NBER WORKING PAPER SERIES

THE ECONOMIC IMPACT OF HURRICANE KATRINA ON ITS VICTIMS:

EVIDENCE FROM INDIVIDUAL TAX RETURNS

Tatyana Deryugina

Laura Kawano

Steven Levitt

Working Paper 20713

http://www.nber.org/papers/w20713

NATIONAL BUREAU OF ECONOMIC RESEARCH

1050 Massachusetts Avenue

Cambridge, MA 02138

November 2014

We thank Jesse Gregory, Bruce Sacerdote, and participants at the 2014 ASSA meetings and 2014 NBER

Summer Institute for helpful comments. Erin Robertson and Eric Andersen provided excellent research

assistance. The views expressed herein are those of the authors and do not necessarily reflect the views

of the National Bureau of Economic Research or the policy of the U.S. Department of Treasury.

NBER working papers are circulated for discussion and comment purposes. They have not been peer-

reviewed or been subject to the review by the NBER Board of Directors that accompanies official

NBER publications.

© 2014 by Tatyana Deryugina, Laura Kawano, and Steven Levitt. All rights reserved. Short sections

of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full

credit, including © notice, is given to the source.

The Economic Impact of Hurricane Katrina on its Victims: Evidence from Individual Tax

Returns

Tatyana Deryugina, Laura Kawano, and Steven Levitt

NBER Working Paper No. 20713

November 2014

JEL No. Q54

ABSTRACT

Hurricane Katrina destroyed more than 200,000 homes and led to massive economic and physical

dislocation. Using a panel of tax return data, we provide one of the first comprehensive analyses of

the hurricane’s long-term economic impact on its victims. Katrina had large and persistent impacts

on where people live; small and mostly transitory impacts on wage income, employment, total income,

and marriage; and no impact on divorce or fertility. Within just a few years, Katrina victims’ incomes

fully recover and even surpass that of controls from similar cities that were unaffected by the storm.

The strong economic performance of Katrina victims is particularly remarkable given that the hurricane

struck with essentially no warning. Our results suggest that, at least in this particular disaster, aid

to cover destroyed assets and short-run income declines was sufficient to make victims financially

whole. Our results provide some optimism regarding the costs of climate-change driven dislocation,

especially when adverse events can be anticipated well in advance.

Tatyana Deryugina

Department of Finance

University of Illinois, Urbana-Champaign

Laura Kawano

Department of the Treasury

Steven Levitt

Department of Economics

University of Chicago

1126 East 59th Street

Chicago, IL 60637

and NBER

A data appendix is available at:

http://www.nber.org/data-appendix/w20713

2

Hurricane Katrina is arguably the most destructive natural disaster ever to strike the

United States. The storm killed nearly 2,000 people and destroyed more than 200,000 homes.

Property damage was estimated to be upwards of $100 billion. Eight years later, the population

of New Orleans is nearly 25 percent smaller than before the devastation, and parts of the city

have never been rebuilt.

Despite the magnitude of the disaster, remarkably little is known about the long-term

ramifications for its victims. To date, the research on Hurricane Katrina victims has focused

primarily on their immediate mobility patterns

1

and the impact of the Katrina evacuees on

surrounding areas.

2

Much less is known about the economic impact of the disaster on victims, in large part

because of data limitations. One source of information is the Bureau of Labor Statistics’ Current

Population Survey (CPS), which was revised to include questions that identified Katrina

evacuees from October 2005 through October 2006 (Cahoon et al. 2006, Groen and Polivka

2008a).

3

Using these data, Vigdor (2007) documents an initial negative impact of Hurricane

Katrina on the labor market participation of those who were evacuated, with the effect being

most pronounced for those who were unable to quickly return to their homes. In the medium-run,

the labor market outcomes for those who eventually came back to New Orleans returned to their

1

Approximately 60 percent of evacuees from Louisiana returned to their pre-hurricane addresses within 14 months

(Groen and Polivka 2008b). Gregory (2011) estimates that the Louisiana state government’s Road Home program,

which provided money to residents to rebuild and protect their homes from future storm damage, increased the rate

of rebuilding damaged homes by 11 percent. Those who did not return were more likely to be black, have lower

levels of education, have a low family income, and were unlikely to be homeowners (Groen and Polivka 2010).

Those who did return had moved a median of two times before 2009 (Geaghan 2011).

2

Several papers have also studied the effect of Hurricane Katrina on Houston: the influx of Katrina evacuees

increased Houston’s population by over 3 percent (McIntosh 2008) and is estimated to have decreased wage levels

(De Silva 2010, McIntosh 2008).

3

The American Housing Survey also added questions related to Hurricane Katrina. However, we are not aware of

any relevant research that uses these data.

3

pre-Katrina levels, but negative effects persisted for those who were living in the worst hit areas.

However, a key disadvantage of the CPS data is that it can only be used to identify evacuees,

who may not be representative of the average Katrina victim. Moreover, because the CPS

stopped tracking evacuees in October of 2006, it cannot be used to evaluate longer-run effects.

We are not aware of any other publicly available datasets that allow researchers to identify

individuals who were affected by the hurricane and link them to post-Katrina outcomes.

4

In this paper, we use a previously untapped data source—individual tax returns—to

undertake one of the first systematic analyses of the long-term social and economic

consequences of Hurricane Katrina for those who lived in New Orleans prior to the storm.

5

We

draw our sample from the universe of individual tax returns filed between 1999 and 2010. Two

features of tax return data allow us to analyze the long-run impacts of Hurricane Katrina. First,

tax returns contain filing addresses, which allows us to reliably identify those residing in New

Orleans before the storm struck. Second, we are able to link tax returns over time and thus

construct a panel of households that spans twelve years, with Hurricane Katrina occurring

roughly in the middle of that period. Tax returns contain rich information about incomes from

different sources, such as wages and salaries, self-employment, unemployment insurance, and

retirement accounts. Many of these sources are not well-measured in survey data. We can also

use the tax returns to infer mobility and changes in household composition (e.g., births, marriage,

and divorce).

4

For example, unlike other recent decennial censuses, the 2010 PUMS survey does not ask respondents where they

resided five years earlier. In light of the timing of Hurricane Katrina (September 2005), knowing where people

lived in April 2005 (five years prior to the 2010 Census) would have proven invaluable in the study of Katrina’s

impact.

5

Using Longitudinal Employer-Household Dynamics data, Groen et al. (2014) estimate the wage income trajectory

of a broader set of Hurricane Katrina and Rita victims. Their wage findings mirror ours; because of the richness of

our data, we are also able to look at a number of other outcomes.

4

Even with excellent data, empirical challenges remain. Estimating the causal impact of

Hurricane Katrina requires finding a credible comparison group to serve as a counterfactual for

the experiences of New Orleans residents in the absence of the hurricane. However, finding such

a group is difficult. Ideally, we would compare those hit by the hurricane (the treatment group)

to a set of similar people who were unaffected (the control group). An obvious strategy would

be to select a set of control cities that looked like New Orleans on a range of dimensions prior to

the storm. Unfortunately, New Orleans is unique in many ways, making it difficult to find good

matches. Additionally, the diaspora out of New Orleans in response to the hurricane appears to

have affected labor market conditions in other cities (De Silva 2010, McIntosh 2008). A

comparison of New Orleans residents whose homes are directly affected by the flood to those

who were spared (e.g., because the homes were built on high ground) suffers from obvious

endogeneity problems as well.

In light of these difficulties, our preferred empirical approach is to first select U.S. cities

that are reasonably similar to New Orleans prior to 2005, using data from the 2000 U.S.

Decennial Census and the 2001-2005 American Community Survey. We construct our panel of

all New Orleans residents and a random subsample of households from the control cities from

the universe of tax returns spanning 1999 to 2010. We then calculate propensity scores and use

inverse propensity score weighting in our analysis (Hirano et al. 2003). The richness of our data

allows us to use a number of characteristics to construct the propensity score, including age,

marital status, employment and homeownership statuses, number of kids, wage income, and

adjusted gross income for each year between 1999 and 2004.

6

We examine how a wide range of

economic and social outcomes changed for Katrina victims relative to the control group.

6

As we demonstrate below, our basic findings are robust to a wide range of assumptions regarding this procedure.

5

A number of key results emerge. First, the hurricane had large and persistent impacts on

where people live. Over one-fourth of New Orleans households were displaced by the storm in

2005-2006. Five years later, they remain geographically dispersed and appear to have settled

down. Second, and more surprisingly, we find only small and transitory impacts on the wage

earnings and total income of the victims. In 2006, the year after the storm, wage and salary

income for the average Katrina victim in our sample is roughly $2,200 lower than their matched

counterparts. Remarkably, the earnings gap is erased the following year, and by 2008, the

hurricane victims actually have higher wage income and total income than control households.

Even those who lived in the most damaged areas do not have lower earnings in the long run,

although they are slightly more likely to report no wage income. Consistent with these wage

earnings responses, we find that while unemployment receipts and non-employment among the

Hurricane Katrina victims spike after the storm, the differences disappear by 2007 and 2009,

respectively. Five years later, Hurricane Katrina victims are less likely to be receiving

unemployment benefits. Third, savings appear important for weathering the storm: households,

on average, took significant distributions from their retirement accounts in 2005-2010, taking

advantage of a special exemption from the early withdrawal penalty. Finally, an increase in

marriage probabilities is observed immediately after the storm, but we find little long run impact

on divorce. In some sub-groups, the reported number of child dependents falls, but the pattern is

more consistent with changes in living arrangements than with a drop in fertility.

One possible explanation for the fast earnings recovery that we document for Hurricane

Katrina victims is that strong ties to a place, especially a place with limited economic

opportunities such as New Orleans, have adverse economic consequences.

7

When forced by an

7

Such rationales have been used in support of the Federal Moving to Opportunity (MTO) program, a randomized

experiment that provided vouchers to households in high-poverty areas so that they could relocate. Overall, analyses

6

exogenous shock to migrate, people are able to choose from a wide range of possible locations to

move to, and they seem to choose places that offer them better economic opportunities.

