UNITED STATES DEPARTMENT OF AGRICULTURE

Rural Utilities Service

BULLETIN 1780-2

RD-GD-2013-70

SUBJECT: Preliminary Engineering Reports for the Water and Waste Disposal

Program

TO: Rural Development State Directors, RUS Program Directors, and State Engineers

EFFECTIVE DATE: Date of approval.

OFFICE OF PRIMARY INTEREST: Engineering and Environmental Staff, Water

and Environmental Programs

INSTRUCTIONS: This bulletin replaces existing RUS Bulletins 1780-2 (September 10,

2003), 1780-3 (October 2, 2003), 1780-4 (October 2, 2003), and 1780-5 (October 2,

2003).

AVAILABILITY: This bulletin and all the exhibits, as well as any Rural Development

instruction or Rural Utilities Service instructions, regulations, or forms referenced in this

bulletin are available at any Rural Development State Office. The State Office staff is

familiar with the use of the documents in their States and can answer specific questions

on Agency requirements.

This bulletin is available on the Rural Utilities Service website at

http://www.rurdev.usda.gov/RDU_Bulletins_Water_and_Environmental.html.

PURPOSE: This bulletin assists applicants and their consultants with instructions on

how to prepare a Preliminary Engineering Report as part of an application for funding as

required by 7 CFR 1780.33(c) and 7 CFR 1780.55.

MODIFICATIONS: Rural Development State Offices may modify this guidance when

appropriate to comply with State statutes and regulations in accordance with the

procedures outlined at Rural Development Instruction 2006-B (2006.55).

4/4/13

____________________________________________

__________________

JACQUELINE M. PONTI-LAZARUK

Date

Assistant Administrator

Water and Environmental Programs

DISCLAIMER: The contents of this guidance document does not have the force and effect of law and is

not meant to bind the public in any way. This document is intended only to provide clarity to the public

regarding existing requirements under the law or agency policies.

Bulletin 1780-2

Page 2

TABLE OF CONTENTS

1 GENERAL

2 PURPOSE

3 HOW TO USE THE INTERAGENCY TEMPLATE

Exhibit One Interagency Preliminary Engineering Report Template

INDEX:

Application Document

Preliminary Engineering Report

Project Planning

Water and Waste Disposal Facilities

ABBREVIATIONS

CDBG – Community Development Block Grant

CFR – Code of Federal Regulations

EDU – Equivalent Dwelling Unit

EPA – Environmental Protection Agency

GAO – Government Accountability Office

GPCD – Gallons per Capita per Day

HUD – Department of Housing and Urban Development

O & M – Operations and Maintenance

PER – Preliminary Engineering Report

RD – Rural Development

RUS – Rural Utilities Service

SRF – State Revolving Fund

USDA – United States Department of Agriculture

WEP – Water and Environmental Programs

WWD – Water and Waste Disposal

Bulletin 1780-2

Page 3

1 GENERAL

A PER is a planning document required by many state and federal agencies as part of the

process of obtaining financial assistance for development of drinking water, wastewater,

solid waste, and stormwater projects. An applicant for funding from the WWD program

must submit a PER as required by 7 CFR 1780.33(c) and 1780.55. The PER describes

the proposed project from an engineering perspective, analyzes alternatives to the

proposal, defines project costs, and provides information critical to the underwriting

process.

In 2012 the USDA, Rural Development (RD), Rural Utilities Service, Water and

Environmental Programs formed a working group to develop an interagency template for

PERs for use by both federal agencies and state administering agencies. The USDA-led

working group included 36 individuals representing 4 federal agencies, 16 state agencies,

the Border Environment Cooperation Commission, and the North Carolina Rural Center.

Also, the effort was supported by the Small Community Water Infrastructure Exchange.

On January 16, 2013, the principals of the federal participants executed an interagency

memorandum supporting use of the interagency template, attached as Exhibit One.

2. PURPOSE

This bulletin provides information and guidance for applicants and professional

consultants in developing a PER for submittal with an application for funding. RD State

Offices should provide a copy of the Bulletin to applicants and consulting engineers upon

request or refer them to the website listed on the Bulletin’s cover sheet for an electronic

copy.

3 HOW TO USE THE INTERAGENCY TEMPLATE

There has been increasing interest throughout the government at both state and federal

levels to improve coordination between funding agencies in the processes involved in

applications for infrastructure funding. A recent GAO report, “Rural Water

Infrastructure: Additional Coordination Can Help Avoid Potentially Duplicative

Application Requirements” (GAO-13-111), released October 16, 2012, called the effort

of the working group led by USDA to develop the attached Interagency PER Template

“encouraging” and stated that it would “help communities”.

Content of a PER: The attached Interagency PER Template describes the content of a

PER and should be used without modification, except for items noted below. Often an

applicant will initially consider only a single funding source and later determine that an

application to additional funding agencies is necessary. To avoid having to revise the

PER to meet the additional agencies’ needs, the consulting engineer should provide

Bulletin 1780-2

Page 4

responses to all sections of the PER outline, unless specific sections do not apply to a

proposed project.

