DISCUSSION DRAFT

A Reconsideration of Fiscal Policy in the Era of Low Interest Rates

Jason Furman and Lawrence Summers

1

November 30, 2020

The last generation has witnessed an epochal decline in real interest rates in the United

States and around the world despite large buildups of government debt. As Table 1 illustrates

U.S. ten-year indexed bond yields declined by more than 4 percentage points between 2000 and

early 2020 even as projected debt levels went from levels extremely low by historical standards

to extremely high by historical standards. Similar movements have been observed at all

maturities and throughout the industrial world. Available market data suggests that the COVID

crisis has depressed real interest rates despite raising government debts, likely by increasing

inequality, uncertainty and the use of information technology.

Table 1

Note: Debt-to-GDP forecast is the CBO 10-year ahead forecast (2030 from June 2019 Alternative Fiscal Scenario for 2020). Real

interest rates are based on 10-year Treasury Inflation Protected Securities (TIPS) from January 2000 and February 2020.

Source: Congressional Budget Office (2000, 2019b); U.S. Department of the Treasury; authors' calculations.

This paper argues that while the future is unknowable and the precise reasons for the

decline in real interest rates are not entirely clear, declining real rates reflect structural changes in

the economy that require changes in thinking about fiscal policy and macroeconomic policy

more generally that are as profound as those that occurred in the wake of the inflation of the

1

Jason Furman is a Professor of the Practice of Economic Policy jointly at the Harvard Kennedy School and the

Economic Department at Harvard University as well as a non-resident Senior Fellow at the Peterson Institute for

International Economics. Lawrence Summers is the Charles W. Eliot Professor and President Emeritus at Harvard.

The authors are indebted to extraordinary research assistance by Wilson Powell III and additional research

assistance by Joseph Kupferberg. The authors have benefited from innumerable conversations on these topics with

many people over the years and specific inputs to this paper from Wendy Edelberg, Richard Kogan and Brian Sack.

2000 2020

Debt-to-GDP (10-year ahead forecast) 6% 109%

Real Interest Rates 4.3% -0.1%

U.S. Debt is Much Higher

But Interest Rates Are Much Lower

2

1970s. In terms of the dichotomy posed by Blanchard and Summers (2019) we believe the

evidence points increasingly towards revolution rather than evolution.

Our analysis begins by considering the downward trend in real rates. We note that with

massive increases in budget deficits and government debt, expansions in social insurance, and

sharp reductions in capital tax rates, one would have expected to see increasing real rates if

private sector behavior had remained constant. We suggest that changes in the supply of saving

associated with lengthening life expectancy, rising uncertainty and increased inequality along

with reductions in the demand for capital associated with demographic changes, demassification

of the economy, and perhaps changes in corporate behavior have driven real interest rates down.

It may well be that, as suggested by Stansbury and Summers (2020), declines in the sensitivity of

spending to real rates due to declines in interest-sensitive spending as a share of GDP and other

factors have exacerbated the decline in real rates. We argue that neutral real rates are as likely to

fall below their levels immediately prior to COVID as they are to rise above them. Finally, we

consider the role of monetary policies, changing asset supplies and risk premiums in affecting

long-term real rates concluding that they are likely minor and, in any event, that the precise

reasons for declining real rates do not much affect their implications for fiscal policy.

We discuss three implications for fiscal policy that follow from low interest rates:

First, fiscal policy must play a crucial role in stabilization policy in a world where

monetary policy can counteract financial instability but otherwise is largely “pushing on a string”

when it comes to accelerating economic growth. The roughly 600 basis point reductions in rates

that have been found necessary to counteract recessions will be infeasible for the foreseeable

future. Limitations on how far interest rates can be reduced given the zero lower bound and the

possible inefficacy of lower rates in stimulating demand raise the possibility that full

employment may be infeasible with overly restrictive fiscal policies. Even if full employment is

feasible with a given fiscal policy there is the possibility that the necessary very low interest rate

level will be associated with excessive leverage and put financial stability at risk. These views

represent a departure from the orthodoxy of the last generation. They open up the prospect that

countries may be less constrained by fiscal space because fiscal expansions themselves can

improve fiscal sustainability by raising GDP more than they raise debt and interest payments.

They also imply that policymakers need to do more to both improve automatic recession

insurance and also find more ways to use fiscal policy to expand demand without increasing

3

deficits, for example through balanced budget multipliers, more progressive fiscal policy and

also expanded social insurance.

Second, we reconsider traditional views about the dangers of debt and deficits. We note

that in a world of unused capacity and very low interest rates and costs of capital, concerns about

crowding out of desirable private investment that were warranted a generation ago have much

less force today. We argue that debt-to-GDP ratios are a misleading metric of fiscal sustainability

that do not reflect the fact that both the present value of GDP has risen and debt service costs

have fallen as interest rates have fallen. Instead we propose that it is more appropriate to

compare debt stocks to the present value of GDP or interest rate flows with GDP flows. We note

that at current and prospective interest rate levels nominal and real Federal debt service is likely

to be low not high by historical standards over the next decade, a point that is strengthened when

account is taken of interest recycled to the Treasury by the Federal Reserve and interest receipts

on Federal financial assets. Moreover, current debt levels are at low rather than high levels

relative to calculations of the present value of GDP or prospective tax receipts. The kind of

reasoning employed in formulating the Maastricht criteria a generation ago does not suggest

alarm about current debt levels or those over the next decade in the United States or most

European countries. While current projections do raise concerns over the fiscal situation beyond

2030 we note that that there is enormous uncertainty and that much of the issue would be

addressed if necessary reforms internal to Social Security and Medicare were undertaken.

Third, we consider the issue of borrowing in the context of how the borrowed funds are

used. We highlight that traditional notions of financial responsibility for households and

businesses hold that borrowing in order to invest in assets that have a return well in excess of the

cost of borrowing increases creditworthiness and benefits future stakeholders. Think for example

of a household that accumulates equity by owning rather than renting the home in which it lives

or a business that owns rather than leases its headquarters. Drawing on recent work considering

dynamic scoring effects of various Federal expenditure programs we argue that borrowing to

finance appropriate categories of Federal expenditure pays for itself in Federal budgetary terms

on reasonable assumptions.

We conclude with thoughts on appropriate guidelines for U.S. fiscal policy. We reject

traditional ideas of a cyclically balanced budget on the grounds that it would likely lead to

inadequate growth and excessive financial instability. We set the goal that fiscal policy should

4

advance economic growth and financial stability. Achieving this goal depends on both improving

responses to downturns and expanding and improving public investment. As a new guidepost,

we propose that fiscal policy focus on supporting economic growth while preventing real debt

service from being projected to rise quickly or to rise above 2 percent of GDP over the

forthcoming decade. We also propose three guidelines that would be consistent with achieving

this broader objective within the guidelines we recommend: (i) undertaking substantial

emergency spending that is not paid for in response to economic downturns; (ii) paying for all

long-term commitments with broad exceptions for ones that plausibly pay for themselves in

present value; and (iii) improving the composition of government to make it more supportive of

demand and also more efficient.

The surprising and likely long-lasting decline in interest rates

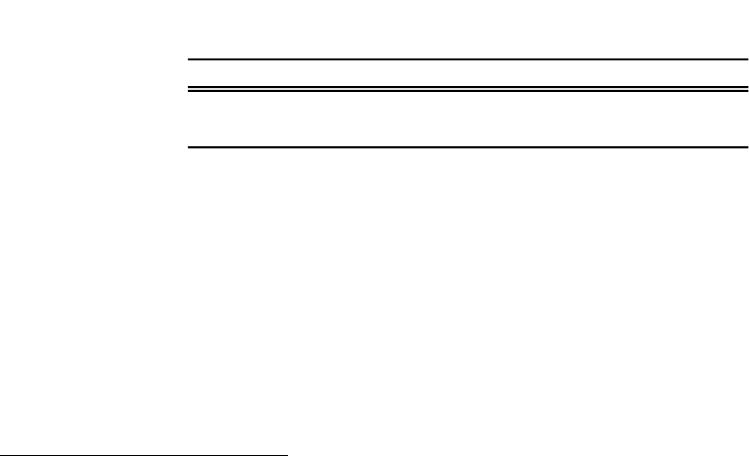

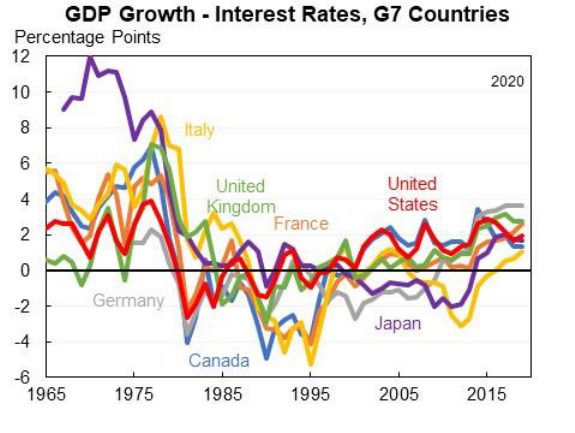

As striking as any development in the global economy over the last generation is the

large and sustained fall in real global interest rates. As Figure 1 illustrates it has been a feature of

all the G7 economies and more broadly has been universal in the industrial world. A clear

downward trend in longer term real rates antedates the 2008 financial crisis and has continued

since it was substantially resolved. The observations that the trend has been equally pronounced

in long- and short-term real rates, has lasted over 30 years and has coincided with constant or

slightly declining rather than increasing inflation and inflation expectations suggest that it is a

real rather than a monetary phenomenon.

