WORKING PAPER NO. 109

THE DYNAMICS OF FOREIGN PORTFOLIO INFLOWS AND

EQUITY RETURNS IN INDIA

AMITA BATRA

September 2003

INDIAN COUNCIL FOR RESEARCH ON INTERNATIONAL ECONOMIC RELATIONS

Core-6A, 4

th

Floor, India Habitat Centre, Lodi Road, New Delhi-110 003

Table of Contents

Foreword.................................................................................................................. 1

Abstract.................................................................................................................... 2

I. Introduction............................................................................................................. 3

II. Survey of Literature ............................................................................................... 4

III. Theoretical Foundations......................................................................................... 5

IV. Data ........................................................................................................................ 11

V. Empirical Analysis................................................................................................ 13

V.1 Positive Feedback Trading ............................................................................... 13

V.2 Herding............................................................................................................... 19

V.3 Destabilizing?..................................................................................................... 22

VI. Conclusions............................................................................................................ 23

Appendix.......................................................................................................................... 25

References........................................................................................................................ 27

2

Foreword

After a series of financial crises in the late 1990s, doubts have been expressed

about the wisdom of promoting free cross –border portfolio flows. Foreign Institutional

Investors (FIIs) constituting a major proportion of these cross –border capital flows are

considered to be driven by “animal spirits” rather than rational investment decisions. The

FIIs have often been blamed for large and concerted withdrawals of capital from

countries in times of crisis, despite evidence showing that domestic/resident investors are

often the first to exit at times of crisis, perhaps because of better information.

Foreign portfolio inflows through FIIs, in India, are important from the policy

perspective, especially when the country has emerged as one of the most attractive

investment destinations in Asia. In this paper an effort has been made to develop an

understanding of the investment decisions, trading strategies and behavior of the FIIs in

the Indian equity market.

This paper reveals aggregate evidence of FIIs chasing trends and adopting

positive feedback trading on a daily basis even though no such behavior is evident over

horizons of a month or so. This evidence seems to support the hypothesis that resident

investors have better information on a daily basis, thus making it essential for FIIs to use

price signals to discern underlying information that may have triggered them. Once the

information is in public domain basic analysis of the implications for stock returns

becomes more important. Thus, while FIIs do tend to herd together in the stock market,

their trading behavior does not appear to be destabilizing for the Indian equity market.

I do hope that this paper will serve as a useful source and provide valuable

reference material for researchers and policymakers associated with and interested in

foreign portfolio inflows in India.

Arvind Virmani

Director & Chief Executive

ICRIER

September 2003

1

Abstract

The Foreign Institutional Investors (FIIs) have emerged as important players in the Indian

equity market in the recent past. This paper makes an attempt to develop an

understanding of the dynamics of the trading behavior of FIIs and returns in the Indian

equity market by analyzing daily and monthly data. From our analysis we find that there

is strong evidence of FIIs chasing trends and adopting positive feedback trading strategies

at the aggregate level on a daily basis. However there is no evidence of positive feedback

trading on a monthly basis. The results of our analysis also indicate that foreign investors

have a tendency to herd together in their trading activity in India. The trading behavior

and biases of the FIIs do not appear to have a destabilizing impact on the equity market.

2

The Dynamics of Foreign Portfolio Inflows and Equity Returns in India

Amita Batra

7

I. Introduction

With the emerging market crises of the late 1990s, the role of Foreign Portfolio

Investment (FPI) and the major players therein i.e. the foreign institutional investors

(FIIs) has come under intense scrutiny by academics as well as policymakers. A general

perception about the FIIs is that they are speculators and their investment is motivated by

short- term gains. The FIIs in pursuit of short- term gains adopt short- term trading

strategies such as positive feedback trading and herding (i.e. buy or sell stocks together as

a group). Such behavioral biases of FIIs, it is believed, may lead to price overreaction and

contribute to the creation or exacerbation of a financial crisis.

In case of India, investment by FIIs has seen a steady growth since the opening of

the equity markets in September 1992. The share of FIIs in total FPI has increased from

47% in 1993-94 to around 74% in 2001-2002. FIIs have also acquired a significant

presence in the Indian stock market. The share of their trading in total turnover attained a

high of almost 30% in October 2001. In total market capitalization

1

FIIs account for

about 13% and they make about 50-60% of average daily deliveries on the stock market.

Notwithstanding the FIIs being important players in the Indian stock market and

that there are strongly held views on their trading behavior biases, little empirical analysis

on the subject in the Indian context has been undertaken. In this paper an effort has been

7

Sincere thanks are offered to Prof. Arvind Virmani for giving invaluable suggestions that helped me

finalize the paper. Thanks are due to an anonymous referee for making useful comments on the first draft.

Constructive suggestions by Dr. Wilima Wadhwa at the ICRIER seminar are thankfully acknowledged.

Research assistance provided by Mr. Puneet Sudan is appreciated.

1

Note that of total market capitalization only half is floating stock.

3

made to develop an understanding of the dynamics of the FII inflows and equity returns

in the Indian equity market.

The paper is organized as follows. In addition to Introduction in section one a

brief survey of the literature is presented in section two. In the following section the

theoretical foundations of positive feedback trading and herding are discussed. The data,

data sources and summary statistics of net equity purchases and equity returns are

presented in section four. Empirical estimation comprising three parts on positive

feedback trading, herding and impact of FII trading on stock market stability is given in

section five. Section six concludes.

II. Survey of Literature

Dornbusch and Park (1995) argue that foreign investors pursue positive feedback

trading strategies that make stocks overreact to changes in fundamentals. Bohn and Tesar

(1996) and Clark and Berko (1996) show a positive contemporaneous relation between

equity flows and stock returns using monthly data for Mexico. Choe, Kho and Stulz

(1998) have examined the impact of foreign investors on stock returns in Korea before

and after the 1997 Asian crisis using daily trade data. They find evidence of positive

feedback trading before the crisis. During the crisis period their study reveals a

weakening of the herding effect and disappearance of positive feedback trading by

foreign investors. In addition they find no evidence of a destabilizing effect of the trades

by foreign investors on Korea’s stock market. Using the measure for herding as

developed by Lakonishok, Shleifer and Vishny [LSV (1992)], Kim and Wei (2002) also

show strong tendencies for herding by foreign investors and offshore investment funds in

Korea in a similar time period. Bonser-Neal et al (2002) analyze the foreign trading

behavior on the Jakarta stock exchange (Indonesia) between 1995 and 2000.They detect

herding and positive feedback trading by foreign investors, but find no evidence to

indicate that such trading behavior by foreign investors destabilized the market prices

during the Asian crisis. Griffin et al (2002) use a theoretical model and empirical analysis

to show that global stock return performance is an important factor in understanding

4

equity flows. Richards (2002) using data for daily net purchases by foreigners in six

Asian emerging equity markets over 1999-2001 gives strong evidence of positive –

feedback trading with respect to domestic, US and regional equity returns.

