Policy Framework and its

Deployment Mechanism in India

Carbon Capture,

Utilization and

Storage (CCUS)

November 2022

Authors and Acknowledgements

Atanu Mukherjee, Principal Investigator,

M. N. Dastur & Co. (P) Ltd.

Saurav Chatterjee, Co-Principal Investigator,

M. N. Dastur & Co. (P) Ltd.

Authors Acknowledgment

The team is grateful for the mentorship and inputs provided by:

Dr. V. K. Saraswat, Member, NITI Aayog

Dr. Neeraj Sinha, Sr. Adviser (S&T), NITI Aayog

Shri Rajnath Ram, Adviser (Energy), NITI Aayog

Leadership

The study was carried out with the financial support of NITI Aayog,

Government of India and conducted by M. N. Dastur & Co. (P) Ltd.

The team is grateful for the input and contributions received from:

Shri Jawahar Lal, Deputy Chief Engineer, NITI Aayog

Shri Naveen Kumar Vidyarthi, Director (Energy), NITI Aayog

Shri Amit Verma, Director (Energy), NITI Aayog

Shri Manoj Kumar Upadhayay,

Deputy Advisor (Energy), NITI Aayog

Dr. Abhinav Trivedi, Consultant, NITI Aayog

Shri Akash Jain, Young Professional, NITI Aayog

Abhijit Sarkar, Vice President, Dastur International, Inc.

Dr. Suprotim Ganguly, Techno-Strategic Advisor,

M. N. Dastur & Co. (P) Ltd.

Arunava Maity, Sr. Principal Analyst, M. N. Dastur & Co. (P) Ltd.

Dr. Vikram Vishal, Convenor - National Centre of Excellence in

Carbon Capture and Utilization, IIT Bombay

Dr. Ken Medlock, Baker Institute, Rice University

Phil Amick, Principal, Dastur Energy Inc.

Dr. Susan D. Hovorka, The University of Texas at Austin

Saptarshi Bhattacharya, M. N. Dastur & Co. (P) Ltd.

Anand Senguttuvan, M. N. Dastur & Co. (P) Ltd.

Arnab Adak, M. N. Dastur & Co. (P) Ltd.

Debarka Chakraborty, M. N. Dastur & Co. (P) Ltd.

Anindya Majumdar, M. N. Dastur & Co. (P) Ltd.

Pratyush Kumar, M. N. Dastur & Co. (P) Ltd.

We would also like to thank the following organizations who provided

valuable inputs in shaping the report:

Shri A. Balan, Member (Planning),

Central Electricity Authority, India

Shri A K Rajput, Chief Engineer, Central Electricity Authority, India

Shri Neelesh Kr Sah, Joint Secretary,

Ministry of Environment, Forest and Climate Change, Govt. of India

Shri Gurdip Singh, Chairman and Managing Director,

National Thermal Power Corporation Ltd.

Shri Nalin Singhal, Chairman and Managing Director,

Bharat Heavy Electricals Ltd.

Shri U K Bhattacharya, Director,

National Thermal Power Corporation Ltd.

Shri Anirban Das Gupta, Director-in-Charge,

Steel Authority of India Ltd.

Shri Sanjay Shrivastava, Executive Director -

Chief Carbon Management & Sustainability Group,

Oil and Natural Gas Corporation Ltd.

Shri Peeyush Kumar, Officer on Special Duty,

Ministry of Coal, Govt. of India

Dr. Anita Gupta, Adviser / Scientist G,

Department of Science & Technology

Shri Sanjay Singh, Scientist G, Technology Information

Forecasting and Assessment Council

Dr. Deepak Saxena, Executive Director, Indian Oil Corporation Ltd.

Shri Pradeep, Executive Director, Technology Information

Forecasting and Assessment Council

Shri Gaurav Mishra, Executive Engineer,

Reservoir, Oil and Natural Gas Corporation Ltd.

Shri Sujit Mitra, General Manager - Reservoir,

Oil and Natural Gas Corporation Ltd.

Smt. Neha Verma, Director, Ministry of Steel, Govt. of India

Shri Paramjeet Singh, Additional Industrial Advisor,

Ministry of Steel, Govt. of India

Dr. Mukesh Kumar, Director - Steel Research & Technology

Mission of India, Ministry of Steel, Govt. of India

Shri Kumar Saurabh, Deputy Director,

Ministry of Power, Govt. of India

Ms. Soujanya Mondal, Senior Manager, Corporate Strategy,

Planning & Advocacy, Gas Authority of India Ltd.

Shri Rahul Buswala, Strategy Manager,

Carbon Capture, Bharat Heavy Electricals Ltd.

Acknowledgment

Available at:

NITI Aayog: www.niti.gov.in

Disclaimer

M. N. Dastur & Co. (P) Ltd. has received the financial assistance under the Research Scheme of NITI Aayog to prepare the report. While due care has

been exercised to prepare the report using the data from various sources, NITI Aayog does not confirm the authenticity of data and the accuracy of

the methodology to prepare the report. NITI Aayog shall not be held responsible for finding or opinions expressed in the document. This

responsibility completely rests with M. N. Dastur & Co. (P) Ltd.

03

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

04

About DASTUR

M. N. Dastur & Company (P) Ltd. along with Dastur Energy (DASTUR)

conceptualizes, designs, and develops business, technology, engineering and policy

blueprints for clean energy systems for enterprises, governments, and institutions.

DASTUR envisions the enablement of an affordable and clean energy future

through industrial decarbonization, carbon capture, low-carbon alternative fuels

and low-carbon transformation of solid fuels and hydrocarbons. DASTUR has

conceptualized and designed several pioneering industrial-scale low-carbon

projects worldwide in hydrogen, methanol, chemicals, steel, hydrocarbons, power,

and carbon capture, and works with governments and international institutions on

policy and market design aspects for enabling a low-carbon economy. DASTUR’s

intellectual property and operating frameworks help design commercially viable

and sustainable energy solutions using low-carbon energy technologies and

carbon capture utilization and storage. DASTUR optimizes the design of integrated

clean energy systems for superior long-term techno-economic performance that

include emerging energy systems like industrial carbon capture systems, CO

2

utilization and sequestration, clean baseload power, clean hydrogen production,

net-negative gasifier complexes, methanol ecosystems, waste gas conditioning and

use, clean chemicals, and clean materials. DASTUR’s intellectual assets in clean

energy systems, economics, and finance help shape policies and strategies in clean

energy market designs, carbon capture, carbon credit & trade mechanisms,

regulatory frameworks, and macro-energy strategies for nations and institutions.

By designing scalable clean energy systems which are pragmatic, commercially

viable, and competitive, DASTUR makes sustainability and climate goals real,

achievable, and implementable.

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

05

Executive Summary 15

1. Introduction 27

2. Analysis of Sector-wise CO

2

Emissions 35

3. Overview of CO

2

Capture & Utilization Technologies 67

4. Potential for CO

2

Storage in India 93

5. CCUS Policy Framework for India 111

6. Investment and Financing Mechanism 135

7. Conclusions 157

Bibliography 163

Contents

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

06

List of Figures

Figure E-1 The 70% Emissions Challenge

Figure E-2 Sector-wise CO

2

Emissions (in mtpa)

Figure E-3 Cost Curve for CO

2

Capture Across

Industries/Sectors

Figure E-4 Mega Scale CO

2

Cluster Model

Figure E-5 Region-wise Storage Clusters in India

Figure 1.1 The 70% Emissions Challenge

Figure 2-1 Illustration of Emission Types and Boundary

Consideration

Figure 2-2 Sector-wise CO

2

Emissions, mtpa

Figure 2-3 Break-up of Installed Generation Capacity, GW

Figure 2-4 Break-up of Generation, Billion Unit

Figure 2-5 Break-up of Thermal Power Plants by Fuel

(Power Sector at a Glance ALL INDIA)

Figure 2-6 PFD of Coal-fired TPP

Figure 2-7 Schematic Representation of Gas Turbine

Figure 2-8 NGCC Power Plant Schematic Diagram

Figure 2-9 Share of Total CO

2

Emissions by Each Prime

Mover, mtpa

Figure 2-10 State-Wise Analysis of CO

2

Emissions (mtpa)

Figure 2-11 Crude Steel Capacity & Production in Last

5 Years (in mtpa)

Figure 2-12 Process Route Wise Steel Production and

Contribution (in mtpa)

Figure 2-13 Various Iron and Steel Making Routes in India

Figure 2-14 CO

2

Emission (in tonne) per tonne of Finished

Steel BF-BF route

Figure 2-15 Region-wise Distribution and Total CO

2

Emissions (in mtpa)

Figure 2-16 Cement Production (in mtpa)

Figure 2-17 Per Capita Cement Consumption in 2018 (in kg)

Figure 2-18 Cement Production (in mtpa)

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Figure 2-19 Top 10 Cement Clusters Based on Cumulative

Capacity

Figure 2-20 Cement Demand (in mtpa) and Per-capita

Cement Consumption (in kg)

Figure 2-21 Typical Process Flow Diagram for Cement

Making

Figure 2-22 Typical CO

2

Cascade (in kg of CO

2

per tonne

of cement)

Figure 2-23 Cement Plant CO

2

Emission Projection

(in mtpa)

Figure 2-24 Simplified Block Flow Diagram of Hydrogen

Generation Units (HGUs)

Figure 2-25 Domestic Oil Production (in mtpa)

Figure 2-26 Natural Gas Production - FY 2014-15 to FY

2019-20 (in billion cubic meter)

Figure 2-27 Oil Production by Operator in FY 2019-20

(in mtpa)

Figure 2-28 Natural Gas Production in FY 2019-20 (in

billion cubic meters)

Figure 2-29 Carbon Emission by E&P Operator in FY

2019-20 (in mtpa of CO

2

eq)

Figure 2-30 Emissions Projection for 2030, MT CO

2

eq

Figure 2-31 A Typical Coal Gasification Based Ecosystem

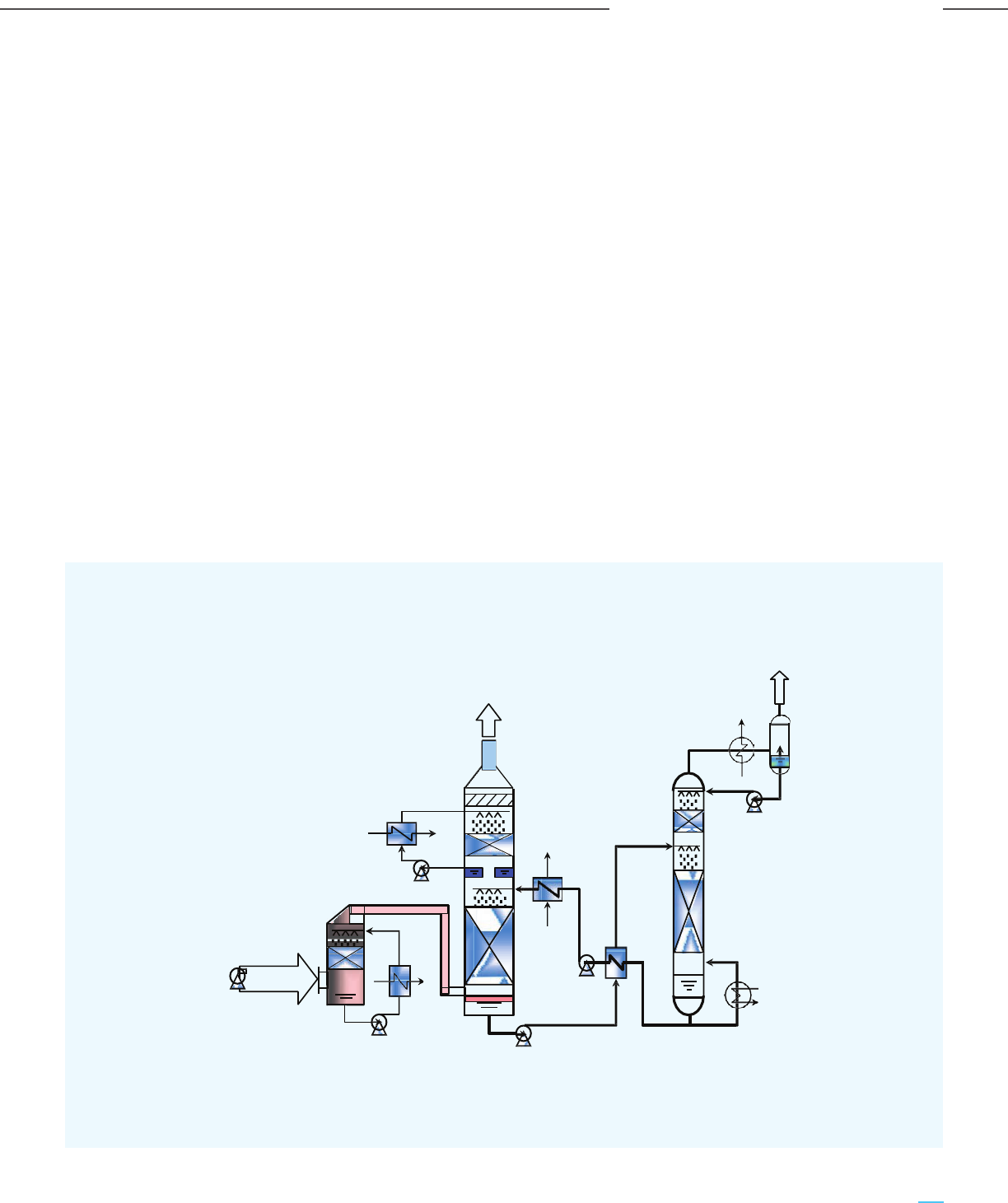

Figure 3-1 Scheme of Post-combustion, Pre-combustion &

Oxy-fuel combustion

Figure 3-2 Simplified Representation of CO

2

Capture

Technologies

Figure 3-3 Schematic Representation of Working Principle

of Solvent-Based CO

2

Capture

Figure 3-4 Schematic Representation of CO

2

Absorption

Capacity of Chemical and Physical Solvents as

a Function of the Partial Pressure of CO

2

Figure 3-5 Operating Regimes of Various Solvents for

CO

2

Capture

Figure 3-6 Typical Flow Diagram of a Chemical Solvent

Based CO

2

Capture

Figure 3-7 Process Flow Diagram of Air Liquide’s Amine

Based CO

2

Capture

Figure 3-8 Process Flow Diagram of a Pilot Slipstream

Test Unit at National Carbon Capture Center,

USA using ION’s Proprietary ICE-21 Solvent for

CO

2

Capture

Figure 3-9 Process Flow Diagram of KM CDR CO

2

Capture

using Proprietary KS-1 Solvent

Figure 3-10 Process Flow Diagram of the Amine Guard

™

FS

CO

2

Capture using Proprietary UCARSOL

™

Solvent

Figure 3-11 Process Flow Diagram of Baker Hughes Chilled

Ammonia Process (CAP) using Ammonium

Carbonate Solvent

Figure 3-12 Basic Process Flow diagram of the Rectisol

®

Process

Figure 3-13 Basic Process Flow Diagram of the Selexol

™

Process

Figure 3-14 Basic Process Flow Diagram of Air Products’

VSA Technology

Figure 3-15 Five-step Pressure-swing Cycle of UOP’s

Polybed

™

PSA Systems

Figure 3-16 Process Flow Diagram of the Cryocap

™

H

2

Technology

Figure 3-17 Summary of Major Large Scale Carbon Capture

Commercial Projects

Figure 3-18 Cost Curve for CO

2

Capture Across

Processes/Industries

Figure 3-19 Possible CO

2

Utilization Pathways

Figure 3-20 A Simplified Schematic of CO

2

Mineralization

Process

Figure 3-21 Typical Schematic for the CO

2

Hydrogenation

Process along with Integration with Carbon

Capture Unit

Figure 3-22 Systematic Indigenization of Technology

through Technology Transfer

Figure 3-23 Promising CO

2

Utilization Technology

Propositions

Figure 4-1 Working of CO

2

EOR

Figure 4-2 Working of CO

2

ECBMR

Figure 4-3 Classification of CO

2

Storage Potential of

Sedimentary Basins of India

Figure 4-4 Major Sedimentary Basins in India with their

CO

2

Storage Potential

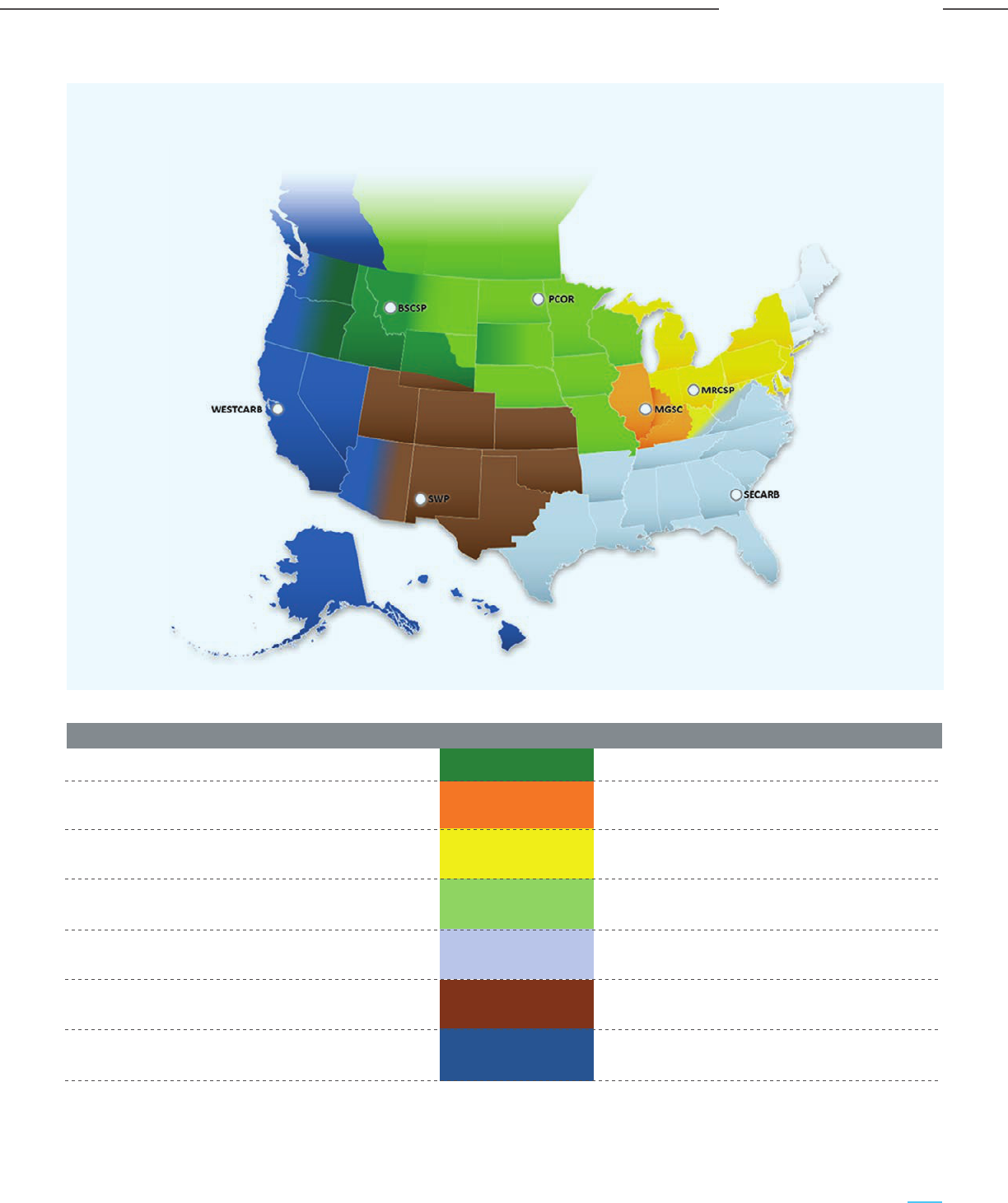

Figure 4-5 Seven RSCPs Funded by the US DOE

Figure 5-1 CCUS Hub and Cluster Framework

Figure 5-2 CCUS Cluster Around the World

Figure 5-3 Rotterdam CCS Cluster

Figure 5-4 Timeline Denver City Hub

Figure 5-5 Denver City Storage

Figure 5-6 ACTL Map

Figure 5-7 ACTL Timelines

Figure 5-8 Mega Scale CO

2

Cluster Model

Figure 5-9 Region-wise Storage Clusters in India

Figure 6-1 Utility Costs Considered

Figure 6-2 Sector-wise CO

2

emission and Contribution

Figure 6-3 Incentives such as the Product Linked

Incentive (PLI) scheme create a level playing

field for low-carbon products

Figure 6-4 CCUS Financing Mechanism

Figure 6-5 Results of CCUS Financing Analysis – Financing

Option 1 (Clean Energy Cess)

