Simpson Thacher & Bartlett LLP

Leveraged Finance 101:

A Covenant Handbook

i

In 1998, at the depths of the Russian debt crisis, the leveraged finance team at

Simpson Thacher had some time on their hands, so we set about to create a

treatise on high yield debt. Having just been reissued in its seventh edition, we

believe that our The Definitive Guide to High Yield Covenants remains the

premier guide to the intricacies of high yield debt securities for issuers, bankers

and practitioners, and demand for the Definitive Guide has grown with the

market.

While the devil may be in the details in leveraged finance, we have long

recognized that a more straightforward primer is sometimes more helpful and

appropriate. In that light, we created Leveraged Finance 101: A Covenant

Handbook.

This Covenant Handbook consists of two concise guides, which cover the

covenants for each of the key leveraged finance markets. The Concise Guide to

High Yield Notes explains the key impacts of high yield covenants on the

financial and strategic flexibility of issuers, as well as the typical areas of focus for

investors in high yield debt securities. The Concise Guide to Credit Financing

provides a primer on the differences between the covenants and other key terms

found in loan financings and those in high yield debt securities.

We hope you find this Handbook to be a useful tool and, of course, if you have

any questions or would like a copy of The Definitive Guide to High Yield

Covenants, please do not hesitate to contact us at LevFin@stblaw.com. We have a

preeminent position in the leveraged finance markets and would be happy to be

of service.

The Simpson Thacher Team

PAGE 1

Concise Guide to

High Yield Notes

Introduction

This Concise Guide to High Yield Notes is meant to be exactly that — a clear overview of the

typical high yield covenant package with a focus on the basic structure and principles of the

covenants. Some readers may find it useful in preparing for a negotiation of business terms in a

high yield transaction. Others may use it as an introduction to our Standard Form and as a

prelude to digging deeper into specific provisions.

This Concise Guide to High Yield Notes is not an explanation of every term or even every

covenant that you may encounter in negotiating a high yield deal, which would have produced a

guide that was far from concise. As a result, you will find exceptions to many of the basic

provisions we describe. But even when you encounter exceptions, we think you will recognize

the basic architecture of a high yield deal that we outline in the following pages.

Organization

We have organized this Concise Guide to High Yield Notes in the following order:

• crucial concepts that we highlight to set the stage for the discussion of the covenants;

• the restricted payments covenant limiting dividends, distributions, redemptions of junior

capital and investments;

• the debt and lien covenants limiting the ability to incur unsecured and secured debt and

which, together with the restricted payments covenant, are usually the most heavily

negotiated;

• the asset sale and change of control covenants;

• covenants governing additional “plumbing” matters: transactions with affiliates, limitations

on subsidiary distributions, mergers and reporting;

• optional redemption provisions; and

• key definitions of Consolidated Net Income and Consolidated EBITDA.

The order of our guide does not follow the order in which you typically find these provisions in

an offering document or an indenture. Instead, we begin with the most negotiated covenants

and then highlight crucial concepts they illustrate through the rest of the covenant package.

PAGE 2

Crucial Concepts

A Delicate Balance

High yield covenants always seek to strike a delicate balance that requires the collaboration of

issuers with the underwriters or initial purchasers who resell the high yield notes to investors:

• On the one hand, the covenants provide protection for high yield investors against an

issuer’s overextending itself or unwisely using cash (i.e., the covenants seek to preserve

cash/assets and/or cash flow).

• On the other hand, the covenants must provide flexibility for the issuer to operate its

business and grow over the life of the notes.

In other words, the covenants protect the investors’ ability to be paid principal and interest on

the notes while preserving the issuer’s ability to run its business and grow without undue

restrictions.

Restricted and Unrestricted Subsidiaries

High yield covenant packages are focused on regulating the ability of the issuer and its

“restricted subsidiaries” to service their debt and achieve the delicate balance described above.

“Restricted Subsidiaries” are subject to the covenants, and their consolidated net income and

consolidated EBITDA are included when calculating the important ratios and baskets that are

employed in several of the covenants. Those restricted subsidiaries include both subsidiaries

that guarantee the notes and subsidiaries that do not provide guarantees.

