Journal of Financial Economics 31(1992) 13-43. North-Holland

The impact of institutional trading on

stock prices*

Josef Lakonishok

Cnirersity of Illinois at (;rbana-Champaign. Champuign. IL 61820. USA

Andrei Shleifer

Hurcard tiniwrsir~. Cambridge. MA 02138. L’SA

Robert W. Vishny

L’nicersiry 01’ Chicago, Chicago. IL 60637, USA

Received September 1991, tinal version received March 1992

This paper uses new data on the holdings of 769 tax-exempt (predominantly pension) funds. to

evaluate the potential effect of their trading on stock prices. We address two aspects of trading by

these money managers: herding, which refers to buying (selling) simultaneously the same stocks as

other managers buy (sell), and positive-feedback trading, which refers to buying past winners and

selling past losers. These two aspects of trading are commonly a part of the argument that

institutions destabilize stock prices. The evidence suggests that pension managers do not strongly

pursue these potentially destabilizing practices.

1. Introduction

Instead of merely buying and holding the market portfolio, most investors

follow strategies of actively picking and trading stocks. When investors trade

actively, their buying and selling decisions may move stock prices. Understand-

ing the behavior of stock prices thus requires an understanding of the invest-

ment strategies of active investors.

Correspondence ro: Robert W. Vishny, Graduate School of Business, University of Chicago, 1101

East 58th Street. Chicago, IL 60637, USA.

*We are grateful to Louis than, Kenneth Froot (the referee). Lawrence Harris. hIark Mitchell.

Jay Ritter. Jeremy Stein. and Richard Thaier for helpful comments; and especially to Gil Beebower

and Vasant Kamath for their helpful advice. Financial support from NSF. LOR-Nikko, and

Dimensional Fund Advisors is gratefully acknowledged.

030%405X.92 SO5.00 c 1992-Elsevier Science Publishers B.V. All rights reserved

24 J. Lakonishok er ui., The impucr of insrrrurional rrading on stock prices

Institutional investors hold about 50% of the equities in the United States. In

1989. their trading and that of member firms accounted for 70% of the trading

volume on the New York Stock Exchange [Schwartz and Shapiro (1992)]. To

see if institutional investors’ trades influence stock prices. we empirically exam-

ine the trading patterns of institutional investors, focusing in particular on the

prevalence of herding and positive-feedback trading, which are associated with

the popular belief that institutional investors destabilize stock prices. We evalu-

ate a sample of 769 all-equity tax-exempt funds, the vast majority of which are

pension funds, managed by 341 different institutional money managers. The

data were provided by SEI, a large consulting firm in financial services for

institutional investors. The sample is particularly appropriate for addressing the

questions of herding and positive-feedback trading in that the money managers

directiy compete with each other: they pursue the same customers and they are

evaluated by the same service. [For an analysis of the investment performance of

the money managers in this sample, see Lakonishok, Shleifer, and Vishny

(1992).] There is thus more scope for finding herding and positive-feedback

trading in this sample of institutions than in a random sample of institutions.

Our data consist of end-of-quarter portfolio holdings for each of the 341

money managers from the first quarter of 1985 through the last quarter of 1989.

These data enable us to estimate how much each manager bought and sold of

each stock in each quarter. We can then test for herding by assessing the degree

of correlation across money managers in buying and selling a given stock (or

industry grouping). We can also test for positive-feedback trading by examining

the relationship between money managers’ demand for a stock and the past

performance of that stock. Finally, we can test the relationship between the

excess demand by institutions and contemporaneous stock price changes

directly. The results of these tests will shed light on the potentially destabilizing

effect of institutional investors.

In brief, our results suggest that neither the stabilizing nor the destabilizing

image of institutional investors is accurate. The evidence suggests that pension

fund managers herd relatively little in their trades in large stocks (those in the

top two quintiles by market capitalization), which is where over 95% of their

trading is concentrated. There is some evidence of more herding in smaller

stocks, but even there the magnitude of herding is far from dramatic. As far as

trading strategies go, institutions appear to follow neither positive- nor nega-

tive-feedback strategies, on average. There is some evidence of positive-feedback

trading in smaller stocks, but not in the large stocks which make up the

institutions’ preferred holdings. Finally, the correlation between the excess

demand by institutions for a stock in a given quarter and the price change of the

stock in that quarter is extremely weak, which provides some evidence against

the view that large swings in institutional excess demand drive price movements

of individual stocks. The overall picture that emerges from this paper is one of

institutional investors pursuing a broad diversity of trading styles that, to a large

J. Lakonishok er al., The impucl of institutional trading on stock prices 25

extent, offset each other. Of course, without an accurate measure of the relevant

elasticities of demand for stocks, we cannot rule out the possibility of large price

impacts from what appear to be small amounts of herding or positive-feedback

trading.

Our results are most closely related to research done some twenty years ago

by Kraus and Stall (1972), who address the question of ‘parallel trading’ (which

is the same as herding) by institutions using data from the SEC study of

institutional investors on monthly changes in holdings. They find little evidence

of herding and weak evidence of a contemporaneous relationship between price

changes and excess demand by institutions. Also of great interest and relevance

is the study of mutual funds by Friend, Blume, and Crockett (1970), who find

that mutual funds tend to buy stocks which in the previous quarter were bought

by successful funds, whom they are probably imitating. Such behavior would

lead to herding as well as to positive-feedback trading.

In the next section of this paper, we discuss some differing views of the impact

of institutional investors on stock prices and review relevant research. Section 3

describes our data in more detail. In section 4 we examine the issue of herding,

and section 5 deals with feedback trading strategies. Section 6 presents direct

evidence on the correlation between institutional demand and stock prices;

section 7 concludes the paper.

2. Theories of the impact of institutional trading on prices

According to one view, institutions destabilize stock prices, which usually

means that prices move away from fundamental values, thereby increasing

long-run price volatility. This view rests to a large extent on two premises. The

first premise is that swings in institutional demand have a larger effect on stock

prices than swings in individual demand, in part because institutions have much

larger holdings than most individuals and therefore have larger trades. More

importantly, however, price destabilization may be aggravated by herding, or

correlated trading across institutional investors. When several large investors

attempt to buy or sell a given stock at the same time, the effect on price can be

large indeed. A pension fund manager has described this problem succinctly:

‘Institutions are herding animals. We watch the same indicators and listen to the

same prognostications. Like lemmings, we tend to move in the same direction at

the same time. And that, naturally, exacerbates price movements’ [ Wall Street

Journal (October 17, 1989)].

There are several reasons why herding might be more prevalent among

institutions than among individuals. First, institutions might try to infer in-

formation about the quality of investments from each others’ trades and herd as

a result [Shiller and Pound (1989), Banerjee (1992), Bikhchandani, Hirshleifer,

and Welch (1992)]. Since institutions know more about each others’ trades than

‘6 J. Lakonishok et al., The impact of institubonal trading on stock prices

do individuals, they will herd to a greater extent. Second, the objective difficul-

ties in evaluating money managers’ performance and separating ‘luck’ from

‘skill’ create agency problems between institutional money managers and fund

sponsors. Typically, money managers are evaluated against each other. To

avoid falling behind a peer group by following a unique investment strategy,

they have an incentive to hold the same stocks as other money managers

[Scharfstein and Stein (1990)-J. Third, institutions might all react to the same

exogenous signals, such as changes in dividends or analysts’ recommendations,

and herd as a result. Again, because the signals reaching institutions are

typically more correlated than the signals that reach individuals, institutions

might herd more. When large institutional money managers end up on the same

side of the market, we expect the stock price to move provided the excess

demand curve for this stock slopes downward.

Herding does not necessarily destabilize stock prices, however. As we men-

tioned above, institutions might herd if they all react to the same fundamental

information in a timely manner. If so, they are making the market more efficient

by speeding up the adjustment of prices to new fundamentals. Or they might

herd if they all counter the same irrational moves in individual investor

sentiment, which would also have a stabilizing effect. In such cases, observing

herding is not sufficient to conclude that institutional investors destabilize

prices.

This leads to the second premise of the argument that institutions destabilize

stock prices: their strategies tend not to be based on fundamentals, possibly

because of agency problems in money management. Fundamental strategies,

such as contrarian investment strategies of buying ‘cheap’ high-dividend-yield

or high-book-to-market stocks, often take a long time to pay off, and may

actually do very badly in the short run relative to a popular benchmark such as

the S&P 500. Since money managers can be dismissed after only a few quarters

of bad performance, contrarian strategies put managers at significant risk. As

a consequence, money managers might follow short-term strategies based not

on fundamentals but on technical analysis and other types of feedback trading.

One particularly common example of a potentially destabilizing short-term

strategy is trend chasing, or positive-feedback trading [De Long et al. (1990),

Cutler, Poterba. and Summers (1990)], which is simply the strategy of buying

winners and selling losers. Such trading might be driven by a belief that

trends are likely to continue, a popular concept in the behavioral literature

[Andreassen and Kraus (1988)]. From the money manager’s perspective, the

strategy of adding winners to the portfolio and eliminating losers has the added

advantage of removing ‘embarrassments’ from the portfolio for the sake of the

sponsors, i.e.,

‘window dressing’ [Lakonishok et al. (1991)]. Positive-feedback

trading is destabilizing if it leads institutions to jump on the bandwagon and buy

overpriced stocks and sell underpriced stocks, thereby contributing to a further

divergence of prices away from fundamentals. Positive-feedback trading is not

J. Lakonishok et al.. The impacf of instifulional wading on stock prices

27

necessarily a destabilizing strategy, however; such trading will bring prices closer

to fundamentals if stocks underreact to news.

