FYI-203 REV. 7/2021

FYI-203

FOR YOUR INFORMATION

Tax Information/Policy Office P.O. Box 630 Santa Fe, New Mexico 87504-0630

Gross Receipts Tax Holiday

This publication provides general information on the application of gross receipts tax to retail sales

of certain tangible personal property sold during the first weekend of August from 12:01 a.m. on

the first Friday to midnight the following Sunday.

This information is as accurate as possible at time of publication. Subsequent legislation, new

state regulations, and court cases may affect its accuracy. For the latest information please check

the Taxation and Revenue Department’s web site at www.tax.newmexico.gov.

CONTENTS

General Summary Of The Gross Receipts Tax Holiday .............................................................. 2

Nontaxable Transactions During The Tax Holiday ...................................................................... 2

Taxable Transactions During The Tax Holiday ............................................................................ 2

Definitions ................................................................................................................................... 3

Other Taxable Items Sold During The Tax Holiday ..................................................................... 3

Types Of Sales/Exchanges ......................................................................................................... 4

Reporting Gross Receipts From Eligible Tax Holiday Sales ........................................................ 5

Filing The Tax Return .................................................................................................................. 5

List Of Taxable And Nontaxable Items ........................................................................................ 5

Taxpayer Information ................................................................................................................ 15

For Further Assistance .............................................................................................................. 16

New Mexico

Taxation and Revenue Department

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 2

General Summary of the Gross Receipts Tax Holiday

The 2005 New Mexico Legislature established a deduction (Section 7-9-95 NMSA 1978) from

gross receipts for retail sales of tangible personal property within a prescribed period every year in

August. When retailers may deduct gross receipts, they have no need to recover tax costs from

some customers. Customers can therefore buy these items during this period free of tax. For a

more detailed list of taxable and nontaxable items, please see page 6 of this FYI, “List of Taxable

and Nontaxable Items”.

The prescribed period of the annual “gross receipts tax holiday” is the first weekend of August

from 12:01 a.m. on the first Friday to midnight the following Sunday.

Nontaxable Transactions During the Tax Holiday

The law limits the tax-holiday deduction to receipts of retailers from sales of the following types of

items please see page 6 of this FYI for a more detailed list of taxable and nontaxable items for the

tax holiday.:

• Clothing or shoes sold for less than $100; however, accessories and special clothing or

footwear primarily designed for athletic activity or protective use and not normally worn

beyond the scope of the athletic activity or protective use remain taxable;

• Desktop, laptop, notebook, or tablet computers sold for no more than $1,000, and any

associated monitor, speaker or set of speakers, printer, keyboard, microphone, or mouse

sold for no more than $500, and

• School supplies students normally use in a standard classroom for educational purposes.

The law specifically lists notebooks, paper, writing instruments, crayons, art supplies,

rulers, bookbags, backpacks, handheld calculators, maps, and globes as deductible

during the tax holiday. The law specifically excludes watches, radios, compact disc

players, headphones, sporting equipment, portable desktop telephones, copiers, office

equipment, furniture, or fixtures. The law does not consider such items to be school

supplies that students normally use in a standard classroom. Sales of those items are

taxable during the three-day period.

Taxable Transactions During the Tax Holiday

Even when the transactions take place during the gross receipts tax holiday, gross receipts tax is

due and payable on gross receipts from:

• Sales of services performed on otherwise qualifying tangible personal property; for

example, clothing alterations, repair and dry cleaning, or computer services, installation

and repair (Regulation 3.2.242.15 NMAC);

• Sales of all other services performed in New Mexico during the tax holiday, including, but

not limited to, construction, repair, maintenance, landscaping, medical treatment, physical

examinations for school purposes, etc;

• Leasing or renting tangible personal property that would be deductible if sold by a retailer

during the tax holiday, and receipts from all other leasing or rental activity conducted

during that weekend (Regulation 3.2.242.15 NMAC);

• Sales of licenses and other intangible personal property;

• Sales of all tangible personal property not identified by law or regulation as deductible

during the tax holiday;

• Sales of tangible personal property that the law specifically identifies as taxable if sold at

retail during the tax holiday. Such property includes watches, radios, compact disc players,

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 3

headphones, sporting equipment, portable desktop telephones, copiers, office equipment,

furniture or fixtures, everyday clothing priced at $100 or more, clothing designed for

special athletic activity or protective use, accessories, and

• Sales of qualifying items that exceed the allowable value established by statute or

regulation (see “definition of school supplies” below).

Definitions

Standard Classroom is a classroom (1) located in a school; (2) configured for a general

education curriculum, and (3) containing no specialized equipment such as scientific laboratory

equipment or musical instruments (Regulation 3.2.242.7 NMAC).

School Supplies Normally Used by Students in a Standard Classroom for Educational

Purposes means implements and materials typical students normally use in a general education

curriculum. Such supplies must be priced under $30 per unit for notebooks, paper, writing

instruments, crayons, art supplies, paper clips, staples, staplers, scissors, and rulers; under $100

per unit for bookbags, backpacks, maps, and globes; and under $200 handheld calculators.

Please note that these items need not be used for school purposes, but they must meet the

criteria for items normally used by students in a standard classroom setting (Regulation 3.2.242.7

NMAC).

Items Normally Sold as a Unit are items usually sold in pairs, sets, boxes, cartons, cases or

other quantity containers, or items sold as a package in a single transaction. Those items must

continue to be sold as units during the holiday. They cannot be broken down, priced separately

and sold as individual items to qualify for the deduction; for example, a retailer cannot sell a $180

pair of shoes singly for $90 each to qualify for the deduction offered for clothing under $100

(Regulation 3.2.242.8 NMAC).

