Page 1 of 5

Questions? Go to Fidelity.com/movemoney or call 800-343-3548.

One-Time Withdrawal – IRA

Use this form to make a one-time, tax-reportable distribution from a Traditional, Rollover, Roth, SEP, SIMPLE, or Inherited IRA.

Do NOT use this form for Defined Contribution Retirement Plan accounts, annuities, nonretirement accounts, or for any IRA-to-IRA

transfer. Also, do NOT use this form to purchase an investment in your IRA. Go to Fidelity.com/forms to find the appropriate form.

Type on screen or fill in using CAPITAL letters and black ink. If you need more room for information or signatures, make a copy of the

relevant page.

Helpful to Know

• It is your responsibility to ensure that your IRA distributions

comply with IRS rules. All transactions made using this form

are reported to the IRS as an IRA distribution. You may want

to consult a tax advisor as such distribution generally results

in taxable income to you.

• You should also confirm that Fidelity has your most current

address prior to submission so that we can withhold

appropriate taxes. See the General Instructions and the

Marginal Rate Tables contained in the IRS Form W-4R at

Fidelity.com/W-4R for additional information. To update your

address, go to Fidelity.com.

• Nonresident aliens must provide IRS form W-8BEN and a U.S.

or foreign tax identification number.

• If you are making withdrawals from more than one IRA, you

must complete a separate form for each account.

• If this form directs Fidelity to sell shares of any security, be

aware that the timing of the transaction depends on when we

receive this form, which is outside of your control. To better

control the timing of the transaction, you should direct the

sale of securities online or through a Fidelity representative.

Note: Certain securities (such as options, certain fixed income

securities, and thinly traded securities) may not be eligible to

sell via this form, which may result in Fidelity not being able to

process this withdrawal as requested.

• For mutual funds, note that:

– Withdrawals could trigger redemption or transaction fees

(see the applicable fund prospectus).

– If a fund is closed to new investors, you will not be able to

purchase new shares of the fund in the future

if you draw your fund balance down to zero.

•

Any fees charged or expenses incurred in connection with

your instructions will be assessed at the “rep-assisted” rates.

Fees and expenses may be lower if you instead place your

trades online. Please refer to the Schedule of Fees for more

information.

• If you are rolling over these assets to an employer plan, you may

be responsible for obtaining your Plan Administrator’s consent.

1. Account Owner

Name Fidelity IRA Number

Social Security or Taxpayer ID Number Primary Phone

2. Request Reason

Normal You are AT LEAST 59½ at the time of distribution.

Early distribution You are younger than 59½ at the time of distribution. An IRS early distribution penalty may apply.

Note: A distribution from a Roth IRA will be reported as an early distribution.

Death of original IRA owner For inherited accounts only.

Direct rollover to a workplace retirement plan, such as a 401(k):

Plan Name

Phone number may

be used if we have

questions, but will not

be used to update your

account information.

Check ONLY one.

If directing your distri-

bution to an HSA as

a qualified HSA fund-

ing distribution, check

either “Normal” or

“Early distribution,“

as appropriate.

1.932150.111 006891001

Form continues on next page.

Print

Reset

Save

Page 2 of 51.932150.111 006891002

3. Distribution Amount

If this form directs Fidelity to sell shares of any securities (including mutual funds), be aware that:

• The timing of the transaction (i.e., when

your trade is processed) depends on

when we receive this form, which is

outside of your control. Trades may take

up to five business days to process once

determined to be in good order.

• If you want to better control the timing

of the transaction, you should direct the

sale of securities online or through a

Fidelity representative.

• If you withdraw all assets from your source

account, that account will be closed.

• Once we receive this form in good order,

you cannot cancel your distribution request.

In the event that transactions cannot be processed within five business days of determining your request to be in good order,

Fidelity will notify you and you may have to resubmit your request on the unsold positions within your account.

ALL core cash and Fidelity money market funds in your brokerage account

Skip to Section 4.