As against the existing empirical literature that concentrates largely on stock /

firm level analysis, our study has broader coverage. It attempts to analyze aggregate

trading by FIIs in India rather than stock level trades of individual investors. Further,

keeping in view the greater possibility of homogeneity of trading behavior in one group,

our analysis includes all the FIIs rather than one subset of FIIs as has been the case in

earlier studies relating to feedback trading and herding.

III. Theoretical Foundations

Positive feedback trading pattern can result from extrapolative expectations about

prices, from stop – loss orders i.e. automatic selling when the price falls below a certain

point, from forced liquidations when an investor is unable to meet her margin calls or

from portfolio insurance investment strategy which calls for selling stocks when the price

falls and buying it when the price rises.

Our analysis on positive feedback trading tests the hypothesis that net equity

demand by FIIs is driven by recent returns in the equity market of the host country. This

can be viewed as a general exploration of the Brennan and Cao (1997) model that

suggests that net inflows should be a linear function of returns across equity markets.

This model explains why flows would depend on returns in contrast with the more often

discussed and tested, mean –variance model that produces no flows because of changes in

asset prices. A brief outline of the Brennan and Cao (1997) model on international

portfolio investment followed by the model specification for the present analysis is given

below

.

5

The Brennan and Cao Model

The optimal trading strategy of the individual investor i is given by

,

~

)(

~

)

~~

()

~~

(

~~~

1

0

1

∇−−+−−−=−≡∇

∑

−

=

−

t

j

tj

i

j

t

ttt

i

t

i

t

i

t

i

t

i

t

PSS

r

X

PUSPZSrDDD

……. (1)

1

~~~

−−≡∇ tPPPwhere

tt

Equation (1) shows that the trading strategy of investor

i

in period depends on:

t

the difference between his vector of private signals in period (Zt) and the vector of

prices, , weighted by his private signal precision matrix, ,

t

i

t

t

P

~

S

the difference between the vector of the average private signal,

U

, and the vector of

prices, , weighted by the average private signal precision matrix, ,

~

t

P

~

t

S

the vector of supply shocks due to new liquidity traders in session ,

t

X

~

the vector of price changes, , weighted by the difference between the investor's

private signal precision matrix and the market average precision matrix,

,

accumulated for all sessions up to session

t

.

t

P

~

∇

j

i

j

SS

−

1

−

Since the econometrician observes neither the supply shock nor the private

signals, it is convenient to consider the expected trade of investor

conditional on the

vector of price changes at time ,

∇

.

i

t

t

P

~

The conditional expected trade vector might be written as:

6

]

~

]

~

|/

~

[

~

[]

~

|

~

[

t

i

tttt

i

tt

i

t

PPrtXEPrPDE

∇Ω−∇+∇Γ=∇∇

ω

where

,

t

i

t

i

t

SS

−=

ω

the marginal informational (dis)advantage of investor arising from

private signals received at time

i

t

,

t

i

t

t

oj

i

j

i

t

KK

−==Ω

∑

=

ω

the cumulative informational (dis)advantage of the investor

arising from all the private signals received up to time t.

]

~

[]

~

,

~~

[

1

1

tttt

PVarPPUCov

∇∇−=Γ

−

−

The following simple results can be obtained in a single security setting:

0

>Γ

t

so that the trades of an investor with no cumulative information advantage ( =

0), but with positive marginal information advantage (

> 0), will be positively

correlated with the current price change; the trades of an investor with a positive

cumulative information advantage , but with no marginal information

advantage

, will be negatively correlated with the price change in the current

period.

i

t

Ω

i

t

ω

)0(

>Ω

i

t

)0(

=

i

t

ω

Thus the relation between the trades of well and poorly informed investors and

price changes is critically related to the extent to which the information (dis)advantage

arises from a marginal private information advantage in the current period, or from an

accumulation of superior private information signals in the past. To derive testable

implications from the model it will be necessary to make an assumption about the relative

magnitudes of the cumulative and marginal information advantages of domestic

investors.

7

To develop the implications of the model for international portfolio investment,

consider a setting in which there are M countries indexed m. The market portfolio of each

country is treated as a single risky asset, currency risk is ignored and assume that

investors in all countries have access to the same riskless asset whose return is zero.

Let

denote the measure of domestic investors in country m. Then, from equation (2),

the vector of conditional expected trades by investors in country m is given by:

m

µ

]

~

]

~

|/

~

[

~

[]

~

|

~

[

t

i

tttt

i

tt

i

t

PPrtXEPrPDE

∇Ω−∇+∇Γ=∇∇

ω

……(3)

Assuming that the contribution of noise traders in country m to the aggregate

supply shock, , is . Then, adding the trades on noise traders to those of the

(rational) investors, and dropping the time subscript, the expectation of the vector of

aggregate security purchases by all individuals in country m (including noise traders),

, conditional on the vector of prices changes, , is

t

X

~

t

m

X

~

µ

m

Π

~

P

~

∇

E

[

]

PP

mm

~~

|

~

∇Θ=∇Π

(4)

where

[

]

mmm

r

Ω−Γ≡Θ

ω

, ,

di

i

mi

m

ωω

ε

∫

≡

di

i

mi

m

Ω≡Ω

∫

ε

Equation (4) implies that portfolio flows can be written as a linear function of

price changes in the M market portfolios plus an orthogonal error term. If there are no

differences in information precisions across countries, then

and portfolio

flows will be independent of market returns. If there are differences in information

endowments, the conditional expectations of portfolio flows will be linearly dependent on

the vector of price changes

0

=Ω=

mm

ω

2

.

2

Allowing for lagged decision making by foreign investors, the flows may be expressed as a linear

function of recent returns.