Other Taxable Items Sold During the Tax Holiday

Ineligible for the deduction from gross receipts for the sale of tangible personal property during

the gross receipts tax holiday, in addition to those specifically excluded by statute and listed on

page 2 under “taxable transactions” are the following items:

• E-readers that only have the ability to access the internet but that have no other

computing functions such as word processing, spreadsheet capabilities, etc.;

• Personal digital assistants (PDAs), MP3 players, cassette players and recorders, cameras,

books, magazines, and other periodicals;

• All computer and computer-related equipment not specifically listed by statute or

regulation as deductible (see page 2) unless bundled with and included in the price of a

deductible item within the price limits set by law;

• All computer software unless bundled with and included in the price of a deductible item

within the price limits set by law;

• Musical instruments;

• All games, including video games, board games, computer games, and handheld gaming

devices;

• Materials and equipment for making, repairing, or altering clothing; for example, cloth or

other fabric, textile or material, thread, yarn, needles, buttons, zippers, and patterns;

• Athletic and protective gloves, pads, supporters, and helmets;

• Swimwear, cover-ups, and caps;

• Specialized footwear not readily available for streetwear, including ski boots, riding boots,

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 4

waders, bowling shoes and shoes with cleats or spikes;

• Briefcases and luggage;

• Prerecorded CDs, DVDs, and cassette tapes, and

• Other specialized school instruments or work tools.

Types of Sales/Exchanges

The statute limits the gross receipts tax deduction to the times specified. Accordingly,

transactions either partly or wholly outside the time limits of the holiday may pose problems for

some retailers and their customers. Some of those transactions are:

Rain Checks. A rain check assures the customer that a sold-out or out-of-stock sale item may

be purchased after the sale at the sale price. Receipts from qualified sales of tangible personal

property made with a rain check issued during the term of the tax holiday are deductible from

gross receipts. Sales made and paid for with a rain check outside the term of the tax holiday are

fully taxable regardless of when the rain check is issued (Regulation 3.2.242.9 NMAC).

Layaway Sales. When retailers hold merchandise on a layaway plan at a customer’s request,

they are performing a service. A layaway is not a completed retail transaction. It follows that:

1. The initiation of a layaway plan is not a sale even when the customer pays a deposit to

the retailer. A “sale” takes place only when the final payment occurs and the

merchandise is delivered to the customer. Until then the customer does not own the

property. The sale is not complete;

2. Final payment and delivery of the qualifying merchandise must occur during the gross

receipts tax holiday, or the retailer cannot take the deduction offered for the tax holiday,

and

3. If final payment and delivery of qualifying layaway merchandise take place during the tax

holiday, the transaction is deductible when other requirements are met (Regulation

3.2.242.10 NMAC).

Gift Certificates. The retailer’s sale of a gift certificate in and of itself is not taxable. If a gift

certificate sold during the tax holiday is redeemed after the tax holiday ends, however, the

retailer may not take the tax holiday deduction even for qualifying tangible personal property.

The redemption opportunity closes when the tax holiday ends.

Exchanges and Refunds.

1. Qualifying tangible personal property sold at retail during the tax holiday and exchanged

at a later date for an item of the same price remains deductible.

2. Qualifying tangible personal property sold at retail during the tax holiday but later

exchanged for an item of greater or lesser value is subject to the tax (Regulation

3.2.242.11 NMAC).

Internet, Mail Order and Telephone Sales. Receipts from the sale of eligible tangible personal

property to persons with New Mexico billing addresses are deductible to the retailer when:

1. The item is both delivered to and paid for by the customer during the tax holiday period,

or

2. The customer orders and pays for the item and the retailer accepts the order during the

tax holiday, even if delivery of the item takes place after the tax holiday (Regulation

3.2.242.12 NMAC).

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 5

Reporting Gross Receipts from Eligible Tax Holiday Sales

Please note that retailers of qualifying tangible personal property are not required to participate

in the tax holiday or to take the deduction offered. If they do not participate, they pay tax on

otherwise eligible sales and may recover their tax costs from the customer.

Retailers should use the Form TRD-41413, Gross Receipts Tax Return as usual to report and

deduct receipts from the sale of qualifying items sold during the tax holiday. In Column E, add

D0-023 to claim the deduction under Section 7-9-95 NMSA 1978. Note: The Department retired

form RPD-41299, Gross Receipt Tax Holiday to make reporting of this deduction easier for

taxpayers.

Retailers must maintain records of the type of item sold, the date it was sold, and the sales price

of deductible merchandise.

The retailer may take an exemption or a deduction on a transaction only once. If during the

tax holiday the retailer accepts or has a nontaxable transaction certificate on file, and the

customer buys tangible personal property that otherwise qualifies for the tax holiday deduction,

the retailer may not take the deduction for the tax holiday (Section 7-9-95 NMSA 1978). Gross

receipts that are already exempt or deductible under other sections of the Gross Receipts and

Compensating Tax Act are ineligible for the tax holiday deduction.

Filing the Tax Return

Paper Form TRD-41413, Gross Receipt Tax Return:

The Form TRD-41413, Gross Receipts Tax Return can be located in printer-friendly format at

https://www.tax.newmexico.gov/forms-publications/ .

Please note that prior to July 1, 2021 it was necessary to file form RPD-41299, Gross Receipts

Tax Holiday with the CRS-1 Form. The form, separately stating the grand total of tax holiday

deductions. Starting July 1, 2021, use Form TRD-41413, Gross Receipts Tax Return and

separately report this deduction using the deduction code D0-023.

Online Filing: The Department recommends filing online through the Taxpayer Access Point

(TAP) whenever possible. TAP can be located here: https://tap.state.nm.us/Tap. If you file your

gross receipts tax return online select the deduction code D0-023 to report this deduction

List of Taxable and Nontaxable Items

This FYI contains a list, intended as general guidance and by no means all-inclusive, of both

taxable and nontaxable items for quick reference by retailers taking part in the gross receipts tax

holiday during the first weekend of August.

The list below is divided into categories, but please note that within some categories there is a set

dollar maximum. To qualify for the deduction, clothing or shoes must be priced at less than $100

per unit. The price limit for desktop, laptop or notebook computers is $1,000, and for related

computer hardware it is $500. School supplies for use in standard, general-education classrooms

must be under $30 per unit. There are items specifically excluded by statute in all categories.

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 6

Those items are always taxable.

