FactSet OnDemand – Web Services

Reference Manual

Doc version - 2.0.2

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

2

Revision History

Effective Date

Version Number

All Sections

Changes Made

11/08/2021

2.0.2

Copyright and template

updated.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

3

Table of Contents

Revision History ....................................................................................................................................................... 2

Notice ......................................................................................................................................................................... 5

Trademarks ............................................................................................................................................................... 5

FactSet Consulting Services .................................................................................................................................. 6

Preface ...................................................................................................................................................................... 7

Intended Audience ............................................................................................................................................... 7

1. Introduction .......................................................................................................................................................... 8

1.1. FASTFetch Service ...................................................................................................................................... 8

1.1.1. Factlets ................................................................................................................................................... 8

2. HTTPS Requests and Responses .................................................................................................................... 8

2.1. OnDemand URL Syntax .............................................................................................................................. 8

2.2. Optional Query String Parameters ............................................................................................................. 9

2.2.1. Example URLs ....................................................................................................................................... 9

2.2.2. Format................................................................................................................................................... 11

2.2.3. Orientation ............................................................................................................................................ 11

3. FactSet Languages ........................................................................................................................................... 12

3.1. FactSet Screening Language ................................................................................................................... 12

3.2. FactSet Query Language .......................................................................................................................... 12

3.3. Date Format ................................................................................................................................................ 12

3.3.1. Absolute Dates .................................................................................................................................... 12

3.3.2. Relative Dates ..................................................................................................................................... 13

3.4. Understanding Rotated Databases.......................................................................................................... 13

3.5. OnDemand Factlet Requests ................................................................................................................... 15

3.5.1. Standard Factlets ................................................................................................................................ 15

3.5.2. Specialized Factlets ............................................................................................................................ 15

4. ExtractDataSnapshot ........................................................................................................................................ 17

5. ExtractFormulaHistory ...................................................................................................................................... 23

6. CorporateActionsDividends .............................................................................................................................. 27

7. CorporateActionsSplits ..................................................................................................................................... 34

8. ExtractBenchmarkDetail ................................................................................................................................... 38

9. ExtractOFDBItem ............................................................................................................................................... 44

10. ExtractScreenUniverse ................................................................................................................................... 50

11. ExtractOptionsSnapshot ................................................................................................................................. 53

12. ExtractSPARData ............................................................................................................................................ 55

13. ExtractVectorFormula ..................................................................................................................................... 61

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

4

14. ExtractEconData .............................................................................................................................................. 66

15. ExtractAlphaTestingSnapshot ....................................................................................................................... 72

16. LSD_Ownership ............................................................................................................................................... 78

17. UploadToOFDB ............................................................................................................................................... 82

17.1. Creating a New OFDB ............................................................................................................................. 82

17.2. Modifying an Existing OFDB ................................................................................................................... 82

18. EstimatesOnDemand ...................................................................................................................................... 84

18.1. Estimates Report - Actuals ..................................................................................................................... 86

18.2. Estimates Report – Broker Snapshot .................................................................................................... 89

18.3. Estimates Report – Consensus ............................................................................................................. 90

18.4. Estimates Report – Guidance ................................................................................................................ 91

18.5. Estimates Report – Surprise ................................................................................................................... 92

18.6. Estimates Report – Consensus Recommendation ............................................................................. 94

18.7. Estimates Report – Detailed Recommendation ................................................................................... 95

18.8. Appendix .................................................................................................................................................... 97

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

5

Notice

This manual contains confidential information of FactSet Research Systems Inc. or its affiliates

("FactSet"). All proprietary rights, including intellectual property rights, in the Licensed Materials will

remain property of FactSet or its Suppliers, as applicable. The information in this document is subject to

change without notice and does not represent a commitment on the part of FactSet. FactSet assumes no

responsibility for any errors that may appear in this document.

Trademarks

For FactSet Research Systems trademarks and registered trademarks, all rights reserved. For

information about he the third-party software that is delivered with the product, refer to the third-party

license file on your installation media that is specific to your release. All other brand or product names

may be trademarks of their respective companies.

FactSet is a registered trademark of FactSet Research Systems, Inc.

Microsoft is a registered trademark, and Windows is a trademark of Microsoft Corporation.

Linux is a registered trademark of Linus Torvalds.

Cisco is a trademark of Cisco Systems, Inc.

UNIX ® is a registered trademark of The Open Group.

Intel is a registered trademark of Intel Corporation.

XWindows is a registered trademark of Massachusetts Institute of Technology.

All other brand or product names may be trademarks of their respective companies.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

6

FactSet Consulting Services

North America - FactSet Research Systems Inc.

United States and Canada

+1.877.FACTSET

Europe – FactSet Limited

United Kingdom

0800.169.5954

Belgium

800.94108

France

0800.484.414

Germany

0800.200.0320

Ireland, Republic of

1800.409.937

Italy

800.510.858

Netherlands

0800.228.8024

Norway

800.30365

Spain

900.811.921

Sweden

0200.110.263

Switzerland

0800.881.720

European and Middle Eastern countries not listed above

+44.(0)20.7374.4445

Pacific Rim- FactSet Pacific Inc.

Japan Consulting Services (Japan and Korea)

0120.779.465 (Within Japan)

+81.3.6268.5200 (Outside Japan)

Hong Kong Consulting (Hong Kong, China, India, Malaysia,

Singapore, Sri Lanka, and Taiwan)

+852.2251.1833

Sydney Consulting Services

1800.33.28.33 (Within Australia)

+61.2.8223.0400 (Outside Australia)

E-mail Support

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

7

Preface

This document describes how to use the FactSet OnDemand DataFeed service that provides data and

calculations for client applications via a URL call to a web server at FactSet.

Intended Audience

The users should be familiar with the XML language and HTTPS protocol. This document will describe

the syntax needed for proper request formatting as well as the rules for processing responses. In addition,

complete code examples are included, which further illustrate the use of this service.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

8

1. Introduction

OnDemand provides synchronous access to data via the standard HTTPS protocol. Data can be returned

in several formats. You can make custom requests by changing the request URL to contain the

parameters you need.

1.1. FASTFetch Service

The OnDemand FASTFetch service from FactSet Research Systems provides data and calculations for

your applications via a URL call to a web server at FactSet. You receive data via pre-configured templates

that use FactSet FQL and Screening codes. Data is returned in various standard and customized formats,

such as XML or delimited text.

1.1.1. Factlets

The basic building block of FASTFetch is a FactSet Applet or “Factlet”. These Factlets are application

components that encapsulate business logic and data collection procedures. A Factlet can be a simple

data request or can invoke complex application logic. Factlets support multiple result formats that you

can choose from (e.g., XML, Delimited, Excel).

The key features of FASTFetch are:

• Adaptability – The flexibility of this model provides access to data beyond a simple security-based

requests, into requests for benchmark, aggregates, and economic data to name a few.

• Speed and Efficiency – FASTFetch is capable of cross referencing and dealing with time series for

a high amount of data in a relatively quick period of time. These can be simple requests of multiple

identifiers and codes over time or can be used for massive daily feeds, which would ordinarily take

days to run.

• Expanding Output Viewing – FASTFetch outputs can be changed via the orientation parameter of

the Factlets, allowing different ways of viewing data. Orientation is the term given to the rows and

columns retrieved by Factlets based on the entity, time, or item information. By changing the

orientation of these arguments, the data is returned in the way you desire.

2. HTTPS Requests and Responses

Receiving data via FASTFetch OnDemand is accomplished via simple URL requests that returns results

in flexible formats. A standard “name=value” pairing convention is used within the URL providing

consistency along with the power of customization.

The Factlet parameter specifies the stored procedure to generate the data. There are many standard

Factlets available.

2.1. OnDemand URL Syntax

A URL can be divided into the following arguments:

<protocol>://<base URL>/<service>?<optional query string parameters>

Example

https://datadirect.factset.com/services/FASTFetch?Factlet=ExtractFormu

laHistory&ids=fds

where:

Protocol

OnDemand information is transmitted via the HTTPS protocol for secure data delivery. In the above

example, the protocol argument is https.

Base URL

The base URL argument identifies the host web address and base path of a OnDemand service. In the

above example, the base URL is datadirect.factset.com/services.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

9

Service

The service argument identifies the OnDemand service being called. In the previous example, the service

argument is FASTFetch, which is a request to the FactSet OnDemand Service. Other OnDemand

services include, but are not limited to: DataFetch, DFSnapshot, Chart, and Research.

Factlet Name

The Factlet name argument identifies the name of the Factlet to call. Factlet name is a required argument;

if it is not defined, the URL will fail. In the above example, the Factlet name is

Factlet=ExtractFormulaHistory.

2.2. Optional Query String Parameters

Optional parameters can be supplied in the URL or in the POST part of the request, depending on the

length of their values (i.e. long lists of Ids are best sent with a POST).

Parameter

Description

ids

lists entity identifiers separated by commas

items

lists FactSet data items (e.g., P PRICE)

dates

lists the start date, end date, and frequency, separated by colons (:),

currency

specifies the currency the data is returned in, using a three-character ISO code

(e.g., ‘USD’ or ‘EUR’)

format

specifies the format of the data returned (e.g., “EXCEL”), default is XML

orientation

specifies the layout of the data returned (e.g., “EIT”), default is “None”

cutoff

specifies the maximum number of entities in a download, usually used with a

Factlet that returns a large universe

Ison

specifies the FQL value that extracts universe; e.g., ison_sp500 is entered as

ison=sp500 and

ISON_MSCI_WORLD(0,1) is written as ison=msci_world

isonParams

specifies ison codes that use parameters; e.g., ISON_MSCI_WORLD(0,1) is

written as isonParams=0,1

The optional query string specifies a list of service-specific parameters. The query string begins after the

Factlet name and contains a list of name=value pairs separated by ampersands (&).

2.2.1. Example URLs

The following examples explore how altering the URL will change the results returned for a given

FASTFetch call.

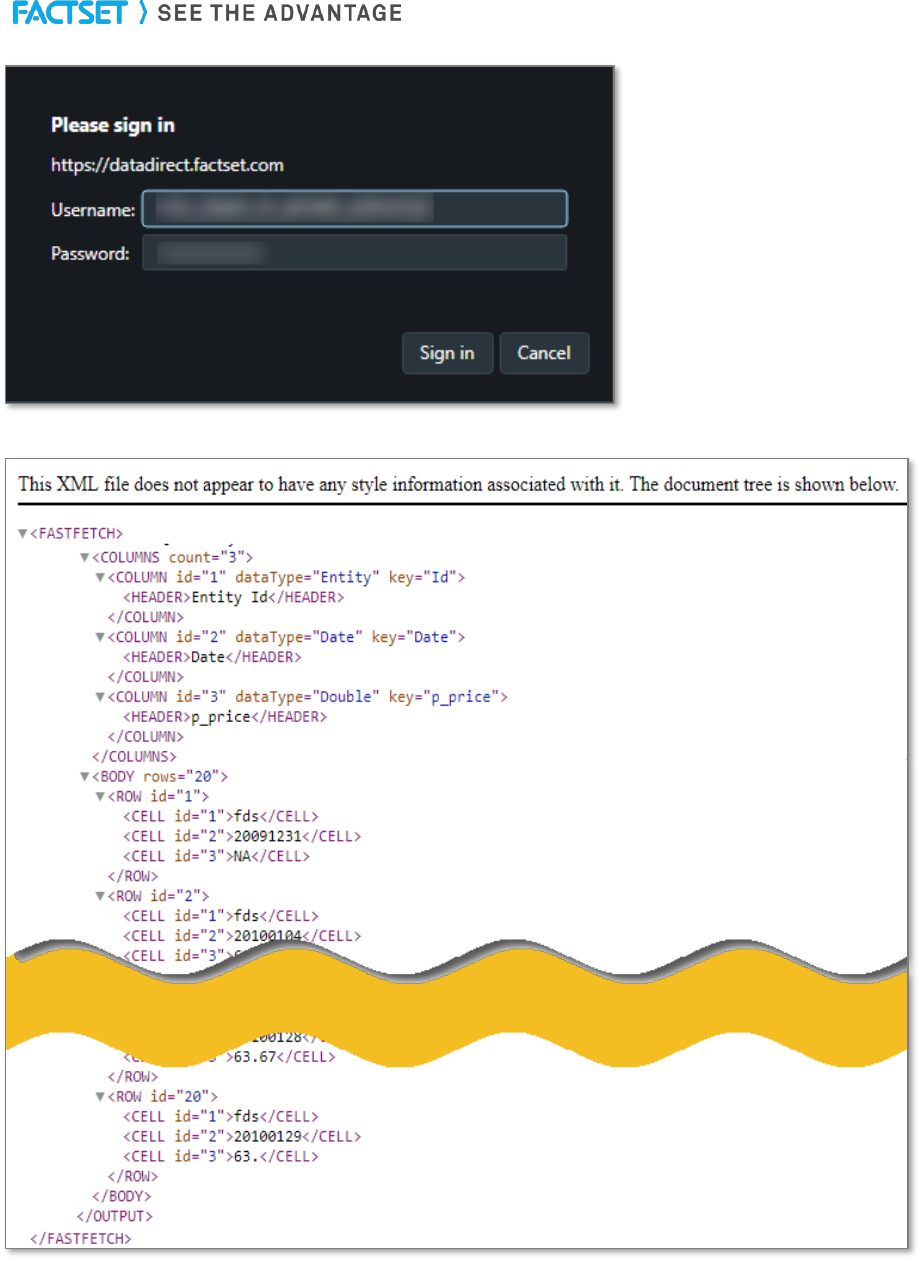

In the following FASTFetch example, company data is requested for the identifier FDS (FactSet) using the

ExtractFormulaHistory Factlet. The price at the end of the month between January and September of 2010

is requested. The data is oriented by equity, time, and item (i.e. price in this example).

https://datadirect.factset.com/services/fastfetch?factlet=ExtractFormulaHis

tory&ids=fds&dates=20100101:20100130&items=p_price&orientation=eti&format=x

ml

After providing authentication, data for the requested entities will be returned:

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

10

This data can be returned in multiple formats, such as XML, PIPE, or CSV by changing the format

argument in the URL.

Special Characters in the URL

Notice the “%20” within the URL. This is a URL encoded space and is needed in most web browsers to

ensure that the URL is read correctly, and the data is returned in a proper manner. While some browsers

do support spaces in the URL, it is recommended to use “%20” in place of a space to avoid any data

retrieval issues.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

11

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmark

Detail&format=xml&ids=SP50&items=_SP_CLASS_GICS(0,,,%20%27%27SEC%27%27,%20

%27%27NAME%27%27)&dates=0

This is especially important when using certain formula libraries in your URL, some libraries have spaces

in their name, while other have underscores. Omitting the “%20” or the substitution of an underscore in

place of the “%20” can result in either a broken URL, or the retrieval of incorrect data so it is important

that the “%20” is used properly.

2.2.2. Format

The following formats are supported by FactSet OnDemand. Custom formats can be developed according

to an application’s specification. By default, format is set to return in XML.

Parameter

Description

XML

Extensible Markup Language

PIPE

Vertical bar delimited (“|”) rows and columns

CSV

Comma Separated Values in rows and columns with values appropriate for reading

into Microsoft Excel

HTML

HyperText Markup Language

2.2.3. Orientation

There are three main dimensions to the data returned by FASTFetch: entity, data item, and time. The

order of layout is controlled by the orientation parameter. The value should be set to some combination

of the letters, “E”, “I”, and “T”. For example, the “ETI” layout for a “PIPE” formatted file is shown below.

The first two dimensions appear in the first two columns and the last dimension is displayed along the

rows.

ETI Orientation with “PIPE” Format

Extract Data - Entity x Time X Item

Entity Id | Date | p_price | p_volume

Entity | Date | Double | Double

Id | Date | p_price | p_volume

IBM|3-Jan-2005|97.75|5301.4 IBM|4-Jan-2005|96.7|5711.

PG|3-Jan-2005|55.19|4858.5 PG|4-Jan-2005|54.5|5548.6

There is also a “none” orientation that places one value to an entry and labels the Data Items in their own

column. It is by default if no orientation is specified.

Sample None Orientation with “PIPE” Format

Extract Data

Entity Id | Date | Date Item_Value

Entity | Date | String | Variant

Id | Date | DataItem | Value

IBM | 1/3/2005 | p price|97.75

IBM | 1/3/2005 | p volume | 5301.4

For additional information, see Online Assistant page 14233.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

12

3. FactSet Languages

FactSet stores all the available data in proprietary database structures on FactSet computers. This allows

FactSet to adjust the way data is stored, so that clients can access data as efficiently as possible.

Most datasets available on FactSet are stored in two different ways, so as to facilitate two different data

access methods. These two options use the FactSet Query Language (FQL) for timeseries requests and

the FactSet Screening Language (Screening) to efficiently extract data for a large universe of securities

as of a single date.

3.1. FactSet Screening Language

To facilitate efficient access to a data item of a single time period for a universe of securities, FactSet offers

an optimized cross-sectional data access method with the Screening Language. Given a data item, for

example EPS, and a time period. For example, Q4 2010, data for every entity in the specified universe can

be fetched using the Screening Language.

By default, the FactSet Screening Language does not allow iteration and therefore cannot be used to

return a time series of data with a single request code. To request data of a single historical date, it can

be specified either as an absolute or a relative date.

Note: Certain screening formulas are current only. If an option for a date argument is not available when

selecting a formula means that the formula does not accept a date reference.

3.2. FactSet Query Language

FQL is a proprietary data retrieval language used to access FactSet data.

The advantages of using FQL are:

• The ability to specify dates for any database using the same formats. With FQL, date formats are

flexible. You can use a number of consistent date formats (defined by FQL) for all databases which

makes using and combining data from different databases easier than ever.

• The ability to iterate items, formulas, and functions at any frequency. With FQL, you can iterate items,

formulas, and functions at any frequency. For example, you can request a series of weekly price to

earnings ratios.

• To request a time-series of data, a start date, end date and frequency needs to be specified. If a date

is not specified, data is returned from the most recent time period. The dates can be designated as

absolute dates or relative dates.

3.3. Date Format

The following sections explain how to define the Absolute and Relative dates.

3.3.1. Absolute Dates

FactSet Screening Language helps you define the absolute dates in the following manner:

Date Format

Description

Example

MM/DD/YYYY

Specific day

Note: DD/MM/YYYY is not a valid date

format

7/11/1999

MM/YYYY

Month-end

6/1999

YY/FQ or YYYY/FQ

Fiscal quarter-end

1999/1F, 2000/3F,

2001/2F

YY/CQ or YYYY/CQ

Calendar quarter-end

1999/1C, 00/3C,

2001/1C

YY or YYYY

Fiscal year-end

2000, 01, 1999

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

13

3.3.2. Relative Dates

Relative dates represent a date relative to the most recently updated period.

For example:

• 0 (zero) - represents the most recently updated period; The zero date is determined by the default

time period or the natural frequency of the data being requested. Zero (0) when used with monthly

data indicates the most recent month end.

• -1(Negative one) - represents the time period prior to the most recently updated. Negative one (-1)

when used with annual data indicates one fiscal year prior to the most recently updated fiscal year.

The following table lists the Relative Date Arguments and its descriptions.

Arguments

Description

D

0D is the most recent trading day, -1D is one trading day prior to most recent trading

date.

WE

0WE is the most recent trading weekend, -1AW is the one actual week (7 days) prior

to the most recent trading week.

W

0W is the last day of the most recent trading week (usually Friday), -1W is the last

trading day of the prior week.

AM

0AM is the most recent trading day, -1AM is the same day, one actual month prior to

most recent trading day.

M

0M is the last trading day of the most recent month, -1M is the last trading day of the

prior month.

AQ

0AQ is the most recent trading day, -1AQ is the same day 3 months prior to most

recent trading day.

Q

0Q is the last trading day of the company’s most recent fiscal quarter, -1Q is the last

day of the prior to most recent fiscal quarter.

CQ

0CQ is the last trading day of the most recent calendar quarter (March, June,

September, or December), -1CQ is the last trading day of the prior calendar quarter.

AY

0AY is the most recent trading day, -1AY is one actual year (365 days) prior to most

recent trading day.

Y

0Y is the last trading day of the company’s most recent fiscal year, -1Y is the last

trading day of the prior fiscal year.

CY

0CY is the last trading day of the most recent calendar year (the last trading day in

December), -1CY is the last trading day of the prior calendar year.

3.4. Understanding Rotated Databases

FactSet has two primary engines for retrieving data: Data Downloading and Universal Screening. The

Data Downloading engine is non-rotated and the Universal Screening engine is rotated.

Note: When you use Screening syntax to download data, the formula relies on the Screening engine;

therefore, it uses rotated data.

FactSet's databases containing company information are used in two different ways:

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

14

1. To generate reports or charts on data for a particular company.

Example:

Price History report - you may use this report to view High, Low, Close, and Volume information

for a single company, such as IBM.

2. To search through many companies' data in order to screen for companies or to generate aggregate

statistics on sets of companies.

Example:

Universal Screening application - you may use this application to find all companies with an EPS

greater than $2.

If only one database were available on FactSet, it would take too long to be able to accommodate both

of the above features in an efficient manner. FactSet needed to develop an intelligent method of laying

the data out on disk to make the "read operation" on the database as efficient as possible.

The solution was to have two copies of the database - one for each of the above desired features.

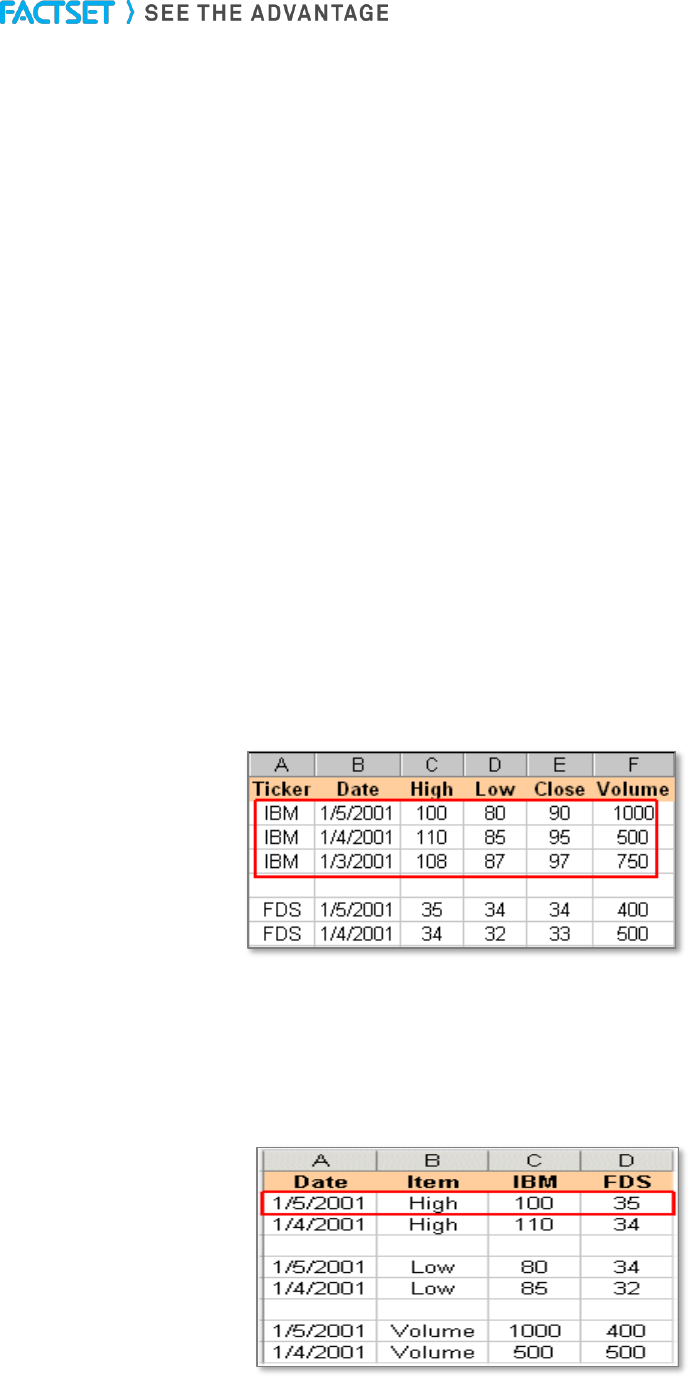

FactSet uses a non-rotated database for the single-company reports, and a rotated database for

Universal Screening and quantitative modeling applications, such as Alpha Testing.

FactSet first updates the single company database version. Next, a program runs to "rotate" the

database each night. The program reads through the single-company database (record by record) and

re-sorts the database by date to generate a rotated database file.

From a user's perspective, you are using the same database, only in different ways.

Example:

• Non-rotated database - The FactSet Daily Prices database is used in the Price History report.

All the data for IBM is consolidated in one part of the database, allowing FactSet to quickly read the

data from the disk and generate a report/chart, such as a price chart. (The data within the red box is

accessed in one "read" of the database, making the Price History report fast.)

