Working Paper Series

Financial stability considerations in

the conduct of monetary policy

Paul Bochmann, Daniel Dieckelmann,

Stephan Fahr, Josef Ruzicka

Disclaimer: This paper should not be reported as representing the views of the European Central Bank

(ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

No 2870

Abstract

We empirically analyze the interaction of monetary policy with financial stability and the

real economy in the euro area. For this, we apply a quantile vector autoregressive model

and two alternative estimation approaches: simulation and local projections. Our specifi-

cations include monetary policy surprises, real GDP, inflation, financial vulnerabilities and

systemic financial stress. We disentangle conventional and unconventional monetary policy

by separating interest rate surprises into two factors that move the yield curve either at the

short end or at the long end. Our results show that a build-up of financial vulnerabilities

tends to be accompanied initially by subdued financial stress which resurges, however, over

a medium-term horizon, harming economic growth. Tighter conventional monetary policy

reduces inflationary pressures but increases the risk of financial stress. We find unconven-

tional monetary policy to be similarly effective in reducing inflation, but with a lower adverse

effect on growth and financial stress. Tighter unconventional monetary policy is also found

to have a dampening effect on the build-up of financial vulnerabilities.

Keywords: monetary policy, financial stability, macroprudential policy, quantile regres-

sions, monetary policy identification.

JEL codes: E31, E52, G01, G10.

ECB Working Paper Series No 2870

1

Non-technical summary

The interplay of monetary policy, financial conditions and the real economy has been part of

a long-standing macro-financial debate. Monetary policy transmits to the real economy by

affecting financial conditions which themselves are taken into consideration in the conduct of

monetary policy to stabilize inflation and the real economy. In this transmission process, mon-

etary policy may enhance financial stability during slowdowns by supporting the debt servicing

capacity of economic and financial sectors, while tighter monetary policy during exuberant times

can attempt to mitigate financial imbalances by implicitly leaning against the wind of frothy

market conditions.

By expanding the empirical quantile regression framework of Chavleishvili and Kremer (2021)

to include monetary policy shocks, inflation and financial vulnerabilities we analyze the inter-

action of monetary policy with financial stability conditions and the real economy. We estimate

impulse response functions of a quantile vector autoregressive model via two estimation tech-

niques. First, using a simulation approach, following Ruzicka (2021b), and, second, using local

projections as in Ruzicka (2021a). These quantile methods capture potential asymmetries in the

interactions between economic activity, financial stability variables and monetary policy over

the full distribution of the variables. Our specifications contain a range of interest rate shocks

along the euro area yield curve as measure for monetary policy, euro area real GDP, euro area

HICP inflation, the Systemic Risk Indicator (SRI) of Lang et al. (2019) as a measure of financial

vulnerabilities and the Composite Indicator of Systemic Stress (CISS) of Hollo et al. (2012) as

a measure of financial stress. All models are estimated on monthly euro area data from 2002 to

2019.

Our results show that surging financial stress has a strong short-term impact on economic

growth, especially on the lower tail of the GDP distribution, in line with Adrian et al. (2018). A

build-up of financial vulnerabilities tends to initially be accompanied by subdued financial stress,

but financial stress surges over the medium term. Finally, tightening conventional monetary

policy reduces real GDP growth and inflationary pressures accompanied by increasing financial

stress. Unconventional monetary policy, such as quantitative easing, identified as surprises

in longer-term interest rates are found to be similarly effective in reducing inflation but have

a smaller ’sacrifice ratio’ for GDP growth and financial stress. We also find that financial

vulnerabilities tend to mildly recede following tighter unconventional monetary policy.

ECB Working Paper Series No 2870

2

The empirical results lend themselves to counterfactual analysis on the trade-offs that mon-

etary policy faces when pursuing price stability. The implemented exercises using 1-year ahead

forecasts reveal that monetary policy has faced a trade-off during the global financial crisis:

either tighten to stabilize inflation forecasts at 2% or loosen to curb stress and prevent tail risks

to economic growth to increase.

ECB Working Paper Series No 2870

3

1 Introduction

The interplay of monetary policy, financial conditions and the real economy has been part

of a long-standing macro-financial debate. Monetary policy transmits to the real economy to a

large extent by affecting financial conditions. Equally, monetary policy takes financial conditions

into account to stabilize inflation and the real economy (Mishkin, 2007; European Central Bank,

2021). During slowdowns monetary policy can enhance financial stability by supporting the debt

servicing capacity of the non-financial sector and by containing losses for the financial sector.

In the extreme event of a financial crisis, monetary policy – especially through liquidity support

– is crucial to contain financial stress and to avoid the materialisation of adverse equilibria

(Mishkin, 2009; Bekaert et al., 2013). At the same time, however, the theoretical literature

suggests that accommodative monetary policy could create financial vulnerabilities by raising

asset values, lowering risk premia, increasing leverage and increasing maturity and liquidity

mismatches (Ajello et al., 2022).

During financial exuberant times tighter monetary policy can help mitigate financial im-

balances by implicitly leaning against the wind of frothy market conditions. This would help

reduce the likelihood and severity of future financial crises. However, the empirical evidence on

the general effect of monetary policy on financial vulnerabilities and its effectiveness in leaning

against the wind is mixed and entails trade-offs (Svensson, 2017; Kockerols and Kok, 2019; Schu-

larick et al., 2021; Boyarchenko et al., 2022). One monetary policy trade-off involves interactions

between macro variables such as inflation and GDP growth, and financial stability, as measured

by financial stress and vulnerabilities. A second trade-off in the conduct of monetary policy

relates to the management of tail risks for the real economy relative to tail risks for financial

stability. Finally, an intertemporal trade-off relates the potential impact of monetary policy on

short-term financial stress relative to adjustments to economic and financial vulnerabilities in

the medium-term.

In this paper, we empirically analyze the interaction of monetary policy shocks, financial

stability conditions and the real economy in the euro area. We do so by estimating impulse re-

sponse functions of a quantile vector autoregressive model via two estimation techniques, namely

through simulation, following Ruzicka (2021b), and local projections as in Ruzicka (2021a). The

specifications include five variables: a range of interest rates from the euro area yield curve

as measure for monetary policy, euro area real GDP, euro area HICP inflation, the Composite

ECB Working Paper Series No 2870

4

Indicator of Systemic Stress (CISS) of Hollo et al. (2012) as a measure of financial stress, and

the Systemic Risk Indicator (SRI) of Lang et al. (2019) as a measure of financial vulnerabilities.

Importantly, quantile methods capture potential asymmetries in the interactions between eco-

nomic activity (GDP and inflation), financial stability conditions (SRI and CISS) and monetary

policy shocks over the full distribution of the variables, including for impulse response analysis.

While macroeconomic conditions are typically summarized by real GDP and inflation, fi-

nancial stability conditions are less clearly defined. The SRI is our vulnerability metric and

characterizes the general state of the financial environment and serves as a ‘barometer’ for the

financial system (Duprey and Roberts, 2017). In exuberant times with elevated vulnerabilities,

the propagation of small shocks may result in amplifications for the economy, absent in normal

times (Lang et al., 2019). While vulnerability indicators contain forward-looking information,

they provide only limited information for the materialisation of stress at a specific point in time

in the future, given the uncertainty surrounding the future materialisation of shocks. For this,

our stress metric, the CISS, captures the materialization of financial instability and serves as

a ‘thermometer’ for the financial system (Chavleishvili and Kremer, 2021). The distinction of

financial vulnerability and stress is especially important to capture the intertemporal relation

between the initial build-up of vulnerabilities and subsequent downside tail risks to the financial

system and real economy.

Similarly to financial conditions, the monetary policy stance is only imperfectly summarized

by the short-term policy interest rate, given purchases of longer-term securities. Since the global

financial crisis, central banks have made active use of their balance sheets and forward guid-

ance. Monetary policy rates predominantly impact short-term market rates, forward guidance

affects interest rates further into the future, and purchases of medium- to long-term securities

affect interest rates over longer maturities. To capture monetary policies and their effects in an

empirical macro-financial estimation framework, we use monetary policy surprises in risk-free in-

terest rates between one month and ten years over a narrow time window (covering press release

and subsequent press conference) around the communication of ECB monetary policy decisions

contained in the “Euro Area Monetary Policy Event-Study Database” developed and regularly

updated by Altavilla et al. (2019). From these surprises we estimate a short- and long-term

factor of interest rate surprises and identify monetary policy shocks following G¨urkaynak et al.

