Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 1

Huawei ITO Utilizes Key ICT

Transformation Metrics to Deliver

Next Generation of IT Services

Key Service Provider Metrics Market Study

February 2016

TBR

TECH N O LO GY BU SIN ESS RESEARCH , IN C.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 2

TBR

Table of contents

1. Telecom operators face ICT disruption

2. The rationale for IT outsourcing to support ICT transformation

3. Success metrics for ITO

4. Huawei’s ITO offerings form a comprehensive solution

5. Operators leverage Huawei’s ITO solution for ICT transformation

6. TBR perspective

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 3

Telecom operators face ICT disruption

To say telecom operators face challenging business conditions is an understatement. They

operate in an industry where traditional services enabled by a standard telecom

infrastructure are no longer enough. Lower costs and accelerated time to revenue are

required to prevent operator business models from failing.

“We cannot survive the way we are going,” said Telefonica CTO Enrico Blanco. “Traffic

grows at 50% every year and 100% in some countries. Our network will be growing; we

will be improving access and improving capabilities every day. But revenues are not

growing at this rate; we have to lower our cost. We need to use additional business levers.

In my mind there are no options — now is the time.”

Blanco’s sentiments reflect boardroom discussions worldwide. The industry faces

limitations in cost control and revenue growth:

Factors preventing cost control:

o Opex out of control — In 2015 average opex grew from 77% of total

operator spend to 82% to fund expanding network operations, according to

TBR’s review of global operator spending based on company financial

statements.

o Data growth without limit — Data traffic is estimated to grow tenfold by

2019, requiring continued capacity builds and spectrum purchases,

according to operators interviewed by TBR.

Factors preventing revenue growth:

o Price wars — Disruptive operators that start price wars, lowering average

revenue per user (ARPU) for everyone, are operating in saturated markets

where subscriber growth is limited.

o Digital competition — Digital service providers (including cable, over-the-

top and cloud firms) are competing through “freemium” and advertiser-

sponsored services, squeezing the ability of operators to earn revenue from

data.

Operators have tried to add new services to their business models with mixed results,

largely because their costs have not changed and services revenue growth is limited. This

dilemma is similar to that faced by their peers in the information and communications

technology (ICT) industry. The industry is evolving rapidly as new technologies and

economic models disrupt traditional businesses. TBR benchmarks continue to track flat or

declining revenue across traditional segments such as telecom and IT, while new

segments such as cloud, software-defined data center and digital business grow at

double-digit rates. New products, services, value chains and business models are required

as evolution shakes the foundation of the ICT business.

Increasingly, telecom operators must see themselves as ICT companies. They must find

market share, revenue and profit in the new economy, and evolve and compete with their

infrastructure in new ways.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 4

TBR

The rationale for IT outsourcing to support ICT transformation

Rapidly moving to a more competitive ICT infrastructure requires telecom operators to

reconsider or adapt investments to manage their evolving networks. TBR research

indicates three types of approaches to technology management are emerging in the new

paradigm:

1. Investing in business outcomes, enabled by technology, where a third-party

supplier provides the innovative platforms and the operator leverages those

platforms to create business value

2. Building solutions, but outsourcing technology components

3. Owning and controlling the solution and the basic technology with a goal of using

the technology to innovate to create differentiated business value.

TBR believes operators are shifting their budgets — as much and as quickly as possible —

from buying, assembling and integrating technology components. Operators are instead

purchasing supplier offerings that deliver their needed outcomes (approach No. 1 or No.

2), due to the realization the best way to reap the innovation of ICT infrastructure is to

acquire it from suppliers rather than creating it in their labs. Also, industry pressures

increasingly dictate the time-to-market advantages of acquiring built technology.

Operators are realizing the value of business-outcome-based investment at a time when

they must also evolve their infrastructures. This combination is leading rapidly to a new

wave of outsourcing where operators are seeking new relationships with suppliers. PwC

calls this wave “second-generation outsourcing,” and one executive stated it is “turning

over entire domains — such as IT, mobile network operations and cable networks — to

vendors.” The executive went on to say, “The goals of this effort, which we call re-

sourcing, are to gain greater flexibility in transforming their own operational models, to

restore some of the capabilities lost in turning over operational control to vendors in the

past and to reboot their innovation efforts.”

TBR believes this form of outsourcing is becoming a preferred way to drive infrastructure

evolution toward more agile ICT infrastructure. Critical to this approach is the evaluation

of initiatives in the separate domains of network operations and IT/data center. The new

ICT infrastructure requires convergence of these domains. Many operators started

evolving their networks. What is needed is a parallel IT outsourcing (ITO) program that

will evolve to match the requirements of the new network infrastructure.

Furthermore, the evolution of ITO supports the requirement for operators to extend

business models deeper into the enterprise, where similar evolutions are taking place.