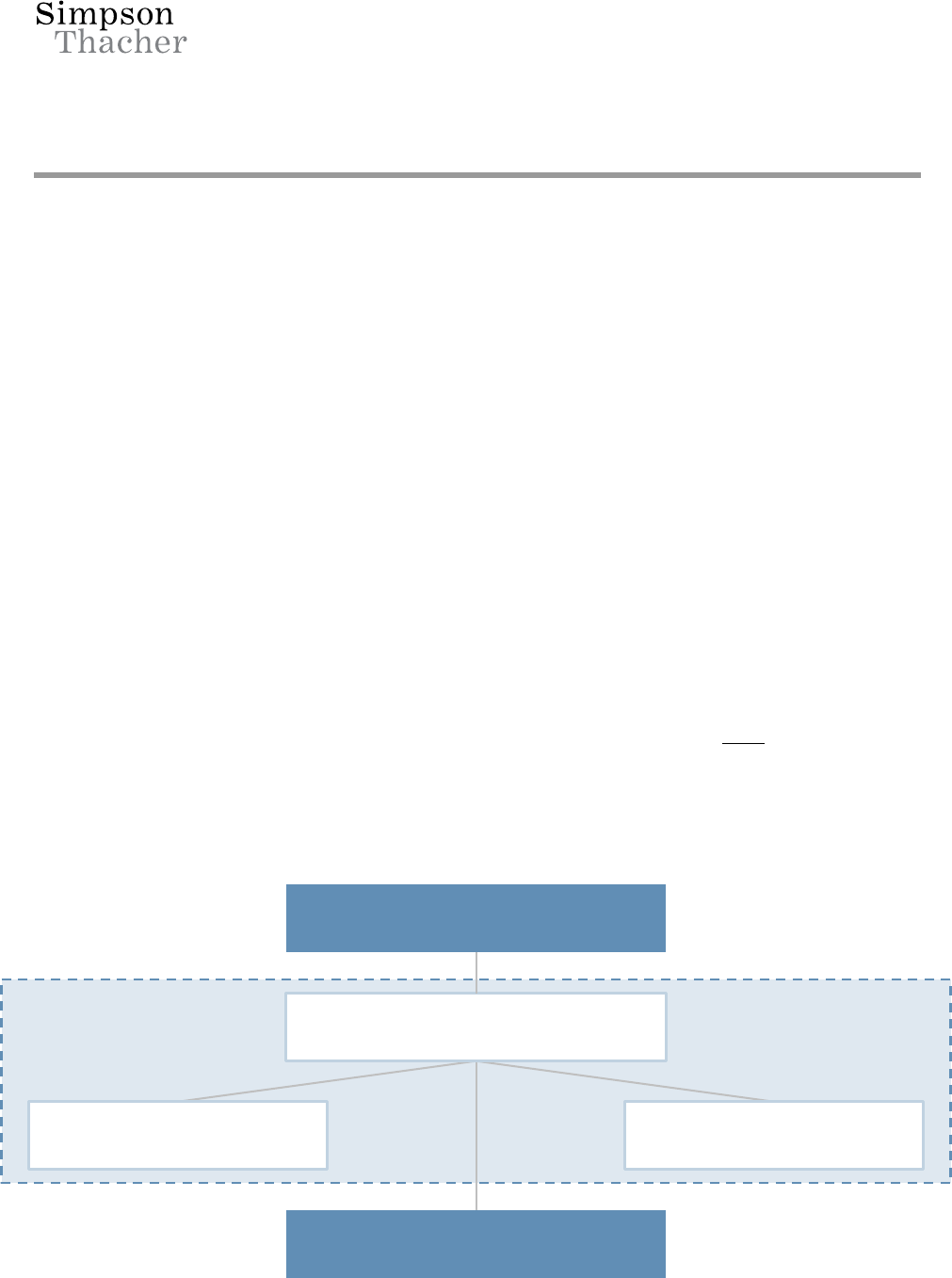

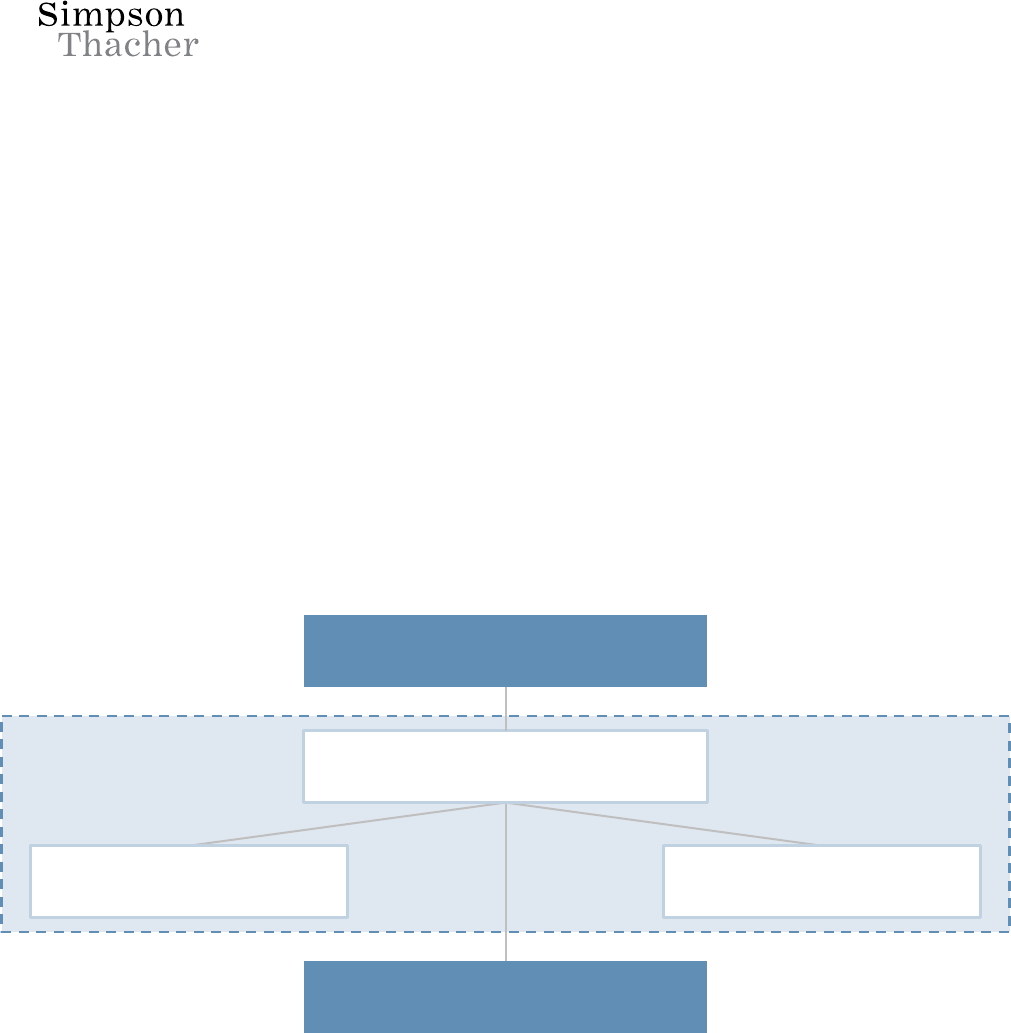

Said another way, each high yield covenant package regulates only the activities of the “credit

group,” or the entities in the “credit box” shown below.

Unrestricted Subsidiaries

Issuer

Subsidiary

Guarantors

Non-Guarantor

Restricted Subsidiaries

Credit Group

Holding Company /

Equity holders

PAGE 3

High yield covenants are flexible in permitting transactions between the issuer and its restricted

subsidiaries or among restricted subsidiaries — in many cases, whether or not those restricted

subsidiaries are guarantors or non-guarantors. In other words, there is significant flexibility

across the “restricted group.”

What high yield covenants do not reach (for the most part) are unrestricted subsidiaries, which

are subsidiaries that the issuer specifically designates as beyond the scope of the covenant

package. As a result, there are some significant implications to designating a subsidiary as

“unrestricted”:

• the issuer usually cannot count that subsidiary’s net income when it calculates consolidated

net income (and related financial metrics / ratios) unless the issuer actually receives cash

from the unrestricted subsidiary; and

• most interactions between the credit group (the issuer and its restricted subsidiaries), on

one hand, and an unrestricted subsidiary, on the other, are treated as if they were

transactions with an unrelated third party and must comply with all the covenants.

Because of these limitations, unrestricted subsidiaries are relatively rare, but you will encounter

them, for example, when a subsidiary cannot be subject to the covenants for regulatory or other

business reasons (i.e., project finance) or if an issuer intends to sell or merge a subsidiary.

Incurrence vs. Maintenance

High yield covenants are incurrence tests rather than maintenance tests. Unlike a traditional

credit agreement, which requires an issuer to meet quarterly maintenance covenants (such as

leverage ratios and interest coverage ratios), high yield covenants are usually tested only when

an issuer or a restricted subsidiary actually does something — like pay a dividend, incur debt or

grant a lien. This theme underlies almost all the covenants.

Made to Last

High yield covenants are designed to last for the entire term of the notes, which is typically

seven to ten years. High yield indentures are generally difficult and expensive to amend, and this

is a primary reason that high yield covenants are more flexible than traditional credit agreement

covenants. Credit agreement amendments are fairly common, and credit agreement covenant

packages are often designed to require a borrower to seek consent from its lenders for

noteworthy departures from its ordinary course of business.

High yield notes, however, are securities that are usually widely held, and high yield investors

traditionally do not expect to be approached for consent, except in special circumstances. In

addition, unlike the administrative agent under a typical credit agreement, the trustee under a

high yield indenture will not closely monitor or be in frequent contact with an issuer.

As a result, amending a high yield indenture requires a formal consent solicitation process that

follows an established market practice. If that consent solicitation is coupled with a tender offer

PAGE 4

for the notes, the tender offer must also follow the federal securities laws and the specific rules

of the SEC that govern tender offers.

1

With those concepts in mind, we now turn to the first covenant.

Limitation on Restricted Payments

We start with the restricted payments covenant, often called the “RP covenant,” because it goes

to the heart of the high yield covenant structure — and because it’s one of the most negotiated

covenants.

The RP covenant regulates the amount of cash and other assets that are allowed to flow out of

the “credit box” that we described in Crucial Concepts. This covenant walks a “delicate balance

between the different goals of the issuer and its investors:

• the issuer’s desire to invest in its business;

• the issuer’s desire for flexibility in managing the different equity and debt tranches of its

capital structure;

• the noteholders’ desire to preserve the issuer’s cash flow for debt service; and

• equity holders’ desire to receive dividends and other returns on their investments in the

issuer.

The RP covenant has an ambitious goal: to balance these interests in a way that gives everyone

what they want (or at least some degree of what they want) throughout the life of the notes.

To do this, the typical RP covenant first defines “restricted payments” to include:

• cash dividends and other distributions;

• the redemption or repurchase of the issuer’s capital stock;

• the redemption or repurchase of subordinated debt obligations prior to their scheduled

maturity; and

• “restricted investments,” which are investments that are not listed as “permitted

investments.”

After defining restricted payments, the typical RP covenant has three keytypes of exceptions:

• the “builder basket,” which allows the issuer to build its capacity for restricted payments

over time;

• negotiated exceptions (also referred to as “baskets”) that the issuer can use even if it hasn’t

been able to build capacity under the builder basket; and

• a list of permitted investments.

______________________________

1

We are assuming that the high yield notes are sold in several U.S. states and are subject to the U.S.

federal securities laws.

PAGE 5

The “Builder Basket”

One of the quintessential features of a high yield covenant package is the builder basket, which

reflects a simple compromise between the desires of the issuer (and its equity holders), on one

hand, and the noteholders, on the other. All of these parties are united in one goal: they want the

issuer to generate as much income and cash flow as possible. To this end, the builder basket

encourages the issuer to grow the pie for everyone and slices the pie so that half of the net

income it generates can be used for restricted payments, and the other half is reserved for the

needs of the business, including debt service.

The issuer generally can make restricted payments in an aggregate amount that includes:

• 50% of cumulative consolidated net income since the issue date, but minus 100% of any

consolidated net loss; plus

• 100% of the net cash proceeds, or the fair market value of non-cash proceeds, from the sale

or issuance of common equity or from capital contributions; plus

• the amount of debt converted into common equity; plus

• net reductions in restricted investments.

