Answers to Frequently Asked Questions about

Conservation Use Valuation and

Preferential Agricultural Assessment

A p

resentation of the most frequently asked questions and answers collected

over the past several years for ad valorem tax issues in Georgia

Muscogee County Board of Assessors

3111 Citizens Way

Columbus, GA 31906

706-653-4398

1

Answers to Frequently Asked Questions about Conservation Use Valuation and

Agricultural Preferential Assessment

November 2022

Suzanne Widenhouse, Chief Appraiser

Muscogee County Board of Assessors

INTRODUCTION

Georgia Code Section 48-5-7.4 allows for up to 2,000 acres of real property of a

single owner, the primary purpose of which is any good faith production, including

but not limited to, subsistence farming or commercial production from or on the land

of agricultural products or timber who meet certain criteria of ownership to enter into

a ten year covenant agreement.

P

rimary purpose is defined as "the principle use to which the property is devoted, as

distinct from an incidental, occasional, intermediate or temporary use for some other

purpose not detrimental to, or in conflict with its primary use.

Th

is booklet contains a listing of questions and answers collected over the past

several years dealing with these ad valorem tax issues. A careful reading of these

contents will foster a better understanding among taxpayers of how these property tax

programs function.

C

UVA refers to Conservation Use Valuation Assessment

FMV refers to Fair Market Value

2

CONSERVATION USE VALUATION AND AGRICULTURAL

PREFERNTIAL ASSESSMENT

_______________________________________________________________________________

Which is better for me as a Muscogee County landowner: fair market value (FMV),

Agricultural Preferential Assessment, or Conservation Use Valuation Assessment (CUVA) of

my land?

It really depends on your planned use for the land over the life of the covenant. For qualified

landowners planning to continue the land use in agricultural or forest production, either program can

earn tax benefits and serve as an incentive for continued agricultural and forest production.

Agricultural Preferential Assessment generally provides a 25 percent tax advantage over the Fair

Market Value. (FMV)

Conservation Use Valuation can offer significant savings, in some cases greater than 50% from FMV.

Alternatively, to maintain a greater flexibility over the use of your land, accept a FMV basis for your

ad valorem taxes.

Why should I be interested in Conservation Use Valuation for ad valorem taxation?

All landowners who qualify for Conservation Use Valuation are entitled to have their land valued

according to its current use (agriculture, forestry, or environmentally sensitive) instead of the Fair

Market Value for ad valorem taxation. This can reap large tax benefits. Another benefit of CUVA is

that the value changes are limited to +/- 3 percent a year and a total of +/- 34.39 percent over the life

of the 10-year covenant.

Why should I be interested in Agricultural Preferential Assessment?

All landowners who qualify for Agricultural Preferential Assessment are entitled to have their property

valued for assessment at 75 percent of FMV for ad valorem taxation. In most cases, 25 percent tax

savings will be realized with Agricultural Preferential Assessment. However, Agricultural Preferential

Assessment values change as fast as FMV changes and offer no degree of certainty on the property

tax burden.

If Conservation Use Valuation offers large savings and appears to be more stable, why would I

consider Agricultural Preferential Assessment?

Agricultural Preferential Assessment applies to all land and up to $100,000 dollars in building value

on agricultural production and storage buildings. Conservation Use Valuation applies only to land

values and has no effect on building values. A taxpayer that has a small amount of land with a good

number of agricultural buildings, such as chicken farming, may receive greater benefits under

Agricultural Preferential Assessment.

How does the value of my land under the Conservation Use covenant change: per year, per 10

years?

Conservation Use values for land cannot change more than 3 percent per year or more than 34.39

percent over the life of the covenant.

3

Remember that your land will be taxed according to Fair Market Value at the end of the covenant

unless you renew the covenant.

Who is eligible for Conservation Use Valuation and/or Agricultural Preferential Assessment?

Natural or Naturalized Citizens

Family Farm Corporations who earns at least 80% of their income from farming

Non-profit conservation organizations, estates and trust may be eligible

What factors are considered in determining if my property is qualified?