Figure 6-5 Results of CCUS Financing Analysis – Financing

Option 2 (Bonds and Govt. Budget Support)

Figure 6-6 SPV Framework to Finance Gasification

Projects in a Deficit-Neutral Way

07

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

08

List of Tables

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Table E-1 Estimated CO

2

Storage Capacity in India

Table E-2 Sector-wise Typical Carbon Capture Capital

Charge and Cash Cost

Table E-3 CCUS Funding through Clean Energy Cess

Table E-4 CCUS Funding with Bonds and Government

Budgetary Support

Table 1-1 Large Scale CCUS facilities in operation in 2020

Table 2-1 Flue Gas Characteristics of Coal-Fired Thermal

Power Plants

Table 2-2 Flue Gas Characteristics of Coal-Fired Thermal

Power Plants

Table 2-3 Overall Analysis of CO

2

Emissions from the Power

Sector in India

Table 2-4 CO

2

Emissions by Prime Mover for Plants with

Minimum 2 mtpa Capturable CO

2

Table 2-5 District-wise CO

2

Emission Analysis

Table 2-6 Energy & CO

2

Volume Projections for

FY 2029-30

Table 2-7 CO2 Direct Emission Intensities for Various Iron

Making Routes

Table 2-8 Major Players of Cement Industry and Capacity

in mtpa)

Table 2-9 State-wise Cement Capacity

Table 2-10 Top 20 Districts/Clusters and Aggregate Capacity

Table 2-11 Plant Capacity Distribution

Table 2-12 Consumption Parameters

Table 2-13 Gas Composition at Different Source Points

Table 2-14 CO

2

Concentration at Different Refinery Units

Table 2-15 Cracker Furnace Flue Gas Composition

Table 2-16 Total CO

2

Emissions from Refineries,

Petrochemicals & Fertilizers

Table 2-17 Total CO

2

Emissions from Oil & Gas Upstream

Operations

Table 2-18 Total CO

2

Emission from Coal Gasification

Table 2-19 Sector-wise CO

2

Emissions and Interventions

Required

Table 3-1 Comparison of Various Flow Schemes of UOP

Amine Guard

™

FS Technology

Table 3-2 Comparative Analysis of Various Classes of CO

2

Capture Technologies

Table 3-3 Various CO

2

Utilization Pathways

Table 4-1 CO

2

EOR Storage Capacity Estimates

Table 4-2 CO

2

ECBMR Storage Capacity Estimates

Table 4-3 CO

2

Storage Capacity Estimation for Deep

Saline Aquifers

Table 4-4 Basalt Formation CO

2

Storage Capacity Estimates

Table 4-5 Theoretical CO

2

Storage Capacity in India

Table 5-1 EU Funding Schemes for CCUS

Table 5-2 Carbon Pricing System Adopted by Different

Provinces of Canada

Table 5-3 Comparison of Carbon Credits/Incentives and

Carbon Tax Based Policy

Table 5-4 Key Elements of a CCUS Policy Framework

for India

Table 5-5 Sedimentary Basins Spanning Across Multiple

Regions

Table 6-1 Capex and Opex Considerations for CCUS Retrofit

Table 6-2 Sector-wise Typical Carbon Capture Capital Cost

Table 6-3 Sector-wise Typical Carbon Capture Cash Costs

Table 6-4 Sector-wise Typical Carbon Capture Cash Costs

and Capital Charges

Table 6-5 Carbon Capture Volume in Two Scenarios and

Tentative Investment

Table 6-6 Assumptions/Considerations for CCUS Financing

Analysis

Table 6-7 45Q Tax Credit Amounts

Table 6-8 Tax Credits for Hydrogen Production in USA -

Inflation Reduction Act of 2022

Table 6-9 Probable Distribution of 750 mtpa and low-C

Product Volume

Table 7-1 Sector-wise CO

2

Emissions and Interventions

Required

Table 7-2 Theoretical CO

2

Storage Capacity in India

Table 7-3 Key Elements of a CCUS Policy Framework

for India

Table 7-4 Sector-wise Typical Carbon Capture Capital

Charge and Cash Cost

Abbreviations

ACTL Alberta Carbon Dioxide Trunk Line

AD Accelerated Depreciation

ADB Asian Development Bank

ARRA American Recovery and Reinvestment Act

BEE Bureau of Energy Efficiency

BF Blast Furnace

BGS British Geological Society

BOF Basic Oxygen Furnace

BOO Build-Own-Operate

CAP Chilled Ammonia Process

CBAM Cross Border Adjustment Mechanism

CBM Coal Bed Methane

CCF Climate Change Fund

CCFC Carbon Capture Finance Corporation

CCL Central Coalfields Limited

CCM Carbon Concentrating Mechanism

CCUS Carbon Capture Utilization and Storage

CDU Crude Distillation Unit

FCC Fluid Catalytic Cracking

CEA Central Electricity Authority

CEIL Cairn Energy India Limited

CFD Contracts-for-Difference

CGP Co-Gen Plant

CIF CCUS Infrastructure Fund

CIFIA Infrastructure Finance and Innovation Act

CIL Coal India Limited

CIR Color Infrared

CO Carbon Monoxide

Coal DR Coal Based DR Processes

COG Coke Oven Gas

CRF Capital recovery factor

CRI Carbon Recycling International

DAC Direct Air Capture

DEPG Dimethyl Ether of Polyethylene Glycols

DGH Directorate General of Hydrocarbons

DOE Department of Energy

DRCF Dual Refrigerant CO

2

Fractionation

DVP Deccan Volcanic Province

E&P Exploration and production activities

EAF Electric Arc Furnace

EBP Ethanol Blend Petrol

ECBMR Enhanced Coal Bed Methane Recovery

ECL Eastern Coalfields Limited

EIB European Investment Bank

EMIT Electromagnetic Induction Tomography

EOR Enhanced Oil Recovery

09

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

EPA Environmental Protection Agency

ERT Electrical Resistance Tomography

ESP Electrostatic Precipitator

EU ETS European Union Emissions Trading System

EXIM Export Import Bank of the United States

FCC Fluid Catalytic Cracking

FECM Fossil Energy and Carbon Management

FT Fischer-Tropsch

FTE Full Time Equivalent

Gas DR Gas Based DR Processes

GBI Generation Based Incentives

GBS Gross Budgetary Support

GFANZ Glasgow Financial Alliance for Net Zero

GGPPA Greenhouse Gas Pollution Pricing Act

GT Giga Tonne

GTPA Gigatonne Per Annum

HGU Hydrogen Generation Unit

HP High Pressure

IEA International Energy Agency

IECM Integrated Environmental Control Model

IETF Industrial Energy Transformation Initiative

IF Induction Furnace

IFC International Finance Corporation

ION ION Clean Energy

IP Intellectual Property

IPCC Intergovernmental Panel on Climate Change

JTF Just Transition Fund

JTM Just Transition Mechanism

KM CDR

™

Kansai Mitsubishi Carbon Dioxide Recovery

LCA Life Cycle Analysis / Life Cycle Assessment

LCFS Low Carbon Fuel Standard

LETS Low Emission Technology Statement

LIC Life Insurance Corporation

LP Low-Pressure

MDEA Methyl diethanolamine

MHI Mitsubishi Heavy Industries Ltd

MRV Monitoring Reporting and Verification

framework

MTPA Million Tonne Per Annum

MVA Monitoring Verification and Accounting

NAS Non Aqueous Solvent

NCEEF National Clean Energy and Environment Fund

NETL National Energy Technology Laboratory

NEXI Nippon Export and Investment Insurance

NGCC Natural Gas Combined Cycle

10

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

11

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

OBPS Output Based Pricing System

OPC Ordinary Portland Cement

OPGC Odisha Power Generation Corporation Limited

OPGGSA Offshore Petroleum and Greenhouse Gas

Storage Act 2006

PLI Production Linked Incentive

PMAY Pradhan Mantri Awas Yojana

PP Power Plant

PPC Portland Pozzolana Cement

PSA Pressure Swing Adsorption

PSC Portland Slag Cement

RCF Rashtriya Chemicals & Fertilizers

RCP Rotterdam Cluster Project

RCSPs Regional Carbon Sequestration Partnerships

RRF Recovery and Resilience Facility

SAR Synthetic Aperture Radar

SECARB Southeast Regional Carbon Sequestration

Program

SECL South-Eastern Coalfields Limited

SMR Steam Methane Reforming

SSEB Southern States Energy Board

syngas Synthesis Gas

T&S Transport and Storage

TCF Trillion Cubic Feet

TIER Technology Innovation and Emissions Reduction

TIFAC Technology Information Forecasting and

Assessment Council

TSA Temperature Swing Adsorption

UIC Underground Injection Control

UKRI UK Research and Innovation’s

URR Ultimate Recoverable Reserves

USIDFC US International Development Finance

Corporation

VDU Vacuum Distillation Unit

VGas Volume of Methane

VRM Vertical Roller Mill

VSA Vacuum Swing Adsorption

VSP Vertical Seismic Profile

WCL Western Coalfields Limited

12

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

13

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

14

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive

Summary

Carbon Capture, Utilization and Storage is an Essential

Imperative for India to Reach its Decarbonization Goals

India is the 3rd largest emitter of CO

2

in the world

after China and the US, with estimated annual

emissions of about 2.6 gigatonne per annum (gtpa).

The Government of India has committed to reducing

CO

2

emissions by 50% by 2050 and reaching net zero

by 2070. The growth of renewable power capacity has

been one of the key success stories of the clean

energy transition in India; however, the power sector

only contributes to about 1/3 rd of the aggregate CO

2

emissions, which will continue to abate as renewables

increasingly replace fossil fuel based power

generation. The growing industrial economy emits

close to another third of the aggregate emissions that

are hard to abate, and will continue to increase unless

new technologies and carbon abatement mechanisms

are deployed. At the same time, while India phases

down the use of coal over time, India will be

dependent on fossil energy sources like coal for a long

time to support the industry and meet the

requirements for affordable and reliable baseload

power. Therefore, India’s decarbonization pathway

has to also embrace technologies which will abate

emissions from the hard to abate industrial sectors as

well as for residual baseload power generation.

Carbon Capture Utilization and Storage (CCUS) has an

important and critical role to play in decarbonizing the

industrial sector, which is hard to electrify and hard to

abate, due to the use of fossil fuels not only as a

source of energy but within the process itself. CCUS

also has an important role to play in decarbonizing the

power sector, given India’s present reliance on coal

for meeting over 70% of its electricity needs. Even if

India is able to substantially green the grid and meet

the target of 500 GW installed capacity of renewables

by 2030, there would still be a need to meet the

baseload power demand from fossil fuels (most likely

coal) or other dispatchable sources, given the

intermittency and non-dispatchable nature of solar

and wind power.

Direct Air Capture (DAC) that directly captures dilute

CO

2

(415 ppm) from the air, may also emerge as a

form of carbon capture that has wide applicability as it

is independent of the source and concentration of the

emission stream. However, DAC is still in its early

stages and the economics (present cost of DAC is

estimated to range between US$ 400-800/tonne of

CO

2

) and scale of operations are yet to be established.

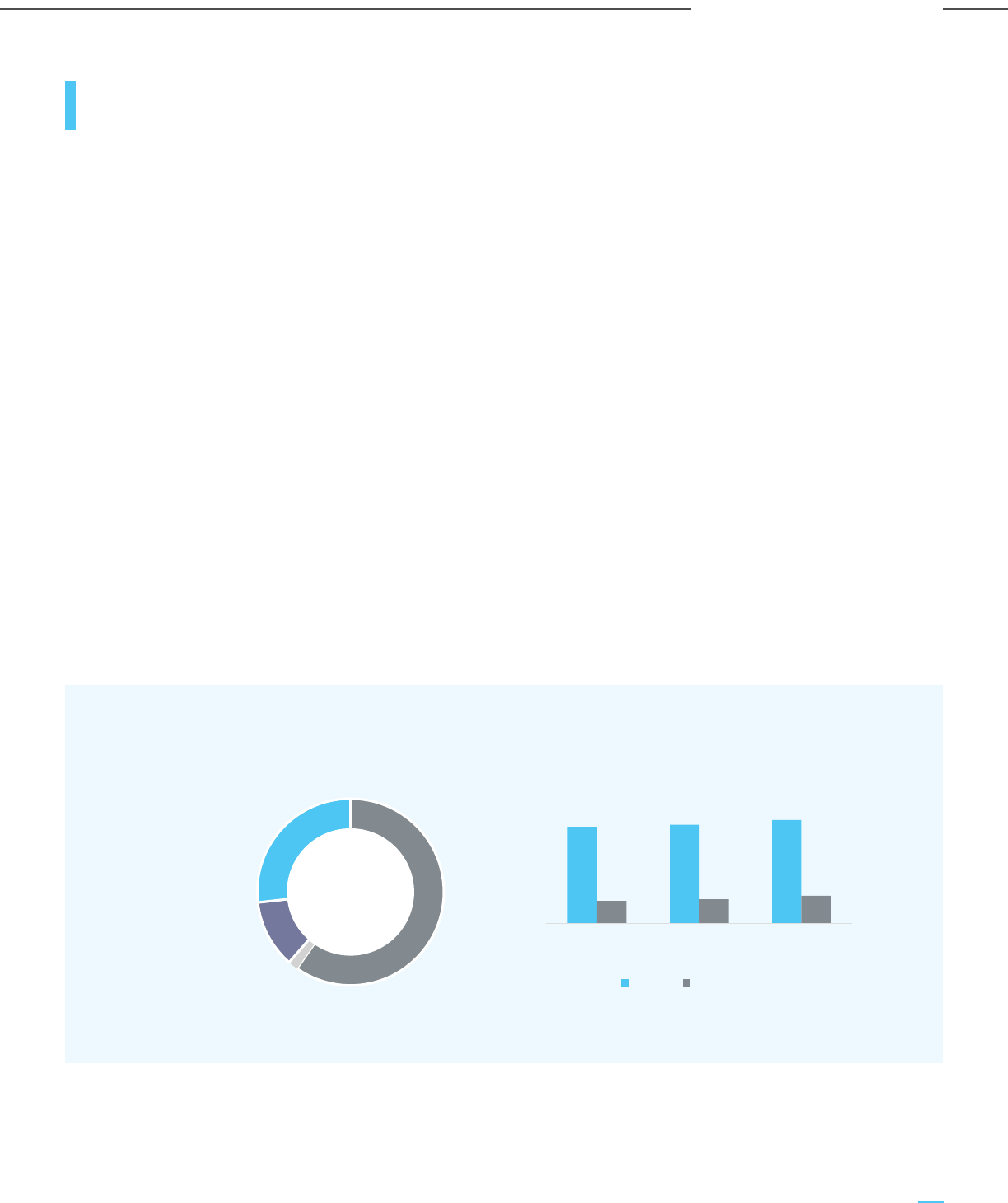

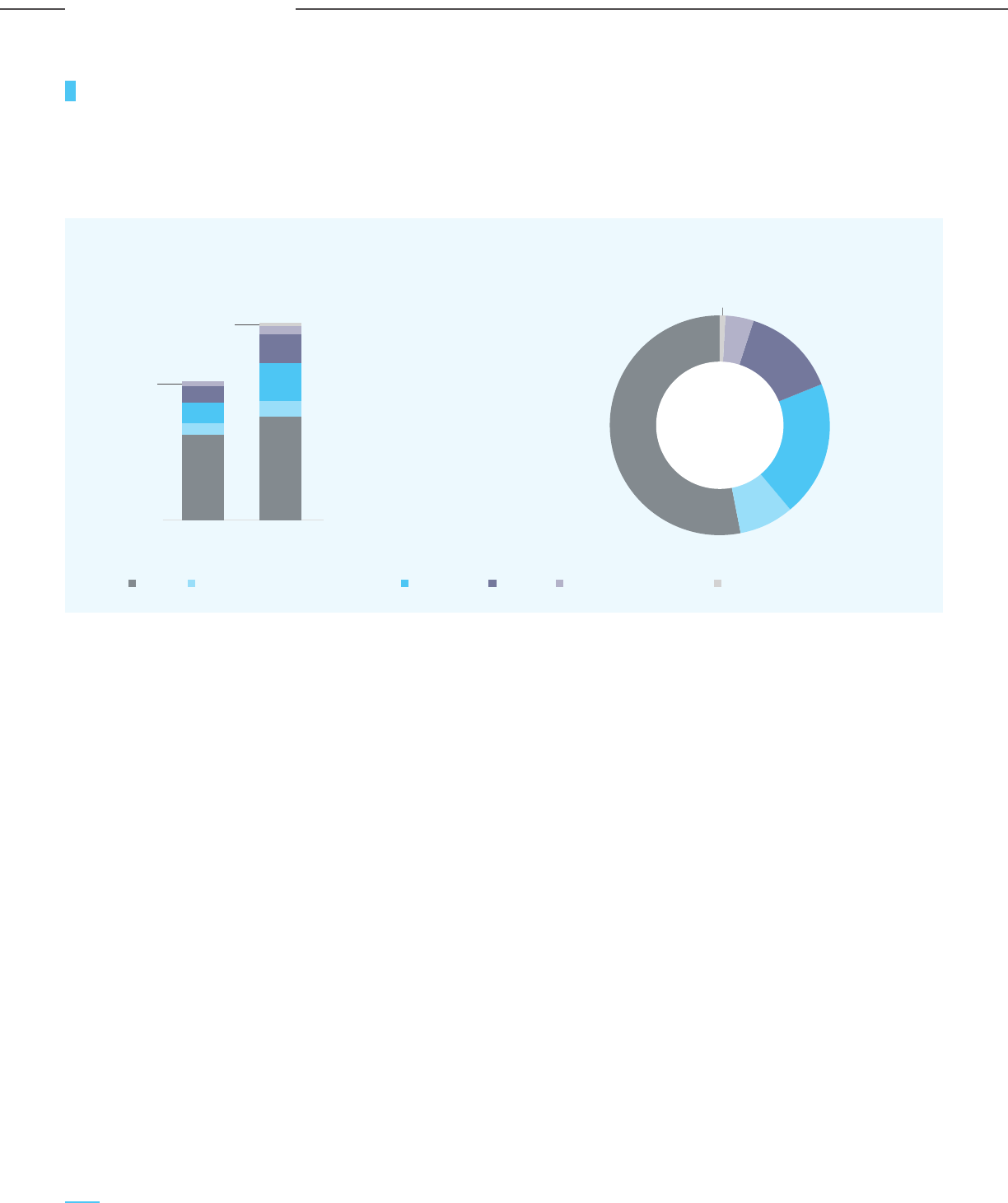

Figure E-1: The 70% Emissions Challenge

16

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

Industry

Agriculture

Transport

Building

Electricity

31%

~30%

2.6

gtpa

~70%

20

10

5

India

A Policy Driven Approach is

Required for CCUS

Industrial Sector Needs to be

a Key Focus Area for CCUS

CCUS is key to ensuring sustainable development and

growth in India, particularly for the production of

clean products and energy, leading to an

Indian economy. The areas where CCUS can

contribute to sustained economic growth in India

are manifold:

a. Energy, materials & food security and

self-sufficiency: CCUS offers the only known

technology for decarbonizing the hard-to-electrify

and CO

2

- intensive sectors such as steel, cement,

oil & gas, petrochemicals & chemicals, and

fertilizers. These sectors are critical to the

continued growth of the Indian economy and for

ensuring energy, materials and food security for

the country.

