UNDERSTANDING CANADIAN PUBLIC

SECTOR FINANCIAL STATEMENTS

www.bcauditor.com

June 2014

Who Will Find this Guide Helpful 3

What a Set of Public Sector

Financial Statements Includes

5

The Statement of Financial Position 9

The Statement of Operations 14

The Statement of Remeasurement Gains and Losses 19

The Statement of Cash Flow 23

The Statement of Change in Net Debt 26

Financial Statement Note Disclosures 29

The Importance of the Financial

Statement Discussion and Analysis

33

The Importance of the Independent

Auditor’s Report

35

Appendix A:

Why the public sector has different

accounting standards than the private sector

39

Appendix B:

How the standard-setting process in Canada

results in high-quality public sector

accounting standards

41

TABLE OF CONTENTS

WHO WILL FIND THIS GUIDE HELPFUL

All Canadian public sector entities – federal, provincial

and local governments, as well as most organizations controlled by them – prepare

nancial statements. e majority of those statements are prepared according to public

sector accounting standards adopted across Canada.

Public sector nancial statements are read and used by a broad group of readers such

as elected legislators and councillors, board members, credit rating agencies, and other

interested members of the public. As a result, public sector nancial statements must

meet the needs of a broad range of users.

e purpose of this guide is to help all these readers – and specically those who are

not familiar with public sector nancial statements – improve their ability to review

and interpret government nancial reports. e guide describes the unique aspects

of nancial performance and accountability that one can nd when the nancial

statements are prepared in accordance with the CPA Canada Public Sector Accounting

(PSA) Handbook. Aer reading this guide you should have a general understanding of

the following:

What is included in a set of public sector nancial statements;

e key measures of public sector nancial position and performance;

Why reading the notes to the nancial statements is important;

How nancial statement discussion and analysis from management supplements

the audited nancial statements; and

Why the independent auditor’s report should be read before using the nancial

statements.

You may nd it useful to have this guidance at hand when reviewing a set of public

sector nancial statements.

We have also provided in each section questions you should consider asking when

reviewing a set of nancial statements. is does not include all possible questions but

provides a starting point for questions to ask.

Why does the public

sector have dierent

accounting standards than

the private sector? To nd

out, see Appendix A.

How has the standard-

seing process in Canada

resulted in high-quality

public sector accounting

standards? To nd out, see

Appendix B.

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

3

SCOPE OF THE GUIDE

is guide describes the nancial statements of public sector entities that prepare their

nancial statements using the CPA Canada Public Sector Accounting Handbook issued by

the Public Sector Accounting Board.

e guide does not cover the nancial reporting requirements of: government business

enterprises,

1

organizations that have opted to apply the standards applicable for

business enterprises, or government not-for-prot organizations that have opted to

follow the not-for-prot standards set out in the Public Sector Accounting Handbook.

is guide reects Canadian public sector accounting standards at the date of

publication; however, accounting standards change frequently. e guidance provided

here is a basic summary of Canadian public sector nancial reporting and should not

be relied on as accounting advice.

1 The Public Sector Accounting Handbook directs government business enterprises to adopt the accounting

standards for publicly accountable enterprises in Part I of the CPA Canada Public Sector Handbook –

Accounting (2014). The standards contained in Part 1 are the International Financial Reporting Standards

(IFRS) set globally by the International Federation of Accountants.

WHO WILL FIND THIS GUIDE HELPFUL

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

4

Canada’s public sector accounting standards aim to ensure

that a public entity’s nancial statements:

account for the full nature and extent of the nancial aairs and resources that

the entity controls;

show the entity’s nancial position at the end of the scal period, so the entity’s

ability to nance its activities and provide future services can be evaluated;

describe the entity’s change in nancial position during the scal period; and

demonstrate the entity’s accountability for the management of the resources,

obligations and nancial aairs for which it is responsible.

is means that nancial statements should provide readers with a clear understanding

of the assets, liabilities, revenues and expenses of the entity in question. Public sector

nancial statements are prepared using the accrual basis of accounting. is method

records transactions and their eect when they occur, which is oen in a dierent

period than when the associated cash exchanges to sele the transaction.

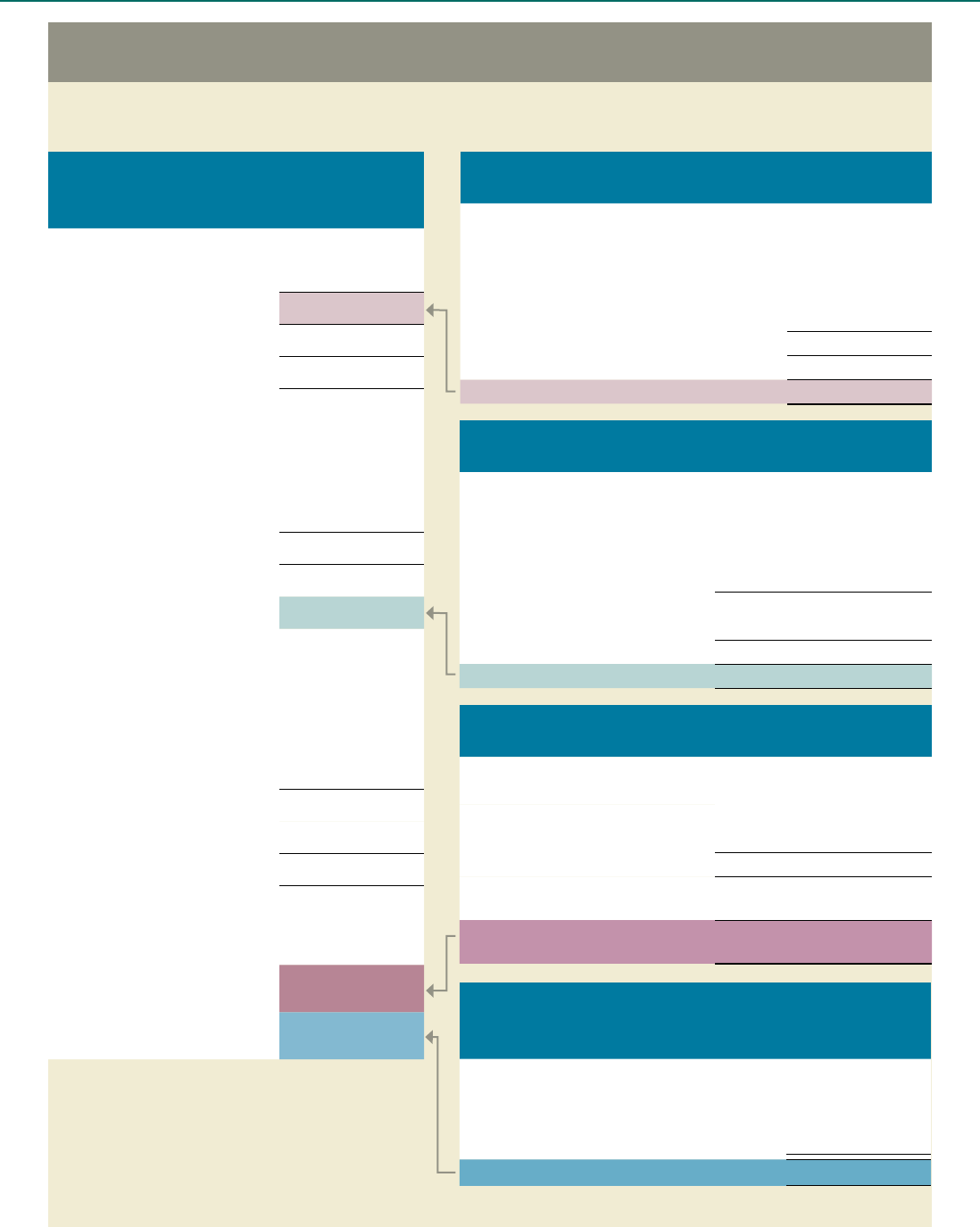

FIVE SEPARATE STATEMENTS MAKE

UP A FULL SET OF FINANCIAL

STATEMENTS

e ve separate nancial statements, shown in Exhibit 1, are described briey below

and in more detail in the pages that follow.