The nature of the terrain

The density of the marketable product on the land

The past usage of the land

The economic merchantability of the agricultural product

The utilization or non-utilization of recognized care, cultivation, harvesting, and like practices

applicable to the product involved and the implementations of any plans

What are considered the allowable uses for a property in order to be eligible for conservation

use valuation?

The land uses required for Conservation Use Valuation are good faith agricultural/forest production

and environmentally sensitive land including:

Raising, harvesting or storing crops

Feeding, breeding or managing livestock or poultry

Producing plants, trees, fowl or animals

Production of aquaculture, horticulture, floriculture, forestry, dairy, livestock, poultry and

apiarian products

Maintaining a wildlife habitat (additional requirements may apply)

Must use 50% or more of the property in a qualifying use.

How do I sign up for one of these programs?

Forms and details are available at the County Board of Assessors Office. You can come by and pick

one up or one will be mailed to you upon request. The Board of Assessors requires the following

when submitting your application:

Application must be signed by all landowners along with percentage of ownership

Application must be notarized

Applicant must designate on tax map the exact parcel and acreage being placed in

covenant

Applications for less than 10 acres, must be accompanied by additional proof of

agricultural or forestry use to be considered

$25.00 Recording Fee collected upon filing of the application to the Board of Assessors.

Money order, cashier check or business checks only. The Clerk of Superior Court does not

accept personal checks.

You enter a 10-year covenant with the County whereby you agree to continue your property in

agricultural or forestry production.

4

When I sign up for one of these covenants, is it some way recorded with the deed to my land?

Once your application is approved, the filing fee previously collected and the covenant agreement will

be placed on record in the Clerk of Superior Court Office of Muscogee County. A title search of your

property should show that your property is under covenant. This is for the protection of both the

potential seller and/or buyer who may not be aware of the covenant, and any penalties that may occur

due to a transaction.

When can I sign up for either of these programs?

The earliest anyone may sign up for Conservation Use Valuation or Agricultural Preferential

Assessment is January 2 of each year. The filing time runs from January 2 until April 1.

In addition, every taxpayer receives an annual assessment notice. You may make application along

with, or in lieu of an appeal, during the 45-day appeal period. This must be done within 45 days of

the date of your annual assessment notice.

How much land can I enter into Conservation Use Valuation and/or Agricultural Preferential

Assessment?

Up to 2,000 acres in Georgia can be entered in Conservation Use covenants. At the same time, up to

2,000 other acres in Georgia may be entered into Agricultural Preferential Assessment. Presently there

is no minimum acreage for Conservation Use Valuation.

But, landowners with less than 10 acres must give additional proof that the "primary use" of the

property is for bona fide agricultural production purposes. If you file Internal Revenue Service

Schedule E, reporting farm related income or loss, or a Schedule F, with Form 1040, or, if applicable,

a Form 4835, pertaining to such property no further documentation is required.

If you do not file any of the above documents, you must provide documentation of bona fide

agricultural use on the property. This would include receipts of farm products purchased or sold.

How many Conservation Use Covenants can I have? Does all of my land have to be in the same

county?

You may have a separate covenant for each legally definable tract of land you own. No one covenant

can cross county lines or state boundaries. Separate covenants can be held in separate Georgia

counties. Tract means a parcel of property with boundaries designated by the Board of Assessors to

facilitate proper identification of the property on their maps and records.

What happens if I want to get out of the covenant before the 10-year period is up?

You are bound by legal agreement with Muscogee County for the duration of the 10-year covenant to

maintain the Conservation Use. There are four conditions under which you can end a covenant with

no penalty, or a one-year penalty. These are:

If you or any party to the covenant dies during the period of the covenant, the covenant ends. This is

considered a no penalty breach.

If any part of your property is taken, or is conveyed, to a party with the power of eminent domain, the

covenant may end. If this occurs, this is a no penalty breach.

5

If you become medically unable to continue the land in its qualifying use, the covenant ends. The

Board of Assessors requires letters from two (2) doctors stating the medical reason that a landowner

cannot continue to farm. If tax savings have been enjoyed during the year this occurs, then a one-year

penalty is applied.