A completely opposing view of institutional investors is that they are rational

and cool-headed investors who counter changes in the sentiment of individual

investors. Unlike individual investors, institutions are exposed to a variety of

news reports and analyses, as well as to the guidance of professional money

managers, which puts them in a better position to evaluate the fundamentals.

According to this view, institutions will herd if they all receive the same

information and interpret it similarly, or if they counter the same swings in

individual investor sentiment. But they will not herd if they receive uncorrelated

information or interpret the same information in different ways. This view also

predicts that rational institutions are likely to pursue negative-feedback stra-

tegies, i.e., buying stocks that have fallen too far and selling stocks that have

risen too far.

There is also a third, and more neutral, view of institutional investors, which is

that institutions are neither smart negative-feedback investors nor destabilizers

who herd and chase trends. Instead, institutions are heterogeneous: they use

a broad variety of different portfolio strategies which by and large offset each

other. Their trading does not destabilize asset prices because there are enough

negative-feedback traders to offset the positive-feedback traders. Moreover, the

diversity of the trading strategies is great enough that the aggregate excess

demand by institutions is close to zero, so that no herding emerges in equilib-

rium. Institutional pursuit of the various trading strategies is therefore fairly

benign, for despite generating a substantial trading volume, institutions are not

destabilizing stock prices.

3. Data

Our analysis is based on a sample provided by SE1 of 769 tax-exempt equity

funds. According to the SE1 definition, equity funds hold at least 90% of their

assets in equities. For each fund, at the end of each quarter from 1985 through

1989, the dataset contains the number of shares held of each stock. Most of the

fund sponsors are corporate pension plans, but there are also a few endowments

as well as state and municipal pension funds.

The total amount under management in these 769 funds at the end of 1989 is

$124 billion, or about 18% of the total actively-managed holdings of pension

funds. The average equity holdings of a fund are $161 million. Equity purchases

and sales are estimated based on changes in end-of-quarter holdings of all

NYSE, AMEX, and OTC stocks. The prices used to estimate dollar values are

averages of beginning- and end-of-quarter stock prices. All holdings and prices

are adjusted for stock splits and stock dividends. The data do not allow us to

measure intraquarter round-trip transactions, although such transactions are

28 J. Lakonishok er al.. The impacr of institutional wading on slack prices

infrequent and should have a minor impact on the results, particularly since we

are more interested in price destabilization over horizons of a quarter or more.

Typically, a money manager has more than one fund under management. In

our case, the 769 funds are managed by 341 different money managers, with the

number of funds per manager ranging from one to 17. In general, different funds

managed by the same manager have similar, if not identical, holdings. Therefore,

the appropriate unit of analysis is a money manager rather than a fund, and so

all the holdings of different funds with the same money manager are aggregated.

Of course, money managers in our sample might manage additional funds that

are not in our sample if these funds are not evaluated by SEI. The average

portfolio of a money manager in our sample at the end of 1989 is $363 million.

Twenty-three money managers had more than one billion dollars under man-

agement and the largest money manager in the sample had 12 billion dollars.

An important part of this paper will be the distinction between the trading

strategies of money managers in large and small stocks, although the vast

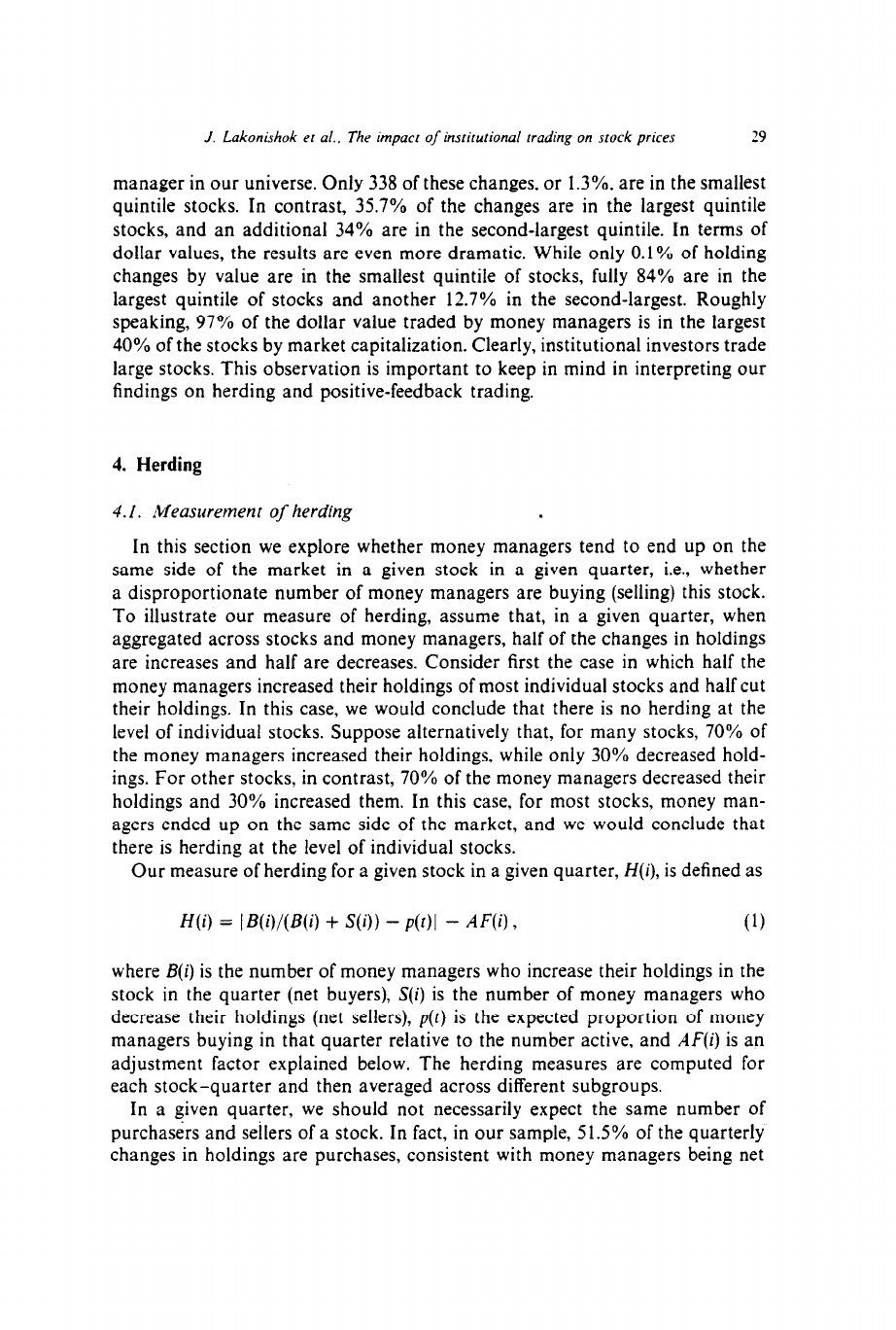

majority of holdings and trading of these investors are in large stocks. Table 1

presents information on buying and selling activity by size (market capitaliza-

tion) quintiles. The cut-off points for size quintiles were determined from the

universe of NYSE and AMEX stocks and updated quarterly. The table presents

the number of portfolio changes and the dollar value traded in each size quintile.

Taking each quarterly change in a stock as a separate observation, we have

a total of 26,292 cases where holdings were changed by at least one money

Table 1

Sample characteristics for quarterly holdings changes by 341 tax-exempt money managers in the

period 19851989.

Number of quarterly changes in holdings and dollar value of changes (in millions) by size (market

capitalization) quintiles determined from the universe of NYSE and AMEX stocks. The numbers in

parentheses are the percentage of the number of all changes in holdings and the percentage of the

dollar value of all changes in holdings that occur in the respective size quintiles.

Quintile

Number of changes in holdings

(percent in quintile)

Dollar value of changes in

holdings in millions

(percent in quintile)

I (smallest) 338

(1.3%)

2 2,087

(7.9%)

3 5,515

(21.0%)

4 8,963

(34.0%)

5 (largest) 9,389

(35.7%)

270

(0.1%)

1,648

(0.4%)

11,030

(2.8%)

50.373

(12.7%)

333,310

(84.0%)

J. Lakonishok et al., The impact of institutional trading on stock prices 29

manager in our universe. Only 338 of these changes, or 1.3%, are in the smallest

quintile stocks. In contrast, 35.7% of the changes are in the largest quintile

stocks, and an additional 34% are in the second-largest quintile. In terms of

dollar values, the results are even more dramatic. While only 0.1% of holding

changes by value are in the smallest quintile of stocks, fully 84% are in the

largest quintile of stocks and another 12.7% in the second-largest. Roughly

speaking, 97% of the dollar value traded by money managers is in the largest

40% of the stocks by market capitalization. Clearly, institutional investors trade

large stocks. This observation is important to keep in mind in interpreting our

findings on herding and positive-feedback trading.