Short-Lived Assets: The short-lived asset table in Appendix A is a list of examples of

short-lived assets. Depending on local practices and applicants, some of these items may

not be considered short-lived assets if they are considered part of O&M or long-term

capital financing. Consulting engineers and applicants should coordinate with each other

and with the Agency to determine which items should be considered short-lived assets for

specific projects.

Engaging State Partners: State Offices should engage funding partners to encourage state-

wide adoption of the attached template as a standard for all state leveraging partners.

Existing state-level agreements resulting from previous coordinated efforts for adopting a

standard PER outline must be modified or replaced with this template. Efforts underway

to adopt new state-level PER outlines must use this template. State-level agreements

implementing this template between various leveraging partners should keep additional

requirements to a minimum, but should not remove any required sections from the

template.

Income Projections for Underwriting Purposes:

The State Office uses some of the information from the PER, especially Sections 6 (e)

and (f), for underwriting purposes. Note that for income projection purposes, every effort

should be made to identify actual data regarding water usage or wastewater generation.

For metered systems, actual data should be used.

When financing construction of a new system or improvements to an existing system

without any existing usage data, water use and wastewater generation approximations for

income projection purposes should, if at all possible, be based on information from

surrounding similar communities and systems. The source of data used should be

documented in the PER.

The value of 100 GPCD shown in Section 6 is a general value and may not be

appropriate for many rural systems financed with WWD funds, so in the absence of

reliable data, a value of 5000 gallons per EDU per month (approximately 67 GPCD or

167 GPD per EDU) should be used.

Exhibit One: Interagency Preliminary Engineering Report Template

January 16, 2013

INTERAGENCY MEMORANDUM

Attached is a document explaining recommended best practice for the development of

Preliminary Engineering Reports in support of funding applications for development of drinking

water, wastewater, stormwater, and solid waste systems.

The best practice document was developed cooperatively by:

US Department of Agriculture, Rural Development, Rural Utilities Service, Water and

Environmental Programs;

US Environmental Protection Agency (EPA), Office of Water, Office of Ground Water

and Drinking Water and Office of Wastewater Management;

US Department of Housing and Urban Development (HUD), Office of Community

Planning and Development;

US Department of Health and Human Services, Indian Health Service (IHS);

Small Communities Water Infrastructure Exchange;

Extensive input from participating state administering agencies was also very important to the

development of this document.

Federal agencies that cooperatively developed this document strongly encourage its use by

funding agencies as part of the application process or project development. State administered

programs are encouraged to adopt this document but are not required to do so, as it is up to a

state administering agency’s discretion to adopt it, based on the needs of the state administering

agency.

A Preliminary Engineering Report (Report) is a planning document required by many state and

federal funding agencies as part of the process of obtaining financial assistance for development

of drinking water, wastewater, solid waste, and stormwater facilities. The attached Report

outline details the requirements that funding agencies have adopted when a Report is required.

In general the Report should include a description of existing facilities and a description of the

issues being addressed by the proposed project. It should identify alternatives, present a life

cycle cost analysis of technically feasible alternatives and propose a specific course of action.

The Report should also include a detailed current cost estimate of the recommended alternative.

The attached outline describes these and other sections to be included in the Report.

Projects utilizing direct federal funding also require an environmental review in accordance with

the National Environmental Policy Act (NEPA). The Report should indicate that environmental

issues were considered as part of the engineering planning and include environmental

information pertinent to engineering planning.

2

For state administered funding programs, a determination of whether the outline applies to a

given program or project is made by the state administering agency. When a program or agency

adopts this outline, it may adopt a portion or the entire outline as applicable to the program or

project in question at the discretion of the agency. Some state and federal funding agencies will

not require the Report for every project or may waive portions of the Report that do not apply to

their application process, however a Report thoroughly addressing all of the contents of this

outline will meet the requirements of most agencies that have adopted this outline.

The detailed outline provides information on what to include in a Report. The level of detail

required may also vary according to the complexity of the specific project. Reports should

conform substantially to this detailed outline and otherwise be prepared and presented in a

professional manner. Many funding agencies require that the document be developed by a

Professional Engineer registered in the state or other jurisdiction where the project is to be

constructed unless exempt from this requirement. Please check with applicable funding agencies

to determine if the agencies require supplementary information beyond the scope of this outline.

Any preliminary design information must be written in accordance with the regulatory

requirements of the state or territory where the project will be built.

Information provided in the Report may be used to process requests for funding. Completeness

and accuracy are therefore essential for timely processing of an application. Please contact the

appropriate state or federal funding agencies with any questions about development of the Report

and applications for funding as early in the process as practicable.