If your land is taken from you through foreclosure, the covenant ends. If tax savings have been enjoyed

during the year this occurs, then a one-year penalty is applied.

Otherwise to get out of the covenant early you must pay a tax penalty equal to

twice the tax savings enjoyed to date, plus interest.

What are the penalties for breach of the Conservation Use Valuation and Agricultural

Preferential Assessment covenant?

Breaching a Conservation Use covenant results in a penalty that applies to the entire tract that is placed

under an original covenant, even if the breach occurred on only a small portion of the tract under

covenant. The penalty paid by the original covenant holder will be an amount equal to twice the

property tax savings incurred from the year the covenant was entered until it was breached, plus

interest.

In the event that a portion of the land under a Conservation Use covenant is sold to a qualifying

landowner, who later breaks the covenant, penalties also apply to the entire tract under the original

covenant. Under this condition, there will be a pro-rata assessment of the penalty against each of the

parties of the covenant in proportion to the tax benefit enjoyed by each. This means that the original

covenant holder will pay a fine based on the tax savings enjoyed on all of the acreage, from the

beginning of the covenant up to the time of sale of land, and of the breach. The subsequent covenant

holder would pay a fine based on the tax benefits enjoyed from the time of covenant land purchase up

to the time of the breach. Please be aware that the penalty plus interest constitutes a lien against the

property.

Penalties for the Agricultural Preferential covenant are assessed as the tax benefits enjoyed during

only the year of the breach, times a factor of:

•5 if breached during the 1

st

or 2

nd

year

•4 if breached during the 3

rd

or 4

th

year

•3 if breached during the 5

th

or 6

th

year

•2 if breached during the 7

th,

8th, 9

th

or 10th year

The landowner in the original covenant pays the penalty.

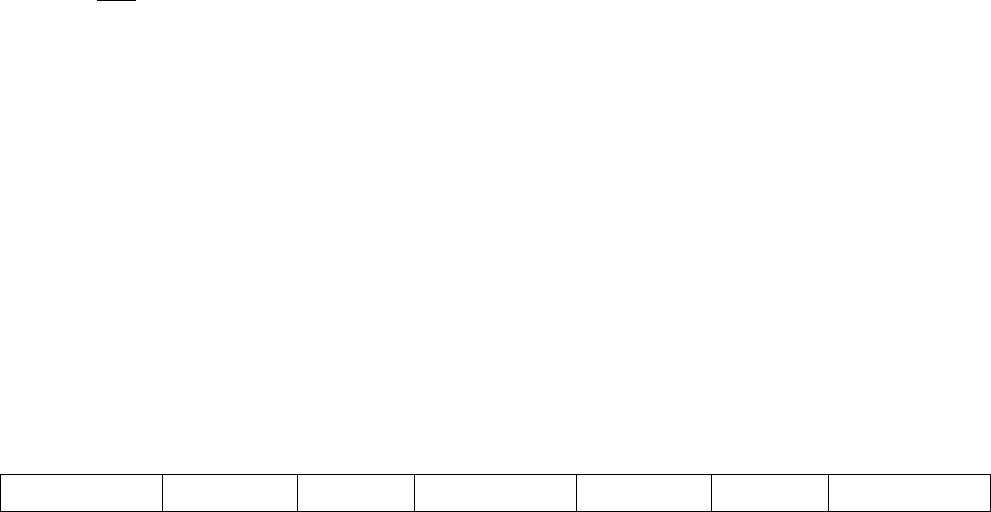

Exactly how is a Conservation Use breach penalty calculated?

The Board of Assessors office maintains the FMV of the property for each year of the covenant. They

also calculate the CUVA value for the property. The difference between the actual FMV and the

CUVA value becomes an annual exemption for the taxpayer. The tax savings benefit is calculated

from the amount of the exemption.

The following is an example of how a penalty might be calculated if a covenant was breached in the

6

th

year of the agreement, and the parcel is vacant with no homestead exemptions.