2

However, before an issuer can use the builder basket, it must be sure that (1) there is no default

under the indenture and (2) it would be able to incur $1.00 of debt under the fixed charge

coverage ratio (or leverage ratio, in a limited number of deals) described under “Limitation on

Debt” below, which is an indication of the issuer’s financial health.

A word of caution before we move on: In high yield, the financial definitions that flow through

the covenants are not always what they seem. Although the RP builder basket is based on

consolidated net income, the definition is heavily negotiated and usually excludes a number of

items. We explain these financial definitions in more detail under “Consolidated Net Income

and EBITDA.”

Key Restricted Payment Baskets

The RP covenant recognizes that issuers may need or want to make certain types of restricted

payments even if they have no capacity under the builder basket. And the covenant also permits

certain restricted payments that have no significant effect on the issuer’s ability to pay interest

and principal on the notes. Here are some of the common exceptions:

• exchanges of capital stock, redeemable stock

3

or subordinated obligations of the issuer for

capital stock of the issuer;

• refinancing of subordinated obligations with subordinated obligations;

______________________________

2

In a few industries, you will see other formulas. Largely for historical reasons, for example,

telecommunications, media and technology companies often have an RP builder based on 100% of

Adjusted EBITDA minus 1.4 times consolidated interest expense.

3

Redeemable stock (sometimes known as disqualified stock) is capital stock that is treated as debt

because it is mandatorily redeemable, convertible into debt or redeemable at the option of the holder

during the life of the notes or during the 91-day bankruptcy preference period after the notes mature.

PAGE 6

• redemptions of subordinated obligations pursuant to asset sale or change of control

covenants in other debt instruments;

• redemptions of management equity;

• for public companies, a basket for periodic dividends;

• a general restricted payments basket; and

• in many deals, an unlimited basket for restricted payments, so long as the issuer meets a

negotiated leverage ratio.

Often, the most heavily negotiated features of the RP covenant are the general restricted

payments basket, the leverage ratio-based exception (if there is one) and specific exceptions that

an issuer may request because of its particular capital structure, business or announced share

repurchases and/or dividend policy.

“Dinging the Builder”

The exceptions described above increase the issuer’s flexibility in operating its business and

managing its capital structure. Keep in mind that use of some of these exceptions “dings,” or

reduces, the builder basket, and those reductions could even cause the builder basket to be a

negative number.

This is often a negotiated point, but in general, the baskets that can be used to send cash to

equity holders, such as the general restricted payments basket, will often “ding the builder.”

Here’s an example:

Example:

Company A wants to pay a $50 dividend. It has accumulated $100 in its builder basket and

has a $50 general restricted payments basket. The RP covenant stipulates that payments

made under the $50 general restricted payments basket “ding the builder.” So if Company A

uses the general restricted payments basket to pay the dividend, its builder basket will be

reduced to $50 (as it would if the builder basket were used to pay the dividend).

Note that the permitted investments described below are not treated as restricted payments and,

therefore, never “ding the builder.”

Permitted Investments

The last component of the RP covenant is the definition of “permitted investments,” which lists

the investments that the issuer and its restricted subsidiaries can make, regardless of capacity

under the builder basket. Some of these are ordinary course investments, and others are

specifically tailored to the issuer’s business. The key permitted investments often include the

following:

• intercompany investments in the issuer or a restricted subsidiary;

• investments in a person in a similar business that becomes a restricted subsidiary or merges

into the issuer or a restricted subsidiary as a result of the investment;

PAGE 7

• investments in cash and cash equivalents;

• guarantees issued in accordance with the debt covenant;

• investments in joint ventures and unrestricted subsidiaries; and

• a general permitted investments basket.

Before we move on, it’s worth pausing for a moment on the exception that permits investments

in a person that becomes a restricted subsidiary or merges into the issuer or its restricted

subsidiaries as a result of the investment. This unassuming exception is one of the most flexible

features of high yield covenants. Through this exception, an issuer can make unlimited

acquisitions, as long as the target becomes a restricted subsidiary (or merges into the issuer or a

restricted subsidiary) and the issuer complies with the other covenants in the indenture. Unlike

many syndicated credit facilities, high yield notes do not directly regulate the size and type of

acquisitions. Instead, the high yield covenant package generally permits these acquisitions, as

long as the target joins the consolidated “credit box,” allowing the business to benefit from the

net income and cash flow it generates.

Reclassification

Some indentures include a reclassification concept that permits the issuer to divide, classify and

even retroactively reclassify its restricted payments (and in some indentures, permitted

investments) among different baskets.

Example:

Company A wants to pay a $50 dividend. Company A has $0 in its builder basket and a $50

general restricted payments basket. Company A uses its general restricted payments basket

to pay the $50 dividend, using up that basket. A year later, Company A has accumulated

$100 in its builder basket and is otherwise able to use the builder basket. Since its indenture

allows for reclassification, Company A may now reclassify the dividend payment as if it had

originally used the builder basket to pay the dividend, which would reduce the builder basket

to $50 and would give Company A access to the full $50 general restricted payments basket,

permitting it to make dividends later even if it then cannot use the builder basket.

We now move on to the second of the two most heavily negotiated covenants, the debt covenant.

Limitation on Debt

The debt covenant restricts how much debt the issuer can incur and the type of debt that it can

incur. High yield issuers often have significant debt to begin with (one of the reasons they are

high yield issuers and not investment grade issuers) and may need to incur more debt over the

life of the notes for working capital, to refinance existing debt and to grow the business.

High yield investors care very much about leverage and, when analyzing an issuer, often ask

themselves, “How much debt am I comfortable letting the company incur, and how much of that

debt can be senior to me?”

PAGE 8

It’s important to remember that the debt covenant, like other high yield covenants, is an

incurrence covenant, which means that it’s tested only when debt is incurred. This is a crucial

distinction from the maintenance covenants that you find in traditional credit agreements,

which often require the borrower to test a leverage ratio, interest coverage ratio or other ratios

every quarter. A high yield debt covenant is more flexible because there is no periodic testing of

leverage or other financial metrics — the issuer only has to worry about the debt covenant at the

time it incurs debt.

The debt covenant goes hand in hand with the lien covenant, which we will describe after this.

High yield debt covenants have two main components: the ability to incur “ratio debt” and a

series of negotiated baskets and exceptions. But first, it’s worth pausing to consider the

definition of “Debt.”

What is “Debt”?

The typical high yield debt covenant governs the incurrence of traditional debt, such as debt for

borrowed money, bonds, notes and capital leases that appear on the balance sheet. But the debt

covenant also encompasses other obligations that may not strike you as traditional “debt” of the

issuer, including:

• net hedging obligations;

• obligations of other persons that the issuer or its restricted subsidiaries guarantee or secure;

• the mandatory redemption or repurchase price of “redeemable stock” of the issuer and its

restricted subsidiaries;

4

and

• the principal amount, redemption price or liquidation preference of preferred stock of

restricted subsidiaries (or sometimes simply non-guarantor subsidiaries).

Whether or not these items appear on the balance sheet, they have the potential to become

“debt-like” obligations. Therefore, high yield covenants treat them as debt.

Ratio Debt

The “ratio debt” component of the debt covenant prohibits the issuer and its restricted

subsidiaries from incurring debt unless it meets a specified financial ratio — usually a “fixed

charge coverage ratio” of at least 2.00 to 1.00 — on a pro forma basis after giving effect to the

incurrence of the debt.

5

The fixed charge coverage ratio is typically the ratio of EBITDA for the

last four fiscal quarters to fixed charges, which includes interest expense (including capitalized

______________________________

4

As you will recall from our discussion of the RP covenant, redeemable stock is capital stock that is treated as debt

because it is mandatorily redeemable, convertible into debt or redeemable at the option of the holder during the life of

the notes or during the 91-day bankruptcy preference period after the notes mature.

5

In a few industries, you will encounter other minimum fixed charge coverage ratios like 2.25 to 1.00 or 1.75 to 1.00.

And in a few industries, you will see other formulations, such as ratio debt based on a leverage ratio (or even the

ability to use either a fixed charge coverage ratio or a leverage ratio). But in the great majority of high yield deals, a

minimum fixed charge coverage ratio of 2.00 to 1.00 is the norm.