1. Statement of Financial Position – is is the overarching

statement that summarizes an entity’s nancial position at a point in time. Changes

in the nancial position of the entity are summarized in the following four

statements.

2. Statement of Operations – is statement explains the change in

the overall nancial position of the entity during the accounting period except for

those changes reported separately in the Statement of Remeasurement Gains and

Losses.

3. Statement of Remeasurement Gains and Losses

is statement explains the change in the overall nancial position of the entity

during the accounting period due to remeasurements related to unrealized gains

and losses on specic nancial assets and liabilities recorded at fair value, and

unrealized foreign exchange gains and losses.

2

4. Statement of Cash Flow – is statement explains the change in

cash and cash equivalents from the prior year and provides important information

about the entity’s ability to generate cash to meet its cash requirements.

5. Statement of Change in Net Debt – is statement reconciles

the change in net debt for the current and prior year. Net debt is a nancial

performance measure unique to public sector nancial reporting and is explained in

the next section.

2 Governments are not required to present this statement until fiscal periods beginning on or after April

1, 2016. Some government organizations are now required to report remeasurement gains and losses;

however, as many do not have such transactions to report this statement is often not included.

WHAT A SET OF PUBLIC SECTOR

FINANCIAL STATEMENTS INCLUDES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

5

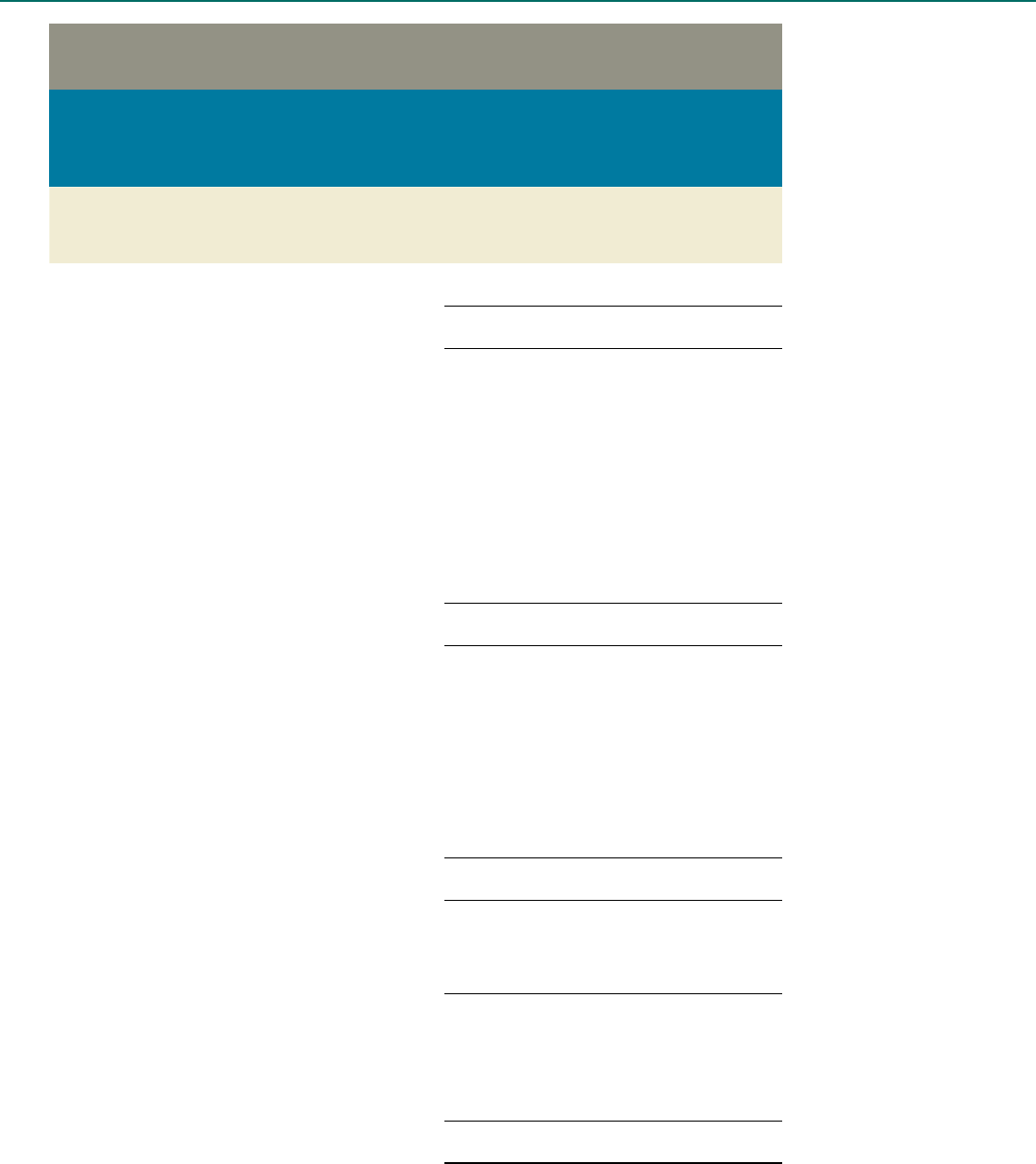

Exhibit 1: How the Statement of Financial Position links to the other financial statements

Note: these are simplified statements for illustration and do not include all the categories required by the public sector accounting standards.

WHAT A SET OF PUBLIC SECTOR

FINANCIAL STATEMENTS INCLUDES

PUBLIC SECTOR ENTITY

Statement of Financial Position

- As at March 31, 2014

2014 2013

Financial Assets

Cash and cash equivalents XXX XXX

Accounts receivable XXX XXX

Total Financial Assets XXX XXX

Liabilities

Accounts payable and acrued

liabilities

XXX XXX

Debt XXX XXX

Total Liabilities XXX XXX

Net nancial assets (debt) XXX XXX

Non-Financial Assets

Tangible capital assets XXX XXX

Inventories of supplies XXX XXX

Total Non-nancial Assets XXX XXX

Accumulated surplus (decit) XXX XXX

Accumulated surplus (decit)

is comprised of:

Accumulated operating surplus

(decit)

XXX XXX

Accumulated remeasurement gains

(losses)

XXX XXX

PUBLIC SECTOR ENTITY

Statement of Cash Flow - For the year ended March 31, 2014

2014 2013

Operating Transactions XXX XXX

Capital Transactions XXX XXX

Investing Transactions XXX XXX

Financing Transactions XXX XXX

Increase in cash and cash equivalents XXX XXX

Cash and cash equivalents at beginning of year XXX XXX

Cash and cash equivalents at end of year XXX XXX

PUBLIC SECTOR ENTITY

Statement of Net Debt - For the year ended March 31, 2014

Budget

2014

Actual

2014

Actual

2013

Annual operating surplus XXX XXX XXX

Acquisition of tangible capital assets (XXX) (XXX) (XXX)

Amortization of tangible capital assets XXX XXX XXX

Changes in other non nancial assets XXX XXX XXX

(Increase)/decrease in net debt XXX XXX XXX

Net debt at beginning of year XXX XXX XXX

Net debt at end of year XXX XXX XXX

PUBLIC SECTOR ENTITY

Statement of Operations - For the year ended March 31, 2014

Budget

2014

Actual

2014

Actual

2013

REVENUES XXX XXX XXX

EXPENSES XXX XXX XXX

Operating Surplus (Decit) XXX XXX XXX

Accumulated operating surplus (decit) at

beginning of year

XXX XXX XXX

Accumulated operating surplus (decit) at

end of year

XXX XXX XXX

PUBLIC SECTOR ENTITY

Statement of Remeasurement Gains and Losses -

For the year ended March 31, 2014

2014 2013

Accumulated remeasurement gains (losses)

at beginning of year

XXX XXX

Net remeasurement gains (losses) XXX XXX

Accumulated remeasurement gains (losses) at end of year XXX XXX

Statement of Financial Position Statements Explaining Changes in

Financial Position

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

6

WHAT THE FINANCIAL STATEMENTS

REVEAL ABOUT FINANCIAL

PERFORMANCE AND ACCOUNTABILITY

e nancial statements tell the nancial performance story for the current and prior

scal periods. Exhibit 2 summarizes the nancial performance measures, or indicators,

presented on each nancial statement.