4. Herding

4. I. Measurement of herding

In this section we explore whether money managers tend to end up on the

same side of the market in a given stock in a given quarter, i.e., whether

a disproportionate number of money managers are buying (selling) this stock.

To illustrate our measure of herding, assume that, in a given quarter, when

aggregated across stocks and money managers, half of the changes in holdings

are increases and half are decreases. Consider first the case in which half the

money managers increased their holdings of most individual stocks and half cut

their holdings, In this case, we would conclude that there is no herding at the

level of individual stocks. Suppose alternatively that, for many stocks, 70% of

the money managers increased their holdings, while only 30% decreased hold-

ings. For other stocks, in contrast, 70% of the money managers decreased their

holdings and 30% increased them. In this case, for most stocks, money man-

agers ended up on the same side of the market, and we would conclude that

there is herding at the level of individual stocks.

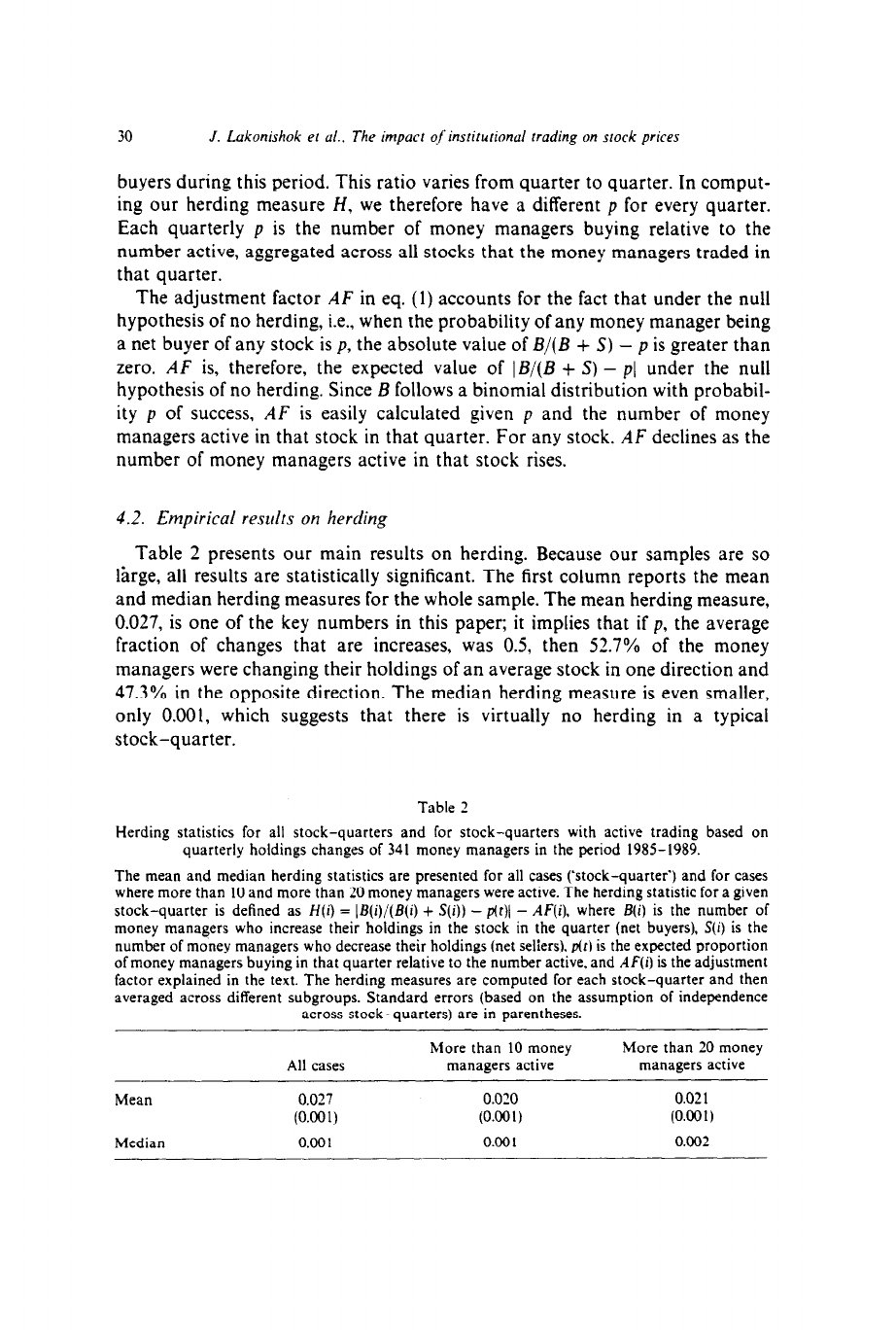

Our measure of herding for a given stock in a given quarter, H(i), is defined as

W) = IB(i)l(B(i) + S(i)) - p(t)] - AF(i),

where B(i) is the number of money managers who increase their holdings in the

stock in the quarter (net buyers), S(i) is the number of money managers who

decrease their holdings (net sellers), p(t) is the expected proportion of money

managers buying in that quarter relative to the number active, and AF(I’) is an

adjustment factor explained below. The herding measures are computed for

each stock-quarter and then averaged across different subgroups.

In a given quarter, we should not necessarily expect the same number of

purchasers and sellers of a stock. In fact, in our sample, 51.5% of the quarterly

changes in holdings are purchases, consistent with money managers being net

30 J. Lukonishok et (11.. The impact of institurional trading on stock prices

buyers during this period. This ratio varies from quarter to quarter. In comput-

ing our herding measure H, we therefore have a different p for every quarter.

Each quarterly p is the number of money managers buying relative to the

number active, aggregated across all stocks that the money managers traded in

that quarter.

The adjustment factor AF in eq. (1) accounts for the fact that under the null

hypothesis of no herding, i.e., when the probability of any money manager being

a net buyer of any stock is p, the absolute value of B/(B + S) - p is greater than

zero. AF is, therefore, the expected value of IB/(B + S) - pi under the null

hypothesis of no herding. Since B follows a binomial distribution with probabil-

ity p of success, AF is easily calculated given p and the number of money

managers active in that stock in that quarter. For any stock, AF declines as the

number of money managers active in that stock rises.

4.2. Empirical results on herding

Table 2 presents our main results on herding. Because our samples are so

large, all results are statistically significant. The first column reports the mean

and median herding measures for the whole sample. The mean herding measure,

0.027, is one of the key numbers in this paper; it implies that if p, the average

fraction of changes that are increases, was 0.5, then 52.7% of the money

managers were changing their holdings of an average stock in one direction and

47.3% in the opposite direction. The median herding measure is even smaller,

only 0.001, which suggests that there is virtually no herding in a typical

stock-quarter.

Table 2

Herding statistics for all stock-quarters and for stock-quarters with active trading based on

quarterly holdings changes of 341 money managers in the period 1985-1989.

The mean and median herding statistics are presented for all cases (‘stock-quarter’) and for cases

where more than 10 and more than 20 money managers were active. The herding statistic for a given

stock-quarter is defined as H(i) = IB(i)/(B(i) + S(i)) - p(t)1 - Af(i), where B(i) is the number of

money managers who increase their holdings in the stock in the quarter (net buyers), S(i) is the

number of money managers who decrease their holdings (net seliers), p(r) is the expected proportion

of money managers buying in that quarter relative to the number active, and AF(i) is the adjustment

factor explained in the text. The herding measures are computed for each stock-quarter and then

averaged across different subgroups. Standard errors (based on the assumption of independence

across stock-quarters) are in parentheses.

Mean

Median

All cases

0.027

(0.001)

0.00 1

More than 10 money

managers active

0.020

(0.001)

0.00 I

More than 20 money

managers active

0.02 1

(0.001)

0.002

J. Lakonishok et al.. The impact of insrirurional trading on stock prices

31

Perhaps we should not be surprised by how low this number is. In the market

as a whole, aggregating across all traders, there can be no herding, since for

every share bought there is a share sold. If our sample of money managers is

a random sample of traders, we would not expect to find any herding. Herding

can only be detected within subsets of investors. Since we are analyzing one such

subset (pension fund managers), herding within this subset can certainly exist,

although we do not find any evidence thereof.

Some might argue that we should look within a finer subset of money

managers who share a similar investment style in order to detect herding, but we

are not persuaded by this argument. For one thing, virtually all of the money in

our sample is managed by stock-picking pension fund managers evaluated by

the same service. We do not have individuals or even most types of institutional

investors. It is hard to believe that we have a random sample of U.S. equity

investors, given how homogeneous our sample is by construction. In fact, we

have argued earlier that restricting our sample to all-equity pension fund

managers evaluated by the same service significantly increases the chances of

detecting herd behavior.

Moreover, suppose that there are some large subgroups of institutions, with

each subgroup practicing a distinct investment philosophy, and suppose that

there is a great deal of herding among members of each subgroup. This would

raise two possibilities. First, the strategies of different subgroups are uncor-

related and, hence, they do not counter each others’ demand shifts. For example,

growth money managers destabilize growth stocks and value money managers

destabilize low-P/E stocks. Our measure of herding calculated even on a ran-

dom sample of institutions would detect the herding that was going on, since the

subgroup of institutions trading in parallel would cause the whole set of

institutions to be on one side of the market, with individuals taking the other

side. Our results reject this possibility, since we do not find much herding

looking over all stocks.