PAGE 9

interest), dividends on redeemable stock and dividends on preferred stock of restricted

subsidiaries (or sometimes simply non-guarantor subsidiaries).

In other words, to incur ratio debt, an issuer needs to be generating enough EBITDA to more

than cover its debt service costs. But the good news for issuers is that so long as they meet the

ratio on a pro forma basis, they can incur unlimited unsecured debt.

It’s important to remember that this covenant regulates unsecured debt and that there is a

separate lien covenant that governs the granting of liens to secure debt. So if an issuer meets the

ratio, it can incur unlimited unsecured debt, but if it wants to secure that debt, it needs to

comply with the lien covenant.

But who exactly can use the ratio debt provision? This is often a negotiated point. The

traditional formulation of the provision allows only the issuer and the guarantors to incur ratio

debt. However, many deals allow the issuer and any of its restricted subsidiaries to use the

basket. In these instances, any ratio debt incurred by a non-guarantor subsidiary will be

structurally senior to the high yield notes being issued. To address this issue, there is often a

negotiated cap on ratio debt that may be incurred by a non-guarantor subsidiary, limiting the

structural subordination of the high yield notes investors’ claims under the indenture.

Key Debt Baskets

The debt covenant recognizes that issuers may need or want to incur certain types of debt even if

they cannot incur any ratio debt. Here are some of the common exceptions:

• debt under a credit facility or other Debt Facility (which we explain below), capped at a

negotiated dollar amount, borrowing base level (for ABL facilities) and/or a specified

leverage level;

• debt existing on the date of the indenture and refinancings of that debt;

• purchase money debt or capital lease obligations, capped at a negotiated dollar amount;

• acquired debt and, in some cases, debt incurred to finance an acquisition, subject to meeting

a fixed charge coverage ratio test (and often permitted if the ratio simply does not get worse

on a pro forma basis);

• foreign subsidiary or non-guarantor debt;

• a general debt basket;

• certain intercompany debt; and

• guarantees by the issuer or restricted subsidiaries of certain debt permitted under the debt

covenant.

In addition to negotiated dollar amounts, certain of the exceptions typically include “growers”

that allow the cap to increase based on a percentage of total assets, total tangible assets or,

increasingly, EBITDA for the last four fiscal quarters.

The most heavily negotiated features of the debt covenant are often the Debt Facility basket and

the general debt basket. Debt under the Debt Facility basket can be secured under the lien

covenant, so in most transactions (except a first lien notes offering secured by the same

collateral) investors know that any debt incurred under that basket will be senior to the notes.

PAGE 10

Also, the Debt Facility is usually sized to include any incremental or “accordion” credit facility

that is built into the issuer’s senior credit facilities. Investors focus on the general basket because

it is an open-ended basket that can be used for anything, and some deals also allow it to be

secured under the lien covenant.

Debt Facility Definition

Again, the definitions are critical to this covenant. The “Debt Facility” basket (also called the

“credit facility basket”) was originally designed to pick up the secured bank credit facilities that

are typically more senior in the capital structure than the high yield notes. However, most high

yield indentures these days define “Debt Facility” or “Credit Facility” to include any issuance of

debt securities, whether as a refinancing of the senior credit facilities or otherwise. So investors

now typically view the “Debt Facility” basket as a general debt basket that may be secured,

including any secured debt that may be incurred under the issuer’s senior credit facilities.

Example:

Company A has a $50 Debt Facility basket and has used that basket to draw $50 under its

credit facility. Company A wants to incur $50 of secured bonds to pay down its borrowings

under its credit facility. If the definition of “Debt Facility” picks up bonds and the lien

covenant allows those bonds to be secured, then Company A will be permitted to incur the

$50 of secured bonds and pay down the $50 of borrowings under its Debt Facility basket

without using up any other baskets.

If Company A’s credit facility were a revolving credit facility, however, Company A would not

want to use the Debt Facility basket to refinance outstanding revolving loans with secured bonds

because doing so would prevent Company A from using the Debt Facility basket to borrow under

its revolver in the future.

Reclassification

Unlike the RP covenant, where reclassification is less common, almost every indenture includes

a debt reclassification concept that permits the issuer to divide, classify and even retroactively

reclassify its incurrence of debt among different baskets.

Example:

Company A wants to incur $50 of unsecured debt. On Day 1, Company A is not able to incur

ratio debt, so it uses its $50 general debt basket to incur the debt. A month later after a new

fiscal quarter has ended, Company A is able to incur ratio debt and would have been able to

incur the $50 under the ratio. Company A may now reclassify the debt incurrence as if it had

used the ratio to incur the $50 to begin with, which frees up the $50 general debt basket for

other uses.

PAGE 11

The one consistent exception to the reclassification provision is that indentures generally do not

permit an issuer to reclassify debt under its senior credit facilities that was incurred under the

Debt Facility basket as of the closing date.

Example:

Company A has a $500 term loan incurred under a Debt Facility basket of the same size.

Even if Company A is able to incur ratio debt in the future, Company A will generally not be

allowed to reclassify debt under the term loan as ratio debt. In addition, there is a permitted

lien basket for debt incurred under the Debt Facility basket, but that is not the case for ratio

debt, which could only be secured by accessing a different permitted lien basket, if available.

Because debt incurred under the Debt Facility basket is usually effectively senior to the high

yield notes (except in a first lien notes offering secured by the same collateral), allowing the

reclassification of Debt Facility debt would permit a potentially unlimited amount of secured

debt to be incurred ahead of the high yield notes.

A Note About the Fixed Charge Coverage Ratio and Basket “Stacking”

A final note about the calculation of the fixed charge coverage ratio before we leave the debt

covenant: While you can slice and dice the baskets largely as you wish when incurring debt,

issuers need to be careful when incurring ratio debt in connection with using other debt baskets.

Example:

Company A wants to incur $100 of debt, and it has the standard ratio debt provision as well

as a $75 general debt basket. Let’s assume that there are no other debt baskets that Company

A can use to incur the new debt. Company A knows that it can incur only $80 of new debt

while satisfying the pro forma 2.00 to 1.00 fixed charge coverage ratio test (i.e., if Company A

incurs more than $80 of new debt, it will not be able to use the ratio debt provision). So

Company A asks if it can simultaneously incur $80 as ratio debt and use $20 of its general

debt basket to incur the new debt, leaving it with a $55 general debt basket. This approach

has not historically been available under a typical indenture because the fixed charge

coverage ratio calculation must be on a pro forma basis for all the debt incurred at that time.

As a result, if Company A wants to use the ratio debt provision, it must meet the 2.00 to 1.00

fixed charge coverage ratio on a pro forma basis for the incurrence of the full $100 of new

debt.

However, to address this issue, indentures increasingly include “stacking” provisions. These

provisions allow issuers to “stack” debt incurred in reliance on fixed baskets on top of debt

incurred in reliance on the ratio test when the applicable ratio would not have been satisfied

had the ratio been calculated inclusive of the fixed basket amount.

We now move to the liens covenant, which goes hand in hand with the debt covenant.

PAGE 12

Limitation on Liens

As we explained earlier, when an issuer decides to incur secured debt, it needs to comply with

both the debt covenant and the lien covenant. The lien covenant is focused on protecting the

high yield investors’ priority in the capital structure by regulating the incurrence of secured debt

that may be effectively senior to the notes and ensuring that the notes have a senior priority lien

on collateral that secures any junior debt.

In a secured notes offering, the lien covenant seeks to limit the amount of secured debt that will

compete with the secured notes for collateral. On the other hand, in a subordinated or senior

subordinated notes offering, there is typically no prohibition on incurring liens to support senior

debt. The rationale for this is that those noteholders have already agreed to a junior position in

the capital structure, and permitting liens to secure senior debt should be of little consequence

to them.

Equal and Ratable Clause

In an unsecured notes indenture, it is important to keep in mind that the lien covenant is not a

blanket prohibition on the incurrence of secured debt. The lien covenant simply prevents the

issuer and its restricted subsidiaries from encumbering assets to secure other debt unless the

notes are equally and ratably secured. Not surprisingly, a first lien secured notes indenture does

not include an equal and ratable clause because this clause would allow the potentially unlimited

dilution of the collateral that the investors are counting on to support the debt.