(2005), Jaroci´nski and Karadi (2020) and Giuzio et al. (2021). The approach separates surprises

related to conventional monetary policy (short-term rates) from those related to unconventional

ECB Working Paper Series No 2870

5

monetary policy (longer-term maturities).

Our results show that surging financial stress has a strong short-term impact on economic

growth, especially on the lower tail of the GDP distribution, in line with earlier findings such

as Adrian et al. (2018). We also find that while a build-up of financial vulnerabilities tends

to initially be accompanied by subdued financial stress – i.e. below-average financial market

volatility, risk-pricing and excess returns – stress surges over the medium term. This provides

for evidence that financial market tranquility during the initial phase of a financial expansion

hits back with a vengeance down the road. Finally, the estimation indicates that tightening

conventional monetary policy reduces inflationary pressures at the cost of slower real GDP

growth and surging financial stress. Tightening unconventional monetary policy, identified as

surprises in longer-term interest rates, is found to be similarly effective in reducing inflation

as shorter-term rates, but has a smaller impact on growth and financial stress, while financial

vulnerabilities mildly recede. This indicates that conventional and unconventional monetary

policies may at times be complementary for stabilizing the economy and financial system.

The empirical results allow for a quantitative assessment of monetary policy using coun-

terfactuals to shed light on monetary policy trade-offs in its pursuit of price stability. A first

counterfactual traces out the effects of monetary policy on Growth-at-Risk (GaR; the 10th per-

centile of the forecasted GDP growth distribution one year ahead) when setting price stability

at the objective of 2% annual inflation. Especially during the global financial crisis, monetary

policy faced a trade-off: either tightening to stabilizing inflation forecasts at 2% or loosening

to prevent Growth-at-Risk to deteriorate. This analysis indicates the potential beneficial use of

alternative policy measures to offer a complementary angle for stabilisation of the real economy.

Having established the relative efficiency of different policy tools, we illustrate how the esti-

mation results could inform a monetary and macroprudential policy mix to enhance stabilisation

over the sample period. We assume policy objectives of a 2% median inflation forecast one year

ahead and stabilization of GaR at its sample average of -1.08%. Given the relative efficiencies

the policymaker uses a mix of monetary policy (long-end interest rate factor) and macropruden-

tial policy (SRI). The GaR objective is non-symmetric, implying that the policymaker avoids

that GaR falls below the value of -1.08% while focussing solely on the objective of inflation

otherwise. The policymakers thus provides a hedge against crisis outcomes. We compute the

needed counterfactual policies based on the cumulated impulse response functions and find that

relatively large monetary policy shocks would have been needed to bring inflation forecasts back

ECB Working Paper Series No 2870

6

to their target over the period 2005 until the first half of 2009. In contrast, over the earlier as

well as later parts of the sample period our results would have called for looser monetary policy.

Our results also indicate that looser macroprudential policy would have been needed starting

in September 2007 and throughout the global financial crises until September 2009 and again

on a few occasions during the euro area debt crisis to maintain GaR above its historical value.

Forecasts implied by these policy counterfactuals show that they would have been effective in

meeting combined inflation and growth targets, while limiting financial stress.

The remainder of the paper is structured as follows. Section 2 reviews the core elements

of financial stability conditions and monetary policy in the recent literature. In section 3 we

describe our data set, including the indicators used to measure financial stability conditions

and the identification of monetary policy shocks. Next, in section 4 we describe the econometric

specifications. Section 5 presents impulse responses from our quantile vector autoregressions and

uncovers the dynamic interactions of financial vulnerabilities and stress with the real economy,

and the impact of monetary policy shocks. Section 6 covers counterfactual analysis and illus-

trates trade-offs between price stability and financial stability objectives for monetary policy.

It further assesses interactions between monetary policy and macroprudential policy. Finally,

section 7 concludes.

2 Monetary policy and financial stability interactions

Monetary policy frameworks around the globe focus on price stability as their main objective,

often accompanied with additional objectives such as full employment or financial stability.

Monetary policy’s role for financial stability is often subsumed in the effectiveness of monetary

policy transmission or delegated to other policy domains such as macroprudential policy. While

it is generally accepted that monetary policy takes financial stability into account at least in

some form, quantitative trade-offs are less prominent in the literature. Smets (2014) indicates

that the degree to which monetary policy should take financial stability considerations into

account depends crucially on its effectiveness in addressing risks to financial stability, but also

to what degree the financial stability considerations undermine the credibility of the central

bank’s price stability mandate.

Monetary policy faces several challenges when including financial stability considerations.

First, narrow indicators of financial conditions, stress and vulnerabilities (such as metrics of

ECB Working Paper Series No 2870

7

risk-taking, liquidity and leverage) offer only partial measures of financial stability, especially

when considered in isolation, but are not fully comprehensive of prevailing financial stability

conditions. In turn, monetary policy instruments are multiple, and each one may interact differ-

ently with financial stability. Furthermore, at least theoretically, monetary policy may create an

inter-temporal trade-off for financial stability whereby accommodative monetary policy improves

current financial conditions in the short run at the cost of increasing future financial vulnerabil-

ities Adrian and Liang (2018). Empirically, it appears unclear to date whether monetary policy

itself can influence financial vulnerabilities, partly because financial cycles are typically much

longer than the business cycles monetary policy reacts to (Boyarchenko et al., 2022). Ultimately,

monetary policy’s efficacy as a tool for financial stability will depend on the cost-benefit trade-off

of tighter monetary policy for economic activity and inflation.

Our paper relates to different strands of the literature. First, we contribute to the literature

that investigates the empirical relationship between monetary policy and financial stability. The

primary focus of existing studies lies on financial vulnerabilities. However, a (surprise) monetary

tightening could also lead to acute episodes of surging financial stress and an abrupt tightening

of financial conditions. Recent literature (Adrian et al., 2019; Figueres and Jaroci´nski, 2020)

points to the importance of associated indicators for short-term (up to one year ahead) downside

risks to economic growth. Boyarchenko et al. (2022) provide a recent and detailed review of the

empirical literature studying the relationship between monetary policy and financial vulnerabil-

ities. Overall, the authors conclude that empirical evidence on the link between monetary policy

and financial vulnerabilities is limited.

However, the current literature does not rule out causal effects of monetary policy on finan-

cial vulnerabilities. Several research gaps emerge from this existing literature, some of which our

paper attempts to fill: Existing studies focus primarily on the United States while analyses for

the euro area are scarce. Furthermore, existing studies differ in their measurement of financial

vulnerabilities and focus mostly on narrow concepts such as asset valuations in selected mar-

kets, risk-taking by banks or other intermediaries, leverage and liquidity-maturity mismatches

or leverage of financial intermediaries, households and businesses. However, vulnerabilities that

have material impacts on the real economy appear to emerge from the interplay of asset prices

and credit (Jord`a et al., 2015) and we therefore employ a broad indicator of financial vulnera-

bilities in this paper.

Second, we estimate the dynamic interactions of macroeconomic, financial and monetary pol-

ECB Working Paper Series No 2870

8

icy variables using multivariate quantile regression techniques. Quantile regressions of Koenker

and Bassett Jr (1978) have been extended to multivariate dynamic frameworks in various

ways. One approach involves multiple equations and iteration or simulation (White et al.,

2015; Chavleishvili and Manganelli, 2019; Montes-Rojas, 2022; Ruzicka, 2021b). The other ap-

proach focuses on a single-equation setup and direct estimation through local projections of

Jord`a (2005) in combination with quantile regression – a prominent example is the work of

Adrian et al. (2019). Identification, smooth estimation, and inference for quantile regression

local projections is studied by Ruzicka (2021a). A unique feature of our paper is that we employ

both estimation approaches by using the methods from Ruzicka (2021b) as well as from Ruzicka

(2021a). Doing so, we obtain two valid estimates, which trade off bias and variance of impulse

response functions differently. In a least squares regression setting, Plagborg-Møller and Wolf

(2021) show that at shorter forecast horizons local projections are comparable with structural

vector autoregressions (Sims, 1980, SVAR), whereas at longer forecast horizons the local pro-

jections have lower bias but higher variance. We expect that the same phenomenon arises in a

quantile regression setting, as well.