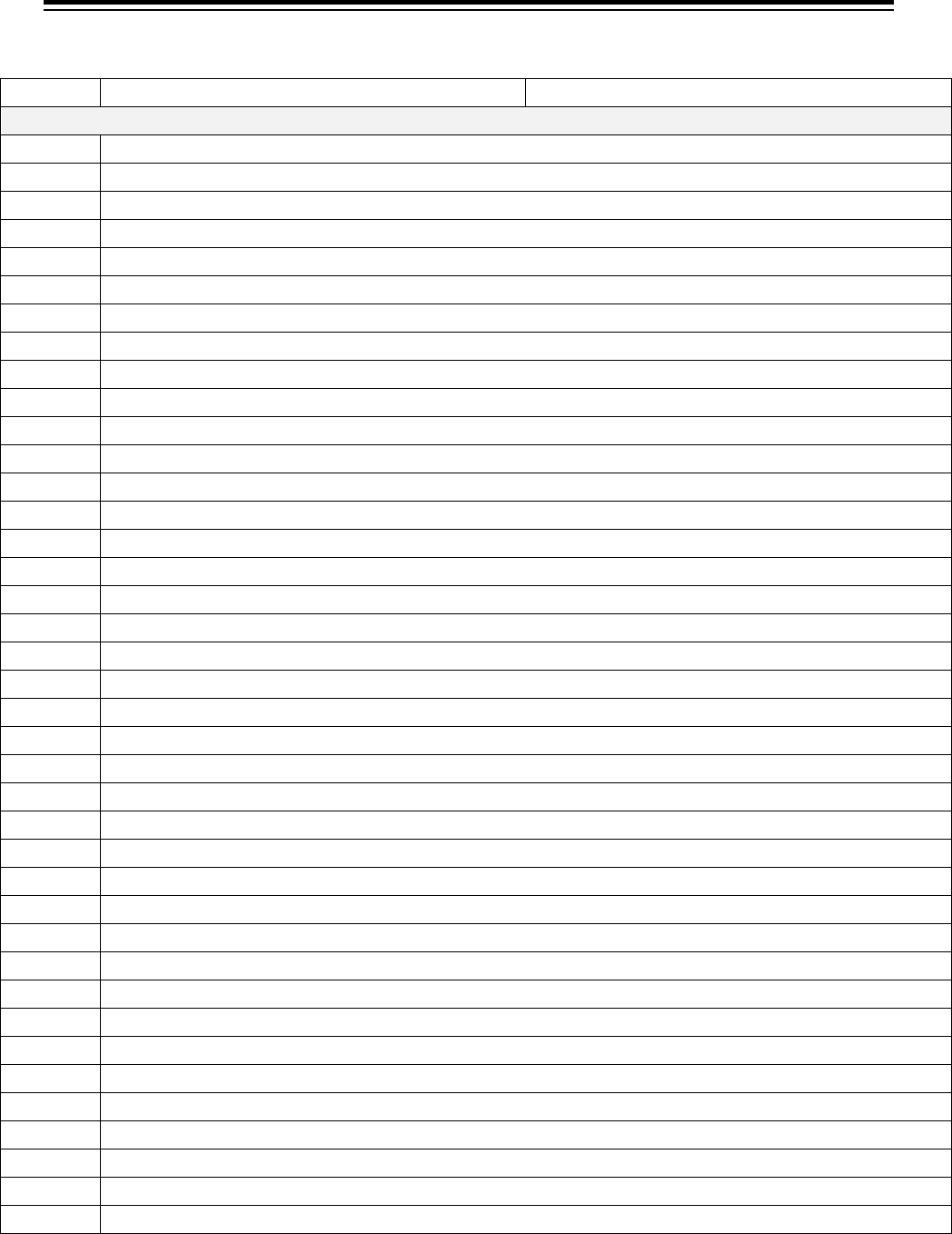

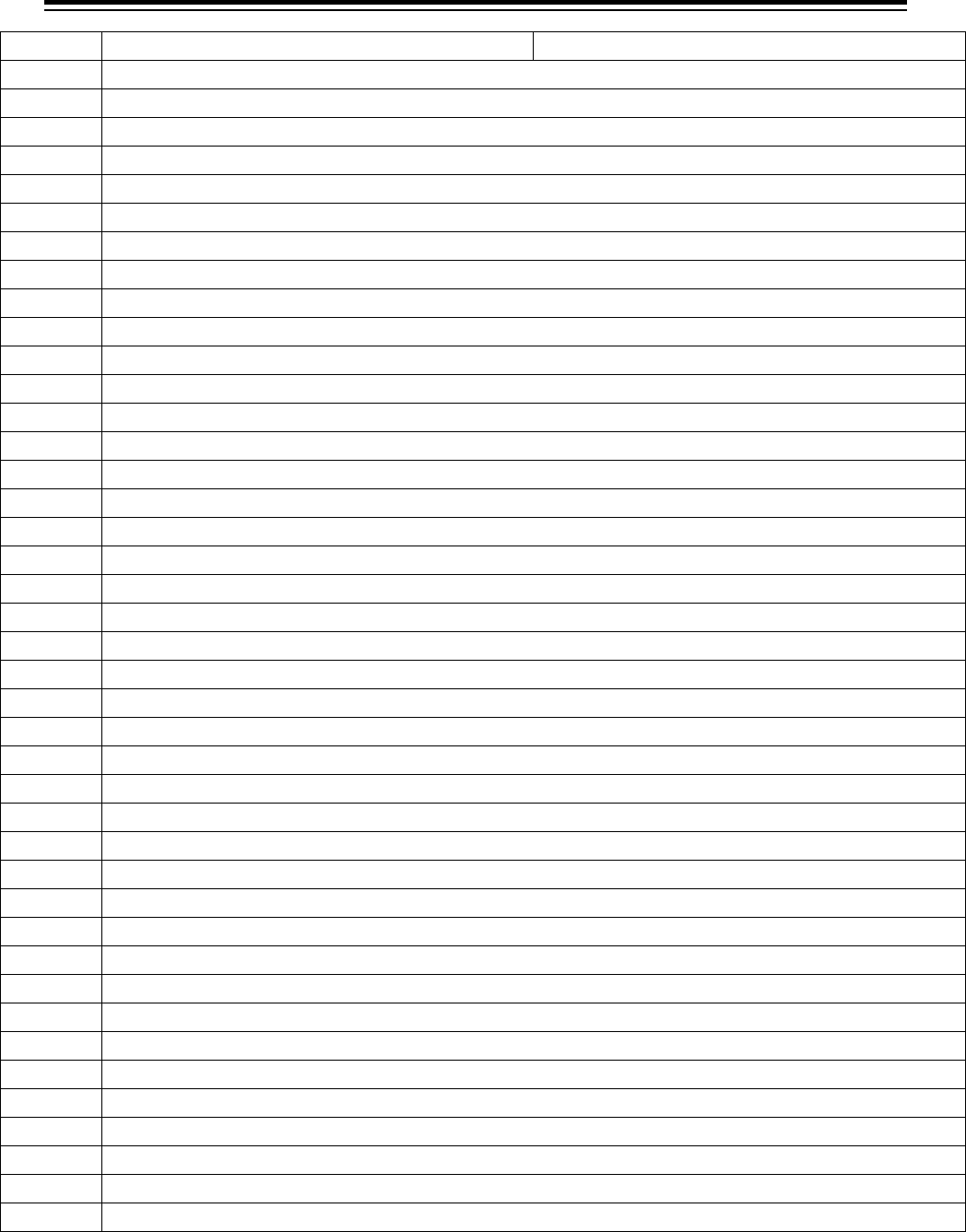

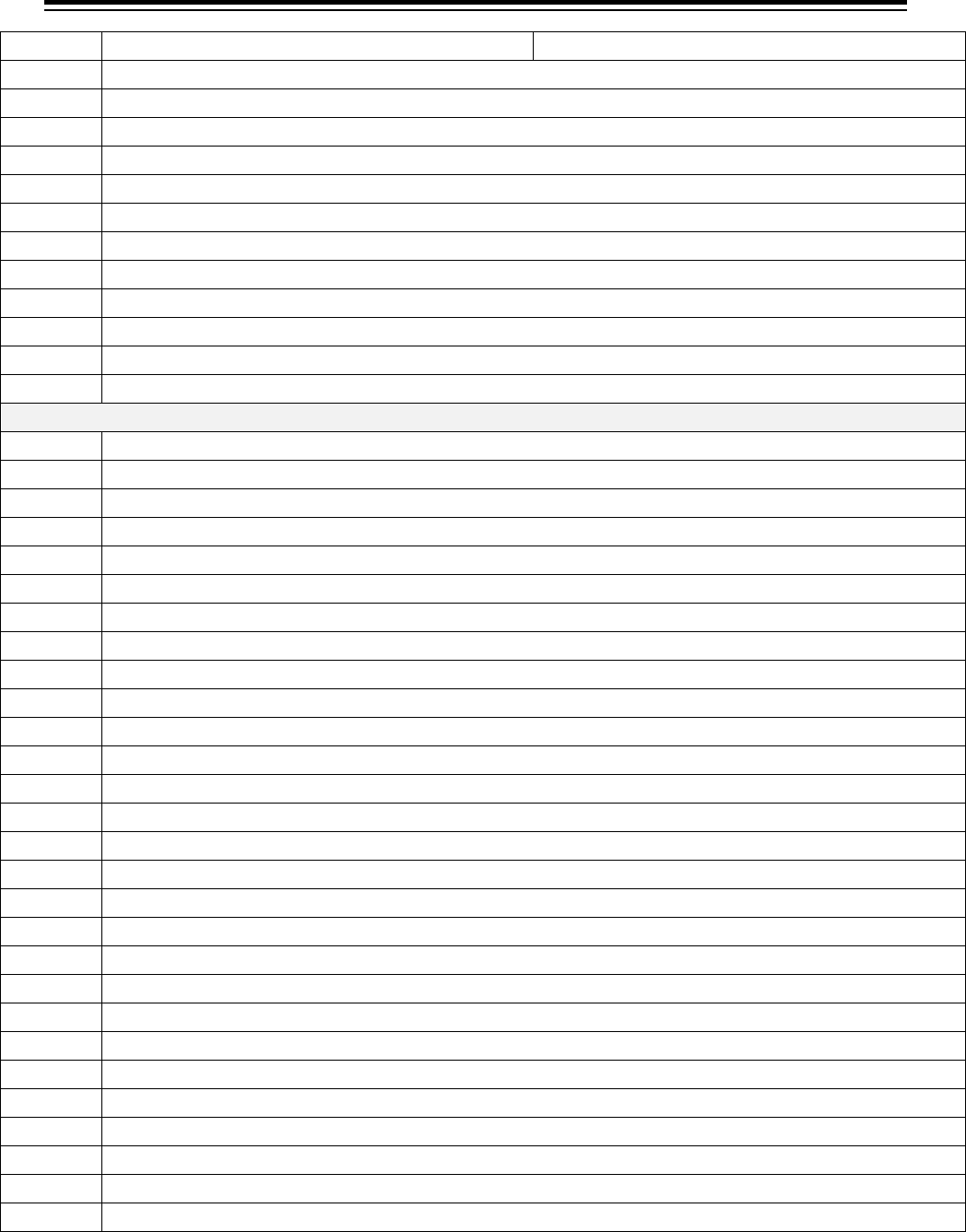

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

Article of Clothing, Footwear and Accessories (less than $100)

NT

Aerobic clothing

T

Antique clothing (collectable - not for wear)

NT

Antique clothing (for wear)

T

Appointment books

NT

Aprons/Clothing shields

T

Arch supports

T

Arm warmers

T

Athletic gloves, pads, supporters

T

Athletic or sport uniforms or clothing

NT

Athletic socks

T

Athletic supporters

NT

Baby clothes

NT

Baby diapers

T

Ballet shoes

T

Bandanas

T

Barrettes and bobby pins

T

Baseball gloves

T

Baseball shoes with cleats

T

Bathing suits, caps, and cover-ups

T

Batting fabric

T

Beach caps and coats

T

Belt buckles (when sold separately)

T

Belts for weightlifting

NT

Belts with buckles attached

NT

Belts without buckles

NT

Bibs

T

Bicycle shoes with cleats

T

Billfolds, wallets

T

Blankets

NT

Blouses

T

Bobby pins

T

Boots, specialty (including but not limited to climbing, fishing, hiking, riding, ski, waders)

NT

Boots, general purpose (winter, dress, cowboy)

NT

Bow ties

NT

Bowling shirts

T

Bowling shoes

T

Bracelets

T

Braces and supports worn to correct or alleviate a physical incapacity or injury

NT

Bras

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 7

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Bridal apparel, sold

NT

Bridal gowns and veils, sold

T

Briefcases

T

Buttons

NT

Camp clothing

NT

Caps and hats, including sports

T

Checkbook covers

NT

Chef’s uniforms

T

Chest protectors

NT

Choir and altar clothing

T

Cleated and spiked shoes

NT

Clerical vestments

T

Cloth and lace, knitting yarns and other fabrics

T

Clothing repair items such as thread, buttons, tapes, iron-on patches, and zippers

