REPORT OF THE

MARKET MISCONDUCT TRIBUNAL

OF HONG KONG

on whether any market misconduct has taken place

in relation to the listed securities of

Meadville Holdings Limited

on and between 14 September and 17 November 2009

and on other related questions

i

INDEX

Paragraphs

Chapter 1

INTRODUCTION

1-10

- The Notice

3-10

Chapter 2

THE LAW

11-28

- Insider dealing

12-14

- Specific information

15-21

- The Standard of Proof

22-23

- Circumstantial evidence and inferences

24

- Good character

25-26

- Lies

27

- Prejudice from delay

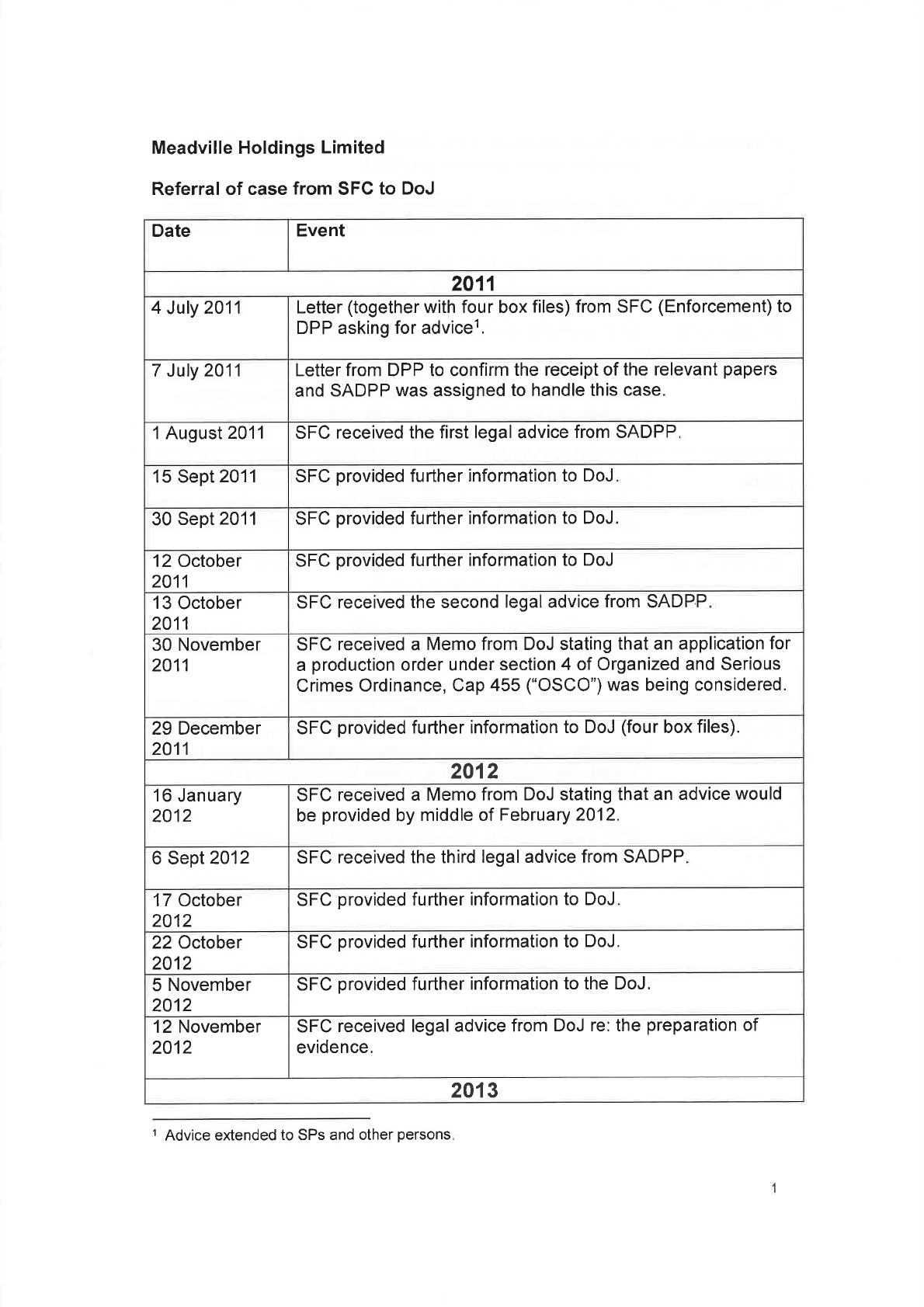

28

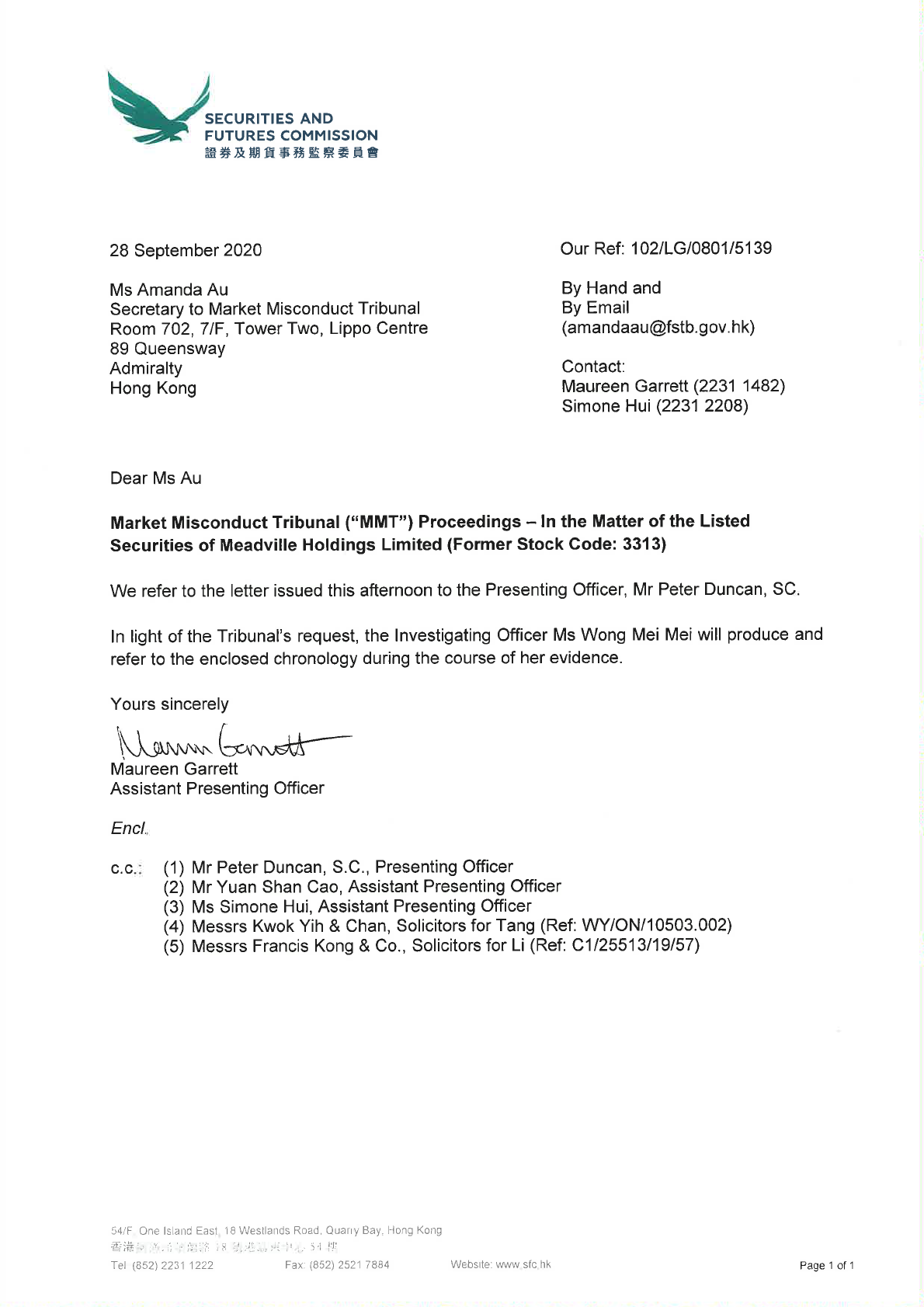

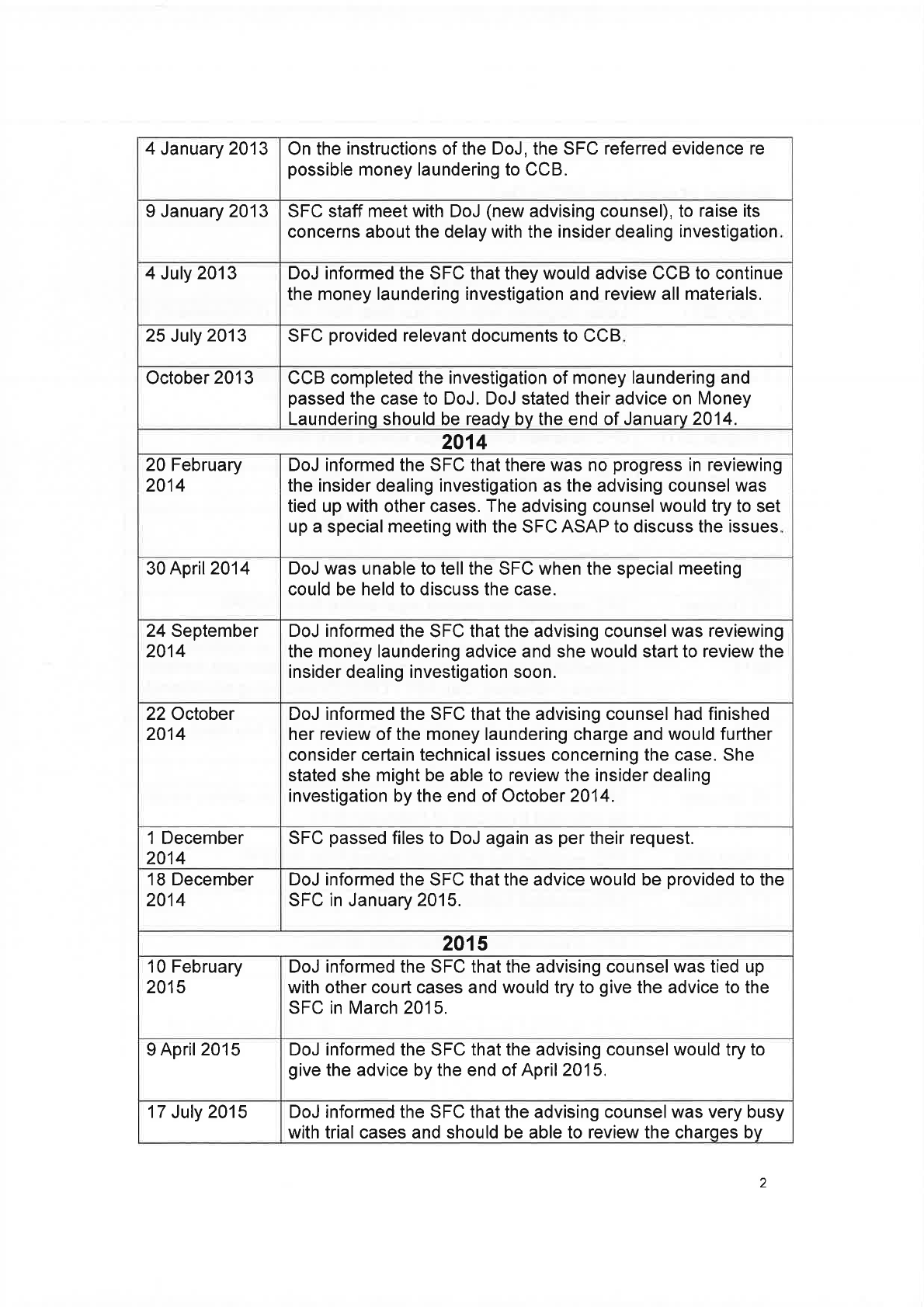

Chapter 3

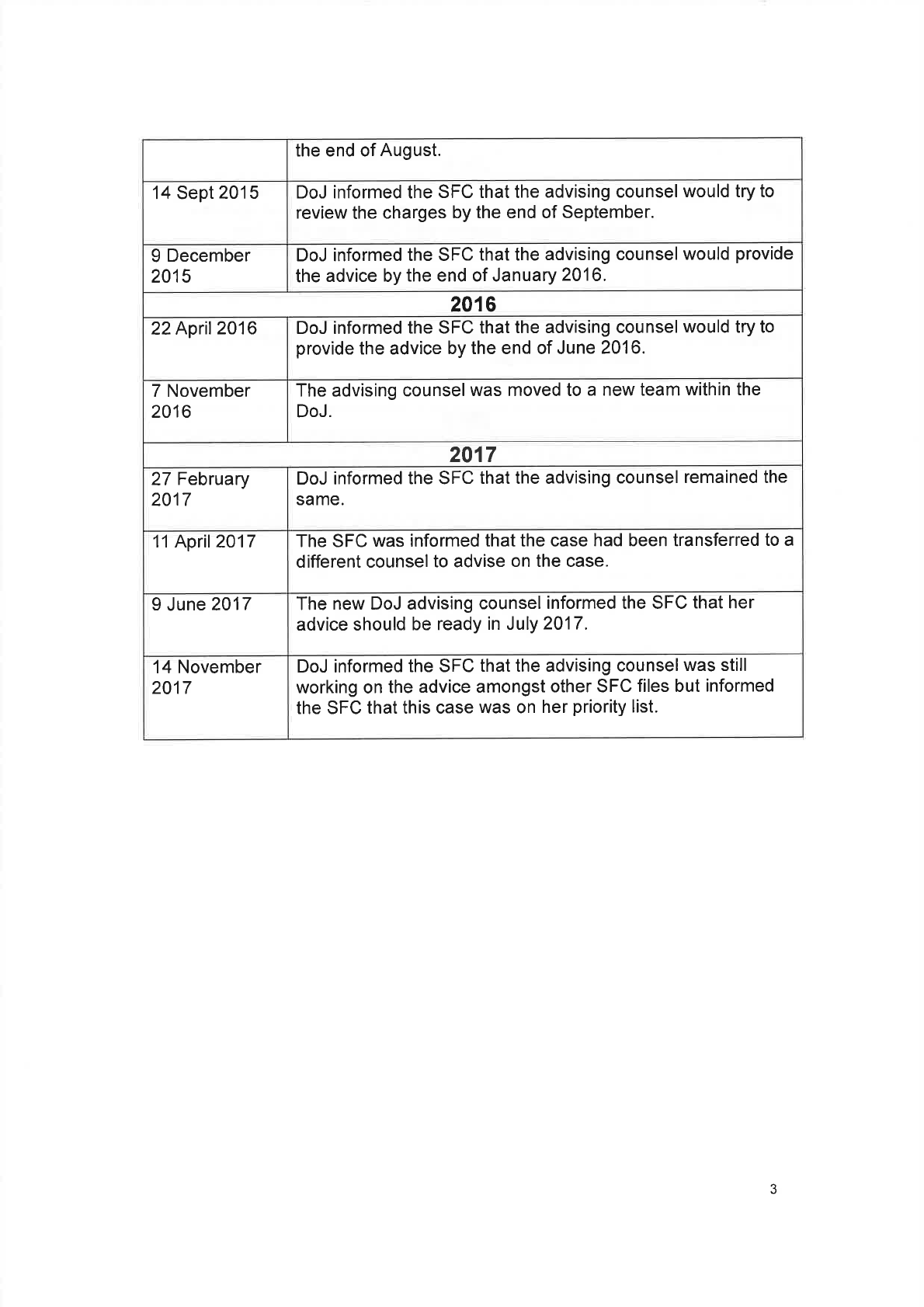

THE EVIDENCE

29-125

The factual evidence

(i) Ms Wong Mei Mei

30-56

- Inordinate and prejudicial delay

32-37

- Section 183 (1) Notices: 10 April and 14 May 2010

38