The second possibility is that although money managers herd within sub-

groups, the subgroups trade with each other so as to systematically counter each

other’s effects on prices. For example, if growth money managers buy a stock,

value money managers sell it to them. But in this case, there is no destabilization

since money managers just trade with each other. This possibility is consistent

with our evidence of very little herding by institutional investors.

For many stocks in our sample, the number of managers who changed their

holdings in that stock is quite small. In table 2 we also provide herding results

for stocks in which a substantial number of money managers were active. This

restriction eliminates many of the smaller stocks. The results are similar to our

earlier findings of little herding.

Another intuitive way to look at herding is to examine the fraction of purchas-

ing behavior of an individual money manager that can be explained by the actions

of other money managers. We run a regression across stock-quarters, in

3’

J. Lokonishok er al.. The impact of insritutional truding on srock prices

which the dependent variable gets the value of one if a randomly-chosen money

manager who traded in that stock-quarter is a net buyer, and zero if he is a net

seller. The independent variable is the fraction of money managers active in that

stock in that quarter who were buyers (excluding the randomly-chosen money

manager whose behavior we are trying to explain). The slope coefficient in this

regression is 0.05 (t = 13.Q but more interestingly, the R-squared is only 0.7%.

indicating that. in a cross-section, less than 1% of an individual money man-

ager’s behavior in a stock can be explained by the aggregate behavior of other

money managers in that stock. In sum, the money managers in our sample do

not seem to herd very much; most likely, they use a variety of trading styles that

result, on average, in uncorrelated trading decisions.

4.3. Further results

We have established so far that, on average, there does not seem to be much

herding in individual stocks in our sample. This does not preclude the possibility

of more extensive herding in certain types of stocks, such as stocks of a particu-

lar size or performance record. Institutions might also be more apt to herd in

industry groups as opposed to individual stocks. Finally, herding may be more

prevalent among subgroups of pension fund managers than in the aggregate.

These possibilities are explored below.

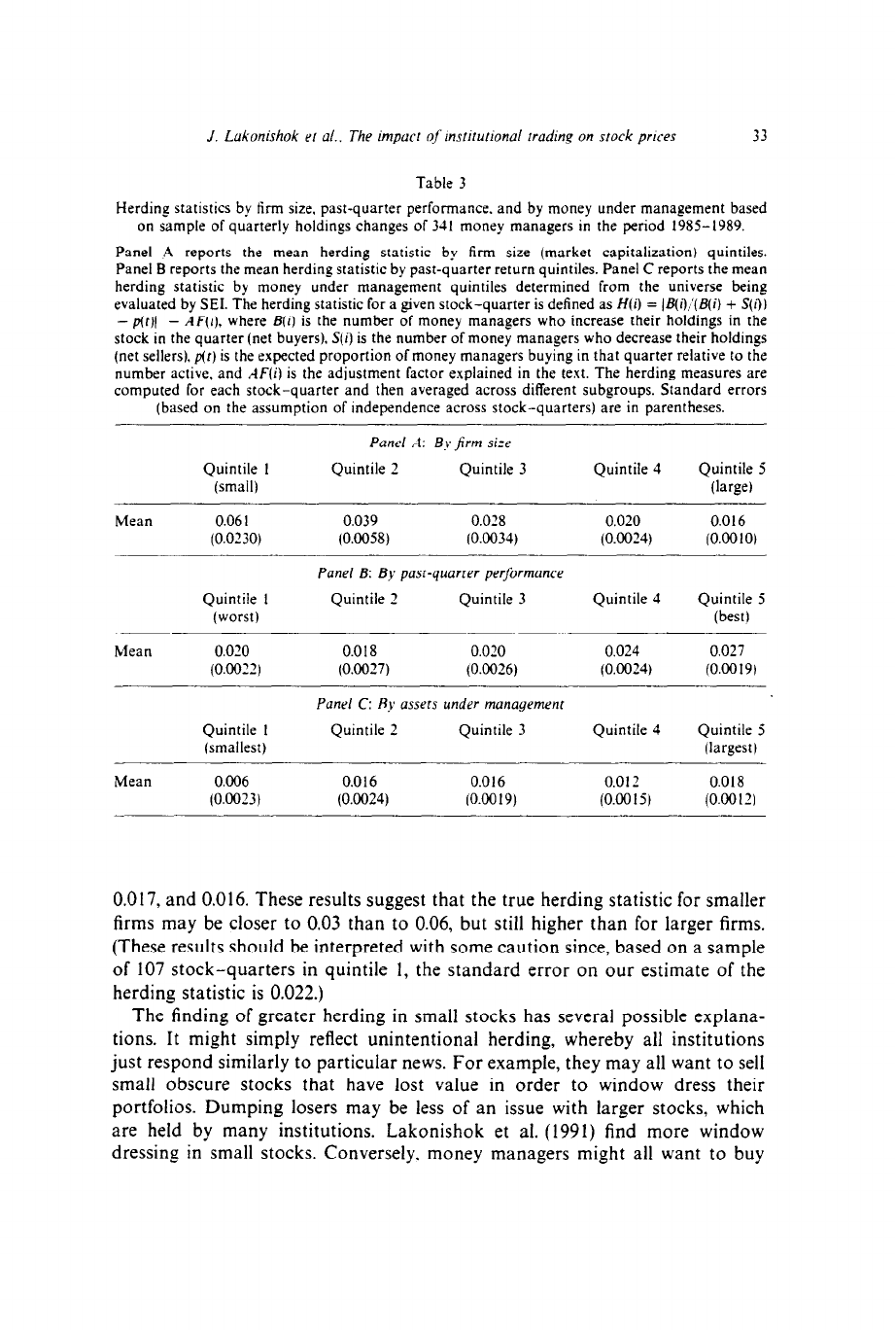

Panel A of table 3 shows herding by stock size. The stocks in which the money

managers were active in a given quarter were assigned into size quintiles. The

cut-off points for the size quintiles were determined from the universe of NYSE

and AMEX stocks and updated quarterly. Herding was then examined within

each of the size groups. The results reveal more herding by institutional inves-

tors in small stocks than in large stocks; the observed relationship is monotonic

in size. For the smallest quintile stocks, our herding measure is 6.1%, while for

the largest stocks it is only 1.6%.

There is some reason to believe that the herding statistic for smaller firms is

upward-biased. If the firm is either issuing or repurchasing shares from the

public, we should observe herding in any random sample of investors, simply

because the issuing (repurchasing) firm is the unobserved other party to the

transaction. But this does not really amount to meaningful correlation among

the strategies of investors.

In small firms for which we observe fewer normal trades to start with,

repurchase and issue activity may be a larger fraction of the trading activity we

observe. The data support this view. When we look at the subsample consisting

of only those stock-quarters in which the number of outstanding shares of the

firm did not change either way by more than 2%, we find noticeably less herding

for the smaller firms and no appreciable difference for the larger firms relative to

the results for the full sample. The herding statistics for this subsample of

stock-quarters for quintiles 1 through 5 respectively are: 0.028, 0.031, 0.023,

J. Lukonishok ri al.. The impacr of mstitu/ional rrading on stock prwes 33

Table 3

Herding statistics by lirrn size, past-quarter performance. and by money under management based

on sample of quarterly holdings changes of 341 money managers in the period 1985-1989.

Panel A reports the mean herding statistic by firm size (market capitalization) quintiles.

Panel B reports the mean herding statistic by past-quarter return quintiles. Panel C reports the mean

herding statistic by money under management quintiles determined from the universe being

evaluated by SEI. The herding statistic for a given stock-quarter is defined as H(i) = jB(i)j’(B(i) + S(I))

- p(t)1 - AQi), where B(i) is the number of money managers who increase their holdings in the

stock in the quarter (net buyers). S(i) is the number of money managers who decrease their holdings

(net sellers), p(r) is the expected proportion of money managers buying in that quarter relative to the

number active. and Af(i) is the adjustment factor explained in the text. The herding measures are

computed for each stock-quarter and then averaged across different subgroups. Standard errors

(based on the assumption of independence across stock-quarters) are in parentheses.

Quintile I

(small)

Panel A: B~firm si:e

Quintile 2 Quintile 3 Quintile 4

Quintile 5

(large)

Mean 0.06 I 0.039 0.028

0.020 0.016

(0.0230) (0.0058)

(0.0034) (0.0024)

(0.0010)

Quintile I

(worst)

Panel B: By past-quarter performance

Quintile 2

Quintile 3

Quintile 4 Quintile 5

(best)

Mean

0.020

0.018 0.020 0.024

0.027

(0.0022) (0.0027)

(0.0026)

(0.0024) (0.0019)

Quintile I

(smallest)

Panel C: Ay assets under management

Quintile 2 Quintile 3 Quintile 4 Quintile 5

(largest)

Mean

0.006 0.016 0.016 0.012 0.018

(0.0023) (0.0024) (0.0019) (0.00 15) (0.0012)

0.017, and 0.016. These results suggest that the true herding statistic for smaller

firms may be closer to 0.03 than to 0.06, but still higher than for larger firms.

(These results should be interpreted with some caution since, based on a sample

of 107 stock-quarters in quintile 1, the standard error on our estimate of the

herding statistic is 0.022.)