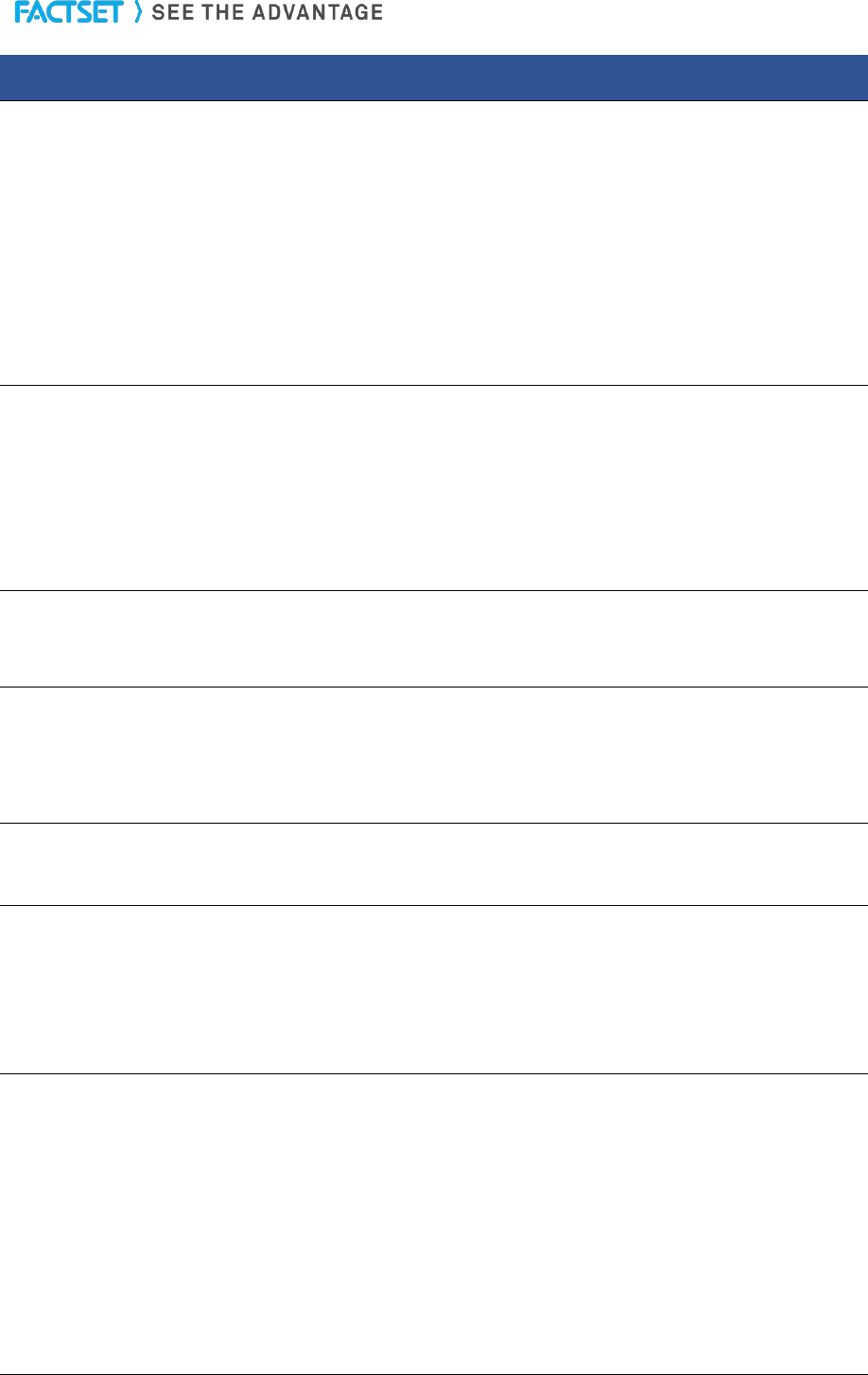

• Rotated database - The FactSet Daily Prices database is used in the Universal Screening application.

In this database, the data is sorted by date and by type (basically, the non-rotated database is flipped

on its side). The data within the red box is accessed in one read. For example, in one read, you can

quickly get the high price for all companies in the database for 1/5/2001. If you used the non-rotated

database to perform this task, the process would take very long because every piece of data for each

company would need to be read.

Note: All databases created since 1994 (otherwise referred to as FDB), including OFDB databases, rotate

automatically.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

15

3.5. OnDemand Factlet Requests

The following is a list of the Factlets available using OnDemand Web Service, MATLAB, R, Developer’s

Toolkit and SAS integrations. Not all Factlets are available in all integrations. The description for each

Factlet also highlights if the Factlet should be used with FQL or Screening syntax.

The Factlets should be chosen depending on the dataset required. There are general Factlets using either

actual screening or FQL codes as input (to find the correct code please use the FactSet Sidebar look-up

dialog) and specialized Factlets used for specific datasets.

3.5.1. Standard Factlets

The Standard Factlets below are used for Screening data, Economics data and FQL data. For the exact

input syntax, the FactSet Sidebar dialog box can be used.

3.5.2. Specialized Factlets

The specialized Factlets are developed for different content sets or specialized data structures. These

Factlets have been developed to simplify and standardize the data retrieval of more complex data

structures.

Factlet

FactSet syntax used

by Factlet

CorporateActionsDividends

Function is used for extracting stock dividend information.

FQL

CorporateActionsSplits

Function is used for extracting stock split information

FQL

EstimatesOnDemand

Function provides access to FactSet sourced company level estimates data.

The data is accessed through the following reports that are available with this

function: Actuals, BrokerDetail, BrokerSnapshot, Consensus, Guidance,

Surprise, Detailed Recommendations and Consensus Recommendations.

FQL

ExtractAlphaTestingSnapshot

Function provides access to data from AlphaTesting model results. Alpha

Testing is a tool available in the FactSet workstation used to assess the

relationship between one or more variables and subsequent returns over time.

A subscription to Alpha Testing in FactSet is necessary to extract this data in

the stat packages.

FQL

ExtractDataSnapshot

Function is used for extracting one or more items for a list of ids for 1 date,

both for equity or fixed income securities. Should be used to efficiently extract

data for a large universe of securities as of a single date.

The data can also be retrieved using a backtest date to avoid look-ahead bias

in the analysis. The backtest functionality is available to clients subscribing to

one of FactSet’s quantitative applications, such as Alpha Testing or Portfolio

Simulation.

Screening

ExtractEconData

Function provides access to a broad array of macroeconomic content,

interest rates and yields, country indices and various exchange rate

measures from both the FactSet Economics and the Standardized Economic

databases.

FQL

ExtractFormulaHistory

Function is used for extracting one or more items for one security, an index or

a list of securities over time.

FQL

Factlet

FactSet syntax

used by Factlet

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

16

Factlet

FactSet syntax used

by Factlet

ExtractBenchmarkDetail

Function is used for extracting multiple data items for a benchmark. Benchmark

data can be retrieved using other functions, such as with

ExtractFormulaHistory, but the ExtractBenchmarkDetail function allows a user

to retrieve a more comprehensive overview of the index constituent data,

without additional codes or calculations. In the default output, identifiers are

sorted in descending order by weight in the index and each row shows the

index id, company id, date, ticker, and weight. Additional items are displayed at

the end.

Screening

Note: The Extract-

BenchmarkDetail

function by default uses

Screening codes entered in

the Items argument of the

syntax. If using an FQL

code, enter an _ before the

FQL items code.

ExtractOFDBItem

Function provides access to a list of securities and multiple data items for a

range of dates uploaded into a single Open FactSet Database (OFDB).

Screening

Note: The Extract-

OFDBItem function by

default uses Screening.

FQL should be used when

using ids with spaces or

short positions, indicated in

the OFDB with an _S.

ExtractOFDBUniverse

Function provides access to a list of securities belonging to a single Open

FactSet Database (OFDB) file as of a single date.

FQL

ExtractScreenUniverse

Function used for extracting a list of Identifiers stored in a single FactSet

screen. In the FactSet workstation, a user can screen for securities based on

specified criteria and store the result using FactSet Universal Screening for

equity or debt securities.

Screening

ExtractOptionsSnapshot

Function is used for extracting options data for one or more conditions from the

FactSet-Options Derived Values database

FQL

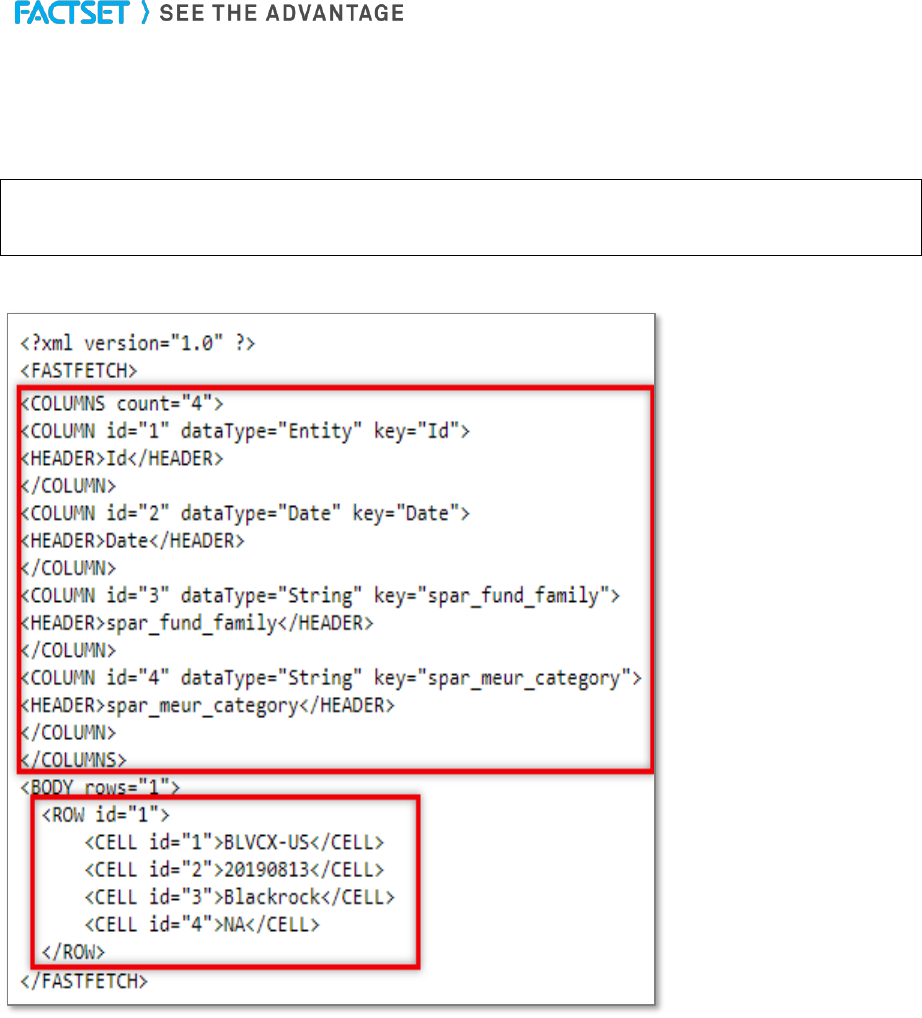

ExtractSPARData

Function is used for displaying SPAR data for specified funds from databases

that includes S&P, Lipper, Morningstar, Russell, eVestment, Nelson,

Rogerscasey, and PSN. A subscription to SPAR in FactSet is necessary to be

able to extract this data in stat packages.

FQL

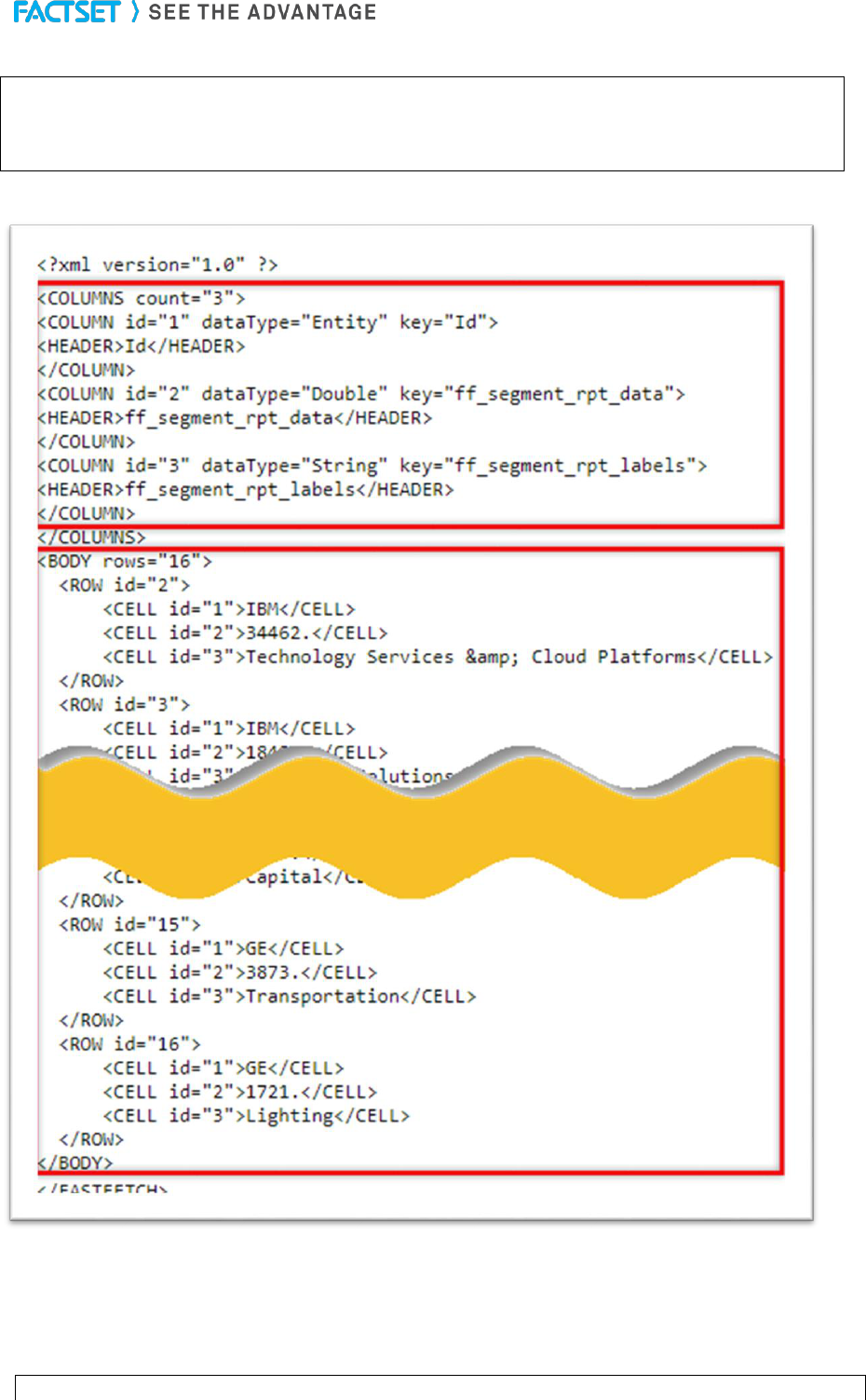

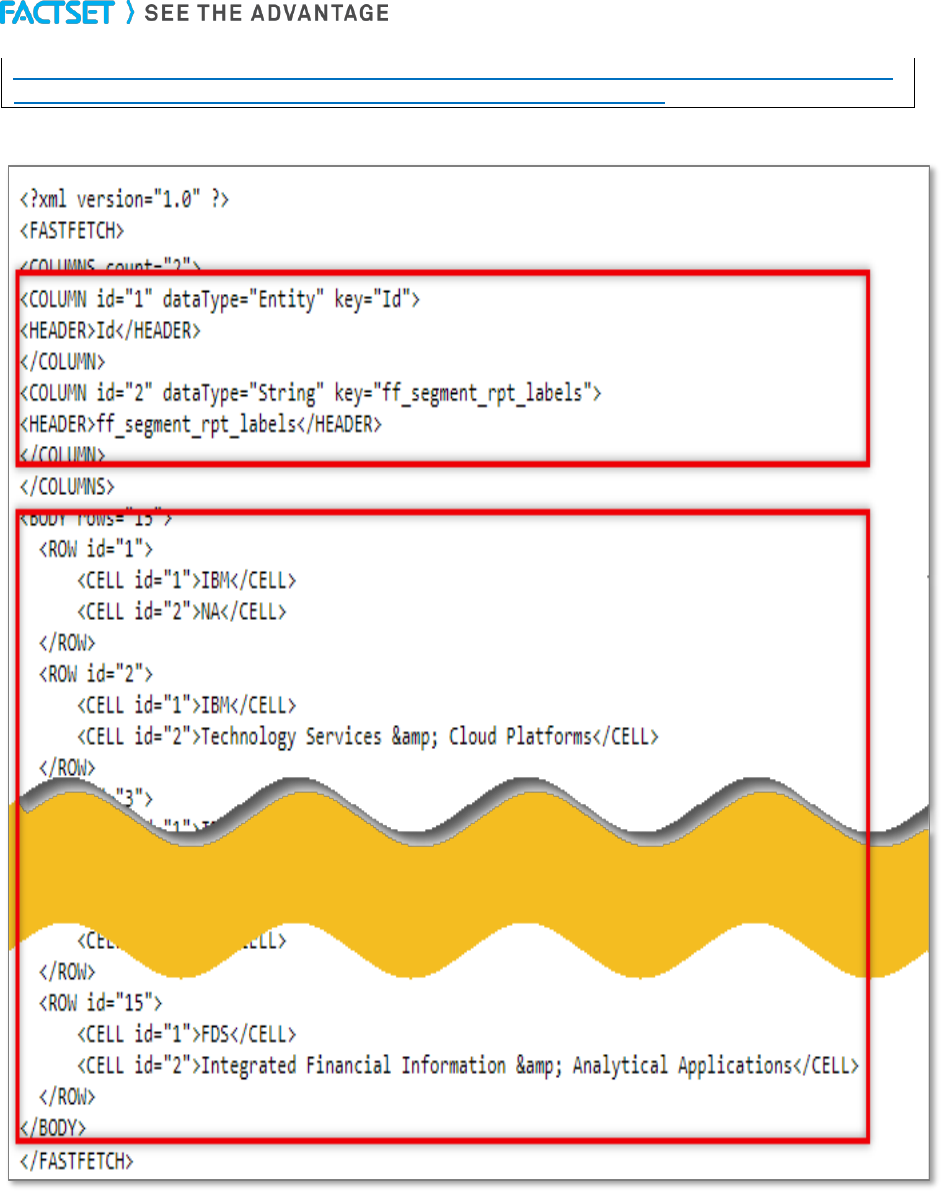

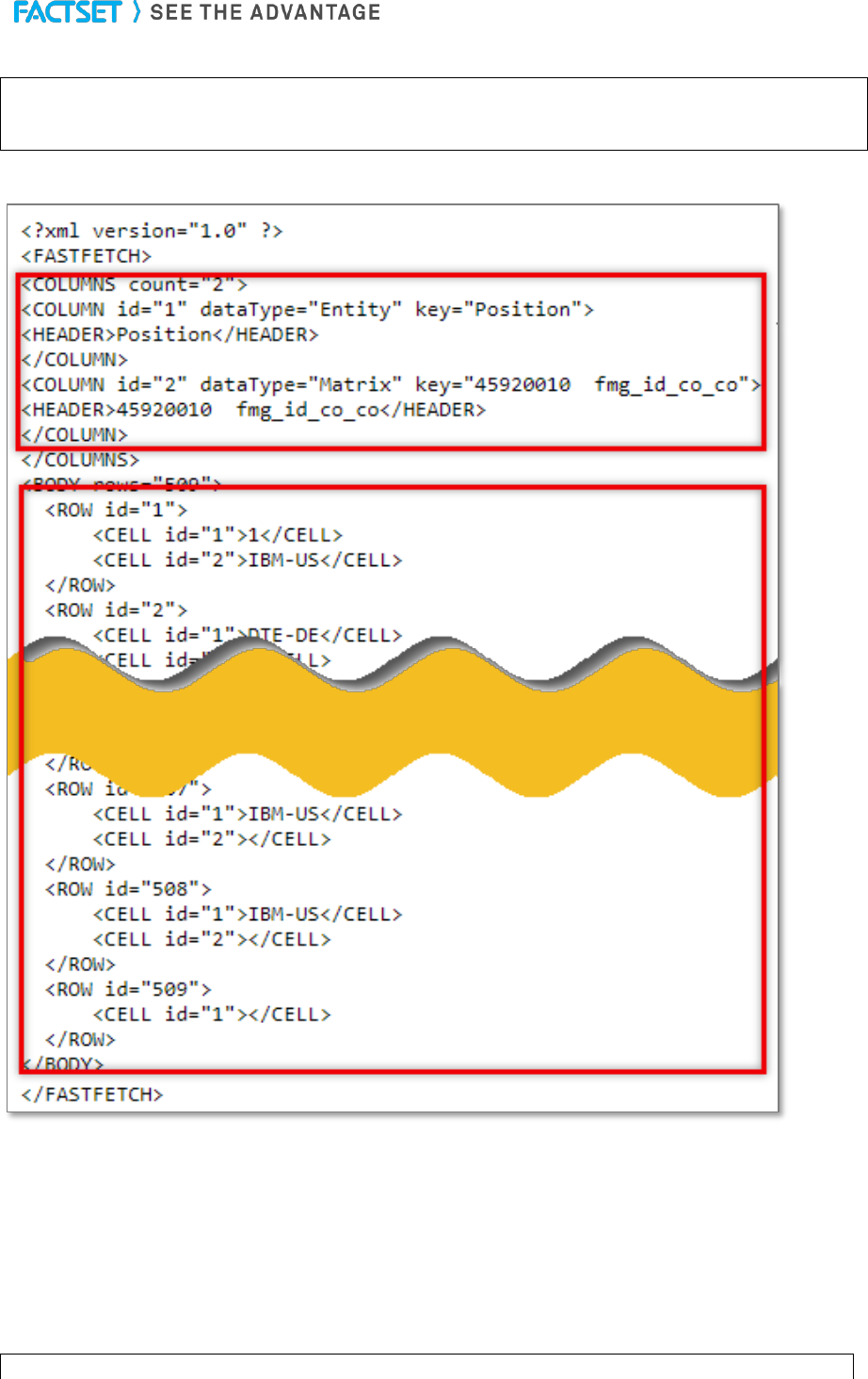

ExtractVectorFormula

ExtractVectorFormula function is used for extracting FactSet data that is stored

in a vector data format, where the data array does not have a predefined size

and is organized by the vector position. A vector can be thought of as a list that

has one dimension, a row of data. A vector position allows for a particular

element of the array to be accessed.

ExtractVectorFormula handles non-sequential data with support for matrix or

vector output. The nature of the data determines if the output is a matrix or

vector, it is not specified in the function to choose which format the data is

returned in. This type of data includes corresponding geographic or product

segment breakdowns for a company or detailed broker snapshot or history

estimates/analyst information.

FQL

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

17

Factlet

FactSet syntax used

by Factlet

LSD_Ownership

FactSet Ownership database collects global equity ownership data for

institutions, mutual fund portfolios, and insiders/stake holders. Detailed

ownership data can be extracted by company or by holder (institution, mutual

fund, and insider/stake). The LSD_Ownership function is used for extracting

one or more data items from the FactSet Ownership database for one or

multiple securities or holders.

FQL

4. ExtractDataSnapshot

The ExtractDataSnapshot function is used to efficiently extract data for multiple ids for a single date. This

function uses FactSet Screening Language. The FactSet Screening Language is a way to efficiently

extract data for a large universe of securities as of a single date.

The data can also be retrieved using a backtest date to avoid having look-ahead bias in the analysis. The

backtest functionality is available to clients who subscribe to FactSet’s quantitative applications in the

workstation, such as Alpha Testing and Portfolio Simulation.

The syntax for the ExtractDataSnapshot function is-

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractDataSnapshot&ids=&items=&date=&o

ptioanal_arguments.

where,

Optional arguments

curr

The currency in which the data is to be returned, using a string with the three-

character ISO code (e.g. ‘USD’ or ‘EUR’).

cal

Calendar setting, arguments include:

• FIVEDAY: Displays Monday through Friday, regardless of whether there

were trading holidays.

• FIVEDAYEOM: Displays Monday through Friday including a weekend date if it

falls on the last day of the month. When the month-end does not fall on a

weekend, the calendar will act just as the standard five-day calendar.

• SEVENDAY: Displays Monday through Sunday.