- Provenance of the monies used to buy shares in the

account of Ms Li

39

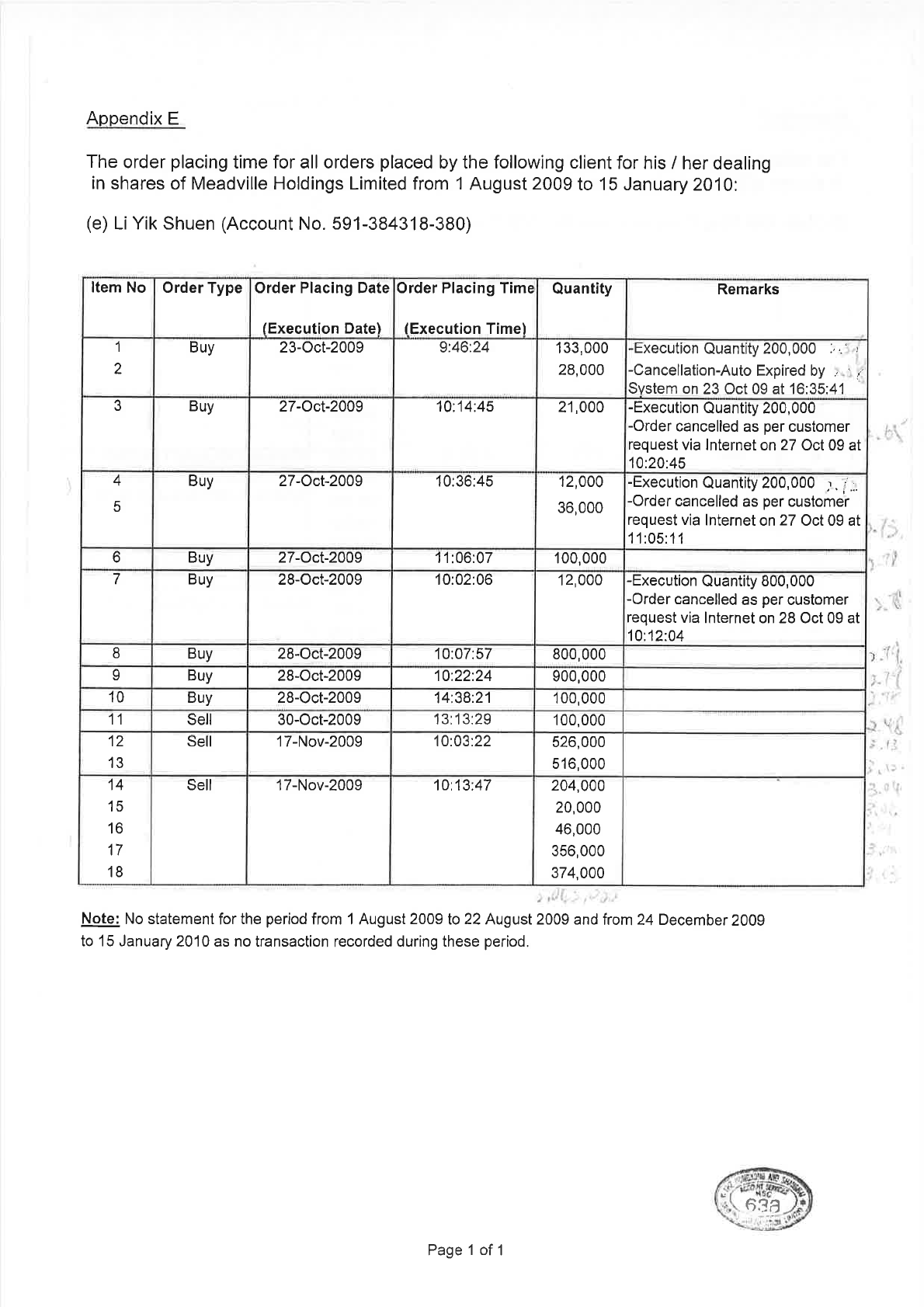

- Records of telephone calls between Mr Tang and

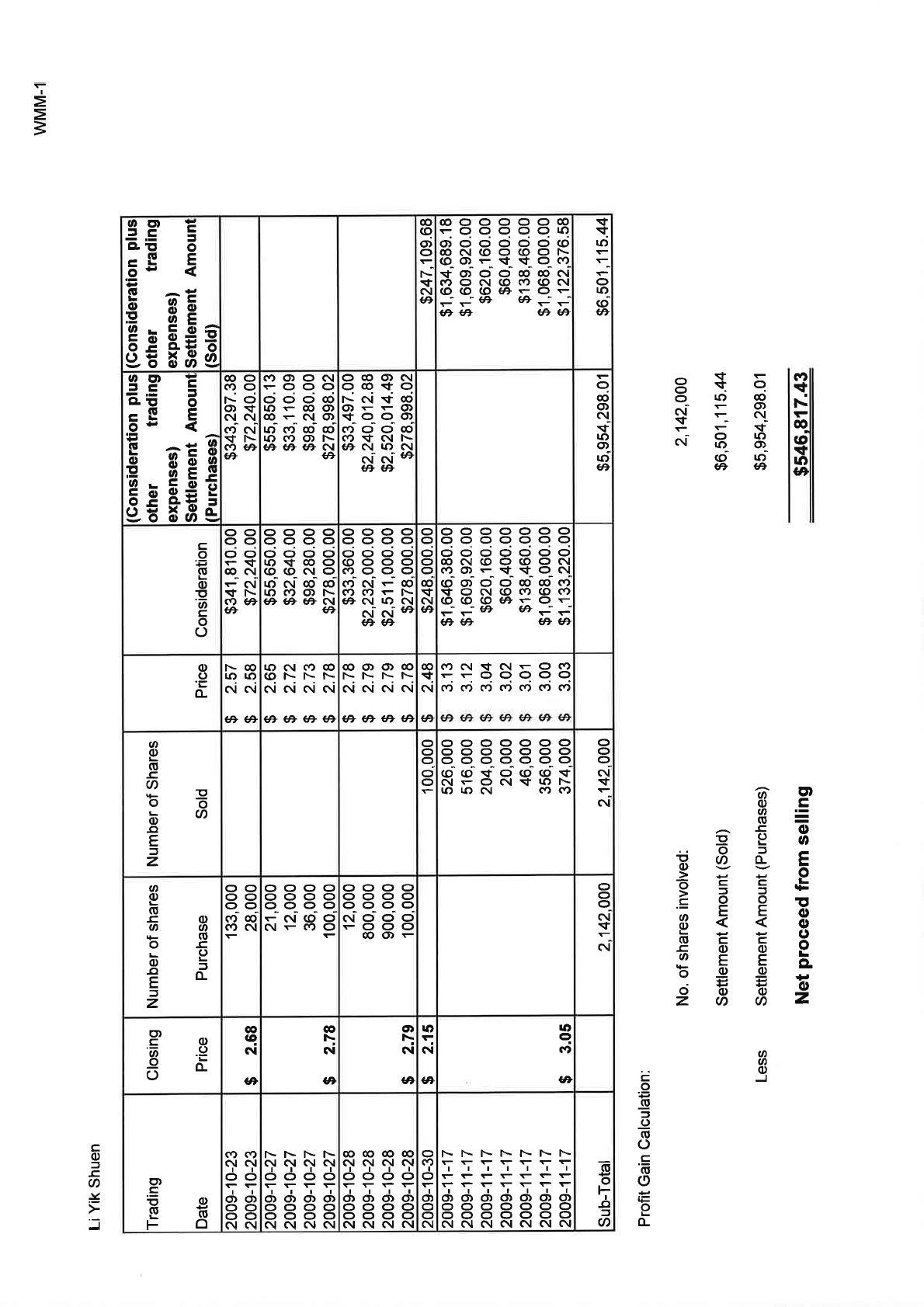

Ms Li

40

- 29 and 30 October 2009: negotiations between

Meadville and TTM

41-45

- Ms Li’s dealing in Meadville shares

46-47

- 31 October 2009

48-49

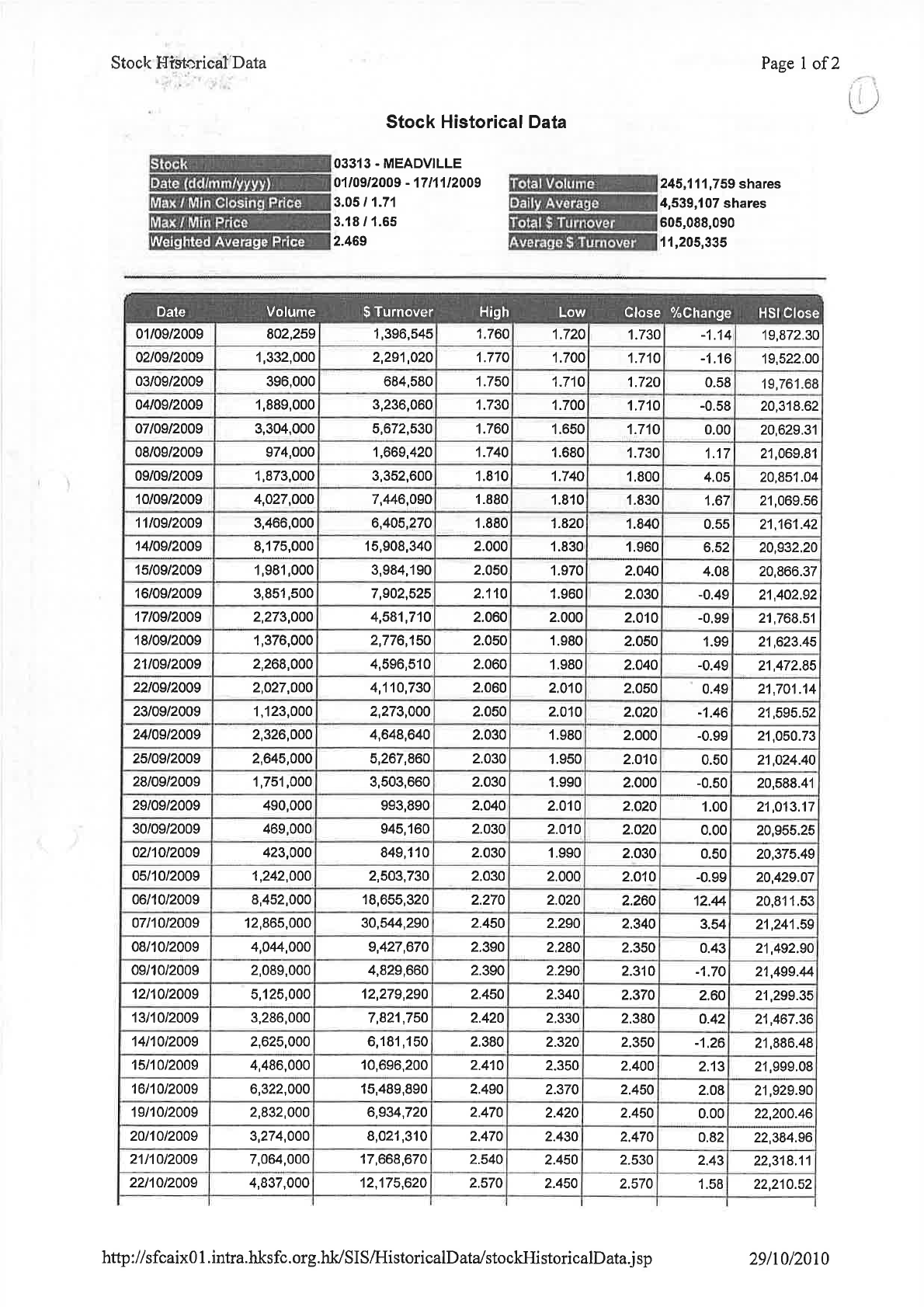

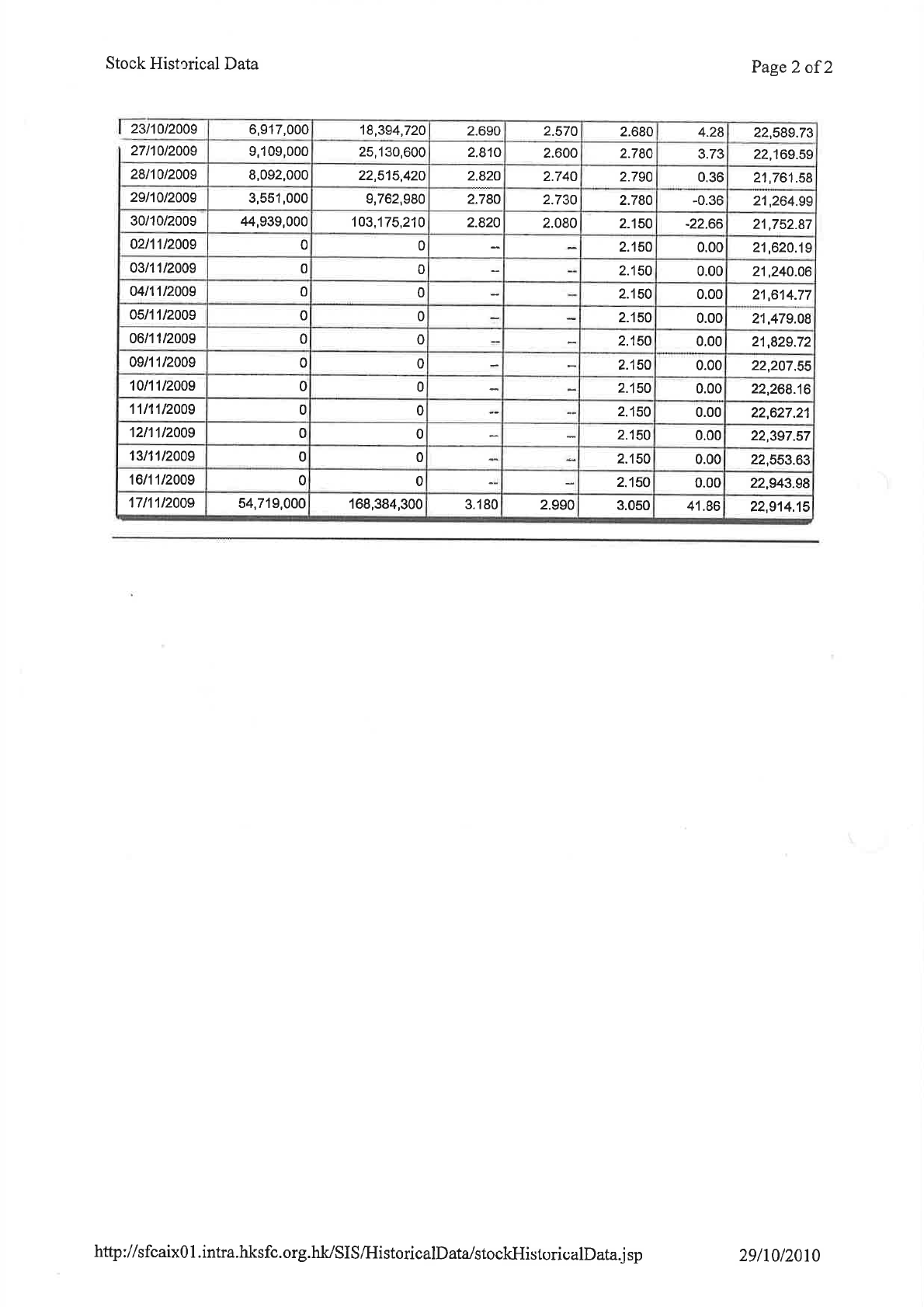

- 11 and 16 November 2009

50

- Public information about Meadville

51-52

- Instructions to the SFC’s expert witness

53-56

(ii) Mr Tang Chung Yen, Tom

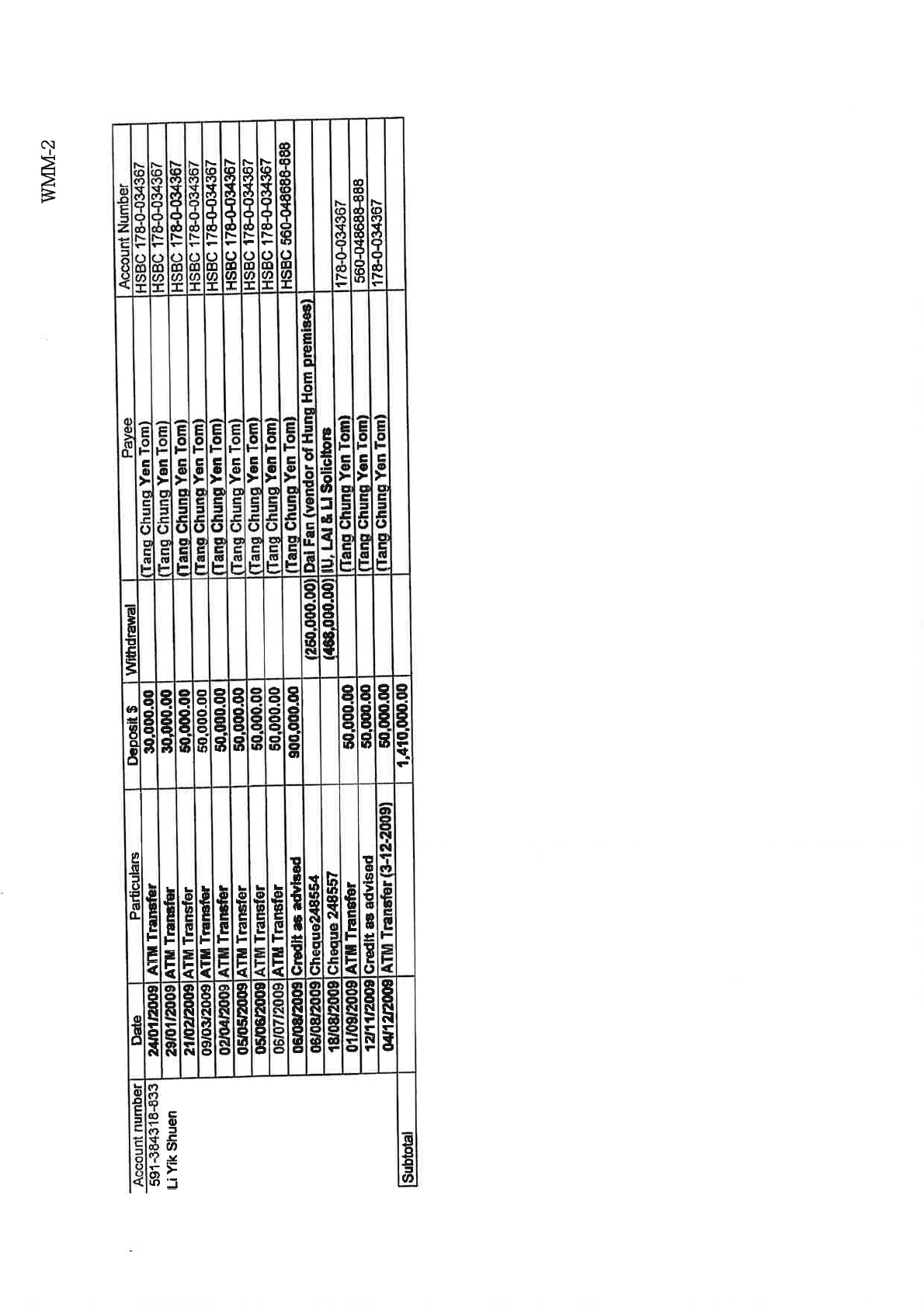

57-88

- Relationship with Ms Li

58-62

- Money transfers to Ms Li

63-68

ii

Paragraphs

- Counselling or procuring Ms Li to deal in

Meadville shares and/or disclosing relevant

information to Ms Li

69-72

- Leakage of information in relation to Meadville

73-88

(iii) Ms Li Yik Shuen

89-125

- Personal background

89

- Ms Li’s relationship with Mr Tom Tang

90-93

- Ms Li’s purchase of shares

94-95

- Ms Li’s purchase of a flat at Laguna Verde

96-97

- Ms Li’s purchase of Meadville shares

98

- The circumstances in which Ms Li traded in

Meadville shares

99-113

- The purchase, payment for, sale of Meadville

shares and remittance of the proceeds

114-125

- 23 October 2009

115-119

- 27 October 2009

120-121

- 28 October 2009

122

- 30 October 2009

123-124

- 17 November 2009: the sale of the balance of

Ms Li’s Meadville shares

125

Chapter 4

EXPERT EVIDENCE

126-319

(i) Mr Karl Lung

126-225

Meadville

126-129

(a) Shares in issue

126

(b) Financial performance

127

(c) Trading in Meadville’s shares

128-129

(i) Price

128

(ii) Volume

129

The SFC’s Instructions

130-153

Who were accustomed, or would have been likely, to

deal in the shares of Meadville?