8

It may be noted that Brennan and Cao predict a positive relationship between

flows and recent returns on the assumption that the information of the locals is the result

of a gradual process of superior information acquisition rather than of periodic large

information leakages to locals. A negative relation is possible if neither investor has a

cumulative information advantage, but locals have a marginal informational advantage

(i.e. better access to news).

Based on equation (4) above we specify the model for the present analysis. The

portfolio inflows i.e. net purchases of stocks by FIIs (NFIIP) is modeled as a function of

recent returns on the market portfolio of only one country i.e. the host country. Our

model specification is thus as follows:

Model Specification

NFIIP

t

=

γ

R

t-1

Where

NFIIP

t

denotes net equity purchases by FIIs at time t.

R

t-1

denotes returns in the previous period. As our analysis is restricted to one

country, i.e. India, the FII equity demand is modeled as a function of the returns on the

market portfolio (index) of India as represented by R

t-1.

γ

>0 refers to the case of positive feedback traders.

γ

<0 indicates a case of

negative feedback trading. The negative feedback trader exhibits a “buy low, sell high

strategy” Negative feedback trading can result from profit taking as markets rise or from

investment strategies that target a constant share of wealth in different assets.

If indeed the trading by foreign investors is related with returns, there are several

views as to whether this reflects the informational advantage or disadvantage of foreign

investors. Further there are differing views on the possible creation of price pressure,

9

herding bias and destabilizing effects of trading by FIIs. Some theoretical rationales that

have been developed to explain the herding bias in investor trading are as follows:

Reputational Herding

3

, investors may disregard their private information and

trade with the crowd due to the reputational risk of acting differently from other

managers (Scharfstein and Stein (1990)).

Investigative Herding, managers may trade together simply because they receive

correlated private information, perhaps from analyzing the same indicators (Froot,

Scharfstein and Stein (1992)) and (Hershleifer, Subrahmanyam and Titman (1994)).

Informational cascades- managers may infer private information from prior trades

of better-informed managers and trade in the same direction (Bikchandani, Hershleifer

and Welch (1992)),

Institutional investors may share an aversion to stocks with certain characteristics,

such as stocks with lower liquidity or stocks that are less risky (Falkenstein 1996).

While there exist several alternative rationales to explain herding, there is not, to

our knowledge, any theoretical model that takes into account these alternative rationales

to derive explicit predictions regarding herding by different groups of investors.

Pioneering empirical work to quantify herding has been undertaken by Lakonishok,

Shleifer and Vishny (LSV 1992) and Wermers (1999). We follow both LSV and

Wermers to measure the extent of herding by FIIs in India.

3

In The General Theory, John Maynard Keynes (1936 pp. 157-58) expresses skepticism about the ability

and inclination of “long term investors” to buck market trends and ensure efficient investment. In his view,

investors may be reluctant to act according to their own information and beliefs, fearing that their

contrarion behavior will damage their reputation as sensible decision makers

10

IV. Data

Basic Data

The analysis is undertaken using daily data. Daily data give more precise results

and are better able to capture the lead – lag dynamics between net equity purchases by

FIIs and equity returns. However as a longer series on both the equity returns and the FII

equity purchase and sales with a monthly frequency is available some results based on

monthly data are also presented to gain further insight into the trading behavior of FIIs

based on long horizon returns

4

. The average of the daily closing values of the price index

is used to arrive at the monthly data.

The returns are calculated for the sensex. Sensex was a natural choice for

inclusion in the study, as it is the most popular market index and widely used by market

participants for benchmarking.

Returns are proxied by the log difference change in the price index.

R

t

= log P

t

– log P

t-1

R

t

= return at time t

P

t,

P

t-1

= closing value of the stock price index at time t, t-1.

Days when there is no trading are omitted and the price change is calculated from

the last day the market was open. Local currency returns are used

5

.

Data on FII equity purchases and sales on daily and monthly basis for our

reference period are used. This is as available from the Securities and Exchange Board of

India (SEBI).

4

Weekly data was also analyzed. The results are not reported as they were not significantly different from

those for monthly data.

5

Typically, local market securities settle in local currency.

11

Sample Period

In the daily analysis we are constrained by the availability of data. Daily data on

FII equity purchase and sales are available from January 2000 to December 2002.

January 2000 to December 2002 is therefore our reference period for the daily analysis.

On a monthly basis, however data for both the sensex and the FII equity purchase and

sales is available from January 1994 to December 2002 and so the analysis on the

monthly basis is undertaken for this reference period. A further sub sample analysis is

undertaken for the monthly data. The sub samples are drawn as per an endogenous break

date analysis for the total turnover series to examine if the FIIs alter their trading

strategies when the total turnover series reveals a structural break. For herding, the sub

samples are identified to examine if the FIIs reveal excess herding in times of pressure (a

financial crisis in the region i.e. the East Asian crisis) in the stock market.

Descriptive statistics

A brief summary of the descriptive statistics for net equity purchases by FIIs and

the equity returns in the Indian stock market over 2000 – 2002 are presented in the

Appendix. Data on the autocorrelation structure of daily net equity purchases by FIIs and

trading imbalance (normalized excess purchases) and daily returns upto five lag periods

are also presented. The extent of predictability in daily net equity purchases by FIIs is

positive but small. The positive autocorrelation could be on account of investors

responding to new information in the same direction but with different speeds or simply

because some investors establish positions slowly. The first order autocorrelation is .16

for the trading imbalance and .26 for excess equity purchases and this falls over

subsequent periods. The median autocorrelation in net daily equity purchases by FIIs is

.05. The first order autocorrelation in returns is even lower and turns negative at lag two.

Median autocorrelation in daily net returns is very small (-.0190) and negative.

12

V. Empirical Analysis

Our empirical analysis comprises three parts. In part one we examine if trading by

FIIs reveals any trends of positive feedback trading. In part two we examine if there is

evidence of herding by the FIIs. In the last part we analyze the destabilizing impact, if

any, of the FII trading strategies on stock prices in India.

V.1 Positive Feedback Trading

Positive feedback trading describes the strategy of rushing in when the markets are

booming and rushing out when the markets are on the decline. Hence it predicts a relation

between the past performance of the market (as indicated by the value of the market

index) and the current FII investment. Based on the model specified in section III we

estimate the following regression

6

:

TRIM

t =

γ

R

t-1

+

ε

t

…………………………………………………………………..(V.1)

where

TRIM, the dependent variable is defined as normalized trading imbalance of FIIs

i.e. excess purchases normalized by total trade undertaken by FIIs at time t

TRIM is conditioned on the sign of the market return of the previous day (R

t-1

), the same

day (R

t

) and the day after (R

t+1

).