b. Enabling the sunrise sectors of coal gasification

and low-carbon hydrogen economy: CCUS is

expected to play a major role in enabling the

hydrogen economy in India, through the

production of blue hydrogen (i.e. coal gasification

based hydrogen production coupled with CCUS)

based on the utilisation of India’s rich

endowments of coal. Given the current cost

structure of green hydrogen at US$ 5-6/kg,

cost-competitive blue hydrogen production at

around US$ 2/kg can provide a pathway for the

hydrogen economy in the future.

c. Sustenance of existing emitters: Nearly

two-thirds of India’s 144 mtpa crude steel capacity

and 210 GW of coal-based power capacity have an

age of less than 15 years and cannot be wished

away or stranded and need to be made

sustainable by retrofitting with CO

2

capture and

disposition infrastructure. Significant economic

costs and damages (estimated to be in the range

of US$ 6 billion/year by 2050) can be avoided by

ensuring the sustenance of existing emitters by

implementing CCUS.

While CCUS enables competitive and sustainable sunrise

industries in certain sectors in India, it also imposes

costs on other sectors – particularly for the adoption of

CCUS by existing emitters. The initial adoption of CCUS

implementation in such sectors will impose costs as

they start internalizing the negative externality of

emission of CO

2

into the atmosphere, whose cost is

currently borne by society. As more CO

2

utilization

technologies develop and learning curve effects set in,

CCUS costs can come down significantly and new

industries around carbon utilization will also develop.

Therefore, to enable the sustainable development of

the Indian economy, economy-wide adoption of CCUS

will require policy support to initiate and accelerate

deployment through economic incentives. These

economic incentives can take various forms like tax or

cash subsidy on the captured CO

2

, viability gap

funding, loan guarantee, demonstration project

support and R&D incentives.

India’s power and industrial sectors contributed

around 1,600 mtpa of CO

2

emissions (around 60%)

out of the total emissions of 2,600 mtpa in 2020.

The remaining 40% of emissions come from

distributed point emissions sources like agriculture,

transport, and buildings which are not amenable for

CCUS. Fuelled by economic growth across sectors as

well as rapid urbanization, emissions from these

sectors are expected to increase to nearly 2,300

mtpa by the year 2030, thus making their capture

and abatement critical.

1,004

1,210

177

240

450

196

325

2030 CO

2

emission

56

125

2020 CO

2

emission

2,291

27

102

1,621

Coal Gasifcation

NG based H

2

production Upstream O&G/Refinery/Chemicals

Cement

Iron & Steel

Power

Figure E-2: Sector-wise CO

2

Emissions (in mtpa)

17

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

CCUS has an integral role to play in the

decarbonization and sustenance of all these industries

and sectors, which are critical and vital pillars of the

Indian economy.

Steel: The future growth of the steel

industry in India is largely expected to be

based on fossil fuels and the CO

2

-intensive

BF-BOF route, given the scarcity of scrap

and natural gas in India. CCUS is

necessary for ensuring the sustainability of this

critical sector of the Indian economy and also

ensuring export competitiveness.

CCUS can also enable the scalable and profitable

conversion of waste gases from Blast Furnace, Coke

Oven and Basic Oxygen Furnaces of Integrated Steel

Plants to blue hydrogen at a cash cost of less than Rs.

100 per kg. Blue hydrogen can be used within the steel

plant as a source of clean energy or for producing clean

DRI. The blue hydrogen can also be sold to external

consumers, thus propelling the clean hydrogen

economy in India.

Cement: Cement is another major CO

2

emitting sector, where fossil fuels are

difficult to replace in the cement-making

process. The capture, sequestration and

conversion of CO

2

to aggregates and

other chemical products provide synergies for the

cement sector.

Oil & gas, refineries and chemicals: This

is another hard-to-abate sector, where

CCUS is essential for ensuring

sustainability. Carbon capture is inbuilt in

many of the processes, which makes CCUS costs

competitive for this sector.

Hydrogen production: The

cost-competitive production of blue

hydrogen using India’s rich coal

endowments is key to enabling the

hydrogen economy of the future. Carbon capture is

inbuilt in the H

2

production process, leading to

cost-competitive CCUS.

Coal gasification: Coal gasification is a

sunrise sector and key to ensuring the

materials and energy security of India,

based on India’s rich endowments of coal.

CCUS is critical to enabling the coal gasification

economy in India and the production of clean

products.

Thermal power: Even with the expected

growth in renewable energy capacities,

coal-based power will continue to meet

more than 50% of electricity demand in India in the

foreseeable future. As the largest emitter of CO

2

,

CCUS of the power sector is essential for meaningful

decarbonization and ensuring energy security in India.

Appropriate Carbon Capture

Technologies for Different

Applications

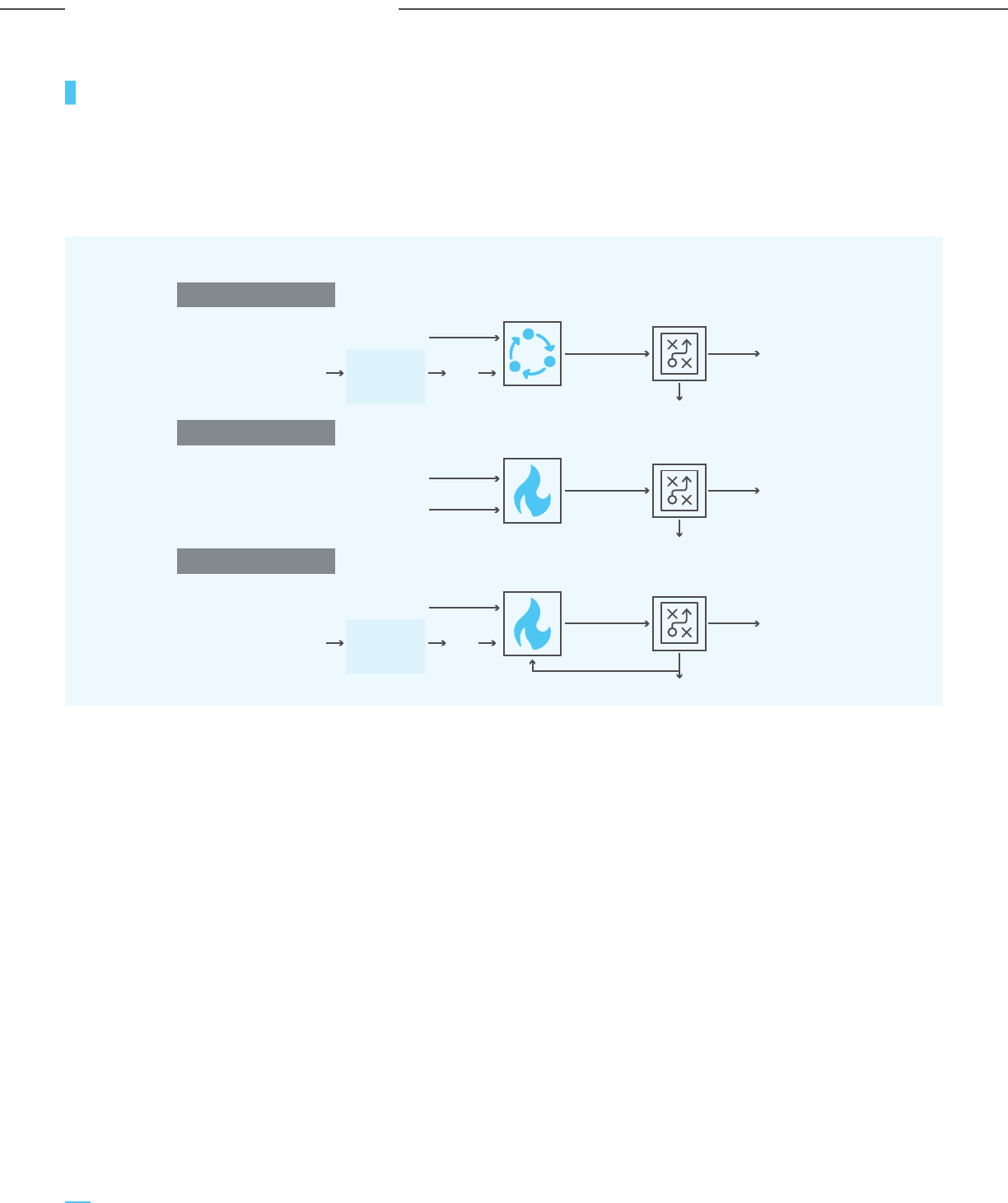

There are different categories and types of

commercial-scale carbon capture technologies and

their suitability or appropriateness for different

applications/sectors depends on the typical CO

2

gas

stream composition:

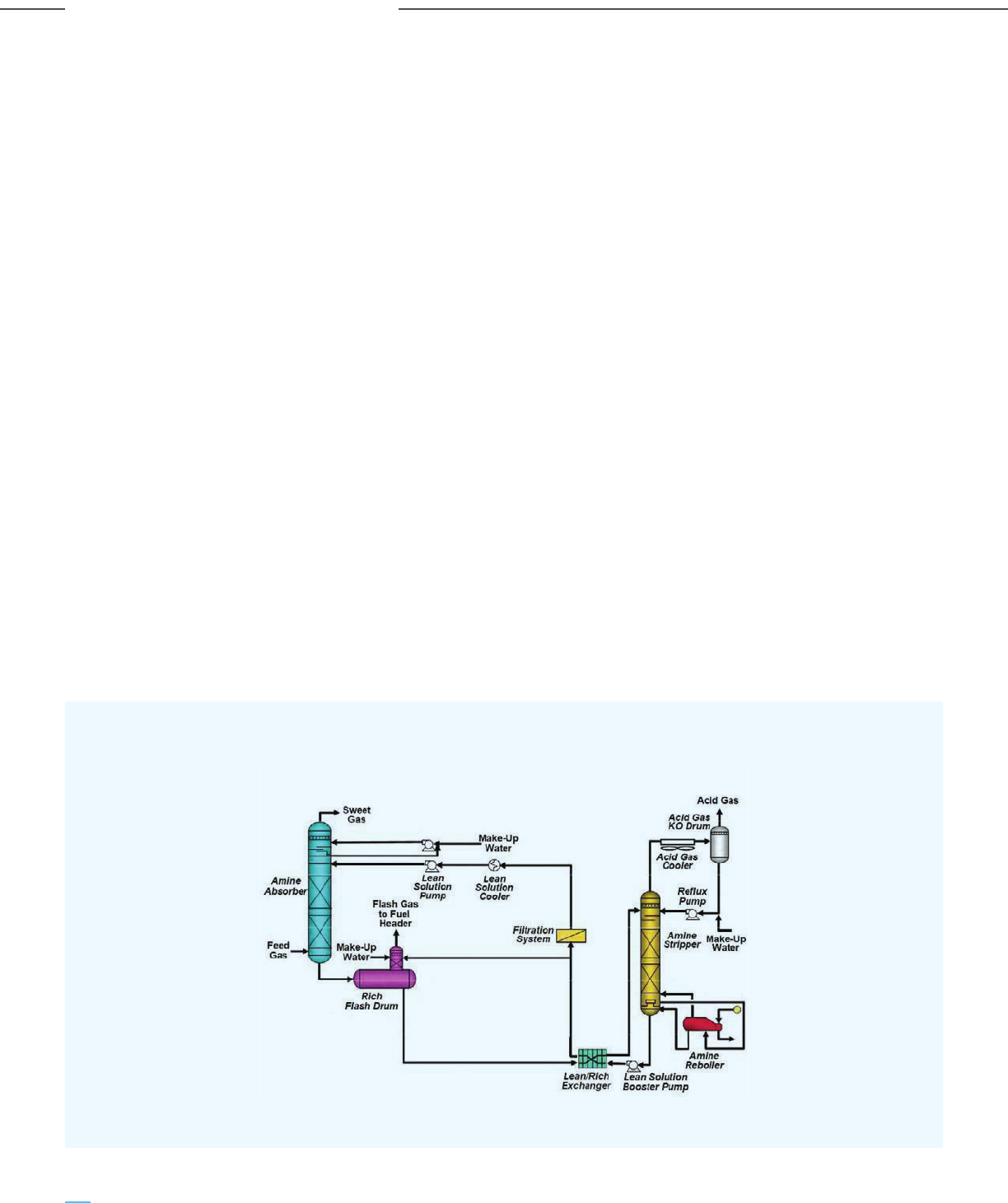

a. Chemical solvent-based CO

2

capture

technologies: preferred when dealing with gas

streams that are lean in CO

2

and have relatively

lower pressures, such as flue gas streams from

power plants, BF gases in steel plants, gas streams

in refineries or chemicals plants. The cost and

availability of steam is also a key factor as

regenerating the solvent requires large quantities

of steam.

b. Physical solvent-based CO

2

capture

technologies: these work well on gas streams with

relatively higher CO

2

concentration and pressure,

such as pre-combustion capture in the case of

gasification projects.

c. Adsorption-based CO

2

capture: suitable for gas

streams with moderate to high pressure and

moderate CO

2

concentration such as SMR flue gas

or BF gas.

d. Cryogenic CO

2

capture: preferred in cases where

the cost of power is low. This technology can be

applied for carbon capture from the PSA tail gas

of Steam Methane Reforming Units (for producing

H

2

) and provides a unique advantage of increasing

the yield/recovery of hydrogen production from

the same quantity of feedstock (natural gas).