133-135

iii

Paragraphs

Was that information generally known to those persons

accustomed to or likely to deal in Meadville shares?

136-140

If known, would it likely have materially affected the

price of Meadville shares?

141-142

How and to what extent would it have affected the

price? Would it have been likely to have had a

materially positive effect on the share price between

23 and 28 October 2009?

143-146

What was the main reason for the price and volume at

which Meadville shares traded in the period

23 October to 16 November 2009?

147-149

What was the main reason for the price and volume at

which Meadville shares traded after the

Announcement?

150-153

- The increase in the price at which Meadville shares

traded in 2009: 3 periods

154

- The reasons for the increase in the price at which

Meadville shares traded in 2009

- Context: Meadville’s shares underperformed

the HSI (February 2007 to October 2009)

155-156

- Media reports: factors relevant to the rise in the

price/volume of trading in Meadville’s shares

157

- Meadville’s Annual General Meeting: 2 June

2009-media reports

158-165

- Meadville’s Interim Report 2009: 17 August 2009

166-172

- 18 August 2009: media reports

173-182

- 6-27 October 2009: media reports 7 and 8 October

2009

183-190

- 30 October 2009: 22.66 per cent drop in Meadville

share price and suspension of trading at 3:19 p.m.

191-200

- 31 October 2009: media reports-Apple Daily and

Ming Pao Daily News

201-206

iv

Paragraphs

- Media reports: November 2009

207-220

- 11 November 2009

207-209

- 12 November 2009

210-212

- 16 November 2009

213-215

- 17 November 2009

216-220

- Mr Lung’s opinion: unlikelihood of news/rumours

circulating in the market for about a year before

30 October 2009

221-225

(ii) Mr Clive Rigby

226-287

- The price and volume of trading in Meadville

shares

226

- Those accustomed to or would be likely to deal in

Meadville shares

227

- Trading in Meadville shares:

228-230

(i) May to June 2009

228-229

(ii) June to October 2009

230

- Leaks of the negotiations

231-232

- 3 June 2009: TTM’s revised offer

233-236

- Due diligence

237

- 2 October 2009

238-242

- Other contributing factors to the rise in price and

volume of trading in Meadville shares

243-258

Meadville:

243-247

(i) positive news

243-247

Mr Henry Tang:

(ii) the Chief Secretary and (iii) aspirant CE

248-249

(iv) Meadville’s underperformance: Hang Seng

Index and IPO price of $2.25

250

- ‘Stock in Play’

251-254

- 29 October 2009

255

- 30 October 2009: trading in Meadville shares

256

- Individual traders

257

v

Paragraphs

- Panic selling/margin calls/stop-loss orders

258

- During the period 23 October to 17 November

2009, was information relating to the Transactions

generally known?

259

- Media reports on 31 October and in

November 2009

260-262

- Attribution of ‘rumours’ asserted in the media

263-268

- Generally known

269

- Specific information

270-273

- Mr Lung’s opinion that information of the

Transactions was not generally known

274-283

(i) No media reports of rumours of the

Transactions prior to suspension of trading

275-281

(a) Media reports of the names of the parties

to the Transactions

276-278

(b) The structure of the deal

279

(c) The price per Meadville share

280-281

(ii) No SFC/SEHK investigation

282

(iii) Rumours of the Transactions/collapse: the rise

and fall to be expected of Meadville’s share

price

283

- 23 October 2009: the Meadville Board meeting

284

- Trading in Meadville shares: 23-29 October 2009

285

- The performance of Meadville shares after the

Announcement of 16 November 2009

286-287

(iii) Mr Charles Li

288-319

- Rumours of the Transactions: generally known

288-295

- Materially affect the price

296-297

Conclusion: the information was generally known

and not relevant information

298-300

- The causes of the rise in price at which Meadville

shares traded

301

vi

Paragraphs

Conclusion

302-305

- Other factors

306-319

- Mr Henry Tang

306-307

- Meadville’s underperformance

308

- Growth momentum

309-310

- Trading liquidity of Meadville shares

311-315

- No media reports of rumours of the proposed

transaction prior to 31 October 2009

316-319

Chapter 5

FINDINGS

320-401

- Specific information

322-326

- Not generally known to those who were accustomed or

would be likely to deal in Meadville shares

327

- Who were accustomed or would be likely to deal in

Meadville shares?

- Delay

328-336

- Prejudice from delay

337-340

- Not generally known

341

- Media reports: 1 April to 30 October 2009

342-345

- 31 October 2009: Apple Daily and Ming Pao Daily

News

346-349

- Media reports in November prior to the Announcement

on 16 November 2009

350-354

- Generally known: the significance of the absence of

any media reports of rumours of the proposed

transactions

355-359

- Would knowledge of the specific information have

materially affected the price at which Meadville shares

traded?

360

- 17 November 2009: the resumption of trading in

Meadville shares

361-363

Conclusion

364

- Ms Li’s dealing in Meadville shares

365

vii

Paragraphs

- The circumstances of Ms Li’s purchase of Meadville

shares

366-369

- Ms Li’s credibility

370

- Ms Li’s records of interview

371-374

- Ms Li’s relationship with Mr Wu Feng

375-378

- The reasons for Ms Li’s purchase of Meadville shares

379-380

- Ms Li’s possession of relevant information

381-384

- Ms Li’s receipt of the relevant information from

Mr Tang

385

Conclusion

386

- Mr Tang Chung Yen

387-388

- Did Mr Tang disclose relevant information to Ms Li or

counsel or procure her to deal in Meadville shares?

389-392

- Mr Tang’s relationship with Ms Li

393-395

- Mr Tang’s financial support of Ms Li

396-397

- Did Mr Tang counsel or procure Ms Tang to deal in

Meadville shares?

398

- Did Mr Tang disclose relevant information to Ms Li?

399

- Did Mr Tang disclose the relevant information

knowing or having reasonable cause to believe that

Ms Li would use the information to deal in Meadville

shares?

400

Conclusion

401

The profit gained by Ms Li as a result of her market

misconduct

Attestation to the Report

402

viii

APPENDICES

Pages

1

- Referral of case from SFC to DoJ

A 1-5

2

- Orders to buy and sell placed by Ms Li for Meadville

shares from 1 August 2009 to 15 January 2010

A 6

3

- The quantity and price of Meadville shares acquired and

sold in response to Ms Li’s orders to buy and sell

A 7

4

- Payments made from Mr Tang’s bank accounts to the

HSBC account of Ms Li in 2009

A 8

5

- Meadville Stock Historical Data/Stock Price Details

A 9-14

1

CHAPTER 1

INTRODUCTION

1. Meadville Holdings Limited (“Meadville”), was a company incorporated in the

Cayman Islands, and was formally listed on the Stock Exchange of Hong Kong Limited

(“SEHK”). Meadville’s principal businesses were the manufacture and distribution of printed

circuit boards (“PCB Business”) and laminates and prepregs (“Laminate Business”). On 30

October 2009, Meadville shares fell from HK $2.78 to HK $2.15, when trading in the shares

was suspended at 15:19 hours. On 16 November 2009, Meadville issued an Announcement of:

1

(a) the signing of transaction agreements for the sale by Meadville of the PCB Business

to TTM Technologies, Inc. (“TTM”), a company incorporated in Delaware, United

States of America, whose shares were listed on the NASDAQ stock exchange, the

sale of the Laminate Business to Top Mix Investments Limited, a British Virgin

Islands-incorporated company, indirectly owned by Tang Hsiang Chien; and

(b) the proposed distribution to shareholders on the Distribution Date by way of

dividend of the aggregate consideration from the sale of the PCB Business and the

Laminate Business in cash and TTM shares, so that the aggregate value of each

Meadville share was approximately HK $3.47.

2

2. On 17 November 2009, trading in Meadville shares resumed and the price rose, from

the price at which trading was suspended on 30 October 2009, namely HK $2.15, to HK $3.05.

The Notice

3. By a Notice

3

, dated 10 September 2019, issued pursuant to section 252(2) and Schedule

9 of the Securities and Futures Ordinance, Cap. 571(“the Ordinance”) the Securities and

Futures Commission (“the SFC”) informed the Market Misconduct Tribunal (“the Tribunal”)

that it appeared to the SFC that “market misconduct within the meaning of section 270, Part

XIII of the Ordinance has or may have taken place in relation to dealings” in the securities of

Meadville, to whom it referred to as MHL, and required the Tribunal:

1

HB-1, pages 156-279.

2

HB-1, page 159.

3

Tribunal Bundle, pages 4-9.

2

“to conduct proceedings and determine:

(a) whether any market misconduct has taken place;

(b) the identity of any person who has engaged in the market misconduct

found to have been perpetrated; and

(c) the amount of any profit gained as a result of the market misconduct found

to have been perpetrated.”

4. Further, the Notice stipulated:

“Persons suspected to have engaged in market misconduct

(1) Tang Chung Yen, Tom (“Tang”)

(2) Li Yik Shuen (“Li”)”

5. In the ‘Statement for Institution of Proceedings’, it was stipulated that:

“(a) Tang was an Executive Director and the Chairman of MHL; and

(b) Tang and Li were in an intimate relationship.”

6. Of the steps taken in the negotiations between the parties that led to the Announcement,

dated 16 November 2009, it was stated that:

“2. In around January 2008, TTM Technologies, Inc. (“TTM”), a company

incorporated in the United States whose shares were listed on the NASDAQ stock

exchange, approached MHL regarding a potential acquisition/merger.

3. Negotiations ensued and by late July 2009 the proposed acquisition was expected

to be proceeded with by separate sales of the PCB Business to TTM and the

Laminate Business to the Tang family (headed by Tang’s father, Tang Hsiang

Chien). The sales proceeds would then be distributed to MHL’s shareholders

(“Proposed Transaction”).

4. By the beginning of October 2009, it was expected that the amount to be distributed

to MHL’s shareholders would be about HK$3.40 per share.

5. On 23 October 2009, a board meeting of MHL was held to discuss the Proposed

Transaction (“Board Meeting”). Tang chaired the meeting. The directors of MHL

resolved, inter alia, to proceed with the Proposed Transaction.

3

6. Following a pause in the subsequent negotiations between TTM and MHL the share

price of MHL fell by about 23%, from HK$2.78 to HK$2.15, on 30 October 2009

4

.

Trading in MHL’s shares was suspended in the afternoon of 30 October 2009 and

remained suspended until the end of 16 November 2009.”

7. Of the significance of that information, it was asserted:

5

“9. The information that it was proposed that MHL sell its principal businesses and

that there would be the payment of a dividend of about HK$3.40 per share to

MHL’s shareholders (“Information”) was specific information about MHL and its

listed securities.

10. The Information was not generally known to the persons who were accustomed or

would have been likely to deal in the shares of MHL until 16 November 2009, but

would if generally known to them before then have been likely to materially affect

the price of MHL’s shares.

11. The Information was accordingly “relevant information” within the meaning of

section 245(2) of the Ordinance (as applicable to dealings in 2009)

6

.”

8. Of Mr Tang, it was asserted:

“12. As a director or employee of MHL, Tang was a person “connected with” MHL (by

virtue of section 247(1)(a) of the Ordinance).

Tang’s possession of the relevant information

13. By reason of the fact that:

(a) he was involved in the negotiations between TTM and MHL;

(b) he was an Executive Director and the Chairman of MHL; and

(c) he was present at the Board Meeting,

Tang had the Information.”

9. Of Ms Li’s dealings in Meadville shares it was stated:

“14. Li purchased MHL shares in the morning of 23 October 2009 (the date of the Board

Meeting). She bought 161,000 shares at between HK$2.57 and HK$2.58 per share.

She had never previously purchased MHL shares.

4

During the month of October 2009, MHL’s share price rose from HK$2.03 on 2 October to HK$2.78 on

29 October, an increase of about 37%. By comparison, the Hang Seng Index rose by about 4.4% during the same

period.

5

Tribunal Bundle, pages 6-7.

6

It is to be noted that “relevant information” was the term used in the context of insider dealing prior to the

amendments to the Ordinance which came into effect on 1 January 2013. These amendments made no

substantive change to the definition of what is now called “inside information”.

4

15. On 27 October 2009, Li bought a further 169,000 MHL shares at between HK$2.65

and HK$2.78 per share.