3

THE IMPORTANCE OF THE NOTES TO

FINANCIAL STATEMENTS

Supporting the ve nancial statements are the explanatory notes that go along with

them. ese notes (referenced on each applicable statement) provide expanded

disclosures on the reported amounts. An entity’s reported nancial results cannot be

fully understood without reading the notes to the nancial statements.

3 Governments are not required to present this statement until fiscal periods beginning on or after April 1,

2016. Some government organizations are now required to report remeasurement gains and losses; however,

as many do not have such transactions to report this statement is often not included.

Exhibit 2: Performance and accountability measures by financial statement

Financial

performance &

accountability

measures

Statement

of Financial

Position

Statement of

Operations

Statement of

Remeasurement

Gains and

Losses

3

Statement of

Cash Flow

Statement of

Change in Net

Debt

Net nancial assets

or debt

Accumulated surplus

or decit

Budget to actual

comparisons

Annual operating

surplus or decit

Net remeasurement

gains or losses

Cash ow by activity

WHAT A SET OF PUBLIC SECTOR

FINANCIAL STATEMENTS INCLUDES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

7

QUALITATIVE CHARACTERISTICS

OF PUBLIC SECTOR FINANCIAL

STATEMENTS

To eectively communicate nancial information, nancial statements must go beyond

the numbers. To do this, nancial statements must also meet the following qualitative

characteristics:

Timely – For the information to be useful, the nancial statements should be

published as soon as possible aer the annual reporting period. e value of the

information for decision making or accountability purposes decreases over time.

Comparable – Financial statements must show results on a consistent basis to

enable readers to compare the current and prior periods and make assessments on

whether the entity’s nancial position is improving or deteriorating.

Reliable – e information presented in nancial statements must be accurate and

complete if it is to be seen as reliable. In the public sector, nancial statements are

normally audited by an independent auditor to provide assurance for readers that

the information is reliable. e last section of this guide discusses the information

communicated by an auditor’s report.

Understandable – e information in the nancial statements must be clearly

presented and explained so that readers with a reasonable interest in interpreting

what the information means can understand it.

WHAT A SET OF PUBLIC SECTOR

FINANCIAL STATEMENTS INCLUDES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

8

The Statement of Financial Position presents an entity’s

nancial assets and liabilities at a point in time. e statement layout provides two

key performance measures of the entity’s ability to nance its operations and provide

future services.

e main sections of this statement are described below along with an explanation of

how the unique presentation of assets within the statement generates the two nancial

position performance measures. Exhibit 3 is a sample statement of nancial position

for your reference as you read this section.

FINANCIAL ASSETS

Financial assets are the nancial resources an entity controls and can use to pay what it

owes to others. ese assets include cash, accounts receivable, investments, and assets

that are convertible to cash or that generate cash so that the entity can pay its liabilities

as they come due.

Information about the liquidity of an entity’s nancial assets is not presented on the

Statement of Financial Position. (Liquidity means how quickly assets can be used to

pay bills.) However, the notes to the nancial statements include disclosures on the

liquidity of an entity’s nancial assets.

LIABILITIES

Liabilities are existing nancial obligations to outside parties at the date of the nancial

statements. ey result from past transactions and events and will lead to the future

sacrice of economic benets (e.g., nancial assets).

Common liabilities are accounts payable, debt, employee pension obligations, and

unearned revenue. Users should also read the notes to the nancial statements to beer

understand the nature of an entity’s liabilities and when liabilities are due.

FINANCIAL PERFORMANCE MEASURE:

NET DEBT OR NET FINANCIAL ASSETS

Net debt is a term unique to public sector nancial reporting. It is the dierence

between an entity’s nancial assets and liabilities at a point in time. is performance

measure provides readers with important information regarding the entity’s

requirement to generate future revenues to fund past services and transactions.

THE STATEMENT OF FINANCIAL POSITION

Statement of Financial

Position: nancial

statement elements

• assets (nancial and

non-nancial)

• liabilities

Financial accountability

and performance

measures

• net debt or net nancial

assets

• accumulated surplus or

decit

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

9

Financial assets are the resources available to sele an entity’s liabilities to external

parties. When liabilities exceed nancial assets, an entity is in a net debt position.

Entities in a net debt position must generate future revenues to cover the cost of past

transactions and events. e reverse is true when an entity is in a net nancial asset

position (nancial assets exceed liabilities). Entities in a net nancial asset position

have sucient nancial assets to sele existing liabilities.

To understand how an entity’s net debt (or net nancial asset) position has changed,

users should read the statement of change in net debt.

NON-FINANCIAL ASSETS

Non-nancial assets are assets that an entity will use up when providing future services to the

public. ese assets are not normally used by an entity to sele its liabilities with external

parties. As a result, they are shown separately in the Statement of Financial Position.

Oen, the most signicant group of assets within this category are tangible capital

assets, like buildings or roads, which are acquired to provide services over many years.

As entities deliver services, the estimated portion of the assets used is recorded as

an expense in the Statement of Operations. e balance presented represents the

remaining service potential of the non-nancial assets.

Crown lands and natural resources inherited in right of crown and all intangible

assets are not recognized as assets in public sector nancial statements. When these

assets are important to an entity’s ability to generate revenues or deliver services,

additional information should be included in either the notes to the nancial

statements or in the nancial statement discussion and analysis accompanying the

nancial statements.

FINANCIAL PERFORMANCE MEASURE:

ACCUMULATED SURPLUS OR DEFICIT

e accumulated surplus or decit represents the net recognized economic resources

(all assets and liabilities) of the entity at the date of the nancial statements. is

measure provides the net economic position of the entity from all years operations at a

point in time.

e accumulated surplus or decit is comprised of all of the past :

operating surpluses or decits; and

remeasurement gains and losses.

When total assets exceed total liabilities, the entity is in an accumulated surplus

position. An accumulated surplus position means that the entity has net positive

resources that, subject to direction of the government or governing board, could be

used to provide future services. However, when an entity is in an accumulated decit

position (total liabilities exceed total assets), the entity must fund past transactions

and events from future revenues. An accumulated operating decit position means the

entity has borrowed to nance annual operating decits.

THE STATEMENT OF FINANCIAL POSITION

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

10

As noted in Exhibit 1, the statement of operations and statement of remeasurement

gains and losses provides information explaining the change in the accumulated surplus

or decit position of the entity over the past two scal years.

PUBLIC SECTOR ENTITY

Statement of Financial Position

As at March 31, 2014

Note 2014 2013

FINANCIAL ASSETS

Cash and cash equivalents 2 1,908 1,573

Accounts receivable 3 1,864 1,708

Portfolio investments 4 2,254 1,331

Derivatives 5 35 -

Loans 6 4,909 5,659

Inventories for resale 7 109 135

Total Financial Assets 11, 0 7 9 10,406

LIABILITIES

Accounts payable and accrued liabilities 8 2,383 2,644

Derivatives 9 10 105

Debt 10 9,398 9,796

Pension obligation 11 4,813 4,890

Other accrued liabilities 12 1,395 1,510

Deferred revenue 13 308 331

Total Liabililies 18,307 19,276

Net nancial assets (debt) 14 (7,228) (8,870)

NON-FINANCIAL ASSETS

Tangible capital assets 15 7,218 7,215

Inventories of supplies 16 112 222

Prepaid expenses 17 30 20

Total Non-nancial Assets 7,360 7,457

Accumulated surplus (decit) 18 132 (1,413)

Accumulated surplus (decit) is comprised of :

Accumulated operating surplus (decit) 10 (1,366)

Accumulated remeasurement gains (losses) 122 (47)

132 (1,413)

e accompanying notes are an integral part of these nancial statements.