Questions about this document should be referred to the applicable state administering agency,

regional office of the applicable federal agency, or to the following federal contacts:

Agency Contact EmailAddress Phone

USDA/RUS BenjaminShuman,PE [email protected] 202‐720‐1784

EPA/CWSRF MattKing [email protected] 202‐564‐2871

HUD StephenRhodeside [email protected] 202‐708‐1322

3

Attachment

4

WORKING GROUP CONTRIBUTORS

FederalAgencyPartners

USDA,RuralDevelopment,RuralUtilitiesService(Chair) BenjaminShuman,PE

EPA,OfficeofWater,OfficeofGroundWaterandDrinkingWater KirstenAnderer,PE

EPA,OfficeofWater,OfficeofGroundWaterandDrinkingWater CAPTDavidHarvey,PE

EPA,OfficeofWater,OfficeofWastewaterManagement MattKing

EPA,OfficeofWater,OfficeofWastewaterManagement JoyceHudson

EPA,Region1 CarolynHayek

EPA,Region9 AbimbolaOdusoga

HUD,OfficeofCommunityPlanningandDevelopment StephenM.Rhodeside

HUD,OfficeofCommunityPlanningandDevelopment EvaFontheim

IndianHealthService CAPTDanaBaer,PE

IndianHealthService LCDRCharissaWilliar,PE

USDA,RuralDevelopment,FloridaStateOffice MichaelLangston

USDA,RuralDevelopment,FloridaStateOffice SteveMorris,PE

5

StateAgencyandInteragencyPartners

ArizonaWaterInfrastructureFinanceAuthority DeanMoulis,PE

BorderEnvironmentCooperationCommission JoelMora,PE

ColoradoDepartmentofLocalAffairs BarryCress

ColoradoDepartmentofPublicHealth&Environment MichaelBeck

ColoradoDepartmentofPublicHealth&Environment BretIcenogle, PE

GeorgiaOfficeofCommunityDevelopment SteedRobinson

Idaho,DepartmentofEnvironmentalQuality TimWendland

IndianaFinanceAuthority EmmaKottlowski

IndianaFinanceAuthority ShelleyLove

IndianaFinanceAuthority AmandaRickard,PE

KentuckyDivisionofWater ShafiqAmawi

KentuckyDepartmentofLocalGovernment JenniferPeters

LouisianaDepartmentofEnvironmentalQuality JonathanMcFarland,PE

MaineDepartmentofHealthandHumanServices NormLamie,PE

MinnesotaPollutionControlAgency AmyDouville

MinnesotaPollutionControlAgency CoreyMathisen,PE

MissouriDepartmentofNaturalResources CynthiaSmith

MontanaDepartmentofCommerce KateMiller,PE

NorthCarolinaDepartmentofCommerce OliviaCollier

NorthCarolinaRuralCenter KeithKrzywicki,PE

NorthCarolinaDepartmentofCommerce VickieMiller,CPM

RhodeIslandDepartmentofHealth GaryChobanian,PE

RhodeIslandDepartmentofHealth GeoffreyMarchant

6

ABBREVIATIONS

NEPA – National Environmental Policy Act

NPV – Net Present Value

O&M – Operations and Maintenance

OMB – Office of Management and Budget

Report – Preliminary Engineering Report

SPPW – Single Payment Present Worth

USPW – Uniform Series Present Worth

7

GENERAL OUTLINE OF A PRELIMINARY ENGINEERING REPORT

1) PROJECT PLANNING

a) Location

b) Environmental Resources Present

c) Population Trends

d) Community Engagement

2) EXISTING FACILITIES

a) Location Map

b) History

c) Condition of Existing Facilities

d) Financial Status of any Existing Facilities

e) Water/Energy/Waste Audits

3) NEED FOR PROJECT

a) Health, Sanitation, and Security

b) Aging Infrastructure

c) Reasonable Growth

4) ALTERNATIVES CONSIDERED

a) Description

b) Design Criteria

c) Map

d) Environmental Impacts

e) Land Requirements

f) Potential Construction Problems

g) Sustainability Considerations

i) Water and Energy Efficiency

ii) Green Infrastructure

iii) Other

h) Cost Estimates

5) SELECTION OF AN ALTERNATIVE

a) Life Cycle Cost Analysis

b) Non-Monetary Factors

6) PROPOSED PROJECT (RECOMMENDED ALTERNATIVE)

a) Preliminary Project Design

b) Project Schedule

c) Permit Requirements

d) Sustainability Considerations

i) Water and Energy Efficiency

ii) Green Infrastructure

8

iii) Other

e) Total Project Cost Estimate (Engineer’s Opinion of Probable Cost)

f) Annual Operating Budget

i) Income

ii) Annual O&M Costs

iii) Debt Repayments

iv) Reserves

7) CONCLUSIONS AND RECOMMENDATIONS

9

DETAILED OUTLINE OF A PRELIMINARY ENGINEERING REPORT

1) PROJECT PLANNING

Describe the area under consideration. Service may be provided by a combination of

central, cluster, and/or centrally managed individual facilities. The description should

include information on the following:

a) Location. Provide scale maps and photographs of the project planning area and

any existing service areas. Include legal and natural boundaries and a

topographical map of the service area.

b) Environmental Resources Present. Provide maps, photographs, and/or a narrative

description of environmental resources present in the project planning area that

affect design of the project. Environmental review information that has already

been developed to meet requirements of NEPA or a state equivalent review

process can be used here.

c) Population Trends. Provide U.S. Census or other population data (including

references) for the service area for at least the past two decades if available.