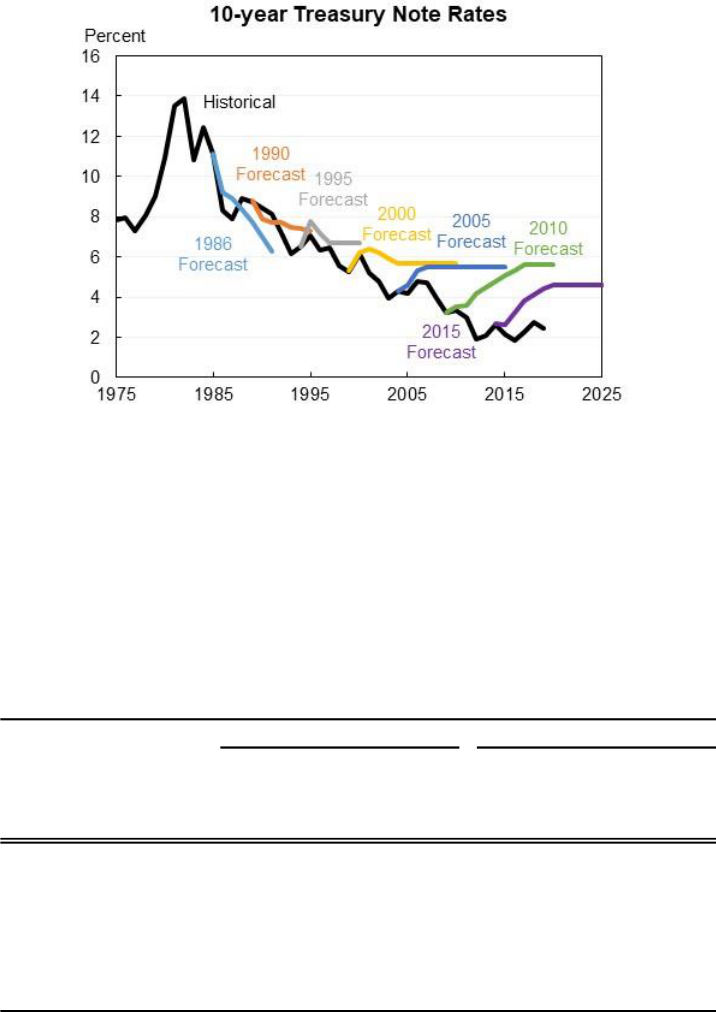

2

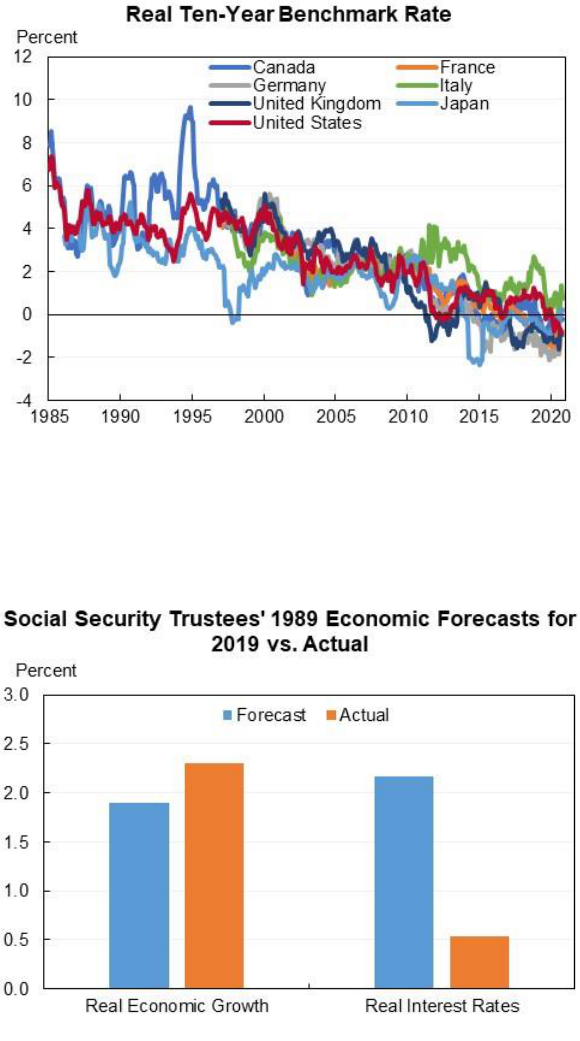

Figure 2 shows that while long-term forecasts largely

expected the slowdown in economic growth due to an aging population, they entirely missed the

large decline in real interest rates.

2

Real interest rates were also negative or low in the 1940s and 1950s (Council of Economic Advisers 2015). This

appears to have been primarily to do with a combination of financial repression, falling debt, high tax rates on

capital, and lack of robust social insurance contributing to high levels of saving.

5

Figure 1

Note: Inflation measured by one-year changes in the core consumer price index (core personal consumption expenditures for

United States).

Source: Bank of Canada; Statistics Canada; Eurostat; Japanese Statistics Bureau; U.S. Bureau of Economic Analysis;

Macrobond; authors’ calculations.

Figure 2

Note: Real interest rates are calculated from forecasted/actual nominal interest rates and forecasted/actual Consumer Price Index

inflation.

Source: The Board of Trustees, Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds (1989, 2020);

authors’ calculations.

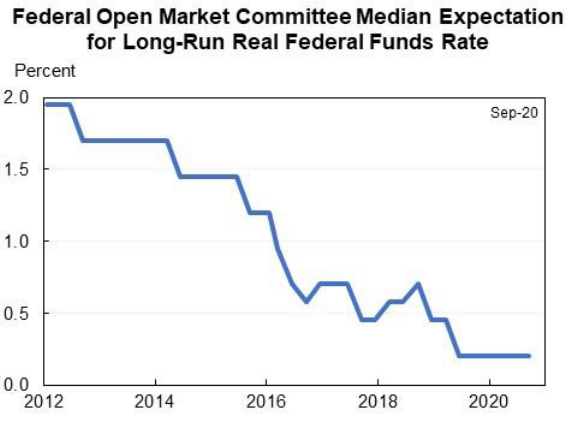

Estimates of the “neutral real interest rate” provided by the Federal Open Market

Committee (FOMC) and economists have also fallen to low levels. The FOMC projection of the

6

neutral real rate derived as the difference between its long-run federal funds rate and inflation

projection is now at an all-time low of 0.2 percent down from 1.95 percent eight years ago as

shown in Figure 3. Aronovich and Meldrum (2020) provide new estimates and a summary of the

findings of existing macro models suggesting a downward trend and a real rate very close to

zero. These estimates all significantly exceed what is priced into markets. As this is written 10

year forward federal funds are priced at 1.4 percent and ten year forward inflation is priced at

2.2 implying a real federal funds rate of -0.9 a decade from now.

Figure 3

Note: Expected long-run real federal funds rate calculated by subtracting long-run expected PCE inflation, adjusted for the

historical divergence from CPI inflation, from the long-run expected federal funds rate.

Source: Federal Reserve Bank of St. Louis; Bureau of Labor Statistics; Bureau of Economic Analysis; Macrobond; authors’

calculations.

Longer-term real interest rates are expected to remain negative. The five-year forward

five-year real indexed bond rate is currently -0.5 percent and the ten-year forward expectation of

the ten-year real interest rate is -0.1 percent. These estimates are more likely to be over- than

underestimates of prospective real short-term rates since they make no allowance for term or

liquidity premiums normally present in these markets. In a mechanical sense, increases in

inflation expectations towards currently targeted levels would reduce real rates unless the Federal

Reserve took offsetting actions. Convergence with other industrial countries would also reduce

U.S. real rates.

7

The decline in interest rates has happened even as public debt levels have risen. In the

United States the real interest rate on ten-year debt was 4.3 percent as measured by the yield on

10-year Treasury Inflation-Protected Securities (TIPS) in January 2000, a time when it was

widely expected that the entire federal debt would be largely paid off over the following decade

as shown in Table 1 above. In February 2020 the economy was in a similar cyclical position but

the debt was on course to rise to more than 100 percent of GDP over the following decade (the

pre-pandemic projection) and at the same time the 10-year TIPS rate had fallen to -0.1 percent.

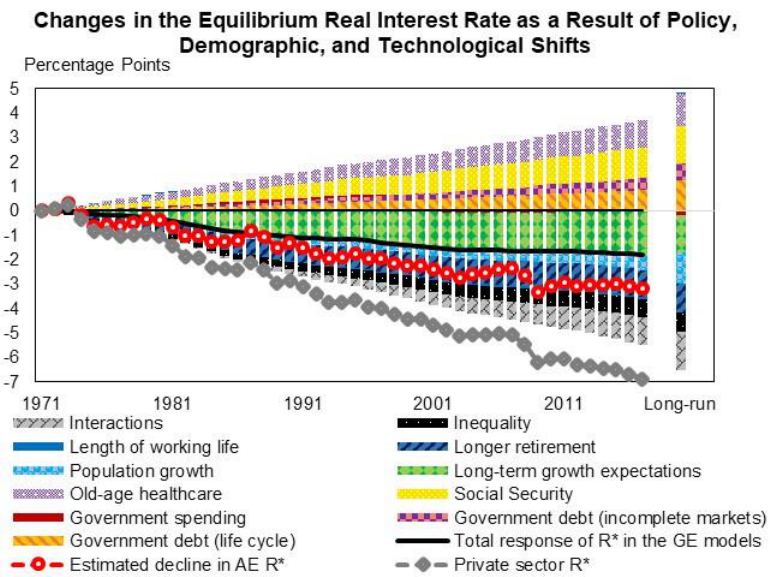

Any discussion of the causes of the decline in real interest rates has to begin with

the observation that the most obvious factors bearing on real rates—government fiscal positions,

social insurance expansions and changes in the after-tax profitability of capital—have all

operated to increase rates. They imply that ceteris paribus neutral real rates in the industrial

world would have declined by about 700 basis points (Rachel and Summers 2019). This suggests

substantial changes in the structure of the private economy. Rachel and Summers (2019) suggest

a tentative decomposition of some of these factors as shown in Figure 4.

Figure 4

Source: Rachel and Summers (2019).

8

At this point we find explanations based on the financial crisis, monetary policy choices

or global factors to be implausible accounts of more than a small part of the decline in real rates.

Declines in real rates predate the financial crisis, continued after financial conditions had

normalized, and are equally pronounced in countries like Canada where the financial crisis was

much less severe and financial institutions remained healthy.

In general, economists doubt the ability of monetary policy to affect real rates over long

horizons. Abnormally easy monetary policies would be expected to manifest themselves in

unusually rapid growth in nominal GDP whereas actual growth has consistently fallen short of

expectations. There is no tendency for declines in real rates to be greater at the short end than at

the long end of the yield curve as one might expect if monetary policy was a primary driver.

Rachel and Summers (2019) consider global factors. There have only been very small

fluctuations in the current account of the industrial countries taken as a group. While the United

States was running a substantial current account deficit in 2005 when Ben Bernanke (2005)

famously invoked a “savings glut” to explain declining U.S. real rates, that deficit roughly

halved over the subsequent decade even as real rates continued to decline.

The evidence is most consistent with structural changes in propensities to save and invest

as the dominant reason for declining real rates. As Summers (2014) argued, factors operating to

raise private saving include longer retirement periods, increased inequality, and rising

uncertainty. Factors operating to reduce private investment include slowing labor force growth,

greater efficiency in the use of capital, for example through companies like Uber and Airbnb, the

impact of information technology in reducing the need for large capital investments, as for

example law firms need much less office space per lawyer, and dramatic reductions in the

relative price of capital goods. Increases in corporate market power and increased pressure on

corporations to pay out cash to shareholders may also contributed to reduced investment.

An alternative line of explanation for low and declining real rates focuses on changes in

risk premiums as relative asset supplies change as argued, for example, by Caballero, Farhi and

Gourinchas (2017). Rachel and Summers (2019) question the importance of this line of thought

noting that required returns on assets aside from government debt like risky debt, real estate and

stocks have moved largely in tandem with debt yields. They note other difficulties with the safe

asset theory including the emergence of negative swap spreads and growing supplies of

government debt in recent years. Another view is that low rates reflect a shift in the risk profile

9

of government debt from providing a source of risk to acting as a hedge (Campbell, Sunderam,

and Viceira 2017), although rates have fallen as much at the short end (which has a beta of zero)

as at the long end so this explanations is unlikely to be an important part of the story.

Ultimately, however, the exact reason for low interest rates makes little difference for the

analysis of fiscal policy except to the degree the explanations bear on the persistence of the

trend. Whatever the cause of low interest rates, their relevant consequence is to limit the ability

of monetary policy to stimulate demand and reduce the cost of borrowing.