Exhibit 3: Sample Statement of Financial Position

Source: Adapted from the CPA Canada Public Sector Accounting Handbook

THE STATEMENT OF FINANCIAL POSITION

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

11

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING A STATEMENT OF

FINANCIAL POSITION – AND HOW TO

FIND THE ANSWERS

1. Is the net debt or net financial asset position of

the entity increasing or decreasing?

is performance measure shows the extent to which sucient nancial assets exist

to discharge liabilities. When assessing trends in the net debt or net nancial asset

position, readers should look to the Statement of Change in Net Debt to identify the

key components of the current trends. Increases or decreases may indicate that:

signicant tangible capital assets have been added (net debt increasing), or the entity

has not fully replaced consumed tangible capital assets (net debt decreasing); or

debt nancing is being used to fund operations (net debt increasing), or current

year revenues exceed operating expenses (net debt decreasing).

e strength of the net nancial asset position (or weakness of the net debt position)

is determined by the ratio of nancial assets to liabilities. When nancial assets

signicantly exceed liabilities the entity will be in a strong net nancial asset position.

However, when liabilities signicantly exceed nancial assets the entity will be in a

weak nancial position. A trend of increasing net debt or decreasing net nancial assets

may indicate that current operations are unsustainable.

e ratio of nancial assets to liabilities is one of the sustainability indicators published

by the Public Sector Accounting Board (PSAB) in Statement of Recommended Practice

(SORP) 4 – indicators of nancial condition. SORP 4 provides guidance to entity’s when

reporting supplementary information on the nancial condition of the entity including

possible sustainability, exibility and vulnerability indicators.

2. Is the accumulated surplus or deficit of the entity

increasing or decreasing, and how strong is the

overall financial position of the entity?

It is important to understand the balance between the entity’s historic revenue generation

and its service delivery. is means looking at current trends to see whether the nancial

position (the accumulated surplus or decit) is increasing or decreasing, as well as the

overall strength of the nancial position in which these results occurred. An entity in

a strong accumulated surplus position may be able to incur annual decits for a longer

period of time than an entity in a weaker nancial position (i.e., accumulated decit

position). e strength or weakness of the accumulated surplus or decit position is

determined by the ratio of assets (nancial and non-nancial) to liabilities. e ratio of

assets to liabilities is one of the sustainability nancial condition indicators recommended

in SORP 4.

THE STATEMENT OF FINANCIAL POSITION

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

12

3. What investment has the entity made in tangible

capital assets for providing future services?

e type of services a public sector entity provides determines the extent to which it

must invest in and maintain tangible capital assets. Some services depend heavily on

long-life tangible capital assets such as sewer and water infrastructure; other services

do not. It is important to rst understand the nature of what services an entity provides

before conclusions can be drawn on an entity’s investment in tangible capital assets.

Considerations when looking at an entity’s tangible capital assets include:

What type and mix of tangible capital assets has the entity acquired (this

information is disclosed in the notes)?

Is the entity acquiring sucient assets (purchases) to replace those that have been

consumed in service delivery (amortization expense)?

What level of resources is the entity spending on maintaining capital assets? (this

may be disclosed in the notes)

To what extent is the entity securing the use of capital assets through operating leases

or other arrangements to supplement the capital asset stock acquired by the entity?

(this information is disclosed in the notes)

e nancial statements can not provide all of the information necessary for making

assessments on the eective management of tangible capital assets. However, the

nancial statements do provide basic information on tangible capital asset purchases,

disposals, estimated service potential and current period usage through amortization,

as well as resources the entity has expended for maintenance of the tangible capital

asset stock.

PSAB has also developed a statement of recommended practice (SORP – 3 Assessment

of tangible capital assets) to assist public sector entities with reporting more detailed

information on tangible capital assets to supplement the basic information contained in

the nancial statements. is includes information on the nature and extent of tangible

capital assets, the condition of assets and the estimated remaining useful life.

THE STATEMENT OF FINANCIAL POSITION

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

13

The Statement of Operations is one of the nancial statements

prepared to explain the changes in the overall nancial position of the entity during the

accounting period. is statement explains the change in the accumulated surplus or

decit from the prior year except changes due to remeasurement gains or losses. Exhibit 4

shows a sample Statement of Operations for your reference as you read this section.

e nancial elements in the Statement of Operations include revenues and expenses.

e performance and accountability measures are the annual surplus or decit and the

comparison of budgeted to actual results.

REVENUES

Revenues are increases in economic resources that result from the entity’s operations,

transactions and events during the accounting period. Revenues result from decreases

in liabilities or increases in assets. Common revenues include:

taxation revenue, such as income or property tax;

transfers from governments, such as federal equalization payments to the provinces

and contributions from a provincial government to service delivery organizations

such as hospitals;

investment income; and

revenues from the sale of goods and services.

EXPENSES

Expenses are decreases in economic resources that result from the entity’s operations,

transactions and events during the accounting period. Expenses result from decreases

to assets or increases in liabilities.

e Statement of Operations presents expenses by function or program, such as health or

education. is presentation conveys the entity’s nancial resource allocation decisions.

e notes to the nancial statements contain additional information on the classication

of expenses by type. For example, amortization expense represents the portion of tangible

capital assets consumed during the year and is disclosed in the notes.

Statement of

Operations: nancial

statement elements

• revenues

• expenses

Financial performance

and accountability

measures

• annual operating surplus

or decit

• budget to actual results

THE STATEMENT OF OPERATIONS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

14

FINANCIAL PERFORMANCE MEASURE:

ANNUAL OPERATING SURPLUS OR

DEFICIT

e annual operating surplus or decit shows whether the revenues raised in the year

were sucient to cover the year’s operating expenses and consequently, whether the

nancial position improved, was unchanged or declined during the year. is measure

explains the overall change in nancial position for entities that do not prepare a

Statement of Remeasurement Gains and Losses.

e impact of an entity’s annual operating surplus or decit must be viewed in the

context of the entity’s overall nancial position. An entity in a strong nancial position

is beer positioned to absorb the impact of annual operating decits than an entity in a

weak nancial position. is makes it important to look at the annual operating surplus

or decit trends over time.

FINANCIAL ACCOUNTABILITY –

BUDGET TO ACTUAL RESULTS

Annual budgets approved by elected ocials and boards convey the nancial policy

and resource decisions for the entity in question. As a result, a key component of

nancial accountability in the public sector is comparing the actual nancial results

with the originally planned results in the budget.

To achieve this reporting objective, the Statement of Operations includes an entity’s

original approved annual budget. is is a unique requirement of public sector nancial

statements. By reporting the budget, you can see how the entity’s revenues and

expenses compared against the original plan.

THE STATEMENT OF OPERATIONS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

15

PUBLIC SECTOR ENTITY

Statement of Operations

For the year ended March 31, 2014

Budget

2014

Actual

2014

Actual

2013

REVENUE (Note 19)

Personal income tax 5,392 5,969 5,655

Corporate taxes 2,642 2,659 3,848

Sales and other taxes 2,080 2,296 2,431

Health and insurance premiums 641 680 652

Fees, permits, licenses and nes 581 651 669

Other revenue 1,237 2,122 1,669

Investment income 409 610 747

Canada health and social transfer 940 970 903

Other transfers 355 365 280

14,277 16,322 16,854

EXPENSE (Note 20)

Education 4,329 4,287 4,168

Health 4,541 4,626 4,457

Agriculture, environment, development 1,706 1,856 1,740

Social services 1,654 1,701 1,709

Transportation and utilites 626 823 807

Recreation and culture 281 272 217

General government 551 627 560

Justice 468 487 462

Interest expense 93 267 183

14,249 14,946 14,303

Operating Surplus (Decit) 28 1,376 2,551

Accumulated operating surplus (decit)

at beginning of year

(1,366) (1,366) (3,917)

Accumulated operating surplus (decit)

at end of year

(1,338) 10 (1,366)

Exhibit 4: Sample Statement of Operations

Source: Adapted from the CPA Canada Public Sector Accounting Handbook

THE STATEMENT OF OPERATIONS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

16

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING A STATEMENT OF

OPERATIONS – AND HOW TO FIND

THE ANSWERS

1. How did the entity’s actual results for revenues

and expenses compare with its approved financial

plan and prior year results?