γ

> 0 indicates positive feedback trading

γ

< 0 indicates a case of negative feedback trading

The model as in equation (V.1) is estimated and then analyzed in three stages as

follows:

6

Our regressions provide no test for informational advantage or otherwise that the FIIs may have.

13

i) Static Analysis

As a first step to estimating the bivariate model in equation (V.1) we do a Granger

–causality test. Granger causality test is used to eliminate the possibility of a simultaneity

bias in the model. Our results for the test show that market returns Granger-cause future

foreign investment flows in India. Thus ensuring one way causality in the model we

proceed with checking for the presence of a unit root in the two variables. Both the

Augmented Dickey Fuller (ADF) and Philips - Perron (PP) tests confirm that variables,

TRIM and Ret., are stationary. The model is then estimated under OLS assumptions.

ii) A Dynamic analysis using a VAR model

()

t

t

t

t

t

TRIM

R

L

TRIM

R

∈+

+=

−

−

1

1

βα

Where L indicates the lag structure

7

.

The above specified VAR

8

system is used to analyze the impact of innovations in

returns on trading imbalance. For this we specify the channels of causality using the

standard “identification by ordering” methodology. The channel of causality is as

established from the results of the Granger – causality test. The Impulse Response

Functions (IRFs) so generated allow us to trace the time path of the impact of shocks on

the variables contained in the VAR.

iii) As the flows are somewhat predictable, it might only be the unexpected or

surprise component of flows that is related to lagged returns. To test for this a

series of unexpected trading imbalance (UTRIM) on day t is constructed.

Unexpected TRIM was derived as actual imbalance less expected flows. Both the

14

7

We estimate the model with two lags as determined by the AIC and SBC criteria.

8

As both the variables are stationary the VAR model is estimated in levels.

static and dynamic specifications are re-estimated with the unpredictable

component of trading imbalance as the dependent variable. Specifically we ask

the question: do returns predict flows over and above the predictions of lagged

flows?

Results:

Static Model

The results of the Static estimation of equation (V.1) using both TRIM and

UTRIM as dependent variable are shown below in Table V.1:

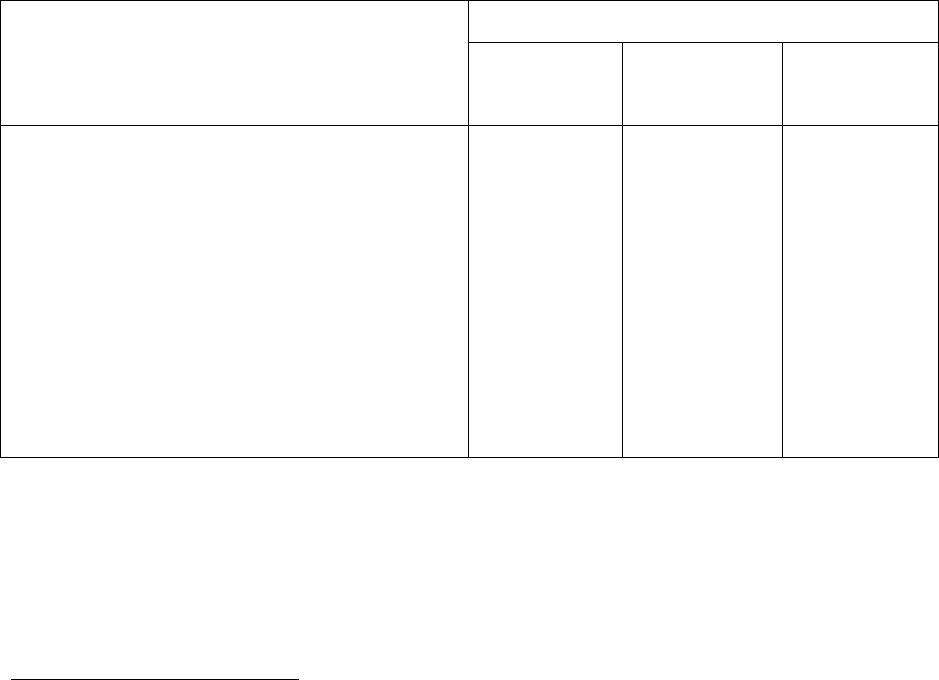

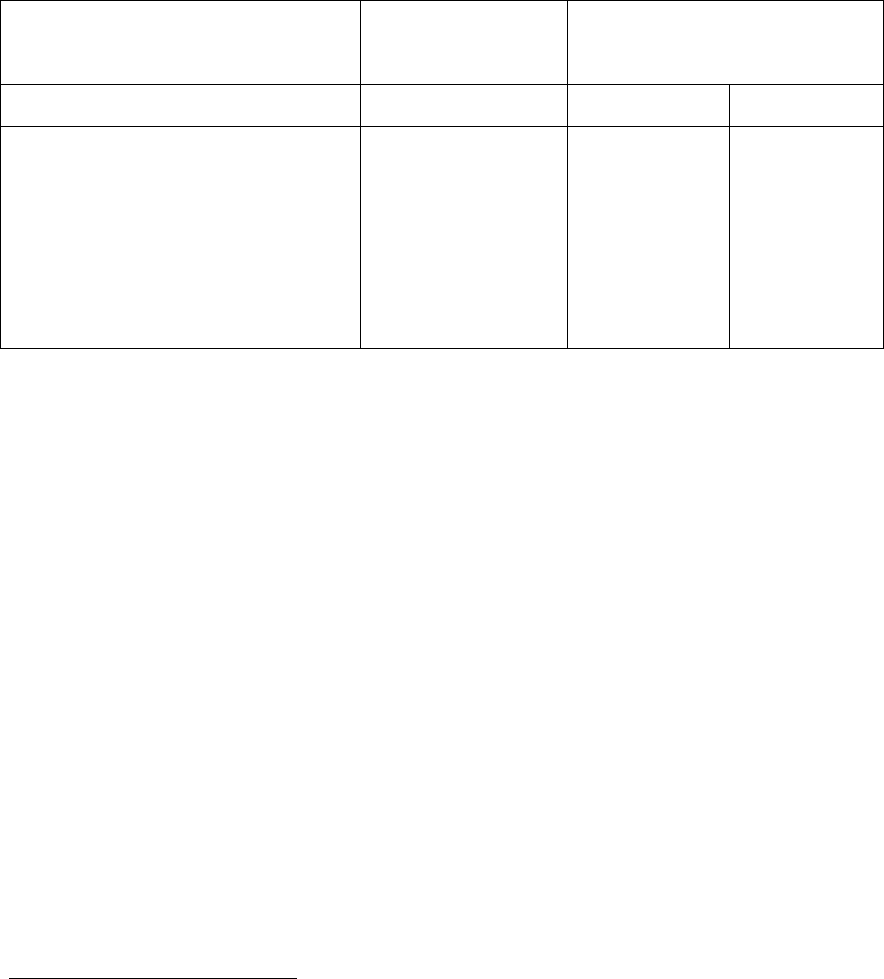

Table V.1

Independent variables

Dependent Variable

Normalized Trade Imbalance

R

R (-1)