Third, our assessment of the impact of monetary policy on financial stability focuses on an

assessment of the tails of the distribution of real economic and financial variables. The estimation

provides impacts for the lower and upper quantiles of these distributions and offers thereby risk

considerations beyond the impact on median or average effects. This relates to other work on the

stance of monetary and macroprudential policy using quantile reqressions, such as in Cecchetti

(2006), Kilian and Manganelli (2008), Duprey and Ueberfeldt (2018), Aikman et al. (2019)

and Carney (2020). The common feature of these approaches resides in the use of the tail of

forecasted variables to infer assessment of risks to the economy or a policy stance. And finally,

we relate to the empirical literature that identifies effects of monetary policy on asset prices

and the macroeconomy using high-frequency financial market surprises around central bank

monetary policy announcements going back to Kuttner (2001), as well as literature about the

identification of monetary policy from such event-study data (G¨urkaynak et al., 2005; Altavilla

et al., 2019; Jaroci´nski and Karadi, 2020; Giuzio et al., 2021).

ECB Working Paper Series No 2870

9

3 Financial stability indicators and identification of monetary

policy shocks

Our data consists of a set of aggregate euro area macro-financial and monetary policy variables,

starting in the beginning of 2002 and running through the end of June 2019 at monthly frequency.

Our baseline model input consists of two macroeconomic variables, namely real GDP growth

and HICP inflation, the Composite Indicator of Systemic Stress (CISS) as a measure of financial

stress (Hollo et al., 2012; Chavleishvili and Kremer, 2021), and the Systemic Risk Indicator

(Lang et al., 2019, SRI) as a measure of financial vulnerabilities,monetary policy shocks built

from surprise rate changes over narrow time windows covering the communication of monetary

policy decisions through press release and the subsequent press conference on ECB Governing

Council monetary policy meeting dates using a data set developed and regularly updated by

Altavilla et al. (2019). The computation of these shocks is explained in detail further below in

Section 3.3.

Figure 1 plots the macro-financial variables used in our estimation which are further sum-

marized in Table 1. We deliberately represent financial stability aspects in our models with

two separate variables, distinguishing between short-term financial stress which can trigger in-

stability and medium-term vulnerabilities which make the financial system more susceptible to

destabilizing triggers. We approximate monthly GDP by interpolating a quarterly GDP series

with a monthly index of industrial production for the euro area.

3.1 Financial stress

The CISS serves as our measure of financial stress and captures the severity of financial crises,

serving as a ‘thermometer’ of financial instability. It is a timely, frequent and publicly available

indicator based on 15 individual indicators grouped into five sub-indices: financial intermediaries,

bond markets, equity markets, foreign exchange markets, and money markets. The contribution

from financial intermediaries is around 30%, that of equity markets around 25%, and each of

the three remaining sub-indexes around 15%.

1

Importantly, the CISS takes into account the

1

The equity market sub-index comprises stock price volatility of non-financial corporations (NFC), a measure

of maximum cumulated stock price losses and a measure of stock-bond correlation. The FX market sub-index

captures the volatility of EUR/USD, EUR/JPY and EUR/GBP exchange rates. The financial intermediaries

sub-index reflects bank stock return volatility, financial-nonfinancial bonds spread, and the cumulated loss of the

book-price ratio of banks. The bond market sub-index captures the volatility of German sovereign bonds (at

10-year maturity), the spread between A-rated NFC and sovereign bonds, and the 10Y interest rate swap spread.

ECB Working Paper Series No 2870

10

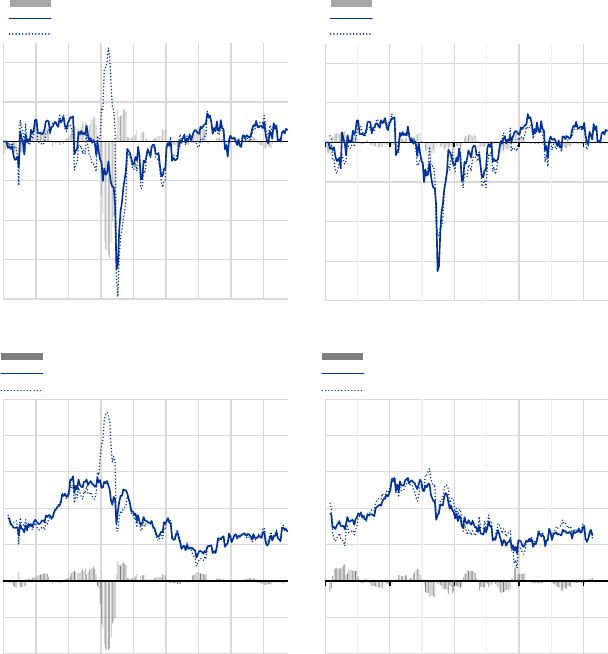

Figure 1: Macro-financial variables, monthly

‐2

‐1.5

‐1

‐0.5

0

0.5

1

1.5

2002M1

2003M1

2004M1

2005M1

2006M1

2007M1

2008M1

2009M1

2010M1

2011M1

2012M1

2013M1

2014M1

2015M1

2016M1

2017M1

2018M1

2019M1

RealGDPgrowth

‐0.6

‐0.4

‐0.2

0

0.2

0.4

0.6

0.8

2002M1

2003M1

2004M1

2005M1

2006M1

2007M1

2008M1

2009M1

2010M1

2011M1

2012M1

2013M1

2014M1

2015M1

2016M1

2017M1

2018M1

2019M1

HICPinflation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2002M1

2003M1

2004M1

2005M1

2006M1

2007M1

2008M1

2009M1

2010M1

2011M1

2012M1

2013M1

2014M1

2015M1

2016M1

2017M1

2018M1

2019M1

CISS

‐0.6

‐0.4

‐0.2

0

0.2

0.4

0.6

2002M1

2003M1

2004M1

2005M1

2006M1

2007M1

2008M1

2009M1

2010M1

2011M1

2012M1

2013M1

2014M1

2015M1

2016M1

2017M1

2018M1

2019M1

SRI

Notes: Monthly data 2002M1-2019M6. Variables are displayed as they enter

our models: real GDP and HICP in first differences of logs (in %), CISS and

SRI in levels.

correlation across sub-components, whereby higher correlation implies higher values of systemic

stress. The CISS leads GDP by up to one quarter (Chavleishvili and Kremer, 2021) and has

been shown to outperform narrower measures of financial conditions in the prediction of one-year

ahead tail risks to euro area output growth (Figueres and Jaroci´nski, 2020).

3.2 Financial vulnerabilities

We capture medium-term financial vulnerabilities with the Systemic Risk Indicator (SRI): a

broad-based cyclical indicator that captures risks stemming from potential overvaluation of

property prices, credit conditions, external imbalances, private sector debt burden and the po-

tential mispricing of risk that serves as a ‘barometer’ of financial instability (Lang et al., 2019).

With the exception of the credit category, the authors use one variable for each of the aforemen-

The Money market sub-index comprises the 3M EURIBOR volatility, its spread to the 3M French T-bill spread,

and a measure of emergency lending of the Eurosystem.

ECB Working Paper Series No 2870

11

Table 1: Summary statistics

Statistic T Mean St. Dev. Min Max

Real GDP 210 0.100 0.359 −1.416 0.910

HICP 210 0.138 0.171 −0.413 0.644

CISS 210 0.177 0.201 0.002 0.913

SRI 210 −0.068 0.296 −0.436 0.542

Notes: Real GDP and HICP is in first differences of monthly logs

(in %). CISS and SRI are in monthly levels.

tioned categories, selecting from a larger pool of potential variables and transformations those

with the best predictive ability for systemic financial crises. In total, Lang et al. (2019) derive

six indicators which are normalized and aggregated as an optimally weighted average in terms

of overall predictive power of the composite indicator.

2

Measures of financial vulnerabilities are typically used to inform macroprudential policies.