16. On 28 October 2009, Li bought a total of 1,812,000 MHL shares at between

HK$2.78 and HK$2.79 per share.

17. In total, Li bought 2,142,000 MHL shares over 3 consecutive trading days (26

October 2009 was a public holiday).

18. On 30 October 2009, Li sold 100,000 MHL shares at HK$2.48 per share in the

afternoon before trading was suspended.

19. When trading resumed on 17 November 2009, Li sold her entire shareholding in

MHL shortly after the market opened, at between HK$3 and HK$3.13 per share.

20. The total purchase price paid by Li for the 2,142,000 MHL shares was

HK$5,954,298.01 (including fees and charges). The total proceeds received by her

from the sales of the same shares were HK$6,501,115.44 (net of fees and charges).”

10. Finally, allegations of insider dealing were made against Mr Tang and Ms Li:

7

“Insider dealing by Tang

21. Being a person connected with MHL and having the Information which he knew

was relevant information in relation to MHL, Tang:

(a) counselled or procured Li to deal in MHL’s shares, knowing or having

reasonable cause to believe that she would deal in them; and/or

(b) disclosed the Information, directly or indirectly, to Li, knowing or

having reasonable cause to believe that she would make use of the

Information for the purpose of dealing in MHL’s shares.

22. Accordingly, Tang engaged or may have engaged in market misconduct contrary

to sections 270(1)(a)(ii) and/or 270(1)(c) of the Ordinance.

Insider dealing by Li

23. Li,

(a) having the Information which she knew was relevant information in

relation to MHL and which she received, directly or indirectly, from

Tang;

(b) knowing that Tang was connected with MHL;

(c) knowing or having reasonable cause to believe that Tang held the

Information as a result of being connected with MHL;

7

Tribunal Bundle, pages 8-9.

5

(d) dealt in MHL’s shares as set out in paragraphs 14 to 19 above.

24. Accordingly, Li engaged or may have engaged in market misconduct contrary to

section 270(1)(e)(i) of the Ordinance.”

6

CHAPTER 2

THE LAW

11. Given that the misconduct alleged against Mr Tang and Ms Li occurred in October 2009,

the relevant statutory provisions are those in the Ordinance which were in force at that date.

12. Section 270 (1) of the Ordinance provided:

(1) Insider dealing in relation to a listed corporation takes place—

(a) when a person connected with the corporation and having information

which he knows is relevant information in relation to the corporation—

(i) …

(ii) counsels or procures another person to deal in such listed

securities or derivatives, knowing or having reasonable cause

to believe that the other person will deal in them;

(c) when a person connected with the corporation and knowing that any

information is relevant information in relation to the corporation,

discloses the information, directly or indirectly, to another person,

knowing or having reasonable cause to believe that the other person will

make use of the information for the purpose of dealing, or of

counselling or procuring another person to deal, in the listed securities

of the corporation or their derivatives, or in the listed securities of a

related corporation of the corporation to or their derivatives;

(e) when a person who has information which he knows is relevant

information in relation to the corporation and which he received,

directly or indirectly, from a person whom he knows is connected with

the corporation and whom he knows or has reasonable cause to believe

held the information as a result of being connected with the

corporation—

(i) deals in the listed securities of the corporation

13. Section 245 (2) provided that:

“relevant information”, in relation to a corporation, means specific information about—

7

(a) the corporation;

(b) a shareholder or officer of the corporation; or

(c) the listed securities of the corporation or their derivatives,

which is not generally known to the persons who are accustomed or would be likely to

deal in the listed securities of the corporation but which would if it were generally

known to them be likely to materially affect the price of the listed securities;

“securities” (證券) means—

shares, stocks…

“listed securities” (上市證券) means—

(a) securities which, at the time of any insider dealing in relation to a

corporation, have been issued by the corporation and are listed;

“listed” (上市) means listed on a recognized stock market, and for the purposes of this

definition, securities shall continue to be regarded as listed during a period of

suspension of dealings in those securities on the recognized stock market;

14. Section 247 (1) provided that:

For the purposes of Division 4, a person shall be regarded as connected with a

corporation if, being an individual—

(a) he is a director or employee of the corporation or a related corporation.

Specific information

15. The term “specific information” is not defined in the Ordinance. However, it has been

considered on a number of occasions by the Insider Dealing Tribunal and subsequently by this

Tribunal. In the Report of the Insider Dealing Tribunal in Chinese Estates Holdings Limited,

dated 25 June 1999, the Tribunal, under the chairmanship of Hartmann J as he was then, said:

8

“Specific information is information which possesses sufficient particularity to be

capable of being identified, defined and unequivocally expressed. In this primary sense

it is to be contrasted with mere rumour, with vague hopes and worries or with

unsubstantiated conjecture. Of course, in the ebb and flow of business affairs, what

begins, for example, as a vague hope or worry may over time acquire sufficient

substance and particularity to be properly defined as specific information. If and when

such a transformation takes place is a question of fact.”

8

The Report of the Insider Dealing Tribunal in Chinese Estates Holdings Limited, page 39.

8

16. In the Report of the Insider Dealing Tribunal in Firstone International Holdings Limited,

dated 2 April 2004, the Tribunal, under the chairmanship of McMahon J said:

9

“…the proposed placement whether described as under contemplation or at a

preliminary stage of negotiation must, in our view, have more substance than merely

being at the stage of a vague exchange of ideas or a “fishing expedition”. When

negotiations or contacts have occurred, as in the present case, there must be a substantial

commercial reality to such negotiations which goes beyond a merely exploratory testing

of the waters and which is at a more concrete stage where the parties have an intent to

negotiate with a realistic view to achieving an identifiable goal.”

17. The Tribunal went on to add:

10

“...there is no need to impose any additional requirement that there be any foresight that

the transaction will “probably” or “likely” come to fruition before information

concerning the contemplated transaction becomes sufficiently specific.

In this regard we adopt the reasoning set out in the Report of the Tribunal in the Stime

Watch inquiry.”

18. In the Report of the Insider Dealing Tribunal in Stime Watch International Holding

Limited, dated 6 December 2002, under the chairmanship of the then Deputy High Court Judge

McMahon, the Tribunal said:

11

“It seems to this Tribunal that there can be no additional requirement that information,

otherwise specific, which relates to a proposed transaction can only be specific if, by

some objective or even subjective measure, that proposed transaction is more probable

than not to proceed or come to fruition.”

19. The Tribunal went on to explain:

12

“The requirement that information be specific relates to the characteristics and contents

of the information concerning the company’s affairs itself and does not logically depend

on whether or not the subject matter of the information, if a proposed course of action,

has any particular likelihood of fruition or success.”

20. In Securities and Futures Commission v Chan Pak Hoe Pablo

13

, Macrae J, as Macrae

VP was then, dismissed the appellant’s appeal against his conviction for an offence, contrary

to section 291(5) and (8) of the Ordinance. In doing so, he considered the ambit of the term

9

The Report of the Insider Dealing Tribunal in Firstone International Holdings Limited, pages 60-61.

10

The Report of the Insider Dealing Tribunal in Firstone International Holdings Limited, page 61.

11

The Report of the Insider Dealing Tribunal in Stime Watch International Holding Limited, pages 84-85.

12

The Report of the Insider Dealing Tribunal in Stime Watch International Holding Limited, page 85.

13

Securities and Futures Commission v Chan Pak Hoe Pablo [2011] 5 HKC 484.

9

‘specific information’. Having cited with approval the various statements of the Insider Dealing

Tribunal in the reports quoted earlier, Macrae J said that he agreed, “For the reasons articulated

in the Stime Watch case”, that there was no requirement that a stage had to be reached in

negotiations where there existed a probable consequence that the agreement would be

successfully concluded before information concerning the transaction became sufficiently

specific.

21. In determining that the appellant was possessed of specific information, Macrae J said:

14

“The proposed sale of all Globalcrest’s shares in Universe to Goldwyn was clearly

beyond the exploratory stage of ‘testing the waters’, mere rumour or a ‘fishing

expedition’. The parties had spent substantial costs in engaging professional financial

consultants and lawyers to advise on the details of the transaction… The fact that the

details of the proposed transaction had encountered obstacles and needed further

negotiation, and would ultimately have to be approved by the Board of Directors of

Universe, the minority shareholders and the regulators did not take it outside the

meaning of ‘specific information’.”

The Standard of Proof

22. Section 252 (7) provided that:

“…the standard of proof required to determine any question or issue before the Tribunal

shall be the standard of proof applicable to civil proceedings in a court of law.”

23. As this Tribunal stated in its Report in Sunny Global Holdings Limited:

15

“That standard is the “balance of probabilities”. In Solicitor (24/7) v The Law Society

of Hong Kong [2008] 2 HKLRD 576 the Court of Final Appeal accepted, the correctness

of the approach to the civil standard of proof expressed by Lord Nicholls of Birkenhead

in Re H & Others (Minors) (Sexual Abuse: Standard of Proof) [1996] AC 563 at p.586

D-G:

“The balance of probability standard means that a court is satisfied

an event occurred if the court considers that, on the evidence, the

occurrence of the event was more likely than not. When assessing the

probabilities the court will have in mind as a factor, to whatever

extent is appropriate in the particular case, that the more serious the

allegation the less likely it is that the event occurred and, hence, the

stronger should be the evidence before the court concludes that the

allegation is established on the balance of probability.”

14

Securities and Futures Commission v Chan Pak Hoe Pablo, paragraph 32.

15

The Report of the Market Misconduct Tribunal in Sunny Global Holdings Limited. (Part 1 & II)-21 July 2008.

10

Circumstantial evidence and inferences

24. In his judgment in the Court of Final Appeal, with which all the other judges agreed, in

HKSAR v Lee Ming Tee

16

Sir Anthony Mason NPJ addressed the proper approach to the

drawing of inferences in circumstances of allegations of gross misconduct:

“In the present case, where the allegation is that senior officers of the SFC deliberately

and improperly terminated an investigation into Meocre Li’s conduct in the Kin Don

placement, in order to avoid the need to make a disclosure which might compromise

Meocre Li’s standing as an expert witness in the trial, that conclusion was not to be

reached by conjecture nor, as the respondent submitted, on a mere balance of

probabilities. It was to be plainly established as a matter of inference from proved facts.

It is not possible to state in definitive terms the nature of the evidence which the court

will require in order to be satisfied, in a civil proceeding, that a serious allegation of

this kind, is made out. It would not be right to say that the requisite standard prescribes

that the inference of wrongdoing is the only inference that can be drawn (cf Sweeney v

Coote [1907] AC 221 at p.222, per Lord Loreburn) for that is the standard which applies

according to the criminal standard of proof. In the particular circumstances, it was for

the respondent to establish as a compelling inference that very senior officers of the

SFC had deliberately and improperly terminated the investigation into Meocre Li’s

conduct for the ulterior purpose alleged, sufficient to overcome the inherent

improbability that they would have done so (see Aktieselskabet Dansk Skibsfinansiering

v Brothers & Others (2000) 3 HKCFAR 70 at pp. 91H, 96G-I, PER Lord Hoffmann).”

Good character

25. The good character of a Specified Person supports his/her credibility in respect of both

his/her evidence in the Tribunal and in his/her records of interview conducted by the SFC

outside the Tribunal. A person of good character is less likely than otherwise might be the case

to have committed the alleged misconduct.

26. There is no dispute that the conduct alleged against the Specified Persons is serious

misconduct. In that context, the observations made by Lord Scott of Foscote NPJ in Nina

Kung alias Nina TH Wang and Wang Din Shin

17

are apposite. In the context of allegations that

Mrs Wang had procured the forgery of a document and, in a conspiracy with another person,

was attempting to obtain probate of it as her husband’s will, which she knew to be forged, Lord

Scott said:

18

“The probability of these allegations being true must be judged on the evidence adduced

in the case. But it must also take account of propensity. If such an allegation is made

against a person with a record of involvement in forgery and fraud, the strength of the

16

HKSAR v Lee Ming Tee (2003) 6 HKCFAR 336; at page 362 E-J, paragraph 72.

17

Nina Kung alias Nina TH Wang and Wang Din Shin (2005) 8 HKCFAR 387.

18

Nina Kung alias Nina TH Wang and Wang Din Shin, paragraph 626.