ONLY the following amount of cash in your brokerage account.

Skip to Section 4.

Dollar Amount

If the amount you indicate is greater

than your core account balance,

your request will be denied.

$

ENTIRE VALUE of your account in cash (all eligible securities will be sold)

ENTIRE VALUE of your account as shares (in kind)

You must choose to distribute into a Fidelity account in

Section 4.

ONLY the following eligible securities and amounts:

Sell and distribute as cash

Distribute as shares (in kind)

Security Name or Symbol

ALL

shares

ONLY this

many shares:

Number of Shares

ONLY this

dollar amount:

Fidelity Mutual Fund

accounts only

.

Dollar Amount

$

Sell and distribute as cash

Distribute as shares (in kind)

Security Name or Symbol

ALL

shares

ONLY this

many shares:

Number of Shares

ONLY this

dollar amount:

Fidelity Mutual Fund

accounts only.

Dollar Amount

$

4. Distribution Method

You must obtain a Medallion signature guarantee in Section 6 if requesting a bank wire, if sending a check to a payee other than the IRA

owner or alternate address, if the requested payment amount or direct rollover to a workplace retirement plan is over $100,000, or if the

address on the account has been changed within the past 10 days.

Distribute into a Fidelity nonretirement, investment-only retirement, Defined Contribution Retirement Plan account,

or your own Fidelity HSA: Requires Medallion signature guarantee if going to an account of which you are not an owner.

Fidelity Nonretirement or HSA Account Number Fidelity Fund Name or Symbol Mutual fund accounts ONLY

Direct rollover to a workplace retirement plan, check paid to a payee other than the IRA owner, or check

mailed to an alternate address:

Workplace Retirement Plan or Other Payee Name

Workplace Retirement Plan Account Number For Benefit Of/Attention

Address

City State/Province ZIP/Postal Code Country

Check ONLY

one and provide

any additional

requested

information.

Check one and

provide all required

information.

Distribution Method continues on next page.

1.932150.111 Page 3 of 5 006891003

Electronic funds transfer (EFT) to a bank or credit union account using EFT instructions already in place on the

account (cash only). This form cannot be used to set up EFT. To add EFT to an account, go to Fidelity.com/eft or com-

plete the Electronic Funds Transfer (EFT) Authorization form.

A. EFT to your bank account. The names on the bank account and the IRA are the same.

B. EFT to someone else. (Available for brokerage accounts only.) The names on the bank account and the IRA

are different.

If EFT has not been established prior to the receipt of this request, a check will be mailed to the address

of record.

Bank Account Number

Check mailed to the address of record

Default if no choice indicated or if we are unable to process your choice.

Bank wire to a bank or credit union account in your name or someone else’s (cash only): Ask the bank for its wire

routing number. The bank may charge a fee for wire transfers.

Wire Recipient

Bank Routing /ABA Number Bank Name

Account Number Account Owner Name(s) Required

Address of Wire Recipient

City State/Province ZIP/Postal Code Country

For Further Credit

Additional Details (if applicable) Instructions to be included with the wire transfer.

Correspondent (Intermediary)

Correspondent Bank Routing/ABA Number Correspondent Bank Name

Account is OUTSIDE the United States:

SWIFT Code Name of Country

Provide bank informa-

tion ONLY if there are

multiple EFT instruc-

tions on the account

identified in Section 1.

All bank wire requests

MUST have a Medallion

signature guarantee. A

notary seal/stamp is

NOT a Medallion

signature guarantee.

FULL address is

required for

international wires.

If the bank uses a corre-

spondent bank, provide

the information here.

Correspondent bank

information may not be

required for all wires.

Indicate if the recipient

bank is outside the

United States.

4. Distribution Method, continued

Form continues on next page.