Comparing planned results with actual results is useful for assessing whether or not the

entity met the nancial objectives set at the beginning of the year. Signicant variances

between planned and actual results may be indicators of:

changes to program oerings or program delivery;

delayed or accelerated program implementation; or

unplanned funding contributions or events.

When signicant variances between planned and actual results occur, the notes

may provide some information. However, readers should nd the rationale for

signicant variances in the unaudited nancial statement discussion and analysis from

management, aached to the nancial statements.

Similar variances and trends may also be observed between current and prior period results.

2. Did the entity raise sufficient annual revenues to

cover annual operating expenses?

One of the primary nancial performance measures is the annual operating surplus

or decit. An entity’s overall nancial position improves with annual surpluses and

declines with annual decits.

Readers should rst consider the trend of the current and prior year results within the

context of the accumulated surplus or decit presented in the Statement of Financial

Position. en they should assess whether the position is improving or deteriorating.

Questions to ask include:

Is the entity consistently generating annual surpluses or decits?

How signicant are the annual surpluses or decits incurred?

Is the overall nancial position (i.e., accumulated surplus or decit) improving or

deteriorating over time?

THE STATEMENT OF OPERATIONS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

17

3. How dependent is the entity on transfers from

other governments or organizations to meet its

operating costs?

An entity may be highly dependent on transfers of resources from governments or

other entities in order to deliver services. Readers should consider how eectively the

entity could respond if those transfers were reduced. Would the entity be able to:

raise additional revenues from its own revenue generating activities such as taxation

or fees?

obtain debt nancing to nance unexpected annual decits?

reduce operating expenses to match potential revenue reductions?

e nancial statement notes will provide some detail on the xed future expenses and

payments the entity cannot avoid, such as debt payments, and contractual obligations.

4. How is the entity allocating resources to the

functions or programs it is accountable for?

e entity conveys its nancial priorities through the planned and actual service costs

presented in the Statement of Operations. Based on their policy decisions, entities

will allocate more or fewer resources to a specic function or purpose. By analyzing

this information, readers can identify changes in nancial priorities. is information

can also be a starting point for asking if the entity is allocating the right amount of

resources to specic functions or programs.

5. Was the annual operating surplus or deficit

impacted by unusual or non-recurring transactions?

When assessing the nancial performance of an entity, it is important to understand

the impact of non-recurring events or non-routine transactions on the nancial results

presented. ese transactions do not create ongoing revenues or expenses for the

entity. erefore, in analyzing the entity’s performance, a reader must consider the

impact of these transactions.

For example, an entity might sell a signicant tangible capital asset and realize a large

gain (revenue) in the current year. is is a one-time revenue source that will not occur

in future periods. e reader should therefore assess what the annual surplus or decit

would have been had this transaction not occurred. If the revenue from this sale was

necessary for an annual operating surplus to occur, the entity may need to generate new

revenue sources to cover future operating expenses.

THE STATEMENT OF OPERATIONS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

18

PSAB approved new accounting standards in 2011

4

that

introduced the new statement of remeasurement gains and losses for public sector

nancial reporting

5

. When entities apply the new standards, the change in the

accumulated surplus or decit of the entity may be explained by two nancial

statements (the statement of operations and the statement of remeasurement gains

and losses). Entities will only prepare this statement when the entity’s operations

require the reporting of remeasurement gains and losses.

Exhibit 5 shows a sample statement of remeasurement gains and losses for your reference.

WHAT ARE REMEASUREMENT GAINS

AND LOSSES?

Remeasurement gains and losses result from the following:

Fair value measurement

Public sector accounting standards now require that the recognized value of specic

nancial assets and liabilities be updated annually using the current fair value.

ese include certain derivative nancial instruments and investments in publicly

traded equity instruments. Entities may also elect to value other nancial assets and

liabilities using fair value when they are evaluated and managed on a fair value basis.

e annual change in the fair value of these assets and liabilities are reported in the

statement of remeasurement gains and losses until the assets are sold or liabilities

are seled.

Foreign currency exchange rate uctuations

When an entity holds foreign currency such as US dollars, the value of the US

dollar cash is subject to changes in foreign exchange rates. To prepare the nancial

statements preparers must convert these monetary nancial assets and liabilities

to Canadian dollars. e annual uctuations that result from changes in exchange

rates are reported in the Statement of Remeasurement Gains and Losses until the

monetary assets or liabilities are used or seled.

Changes in the reported value of assets and liabilities due to fair value measurement or

changes in exchange rates are only included in the Statement of Remeasurement

4 The new standards are 1201 Financial Statement Presentation and Disclosure, 2601 Foreign Currency

Translation and 3450 Financial Instruments. All three accounting standards must be adopted

concurrently.

5 The new accounting standard for financial statement presentation and disclosure must be applied for

fiscal periods beginning on or after April 1, 2016. Entities that transitioned from the CICA Handbook to

the PSA Handbook (most government organizations) were required to apply the new standards for fiscal

periods beginning on or after April 1, 2012.

THE STATEMENT OF REMEASUREMENT

GAINS AND LOSSES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

19

Gains and Losses until the asset or liability is disposed of or seled. When this occurs,

previously reported unrealized gains and losses are transferred from accumulated

remeasurement gains and losses and the entire gain or loss (relative to cost) is

recognized in the statement of operations.

WHAT THE STATEMENT PRESENTS

is statement provides a reconciliation of the opening and closing remeasurement

gains and losses. To do this the statement is structured with four main sections:

1. e opening remeasurement gain or loss position;

2. Current year changes in the remeasurement gains or losses by type;

3. Gains or losses realized in the year and transferred to the statement of operations;

and

4. e ending remeasurement gain or loss position.

WHY ARE REMEASUREMENT GAINS

AND LOSSES NOT REPORTED IN THE

STATEMENT OF OPERATIONS?

Entities cannot anticipate with any certainty how the market values of assets or foreign

exchange rates will change. erefore, the statement of remeasurement gains and losses

was introduced to separately report the nancial impact of these unrealized uctuations

on the nancial position of the entity.

By excluding these changes from the statement of operations, the budget to actual

comparisons presented for accountability purposes in that statement continues to

reect the operations that the entity can traditionally plan for.

WILL ALL PUBLIC SECTOR ENTITIES

PREPARE THIS STATEMENT?

Unlike the other nancial statements explained in this document, this statement may not

be prepared by all entities. e statement mainly captures the nancial changes resulting

from the use of fair values and holding foreign currency monetary assets and liabilities.

An entity will only prepare the statement when it applies to their circumstances.

THE STATEMENT OF REMEASUREMENT

GAINS AND LOSSES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

20

PUBLIC SECTOR ENTITY

Statement of Remeasurement Gains and Losses

For the year ended March 31, 2014

2014 2013

Accumulated remeasurement gains

(losses) at the beginning of the year (47) 0

Unrealized gains (losses) aributable to:

Foreign exchange (35) -

Derivatives 130 (105)

Portfolio investments 54 108

Amounts reclassied to statement of operations

Portfolio investments 20 (50)

Net remeasurement gains (losses) for the year 169 (47)

Accumulated remeasurement gains (losses) at end of year 122 (47)

Exhibit 5: Sample Statement of Remeasurement Gains and Losses

Source: Adapted from the CPA Canada Public Sector Accounting Handbook

THE STATEMENT OF REMEASUREMENT

GAINS AND LOSSES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

21

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING THE FINANCIAL

STATEMENTS– AND HOW TO FIND

THE ANSWERS

1. Why do the entity’s published financial

statements not include a Statement of

Remeasurement Gains and Losses?

Entities generally only include this statement when there are remeasurement gains

or losses to report. erefore, the inclusion of this statement will depend on the

circumstance of the entity. In addition, governments and some government organizations

are not required to adopt the accounting standards that require the reporting of

remeasurement gains and losses until scal periods beginning on or aer April 1, 2016.

e accounting policy note should explain if these standards have been applied.