Key Lien Baskets

The lien covenant contains a very important exception for “Permitted Liens,” and it is here that

most of the negotiation is focused. Over the years, the laundry list of exceptions included in the

definition of “Permitted Liens” has grown, and many of these exceptions reflect ordinary course

liens that are usually not a major concern to investors. However, there are a handful of

important exceptions that include the following:

• liens incurred to secure debt under the Debt Facility basket;

• liens incurred to secure debt under the purchase money debt/capital lease basket;

• liens incurred to secure debt existing on the date of the indenture;

• a general lien basket; and

• in some transactions, liens securing additional secured debt so long as the issuer meets a pro

forma secured leverage ratio test (see below for more details).

In many deals, issuers also have the ability to secure the general debt basket and occasionally

other baskets.

Definitional Pitfalls

There are a couple of definitional items that we wanted to flag for you before moving on.

PAGE 13

The “If You Can Incur It, You Can Secure It” Pitfall

Typically, the “Permitted Lien” exception relating to the Debt Facility basket is a cross reference

to that basket. For example, the “Permitted Lien” exception may refer to “Liens securing clause

(1) of the second paragraph of the debt covenant,” which typically is the Debt Facility basket

discussed above. However, we have seen indentures, particularly in certain industries, that

permit something to the effect of “liens securing Debt Facilities.”

By eliminating the explicit cross reference to the Debt Facility basket, this slight change in

wording allows an issuer to secure any Debt Facility (which, as you remember from the

discussion of the debt covenant, usually includes capital markets offerings), including ratio debt.

Under this formulation, as long as an issuer is able to incur ratio debt that can be characterized

as a Debt Facility, it can secure that debt. In an unsecured deal, this could lead to potentially

unlimited secured debt that would be effectively senior to the notes.

Instead, investors usually want to be able to quantify the debt that may be incurred ahead of the

notes. In most cases, they will insist that the Permitted Lien exception for Debt Facilities be tied

specifically to the related exception to the debt covenant.

Secured Leverage Ratios – the Hidden “Net” and Revolving Facility Debt

In the last bullet point under “Key Lien Baskets,” we noted that some indentures allow an issuer

to incur additional secured debt so long as it meets a pro forma secured leverage ratio test.

Traditionally, this secured leverage ratio is calculated as the ratio of secured debt as of the most

recent balance sheet date to EBITDA for the last four fiscal quarters, pro forma for the

incurrence of the new debt.

However, in analyzing the provision, it is critical to work through the definitions. In some

indentures, the secured debt that is measured is limited to certain kinds of debt (the same is true

of unsecured leverage ratios, if they appear in an indenture). In other indentures, secured debt is

calculated net of cash and cash equivalents (or unrestricted cash and cash equivalents),

sometimes capped at a specified dollar amount. If the issuer’s business generates considerable

cash and there is no cap on the cash that may be “netted” from the secured leverage ratio

calculation, it may be difficult to predict the issuer’s future secured debt capacity.

To avoid a scenario in which the issuer first exhausts the capacity under the secured leverage

ratio basket and then draws down the full amount available under a revolving facility in reliance

on the Debt Facility basket (thus potentially significantly exceeding the negotiated leverage ratio

for this basket), indentures often provide that the leverage ratio is calculated assuming that all

commitments under any revolving facility have been fully drawn.

We wanted to flag these pitfalls as another reminder that the definitions in an indenture are just

as important as the text of the covenants themselves, and a few words in a definition can

sometimes have a dramatic effect on certain business terms of the indenture.

While the restricted payments and debt / liens covenants reflect the most fundamental high

yield covenants, we next turn to the covenants that may require the issuer to offer to repurchase

the notes in connection with certain changes of control and asset sales.

PAGE 14

Change of Control Covenant

This covenant is actually a put right and is often found near the beginning of the covenant

package in a section entitled “Repurchase at the Option of Holders.”

The change of control covenant requires the issuer to offer to purchase the notes from

noteholders at a price equal to 101% plus accrued and unpaid interest if a “change of control” of

the issuer occurs.

The change of control put right is a defining feature of high yield notes. The rationale for giving

investors this put right is that investors purchased the high yield notes based in part on their

comfort with the management and/or the controlling shareholder(s) of the issuer.

Of course, if the trading price of the notes increases (i.e., above 101%) after announcement of a

change of control, then holders will most likely elect not to put. In other words, if the notes trade

up, that typically means that the investors are comfortable with new management and/or the

new owner and would prefer to stay invested in the notes.

Note that the issuer’s senior secured credit agreements typically provide that a change of control

constitutes an event of default and often prohibit prepayment of other debt. As a result, when a

change of control occurs, the issuer would either repay its senior secured credit facility debt or

obtain consents from its lenders before repurchasing any high yield notes under the put.

Definition of Change of Control

Typically, a change of control is defined to occur when:

• a person or group obtains ownership of 50% or more of the voting stock of the issuer (in

certain instances, 35% in the case of widely-held public companies);

• a merger or consolidation occurs in which the equity holders of the issuer before the

transaction do not represent a majority of the equity ownership of the surviving entity;

• the issuer sells all or substantially all of its assets to any “person”; or

• the issuer adopts a plan of liquidation.

The terms “person” and “group” are meant to track the way those terms are used in determining

beneficial ownership of shares for purposes of SEC reporting requirements.

Permitted Holders

When a small group of shareholders already controls an issuer (i.e., a financial sponsor or a

founder), most indentures carve these existing shareholders out of the change of control

definition. These “permitted holders” can typically increase their stakes or buy and sell among

themselves without triggering a change of control put. High yield investors usually understand

that these shifts in ownership can occur within the permitted holder group and are more focused

on the permitted holders’ collective control of the issuer.

PAGE 15

Double Trigger Change of Control

A “double trigger” change of control put right, which is common in the investment grade world,

has increasingly been adopted by high yield issuers in recent years. In a “double trigger” change

of control put, the investor put is only triggered if there is both a change of control and a ratings

downgrade from one or more rating agencies within a specified period following the

announcement of the change of control.

A double trigger is favorable to issuers, since the issuer is not obligated to offer to repurchase the

notes if the rating agencies find that the change of control will not negatively affect the issuer’s

ratings. The double trigger concept effectively shifts to rating agencies the determination as to

whether the change of control is neutral or a positive for investors. Rather than permitting

individual noteholders to decide whether or not to put their notes based on their views of the

transaction, the double trigger provision puts rating agencies in the position of assessing the

impact of the transaction on the financial health of the issuer on behalf of investors.

Double trigger change of control provisions are more common in high yield offerings for issuers

that may be on the cusp of reaching investment grade status, such as issuers with split high

yield/investment grade ratings from the rating agencies.

Limitation on Asset Sales

The high yield asset sale covenant is a surprisingly flexible covenant designed to regulate — but

not prohibit — asset sales. This covenant may be the clearest example of high yield investors’

focus on preserving an issuer’s ability to meet its debt obligations while providing flexibility for

issuers to run their businesses and execute their strategies as they see fit over the life of the

notes.

Unlike a traditional credit agreement, high yield notes do not place strict limits on asset sales.

Instead, the high yield asset sale covenant establishes guidelines that must be followed in any

asset sale and permits the issuer to use the proceeds either to reinvest in the business (which

replenishes its asset base and maintains its ability to generate cash) or to prepay debt that ranks

senior or equal to the notes in the capital structure (which aligns the issuer’s cash flow

requirements with its smaller asset base).

Only if the issuer does not use the proceeds from asset sales in this way (which it almost always

does) is it required to offer to repurchase the high yield notes with those proceeds.

What is an Asset Sale?

Another flexible aspect of the covenant is that “asset sales” do not include every type of sale that

you might imagine. “Asset sale” is broadly defined to include any kind of transfer, sale or

disposition of assets, including issuances or sales of capital stock of subsidiaries. But to avoid

capturing unnecessary items, the definition excludes, among other things:

• intercompany sales;

• inventory sales;

• sales of obsolete equipment;

PAGE 16

• sales that are regulated by the merger covenant or that constitute a change of control; and

• the making of permitted investments or restricted payments, since those actions are

regulated by the restricted payments covenant we described above.

In addition, there is always a de minimis basket that excludes any asset disposition less than a

negotiated dollar threshold.