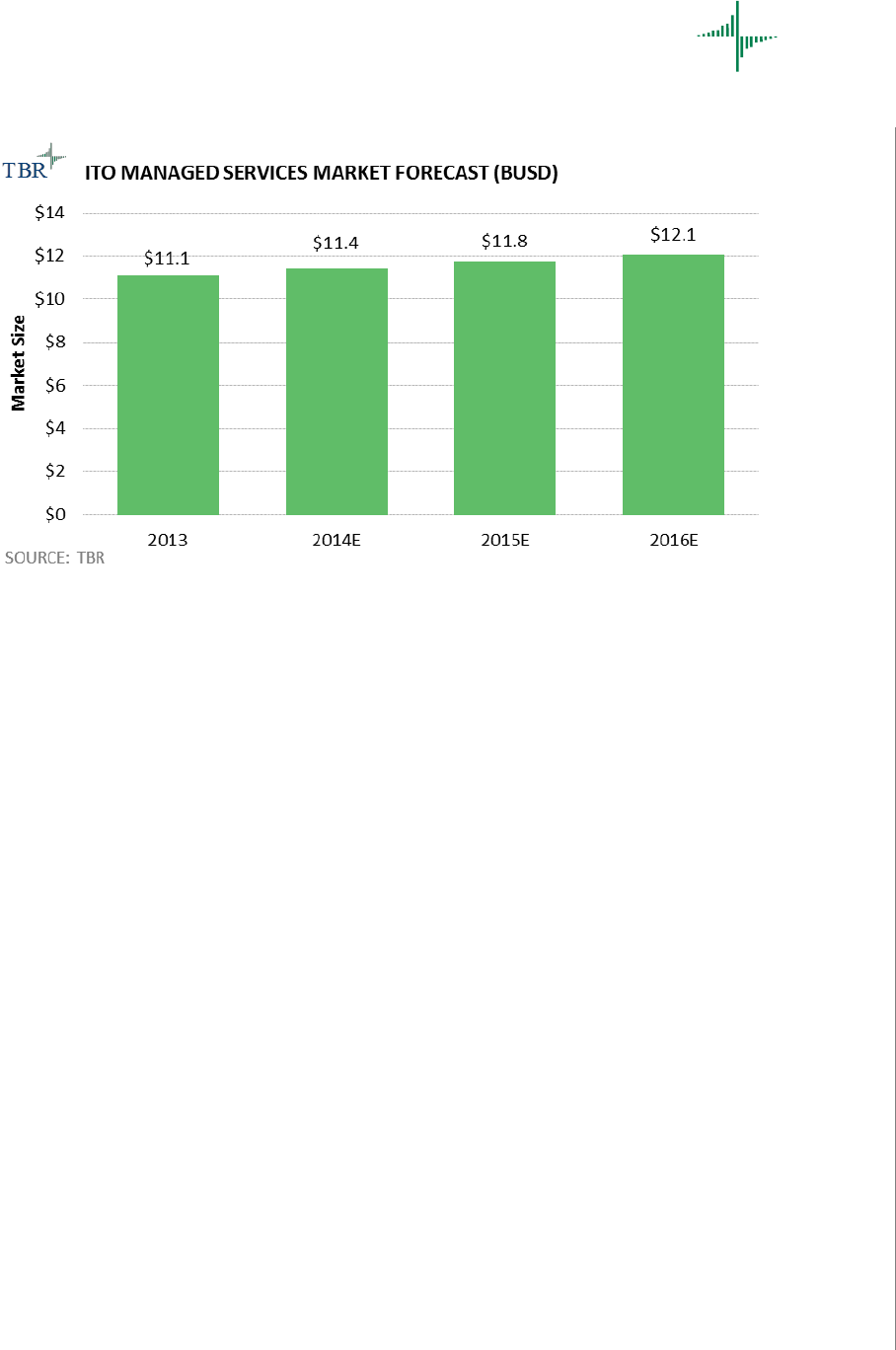

TBR’s Telecom Infrastructure Services Benchmark indicates that for ITO, managed services

will remain a significant investment area as part of ICT transformation. The market is

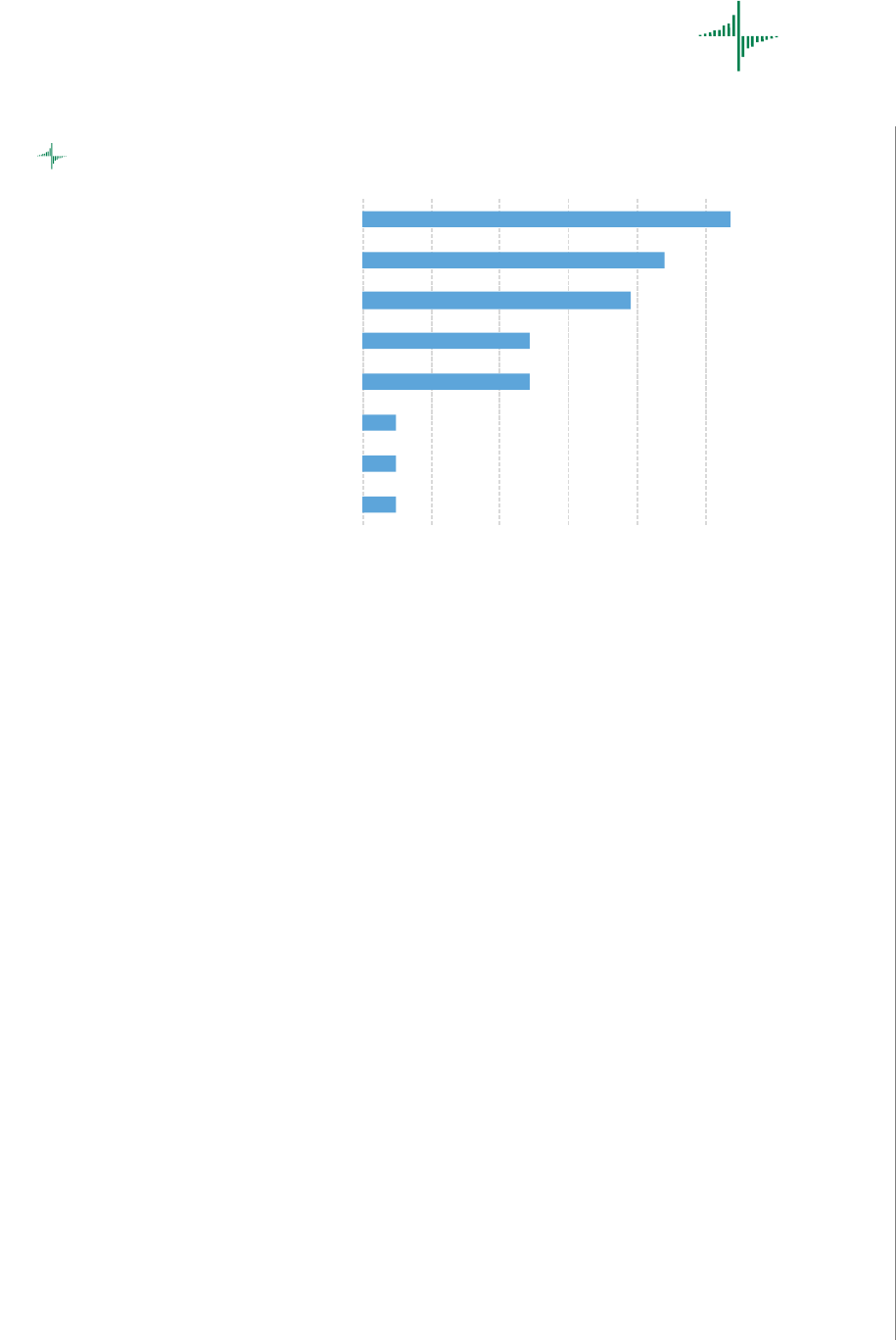

estimated to grow to $12.1 billion in 2016, according to TBR (Figure 1).

