EE_1439_Ferrarini_OL.indd 1 22/09/2014 08:06

Asia and Global

Production Networks

Implications for Trade, Incomes and

Economic Vulnerability

Edited by

Benno Ferrarini

Senior Economist, Economics and Research Department,

Asian Development Bank, Philippines

David Hummels

Professor of Economics, Department of Economics, Purdue

University and Research Associate, National Bureau of

Economic Research, USA

CO-PUBLICATION OF THE ASIAN DEVELOPMENT

BANK AND EDWARD ELGAR PUBLISHING

Edward Elgar

Cheltenham, UK • Northampton, MA, USA

© Asian Development Bank 2014

All rights reserved. No part of this publication may be reproduced, stored in a

retrieval system or transmitted in any form or by any means, electronic, mechanical

or photocopying, recording, or otherwise without the prior permission of the

publisher.

Published by

Edward Elgar Publishing Limited Edward Elgar Publishing, Inc.

The Lypiatts William Pratt House

15 Lansdown Road 9 Dewey Court

Cheltenham Northampton

Glos GL50 2JA Massachusetts 01060

UK USA

The views expressed in this book are those of the authors and do not necessarily

reflect the views and policies of the Asian Development Bank (ADB), its Board of

Governors or the governments they represent.

ADB does not guarantee the accuracy of the data included in this publication and

accepts no responsibility for any consequences of their use.

By making any designation of or reference to a particular territory or geographic

area, or by using the term “country” in this document, ADB does not intend to

make any judgments as to the legal or other status of any territory or area.

ADB encourages printing or copying information exclusively for personal and

noncommercial use with proper acknowledgment of ADB. Users are restricted

from reselling, redistributing, or creating derivative works for commercial purposes

without the express, written consent of ADB.

Asian Development Bank

6 ADB Avenue, Mandaluyong City

1550 Metro Manila, Philippines

Tel +63 2 632 4444

Fax +63 2 636 2444

www.adb.org

A catalogue record for this book

is available from the British Library

Library of Congress Control Number: 2014938802

This book is available electronically in the ElgarOnline.com

Economics Subject Collection

ISBN 978 1 78347 208 6 (cased)

ISBN 978 1 78347 209 3 (eBook)

Typeset by Servis Filmsetting Ltd, Stockport, Cheshire

Printed and bound in Great Britain by T.J. International Ltd, Padstow

v

Contents

List of contributors vii

Foreword by Changyong Rhee ix

List of abbreviations and acronyms xi

1 Asia and global production networks: implications for trade,

incomes and economic vulnerability 1

Benno Ferrarini and David Hummels

2 Developing a GTAP- based multi- region, input–output

framework for supply chain analysis 16

Terrie L. Walmsley, Thomas Hertel and David Hummels

3 The vulnerability of the Asian supply chain to localized

disasters 81

Thomas Hertel, David Hummels and Terrie L. Walmsley

4 Global supply chains and natural disasters: implications for

international trade 112

Laura Puzzello and Paul Raschky

5 Vertical specialization, tariff shirking and trade 148

Alyson C. Ma and Ari Van Assche

6 Changes in the production stage position of People’s Republic

of China trade 179

Deborah Swenson

7 External rebalancing, structural adjustment, and real exchange

rates in developing Asia 215

Andrei Levchenko and Jing Zhang

8 Global supply chains and macroeconomic relationships

in Asia 249

Menzie Chinn

9 Mapping global value chains and measuring trade in tasks 287

Hubert Escaith

vi Asia and global production networks

10 The development and future of Factory Asia 338

Richard Baldwin and Rikard Forslid

Index 369

vii

Contributors

Richard Baldwin is Professor of International Economics at the Graduate

Institute, Geneva, Switzerland; a visiting Research Professor at the

University of Oxford, UK; Director of the Center for Economic Policy

Research (CEPR), UK; and Editor- in- Chief of Vox.

Menzie Chinn is Professor of Public Affairs and Economics at the

RobertM. La Follette School of Public Affairs, University of Wisconsin,

USA.

Hubert Escaith is the Chief Statistician of the World Trade Organization,

Switzerland and Research Associate at the Centre de Recherche en

Développement Économique et Finance Internationale, GREQAM/

DEFI Aix- Marseille University, France.

Benno Ferrarini is Senior Economist in the Economics and Research

Department of the Asian Development Bank, Philippines.

Rikard Forslid is Professor, Department of Economics, Stockholm

University, Sweden.

Thomas Hertel is Distinguished Professor of Agricultural Economics

at Purdue University, USA and founder and Executive Director of the

Global Trade Analysis Project (GTAP).

David Hummels is Professor of Economics, Department of Economics,

Purdue University and a Research Associate of National Bureau of

Economic Research, USA.

Andrei Levchenko is Associate Professor, Department of Economics,

University of Michigan, USA; Faculty Research Fellow, National Bureau

of Economic Research, USA; and Research Fellow, Centre for Economic

Policy Research, UK.

Alyson C. Ma is Associate Professor of Economics, University of San

Diego, USA.

Laura Puzzello is Senior Lecturer in the Department of Economics at

Monash University, Australia.

viii Asia and global production networks

Deborah Swenson is Professor of Economics, University of California –

Davis, USA and a Research Associate of National Bureau of Economic

Research.

Paul Raschky is Senior Lecturer in the Department of Economics at

Monash University, Australia.

Ari Van Assche is Associate Professor of International Business at HEC

Montréal and Research Fellow at CIRANO, Canada.

Terrie L. Walmsley is an Honorary Associate Professor in the Department

of Economics at the University of Melbourne, Australia and Chief

Economist at ImpactECON LLC, USA.