For example, the credit-to-GDP gap is instrumental in the calibration of countercyclical capital

buffers. The SRI increases on average several years before the onset of systemic financial crises

with superior early-warning properties in comparison to the credit-to-GDP gap. In this capacity,

it also has significant predictive power for large declines in real GDP growth three to four years

into the future and its level at the onset of systemic financial crises is highly correlated with

measures of subsequent crisis severity. The SRI therefore provides useful information about

both the probability and the likely cost of systemic financial crises which makes it our preferred

measure of the financial cycle in comparison to other available indicators.

Financial vulnerabilities evolve more slowly and more gradually than the other variables in

our models, reflecting that financial cycles tend to last longer than economic cycles. Indeed,

the within-month interactions between the SRI and the other variables, measured by quantile

impulse responses, are negligible and insignificant – except for financial stress (CISS) at the

90th percentile. On the other hand, financial vulnerabilities can be controlled by a range of

financial stability instruments, microprudential and macroprudential. Due to the negligible

contemporaneous interactions, we can interpret SRI changes as exogenous shocks, and treat the

SRI as the third policy tool, in addition to conventional and unconventional monetary policy.

2

The six sub-indicators used are the two-year change in the bank credit-to-GDP ratio, the two-year growth rate

of real total credit, the two-year change in the debt-service-ratio, the three-year change in the RRE price-to-income

ratio, the three-year growth rate of real equity prices, and the current account-to-GDP ratio.

ECB Working Paper Series No 2870

12

3.3 Monetary policy shocks

A large empirical literature, going back to Kuttner (2001), identifies effects of monetary policy

on asset prices and the macroeconomy using high-frequency, intra-day, financial market price

changes over short time windows covering central bank monetary policy announcements. Based

on such high-frequency event-study data, G¨urkaynak et al. (2005) find that two independent

factors constructed from federal funds futures – the first related to short rates and an independent

second factor related to rates of longer maturities – summarize the effects of U.S. monetary policy

on bond prices and stock returns.

We use their approach to extract two factors from intra-day overnight index swap (OIS) rate

changes over narrow time windows covering the press release as well as the subsequent press

conference about monetary policy decisions on ECB Governing Council monetary policy meeting

dates using the “Euro Area Monetary Policy Event-Study Database”, developed and regularly

updated by Altavilla et al. (2019). These two factors capture surprises along the yield curve as

they are constructed by fitting the time series of surprises in OIS rates of seven maturities (one,

three and six months as well as one, two, five and ten years). Surprises in OIS rates of maturities

longer than two years are only available from August 2011 onward and we proxy these series by

surprises in German government bond yields of the same maturity for the period from January

2002 to July 2011.

To provide a structural interpretation of the two factors, we rotate them as in G¨urkaynak

et al. (2005) such that the second factor is not impacted by surprises in the OIS rate of the

shortest maturity, i.e. its factor loading on the 1-month OIS surprises is set to zero, while im-

posing orthogonality between the two rotated factors. Finally, the rotated factors are rescaled

to match the standard deviations of 3-month OIS surprises for the first factor and 10-year OIS

surprise for the second factor. In this way, the first factor corresponds to shorter maturities –

reflecting surprises related to conventional monetary policy – and the second factor corresponds

to longer maturities, capturing surprises related to unconventional monetary policy. For conve-

nience we label these factors short- and long-end factors, in line with G¨urkaynak et al. (2005).

The corresponding factor loadings are shown in Figure 2.

The short- and long-end factors provide information about interest rate surprises along

the yield curve. Jaroci´nski and Karadi (2020) point out that such surprises reveal, addition-

ally to information about the monetary policy stance, also private central bank information

ECB Working Paper Series No 2870

13

Figure 2: Monetary policy surprise factors - loadings

1m 3m 6m 1Y 2Y 5Y 10Y

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

F1 - short

F2 - long

Notes: The figure shows the estimated factor loadings after rotation.

about the state of the economy. To separate monetary policy from central bank information

shocks, Jaroci´nski and Karadi (2020) use an identification strategy with sign restrictions on high-

frequency stock price changes around monetary policy announcements. A positive co-movement

between intra-day interest rates and intra-day stock prices is interpreted as an information shock

as the central bank reveals new information about the state of the economy. In turn, a negative

co-movement reflects a monetary policy surprise whereby higher interest rates imply a decline

in stock prices, while a fall in interest rates implies higher stock prices. While intuitive, this

method yields implausible results for the euro area; in particular, the response of the monthly

stock index remains insignificant while a monthly BBB bond spread index used in their model

declines after a contractionary monetary policy shock. However, the analysis in our paper

builds on a consistent identification between high-frequency monetary policy shocks and asset

price responses to assess the financial stability implications of monetary policy.

As an alternative to stock prices, we therefore identify monetary policy and information

shocks based on daily changes of non-financial corporate (NFC) bond spreads instead of intra-

day stock price changes, as suggested by Giuzio et al. (2021). More specifically, we identify

monetary policy shocks from positive co-movement of our interest rate factors with daily changes

in BBB-rated euro-denominated NFC bond spreads (at 5-year maturity). Thus, a contractionary

monetary policy shock occurs when interest rates rise and bond spreads widen simultaneously

whereas an expansionary monetary policy shock is characterized by falling interest rates and

narrowing bond spreads. Consequently, central bank information shocks are identified from

ECB Working Paper Series No 2870

14

negative co-movement between interest rate surprises and bond spreads. This identification

strategy improves not only the response of monthly bond spreads but also the response of

monthly stock prices to monetary policy shocks. We use bond spreads from Bank of America

obtained through Bloomberg until March 2007, while from April 2007 we use bond spreads from

iBoxx, which we found to be more liquid compared to those from Bank of America but not

continuously available before April 2007. Summary statistics of the interest rate series, bond

spreads, and identified surprises can be found in Table 2.

Table 2: Summary statistics for monthly interest rate factors and monetary policy surprises

(January 2002 - June 2019), T = 210, in bps.

Mean St. Dev. Min Max

Short-end factor −0.09 2.87 −13.20 16.70

Short-end factor, MP shock 0.03 1.54 −6.34 16.70

Short-end factor, CB info shock −0.11 2.39 −13.20 10.27

Long-end factor 0.00 4.09 −25.77 13.22

Long-end factor, MP shock 0.06 1.97 10.09 −10.21

Long-end factor, CB info shock −0.12 3.52 −25.77 13.22

BBB-rated NFC bond spread changes 0.13 3.40 -8.94 23.52

The cumulated factors of surprises in OIS rates are displayed in Figure 3 together with their

information and monetary policy components, based on the identification using BBB-rated NFC

bond spreads. Increasing values indicate tightening of interest rates relative to the prevailing

market expectations before monetary policy statements.

The short-end factor indicates a tightening of surprises in short rates during the early part

of our sample, followed by a period of loosening leading up to the Global Financial Crisis,

then a short period of tightening at the peak of Global Financial Crisis and finally an overall

loosening of rates over the remainder of our sample period. These dynamics were mainly driven

by surprises identified as central bank information shocks, while monetary policy shocks often

moved in opposite direction and indicate an overall tightening.

In turn, the cumulated long end factor falls strongly in July and August 2008, driven by

central bank information shocks, while gradually tightening for most of the remainder of the

sample period. This long tightening episode appears to be driven at least partially by monetary

policy shocks.

ECB Working Paper Series No 2870

15

Figure 3: Cumulated monetary policy factors 2002-2019

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

-50

-40

-30

-20

-10

0

10

20

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

long end factor

long end factor - CB info.

long end factor - MP

-40

-30

-20

-10

0

10

20

30

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

short end factor

short end factor - CB info.

short end factor - MP

Notes: The figure shows cumulated factors before and after identification with

BBB-rated NFC bond spreads in basis points.

The factors are extracted in a first step using maximum likelihood estimation to employ them

in a second step for estimating quantile treatment effects of policy interventions by minimizing

asymmetric l

1

loss functions. As a result, the two steps of the empirical strategy employ different

loss functions. While it may be possible to use the l

1

loss functions in factor extraction, such

an approach has not been used in the literature on monetary policy event study factors as far

as we know and is not considered in this work either.