18

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

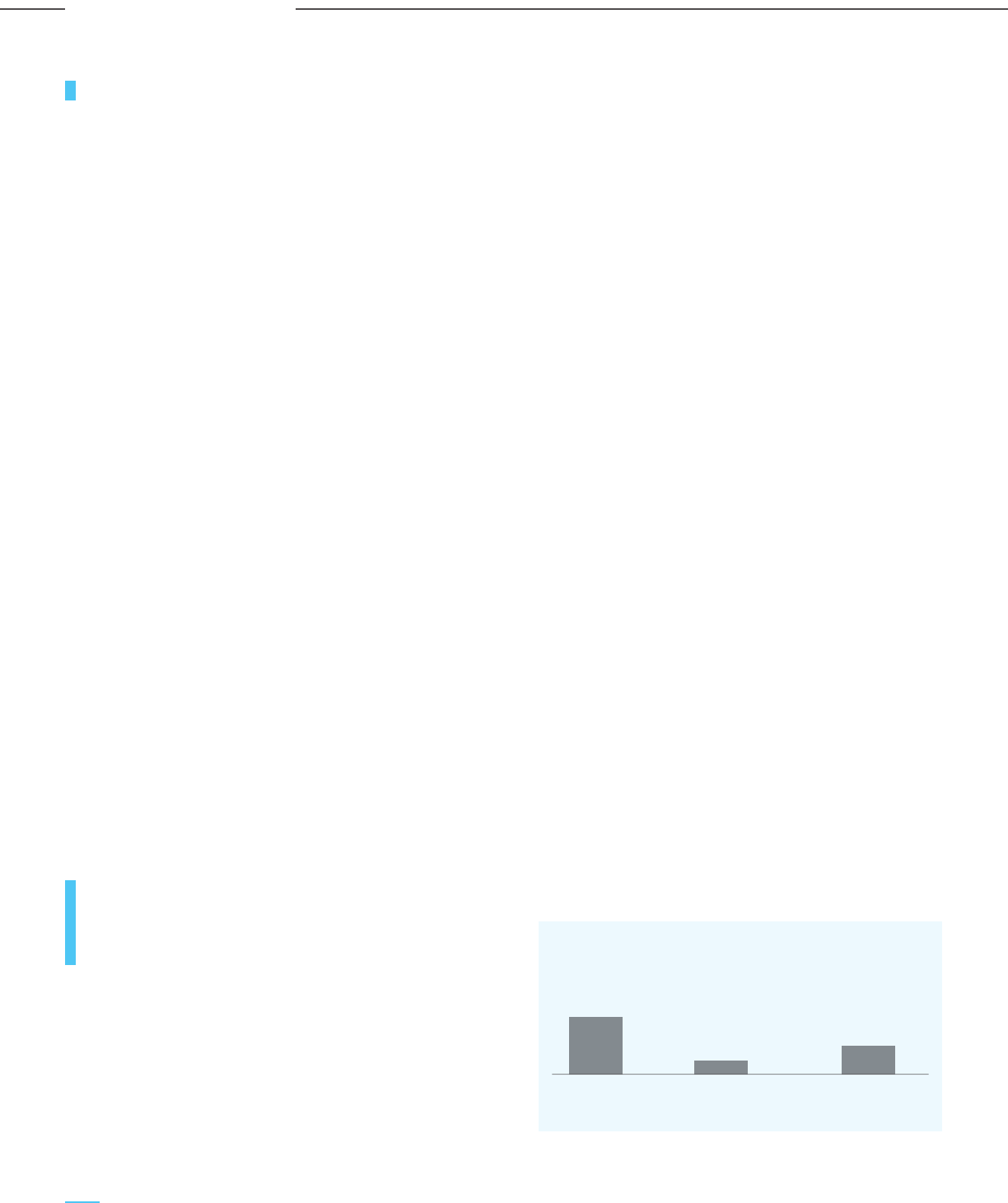

Carbon Capture Costs

Vary Widely Across

Industries/Sectors -

Policy Incentives Need to

be Appropriately Calibrated

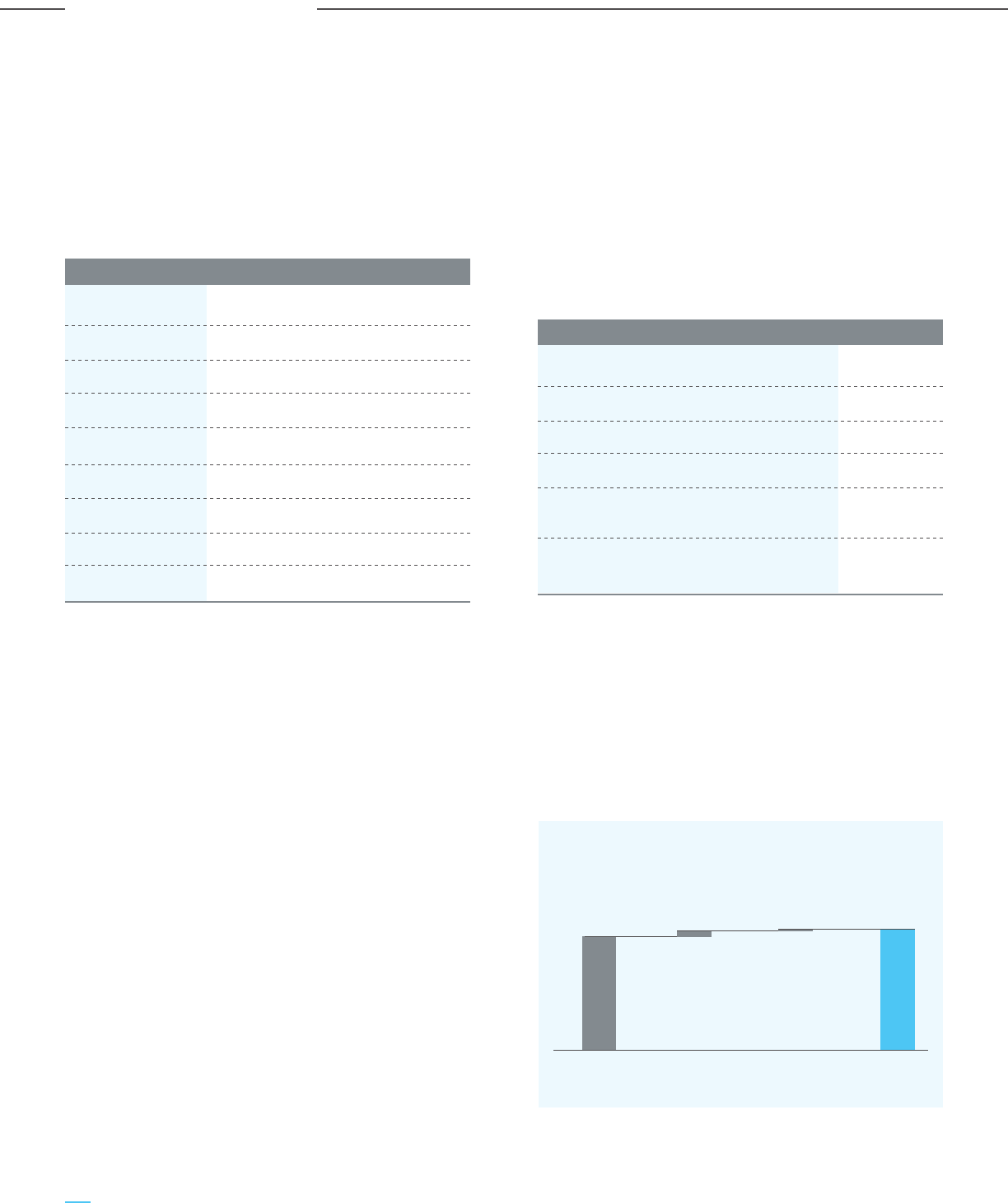

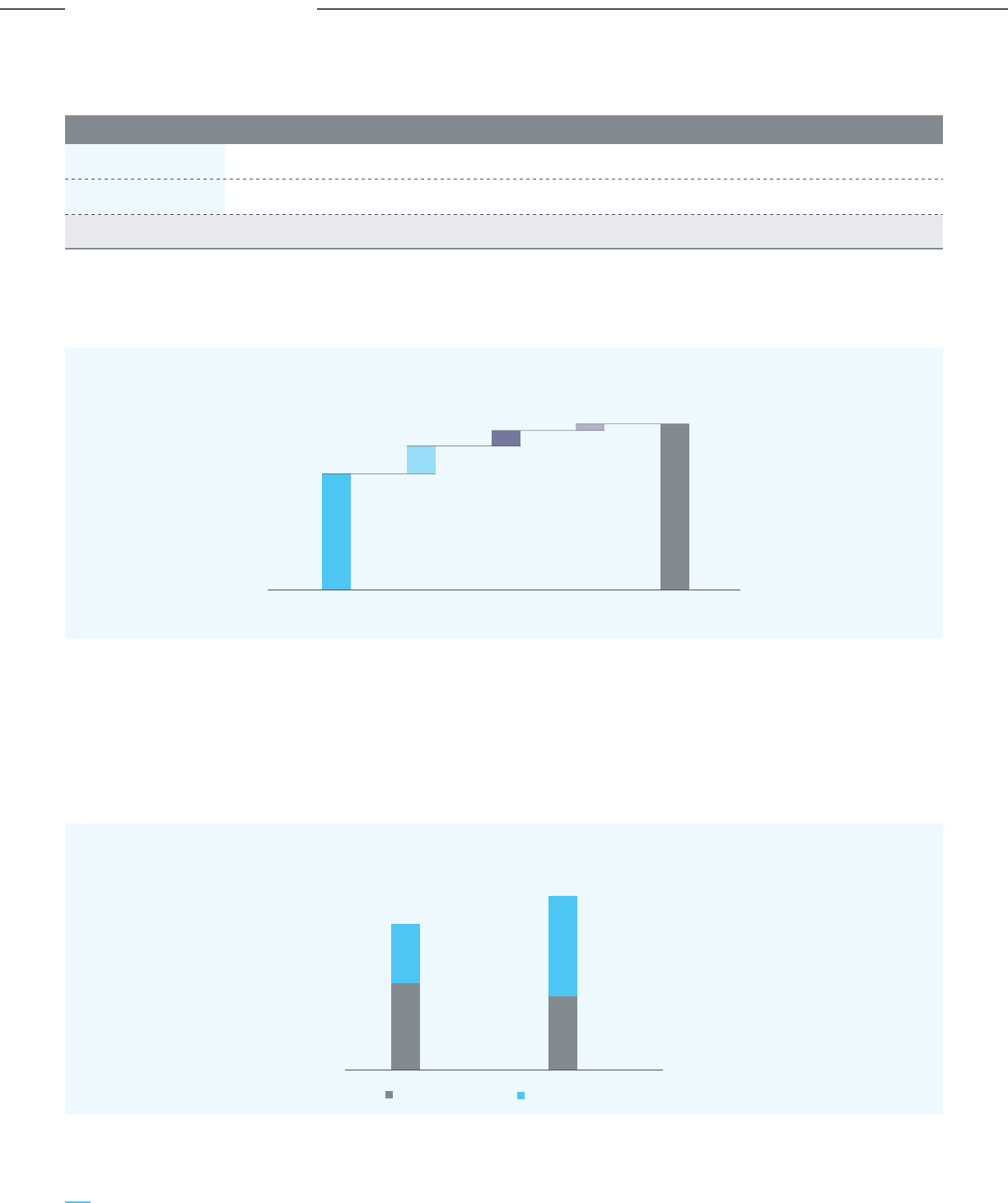

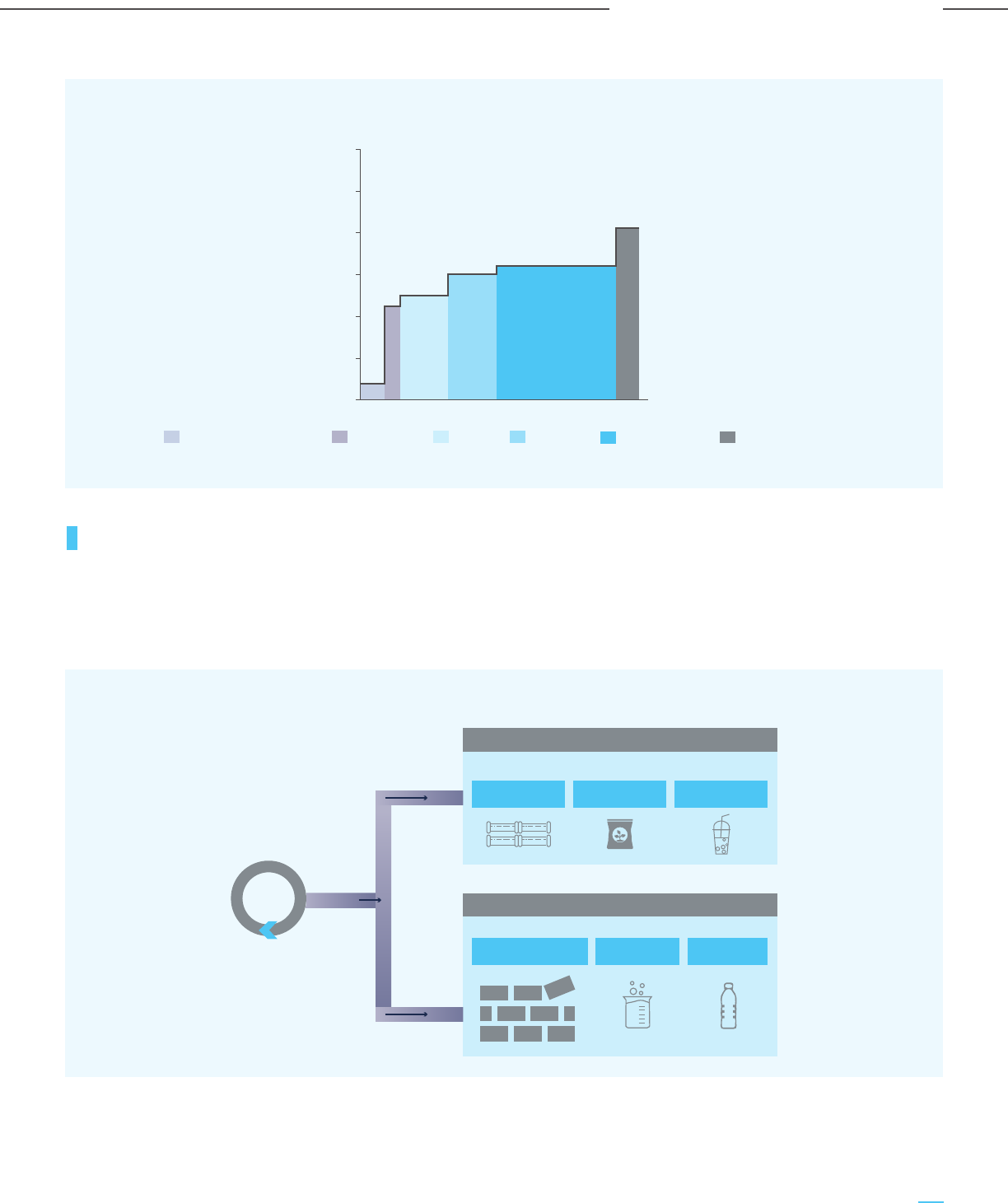

Carbon capture costs (both capital cost and cash

cost) vary widely across industries and sectors, and

depend on CO

2

source characteristics (mainly

pressure & CO

2

concentration), capture technology,

power & steam sourcing costs. The estimated CO

2

capture cost curve for demo scale carbon capture

projects in each sector is provided below,

considering a reference plant size for each sector

and CO

2

delivery and disposition at 100 bar (a).

CO

2

capture cost is the lowest for the gasification

process, as carbon capture is already integrated

within the process. So, the additional cost is only

around Rs. 400/tonneCO

2

, required for polishing and

compression of the CO

2

stream. The capture costs

for other production processes like SMR-based H

2

production, iron & steel, cement, etc. include the

costs for gas processing, carbon capture, and

compression and are hence higher.

Carbon capture costs are amongst the highest for

coal-based power plants, due to the low

Figure E-3: Cost Curve for CO

2

Capture

Across Industries/Sectors

1000

0

400

4100

0 1 2 3 4 5 6 7 8 9 10 11 12

mtpa

2000

3000

4000

5000

6000

Gasification based product

Cement

Iron & Steel

Coal based power

Refinery & Chemical

SMR based H

2

Note: The CO

2

capture costs depicted above include costs for

capture, conditioning and compression to 100 bar (a) and the

amortized capital costs

Converting Captured CO

2

to

Value Added Products -

Opportunity to Profitably

Abate CO

2

Emissions

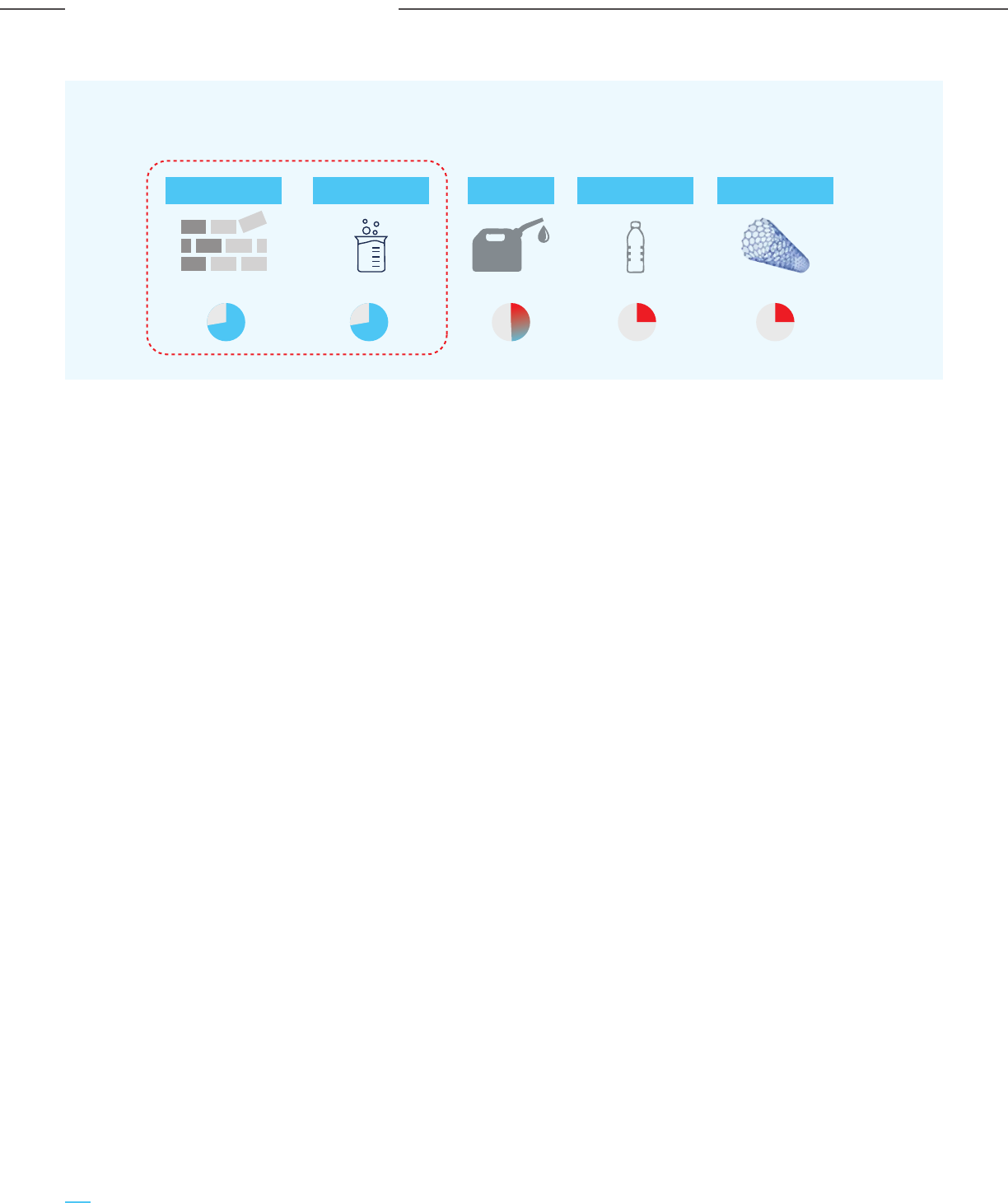

Carbon utilization technologies can provide a wide

variety of opportunities to convert the captured CO

2

to value-added products with a ready market in

India, thus contributing to the circular economy. The

most promising utilization pathways are:

a. Green urea: Green urea can be produced from the

captured CO

2

and cost-competitive green

hydrogen, from renewable energy based

electrolysis of water. Green urea can

replace/complement the traditional LNG/NG

based production and import of ammonia and

urea. The total urea consumption in India is over

30 mtpa, and thus green urea provides a

significant opportunity for CO

2

utilization at scale.

b. F&B applications: CO

2

is utilized in F&B

applications such as carbonated drinks, dry ice,

and modified atmosphere packing; however, the

scales are much lower compared to green urea.

c. Building materials (concrete and aggregates):

There is a large market for aggregates and

concrete in a developing country like India,

providing a pathway for utilizing CO

2

for producing

building materials through concrete curing and

aggregate formation. In these applications

,

CO

2

is

injected in a liquid state without any conversion,

thus reducing the energy requirements.

Additionally, large quantities of wastes such as

steelmaking slag are available as sources of

CaO/MgO, which can be utilized to produce

synthetic aggregates.

d. Chemicals (methanol and ethanol): Conversion

of CO

2

to methanol and ethanol from CO

2

is

proven at a commercial scale in different parts of

the world.

concentration of CO

2

in the power plant flue gas

stream. However, given the share of the power

sector in overall emissions, demo scale CCUS

projects in the power sector are also essential for

CCUS to meaningfully contribute to decarbonization

in India.

19

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

Methanol and ethanol both have important fuel

substitution applications; additionally, methanol is

an intermediate for the production of value-added

chemicals like acetic acid, MTBE, DME, and

formaldehyde, all of which have multiple

downstream applications and offer significant

import substitution opportunities. The conversion

of CO

2

to chemicals thus provides a large-scale

CO

2

utilization and disposition pathway, given the

scale and potential of the downstream chemicals,

and can also help in reducing India’s import bill,

thus laying the foundation for an

economy.

e. Polymers (including bio-plastics): Conversion of

CO

2

to various polymers has been attempted

globally at different scales, and presents another

possible CO

2

utilization route. These polymers

have multiple applications, such as laptop

packaging, cell phone casings, furniture etc. and

provide an interesting futuristic optionality for

CO

2

utilization and conversion.