When portfolio investments are valued using cost, any changes to the fair value of

the investments will be recorded only when the investment is sold or if there is a

permanent impairment in value. To assist readers with understanding the value of an

entity’s investments when the cost basis is used, the notes provide information on the

market value of specic investments.

2. What is the potential exposure of the entity to

future fair value and foreign currency exchange

rate changes?

e notes to the nancial statements should provide you with information to

determine which nancial assets and liabilities result in remeasurement gains and losses

along with the potential impact to nancial results from changes in risk factors.

For example, an entity that issues debt in US dollars is impacted by foreign currency

risk. e value of the liability increases or decreases as exchange rates change (this

change is reported in the Statement of Remeasurement Gains and Losses). e notes

should also provide you with information on the organization’s exposure to this risk

and how it is being managed.

THE STATEMENT OF REMEASUREMENT

GAINS AND LOSSES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

22

The Statement of Cash Flow explains the change in cash and

cash equivalents from the prior year and provides readers with important information

about how the entity generated cash to meet its requirements. Exhibit 6 is a sample

Statement of Cash Flow for your reference as you read this section.

FOUR CATEGORIES OF CASH FLOW

e layout of the statement is designed to show how the entity nanced its activities

during the current and prior year. e statement presents cash ow in four categories.

How the cash is generated and used is shown separately in each case:

1. Operating activities: Cash ow from operating activities demonstrates the extent

to which an entity generates sucient cash ow from revenues to cover the cost of

programs, purchase capital assets and repay debts.

2. Capital activities: is category of activities, unique to the public sector, reects

how the public and private sectors use tangible capital assets dierently. e public

sector normally purchases capital assets to provide services.

Cash ow related to purchasing capital assets, therefore, reects the decision to use

resources to acquire future service potential. Businesses acquire tangible capital

assets to generate future cash ow from the sale of goods and services. erefore,

businesses include transactions related to capital assets within investing activities.

3. Investing activities: Cash ow from investing activities relates to the purchase and

disposal of investments similar to a business. is category includes investments such as

marketable securities and investments in government-controlled business enterprises.

4. Financing activities: Cash ow from nancing activities includes the issuance

and payment of debt obligations by the entity. is category also includes cash

transactions associated with tangible capital assets acquired through a capital lease.

DIRECT OR INDIRECT METHOD OF

PREPAR ATION

e statement of cash ows can be prepared using either the direct or indirect method.

e indirect method is more commonly used in practice, however, the PSA Handbook

describes the direct method as the preferred method.

e dierence between the two methods relates to the presentation of operating

activity information. e indirect method is a reconciliation that adjusts the annual

surplus or decit for non-cash items such as tangible capital asset amortization. e

direct method provides cash inows and outows for each major source of operating

activities such as cash inows from taxation and cash outows from employee

compensation. e additional information provided by the direct method is useful for

estimating future cash ows from operating activities. is information is not available

when the statement is prepared using the indirect method.

Cash equivalents

Short-term, highly liquid

investments that are

readily convertible to

known cash amounts.

Unique Public Sector

Cash Flow Category

Capital activities for

cash ows associated

with investments in non-

nancial assets

THE STATEMENT OF CASH FLOW

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

23

PUBLIC SECTOR ENTITY

Statement of Cash Flow

For the year ended March 31, 2014

2014 2013

OPERATING TRANSACTIONS

Cash received from:

Ta xes 8,239 7,267

Transfers 1,541 1,943

Non-renewable resources 2 ,118 3,808

Fees, permites, licenses and nes 1,581 1,291

Investments 1,564 1,675

Other 3,201 2,706

18,24 4 18,690

Cash paid for:

Salaries, wages, employment 1,345 1,276

Material and supplies 3,192 2,936

Grants and other transfers 12,074 10,290

Financing charge 282 733

Travel and communication 108 102

17,0 01 15,337

Cash provided by operating transactions 1,243 3,353

CAPITAL TRANSACTIONS

Proceeds on sale of tangible capital assets 46 72

Cash used to acquire tangible (294) (250)

Cash applied to capital transactions (248) (178)

INVESTING TRANSACTIONS

Proceeds from disposals and redemptions of portfolio investments 262 2,997

Repayment of loans and advances 768 1,129

Portolio investments (594) (4,089)

Loans and advances (290) (280)

Other (17) (15)

Cash provided by (applied to) investing 129 (258)

FINANCING TRANSACTIONS

Public debt issues 13,970 3,694

Public debt retirement (14,759) (6,175)

Cash applied to nancing transactions (789) (2,481)

Increase in cash and cash equivalents 335 436

Cash and cash equivalents at beginning of year 1,573 1,137

Cash and cash equivalents at end of year 1,908 1,573

Exhibit 6: Sample Statement of Cash Flow (Direct Method)

Source: Adapted from the CPA Canada Public Sector Accounting Handbook

THE STATEMENT OF CASH FLOW

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

24

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING A STATEMENT OF

CASH FLOW – AND HOW TO FIND

THE ANSWERS

1. Did the entity use the direct or indirect method

to prepare the Statement of Cash Flow?

If the entity used the direct method, the reader will have additional information with

which to compare the amounts recognized in the Statement of Operations with the

related cash selement amounts.

2. Did the entity generate sufficient cash flow from

operations to cover the cash requirements during

the period?

Public sector entities use the cash generated from operations to: fund the acquisition

of tangible capital assets; purchase investments; and repay debt nancing. Insucient

cash ow from operating activities may require the entity to sell investments or obtain

additional debt nancing. Readers should assess the extent to which the entity is reliant

on obtaining cash ow from non-operating sources to meet cash requirements.

3. Does the entity have excess cash that could be

used to pay down debt?

Entities need to manage their nancial resources to ensure that sucient cash is on

hand to pay liabilities as they come due. As part of good cash ow management,

entities should therefore look for ways to use excess cash resources to pay down debts

to reduce interest costs or generate additional investment returns.

THE STATEMENT OF CASH FLOW

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

25

As discussed for the Statement of Financial Position, the net debt or

net nancial asset position of a public sector entity is a key indicator of its nancial

position. e Statement of Change in Net Debt reconciles the change in net debt for

the current and the prior year. is information helps readers understand why the net

debt position of the entity changed. A sample Statement of Change in Net Debt is

provided in Exhibit 7.

EXPENDITURES

In the public sector, the accounting standards distinguish between expenses and

expenditures. Expenses are the cost of goods and services consumed during the period.

Expenditures are the costs of goods and services acquired during the period.

e Statement of Change in Net Debt provides information on the extent to which the

expenditures of the scal period were met by the revenues recognized in the Statement

of Operations.

6

An increase in net debt means that more future revenues will be needed

to pay for past transactions and events.

RECONCILIATION OF THE CHANGE IN

NET DEBT

To explain how the expenditures of the period were met by revenues, the statement

reconciles the annual operating surplus or decit shown in the Statement of

Operations (which includes revenues and expenses) to the change in net debt.

e common items that explain the dierence between the annual surplus or decit

and the change in net debt are:

the acquisition and disposal of tangible capital assets;

the current year amortization expense for tangible capital assets (expense for

current year consumption); and

the acquisition and disposal of other non-nancial assets.

FINANCIAL ACCOUNTABILITY –

BUDGET TO ACTUAL RESULTS

As the Statement of Operations does, the Statement of Change in Net Debt also

compares the current period results with the entity’s original spending plans. is

presentation provides key accountability information about the entity’s performance in

achieving its spending objectives.

e incremental budget information in the statement generally relates to the planned

spending to acquire tangible capital assets and other non-nancial assets.

6 For entities that have adopted PS 1201, the statement also shows the extent to which expenditures were

met by revenues recognized in the Statement of Remeasurement Gains and Losses.