4 Quantile modelling

4.1 Estimating quantile treatment effects of structural shocks

The main goal of our estimations is to quantify the impact of exogenous shocks on vulner-

abilities in the real economy and the financial sector. We do so by estimating the effect of

structural shocks on different parts of the distribution of the response variables, namely real

GDP growth, HICP inflation, financial vulnerabilities and financial stress. However, this task

is complex because we need to model the distributions of our endogenous variables, along with

their contemporaneous and dynamic interactions. Specifically, we estimate quantile treatment

effects (see Koenker, 2005, pp. 26–32) of structural shocks. A quantile treatment effect measures

how each quantile of a response variable is affected by a treatment. In our case, the treatment

ECB Working Paper Series No 2870

16

is an exogenous impulse, also called a shock.

We estimate the quantile treatment effects by two different methods. The first is a simulation-

based, two-step approach in form of a quantile vector autoregressive model, while the second

one relies on direct estimation and regularization in form of a quantile local projection approach.

Both methods identify the shocks by recursive short-run restrictions and provide valid estimates

of the quantile treatment effect. However, the methods differ in their finite sample performance

and in robustness to misspecification, especially at longer forecast horizons. In the following, we

provide the general features of the two estimation methods together with basic technical notions

of their setup and refer the reader for additional details to the referenced papers.

The first method – simulation-based – follows Ruzicka (2021b) and is based on the estimation

of the quantile regression process for a system of equations, with subsequent simulation using the

approach proposed by Koenker and Xiao (2006), described in detail in Koenker et al. (2018, pp.

328–329), and also used by Montes-Rojas (2022). It is similar to Chavleishvili and Manganelli

(2019) and Montes-Rojas (2022). However, unlike Chavleishvili and Manganelli (2019), we do

not set any sample paths to their median values and instead consider the full set of possible

sample paths. This increases the computational complexity, but gives a more complete and

agnostic picture of the effects we estimate. Unlike Montes-Rojas (2022) and Chavleishvili and

Manganelli (2019), we do not discretize the model on an ex-ante chosen grid of quantile indices,

but instead estimate the entire quantile regression process, that is, we estimate each quantile

regression for all quantile indices in (0,1). The practical consequence is that our estimates

don’t suffer from unnecessary approximation errors due to discretization. In addition, unlike

Chavleishvili and Manganelli (2019) and Montes-Rojas (2022), we construct confidence intervals

for the quantile treatment effects as in Ruzicka (2021b).

The second method estimates the quantile treatment effects directly by employing the lo-

cal projections of Jord`a (2005) in a quantile regression setting. Local projections estimated by

quantile regressions have become a popular way to capture heterogeneous effects of macroeco-

nomic shocks. However, applied research based on plain quantile regression local projections is

challenging: The estimated impulse response functions tend to wiggle a lot, it is unclear what

the underlying identification conditions are, and it is unclear how to construct closed-form confi-

dence intervals. Ruzicka (2021a) overcomes these challenges by introducing roughness penalties

to smooth the impulse response functions, by establishing the identification conditions, and by

providing closed-from as well as weighted bootstrap confidence intervals.

ECB Working Paper Series No 2870

17

These features are essential for our results for the following reasons. First, if it were not

for the smoothing, the estimated impulse response functions would change abruptly from one

forecast horizon to the next, making them difficult to interpret and less accurate. Second, the

theoretical result of Ruzicka (2021a) reveals which control variables must be included (and which

must not) in order to identify the quantile treatment effect of interest. This is essential for causal

interpretation and to prevent simultaneity bias. Third, the weighted bootstrap doesn’t entail any

tuning parameters, unlike the stationary bootstrap proposed Han et al. (2022) which depends

on a parameter (average block length), whose appropriate choice is nontrivial in practice.

Next, we present the basic technical notions underlying both estimation methodologies: the

data generating process and the impulse response function that measures the quantile treat-

ment effect of interest. For random variables X and Y we denote Q

τ

(Y |X) the τ th conditional

quantile of Y given X. For a stochastic process {Y

t

}, let {F

t

} be its filtration (the informa-

tion known up to time t). We assume the data follow an I-dimensional stochastic process

3

{Y

t

} = {[y

1,t

, y

2,t

, . . . , y

I,t

]} given by

Q

τ

1

(y

1,t

|F

t−1

) =

I

X

i=1

P

X

p=1

a

p1i

(τ

1

)y

i,t−p

+ ε

1

(τ

1

)

Q

τ

2

(y

2,t

|y

1,t

, F

t−1

) = a

021

(τ

2

)y

1,t

+

I

X

i=1

P

X

p=1

a

p2i

(τ

2

)y

i,t−p

+ ε

2

(τ

2

)

.

.

.

Q

τ

I

(y

I,t

|y

1,t

, y

2,t

, . . . , y

I−1,t

, F

t−1

) =

I−1

X

i=1

a

0Ii

(τ

I

)y

i,t

+

I

X

i=1

P

X

p=1

a

pIi

(τ

I

)y

i,t−p

+ ε

I

(τ

I

)

(1)

3

This type of a stochastic process was studied by Chavleishvili and Manganelli (2019), Ruzicka (2021a,b) and

Montes-Rojas (2022). It is a special case of the VAR for VaR of White et al. (2015), who additionally allow

conditional quantiles to depend on the lags of conditional quantiles.

ECB Working Paper Series No 2870

18

This stochastic process can be expressed in a random coefficient representation as

y

1,t

=

I

X

i=1

P

X

p=1

a

p1i

(u

1t

)y

i,t−p

+ ε

1

(u

1t

)

y

2,t

= a

021

(u

2t

)y

1,t

+

I

X

i=1

P

X

p=1

a

p2i

(u

2t

)y

i,t−p

+ ε

2

(u

2t

)

.

.

.

y

I,t

=

I−1

X

i=1

a

0Ii

(u

It

)y

i,t

+

I

X

i=1

P

X

p=1

a

pIi

(u

It

)y

i,t−p

+ ε

I

(u

It

)

(2)

where u

i,t

∼ U[0, 1], y

i,t

is non-decreasing in u

it

a.s. for all i and t, and {u

it

} are independent.

The disturbances {u

it

} in (2) change from one period to the next and represent the realized

values of τ

i

in each time period.

4

The model is identified by recursive short-run restrictions. For example, the second variable

is not allowed to contemporaneously affect the distribution of the first variable, but it may

affect the distribution of the third variable. This recursive ordering is analogous to the one of

Sims (1980). However, note that the identification restrictions are not equivalent to a Cholesky

decomposition of a covariance matrix – in fact, the quantile model above is well-defined even if

the variance of Y

t

doesn’t exist.

In the first, simulation-based approach, we estimate the quantile regression process of all

equations above over all quantile indices in (0,1) and subsequently recover the quantile treatment

effects of shocks by simulation, as outlined earlier. In the second, direct estimation approach,

we rely on the result of Ruzicka (2021a) who shows that for all forecast horizons h ∈ N

0

and all

i, j ∈ {1, 2, . . . , I} in the representation

Q

τ

(y

j,t+h

|F

t−1

, y

1,t

, . . . , y

i,t

) = β

0,j,0,h

(τ) +

i

X

k=1

β

k,j,0,h

(τ)y

k,t

+

I

X

k=1

P −1

X

p=1

β

k,j,p,h

(τ)y

k,t−p

(3)

the slope coefficient β

i,j,0,h

(τ) is the quantile treatment effect of the ith shock on variable j after

h periods at quantile τ . The last equation could be estimated directly by quantile regression,

separately for each forecast horizon. However, such estimates are usually rather inaccurate

and difficult to interpret as they differ dramatically between neighboring forecast horizons. For

4

Koenker et al. (2018)[pp. 313-317, 328-329] discuss the conditional quantile and random coefficient forms of

quantile autoregressive processes, their relations and role in forecasting.

ECB Working Paper Series No 2870

19

that reason we use the smooth quantile local projections estimator of Ruzicka (2021a), which

solves the problem by regularization, shrinking the impulse response functions towards cubic

polynomials via roughness penalties. In addition, we impose a long-run equilibrium constraint

which ensures the impulse response functions converge to a constant function at the final forecast

horizon.