1.932150.111 Page 4 of 5 006891004

5. Tax Withholding

Distributions from your non-Roth IRA are subject to federal and, where applicable, state income tax withholding unless you elect not to

have withholding apply below (if you are a U.S. citizen or other U.S. person). For nonperiodic payments, the default withholding rate is

10%. You can choose to have a different rate by entering a rate between 0% and 100% below. Generally, you can’t choose less than 10%

for payments to be delivered outside the United States and its possessions. If you made nondeductible contributions to your IRA, this may

result in excess withholding from your distributions. If you elect not to have withholding apply to your distributions or if you do not have

enough federal income tax withheld from your distribution, you may be responsible for payment of estimated tax. You may incur penalties

under the estimated tax rules if your withholding and estimated tax payments are not sufficient. See “State Tax Withholding — IRA

Withdrawals” at the end of this form.

Do NOT complete this section if you are a nonresident alien. Instead, the nonresident alien tax-withholding rate of 30% will apply.

Complete if you would like a rate of withholding that is different from this default withholding rate. You should review the General

Instructions and the Marginal Rate Tables contained in the IRS Form W-4R at Fidelity.com/W-4R for additional information, which you can

download for free. If you don’t have access to a computer, you may request a copy by calling Fidelity, or the IRS at 800-829-1040.

Federal

Do NOT withhold federal taxes.

Withhold federal taxes at the rate of:

Percentage

Whole numbers; no dollar amounts or

decimals. Note that if there is federal tax

withholding, certain states require that

there also be state tax withholding.

%

State

Do NOT withhold state taxes unless required by law.

Withhold state taxes at the applicable rate.

Withhold state taxes at the rate of:

Percentage

Whole numbers; no dollar amounts

or decimals.

%

6. Signature and Date Account owner must sign and date.

By signing below, you:

• Authorize and request the custodian for

the Fidelity IRA, Fidelity Management

Trust Company and its agents, affiliates,

employees or successor custodians

(Fidelity) to withdraw the amount indicated

in Section 3 of this form.

• Acknowledge that non-Roth IRA distribu-

tions will generally be taxed as ordinary

income and may be subject to a 10% early

withdrawal penalty if taken before age 59½.

• Acknowledge that distributions from a

Roth IRA that are attributable to earnings

may be taxed as ordinary income and may

be subject to a 10% early withdrawal pen-

alty unless certain conditions are met.

• Acknowledge that Fidelity is not respon-

sible for changes in the value of assets that

may occur during the distribution process.

• Acknowledge that distributions made from

any SIMPLE IRA prior to age 59½ and

within the first two years of participating

in an employer’s SIMPLE IRA plan may be

subject to a 25% penalty.

• Acknowledge that if taking Substantially

Equal Periodic Payments, it is your respon-

sibility to comply with the IRS rules, and

that Fidelity reports such distributions as

“Early Withdrawal — no known exception”

in accordance with IRS requirements.

• Indemnify Fidelity from any liability

in the event that you fail to meet any

IRS requirement.

• Confirm, if you are not a U.S. person,

that you have attached or have on file

with Fidelity IRS Form W-8BEN that

includes your U.S. or foreign tax identifica-

tion number.

• Have viewed, read, and understand the IRS

Instructions for Form W-4R.

• Certify that the address associated with this

account is current and up to date.

Customers requesting EFT:

• Authorize and request Fidelity to make EFT

distributions from the Fidelity IRA listed in

this form by initiating debit entries to the

account indicated in this form.

• Authorize and request the bank named in

Section 4 to accept debit entries initiated

by Fidelity in such account and to debit the

same account without responsibility for the

appropriateness or for the existence of any

further authorization.

Customers transferring assets to an HSA:

• Acknowledge that qualified HSA funding

distributions are not subject to the 10%

early withdrawal penalty when transferred

directly to an HSA.

Customers transferring to a Fidelity Profit

Sharing or Self-Employed 401(k) Retirement

Plan account:

• Acknowledge that you have obtained

Plan Administrator consent to roll over the

amount listed on this form into your Fidelity

Retirement Plan account.

Customers requesting trade processing:

• Authorize Fidelity to process trades on

your behalf.