The decline in interest rates has three important implications: (i) as monetary policy is

limited in its ability to stabilize the economy and financial system, fiscal policy must play a

critical role; (ii) fiscal sustainability cannot be assessed by traditional debt-to-GDP ratios but

should instead be understood with measures like nominal or real interest as a share of GDP; and

(iii) many public investments pay for themselves, or come close to paying for themselves, and

the risk of not undertaking these investments is larger than the risk of doing too little deficit

reduction. The remainder of this paper discusses these three implications in turn.

Implication 1: Active Use of Fiscal Policy is Essential in Order to Maximize Employment

and Maintain Financial Stability in the Current Low Interest Rate World

Traditional thinking for the last half century has held that monetary policy should take

primary responsibility for stabilizing aggregate demand and ensuring low inflation. This is the

essential economic theory behind the widely implemented idea of independent central banks with

targets. Fiscal policy is seen as operating through automatic stabilizers and through discretionary

stimulus packages at moments of major distress. Fiscal policy is seen largely through the prism

of microeconomic efficiency, fairness and equality, and the desire to promote investment by

avoiding crowding out.

This thinking is no longer appropriate if monetary policy cannot be relied on to stabilize

the economy or to ensure that inflation targets are achieved. We believe that this will be the case

for as long as interest rates remain anywhere near current and prospective levels. Moreover, there

is a real risk that contractionary fiscal policies will jeopardize financial stability by forcing

decreases in interest rates that may encourage excessive leverage and asset price bubbles.

10

The challenges associated with low interest rates

The clearest challenge associated with lower equilibrium interest rates is constraints on

monetary policy. In 2000 David Reifschneider and John Williams published a paper predicting

that the federal funds rate would be at the zero lower bound 5 percent of the time. Since the

publication of the paper it has been at the zero lower bound 38 percent of the time. And it has

been at the bound 59 percent of the time since the onset of the financial crisis. As we write,

option markets suggest that five years out there is a 72 percent chance that nominal rates will be

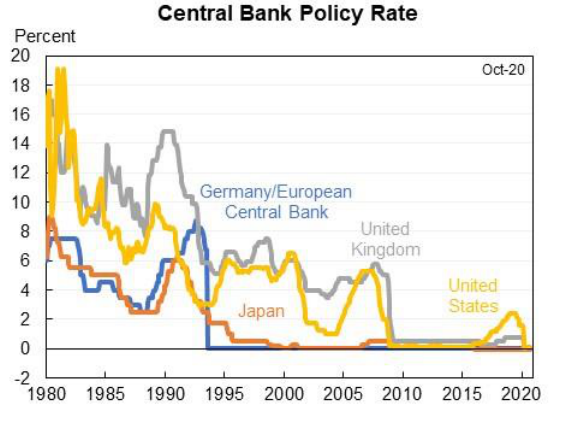

at their current level of effectively zero or even negative. As shown in Figure 5, interest rates in

other major economies, most notably Japan, have also been at an effective lower bound (often

negative) for much of the time in recent decades.

Figure 5

Source: European Central Bank; Bank of Japan; Bank of England; Federal Reserve; Macrobond; authors’ calculations.

In the United States, the average policy interest rate reduction in the nine recessions

before the pandemic was 630 basis points. Even if the long-run nominal federal funds rate

reaches the FOMC’s expectation of 2.5 percent, something the market doubts, that would leave

less than half as much room to respond to future recessions as past recessions with only a little

additional room if rates are allowed to go negative. The European Central Bank and Bank of

Japan may have even less room to respond to future recessions, and in fact neither of them was

able to cut rates in response to the current recession because they were already at the effective

lower bound. While rate reductions can be augmented by measures like quantitative easing and

11

forward guidance or even yield curve control, the only effect of such measures is to reduce term

premiums. Given their current low level this is unlikely to add much to the efficacy of monetary

policy. How much investment would be done at a zero percent ten-year Treasury rate that would

not be done at a one percent ten-year Treasury rate?

The consequence, if not compensated for by more active fiscal policy, would be longer

and more severe recessions. Moreover, it is at least plausible that recessions have hysteresis

effects and reduce subsequent potential output through effects on both labor force scarring and

subsequent productivity (e.g., Adler et al. 2017; Oreopoulos, von Watcher, and Heisz 2012;

Yagan 2019; DeLong and Summers 1988).

The importance of setting fiscal policy on the basis of the need to maintain aggregate

demand is highlighted by a counterfactual calculation. While there was much controversy over

the content of the 2010 National Commission on Fiscal Responsibility and Reform’s (commonly

known as the Bowles-Simpson commission) recommendations for moving towards budget

balance, there was, at the time, little debate over the merits of their objective. The Bowles-

Simpson plan would overtime have represented about a 4 percent of GDP annual shift towards

austerity by the end of the decade. Given that for much of the period unemployment was above

its sustainable non-accelerating inflation rate of unemployment (NAIRU) level, this would have

adversely impacted aggregate demand. For 5 years during this decade the federal funds rate was

at its lower bound and at no point did it exceed 2.5 percent. It is therefore not remotely plausible

that a lower rate path could have offset more than a small fraction of the reduction in aggregate

demand the fiscal contraction would have produced. The result likely would have been even

more economic slack and inflation further below target.

This is of course a hypothetical calculation. Had a major recession ensued, fiscal policy

responses would surely have been implemented. The point is that with our current economic

environment, fiscal policies need to be set with a view to maintaining full employment.

A second, related, challenge is financial stability. Lower interest rates lead to a shift to

riskier assets, higher leverage, and the possibility of bubbles as investors reach for yield, and

reduce the capital of banks, which have been unable to reduce deposit rates as much as lending

rates (e.g. Borio, Gambacorta, and Hoffman 2015; Dell’Ariccia, Laeven and Suarez 2017). This

may be exacerbated by central bank asset purchases which have increasingly become a tool to

provide additional support for the economy at the effective lower bound (Bernanke 2020).

12

Finally, in addition to complicating countercyclical policy in recessions it is possible that

there is also a chronic lack of demand that makes it impossible for the economy to grow

normally even outside of recessions. The experience of the United States in 2018-19 is

instructive in this regard. These were the ninth and tenth years of an economic expansion with a

record number of months of consecutive job growth and a relatively low unemployment rate.

Nevertheless, the stance of macroeconomic policy in these two years was what one would

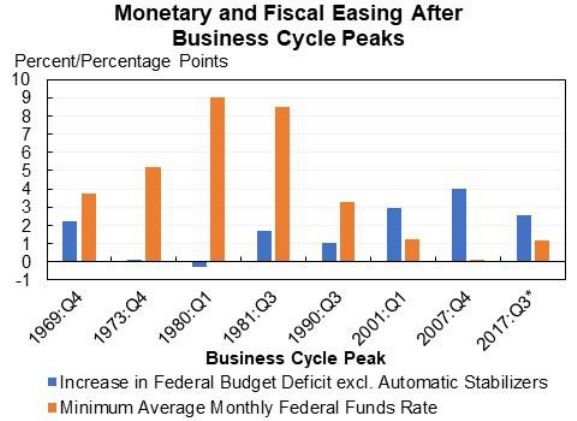

associate with a moderate to severe recession as shown in Figure 6. The fiscal stimulus was

larger than that of most recessions since the 1960s and interest rates were cut to levels that were

also more accommodative than in most previous recessions. This public support, not private

demand, helped the economy to grow at a 2.6 percent annual rate. Moreover, even with this

extraordinary monetary and fiscal stimulus the inflation rate still remained below the Federal

Reserve’s 2 percent target over this period.

Figure 6

Note: Increase in budget deficit is measured 8 quarters from peak; federal funds rate is minimum from peak through 24 months

after peak.

Source: Congressional Budget Office (2020c); Federal Reserve; Macrobond; authors’ calculations.

Lower equilibrium interest rates make it clear that economies will be in liquidity traps,

where the interest rate needed to equilibrate saving and investment is an unattainable negative

rate, much more often in future recessions. The experience of 2018-19 raises the prospect that

the liquidity trap may not just be confined to downturns but that secular stagnation may be a

13

chronic problem of the demand for loanable funds falling short of the supply of funds at any

nominal interest rate above zero even in normal times.

Central bank policy interest rates are at or near zero in all of the major advanced

economies leaving little if any additional scope for monetary policy to support additional

demand and speed the closing of output gaps.

Low interest rates mean that countries cannot afford not to undertake fiscal expansions

The main concerns about fiscal expansion in economic downturns is that they will lead to

unsustainable debt and may not be affordable in countries that currently have high debt levels.

This concern is misplaced. At a minimum, countries can always come back later to raise

revenues or reduce spending in order to get debt trajectories back on a desired course. More

importantly, this may not even be needed as fiscal support may help fiscal sustainability by

increasing output more than it raises debt, thus reducing the debt-to-GDP ratio.

3

A range of academic research and modelling by organizations such as the IMF and

Organisation for Economic Co-operation and Development (OECD) in recent years has found

that fiscal expansions in depressed economies can reduce the debt-to-GDP ratio. DeLong and

Summers (2012) found that even a small amount of hysteresis would result in a fiscal expansion

increasing GDP by more than it increases debt, resulting in a reduction in the debt-to-GDP ratio.

This view is supported by the empirical evidence in Auerbach and Gorodnichenko (2017), who

use a variety of specifications of fiscal shocks in a panel data set of advanced economies and find

that “a fiscal stimulus in a weak economy may help improve fiscal sustainability along the

metrics we study,” namely debt-to-GDP ratios and credit default swap spreads.

Most of the major macroeconomic models also have the property that fiscal expansions in

depressed economies at the zero lower bound can improve fiscal sustainability. The OECD

(2016) showed that public investment reduced the debt-to-GDP ratio in most of the advanced

economies in both its National Institute’s Global Econometric Model (NiGEM) and Fiscal

Maquette (FM) models. The IMF found similar results in modelling of demand-side policies

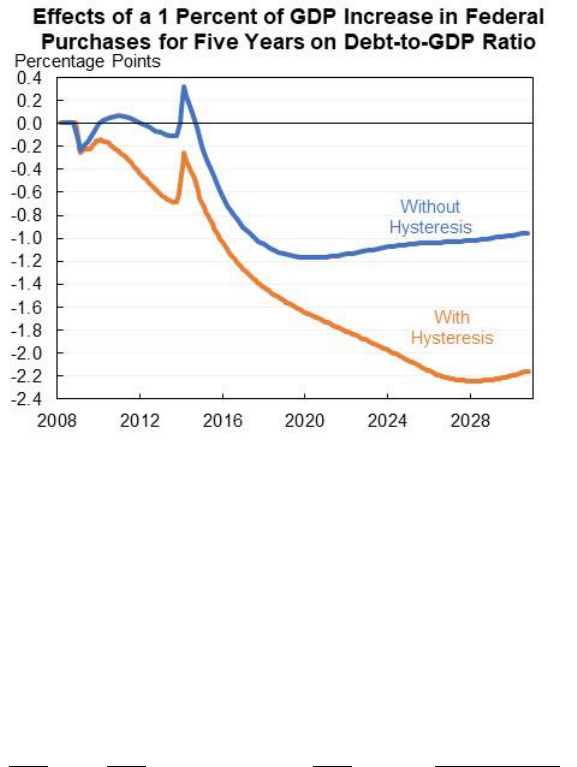

(Gaspar, Obstfeld and Sahay 2016). Ball, Delong and Summers (2017) report a run of the

Federal Reserve staff’s FRB-US model which shows that a 1 percentage point increase in fiscal

3

In the next section we will talk about the limitations of debt-to-GDP as a metric. We use that metric here because it

was the basis of the research we are citing.