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 5

TBR

Figure 1: Operator spending on managed services for ITO

Success metrics for ITO

While operators routinely expect 20% to 30% opex reduction from cost-savings-driven

outsourcing, the second-generation multidomain outsourcing driven by business

outcomes requires a new set of metrics to assess value.

ITO, in particular, requires a different measurement approach as the conventional IT

metrics are limited to generic data centers, not the operational requirements of telecom

operators.

TBR conducted interviews with regional operators engaged in outsourcing to determine

which metrics they are applying, or would like to apply, to their ITO engagements. TBR

fielded a study in December 2015 and January 2016 with the following objectives:

Uncover key metrics that will help define how to measure success of ITO services

based on primary research from service providers.

Uncover insights on industry trends and challenges and uncover demands of

carriers for the ICT transformation process for internal transformation and for

enterprise customers.

TBR included large telecom operators such as Millicom, MTN and Telefonica in its study,

conducting in-depth interviews with senior managers with insight into their organizations’

ITO and ICT transformation processes.

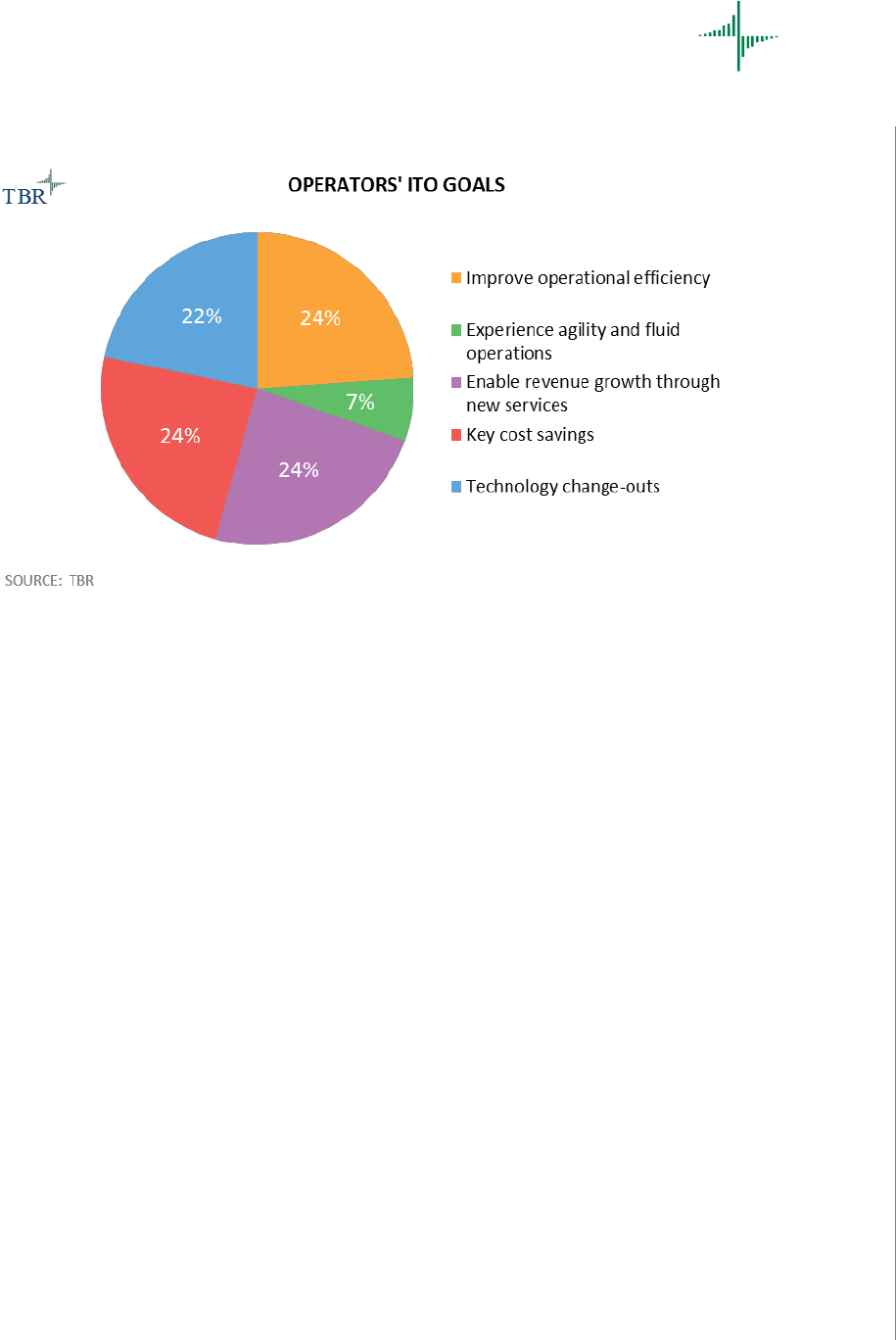

The operators interviewed still placed cost savings as the highest priority, tied with

improving operational efficiency (which drives cost savings) and enabling revenue growth

by introducing new services. Respondents also gave significant weight to evolving

technology infrastructure through platform change-outs. The goal of increasing overall

agility and fluid operations was the lowest priority (Figure 2). TBR believes as

organizations enter ICT transformation, agility will become a more prominent goal.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 6

TBR

Figure 2

New services appear to be the major additional driver of cost savings. One senior

manager stated the purpose of ITO was to “enhance the innovation process, thereby

offering new products by moving toward the digital world and meanwhile enhancing our

facilities in areas of procurement.” The manager continued, “With regard to the service

that we have implemented [this] includes enterprise and M2M [machine-to-machine]

technology.”