The finding of greater herding in small stocks has several possible explana-

tions. It might simply reflect unintentional herding, whereby all institutions

just respond similarly to particular news. For example, they may all want to sell

small obscure stocks that have lost value in order to window dress their

portfolios. Dumping losers may be less of an issue with larger stocks, which

are held by many institutions. Lakonishok et al. (1991) find more window

dressing in small stocks. Conversely. money managers might all want to buy

34 J. Lukonuhok er al., The impucr of‘ rns~iturional rrading on stock prices

a well-performing small stock because higher market capitalization increases the

stock’s liquidity and coverage by analysts.

Intentional herding should also be more prevalent in small stocks. There is

less public information about these stocks, and, therefore, managers are much

more likely to pay attention to each others’ behavior and make decisions based

on the trades of others in these stocks. This view of herding is consistent with

Banerjee’s (1992) idea that herding might result from rational inference under

very limited information. The result of greater herding in small stocks is also

consistent with Scharfstein and Stein’s (1990) agency interpretation of inten-

tional herding: fund managers may sell a small stock that other managers sell in

order to avoid embarrassment, but holding onto IBM when others sell it is

probably acceptable.

We also examine herding conditional on past performance of the stocks.

At the beginning of every quarter, we divide the universe of NYSE and

AMEX stocks into past-quarter performance quintiles. Stocks in which the

money managers traded were then assigned into these quintiles, and herding

measures computed for each group. The results are in panel B of table 3.

Herding does not seem to depend on past stock performance. At most, there

is some weak indication of slightly more herding in better-performing

stocks.

One might argue that herding should be more pronounced within certain

industry groups of stocks, such as technology stocks, whose cash flows are more

uncertain. For example, one might expect to observe more herding in Genentech

than in a less-glamorous stock like General Motors. To test this hypothesis, we

divide the stocks in our sample into eleven broad industry groupings, provided

to us by SEI, and compute our herding measure for each group. Again. we do

not find much herding in any group. The measure of herding within various

industry groups ranged between 0.029 and 0.015. There is no industry with an

unusually large degree of herding.

Another hypothesis is that money managers herd in their portfolio allocations

across industries rather than across individual stocks. For example, when

money managers are ‘excited’ about computer stocks, one of them might buy

IBM, another might buy Apple Computer, and a third might buy COMPAQ,

leading to significant herding at an industry but not a firm level. To test this

hypothesis, we look at the 54 two-digit SIC industries with at least ten stocks

traded in our sample in each quarter. For each money manager, and for each

‘industry-quarter’, we compute the dollar purchases and dollar sales. A value of

one was assigned to a money manager if he was a net buyer and zero if he was

a net seller. For each industry-quarter, then, we had the number of buyers and

the number of sellers, and could compute our herding measure while treating the

whole industry as if it were a single stock. This calculation produced a herding

measure of 0.013, suggesting even less herding at the industry level than at the

individual stock level.

J. Lukonishok et al.. Thr impact of insrirurional trading on stock prices 35

A final issue is the possibility of herding among subsets of money managers.

One alternative is that money managers with a similar amount of money under

management herd with each other, on the theory that similarly-sized money

managers are in more direct competition for fund sponsors. Accordingly, we

divide our money managers into quintiles each year by asset size under manage-

ment, and compute our measure of herding within manager-size quintiles. Panel

C of table 3 presents the results. There is less herding among the smallest

managers than among the largest managers, but neither group herds a lot. Like

the evidence on the subgroups of stocks and industries, this evidence on

subgroups of money managers reveals little herding.

We conclude with an important caveat. It is possible that while there is very

little herding in individual stocks and industries, there are times when money

managers simultaneously move into stocks as a whole or move out of stocks as

a whole. Since our data set contains only all-equity funds, we cannot examine

this type of herding.

5. Feedback strategies

At any level of herding, institutional investors have more potential to destabil-

ize asset prices if they follow strong positive-feedback strategies. So far, our

analysis has been based on a count of money managers, which is the right

measure of herding, and not on the amount of excess demand. From the point of

view of destabilization of prices, however, the relevant variable is excess de-

mand. We therefore compute the current quarter’s net buying (aggregated

across all money managers in a given stock) conditional on the past quarter’s

and on the past year’s stock performance.

We use two measures of excess demand in a quarter, Dratio (dollar ratio) and

Nratio (numbers ratio). For a given stock-quarter, i, Dratio is defined as

Dratio(i) = [$buys(i) - Ssells(i)]/[%buys(i) + Ssells(i)] ,

(2)

where $buys(i) is the total dollar increases by all money managers in the given

stock-quarter (evaluated at the average price during the quarter) and &ells(i) is

similarly defined as the total dollar decreases in holdings. Similarly, Nratio is

defined as

Nratio(i) = #buys(i)/ # actice ,

(3)

where #buys(i) is the number of money managers increasing the holding of the

stock in quarter i and #active is the number of money managers changing

their holdings. In the results presented below, Dratios and Nrarios are simple

averages taken over all stock-quarters in a given group. We use two measures

36 J. Lakonishok t-1 al., The impact 01‘ insrirutional trading on stock pries

because they might, in principle, yield different results. For example, most

managers might be engaged in positive-feedback trading, but the negative-

feedback managers might be making the larger trades, in which case trend

chasing would show up in the Nratio but not in the Dratio.

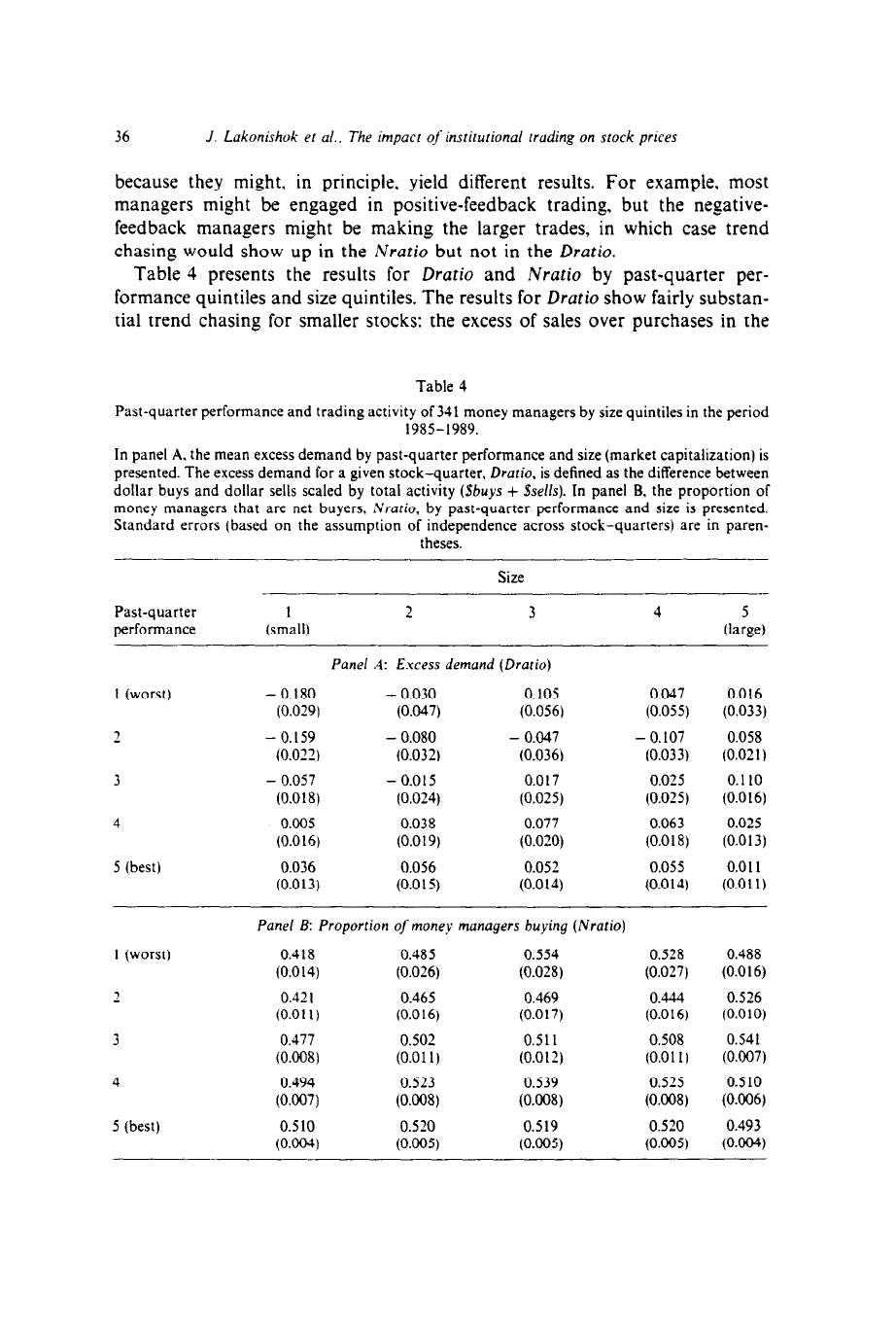

Table 4 presents the results for Dratio and Nratio by past-quarter per-

formance quintiles and size quintiles. The results for Dratio show fairly substan-

tial trend chasing for smaller stocks: the excess of sales over purchases in the

Table 4

Past-quarter performance and trading activity of 341 money managers by size quintiles in the period

1985-1989.