14

stimulus reduces the debt-to-GDP ratio by 2.2 percentage points after 20 years, as shown in

Figure 7.

Figure 7

Source: Reifschneider and Summers as reported in Ball, DeLong, and Summers (2017)

Auerbach and Gorodnichenko find their result still holds at high debt levels, a finding

that is echoed in the OECD modelling which does not evidence any relationship between the

level of debt and whether fiscal policy pays for itself. In general, the higher a country’s debt the

more the growth rate-interest rate differential matters for its fiscal trajectory and the less that the

cost of stimulus itself matters for debt dynamics, as shown in the standard debt dynamics

equation:

≈

where r is the real interest rate, g is the real growth rate of GDP, and the primary deficit is the

difference between non-interest spending and revenues. To the degree that it can raise growth

rates relative to interest rates, then fiscal stimulus will have even larger favorable effects on debt

dynamics in a high debt economy than a low debt economy.

The case for a fiscal expansion in a depressed economy at the effective lower bound does

not rest on nor require that fiscal expansions reduce the debt-to-GDP ratio. Fiscal expansions

could easily pass a cost-benefit test even without these effects, but to the degree to which the

dynamic cost is smaller than the static cost, or even negative, the net benefit will be even larger.

15

The importance of automatic recession insurance

The increasingly limited effects of monetary policy call not just for discretionary

responses in situations like the current moment but also for improvements in the automatic

stabilizers, especially in countries like the United States that have weak automatic stabilizers.

Automatic stabilizers are spending increases or tax cuts that happen automatically when the

economy weakens. For example, when more people lose jobs labor tax payments go down and

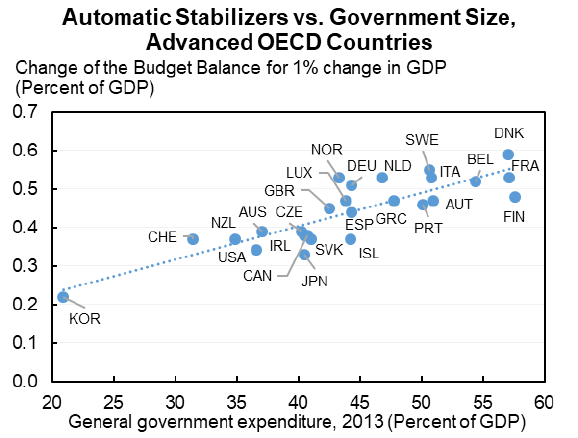

unemployment insurance benefits go up. The magnitude of automatic stabilizers is generally

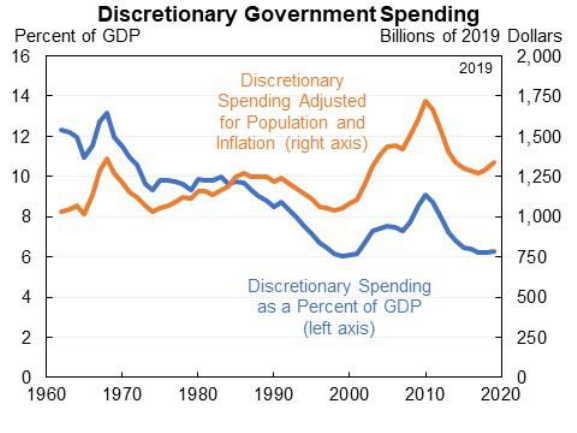

related to the size of government, as shown in Figure 8. Some European countries with larger

stabilizers have, however, undone them with discretionary fiscal contractions in past periods of

economic weakness.

Figure 8

Note: Dotted line is linear trend.

Source: International Monetary Fund (2015).

One way to make automatic stabilizers larger would be to increase both revenues and

expand benefits. An alternative approach is to build in specific macroeconomic contingencies

that trigger additional assistance when, for example, the unemployment rate rises above a certain

level (Boushey, Nunn, and Shambaugh 2019). This automatic recession insurance could include

national transfers to subnational units that have a harder time borrowing in downturns, increased

unemployment insurance benefits, or other transfers like nutritional assistance or even across-

the-board cash transfers.

16

There are four arguments for establishing more automatic contingent policies. First, they

can lessen downturns and speed economic recoveries by overcoming the political limitations of

discretionary fiscal policy which often gets slowed down by recognition lags, political debates,

and may end prematurely as the political system tires of change. Second, automatic contingent

policies can be more regionally differentiated, for example they can be based on state-level or

other subnational economic measures so as to provide the greatest assistance where it is most

needed, including in response to regional recessions. Third, they often make microeconomic

sense. For example, the optimal level of unemployment insurance depends on the unemployment

rate because when the unemployment rate rises moral hazard concerns about discouraging job

seeking diminish and the importance of consumption smoothing rises (Baily 1978 and Chetty

2008). Finally, they may advance additional priorities; for example, providing assistance to states

and localities can help prevent damaging cuts to education (Fiedler, Furman, and Powell 2019).

Aggregate demand can be further increased in a budget neutral manner

Given that interest rates are at essentially lower-bound levels around the world even in

the presence of substantial deficits, the case that maintaining full employment requires more than

monetary policy is compelling. The obvious concern is that expansionary fiscal policy may not

be sustainable if it leads to excessive debt accumulation. We have already noted that

expansionary fiscal policy may actually reduce levels of debt relative to GDP by stimulating

growth and increasing revenue collections. There is a further crucial point as well—it is possible

for fiscal policy to stimulate demand without increasing the deficit or the level of government

indebtedness.

First, fiscal policy can take advantage of the balanced budget multiplier whereby

spending has (over time) a higher multiplier than taxes (Haavelmo 1945) because increases in

spending increase demand dollar for dollar whereas, particularly in the case of very progressive

tax increases, taxes are paid out of funds that otherwise would have been saved. A reasonable

estimate is that the spending financed by taxes on high-income households is at least half as

potent in stimulating the economy as spending financed by borrowing

Second, fiscal policy can shift in a more progressive direction. One of the causes of lower

interest rates has been the increase in inequality which has resulted in larger incomes for higher-

income households who are the most likely to save it. Offsetting the increase in inequality would

17

reduce net national saving for any given interest rate, something that has often been viewed as a

minus for economic growth but in the current circumstances would be welcome (e.g., Koo and

Song 2016). Note that in general a larger government generally is a more progressive one so the

first and second recommendations are related.

Finally, public support for retirement, health care, college and other large, lumpy and

sometimes uncertain needs reduce the need for lifecycle and precautionary saving, thus boosting

consumption demand. When Keynes visited the United States during World War II, he

highlighted maintaining demand as an important virtue of the then recently adopted Social

Security system. In all cases the expanded public support could be paid for on a pay-as-you-go

basis so that they need not change the short- or long-run deficit.

Implication 2: Lower Interest Rates Necessitate New Measures of a Country’s Fiscal

Situation

The debt-to-GDP ratio is the most common measure of a country’s fiscal situation used

by policy makers and is enshrined in rules that govern fiscal policy. Recently some have been

alarmed as the debt-to-GDP ratio has risen across the world and now stands at more than 100

percent in the majority of G7 economies, as shown in Table 2.

Table 2

Note: In international comparisons, U.S. values are for general government, not federal government.

Source: International Monetary Fund; Macrobond.

Canada 46

France 110

Germany 54

Italy 149

Japan 177

United Kingdom 98

United States 107

Memo: G7 Countries 110

General Government Net Debt as

a Percentage of GDP, 2020

18

Debt levels have been a leading metric for public policy but the decline in interest rates

shows how problematic this measure is. For example, in 1992 the Maastricht Treaty set a limit of

60 percent debt-to-GDP ratio for countries in the euro zone. At the time, ten-year German bonds

had a nominal interest rate of 7.8 percent or a real interest rate of about 5 percent. In 2019 the

nominal interest rate on ten-year German bonds had fallen to -0.2 percent or a real interest rate of

about -2 percent. At interest rates prevailing in 1992, a country with a 60 percent debt-to-GDP

ratio paid about 5 percent of GDP in interest. Today, Japan with a 177 percent debt-to-GDP ratio

is expected to pay 0.2 percent in interest and the United States with a 107 percent debt-to-GDP

ratio for general government is expected to pay 2.0 percent of GDP in interest, with the real

interest after accounting for inflation being negative or close to zero in both countries. If a 60

percent debt-to-GDP ratio made sense as a ceiling in 1992 it definitely no longer does. Instead a

much higher ceiling would be appropriate today. This is a vivid illustration of how the debt-to-

GDP metric is flawed and why it should be replaced with other measures of a country’s fiscal

position. Importantly, these other measures generally show that fiscal positions are better today

than they were a few decades ago as the favorable debt sustainability dynamic associated with

lower interest rates outweighs the increase in the debt itself.

Shifting from the debt-to-GDP metric is part of a broader reappraisal of the ways in

which the current debt and deficit situation is less of a concern in an economy in which growth

rates have often exceeded interest rates in the past and are likely to continue to exceed them for

sometime in the future (see, e.g., Elmendorf and Sheiner 2017, Blanchard 2019, Furman 2016,

DeLong and Summers 2012).

The debt-to-GDP metric has three shortcomings that make it a misleading metric of a

country’s fiscal position:

1. It ignores the fact that debt can be repaid over time. Debt is a stock (an amount estimated

at a point in time that does not need to be repaid immediately) while GDP is a flow

(measured over a discrete period of time). A stock-stock perspective on the debt

compares the debt to the present value of GDP over the indefinite future. With lower

interest rates, the present value of future GDP is higher and debt is correspondingly more

manageable over time.

19

2. It ignores interest rates. Relatedly, at lower real interest rates a given amount of debt is

less costly. The stock-stock perspective is based on a very speculative measure of the

present value of GDP over an infinite horizon, a metric that requires knowing growth and

interest rates for the indefinite future. In contrast a flow-flow perspective looks at how

much that debt costs today, in interest payments, as compared to income today, providing

a sense of how affordable that debt is.

3. It is a backward-looking concept. The public debt is effectively the sum of the unified

deficits that a country has run from its inception (with some adjustments for financial

transactions). It does not reflect scheduled future policies, like pensions, or likely future

policies, like the cost of responding to future emergencies. It also does not incorporate the

ability to respond to evolving debt concerns with future tax increases or spending cuts.

The next three subsections address these considerations in more detail including showing how

more coherent measures of the fiscal situation dramatically changes our understanding of fiscal

sustainability, making it clear that most major advanced economies are in better fiscal shape

today than they were twenty or thirty years ago when their debt levels were much lower.

The debt is less of a concern: a stock-stock perspective

While interest rates have come down dramatically, growth rates have fallen much less.