Consistent with this hypothesis, Sacerdote (2012) reports that forced school changes because of

Hurricane Katrina had an immediate negative impact on school outcomes for displaced children,

followed by positive long-run effects on test scores. However, we find that the increase in wage

earnings was concentrated among those who eventually returned to New Orleans. Moreover, we

find that housing costs in New Orleans increased by roughly the same amount as wage incomes,

relative to control cities. These two facts suggest that while the incomes and employment of

Hurricane Katrina victims recovered quickly, the income growth we document reflects nominal,

rather than real, increases. Importantly, our results do not imply that the utility of the storm

victims improved. We cannot measure the non-pecuniary costs of the disruption created by

Hurricane Katrina, but the fact that people tend to stay in a particular place when not hit by

exogenous shocks suggests that these costs are high.

Our study sheds light on the appropriate levels of disaster relief and insurance. Diverse

sources of aid were made available to Hurricane Katrina victims to ease the negative impacts of

displacement and economic loss. Direct disaster relief amounted to slightly over $100 billion

(Hoople 2013). Per capita unemployment insurance payments in New Orleans doubled from $63

per resident in 2004 to $126 per resident in 2005 and $167 per resident in 2006.

8

Some aid was

also implemented through the federal tax system. The Work Opportunity Tax Credit, a program

that offers tax incentives for firms to hire individuals from certain disadvantaged groups, was

expanded to include individuals living in areas affected by Hurricane Katrina. Residents of New

Orleans were allowed to make early withdrawals from their retirement accounts without paying

of the MTO indicate that there was little impact of moving on economic outcomes, although the program had some

non-pecuniary benefits (Kling, Liebman, and Katz 2007).

8

Authors’ calculations using Regional Economic Information Systems data.

7

the early withdrawal penalty. Finally, it is estimated that charitable donations related to

Hurricane Katrina were upwards of $4.25 billion.

9

While our study cannot precisely identify

what would have happened in the absence of this aid, it appears to have been adequate to avert

harmful long-run economic effects.

Our results also speak to the appropriate level of ex ante mitigation spending (Becker,

Murphy, and Topel 2011). The longer the effects of shocks like Hurricane Katrina last, the

larger the economic and welfare losses and, correspondingly, the benefit of public mitigation

measures, such as investments in stronger levees. While we cannot measure the magnitude or

duration of utility losses, the highly transitory nature of the income losses caused by Katrina

suggests that the long-run economic effects of natural disasters need not be a significant

consideration for ex ante mitigation spending decisions.

Finally, our results have important implications for the debate about climate change. If

the predictions of current climate models come true, the intensity of hurricanes, along with the

frequency and severity of other extreme weather events, will increase over time (IPCC, 2013). In

addition, rising ocean levels and temperatures will likely lead to substantial population

movements in upcoming centuries (Barbieri et al. 2010; Feng, Krueger, & Oppenheimer 2010;

and McGranahan, Balk, & Anderson 2007). The investments that society is willing to make to

mitigate climate change related costs (e.g., through carbon taxes, geoengineering solutions, or

technology to protect existing cities from rising oceans) depend critically on the economic

consequences of extreme weather events and the costs associated with relocating. The absence of

long-run economic losses from Hurricane Katrina suggests that this component of the costs of

9

This and other statistics about Hurricane Katrina-related charitable giving are taken from Charity Navigator

(http://www.charitynavigator.org/index.cfm/bay/katrina.facts.htm). Hurricane Katrina was a boon to charities:

donations to human services organizations in 2005 were 28 percent higher, and 36 percent of 2005 disaster relief

donations was made to victims of Hurricanes Katrina and Rita.

8

climate change is unlikely to be large, at least in developed countries.

10

In addition, the

economic losses associated with forced dislocation from an unexpected event like Hurricane

Katrina likely represent an upper bound on the costs associated with a dislocation that comes

with decades of advance notice due, for instance, to rising ocean levels.

11

The remainder of the paper is structured as follows. Section II provides additional

background on Hurricane Katrina. Section III describes the data sources used in the analysis,

with emphasis on the tax return data. Section IV presents the findings. Section V concludes.

Section II: Background on Hurricane Katrina

Tropical Depression 12 developed on August 23, 2005.

12

It quickly grew in size and

strength, and by the following day it was named Tropical Storm Katrina. Katrina developed into

a Category 1 hurricane as it traveled northwest across the Bahamas. It first made landfall August

25 on the coast of Florida, causing only a handful of deaths. It then moved westward across the

Gulf of Mexico and at its peak strength was a Category 5 storm with wind speeds clocked at over

170 miles per hour. By the time Katrina reached the Louisiana coast on August 29, it had

sustained winds that placed it as a strong Category 3 storm. In New Orleans, wind speeds were

well over 100 miles per hour.

13

10

Our results are less informative regarding what long-run economic costs of natural disasters might be in

developing economies. For instance, it is estimated that more than 26 million people in low-lying areas of

Bangladesh will be forced to relocate over the next half-century (Bierman and Boas 2010). Additionally, our results

come with the caveat that what we observe is conditional on the government aid, insurance, and charitable activities

that occurred. The impact on victims absent these resources might have been very different.

11

Moreover, aid for displaced individuals will likely be much smaller for those who can more reasonably anticipate

the effects of climate change than those who are suddenly impacted by a natural disaster.

12

The basic facts about Hurricane Katrina cited throughout are from publications of the National Oceanic and

Atmospheric Administration.

13

Meteorologists categorize hurricanes on a scale from 1 to 5. A Category 1 hurricane has wind speeds ranging

from 74 to 95 miles per hour, while a Category 5 storm has wind speeds over 155 miles per hour, causing extensive

property damage, power outages, and potentially high fatality and injury rates (Schott et al. 2012).

9

The government realized early on that Katrina had the potential to be the “perfect storm,”

causing massive wind damage and storm surges. New Orleanians had long known that a direct

hit on New Orleans might have catastrophic results. The city is situated largely below sea level,

protected from flooding by a system of canals and levees along the Mississippi River to the south

and east and Lake Pontchartrain to the north. A breach in the levees would cause massive

flooding throughout the area. Once flooded, ridding the city of water would be a massive

undertaking because New Orleans sits at the bottom of a bowl-shaped area of land.

New Orleans Mayor Ray Nagin issued a voluntary evacuation order the evening of

August 25, four days before the storm struck the Louisiana coast. The following morning, he

changed the voluntary evacuation order to the city’s first ever mandatory evacuation. President

George W. Bush urged residents to prepare for the worst.

14

Two days before landfall, the city

converted all highway lanes to outbound. Even so, evacuees faced gridlock.

With all signs pointing toward a catastrophic storm, the great majority of city residents

evacuated. Still, nearly 100,000 New Orleans–area residents prepared much as they had done in

the past: by boarding their windows, stocking up on nonperishable foods, and throwing hurricane

parties.

15

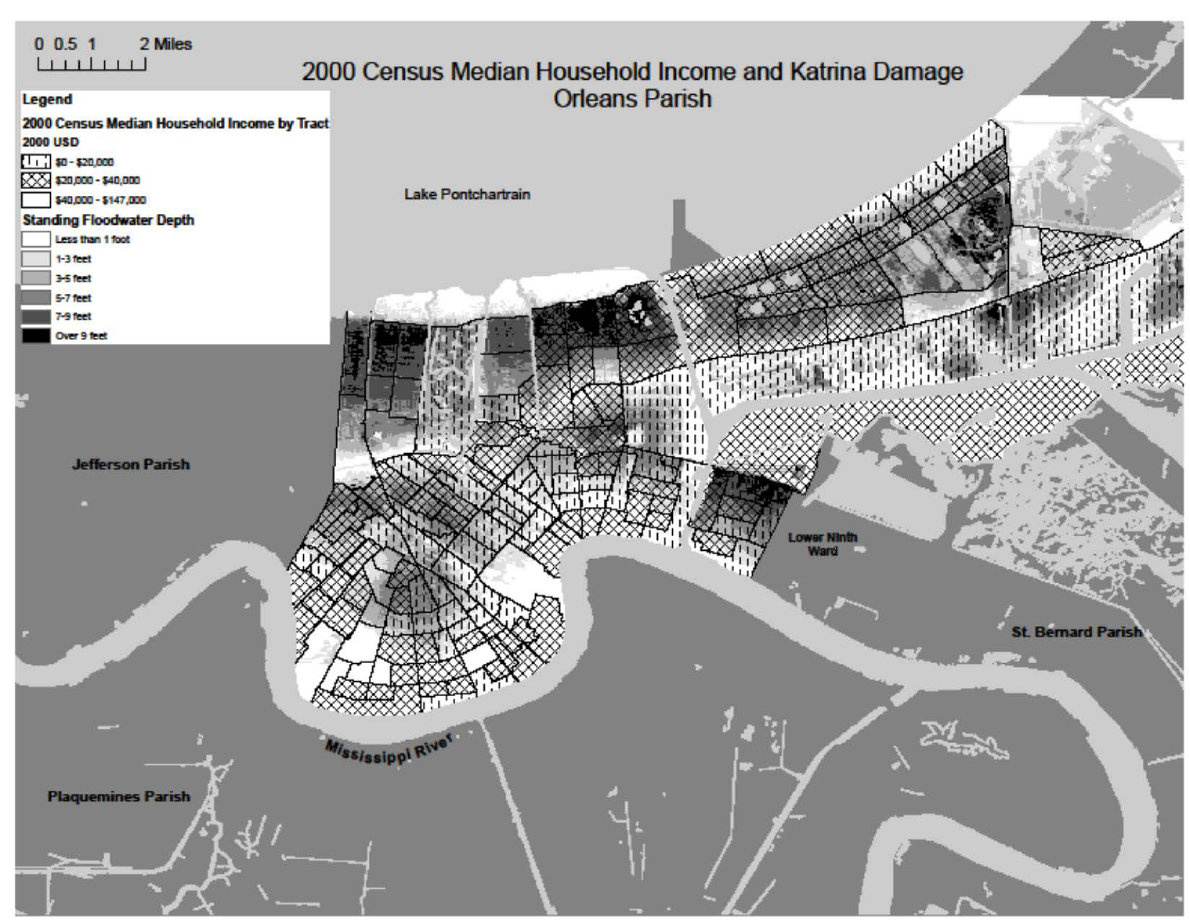

Katrina reached Louisiana’s coast on Monday, August 29. Lake Pontchartrain breached

the area’s levees. Water pumps and the sewage system couldn’t keep up with the deluge, leaving

80% of New Orleans under water. Figure 1 shows a map of the New Orleans area with deeper

flooding captured by a darker shade, and median household income denoted with cross-hatching.