Asset Sale Requirements

Almost every asset sale covenant requires that (1) the issuer receive fair market value for the

assets and (2) a specified percentage (typically 75%) of the consideration be received in the form

of cash or cash equivalents. The 75% cash consideration test is generally applied to each asset

sale, but in certain indentures, the test is cumulative so that the issuer can complete an asset

sale with less than 75% cash consideration so long as the running tally of cash is 75% or more of

the total consideration from assets sales during the life of the notes. In addition, there are a

couple of interesting provisions relating to the 75% prong that are worth highlighting.

Permitted Asset Swaps

Some indentures carve out asset swaps from the 75% cash consideration prong, as long as the

swaps are at fair market value and other requirements are met. This makes sense when an issuer

is simply exchanging one asset for a substantially similar asset, especially in industries where

swaps are common.

Designated Non-Cash Consideration

Most indentures have a “designated non-cash consideration” basket that is subject to a

negotiated threshold. In other words, the issuer can receive a certain amount of non-cash

proceeds and simply designate them as cash for purposes of the asset sale covenant.

Use of Asset Sale Proceeds

Once an issuer has jumped over the hurdles we describe above, the rest of the asset sale

covenant is a fairly low bar for most issuers. Within the period allowed by the indenture (usually

365 days, although it can be longer or shorter depending on the issuer and the industry), the

issuer must either:

• prepay debt that ranks senior in right of payment (or effectively senior because it is secured

with a priority lien or, in some indentures, structurally senior because it is incurred at a non-

guarantor subsidiary) to the notes;

• prepay the notes (or other pari passu debt as long as it prepays the notes equally and

ratably); or

• reinvest in assets, other than working capital assets, that are useful in its business, which can

include capital expenditures and acquisitions.

Traditional senior secured credit agreements require that net proceeds of asset sales be applied

to prepay senior secured debt, so the high yield asset sale covenant allows an issuer to comply

with its senior secured credit agreements — or even prepay its senior-ranking debt voluntarily.

But if the issuer has cash left over, beyond prepaying the notes through open market purchases

PAGE 17

or otherwise, the asset sale covenant provides a great deal of flexibility to invest the cash in its

business, especially since high yield issuers that are growing their businesses often have

significant capital expenditure programs and frequently undertake acquisitions. The covenant is

also flexible enough to permit issuers to temporarily pay down revolving loan borrowings and

later use an equivalent amount of cash to reinvest in the business.

Asset Sale Offers

If an issuer is unable to apply the net proceeds of an asset sale in the time allowed, it must then

make an offer to acquire notes at par plus accrued and unpaid interest once those excess

proceeds reach a negotiated threshold. If the offer is oversubscribed, then the issuer purchases

the notes on a pro rata basis. If it’s undersubscribed, then the issuer can use the remainder for

general corporate purposes, and the excess proceeds amount is reset to zero.

All this means that very few asset sale offers occur in practice. Because most issuers use the

proceeds either to delever or to reinvest in their business, the reality is that the key components

of this covenant are the fair market value and 75% cash consideration requirements. But high

yield investors take comfort in knowing that the proceeds cannot automatically be used for

general corporate purposes or to pay dividends without first complying with the covenant.

We next turn to the remaining key covenants, which govern an array of activities of a high yield

issuer, such as merger requirements and reporting obligations. While these covenants are often

less controversial and less negotiated, we have taken care to highlight potential pitfalls they may

present.

Limitation on Affiliate Transactions

The limitation on affiliate transactions covenant limits the issuer’s ability to enter into

transactions with affiliates unless those transactions are on terms no less favorable than would

be available for similar transactions with unrelated third parties. The covenant is designed to

prevent value from leaking out from the credit group to affiliates that are not subject to the

covenants of the indenture.

The definition of “affiliate” is typically based on the traditional SEC definition, which includes

persons that control, are controlled by or are under common control with the issuer. Sometimes

the definition specifies a beneficial ownership threshold (i.e., 10%) above which an ownership

interest is deemed to be an affiliate relationship.

Affiliate Transaction Requirements

By now, you will have noticed that high yield covenants generally limit activities but do not

prohibit them, and the affiliate transactions covenant is no exception. The covenant simply sets

thresholds above which special approval is required, and the covenant includes a number of

exceptions that are not subject to the covenant at all.

If the transaction value is more than a negotiated threshold, then the transaction generally must

be approved by a majority of the board of directors, including a majority of the independent

directors who do not have an interest in the transaction.

PAGE 18

If the transaction exceeds a higher threshold of value, traditional indentures require a fairness

opinion from an independent investment bank or appraisal firm. In recent years, however,

indentures increasingly have dispensed with this requirement, partly because both issuers and

underwriters have realized that complex or unusual affiliate transactions can be difficult and

expensive for an appraisal firm to value.

Key Exceptions

Most deals include a negotiated de minimis transaction threshold under which the issuer need

not worry about the covenant. In addition, there are several common exceptions:

• the making of restricted payments and (most or all) permitted investments, since those are

already covered by the restricted payments covenant;

• compensation and employee benefit arrangements between the issuer and its officers,

directors and consultants;

• intercompany transactions;

• ordinary course transactions with customers, suppliers and joint venture partners;

• issuance of capital stock to certain permitted holders;

• in financial sponsor deals, payment of management fees to the sponsor and engagement of

the sponsor’s affiliates for services; and

• loans to employees in the ordinary course.

In general, although there is some negotiation of the special approval thresholds we describe

above, the affiliate transactions covenant does not generate significant controversy.

Limitation on Restrictions on Distributions from Restricted

Subsidiaries

This covenant is often referred to as the “no dividend stopper” covenant. It’s an important

covenant, but it falls into the category of covenants that are usually not highly negotiated. The

covenant’s purpose is to prevent an interruption in the flow of cash from subsidiaries to the

issuer so that the issuer will enjoy the full benefit of the cash-generating capabilities of the

consolidated entity to support its debt service requirements.

The covenant governs the ability of the issuer and its restricted subsidiaries to enter into any

arrangement that would limit:

• the payment of dividends or distributions to the issuer or a restricted subsidiary;

• the making of loans or advances to the issuer or a restricted subsidiary; or

• the sale, lease or transfer of assets to the issuer or a restricted subsidiary.

PAGE 19

Key Exceptions

The covenant contains a number of exceptions for existing “dividend stoppers,” ordinary course

arrangements or arrangements that place noteholders in no worse position than existing debt

agreements. The common exceptions include:

• amendments or refinancings of existing agreements, so long as they are no more restrictive

than the existing encumbrances and restrictions;

• restrictions that have “come over” with acquired subsidiaries;

• restrictions arising by law;

• restrictions arising in merger and acquisition transactions;

• purchase money obligations restricting the transfer of acquired property; and

• restrictions in other permitted debt.

A cautionary note about this covenant is in order. Although it’s often not heavily negotiated, it’s

crucial to pay attention to the exceptions to ensure that they contain the appropriate level of

flexibility for any financing arrangements that an issuer may need to pursue over the life of the

notes. If an issuer wants the ability to incur debt at a foreign subsidiary, for example, it needs to

negotiate exceptions that would permit the restrictions on subsidiary distributions that are

embedded in a covenant package, such as customary restricted payments and lien covenants.

Reporting

The reporting covenant aims to ensure the flow of information that high yield investors need to

support trading in the notes and to monitor the performance of the issuer.

Reporting covenants can vary fairly significantly depending on whether the issuer is a public or

private company, and whether the notes were issued in an SEC-registered or private transaction.

To understand how the covenant works, we need to start with a bit of background on the

differences between selling high yield notes in (1) a public deal, (2) a private deal under Rule

144A

6

with a later requirement to register the notes with the SEC and (3) a private deal under

Rule 144A that stays private and is never registered with the SEC, which investors call “144A-

for-life” or “private-for-life.”

“Back End” Registration Rights and 144A-for-Life Deals

High yield notes are typically initially sold in the 144A market. In the early days of the high yield

market, securities sold in the 144A market included an obligation to complete a “back end”

exchange offer, which is an offer to allow holders to exchange the privately placed securities for

freely transferable, SEC-registered securities within a specified period after the closing. The

“back end” requirement reduced (or even eliminated) any negative impact on the coupon rate of

the notes from having been sold as (at least then) relatively less liquid 144A securities. In

______________________________

6

Rule 144A under the Securities Act of 1933 allows private resales to “qualified institutional buyers,” or

“QIBs” for short. High yield notes sold under 144A are often sold concurrently to non-U.S. investors

pursuant to Regulation S under the Securities Act.