NT

Coats and wraps

T

Coin purses

NT

Corsets and corset laces

T

Cosmetic bags

T

Cosmetics

T

Costumes

NT

Coveralls

NT

Cowboy boots

NT

Diapers (adult and baby, cloth, or disposable)

NT

Dress gloves and shoes

T

Dress shields

NT

Dresses

NT

Earmuffs

T

Elastic ponytail holders

T

Elbow pads

NT

Employee uniforms, but not athletic or protective

T

Fabric

T

Fanny packs

T

Fins

T

Fishing boots (waders)

T

Fishing vests (non-flotation)

T

Football pads, pants, shoes, gloves

NT

Formal clothing, sold

NT

Fur clothing, coats, and stoles

NT

Galoshes

T

Garment bags

NT

Garters/garter belts

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 8

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Girdles, bras, and corsets

T

Gloves (protective), such as rubber, surgical, welding, work, and garden

T

Gloves (sports), i.e., baseball, bicycle, football, golf, handball, hockey, racquetball, tennis, and

weightlifting

NT

Gloves and mittens (generally), such as dress, winter, and leather

T

Goggles

NT

Golf clothing, caps, dresses, shirts, skirts, pants

T

Golf gloves

NT

Graduation caps and gowns

T

Hair bows, clips, nets, and bands

T

Hand muffs

T

Handbags and purses

T

Handkerchiefs

T

Hard hats

NT

Hats (general purpose: cowboy, baseball, knit)

T

Headbands

T

Helmets (bike, baseball, football, hockey, motorcycle, sports)

NT

Hosiery (panty hose, support, etc.)

T

Hunting vests

T

Insoles

NT

Jackets

NT

Jeans

NT

Jerseys - other than athletic wear

T

Jewelry

NT

Jogging apparel

NT

Jogging bras

T

Knee pads

NT

Lab coats

T

Leg warmers

NT

Leotards

T

Life jackets and vests

NT

Lingerie

T

Martial arts attire

T

Mitts (baseball fielder’s glove, hockey, etc.)

NT

Neckwear, including ties and scarves

NT

Nightgowns and night shirts

NT

Overshoes and rubber shoes

T

Pads (football, hockey, soccer, elbow, knee, shoulder)

NT

Pajamas

NT

Pants

NT

Ponchos

T

Ponytail holders

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 9

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Prom dresses

T

Protective masks (athletic, sport or occupational)

T

Purses

NT

Raincoats, rain hats, and ponchos

NT

Religious clothing

T

Riding pants

NT

Robes

NT

Rubber thongs, flip-flops

NT

Running shoes without cleats

T

Safety clothing and glasses

T

Safety shoes not adaptable for streetwear

NT

Sandals

NT

Scarves

T

Scuba gear

NT

Shawls and wraps

T

Shin guards and padding

NT

Shirts

T

Shoe inserts

NT

Shoelaces

NT

Shoes, general athletic

T

Shoes, specialty: athletic, ballet, bicycle, bowling, cleated, football, golf, jazz/dance, soccer, track, etc.

T

Shoes with cleats, spikes

NT

Shoes without cleats

NT

Shorts

T

Shoulder pads (football, hockey, sports)

T

Shoulder pads, for dresses, jackets, etc. (but not athletic or sport protective pads)

T

Shower caps

T

Skates (ice, in-line, roller)

T

Ski Boots

NT

Ski masks

T

Ski suits (snow)

T

Ski vests (water)

T

Skin diving suits

NT

Skirts

NT

Slacks

NT

Sleepwear, nightgowns, pajamas

NT

Slippers

NT

Slips

NT

Sneakers

NT

Socks

T

Sports clothing and uniforms and equipment such as mitts, helmets, and pads

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 10

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

T

Sports pads (football, hockey, soccer, knee, elbow, shoulder)

NT

Stockings

NT

Suits, slacks, jackets, and sports coats

NT

Suspenders

NT

Sweat suits

T

Sweatbands: arm, wrist, head

NT

Sweaters

NT

Sweaters, sweatpants

T

Swim masks, fins, goggles

T

Swimsuits and trunks

T

Tap dance shoes

T

Tennis skirts and dresses

NT

Tennis shoes

NT

Ties/neckwear

NT

Tights

NT

Trousers

NT

T-shirts

NT

Tuxedos, purchased

NT

Undergarments such as long johns

NT

Underwear

NT

Uniforms (occupational, military, scouting, school)