In panel A, the mean excess demand by past-quarter performance and size (market capitalization) is

presented. The excess demand for a given stock-quarter, Dratio, is defined as the difference between

dollar buys and dollar sells scaled by total activity @buys + Ssells). In panel B. the proportion of

money managers that are net buyers, Nrario, by past-quarter performance and size is presented.

Standard errors (based on the assumption of independence across stock-quarters) are in paren-

theses.

Size

Past-quarter

performance (smlall)

2 3

4 5

(large)

I (worst) - 0.180

(0.029)

2 - 0.159

(0.022)

3 - 0.057

(0.018)

4 - 0.005

(0.016)

5 (best) 0.036

(0.013)

Panel A: E.xcess demand (Dratio)

- 0.030

(0.047)

- 0.080

(0.032)

- 0.015

(0.024)

0.038

(0.019)

0.056

(0.015)

0.105

(0.056)

- 0.047

(0.036)

0.017

(0.025)

0.077

(0.020)

0.052

(0.014)

0.047

(0.055)

- 0.107

(0.033)

0.025

(0.025)

0.063

(0.018)

0.055

(0.014)

0.016

(0.033)

0.058

(0.021)

0.110

(0.016)

0.025

(0.013)

0.011

(0.01 I)

Pane/ B: Proportion of money managers buying (Nratio)

1 (worst) 0.418 0.485 0.554 0.528 0.488

(0.014)

(0.026) (0.028) (0.027)

(0.016)

2 0.42 I 0.465 0.469 0.444 0.526

(0.01 I) (0.016) (0.017) (0.016)

(0.010)

3 0.477 0.502 0.511 0.508 0.541

(0.008) (0.011) (0.012)

(0.011)

(0.007)

4 0.494 0.523 0.539 0.525 0.510

(0.007)

(0.008)

(0.008) (0.008)

(0.006)

5 (best) 0.510 0.520 0.519 0.520 0.493

(0.004)

(0.005) (0.005) (0.005)

(0.004)

J. Lakonishok et ul.. The impact of inslirurional wading on srock prices 37

worst-performing smallest stocks is 18% of total value traded, whereas the

excess of purchases over sales among best-performing smallest stocks is 3.6%.

A similar pattern is also observed in the second-smallest size category. More-

over, in both of these size quintiles, excess demand is monotonically increasing

in performance. As we move to larger stocks, the relationship between excess

demand and past performance disappears. Among the largest quintile stocks,

where increases in holdings always exceed decreases, there is no evidence

whatsoever of positive-feedback trading. The results thus reveal positive-feed-

back trading for smaller but not for larger stocks. Aggregating across all size

groups, we do not see any evidence of positive-feedback trading on average,

because of the concentration of trades in larger stocks.

The results for Nratio also point to positive-feedback trading in small but not

in large stocks. In small stocks, only 42% of money managers changing their

holdings of the worst performers are buyers, whereas 51% of the money

managers changing their holdings of the best performers are buyers. Within this

size quintile, Nratio increases monotonically with past performance. Positive-

feedback trading is still evident in the second size quintile, but disappears in

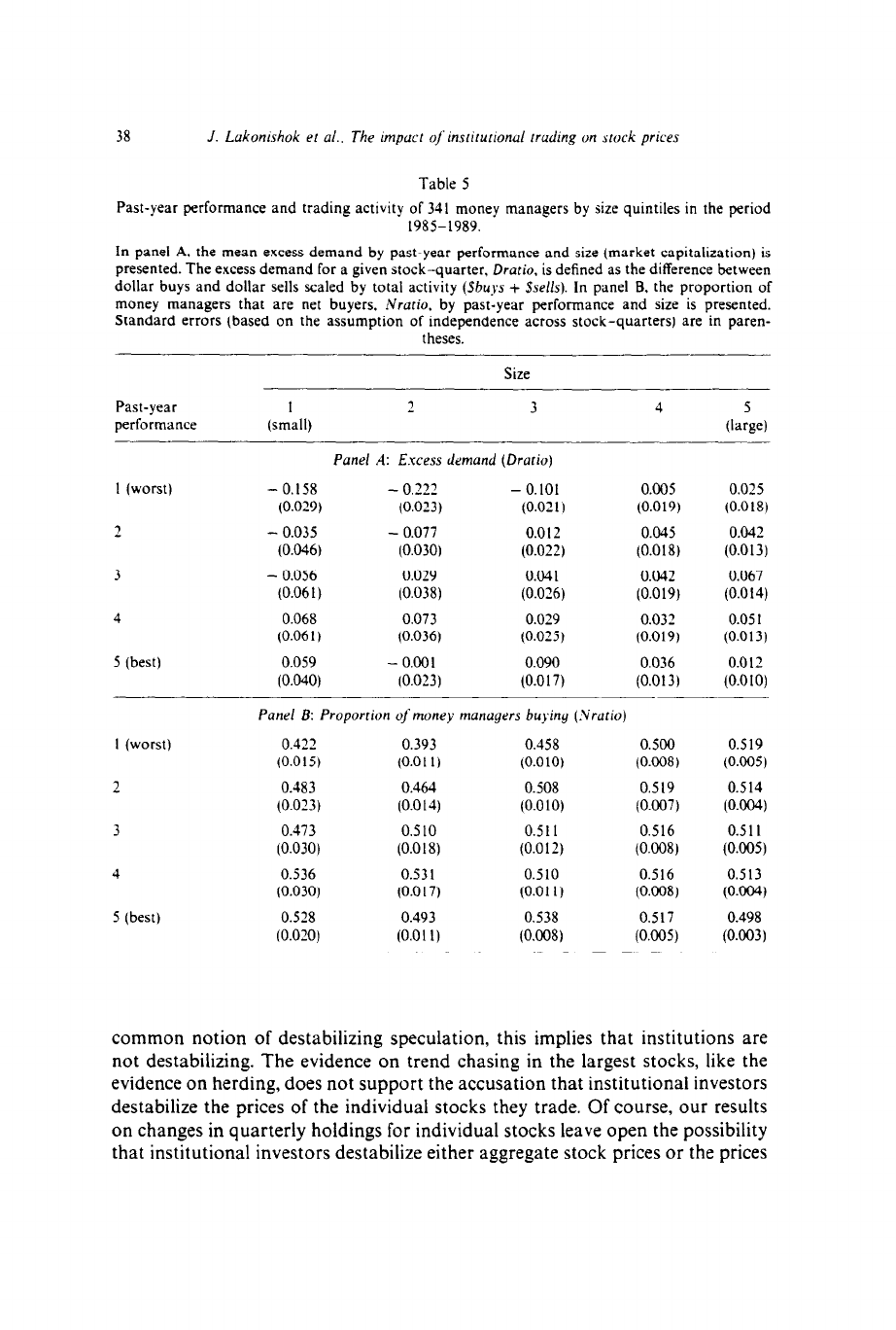

larger quintiles. Finally, table 5 reports the results on trading as a function of

past-year performance and size. Consistent with the results in table 4, there is

evidence of positive-feedback trading in small but not in large stocks.

The finding of positive-feedback trading in smaller stocks is intriguing. Per-

haps the most obvious explanation is window dressing: money managers dump

losers among small stocks to dress up their portfolios. The strategy of dumping

small stock losers makes sense if sponsors are less sensitive to holdings of poorly-

performing blue chips than to holdings of poorly-performing unknown stocks.

The observed positive-feedback strategies in smaller stocks might also be

a consequence of institutional practices and constraints. For example, past

losers dumped by money managers might be firms who stopped dividend

payments. Some institutions might be prohibited from holding such stocks,

Alternatively, money managers might restrict their holdings of small-capitaliza-

tion or illiquid stocks. These factors create a positive correlation between past

returns and institutional excess demand. In any case, whether we are finding

evidence of behavioral strategies, agency problems, or of simple institutional

restrictions, positive-feedback trading might have an impact on share prices of

small stocks.

Interestingly, our result for small stocks is supportive of the evidence that

overreaction identified by De Bondt and Thaler (1985) is concentrated in small

stocks [Chopra, Lakonishok, and Ritter (1992)]. If institutional investors change

their demand for these stocks in response to extreme performance, and if their

demand affects prices in the short run, we would expect to observe overreaction.

The preferred holdings of institutional investors are large stocks, however,

which is where their trading strategies are probably most important. For these

stocks, we see no evidence of positive-feedback trading. Under the most

38 J. Lakomshok el al.. The unpuct of insri~lonul rrading on stock prices

Table 5

Past-year performance and trading activity of 341 money managers by size quintiles in the period

1985-1989.

In panel A, the mean excess demand by past-year performance and size (market capitalization) is

presented. The excess demand for a given stock-quarter, Dratio, is defined as the difference between

dollar buys and dollar sells scaled by total activity (Sbuys + Sells). In panel B. the proportion of

money managers that are net buyers, Nrario, by past-year performance and size is presented.

Standard errors (based on the assumption of independence across stock-quarters) are in paren-

theses.