PAGE 20

addition, certain buy side investors at the time operated under investment guidelines that

limited the amount of securities they could buy without “back end” registration rights.

However, after the adoption of Sarbanes-Oxley and the related SEC rules and regulations,

private companies pointed to the expensive compliance burdens of the SEC’s Regulation S-X,

which governs the financial statements that must be included in an SEC-registered deal, and

began to resist the obligation of a “back end” exchange offer. In addition, the number of 144A-

for-life deals increased due to a rise in the number of secured high yield deals because the

requirements of Rule 3-16 of Regulation S-X (which then required financial statements in SEC-

registered deals for certain subsidiaries the stock of which are pledged as collateral) are onerous

and costly. Indentures for SEC-registered notes must also comply with the Trust Indenture Act

of 1939, which imposes extra requirements on issuers of secured notes.

As a result of these factors, the market has completely shifted to a default setting in favor of

private-for-life deals, which are no longer considered to have a notable pricing impact, and

“back end” registration rights are rarely required except in certain very large scale deals or

investment grade offerings. Even when Rule 3-16 was largely superseded in early 2021 by Rule

13-02 of Regulation S-X, which requires summarized financial information for affiliates whose

securities are pledged as collateral in SEC-registered deals, rather than full financial statements,

the market had already shifted away from “back end” exchange offers and has not shifted back.

Reporting Requirements

The basic requirement of the reporting covenant, whether or not the issuer is a public company

subject to the SEC’s periodic reporting requirements, is to provide noteholders:

• an annual report containing information that would be in a Form 10-K;

• quarterly reports containing information that would be in a Form 10-Q;

• reports about certain events that contain information that would be in a Form 8-K; and

• quarterly conference calls with management.

The traditional reporting covenant requires an issuer to provide noteholders with the

information that a public company would report to the SEC and often permits an issuer to

deliver the information by posting it on a website.

All this makes sense for public companies and 144A deals with “back end” registration rights,

which will become public companies through the registration of the notes, if they are not public

already. But what about private companies and 144A-for-life deals?

Especially in 144A-for-life deals, issuers have been successful in negotiating modifications to

these requirements. The key modifications are as follows:

• Timing. Private companies may need more time to prepare their annual or quarterly reports

than the SEC rules allow. Some indentures, therefore, provide an extended deadline for the

issuer to produce its annual and quarterly reports. And in some cases, a new high yield

issuer negotiates a longer “holiday” period for its first annual report and first one or two

quarterly reports. These new issuers argue that they need extra time to become accustomed

to reporting according to SEC standards.

PAGE 21

• Content. Indentures often require that issuers provide only the types of information in their

reports that they otherwise provided in the offering document for the notes. In 144A-for-life

deals, issuers often negotiate exceptions so that they will not need to provide all the

information that would be required in SEC reports. These issuers argue that some

information included in SEC reports may not be materially meaningful to noteholders, such

as detailed executive compensation information. In fact, in some, but by no means all, 144A-

for-life deals, issuers are only required to provide annual and quarterly financial statements

with an MD&A discussion and may omit other disclosure (i.e., risk factors or a business

section) from their reports to noteholders that would otherwise appear in an SEC report.

• 8-Ks. In 144A-for-life deals, it has become increasingly acceptable to list the Form 8-K-like

reports that an issuer needs to provide, dispensing with the requirement to report certain

events that may not be material to noteholders.

Additionally, in some deals, issuers also negotiate an extended grace period for the related event

of default under the indenture. For example, you may see a 60-day cure period for most

covenant breaches under the indenture, but a 90-day cure period for a covenant breach under

the reporting covenant. These requests for an extended grace period have their roots in events

several years ago when issuers with accounting-related reporting delays found their problems

compounded by threatened accelerations of their notes due to their breaches of the reporting

covenant.

Conference Call Requirements

In addition to providing reports to noteholders, the issuer is typically required to hold live

quarterly conference calls with the opportunity to ask questions of management. We’ve seen

underwriters and issuers debate this requirement in numerous deals. Issuers who are public

companies sometimes argue that they already host earnings calls for their equity investors as a

matter of course and that noteholders are free to listen in. More often than not, however,

noteholders do not require a call dedicated to debt investors, but they require the comfort of

knowing they will always have quarterly access to management, even if the issuer goes private

and ceases to host calls for equity investors.

Multiple Levels of Reporting

Sometimes companies struggle with having to report at multiple levels. Let’s take an easy

example: Company A (a private company) issues notes with a traditional reporting covenant. A

year later, Company A completes an IPO, but the entity that goes public is the direct parent of

Company A. So that issuer is now stuck in a situation where the direct parent of Company A

must file reports with the SEC, but the notes reside one level down at Company A, which still has

an independent contractual obligation to provide reports to noteholders.

To address this problem, many indentures have a provision allowing a parent company’s

periodic reports to satisfy the reporting covenant as long as the parent guarantees the notes.

Remember that if an issuer makes use of this provision, that does not mean that the parent

entity becomes subject to the covenants under the indenture. The parent can choose to provide a

guarantee to enable the issuer to avoid duplicative reporting requirements, but the covenants

would continue to apply only to the issuer and its restricted subsidiaries.

PAGE 22

Mergers and Consolidations

The merger and consolidation covenant is designed to prevent a business combination in which

the surviving obligor for the notes is not financially healthy, as measured by the ratio test

described below. The covenant also seeks to ensure that noteholders will have enforceable rights

against the surviving entity in a merger, consolidation or transfer of all or substantially all the

assets of the issuer or a subsidiary guarantor.

Covenant Requirements

The typical conditions for a merger, consolidation or transfer of all or substantially all assets of

the issuer include:

• the continuity of the issuer’s existence or the assumption of the indenture by a U.S.

successor (i.e., the notes must travel with the surviving entity in the transaction);

• the absence of a default;

• the ability of the issuer to incur a $1.00 of debt under the fixed charge coverage ratio used in

the debt covenant (or, very frequently, no deterioration in the fixed charge coverage ratio);

• the continued effectiveness of any guarantees of the notes; and

• the delivery of certificates and legal opinions.

The typical conditions for a merger, consolidation or transfer of all or substantially all assets of a

subsidiary guarantor usually mirror those above but do not include the $1.00 of debt test, which

applies only to transactions involving the issuer.

There are also a handful of customary exceptions to the covenant, including one that permits

mergers of subsidiary guarantors with and into other subsidiary guarantors or the issuer. The

covenant also typically permits tax-motivated reincorporations in another state or, in some

cases, another country.

Interaction with Change of Control Covenant and Asset Sale Covenant

Always remember that every covenant must be tested independently to assess the implications

of a given transaction. A business combination could comply with the merger and consolidation

covenant but still trigger the change of control covenant described above.

On the other hand, if an issuer sells “all or substantially all” of its assets to a third party in

compliance with the merger and consolidation covenant, the issuer generally will not need to

comply with the asset sale covenant because the definition of “asset sale” usually carves out sales

of all or substantially all assets of the issuer so long as the transaction complies with the merger

and consolidation covenant.

“All or Substantially All”

One of the most interesting — or frustrating — aspects of this covenant is the ambiguity that

surrounds the phrase “all or substantially all.” While virtually every indenture uses some

variation of that phrase, there is no bright line definition. Instead, courts tend to analyze

PAGE 23

qualitative and quantitative facts and circumstances, and the quantitative factors can include

revenues, assets and operating income, weighted as the court sees fit. In the face of this

uncertainty, we always encourage issuers to raise the issue with their counsel if there is any

doubt about whether the business being sold may constitute “all or substantially all” of their

assets.

Optional Redemption

One of the distinctive elements of high yield notes are the optional redemption provisions. As a

general matter, high yield notes are not redeemable at the option of the issuer for a specified

number of years to permit investors to lock in an interest rate for a significant period of time.