T

Uniforms for sport

NT

Vests, except hunting and water

NT

Walking shoes

T

Wallets, billfolds

T

Weightlifting belts

T

Wet and dry diving suits

NT

Windbreakers

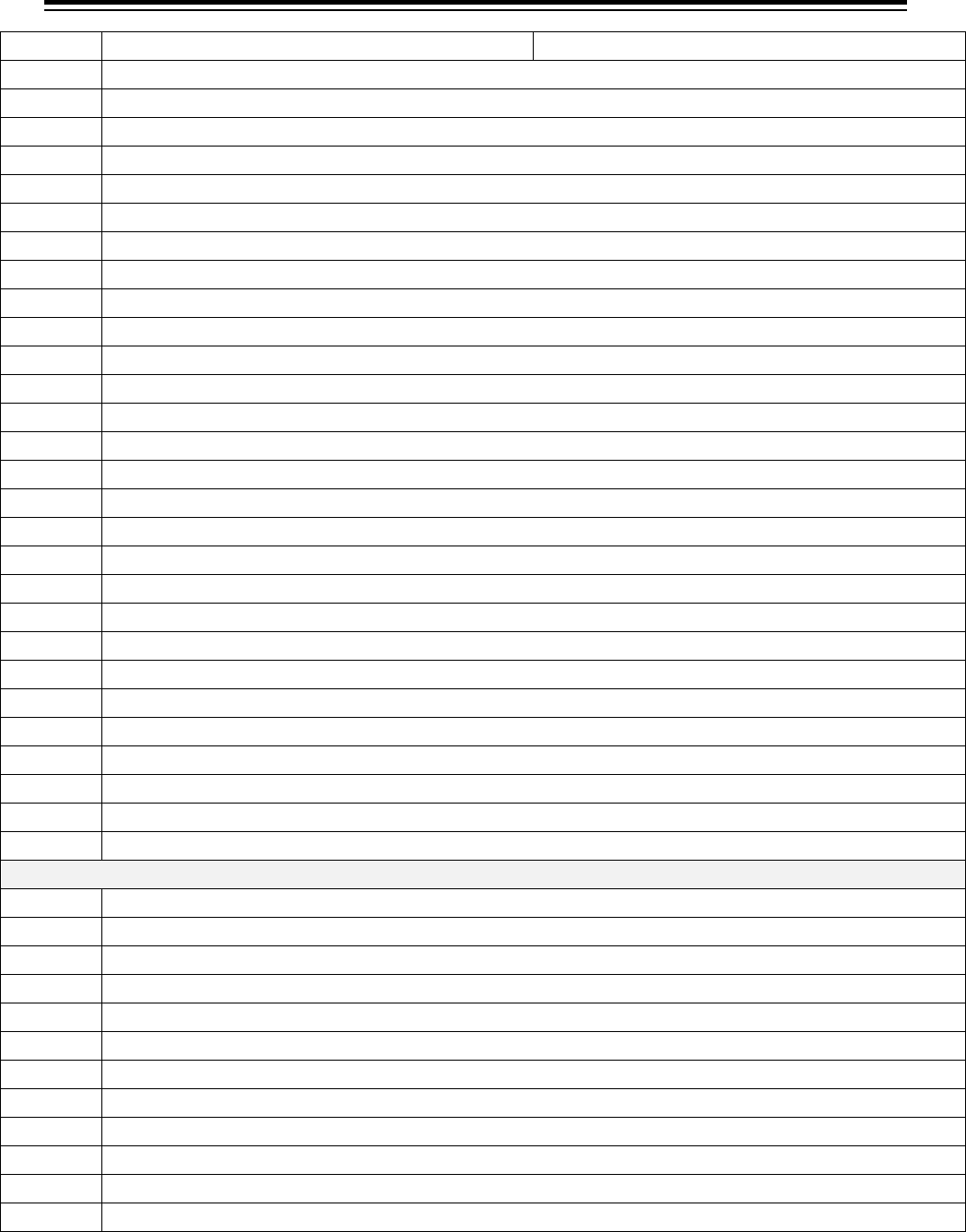

Computers (up to $1,000) and Computer-Related Items (up to $500)

NT

CD (blank)

T

CD (pre-recorded music, voice or otherwise)

NT

Central processing unit

NT

Computer (desktop, laptop, notebook, and tablet)

NT

Computer cables

NT

Computer disks (floppies and blank CDs)

NT

Computer hard drive

NT

Computer ink cartridges

NT

Computer keyboards

NT

Computer memory equipment

NT

Computer memory equipment (disks, flash/thumb drives)

NT

Computer microphones

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 11

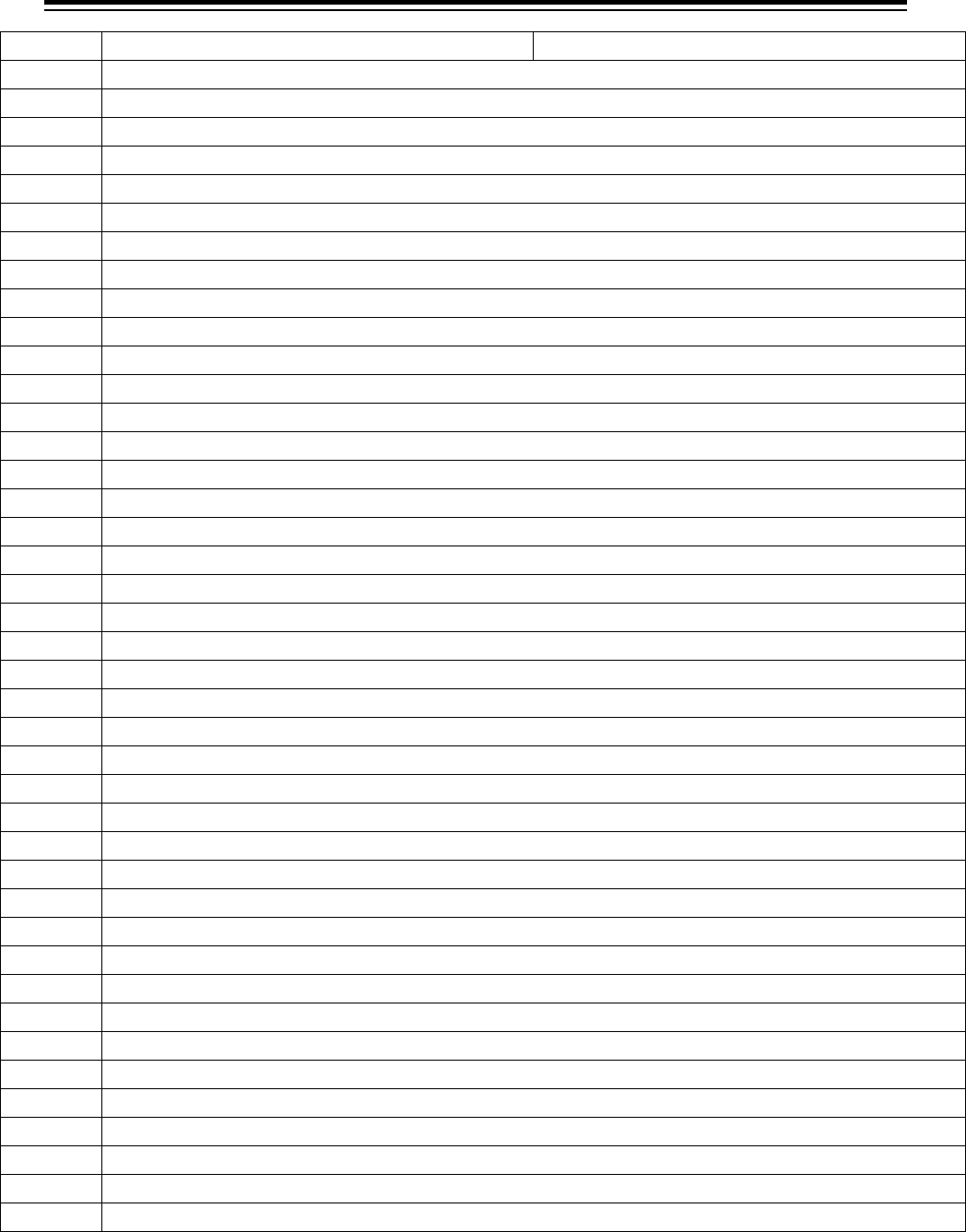

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Computer modems

NT

Computer monitor

NT

Computer motherboards

NT

Computer mouse

NT

Computer paper

NT

Computer printer

T

Computer scanners

NT

Computer speakers

T

Computer video camera

T

Computer software - unless bundled with a qualified computer sale

NT

Computer Zip drives

T

Computer/Software manuals

NT

E-Readers (if the model has computing functions such as word processing, spreadsheets, etc.)