R(+1)

TRIM

.5309

(1.0052)

3.49

(6.8159)*

.936

(1.7735)

UTRIM

.6568

(1.2779)

3.62

(7.2785)

7

1.06

(2.0686)

Figures in parentheses are t ratios

* Significant at .5%

A significant and positive relation between lagged daily returns and trade

imbalance is observed. There is strong evidence that FIIs have been positive feedback

traders at the aggregate level tending to buy following good news in the equity market in

India. With UTRIM as dependent variable the results remain unchanged. A highly

significant indication of the unexpected component of the variable TRIM following

lagged returns is observed.

15

The similarity of results for both the regressions using TRIM and UTRIM as

dependent variables could be on account of a very small predictable component in both

the series. As indicated in section IV the extent of autocorrelation at lag one is only 16

per cent for TRIM and 26 per cent for net purchases.

The static regression analysis has also been undertaken for the monthly data

9

and

the results are as shown in Table V.2 below:

TABLE V.2

Independent variables

Dependent variable:

Normalized Trade Imbalance

TRIM

R R (-1) R(+1)

1994:02 2002:07

1994:02 1998:02

10

1998:03 2002:06

.514

(1.0284)

1.146

(1.1356)

-.047

(-.1794)

.177

(.3513)

.67

(.6429)

-.237

(-.903)

.633

(1.2354)

1.0327

(1.0027)

.276

(1.0486)

Figures in parentheses are t ratios

There is no indication of positive feedback trading in monthly data. For monthly

data on the unpredictable component of trading imbalance (UTRIM) there is no

indication of positive feedback trading at all

11

. On a monthly basis the series of TRIM are

9

Exogeneity of variables for monthly data is established using Granger causality and Hausman test. The

results of the latter are presented in the Appendix.

10

For monthly data the analysis is carried out for the full sample and two sub periods. The sub periods are

classified by an endogenous break date analysis. We carry out this structural break test for total turnover

series. The test yields 1998:02 as indicative of a break in the total turnover series. We then proceed to

examine if the structural break in the FII turnover is accompanied by a change in their trading strategies

also.

11

Results not presented here but available with the author.

16

highly autocorrelated. It is possible that the FII investment is not led by returns, that is the

FIIs are not indulging in return chasing but is led by their own trade on a monthly basis.

From the static regression estimation results we can conclude that FIIs buy following

high previous day stock returns but respond very little with respect to previous month

stock returns

Dynamic Analysis (VAR)

The graphs for the Impulse Response Functions (IRFs) as generated by the

bivariate VAR model are shown in Figures 1 and 2 for lagged daily returns and lagged

monthly returns respectively. The response of TRIM to one S.E error shock to returns on

the previous day is sharp, significant but short lived. For the unexpected flows the lagged

returns are highly significant and the impact as seen through the Impulse Response

graphs trace a very sharp response of the UTRIM to lagged returns. The impact however

dies very soon. For monthly returns no significant feedback trading is observed

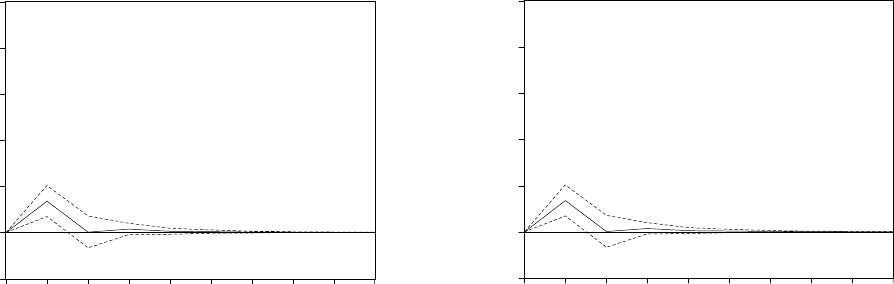

Figure 1: Response to a Shock to Lagged Daily Returns

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

1 2 3 4 5 6 7 8 9 10

Response of TRIM to RET(-1)

Response to One S.D. Innovations ± 2 S.E.

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

1 2 3 4 5 6 7 8 9 10

Response of UTRIM to RET(-1)

Response to One S.D. Innovations ± 2 S.E.

17

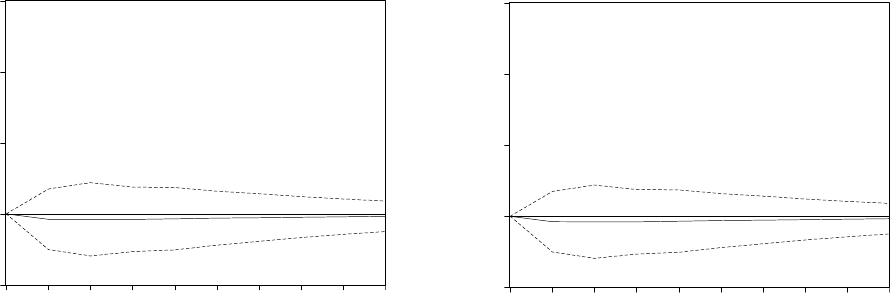

Figure 2: Response to a Shock to Lagged Monthly Returns

-10

0

10

20

30

1 2 3 4 5 6 7 8 9 10

Res pons e of TRIM to RET(-1)

Response to One S.D. Innovations ± 2 S.E.

-10

0

10

20

30

1 2 3 4 5 6 7 8 9 10

Response of UTRIM to RET(-1)

Response to One S.D. Innovations ± 2 S.E.