• Acknowledge that you are delegating to

Fidelity the discretion to determine the

price and time at which certain securities

should be sold pursuant to your instructions

contained in this form.

• Acknowledge that trades may take up to

five business days to process once the

request is received and determined to be in

good order, and that your authorization shall

remain in effect during the entire period.

• Acknowledge that certain securities cannot

be sold through this form and may require

you to call a representative or go online to

process the trades.

For Connecticut Residents:

• Acknowledge that, as a resident of CT,

your distributions from retirement accounts

are subject to the highest marginal tax

rate. If you are exempt from state tax,

you have the option to elect out of state

tax withholding. Otherwise, penalties

may apply. The penalty for reporting false

information is a fine of not more than

$5,000, imprisonment for not more than

five years, or both.

• Confirm that your state tax withholding

election is true, complete, and correct.

Check one in each

column. IRA owner’s

legal/residential

address determines

which state’s tax

rules apply.

Signature and Date continues on next page.

Did you sign the form? Send the ENTIRE form

to Fidelity Investments.

Questions? Go to Fidelity.com/movemoney

or call 800-343-3548.

Regular mail

Fidelity Investments

Attn: Retirement Distributions

PO Box 770001

Cincinnati, OH 45277-0035

Overnight mail

Fidelity Investments

Attn: Retirement Distributions

100 Crosby Parkway KC1B

Covington, KY 41015

On this form, “Fidelity” means Fidelity Brokerage Services LLC and its affiliates. Brokerage services are

provided by Fidelity Brokerage Services LLC, Member NYSE, SIPC. 592522.12.0 (11/22)

1.932150.111 Page 5 of 5 006891005

A Medallion signature guarantee is required:

• to send a check to an alternate address or payee.

• to send a direct rollover to a workplace retirement plan AND the amount is greater than $100,000.

• to request a bank wire.

• if the address on the account has been changed within the past 10 days.

• if the withdrawal is going to a Fidelity account with no common owner.

• if the transaction is greater than $100,000.

If the form is completed at a Fidelity Investor Center, the Medallion signature guarantee is not required. You can get a Medallion signature

guarantee from most banks, credit unions, and other financial institutions. A notary seal/stamp is NOT a Medallion signature guarantee.

PRINT OWNER NAME

MEDALLION SIGNATURE GUARANTEE

OWNER SIGNATURE

SIGN

X

DATE MM/DD/YYYY

DATE

X

6. Signature and Date, continued

Federal and State Tax Withholding — IRA Withdrawals

Helpful to Know

• Federal and state tax withholding rules can change, and

the information cited below may not reflect the current

withholding from a federal or state perspective. Consult

your tax advisor, the IRS, and/or your state taxing

authority to obtain the most up-to-date information

pertaining to your situation.

• The IRS requires Fidelity to provide you with the

Marginal Rate Tables and the Tax Withholding

Instructions from the IRS Form W-4R.

• Each state sets its own withholding rates and require-

ments on taxable distributions. We apply these rates

unless you direct us not to (where permitted) or you

request a higher rate.

• Your account’s legal/residential address determines

which state’s tax rules apply. You should confirm that

the address on your account is current prior to submit-

ting your request.

• You are responsible for paying your federal, state, and

local income taxes and any penalties, including penal-

ties for insufficient withholding.

• Withholding taxes for Roth IRA distributions is optional.

• The federal and/or state tax withholding rate, if

indicated, must be provided as a whole number from

1% to 100% for any one-time withdrawals, or from 1%

to 99% for any automatic withdrawals.

Federal Tax Withholding Information

2024 Marginal Rate Tables

You may use these tables to help you select the appropriate withholding rate for this payment or distribution. Add your

income from all sources and use the column that matches your filing status to find the corresponding rate of withholding.

See the General Instructions section for more information on how to use this table. (Note: This is an excerpt from the IRS

Form W-4R. For the complete copy, please go to Fidelity.com/W-4R or IRS.gov/pub/irs-pdf/fw4r.pdf.)