As a result, the difference between growth rates and interest rates has risen in all of the G7

economies over the last three decades and is a substantial positive number in all of them ranging

from 1.1 in Italy to 3.7 in Germany as shown in Figure 9. Growth rates exceeding interest rates is

the norm not the exception, occurring about two thirds of the time since 1871 in the United

States and for much of the time in other major economies as well (Blanchard 2019).

20

Figure 9

Note: GDP growth is average annual growth rate over prior 5 years. Interest rates are average of 10-year and 3-month

government bond yields.

Source: World Bank; Macrobond; Global Financial Database; authors’ calculations.

When growth rates exceed interest rates the present value of GDP is infinite. This means

that over time the economy will outgrow its debt and associated interest so that the debt will

disappear relative to the economy. From a stock-stock perspective, the debt stock is 0 percent of

the present value of GDP stock. This is a more favorable fiscal situation than most of the G7

economies appeared to enjoy in the early 1990s when interest rates were substantially above

growth rates so that the present value of GDP was finite and debt was a positive fraction of the

present value of GDP.

Interest rates could rise and growth rates could fall in which case the present value of

GDP could be finite. In the United States the only regular and systematic measure of GDP over

an infinite horizon we are aware of is produced by the Social Security Trustees. Any estimate of

this quantity is highly speculative and subject to massive uncertainty, and we have our quibbles

with some of their specific assumptions, but this measure provides a useful benchmark with

which to assess how the U.S. debt appeared at various points in time.

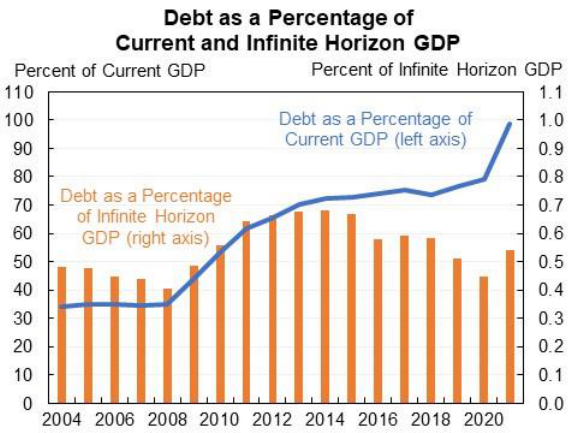

According to the latest Social Security Trustees Report (2020) the present value of GDP

over an infinite future was $3.8 quadrillion on January 1, 2020. As of November 19, 2020, the

U.S. federal debt held by the public was $21.2 trillion. Adjusting these to have the same dates,

debt is 0.5 percent of infinite horizon GDP. In other words, a 0.5 percentage point increase in

revenue as a share of GDP or reduction in spending as a share of GDP would be sufficient to pay

21

off the entire debt. This is smaller than or similar to what policymakers would have thought at

various times in the past as shown in Figure 10 even as the debt has nearly tripled as a share of

current GDP.

Figure 10

Note: 2021 value is based on debt as of November 19, 2020.

Source: The Board of Trustees, Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds; Federal Reserve

Bank of Philadelphia, Survey of Professional Forecasters; Department of the Treasury; Macrobond; authors’ calculations.

This intuition applies more broadly. For example, a decline in r – g from 1.0 to 0.5

doubles the present value of GDP—and so makes twice as much debt sustainable relative to the

future stock of GDP. This ½ percentage point decline in r – g is an order of magnitude smaller

than the actual 5 percentage point reduction in r – g in the median G7 economy since 1990.

The debt is less of a concern: a flow-flow perspective

The stock-stock perspective relies on a highly uncertain extrapolation of fiscal conditions

into the indefinite future. An alternative coherent metric avoids that problem by comparing the

flow of interest on the debt to the flow of annual GDP. The two measures are, of course, related

as lower interest rates raise the present value GDP and make it more possible to pay the debt off

over time.

The more analytically relevant measure is real interest payments as a share of GDP. Real

interest rates adjust for inflation by comparing the real interest rate paid on the debt to the size of

GDP. Equivalently, it can be understood as nominal interest payments as a share of GDP minus

22

the amount that the debt is inflated away each year as a share of GDP. Specifically, the formula

is:

.

In implementing this concept we smooth inflation by averaging it over five years, which comes

closer to the concept of expected inflation which is relevant for real interest rates. As one would

expect, real interest as a share of GDP falls when, all else equal, nominal interest rates fall,

inflation rises, nominal GDP rises, or when the debt rises. This last effect is because the larger

the debt-to-GDP ratio the more an economy benefits from the inflation that partly erodes the

debt.

Real interest payments as a share of GDP are more analytically relevant than the more

commonly used nominal interest payments as a share of GDP. For example, consider two

economies that both have debt-to-GDP ratios of 100 percent and nominal interest rates of 4

percent. Nominal interest costs as a share of GDP are thus 4 percent in each economy. Assume

now that the first economy has no inflation and the second economy has 4 percent inflation. For

simplicity assume there is no real growth in either economy. The no inflation economy has a real

interest to GDP ratio of 4 percent, the amount it needs to raise revenues or reduce non-interest

spending in order to stabilize the debt-to-GDP ratio. In contrast, the second economy has a real

interest to GDP ratio of 0 percent so it need not raise taxes or cut non-interest spending to offset

the cost of its debt. That is because the second economy is able to deflate away the debt by an

amount equal to its nominal interest payments.

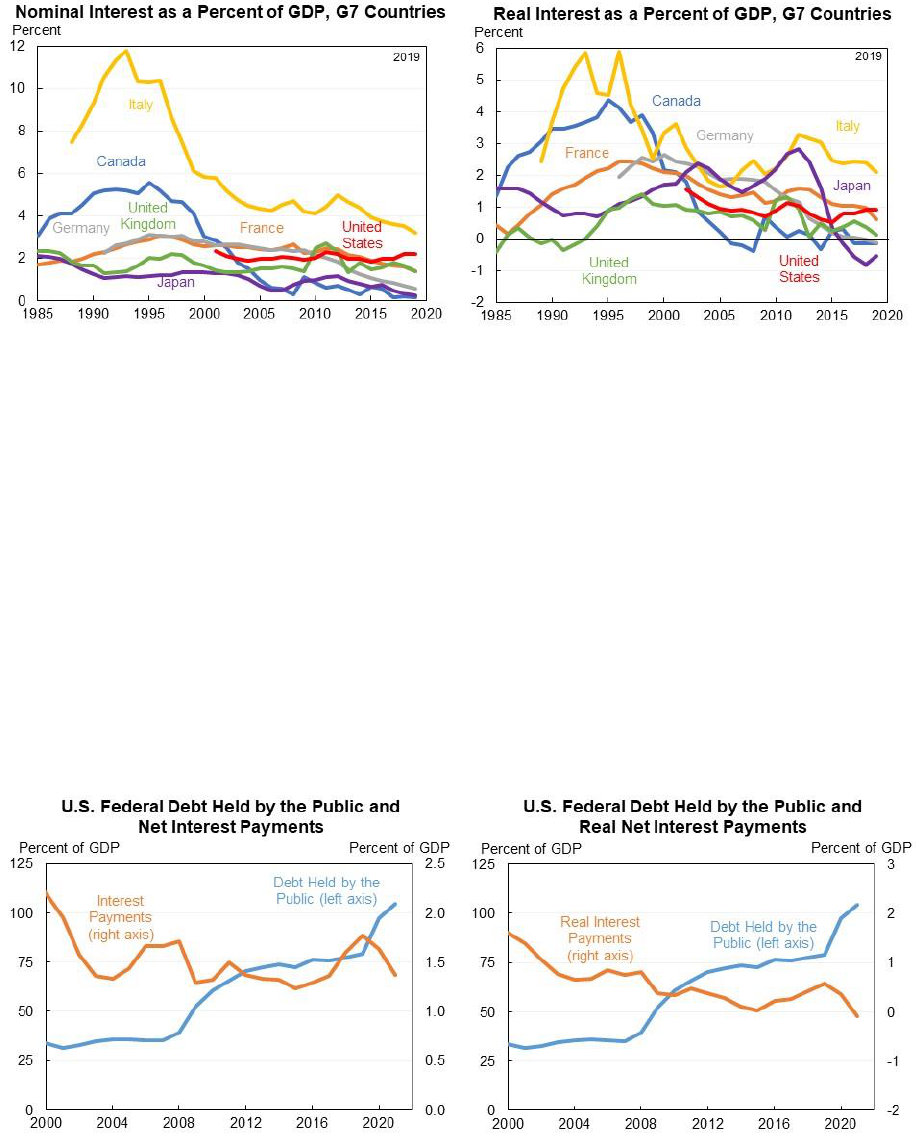

Both nominal interest payments and real interest payments have fallen as a share of GDP

across the G7 economies and are generally lower today than they have been in decades as shown

in Figures 11a and 11b.

4

4

These figures show general government net interest payments, which in the United States includes payments by

federal, state, and local governments.

23

Figure 11a Figure 11b

Note: General government, including for United States.

Source: International Monetary Fund, Macrobond; authors’ calculations.

The U.S. experience over the last twenty years provides a vivid example of how different

the analytically meaningful flow-flow perspective is from the misleading stock-flow perspective

conveyed by debt-to-GDP ratios. In 2000 U.S. Federal debt was 34 percent of GDP, not far from

its post-war low. Since then the debt-to-GDP ratio rose almost monotonically, nearly tripling to

over 100 percent of GDP. At the same time both nominal and real interest rates have fallen so

that both nominal and real interest as a share of GDP have fallen nearly monotonically and are

now towards the low end of the range as shown in Figure 12a and 12b.

Figure 12a Figure 12b

Note: 2021 values are projections.

Source: Office of Management and Budget; Congressional Budget Office; Macrobond; authors’ calculations.

24

BOX I – Adjusting debt and interest payments to reflect the Federal government’s

complete balance sheet

The federal U.S. debt and net interest data used in this paper has followed U.S.

scorekeeping conventions which are at variance with the economically relevant concepts. In

addition to liabilities the Federal government also has financial assets, the largest of which is

direct student loans and the second largest of which is cash at the Treasury. The relevant concept

of debt for both fiscal sustainability and assessing macroeconomic effects is the debt held by the

public net of financial assets. As the CBO (2020d) explains, “Debt net of financial assets also

provides a more comprehensive picture of the government’s overall effect on credit markets than

does debt held by the public. When the government borrows to make loans that will be repaid in

the future, the overall supply of credit is essentially unchanged. Therefore, the issuance of that

debt does not crowd out, or take the place of, debt issued in the private sector to the same degree

that debt issued for other purposes does.” For example, when the Federal government shifted

from guaranteeing private student loans to making direct loans itself its financial position and

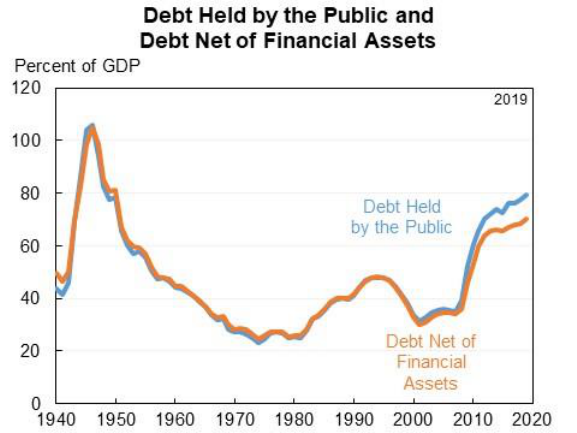

risks were essentially unchanged but the debt held by the public rose. Figure I.1 shows the

divergence between debt held by the public and debt net of financial assets which has grown

over time and is now about 9 percentage points.