FAIR

MARKET

CURRENT

USE

EXEMPT

AMOUNT

MILLAGE RATE

TAX

SAVINGS

PENALTY

$ AMOUNT

PENALTY

6

VALUE

VALUE

*

195,000

92,000

41,200

.03350

$ 1380.20

X 2

$2760.40

195,000

94,760

40,096

.03120

$1250.90

X 2

$2501.80

260,000

97,600

64,960

.03280

$2130.60

X 2

$4261.20

260,000

100,500

63,800

.03275

$2089.40

X 2

$4178.80

260,000

103,500

62,600

.03270

$2047.00

X 2

$4094.00

288,000

106,600

72,560

.03258

$2364.00

X 2

$4728.00

TOTAL PENALTY

DUE AT

BREACH

$22,524.20

*Exempt amount is the difference between the FMV and the CUVA value multiplied times the assessment

level of 40 percent.

(195,000 - 92,000 = 103,000 X .40 = 41,200)

The penalty amount will vary from covenant to covenant due to the fact that the FMV and the CUVA

value will be different for each parcel.

A

s shown above, the FMV changed between the second and third year. Thus the penalty amount

increased between the second and third year. This demonstrates the importance of keeping up with

the FMV, even though you are not being taxed on that amount.

I

n fact the tax amount due under Conservation Use for the first year would be $1,232.80. Without the

Conservation Use covenant, the tax due would be $2,613.00. So as you can see this covenant can offer

substantial tax savings.

Looking at the previous chart, what would be the penalty if I breached the covenant due to

foreclosure or a medically demonstrated illness during the 6

th

year?

I

f the covenant is breached due to foreclosure or a medically demonstrated illness, and tax benefits

have been received for that year, then only the penalty amount due for the year in which you breach is

due. Under one of these circumstances, the penalty due would be $4,728.00.

Can I change agricultural/forestry uses of the Conservation Use covenant land during the 10-

year period?

Yes, you can change among good faith production of agriculture or forestry crops provided that you

notify the Muscogee County Board of Assessors in writing of the intended use change. Failure to

notify constitutes a breach of the covenant with penalties as described.

Can I sell land that is under the Conservation Use Covenant?

Y

es. But to avoid a penalty, the buyer must continue the terms of the original covenant and enter a

new continuance Conservation Use covenant for the land purchased. The buyer must also be someone

who is eligible to enter into an original covenant. The sign-up period for the new owner is during the

next year’s regular sign-up period, January 1 through April 1. The landowner under the original

covenant remains in that covenant, unless all land under covenant was sold. But the original covenant

holder still remains legally responsible for any penalty assessed against benefits earned before the sale.

W

hen selling land under covenant, it may be wise to have your attorney include language with the

property deed requiring the new owner to continue land use under provisions of the original covenant.

What happens if my spouse and I jointly own property entered in a Conservation Use Covenant

and we divorce during the covenant period with one of us gaining the deed to the property?

7

Department of Revenue Regulations state that when there is a change in ownership of property

receiving current use assessment, the new owner must apply for a continuation of the covenant. This

application must be made on or before the deadline for filing returns, which is April 1.

In the event of a divorce, the original parties to the covenant remain liable for any breach of the

covenant. Responsibility for penalties due to a covenant breach should be specified in divorce decrees,

contracts, etc.

