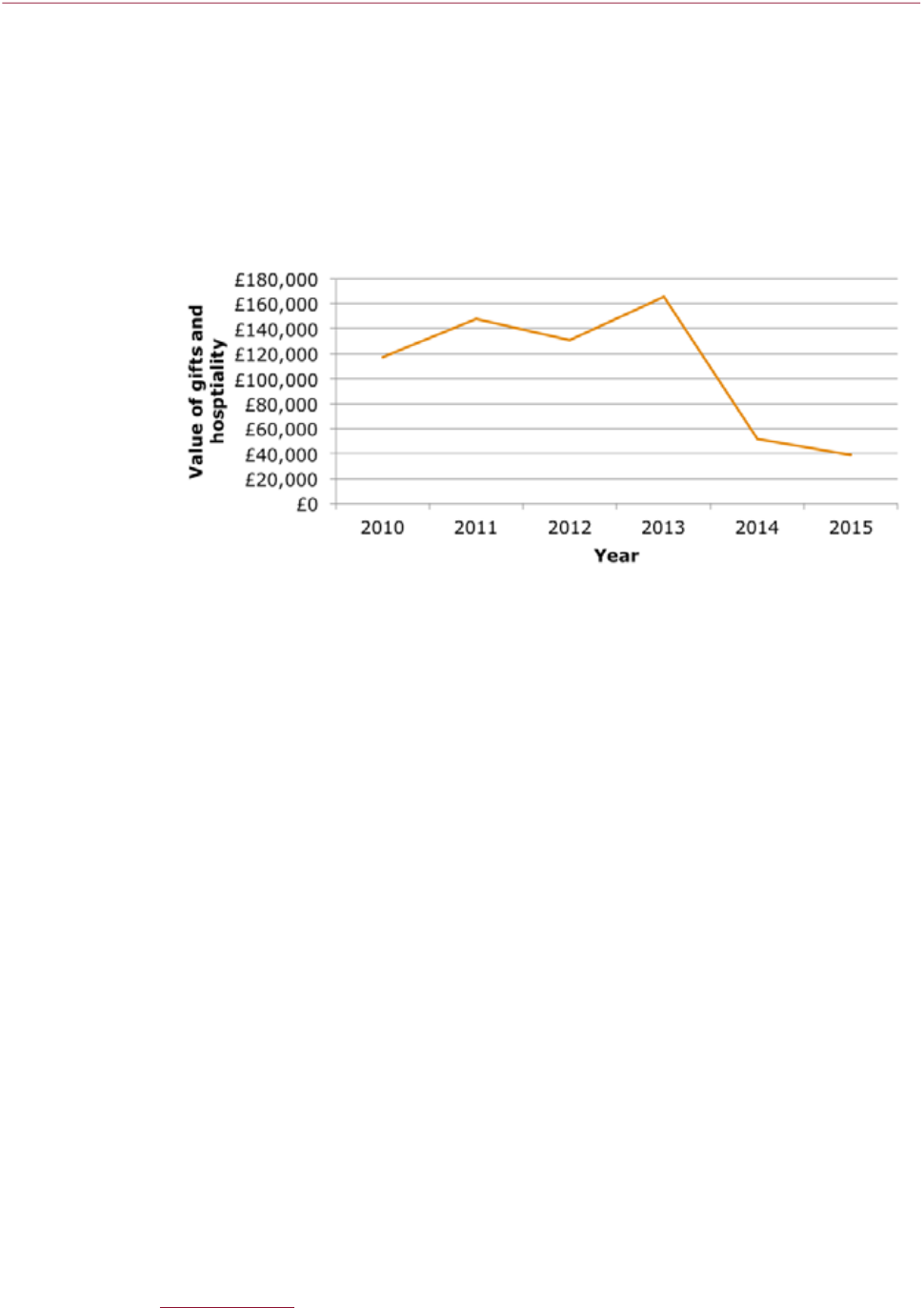

41 Calculation based on the median value of holdings of £25k per unit/investment trust holding household; original data based on

estimates www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/compendium/wealthin

greatbritainwave4/2012to2014/chapter5financialwealthwealthingreatbritain2012to2014

42 FCA internal data

43 Those firms which still had ‘authorised’ status in May 2016, which had been authorised between 2011 and 2015. This does not

include registered firms. For example, between 2014-15 131 additional legal entities were registered, all of which were small

UK-registered AIFMs.

Financial Conduct Authority 33November 2016

MS15/2.2

Asset Management Market Study – Interim Report

Figure3.3: Number of authorised asset management firms

44

Source – FCA Data based on firm reporting (AUM greater than zero) up to September 2016

3.14 The fund market continues to grow, both in terms of total assets under management (AUM)

and net flows into funds.