THE STATEMENT OF CHANGE IN NET DEBT

(FINANCIAL ASSETS)

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

26

PUBLIC SECTOR ENTITY

Statement of Change in Net Debt

For the year ended March 31, 2014

Budget

2014

Actual

2014

Actual

2013

Operating Surplus 28 1,376 2,551

Acquisition of tangible capital assets (294) (294) (250)

Amortization of tangible capital assets 226 226 230

(Gain) loss on sale of tangible capital assets - (5) (19)

Proceeds on sale of tangible capital assets - 46 72

Write-downs of tangible capital assets - 24 44

(68) (3) 77

Acquisition of supplies inventory - - (324)

Acquisition of prepaid expenses - (30) (20)

Use of supplies inventory - 110 102

Use of prepaid expenses - 20 -

- 100 (242)

(40) 1,473 2,386

Net remeasurement gains (losses) 169 (47)

(Increase) decrease in net debt (40) 1,642 2,339

Net debt at beginning of year (8,870) (8,870) (11,209)

Net debt at end of year (8,910) (7,228) (8,870)

Exhibit 7: Sample Statement of Change in Net Debt

Source: Adapted from the CPA Canada Public Sector Accounting Handbook

THE STATEMENT OF CHANGE IN NET DEBT

(FINANCIAL ASSETS)

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

27

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING A STATEMENT OF

CHANGE IN NET DEBT – AND HOW

TO FIND THE ANSWERS

1. How did actual spending on capital assets

compare with the original plan?

As the Statement of Operations does, the Statement of Change in Net Debt also

provides accountability information on how actual results compared with previously

communicated plans. Readers should assess whether actual spending on capital assets

exceeded, met, or fell below planned acquisitions.

Readers should also seek additional information on the entity’s investing decisions in

the Financial Statement Discussion and Analysis (FSD&A), including explanations for

signicant variances between planned and actual results.

2. How were expenditures for the current and

prior period financed?

e Statement of Change in Net Debt highlights how entity expenditures were

nanced. Readers should assess whether the entity raised sucient operating revenues

to nance reported expenditures.

Net debt increases when insucient operating revenues are raised to nance

expenditures. erefore, when operating revenues are insucient to nance

expenditures, readers should assess what expenditures the entity was required to

nance with increased liabilities.

Entities commonly nance the purchase of long-lived tangible capital assets with debt.

When the purchase of tangible capital assets exceeds the current year consumption of

tangible capital assets in operations, the net debt of the entity will increase. erefore,

net debt may increase signicantly in periods when the entity makes signicant

investments in tangible capital assets. And the reverse can occur: net debt may decrease

signicantly in periods when an entity makes limited tangible capital asset investments.

THE STATEMENT OF CHANGE IN NET DEBT

(FINANCIAL ASSETS)

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

28

The notes and schedules are an integral part of the nancial statements

and form the majority of pages in a set of nancial statements. e note disclosures must be

read to fully understanding the results presented in the nancial statements.

Note disclosures provide you with a variety of information on the entity’s current and

future nancial performance including:

the basis on which the nancial statements were prepared – what is recognized,

when it is recognized and what amount is recognized;

expanded details on items recognized in the nancial statements – the nancial

statements present highly summarized information. e notes provide more

detailed information of what is included in the nancial statements;

items not recognized in the nancial statements – what is not recognized can be as

important as what is recognized when assessing the nancial results; and

details for future transactions of the entity – the notes provide information on

future liabilities and transactions of the entity that result from existing transactions.

While all disclosures required by the Public Sector Accounting Handbook are essential for

fairly presenting an entity’s nancial results, specic aention should be paid to those

summarized in the table below:

Note disclosure Why the disclosure is important

e reporting entity e nancial statements should include the nancial position and results of all

activities that the entity controls.

Governments and government organizations may establish separate legal entities

to administer specic programs or policies. e nancial position and results of

all controlled entities should be consolidated.

7

e notes to the nancial statements describe all entities consolidated and how

the results are consolidated.

e schedules to the nancial statements provide summarized nancial

statements for all government business enterprises.

Signicant accounting policies All nancial reporting frameworks require preparers to exercise professional

judgement when applying accounting principles.

e signicant accounting policies describe the recognition and measurement

policies applied when preparing the nancial statements.

Where the accounting standards provide preparers with options, the signicant

accounting policies should describe which option the entity selected for

preparing the nancial statements.

7 Government business enterprises and government business partnerships are consolidated using the

modified equity method. The accounting policies for these entities are not conformed to those of the

parent organization for consolidation purposes and the financial results are not consolidated on a line-by-

line basis.

FINANCIAL STATEMENT NOTE DISCLOSURES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

29

Note disclosure Why the disclosure is important

Estimates and measurement

uncertainty

To produce timely information for readers, preparers must make estimates for

some transactions that will sele at future dates. Preparers must use all available

information at the date of the nancial statements to support their estimates.

When it is reasonably possible that an estimate recorded could change by a

material amount within the next year, management should disclose information

for the reader to understand the nature of the uncertainty and the range of

amounts. Common disclosures for measurement uncertainty relate to taxation

revenues, and pension benet liabilities.

Alternative presentation of expenses e Statement of Operations presents expenses by function or program, such

as health or education services. e notes include supplementary reporting on

the resources used to deliver those services (e.g., employee salaries and benets,

transfers to individuals or organizations, building rent, maintenance expenses).

is disclosure provides critical information about how an entity delivers

services.

Subsequent events e nancial statements present the nancial position and results at a specic

point in time. However, transactions or events aer that date but before the

release of the nancial statements can change the reported performance or

signicantly aect future performance results.

e notes to the nancial statements should disclose information on material

subsequent events so that readers can assess the impact of those events on

reported performance or the potential future performance of the entity.

Contractual obligations Contractual obligations are future liabilities that will be recorded when the terms

of agreements or contracts in place at the nancial statement date are met.

Contractual obligation note disclosure provides readers with key information

about an entity’s future nancial exibility for program delivery.

Contingencies Contingencies exist when it is unclear whether the entity has an obligation to an

external party or is entitled to receive assets. e uncertainty is resolved when a

future event conrms the obligation or entitlement.

A common example of a contingent liability is a lawsuit against an entity.

Whether a liability exists is conrmed by a court ruling on the external party

claim.

Contingent liabilities may or may not be recorded in the nancial statements.

Contingent assets are not recorded in the nancial statements until the

conrming event occurs. e notes to the nancial statements provide

information explaining the impact of contingencies on the reported amounts and

the potential impact of contingencies to future nancial performance.

FINANCIAL STATEMENT NOTE DISCLOSURES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

30

Note disclosure Why the disclosure is important

Accounting for pension plans and other

employee future benets

Accounting for employee pension plans and other employee future benets is

a complex area of accounting in both the public and private sector. Liabilities

associated with these plans are not always recognized in an entity’s nancial

statements when applying PSA standards. When liabilities are recognized, the

amounts recognized are usually complex estimates prepared in consultation with

actuaries.

e notes provide extensive disclosure on the accounting for these benets.

ese disclosures must be read carefully to fully understand how the accounting

for these benets impacts the nancial results presented.

Debt Governments frequently nance a portion of their expenditures with debt. e

notes provide extensive information on the terms of an entity’s borrowings and

the nancial risks associated with those borrowings. Common information

contained in the notes includes:

e total principal borrowed and the repayment timing;

e interest expense associated with the borrowings;

Funds the entity is required to set aside under the borrowing terms to nance

future debt principal repayments; and

Assets the entity pledged as collateral for the amounts borrowed.

Additional information on nancial risks associated with debt will also be

included in the notes.

Financial instrument risk disclosures

8

Financial instrument disclosures required by the accounting standards provide

readers with an understanding of the nature and extent of risks that arise from

nancial instruments held by a public sector entity supplemented with how the

entity manages those risks. Common risks from nancial instruments include

credit risk, liquidity risk, interest rate risk, price risk and foreign currency risk.

e accounting standards also allow for these disclosures to be included in the

unaudited nancial statement discussion and analysis (FSD&A) aached to the

nancial statements instead of the notes.

8 Government and some government organizations do not have to adopt the accounting standards requiring risk disclosures until fiscal periods beginning on or after

April 1, 2016.

FINANCIAL STATEMENT NOTE DISCLOSURES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

31

POTENTIAL QUESTIONS TO ASK

WHEN REVIEWING NOTES TO

FINANCIAL STATEMENTS – AND HOW

TO FIND THE ANSWERS IN THEM

1. What is the entity’s potential exposure to

contingent liabilities?