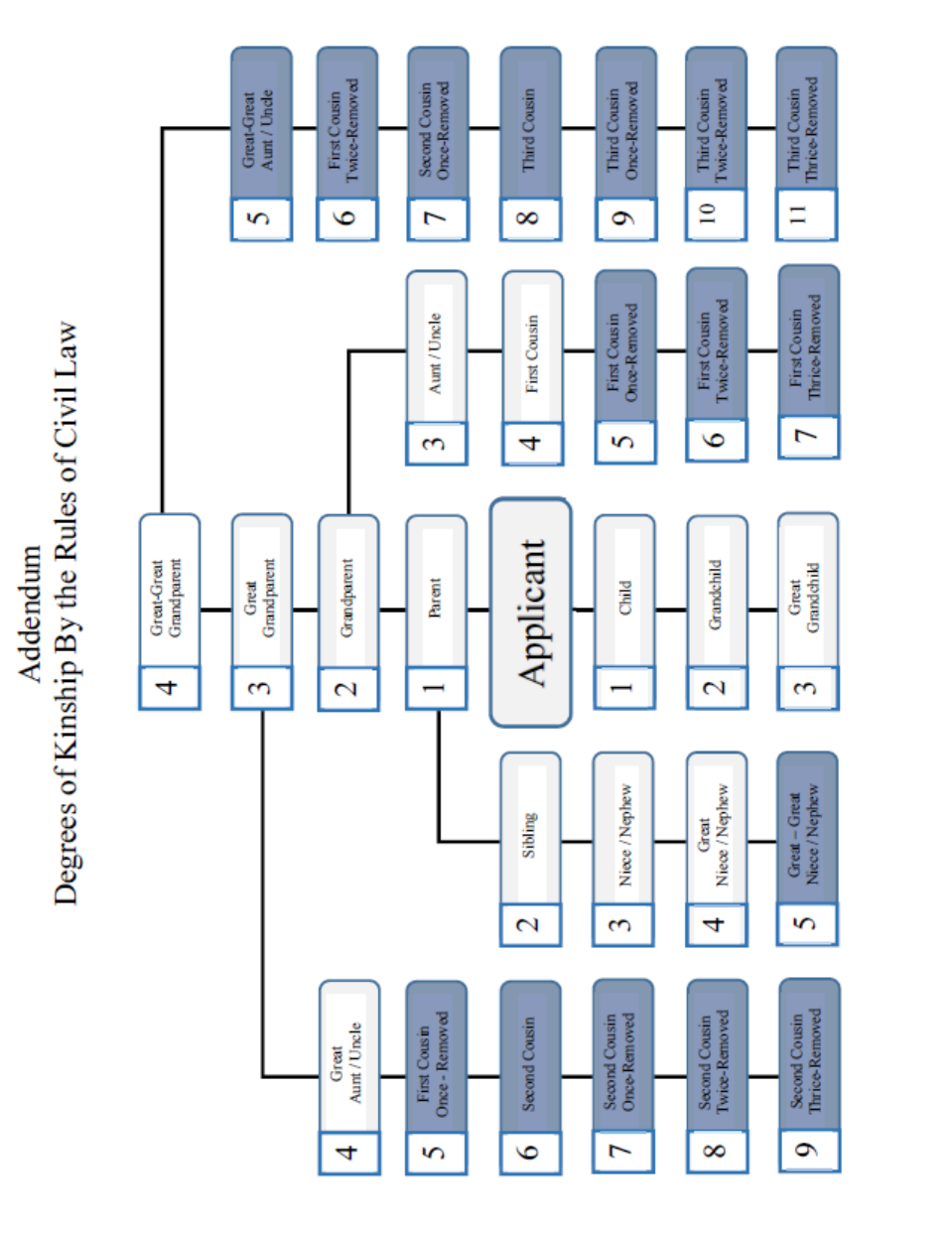

Can members of my family build a home and live on Conservation Use Covenant land?

1. The part of the property so transferred (by plat and deed) is to be used for single-family

residential purpose. Starting within one year of the start date for the building of the dwelling and

continuing for the remainder of the covenant period, the residence is to be occupied within 24

months from the date of the start by a person who is related within the fourth degree of civil

reckoning to an owner subject to the covenant. (see attached addendum for description of

Degrees of Kinship)

2. The part of the property so transferred, taken together with any other part of the property so

transferred to the same relative during the covenant period, does not exceed a total of five acres;

and in any such case the property so transferred shall not be eligible for a covenant for bona fide

conservation use.

What happens if the original covenant holder dies during the life of the covenant or cannot

carry out the requirements of the covenant?