While operators’ ITO goals remain fairly consistent (Figure 2), varied approaches to

metrics enable them to drive their ITO engagements in different directions. For example,

how cost savings, operational efficiency, new service growth and agility are measured

helps define the nature of the technology platforms required, the number of domains

included and the scope of the agreement with suppliers.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 7

TBR

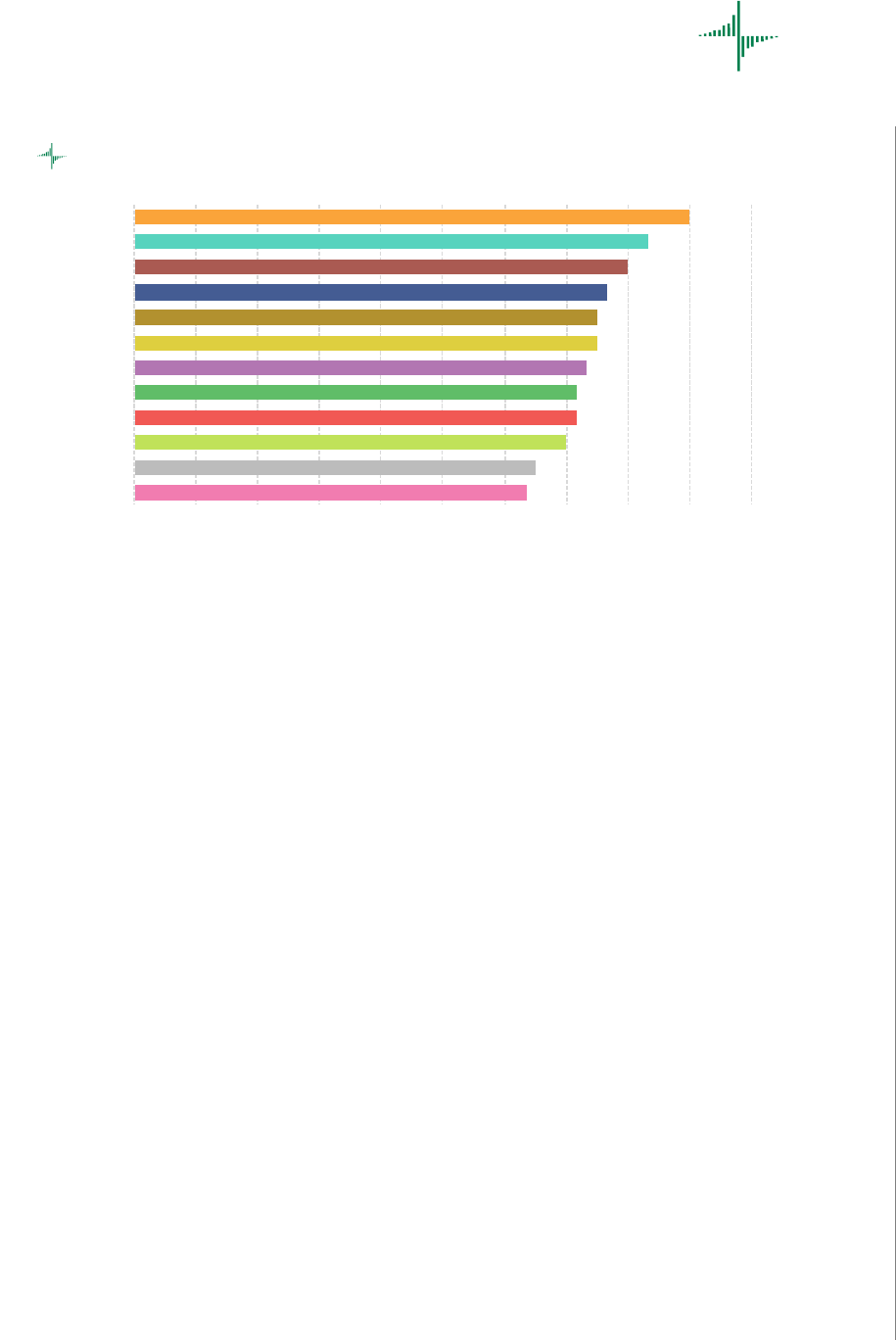

Figure 3

As Figure 3 illustrates, metrics can vary widely from a focus on personnel, asset utilization

or operational cost reduction driven by process standardization to reducing back-office

activity. According to TBR research, having a more streamlined, standardized process and

lower operating expenses were the highest-rated key metrics.