14

And in yet another New Orleans evacuation first, meteorologist Nash Robert’s himself left the city; in his over 50

years as the local authority on hurricanes, Roberts had not once evacuated.

15

In previous years, voluntary evacuations had been called for hurricanes that had caused minimal damage. Just the

year before, Hurricane Ivan had fizzled out before reaching Louisiana. Locals also thought they had already seen—

and survived—the worst, 1965’s Hurricane Betsy. A Category 3 storm, Hurricane Betsy killed approximately 75

people in Louisiana and incurred over $10 billion in damage in present-day dollars (Sugg 1966). It was also the

reason for New Orleans’ supposedly improved levee system—the very system that Katrina breached (National

Geographic News 2005).

10

The worst flooding – more than nine feet of standing water occurred near Lake Pontchartrain and

in the lower ninth ward, but serious flooding was seen throughout the city. A few areas of the

city sustained minimal damage; these neighborhoods tended to be relatively affluent.

Nearly 60,000 members of the National Guard were sent to help with rescue and

recovery, in an effort that one command sergeant referred to as “far more difficult that anything

we faced in Iraq.”

16

Soon thereafter, President Bush declared Katrina “one of the worst natural

disasters in our nation’s history” (Washington Post 2005). Statistics back up this statement. Not

since the devastating Florida hurricane of 1928 had a natural disaster claimed as many American

lives.

17

Katrina ranks as the most expensive storm, causing over $100 billion in damage, more

than twice as much as the next storm, Hurricane Andrew (Blake, Landsea, & Gibney 2011).

Nearly two years later, over 600,000 individuals had yet to return to their homes in the broader

affected areas. Nearly nine years later, New Orleans’s population recovered to only 75 percent

of its pre-Katrina level.

Section III: Data and Identification

Our data are drawn from the universe of U.S. federal tax returns filed between 1999 and 2010.

18

To construct our sample, we begin by identifying all households whose tax returns were filed in

New Orleans for the 2004 tax year (i.e., those that were due to be filed in April 2005) based on

filing zip code.

19

We classify these households as victims of Hurricane Katrina, which hit New

Orleans in August 2005. For each household, we collect data from tax records for the years 1999

16

The PBS NewsHour, September 8, 2005.

17

This figure doesn’t take into account the many other Katrina-related fatalities, including an estimated 600,000 pets

and animals that died or were left without shelter, and nearly the entire fish population of the world-renowned New

Orleans Aquarium of the Americas (AP 2009; CNN 2005).

18

These data are housed at the Internal Revenue Service’s (IRS) Compliance Data Warehouse and contain

transcribed data from all individual tax returns beginning in 1999.

19

Throughout, we refer to tax filing units as “households”.

11

through 2010.

20

Specifically, we obtain information on the household’s income from wages and

salaries, self-employment (Schedule C) income or losses, income from unemployment

compensation, adjusted gross income, Social Security income, and gross retirement account

distributions from IRS Form 1040. To reduce the influence of outliers, we winsorize the adjusted

gross income, wage income, and retirement account distributions by replacing the values above

the 1

st

and 99

th

percentiles with the values at those percentiles. We additionally collect the

demographic characteristics that can be obtained from tax records: filing status, number of child

dependents at home or away from home, age of the primary filer, and filing address. We drop tax

filers who are reported to be under 16 or over 100 years old at any point during our sample. We

use filing status to infer marital status. We define a movement from “married filing jointly” to

single filer status as a divorce and the opposite movement between these filing statuses as a new

marriage.

21

Our panel of tax return data has several advantages over other datasets that might be used

to analyze the long-run economic impacts of Hurricane Katrina. First, we are able to track

individual outcomes regardless of where victims eventually reside. The CPS only tracked

evacuees, and location-specific datasets only track those who stay and those who move in. Thus,

both aggregated city-level and evacuee-based analyses will miss a substantial portion of

outcomes. Moreover, because there are likely to be differences between those who ultimately

returned to New Orleans, those who permanently relocated, and those who never left, such

analyses will suffer from sample selection problems. Second, although our data lacks potentially

important demographic characteristics, such as education and race, it contains highly detailed

20

For our analysis, we track households by the primary filer. We do not follow individuals who are secondary filers

or dependents on a 2004 tax return, but are no longer claimed by the primary filer.

21

We do not use “married filing separately” (MFS) as an indicator for marriage. Very few married couples file

separately, and those that do are often in the process of getting divorced.

12

information on income amounts and sources. This allows us, for example, to accurately measure

the role played by unemployment insurance, self-employment, and dis-saving. Finally, a long

pre-period of data allows us to directly see whether any of our conclusions are affected by

differential pre-trends.

As noted earlier, New Orleans is a unique city in many ways, with a high reliance on

tourism, low income levels and employment rates, and a high percentage of black residents. It is

difficult, therefore, to construct a compelling control group using only city-level data.

22

Thus,

after identifying cities that most closely resemble New Orleans, we turn to propensity score

weighting as our primary empirical method (Hirano et al. 2003). This methodology allows us to

compare the outcomes of individual Hurricane Katrina victims to controls while accounting for

differences in their observable characteristics. A closely related method, propensity score

matching, where a Hurricane Katrina victim is matched to the control individual with the closest

propensity score, yields very similar results (Rosenbaum and Rubin 1983).

We begin the process of control selection by identifying cities that share basic traits with

New Orleans. To choose this set, we focus on three pre-Katrina dimensions: median earnings,

the population growth rate, and the percent of population that is black.

23

The first two variables

are meant to capture the general economic environment in the household’s city of residence. The

last variable is important because we do not observe race in tax return data. If there are race-

22

Consequently, it is difficult to implement, for instance, the synthetic control approach of Abadie et al. (2010)

which computes weights for potential control cities such that their weighted average is similar to the treatment group

in the pre-period.

23

To choose a set of cities for the control universe, we start with the universe of American cities with populations

over 100,000 and compute the within-year differences between each potential control city and New Orleans for the

three outcomes mentioned above. We normalize each outcome by its standard deviation in that year to make the

magnitudes comparable and square the normalized measure to penalize large deviations. For each city, we then

compute the sum across the five years and three outcomes to come up with the sum of squared normalized

differences from New Orleans. We rank cities according to this measure and select the ten most closely resembling

New Orleans.

13

specific trends and we do not have a sample that is balanced along this dimension, our results

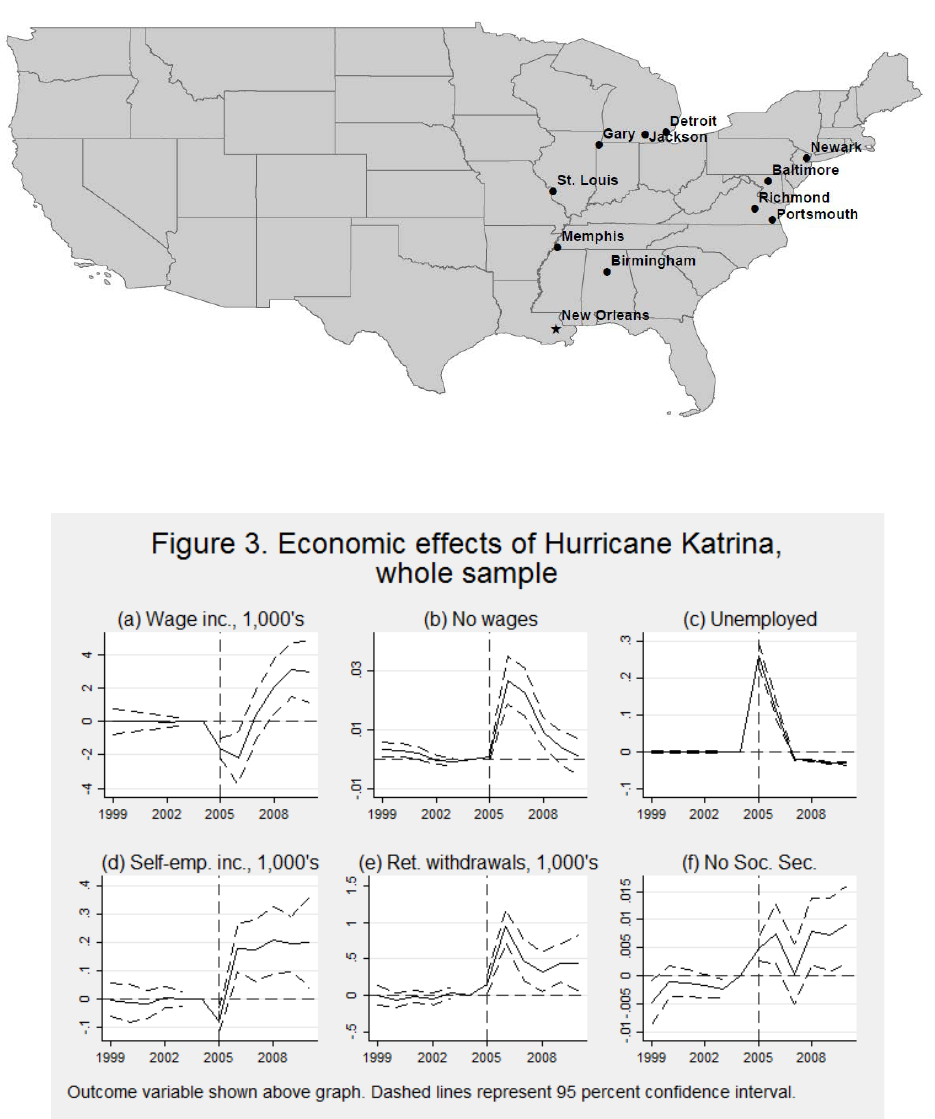

may be biased. The ten cities from which we draw controls are: Baltimore, MD; Birmingham,

AL; Detroit, MI; Gary, IN; Jackson, MI; Memphis, TN; Newark, NJ; Portsmouth, VA;

Richmond, VA; and St. Louis, MO. Table 1 presents descriptive statistics for these cities, and

Figure 2 shows them on a map. Essentially, these are the blackest, poorest large cities in the

United States, but on average they are slightly less black and slightly richer than New Orleans.