If the original covenant holder dies before the Conservation Use or Agricultural Preferential covenant

expires, the agreement is nullified, and the covenant ends without penalty, or the heirs have the option

to continue the covenant without penalty.

If the property owner ends the covenant because of a foreclosure or medically documented illness, the

covenant is breached. But only the tax savings incurred in that particular year will be forfeited.

Under these circumstances, the property owner may not be eligible to immediately reapply.

What happens if the County or State wants some of my land for right-or-way?

When a public body (government) acquires the land through eminent domain, the covenant ends. You

may be entitled to sign up again, if you choose.

Property that is either given or sold to schools and power companies would also include in this group.

What do I do if I want to enter my land in a Current Use Covenant but feel that I may want to

develop some of the land before the 10 years is up?

The best approach would be to enroll only the land that you intend to keep in the qualifying uses for

the life of the covenant. This means to create a new legal description for separate tracts.

For example, if you own 100 acres and feel you may want to develop or sell a portion during the 10

year covenant period, you will be required to submit a legal description to the Board of any property

that will not be included in the covenant. This legal description can be by deed or by survey.

8

Can I lease my covenant land out for hunting, pine straw harvest, charging of admission for

fishing purposes or other qualifying uses without penalty?

When one-half or more of the area of a single tract of real property is used for a qualifying purpose,

then such tract shall be considered as used for such qualifying purpose unless some other type of

business is being operated on the unused portion; provided, however, that such unused portion must

be minimally managed so that it does not contribute significantly to erosion or other environmental or

conservation problems. The lease of hunting rights or the use of the property for hunting purposes

shall not constitute another type of business. The charging of admission for use of the property for

fishing purposes shall not constitute another type of business

Can I lease my covenant land for other purposes, such as cell towers?

Leasing a portion of the property subject to the covenant, but in no event more than six acres of every

unit of 2,000 acres, for the purpose of placing thereon a cellular telephone transmission tower. Any

such portion of such property shall cease to be subject to the covenant as of the date of execution of

such lease and shall be subject to ad valorem taxation at fair market value.

Caution should be taken if you are considering leasing for any purpose other than cell towers, hunting

or agricultural purposes.

What is the status of my house and yard if I currently enrolled in an Agricultural Preferential

or Conservation Use covenant and also live on the property?

For Agricultural Preferential

and Conservation Use, Georgia law now states: Such property

excludes the entire value of any residence and its underlying property; as used in this subparagraph,

the term "underlying property" means the minimum lot size required for residential construction by

local zoning ordinances or two acres, whichever is less. This provision for excluding the underlying

property of a residence from eligibility in the conservation use covenant shall only apply to property

that is first made subject to a covenant or is subject to the renewal of a previous covenant on or after

May 1, 2012.

Covenants entered into before May 1, 2012 are not subject to this portion of the law, unless they

transfer ownership, and are required to file for a continuance application. It also applies if you acquire

new acreage and request it to be added to an existing covenant.

In Muscogee County, the minimum lot size required for residential construction is TWO acres. If you

have more than one residence on the property, two acres must be cut out for each residence/mobile

home.

If I own 10.75 acres and my house, and I have to have my house cut out with two acres, would

I be required to submit additional information?

Yes. If your tract is 10.75 acres, with a residence, you must cut the house and two acres out.

Your application for conservation use would be based on 8.75 acres and subject to the requirements

for tracts 10 acres and less.

If you have a tract of 12 acres or less with a residence, you must cut the house out plus 2 acres and

would be subject to the same requirement.

9

Can I sell my house and yard that is located on Conservation Use covenant land, or rent it out,

without breaking my covenant agreement, even when the remaining land stays in the qualifying

use?

No. Leasing is permitted if the lessee meets the qualification under O.C.G.A. § 48-5-7.4 (a)(1)(C) and

the use remains the same as the original covenant. Owner must notify the Muscogee County Board of

Board of Assessors if there are any changes to the original covenant to determine if a breach has

occurred.

If I acquire additional acreage that joins my property under a covenant, can I include it with

my covenant?