11

other evidence necessary to satisfy the balance of probability test is obviously less than

would otherwise be required. Evidence of propensity must go into the balance…

Evidence to a very high standard of cogency indeed is necessary before the court can

be justified in finding either to be dishonestly involved in a conspiracy to promote a

forged will.”

Lies

27. Lies by themselves prove nothing, save that they have been told. Of course, the fact

that the person has told lies may be relevant to an assessment of his/her credibility. There may

be reasons for lies that are consistent with the absence of any wrongdoing, or the particular

alleged wrongdoing. A Specified Person may have lied, not out of a realisation that they are

culpable of insider dealing, but out of a fear that they may have committed some other

wrongdoing, or that others would view their conduct as improper or a feeling that truth was

unlikely to be believed. It is only if such reasons for lying by a Specified Person can be

excluded that the lies of the Specified Persons can be used to confirm or support other evidence

which is indicative of their culpability of insider dealing. Then, it can be used to support an

inference of insider dealing. Before a lie of a Specified Person can be used in that way, the

Tribunal must be satisfied that the lie was deliberate and material.

Prejudice from delay

28. It is to be noted that, although the SFC began its enquiry into dealings in Meadville’s

shares prior to the Joint Announcement of Meadville and TTM on 16 November 2009, at least

as early as 19 November 2009, it did not issue the Notice to the Tribunal instituting these

proceedings until 10 September 2019. On 11 September 2019, the Tribunal directed the SFC

to serve the Notice, together with other related material, on the Specified Persons. As noted

subsequently, the Specified Persons have raised the issue of prejudice said to result to each of

them in the conduct of their cases from that passage of time. The Chairman has directed the

Tribunal that it is to consider and to take into account, if appropriate, whether or not the passage

of time, from the occurrence of the events the subject of this hearing to the serving of the Notice

on the Specified Persons, has resulted in an inability in the Specified Persons to retrieve or

collect evidence, in particular relating to what specific information was available in the market

at the relevant time. Similarly, the Tribunal is to have regard to those matters in respect of the

loss of memory of relevant events generally likely to have occurred to either or both of the

Specified Persons. In doing so, the Tribunal is to have regard to whether or not either or both

of the Specified Persons was responsible in any way for the delay in instituting these

proceedings. The Tribunal has been directed that, if it finds such prejudice to have occurred to

12

one or both of the Specified Persons, to take that into account in their favour in making its

findings and determinations.

13

CHAPTER 3

THE EVIDENCE

29. At the hearing the Tribunal received evidence in the form of documents produced by

the SFC, reflecting relevant material obtained in their enquiries, including in large part

responses in writing by persons responding to notices from the SFC to adduce documentation

or provide explanations. In addition, that material included two records of interview of each of

Mr Tang and Ms Li, conducted of the former on 18 May and 20 July 2010 and the latter on 20

April and 9 July 2010. Also, the SFC adduced into evidence two witness statements of Ms

Wong Mei Mei, a senior manager of the SFC, and three expert witness statements from Mr

Karl Lung. For their part, Mr Tang and Ms Li each provided written witness statements and

each relied on an expert witness statement produced on their behalf, by Mr Clive Rigby for Mr

Tang and by Mr Charles Li for Ms Li. The Tribunal received oral evidence from each of those

witnesses.

The factual evidence

(i) Ms Wong Mei Mei

30. Ms Wong Mei Mei testified that she was one of 24 officers of the Enforcement Division

of the SFC who were the recipients of a written ‘Direction to Investigate’ signed by Ms Karen

Ngai, the Director of Enforcement, dated 20 January 2010. It stated:

19

“I have reasonable cause to believe that during or around the period from 14 September

2009 to 17 November 2009:

(a) offences of insider dealing may have been committed in respect of dealing

in the shares of Meadville Holdings Limited, contrary to section 291 of the

Securities and Futures Ordinance (Cap. 571);

(b) persons may have engaged in insider dealing in respect of dealing in the

shares of Meadville Holdings Limited, contrary to section 270 of the

Securities and Futures Ordinance (Cap. 571).”

31. Ms Wong said that it was only after receipt of that Direction that she became involved

in the investigation

20

. However, it is apparent from the letters and Notices served by the SFC

19

HB-4, page 1784.

20

Transcript; Day 1, page 22.

14

and the returns from recipients that the SFC investigations began as early as 19 November 2009.

For example, by a letter of that date, the SFC informed Meadville that it was “conducting an

enquiry into the dealing in shares of Meadville prior to” Meadville’s Announcement, dated 16

November 2009.

21

The SFC requested that Meadville provide information as to the date on

which the terms of the transactions set out in the Announcement were determined, the date on

which the dividend distribution was first contemplated and the terms of the dividend

distribution determined, in particular who was privy to that information. In addition, it

requested Meadville to provide a timetable of events leading up to the Announcement. For its

part, Meadville responded to that request by a letter to the SFC signed by Mr Tang on behalf

of Meadville, dated 4 December 2009.

22

Inordinate and prejudicial delay

32. Those events are given particular relevance by the complaints made on behalf Mr Tang

and Mr Mak in their respective Opening Submissions filed with the Tribunal, dated 14

September 2020. For Mr Tang, Mr Yu SC contended that the “inordinate delay” in bringing

these proceedings before this Tribunal has “occasioned prejudice to Mr Tang.” The prejudice

was said to have different components: namely, the inability “to retrieve or collect evidence

relating to what precise information was available in the market” and Mr Tang’s “inevitable

loss of memory”, so that he would have difficulties in recalling “matters which could assist

him in demonstrating his innocence, and/or exonerate him from the suspicions that arise.” For

his part, Mr Mak, on behalf of Ms Li, invited the Tribunal to have regard to the “substantial

delay on the part of the SFC in commencing the present proceedings i.e. more than 10 years’

time has lapsed since Ms Li dealt in the Meadville shares and/or since the SFC initiated

investigations against Ms Li and Tang” when having regard to the resulting “prejudice and/or

unfairness caused to Ms Li.”

33. It was in those circumstances that the Tribunal requested the Presenting Officer in a

letter, dated 28 September 2020, to present evidence of the circumstances that had resulted in

the fact that, notwithstanding that the impugned events occurred in October 2009, the Notice

from the SFC to the Tribunal was served on only 10 September 2019. For her part, Ms Wong

responded on the same day by producing a chronology under the rubric “Referral of case from

21

HB-2, pages 1002-1003.

22

HB-4, pages 1042-1062.

15

SFC to DoJ”.

23

On 4 July 2011, the Enforcement Division of the SFC had sought legal advice

from the Director of Public Prosecutions. Ms Wong said that the advice sought extended

beyond the Specified Persons to “other persons”. That advice had been sought because the SFC

considered that criminal prosecutions might be brought against some of the traders.

24

Legal

advice was received by the SFC on 1 August and 13 October 2011. On 30 November 2011, the

SFC was advised that the Department of Justice was considering seeking a Production Order.

On 6 September 2012, a third legal advice was received. On 12 November 2012, legal advice

was received on the preparation of evidence. On 4 January 2013, on the instructions of the

Department of Justice, the SFC referred evidence in respect of possible money-laundering

offences to the Commercial Crimes Bureau. Within a week, the SFC expressed its concerns to

the Department of Justice of the delay in providing advice on the issue of insider dealing. In

October 2013, the Commercial Crimes Bureau completed its investigation.

34. In the years 2014, 2015, 2016 and 2017 the SFC was advised that the requested advice

was not available. The SFC was told that the counsel was busy with other matters. On 9 April

2018, the SFC received the final advice from the Department of Justice that there was

insufficient evidence to prosecute any of the traders for any offence. In August 2018, the SFC

engaged counsel to consider the possibility of commencing proceedings in this Tribunal. On

27 June 2019, the SFC sought the consent of the Department of Justice to proceed in the

Tribunal, which consent was received on 8 August 2019.

35. Ms Wong explained

25

that section 252A (1) of the Ordinance provided that the SFC

could not institute proceedings in the Tribunal unless it had obtained the consent of the

Secretary for Justice and that consent could be withheld in respect of any conduct only if and

so long as:

“(a) proceedings for an offence under Part XIV are contemplated in respect of the same

conduct; or

(b) proceedings for an indictable offence (other than an offence under Part XIV) are

contemplated, or have been instituted, in respect of the same conduct and the

23

Ms Wong’s witness statement; WMM-6, pages 16-20. Appendix 1.

24

Transcript; Day 1, page 25.

25

Transcript; Day 1, pages 29-32.

16

institution of proceedings under section 252 would be likely to cause serious

prejudice to the investigation or prosecution of that offence.”

36. In cross-examination by Mr Yu, Ms Wong said that the concerns about money-

laundering and the consideration of an application for a Production Order had nothing to do

with Mr Tang. It was her recollection that the suspicions of money laundering were in relation

to Ms Li’s accounts.

26

She agreed that on 9 January 2013 the SFC had raised concerns with the

Department of Justice about delay in the insider dealing investigation. The Direction to

investigate had been issued by the Director of Enforcement of the SFC on 20 January 2010.

Notwithstanding, the delay, consideration had not been given to applying to the Secretary for

Justice for consent to initiate proceedings in this Tribunal.

27

For her own part, she reported to

the “senior management” of the SFC with an update of progress in the case of the SFC every

three months. That was a report to a board of the Enforcement Division, including the

Executive Director of Enforcement, and consisted of a written report and an oral presentation.

There was no dispute that Mr Mark Stewart had been Executive Director of Enforcement from

25 September 2006 to 24 September 2015, after which Ms Maureen Garrett was Interim Head

of Enforcement from 24 August 2015 to 2 May 2016. Then, Mr Thomas Atkinson became

Executive Director of Enforcement on 3 May 2016 and remained in that position to date. In

cross-examination by Mr Mak, Ms Wong acknowledged that Ms Maureen Garrett was an

Assistant Presenting Officer in these proceedings.

28

37. Ms Wong said that she was unable to assist as to what action, if any, the senior

management had taken to get the Department of Justice to take action so that the matter was

not unduly delayed.

29

Section 183 (1) Notices: 10 April and 14 May 2010

38. In a consideration of the delay in commencing the proceedings, it is relevant to note

that Notices, pursuant to section 183 (1) of the Ordinance, were served on Ms Li and Mr Tang

on 12 April and 14 May 2010 respectively. Those Notices stated:

30

“You are a person under investigation.

26

Transcript; Day 1, page 80.

27

Transcript; Day 1, page 81.

28

Ms Wong's witness statement; WMM-8.

29

Transcript; Day 1, pages 83-84.

30

HB-5, page 2585. HB-6, page 2839.

17

I require you to:

• attend before me at… and answer any question relating to the matters under

investigation that I may raise with you, and

• give full assistance in connection with our investigation which you are

reasonably able to give.”

Attached to the Notices were copies of the Direction to Investigate, dated 20 January 2010,

together with copies of sections 182-5 and 187 of the Ordinance. Section 184 provides that a

failure to comply with the requirements is a criminal offence.

Provenance of the monies used to buy shares in the account of Ms Li

39. In cross-examination by Mr Yu, Ms Wong confirmed that there was no evidence of

which she was aware that the monies used by Ms Li to purchase Meadville shares, as detailed

in WMM-1, came from Mr Tang. Moreover, she agreed that the evidence showed that the bulk

of those monies certainly did not come from Mr Tang.

31

Records of telephone calls between Mr Tang and Ms Li

40. Ms Wong agreed that the half page schedule entitled “Summary of phone calls”

32

between two stipulated telephone numbers of Mr Tang and Ms Li in October 2009 was not a

complete record of telephone calls between telephones known to be used by them. Ms Wong

said it was a “Highlight”.

33

She was aware of another telephone number used by Ms Li and

acknowledged that the telephone records of telephone calls made from that telephone to Mr

Tang’s telephone described telephone calls from one to the other on 1, 4, 6, 9 and 11 October

2009.

34

She was not aware of any telephone conversation between Mr Tang and Ms Li on 23,

27 and 28 October 2009.

35

She agreed that the pattern of telephone calls between the two of

them were of calls of a short duration, generally at lunchtime or in the afternoon.

36

29 and 30 October 2009: negotiations between Meadville and TTM

41. Ms Wong acknowledged that the response by Meadville, dated 4 December 2009, to

multiple enquiries made of the company by the SFC, dated 19 November 2009, included a

31

Transcript; Day 1, page 32.