Population projections for the project planning area and concentrated growth

areas should be provided for the project design period. Base projections on

historical records with justification from recognized sources.

d) Community Engagement. Describe the utility’s approach used (or proposed for

use) to engage the community in the project planning process. The project

planning process should help the community develop an understanding of the

need for the project, the utility operational service levels required, funding and

revenue strategies to meet these requirements, along with other considerations.

2) EXISTING FACILITIES

Describe each part (e.g. processing unit) of the existing facility and include the following

information:

a) Location Map. Provide a map and a schematic process layout of all existing

facilities. Identify facilities that are no longer in use or abandoned. Include

photographs of existing facilities.

b) History. Indicate when major system components were constructed, renovated,

expanded, or removed from service. Discuss any component failures and the

cause for the failure. Provide a history of any applicable violations of regulatory

requirements.

c) Condition of Existing Facilities. Describe present condition; suitability for

continued use; adequacy of current facilities; and their conveyance, treatment,

storage, and disposal capabilities. Describe the existing capacity of each

component. Describe and reference compliance with applicable federal, state, and

local laws. Include a brief analysis of overall current energy consumption.

Reference an asset management plan if applicable.

10

d) Financial Status of any Existing Facilities. (Note: Some agencies require the

owner to submit the most recent audit or financial statement as part of the

application package.) Provide information regarding current rate schedules,

annual O&M cost (with a breakout of current energy costs), other capital

improvement programs, and tabulation of users by monthly usage categories for

the most recent typical fiscal year. Give status of existing debts and required

reserve accounts.

e) Water/Energy/Waste Audits. If applicable to the project, discuss any water,

energy, and/or waste audits which have been conducted and the main outcomes.

3) NEED FOR PROJECT

Describe the needs in the following order of priority:

a) Health, Sanitation, and Security. Describe concerns and include relevant

regulations and correspondence from/to federal and state regulatory agencies.

Include copies of such correspondence as an attachment to the Report.

b) Aging Infrastructure. Describe the concerns and indicate those with the greatest

impact. Describe water loss, inflow and infiltration, treatment or storage needs,

management adequacy, inefficient designs, and other problems. Describe any

safety concerns.

c) Reasonable Growth. Describe the reasonable growth capacity that is necessary to

meet needs during the planning period. Facilities proposed to be constructed to

meet future growth needs should generally be supported by additional revenues.

Consideration should be given to designing for phased capacity increases.

Provide number of new customers committed to this project.

4) ALTERNATIVES CONSIDERED

This section should contain a description of the alternatives that were considered in

planning a solution to meet the identified needs. Documentation of alternatives

considered is often a Report weakness. Alternative approaches to ownership and

management, system design (including resource efficient or green alternatives), and

sharing of services, including various forms of partnerships, should be considered. In

addition, the following alternatives should be considered, if practicable: building new

centralized facilities, optimizing the current facilities (no construction), developing

centrally managed decentralized systems, including small cluster or individual systems,

and developing an optimum combination of centralized and decentralized systems.

Alternatives should be consistent with those considered in the NEPA, or state equivalent,

environmental review. Technically infeasible alternatives that were considered should be

mentioned briefly along with an explanation of why they are infeasible, but do not

require full analysis. For each technically feasible alternative, the description should

include the following information:

a) Description. Describe the facilities associated with every technically feasible

alternative. Describe source, conveyance, treatment, storage and distribution

11

facilities for each alternative. A feasible system may include a combination of

centralized and decentralized (on-site or cluster) facilities.

b) Design Criteria. State the design parameters used for evaluation purposes. These

parameters should comply with federal, state, and agency design policies and

regulatory requirements.

c) Map. Provide a schematic layout map to scale and a process diagram if

applicable. If applicable, include future expansion of the facility.

d) Environmental Impacts. Provide information about how the specific alternative

may impact the environment. Describe only those unique direct and indirect

impacts on floodplains, wetlands, other important land resources, endangered

species, historical and archaeological properties, etc., as they relate to each

specific alternative evaluated. Include generation and management of residuals

and wastes.

e) Land Requirements. Identify sites and easements required. Further specify

whether these properties are currently owned, to be acquired, leased, or have

access agreements.

f) Potential Construction Problems. Discuss concerns such as subsurface rock, high

water table, limited access, existing resource or site impairment, or other

conditions which may affect cost of construction or operation of facility.

g) Sustainability Considerations. Sustainable utility management practices include

environmental, social, and economic benefits that aid in creating a resilient utility.

i) Water and Energy Efficiency. Discuss water reuse, water efficiency, water

conservation, energy efficient design (i.e. reduction in electrical demand),

and/or renewable generation of energy, and/or minimization of carbon

footprint, if applicable to the alternative. Alternatively, discuss the water and

energy usage for this option as compared to other alternatives.

ii) Green Infrastructure. Discuss aspects of project that preserve or mimic

natural processes to manage stormwater, if applicable to the alternative.

Address management of runoff volume and peak flows through infiltration,

evapotranspiration, and/or harvest and use, if applicable.

iii) Other. Discuss any other aspects of sustainability (such as resiliency or

operational simplicity) that are incorporated into the alternative, if applicable.