If a qualified owner has entered into an original bona fide conservation use covenant and subsequently

acquires additional qualified property contiguous to the property in the original covenant, the qualified

owner may elect to enter the subsequently acquired qualified property into the original covenant for

the remainder of the ten-year period of the original covenant; provided, however, that such

subsequently acquired qualified property shall be less than 50 acres.

"Contiguous" means real property within a county that abuts, joins, or touches and has the same

undivided common ownership. If an applicant's tract is divided by a county boundary, public roadway,

public easement, public right of way, natural boundary, land lot line, or railroad track, then the

applicant has, at the time of the initial application, a one-time election to declare the tract as contiguous

irrespective of a county boundary, public roadway, public easement, public right of way, natural

boundary, land lot line, or railroad track.

If this occurs, you would be subject to the changes in the law that require any residence and two acres

(if applicable) to be delineated out at the time you opt to combine properties.

What if I want to change between Agricultural Preferential Assessment and Conservation Use

Valuation?

There is no apparent time limit set by Georgia law on when you can change from an existing

Agricultural Preferential Assessment covenant to a Conservation Use covenant. However, you can

change from Preferential Assessment to Conservation Use, for a particular covenant, only once.

You cannot change from an existing Conservation Use covenant to a new Agricultural Preferential

Assessment covenant except at the end of the Conservation Use agreement.

How much is my land worth under the Conservation Use covenant? Who decides what it is

worth? How is a particular piece of land given a value?

Conservation Use land value is based on its use, location and soil productivity. Annually the Georgia

Department of Revenue publishes a table of values for all Conservation Use land in Georgia. The

table of values is available at the Muscogee County Board of Assessors Office, University of Georgia

Cooperative Extension Service County Office, the Georgia Forestry Association, Georgia Farm

Bureau Federation and the Georgia Forestry Commission.

Once your application has been approved, the acreage of your parcel is broken down by soil

classification. Then the soil types are costed against the above table and totaled for a new Conservation

Use value.

10

While my land is in a Conservation Use covenant, how do I keep up with its Fair Market Value

(FMV)?

Th

e Board of Assessors Office will continue to notify the taxpayer of any changes to the FMV of the

covenanted property. Remember the difference between FMV and Conservation Use value is the basis

for calculating any penalty. So, pay careful attention each year to the FMV of your land, even while

in a protective covenant.

What happens if I want to divide my property for estate planning purposes or deed off portions

while I am in the covenant?

I

f you do not change the use of the property, each party may be eligible to file for continuance of the

original covenant. It would be wise to discuss this with the Board of Assessors office to make sure

that the division will be done in a manner that would not breach the covenant.

The Board of Assessors should be consulted before building any improvements on property

divided for estate planning purposes.

If I choose to place my property into a LC, LLC, LP, Family Farm Corporation etc., for estate

planning purposes or other income tax purposes, how will this affect my covenant?

If property is placed in any of the above, there are specific requirements under the law. The partnership

or family farm corporation MUST derive 80% of its income from bona fide agricultural production

purposes within this state. It may NOT receive more than 20% of its income from other non-related

agricultural purposes, such as dividends on stocks and bonds other non-agricultural investments, rental

income, etc. The property tax along with any maintenance fees are expenses to the property in which

income derived from the property is used to pay such expenses and such income must be at least 80%

from bona fide agricultural use.

A

ll parties of the partnership or corporation must be related to each other within the fourth degree of

civil reckoning (see addendum containing Degrees of Kinship), except that there is an allowance for

a non-related 5% ownership for management purposes.

Th

e Muscogee County Board of Assessors will require the following along with your application under

these circumstances:

C

opy of your certificate of corporation filed with the Secretary of State

Copy of the income tax return for the partnership or corporation, and

An affidavit that the parties are related to each other in accordance with the law

What happens if I divide my property or sell it, and the new owners do not come in and file for

a continuance covenant?