32

Ms Wong’s witness statement; WMM-3, page 3.

33

Transcript; Day 1, page 35.

34

HB-4, pages 1946-1949.

35

Transcript; Day 1, pages 40-41.

36

Transcript; Day 1, page 42.

18

schedule under the rubric, ‘Timetable of Events Leading Up to the Announcement dated 16

November 2009’. In respect of 29 October 2009, it asserted:

37

“The intended date of signing of the transaction agreements and the credit agreement

was cancelled and all relevant parties (including the banks) were informed of the

cancellation.”

42. Ms Wong said that a colleague had made the note of a telephone conversation

apparently held with Mr Joseph Wong, legal counsel of Meadville, on 11 December 2009

which noted that:

38

“He mentioned that the cancellation was mostly due to disagreement between

managements from Meadville and TTM regarding future distribution of corporate

management responsibilities and non-compete agreement… All signing parties

including bankers and lawyers were also informed. No definite signing date was

decided then.”

43. Ms Wong replied in the negative to a question from the Chairman when asked if there

was any “primary evidence-emails, letters, notes-showing that bankers and lawyers were

informed that there had been a hiccup in the signing?”

39

She said that Merrill Lynch, TTM and

UBS all provided descriptions of the events of 29 and 30 October 2009 in chronologies they

had provided to the SFC in response to similar enquiries made of them, dated 19 November

2009. Merrill Lynch said: “Meeting in Hong Kong between Meadville and TTM to discuss

transaction structure in terms.” TTM said: “TTM and Meadville meet in Hong Kong to

negotiate transaction agreements. TTM updates UBS following the discussions.” Finally, UBS

said: “TTM and Meadville meet in Hong Kong to try to negotiate transaction agreements.”

None of them had mentioned cancellation of the signing of agreements.

40

44. For her part, she had asked TTM in an email, dated 19 January 2011:

41

“According to our information, there was a plan to sign the transaction agreements in

Hong Kong between 29 and 30 October 2009 but was cancelled eventually. We would

be much obliged if you could provide the following information …

(Insert: the answers received by the SFC from TTM are in italics)

37

HB-2, page 1061.

38

HB-6, page 3056.

39

Transcript; Day 1, page 56.

40

Transcript; Day 1, pages 57-58.

41

HB-3, page 1065.

19

1) Whether there was a plan to sign at the time. If yes, why the signing

was cancelled?

The meetings in Hong Kong on Oct 29 and Oct 30 were part of the ongoing

negotiations. At the meeting we decided to pause the negotiations while both

sides assessed the situation.

2) When, where and the time that the decision about the cancellation was

made;

We paused the negotiations on the morning of Oct 30.

3) The identities of all persons who became aware of the potential for

termination.

Representing TTM were…

Representing Meadville were Tom Tang, Mai Tan (g), Canice Chung, Joseph

Wong, and Rachel Ng.”

Ms Wong acknowledged that no direct answer was received as to whether or not there was a

plan to sign at the time or as to when the problem surfaced.

42

45. It is to be noted that, for his part, in his witness statement Mr Tang said, “on 29 October

2009, TTM and MHL were scheduled to finalise the terms of the transaction agreement. The

signing of the transaction agreements was expected to occur around those two days.” He said

that, TTM having requested additional restrictive conditions on the shares held by the Tang

family, there was no immediate agreement “and we paused our negotiations.”

43

Ms Li’s dealing in Meadville shares

46. HSBC provided the SFC with a Schedule setting out Ms Li’s trading in Meadville

shares.

44

It described buying of Meadville shares on 23, 27 and 28 October 2009 and selling

those shares on 30 October and 17 November 2009. Ms Wong agreed that the column headed

“Order Placing Time (Execution Time)” in fact described the time the order was placed. She

agreed that the column headed “Remarks” in which there was described “Execution quantity”

in fact described the quantity of the order. An earlier reply from HSBC to the SFC stated of Ms

Li’s account:

45

“The modes of order placing: By Internet

42

Transcript; Day 1, page 59.

43

Mr Tang’s witness statement, paragraph 13.

44

HB-4, page 2051. Appendix 2.

45

HB-4, page 1816.

20

The types of order placing: Limit Order”

47. A Schedule, WMM-1, attached to Ms Li’s witness statement described the quantity and

price of Meadville shares acquired and sold in response to Ms Li’s orders to buy and sell.

46

It

stipulated that overall Ms Li had made a profit of $546,817.43. Ms Wong agreed that the

telephone records provided to the SFC by Smartone Mobile Communications Ltd described a

telephone call initiated from the telephone registered in Ms Li’s name to a number registered

in Mr Tang’s name at 12:44:55 on 30 October 2009.

47

It was 44 seconds in duration. HSBC

records described an order in Ms Li’s account to sell 100,000 Meadville shares at 13:13:29 on

30 October 2009, which was executed that afternoon at $2.48 per share.

48

The last trade in

Meadville shares on 30 October 2009 was a transaction involving 10,000 shares at 15:18:51

hours.

49

At the request of Meadville, trading in its shares was suspended on the SEHK at 15:19

hours that day.

50

Ms Wong agreed that clearly there was ample time available for Ms Li to

have placed other sell orders prior to suspension of trading if she had so wished.

51

31 October 2009

48. Ms Wong agreed that on the following day, 31 October 2009, both the Apple Daily

52

and the Ming Pao Daily News

53

published articles describing the plunge in the Meadville’s

share price to $2.15, on a turnover of $103 million, which represented a drop of about 23% on

the day. Ms Wong pointed out that the articles were published after Meadville shares have been

suspended the previous afternoon.

54

The Apple Daily said, “an outpouring of sell orders was

caused by a market rumour that the sell-out transaction encounters hiccups and may therefore

fall through.” The Ming Pao Daily News said, “…there have been diverse (speculations) in the

market, among which a more widely held view was that… a US-funded enterprise had made

an acquisition offer at the price of $3 per share. It was also said that the substantial shareholders

intended to privatise (the company) and then sell the entire company. However, it was said

yesterday that the US-funded buyer had decided to call off the negotiation, triggering the recent

massive sell-off by funds speculating on the notion of a sale of Meadville.”

46

Ms Wong’s witness statement, page 1. Appendix 3.

47

Transcript; Day 1, page 60. HB-4, page 1954.

48

HB-4, page 2051.

49

HB-6, page 3096.

50

HB-2, page 995; Meadville's Announcement on 30 October 2009.

51

Transcript; Day 1, page 63.

52

HB-1, pages 118-120.

53

HB-1, pages 114-117.

54

Transcript; Day 1, page 67.

21

49. In cross-examination by Mr Mak, Ms Wong agreed that the SFC had not made enquiries

of either Apple Daily or Ming Pao Daily News of the basis on which they stipulated in the

respective articles an offer price of $3 per share.

55

11 and 16 November 2009

50. Ms Wong agreed that a subsequent article in the Ming Pao Daily News on 11 November

2009 also referred to the rumour of a US-funded enterprise’s offer to acquire Meadville at $3

per share.

56

The article asserted “Financial website Infocast cited information as saying

yesterday that Meadville is currently in talks with North American PCB manufacturer TTM

Technologies over details of the merger and acquisition”.

57

She acknowledged that an article

in the Apple Daily on 16 November 2009 said that the substantial shareholder of Meadville

“may sell all of its shares to a US NASDAQ-listed industry peer TMM Technologies at $3.50

per share.”

58

Public information about Meadville

51. In her witness statements, Ms Wong described two separate searches that had been

made by the SFC to obtain public information about Meadville. Each of those searches had

been performed through Wisers’ News platform, operated by Wisers Information Ltd, which

she said maintains “a database of all major key local newspapers and magazines and hundreds

of local and regional publications” covering “newspaper publication and web news of all

regions (Mainland China, Hong Kong, Macau, Taiwan and overseas).” In cross-examination

by Mr Yu, she agreed that the searches did not cover “social media blogs or online forums”.

59

52. The first search, conducted on or around 17 November 2009, encompassed the period

30 October to 18 November 2009 and produced 43 articles. A second search conducted on 25

June 2018, encompassed the period 6 June 2008 to 17 November 2009 and produced 178

articles, although she noted that 10 of the articles found in the first search were not found in

the second search. The second search was conducted in the course of preparing instructions to

an expert witness, Mr Karl Lung, the date of 6 June 2008 was chosen to match the date at which

Meadville and TTM approached each other.

55

Transcript; Day 2, page 4.

56

Transcript; Day 1, pages 68-70.

57

HB-1, pages109-110.

58

Transcript; Day 1, page 72.

59

Transcript; Day 1, page 75.

22

Instructions to the SFC’s expert witness

53. In instructions to its expert witness, Mr Karl Lung, the SFC posed a series of questions

of him in relation to the period 23 October to 16 November 2009. The former date was the date

of Meadville’s board meeting. The instructions stated that the related board minutes described

“the proposed sale of Meadville’s principal businesses (i.e. the PCB and laminate businesses)

and the payment of a special dividend of around HK $3.40 per share to Meadville

shareholders”.

60

In cross-examination by Mr Yu, Ms Wong agreed that the minutes did not

contain a specific reference to “a special dividend of around HK $3.40 per share”. Rather, the

consideration, from which the dividend was to be distributed, was a combination of cash and

TTM shares. She agreed that the value of the final dividend depended on the price of TTM

shares at the time of completion of the transaction.

61

The Joint Announcement by Meadville

and TTM of the completion of the transaction, dated 9 April 2010, said that the proposed

distribution was the “equivalent to each Shareholder receiving a dividend of approximately HK

$3.17 for each Meadville Share.”

62

Ms Wong agreed that the closing price of TTM shares

quoted on NASDAQ fluctuated: on 6 June 2008 it was US $14.63, on 20 November 2008 it

was US $3.90; on 23 October 2009 it was US $11.19, whereas on 28 October 2009 it was US

$9.99.

63

54. Meadville’s Announcement, dated 16 November 2009, described the component parts

of the proposed distribution by way of dividend per Meadville share, namely HK $1.867 cash

and 0.0185 of a TTM share. Based on the closing price per TTM share on the last trading date

of US $11.21, it was stated that the dividend represented approximately HK $3.47 for each

Meadville share.

64

US $11.21 was the closing price of TTM shares on 13 November 2009.

55. It is to be noted that in cross-examination by Mr Duncan, Mr Tang acknowledged that

in discussions between Meadville and Merrill Lynch, on or around 2 October 2009, about the

financial modelling of the proposed dividend distribution, each party had produced a

spreadsheet,

65

from which it could be readily calculated that Meadville estimated that the

dividend would be $3.35, whereas Merrill Lynch calculated it would be $3.452.

66

60

Expert Bundle-1, page 14.

61

Transcript; Day 1, pages 89-90.

62

HB-2, page 995-4.

63

Transcript; Day 1, page 92.

64

HB-1, pages 193-194.

65

HB-3, pages 1138-1141.

66

Transcript; Day 2, pages 70-74.

23

56. Her attention having been drawn by Mr Mak to the upward movement in the price and

volume of trading in Meadville shares in the period 1 April to 14 September 2009, namely from

a daily High of $0.88 to $2.00 respectively, with only about 7 million shares traded on 19 May,

but more than 37 million and 48 million shares traded on 22 May and 3 June 2009 respectively,

Ms Wong acknowledged that, as far as she was aware, the SFC had made no enquiries as to

what accounted for the rise in price and traded volume of April shares. Similarly, she accepted

that no investigation had been made by the SFC as to whether there were leaks in that period

on the discussions regarding the transaction.

67

(ii) Mr Tang Chung Yen, Tom

57. Mr Tom Tang was the Chairman and an executive director of Meadville, which was

listed on the SEHK in 2007.

Relationship with Ms Li

58. In his witness statement, Mr Tang said that he met Ms Li for the first time in a Bar in

Macau in around 1999 or 2000. He did not wish to disclose his real identity and introduced

himself by the alias, Stephen. For her part, she said that she was called Miao Jing. He

understood that she was from Lanzhou in Gansu province. Nevertheless, they conversed with

each other in Cantonese. He kept in contact with her by telephone and then they met from time

to time. They shared a common interest in cuisine and wine.

59. In cross-examination, he said that he had always referred to her as Miao Jing and did

so even until today. He acknowledged that they enjoyed a sexual relationship. He said that he

had told her that he was married on the first occasion that they met.