45

In 2014, there were 104 newly launched funds which were classified

to IA sectors

46

receiving £60billion in net sales over the year. In 2015, there were 172 new

fund launches.

47

Equities have been the predominant choice of asset class for flows into newly

launched funds in recent years.

48

3.15 The asset management industry does not appear particularly concentrated,

49

with the top ten

asset managers accounting for around 55% of the assets under management.

50

However, a

large number of competitors does not necessarily mean there is effective competition. Effective

competition implies that firms have sufficient incentives to identify and satisfy clients’ demands

as efficiently as possible and constantly seek to win the business of clients who use rivals’

services. The benefits of achieving effective competition include lower prices for investors,

better quality service and greater innovation.

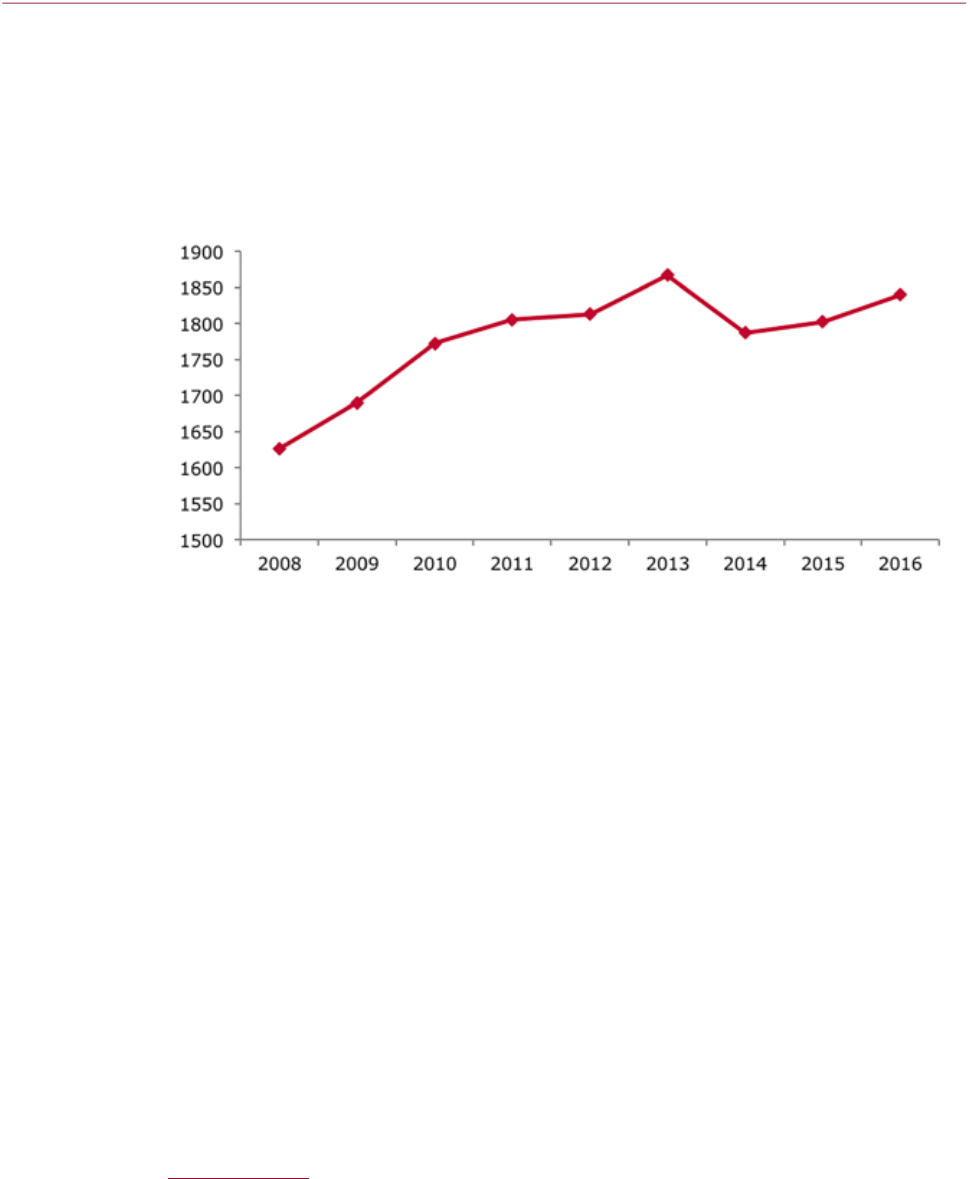

3.16 For example, as shown in Figure 3.4, there is considerable clustering of prices for active

equity funds at both 1% and 0.75% for clean share classes (those that do not include

distributionpayments).