T

he Board of Assessors will send both the transferee and the transferor a notice of the Board’s intent

to assess a penalty for the breach of the covenant. The notice shall be entitled Notice of Intent to

Assess Penalty for Breach of a Conservation Use Covenant and shall set forth the following

information:

*T

he requirements of the new owner of a property currently under a “Covenant” to apply for a

continuation within 30 days of the date of postmark of the notice;

11

*T

he new owner of a property currently receiving current use assessment must continuously devote

the property to an applicable bona fide qualifying use for the duration of the covenant;

*

The change to the assessment if the covenant is breached, and;

*T

he amount of the penalty if breached.

If I make application, what will the Board of Assessors look at to determine if I qualify?

T

he Board will review the current use of the property. An appraiser from the Board of Assessors

Office will perform an on-site inspection of the property and prepare a report for the Board of

Assessors.

Y

ou should submit any documentation you have regarding the bona fide conservation use of the

property. Examples would be:

F

ederal Income Tax Schedule “E” or “F”

Timber Management Plans

Receipts of sale of hay, livestock, produce, etc.

Receipts for purchase of feed, fertilizers, seed, equipment, etc.

Any documentation that will assist the Board in determining the qualifying use.

If I have property that has been under a conservation use or preferential agricultural covenant

for 10 years, will my covenant automatically be renewed at the end of the 10 years?

N

o. You must sign a release of the first 10-year covenant and the exemption ends, The Board of

Assessors office will send you notification that your covenant is about to expire.

Y

ou must make application for a new 10-year covenant, if you desire the exemption to continue.

If you apply for your second 10-year period, on the exact same tract, it is considered a RENEWAL

COVENANT.

If I had the exemption before, I should automatically qualify again, right?

N

ot necessarily. Ten years is a long period, and many changes can occur.

C

hanges in ownership, changes in use and other factors may have occurred that need to be reviewed.

A

lso, since this type of covenant was originally placed into law in 1992, there have been changes made

to the law, as well as changes to state regulations. Other changes have occurred due to court cases

that clarify the law. These changes include making it more difficult for smaller tracts to enter into

these covenants, clarification of the type of income allowed (no, non-agricultural related rental

income) and clarification of the definition of primary use of the property.

Were there any changes that benefit the taxpayer?

Yes, the law now states that if you enter into a second ten-year covenant, it is considered a renewal

covenant.

I

f you decide to sell your property or change the use during the 6

th

though the 10

th

year of your renewal

covenant, you only have to pay the taxes that would have been due if you were not in the covenant.

12

The

re is no penalty amount, but you do have to pay taxes at the fair market basis for years you have

been in the renewal covenant.

Th

ere is also a change that allows for an early out provision, if any one of the parties of the covenant

turns 65 years of age during a renewal covenant.

What do I do if I am turned down for a Current Use covenant?

If

your application is turned down, you may appeal the decision of the Board of Assessors. This must

be done, in writing, within 45 days of the date of the letter of notification. If you supply additional

documentation as proof of qualification, the Board will review your documents. If upon further review

your application is still denied, your appeal will be forwarded to the Board of Equalization for a

hearing.

If I have questions, who and where do I call for answers?

Any time you have questions regarding making application, or changing the use of your property,

you can contact one of the following persons at the Muscogee County Board of Assessors Office at

706-653-4398:

Paul Borst – Residential Division

Manager

Jeff Milam – Commercial Division Manager

Leilani Floyd – Administrative Division Manager

Glen Thomason – Deputy Chief Appraiser

Suzanne Widenhouse - Chief Appraiser/ Secretary to Board of Assessors

13

Answers to Frequently Asked Questions about Conservation Use Valuation and

Agricultural Preferential Assessment

Prepared by: S. Widenhouse

Chief Appraiser

Approved for Distribution by: S. Widenhouse

Muscogee County Board of Assessors J. Govar, Chairman

T. Carmack, Vice Chairman

T. Hammonds, Assessor

L. Sandifer-Hicks, Assessor

K. Jones, Assessor

___________________________________________________________________

For Further Information Contact:

Muscogee County Board of Assessors Office

Monday – Friday

8:00 a.m. – 5:00 p.m.

706-653-4398

14