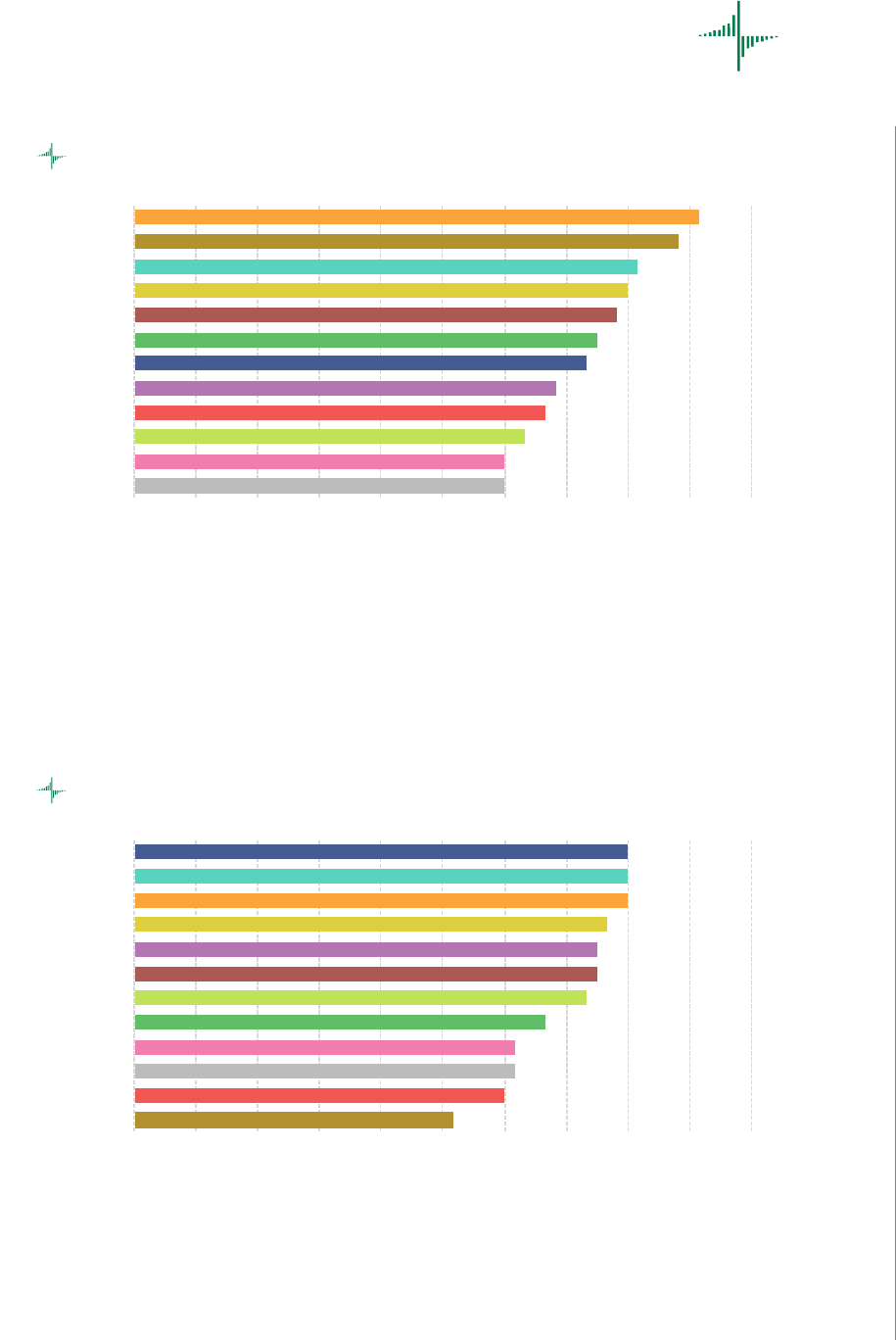

Figure 4

For operators targeting increased agility and more fluid operations, ITO metrics depicted

in Figure 4 reflect nearly equal priority. These priorities include different ways to measure

reduced time to provision or change a new service. Less prominent, but still a high-

priority metric, is reduced time to add applications and services based on partner

offerings. TBR believes this metric will become increasingly important as operators

embrace new business models.

0%

3%

3%

3%

3%

3%

3%

3%

8%

11%

32%

32%

Reduction in software licenses

Depreciation cost

Opex per site

Back-office escalation rate

Avoid reuse of assets and duplication of efforts

Monitor quality

Procurement performance improvement

Eco-responsibility and procurement

Reduced headcount

Increased asset utilization

Lower operating costs

Greater process standardization

% of Respondents

OPERATIONAL EFFICIENCY METRICS USED

SOURCE: TBR

TBR

3%

10%

13%

23%

26%

26%

% of Respondents

INCREASED AGILITY METRICS USED

SOURCE: TBR

TBR

Service delivery platform integrated

into operations

Reduced time to add applications/services

from developers

Reduced time to add applications/services

from partners

Reduced time to ma ke adjustments in

cus tomer change requests

Reduced time to ma rket for new services

Increased s peed of service provisioning

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 8

TBR

Figure 5

As shown in Figure 5, operators’ views of metrics regarding enabling new services are

more general, led by the need to add partners and business opportunities. Operators are

still identifying ways to measure and address new services beyond traditional network

value-added voice and data models. TBR’s findings suggest operators are looking more to

partners and new business than to developers.

Figure 6

Cost-savings metrics revolve around equal parts opex and capex savings with nearly equal

shares drawn from communications technology (CT) and IT budgets. Supplier

performance and consolidation are also parts of current outsourcing metrics as shown in

Figure 6.

2%

2%

12%

14%

14%

28%

28%

Real-time charging of services

Seamless integration

Reduced time to recognize revenue

Increase cross-sell/upsell per subscriber

Increased number of developers

Increased number of partners

Increase new business opportunities

% of Respondents

ENABLE NEW SERVICES METRICS USED

SOURCE: TBR

TBR

2%

2%

2%

2%

8%

17%

21%

23%

23%

Supplier performance

Disposal of noncore assets

Improvements with cost accounting tools

Tools to monitor changes

Reduction in number of suppliers

IT budget reduction

CT budget reduction

Lower capex costs

Lower opex costs

% of Respondents

KEY COST-SAVINGS METRICS USED

SOURCE: TBR

TBR

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 9

TBR

Figure 7

Despite the urgency to evolve to a new, more agile infrastructure, as seen in Figure 7,

legacy integration remains the most common metric when operators measure technology

change. The overall theme of reducing the time to change is reflected in all metrics.

ITO is an important driver in ICT Transformation

As illustrated by Figure 8, specific operator ICT transformation strategies have yet to

coalesce, indicating a market opportunity for vendors to provide strategic guidance and

consulting as well as point solutions. Operators indicate a wide variety of ICT

transformation managed services focus areas, with the least popular responses

(workplace/end-user computing transformation and NFV [network functions virtualization]

integration and operations) just eight percentage points below the most popular (data

center transformation). As more managed services focus areas are defined, operators

need guidance to determine and prioritize the areas they should outsource to align with

present needs and objectives. As awareness grows and vendors tout reference wins, TBR

expects vendors with strong positions in both CT and IT — such as Huawei — to benefit.

Figure 8

2%

2%

2%

12%

12%

20%

22%

27%

Rate of innovation

Rate of application change

Percent of urgent changes

Reduced time to deploy new IT infrastructure

Reduced time to deploy new CT infrastructure

Reduced time to upgrade infrastructure

Reduced time to integrate new infra. with ops.

Reduced time to integrate new and legacy infra.

% of Respondents

TECHNOLOGY CHANGE METRICS USED

SOURCE: TBR

TBR

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 10

TBR

ITO is a key requirement for operators and an initial step in their strategic approach to ICT

transformation, as ITO will lower opex, drive operational efficiency and enable growth

through the faster introduction of new services.

8%

11%

10%

10%

11%

13%

5%

5%

10%

7%

9%

0%

100%

ICT TRANSFORMATION MANAGED SERVICES FOCUS AREAS

Governance integration and operations

Management integration and operations

SDN integration and operations

NFV integration and operations

Workplace/end-user computing transformation

Data center transformation

Improving end-to-end information management

Improving end-to-end application management

Providing end-to-end integrated service delivery infrastructure

Establishing a DevOps digital service innovation capability

Establishing a cloud services infrastructure for enterprise services

TBR

SOURCE: TBR

Note: Does not add up to 100% due to rounding.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 11

TBR

Figure 9

IT transformation capability, as shown in Figure 9, is led, unsurprisingly, by IT firms

holding incumbent positions in operators’ IT environments. The most notable exception is

Huawei’s No. 4 position, which places it ahead of traditional CT rivals Alcatel-Lucent,

Ericsson and Nokia. Huawei was early to recognize the convergence of CT and IT and

focused on transforming its portfolio and adding IT services and products. Huawei’s

transformation was noted by customers, with one chief technology and information

officer surveyed calling Huawei one of the most “trusted partners to provide managed

services for a converged IT and CT infrastructure.” The respondent said, “It has

transformed its managed services to become a next-generation provider to offer

managed solutions to overcome all the challenges related to ICT and convergence.”