5

We set the optimal value of the roughness penalty by the Bayesian information

criterion (Schwarz, 1978), as adapted for this setup by Ruzicka (2021a). Following Ruzicka

(2021a), we construct the confidence intervals by the weighted bootstrap with undersmoothing

(using standard exponential weights; the roughness penalty for confidence intervals is one quarter

of its value for point estimates.)

We collect the quantile treatment effects at different horizons into a quantile impulse re-

sponse function, using the definition of Ruzicka (2021b). The quantile impulse response function

QIR(j, i, h, τ, s) is the response of the jth variable at quantile τ to the ith shock of size s after

h periods, formally

QIR(j, i, h, τ, s) = Q

τ

h

y

j,t+h

ε

i

(u

it

) := ε

i

(u

it

) + s

i

−Q

τ

h

y

j,t+h

i

(4)

=

∂Q

τ

[y

j,t+h

|u

it

]

∂ε

i

(u

it

)

s (5)

where the notation ε

i

(u

it

) := ε

i

(u

it

) + s represents a modified version of the process, with ε

i

(u

it

)

substituted by ε

i

(u

it

)+s for all u

it

∈ [0, 1]. For some variables we are interested in the cumulative

effect of a shock through cumulative quantile impulse response functions, given by

QIRC(j, i, h, τ, s) = Q

τ

"

h

X

k=0

y

j,t+k

ε

i

(u

it

) := ε

i

(u

it

) + s

#

−Q

τ

"

h

X

k=0

y

j,t+k

#

(6)

=

∂Q

τ

"

h

X

k=0

y

j,t+k

u

it

#

∂ε

i

(u

it

)

s (7)

4.2 Counterfactual scenarios – linking forecasts and impulse responses

The quantile impulse response function as defined above involves an intervention at a single

point in time. However, it is also possible to allow interventions in various consecutive time

periods. This is more complicated, but it is useful in order to isolate the effects of sustained

policy interventions. To be specific, we work with monthly data, the interventions are introduced

5

For our two models, the forecast horizon is up to 72 months and 12 months, respectively.

ECB Working Paper Series No 2870

20

in 12 consecutive months, and the response variable is a monthly growth rate. Formally, the

intervention at time t + m is of size s

m

, where m ∈ {0, 1, . . . , 11}. We want to see the effect of

the interventions on the τ th quantile of

P

11

k=0

y

j,t+k

, which represents the year-over-year growth

rate of the response variable. Using the same notation as in (4), the effect of the sequence of

interventions is

Q

τ

"

11

X

k=0

y

j,t+k

∀m ∈ {0, 1, . . . , 11}: ε

i

(u

i,t+m

) := ε

i

(u

i,t+m

) + s

m

#

−Q

τ

"

11

X

k=0

y

j,t+k

#

(8)

It can be shown

6

that (8) equals

11

X

l=0

QIRC(j, i, l, τ, s

11−l

) (9)

The sequence of external impulses can be combined with quantile forecasts into a counter-

factual scenario. Such a scenario shows how quantile forecasts would have responded to policy

interventions in the past. Recall that F

t−1

represents the information known at time t − 1. The

forecast of the year-over-year growth rate of the ith variable is represented by

Q

τ

"

11

X

k=0

y

j,t+k

F

t−1

#

(10)

Next, we introduce policy interventions over 12 consecutive months. The forecast changes to

Q

τ

"

11

X

k=0

y

j,t+k

F

t−1

, ∀m ∈ {0, 1, . . . , 11}: ε

i

(u

i,t+m

) := ε

i

(u

i,t+m

) + s

m

#

(11)

and represents our counterfactual scenario. It turns out that

7

(11) equals (12)

Q

τ

"

11

X

k=0

y

j,t+k

F

t−1

#

+

11

X

l=0

QIRC(j, i, l, τ, s

11−l

) (12)

which comprises the quantile forecast (the first term) and the effect of the sequence of interven-

tions (the second term).

This form of a counterfactual scenario does not set any specific sample path and so it is differ-

ent from the one in Chavleishvili et al. (2021). Fixing a sample path ex ante as in Chavleishvili

6

Proof A.2 in the appendix.

7

Proof A.3 in the appendix.

ECB Working Paper Series No 2870

21

et al. (2021) obviates the need to run a large number of simulations. However, since our coun-

terfactual scenario is based on a sequence of exogenous interventions, we can calculate (9) just

by summing up the cumulative quantile impulse response functions. These must be estimated

beforehand, either by simulation or by direct estimation through local projections.

Finally, the counterfactual scenario gives us a way to quantify the contribution of interven-

tions (observed or estimated) on the in-sample quantile forecasts over a specific time horizon.

In our case, the interventions are monetary policy surprises. Formally, consider interventions to

variable i at time t + l of size s

t+l

, where 0 ≤ l ≤ 11. Then the term

11

X

l=0

QIRC(j, i, l, τ, s

t+11−l

) (13)

measures how the year-over-year growth rate of the jth variable would change if the interventions

s

t

, s

t+1

, . . . , s

t+11

were replaced by zero. We interpret (13) as the contribution of the interven-

tions to the year-over-year growth rate of variable j over the time horizon t, t + 1, . . . , t + 11.

4.3 The setup: real economy, financial variables and monetary policy

Based on the general framework described in the previous section, we outline the specific model

setup for an economy with financial interactions. In brief, we estimate three models. The first

one encompasses economic activity, price level, financial vulnerabilities, and financial stress. We

obtain the second model by incorporating short-term rates. Finally, we replace the short-term

rates by long-term rates to arrive at our third model. These models are estimated separately

to ensure tractability, results from one combined model with both monetary policy series are

qualitatively similar but subject to wider confidence bands.

We estimate each of the three models using the two alternative methods described earlier,

that is, with a simulation-based approach as well as with a local projection approach. Both

approaches rely on the same identification assumptions. Theoretically, the estimates from both

methods converge to the same limit in large samples, provided our model is correctly specified.

All specifications include three lags of all the included variables.

The first model combines real GDP growth and HICP inflation with variables of financial

vulnerabilities and systemic stress into a four-variable model of their entire distribution. Fi-

nancial vulnerabilities are captured by the SRI and financial stress is measured by the CISS.

Identification is achieved through recursive short-run restrictions: Hereby real GDP growth is

ECB Working Paper Series No 2870

22

placed first, HICP inflation second, the SRI third and CISS fourth. The identification strategy

thus implies that the financial stress variable (placed fourth) can react contemporaneously to

macroeconomic and SRI shocks, while the SRI (placed third) can only react contemporaneously

to shocks to output growth and HICP inflation. In turn, real output growth only reacts with

a lag to shocks of inflation, the SRI, and stress. This follows standard assumptions in the

empirical literature such as Kilian (2009) and Gilchrist and Zakrajˇsek (2012). The estimates

and the identification strategy allow us to quantify amplifications of risks for future economic

activity caused by elevated levels of financial imbalances as well as financial stress. This is rel-

evant for modelling the variables over time and for the counterfactual policy scenarios. In this

four-variable model we consider impulse responses up to 72 months ahead.

The second and third model append the previous four-variable model by adding either the

short-end or the long-end monetary policy surprise factors (while results based on central bank

information shocks are shown in the appendix). The monetary policy series are ordered first so

as to contemporaneously affect all the other variables in the system. Given that we investigate

the monetary policy effects on different parts of the distribution of the response variables while

having a modest sample size, we focus on impulse responses over the short-run, up to 12 months

ahead. Even though we cannot comment on medium term monetary policy effects, Doh and

Foerster (2022) show that monetary policy transmission lags have shortened after 2009, at least

in the United States.

5 Results

With model specifications and the monetary policy shock identification fully established, this

section focuses on the estimation results and their interpretation. We discuss the quantile im-

pulse response functions in two blocks starting with those based on the model without monetary

policy surprises which we show up to 72 months ahead, followed by those from the two models

that include monetary policy surprises, for which we focus on short-term dynamics of up to 12

months ahead.