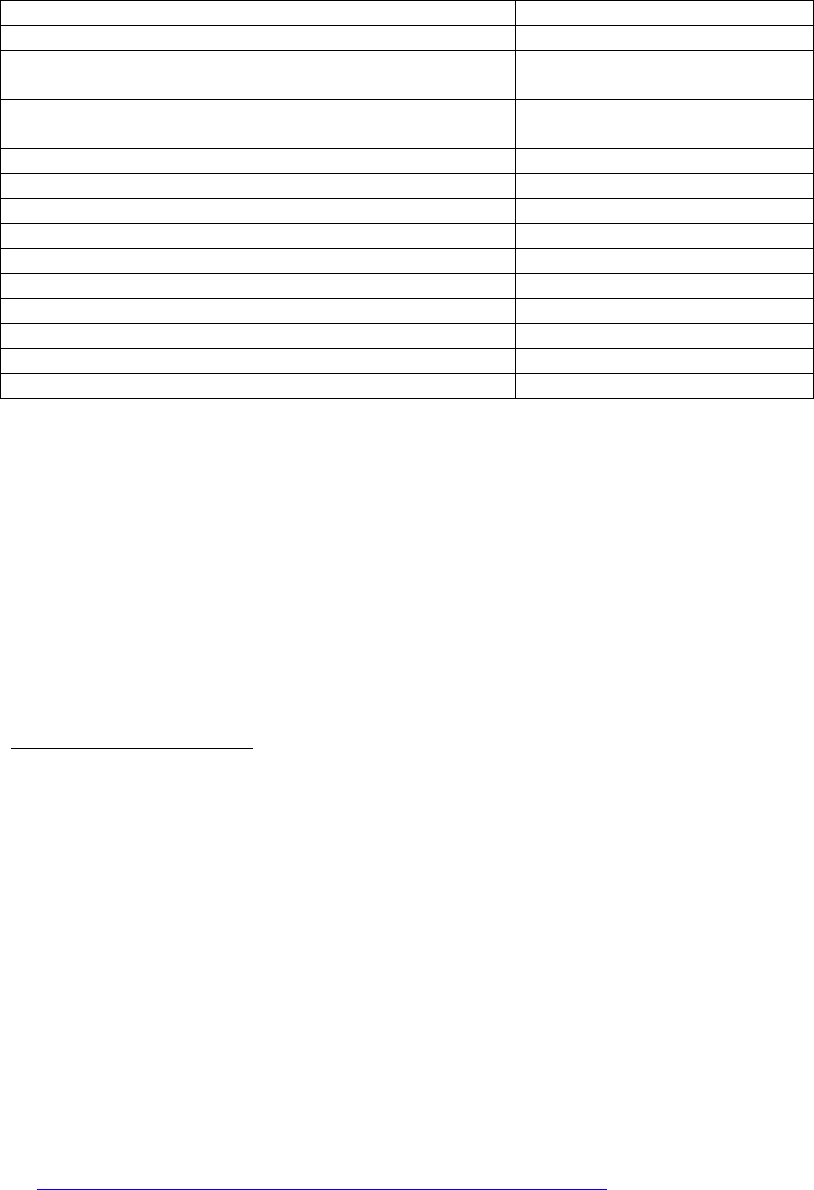

h) Cost Estimates. Provide cost estimates for each alternative, including a

breakdown of the following costs associated with the project: construction, non-

construction, and annual O&M costs. A construction contingency should be

included as a non-construction cost. Cost estimates should be included with the

descriptions of each technically feasible alternative. O&M costs should include a

rough breakdown by O&M category (see example below) and not just a value for

each alternative. Information from other sources, such as the recipient’s

accountant or other known technical service providers, can be incorporated to

assist in the development of this section. The cost derived will be used in the life

cycle cost analysis described in Section 5 a.

12

Exam

p

le O&M Cost Estimate

Personnel (i.e. Salary, Benefits, Payroll Tax,

Insurance, Trainin

g)

Administrative Costs (e.g. office supplies, printing,

etc.

)

Water Purchase or Waste Treatment Costs

Insurance

Ener

gy

Cost

(

Fuel and/or Electrical

)

Process Chemical

Monitorin

g

& Testin

g

Short Lived Asset Maintenance/Re

p

lacement*

Professional Services

Residuals Dis

p

osal

Miscellaneous

Total

* See Appendix A for example list

5) SELECTION OF AN ALTERNATIVE

Selection of an alternative is the process by which data from the previous section,

“Alternatives Considered” is analyzed in a systematic manner to identify a recommended

alternative. The analysis should include consideration of both life cycle costs and non-

monetary factors (i.e. triple bottom line analysis: financial, social, and environmental). If

water reuse or conservation, energy efficient design, and/or renewable generation of

energy components are included in the proposal provide an explanation of their cost

effectiveness in this section.

a) Life Cycle Cost Analysis. A life cycle present worth cost analysis (an

engineering economics technique to evaluate present and future costs for

comparison of alternatives) should be completed to compare the technically

feasible alternatives. Do not leave out alternatives because of anticipated costs;

let the life cycle cost analysis show whether an alternative may have an

acceptable cost. This analysis should meet the following requirements and should

be repeated for each technically feasible alternative. Several analyses may be

required if the project has different aspects, such as one analysis for different

types of collection systems and another for different types of treatment.