T

E-Readers (Internet access only, no other computing functions)

T

Headsets, for use with a computer

T

Joy sticks

NT

Printer paper

NT

Tablet Computers

School Supplies (under $30) & Other School Items (applicable price limitations listed below)

NT

Assignment books

T

Backpacks (for hiking and similar activities)

NT

Backpacks (for school) – under $100

NT

Binders

NT

Binder clips

NT

Blue books

NT

Book bags

NT

Book covers

NT

Book markers

NT

Books (for school) – under $30

T

Books (not for school use)

NT

Calculators – under $200

NT

Canvas for oil painting

NT

Cellophane (transparent) tape

NT

Chalk

NT

Chalkboard erasers

T

Chalkboards

NT

Clipboards

NT

Construction paper

NT

Correction tape, fluid, or pens

NT

Colored pencils

T

Compact disc players

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 12

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Compasses

NT

Composition books

NT

Crayons, watercolors, and other art supplies

NT

Daily planners

NT

Data storage devices, such as CD drives

T

Digital cameras

T

Digital video cameras

NT

Divider folders

T

Dry boards for writing

T

Duffel bags

NT

Erasers

T

FAX machines

NT

File jackets

NT

Flash cards

NT

Folders

NT

Glue and glue refills (stick and liquid)

NT

Graph paper

T

Gym bags

NT

Highlighters

NT

Index cards

NT

Labels

NT

Loose-leaf binders

NT

Maps and globes - under $100

NT

Markers

NT

Masking tape

NT

Memo pads

NT

Modeling clay

NT

Notebook filler paper

NT

Notebooks

NT

Oil paints

NT

Paper (notebook or printer)

NT

Paste

NT

Pen ink

NT

Pencil box

NT

Pencil erasers

NT

Pencil lead

NT

Pencil sharpener

NT

Pencils, including mechanical and refills

NT

Pens, including felt, ballpoint, fountain, and refills

NT

Portfolios

NT

Poster board

New Mexico Taxation and Revenue Department

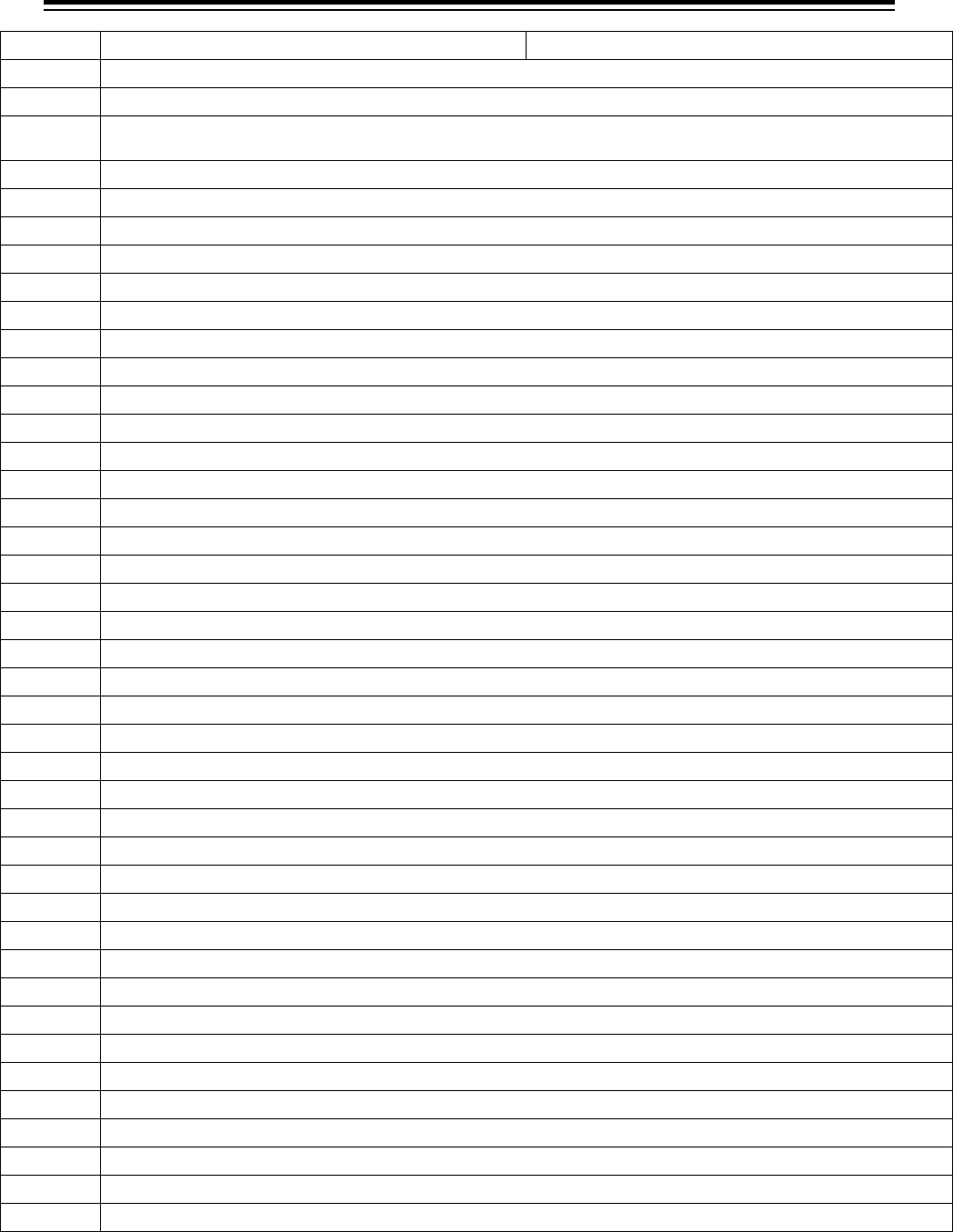

FYI-203 REV. 7/2021 Page 13

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

NT

Poster paper

NT

Legal pads

NT

Lunch boxes

NT

Protractors

NT

Rulers

NT

Scissors

NT

Sheet protectors

NT

Staplers and staples

NT

Tape and tape refills and dispenser

NT

USB flash drives; thumb drives

NT

Watercolor paint set

NT

ZIP drives

Other Items

T

Cellular telephones

T

Crib blankets

T

Diaper bags

T

Eyewear

T

Game controllers

T

Games - board, video, computer, action, adventure, role playing

T

Ice skates

T

Key chains and cases

T

Luggage

T

Magazines

T

Movies (DVD and VCR)