44 Reporting an AUM of more than zero.

45 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

46 Different categories of funds which have been developed by the IA.

47 Based on Morningstar data.

48 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

49 We estimate a Herfindahl-Hirschmann Index of 780 which indicates that the asset management industry is not particularly

concentrated. The Herfindahl-Hirschman Index (HHI) calculates the sum of the squares of the market shares of all firms in the

market, in order to obtain an overall figure that indicates the level of concentration in a market, accounting for the relative size of

the firms. This estimate should be treated with caution due to our method for estimation. We have based our estimate on assets

reported by regulated firms in regulatory returns. Amendments were made to reflect market shares at a group level and estimated

cross-holdings. This result is not inconsistent with other third party calculations.

50 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

34 Financial Conduct AuthorityNovember 2016

MS15/2.2

Asset Management Market Study – Interim Report

Figure3.4 AMC by size of fund

3.17 The top ten fund operators

51

represent approximately 47% of the total UK authorised funds

under management at the end of 2015.

52

This proportion has remained broadly unchanged

since the 1990s, though the firms in the top 10 have changed over time.

53

3.18 There has been a slight increase in concentration in equity products over recent years, and

multi-asset and fixed income markets appear to be fairly stable.

51 This could be the Authorised Fund Manager, Authorised Corporate Director or the person appointed or responsible for managing of

the property held for, or within, a scheme. For the full regulatory definition see the FCA Handbook.

52 The IA define ‘UK authorised funds’ in this context as UK-domiciled authorised investment funds (whichincludeauthorised Unit

Trusts and OEICs).

53 Asset Management in the UK 2015-2016, A summary of the IA Annual Survey (September 2016)

www.theinvestmentassociation.org//assets/files/research/2016/20160929-amsfullreport.pdf