1. The analysis should convert all costs to present day dollars;

2. The planning period to be used is recommended to be 20 years, but may be any

period determined reasonable by the engineer and concurred on by the state or

federal agency;

3. The discount rate to be used should be the “real” discount rate taken from

Appendix C of OMB circular A-94 and found at

(www.whitehouse.gov/omb/circulars/a094/a94_appx-c.html);

4. The total capital cost (construction plus non-construction costs) should be

included;

13

5. Annual O&M costs should be converted to present day dollars using a uniform

series present worth (USPW) calculation;

6. The salvage value of the constructed project should be estimated using the

anticipated life expectancy of the constructed items using straight line

depreciation calculated at the end of the planning period and converted to

present day dollars;

7. The present worth of the salvage value should be subtracted from the present

worth costs;

8. The net present value (NPV) is then calculated for each technically feasible

alternative as the sum of the capital cost (C) plus the present worth of the

uniform series of annual O&M (USPW (O&M)) costs minus the single payment

present worth of the salvage value (SPPW(S)):

NPV = C + USPW (O&M) – SPPW (S)

9. A table showing the capital cost, annual O&M cost, salvage value, present

worth of each of these values, and the NPV should be developed for state or

federal agency review. All factors (major and minor components), discount

rates, and planning periods used should be shown within the table;

10. Short lived asset costs (See Appendix A for examples) should also be included

in the life cycle cost analysis if determined appropriate by the consulting

engineer or agency. Life cycles of short lived assets should be tailored to the

facilities being constructed and be based on generally accepted design life.

Different features in the system may have varied life cycles.

b) Non-Monetary Factors. Non-monetary factors, including social and

environmental aspects (e.g. sustainability considerations, operator training

requirements, permit issues, community objections, reduction of greenhouse gas

emissions, wetland relocation) should also be considered in determining which

alternative is recommended and may be factored into the calculations.

6) PROPOSED PROJECT (RECOMMENDED ALTERNATIVE)

The engineer should include a recommendation for which alternative(s) should be

implemented. This section should contain a fully developed description of the proposed

project based on the preliminary description under the evaluation of alternatives. Include

a schematic for any treatment processes, a layout of the system, and a location map of the

proposed facilities. At least the following information should be included as applicable

to the specific project:

a) Preliminary Project Design.

i) Drinking Water:

Water Supply. Include requirements for quality and quantity. Describe

recommended source, including site and allocation allowed.

14

Treatment. Describe process in detail (including whether adding,

replacing, or rehabilitating a process) and identify location of plant and

site of any process discharges. Identify capacity of treatment plant (i.e.

Maximum Daily Demand).

Storage. Identify size, type and location.

Pumping Stations. Identify size, type, location and any special power

requirements. For rehabilitation projects, include description of

components upgraded.

Distribution Layout. Identify general location of new pipe, replacement,

or rehabilitation: lengths, sizes and key components.

ii) Wastewater/Reuse:

Collection System/Reclaimed Water System Layout. Identify general

location of new pipe, replacement or rehabilitation: lengths, sizes, and key

components.

Pumping Stations. Identify size, type, site location, and any special power

requirements. For rehabilitation projects, include description of

components upgraded.

Storage. Identify size, type, location and frequency of operation.

Treatment. Describe process in detail (including whether adding,

replacing, or rehabilitating a process) and identify location of any

treatment units and site of any discharges (end use for reclaimed water).

Identify capacity of treatment plant (i.e. Average Daily Flow).

iii) Solid Waste:

Collection. Describe process in detail and identify quantities of material

(in both volume and weight), length of transport, location and type of

transfer facilities, and any special handling requirements.

Storage. If any, describe capacity, type, and site location.

Processing. If any, describe capacity, type, and site location.

Disposal. Describe process in detail and identify permit requirements,

quantities of material, recycling processes, location of plant, and site of

any process discharges.

iv) Stormwater:

Collection System Layout. Identify general location of new pipe,

replacement or rehabilitation: lengths, sizes, and key components.

Pumping Stations. Identify size, type, location, and any special power

requirements.

15

Treatment. Describe treatment process in detail. Identify location of

treatment facilities and process discharges. Capacity of treatment process

should also be addressed.

Storage. Identify size, type, location and frequency of operation.

Disposal. Describe type of disposal facilities and location.

Green Infrastructure. Provide the following information for green

infrastructure alternatives:

Control Measures Selected. Identify types of control measures

selected (e.g., vegetated areas, planter boxes, permeable pavement,

rainwater cisterns).

Layout: Identify placement of green infrastructure control measures,

flow paths, and drainage area for each control measure.

Sizing: Identify surface area and water storage volume for each green

infrastructure control measure. Where applicable, soil infiltration rate,

evapotranspiration rate, and use rate (for rainwater harvesting) should

also be addressed.