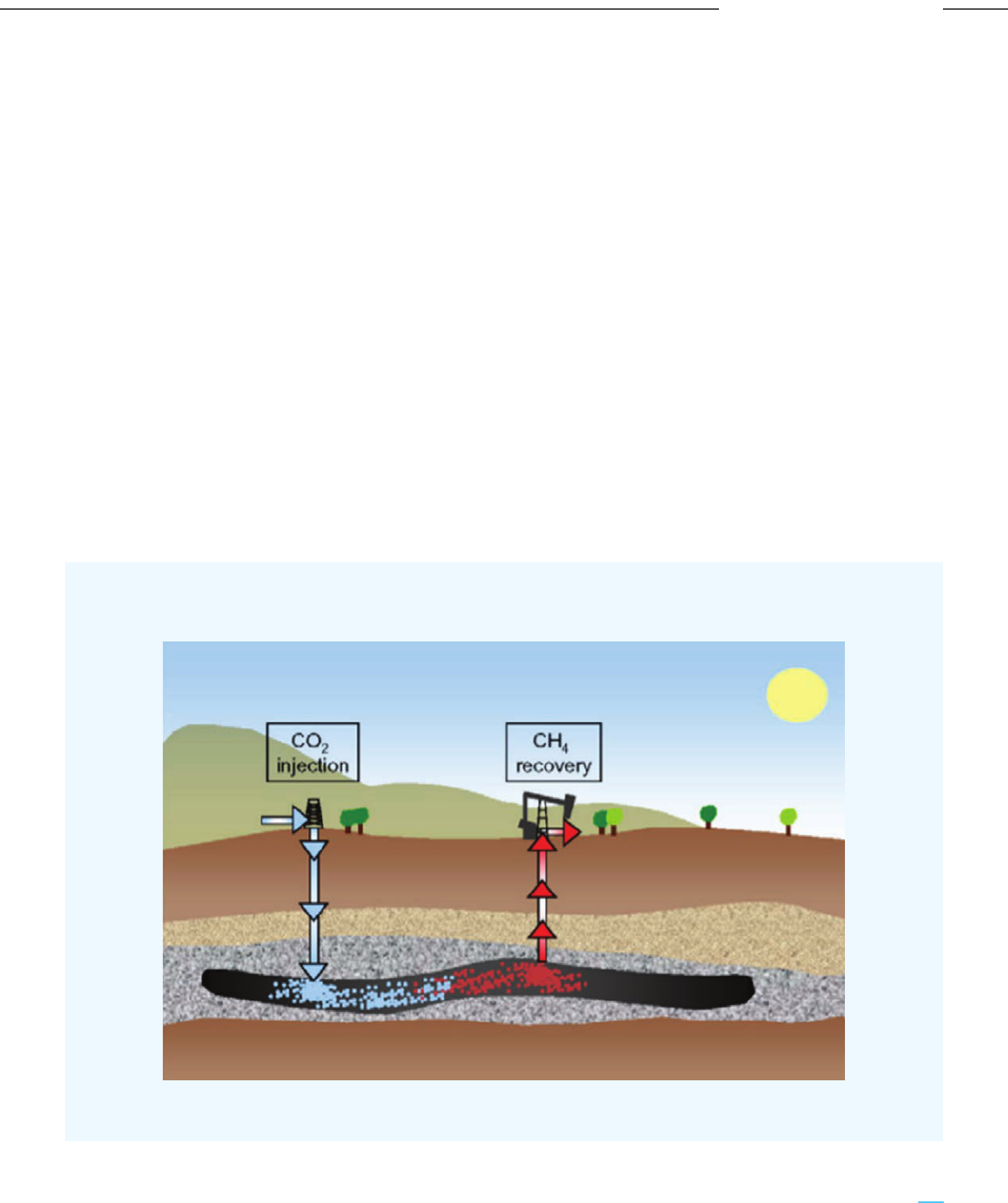

f. Enhanced Oil Recovery (EOR): CO

2

based EOR

has been successfully operating for decades for

producing low-carbon oil from maturing oil fields

in North America and other geographies. For

carbon capture projects in India with proximity to

oil fields, CO

2

EOR can play a role in residual oil

extraction that is environmentally sustainable and

economically feasible.

The technology, scale and economics for commercial

deployment are important determinants of how

existing carbon utilization technologies as well as

new technologies develop in India and compete in

markets. Policy support for carbon utilization and

conversion technologies through offtakes, PLI, price

support and R&D incentives will be necessary for

carbon utilization markets to develop.

However, one needs to be cognizant of the fact that

even with developed carbon utilization technologies,

the impact of carbon conversion technologies on

carbon abatement through carbon capture and

utilization will be modest. The sheer scale of CO

2

emission abatement requires that sequestration be

an essential complement to carbon utilization

technologies in the CCUS value chain.

Promoting Innovation,

Development, Transfer and

Adoption of CCUS

Technologies is Key to Rapid

Decarbonization in India

Government support and incentivization are needed

to promote the adoption and development of CCUS

technologies at a commercial scale in India.

A multi-pronged approach is recommended:

a. Technology transfer: Technologies for carbon

capture, CO

2

sequestration and EOR have been

demonstrated at a commercial scale for almost 50

years in many parts of the world and particularly

the US. While the development of indigenous

technologies is certainly desirable, the immediate

focus should be on the transfer, assimilation and

adoption of proven TRL 8 and 9 technologies in

the CCUS domain. The Government of India may

fund CCUS demonstration projects in sectors such

as coal-based power, steel, cement, refining &

petrochemicals based on commercially proven

technologies, thus reducing the technology risks,

operational risks and costs for CCUS projects in

India and avoiding the reinvention of the wheel.

Engagement with technology suppliers is also

important to ensure the transfer and

indigenization of technology and Intellectual

Property (IP). Policy support for the transfer of

technology and indigenization will not only

support the manufacturing of CCUS equipment for

India at a low cost, but also create export

opportunities.

b. Promoting R&D in novel CO

2

utilization

technologies: CO

2

utilization technologies are

relatively less developed, compared to capture

technologies. Technologies which have great

potential for India, such as CO

2

to methanol and

CO2 to aggregates, are at TRL levels of 4-5 and

6-7 only, respectively. Other propositions such as

CO

2

to synthetic fuels, polymers and novel

materials like carbon nanotubes are even further

behind on the development curve.

20

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

The Government of India should promote an

ecosystem to foster R&D and innovation in CO

2

utilization technologies and new products &

applications based on CO

2

utilization. Similarly, in

the area of capture technologies, the

Government’s policy incentives should encourage

R&D in DAC as a possible future option. The

developments are multi-faceted and given the

difficulty in predicting the innovation and

development trajectory, there is a need to fund,

foster and incubate innovation-based ecosystems

through national centres of excellence such as the

National Centre of Excellence in Carbon Capture

and Utilization at IIT Bombay.

c. Private sector participation: Private sector

participation is essential to promote the transfer

and commercialization of existing CCUS

technologies and also push the envelope for the

development of new and emerging technologies,

particularly CO

2

utilization technologies.

Public/government funding and favourable

policies are required to incentivize & de-risk CCUS

projects, promote private sector participation and

enable viable CCUS business models and value

chains to emerge. Similar to the US DOE and UK

Infrastructure Bank’s support for the development

of novel technologies and projects in CCUS, India

also needs government institutional frameworks

and grants to strategically support new and

emerging CCUS technologies, as well as CCUS

projects across the full project/funding cycle.

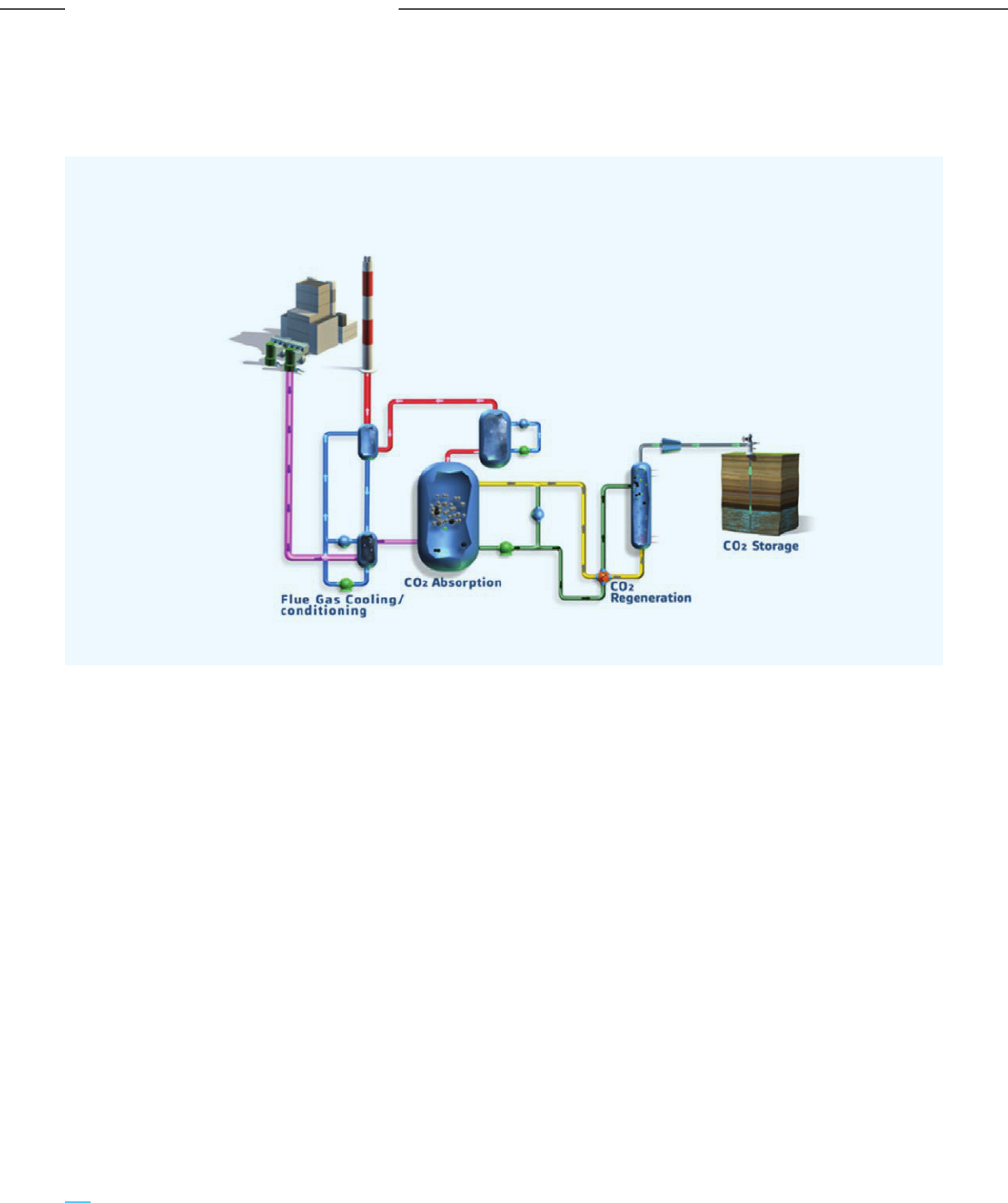

Geological Storage is Critical

for CO

2

Disposition at Scale

For effective CCUS adoption at scale, apart from the

conversion of CO

2

to useful value-added products, there

needs to be a clear strategy and pathway for the

disposition of the captured CO

2

through permanent

geological storage. Save any miraculous technological

innovation at the commercial scale for carbon

abatement technologies, the only commercial

large-scale (giga tonne scale) CO

2

disposition option is

geological sequestration.

The options for the geological storage of CO

2

include

EOR (Enhanced Oil Recovery), ECBMR (Enhanced Coal

Bed Methane Recovery) and permanent storage options

like saline aquifers and basalt storage. However, the

geological data on the pore space availability in India for

the storage of CO

2

is limited, especially for saline

aquifers and basaltic storage. In the case of EOR and

ECBMR, the data availability is better given the prior

exploration activities for facilitating hydrocarbon (both

oil & gas and coal) extraction.

Theoretical assessments and estimates by the British

Geological Society and IIT Bombay indicate a large

potential for CO

2

storage in India, to the tune of 400 –

600 Gt.

However, to make the geological storage of CO

2

a

reality, further work needs to be supported by the

Government of India, especially in the areas of

source-sink mapping, pore space mapping,

geological characterization of the most promising

CO

2

storage regions & basins and developing the CO

2

storage infrastructure through characterization,

validation and development of commercial scale (at

least 1 mtpa) CO

2

injection programmes in the

selected sites. Similar programmes have been

funded in the US by the US DOE in the form of a

network of seven Regional Carbon Sequestration

Partnerships (RCSPs), to develop the regional

infrastructure for carbon capture and storage

across seven identified regions of the US.

A review of carbon capture projects around the world

reveals that a policy framework and Government

support for CCUS are key to managing project costs &

risks, incentivizing the private sector and establishing

the CCUS value chain comprising CO

2

capture,

transportation and storage.