Due to the large size of the data, we draw a random 10% sample of 2004 residents in

these cities to form the basis of our control group. We collect data spanning 1999 to 2010 for

these households in a similar fashion to our sample of 2004 New Orleans residents. We then

calculate a propensity score using the primary tax filer’s age, marital status, employment and

homeownership statuses, the number of kids, wage income, and adjusted gross income for each

year between 1999 and 2004. We then use the inverse of the propensity scores as weights in our

analysis. Our preferred specification also omits individuals whose propensity scores lie outside

the range of propensity scores in the other group. In other words, we impose the “common

support” restriction. A key advantage of propensity score weighting over propensity score

matching is that the former utilizes the full sample instead of restricting the number of controls to

be equal to the number of treated units, thus increasing power. Another important advantage is

that inverse propensity score weighting takes into account how similar the control units are to the

treated ones. However, as we discuss later, our results are robust to employing one-to-one

matching.

The summary statistics for the treatment and control groups prior to Hurricane Katrina

(years 1999-2004) are presented in Table 2. The average New Orleans resident in our sample is

about 44 and claimed 0.7 dependents. About 25% of New Orleans residents are married and

14

36% own homes. They earned about $42,000 in adjusted gross income (AGI) each year, of

which $30,000 was from wages, $1,600 was from retirement accounts, $1,000 was from self-

employment, and $100 was from unemployment compensation. About 3.5% report some

unemployment benefits, and almost 13% report no wage income.

Compared to the random 10% sample from the control cities, whose summary statistics

are presented in the second column, New Orleans residents are slightly less likely to be married

and significantly less likely to be homeowners. They are significantly less likely to report

receiving unemployment insurance payments, but slightly more likely to report no wage income.

They also have marginally lower wage earnings and retirement account distributions. However,

there are no differences in their age, fertility, moving propensity, and adjusted gross incomes.

The propensity score weighting approach allows us to further reduce the existing differences, in

many cases eliminating them.

One concern about using tax returns to examine the impacts of Hurricane Katrina is that

they provide information only on the tax filing population.

24

We provide some summary

statistics about our New Orleans sample in order to gauge the representativeness of the tax return

data. We identify 186,894 households filing taxes in New Orleans for 2004, comprising of

357,657 individuals (including the primary tax filer, spouses, and dependents). This accounts for

over 72% of the New Orleans population as of July 1, 2005, according to the Census Bureau

population estimates.

25

We further compare the age distribution implied by New Orleans tax

returns to the New Orleans population breakdown by age from the Surveillance, Epidemiology,

and End Results (SEER) database. In 2004, tax returns capture roughly 80% of those aged 0-24

24

For the 2004 tax year, the filing threshold was $7,950 in gross income for single filers and $15,900 for those

married filing jointly if there were zero blind or elderly exemptions. Those with incomes below the filing threshold

were not required to file a tax return.

25

The July 1, 2005 population of New Orleans was estimated to be 494,294.

15

and 70% of those in their prime working years (age 25-65). The biggest gap is the elderly (over

age 65), where we capture roughly 48% of the population.

26

Thus, some caution is warranted

when interpreting our estimates for the oldest age group.

Because non-filing tends to be a low-income phenomenon, we next consider the incomes

of those we identify in tax return data. Almost 22% of New Orleans households report an AGI of

at most $10,000 in 2004. Of these, almost half report AGI of at most $5,000. Thus, we have a

significant number of treated households with low income levels. There are several reasons to

file a tax return even if a household falls below the federal filing threshold, including getting a

tax refund for taxes that were over-withheld or taking advantage of the Earned Income Tax

Credit and other refundable tax credits. At the upper tail of the income distribution, the 95

th

percentile falls at a little over $120,000. These statistics fall below the national percentiles of the

income distribution, reflecting the fact that New Orleans is a relatively poor city. They also make

us fairly confident that we are not missing a large fraction of low-income New Orleans residents.

Lastly, because mobility has been the focus of much work examining the impacts of

Hurricane Katrina, we compare other published statistics on mobility after the hurricane to the

geographic mobility implied by tax filing addresses for New Orleans residents in subsequent

years. Nearly 53% of New Orleans residents either filed their 2005 tax return (which would be

due in April of 2006) in a different city or did not file a tax return.

27

According to the Census

Bureau population estimates, New Orleans was 53% smaller as of July 2006. Of those who filed

tax returns in a different city in 2006, 32% filed their tax return from a New Orleans address by

2010.

26

The 0-24 age group includes all kids claimed on a tax return, primary tax filers who are age 24 or below, and also

their spouse if married. We treat all secondary filers as though they are in the same age category as their spouse.

27

Nearly 40% of households filed their tax return in a different city.

16

Section IV: Methodology and Results

Having identified a control group for the pre-Katrina New Orleans residents in our

sample, we run regressions of the form:

=

1

[

=

]

,

+

+

+

(1)

where i indexes households and t is the filing year. The variable Y corresponds to one of our

outcome variables. 1

[

=

]

is an indicator equal to one if the observation falls in year , while

is an indicator variable that is equal to one if the individual lived in New Orleans in

2004 and zero otherwise. Household- and year- fixed effects are included in the specification.

Standard errors are clustered by the household’s 2004 zip code. We weight each regression by

the inverse of the household’s estimated propensity score.

The key coefficients in the specification are the time-varying s, which capture any

systematic gap between the outcomes of those who lived in New Orleans in the year prior to

Katrina and the control individuals. If the control group is properly selected, the pre-2005 s

should be close to zero, while the post-2005 s will correspond to the causal effect of Katrina on

each outcome.

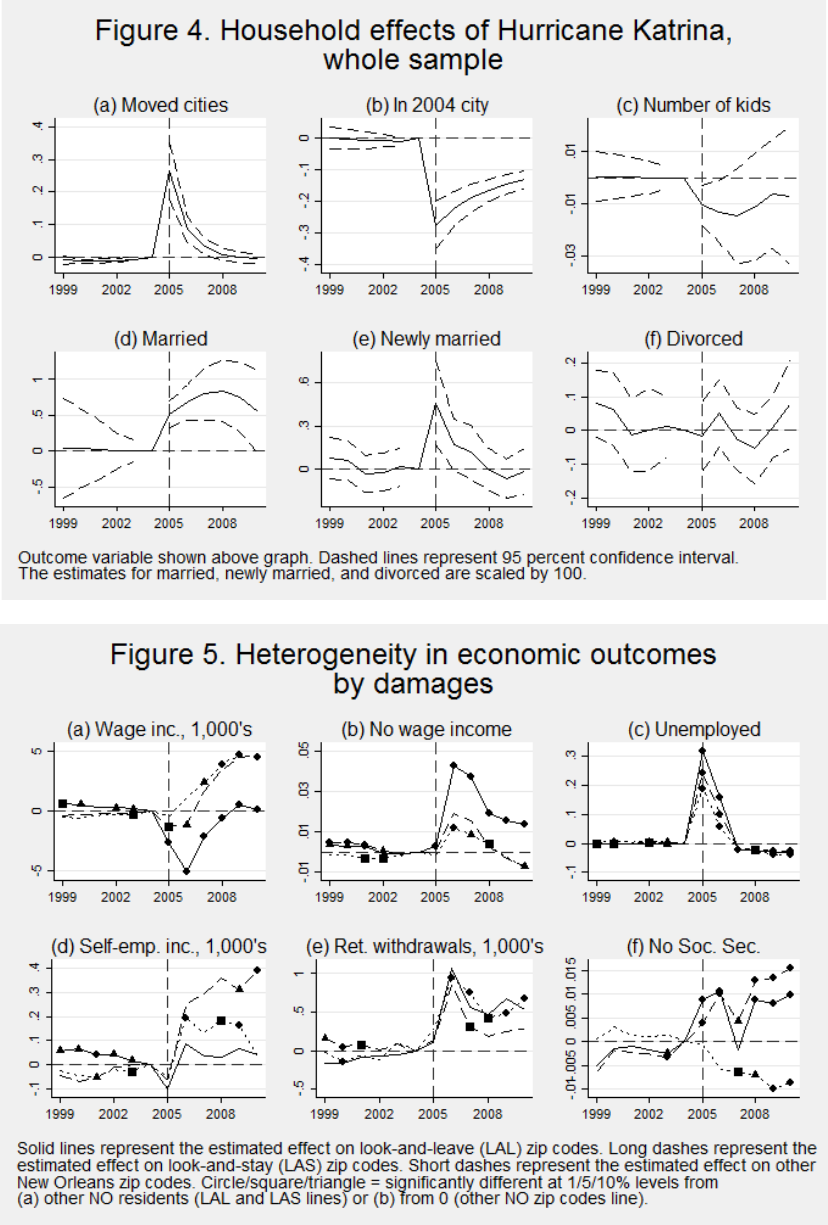

The estimated s and corresponding 95% confidence intervals are presented graphically

in Figures 3 and 4.

28

Each sub-graph corresponds to a different dependent variable, as indicated

above each plot. In each case, the effect in 2004 is normalized to zero, so all estimates are

28

The exact point estimates and standard errors for Figures 2-6 can be found in the Online Appendix. Estimates

corresponding to Figures 7-9 available upon request.