Overflow: Describe overflow structures and locations for conveyance

of larger precipitation events.

b) Project Schedule. Identify proposed dates for submittal and anticipated approval

of all required documents, land and easement acquisition, permit applications,

advertisement for bids, loan closing, contract award, initiation of construction,

substantial completion, final completion, and initiation of operation.

c) Permit Requirements. Identify any construction, discharge and capacity permits

that will/may be required as a result of the project.

d) Sustainability Considerations (if applicable).

i) Water and Energy Efficiency. Describe aspects of the proposed project

addressing water reuse, water efficiency, and water conservation, energy

efficient design, and/or renewable generation of energy, if incorporated into

the selected alternative.

ii) Green Infrastructure. Describe aspects of project that preserve or mimic

natural processes to manage stormwater, if applicable to the selected

alternative. Address management of runoff volume and peak flows through

infiltration, evapotranspiration, and/or harvest and use, if applicable.

iii) Other. Describe other aspects of sustainability (such as resiliency or

operational simplicity) that are incorporated into the selected alternative, if

incorporated into the selected alternative.

e) Total Project Cost Estimate (Engineer’s Opinion of Probable Cost). Provide an

itemized estimate of the project cost based on the stated period of construction.

Include construction, land and right-of-ways, legal, engineering, construction

program management, funds administration, interest, equipment, construction

contingency, refinancing, and other costs associated with the proposed project.

The construction subtotal should be separated out from the non-construction

costs. The non-construction subtotal should be included and added to the

16

construction subtotal to establish the total project cost. An appropriate

construction contingency should be added as part of the non-construction subtotal.

For projects containing both water and waste disposal systems, provide a separate

cost estimate for each system as well as a grand total. If applicable, the cost

estimate should be itemized to reflect cost sharing including apportionment

between funding sources. The engineer may rely on the owner for estimates of

cost for items other than construction, equipment, and engineering.

f) Annual Operating Budget. Provide itemized annual operating budget

information. The owner has primary responsibility for the annual operating

budget, however, there are other parties that may provide technical assistance.

This information will be used to evaluate the financial capacity of the system.

The engineer will incorporate information from the owner’s accountant and other

known technical service providers.

i) Income. Provide information about all sources of income for the system

including a proposed rate schedule. Project income realistically for existing

and proposed new users separately, based on existing user billings, water

treatment contracts, and other sources of income. In the absence of historic

data or other reliable information, for budget purposes, base water use on 100

gallons per capita per day. Water use per residential connection may then be

calculated based on the most recent U.S. Census, American Community

Survey, or other data for the state or county of the average household size.

When large agricultural or commercial users are projected, the Report should

identify those users and include facts to substantiate such projections and

evaluate the impact of such users on the economic viability of the project.

ii) Annual O&M Costs. Provide an itemized list by expense category and project

costs realistically. Provide projected costs for operating the system as

improved. In the absence of other reliable data, base on actual costs of other

existing facilities of similar size and complexity. Include facts in the Report

to substantiate O&M cost estimates. Include personnel costs, administrative

costs, water purchase or treatment costs, accounting and auditing fees, legal

fees, interest, utilities, energy costs, insurance, annual repairs and

maintenance, monitoring and testing, supplies, chemicals, residuals disposal,

office supplies, printing, professional services, and miscellaneous as

applicable. Any income from renewable energy generation which is sold back

to the electric utility should also be included, if applicable. If applicable, note

the operator grade needed.

iii) Debt Repayments. Describe existing and proposed financing with the

estimated amount of annual debt repayments from all sources. All estimates

of funding should be based on loans, not grants.

iv) Reserves. Describe the existing and proposed loan obligation reserve

requirements for the following:

Debt Service Reserve – For specific debt service reserve requirements

consult with individual funding sources. If General Obligation bonds are

proposed to be used as loan security, this section may be omitted, but this

should be clearly stated if it is the case.

17

Short-Lived Asset Reserve – A table of short lived assets should be

included for the system (See Appendix A for examples). The table should

include the asset, the expected year of replacement, and the anticipated

cost of each. Prepare a recommended annual reserve deposit to fund

replacement of short-lived assets, such as pumps, paint, and small

equipment. Short-lived assets include those items not covered under

O&M, however, this does not include facilities such as a water tank or

treatment facility replacement that are usually funded with long-term

capital financing.

7. CONCLUSIONS AND RECOMMENDATIONS

Provide any additional findings and recommendations that should be considered in

development of the project. This may include recommendations for special studies,

highlighting of the need for special coordination, a recommended plan of action to

expedite project development, and any other necessary considerations.