Size

Past-year

performance

1

(small)

2 3 4

5

(large)

Panel A: Excess demand (Drario)

I (worst) - 0.158 - 0.222

- 0.101 0.005

(0.029)

(0.023)

(0.021)

(0.019)

2 - 0.035 - 0.077

0.012

0.045

(0.046)

(0.030)

(0.022) (0.018)

3 - 0.056 0.029

0.041 0.042

(0.06 1)

(0.038)

(0.026) (0.019)

4 0.068 0.073

0.029 0.032

(0.06 I )

(0.036)

(0.025)

(0.019)

5 (best) 0.059 - 0.001

0.090 0.036

(0.040) (0.023) (0.0 17) (0.013)

0.025

(0.018)

0.042

(0.013)

0.067

(0.014)

0.05 I

(0.013)

0.012

(0.010)

Panel E: Proportion of money manugers buying (.Vrutio)

I (worst) 0.422 0.393

0.458 0.500

(0.015) (0.01 I)

(0.010) (0.008 )

2 0.483 0.464

0.508 0.519

(0.023) (0.014) (0.0 IO) (0.007)

3 0.473 0.510

0.511 0.516

(0.030) (0.018)

(0.012) (0.008)

4 0.536 0.531

0.510 0.516

(0.030) (0.017)

(0.01 I) (0.008)

5 (best) 0.528 0.493

0.538 0.517

(0.020)

(0.01 I)

(0.008) (0.005)

0.519

(0.005)

0.514

(O.@w

0.511

(0.005)

0.513

(ww

0.498

(0.003)

common notion of destabilizing speculation, this implies that institutions are

not destabilizing. The evidence on trend chasing in the largest stocks, like the

evidence on herding, does not support the accusation that institutional investors

destabilize the prices of the individual stocks they trade. Of course, our results

on changes in quarterly holdings for individual stocks leave open the possibility

that institutional investors destabilize either aggregate stock prices or the prices

J. Lakunishok et ~1.. The mpucr of m.srrrr&md rruding on stock prices

39

of individual stocks day-to-day or week-to-week without much affecting the

quarterly time series of stock prices.

6. Institutional excess demand and contemporaneous price movements

Thus far, we have found little evidence that institutions destabilize stock

prices through either herding or positive-feedback trading. In this section, we

analyze the direct relationship between demand for stocks by our money

managers and contemporaneous stock returns.

Of course, even if institutions affect prices, they might move them toward,

rather than away from, fundamentals. More importantly, our data set is not

ideal for analyzing the impact of institutional demand on prices. Our quarterly

data does not enable us to distinguish between the impact of trades on prices

and within-quarter trading strategies that respond to within-quarter price

moves. For example, if we found that a particular group of stocks that institu-

tions bought in a quarter rose in price in that quarter, it could be evidence either

of positive-feedback trading in response to short-term price moves, or of the

effect of institutional trading on prices, or even of both effects operating at the

same time. In interpreting the results presented below, it is crucial to recognize

this limitation of quarterly data.

Table 6 presents some basic statistics on the relationship between institu-

tional demand for stocks in a quarter and size-adjusted excess returns in that

quarter, computed by deducting from the quarterly buy-and-hold stock return

the return on an equally-weighted quarterly buy-and-hold portfolio of the same

size decile. The cut-off points for size deciles were updated quarterly. In each

quarter, we divided stocks traded by our money managers into two broad

categories: stocks of which in aggregate they were net buyers and those of which

in aggregate they were net sellers. Each category is, in turn, divided into three

groups depending on the size of the imbalance between dollar purchases and

dollar sales (scaled by market capitalization). Small excess refers to the bottom

quartile of stocks in terms of dollar excess demand, medium excess to the middle

half, and large excess to the quartile of firms with largest excess demand in dollar

terms. The same groups are defined for firms for which sales exceed purchases.

The results in table 6 show a statistically-significant size-adjusted excess

return of 1.8% per quarter for firms that were bought, on net, by our money

managers. This result may reflect a price impact of institutional trades, which

might, but does not have to be destabilizing. The positive excess return could

also result from positive-feedback trading in response to recent price increases,

without causing these increases. When we look at the subcategories of net

buying by the magnitude of our institutions’ excess demand, we find that the

abnormal return is actually somewhat smaller for large excess demand cases

than for cases with small excess demand.

40

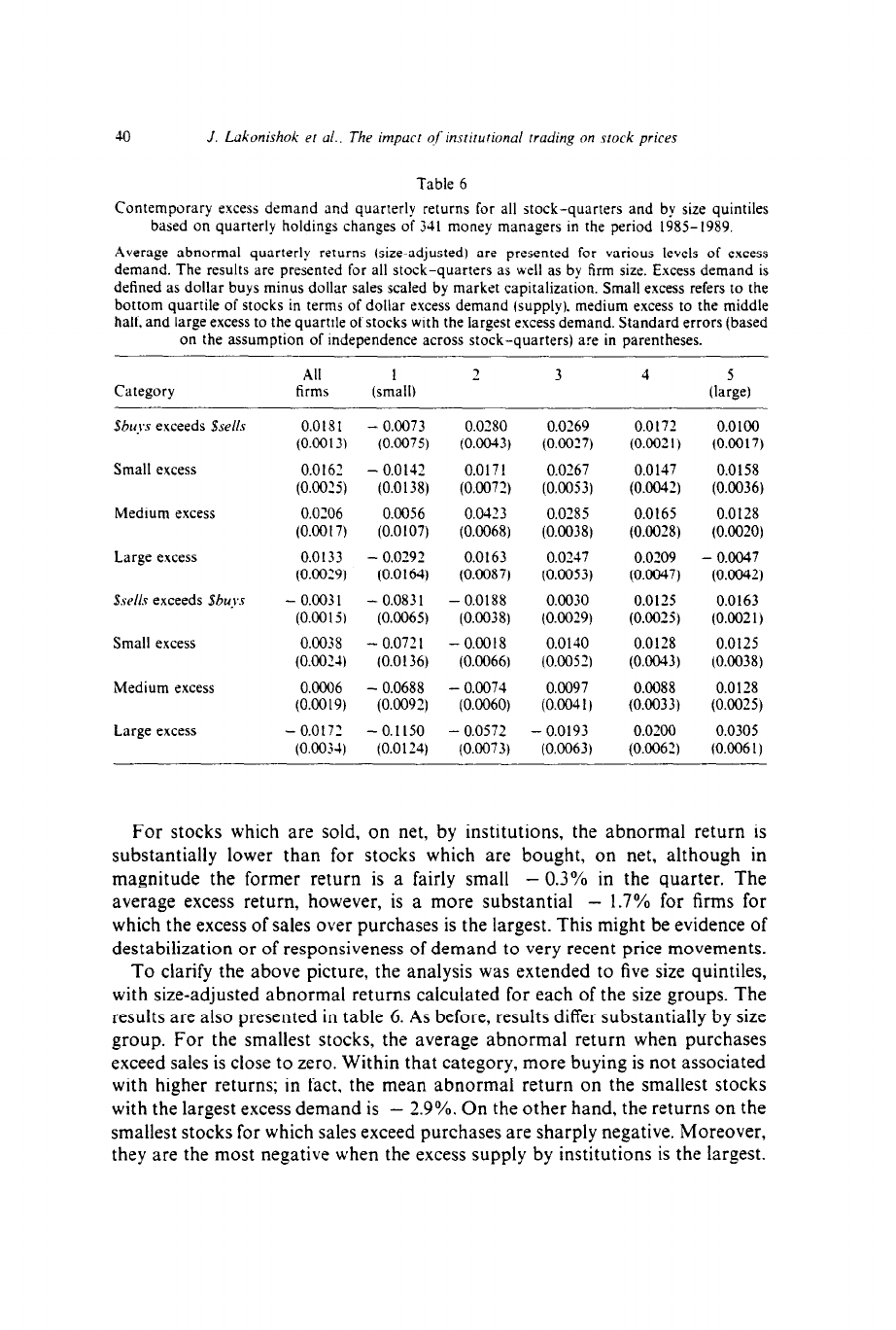

J. Lakonishok er ul.. The impucr q/ mtirutional trading on stock prices

Table 6

Contemporary excess demand and quarterly returns for all stock-quarters and by size quintiles

based on quarterly holdings changes of 341 money managers in the period 1985-1989.

Average abnormal quarterly returns (size-adjusted) are presented for various levels of excess

demand. The results are presented for all stock-quarters as well as by firm size. Excess demand is

defined as dollar buys minus dollar sales scaled by market capitalization. Small excess refers to the

bottom quartile of stocks in terms of dollar excess demand (supply). medium excess to the middle

half. and large excess to the quartile of stocks with the largest excess demand. Standard errors (based

on the assumption of independence across stock-quarters) are in parentheses.