17

relative to that baseline year. We include a vertical line in 2005, which corresponds to the year

of Hurricane Katrina. We also add a horizontal line at zero to provide a reference point. Overall,

we see that for many of our outcome variables, there are little or no statistical differences

between our treatment and control groups prior to 2005. The similarities indicate that our

selection of control cities and propensity score weighting techniques are doing a reasonable job

of finding a comparable group for Hurricane Katrina victims.

Our results reveal that the hurricane had significant and notable effects on labor market

outcomes. In panel (a) of Figure 3, we see that prior to 2005 there is almost no difference in the

wage earnings of the New Orleans residents and the controls (this close correspondence is

mechanical because our propensity score includes pre-2005 wage income).

In the year of

Katrina, New Orleans residents experienced a negative wage income shock of approximately

$1,600 or about 4.4% of the mean wage income in the sample. This relatively small decline

reflects the fact that tax returns provide an annual measure of wage income; if we attribute the

entire loss to the last four months of the calendar year, the wage income fall constitutes a

substantively larger immediate economic impact on these households. The gap in wage income

increases to about $2,200 in the following year but, remarkably, disappears just two years after

the storm. Moreover, by 2010 wage incomes are on average almost $3,000 higher among the

New Orleans group.

29

Overall, the later wage income increases appear to more than offset the

initial drop.

We next consider two measures of unemployment that can be detected in tax return data.

The first is non-employment, as measured by an indicator for whether the household reported

29

Our results are similar if we look at adjusted gross income, which includes other sources of income such as capital

gains, dividends, and unemployment benefits. See Online Appendix Figures A4-A8.

18

any wage income (panel (b)). The second is the receipt of unemployment insurance benefits,

which have been taxable since 1987 (panel (c)). Both of these measures corroborate the evidence

found in our wage measure: a short-run decline in labor market outcomes followed by a quick

recovery. Specifically, there is no effect on non-employment in 2005, which is again an artifact

of tax returns containing annualized labor market outcome measures; much of the 2005 tax year

predates the storm. In 2006 and 2007, Hurricane Katrina victims are, respectively, 2.7 and 2.3

percentage points more likely to report earning no wage income than the control group. By 2008

that difference shrinks to 0.9 percentage points, and by the next year there is no difference

between the 2004 New Orleans residents and the control group.

Panel (c) shows that the pattern of unemployment qualitatively resembles that of income

and non-employment. New Orleans residents experience a 26 percentage point increase in the

probability of unemployment benefit receipt in 2005 and an 11 percentage point increase in

2006. The large magnitude of the increase in unemployment receipt likely reflects individuals

qualifying for the federal Disaster Unemployment Assistance program, which is available to

those who became unemployed because of a disaster but do not meet their state’s unemployment

benefits requirements. Additionally, in 2006 Congress passed legislation granting Hurricane

Katrina and Rita victims up to 13 extra weeks of unemployment benefits. Finally, Louisiana

loosened documentation requirements in the aftermath of the storm, raising the possibility that

some individuals who did not qualify for any unemployment program received compensation.

The spike in unemployment receipts is short-lived: in 2007-2010, New Orleans residents are 2-3

percentage points less likely to receive unemployment benefits.

In panel (d), we consider whether the negative impacts of Hurricane Katrina on wage and

salary employment were mitigated by transitions into self-employment. Following a drop of

19

about $75 in 2005, we find a significant $180 rise in self-employment income in 2006, which

corresponds to almost 18% of the mean self-employment income in our sample. In 2010, self-

employment income is about $200 higher than before the hurricane. However, given the low

magnitude and low frequency of self-employment in our sample, this increase does not augment

total income very much.

30

Our data also allow us to (imperfectly) observe the extent to which Hurricane Katrina

victims drew on their savings to weather the storm’s impact. The savings measure we consider is

gross distributions from retirement accounts, depicted in panel (e) of Figure 3. Typically,

retirement savings accounts are given preferential tax treatment in order to incentivize saving for

retirement and have penalties associated with tapping into these funds prior to a specific age.

Between August 25

th

of 2005 and January 1

st

of 2007, however, Hurricane Katrina victims could

withdraw up to $100,000 from their retirement accounts without incurring the early withdrawal

penalty. They could also spread taxes on these withdrawals over a three-year period.

31

These

policies were meant to provide easier access to retirement savings to buffer the shock of

Hurricane Katrina when precautionary savings proved insufficient. It appears that people took

advantage of this opportunity: retirement account withdrawals by Hurricane Katrina victims

increase by about $150 in 2005 and about $940 in 2006, a large increase compared to the sample

mean of $2,600. Annual withdrawals remain higher than those of the controls throughout the

30

About 85% of New Orleans residents reported no self-employment income in the pre-Katrina period.

31

The special provision was announced on October 17, 2005. See http://www.irs.gov/uac/Tax-Favored-Treatment-

for-Early-Distributions-from-IRAs-and-other-Retirement-Plans-for-Victims-of-Hurricane-Katrina.

20

sample period. The sum of the coefficients implies that Hurricane Katrina led to extra retirement

account withdrawals of about $2,800 per person over the sample period.

32

Given the persistence of withdrawals, a natural follow-up question is whether the storm

pushed some individuals to retire earlier than they would have otherwise. In panel (f), we look at

a more direct measure of retirement – whether or not the household is receiving any Social

Security payments. We find the opposite of what the retirement withdrawals suggest: the

hurricane caused people to be less likely to claim Social Security throughout the post-Katrina

period, thus suggesting that they are delaying retirement.

33

Our interpretation of these seemingly

contradictory findings is that the retirement account withdrawals are used to replace lost incomes

and destroyed assets. A negative wealth shock, especially one that hits close to retirement, is

likely to make an individual both draw down on savings and delay retirement in order to replace

those savings. However, it is also possible that the decrease in the propensity to claim Social

Security is at least partly driven by the disproportionate mortality of the elderly during the

onslaught of Hurricane Katrina.

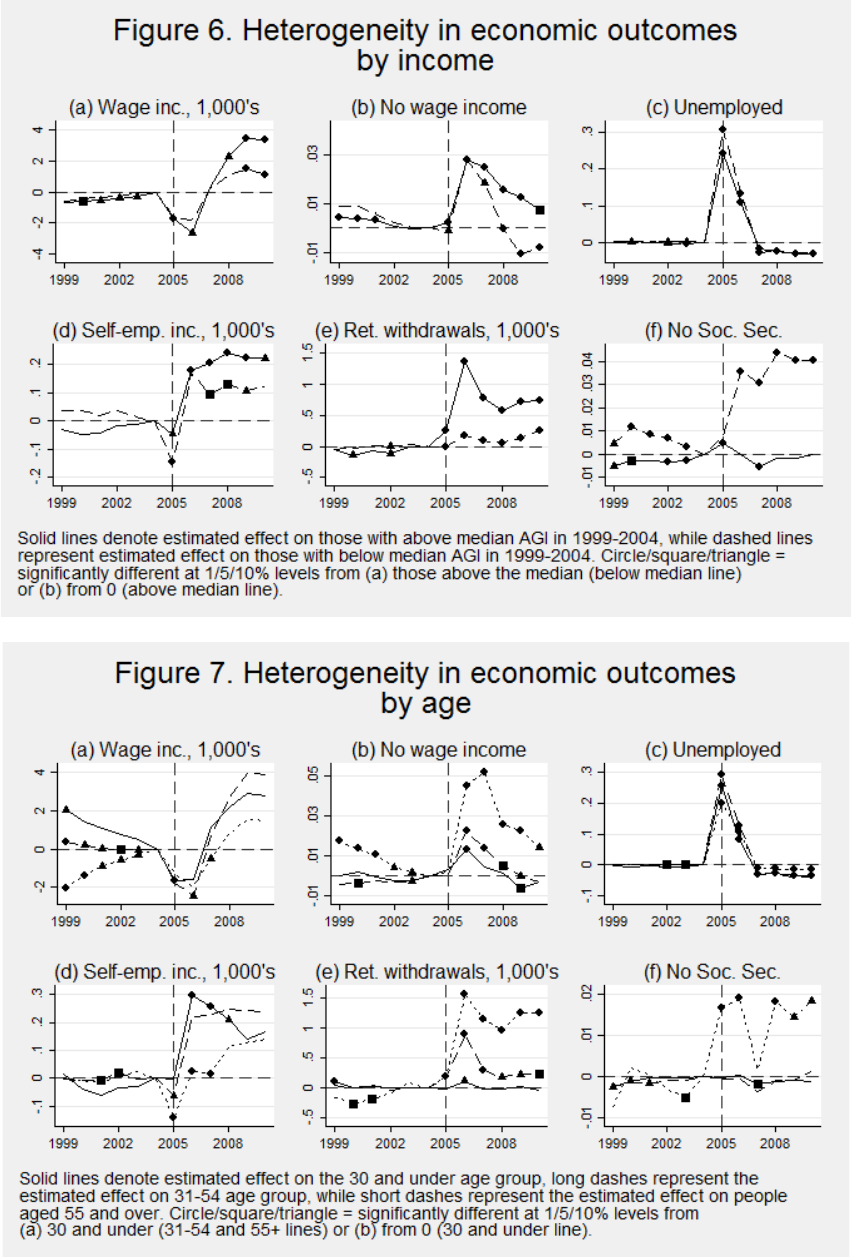

We next turn to effects of Hurricane Katrina on mobility. Panel (a) of Figure 4 reports

whether the household moved cities that year. Relative to control households, an extra one-

fourth of New Orleans residents left the city in the year of Katrina. New Orleans households are

also 8 percentage points more likely to switch cities the following year and 3 percentage points

more likely to switch cities in 2007. After that, mobility rates are not statistically significantly

32

In Figure A4 of the Online Appendix, we show that this increase is mostly driven by the extensive margin of more

individuals withdrawing money from retirement accounts.