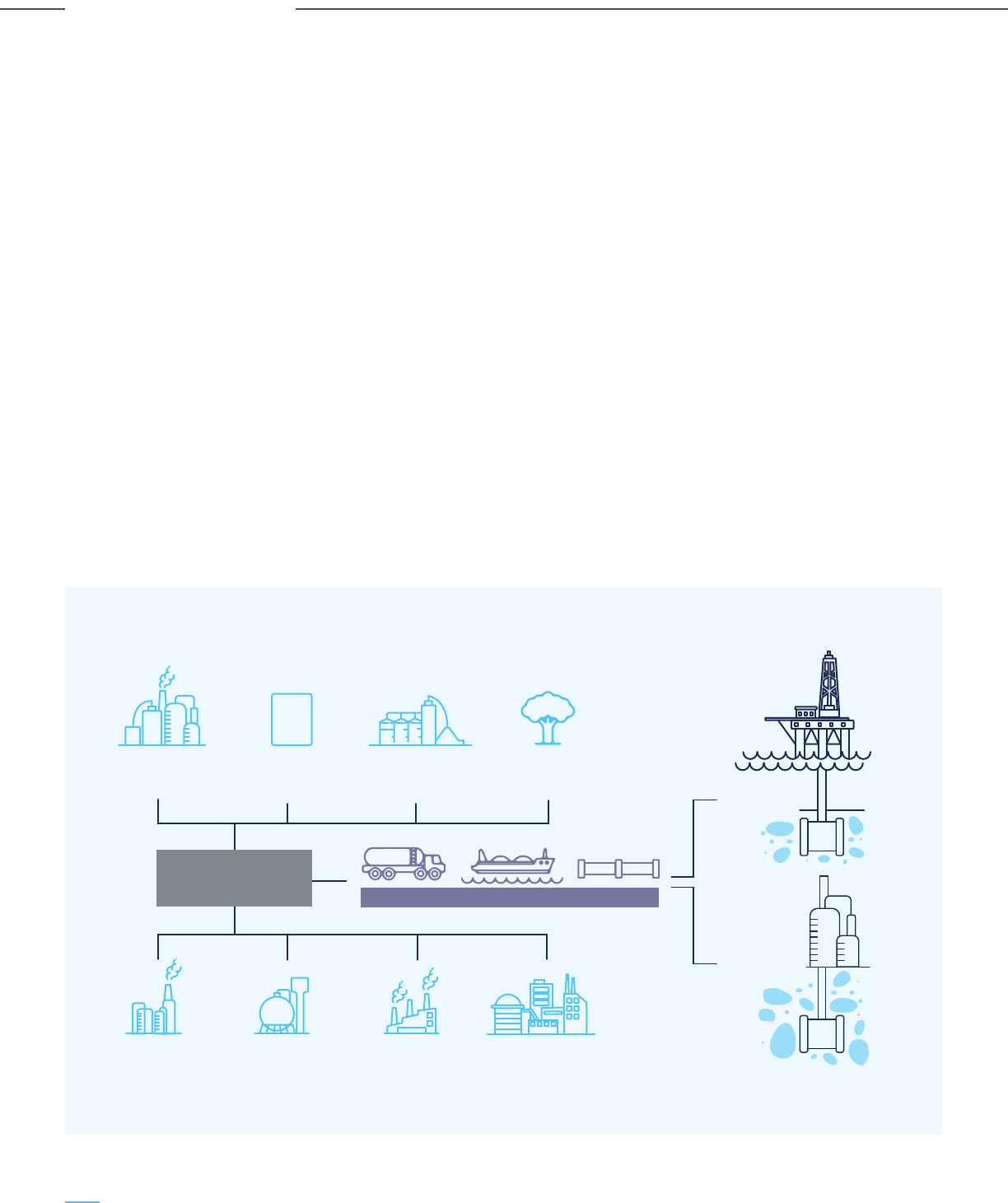

Supportive Incentive Based

Policy Framework is Key to

CCUS Adoption in India

Table E-1: Estimated CO

2

Storage Capacity in India

3.4 Gt

Total

EOR

ECBMR

Saline

acquifers

Basaltic

formations

Well established in North

America; oil recovery possible

to the extent of 30-60%

3.5 - 3.7 Gt

CO

2

injected in unmineable coal

seams; further R&D required

before commercial deployment

291 Gt

No economic benefit - but

potential of large scale CO

2

storage

97 - 315 Gt

More recent developments

vis-à-vis saline aquifers

400 - 600 Gt

21

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

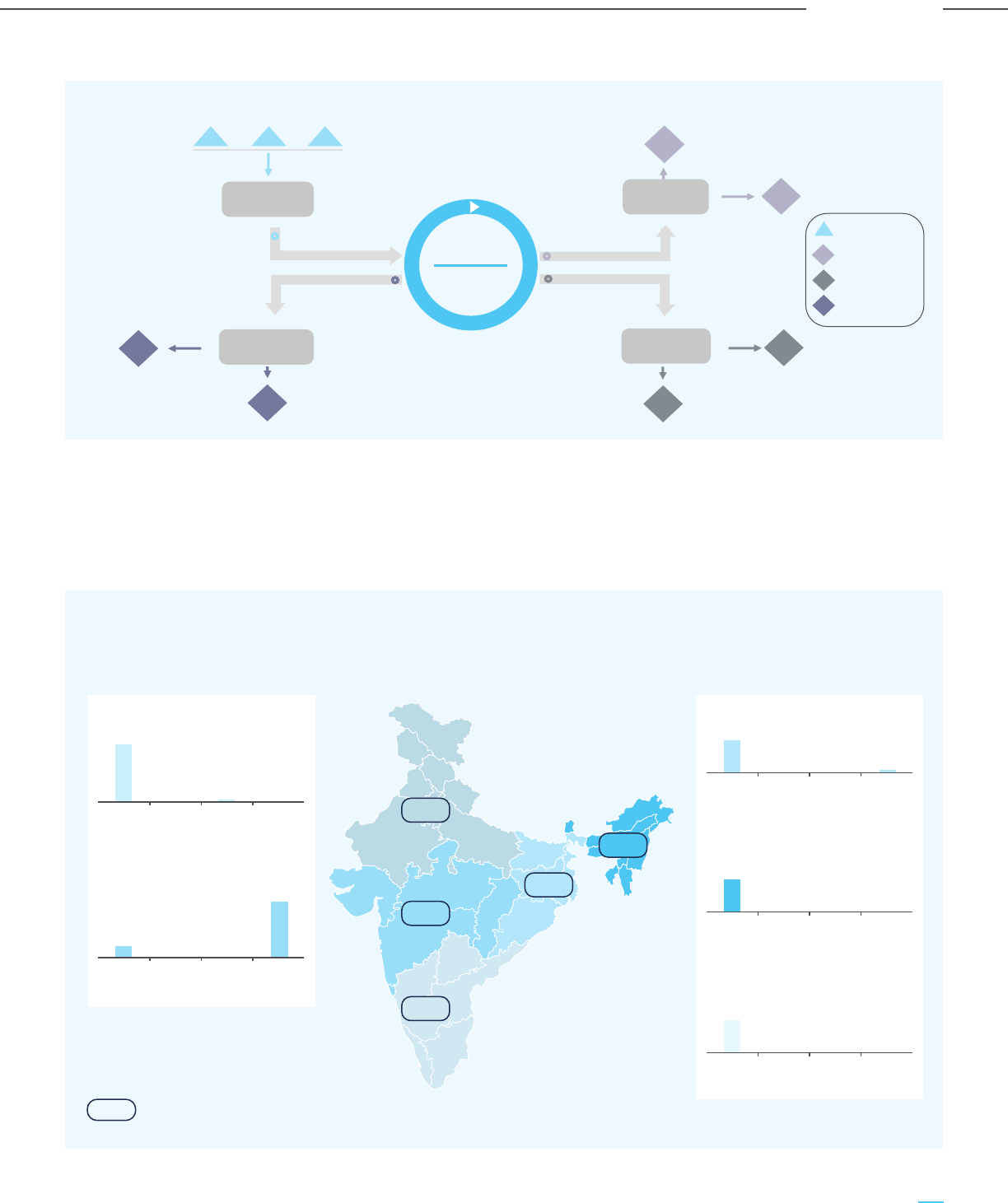

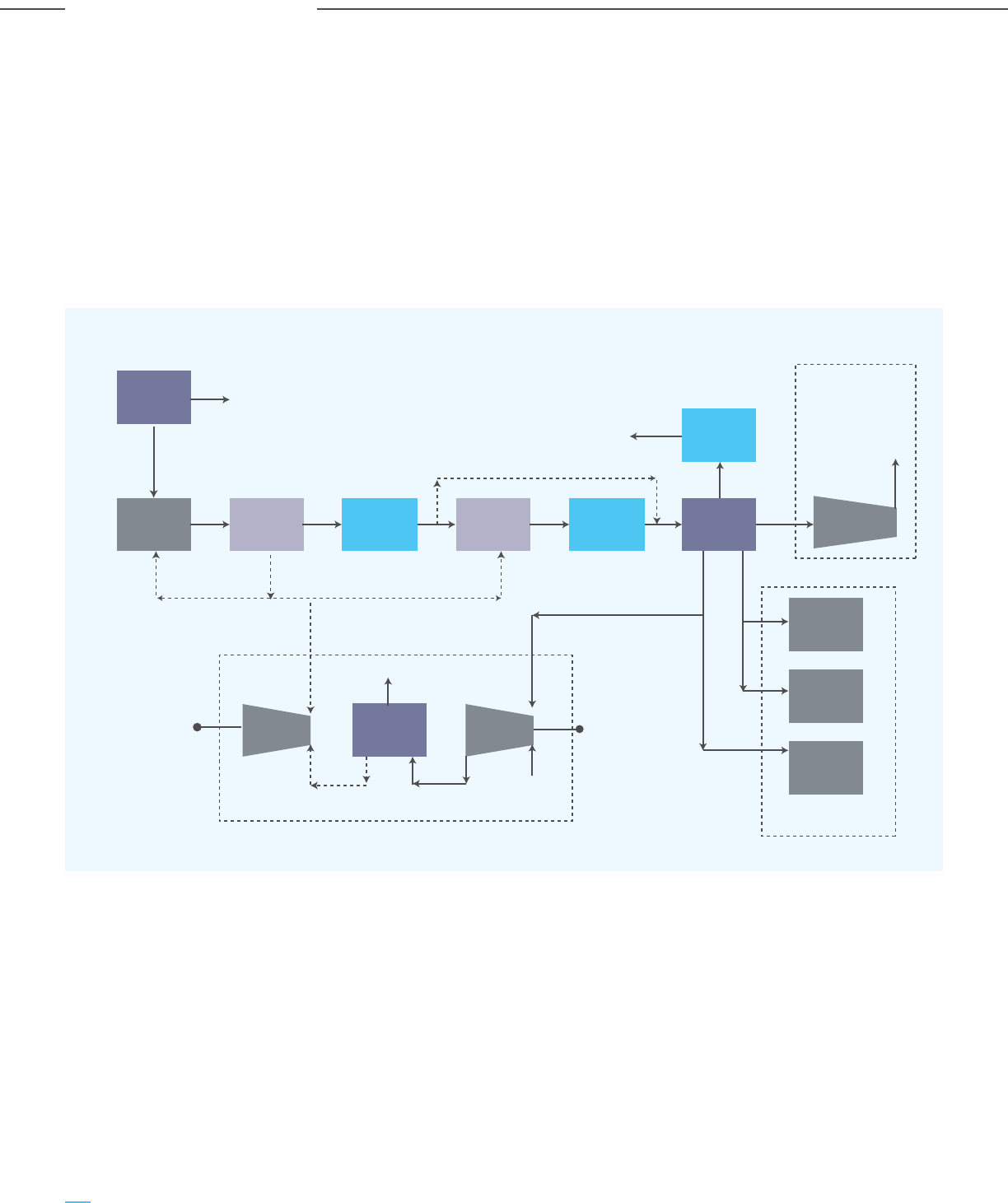

Hub and Cluster Model Critical to Drive CCUS Economics and

Implementation at Scale

Given the cost and risks associated with CCUS projects,

CCUS clusters are necessary to drive CO

2

capture,

transport and disposition at scale and create a

meaningful decarbonization impact. CCUS clusters

incentivize emission-intensive co-located facilities (both

industrial facilities and power plants) to form a capture

cluster and connect to large-scale CO

2

storage sites

using oversized shared transport infrastructure (which

can be shared by multiple emitters), as well as options

for utilization of CO

2

to produce low carbon

downstream products. The anchor project would be

large CO

2

emitters, viz. a thermal power plant or a large

industrial facility, which can cover the initial

infrastructure costs, thereby reducing the cost for new

joiners to the cluster. Similarly, CO

2

disposition clusters

can be spread across multiple but reasonably closely

located geological sequestration sites, oil fields for

enhanced oil recovery (EOR) or CO

2

utilization projects.

A carbon credits-based policy is most suited for a

developing country like India, to incentivize CCUS

adoption and bring down the cost of carbon capture,

establish markets for low-carbon products and

decarbonize India’s large and relatively young

industrial asset base by offsetting carbon capture

costs. The key elements for the recommended CCUS

policy framework for India are:

a. Policy path: CCUS policy in India should be

carbon credits or incentives based, to seed and

promote the CCUS sector in India through tax and

cash credits and provide early stage financing and

funding mechanisms for CCUS projects

b. Hub & cluster business model: The policy

framework should promote the creation of

regional hub & cluster models to drive economies

of scale across the CCUS value chain, with defined

roles for emitters, aggregators, hub operators,

disposers and conversion agents.

c. Low carbon products: Low carbon or

carbon-abated products need to be supported

through preferential procurement in Government

tenders and Production Linked Incentive (PLI)

schemes.

Emitters and storage sites can connect through

storage and transportation hubs, similar to natural

gas hubs for the collection and distribution of natural

gas across different producers and consumers.

The services provided by such hubs would include the

compression and transportation of CO

2

, and

substantially lower the cost of transportation

infrastructure between emitters and CO

2

injection points.

Because of the high mobilization and laying expenses,

the economics of CCUS cluster projects in the initial

years is quite challenging due to lower CO

2

volumes

and the outsized infrastructure created. This can be

overcome through long-term and low-cost financing

through Government support and access to

international clean funds.

d. Environmental and social justice: CCUS policy

should protect communities most affected by

environmental and climate change by ensuring

the distribution of the economic value created by

CCUS and the protection of jobs in traditional

sectors (viz. coal mining etc.) affected by

migration to clean energy systems.

e. Accounting and regulatory framework: To

incentivize carbon capture in different sectors,

there is a need to establish a baseline of regulated

emission levels and allowances for different

sectors, and also adopt a Life Cycle Analysis (LCA)

framework that looks beyond just the direct Scope

1 emissions and takes into account Scope 2 and

Scope 3 emissions and ensures effective carbon

abatement.

f. Risk mitigation: For CCUS policy to be effective

in India and encourage wider and private sector

participation, there is a need to de-risk CCUS

projects by limiting the liability and ownership of

CO

2

across the CCUS value chain and monitoring

risk through appropriate Monitoring, Verification

and Accounting (MVA) frameworks.