Category

All 1

2 3

4

5

firms

(small)

(large)

SbtrJs exceeds &ells

Small excess

Medium excess

Large excess

dsel1.s exceeds Sbu.r.r

Small excess

Medium excess

Large excess

0.0181

(0.0013)

0.0162

(0.0025)

0.0206

(0.0017)

0.0133

(0.0029)

- 0.003 I

(0.0015)

0.0038

(0.002~)

O.OCO6

(0.0019)

- 0.0172

(0.003-1)

- 0.0073

(0.007s)

- 0.0142

(0.0138)

0.0056

(0.0107)

- 0.0292

(0.0164)

0.0280

(0.0043)

0.0171

(0.0072)

0.0423

(0.0068)

0.0163

(0.0087)

- 0.083 I - 0.0188

(0.0065) (0.0038)

- 0.072 I

(0.0 136)

- 0.0018

(0.0066)

- 0.0688

(0.0092)

- 0.1150

(0.0124)

- 0.0074

(0.0060)

- 0.0572

(0.0073)

0.0269

(0.0027)

0.0267

(0.0053)

0.0285

(0.0038)

0.0247

(0.0053)

0.0030

(0.0029)

0.0140

(0.0052)

0.0097

(0.004 I)

- 0.0193

(0.0063)

0.0172

(0.002 I)

0.0147

(0.0042)

0.0165

(0.0028)

0.0209

(0.0047)

0.0125

(0.0025)

0.0128

(00043)

0.0088

(0.0033)

0.0200

(0.0062)

0.0100

(0.0017)

0.0158

(0.0036)

0.0128

(0.0020)

- 0.0047

(0.0042)

0.0163

(0.0021)

0.0125

(0.0038)

0.0 I28

(0.0025)

0.0305

(0.006 I)

For stocks which are sold. on net, by institutions, the abnormal return is

substantially lower than for stocks which are bought, on net, although in

magnitude the former return is a fairly small - 0.3% in the quarter. The

average excess return, however, is a more substantial - 1.7% for firms for

which the excess of sales over purchases is the largest. This might be evidence of

destabilization or of responsiveness of demand to very recent price movements.

To clarify the above picture, the analysis was extended to five size quintiles,

with size-adjusted abnormal returns calculated for each of the size groups. The

results are also presented in table 6. As before, results differ substantially by size

group. For the smallest stocks, the average abnormal return when purchases

exceed sales is close to zero. Within that category, more buying is not associated

with higher returns; in fact, the mean abnormal return on the smallest stocks

with the largest excess demand is - 2.9%. On the other hand, the returns on the

smallest stocks for which sales exceed purchases are sharply negative. Moreover,

they are the most negative when the excess supply by institutions is the largest.

J. Lakonishok et d.. The impact of institutional truding on stock prices 41

This evidence suggests that, within the smallest stocks, either institutions sell

recent losers, or they depress the prices of stocks they sell.

The results for the second size quintile are consistent with either intraquarter

positive-feedback trading or the direct impact of institutional trades on share

prices. The mean abnormal return for stocks for which purchases exceed sales is

2.8%, and the mean return for stocks for which sales exceed purchases is

- 1.8%. These returns are roughly monotonic in the magnitude of excess

demand. In the third size quintile, we again see positive returns for stocks for

which purchases exceed sales, but negative returns only for stocks for which

the excess of sales over purchases is the largest. Again, however, there is a

rough monotonic relationship between excess demand and abnormal returns,

indicating either price pressure by institutions or intraquarter positive-feedback

trading.

Even these rough relationships, however, disappear in the two largest size

quintiles, in which institutional trading is concentrated. In the fourth quintile,

both the stocks which are bought, on net, and sold, on net, earn a positive excess

return. Moreover, stocks for which the excess supply by institutions is the largest

have an abnormal return of 2.0%. In the largest quintile, stocks which institu-

tions buy, on net, have lower abnormal returns than stocks which institutions

sell, on net, which seems more consistent with stabilizing negative-feedback

trading. Indeed, stocks with the largest excess demand have a return of - OS%,

and stocks with the largest excess supply have a return of 3.1%. What little

support we saw for positive-feedback trading or price pressure from institutions

in smaller quintiles disappears in the largest two quintiles.

In sum, the results of this section are the least conclusive. Stocks that

institutions buy, on net, have higher contemporaneous abnormal returns than

stocks that institutions sell, on net.’ However, a closer inspection reveals that

‘In tables 4 and 5. we explored the relation between past returns and current excess demand by

money managers. In table 6, we looked at current returns and current excess demand. Another

question is: What is the relation between future returns and current excess demand? This question

has more to do with the short-run profitability of the strategies pursued by pension managers than

with the destabilization question. Friedman (1953) has argued that if prices move in one’s favor after

trading. then one has contributed to price stabilization. The problem is how to rule out strategies

that are short-run-profitable but may actually be destabilizing in the long run. This problem is

especially serious when future returns cannot be estimated very precisely o\er a long period of time.

We have examined the relationship between current excess demand and one-quarter-ahead

returns without drawing conclusions about the role of institutions in promoting price stability from

these results. The evidence. while quite mixed. suggests that pension fund trading in the smallest

three quintiles of stocks is profitable in the short run. while trading in the two largest quintiles is

neither particularly profitable or unprofitable in the short run. In other words, when pension funds

are net sellers ofsmaller stocks. future prices tend to fall over the next quarter and prices tend to rise

when the funds are net buyers. However. the magnitude of the future return differences as a function

of past excess demands is relatively small and there are also some anomalous aspects of the results.

For example, across all five quintiles. some of the most negative returns occur after large net buying

by fund managers in the previous quarter.

J. Lakonishok et al.. The impact of institutional trading on stock prices

this result is driven by the smaller stocks, particularly those in the second and

third quintiles. In the largest two quintiles, the pattern of abnormal returns for

the net buy and net sell cases is essentially identical. For the smallest quintile

stocks, when institutions are net sellers, a monotonic relationship between

gradations of excess supply and abnormal returns is observed. However, no such

relationship exists for stocks which institutions buy, on net. In light of this

evidence, the destabilizing effect of institutions in individual stocks, even if it

exists, is unlikely to be large.

7. Conclusion

This paper has presented evidence on the herding and trend-chasing behavior

of institutional money managers. For smaller stocks, we find weak evidence of

herding and somewhat stronger evidence of positive-feedback trading. However,

the evidence shows relatively little of either herding or positive-feedback trading

in the largest stocks, which constitute the bulk of most institutional holdings

and trading. There is also no consistent evidence of a significant positive

correlation between changes in institutional holdings and contemporaneous

excess returns, except again in small stocks where we may just be observing

intraquarter positive-feedback trading. We conclude that there is no solid

evidence in our data that institutional investors destabilize prices of individual

stocks. Instead, the emerging image is that institutions follow a broad range of

styles and strategies and that their trades offset each other without having

a large impact on prices. We must conclude, however, with two important

caveats. First, our results do not preclude either market-wide herding, such as

would occur if money managers followed each other in market-timing strategies,

or herding in individual stocks that only shows up when measured at shorter

time intervals such as daily or weekly. Second, our results do not rule out the

possibility of highly inelastic demands for stocks which cause relatively small

amounts of institutional herding or positive-feedback trading to have relatively

large effects on stock prices.

References

Andreassen. Paul and Alan Kraus. 1988, Judgmental prediction by extrapolation, Working paper

(Harvard University. Cambridge. MA).

Banerjee. Abhijit. 1992. A model of herd behavior, Quarterly Journal of Economics. forthcoming.

Bikhchandani. Sushil, David Hirshleifer, and Ivo Welch, 1992. A theory of fads, fashion. custom. and

cultural change as informational cascades, Journal of Political Economy, forthcoming.

Chopra. Navin. Josef Lakonishok, and Jay Ritter, 1992. Measuring abnormal returns: Do stocks

overreact?. Journal of Financial Economics 3 I, 235-268.

Cutler, David. James M. Poterba. and Lawrence H. Summers, 1990, Speculative dynamics and the

role of feedback traders. American Economic Review. Papers and Proceedings 80. 63-68.

J. Lakonishok et al.. The impact of institutional trading on stock prices

43

De Bondt. Werner and Richard Thaler, 1985. Does the stock market overreact?, Journal of Finance

40. 793-809.

De Long. J. Bradford. Andrei Shleifer. Lawrence H. Summers. and Robert J. Waldmann, 1990,

Positive feedback investment strategies and destabilizing rational speculation, Journal of Fi-

nance 45, 379-395.

Friedman. Milton, 1953. The case for floating exchange rates. in: Essays in positive economics

(L’niversity of Chicago Press. Chicago, IL).

Friend. Irwin. Marshall Blume. and Jean Crockett. 1970, Mutual funds and other institutional

investors (McGraw-Hill. New York. NY).

Kraus. Alan and Hans R. Stoll, 1972. Parallel trading by institutional investors, Journal of Financial

and Quantitative Analysis 7. 2107-2138.

Lakonishok, Josef. Andrei Shleifer, and Robert W. Vishny, 1992, The structure and performance of

the money management industry. Brookings Papers on Economic Activity: Microeconomics,

forthcoming.

Lakonishok. Josef, Andrei Shleifer, Richard Thaler, and Robert W. Vishny. 1991, Window dressing

by pension fund managers. American Economic Review, Papers and Proceedings 81, 227-231.

Scharfstein. David S. and Jeremy C. Stein, 1990, Herd behavior and investment. American Economic

Review 80, 465-479.

Schwartz. Robert and James Shapiro. 199 2. The challenge of institutionalization for the equity

market, Working paper (New York University, New York, NY).

Shiller. Robert J. and John Pound, 1989, Survey evidence on diffusion of interest and information

among invzestors. Journal of Economic Behavior and Organization IO. 47-66.