• AAM: For Exchange code, uses the calendar of a specific exchange,

represented by the exchange code. If there is no calendar available for a

specific exchange, the calendar will default to FIVEDAY.

universe

Screening expression to limit the universe

ison

Ison-codes can be used to limit the universe ISON_MSCI_WORLD(0,1) is written

as ‘ison’,’msci_world’,’isonParams’,’0,1’

isonParams

The arguments within brackets in the ison-code

data

variable name for the data returned

ids

CellString array with a list of one or multiple security identifiers

items

CellString array with a list of one or more FactSet data items in the Screening language

backtestDate

The backtest date for which the data is retrieved. If no date is specified, a backtest date will

not be set. The date can be entered using a relative date or absolute date.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

18

OFDB

Universe is the constituents of an OFDB file, default directory is Client, if the OFDB

is stored in another location the path must be included

OFDBDate

Specific date for the constituents of the OFDB

universeGroup

Specifies what mode of screening to use. The default screening mode is Equity. For

Fund screening and Debt screening the universeGroup argument has to be used

with either FUND or DEBT respectively.

decimals

Positionally set according to the items in the selection, i.e. ‘decimals’,’,,3,4,3’

Example 1

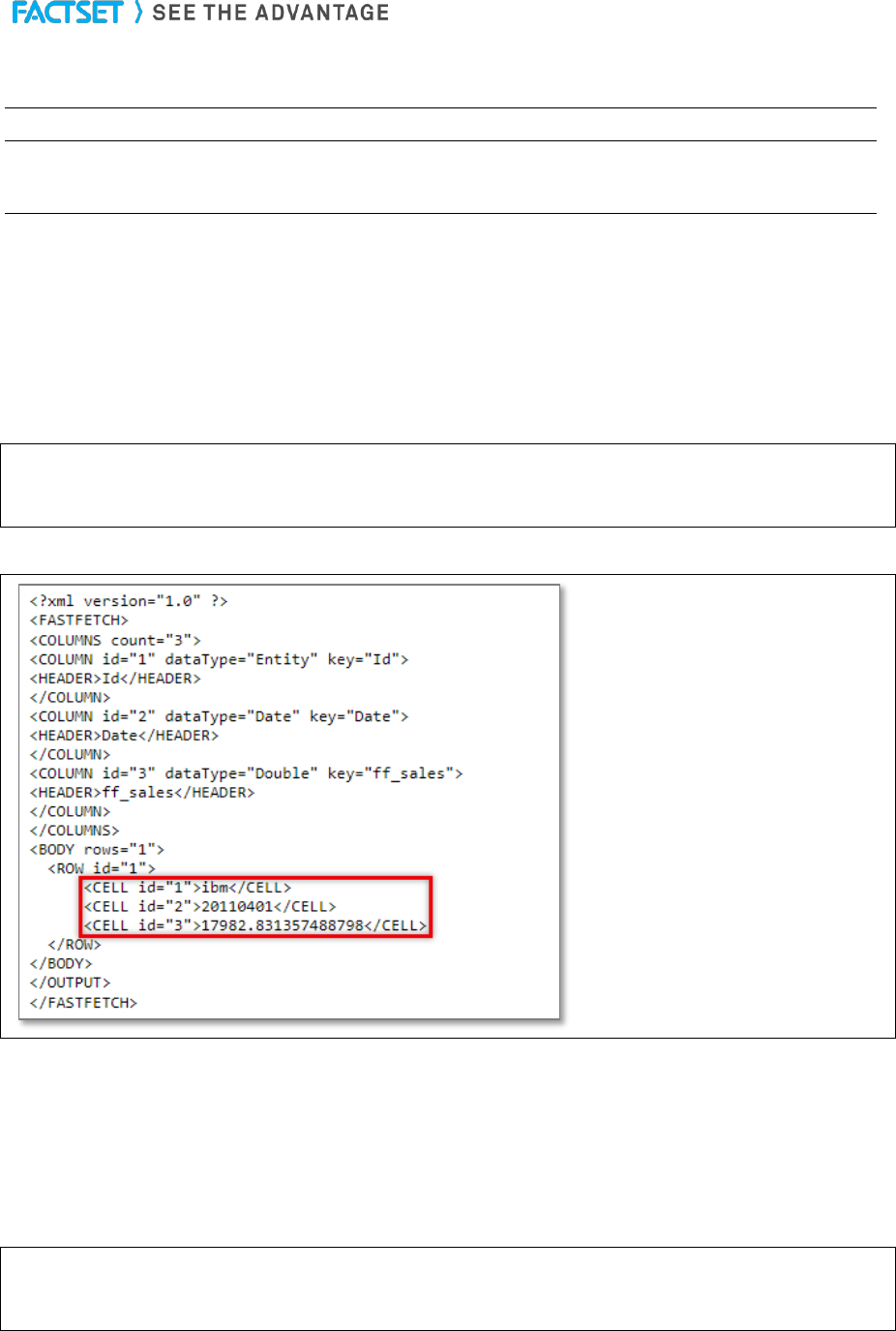

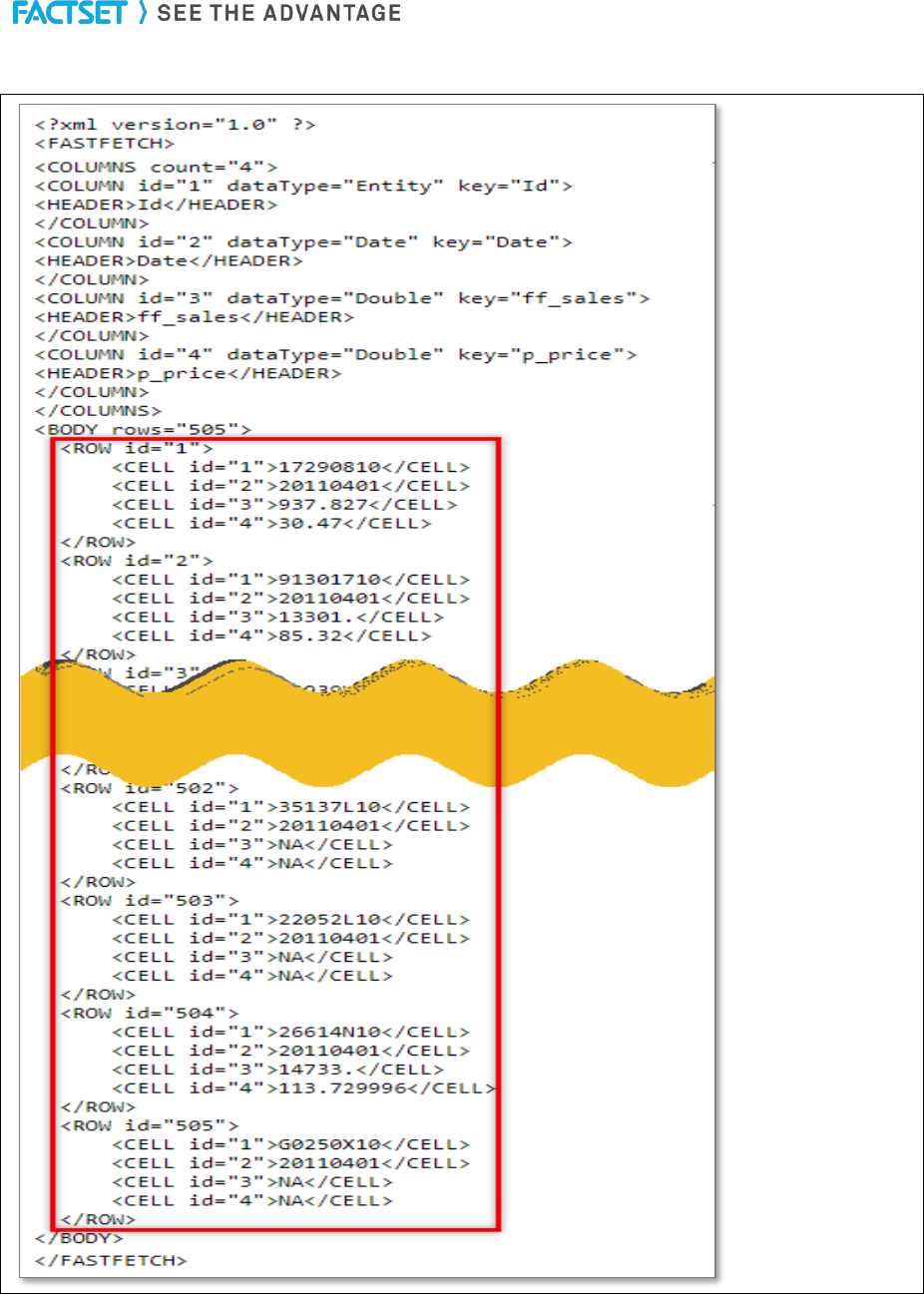

This example uses the standard Screening syntax to retrieve the quarterly sales value from the FactSet

Fundamentals database for IBM using the Screening code FF_SALES (QTR,20110401,RF,EUR). The

data is retrieved in currency set to Euro, as of 04/01/2011. The RP default argument in the FactSet

Fundamentals database codes reflects that the data is the Latest Preliminary for the Reported Period

(alternative arguments could be for example RF, for the Latest Fully Reported Period, among others).

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractDataSnapshot&ids=ibm&items=FF_S

ALES(QTR,20110401,RP,EUR)&dates=20110401

Output

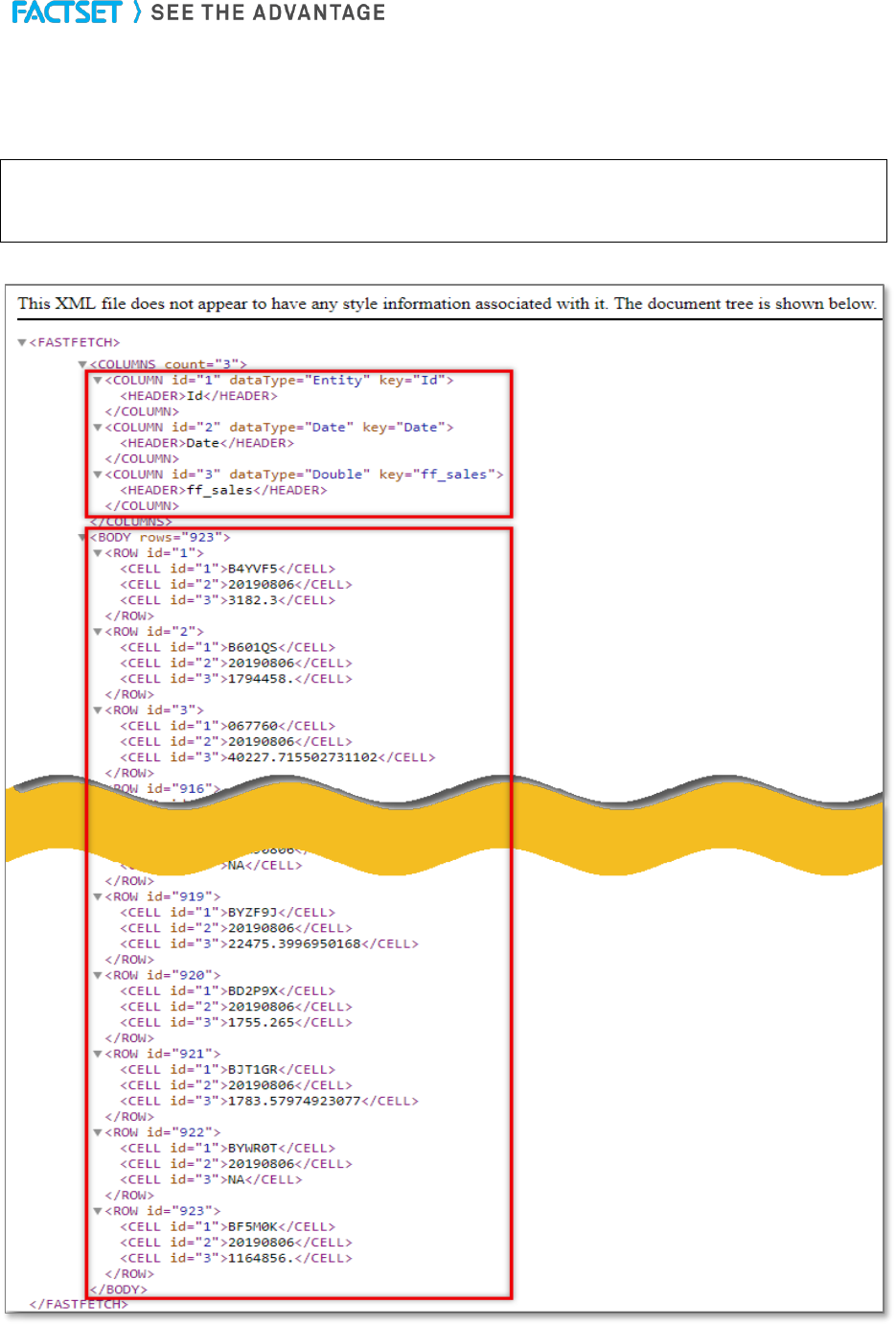

Example 2

In this example, instead of specifying securities in the ids field, as was done in Example 1 above, the

universe is specified as the constituents of an index using a so called ISON-code, here S&P 500. The

items specified - price and sales, are extracted for all constituents of the index. The syntax to extract the

price from the pricing database is using the code P_PRICE(20110401) and sales from the FactSet

Fundamentals database is using the code FF_SALES(QTR,20110401). The code to retrieve the current

constituents of S&P 500 is ISON_SP500.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractDataSnapshot&items=FF_SALES(QT

R,20110401),P_PRICE(20110401)&dates=20110401&ison=SP500

The universe is specified at the end of the code with the ison and sp500 arguments, which are broken

down from the actual Screening syntax for this universe which is using the code ISON_SP500.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

19

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

20

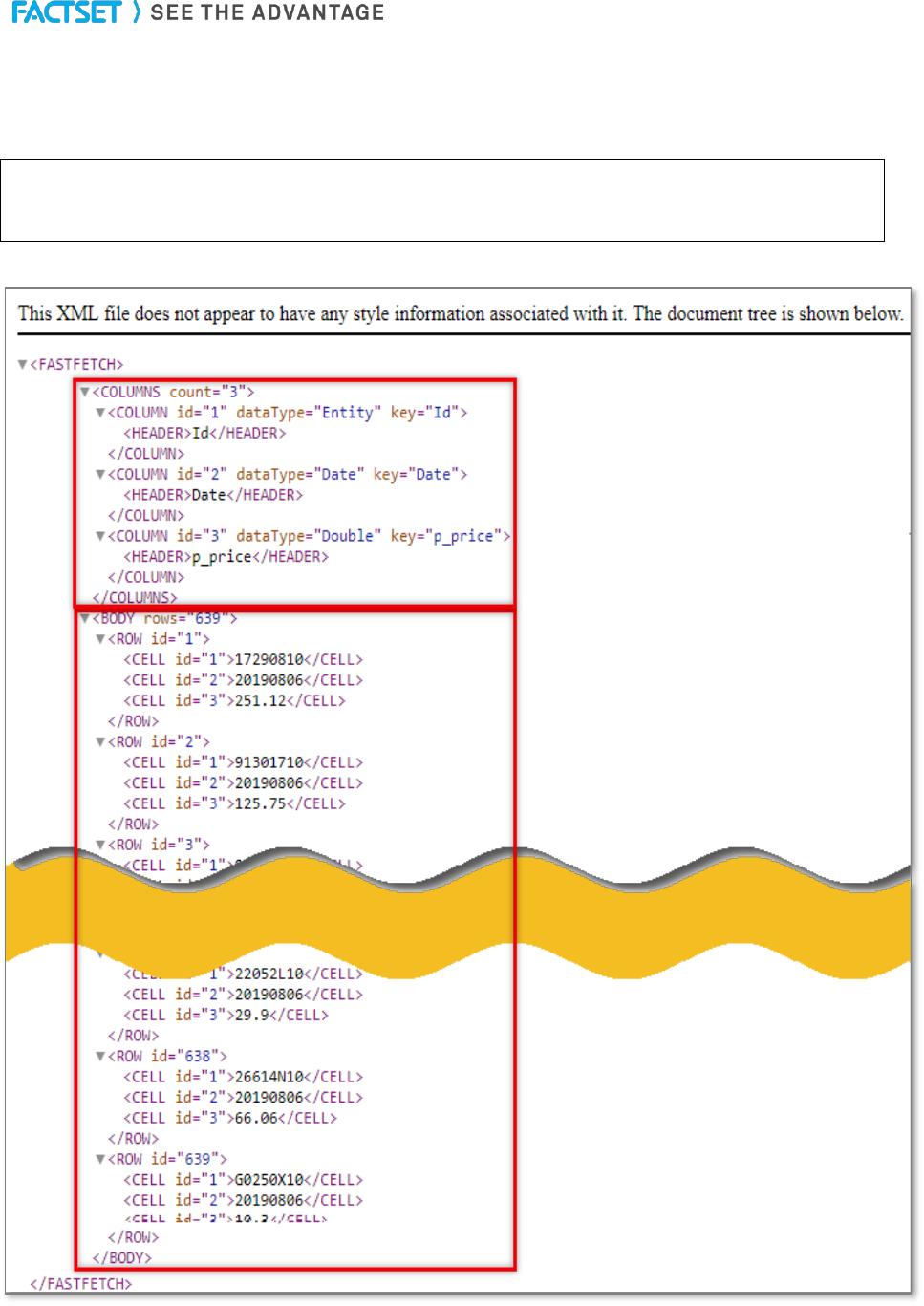

Example 3

In this example, the latest quarterly sales with the FactSet Fundamentals code FF_SALES in local

currency for the specified universe as the constituents of the MSCI EAFE index is retrieved. The

Screening code for this universe is ISON_MSCI_EAFE(0,1).

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractDataSnapshot&format=xml&items=FF

_SALES(QTR,0)&date=0&ison=msci_eafe&isonparams=0,1

Output

Note: The isonParams part of the code is used to specify the arguments within the brackets of the

ISON_xxx code, here 0,1.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

21

Example 4

In this example, the latest closing price for the constituents of the MSCI USA index, using the pricing

database code P_PRICE is extracted. The Screening code for this Universe is

ISON_MSCI_COUNTRY(984000,0,CLOSE,OFF).

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractDataSnapshot&format=xml&items=P_

PRICE(0)&date=0&ison=msci_country&isonparams=984000,0,close,OFF

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

22

Example 5

In this example, extract the decile ranking of the S&P 500 companies based on the most recently reported

quarterly earnings per share (EPS) using the FactSet Fundamentals formula FF_EPS. The FactSet

UDECILE function returns the decile rank (1-10) of a company against a specified universe when both

the company and the universe are evaluated for the same formula. The number 1 is the highest rank and

is assigned to the companies which fall within the top decile of the specified universe, in this case the

S&P 500.

URL:

https://datadirect.factXset.com/services/FastFetch?factlet=ExtractDataSnapshot&format=xml&items=

UDECILE(ISON_SP500,FF_EPS(QTR,0))&date=0&ison=SP500

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

23

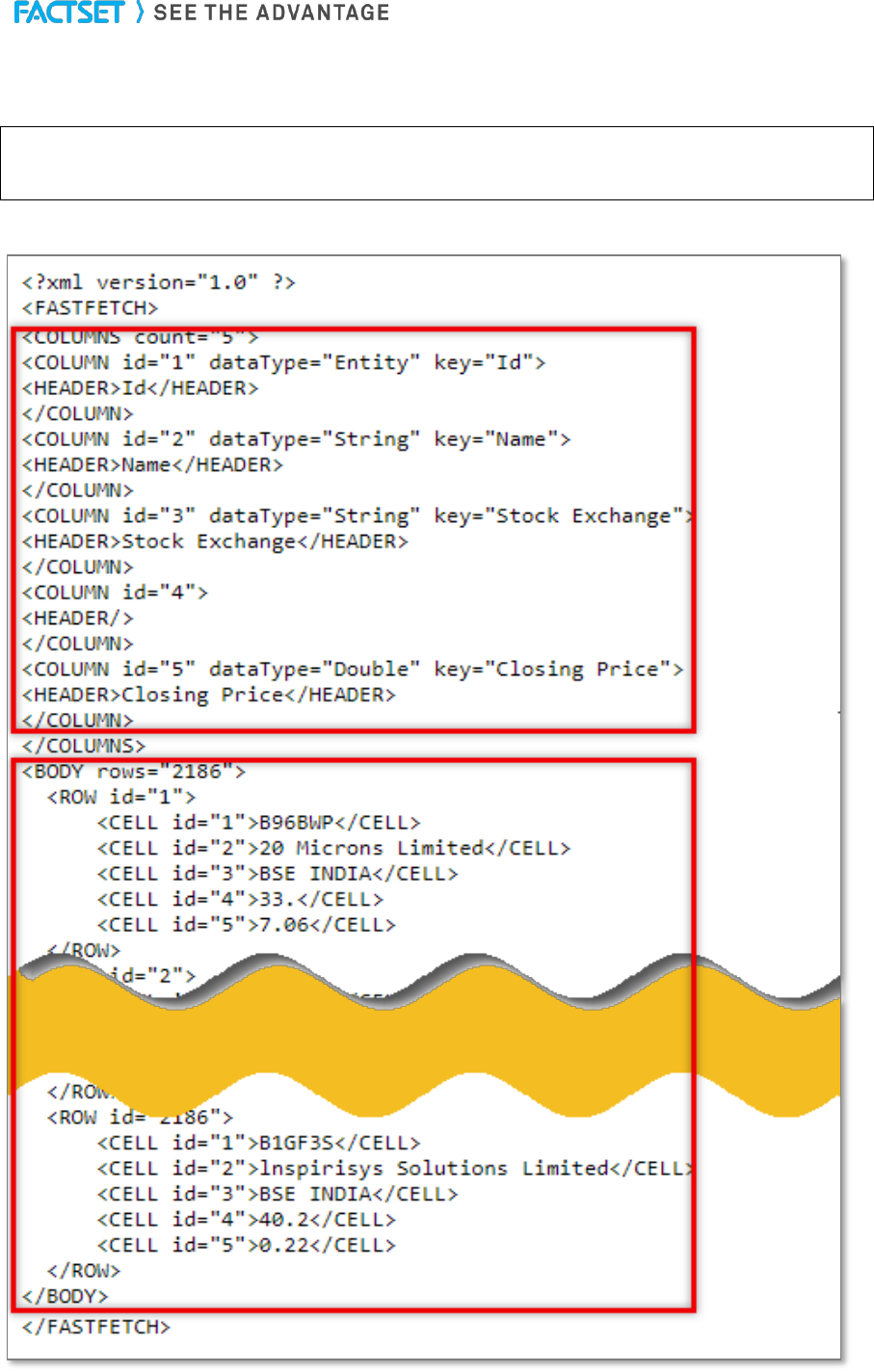

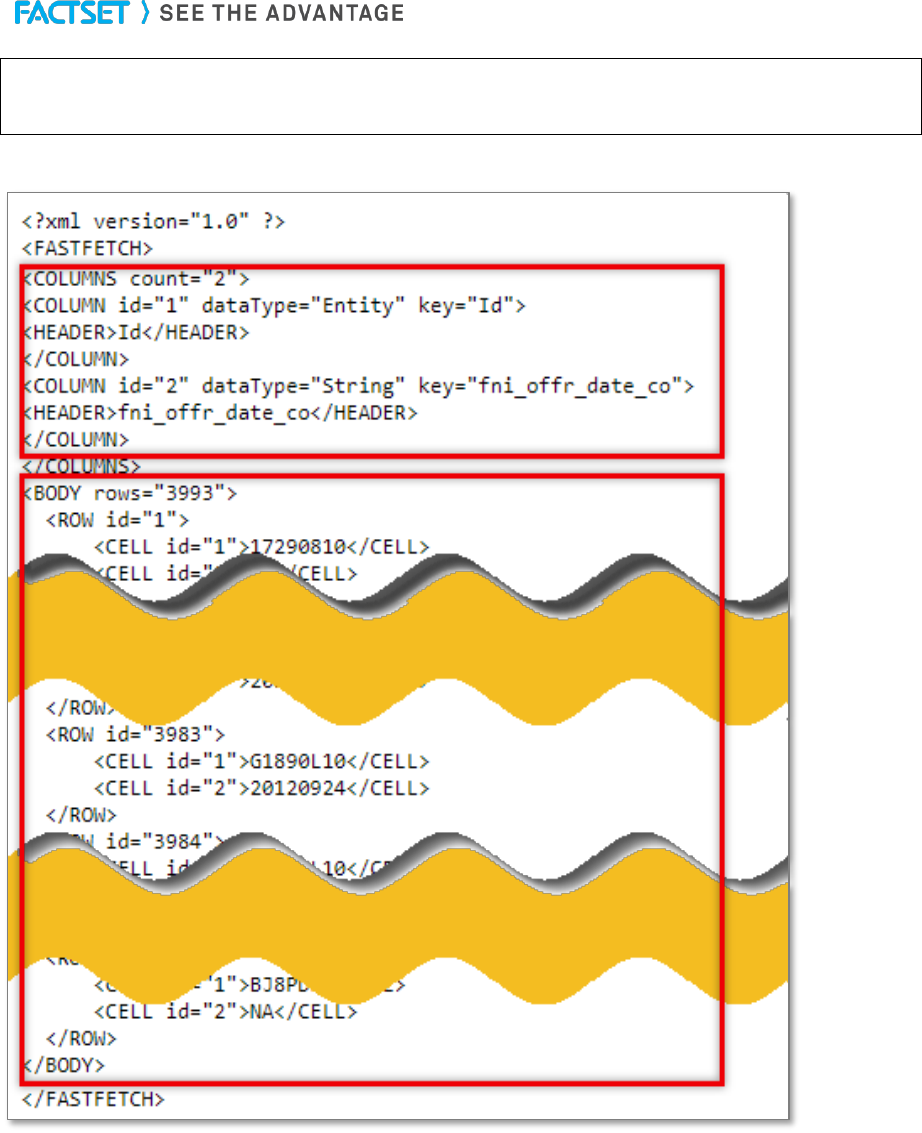

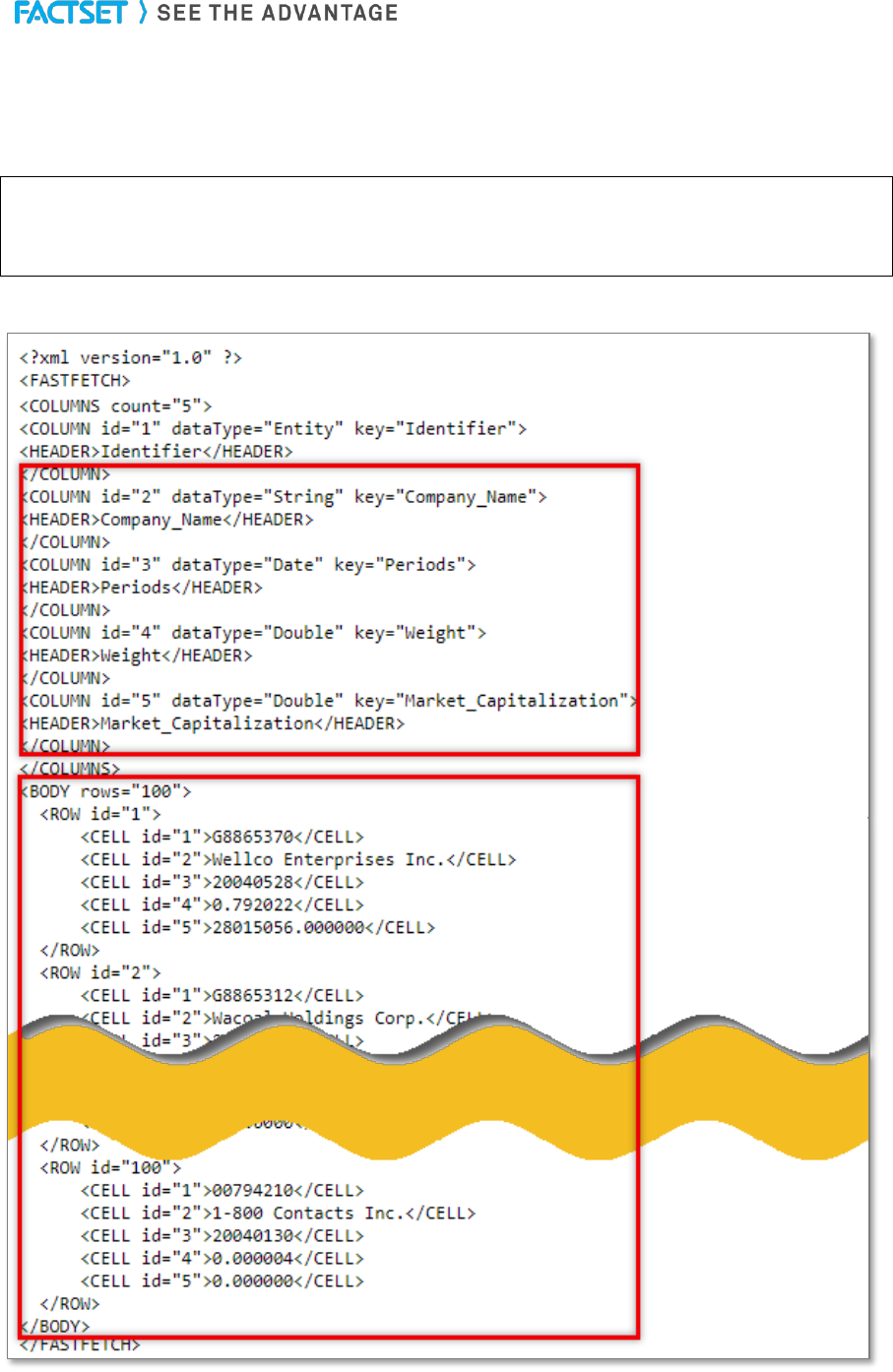

5. ExtractFormulaHistory

The ExtractFormulaHistory function is used for extracting one or more items for one security, an index or

a list of securities over time. The function is using the FactSet Query Language (FQL), which is a

proprietary data retrieval language used to access a time-series of FactSet data.