Figure I.1

Source: Office of Management and Budget; Richard Kogan’s calculations.

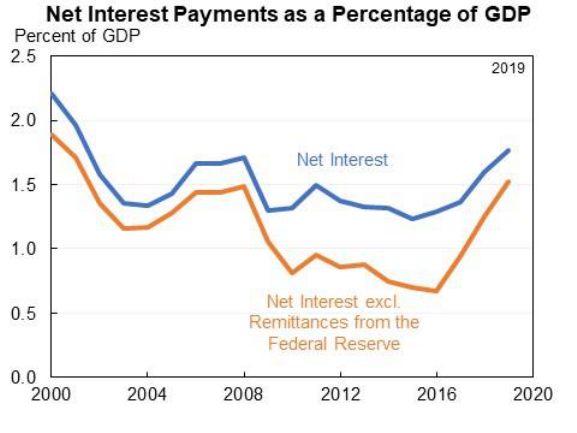

The Federal budget defines “net interest” largely as the interest paid on Treasury bonds

with adjustments for other interest paid and received by other Federal agencies (for example, the

equity earnings of the National Railroad Retirement Investment trust partly offset net interest).

The data do not count the Federal Reserve as part of the Federal government even though it is

clearly a Federal agency and the Treasury’s and Federal Reserve’s balance sheets should be

thought of on a consolidated basis for thinking about fiscal sustainability and the macroeconomy.

Put another way, fiscal analysis should essentially not count the Treasury debt held by the

Federal Reserve but should add the Federal Reserve’s reserves because these are effectively

interest-bearing short-term debt. In 2019 the Federal Reserve earned interest of $103 billion

largely on its Treasury and mortgage securities while paying $41 billion in interest mostly on

25

reserves. This $62 billion interest spread reflected the higher interest rates it received on its

longer-term assets than it paid on its shorter-term debt and $55 billion of this spread was remitted

to the Treasury. Thus, the Federal government’s consolidated net interest should subtract out

remittances to the Federal Reserve which are currently inaccurately classified as a receipt (or

revenue item) not as net interest. Figure I.2 shows the gap between net interest and net interest

minus Federal Reserve remittances over the recent past. The gap between these two is likely to

grow substantially over the next several years as the Federal Reserve has expanded its balance

sheet but the latest CBO projections expect it to come back down to 0.2 percent of GDP in 2030

(CBO 2020a).

Figure I.2

Source: Office of Management and Budget; authors’ calculations.

END BOX-------------------------------------------------------------------------------------------------------

Looking forward: the debt is not “spiraling” over the next decade and interest payments are

modest

Debt relative to the present value of GDP and real interest payments relative to GDP are

both coherent and meaningful measures and both of them are superior to the largely incoherent

concept of debt relative to GDP. All three of these measures, however, suffer from the same

shortcoming: they do not reflect the future fiscal trajectory which may dwarf the cumulative

historical trajectory.

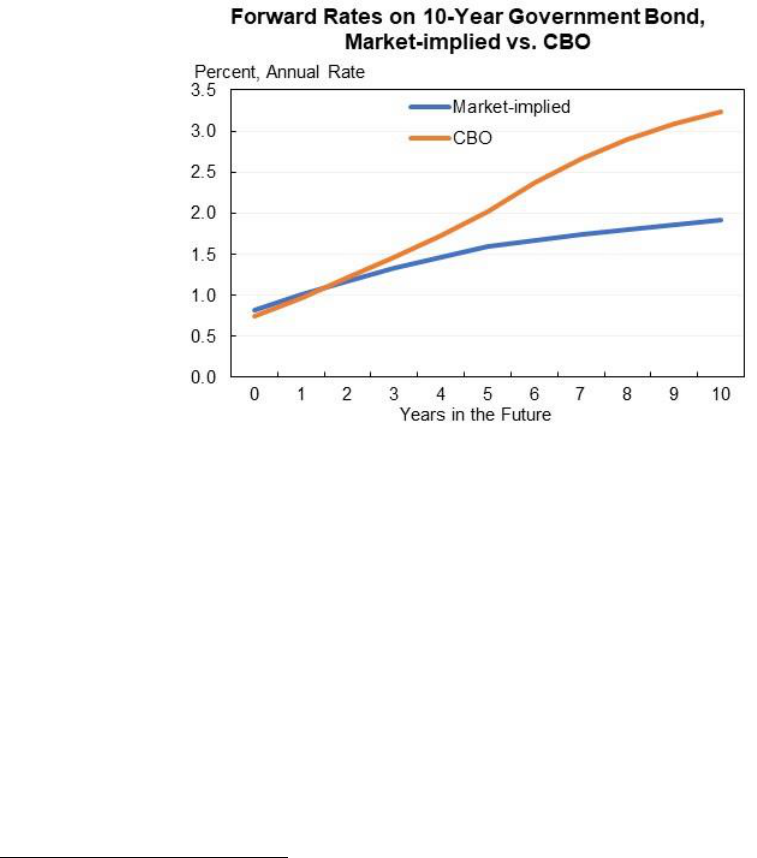

Looking forward it is plausible that interest rates will rise from their current

extraordinarily low levels, with the CBO forecasting a steeper increase in interest rates than

26

financial markets are expecting (Figure 13). CBO also projects spending on Social Security and

health programs to rise, with revenues as a share of GDP expected to rise as well.

Figure 13

Note: Market-implied rates as of November 27, 2020. CBO based on Q4 forecasts.

Source: Congressional Budget Office (2020b); Bloomberg.

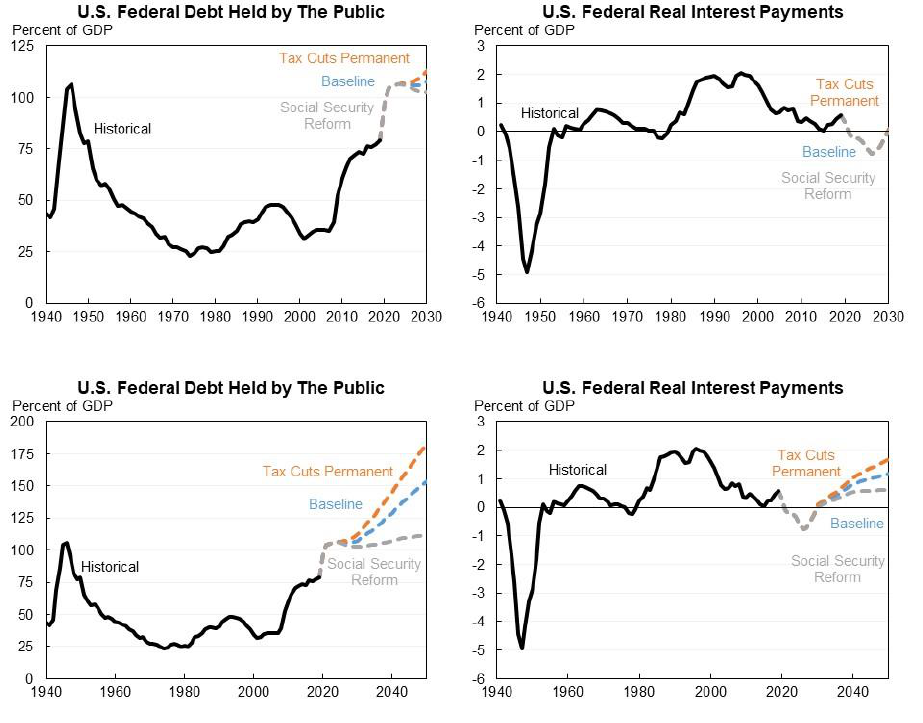

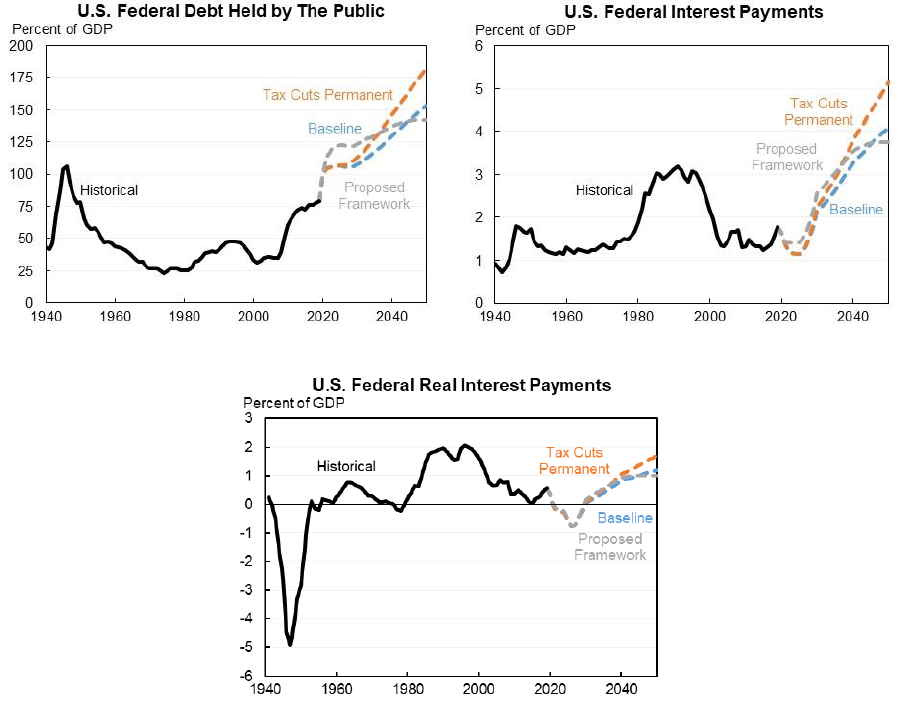

For the United States, the latest estimates show that the debt will rise but then level off at

a higher level (Figure 14a). Real interest payments will be low as a share of GDP but then

increase towards the end of the ten-year budget window (Figure 14b), but will still end up well

below their historical average. The estimates shown are for three scenarios: one based on the

latest CBO baseline which largely assumes current law continues, one that adds in the cost of

making the expiring provisions of the 2017 tax cuts permanent, and one that follows current law

in assuming Social Security is reformed (in the spirit of Blahous 2017 on the proper baseline).