The analysis using the VAR model reinforces our conclusion from the static

estimation i.e. FIIs undertake significant positive feedback trading in relation to lagged

daily returns.

As the data reveals a strong tendency for the FIIs to indulge in positive feedback

trading over short horizons, we examine further if the FIIs show a herding bias in their

trading behavior. Before doing so, we briefly recapitulate our conclusions of the analysis

on positive feedback trading by FIIs in the Indian equity market.

Positive Feedback Trading: Conclusions

There is strong evidence that FIIs have been positive feedback investors at the

aggregate level on daily basis.

- FIIs in India are “return chasers” and/or “momentum traders”

A shock to current returns increases flows significantly but the impact is short-lived

The trend chasing - momentum trading characteristic of the FIIs meets the more

stringent test as well

18

- Lagged daily returns help in predicting daily flows over and above the

predictability of past flows

FIIs do not follow their own daily trade. This is evident from the low predictable

component FII net equity purchases by FIIs.

Popular financial press hypothesis of flows impacting returns does not hold true for

India

The trading Horizon of FIIs is possibly a day and not a month

V.2 Herding

In this section we evaluate the extent to which the FIIs herd. Herding or

correlated trading refers to a tendency for a particular investor group’s trade to

accumulate on one side of the market or the other without regard to direction.

Measurement of Herding

We assume that the market comprises of two groups of traders, foreign investors

and domestic investors. We calculate herding from the foreign investor’s perspective

. We

follow the measure proposed by Lakonishok, Shleifer and Vishny [LSV (1992)] and

Wermers (1998) to investigate the extent of herding by FIIs in India. The LSV measure is

as follows:

HM = | p(t) – E[p(t)]| - E| p(t) – E[p(t)]| ……………………………….. (V.2)

where

p (t) is the proportion of “buy” trade by FIIs on day t.

E| p (t)-E[p (t)] | is the adjustment factor to allow for random variation around the

expected proportion of “buys” under the null hypothesis of independent trading decisions

by FIIs. The adjustment factor assumes that p(t) follows a binomial distribution with the

probability E[p(t)] of success. For E[p (t)] a proxy that is the average “buy” trade during

the entire period of reference is used.

19

Implicitly equation (V.2) defines and measures herding as the tendency of a

subgroup of investors to trade a given stock (in our case stock index) together and in the

same direction, more often than would be expected by investors trading randomly and

independently

12

. The average of HM over the entire sample period gives the extent to

which FIIs herd in India. A positive and significant HM

13

is evidence of herding by FIIs.

Modified Herding Measure

We also use a modified herding measure (Wermers-1999) to examine if in a

particular period the FIIs were buying (or selling) in a proportion greater than the average

trade during that period. For monthly data this conditional measure is further examined

for a time period of excessive pressure (financial crisis in the region – East Asian crisis)

to see if the trading pattern by the FIIs in this period is any different from the other “more

normal” time period. The relation between the conditional and unconditional measure is

as follows:

Buy Herding Measure: BHM (t) = HM (t)|p (t)>E[p (t)]

Sell Herding Measure: SHM (t) = HM (t)|p (t)<E[p (t)]

Average of BHM and SHM will reveal if the FIIs herd into or out of the Indian

stock market at any time point. In computing these measures we are assuming that each

trade is originating from different institutional investors. It is possible otherwise that

herding may be on account of the same investor executing multiple trades. We however

do not have data to this level of detail and hence the assumption.

12

The LSV measure uses only the number of investors on the two sides of the market, without regard to the

extent of trade that they indulge in, to assess the extent of herding. In situations where, if the buyers and

sellers on either side are same in number but one side exceeds the other in terms of its trade (i.e. buy or sell

imbalance) the LSV measure may not be able to capture herding even though it may exist in the market.

We hope to correct for this deficiency in the LSV measure as we use the trade (buy) imbalance rather than

the number of FIIs on either side of the market.

13

The herding measure may be thought of as a measure of dispersion.

20

We compute the herding measure using daily and monthly horizon. The results for the

herding measures are presented in Table V.3 below.

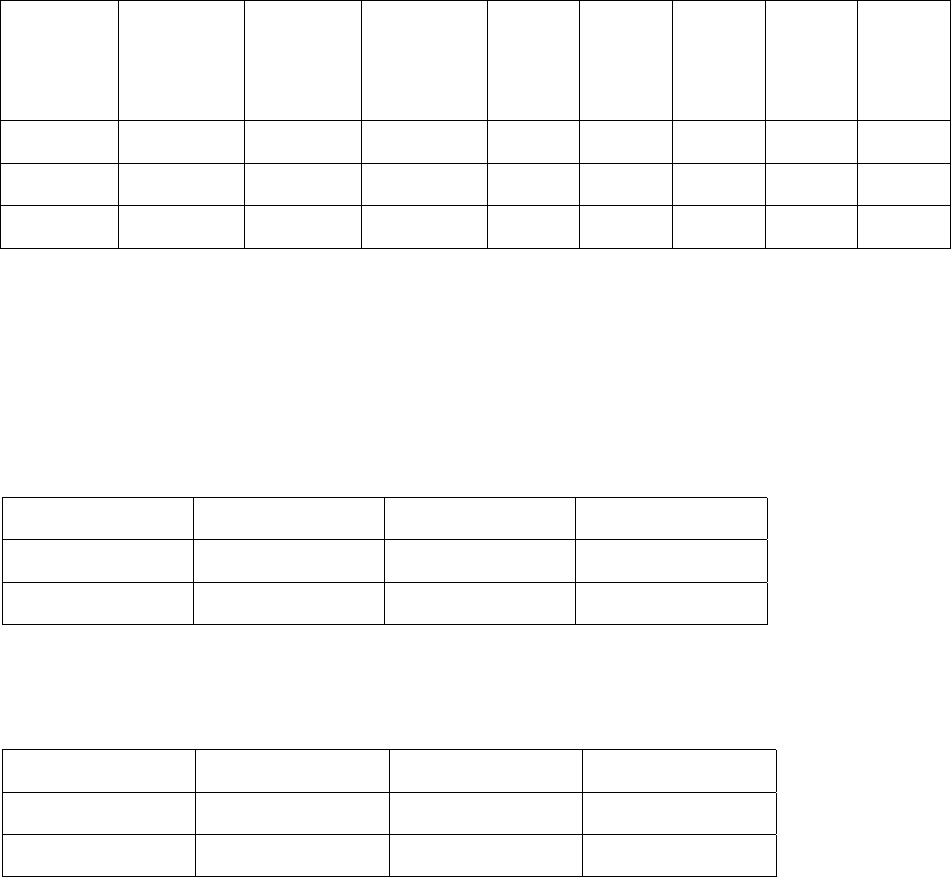

Results:

Table V.3: Herding Measures (%)

LSV Herding

Measure (%)

Conditional HM (%)

BHM SHM

Daily (full sample)

Monthly (full sample)

Sub period (EA crisis)

Pre sub period

9.41

14.72

13.31

24.02

9.04

14.31

6.79

22.6

9.82

15.16

20.97

26.5

Daily data extends from January 4, 2000 to December 30, 2002.