Single

or

Married filing separately

Married filing jointly

or

Qualifying surviving spouse

Head of household

Total income

over—

Tax rate for every

dollar more

Total income

over—

Tax rate for every

dollar more

Total income

over—

Tax rate for every

dollar more

$0

14,600

26,200

61,750

115,125

206,550

258,325

623,950*

0%

10%

12%

22%

24%

32%

35%

37%

$0

29,200

52,400

123,500

230,250

413,100

516,650

760,400

0%

10%

12%

22%

24%

32%

35%

37%

$0

21,900

38,450

85,000

122,400

213,850

265,600

631,250

0%

10%

12%

22%

24%

32%

35%

37%

*If married filing separately, use $380,200 instead for this 37% rate.

Page 1 of 3

1.964543.108

General Instructions on Federal Tax

Withholding

Nonperiodic payments—10% withholding. Your payer

must withhold at a default 10% rate from the taxable amount

of nonperiodic payments unless you enter a different rate.

Distributions from an IRA that are payable on demand are

treated as nonperiodic payments. Note that the default rate

of withholding may not be appropriate for your tax situation.

You may choose to have no federal income tax withheld.

See the specific instructions below for more information.

Generally, you are not permitted to elect to have federal

income tax withheld at a rate of less than 10% (including

“-0-”) on any payments to be delivered outside the United

States and its territories.

Note: If you don’t give Form W-4R to your payer, you

don’t provide an SSN, or the IRS notifies the payer that you

gave an incorrect SSN, then the payer must withhold 10% of

the payment for federal income tax and can’t honor requests

to have a lower (or no) amount withheld. Generally, for pay-

ments that began before 2024, your current withholding

election (or your default rate) remains in effect unless you

submit a new withholding election.

Payments to nonresident aliens and foreign estates.

Do not use Form W-4R. See Pub. 515, Withholding of Tax on

Nonresident Aliens and Foreign Entities, and Pub. 519, U.S.

Tax Guide for Aliens, for more information.

Tax relief for victims of terrorist attacks. If your disability

payments for injuries incurred as a direct result of a terrorist

attack are not taxable, enter “-0-”. See Pub. 3920, Tax Relief

for Victims of Terrorist Attacks, for more details.

Specific Instructions for IRS Form W-4R

Line 1b

For an estate, enter the estate’s employer identification

number (EIN) in the area reserved for “Social security

number.”

Line 2

More withholding. If you want more than the default rate

withheld from your payment, you may enter a higher rate on

line 2.

Less withholding (nonperiodic payments only). If permit-

ted, you may enter a lower rate on line 2 (including “-0-”) if

you want less than the 10% default rate withheld from your

payment. If you have already paid, or plan to pay, your tax

on this payment through other withholding or estimated tax

payments, you may want to enter “-0-”.

Suggestion for determining withholding. Consider using

the Marginal Rate Tables on page 1 to help you select the

appropriate withholding rate for this payment or distribution.

The tables are most accurate if the appropriate amount of

tax on all other sources of income, deductions, and credits

has been paid through other withholding or estimated tax

payments. If the appropriate amount of tax on those sources

of income has not been paid through other withholding or

estimated tax payments, you can pay that tax through

withholding on this payment by entering a rate that is greater

than the rate in the Marginal Rate Tables.

The marginal tax rate is the rate of tax on each additional

dollar of income you receive above a particular amount of

income. You can use the table for your filing status as a guide

to find a rate of withholding for amounts above the total

income level in the table.

To determine the appropriate rate of withholding from

the table, do the following. Step 1: Find the rate that

corresponds with your total income not including the pay-

ment. Step 2: Add your total income and the taxable amount

of the payment and find the corresponding rate.

If these two rates are the same, enter that rate on line 2.

(See Example 1 below.)