5

5

Under current law Social Security and Medicare cannot pay full benefits after their trust funds are exhausted,

which are projected to be 2034 and 2026 respectively according to the Trustees (The Board of Trustees, Federal

Old-Age and Survivors Insurance and Federal Disability Insurance Trust Fund 2020; The Boards of Trustees,

Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds 2020) and 2031 and 2024

respectively according to CBO (2020f). Current law essentially requires Social Security reform to happen, as has

happened in the past when Social Security ran up against trust fund exhaustion, most recently in 1983. Instead of

abruptly cutting benefits when the trust fund is exhausted our current law baseline smooths the adjustment out over

time starting at 0.5 percent of GDP in 2025 and growing to 1.7 percent of GDP on and after 2035. This is equal to

the present value of the Social Security shortfall as estimated by the Social Security trustees. It is a conservative

reflection of current law because it does not include Medicare and because it is smaller than the adjustment CBO

projects under current law. Doing everything consistently on a CBO baseline would thus show that current law

would result in an even lower debt and interest rate path than we are showing here and throughout this paper.

27

Figures 14c and 14d show the same three scenarios over the next thirty years although, as

discussed in the next section, the uncertainty around forecasts that go out this far is so large they

should not have inordinate weight in policymaking today. See the Appendix for details on these

projections.

Figure 14a Figure 14b

Figure 14c Figure 14d

Social Security reform phased in linearly from 0.5% of GDP to 1.7% of GDP over 10 years beginning in 2025

Source: Office of Management and Budget; Congressional Budget Office; Macrobond; authors’ calculations.

These baseline predictions can serve a useful purpose in assessing the fiscal trajectory but

they also are limited in their ability to answer the question of whether the debt is sustainable by

their assumption of no change in law or policy. This is because they do not answer the question

of whether the fiscal situation could be made sustainable in the future. The United States collects

31 percent of GDP in general revenue, well below the OECD average of 37 percent of GDP or

the OECD maximum of 57 percent of GDP collected in Norway. The United States has often

28

collected revenue that was higher than what it collects today and similar revenue levels have

been proposed by, for example, the National Commission on Fiscal Responsibility (2010). In that

sense the U.S. fiscal situation is by definition sustainable—effectively it has an asset equal to at

least several percent of GDP that it could choose to collect if it needs to. Higher tax countries

have less room in this regard. France, for example, is closer to the top of its Laffer curve so

would have less space to close a fiscal hole with more revenue. Considerations of debt

sustainability need to take into account not just the amount of taxation under the law but the

capacity for taxation.

A bigger issue with forward-looking projections is the tremendous uncertainty they are

subject to, the topic of the next subsection.

The uncertainty in budget forecasts is enormous especially looking forward several decades

Forecasting deficits and debt is extremely difficult and forecasts have very large standard

errors that derive both from unexpected changes in economic variables like growth and interest

rates and also in “technical” factors like the cost of health care and the efficiency of tax

collections. The CBO does a very good job given all of the uncertainties. Its forecasts of deficits

and debt produced since 1984 have been mostly unbiased in the sense that their forecast errors

tend to even out without about half of their forecasts being too optimistic and about half of them

being too pessimistic after adjusting for legislative changes that they were not trying to forecast

(CBO 2019a). In contrast, CBO’s forecasts of net interest as a share of GDP have been

systematically biased toward being too high, in large part because CBO’s forecasts of interest

rates (like those of other forecasters) have consistently been too high, as shown in Figure 15.

29

Figure 15

Source: Congressional Budget Office.

CBO’s forecast errors have, however, been large in both directions and grow over time.

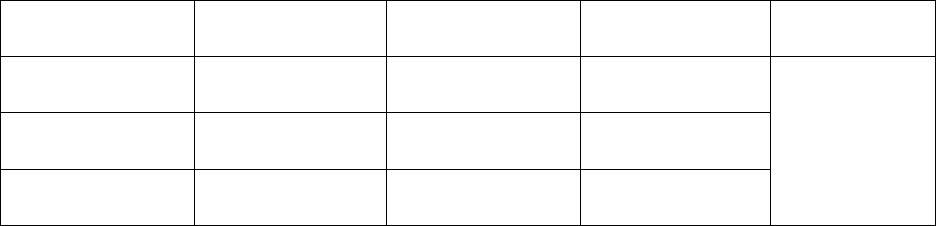

Table 3 shows their own estimates of a two-thirds error band around their forecasts for deficits

and debt along with our estimates, derived from their statistics, of a 90 percent error band.

Table 3

Source: Congressional Budget Office (2019a); authors’ calculations.

CBO does not assess its track record over a longer period, in part because of limitations

in the data that would be needed for such an assessment. Moreover, we have very few very long-

range fiscal forecasts but the ones we have are consistent with the view that the errors grow over

time. One of the earliest long-range forecasts was made by the Government Accountability

Two-thirds

Spread of

Errors

90 Percent

Confidence

Interval

Two-thirds

Spread of

Errors

90 Percent

Confidence

Interval

Year 1 (Current Year) 1.0 1.8 1.5 2.8

Year 2 (Budget Year) 2.1 4.3 3.3 7.8

Year 3 3.0 5.7 6.5 13.4

Year 4 4.0 6.6 8.5 18.2

Year 5 4.1 7.5 12.3 23.4

Year 6 3.8 8.3 17.2 29.2

Deficit

Debt

Measures of Historical Forecast Accuracy as a Percent of GDP

30

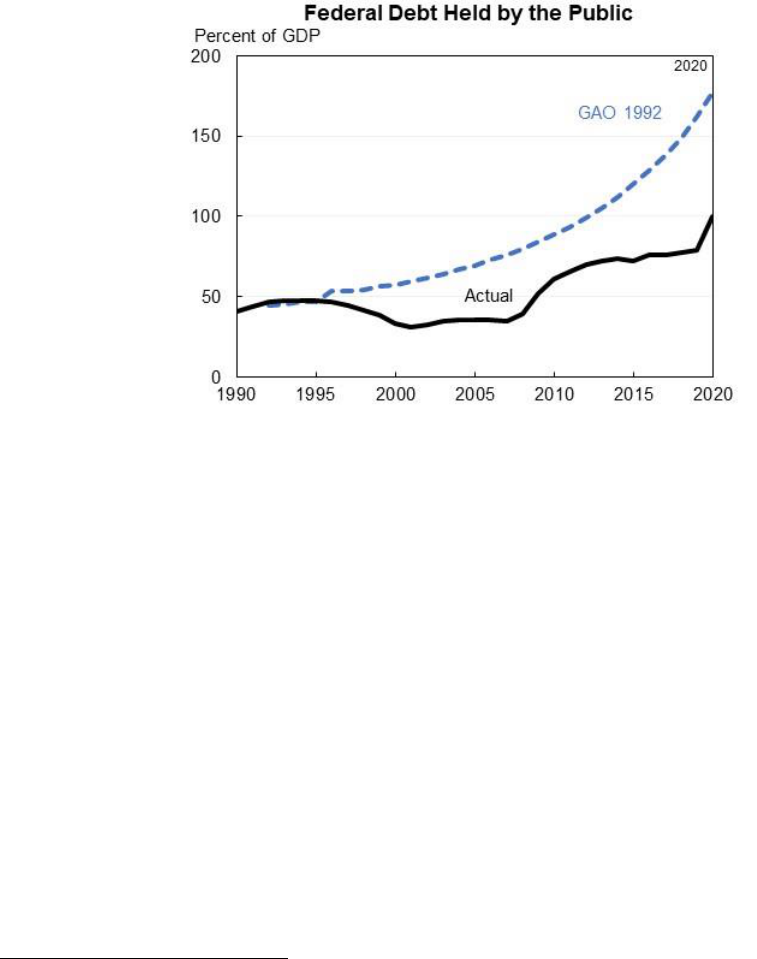

Office (GAO) in 1992 and it projected that the debt would reach 177 percent of GDP by the end

of fiscal year 2020, which is 77 percentage points above the actual debt-to-GDP ratio at the end

of that year as shown in Figure 16. Moreover, legislation adopted since 1992 likely was net debt

increasing so GAO’s economic and technical forecasting error was even larger than this estimate.

Figure 16

Note: GAO estimate converted from GNP to GDP and adjusted for revisions to GDP methodology since publication.

Source: Government Accountability Office (1992); Office of Management and Budget; Bureau of Economic Analysis;

Macrobond; authors’ calculations.

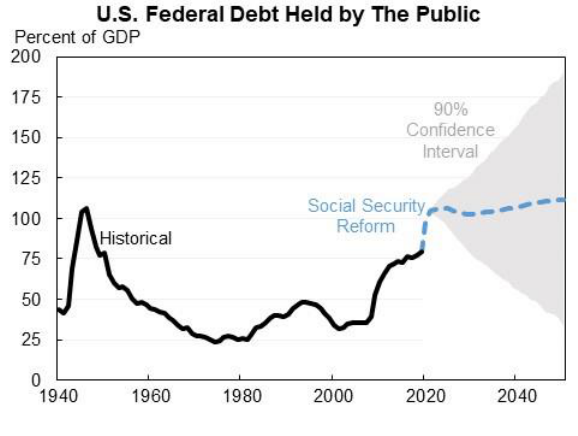

As a back-of-the-envelope way of assessing forecast errors we assume conservatively

that the standard deviation of debt forecast errors grows linearly with time, reflecting the

increased uncertainty as deficit forecast errors accumulate over time. As a result, the 30-year

forecast of the debt-to-GDP ratio would have error bands as shown in Figure 17.

6

In other words,

assuming the tax cuts expire and Social Security is reformed we would expect the debt-to-GDP

ratio to be 112 percent of GDP in 2050 with a two-thirds chance that it falls in the 66 to 157

percent range and a 90 percent chance it falls in the 33 to 190 percent range.

6

The 90 percent uncertainty band is the result of a Monte Carlo simulation of 10,000 draws. The simulation draws

from a distribution that assumes that there is no debt forecast error on average and that the standard deviation of the

debt forecast error for each year increases over time based on the linear relationship observed in CBO’s forecast

errors for years one through year six.

31

Figure 17

Note: Social Security reform phased in linearly from 0.5% of GDP to 1.7% of GDP over 10 years beginning in 2025

Source: Office of Management and Budget; Congressional Budget Office; Macrobond; authors’ calculations.

The impact of uncertainty on current policymaking depends on two factors. First, how

costly and irreversible are steps we take today? If it is costly to take steps today, for example

irreversibly reducing the educational opportunities of children, then in the face of uncertainty it

is better to delay action until more of the uncertainty has been resolved (Dixit and Pindyck

1994). Second, how costly is waiting to act? To the degree that one wants to act on the tax side

there is a cost associated with waiting in that it involves a larger tax increase and thus does not

efficiently smooth tax rates (Barro 1979), although in practice that cost is likely to be relatively

small, especially for countries that are far from the peak of their Laffer curves. To the degree one

wants to act on the spending side waiting may be more constraining as it is harder to give notice

that would allow people to adjust their plans, but even here there is little adjustment that people

understood or adjusted much in response to the decades of notice they got about the increase in

the Normal Age of Retirement for Social Security.

Overall, the conclusion we draw from the uncertainty on forecasts is that policymakers

should put relatively little weight on projections for ten years or more in the future and that large

changes should not be made well in advance based on highly uncertain and possibly inaccurate

forecasts, especially when it is very feasible to make adjustments later.