33

Administrative difficulties in claiming Social Security are unlikely to be driving this result. A GAO report found

that the Social Security Administration was prepared for emergencies such as Katrina and that there were no

widespread problems with individuals receiving their Social Security benefits. See

http://www.gao.gov/new.items/d07219.pdf.

21

different between Hurricane Katrina victims and control households.

34

In panel (b), we look at

the probability of being in the 2004 city of residence. Relative to matched pairs, an extra 27

percent of New Orleans residents have left their city in 2005. Over time, that gap falls roughly in

half as people move back to New Orleans.

Panels (c)-(f) of Figure 4 shows the estimated impact on household composition, namely

the number of child dependents claimed and whether the tax filer is married, as proxied by a

married filing jointly status. There are fewer child dependents claimed among New Orleans

residents in 2005 and 2006, but that gap becomes statistically insignificant in 2007. The

estimated impact is relatively small (0.01 fewer children per household). Because Hurricane

Katrina struck in August of 2005, the drop in the number of children in that tax filing year cannot

correspond to deliberate fertility decisions. However, it could be the result of higher infant

mortality or fewer adoptions, either of related or unrelated children. It may also reflect a decrease

in the number of children living with a New Orleans resident. In the next section, we postulate

that this effect most likely reflects a change in living arrangements rather than a fall in fertility.

Finally, we look at the probability that the tax filer is married (panel (d)). An unexpected

pattern emerges, with the Katrina shock associated with an increase in the share of married

households. The probability of being married continues to grow over the next few years before

stabilizing. The absolute magnitude of the difference is not that large – it reaches about 0.8

percentage points – but is statistically significant. To understand the source of this gap, the next

two pictures show results corresponding to whether the tax return status changes to be newly

34

The estimated coefficients are nearly identical when we look at movement between zip codes as opposed to

between cities, i.e. there is little differential within-city movement of New Orleans residents relative to the controls.

22

married or newly divorced. New Orleans residents are more likely to marry in 2005 and 2006,

but are not less likely to divorce.

Heterogeneity

We explore three key dimensions across which one might expect the economic impact of

the hurricane to be heterogeneous: (1) whether a household’s own home was adversely affected

by the storm, (2) pre-Katrina (2004) income, and (3) age. We should note that these measures

are not unrelated. The average age for those with above (below) median pre-Katrina income is 47

(42), and those who lived in the worst affected areas also had lower incomes, on average. In this

section, we focus on the economic outcomes, and relegate the results on mobility, marriage,

divorce, and number of dependents to the Online Appendix.

While we cannot directly observe the hurricane’s impact on an individual house, we can

use the location of the home as a proxy for the degree of property damages likely experienced by

households in New Orleans. On December 9, 2005, FEMA issued an announcement classifying

10 New Orleans zip codes as “look and stay” zip codes and 7 as “look and leave”.

35

The other

two New Orleans zip codes had no restrictions.

The residents of “look and stay” zip codes were

allowed to return to their homes permanently at that time, if they wished. Those who resided in

the “look and leave” zip codes, which had the greatest damage, could return during the day to

conduct repairs as often as they wished but were not allowed to spend the night. Residents in

these latter zip codes were on average more deeply harmed by Katrina than the rest of New

35

The full text of the announcement can be found on http://www.fema.gov/news-release/residents-17-orleans-

parish-zip-codes-may-return-home-inspect-damage.

23

Orleans.

36

We estimate the long-run impact on these three groups by allowing the effect of

Katrina to vary by whether households resided in (a) a “look and leave” zip code (“LAL”), (b) a

“look and stay” zip code (“LAS”), or (c) a part of the city that was essentially undamaged

(“other”).

37

We do not re-match individuals, and we derive estimates for all three groups from a

single regression to enable us to conduct statistical tests of heterogeneity.

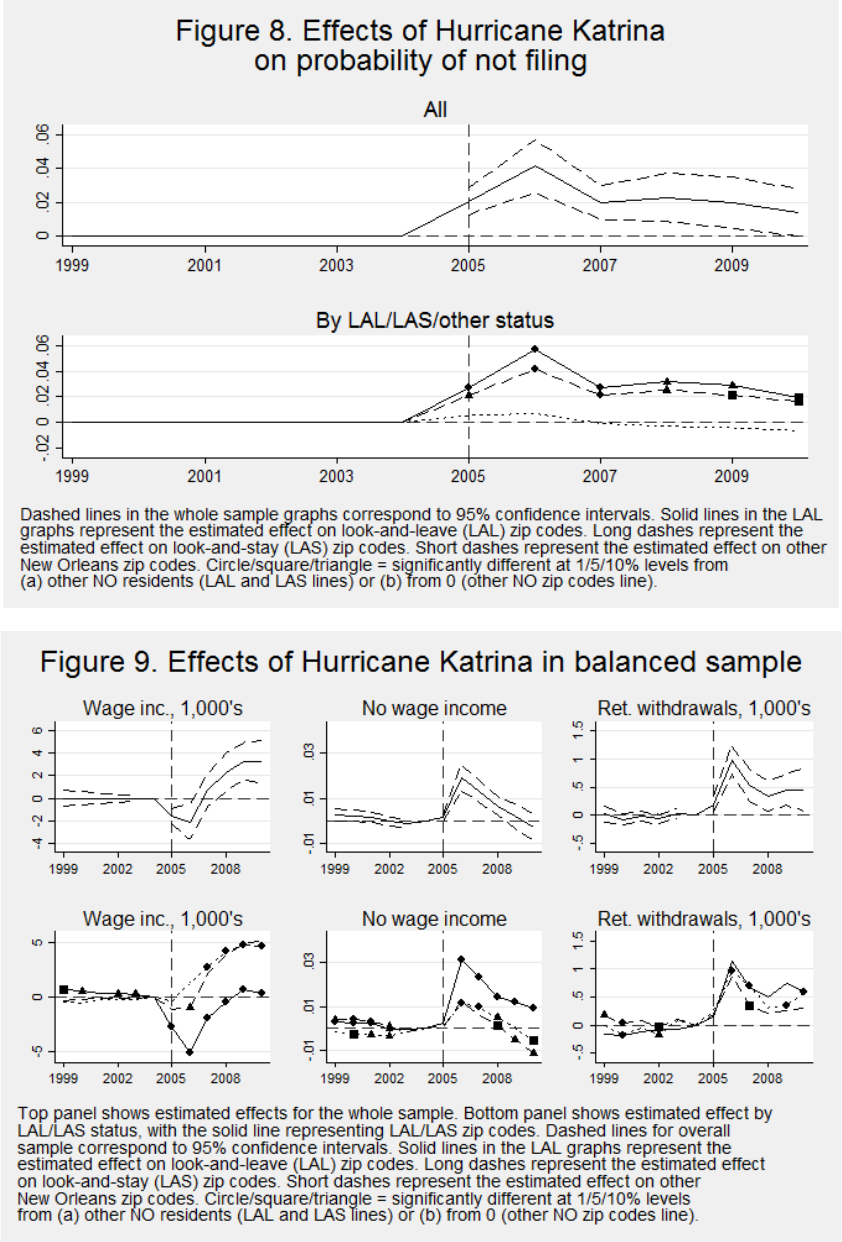

Figure 5 presents a series of pictures similar to those in Figure 3, but dividing the sample

of New Orleans residents into the three groups described above. The solid lines represent the

path of outcomes for LAL residents. The long dashed lines correspond to the outcomes for LAS

residents, while the short dashed lines correspond to the other zip codes. The square, triangle,

and circle symbols on the LAL and LAS lines represent statistically significant differences

between these zip codes and the other New Orleans zip codes which suffered little damage in the

storm, at the 10, 5, and 1 percent level, respectively. The same symbols on the “other” lines

correspond to statistically significant differences from zero.

38

Overall, we find a high degree of correlation between the extent of physical damage

caused by the storm and the negative impact on labor earnings of residents in those areas.

Residents in unaffected areas experience very little in terms of adverse consequences from the

storm. First, they experience no significant wage drop in the aftermath of the storm (panel (a)).

36

The “look and leave”/“look and stay” classifications closely correspond to the extent of flooding. Using post-

Katrina flood maps published by FEMA, we calculate that the mean flood depth exceeded 4 feet in each “look and

leave” zip code, but did so only in one “look and stay” zip code. One of the two zip codes with no restrictions and

three “look and stay” zip codes experienced little or no flooding.

37

We do not distinguish between home-owners and renters in this analysis. While such information is not directly

measured on a tax return, there is some information on a tax return that would identify those who are likely

homeowners: home-mortgage interest deductions and deductions for property taxes paid for those who itemize. This

measure does not capture individuals who have paid off their mortgages and do not pay enough in property taxes for

itemization to be worthwhile. Some results on home-owners versus non-homeowners are provided in Online

Appendix Tables A9-A11.

38

The point estimates for these and other figures can be found in Online Appendix tables. The tables also show

which estimates are statistically different from zero for all three groups.

24

In 2007, their wage incomes begin rising, ending up about $4,500 higher at the end of the sample

period than before Hurricane Katrina. Those in the LAS areas experiences modest wage income

drops of about $1,300 in 2005 and $1,100 in 2006. At the end of the sample period, their wage

incomes are almost $4,700 higher than before. The drop in wage income is concentrated among

those who lived in areas with the greatest damage: their wage incomes are on average $2,600

lower in the year of Hurricane Katrina and about $5,100 lower the year after that. The fall

begins reversing itself in 2007. By 2010, the 2004 LAL residents are earning as much as the

control group, though significantly less than the rest of New Orleans. Part of the reason for the

LAL group falling behind the rest of New Orleans is that those in LAL zip codes are much more

likely to report no wage income compared to the other two groups and the controls throughout

the post-Katrina period (panel (b)).

The three groups look very similar in terms of unemployment receipts (panel (c)),

although the initial increase is significantly higher among the LAL zip codes compared to the

rest of New Orleans. The similarity is understandable because much of the short-term

unemployment was driven by the disappearance of tourism and other economic activities, the

effects of which were felt across the board. Moreover, the locations where individuals from these

three groups worked may be very similar in terms of sustained damages.