If the two rates differ, multiply (a) the amount in the lower

rate bracket by the rate for that bracket, and (b) the amount

in the higher rate bracket by the rate for that bracket. Add

these two numbers; this is the expected tax for this payment.

To get the rate to have withheld, divide this amount by the

taxable amount of the payment. Round up to the next whole

number and enter that rate on line 2. (See Example 2 below.)

If you prefer a simpler approach (but one that may lead to

overwithholding), find the rate that corresponds to your total

income including the payment and enter that rate on line 2.

Examples. Assume the following facts for Examples 1 and 2.

Your filing status is single. You expect the taxable amount of

your payment to be $20,000. Appropriate amounts have

been withheld for all other sources of income and any

deductions or credits.

Example 1. You expect your total income to be $62,000

without the payment. Step 1: Because your total income

without the payment, $62,000, is greater than $61,750 but

less than $115,125, the corresponding rate is 22%. Step 2:

Because your total income with the payment, $82,000, is

greater than $61,750 but less than $115,125, the correspond-

ing rate is 22%. Because these two rates are the same, enter

“22” on line 2.

Example 2. You expect your total income to be $43,700

without the payment. Step 1: Because your total income

without the payment, $43,700, is greater than $26,200 but

less than $61,750, the corresponding rate is 12%. Step 2:

Because your total income with the payment, $63,700, is

greater than $61,750 but less than $115,125, the correspond-

ing rate is 22%. The two rates differ. $18,050 of the $20,000

payment is in the lower bracket ($61,750 less your total

income of $43,700 without the payment), and $1,950 is in the

higher bracket ($20,000 less the $18,050 that is in the lower

bracket). Multiply $18,050 by 12% to get $2,166. Multiply

$1,950 by 22% to get $429. The sum of these two amounts

is $2,595. This is the estimated tax on your payment. This

amount corresponds to 13% of the $20,000 payment ($2,595

divided by $20,000). Enter “13” on line 2.