For example, after a five-year no-call period, ten-year notes are typically redeemable at a

redemption price equal to par plus half the coupon, and the premium then declines ratably to

par two years before maturity. For eight-year notes, the usual formulation is a three-year no-call

period, after which the notes are redeemable at a redemption price equal to par plus 50% or 75%

of the coupon, declining ratably to par on the sixth anniversary of the issuance. In older deals,

eight-year notes typically had a four-year no-call period, in which case the redemption price

after the no-call period is equal to par plus 50% of the coupon, declining ratably to par.

Like almost everything in high yield, there are exceptions. High yield notes usually can, in fact,

be redeemed before the end of the no-call period – but generally at an expensive “make-whole”

price based on the present value of future payments under the notes. And there are a couple of

other exceptions that we describe below.

Exceptions to the No-Call Period

Make-Whole Redemption

Make-whole redemption allows issuers to call the notes during the no-call period at a price equal

to the present value of the optional redemption price on the first optional redemption date and

future interest payments up to that date. The present value for a high yield make-whole

redemption is almost always calculated based on the Treasury rate plus 50 basis points, which

differs from investment grade notes offerings, where the discount to the applicable Treasury rate

varies and is set at pricing. Although an issuer could always launch a tender offer for the notes,

the make-whole redemption provision removes the uncertainty about whether investors will

tender in the offer and what price they will demand.

The Equity Claw

Another significant exception to the no-call period is the ability of an issuer to redeem a portion

of the notes with the proceeds of an “Equity Offering” during the three years after the issuance

date (commonly referred to as the “equity clawback” or “equity claw”). This exception, which is

nearly universal in high yield offerings, permits the issuer to delever after an IPO or after raising

additional equity capital.

Note that the length of this redemption period is not tied to the no-call period but is almost

always a three-year period. You will typically see exceptions only for shorter maturity notes,

such as a five-year note with an “equity claw” for the first two years after issuance.

PAGE 24

Traditionally, issuers were not permitted to redeem more than 35% of the original principal

amount of the notes in an equity “clawback,” although 40% has become increasingly common.

The issuer must pay a redemption price to investors equal to par plus a premium equal to the

full coupon, plus accrued interest. While not a cheap option, it is cheaper than using the make-

whole redemption provision and helps issuers tell the equity market a deleveraging story in

connection with an IPO.

Keep an eye on the definition of “Equity Offering,” as certain transactions permit an equity

clawback only with the proceeds of an IPO or follow-on public offering, while some deals

broaden the definition to include any public or private equity offering, particularly if the issuer is

a portfolio company of a financial sponsor or in an industry in which companies partner with

strategic investors.

Equity clawback provisions typically require the issuer to apply the proceeds of an equity

offering to the redemption of the notes within a specified period of time (generally within 60 to

90 days). In addition, equity clawback provisions also require a certain percentage (i.e., 60-65%)

of the originally issued notes to remain outstanding following completion of the redemption in

order to preserve sufficient liquidity for the remaining notes.

The Interaction among the Redemption Exceptions

These redemption features are not mutually exclusive. In other words, you can use one or more

of the redemption features at the same time. Here is an example:

Example:

Company A issued $100 million aggregate principal amount of 6% eight-year notes with a

four-year no-call period, and the notes contain both the “equity claw” and make-whole

redemptions described above. In Year 3 of the no-call period, Company A goes public and

wants to redeem all of the outstanding notes in connection with the IPO. Let’s assume

Company A receives $100 million of net proceeds from its IPO. As a result, it can redeem

35% of its notes at 106% using the “equity claw” and redeem the rest of the notes using the

make-whole redemption provision.

“Clean up” Redemption Following a Repurchase

Increasingly, high yield indentures include permit an issuer to “clean up” and redeem all of the

remaining notes in the event holders put 90% or more of the outstanding principal amount of a

high yield series in a Change of Control Offer (at a price of 101%), Asset Sale Offer (at a price of

par) or other tender offer (at the tender offer price). This logical provision allows an issuer to

avoid a small stub trading in an illiquid tranche and avoids the need for covenant compliance by

an issuer with a small tranche held by investors that have the concentrated ownership power to

exert undue influence and elevate the price for waivers in the event the issuer needs covenant

relief.

PAGE 25

Key Definitions: Consolidated Net Income and EBITDA

In this Concise Guide to High Yield Notes, we have focused on a high-level overview of the high

yield covenant package. But, as always, the devil is in the details, and a lot of those details reside

in the definitions contained at the back of the description of notes.

We encourage you to review the Standard Form for a full listing and description of the

definitions, but we wanted to flag two key definitions that are among the fundamental building

blocks to the financial ratios used in the covenant — and for that reason are among the most

negotiated definitions.

Consolidated Net Income

Consolidated Net Income is the basis for most of the financial ratios contained in a high yield

indenture, since the definition of Consolidated EBITDA used to calculate the fixed charge

coverage ratio and other ratios begins with an issuer’s Consolidated Net Income. In addition, as

you will remember, the RP “builder basket” used for making restricted payments gives an issuer

credit for 50% of its Consolidated Net Income.

Consolidated Net Income always begins with consolidated net income of the issuer and its

restricted subsidiaries in accordance with GAAP. But it then goes on to exclude a number of

items that either reflect value that may not be accessible for payment of the notes or are viewed

as unrealized, non-recurring or not reflective of the issuer’s ongoing operations.

For example, Consolidated Net Income often excludes items like the following, among others

that may be tailored to the issuer’s business and industry:

• income from unrestricted subsidiaries or equity investments (unless the issuer actually

receives cash);

• income (but not losses) of subsidiaries that are blocked from distributing earnings to the

issuer because of contractual, regulatory or other restrictions;

• extraordinary gains or losses; and

• income or losses from sales of assets outside the ordinary course of business.

Why does Consolidated Net Income usually exclude extraordinary items? Primarily because

high yield investors are keenly aware that 50% of Consolidated Net Income can be used for

restricted payments (i.e., cash exiting the “credit box”), and high yield investors prefer that the

RP “builder basket” be based on a definition that closely follows a GAAP term, albeit with a

few select exclusions, such as extraordinary items.

Consolidated EBITDA

Consolidated EBITDA is the basis for calculating the fixed charge coverage ratio (which is used

in the debt covenant, the RP covenant and the merger covenant) and for calculating leverage

ratios and, in some cases, “grower” baskets in those indentures that have them. Consolidated

PAGE 26

EBITDA begins with Consolidated Net Income and adds back consolidated interest, taxes,

depreciation and amortization, and other negotiated items.

7

In general, Consolidated EBITDA permits an issuer to add back any non-cash charges unless

those charges reflect an accrual for a future cash payment, and that practice is generally

accepted in the market. The negotiations over add-backs in the definition of Consolidated

EBITDA usually center on items that are non-recurring but are cash charges or that do not meet

SEC guidance on reporting non-GAAP metrics. For example, restructuring charges representing

an accrual for cash severance payments to employees is the type of add-back that investors may

push to limit to a negotiated dollar cap.

Another example is the frequent and often heavily negotiated request to add back cost savings

that are achieved from certain acquisitions, mergers or dispositions. For example, issuers and

underwriters may negotiate whether the cost savings must occur within a specified period of

time after the closing date (e.g., 12 to 18 months). In addition, you will often see a negotiated cap

on this add-back, whether as a fixed dollar amount or as a percentage of total Consolidated

EBITDA.

Again, every indenture is different, and the definition is typically tailored to the issuer’s

particular business and industry, as well as other debt agreements.

It’s important to keep in mind that virtually every high yield offering uses an adjusted EBITDA

metric as a marketing tool and presents a calculation in the summary box at the front of the

offering memorandum. It’s in everyone’s interest to make sure that the adjusted EBITDA shown

in the front of the offering memorandum is consistent with the definition in the high yield

covenant package. Also, high yield investors will want an issuer to report its “EBITDA” every

quarter in a manner that is consistent with the covenant definition so that investors can monitor

whether the issuer has the capacity to meet the financial ratios under the indenture.

The Battle of the Add-Backs

You may have noticed that excluding a non-recurring charge from Consolidated Net Income

would have the same effect as adding back that charge in calculating Consolidated EBITDA (if

the charge had been excluded in calculating Consolidated Net Income). So why go through the

trouble of having separate definitions for Consolidated Net Income and Consolidated EBITDA?

The answer to this question lies in where the two definitions are used and how they are