The syntax for the ExtractFormulaHistory function is-

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractFormulaHistory&ids=?&items=?&date

s=?&optional_arguments=?....

where,

data

variable name for the data returned

ids

CellString array with a list of one or multiple security identifiers

items

CellString array with a list of one or more FactSet data items in the Screening language

dates

Date range and frequency entered using actual or relative dates. A valid FactSet frequency

(e.g. ‘d’dates Alternate method of entering dates entered in start:end:freq format. (e.g.

‘20101215:20110115:d’)

Optional arguments

curr

The currency in which the data is to be returned, using a string with the three-character ISO

code (e.g. ‘USD’ or ‘EUR’).

cal

Calendar setting, arguments include:

• LOCAL: Uses the local trading calendar for each security. Local exchange holidays

will be skipped

• FIVEDAY: Displays Monday through Friday, regardless of whether there were

trading holidays.

• FIVEDAYEOM: Displays Monday through Friday including a weekend date if it falls

on the last day of the month. Where the month-end does not fall on a weekend, the

calendar will act just as the standard five-day calendar.

• SEVENDAY: Displays Monday through Sunday.

• AAM: For Exchange code uses the calendar of a specific exchange, represented

by the exchange code. If there is no calendar available for a specific exchange, the

calendar will default to FIVEDAY.

universe

Screening expression to limit the universe

ison

Ison-codes can be used to limit the universe ISON_MSCI_WORLD(0,1) is written as

‘ison’,’msci_world’,’isonParams’,’0,1’

isonParams

The arguments within brackets in the ison-code

OFDB

Universe is the constituents of an OFDB file, default directory is Client, if the OFDB is stored

in another location the path must be included

OFDBDate

Specific date for the constituents of the OFDB

decimals

Positionally set according to the items in the selection, ie ‘decimals’,’,,3,4,3’

dataType

The optional argument allows users to define a data type for a data item column that is NA

for the entire column. This option must be defined for every column/data item requested in

the command if it is used at all.

feelback

Setting to control data is not falling forward and display NAs instead of carrying forward

values, for those databases that do so (using ‘feelback’,’n’).

refresh

This will refresh the connection to FactSet servers to capture the latest database updates.

This only needs to be used when a refresh is necessary. It is not recommended to leave this

argument in every request made. To use this, the refresh argument should be paired with

the value “Y”.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

24

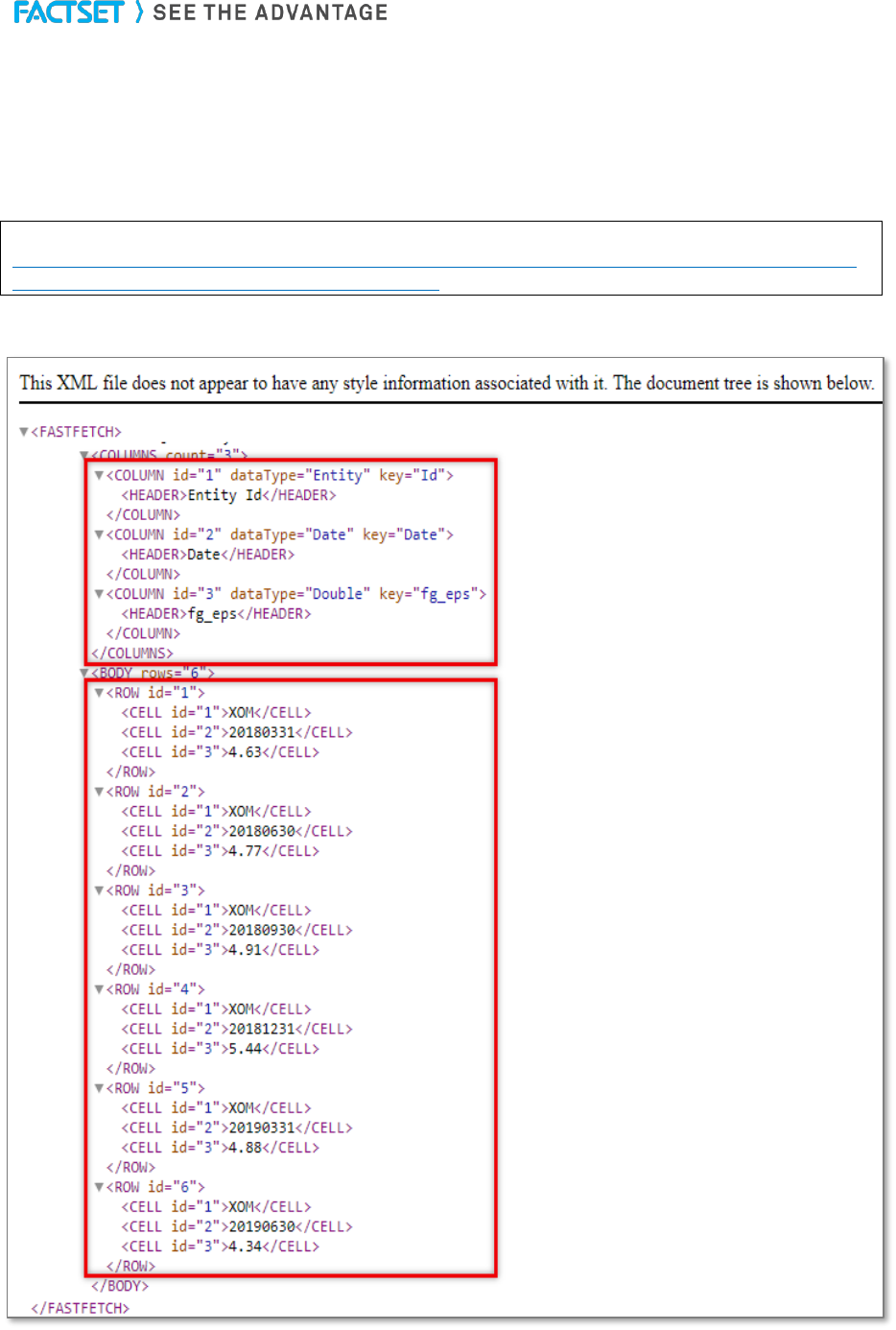

Example 1

In this example extract the last 6 quarters EPS for Exxon Mobile (ticker XOM) using the FQL code

FG_EPS. The date argument is using relative rather than absolute dates. To specify relative dates, enter

the number of periods and a period code, such as D for days, W for weeks, or Q for quarters and Y for

years. When using relative dates, "0" refers to the most recent time period. Therefore, 0Q refers to the

most recent quarter end, while -1Q refers to two quarters ago.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractFormulaHistory&format=xml&ids=X

OM&items=FG_EPS(0Q,-5Q,Q)&dates=0Q:-5Q:Q

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

25

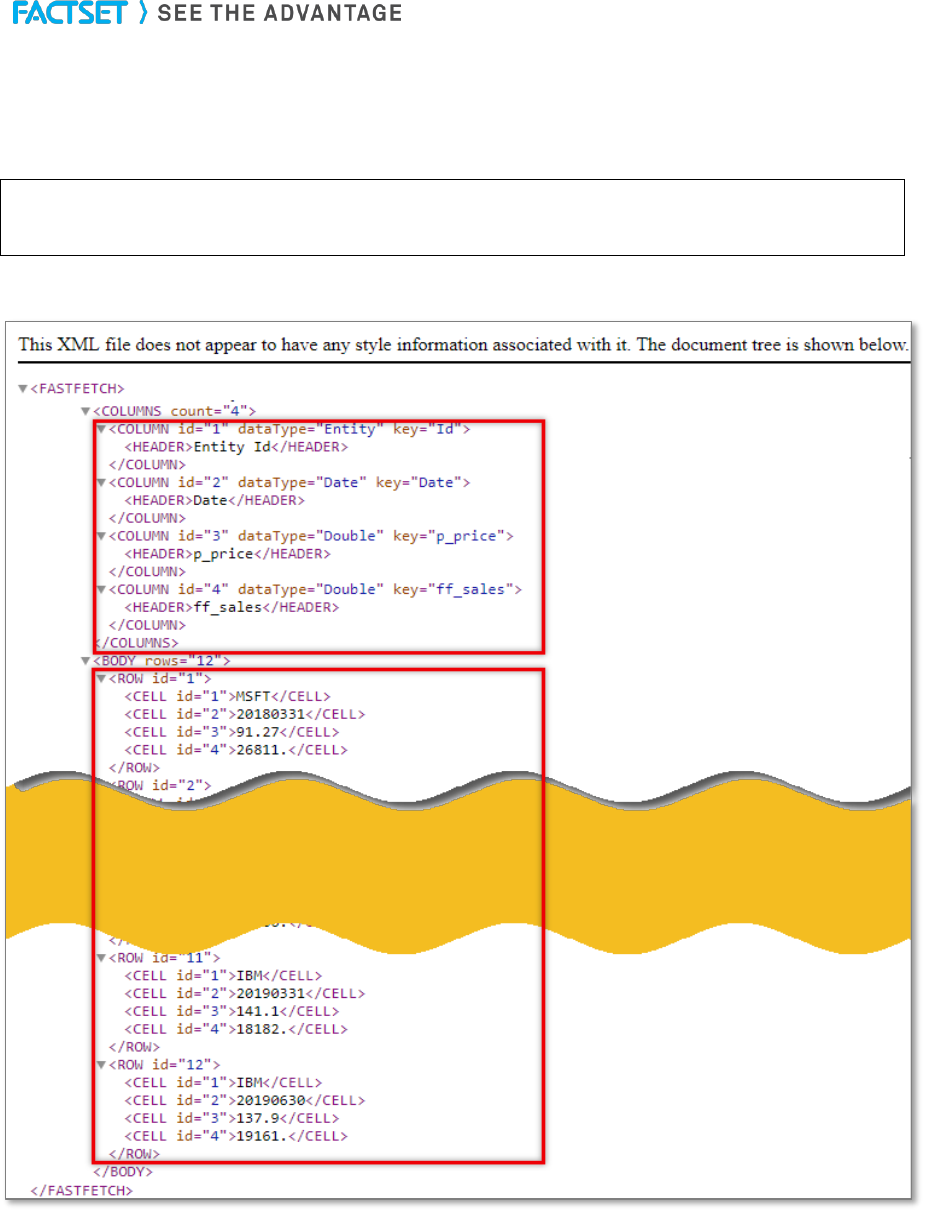

Example 2

In this example, extract the last 6 quarters of pricing and sales data for Microsoft and IBM using the pricing

database with the FQL code P_PRICE and the FactSet Fundamentals database for sales data with the

FQL code FF_SALES. Both P_PRICE and FF_SALES in this example are used in the Items parameter.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractFormulaHistory&format=xml&ids=

MSFT,IBM&items=P_PRICE(-5,0,Q,USD),FF_SALES(QTR,-5,0,Q,,USD)&dates=-5:0:Q

Output

Note: To most efficiently ensure that that the dates for the different items (here price and sales) align

correctly with the dates field, the dates should be included both in the FQL code and in the dates

parameter as specified above.

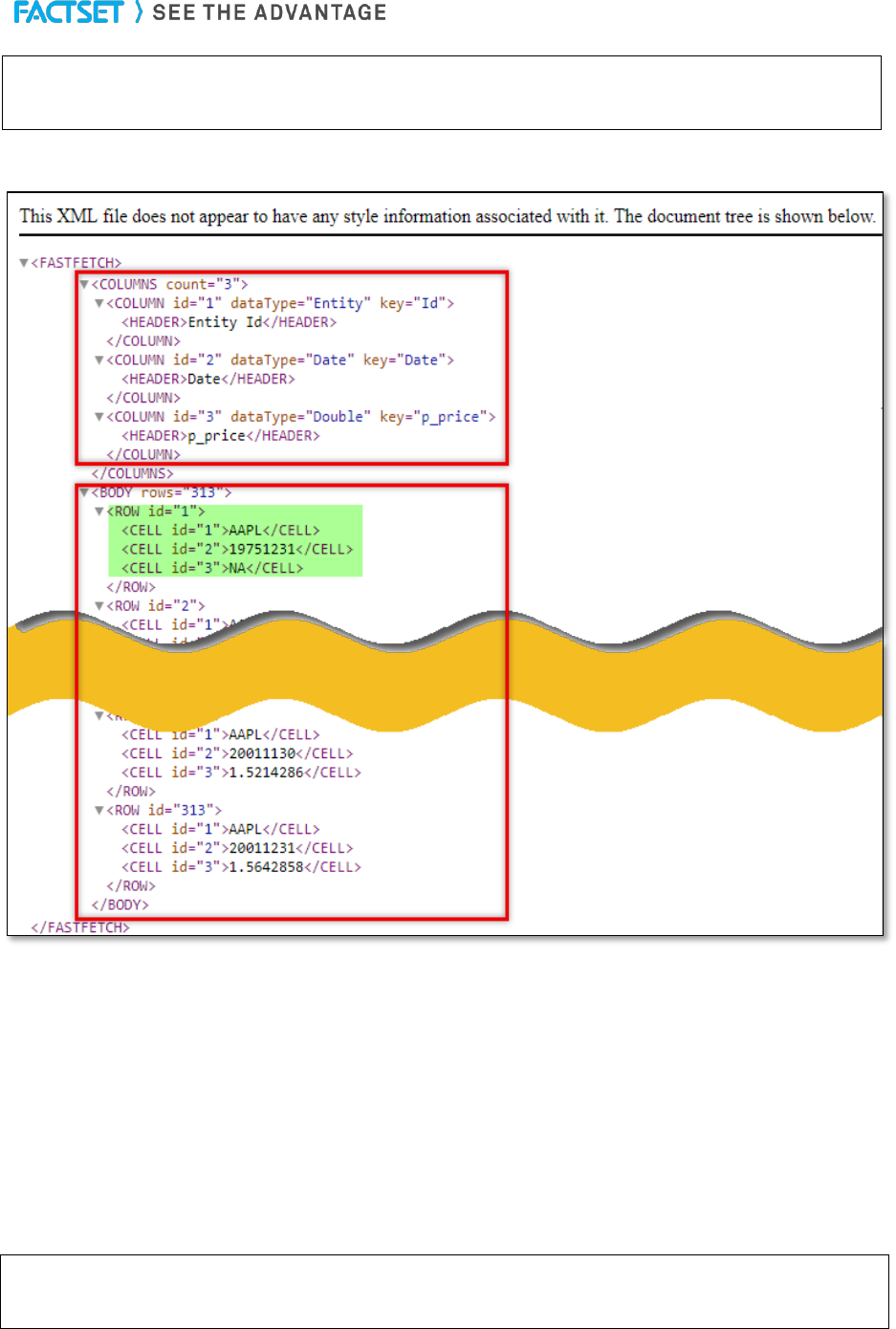

Example 3

In this example, extract the price for Apple for the date range 12/31/1975 until 12/31/2001 on a monthly

frequency. Since there is no available price data for Apple starting in 1975, the data would be NA. When

using the ExtractFormulaHistory function the data type can be specified for treatment of NA’s, for example

as a double or integer.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

26

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractFormulaHistory&format=xml&ids=AA

PL&items=P_PRICE(12/31/1989,12/31/2001,M)&dates=12/31/1989:12/31/2001:M&datatype=double

Output

Note: By default, the data type returned is determined by the first value of the items being returned. In

this case the p_price code returned as a character by default because the values for APPLE are NA (if

the request is made for just IBM with the same date range the p_price data is returned as a double since

the data is available for IBM). But with the addition of the ‘datatype’ optional argument, it is possible to

specify how the data is returned.

Example 4

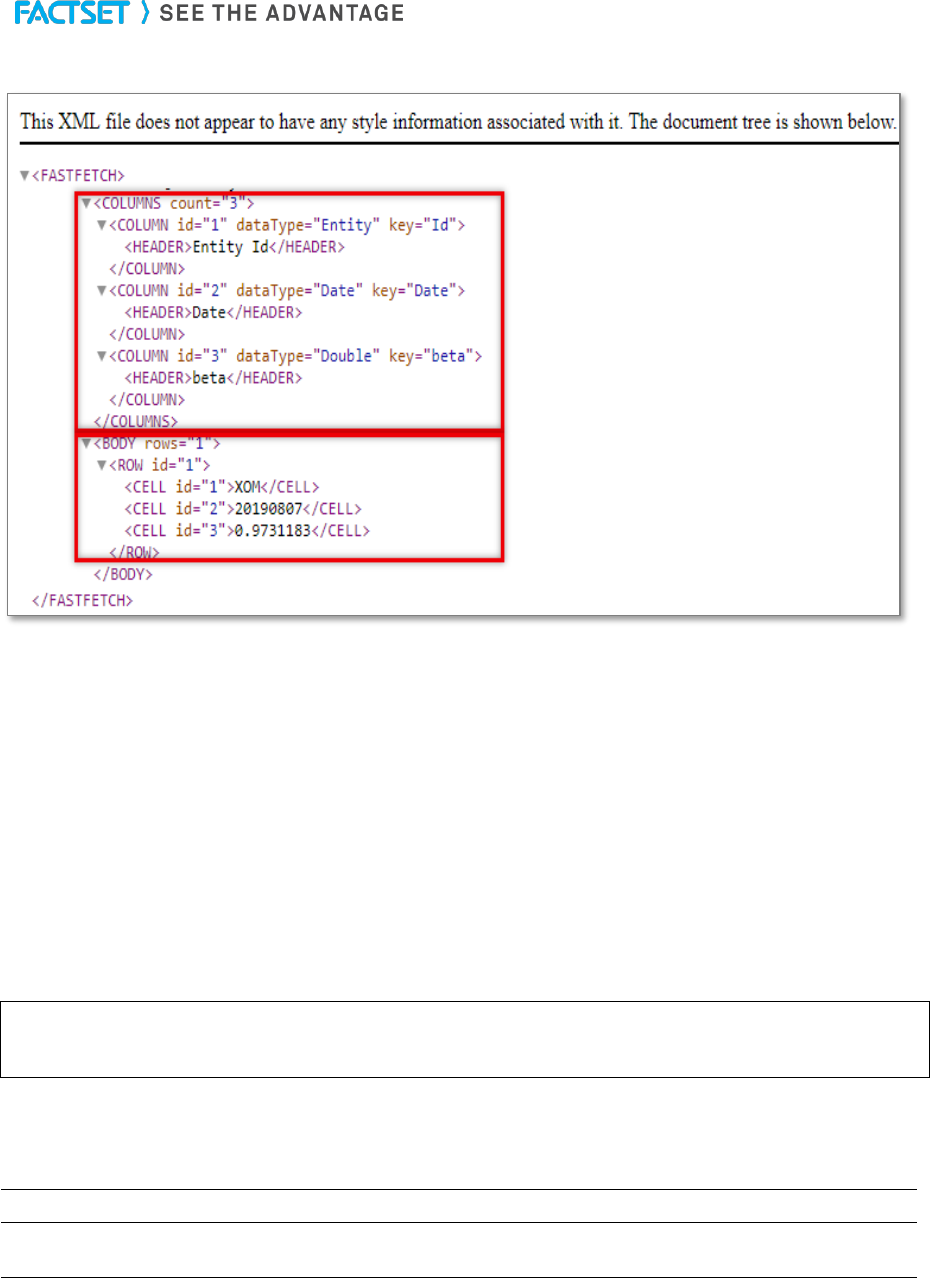

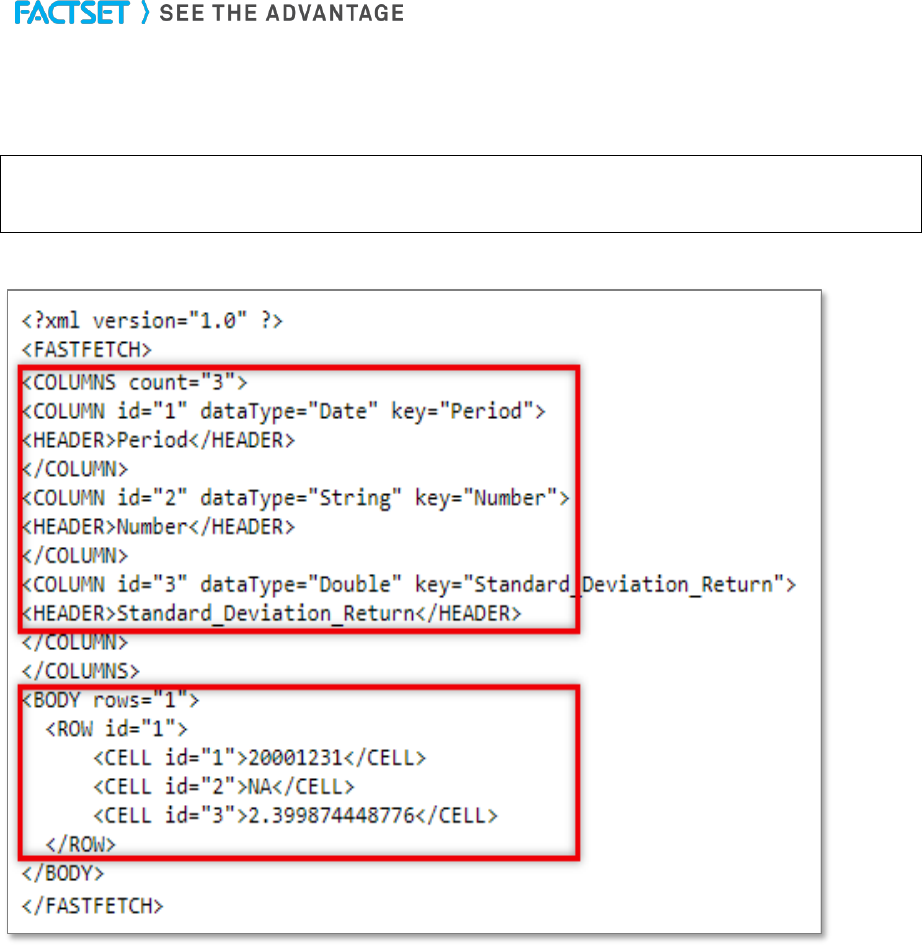

In this example, retrieve the 60-month beta coefficient for Exxon Mobile relative to the S&P 500. The

FactSet BETA function measures a security or portfolio's volatility relative to an index. If a security has a

beta coefficient greater than one, it is considered more volatile. If a security has a beta coefficient of less

than one, its price can be expected to rise and fall more slowly. In the FQL syntax, the BETA function

returns the coefficient relative to an index and over any period of time that you specify.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractFormulaHistory&format=xml&ids=XO

M&items=BETA(%27SP50%27,-0,-59M,M)

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

27

Output

6. CorporateActionsDividends

The CorporateActionsDividends function is used for extracting stock dividend information.

The retrieved stock dividend information using the CorporateActionsDividends function includes special

dividends, which are defined as nonrecurring distribution of assets by a company to its shareholders in

the form of cash. Since it is unlikely to be repeated, it is often used in conjunction with a spinoff.

It also includes stock dividends, which are represented as forward stock splits, not regular cash

distributions.

The policy is, only actions affecting the pro-rata adjustment will be reflected. Because employee bonus

shares are not included in the pro-rata element announced by the company, the policy is to not include

adjustment for employee bonus shares as a part of the stock dividend amount.