32

BOX II: The fiscal gap as an alternative measure of the fiscal situation-------------------------

The fiscal gap is an alternative measure of the fiscal situation that aims to address the

three shortcomings we have discussed: the stock-flow disconnect, falling interest rates and the

need to look forward. It was originally developed by Laurence Kotlikoff and Alan Auerbach and

is regularly updated by government institutions (e.g., CBO 2019b) and academics (e.g.,

Auerbach, Gale, and Krupkin 2019). The concept is the immediate and permanent change in the

primary balance—either through an immediate increase in taxes or an immediate reduction in

non-interest spending—that would be needed to stabilize the debt as a percentage of GDP at its

current value for a specific period of time. As such, the fiscal gap incorporates information not

just about the past debt but also about future primary deficits, GDP, and interest rates.

The fiscal gap is a more meaningful and useful concept than the debt-to-GDP ratio. It

does, however, suffer from three problems. First, unlike measures like nominal or real interest as

a share of GDP it does not provide an objective measure that can be used across time, across

countries, or even measured at a point of time because it depends on projections about the

uncertain future.

Second, and relatedly, fiscal gaps have extremely large error bands because they depend

on deficit and debt forecasts that have extremely large error bands. To put this in perspective, if

the debt follows the mid-course trajectory shown in Figure 17 then the fiscal gap would be 0.5

but at the upper and lower 90 percent confidence intervals the fiscal gap could be anywhere from

-2.0 to +3.2 percentage points as shown in Table II.1. Projecting further in the future results in

even larger errors, with the large majority of infinite horizon fiscal gaps driven by projections

that are decades or more in the future.

Third, the fiscal gap measures the immediate adjustment that would be needed to stabilize

the debt-to-GDP ratio at its current value. Its current value, however, is arbitrary and

uninformative about what the goal of policymakers should be. The primary deficit adjustment

needed to achieve different fiscal targets varies enormously as shown in Table II.1 which shows

the immediate primary balance adjustment needed to achieve different debt-to-GDP goals in

2050. Does the United States need to make an immediate fiscal adjustment of 2.1 percent of

GDP to get the debt down to 50 percent of GDP or would it be reasonable for the debt to rise to

112 percent of GDP through 2050, in which case no adjustment, beyond social security reform,

would be needed? Note that all of the estimates in Table II.1 assume the equivalent of current

law on Social Security (i.e., Social Security reform happens). If a law is passed to continue

paying full benefits after the trust fund is exhausted that would add about 1.3 percent of GDP to

these fiscal gap measures.

33

Table II.1

Note: No change includes Social Security reform phased in linearly from 0.5% of GDP to 1.7% of GDP over 10

years beginning in 2025. Relative to the CBO baseline which assumes current policy for Social Security the fiscal

gaps would be about 1.3 percentage point larger.

Source: Congressional Budget Office; Macrobond; authors’ calculations.

The forward-looking nature of the fiscal gap makes it more informative about fiscal

sustainability but requires forecasts and subjectivity. The tradeoff between an objective but

uninformative measure and a subjective but informative one is largely unavoidable. The fiscal

gap is one metric that policymakers should use but it is important to put it in a broader context

and to that end we think that debt service ratios projected out over a period of about a decade are

a better way to minimize uncertainty and put context on the best fiscal targets.

END BOX-------------------------------------------------------------------------------------------------------

Implication 3: The Scope and Need for Public Investment Has Greatly Expanded

One of the principal arguments made for fiscal rectitude is a desire to avoid burdening

future generations with debt or to make them poorer as debt crowds out private investment. As

Blanchard (2019) recognizes the low level of real interest rates undercuts the force of the

crowding out argument because it implies the “certainty equivalent” productivity of capital is

low. More broadly the argument itself rests on an ethically ambiguous foundation because future

generations are likely to be richer than the current generation even net of any additional fiscal

obligations inherited by them. The utilitarian logic for redistribution from richer to poorer should

also apply across generations.

Even accepting the premise of intergenerational equity it is not obvious that deficit

reduction will make future generations richer and could even leave them poorer. The narrowest

example of this is deferred maintenance which is a cost that is akin to the debt even if it is not

Debt in 2050

Immediate

Primary Deficit

Reduction

90% Confidence Interval

for Debt with Associated

Deficit Reduction

Primary Deficit Reduction

Associated with 90% Confidence

Interval for Debt Target

50 2.1 -29 to 129 -0.5 to 5.1

97 (Fiscal Gap) 0.5 19 to 176 -2.0 to 3.2

112 (No Change) 0.0 33 to 190 -2.4 to 2.7

150 -1.2 71 to 229 -3.4 to 1.3

Immediate Primary Deficit Reduction Necessary to Achieve Selected Debt Targets in 2050

(Percent of GDP)

34

explicitly included or measured in the Federal balance sheet. Investments in infrastructure and

other areas that reduce deferred maintenance can reduce this (unaccounted for liability) and

replace it with a smaller but accounted for liability. The result is measured debt goes up even if

the meaningful liabilities of the Federal government go down. Put another way, it is better to fill

potholes today than to wait and fill them at a cost that grows faster than the interest rate, which is

currently around zero in real terms.

From a demand-side perspective in certain circumstances fiscal expansions can offset

some, all or even more than all of their cost, as discussed above. This happens if they expand

output more than they increase the debt by increasing the utilization of the economy’s potential.

From a supply-side perspective, public investment can also offset some, all or even more

than all of its cost if it has a sufficiently high rate of return in expanding the economy’s potential

itself. More important for a broader set of policies, public investments that have a rate of return

in excess of the interest rate can repay themselves in present value terms. Dickens, Sawhill, and

Tebbs (2006) provided a long-term analysis of investments in early education and found that

they more than pay for themselves over a 75-year horizon. Recently in an important paper

Nathaniel Hendren and Ben Sprung-Keyser (2020) synthesized high-quality research on 133

policy changes and found that numerous policy changes partly or even more than fully paid for

themselves in present value by raising future wages and reducing future government transfers.

As an example of their analysis consider the Perry preschool program:

“For example, “Perry Pre-School [cost] $17,759 in 2006 USD. However, we

estimate that the long-run reductions in transfer payments and increases in tax

revenue offset roughly 92% of these upfront costs. Heckman et al. (2010) estimate

significant earnings increases from ages 19-40, and an increase in earnings of

26% at age 40. We combine their estimated earnings effects with a forecast to age

65 this into a lifetime earnings impact of $70,535. Using a state and Federal

combined tax rate of 12.9% , this implies an increase in tax revenue of $9,607.

Heckman et al. (2010) also estimate that the policy led to a reduction of payments

on welfare programs of $3,941. In addition, there are also induced costs of college

attendance and vocational training whose incidence falls on the government.

Heckman et al. (2010)'s estimates actually imply a fall in such costs, saving the

35

government $2,805. This suggests $16,353 is repaid to the government, implying

a net cost of $1,406 (95% CI of [-9,235, 12,126]). Roughly 92% of the upfront

spending is repaid to the government.”

Many of the programs they examined more than repaid their initial costs including “four major

health insurance expansions to children over the past 50 years. We calculate an average across

those policies and find that for each $1 of initial expenditure they repaid $1.78 back to the

government in the long run.” They found similar results for numerous children’s education

programs like Head Start (in one of three estimates) and more K-12 spending, some college

programs like grants for tuition, and moving to opportunity housing vouchers. Even where they

did not find programs paid for themselves they found a substantial offset in costs.

Hendren and Sprung-Keyser used a 3 percent real discount rate for their analysis, well in

excess of the current or likely future cost of Federal borrowing. With a more realistic discount

rate many more programs, especially investments in education and children, would repay

themselves over time. Note even if an investment does not repay it may still be worth making.

Similarly, investments in infrastructure that have a rate of return higher than the cost of

government debt are worth making and with a sufficient rate of return they will repay themselves

as well. For example, research from the IMF and OECD finds that increased public investment

leads to increased economic growth, which, particularly during periods of economic slack, can

lower the debt-to-GDP ratio (Abiad, Furceri, and Topalova 2015 and Mourougane, et al. 2016).

Research also finds that there are substantial spillovers from investment in research and

development, particularly basic research, and implies current levels of investment are below their

socially optimal level (Bloom, Schankerman, and Van Reenan 2013; Akcigit, Hanley, and

Serrano-Velarde 2020).

The above points depend heavily on what the additional debt is used for. If it is used to

fund effective public programs with high rates of return, like research, infrastructure, education

and investments and support for children, it is very likely to have benefits far greater than the

costs of any additional debt accumulation. Wasteful and poorly designed spending programs or

tax cuts, however, are not justified by this logic.

Also, in the case of infrastructure, even if the investment pays for itself or offsets much of

its cost it still may be desirable to pay for it if the payfor itself has a policy rationale, like a gas

36

tax or vehicle miles travelled fee that addresses other externalities and helps ensure that existing

infrastructure is used better. Nevertheless, if these first best policies are not possible for political

reasons it is still worth doing the second best of unpaid for infrastructure investments.

Overall, it is impossible to be sure exactly what the right balance is but given the very

low interest rates currently and in the foreseeable future it is more likely to be a mistake to

excessively reduce the debt at the expense of more deferred maintenance and foregone

investments than it is to make the opposite mistake and overinvest.

Going Forward: New Objectives, New Guideposts, and New Guidelines

Currently the primary worry for policy in the United States and several other countries is

doing too little to expand the debt, not doing too much. Low interest rates create more scope and

need for expansionary fiscal policy, a reason to reassess views of debt sustainability, and more

reason to undertake public investments. Overall U.S. debt service obligations are currently

modest and the debt is modest relative to future GDP and the ability to generate taxes from this

GDP. Even the more conventional and misleading measure of the debt-to-GDP ratio is stable

over the next decade and assuming current law is complied with, which requires both the tax cuts

to expire and Social Security reform, it will be essentially stable over the next three decades as

well, although could plausibly be anywhere from among the lowest in postwar history to around

190 percent of GDP. Additional investments of about 1 percent of GDP that initially raised the

debt above this path could potentially pay for themselves and to the degree they do not would

still leave interest as a share of GDP below its historic levels.

Understanding how to respond to our challenges requires setting new objectives for fiscal

policy, adopting new guideposts to assess fiscal sustainability, and using new guidelines to set

fiscal policy.

Any fiscal policy approach should be a combination of optimal, understandable and

achievable. Some approaches, like the German balanced budget requirement, are understandable

but would not be achievable for some countries and are very far from optimal for many

countries, including Germany. Even if we knew the optimal approach—and we do not—it would

be of little use if it was not readily understood by the public and possible for policymakers to

37

follow. What follows is something we think is a reasonable combination that is not too far from

what policymakers could understand and implement in a manner that would foster stronger

economic growth, better responses to recessions and greater financial stability.

The objective of fiscal policy

The objective of fiscal policy should be growth and financial stability including the

avoidance of recessions and stronger long-term growth. This calls for more expansionary fiscal

policy both in the short run to combat the current recessionary conditions and over the medium-

and long-run to support demand and expand supply, including through some measures that

increase short-run deficits and debt and also other measures like balanced budget multipliers,

redistribution and expanded social insurance that can expand demand without increasing short-

run deficits and debt.

A new guidepost for fiscal policy: keeping real interest payments below 2 percent of GDP

The room for fiscal expansion is not, however, unlimited and policymakers need a