68

In 2000 or 2001, she came

to live in Hong Kong and lived at different addresses in Hung Hom. Sometimes they met in a

restaurant and on other occasions at her home. In about 2003-2004, Ms Li told him that she

had a daughter. He testified that he did not come to know her name, Li Yik Shuen, until after

the first record of interview had been conducted of him by the SFC on 18 May 2010.

69

Mr Tang

denied that he was “very fond” of Ms Li, rather he was fond of her. The relationship had petered

out in about 2017-2018.

70

In their conversations, he did not ask what she did to make a living,

67

Transcript; Day 2, pages 5-8.

68

Transcript; Day 2, page 81.

69

Transcript; Day 3, pages 2-3.

70

Transcript; Day 2, pages 75-76.

24

although he knew that the monies that he provided her did not accommodate her totally. They

never discussed financial matters or the state of the stock market.

71

60. Notwithstanding their intimate relationship, Mr Tang said in his witness statement that

he “purposefully did not disclose my real name, details of my family, the name of our company,

details of my work or even my work or home address” to Ms Li. Nevertheless, Mr Tang went

on to say in his witness statement that he had explained to Ms Li that “I was in the

manufacturing business concerning electronic components and had to visit my factories in

Dongguan and Shanghai.”

72

61. Notwithstanding those statements, in his evidence-in-chief, Mr Tang said that he took

extra care to keep his personal and business life separate and that Ms Li “actually did not know

about my business or my company.”

73

In cross-examination, Mr Tang said “my business is in

the manufacture of printed circuit board and… laminates. Electronic business could be

anything.”

74

62. In cross-examination, Mr Tang was reminded that in his first record of interview,

conducted on 18 May 2010, having been asked if the person he knew as Miao Jing “know your

occupation in Hong Kong, know what business you were engaged in? Did you tell her?”, Mr

Tang had answered “I have not told her anything about my occupation, which field I am in,

who I am. All of these have never been mentioned.” When asked if the answer was truthful,

Mr Tang responded in the affirmative.

75

Money transfers to Ms Li

63. In his witness statement, Mr Tang said “since around 2001” he had helped Ms Li

financially by transferring $30,000-$50,000 by ATM or bank transfer every month or two. The

attachment to Ms Wong’s statement, WMM-2, described payments made from Mr Tang’s bank

accounts to the HSBC account of Ms Li in 2009.

76

Mr Tang was wrongly described as the

‘payee’. In fact, he made the payments and Ms Li was the recipient. There were two types of

payments: ‘ATM Transfer’ and ‘Credit as advised’. There were eight ATM Transfers of

71

Transcript; Day 2, pages 82-84.

72

Mr Tang’s witness statement, paragraph 25.

73

Transcript; Day 2, page 25.

74

Transcript; Day 2, page 82.

75

Transcript; Day 2, page 91.

76

Ms Wong's witness statement, page 2. Appendix 4.

25

$50,000 on eight different months and two transfers of $30,000 in January 2009. The ‘Credit

as advised’ transactions were for $900,000 and $50,000 respectively. In total, $1,410,000 was

transferred from Mr Tang’s bank accounts to the HSBC bank account of Ms Li in 2009.

64. In cross-examination, Mr Tang said that it was probably around 2007 that he had begun

making regular monthly payments to Ms Li in amounts of $50,000 or so. Those payments

probably continued until 2017, but he had forgotten when they stopped.

77

65. In his witness statement, Mr Tang said that in August 2009, he had issued a cheque in

favour of Li Yik Shuen in the sum of $900,000. He had done so at the request of Ms Li to help

her purchase premises in which to live. He did not ask her for any details about price or the

address of the property. She provided him with the details of the payee’s name, Li Yik Shuen.

66. In cross-examination, having regard to the name of the payee in the cheque, he said that

he did not presume that in fact she was Li Yik Shuen. He had no reason to do so. It could have

been the name of her agent, her friend or a company representative.

78

It having been pointed

out to him in cross-examination that the related deposit form did not provide any details of a

cheque, rather it referred to the transaction as a ‘Transfer’, and having been told that the SFC

had been unable to find such a cheque, Mr Tang said that he was not sure that he had made out

a cheque in the sum of $900,000 as he had stated in his witness statement. Similarly, it having

been pointed out to him that the deposit form stated that the payment of $50,000, dated 12

November 2009, made from his bank account to that of Ms Li had been made by way of

‘Transfer’ and that the name Li Yik Shuen was printed on the form, Mr Tang said that he was

“pretty sure” that he had received copies of the form when he undertook the payment. He

acknowledged that it was obvious that the recipient was Li Yik Shuen. Nonetheless, he denied

the suggestion that he knew that to be her name by that date.

79

67. In re-examination, he said, “I believe at that time I went to the bank and gave the teller

an account number that I would like to transfer $900,000 into that account.” He said that was

“probably because I didn’t want to give her a cheque.” Finally, he said that he gave that

testimony “because there’s only two ways, right, either cheque or counter, right?”.

80

He agreed

77

Transcript; Day 2, page 77.

78

Transcript; Day 3, pages 3-4.

79

Transcript; Day 3, pages 7-8.

80

Transcript; Day 3, pages 31-33.

26

with Mr Yu’s suggestion that he had no independent memory of how the money was advanced.

Similarly, he agreed that if he had not been shown the deposit form in respect of the transfer of

$50,000 to Ms Li’s account on 12 November 2009, he had no recollection of the transaction at

all.

68. In the second record of interview conducted of him by the SFC, Mr Tang was asked

how much money he had provided Ms Li in 2009. He replied, “the year 09-into account, that

should be about $400,000. Yes, I guess that there was $400,000, $300,000-$400,000.”

81

Having informed the SFC that Ms Li had recently bought the premises at which she lived in

Hung Hom, Mr Tang was asked, “Did you give her money for buying it?” Mr Tang replied,

“…she asked me verbally to lend, lend her a sum of money, but the amount was very small,

that is, of course, it was not in the amount of that 1 million odd that you are talking about. A

small amount of money was lent to make up the shortfall.” Having been told that it was

necessary that he disclose the actual amount of money, Mr Tang said “it was 900,000”. In

cross-examination, Mr Duncan suggested to Mr Tang that in describing the amount of money

as “very small” Mr Tang was not providing a truthful answer to the SFC. For his part, Mr Tang

asserted that his answer was truthful, explaining “the answer in reference to is did I give her

several million dollars to invest in securities, that was coming way before in the interviews.”

In re-examination, Mr Tang explained the context of his answer as being, “the question before

was trying to find out whether I lent or gave her money for security investments, equity

investments, stock investments.” He said that when he mentioned “1 million-odd, I think it’s

the 5 million-odd, I think it’s a slip of tongue.” That was a reference to the $5 million that Ms

Li had spent in buying Meadville shares.

82

Counselling or procuring Ms Li to deal in Meadville shares and/or disclosing relevant

information to Ms Li

69. In his evidence-in-chief, Mr Tang denied the allegation made in paragraph 21 of the

Notice, namely that knowing that he was possessed of relevant information in relation to

Meadville, in particular that it was proposed that it sell its principal businesses and that there

would be the payment of a dividend of about HK $3.50 per share to Meadville shareholders,

which information was not generally known to the persons who were accustomed or would

have been likely to deal in Meadville shares until Meadville’s Announcement on 16 November

81

HB-6, pages 3004-3005, counter #s 126-131.

82

Transcript; Day 3, pages 29-31.

27

2009, he had counselled or procured Ms Li to deal in Meadville’s shares, knowing or having

reasonable cause to believe that she would deal in them; and/or that he had knowingly disclosed

that relevant information directly or indirectly to Ms Li, knowing or having reasonable cause

to believe that she would make use of it for the purpose of dealing in Meadville’s shares. That

denial resonated with his response to the SFC in his second record of interview, conducted on

20 July 2010, when asked if he had disclosed to Ms Li “the contents of Meadville’s

announcement in November”, namely “Of course not.”

83

70. In his evidence-in-chief, Mr Tang explained:

84

“Mr Chairman, this is actually rather easy to answer. Number one, I've been sitting on

a listed company for a certain number of years, and I do know this is illegal. I do know

this is a criminal offence, so I will not do it.

Number two, Miao Jing, which you guys refer to as "Ms Li", and I has a relationship

of which I took extra care and extra awareness to keep my personal life and business

life separate. So Miao Jing actually did not know about my business or my company.

Actually, I never really -- I never told her my real name.

Number three, I was -- if I were to somehow benefit Miao Jing, I just need to give her

money. There is no need for me to give her a tip.

And number four, at that time, when the allegation was said, I did not know the final

price, the transaction price of this TTM/Meadville Holdings deal because part of the

consideration was going to be in TTM shares, and TTM shares may fluctuate.”

71. In his witness statement, Mr Tang said that, until he was informed by the SFC in mid-

2010, he was completely unaware that Ms Li had bought Meadville shares in the period 23 to

28 October 2009.

85

That statement resonated with Mr Tang’s answer to the SFC in his second

record of interview.

86

He said that he was unaware that Ms Li traded in any listed shares.

87

Similarly, he was unaware that she had sold some Meadville shares on 30 October and 17

November 2009. Further, he did not know, and was surprised to learn from the SFC, that she

possessed $5.9 million, which monies she had used to buy those Meadville shares.

88

72. At the conclusion of cross-examination, having regard to his pecuniary generosity to

Ms Li, Mr Duncan asked Mr Tang if his generosity to Ms Li extended “to providing her with

83

HB-6; page 3006, counter #156-157.

84

Transcript; Day 2, pages 25-26.

85

Mr Tang's witness statement, paragraph 38.

86

HB-6, page 3007, counter #s 162-165.

87

Mr Tang's witness statement, paragraph 45.

88

Mr Tang's witness statement, paragraph 41.

28

information about the proposed sale by MHL of its businesses.” Mr Tang denied that had

happened.

89

Leakage of information in relation to Meadville

73. In his witness statement, Mr Tang said “I do not exclude the possibility of information

leakage in relation to MHL in around October 2009, prior to the announcement of the PCB

Sale and the Laminate Sale.”

90

Earlier in that statement, he had adverted to the conduct of

formal due diligence from “around August to September 2009”. Of that, he said, “As part of

TTM’s due diligence on the operations and supply aspects of the PCB business of MHL, TTM

sent their representatives to various factories and sites of MHL businesses, including our major

factory in Dongguan, Guangzhou, which was one of the biggest factories in the region.” Of the

manner in which due diligence had been conducted, he said “…the representatives, most of

whom were foreigners, along with their translators and assistant staff, talked with the local

general managers and could be seen to be walking around the Dongguan premises.”

91

Of that,

he said “I suspect that it would not be difficult for the locals of Dongguan to speculate that

there could be a major acquisition to be made on MHL.”

92

74. Mr Tang said that in around late September 2009 he and other representatives of

Meadville had flown to Washington DC to attend a preliminary meeting with CFIUS.

93

He was

in the United States for about five days.

94

The Timetable of Events provided to the SFC by

Meadville described the meeting as having been attended by representatives of both Meadville

and TTM and having occurred on 22 September 2009.

95

75. On 2 October 2009, representatives of Merrill Lynch, Meadville’s financial adviser,

met representatives of Meadville “to discuss the financial modelling of the dividend

distribution.”

96

Merrill Lynch and Meadville each produced a spreadsheet, dated 1 October

2009, addressing the financial modelling of the proposed dividend distribution to Meadville

shareholders.

97

In examination by Mr Duncan, Mr Tang agreed that it could be readily

89

Transcript; Day 3, page 15.

90

Mr Tang's witness statement, paragraph 43.

91

Mr Tang's witness statement, paragraph 10.

92

Mr Tang’s witness statement, paragraph 44.

93

Committee on Foreign Investment in the United States.

94

Mr Tang's witness statement, paragraph 11.

95

HB-2, page 1060.

96

HB-2, page 1060.

97

HB-3, page 1072 and pages 1138-1141.

29

calculated from the spreadsheets that Meadville estimated that the dividend would be $3.35 per

Meadville share, whereas Merrill Lynch calculated it would be $3.452 per share.

98

76. On 3 October 2009, Meadville’s lawyers received draft transaction agreements from

TTM’s lawyers. On 8 October 2009, negotiations between the respective lawyers began on the

terms of the agreements.

99