Page 2 of 3

1.964543.108

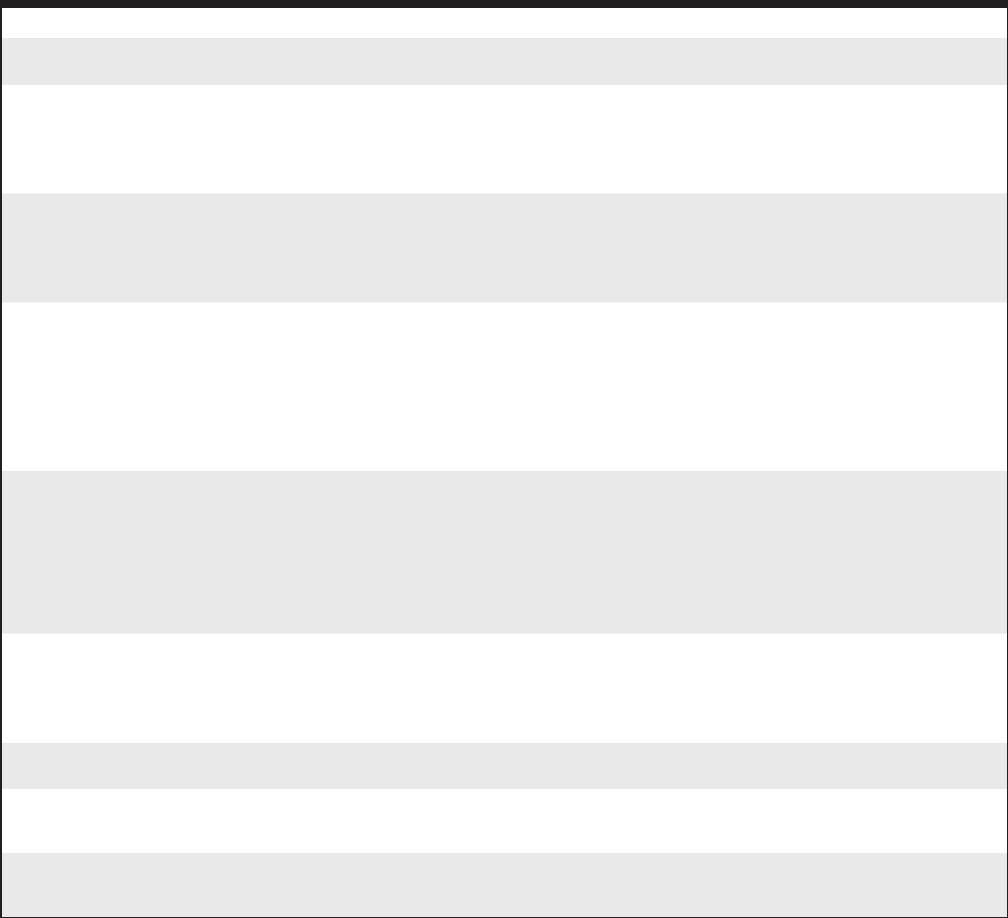

State Tax Withholding Information

State of residence State tax withholding options

AK, FL, HI, NH, NV, SD,

TN, TX, WA, WY

• No state tax withholding is available (even if your state has income tax).

IA, KS, MA, ME, OK, VT

• If you choose federal withholding, you will also get state withholding at your state’s minimum withholding

rate or an amount greater as specified by you.

• If you do NOT choose federal withholding, state withholding is voluntary.

• If you have state withholding, you can request a higher rate than your state’s minimum but not a lower rate,

except on Roth IRA distributions.

AR, CA, DE, MN,

NC, OR

• If you choose federal withholding, you will also get state withholding at your state’s minimum withholding

rate unless you request otherwise.

• If you do NOT choose federal withholding, state withholding is voluntary.

• If you have state withholding, you can request a higher rate than your state’s minimum but not a lower rate,

except on Roth IRA distributions.

CT, MI

• CT and MI generally require state income tax of at least your state’s minimum requirements regardless of

whether or not federal income tax is withheld.

• Tax withholding is not required if you meet certain state requirements governing pension and retirement

benefits. Please reference the CT or MI W-4P Form for additional information about calculating the amount

to withhold from your distribution.

• If you are subject to state tax withholding, you must elect state tax withholding of at least your state’s

minimum by completing the Tax Withholding section.

• Contact your tax advisor or investment representative for additional information about your state’s requirements.

DC

Only applicable if taking

a full distribution of entire

account balance.

• If you are taking distribution of your entire account balance and not directly rolling that amount over to

another eligible retirement account, DC requires that a minimum amount be withheld from the taxable

portion of the distribution, whether or not federal income tax is withheld. In that case, you must elect to

have the minimum DC income tax amount withheld by completing the Tax Withholding section.

• If your entire distribution amount has already been taxed (for instance only after-tax or nondeductible contributions

were made and you have no pre-tax earnings), you may be eligible to elect any of the withholding options.

• If you wish to take a distribution of both taxable and nontaxable amounts, you must complete a separate

distribution request form for each and complete the Tax Withholding section of the forms, as appropriate.

MS

• If you choose federal withholding, you will also get state withholding at your state’s minimum withholding

rate unless you request otherwise.

• If you do NOT choose federal withholding, state withholding will occur unless you request otherwise.

• If you have state withholding, you can request a higher rate than your state’s minimum but not a lower rate,

except on Roth IRA distributions.

OH

• State tax withholding is voluntary. If you choose state withholding, you can choose a higher rate than your

state’s minimum but not a lower rate, except on Roth IRA distributions.

SC

• SC requires state withholding if you have not provided a Tax ID or if you have been notified of a name/

Tax ID mismatch and have not resolved the issue. Otherwise, state tax withholding is voluntary and you can

choose the rate you want.

All other states

(and DC if not taking a

full distribution)

• State tax withholding is voluntary and you can choose the rate you want.