Financial Conduct Authority 35November 2016

MS15/2.2

Asset Management Market Study – Interim Report

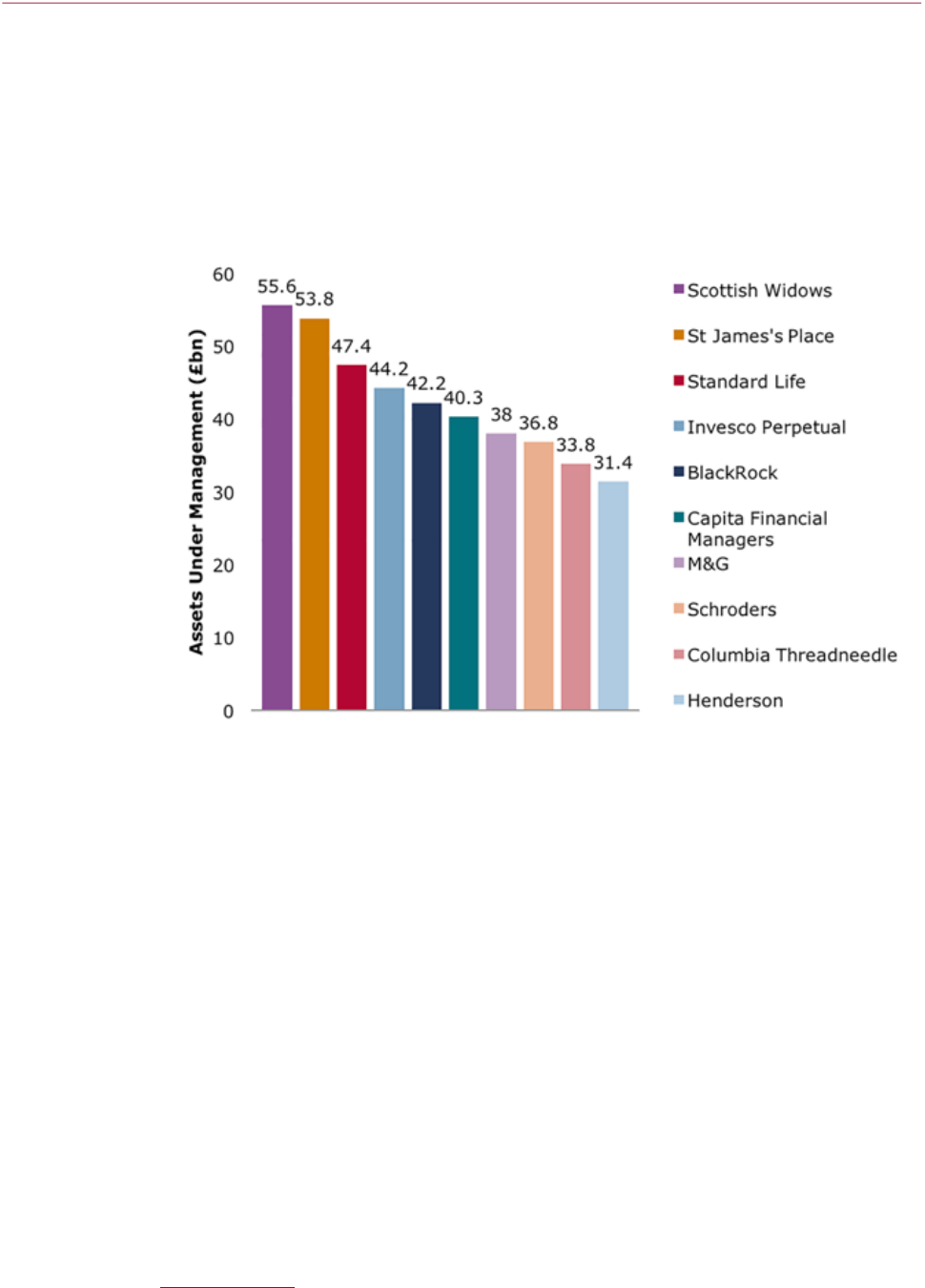

Figure3.5: Top ten UK fund operators by total funds under management as at

endof 2015