The syntax for the CorporateActionsDividends function is:

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=CorporateActionsDividends&ids=&start=&en

d=&optional_arguments...

Where,

data

Variable name for the data returned

ids

Array with a list of one or more security identifiers.

start

Start date from which dividend data should be retrieved. Method of entering date is

in MM/DD/YYYY format.

end

End date for period during which dividend data should be retrieved. The end date

field is for entering a future date for which the dividend data is accessed. It can be

entered as a future date in MM/DD/YYYY format or as a number, e.g. 50, which

reflects 50 days from today which is set as the end date.

Note: When entering number of days, the maximum value that can be entered is

50.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

28

Optional arguments

splitadj

Allows for split adjustment to be specified. This argument must be entered as:

'splitadj','9' to retrieve unadjusted dividends.

ngflag

Specify 'ngflag ','y ' to return a flag that indicate whether the dividend rate

returned is a net or gross. The output would be a G or N flag.

symbol

Argument allows for the CUSIP to be retrieved as the last column (by default

SecId is the first field that is retrieved when running a CorporateActionsDividends

function). This argument must be entered as 'symbol', 'y'.

cur

The optional currency argument to specify the currency in which the stock

dividend data is returned.

universe

Screening expression to limit the universe

secId

Currently, the stat packages display the ticker by default in the first column but

will now display whatever values are entered in the ids= argument. The secId=Y

parameter will now be used to display whatever is entered in the ids= argument.

summary

When ‘summary’ and ’Y’ is used as an argument, it will display a more detailed

view including dividend description and will group dividends paid at the same time

together. This is more common for Australian securities.

Example 1

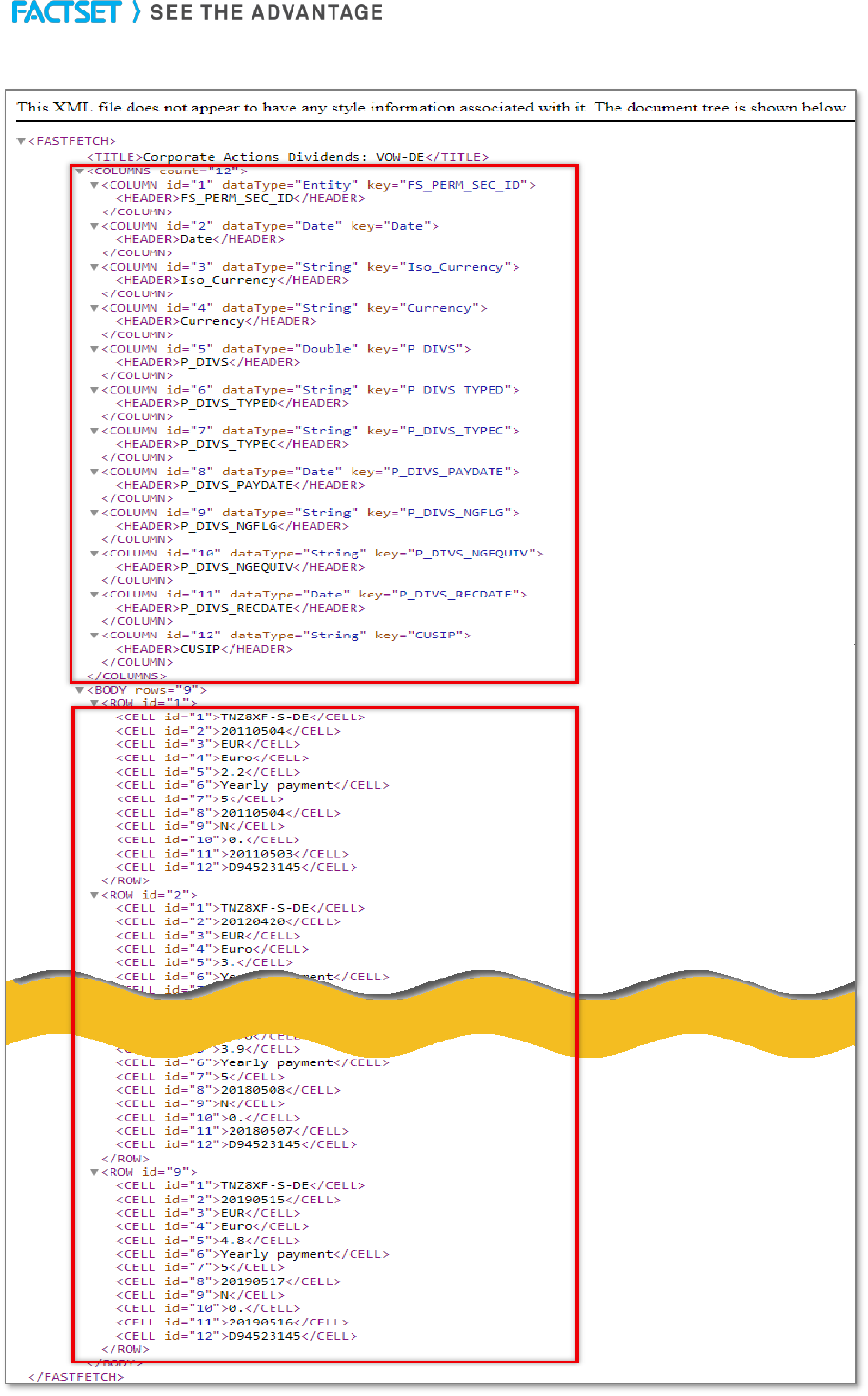

In this example, extract the stock dividend information for Volkswagen from 1/1/2011 up to 1 day from

today.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsDividends&format=xml&ids

=VOW-DE&start=1/1/2011&end=1

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

29

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

30

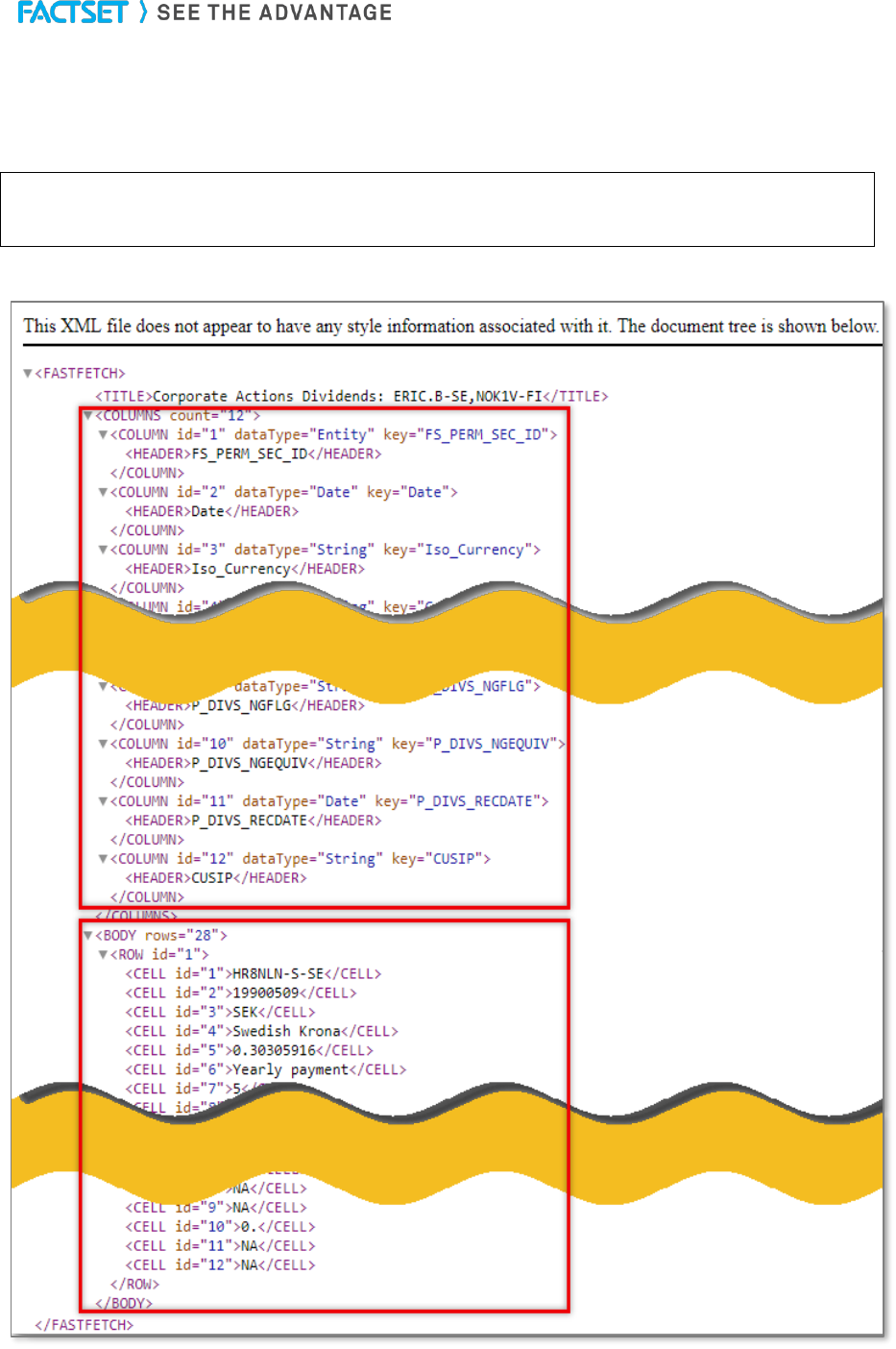

Example 2

In this example, extract the stock dividend information for multiple securities – Ericson and Nokia from

1/1/1990 up to 50 days going forward from today.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsDividends&format=xml&id

s=ERIC.B-SE,%20NOK1V-FI&start=1/1/1990&end=50

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

31

Example 3

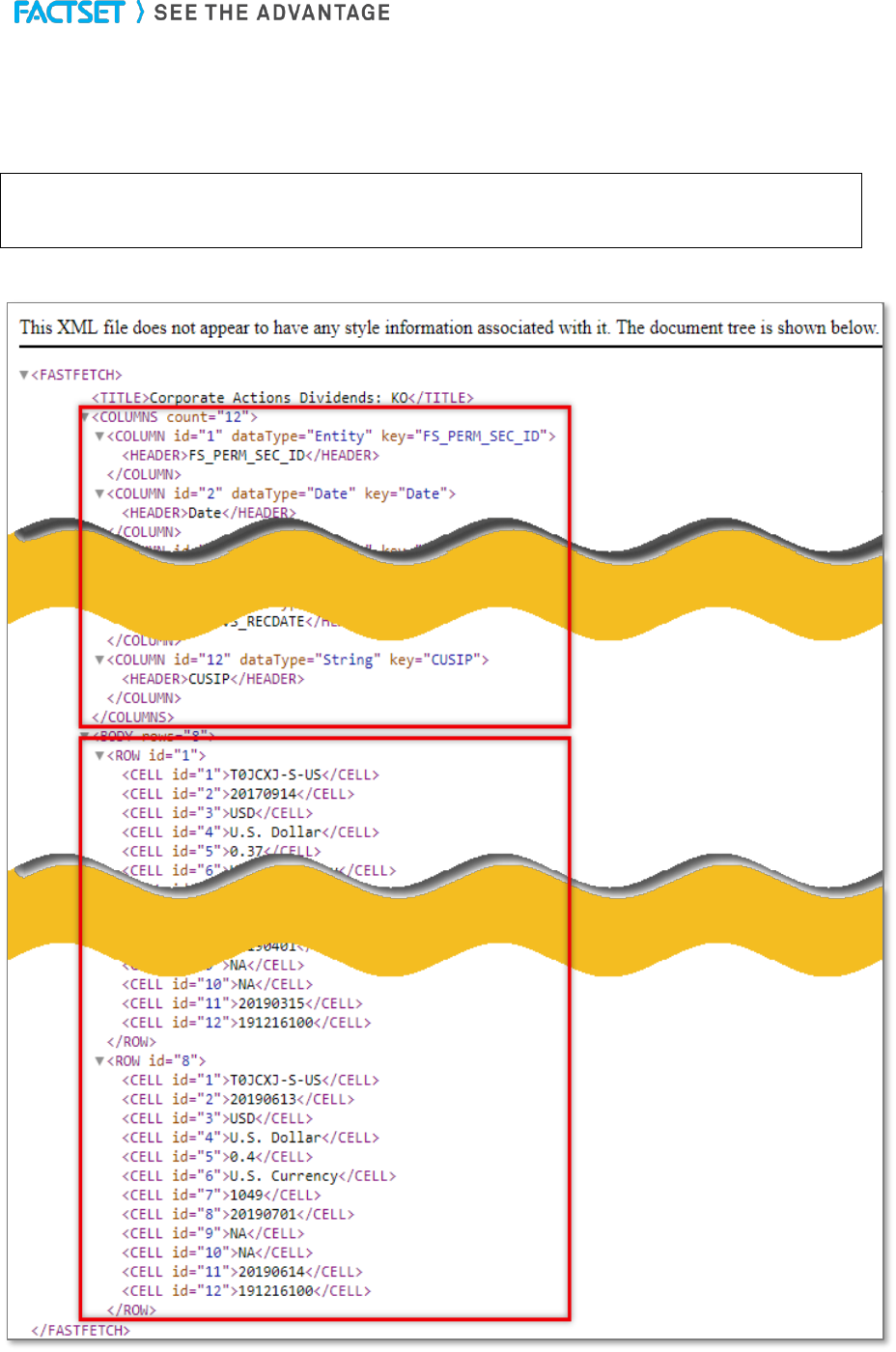

In this example, extract the stock dividend information for Coca-Cola over the last two years, retrieving

the unadjusted dividend.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsDividends&format=xml

&ids=KO&start=-2AY&end=0&splitadj=9

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

32

Example 4

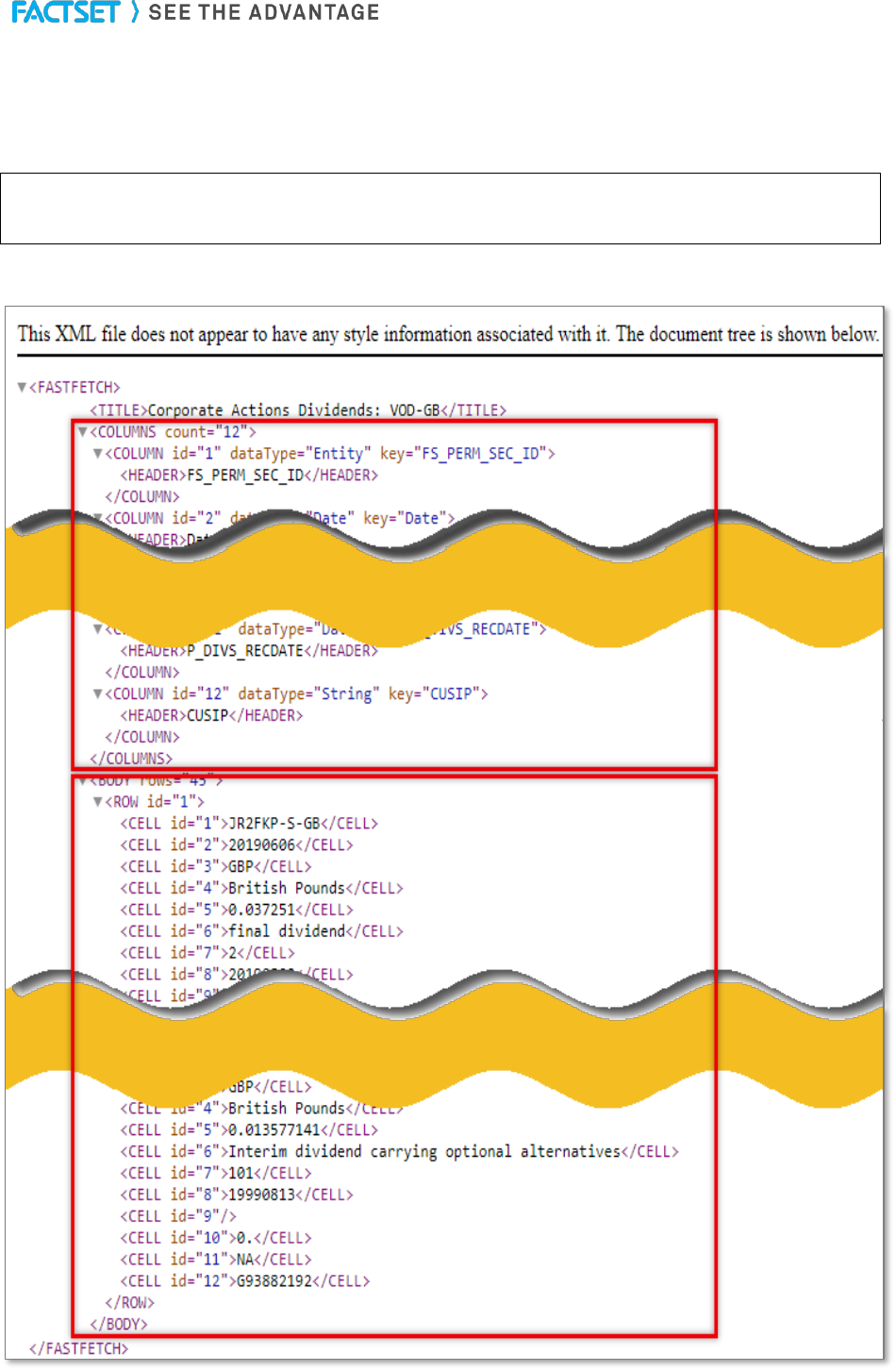

In this example, extract for Vodafone the dividend information over the last 20 years that is flagged for a

dividend rate returned that is a net or gross marker.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsDividends&format=xml&ids

=VOD-GB&start=0&end=-20Y&ngflag=y

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

33

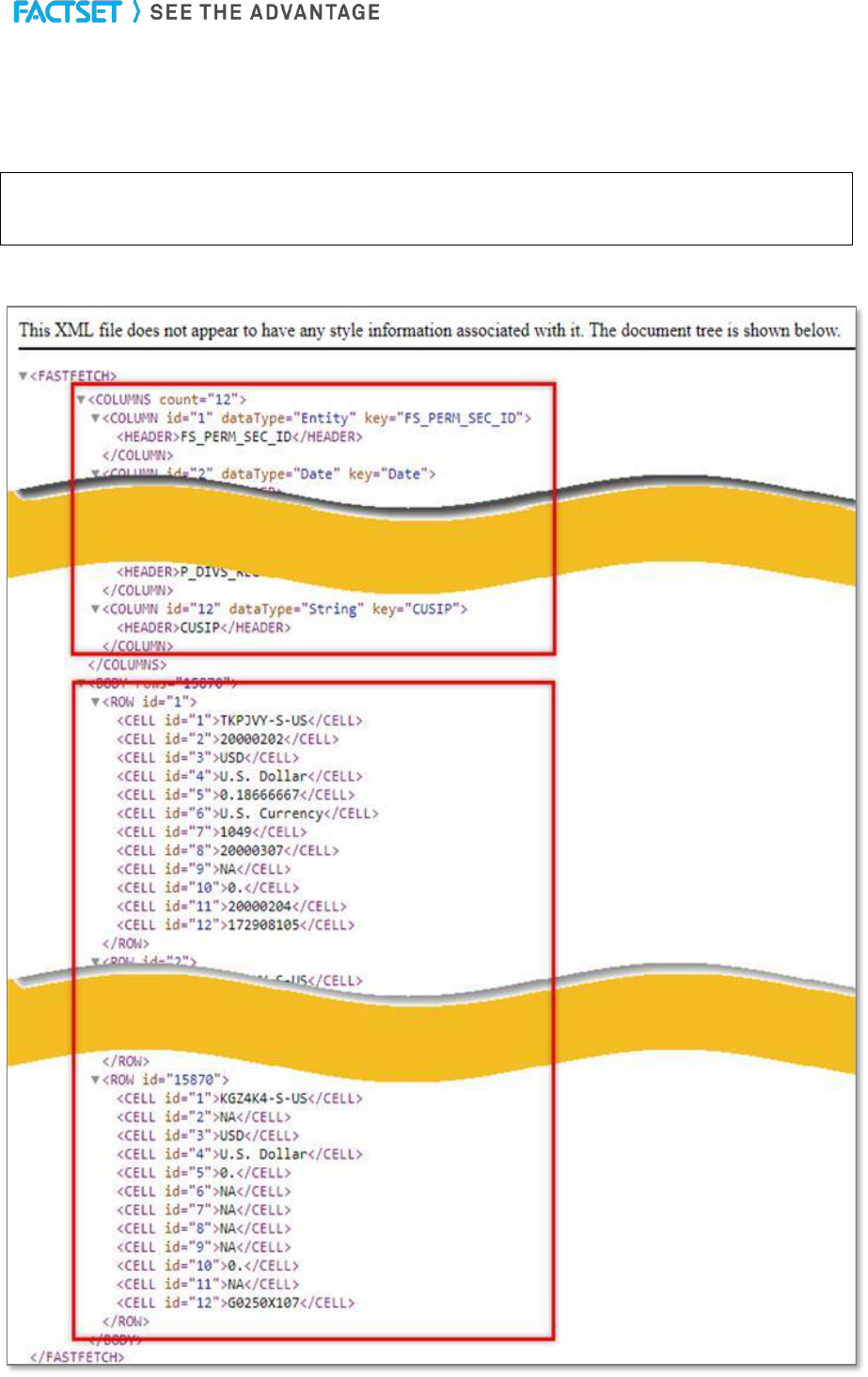

Example 5

In this example, the CUSIP is displayed with the result here for the dividends for the current constituents

of S&P 500 from 1/1/2000 to 12/31/2005.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsDividends&format=xml&

start=1/1/2000&end=12/31/2005&symbol=y&universe=(ison_sp500=1)

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

34

7. CorporateActionsSplits

The CorporateActionsSplits function is used for extracting stock split information.

Corporate Actions - FactSet Stock Split Methodology

The retrieved stock split information using the CorporateActionsSplits function is by ex-date.

The timing of adjustments to historical prices is based on regional settings. For more comprehensive

details regarding split rollover times by region, refer to Online Assistant page 14178.

The syntax for the CorporateActionsSplits function is:

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsSplits&ids=&start=&end=

&optional_aruguments.....

where,

data

Variable name for the data returned

ids

Array with a list of one or more security identifiers.

start

Start date from which split data should be retrieved. Method of entering date is in

MM/DD/YYYY format.

end

End date for period during which dividend data should be retrieved. The end date

field is for entering a future date for which the split data is accessed. It can be

entered as a future date in MM/DD/YYYY format or as a number, e.g. 50, which

reflects 50 days from today which is set as the end date.

Note: When entering number of days, the maximum value that can be entered is

50.