Monthly data extends from January 1994 to December 2002

EA crisis sub period is defined as July 1997 to December 1998.

Both daily and monthly data indicate herding. Herding by foreign investors on a

daily basis averages 9.41 per cent

14

. This implies that the extent to which trade by FIIs

accumulates on one side of the market is 9.41 per cent higher than the expected had the

FIIs trade been independent and random. For monthly data the HM measure is higher at

14.72. The higher HM for the monthly time period may imply that not all FIIs that move

together do so on the same day.

While daily and monthly HM do not reveal any significant difference in the buy

and sell side herding, even though there is a sell side bias in herding it is not very

significant. This however becomes very significant in times of pressure in the region as

revealed by our monthly data results for the sub - period coinciding with the East Asian

crisis. The sub - period shows a distinct pattern of heavy sell side herdingin comparison

14

Note that this HM value is more than that reported by Kim and Wei (2002) and Bonser – Neal et al(2002)

for pre crisis Korea and Indonesia respectively.

21

with the buy side herding during a crisis in comparison with HM prior to the pressure

period. There is a spectacular fall in the HM from pre crisis to crisis period on the buy

side and the fall though not as spectacular as for the buy side is also observed on the sell

side. This could be due to a differential reaction of the investors or because of lack of

liquidity of markets as crisis evolved. It is easier for investors to trade on the same side if

the liquidity is high than when the markets dry up.

The results indicate that foreign investors have a tendency to herd in the Indian

equity market even though they all may not do it on the same day. In times of pressure in

the stock market, on account of a financial crisis in the region there is excessive sell side

herding even though the extent of herding on the average and on either side of the market

during a crisis may be lower than that in the immediately preceding period

V.3 Destabilizing?

In the previous sections, we find evidence that foreign investors engage in herding

and positive feedback trading strategies in the Indian stock market. There has been

considerable debate on whether such trading strategies have adverse impacts on the

financial markets of emerging market economies. Neither positive feedback trading nor

herding may necessarily be destabilizing. The concern about positive feedback trading

however is that it makes stock prices overshoot to new information. Consequently, if

trades by FIIs destabilize markets, we would expect large sales (buys) by FIIs that

decrease (increases) prices to be followed by further price declines (increases).

On examining the data we observe that the days of “buy” imbalance follow

positive index returns, so that FIIs buy following price increases. The price increase

usually does not continue after the purchase by FIIs. In fact same sign (to the trade

imbalance) contemporaneous returns are also not observed. The reverse holds true for

“sell” imbalances. In case of events where price increase persists the returns are

insignificantly different from zero. This implies that even though trading by FIIs reveals

22

trend -chasing behavior there is no consequent persistent impact on prices or returns in

the market.

To investigate further if FIIs have a destabilizing effect on the equity market in

India, we use the event study methodology. We select days of largest buy order and sell

order imbalance. For each of the selected events we examine abnormal returns (based on

constant mean return model) from the preceding five (-5) to the following five (+5) days.

In Table VI.1 below we present the returns and abnormal returns for one such event.

Table Vl.1

Days Relative to the FII Trade Imbalance (Day 0)

-5 -4 -3 -2 -1 0 1 2 3 4 5

"Sell"

Raw Returns -0.03 0.004 -0.007 -0.003 0.011 0.009 0.019 0.001 -0.012 0.019 0.024

AR -0.015 0.029 0.018 0.022 0.014 0.034 0.026 0.013 0.006 0.006 0.044

"Buy"

Raw Returns -0.005 -0.001 0.034 0.002 0.016 0.006 -0.005 0.006 -0.001 0.007 0.001

AR -0.014 -0.01 0.025 0.007 -0.007 -0.003 -0.04 -0.003 -0.01 -0.002 -0.002

In general, on a day of positive net buy order imbalance the abnormal returns

show a negative sign while the reverse is true of the days of net sell order imbalance. The

FIIs therefore do not appear to have a destabilizing influence on stock prices.

VI. Conclusions

In this paper daily and monthly data has been analyzed to explore the trading

behavior of FIIs and the impact of their trading biases upon stock market stability. It is

found that there is strong evidence that FIIs have been positive feedback investors and

trend chasers at the aggregate level on a daily basis. However, there is no evidence of

positive feedback trading on a monthly basis. There are almost no joint dynamics

between long horizon returns and net equity purchases. The results of our analysis also

indicate that foreign investors have a tendency to herd on the Indian equity market even

though they all may not do it on the same day. In times of pressure in the stock market on

23

account of a financial crisis in the region there is excessive sell side herding even though

the extent of herding on the average and on either side of the market during a crisis may

be lower than that in the immediately preceding period. On investigating the impact of

trading imbalance across days we do not find any significant evidence that would make it

possible to attribute equity market instability to FIIs.

24

Appendix

I. Summary Statistics: 2000-2002

Variable

Mean

Median

S.D.

1

ρ

2

ρ

3

ρ

4

ρ

5

ρ

TRIM 0.056838 0.070316 0.24226 0.169 0.149 0.132 0.105 0.07

RET -0.000652 0.000473 0.017237 0.071 -0.015 -0.034 0.035 -0.011

NFIIP 30.85261 21.10 132.508 0.261 0.203 0.181 0.133 0.035

II. Stationarity

Unit Root Tests

TRIM

Test t statistic Critical value Inference(1%)

ADF -9.821 3.4417 No unit root

PP -21.8323 3.4417 No unit root

Ret

Test t statistic Critical value Inference(1%)

ADF -12.1304 3.4417 No unit root

PP -25.3946 3.4417 No unit root

25

III.A. Exogeneity

Granger Causality tests

Null Hypothesis F statistic Critical Value Inference

TRIM does not Granger cause Ret 4.27 6.68 Not reject

TRIM does not Granger cause Ret 31.24 6.68 Reject

The inference is drawn at 1 per cent level of significance but is valid at 5% also.