18

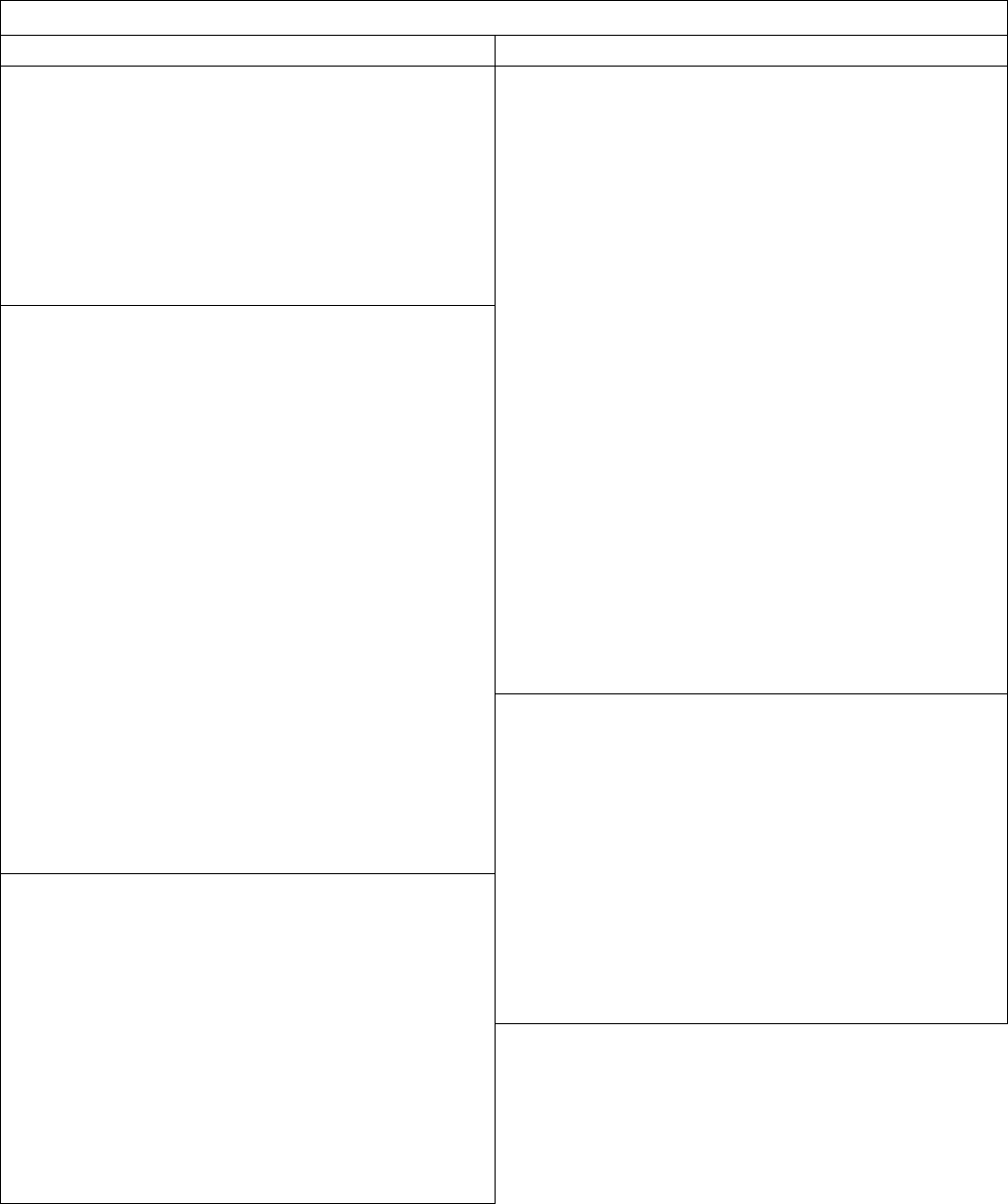

Appendix A: Example List of Short-Lived Asset Infrastructure

EstimatedRepair,Rehab,ReplacementExpensesbyItemwithinupto20YearsfromInstallation)

DrinkingWaterUtilities WastewaterUtilities

SourceRelated

TreatmentRelated

Pumps

Pump

PumpControls

PumpControls

PumpMotors

PumpMotors

Telemetry

Chemicalfeedpumps

Intake/Wellscreens

MembraneFiltersFibers

WaterLevelSensors

Field&ProcessInstrumentationEquipment

PressureTransducers

UVlamps

TreatmentRelated Centrifuges

Chemicalfeedpumps Aerationblowers

AltitudeValves Aerationdiffusersandnozzles

ValveActuators Tricklingfilters,RBCs,etc.

Field&ProcessInstrumentationEquipment Beltpresses&driers

Granularfiltermedia SludgeCollectingandDewateringEquipment

Aircompressors&controlunits LevelSensors

Pumps PressureTransducers

PumpMotors PumpControls

PumpControls Back‐uppowergenerator

WaterLevelSensors ChemicalLeakDetectionEquipment

PressureTransducers Flowmeters

SludgeCollection&Dewatering SCADASystems

UVLamps CollectionSystemRelated

Membranes Pump

Back‐uppowergenerators PumpControls

ChemicalLeakDetectionEquipment PumpMotors

Flowmeters Trashracks/barscreens

SCADASystems Sewerlineroddingequipment

DistributionSystemRelated Aircompressors

ResidentialandSmallCommercialMeters Vaults,lids,andaccesshatches

Meterboxes Securitydevicesandfencing

Hydrants&Blowoffs Alarms&Telemetry

Pressurereducingvalves ChemicalLeakDetectionEquipment

Crossconnectioncontroldevices

Altitudevalves

Alarms&Telemetry

Vaults,lids,andaccesshatches

Securitydevicesandfencing

Storagereservoirpainting/patching