5.1 Impulse responses of macro-financial variables

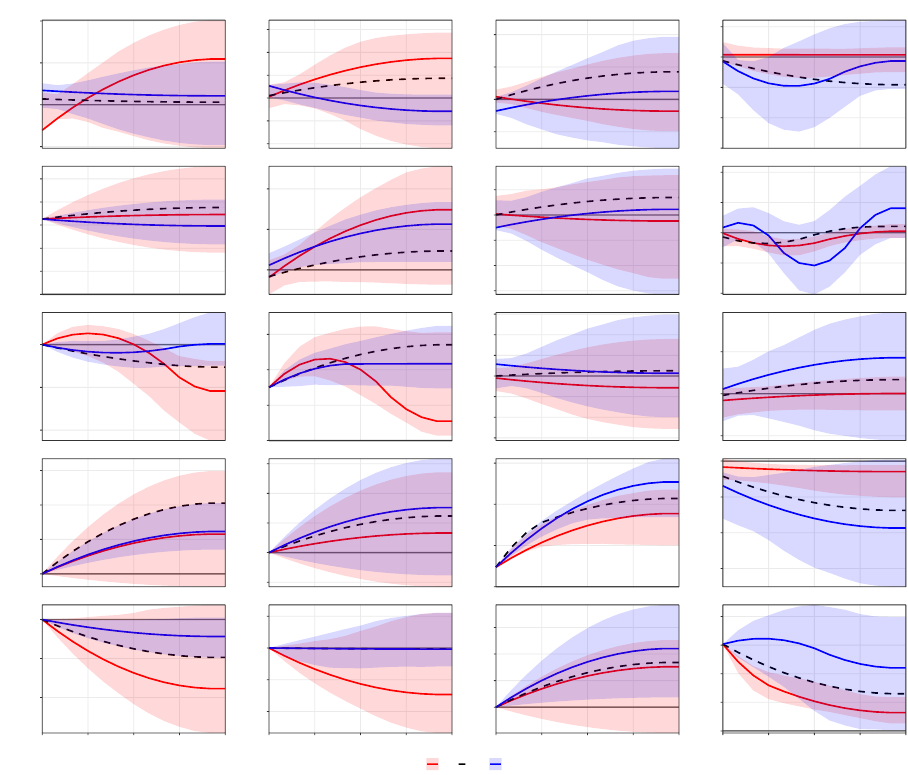

The impulse responses of macroeconomic variables in our quantile setting follow those known

from structural linear VARs in the literature. As Figure 4 shows, an impulse to real GDP leads to

ECB Working Paper Series No 2870

23

a persistent increase of GDP, accompanied by an increase in inflation – with a mild overshooting

– over two quarters. In turn, an impulse to inflation does not imply persistent effects for future

inflation and does not affect real GDP growth in a statistically significant manner. The impulse

responses of the two variables do not indicate heterogeneous dynamics across quantiles.

Figure 4: Impulse Responses of GDP, inflation, financial vulnerability, and stress

(estimated by simulation)

monthly GDP response (cumulative)

0.0

0.2

0.4

0.6

1 SD monthly GDP shock

HICP inf. response (cumulative)

−0.05

0.00

0.05

0.10

0.15

SRI response

−0.050

−0.025

0.000

0.025

0.050

CISS response

−0.02

−0.01

0.00

0.01

−0.1

0.0

0.1

1 SD HICP inf. shock

0.0

0.1

0.2

0.3

−0.050

−0.025

0.000

0.025

0.050

−0.01

0.00

0.01

−0.5

0.0

0.5

1.0

1 SD SRI shock

0.0

0.5

1.0

1.5

0.00

0.05

0.10

0.15

0.20

−0.03

0.00

0.03

0.06

−0.6

−0.4

−0.2

0.0

0 12 24 36 48 60 72

month

1 SD CISS shock

−0.2

−0.1

0.0

0.1

0 12 24 36 48 60 72

month

−0.050

−0.025

0.000

0.025

0.050

0 12 24 36 48 60 72

month

0.00

0.02

0.04

0.06

0.08

0 12 24 36 48 60 72

month

quantile

0.1 0.5 0.9

Notes: Four-variable specification without monetary policy shock. Confidence bands are at 90% and are excluded

for the median response.

In turn, the financial variables provide additional information on the macroeconomic dy-

namics. An innovation of the SRI, reflecting an increase in financial vulnerabilities, implies a

temporary upward deviation of output with a peak after 24 months, whereby the 10th percentile

of the distribution reverts more quickly while the 90th percentile has a larger persistence. The

effects on inflation, on the other hand, appear more persistent, especially for the upper tail of

the distribution. These findings indicate that macroprudential policy targeting the SRI can be

effective in boosting or slowing growth and inflation. As regards the materialisation of stress

ECB Working Paper Series No 2870

24

as captured by the CISS, it exerts a strong downward adjustment for the 10th percentile of the

GDP distribution, in line with the findings in the literature (Adrian et al., 2019; Chavleishvili

and Manganelli, 2019; Chavleishvili and Kremer, 2021). In turn, the inflation rate adjusts in

the short term but rebounds quickly, without statistically significant longer-term effects on the

price level.

As regards the impulse responses of financial vulnerabilities and stress, we find that shocks to

GDP and HICP inflation have only insignificant impacts on financial variables, while the corre-

sponding impulse responses indicate that a positive SRI impulse initiates a persistent medium-

term episode of increasing vulnerabilities, whereby higher quantiles increase relatively more

strongly and cumulate after 24 months compared to the lower quantiles. Together with in-

creasing financial vulnerabilities, financial stress is being dampened in the short-term, especially

for higher quantiles of the CISS. However, as the vulnerabilities indicator recedes, the stress

indicator reverts with financial market stress and losses. This interplay between financial vul-

nerabilities and financial stress reflects a key intertemporal trade-off for policymakers between

short-term gains from exuberant financial conditions and higher risks of financial stress in the

medium term. Shocks to the CISS have only a statistically insignificant impact on the SRI, and

appear to die out after about 24 months.

The impulse responses from the two estimation approaches are qualitatively comparable with

only few exceptions, such as the impact of CISS shocks on the upper part of the SRI distribution

or the effect of the SRI shock on the upper part of the GDP growth distribution.

5.2 Impact of monetary policy shocks

Beyond the macro-financial interactions discussed thus far, we next assess the impact of mone-

tary policy shocks on financial stability conditions and the real economy. For this, we employ

the two monetary policy factors defined in Section 3.3, the short-end factor capturing surprises

in short-term rates and linked to conventional monetary policy, and the long-end factor cap-

turing surprises in longer rates, unrelated to surprises in short-term rates, and thus linked to

unconventional monetary policy. The results for monetary policy shocks feature in this section,

while the impulse responses of the central bank information shocks are shown in the appendix.

As Figures 6 and 7 show, an identified conventional monetary policy tightening shock has

the expected contractionary effect on real GDP growth and HICP inflation, in line with the

monetary policy literature (Bernanke and Mishkin, 1997; Clarida et al., 1999). Beyond the

ECB Working Paper Series No 2870

25

Figure 5: Impulse Responses of GDP, inflation, financial vulnerability, and stress

(estimated by local projections)

monthly GDP response (cumulative)

−0.4

0.0

0.4

0.8

1 SD monthly GDP shock

HICP inf. response (cumulative)

−0.2

0.0

0.2

0.4

0.6

SRI response

−0.09

−0.06

−0.03

0.00

0.03

CISS response

−0.050

−0.025

0.000

0.025

0.050

−0.6

−0.4

−0.2

0.0

0.2

1 SD HICP inf. shock

−0.25

0.00

0.25

0.50

−0.05

0.00

0.05

−0.06

−0.03

0.00

0.03

0.06

0.0

0.5

1 SD SRI shock

−0.2

0.0

0.2

0.4

−0.05

0.00

0.05

0.10

−0.05

0.00

0.05

−1.00

−0.75

−0.50

−0.25

0.00

0 12 24 36 48 60 72

month

1 SD CISS shock

−0.75

−0.50

−0.25

0.00

0.25

0 12 24 36 48 60 72

month

−0.100

−0.075

−0.050

−0.025

0.000

0 12 24 36 48 60 72

month

−0.05

0.00

0.05

0 12 24 36 48 60 72

month

quantile

0.1 0.5 0.9

Notes: Four-variable specification without monetary policy shock. Confidence bands are at 90% and are excluded

for the median response.

macroeconomic effects, a tightening shock also impacts financial stability conditions. In the

short term, the shock raises financial stress measured by the CISS across all quantiles, but

especially so for the upper part of the distribution. This implies that following a tightening

shock, the CISS does not only increase on average, but the distribution also becomes more

asymmetric with a larger right tail, permitting stronger surges in financial stress.