III.B. Hausman Test

Variable Coefficient t-statistic

C 3.80 .6799

Ret 421.85 .2954

Resid. Ret -362.17 -.2543

26

References

Bekaert, Geert and Campbell R. Harvey, 2003. ‘Emerging Markets Finance’, Journal of

Empirical Finance 10, 3-55.

Bikhchandani, Sushil, David Hirshleifer, and Ivo Welch, 1992, ‘A Theory of Fads,

Fashion, Custom, and Cultural Change as Informational Cascades’, Journal of

Political Economy 100, 992-1026.

Bohn, H., and L. Tesar, 1996, ‘U. S. Equity Investment in Foreign Markets: Portfolio

Rebalancing or Return Chasing?’, American Economic Review 86 (2), 77-81.

Bonser-Neal, C, Steven L. Jones, David Linman and Robert Neal, 2002, Herding,

Feedback Trading and Foreign Investors. Indiana University.

Brennan, M., and H. Cao, 1997, ‘International Portfolio Investment Flows’, Journal Of

Finance 52, 1851-1880.

Chakrabarti, Rajesh, FII Flows to India: Nature and Causes, Georgia Institute of

Technology.

Choe, Y., B. C. Kho, and R. M. Stulz, 1998, ‘Do Foreign Investors Destabilize Stock

Markets? The Korean Experience in 1997’, NBER Working Paper 6661, NBER

Cambridge M A.

Choe, Y., B. C. Kho, and R. M. Stulz, 1998, ‘Do Domestic Investors Have More

Valuable Information about Individual Stocks than Foreign Investors?’, NBER

Working Paper 8073

Claessens, Stijn, Susmita Dasgupta and Jack Glen. 1995, ‘Return Behavior in Emerging

Stock Markets’, World Bank Eonomic Review (January) 131-151.

27

Clark, J., and E. Berko,1997, ‘Foreign Investment Fluctuations and Emerging Market

Stock Returns: The Case of Mexico’, Federal Reserve Bank of New York, Staff

Reports 24.

Dornbusch, R. and Y.C.Park, 1995, ‘Financial Integration in a Second Best World: Are

We Sure About Our Classical Prejudices’, in R. Dornbusch and Y.C. Park, eds.,

Financial Opening: Policy Lessons for Korea, Korea Institute of Finance, Seoul,

Korea.

Froot, K., O’ Connell, P., and M. Seasholes, 2001, ‘The Portfolio Flows of International

Investors’, Journal of Financial Economics 59, 151-193

Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein, 1992, ‘Herd on The Street:

Informational Inefficiencies in a Market with Short-Term Speculation’, Journal of

Finance 47, 1461-1484.

Gooptu, Sudarshan. 1993, ‘Portfolio Flows to Emerging Markets, in Portfolio Investment

in Developing Countries’, World Bank Discussion Paper ed. by Stijn Claessens

and Sudarshan Gooptu (Washington: World Bank).

Grinblatt, M., S. Titman and R. Wermers, 1995, ‘Momentum Investment Strategies,

Portfolio Performance, and Herding’, American Economic Review 85, 1088-1105.

Griffin John M., F. Nardari and Rene M. Stulz, 2002, ‘Daily Cross Border Equity Flows:

Pushed of Pulled?’ NBER Working Paper 9000.

Hamao, Y., and J. Mei. 2001, ‘Living with the “Enemy”: An Analysis of Investment in

the Japanese Equity Market’, Journal of International Money and Finance 20:

715-730

28

Hirshleifer, David, Avanidhar Subrahmanayam, and Sheridan Titman, 1994, ‘Security

Analysis and Trading Patterns when Some Investors Receive Information Before

Others’, Journal of Finance 49, 1665-1698.

Hirshleifer, David and Siew Hong Teoh, 2001, ‘Herd Behavior and Cascading in Capital

Markets: A Review and Synthesis’, Working Paper, Ohio State University.

Howell, Michael J. 1993, ‘Institutional Investors and Emerging Stock Markets, in

Portfolio Investment in Developing Countries’, World Bank Discussion Paper ed.

By Stijn Claessens and Sudarshan Gooptu (Washington: World Bank).

Kim, W., and S.Wei, 2002, ‘Foreign Portfolio Investors Before and During A Crisis’,

Journal of International Economics 51, 77-96.

Lakonishok, Josef, Andrei Shleifer, and Robert W. Vishny, 1992, ‘The Impact of

Institutional Trading on Stock Prices’, Journal of Financial Economics 32, 23-44.

Nofsinger, John R. and Richard W. Sias, 1999, ‘Herding and Feedback Trading by

Institutional and Individual Investors’, Journal of Finance, 54, 6, December 2263-

2295.

Richards, Anthony, 2002, ‘Big Fish in Small Ponds: The Momentum Investing and Price

Impact of Foreign Investors in Asian Emerging Equity Markets’, Reserve Bank of

Australia and IMF.

Samal, Kishore C., 1997. Emerging Equity Market in India: Role of Foreign Institutional

Investors, Economic and Political Weekly, October 18, 2729-2732.

Scharfstein, David S. and Jeremy C. Stein, 1990, ‘Herd Behavior and Investment’,

American Economic Review 80, 465-479.

29

Seasholes, M., 2001, ‘Smart Foreign Traders in Emerging Markets’, Unpublished

working paper, University of California, Berkeley.

Sias, Richard W., and John R. Nofsiger, 1998, ‘Herding and Feedback Trading by

Institutional and Individual Investors’, Unpublished working paper, Washington

State University.

Sias, Richard W., and Laura T. Starks, 1997, ‘Return Auto-correlation and Institutional

Investors’, Journal of Financial Economics 46, 103-131.

Sias, Richard W., 2001, ‘The Behavior of Institutional Investors: Tests for Herding,

Stealth Trading, and Momentum Trading’.

Warther, V., 1995, ‘Aggregate Mutual Fund Flows and Security Returns’, Journal of

Financial Economics.

Wermers, Russ, 1999, ‘Mutual Fund Herding and The Impact on Stock Prices’, Journal

of Finance 2, 581-622.

30