Optional arguments

symbol

Argument allows for the CUSIP to be retrieved as the last column (by default

SecId is the first field that is retrieved when running a CorporateActionsSplits

function). This argument must be entered as 'symbol', 'y'.

universe

Screening expression to limit the universe

secId

Currently, the stat packages display the ticker by default in the first column but will

now display whatever values are entered in the ids= argument. The secId=Y

parameter will now be used to display whatever is entered in the ids= argument.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

35

Example 1

In this example, extract the stock split information for Exxon Mobil from 1/1/1990 up to 1 day later from

today.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsSplits&format=xml&ids=X

OM&start=1/1/1990&end=1

Output

Note: The retrieved items with this function are the split factor, the split ratio and any available split

comments.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

36

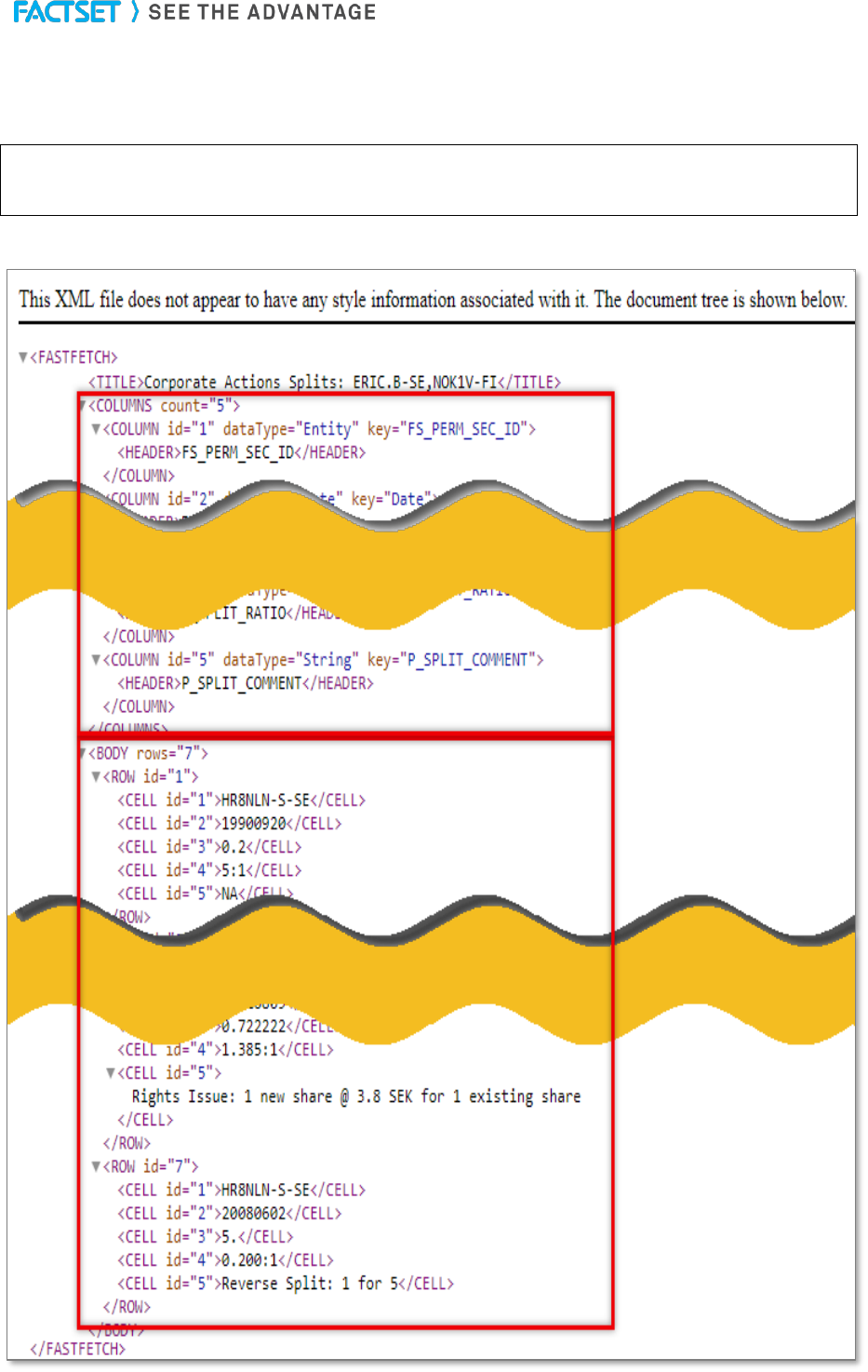

Example 2

In this example, extract the stock split information for multiple securities – Ericson and Nokia from

1/1/1990 up to 50 days from today.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsSplits&format=xml&ids=E

RIC.B-SE,%20NOK1V-FI&start=1/1/1990&end=50

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

37

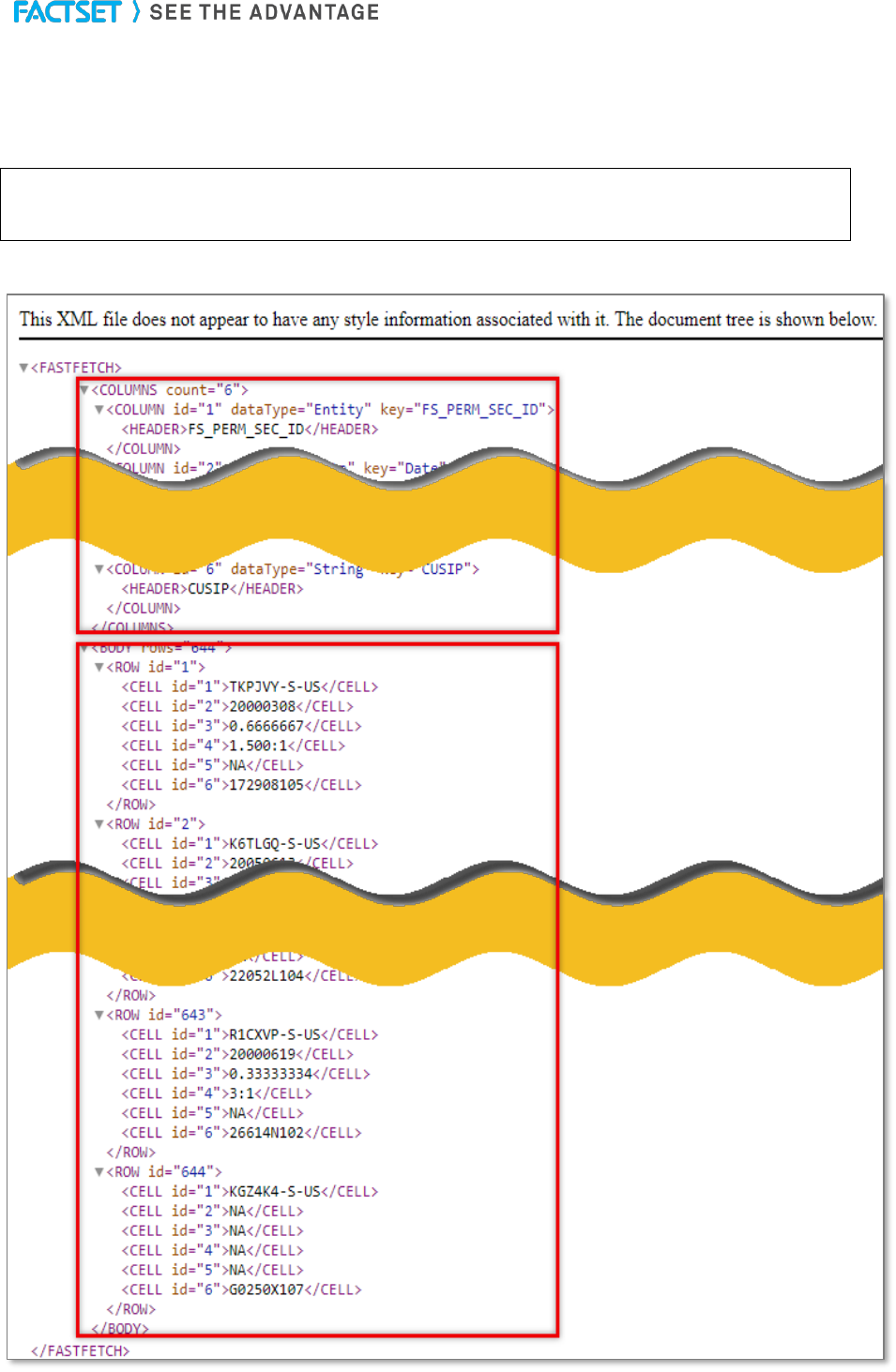

Example 3

In this example the CUSIP is displayed with the result, here for the splits for the current constituents of

S&P 500 from 1/1/1990 to 12/31/2012.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=CorporateActionsSplits&format=xml&start

=1/1/2000&end=12/31/2012&symbol=y&universe=(ison_sp500=1)

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

38

8. ExtractBenchmarkDetail

The ExtractBenchmarkDetail function is used for extracting multiple data items for a benchmark.

Benchmark data can be retrieved using other functions such as ExtractFormulaHistory, but the

ExtractBenchmarkDetail function allows a user to retrieve a more comprehensive overview of the index

constituent data, without additional codes or calculations. In the default output, identifiers are sorted in

descending order by weight in the index and each row shows the index id, company id, date, ticker, and

weight. Additional items are displayed at the end.

Benchmark Data

FactSet clients have access to Equity and Fixed Income Benchmarks, which include Dow Jones, FTSE,

MSCI, Russell, S&P, Barclays, and BofA Merrill Lynch, among a number of others. Access to benchmarks

is based on client subscription to various benchmark providers.

In addition, FactSet Market Aggregates (FMA), combines data from FactSet Fundamentals, Estimates

and Prices to calculate ratios and per share values on an aggregate level. FMA comprises over 3,500

benchmarks including S&P, Russell, MSCI Global, FTSE, STOXX, TOPIX, and many local exchanges.

Benchmarks also include specific sector and industry level indices. This number is constantly expanding

based on client demand.

To request benchmark data as of a single date or as a time-series, dates can be designated as absolute

dates or relative dates. See section 3.3

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractBenchmarkDetail&ids=&items=&d

ates=&optional_arguments.....

where,

data

Variable name for the data returned

ids

Array with a list of one or more benchmark identifiers.

dates

One or more dates; Dates should be entered in start:end:freq format. (e.g.

'20101215:20110115:d')

items

One or more items in Screening syntax, if FQL syntax is required it may be used with an

underscore needs to be appended at the beginning of the code, i.e _P_PRICE

Optional arguments

cutoff

Number of constituents to display; default displays all instances

useBTD

To control the alignment of historical stitching following a merger the useBTD parameter

is used. When FactSet and a benchmark vendor make different choices in picking a

surviving entity symbols can be returned as a dummy ticker to be used as a placeholder.

To return the symbol as of the back test date 'useBTD','ON' should be used.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

39

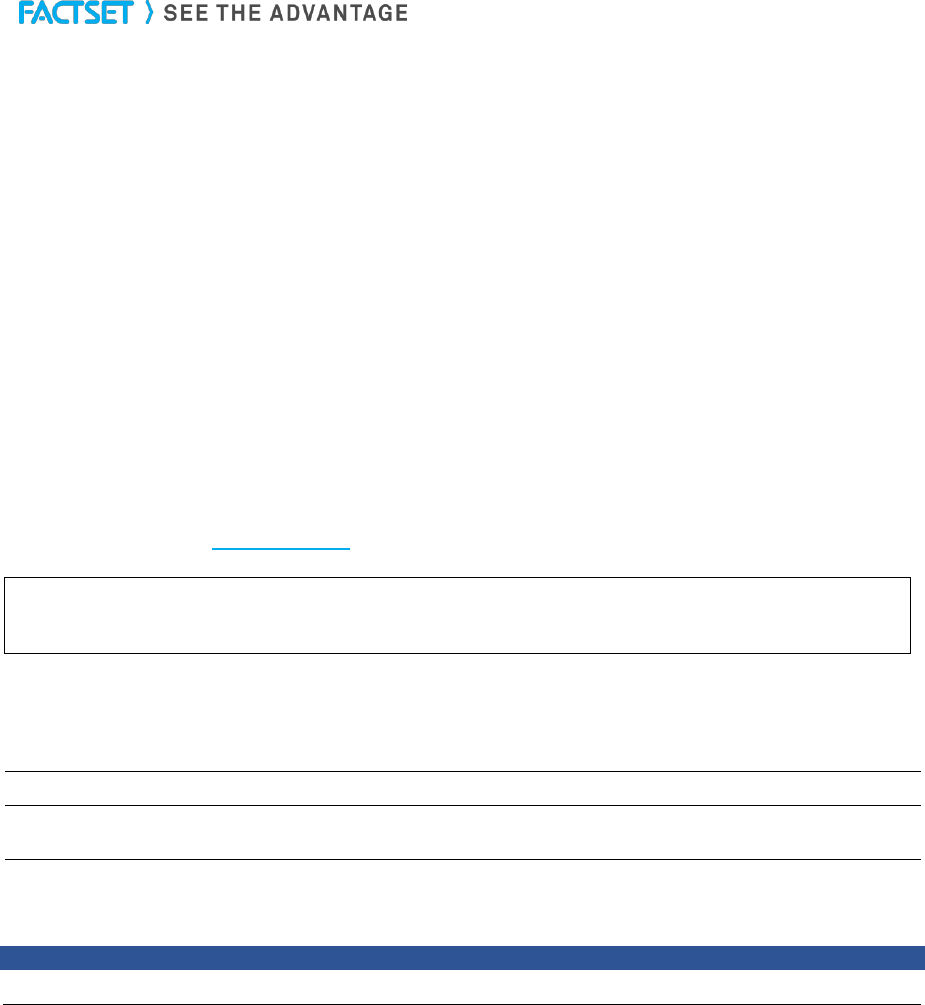

Example 1

In this example, the constituents of the S&P 500 is being extracted, the default columns will always be

available for this Factlet.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmarkDetail&format=xml&ids=S

P50

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

40

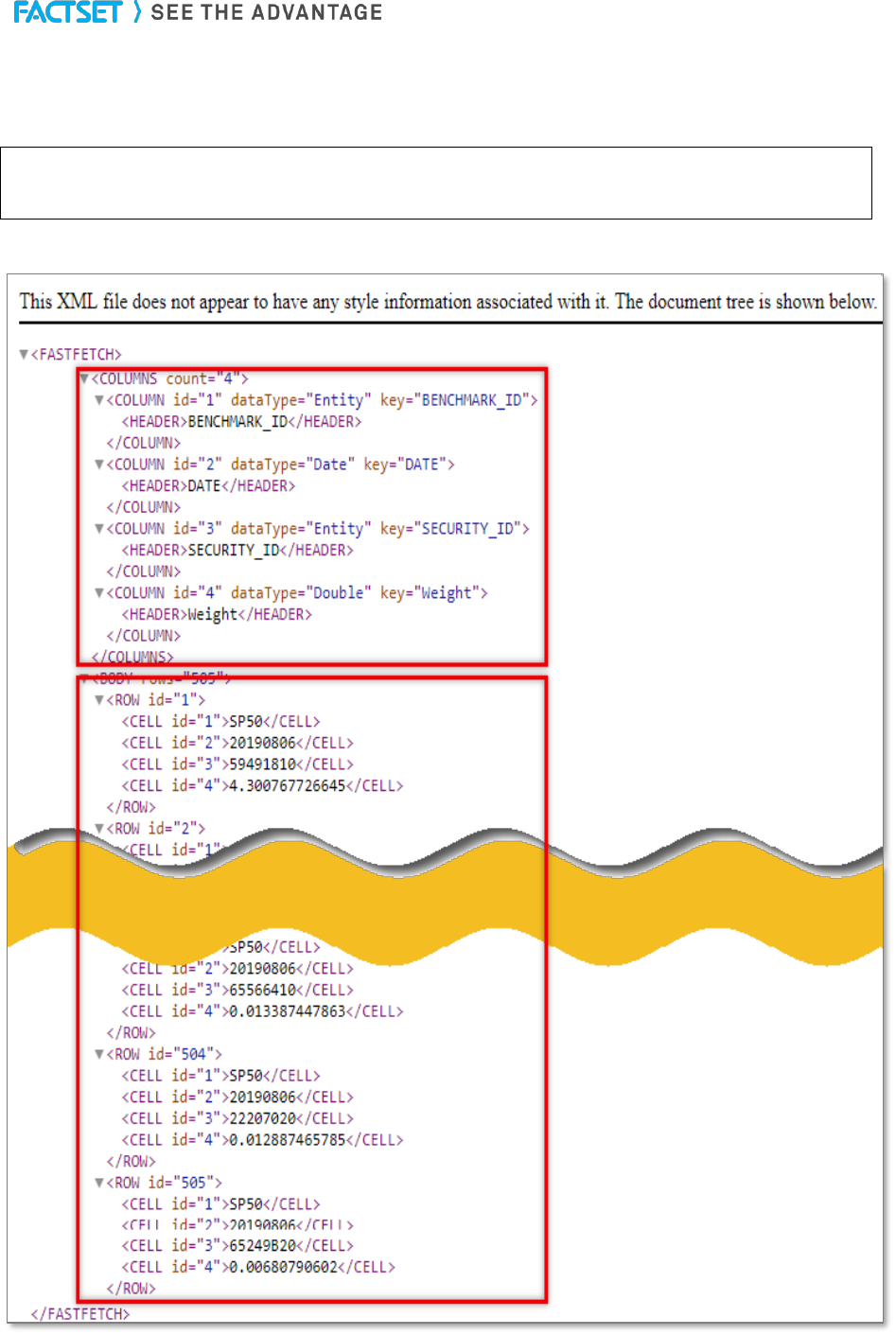

Example 2

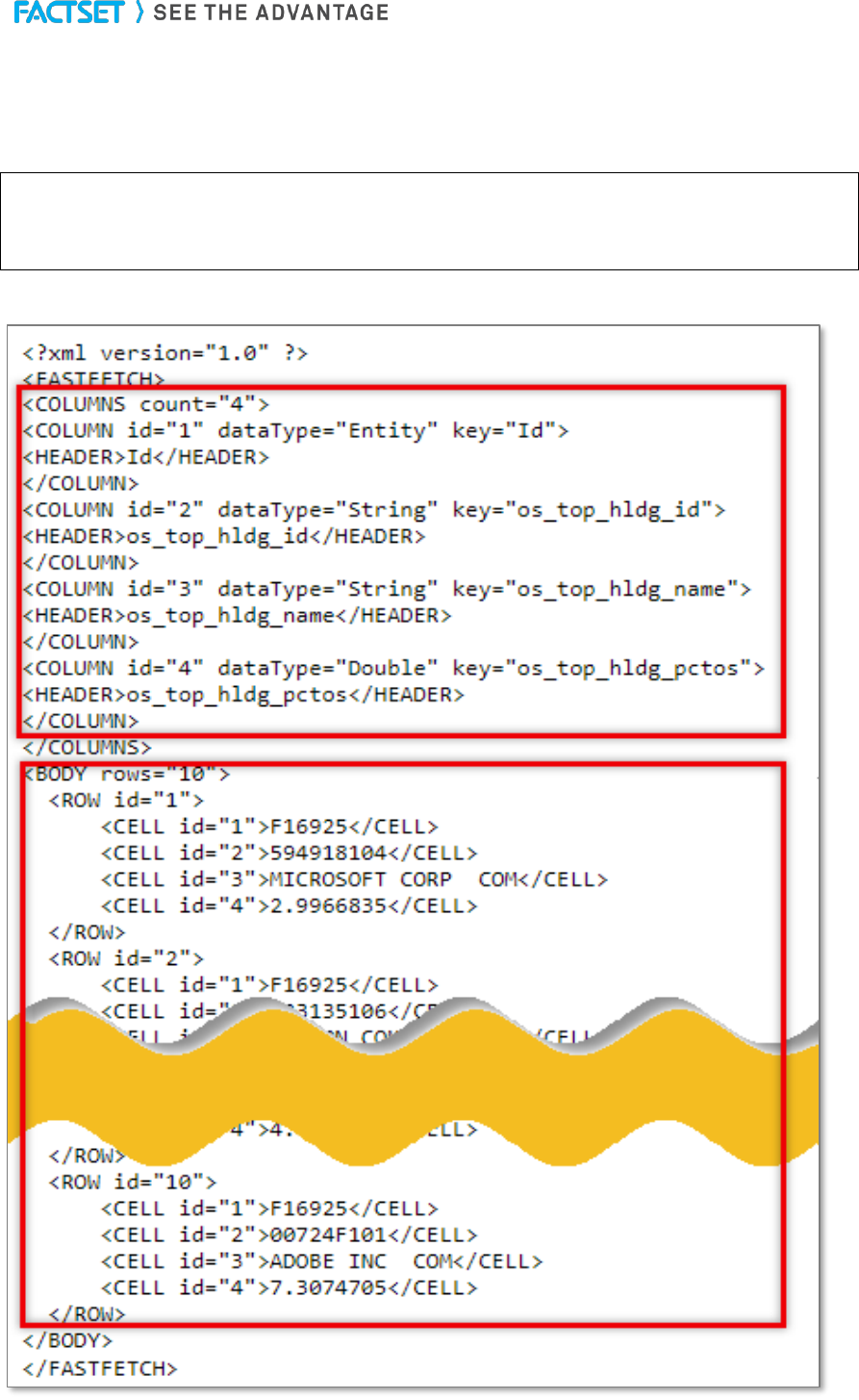

In this example, extract the top 10 holdings for the France CAC 40 index and display the companies’

securities price using the pricing database with the code P_PRICE and the company name using the

code PROPER_NAME.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmarkDetail&format=xml&ids=1

80454&items=P_PRICE,PROPER_NAME&date=0&cutoff=10

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

41

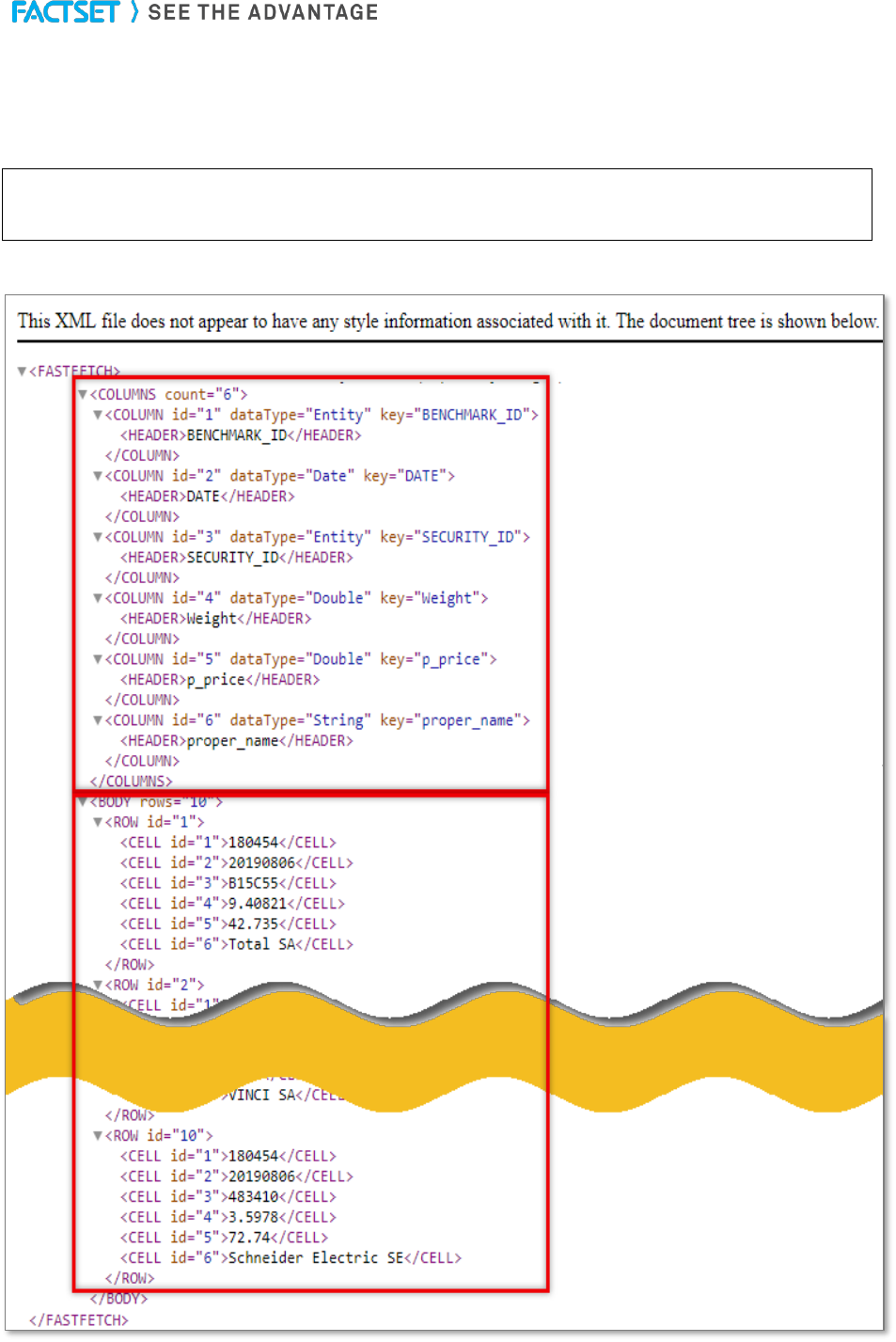

Example 3

In this example, extract the price using the pricing database code P_PRICE for the CAC 40 constituents

for 5 days in January in 2011.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmarkDetail&format=xml&ids=1

80454&items=P_PRICE&dates=20110115:20110120:d

Output

Note: The Constituents are as of the date specified in the dates argument, i.e. if any constituents are

added or removed over the time period this will be reflected in the output.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

42

Example 4

In this example the top 10 constituents for the fixed income index Barclays Capital EUR Corporate (1-5Y)

together with the names of the constituents which include the fixed income securities coupon rate and

maturity date. The index identifier is LHMN6732.