The second row of Figure 5 shows the estimated effects on self-employment income,

retirement account withdrawals, and Social Security claims. The longer-run increases in self-

employment income are concentrated among the LAS residents, who are earning almost $400

more in self-employment income by the end of the sample. We see an increase in retirement

account withdrawals among all three groups. Some of this may be driven by general economic

conditions, as seen in the increased unemployment benefits for all three groups; alternatively,

25

this effect could reflect the fact that withdrawals from retirement accounts became easier due to

the early withdrawal penalty exemption. Finally, in panel (f) we see that the decrease in Social

Security claims is concentrated among the LAL/LAS residents, while residents from other zip

codes actually become more likely to claim Social Security.

Another determinant of how well people were able to cope with the storm may be their

pre-Katrina wealth. Tax returns unfortunately do not measure a household’s stock of wealth. To

look at these differences, we divide the sample in half by whether the household’s average 1999-

2004 adjusted gross income (AGI) was above or below the median 1999-2004 New Orleans

AGI, which is roughly $18,700 in our sample. AGI captures many income sources, such as wage

earnings, business income, capital gains, and income from savings, so this income flow measure

should be correlated with a measure of the stock of wealth.

The results for our measures of labor market outcomes are shown in Figure 6. The initial

wage income declines look similar for both groups, implying that the relative fall is larger for

those with lower earnings.

39

By the end of the sample, both groups are out-earning the control

group, but the income gain of the above-median AGI group exceeds that of the below-median

AGI group by over $2,000.

The fraction of people in each group reporting no wage income is nearly identical in

2006. However, in subsequent years, the above-median income group is much more likely to

report no wage income than the below-median income group and the control group. By 2010, the

below-median income group is more likely to have wage income than the controls, whereas the

above-median income group is less likely to do so. Those with below median income are more

likely to report unemployment income in 2005 and 2006, but the overall patterns of

39

The mean 2004 wage income for those with below and above median AGI is $10,261 and $43,029, respectively.

26

unemployment receipts are very similar (panel (c)). The long-run increases in self-employment

income are significantly higher for the above-median AGI group.

Those with above-median AGI take significantly more out of their retirement accounts

than those with below-median AGI (panel (e)). In 2006, the retirement account withdrawals of

the above-median AGI group increase by almost $1,400 while those of the below-median AGI

group increase by only $180.

40

This differential reliance on retirement savings may reflect that

higher AGI corresponds to higher levels of savings inside retirement accounts. Finally, the

hurricane did not appear to have a consistent effect on Social Security claiming behavior of those

with above-median AGI, while reducing the likelihood of claiming Social Security for the

below-median AGI group by 3-4 percentage points.

The final source of heterogeneity we consider is age. We divide the sample into three

groups based on the age of the primary filer in 2004: (1) those 30 or younger, (2) those aged 31-

54, and (3) those 55 or older. The results are shown in Figure 7. Overall, we find similar wage

income trajectories for all three groups (panel (a)), but the largest and most persistent declines in

labor market participation are experienced by the oldest households (panel (b)). Specifically,

while the initial wage income drop and subsequent recovery are very similar for tax filers or all

ages, the oldest households are significantly more likely to report no wage income for most of

the sample period. Short-term unemployment compensation does not correspond with these

apparent declines in labor market participation, with the oldest households having a slightly

lower probability of reporting unemployment benefits in 2005 and 2006 than those who are

between 31 and 54. However, at the end of the sample period, the unemployment benefit receipt

probabilities among the oldest residents are significantly higher than their younger counterparts’,

40

Much of these increases are driven by the extensive margin of an increased probability of withdrawing from

retirement accounts. See Appendix Figure A6.

27

although all three groups are significantly less likely to report receiving unemployment insurance

income than the control group.

The other income sources that we consider reveal interesting differences in responses to

the wage losses resulting from the storm. Those who are under 55 experience the largest gains in

self-employment income (panel (d)). This response could reflect that becoming self-employed is

difficult for older individuals. However, the estimates at the end of the sample period are noisy

and we cannot detect statistical differences between any of the three age groups in 2010. At the

same time, the oldest households withdrew significantly more money from their retirement

accounts than younger households (panel (e)). Those 30 and under withdrew $115 more in 2006

but otherwise did not draw on their retirement savings, possibly because they did not have many.

Both the 55 and over and the 31-54 age groups continue to have higher retirement withdrawals

than the control throughout the post-Katrina period. Unsurprisingly, the oldest households are the

ones who experience the reduction in the probability of claiming Social Security (panel (f)).

Finally, in the Online Appendix, we show that the decrease in the number of dependents

is concentrated in the 55 and older group. This finding suggests that this decrease may not reflect

fertility, but rather grandparents becoming less likely to be the primary caregiver of their

grandchildren, or older children becoming independent filers following Hurricane Katrina.

Robustness

One concern about our analysis is that we are only capturing the effect on those who file

tax returns. This should be somewhat mitigated by the fact that everyone in our preferred sample

files in years 1999-2004; thus, our results are less likely to be affected by individuals who rarely

28

file. Nevertheless, selective filing can bias our results, especially if Hurricane Katrina changed

the probability of filing a tax return.

Figure 8 shows the effect of Katrina on non-filing behavior for the whole sample, and by

LAL/LAS/other status. Following the hurricane, New Orleans residents are significantly less

likely to file a tax return in each year prior to 2010.

41

Non-filing is particularly pronounced

among those from “look and leave” or “look and stay” zip codes; people from these zip codes are

4-6 percentage points less likely to file in 2006, and 2-3 percentage points less likely to file in

subsequent years. There is no effect on filing behavior in the rest of New Orleans. Because lower

income individuals are generally less likely to file, we might be underestimating the negative

effect of Hurricane Katrina on the overall population by using an unbalanced sample of

taxpayers.

To verify that selective filing is not driving our results, we restrict the sample to

individuals who file each year. The results for three outcomes, wage income, non-employment,

and retirement account withdrawals, are shown in Figure 9. The top panel shows the estimates

for the whole sample, while the bottom panel shows the differential effects by damages to one’s

neighborhood. Overall, selective filing does not appear to be driving our results. The point

estimates and significance levels for all three outcomes as well as most other outcomes not

shown in this figure are very similar to the unbalanced results.

42

41

To calculate the propensity score, we require tax filing units to be present in each year from 1999 through 2004,

resulting in literally no pre-period differences between the control and treatment groups.

42

In the balanced sample, we also estimate a slight but significant increase in divorces in 2006 and a persistent

decrease in the probability of having self-employment income. Additionally, the 2007 dip in the Social Security

estimates disappears. See Online Appendix Figure A7 for more estimates. A full set of results is available upon

request.

29

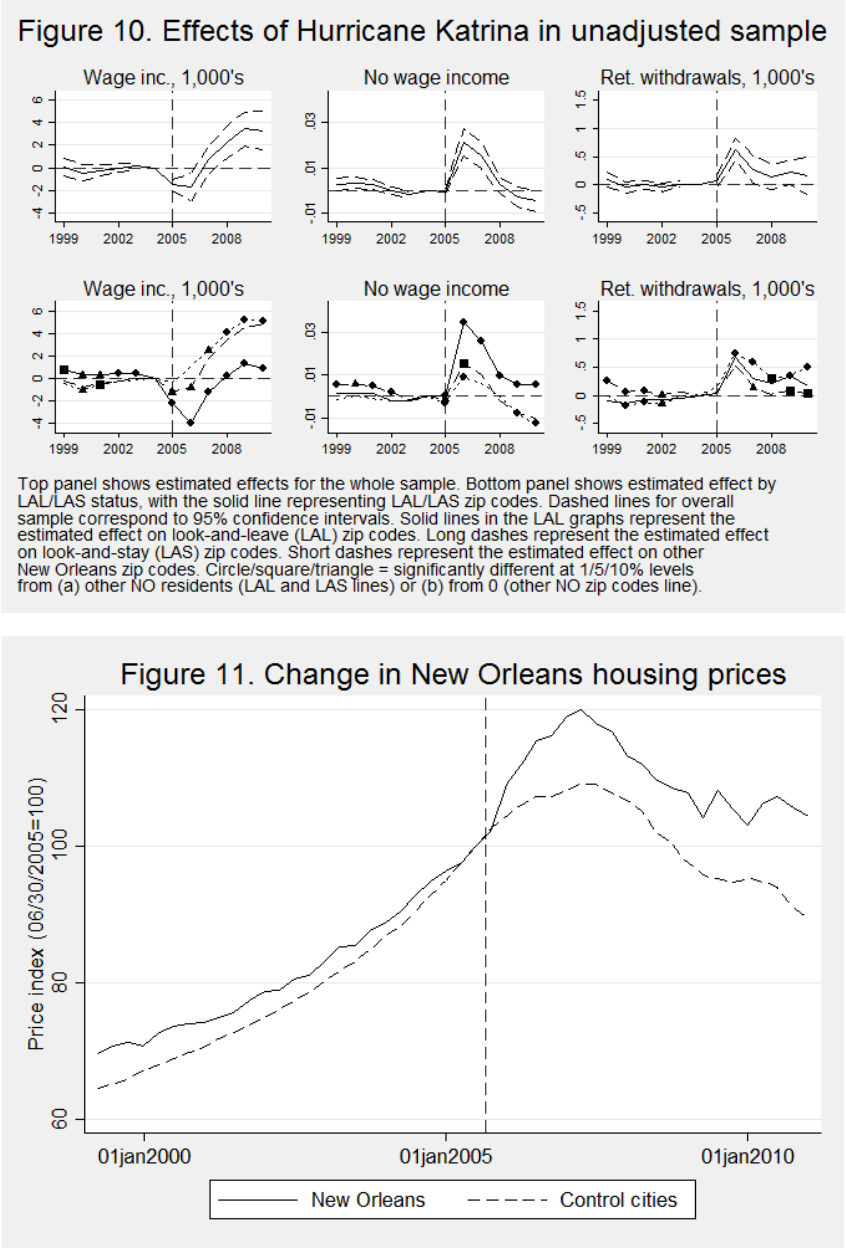

Finally, Figure 10 shows the estimated effect of Hurricane Katrina if we make no

adjustments to the control group, using the full random 10% sample from the ten cities listed in

Table 1. Here, we do not require that the household filed taxes in each year between 1999 and

2004. We also do not employ propensity score weighting or restrict the sample to have common

support. Our results for wage income, non-employment, retirement account withdrawals, and

other outcomes not shown here are very similar to the weighted estimates.