In turn, the impact on systemic risk and medium-term financial vulnerabilities is less clear

cut. It appears that over time, the impact on the SRI is negative, indicating ’taming-the-cycle’

dynamics, but the effects are statistically insignificant.

Impulse responses to an unconventional monetary policy tightening shock differ meaningfully

from those following a shock to the short-end factor. Figures 8 and 9 show that the impact of

a comparable one standard deviation shock on GDP growth is smaller, and statistically not

ECB Working Paper Series No 2870

26

Figure 6: Impulse Responses of monetary policy tightening shock on short-term rates

(estimated by simulation)

monthly GDP response (cumulative)

−0.4

−0.3

−0.2

−0.1

0.0

0.1

1 SD FShort − MP shock

HICP inf. response (cumulative)

−0.20

−0.15

−0.10

−0.05

0.00

SRI response

−0.01

0.00

0.01

CISS response

0.00

0.01

0.02

0.03

0.04

0.0

0.1

0.2

0.3

1 SD monthly GDP shock

−0.025

0.000

0.025

0.050

−0.010

−0.005

0.000

−0.01

0.00

0.01

−0.10

−0.05

0.00

0.05

1 SD HICP inf. shock

0.00

0.05

0.10

0.15

0.20

0.25

−0.010

−0.005

0.000

0.005

0.010

−0.010

−0.005

0.000

0.005

0.010

0.0

0.1

0.2

0.3

0.4

1 SD SRI shock

0.00

0.05

0.10

0.15

0.000

0.025

0.050

0.075

−0.05

−0.04

−0.03

−0.02

−0.01

0.00

−0.3

−0.2

−0.1

0.0

0 3 6 9 12

month

1 SD CISS shock

−0.05

0.00

0.05

0 3 6 9 12

month

−0.010

−0.005

0.000

0.005

0.010

0.015

0 3 6 9 12

month

0.00

0.02

0.04

0.06

0.08

0 3 6 9 12

month

quantile

0.1 0.5 0.9

Notes: Five-variable specification with response of monetary policy shock variable excluded. Confidence bands

are at 90% and are excluded for the median response.

significant, while the impact on HICP inflation is comparable and statistically significant. As

for short-end shocks we find a dampening impact on financial vulnerabilities, this time marginally

significant at least for the 10th percentile. The impact of long-end shocks on financial stress

is found to be insignificant, unlike short-end shocks. Finally, impulse responses to monetary

policy shocks generated from the two estimation approaches are generally comparable for both

monetary policy factors.

ECB Working Paper Series No 2870

27

Figure 7: Impulse Responses of monetary policy tightening shock on short-term rates

(estimated by local projections)

monthly GDP response (cumulative)

−0.4

−0.2

0.0

1 SD FShort − MP shock

HICP inf. response (cumulative)

−0.4

−0.3

−0.2

−0.1

0.0

SRI response

−0.02

−0.01

0.00

0.01

CISS response

−0.050

−0.025

0.000

0.025

0.050

0.075

0.0

0.2

0.4

0.6

1 SD monthly GDP shock

0.0

0.1

0.2

−0.02

−0.01

0.00

0.01

−0.025

0.000

0.025

0.050

−0.3

−0.2

−0.1

0.0

1 SD HICP inf. shock

0.0

0.1

0.2

0.3

−0.01

0.00

0.01

−0.02

0.00

0.02

0.0

0.1

0.2

0.3

1 SD SRI shock

−0.05

0.00

0.05

0.10

0.15

0.00

0.02

0.04

0.06

−0.06

−0.04

−0.02

0.00

−0.6

−0.4

−0.2

0.0

0 3 6 9 12

month

1 SD CISS shock

−0.3

−0.2

−0.1

0.0

0.1

0 3 6 9 12

month

0.00

0.01

0.02

0 3 6 9 12

month

0.00

0.02

0.04

0.06

0.08

0 3 6 9 12

month

quantile

0.1 0.5 0.9

Notes: Five-variable specification with response of monetary policy shock variable excluded. Confidence bands

are at 90% and are excluded for the median response.

6 Counterfactuals

6.1 Impact of monetary policy shocks on inflation and Growth-at-Risk

The empirical quantile models allow us to identify the role of monetary policy in the forecasts of

macro-financial variables and to consider counterfactual analysis. Figure 10 shows the forecasts

for GaR and one year ahead median annual HICP inflation together with the contribution of

monetary policy shocks over time. The monetary policy contributions are constructed as the

12-month cumulative impact of the individual monetary policy surprises in each of these months

ECB Working Paper Series No 2870

28

Figure 8: Impulse Responses of monetary policy tightening shock on long-term rates

(estimated by simulation)

monthly GDP response (cumulative)

−0.2

−0.1

0.0

1 SD FLong − MP shock

HICP inf. response (cumulative)

−0.10

−0.05

0.00

SRI response

−0.015

−0.010

−0.005

0.000

0.005

CISS response

−0.01

0.00

0.01

0.0

0.1

0.2

0.3

0.4

0.5

1 SD monthly GDP shock

−0.04

0.00

0.04

0.08

−0.010

−0.005

0.000

0.005

−0.01

0.00

0.01

−0.10

−0.05

0.00

0.05

0.10

1 SD HICP inf. shock

0.00

0.05

0.10

0.15

0.20

0.25

−0.010

−0.005

0.000

0.005

0.010

−0.01

0.00

0.01

0.0

0.1

0.2

0.3

0.4

1 SD SRI shock

0.00

0.05

0.10

0.15

0.000

0.025

0.050

0.075

−0.05

−0.04

−0.03

−0.02

−0.01

0.00

−0.4

−0.3

−0.2

−0.1

0.0

0 3 6 9 12

month

1 SD CISS shock

−0.10

−0.05

0.00

0.05

0 3 6 9 12

month

−0.01

0.00

0 3 6 9 12

month

0.00

0.02

0.04

0.06

0.08

0 3 6 9 12

month

quantile

0.1 0.5 0.9

Notes: Five-variable specification with response of monetary policy shock variable excluded. Confidence bands

are at 90%.

multiplied with the estimated impulse response function of the relevant horizon. They are thus

conditional on the macro-financial information up to a point t, but conditional on the monetary

policy surprises from t to t + 12.

The largest contributions of conventional monetary policy for GaR and the annual median

inflation forecast (left panels), can be observed over the period 2007–2008 when it exerted

large negative, i.e. tightening, contributions. When excluding these shocks, the Growth-at-Risk

measure would have been positive, instead of falling into negative territory. Our counterfactual

analysis indicates that the cumulative impact of conventional monetary policy shocks helped to

ECB Working Paper Series No 2870

29

Figure 9: Impulse Responses of monetary policy tightening shock on long-term rates

(estimated by local projections)

monthly GDP response (cumulative)

−0.2

−0.1

0.0

0.1

0.2

1 SD FLong − MP shock

HICP inf. response (cumulative)

−0.2

−0.1

0.0

0.1

SRI response

−0.02

−0.01

0.00

0.01

CISS response

−0.04

−0.02

0.00

0.02

0.0

0.1

0.2

0.3

0.4

0.5

0.6

1 SD monthly GDP shock

0.0

0.1

0.2

−0.01

0.00

−0.03

0.00

0.03

0.06

−0.2

−0.1

0.0

1 SD HICP inf. shock

0.0

0.1

0.2

0.3

−0.01

0.00

0.01

−0.03

−0.02

−0.01

0.00

0.01

0.02

0.0

0.1

0.2

0.3

1 SD SRI shock

0.0

0.1

0.00

0.02

0.04

0.06

−0.08

−0.06

−0.04

−0.02

0.00

−0.6

−0.4

−0.2

0.0

0 3 6 9 12

month

1 SD CISS shock

−0.3

−0.2

−0.1

0.0

0.1

0 3 6 9 12

month

0.00

0.01

0 3 6 9 12

month

0.000

0.025