22

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

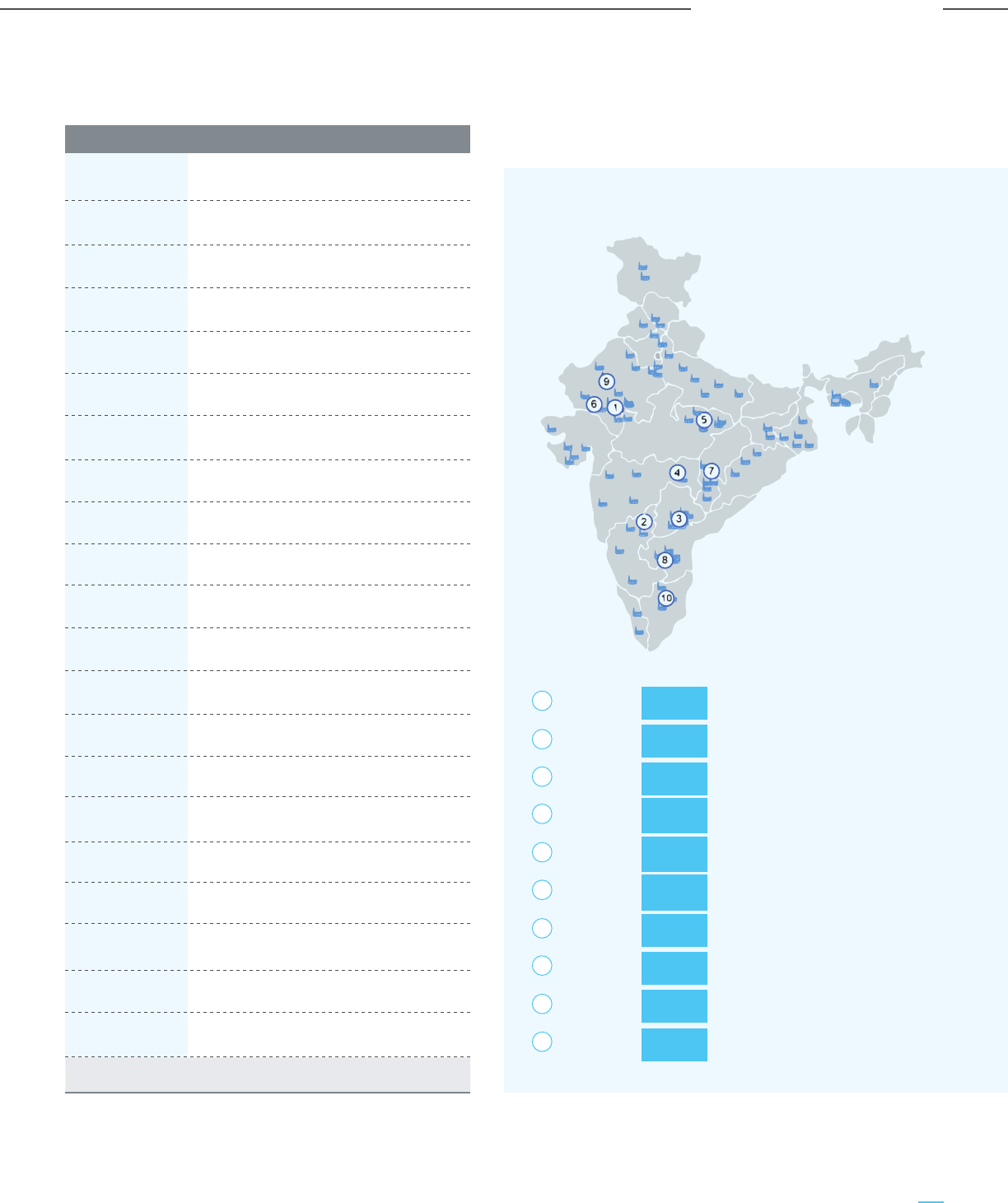

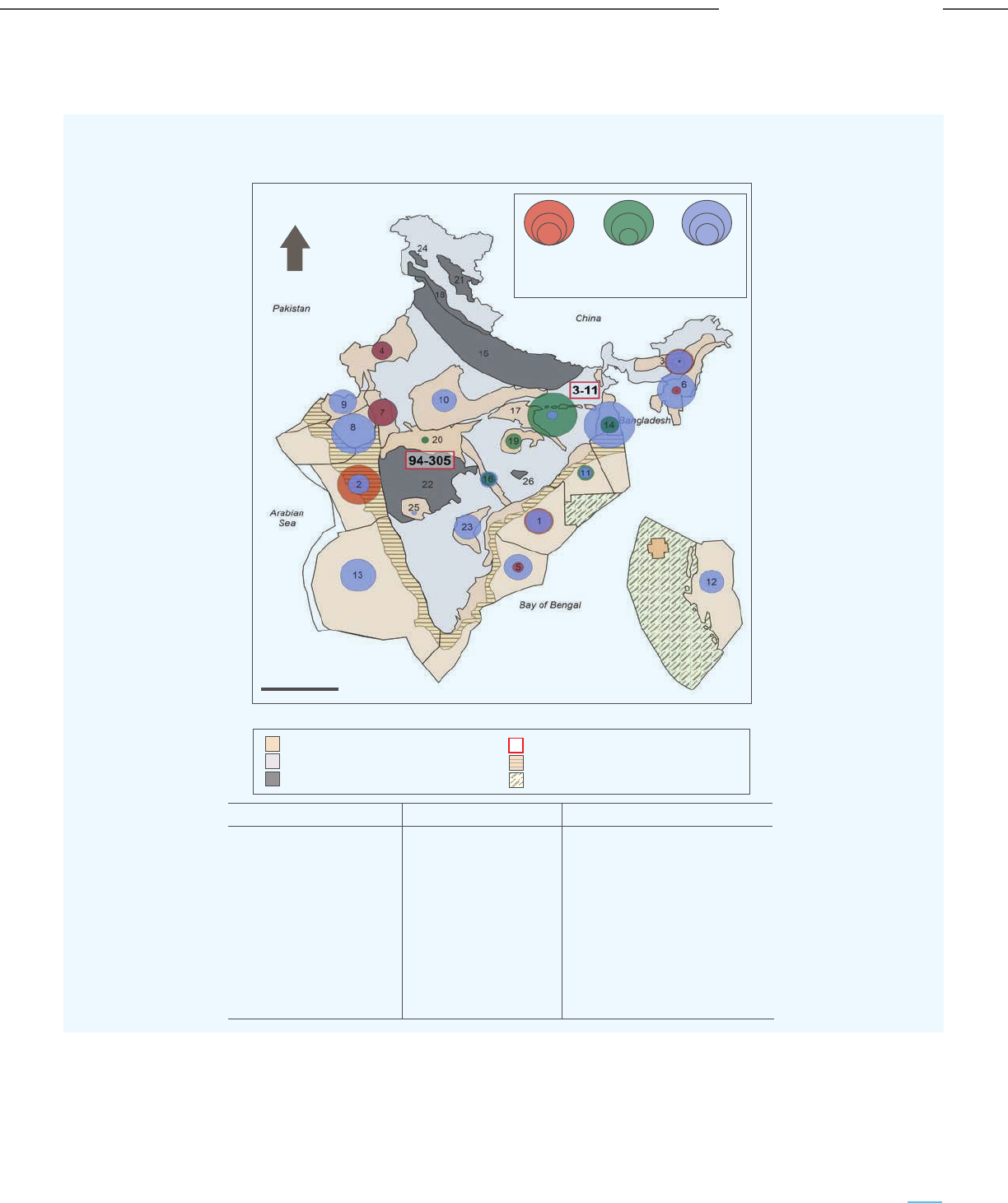

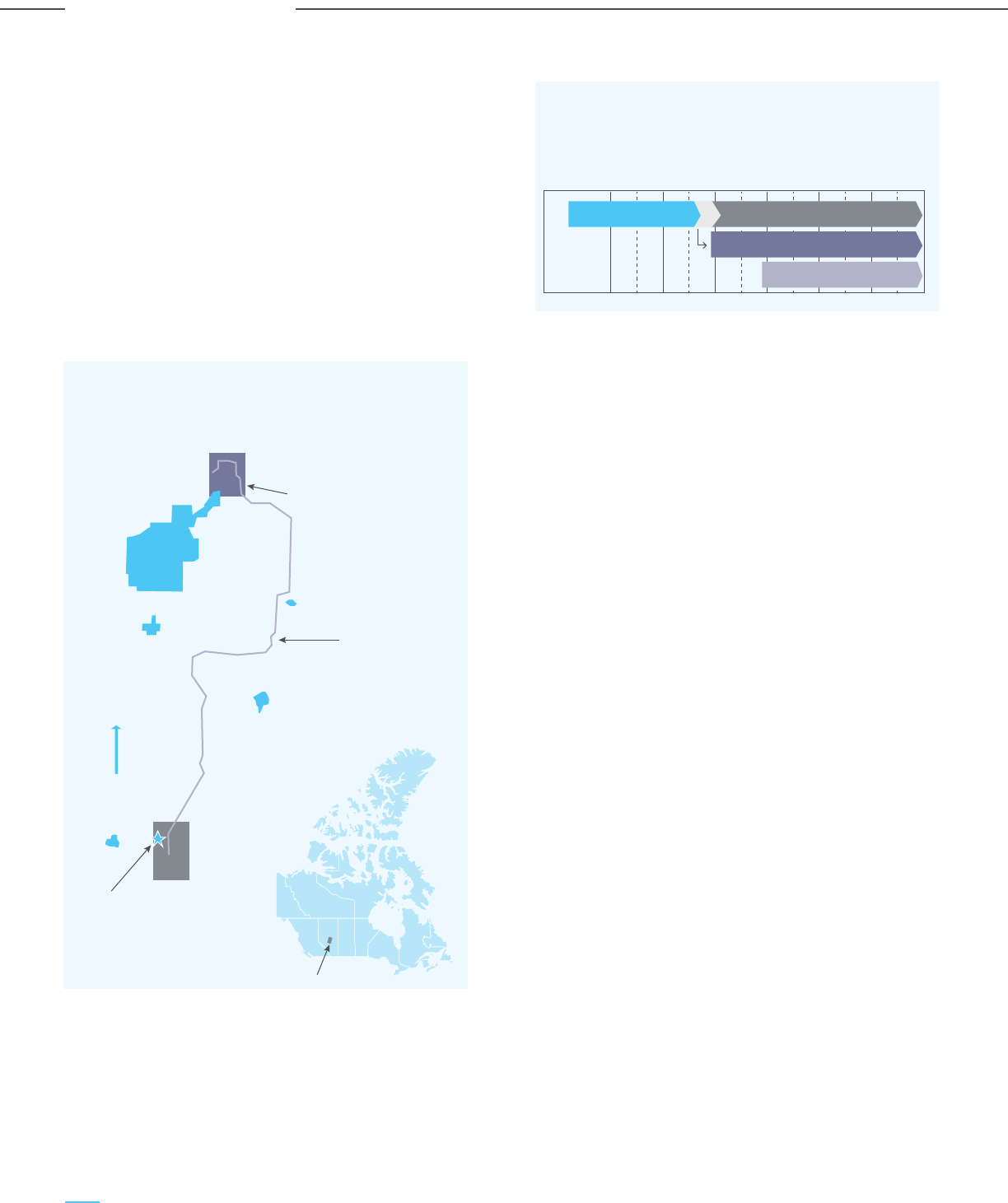

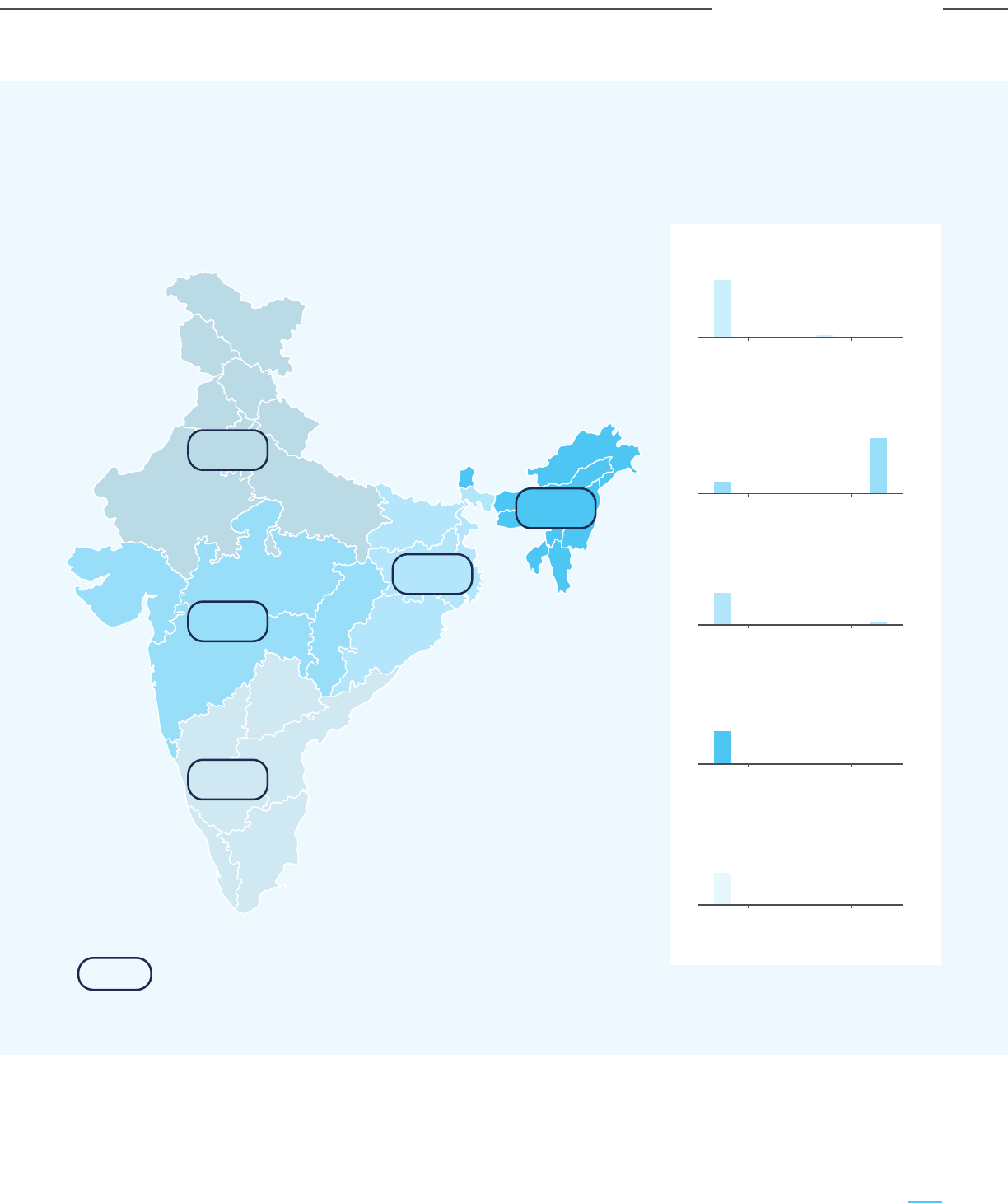

Preliminary analysis shows that there is sufficient

potential for creating regional CCUS clusters in each of

five regions of India (North, South, East, West, and

North-East) and sequestration in deep saline aquifers

has the best potential in all the regions. However, due

to the lack of data on the northern sedimentary basins,

the theoretical storage capacity for the saline aquifers

is low. But as more exploratory activities focused on

CO

2

storage are undertaken, the storage potential in

the northern region is likely to increase.

Figure E-4: Mega Scale CO

2

Cluster Model

Aggregator

E

11

Disposer

EOR Cluster

EOR

HUB

Conversion

Cluster

MeOH

EOR

Regulated Monopoly

Regulated Monopoly

Regulated Monopoly

Demand-Supply

Time Contracts

Regulated Monopoly

E

Emitters

S

Sequestration

Conv

Conversion

EOR

Enhanced Oil

Recovery

S

1

S

2

Mineral

E

12

E

13

Figure E-5: Region-wise Storage Clusters in India

Total Theoretical Storage Capacity of India = 395 - 614 Gt CO

2

7.21 GT

16.58 GT

10.13 GT

0.22 GT

9.01 GT

Region-wise estimated CO

2

emission volumes (2030-2050)

Northem Region: 7.65 Gt CO

2

Saline

aquifer

ECBMR EOR Basalt

7.34

0 0

0.31

Western Region: 388.9 Gt CO

2

Saline

aquifer

ECBMR EOR Basalt

304.9

0.9

80.8

2.3

Southern Region: 76.3 Gt CO

2

Saline

aquifer

ECBMR EOR Basalt

75.2

0.3 00.8

North-Eastern Region: 47.2 Gt CO

2

Saline

aquifer

ECBMR EOR Basalt

46.5

0 00.7

Eastern Region: 47.2 Gt CO

2

Saline

aquifer

ECBMR EOR Basalt

67.2

2.4 10.980

23

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

Carbon Capture Finance Corporation of India –

Institutional Mechanism to Support CCUS Project

Funding, Capital and Cash Costs

Financing CCUS projects can be quite challenging in

a developing country like India, even with incentive

and credits-based policy support. For CCUS to take

off in India, it is important to fund and support initial

demonstration scale CCUS projects. The typical

capital cost and cash costs for CCUS projects in

different sectors can be quite different, depending

on the source and quality of the gas stream and the

extent of CO

2

capture targeted, as shown below.

While the funding for the initial demonstration

projects can be achieved through direct Government

grants and funds, for CCUS to reach scale in India, it

is also important to understand the CCUS

investment requirements over a long-term horizon

and establish a financial framework such as a Carbon

Capture Finance Corporation (CCFC) to support

CCUS projects across their lifecycle. This is

important as CCUS provides an unmatched

opportunity for turbocharging the growth of the

Indian economy by creating a clean-energy based

industrial sector, potentially leading to the

development of new technologies, skills and

high-value employment opportunities in India.

Table E-2: Sector-wise Typical Carbon Capture Capital Charge and Cash Cost

Industry

name

Ref. Plant

capacity

CCU capacity

(mtpa)

Capital Charges

(A), Rs./T

CO

2

Cash Cost

(B), Rs./T

CO

2

Total Capture Cost

(A+B), Rs./T

CO

2

Capital Costs,

Rs. crores

Gasification

based

production

70 ktpa H

2

1 mtpa Rs. 80-100

Crore

90-120 250-300 340-420

NG based

SMR for H

2

production

130 ktpa H

2

0.7 mtpa Rs. 700-800

Crore

900-1,200 1,150-1,400 2,050-2,600

Cement 2.5 mtpa

clinker

2 mtpa Rs. 1,600 to

1800 Crore

800-1,000 1,050-1,600 1,800-2,600

Iron and

Steel

2.0 mtpa

BF-BOF

based ISP

2 mtpa Rs. 1,600-2,000

Crore

1,000-1,300 1,900-2,300 2,900-3,600

Refinery

(CDU & FCC)

5 mtpa crude

processing

1 mtpa Rs. 1,100-1,300

Crore

1,200-1,400 2,700-3,100 3,900-4,500

Coal-based

power

800 MW 5 mtpa Rs. 3,500-4,000

Crore

700-1,000 2,100-2,500 2,800-3,500

Total 11.7 mtpa Rs. 8,600 –

10,000 Crore

24

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

It is estimated that out of the total emissions

emanating from sectors such as coal-based power,

steel, cement, upstream oil & gas operations,

refineries, chemicals, hydrogen production and

gasification, about 85% will be capturable through

CCUS projects. Based on the trajectory of economic &

industrial development in India and the concomitant

growth in CO

2

emissions, it is expected that the

capturable emissions will reach about 2400 mtpa by

the year 2050, the year by which India has committed

to halving its emissions. For CCUS to make a

meaningful contribution to this lofty and laudable

goal, it is envisaged that CCUS projects should capture

at least 30% of the capturable emissions of 2400

mtpa, i.e. around 750 mtpa. To sufficiently incentivize

CCUS projects at the envisaged scale, the following

subsidies are suggested:

a. Subsidy for CO

2

sequestration/storage:

Rs. 4,100/tonne till 2040 and Rs. 3,000/tonne

till 2050

b. Subsidy for CO

2

EOR: Rs. 3,000/tonne till 2040

and Rs. 2,400/tonne till 2050

c. Subsidy for CO

2

utilization: Rs. 2,300/tonne

till 2050

The above subsidy amounts have been estimated

based on the likely CCUS costs in the Indian context

and the likely trajectory of cost reduction from the

increasing scale of CCUS projects, and also the

revenue streams from CO

2

EOR or the coversion of

CO

2

to value-added products.

The total subsidy amount required by the year 2050 to

support 750 mtpa of CCUS is estimated to be around Rs.

210,000 crores. While this is a very significant amount, it

is a necessary expenditure required to support CCUS

and ensure the sustainability of the Indian economy. It is

proposed that the proposed CCFC be developed as a

financial institution to fund CCUS projects through

equity and debt participation, with the objective of

supporting and realizing the carbon neutrality goal. The

CCFC will be funded by low-cost sovereign or

International Green Funds, Carbon Bonds or Climate

Funds. By investing in CCUS projects, along with the

utilization of a part of the incremental tax revenue

generated, it should be possible to fund the carbon

capture credits, eventually leading to subsidy-neutral

CCUS operations. Two alternate mechanisms are

proposed to fund the CCFC.

a. Option 1: CCUS financing through ‘Clean Energy

Cess’ only

It is assumed that CCUS will be funded by the

Clean Energy Cess’ levied on coal. The ‘Clean

Energy Cess’ on coal @ USD 5.3/tonne (Rs. 400

per tonne) will be re-introduced from 1 April 2026,

as the GST compensation cess has been extended

till 31 March 2026. India’s coal and coke

consumption is expected to increase from the

current 1,050 mtpa to around 1,200 mtpa by 2030

at a 2% CAGR. Accordingly, the annual cess

collection is estimated to be around USD 6-7 BB$

(Rs. 48,000 – 53,000 crores). The surplus funds in

the initial period creates an opportunity for the

corpus to grow significantly through re-financing

through appropriate investment vehicles.

Table E-3: CCUS Funding through Clean Energy Cess

Year Fund. Req.,

Thou. crore

Fund available,

Thou. crore

Surplus/Shortfall,

Thou. crore

2023 - 23 23

2030 15 169 154

2040 89 603 514

2050 210 225 15

25

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

b. Option 2: CCUS financing through bond and gross

budgetary support

The government budget and bonds will finance the

subsidy (cash and tax credits) required for CCUS. It

is estimated that 30.5 BB$ (Rs. 2,29,000 crores) of

bonds with a 9% spread in re-investment return,

along with a maximum of 0.5% of the Government’s

spending or the ‘Gross Budgetary Support (GBS)’

can finance 750 mtpa of CCUS by 2050.

It is proposed that the bonds will be raised from the

low-cost national/international bond market and

invested in green projects in India with an assured

return of 9% spread. While the bonds will be raised

and re-invested in the initial years, projected

utilization has been estimated to limit the

government spending on CCUS to be about 0.5% of

the ‘Gross Budgetary Support’.

Table E-4: CCUS Funding with Bonds and Government Budgetary Support

Year Fund. Req.,

Thou. crore

Bond with Return,

Thou. crore

Gross Budgetary Support (GBS),

Thou. crore

2023 - - -

2030 15 - 15 (0.2% of GBS)

2040 89 36 53 (0.4% of GBS)

2050 210 107 103 (0.5% of GBS)

CCUS projects will require upfront capital

investments of US$ 100-150 billion [2022 dollars] for

750 mtpa of CO

2

capture, utilization, and storage.

These investments will develop the market for CO

2

and the positive impact on the Indian GDP is

estimated as US$ 100 to 150 billion over the next 30

years, based on the envisaged improvement and

indigenization of CCUS technology.

In particular, CCUS-enabled coal gasification projects

will generate clean value-added products like

methanol, ammonia, acetic acid, mono-ethylene

glycol, etc. and reduce their imports significantly.

India imports almost US$ 13 billion per annum of

organic chemicals and it is estimated that the

CCUS will have a Material Positive Impact on GDP, Employment

Growth, Energy and Material Security, and Import Substitution

indigenous production of these coal-based chemicals

can replace US$ 7-10 billion of imports by 2050 and

also contribute to the domestic GDP.

CCUS projects will also lead to significant

employment generation, both during the construction

phase and the operating phase, as well as create

significant indirect employment and shape the future

economic development of nearby areas. It is

estimated that the envisaged CCUS target of 750

mtpa by 2050 can create employment opportunities

of 8-10 million full time equivalent (FTE) years in a

phased manner, thus creating a compelling case for

investment in CCUS projects.

26

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Executive Summary

Chapter 1

Introduction

1.1 Background

India is the 3rd largest emitter of CO

2

in the world

after China and the US, with estimated emissions of

2.6 gigatonne per annum (gtpa) in 2019, which

marginally reduced to 2.45 gtpa in 2020 due to the

impact of the COVID-19 pandemic. India’s per capita

CO

2

emissions are about 1.9 tonnes per annum, which

is less than 40% of the global average and about

one-fourth of that of China. However, with rapid

economic growth, infrastructure and industrial

development, as well as a growing population

(expected to overtake China in the next decade and

cross 1.50 billion by 2036), the total CO

2

emissions is

expected to cross 4 gtpa by the year 2030. The

sectoral break-up of the CO

2

emissions reveals that

while renewable energy is making great strides in

India, it can theoretically contribute at most 30% of

the desired decarbonization by replacing fossil

fuel-based power generation.

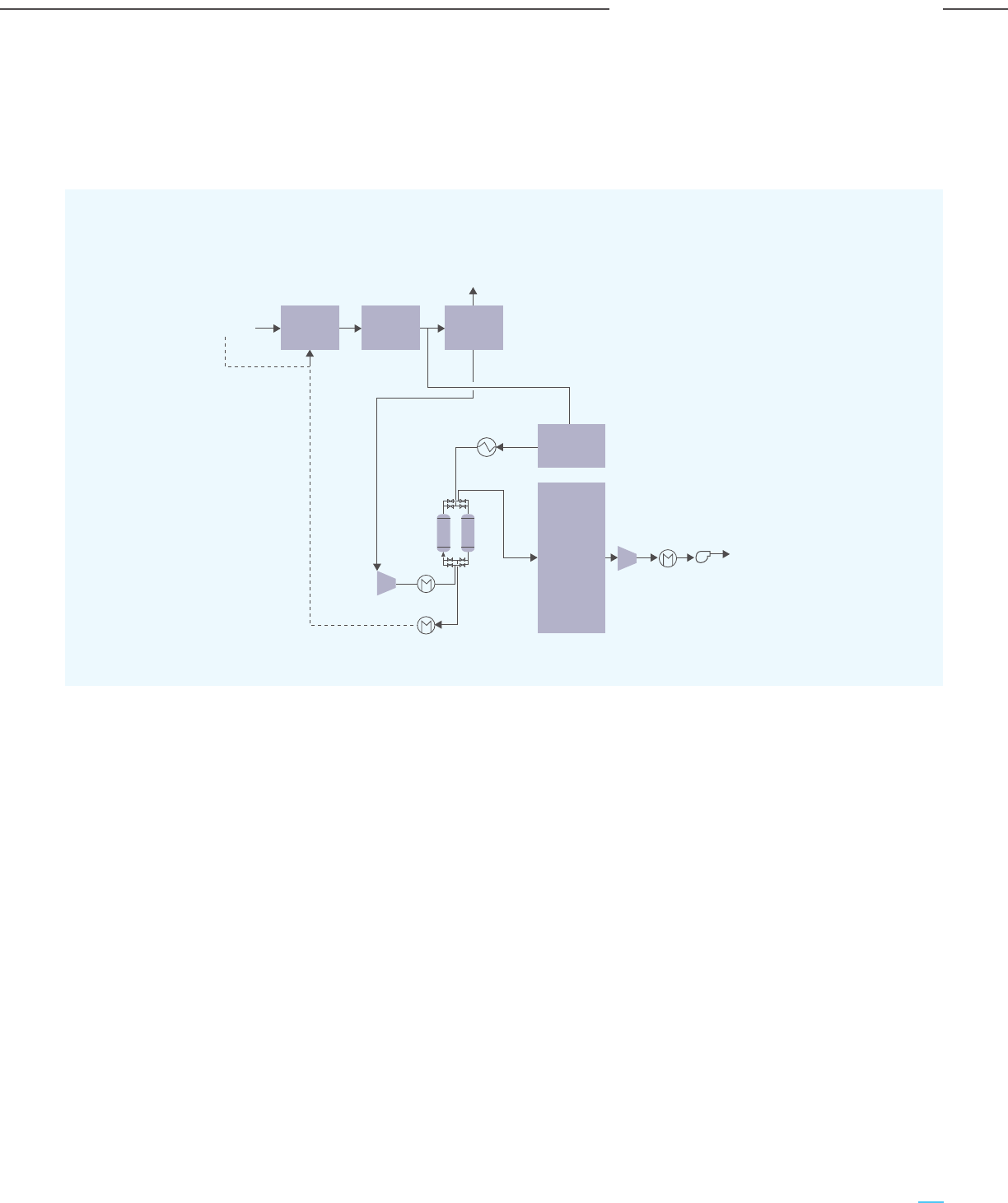

What is CCUS?