43

Our results are also similar when we use nearest neighbor matching instead of propensity

score weighting. Specifically, we can match each New Orleans resident with the control

individual who has the closest propensity score, with and without imposing the common support

restriction. Again, the point estimates and significance levels closely resemble those from our

preferred empirical implementation. One significant exception is that we estimate a slight

increase in marriage in 2008 and 2009 for the non-LAL/LAS residents. However, given the

number of estimated coefficients, this amount of variation in estimates seems reasonable.

Finally, our results are similar if we use Mahalanobis matching, where the pairs are matched

using the pre-Katrina characteristics themselves rather than the propensity score.

A final question is whether the US recession that began in December of 2007 would have

had a similar impact on New Orleans as it did on the controls. In particular, several cities in the

control group, such as Detroit and Gary, have a more industrial economy than New Orleans. The

impact of the recession could have been larger for these cities, biasing our results. Although the

question of how New Orleans would have weathered the recession absent Hurricane Katrina is

43

There are a few differences between the unadjusted estimates and our preferred estimates. Specifically, in the

unadjusted sample, we find lower point estimates for the no wage income indicator and no decline in the number of

dependents. These differences can be explained by differential pre-trends: Katrina victims have higher non-

employment and more dependents in the pre-period. The two differences that do not appear to be driven by pre-

trends is that we find a significant decline in divorces in 2005 and a persistent increase in new marriages when we

don’t use propensity score weighting.

30

fundamentally unanswerable, it is possible to see whether the industrial cities in our control

group were disproportionately affected by the recession. We use Regional Economic Information

System (REIS) data published by the Bureau of Economic Analysis to look at the relative impact

of the recession on the counties in which our control cities are located.

44

Except for Portsmouth

and Baltimore, all of the cities experience a drop in real per capita income between 2007 and

2009. The largest falls (ranging from 8.2 to 8.6%) are in Memphis, Birmingham, and Richmond.

Detroit has the largest fall in the average wage income, however, losing 4.3% between 2007 and

2009. It is followed by Jackson, Newark, St. Louis, and Memphis, where wage income falls by

1.4-2.1%, suggesting that the recession’s impact was not necessarily worse for more industrial

cities. Nevertheless, we exclude Detroit from our control sample as a robustness check. The

estimated wage income and employment effects are very similar, suggesting that heterogeneous

impacts of the recession are not driving our long-run estimates.

Section IV: What explains higher post-Katrina wage income for storm victims?

The results presented above are surprising on two dimensions: (1) how small and

transitory the labor market shocks are for the storm victims, and (2) in just a few years the

income of those hit by the hurricane actually exceeds those of matched controls. These results

stand in stark contrast to studies that track workers over time and find large and long-lasting

wage declines following job losses caused by plant closings, sectoral declines, environmental

regulation, or other economic shocks (e.g., Ruhm 1991; Jacobson et al. 1993; Neal 1995;

Schoeni and Dardia 2003; Kodrzycki 2007; von Wachter et al. 2009; Couch and Placzek 2010;

44

Detailed results available upon request. Baltimore, Portsmouth, Richmond, and St. Louis are independent cities.

For them, REIS provides personal income information at the city level.

31

Walker 2013). A weather-induced shock like Hurricane Katrina is, of course, different from

these economic shocks, most of which devalue a worker’s industry-specific human capital.

Thus, one might plausibly predict that wage incomes of those hit by the hurricane would

eventually equilibrate.

45

What is harder to understand is why income actually outpaces the

controls.

One possibility is that the income differential reflects increases in the cost of living, i.e.

the higher wage incomes do not reflect a real change in the standard of living, but rather, simply

compensate for price changes. This could happen through two mechanisms. First, New Orleans

may have become a more expensive place to live after the storm. A substantial fraction of the

housing stock was destroyed and regulatory restrictions were placed on where new structures

could be located and how they needed to be constructed. The reduced supply of housing could

increase the rental rate of housing, if not offset by reduced demand. Second, if New Orleans had

a low cost of living before the storm relative to the locations where the displaced New Orleans

residents settle, then observed nominal wage incomes might be expected to rise, even though real

wages are unchanged.

To examine whether an increase in the cost of living in New Orleans could explain the

income increase, we compare post-Katrina housing prices in New Orleans and in our control

cities using the Federal Housing Finance Agency (FHFA) housing price index.

46

The

45

Although, our unscientific poll suggests this is not what economists predict. In conversation, we have asked

roughly 20 academic economists what their prediction is regarding the income path of Katrina victims. Virtually

every economist has predicted a larger immediate income decline, greater persistence in income losses, and a steady

state with permanent income losses.

46

The FHFA index is quarterly and is constructed from repeat transactions on single-family homes, excluding loans

that do not conform to Fannie Mae or Freddie Mac loan limits. The geographic areas in the FHFA index are slightly

larger than our control cities. For example, in the FHFA data, New Orleans is combined with neighboring Metairie

and Kenner. To the best of our knowledge, broader regional cost-of-living measures are not available for New

Orleans. ACCRA Cost of Living Index, which includes groceries, utilities, transportation, health care, and other

32

seasonally-adjusted housing price indices for New Orleans and the control cities are shown in

Figure 11. We normalize the June 30

th

, 2005 index values to 100 for both groups.

47

The vertical

dashed line corresponds to August 29, 2005, when hurricane Katrina hit. Prior to Hurricane

Katrina, the housing price index in New Orleans was on average 4% higher than the index for

control cities, although the two series appear to be converging. Hurricane Katrina clearly led to a

sudden and persistent increase in New Orleans housing prices: in the 21 full quarters following

the hurricane, New Orleans house prices are nearly 10% higher than the control group. The

difference grows over time, reaching about 15% in 2010. Thus, by the end of our sample period,

the change in the difference in housing prices almost exactly corresponds to the observed

increase in wage income. Housing is, of course, only one component of overall living costs.

Without better data, it is difficult to know whether cost of living increases fully offset the

nominal increases in wages we observe among Katrina victims.

48

A second possible explanation for the positive long-term impact of Katrina on its victims

are large fixed costs of moving. If moving costs (either financial or psychological) are high, then

people will rationally forego higher earnings available elsewhere unless the expected benefit of

moving is large enough to outweigh the fixed cost. The forced relocation caused by the

hurricane required displaced residents to pay the moving costs, leading to higher wages

(although potentially lower utility levels). Indeed, Kennan and Walker (2010) estimate these

goods and services, in addition to housing prices, does not provide data on New Orleans in any post-Katrina year

except for 2009. For more details, see the FHFA Technical Documentation and the FHFA FAQ website

.

47

Data for the FHFA index are collected monthly from Freddie Mae and Fannie Mac; thus, Hurricane Katrina will

not have affected the June 30

th

index value.

48

Our results are very similar if we use the Freddie Mac housing price index or the seasonally unadjusted version of

the FHFA index. Using the ACS, we estimate a percentage increase in monthly rents paid by renters that is roughly

twice the magnitude of the increase in housing values. One explanation for this difference is that home owners

perceive the rise in housing values to be temporary and therefore anticipate future price depreciation relative to other

markets. If that is the case, home owners demand a higher short-run rental rate in order to be willing to hold the

depreciating asset.

33

fixed costs of moving to be enormous: roughly $300,000 in their sample. This means that even

with reasonable discount rates, a worker might forego $10,000 a year in income if it requires

relocation. The magnitude of the wage increases we see empirically is well within that range.

One prediction of this model is that we should observe higher incomes for people who

leave New Orleans, but not necessarily for those who stay. However, when we split the sample

into who left the city in 2005 and those who did not, we find the opposite pattern: in 2007-2010,

the incomes of “leavers” are significantly lower than the control group’s while the incomes of

“stayers” are significantly higher.

49

This is despite the fact that prior to Hurricane Katrina, the

group that would leave New Orleans has significantly higher earnings than the control (although

the leavers’ wage incomes exhibit a downward trend as well). Of course, these results are

relatively weak evidence against this hypothesis because we ultimately cannot isolate the

exogenous component of the decision to leave New Orleans.

A third possibility is that the Katrina experience and its aftermath changed people in a

fundamental way. For instance, exposure to tragedy might affect a person’s values, identity,

level of risk aversion, etc. These changes might be associated with a greater commitment to the

labor market.

50

One manifestation of this phenomenon might be increased investment in

education, which would also be consistent with a story in which the temporary lack of jobs

makes the opportunity cost of obtaining education lower. Given the limits of our data, it is not

obvious how to convincingly test this hypothesis.

A final explanation for the patterns observed – which again is not easy to test in our data

– is that the storm destroyed assets which were not fully insured, which increased the marginal

49

Results available upon request.

50

Anecdotally, at least, it is said that those who grew up in the Great Depression had a lifelong commitment to

frugality.

34

benefit of work. The fact that earnings in neighborhoods that were essentially unaffected by

Katrina also outrace earnings in the control group (see Figure 5) provides indirect evidence

against this explanation.

Section V: Conclusion

Hurricane Katrina massively and unexpectedly disrupted the lives of New Orleans

residents. The local economy essentially shut down, and hundreds of thousands of people were

forced out of their homes. It is not surprising that the immediate economic experiences of the

storm victims were negative. What is remarkable, however, is the rapidity with which their

economic situation recovered. In our data, within just a handful of years, income of those

affected by the storm actually surpasses those of a matched control group.

Our results have broader implications for several policy areas. With respect to federal