Important: Federal and/or state tax withholding rules can change, and the information cited above may not reflect the current legislation

and/or ruling of your state. Consult with your tax advisor, the IRS, or your state taxing authority to obtain the most up-to-date information

pertaining to your situation.

This tax information is for informational purposes only, and should not be considered legal or tax advice. Always consult a tax or legal

professional before making financial decisions.

We do not provide tax or legal advice and we will not be liable for any decisions you make based on this or other general tax information

we provide.

Fidelity Brokerage Services LLC, Member NYSE, SIPC; National Financial Services LLC, Member NYSE, SIPC 652041.9.0 (01/24)

Page 3 of 3

1.964543.108

Questions? Go to Fidelity.com/security/overview or call 800-343-3548.

Let’s Talk about Protecting Your Money

A wire transfer is an easy, convenient way to send money to people you know. If you provide your information or send money to a scammer,

though, there is often little we can do to help get your money back. Here are some examples of common scams, things to ask yourself

before sending any funds, and what to do next if faced with one of these scams. Remember, in EVERY scenario, the first step is to STOP

communicating with the person immediately!

Romance Scam

What is it? A romance scam is a fraudulent scheme in which a fraudster pretends romantic interest in a target, establishes a relationship,

and then attempts to get money or personal sensitive information from the target under false pretenses.

What to do next if you suspect you’re a victim:

• Talk to someone you trust about your new relationship.

• Do a reverse image search of the person’s picture to see if it’s associated with another name or if the details don’t match.

Grandparent Scam

What is it? A scammer calls or emails you, posing as either a relative in distress or someone claiming to represent the relative (such as a

lawyer or law enforcement agent). The caller explains that the “relative” is in trouble and needs them to wire funds “immediately” for bail

money, lawyer’s fees, hospital bills, or another fictitious expense.

What to do next if you suspect you’re a victim:

• Call the relative (or their parent) directly, at their known phone number.

• If told you have to act quickly, resist that urge.

• Verify, verify, verify!

Sweepstakes/Inheritance Scam

What is it? You receive a notice stating that you’ve won a “big prize” or have received an unexpected inheritance. You’re told that in order

to claim the “prize” or “inheritance,” you need to send funds to cover “processing fees” or “taxes.” Once the money is sent, you never see

your prize or inheritance.

What to do next if you suspect you’re a victim:

• Independently verify the information by consulting reputable resources. Do not rely on resources the scammer gives you, since they are

probably involved in the scam as well.

• Remember, you cannot win a sweepstakes you never entered!

Investment Scam

What is it? An investment scam involves the illegal or purported sale of a financial instrument. The typical investment scam is characterized

by offers of low or no-risk investments, guaranteed returns, etc.

What to do next if you suspect you’re a victim:

• Don’t trust a person or company just because they have a website; a convincing website can be set up quickly.

• Be cautious when responding to special investment offers, especially through unsolicited email.

• Check with other resources regarding this person or company, and inquire about all the terms and conditions.

Watch for red flags Here are some examples of red flags that should make you think twice before sending money.

• A person or company solicits business from you rather than your finding them on your own.

• The requestor asks you to send the wire to a name different from their own.

• After just a few contacts, they profess strong feelings for you and ask to chat with you.

• They threaten legal action if the funds are not sent “right away.”

• The wiring instructions seem unusual, they change, or you’re asked to go to a different financial institution.

• You are coached on how to respond to questions your financial institution might ask you regarding the transaction.

• If you met on a dating site, they will try and move you away from the site and communicate via chat or email instead.

• Messages may be full of typing errors, poorly written, or vague, and may escalate quickly if you show resistance.

• The messages or calls become more desperate and/or persistent, and if you do send money, they ask you to send more.

Remember, if it seems too good to be true, it probably is!

Your security is our top priority. We’re here to help. If you have any concerns or want to know more about how to help protect yourself, talk to a

Fidelity representative or visit Fidelity’s Security Center online at Fidelity.com/security/overview. 928234.1.0 (05/20)

Page 1 of 11.9899061.100