URL:

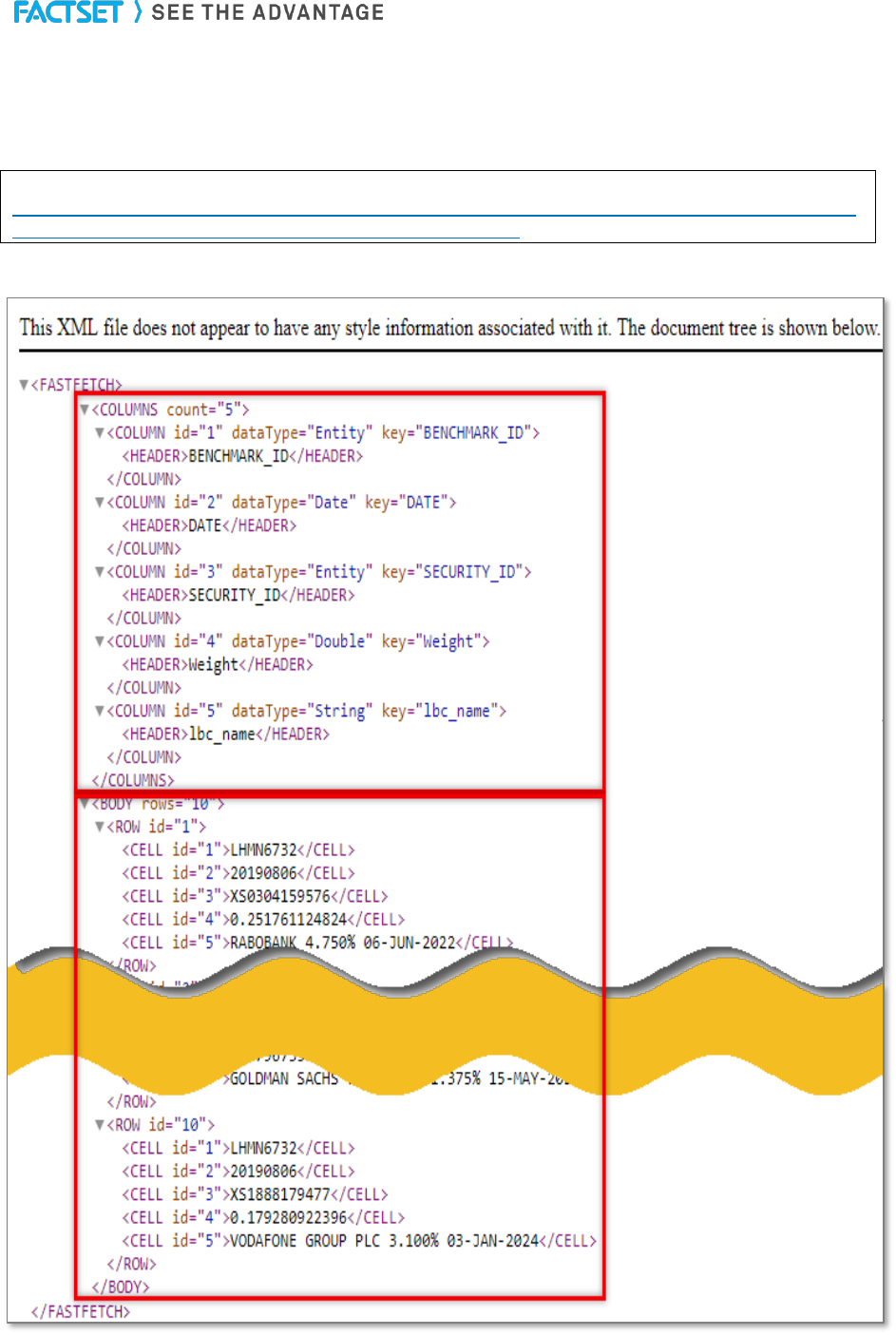

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmarkDetail&format=xml&ids=l

hmn6732&items=lbc_name&universeGroup=debt&cutoff=10

Output

Note: Fixed income indices need to use the ‘universeGroup’,’debt’ argument.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

43

Example 5

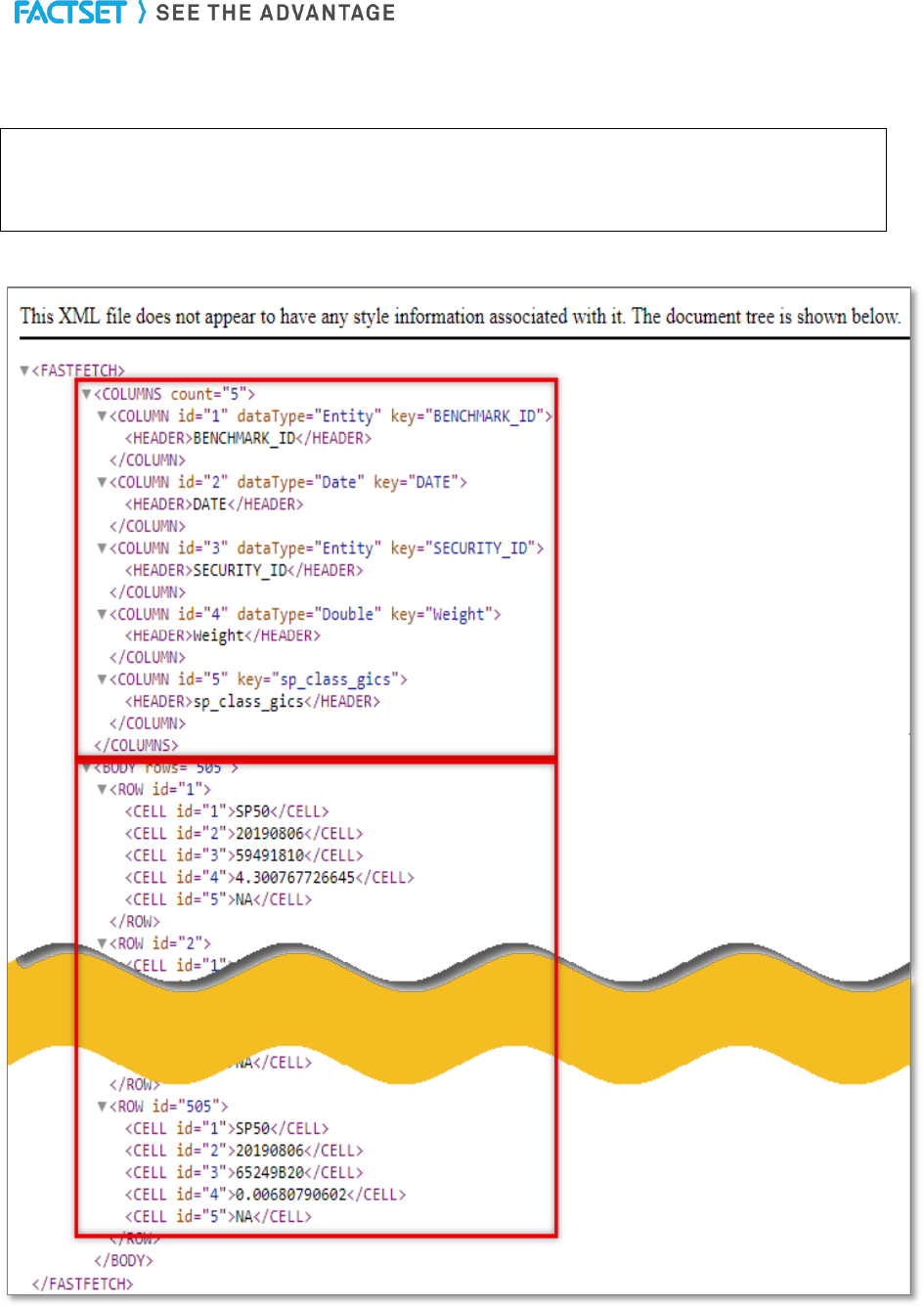

In this example, extract the S&P GICS classified sector names for the constituents of the S&P 500.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractBenchmarkDetail&format=xml&ids=

SP50&items=_SP_CLASS_GICS(0,,,%20%27%27SEC%27%27,%20%27%27NAME%27%27)&da

tes=0

Output

Note: The ExtractBenchmarkDetail Factlet, by default, works with Screening codes entered in the Items

argument of the syntax. If using an FQL code, enter an _ argument before the FQL items code, as

illustrated in this example using _SP_CLASS_GICS.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

44

9. ExtractOFDBItem

The ExtractOFDBItem function provides access to a list of securities and multiple data items for a range

of dates uploaded into a single Open FactSet Database (OFDB).

Open FactSet Database (OFDB)

OFDB is a high-performance multi-dimensional database system used to securely store proprietary

numeric and textual data on FactSet. It is ideal for users who manage large portfolios or maintain

extensive historical proprietary databases. OFDB optimizes large, multi-dimensional databases, giving

FactSet users highly flexible, fast access to large volumes of complex data that can be used in many

different applications. OFDB is based upon Online Analytical Processing technology, which is the basis

for multi-dimensional databases.

The syntax for the ExtractOFDBItem function is:

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractOFDBItem&ofdb=&ids=&items=&d

ates=&optional_arguments.....

where,

data

Variable name for the data returned

OFDB

OFDB file from which the items should be used. The default directory is Client if

other locations are used the path must be specified i.e personal:MyOFDB

ids

Array with a list of securities to extract the data for. If left blank data for all

securities in the OFDB will be extracted.

dates

One or more dates; Dates should be entered in start:end:freq format. (e.g.

'20101215:20110115:d')

items

One or more items from the OFDB

Optional arguments

datesOnly

Displays only the dates that are in an OFDB with the parameter datesOnly’,’Y’

universe

Screening expression to limit the universe

feelback

If the feelback argument is not used, the returned data series will "feel back"

over NAs to find the last actual data point and carry this data forward over the

NAs. For the data not to carry forward, use 'feelback', 'N'. The data is then

returned as it is in the database.

fqlflag

Optional argument that is necessary because by default, the ExtractOFDBItem

factlet goes through screening, but when there are _S in the Identifier or

spaces between the identifiers, it is necessary to extract the data through FQL

to get the values. Need to specify 'fqlflag','y'.

cal

Calendar setting, arguments include:

FIVEDAY: Displays Monday through Friday, regardless of whether there were

trading holidays.

FIVEDAYEOM: Displays Monday through Friday including a weekend date if it

falls on the last day of the month. Where the month-end does not fall on a

weekend, the calendar will act just as the standard five-day calendar.

SEVENDAY: Displays Monday through Sunday.

AAM: For Exchange code uses the calendar of a specific exchange,

represented by the exchange code. If there is no calendar available for a

specific exchange, the calendar will default to FIVEDAY.

unsplit

Displays prices with split adjustments in unsplit form.

currency

The currency in which the data is to be returned, using a string with the three-

character ISO code (e.g. ‘USD’ or ‘EUR’). This will only work when “Currency

Mapping” is used in the OFDB.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

45

Example 1

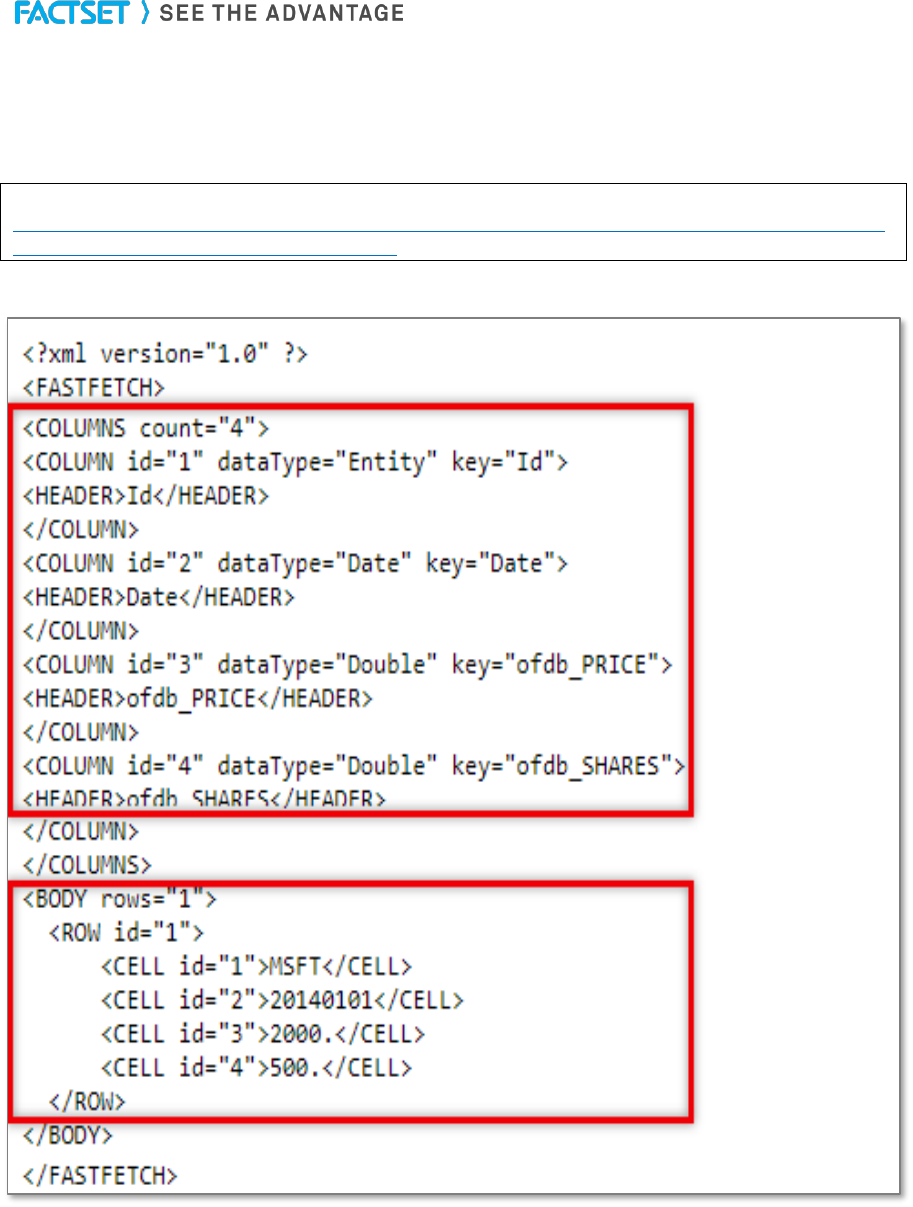

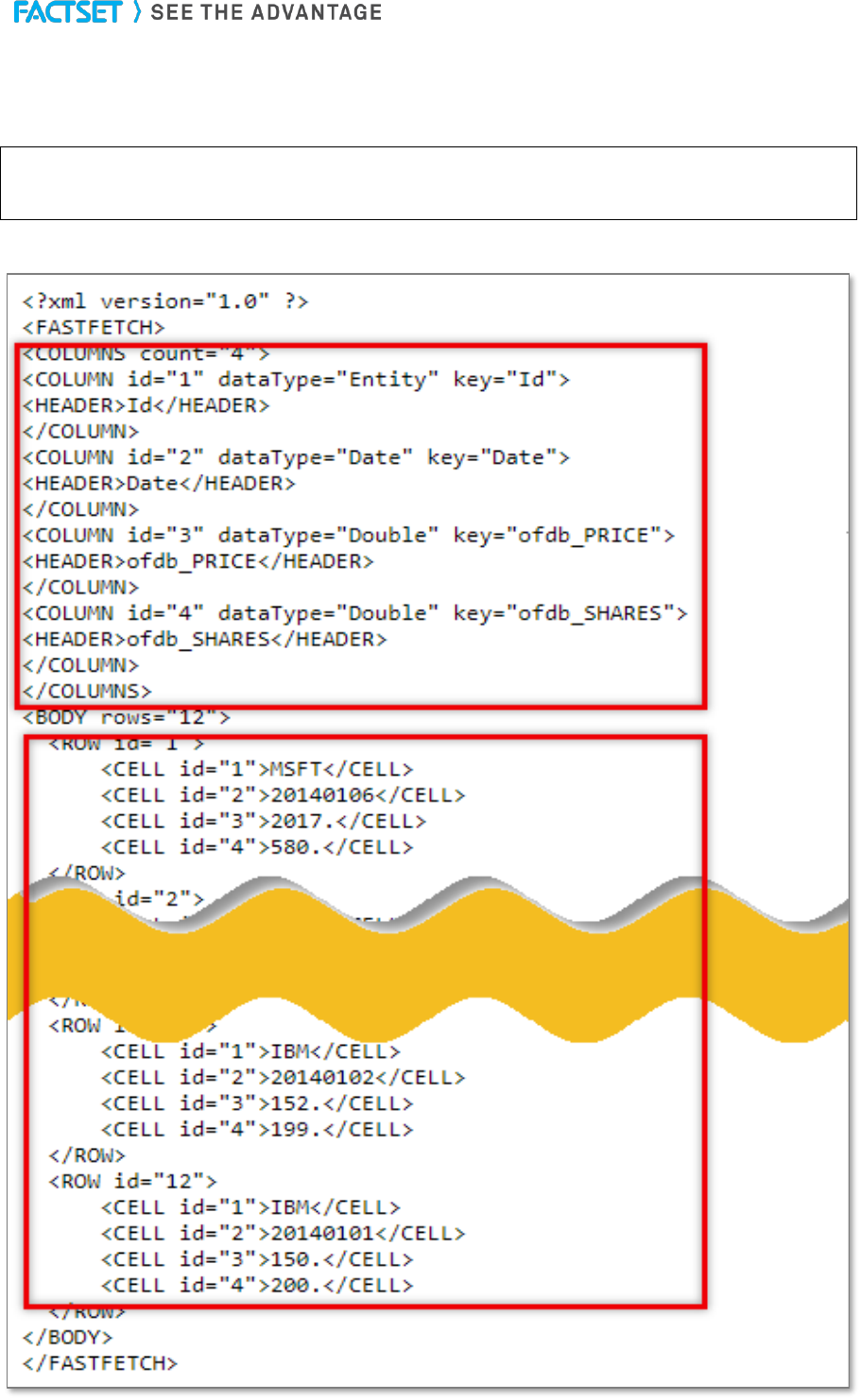

In this example, retrieve the price and shares data uploaded into the OFDB file titled MyPortfolio for

Microsoft as of 4 trading days ago, denoted with the date argument -3D.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractOFDBItem&ofdb=MyPortfolio&ids

=MSFT&items=PRICE,SHARES&date=-3D

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

46

Example 2

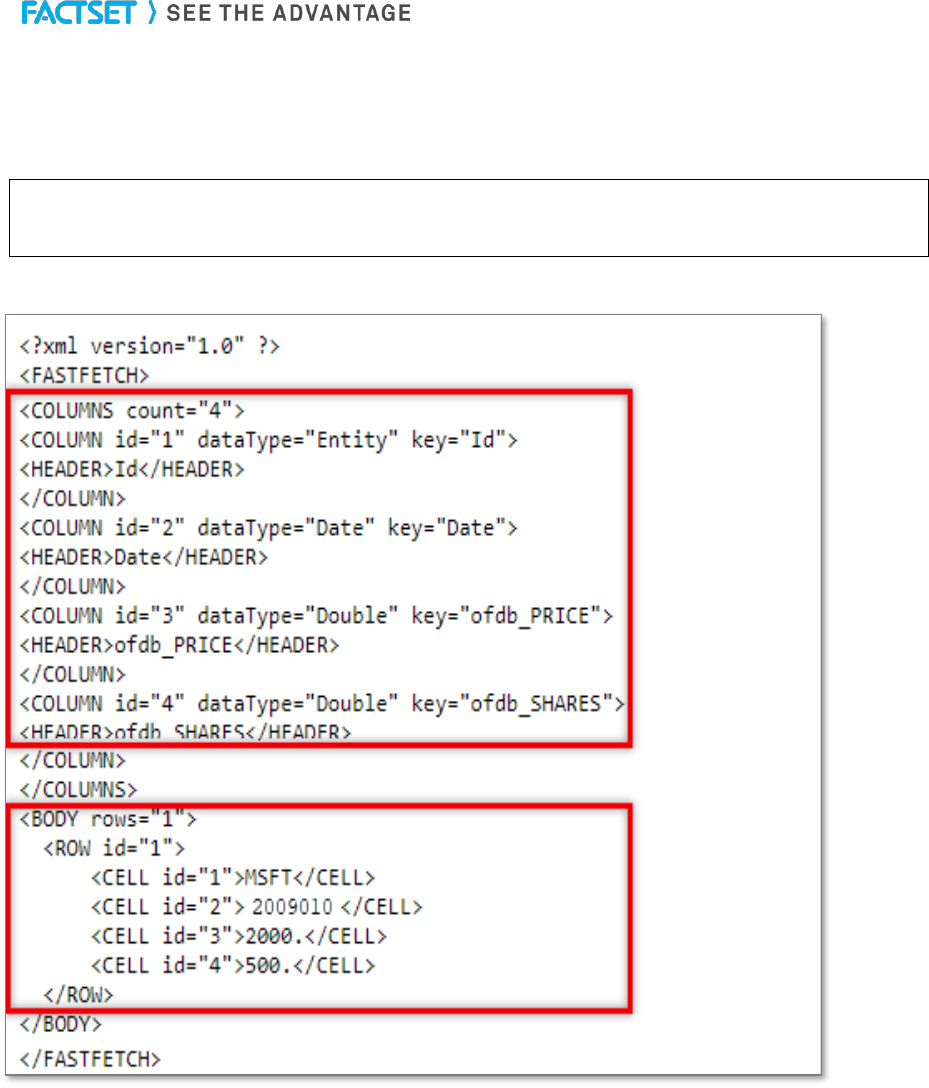

In this example, retrieve the uploaded shares and price data for the securities Microsoft and IBM OFDB

file titled MyOFDB saved in the Personal folder for a relative date range, starting 2 trading days ago and

going back 6 trading days ago.

URL

:https://datadirect.factset.com/services/FastFetch?Factlet=ExtractOFDBItem&ofdb=Personal:MyOF

DB&ids=MSFT,IBM&items=PRICE,SHARES&date=-1:-5D:D

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

47

Example 3

In this example, retrieve the uploaded shares and price data for the securities IBM and GM from an OFDB

file titled MyOFDB for an absolute date range, starting January 2009 and ending December 2011 on a

daily frequency, with the calendar set to FIVEDAY.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractOFDBItem&ofdb=Personal:MyOFD

B&ids=MSFT,IBM&items=PRICE,SHARES&date=20090101:20111231:D&cal=FIVEDAY

Output

Note: If during this date range the OFDB stores a value on a date that falls on a US holiday, by default

the value will be returned as an NA. However, by setting the calendar in this case to FIVEDAY this will

override the default and bring back the value.

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

48

Example 4

In this example, extract the universe of securities stored in the OFDB file titled Europe stored in the

subfolder Client:/Regions and their corresponding shares and price data for the last five days.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractOFDBItem&ofdb=Client:/Regions/

MyOFDB&ids=MSFT,IBM&items=PRICE,SHARES&date=0:-5D:D

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

49

Example 5

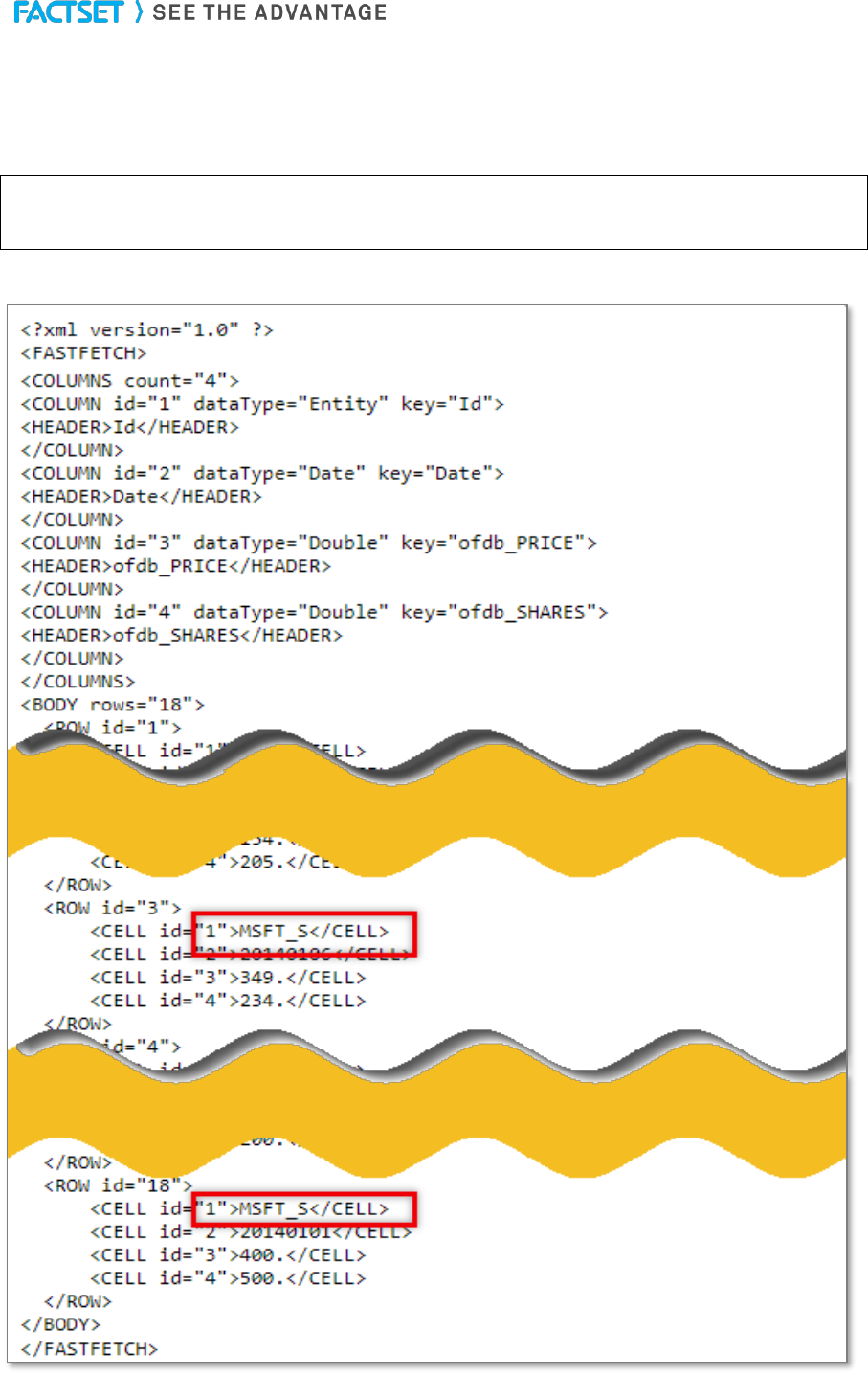

In this example the OFDB contains either symbols with spaces or short positions (symbols denoted with

_S) so the fqlFlag parameter must be used.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractOFDBItem&ofdb=Personal:MyOF

DB&ids=MSFT,IBM&items=PRICE,SHARES&date=0:-5D:D&fqlFlag=Y

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

50

10. ExtractScreenUniverse

The ExtractScreenUniverse function is used for extracting a list of CUSIPS stored in a single FactSet

screen. In the FactSet workstation, a user can screen for equity securities based on specified criteria and

store a list of companies using FactSet Universal Screening for equity or debt securities.

FactSet Universal Screening

Universal Screening in the FactSet workstation allows users to test investment strategies across all

databases simultaneously. It is possible to screen on a predefined investable universe or on tens of

thousands of companies worldwide using data items available on FactSet as the screening criteria.

For a more comprehensive overview of Universal Screening refer to Online Assistant page 20593.

The syntax for the ExtractScreenUniverse function is:

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractScreenUniverse&screen=&optiona

l_arguments....

where,

data

Variable name for the data returned

screen

Universal Screen for which the universe should be extracted. The default location is

Client: for any other location the path must be specified.

name

Optional parameter to display the name of the securities extracted. Specified as

'name', 'Y'.

All

Pulls all of the columns from a saved screen.

backtestDate

Ability to set a backtest date dynamically within the stat packages. This requires an

additional subscription to FactSet’s backtesting utilities.

removeColumns

Ability to hide specific columns from being displayed in the output. Requires the use of

the “All” parameter as well.

includeColumns

Ability to select specific columns to display in the output. Requires the use of the “All”

parameter as well.