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

ZTE

Amdocs

Oracle

Accenture

Dell/EMC

Nokia

Alcatel-Lucent

Ericsson

Huawei

HPE

IBM

Cisco

IT TRANSFORMATION CAPABILITY

TBR

SOURCE: TBR

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 12

TBR

Figure 10

HPE, Cisco and IBM ranked highest in SDN capability, as shown in Figure 10. Huawei beat

out its traditional CT rivals, with one operations head surveyed noting, “Huawei has come

a long way in developing SDN.” Suppliers with proofs of concept and commercial deals

fared well.

Figure 11

As shown in Figure 11, automation and orchestration capability scores were lower in the

aggregate than other surveyed capabilities, suggesting vendors can improve in this area.

Reducing opex costs is a strong driver of automation and orchestration adoption.

Figure 12

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Accenture

ZTE

Amdocs

Nokia

Oracle

Alcatel-Lucent

Dell/EMC

Ericsson

Huawei

HPE

Cisco

IBM

SOFTWARE-DEFINED NETWORKING CAPABILITY

SOURCE: TBR

TBR

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Dell/EMC

Amdocs

Nokia

ZTE

Ericsson

Oracle

Alcatel-Lucent

HPE

Cisco

Accenture

Huawei

IBM

AUTOMATION AND ORCHESTRATION CAPABILITY

SOURCE: TBR

TBR

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 13

TBR

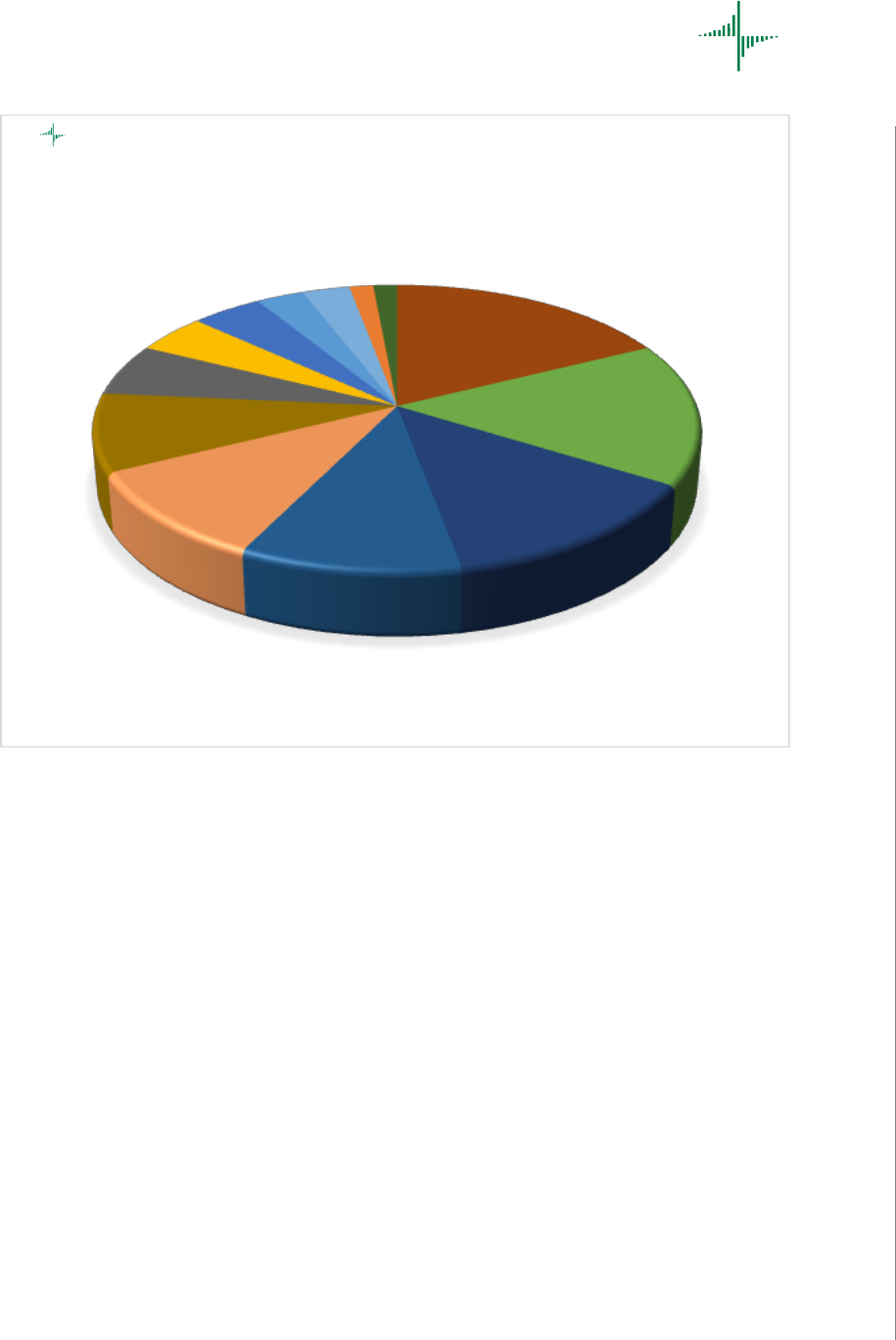

HPE (18%) was ranked as the most trusted vendor, followed by IBM (16%), Cisco (13%),

and Huawei and Accenture tied at 10% as depicted in Figure 12.

One manager of operations and deployments surveyed stated Huawei is “one of the best

companies to help transform network infrastructure. [It is] the leader when we talk about

a converged ICT environment. [Huawei] came up with new SoftCOM and FusionSphere

services that allow operators to make use of NFV and OpenStack technologies to enhance

network performance and capacity.” TBR believes Huawei’s participation in open-

standards groups contributes to and heightens its standing. Operators will become

increasingly comfortable with adding vendors to their IT environments, provided vendors

embrace open-source networking.

Huawei’s ITO offerings form a comprehensive solution

The evolution of an operator’s infrastructure requires transformation of both IT and

communications networks. Huawei can deliver such transformation through its ITO

solution, which consists of its Managed IT Transformation, Managed IT Operation and

Managed Enterprise Cloud offerings.