Entities record contingent liabilities when it is likely that a future event will conrm

that a liability existed. However, in many cases entities are unable to determine what

the likely outcome will be. When the outcome cannot be determined there are no

amounts recorded in the nancial statements. As a result of this uncertainty, the notes

provide readers with information on contingencies to broadly understand how the

resolution could impact the nancial results of the entity.

2. What future goods or services has the entity

secured through contractual arrangements?

It is common to secure the purchase of goods or service in advance through leasing or

other agreements. e notes to the nancial statements provide details on the obligations

the entity will be required to pay when suppliers meet the terms of the agreements.

is information can be a starting point for discussions about the nancial

management of the entity. Considerations would include: is the entity securing the

right resources in advance? Is the entity securing the right amounts and an appropriate

price, and how do the contractual obligations impact the exibility of the entity to

respond to potential changes in nancial circumstances?

3. Does the entity participate in a multi-employer

defined benefit plans such as a pension or long

term disability plan?

Governments frequently establish employee benet plans that multiple government

organizations participate in. When the benet plan liabilities are not segregated by

entity the statement of nancial position does not report their share of the liabilities (or

assets) of the plan. e contributions employers make to these plans are recorded as an

expense in the statement of operations.

As a result of the above, the notes provide information on the overall funded position

of the plan (assets available for benets and accrued benet obligations). is

information can be an indicator of potential increases or decreases to contribution rates

that would impact the entity’s future expenses.

FINANCIAL STATEMENT NOTE DISCLOSURES

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

32

Audited financial statements prepared in accordance with

public sector accounting standards are the most common form of public sector

nancial accountability in Canada. However, nancial statements alone do not provide

readers with all the information necessary to assess an entity’s nancial performance.

is guide has presented some common questions a reader should keep in mind

when reviewing a set of nancial statements. However, fully answering many of these

questions requires additional information from an entity’s management.

A common method used to disclose such information to readers is to supplement the

audited nancial statements with a nancial statement discussion and analysis (FSD&A)

from management. is supplementary nancial reporting gives the entity’s management

a means of explaining the nancial statement results to all readers in a consistent manner.

e FSD&A aached to the nancial statements is unaudited.

Readers of public sector nancial statements should expect that the nancial reporting of

the entity include a FSD&A to supplement the audited nancial statements.

GUIDANCE FOR PREPARING A

FINANCIAL STATEMENT DISCUSSION

AND ANALYSIS

As part of its mandate, PSAB developed a statement of recommended practice

9

to

assist public sector entities with the development of FSD&A reporting. e statement

of recommended practice provides a general framework for determining the most

relevant information to report. A high level summary of the guidance is provided in

Exhibit 8. is exhibit should assist legislators and councillors, board members and

other stakeholders with understanding what management should be reporting to

readers when explaining the nancial statements.

e statement of recommended practice provides management with more detailed

guidance for specic nancial statement elements.

9 Statement of recommended practice SORP – 1 financial statement discussion and analysis

THE IMPORTANCE OF THE FINANCIAL

STATEMENT DISCUSSION AND ANALYSIS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

33

Financial report components

e entity’s nancial report should include an FSD&A along with the

audited nancial statements. e FSD&A should be cross-referenced to the

audited nancial statements.

e entity should include a statement acknowledging its responsibility for

preparing the FSD&A.

Qualitative characteristics

e FSD&A is meant to enhance readers’ understanding of the entity’s nancial

position and changes in nancial position. To do this, the report must have the

following qualitative characteristics:

information must be presented in a way that is understandable to a general

audience;

information presented must be relevant for decision-making or assessing

accountability;

information presented must be consistent with the nancial results

contained in the audited nancial statements; and

the current and historical information presented throughout the report must

be prepared on the same basis to enable comparability.

Key components of a FSD&A

e FSD&A should provide the following supplementary reporting to enhance

readers’ understanding of the nancial statements:

a summary of the signicant events aecting the nancial statements;

analysis that explains the reasons for signicant variances between planned

and current year actual results;

analysis that explains the reasons for signicant variances between current

and prior year results;

analysis of signicant trends (multi-year analysis) for specic nancial

statement elements; and

information on known signicant risks to, and uncertainties associated with,

the entity’s nancial position and changes to nancial position, along with a

discussion of the entity’s approach to managing the identied risks.

THE IMPORTANCE OF THE FINANCIAL

STATEMENT DISCUSSION AND ANALYSIS

Exhibit 8: Summary of SORP 1: Financial statement discussion and analysis

recommended practice

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

34

An entity’s financial statements contain management’s

representations of the entity’s nancial performance, in accordance with Canadian

public sector accounting standards. For those nancial statements to be relevant, the

information must be reliable. A nancial statement audit by an independent auditor

provides readers with assurance on whether the nancial statements prepared by

management are free of material misstatement.

e auditor provides this assurance by expressing an opinion on whether or not the

nancial statements have been prepared in accordance with Canadian public sector

accounting standards. A sample of an unqualied independent auditor’s report is

provided in Exhibit 9.

INFORMATION COMMUNICATED IN

AN INDEPENDENT AUDITOR’S REPORT

e independent auditor’s report on a set of nancial statements explains:

the scope of the audit – Every nancial statement opinion identies the specic

nancial statements and other information subject to audit. e auditor does not

provide assurance on the FSD&A that accompanies the nancial statements.

the responsibilities of management and the auditor – e auditor’s report:

• identies that the nancial statements are the responsibility of management and

the nancial reporting framework management used to prepare the nancial

statements;

• identies the standards followed by the auditor to provide the opinion, and gives a

high-level overview of how the audit was conducted; and

• describes the level of assurance provided by the auditor (audits provide a high level

of assurance that the nancial statements are free of material misstatement – an

error or omission that would inuence or change the decisions of readers when

using the information).

e auditor’s opinion – e auditor provides his or her opinion on the nancial

statements based on the results of the audit. When the auditor does not issue an

unqualied opinion, the report will explain the reasons within the report. e types

of opinions are summarized below.

THE IMPORTANCE OF THE INDEPENDENT

AUDITOR’S REPORT ON THE STATEMENTS

Auditor General of British Columbia | June 2014

Understanding Canadian Public Sector Financial Statements

35

“Emphasis of maer” or “other maer” paragraphs – e use of these paragraphs is

rare. However, when auditors use them, it is to report signicant information that,

in the auditors’ opinion, is fundamental to the reader’s understanding of the

nancial statements. When the auditor includes these paragraphs, it is critical that

readers understand what the auditor is conveying.

Other legal and regulatory requirements – It is common in the public sector that

auditors provide opinions on legal or regulatory requirements such as compliance

with nancial legislation. e auditor’s report presents these requirements

separately from the auditor’s opinion on the nancial statements.

QUESTIONS TO ASK WHEN REVIEWING

AN INDEPENDENT AUDITOR’S REPORT

1. Were the financial statements prepared in accordance

with Canadian public sector accounting standards?

Readers should expect most public sector entities to prepare general purpose nancial

statements in accordance with Canadian public sector accounting standards.

11

However,

governments may direct organizations through legislation to prepare their nancial

statements using an accounting framework other than a framework for general purpose

nancial statements. When this occurs, the independent auditor’s report will bring this to

the reader’s aention through an emphasis of maer paragraph. e emphasis of maer

directs the reader to the note disclosure that describes the dierence between the reporting

framework used and generally accepted nancial reporting frameworks in Canada.

Furthermore, the entity’s nancial statements will not be comparable to other nancial

statements prepared in accordance with Canadian public sector accounting standards.

10 The audit opinion will not use the phrase “present fairly” when the financial statements are prepared

in accordance with a legislative accounting framework that differs from generally accepted accounting

frameworks for preparing general purpose financial statements.

11 When applying the PSA Handbook, government organizations may elect to use International Financial

Reporting Standards (IFRS) as the financial reporting framework for preparing financial statements.

Opinion type Opinion paragraphs

Unqualied opinion e report includes one opinion section:

Opinion

e nancial statements present fairly

10

, in all material

respects, the nancial position and results of the entity.