Example 1

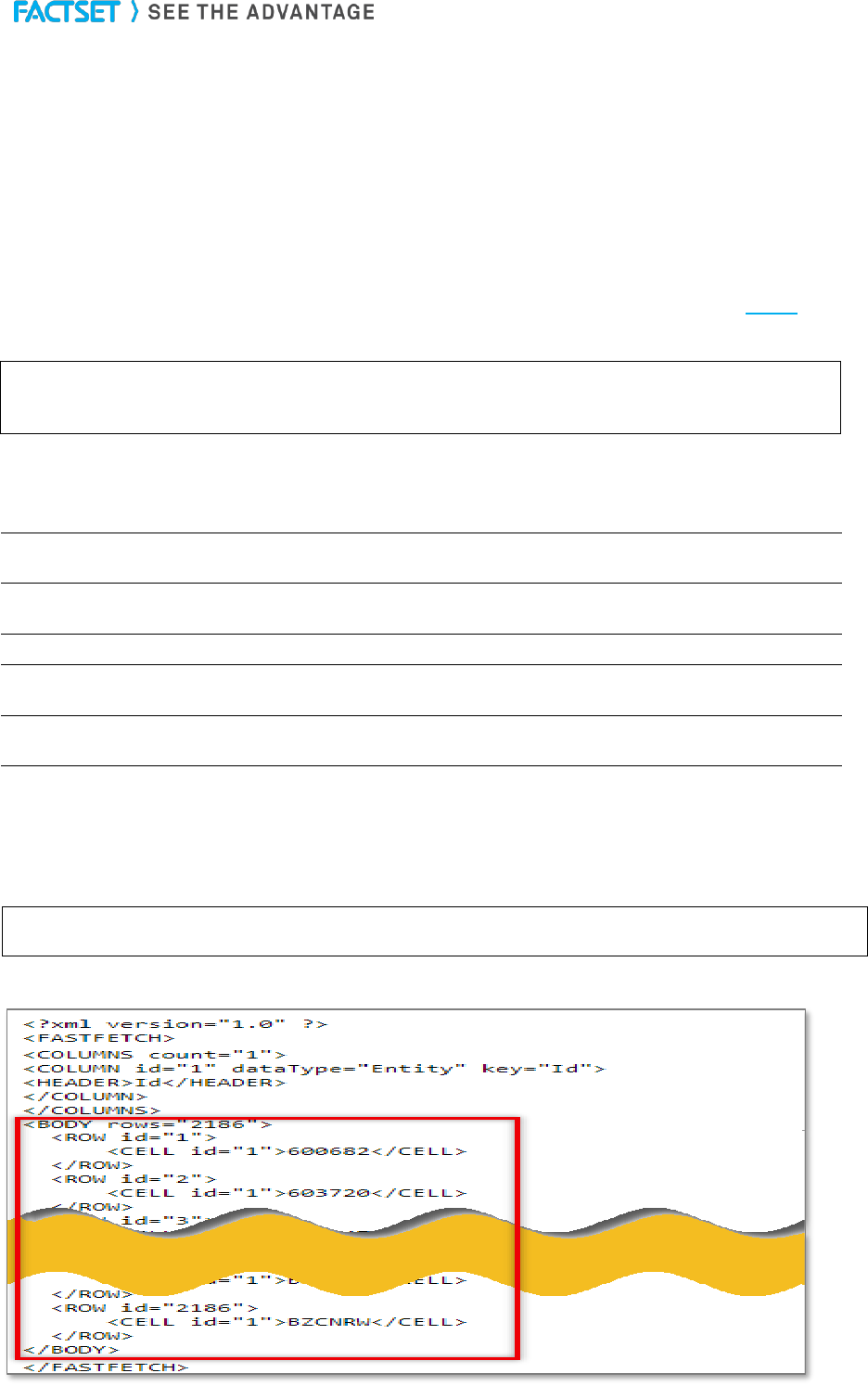

In this example, retrieve the securities stored in the screen titled MyScreen. The output displays the

CUSIPS for each security.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractScreenUniverse&screen=MyScreen

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

51

Example 2

In this example, retrieve all of the securities and parameters saved in the screen. Also, set a backtest

date to 6/30/2014.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractScreenUniverse&screen=Personal:

MyScreen&all=Y&backtestdate=20140630

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

52

Example 3

In this example, retrieve all of the securities returned by the screen, as well as only the first 3 parameters.

URL:

https://datadirect.factset.com/services/FastFetch?Factlet=ExtractScreenUniverse&screen=Personal

:PORTFOLIO%20BUILDING&all=Y&includecolumns=1,3,5

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

53

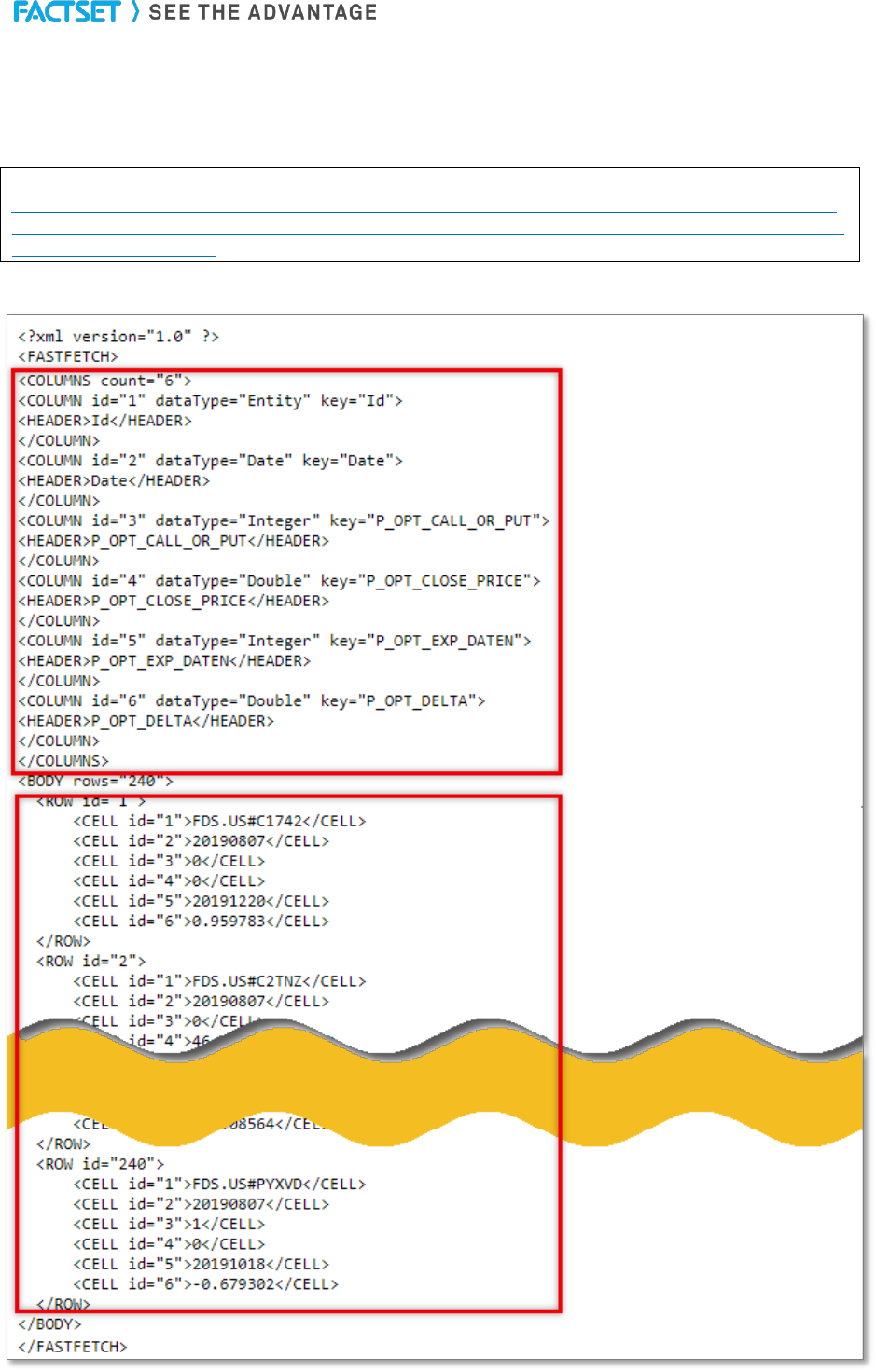

11. ExtractOptionsSnapshot

The ExtractOptionsSnapshot function is used for extracting options data for one or more conditions from

the FactSet-Options Derived Values database.

FactSet-Options Derived Values

The FactSet-Options derived Values provides access to expired options data such as historical pricing,

strike, expiration date, call or put, contract size, option type (equity, index), option style (American or

European), FactSet calculated Greeks (Delta, Theta, Vega, Rho, Gamma), and volatilities (Implied

Volatility, At-the-money Volatility).

The codes that are available for use in statistical packages provide access to option chain symbols for

both actively traded and expired options.

The syntax for the ExtractOFDBItem function is:

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractOptionsSnapshot&items=&date=&op

tional_arguments.....

where,

data

Variable name for the data returned

items

One or more items separated by a comma.

date

One or more dates; Dates should be entered in start:end:freq format. (e.g.

'20101215:20110115:d')

cond1/2/3

Screening condition with "=" or ">" or "<";

P_OPT_UNDERLYING_SECURITY=(default);P_OPT_ALL_VOLUME>

compval1/2/3

Value that meets cond1/2/3

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

54

Example 1

In this example a put or call flag, closing price, expiry date and delta is extracted for the options passing

the screening conditions that FactSet (FDS) is the underlying security and the expiration date is before

20190901.

URL:

https://datadirect.factset.com/services/FastFetch?factlet=ExtractOptionsSnapshot&items=P_OPT_C

ALL_OR_PUT,P_OPT_CLOSE_PRICE,P_OPT_EXP_DATEN,P_OPT_DELTA&ids=FDS&P_OPT_E

XP_DATEN>=20190901

Output

Copyright © 2021 FactSet Research Systems Inc. All rights reserved. FactSet Research Systems Inc. www.factset.com

55

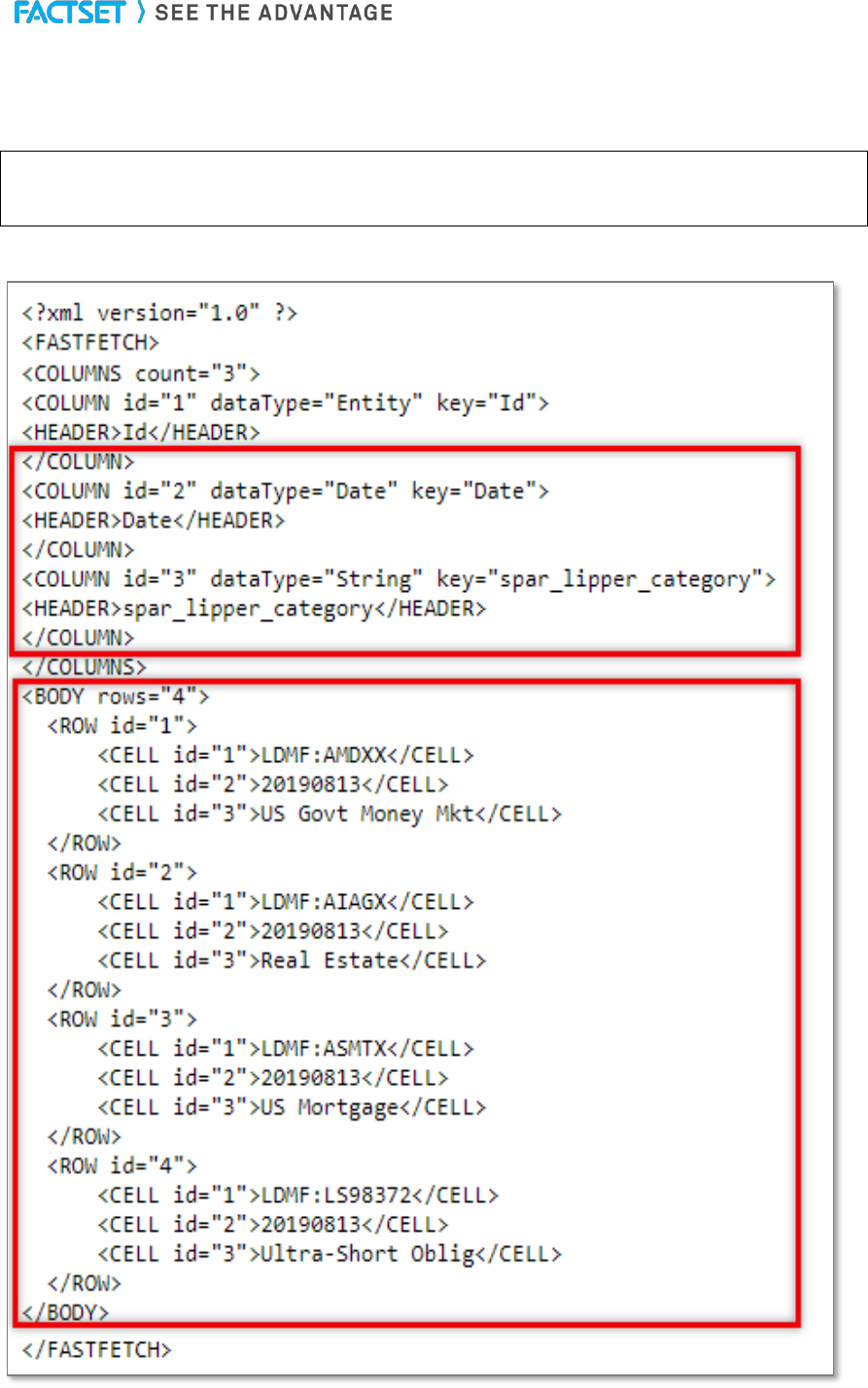

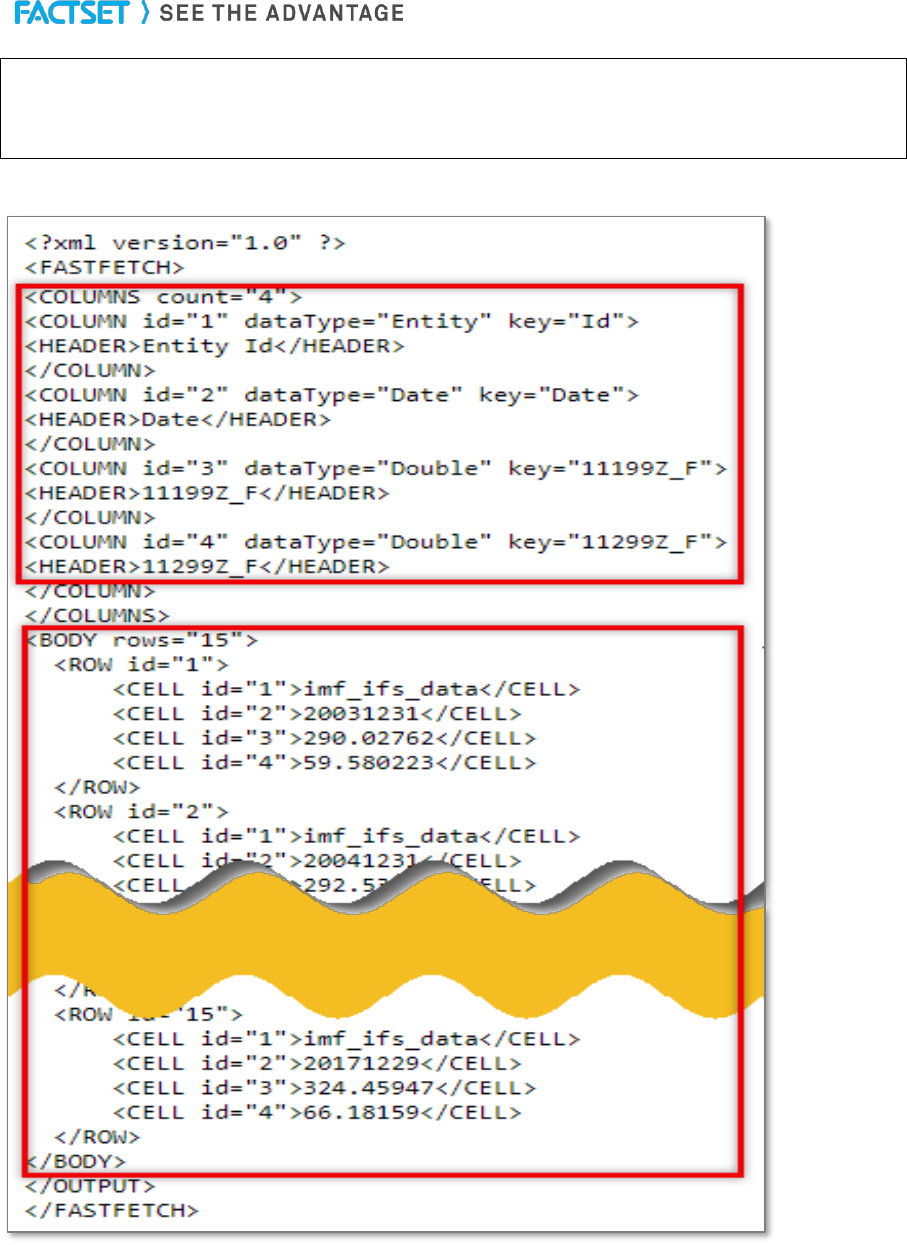

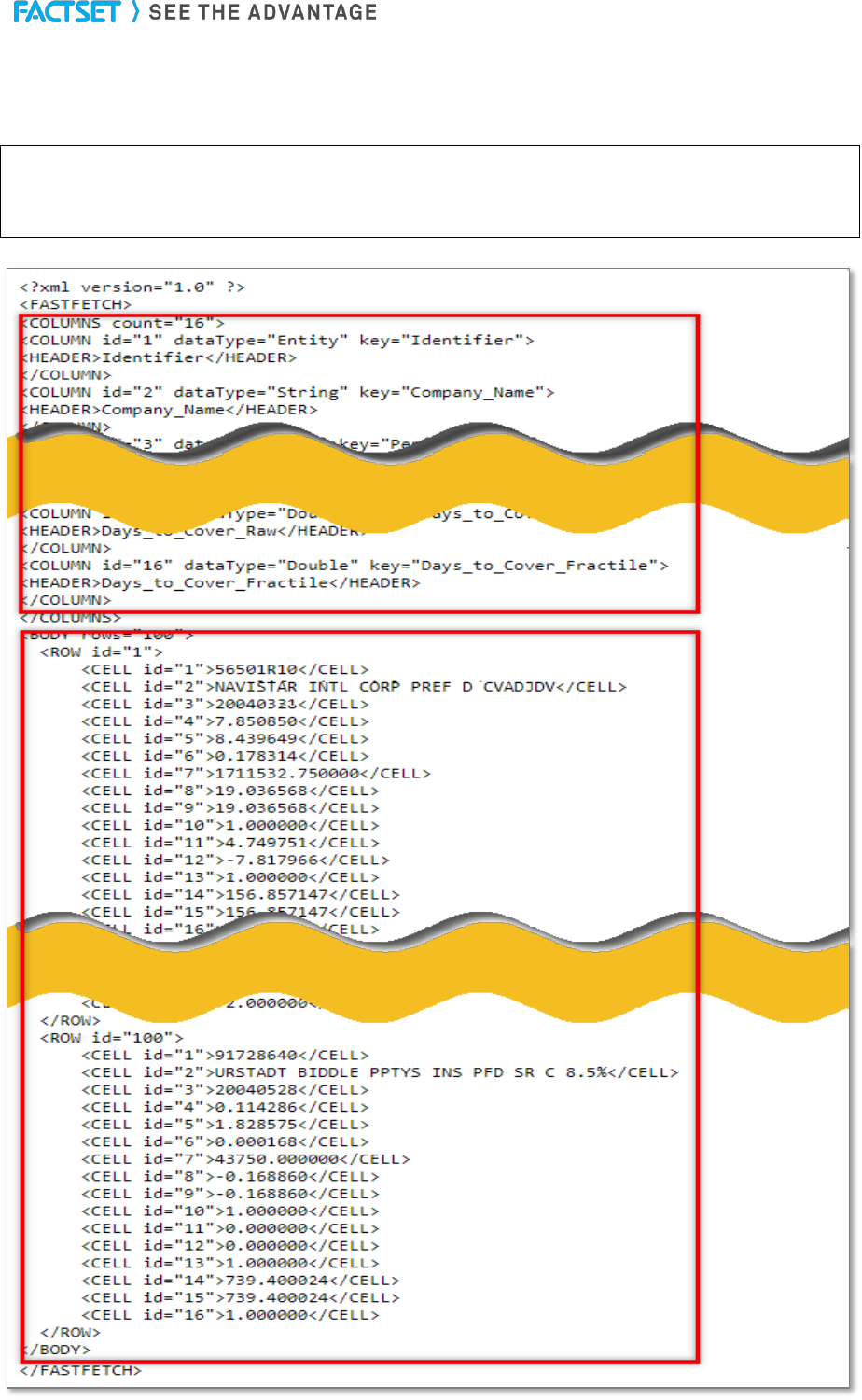

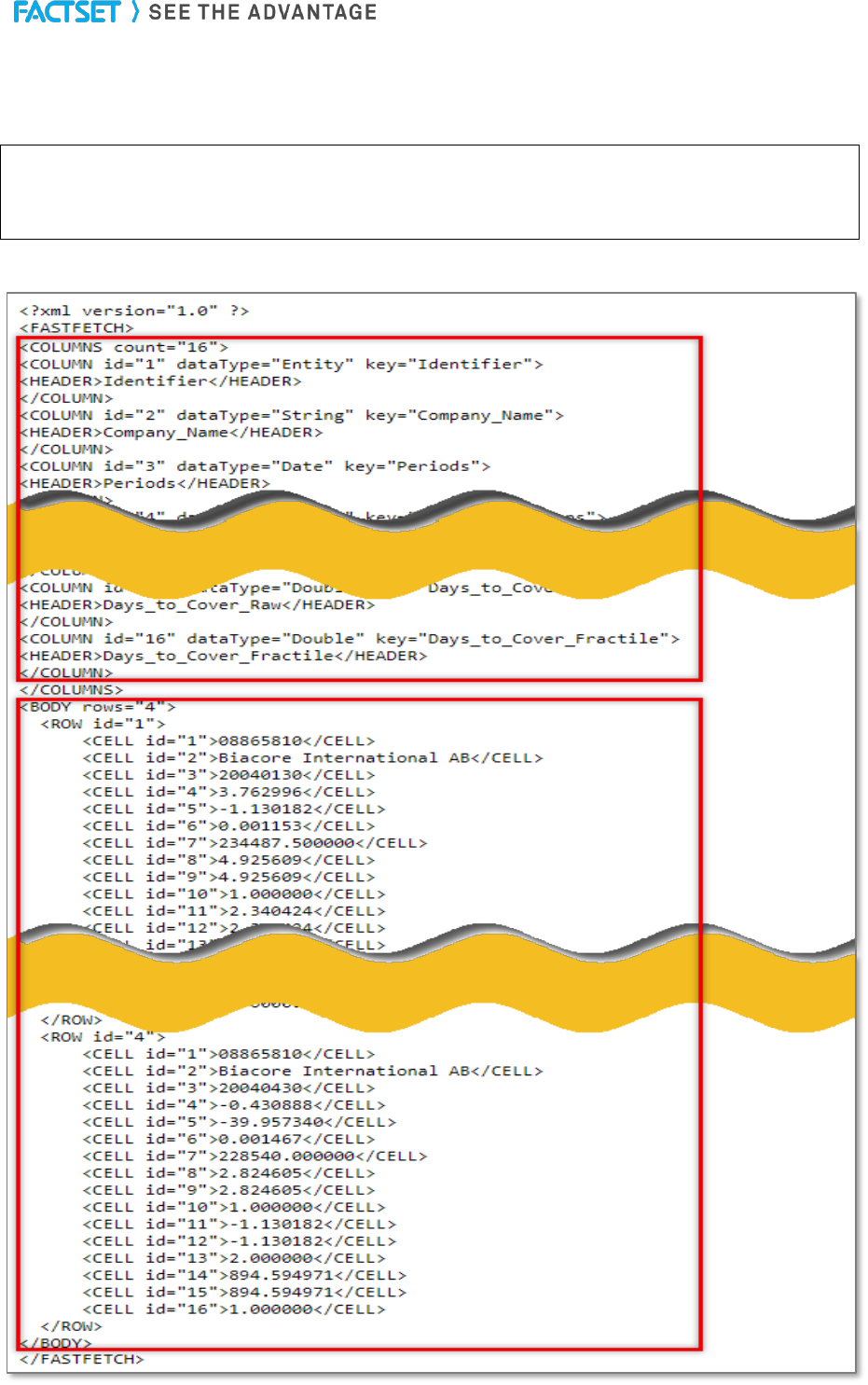

12. ExtractSPARData

The ExtractSPARData function is used for displaying SPAR data for specified funds from databases that

includes S&P, Lipper, Morningstar, Russell, eVestment, Nelson, Rogerscasey, and PSN. A subscription

to SPAR in FactSet is necessary to be able to extract this data in the Statistical Package.

SPAR (Style, Performance, and Risk)

SPAR, FactSet’s returns-based portfolio analysis application, provides reports and charts that can be

used to determine the style, performance, risk, and peer group analysis of selected portfolios,

benchmarks, and competitor funds. SPAR incorporates the industry-standard methodology developed by