Managed IT Transformation

HPE

18%

IBM

16%

Cisco

13%

Huawei

10%

Accenture

10%

Dell/EMC

9%

Ericsson

6%

Oracle

4%

Nokia

4%

Juniper

3%

Alcatel-

Lucent

3%

Broadsoft

2%

Amdocs

2%

TRUSTED PARTNERS FOR TRANSFORMATION

TBR

SOURCE: TBR

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 14

TBR

Huawei’s Managed IT Transformation consists of three approaches to address three

different IT outsourcing scenarios, with the goal of maximizing the benefits of technology

evolution and increased agility.

1. Optimize the existing IT environment — quick win solution

Huawei can help operators establish a standardized service platform to reduce

running costs and assure service quality by:

• Standardizing operations management

• Centralizing service management

• Offering self-service

• Optimizing operation tools

• Improving application performance

Additionally, Huawei can deliver asset value maximization by:

• Consolidating data centers

• Increasing hardware utilization

• Rationalizing software license usage

2. Technology transformation

To improve IT infrastructure utilization rates and reduce the time to deploy new

services, Huawei deploys a solution based on its Dynamic Architecture Blueprint,

which includes:

• Open architecture to consolidate IT commodities

• Network technology evolution

• Unified resource pool

• Automation and orchestration of operations

• Fault tolerance and high availability to support business continuity

• Future workplace — VDI, BYOD

3. Business-led application transformation

To improve business agility, Huawei helps operators adopt cloud technology

environments for business applications transformation, including:

• Service platform enablement (PaaS) to support continuous development

and deployment

• Business application cloud enablement to leverage SaaS

• Operating model evolution (bimodal/DevOps)

• Business service assurance

Managed IT Operation

To optimize the as-is state of the transitional data center environment, Managed IT

Operation establishes a centralized and standardized operation services platform to

deliver a high degree of operational efficiency and service quality in day-to-day

operations. The solution also includes operational management of the transformed

environment during execution of the multiple waves of the transformation and in the

resulting operational state.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 15

TBR

Huawei quickly built its IT capabilities by leveraging assets of its managed network

services including:

• Managed Service Unified Platform (MSUP): an eTOM-, ITIL- and TL9000-

compliant platform for telecom IT operations

• Operation Web Service (OWS): a tool set to maximize automation; provides

the unified service portal as required in the scope of work (SOW)

• Global Service Delivery Centers in India, Mexico and Romania

Through collaboration with its managed network services portfolio, Huawei’s Managed IT

Operation is fully capable of supporting a convergent ICT operation.

Managed Enterprise Cloud

Huawei’s Managed Enterprise Cloud is designed for the changing IT services business

model, where cloud computing brings new revenue opportunities. Huawei can help

operators address their challenges (e.g., small partner ecosystem, lack of a go-to-market

system, small early ROI).

Huawei’s strong cloud ecosystem includes partners offering collaboration, security,

customer relationship management (CRM), enterprise resource planning (ERP) and more.

Huawei also reduces risk for its customers by planning, building and operating the

enterprise cloud and providing go-to-market assistance by offering sales support and

partner management and by working in conjunction with operators in marketing efforts.

Managed Enterprise Cloud consists of Cloud Platform Build, Joint Business Innovation,

Business Operation Support and Operation Management.

This approach enables operators to bring new cloud offerings to market faster, reduce

business risks and spur continual innovation. Huawei acts as a reliable strategic partner by

providing a flexible business model and end-to-end service assurance.

Operators leverage Huawei’s ITO solution for ICT transformation

Ooredoo Kuwait transforms network and IT environments with Huawei ITO

Operator summary: Ooredoo operates in 12 markets in the Middle East, North Africa and

Southeast Asia. The priorities of the Kuwait operation include capturing data growth,

increasing ICT capabilities and improving operational efficiency. Ooredoo Kuwait provides

mobile, broadband Internet and corporate managed services. The company’s subscriber

base in the Kuwait market was 2.4 million as of October. Revenues increased 11% and

EBITDA increased 30.9% year-to-year for the first nine months of 2015.

Project goals: Ooredoo aims to become more cost efficient, decrease the time to market

for new services and improve customer experience. The name UNIFY was given to

Ooredoo’s infrastructure transformation program, which includes the unification of

network operation and IT to create a combined service delivery environment with specific

goals:

• Provide any service using a common delivery environment

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 16

TBR

• Deliver the service anywhere across Ooredoo’s multicountry footprint

• Reduce service creation and delivery time from months to days

• Disrupt the competition by improving service delivery at significantly lower cost

Ooredoo is testing the power of an NFV-based single infrastructure for networks and IT to

deliver services faster and more cost effectively.

Ooredoo’s transformation shifts the company from traditional to virtualized IT

infrastructure as part of Phase 1: IT virtualization, which will deliver higher hardware

utilization, consolidated storage and lower capex. By the end of Phase 2, more than 30%

of UNIFY’s data centers will be consolidated, in which server racks will be reduced by 30%

and proprietary hardware products will be replaced by just a few x86-based hardware

products.

Huawei’s role: Ooredoo Kuwait plans to increase efficiency and reduce the time to

market for new services by outsourcing its infrastructure to Huawei. However, the

company’s outsourcing agreement is no ordinary contract. Ooredoo is outsourcing both

its IT and network operations to Huawei with the plan to unite the two organizations and

build a common infrastructure using the latest innovations of NFV as well as network and

IT operations.

The operator leveraged several vendors for operations, but wanted to simplify operations.

After a few rounds of evaluation, Huawei was selected to support Ooredoo Kuwait’s

transformation. Huawei was selected as the outsourcing partner in September, and the

transition from Ooredoo operations to Huawei was completed in November. The

transition included transferring Ooredoo staff in Kuwait to Huawei, as well as the

operation of all Ooredoo’s Kuwait data centers. Huawei also transferred its staff to the

operations centers supporting the operator.

The next phase of the operation will occur in stages, beginning with a hybrid model in

which Huawei will initially place its staff in Ooredoo data centers and operate some

functions from Huawei’s India-based global Network Operations Center (NOC). Eventually,

more services will be centralized within the NOC, and Ooredoo will no longer have to

operate as many local data centers.

In addition to savings from consolidating and centralizing data center operations,

Ooredoo expects reduced costs from its application development management (ADM)

processes, which were also part of the outsourcing contracts.

Outsourcing to Huawei enables Ooredoo to address two key issues in the UNIFY strategy:

organizational adaptation and skill deficits. Huawei will bring together the network and IT

functions in its operations, and provide the skilled staff to upgrade Ooredoo’s network

and IT operations to NFV capabilities.