Source – IA data

3.19 Certain parts of the sector do have areas of higher concentration. In Liability Driven Investment

(LDI) mandates

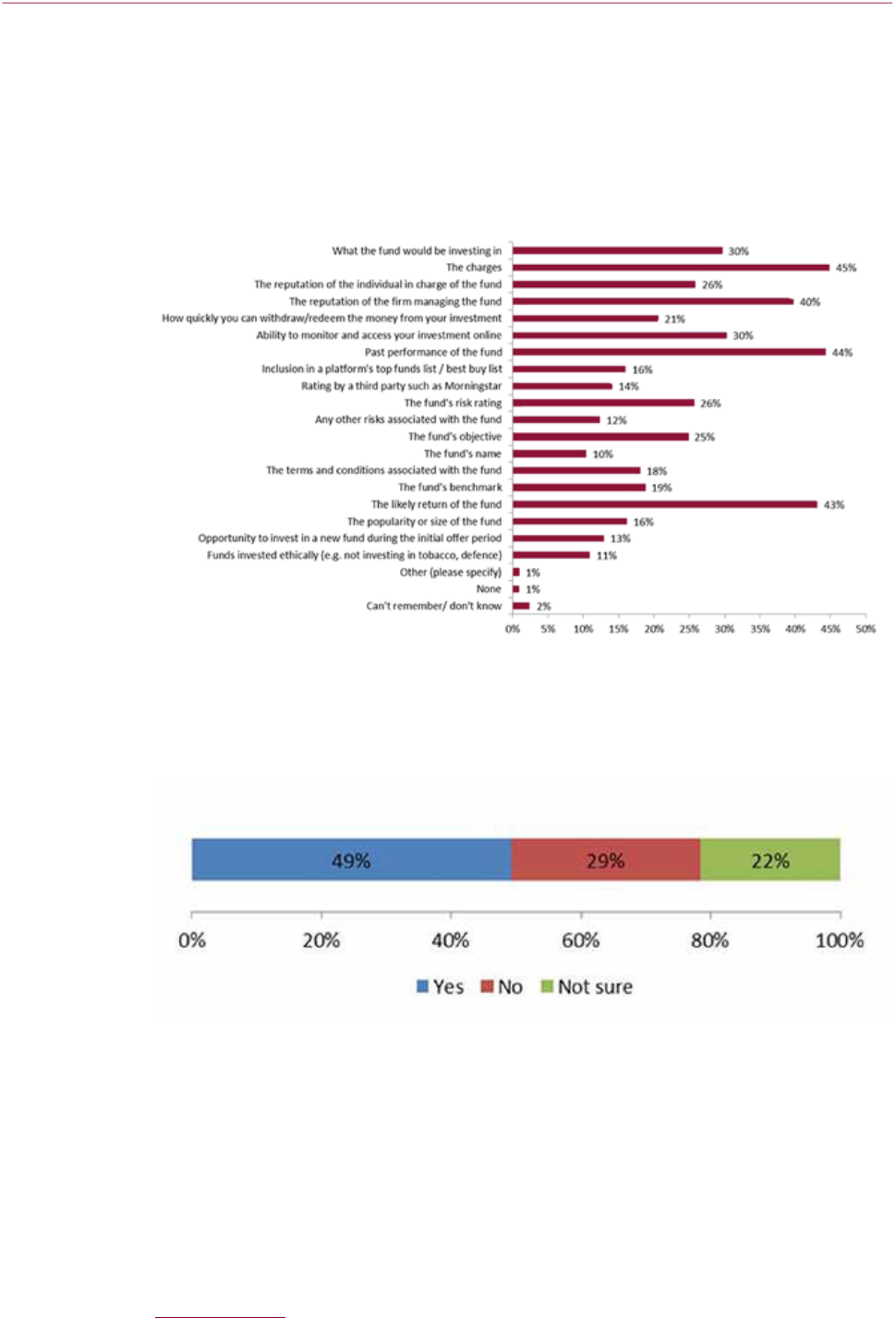

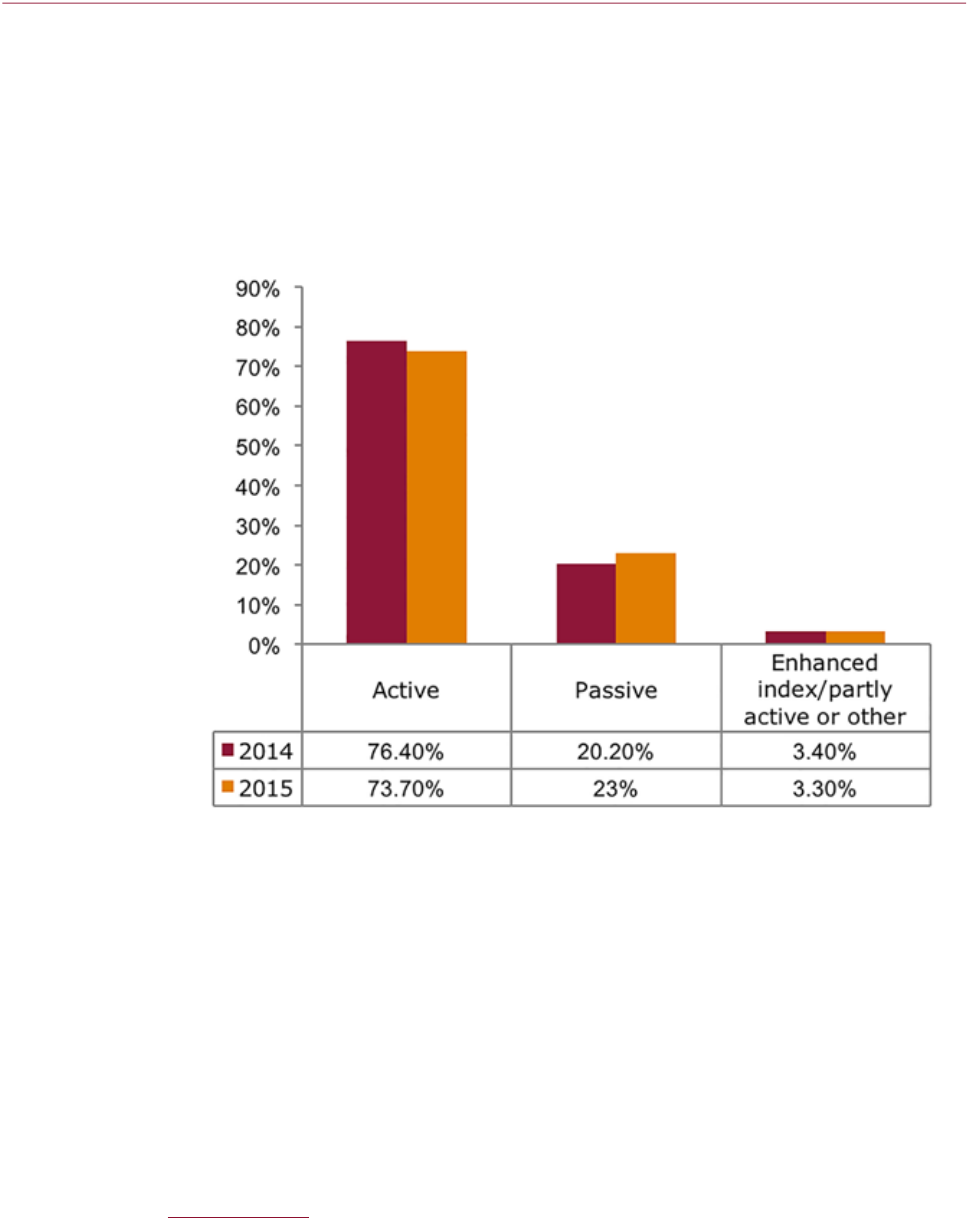

54