The International Energy Agency (IEA) defines Carbon

Capture, Utilization and Storage (CCUS) as a group of

technologies for capturing of CO

2

from large and

stationary CO

2

emitting sources, such as fossil fuel

based power plants and other industries. CCUS also

involves the transport of the captured CO

2

(typically

by pipeline and in certain situations by through

shipping, rail or trucks also) to sites, either for

utilization in different applications or injection into

geological formations or depleted oil & gas fields for

permanent storage and trapping of the CO

2

.

CCUS also includes Direct Air Capture (DAC), which

involves the capture of CO

2

directly from the

atmosphere, although the same is not the focus of this

study, as DAC is still in its early stages and the

economics (present cost of DAC is estimated to range

between US$ 400-800/tonne of CO

2

) and scale of

operations are yet to be established.

Decarbonization Challenge and the Role of CCUS

The decarbonization challenge for India is to identify

scalable and economically sustainable solutions for

the decarbonization of sectors that contribute to 70%

of emissions. CCUS has an important and critical role

to play, especially for India to accomplish net-zero by

2070, as envisioned by the Hon’ble Prime Minister of

India. Though the target date is five decades away, as

the noted author Vaclav Smil has documented in his

work, energy transitions take decades. It is therefore

important to implement the framework and policy

instruments for CCUS to become a reality in India and

make a meaningful contribution to decarbonization

in India.

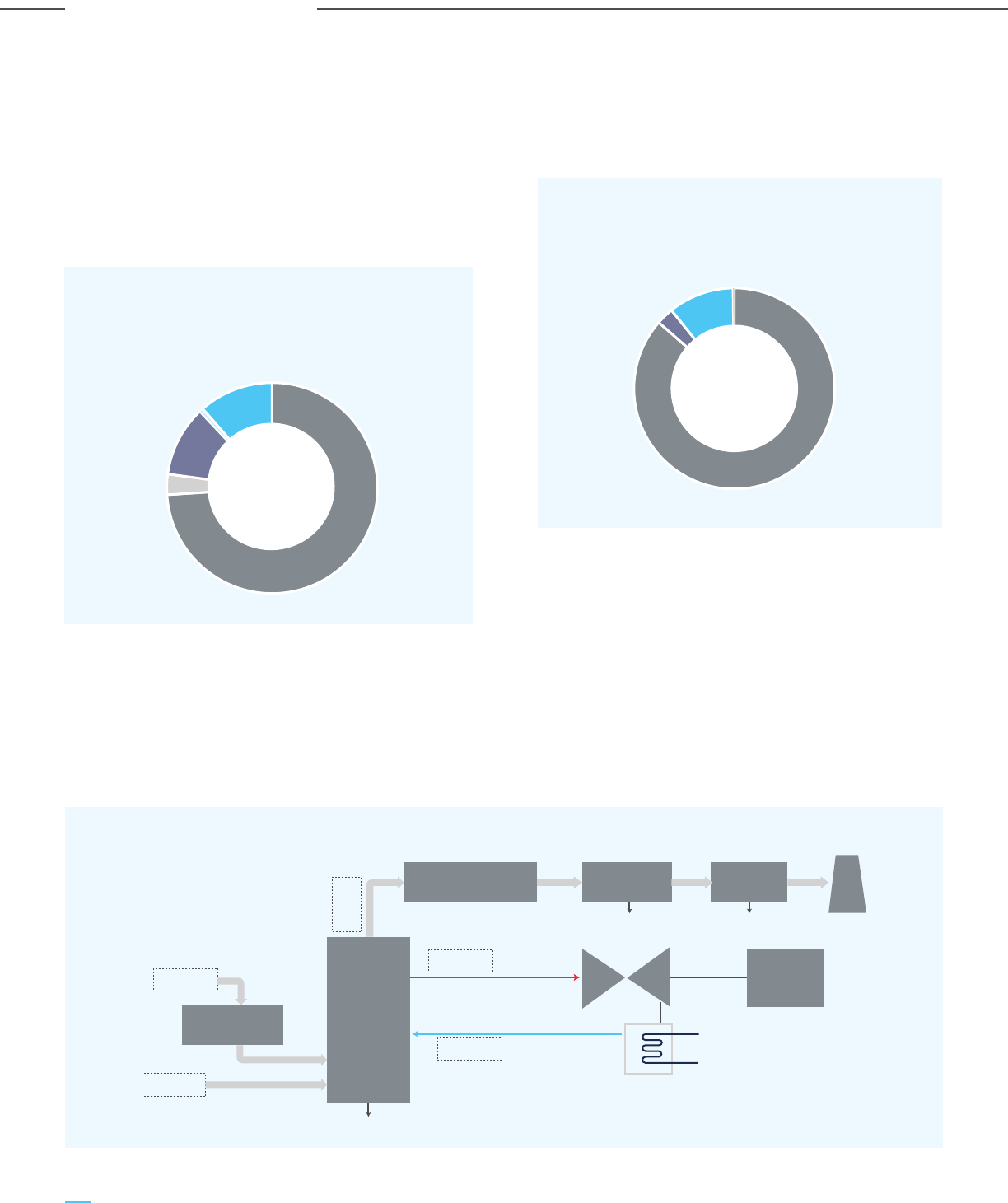

Figure 1.1: The 70% Emissions Challenge

28

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Introduction

Industry

Agriculture

Transport

Building

Electricity

31%

~30%

2.6

gtpa

~70%

20

10

5

India

This study has been prepared by M. N. Dastur & Co. (P)

Ltd. and Dastur Energy Pvt. Ltd., under the tutelage of

the National Institution for Transforming India (NITI

Aayog), Government of India and aims to provide the

policy framework and deployment mechanism for

CCUS at scale to become a reality in India. This study

focuses on CCUS for large point CO

2

emission sources

(with >100 ktpa of CO

2

emissions) such as coal based

power plants and industrial applications. CO

2

emissions from sectors such as agriculture,

transportation and buildings are distributed and

require interventions related to change in fuel (viz.

biofuels), electrification, enhancing thermal &

electrical efficiencies and are outside the purview of

this study.

In particular, industrial applications are hard to

electrify, and industrial CO

2

emissions are hard to

abate due to the use of fossil fuels not only as a

source of energy but also within the process itself.

Carbon Capture Utilization and Storage (CCUS) also

has applications for the power sector, given India’s

present reliance on coal for meeting over 70% of its

electricity needs; even in the future, if India is able to

substantially green the grid power and meet the

target of 500 GW installed capacity of renewables by

2030, there would still be a need to meet the baseload

power demand from fossil fuels (most likely coal) or

other dispatchable sources, given the intermittency

and non-dispatchable nature of solar and wind power.

Thus, CCUS also has a role to play in enabling clean

and green baseload power and ensuring the

sustenance and non-stranding of our over 210 GW of

coal and lignite based thermal power plants.

In their September 2020 report, the International

Energy Agency points out that reaching net-zero

without CCUS is virtually impossible. The

Intergovernmental Panel on Climate Change (IPCC)

also concludes that without CCUS, it would not be

possible to stabilize the CO

2

concentration in the

atmosphere between 450 – 750 ppmv (parts per

million by volume) and limit global temperature

rise between 1.5 to 2 degrees Celsius above

pre-industrial levels.

The adverse climatic effects of a rise in GHG

emissions and global temperatures rises are well

established and proven, and India too has not been

spared from adverse climatic events. As a signatory

of the Paris Agreement 2015, India has committed to

reducing emissions by 50% by the year 2050 and

reaching net zero by 2070. Given the sectoral

composition and sources of CO

2

emissions in India,

CCUS will have an important and integral role to play

in ensuring India meets its stated climate goals,

through the deep decarbonization of energy and CO

2

emission intensive industries such as thermal power

generation, steel, cement, oil & gas refining, and

petrochemicals. CCUS can enable the production of

clean products while utilizing our rich endowments

of coal, reducing imports and thus leading to an

Indian economy. CCUS also has an important

role to play in enabling sunrise sectors such as coal

gasification and the nascent hydrogen economy

in India.

1.2 Global CCUS Landscape

Globally there are about 21 CCUS facilities, with a

capacity of capturing about 40 mtpa of CO

2

or only

0.1% of the 40 gtpa global annual GHG emissions. The

first CCUS projects started in the 1970s and 1980s in

Texas for capturing CO

2

from natural gas processing

plants and supplying it to local oil producers for

utilizing the CO

2

for Enhanced Oil Recovery. Since

then, CCUS has spread to other regions and countries,

viz. Norway, Canada, Australia, Brazil, Canada, China,

Saudi Arabia and the United Arab Emirates. A list of

the operating CCUS facilities as of 2020 is tabulated in

Table 1-1. The extent of public funding support

provided to these CCUS facilities (where applicable) is

also provided.

29

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Carbon Capture Utilization and Storage (CCUS) –

Policy Framework and Deployment Mechanism in India

Introduction

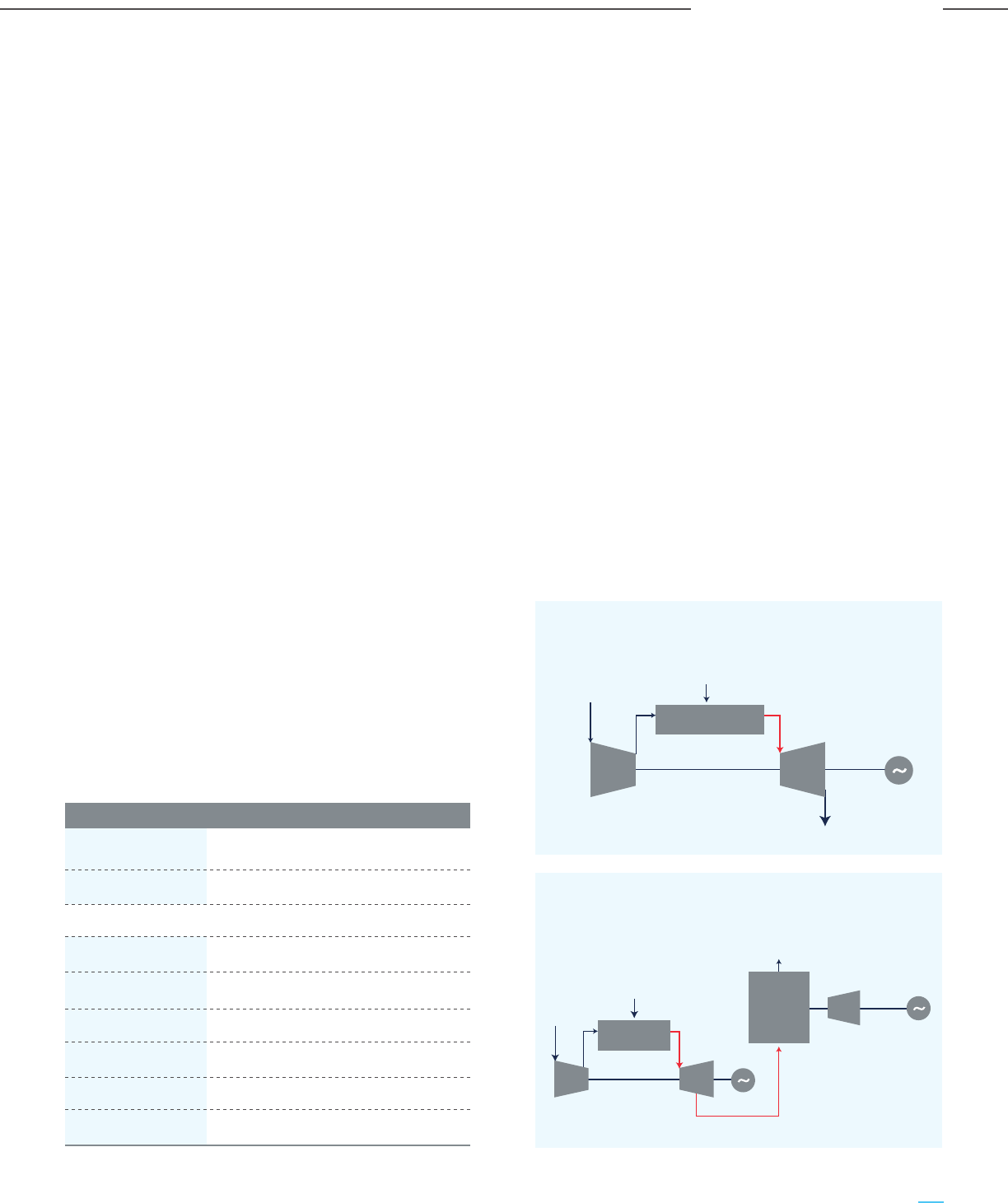

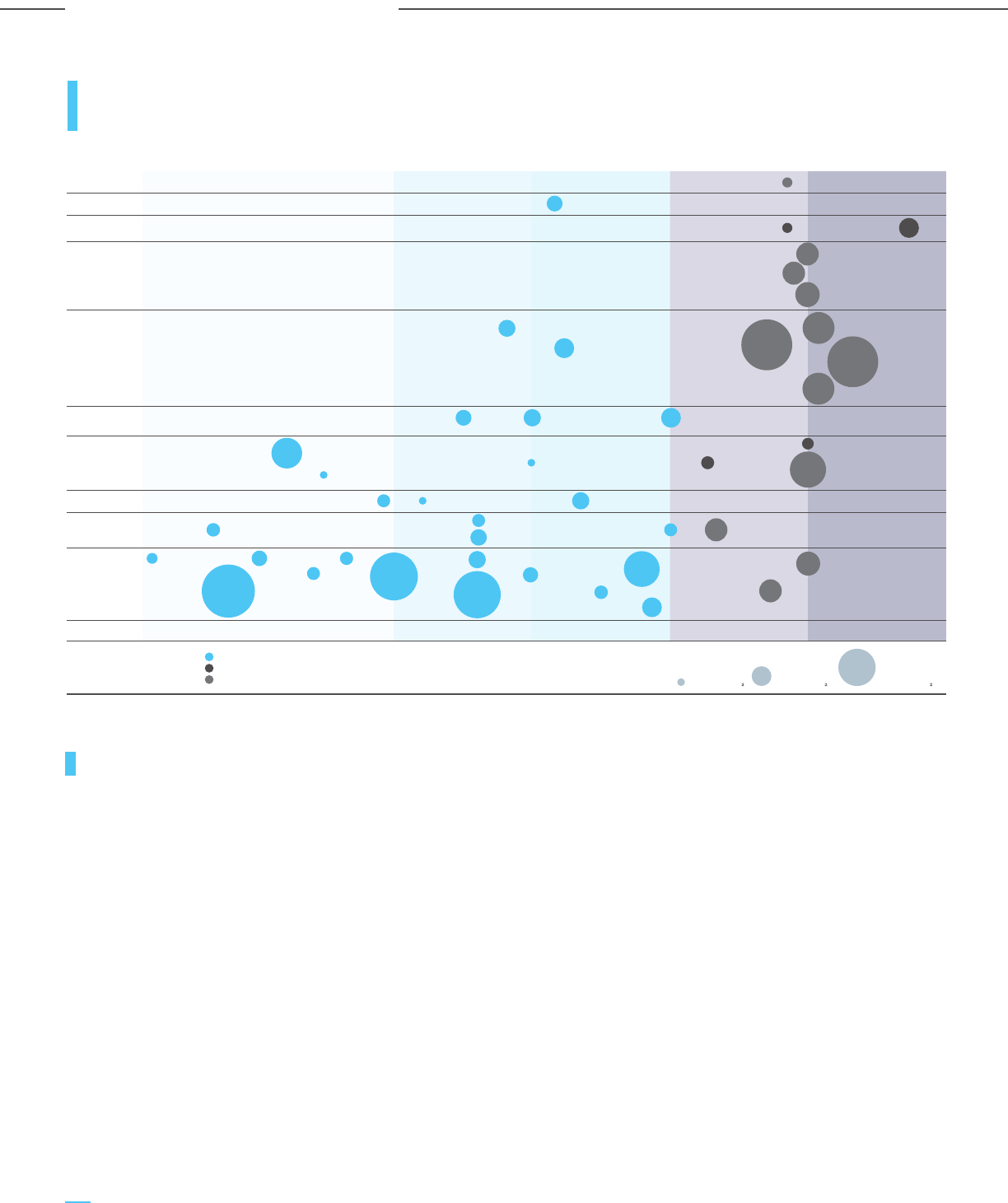

Table 1-1: Large Scale CCUS facilities in operation in 2020

Country Project Operations CO

2

Public Funding CO

2

capture CO

2

start source funding sources capacity disposition

(mtpa)

USA

1972Terrell natural gas plants

(earlier Val Verde)

Natural gas

processing

No 0.5 EORCapital cost: US$

27.6 mn

USA

1982Enid fertiliser Fertilizer

production

No

0.7 EORNot available

Norway

2008Snohvit CO

2

storage

project

Natural gas

processing

No 0.7 StorageNot available

USA

2013Lost Cabin Gas Plant Natural gas

processing

No 0.9 EORProject cost –

US$ 400 mn

USA

2013Coffeyville

Gasification

Fertilizer

production

No 1.0 EORNot available

Brazil

2013Petrobras Santos Basin

pre-salt oilfield CCS

Natural gas

processing

No 3.0 EORNot available

Saudi Arabia

2015Uthmaniyah CO

2

-EOR

demonstration

Natural gas

processing

No 0.8 EORNot available

Canada

2015Quest Hydrogen

production

Yes 1.0 StorageProject cost-

CAD 1.35 bn

Federal Govt. support

– CA$ 120 mn

Alberta Govt. –

CA$ 745 mn

Canada

2014Boundary Dam CCS Power

generation

(coal)

Yes 1.0 EORProject Cost –

CA$ 1.35 bn

Federal Govt.

support – CA$

240 mn

USA

2010Century plant Natural gas

processing

No 8.4 EORProject cost –

US$ 1.1 bn

USA

2013Air Products steam

methane reformer

Hydrogen

production

Yes 1.0 EORProject cost –

US$ 431 mn

US DOE funding –

US$ 284 mn

(through the

American

Recovery and