T

MP3 players and iPods

T

Musical instruments and related items

T

Patterns

T

PDA's

T

Periodicals

T

Sewing accessories (such as measuring tapes, needles, patterns, scissors, pins, thimbles)

T

Shaving kits/bags

T

Suitcases

T

Sunglasses

T

Receiving blankets

T

Tape recorders and microcassettes

T

Thread

T

Umbrellas

T

Videogame devices

T

Watch bands

T

Watches

T

Wigs, toupees, and chignons

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 14

T or NT

Item

“T” is “Taxable”; “NT” is “Nontaxable”

T

Yarn

T

Zippers

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 15

TAXPAYER INFORMATION

General Information. FYIs and Bulletins present general information with minimum technical language.

All FYIs and Bulletins are free of charge and available through all local tax offices and on the Taxation

and Revenue Department’s website at http://www.tax.newmexico.gov/forms-publications.aspx

Regulations. The Department establishes regulations to interpret and exemplify the various tax acts it

administers. Current statutes with regulations can be located on the Departments website for free at

http://www.tax.newmexico.gov/statutes-with-regulations.aspx. Specific regulations are also available at

the State Records Center and Archives or on its web page at http://www.srca.nm.gov/

The Taxation and Revenue Department regulation book is available for purchase from the New Mexico

Compilation Commission. Order regulation books directly from the New Mexico Compilation Commission

at https://www.nmcompcomm.us/

Rulings. Rulings signed by the Secretary and approved by the Attorney General are written statements

that apply to one or a small number of taxpayers. A taxpayer may request a ruling (at no charge) to clarify

its tax liability or responsibility under specific circumstances. The Department will not issue a ruling to a

taxpayer who is undergoing an audit, who has an outstanding assessment, or who is involved in a protest

or litigation with the Department over the subject matter of the request. The Department’s rulings are

compiled and available on free of charge at http://www.tax.newmexico.gov/rulings.aspx.

The request for a ruling must be in writing, include accurate taxpayer identification and the details about

the taxpayer’s situation, and be addressed to the Secretary of the Taxation and Revenue Department at

P.O. Box 630, Santa Fe, NM 87504-0630. The taxpayer’s representative, such as an accountant or

attorney, may request a ruling on behalf of the taxpayer but must disclose the name of the taxpayer.

While the Department is not required to issue a ruling when requested to do so, every request is carefully

considered.

The Secretary may modify or withdraw any previously issued ruling and is required to withdraw or modify

any ruling when subsequent legislation, regulations, final court decisions or other rulings invalidate a

ruling or portions of a ruling.

Public Decisions & Orders. All public decisions and orders issued since July 1994 are compiled and

available on the Department’s web page free of charge at http://www.tax.newmexico.gov/tax-decisions-

orders.aspx.

This publication provides general information. It does not constitute a regulation, ruling, or decision issued

by the Secretary of the New Mexico Taxation and Revenue Department. The Department is legally bound

only by a regulation or a ruling [7-1-60, New Mexico Statutes Annotated, 1978]. In the event of a conflict

between FYI and statute, regulation, case law or policy, the information in FYIs is overridden by statutes,

regulations and case law. Taxpayers and preparers are responsible for being aware of New Mexico tax

laws and rules. Consult the Department directly if you have questions or concerns about information

provided in this FYI.

New Mexico Taxation and Revenue Department

FYI-203 REV. 7/2021 Page 16

FOR FURTHER ASSISTANCE

Tax District Field Offices and the Department’s

call center can provide full service and general

information about the Department's taxes,

taxpayer access point, programs, classes, and

forms. Information specific to your filing

situation, payment plans and delinquent

accounts.

TAX DISTRICT FIELD OFFICES

ALBUQUERQUE

10500 Copper Pointe Avenue NE

Albuquerque, NM 87123

SANTA FE

Manuel Lujan Sr. Bldg.

1200 S. St. Francis Dr.

Santa Fe, NM 87504

FARMINGTON

3501 E. Main St., Suite N

Farmington, NM 87499

LAS CRUCES

2540 S. El Paseo Bldg. #2

Las Cruces, NM 88004

ROSWELL

400 Pennsylvania Ave., Suite 200

Roswell, NM 8820

For forms and instructions visit the Department’s

web site at http://www.tax.newmexico.gov

Call Center Number:

1-866-285-2996

If faxing something to a tax district field

office, please fax to:

Call Center Fax Number:

1-505-841-6327

If mailing information to a tax district field

office, please mail to:

Taxation and Revenue Department

P.O. Box 8485

Albuquerque, NM 87198-8485

For additional contact information please visit the

Department’s website at

http://www.tax.newmexico.gov/contact-us.aspx

This information is as accurate as possible as of the date specified on the publication. Subsequent legislation, new state

regulations and case law may affect its accuracy. For the latest information please check the Taxation and Revenue

Department’s web site at www.tax.newmexico.gov.

This publication provides general information. It does not constitute a regulation, ruling, or decision issued by the

Secretary of the New Mexico Taxation and Revenue Department. The Department is legally bound only by a regulation

or a ruling [7-1-60, New Mexico Statutes Annotated, 1978]. In the event of a conflict between FYI and statute, regulation,

case law or policy, the information in FYIs is overridden by statutes, regulations and case law. Taxpayers and preparers

are responsible for being aware of New Mexico tax laws and rules. Consult the Department directly if you have

questions or concerns about information provided in this FYI.