As the chosen outsourcer Huawei acts as the primary vendor, and the other vendors act

as subcontractors. In Ooredoo’s case, Huawei maintains a significant share of the network

with its own equipment, but Huawei must manage other vendors as on-site

subcontractors.

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 17

TBR

Ooredoo’s UNIFY transformation enables the operator to create a strategy for the

combination of outsourcing, ICT convergence and NFV road map deployment. The cost-

reductions and time-to-service incentives the operator can achieve may be a game-

changer in the Middle East with global reverberations.

Huawei drives Etisalat’s global ICT transformation through managed services

Operator summary: With headquarters in Abu Dhabi, United Arab Emirates (UAE),

Etisalat operates 2G, 3G and LTE networks throughout 18 countries in MEA and APAC

including the UAE, Saudi Arabia, Egypt, Nigeria and Sri Lanka. Etisalat services 169 million

subscribers.

Project goals: Etisalat is in the early stages of what it refers to as its Service Vision 2020,

an NFV- and SDN-driven transformation that includes an infrastructure overhaul

stretching from the data center to the access layer. A cloud-centric architecture will

provide Etisalat with a more agile network to offer new services such as Internet of Things

(IoT) connectivity to its customers.

Huawei’s role: Huawei is a leading ICT provider and strategic partner to Etisalat. For

example, in Nigeria Huawei manages Etisalat’s communications network and, in a

separate agreement signed in 1Q14, Etisalat Nigeria outsourced its IT operations to

Huawei. For the IT portion, Huawei manages technical infrastructure, application

management and user support. Outsourcing ICT to Huawei enables Etisalat to improve

quality, reduce costs, transform infrastructure and increase the speed to market of new

services.

XL Axiata taps Huawei for managed services to accelerate transformation

Operator summary: XL Axiata is a leading operator in Indonesia supplying 2G, 3G and LTE

to select regions including Java and Bali. Historically, XL Axiata is an early mover in

Indonesia, launching 3G and LTE ahead of regional competitors.

Project goals: To accelerate its transformation into a digital telecom operator and address

the domestic rise is data traffic, XL Axiata turns to Huawei for managed services. XL Axiata

is shifting resources from traditional voice traffic to initiatives that enable it to offer

digitally based services. These initiatives include the construction of a network and service

operation center in Jakarta.

Huawei’s role: Huawei is the leading managed services partner for XL Axiata, enabling it

to digitally transform and support new services and applications. Huawei provides its

Managed Services for Total Value of Ownership (TVO), which streamlines network

operations and allows Huawei to manage IT applications such as OSS. Additionally,

Huawei manages XL Axiata’s Digital Merchant (DM) ecosystem.

Telefonica leverages Enterprise Cloud Migration from Huawei to offer

outsourced IT to enterprise customers

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 18

TBR

Operator summary: Telefonica is a leading global telecom operator based in Madrid.

Telefonica’s operations stretch throughout Europe and Asia, and into North and South

America.

Project goals: Telefonica selected Huawei as a strategic partner to enable it to offer cloud

IT services to enterprise customers. The operator can now deliver managed compute,

backup and storage services leveraging its own data centers. Telefonica calls its new

service Telefonica Open Cloud.

Huawei’s role: Huawei is supplying elements of its Managed Enterprise Cloud to enable

Telefonica’s Open Cloud globally. Huawei’s OpenStack-based service is deployed in eight

Telefonica data centers. Brazil, Mexico and Chile will be the first Telefonica markets with

access to the service.

Additionally, Huawei is supporting Telefonica’s business in China, where it is supplying

knowledge and experience to enable Telefonica to penetrate the public cloud market.

Huawei’s managed services accelerate ICT transformation for du and KPN

• Huawei provides managed services for du’s mobile, fixed and broadcast networks in

the UAE. Huawei is well-equipped to carry out the contract, utilizing its three

resource centers and five training centers in the region to deliver comprehensive

services to du. du is transforming its networking operations to prepare for 5G

deployments.

• Netherlands-based KPN selected Huawei as the sole provider of ITO services,

including managing the OSS/BSS, value-added services, delivery and management,

for the operator’s Ortel mobile virtual network operator (MVNO) in Spain. Huawei

was selected due to its role as a provider of network equipment for the broader

KPN Group. The MVNO was launched using KPN’s Magnum platform, which it used

to launch multiple MVNOs in Europe. KPN is one of Huawei’s largest OSS/BSS

customers in Europe.

TBR perspective

Operators will increasingly require ITO services to deliver key cost savings, promote

operational efficiency and enable revenue growth through the introduction of new

services. ICT transformation in an operator’s network and IT environments cannot

become a reality without a strong ITO partner.

Huawei’s expertise in ITO lies in its telecom managed services foundation, but is

strengthened by the vendor’s IT focus, particularly in cloud enablement and the data

center. Huawei has accumulated over 450 cumulative contracts in managed services,

provided integration for more than 480 data centers, completed over 160 cloud

deployments, and engaged in 20 NFV and SDN joint innovation projects with operators.

Huawei must persuade its customers to adopt transformative products and services such

as NFV and SDN. This dilemma is not unique to Huawei, as Ericsson and others face similar

Huawei – Confidential

Huawei ITO Utilizes Key ICT Transformation Metrics to Deliver Next Generation of IT Services February 2016

Technology Business Research, Inc. Page 19

TBR

challenges. Huawei is on the right track to build its partner ecosystem and bring an end-

to-end ICT solution to the market faster, with best-in-class capabilities.

About TBR

Technology Business Research, Inc. is a leading independent technology market research and

consulting firm specializing in the business and financial analyses of hardware, software,

professional services, telecom and enterprise network vendors, and operators.

Serving a global clientele, TBR provides timely and actionable market research and business

intelligence in formats that are tailored to clients’ needs. Our analysts are available to further

address client-specific issues or information needs on an inquiry or proprietary consulting basis.

For more information

TBR has been empowering corporate decision makers since 1996. For more information, visit

www.tbri.com.

This report is based on information made available to the public by the vendor and other public sources. No

representation is made that this information is accurate or complete. Technology Business Research will not be held liable

or responsible for any decisions that are made based on this information. The information contained in this report and all

other TBR products is not and should not be construed to be investment advice. TBR does not make any recommendations

or provide any advice regarding the value, purchase, sale or retention of securities. This report is copyright-protected and

supplied for the sole use of the recipient. © Contact Technology Business Research, Inc. for permission to reproduce.