Jing Zhang is Senior Economist at the Federal Reserve Bank of Chicago,

USA.

ix

Foreword

The past few years have witnessed the emergence of a large and growing

body of research on global value chains (GVCs), that is the creation of

final goods and services through interlinked stages of production scattered

across international borders. Although GVCs are hardly a new phenom-

enon, the attention devoted to the topic largely is. After years of neglect,

policy makers, practitioners and scholars in the field of international

economics have come to agree that global value chains should figure more

prominently in policies, advice and research.

To be fair, there has been earlier work in the business and economics

literature, focused primarily on measurement of the extent, geographic

orientation, and growth in GVCs. But such work was sporadic, and only

during the past three years or so has GVCs as a topic been receiving the

full attention of the international policy community. Efforts have been

directed mainly to gathering necessary statistics and correctly measur-

ing the value- added trade associated with production fragmentation, as

opposed to gross trade statistics, which mask the true origin of the value

added embodied in goods and services traded internationally. Notably,

the World Trade Organization (WTO) Secretariat launched its ‘Made

in the World’ initiative in 2010, and has collaborated since with the

Organisation for Co- operation and Economic Development (OECD) and

other agencies to establish a statistical platform (OECD- WTO TIVA) that

quantifies GVCs and to increase the measurement capacity of the national

and international statistics agencies. Other notable efforts include the

United Nations Conference on Trade and Development UNCTAD- Eora

GVC database, as well as the World Input–Output Database (WIOD),

which was established by a consortium of universities, think tanks and

international bodies with funding by the European Commission and

launched in 2012.

Proper measurement is an important first step in understanding the

extent of GVCs, and a wealth of path breaking statistics and insights

have accrued from recent efforts in that direction. But what remains is

a far harder task: to understand how GVCs change the nature of global

economic interdependence, and how that in turn changes our under-

standing of policies appropriate in this new environment. This volume

x Asia and global production networks

attempts to take on some of this task, with particular focus on two broad

themes.

The first explores the impact of greater integration and interdependence

on economies’ exposure to adverse shocks elsewhere in the world, such as

natural disasters, political disputes, or recessions. Various chapters inves-

tigate to what extent do global value chains serve to transmit and even

magnify shocks across national borders and, when a national economy

absorbs the blow from an international shock, how firms respond. The

second theme looks at the evolution of global value chains at the firm level

and how this will affect competitiveness in Asia. Various chapters explore

theory and data at the firm level to understand the evolution of GVCs

within and across countries.

In this volume, authors bring to bear a wide variety of methodologi-

cal tools and data, and perspectives ranging from the firm-level micro

economy to the global macro economy to help understand how GVCs are

reshaping interdependence in Asia. With its emphasis on analysis, rather

than policy, this volume aims at providing scholars and stakeholders with

an analytical toolbox useful to conceptualizing and assessing the relevant

phenomena. Future work will have to complement these analytical aspects

with in- depth discussions about the policy and regulatory implications

stemming from the latest progress in this line of research, which largely

represents a joint effort and work in progress by a large community of

international and national policy makers, academia, and think- tanks.

I would like to thank Benno Ferrarini and David Hummels for their

outstanding leadership, coordination and management of the research

underlying this volume, and Cindy Castillejos- Petalcorin for invaluable

administrative support and editorial assistance. The volume benefitted

from excellent inputs from Richard Niebuhr as copy editor, and from

helpful advice by Anna Sherwood of the ADB Department for External

Relations on contractual matters concerning its publication. Joseph

Zveglich Jr provided strategic support and guidance throughout the study.

My special acknowledgement goes to the many scholars who contributed

their invaluable expertise to this study.

Changyong Rhee

Chief Economist, Asian Development Bank

xi

Abbreviations and acronyms

ADB Asian Development Bank

AIO Asian input–output

APL average propagation length

ASEAN Association of Southeast Asian Nations

B2B business- to- business

BACI Base pour l’analyse du commerce internationale

BEC Broad Economic Classification

CAD computer- aided design

CDE constant difference of elasticity

CEPII Centre d’Etudes Prospectives et d’Informations

Internationales

CES constant elasticity of substitution

CGE computable general equilibrium

CIF cost, insurance and freight

CNY Chinese yuan

CO

2

carbon dioxide

COMTRADE Commodity Trade Statistics Database

CPC Central Product Classification

CPI consumer price index

CRED Centre for Research on Epidemiology of Disasters

CT coordination technologies

DC developing countries

DGP data- generating process

EA East Asia

EBOPS Extended Balance of Payments Services Classification

ECLAC Economic Committee for Latin America and the

Caribbean

ELE electrical equipment

EM- DAT Emergency Events Database

Eora Eora multi- region input–output database

EU European Union

EUROSTAT European Commission statistics

EXIOBASE global, detailed multi- regional environmentally extended

supply and use/input–output database

xii Asia and global production networks

FAO Food and Agriculture Organization

FDI foreign direct investment

FOB free on board

G5 Group of five (France, Germany, Japan, the United

Kingdom, the United States)

G7 Group of Seven (Canada, France, Germany, Italy, Japan,

the United Kingdom, the United States)

G- 20 Group of Twenty (Argentina, Australia, Brazil, Canada,

the People’s Republic of China, France, Germany, India,

Indonesia, Italy, Japan, the Republic of Korea, Mexico,

the Russian Federation, Saudi Arabia, South Africa,

Turkey, the United Kingdom, the United States, and the

European Union)

GAD Global Antidumping Database

GATT General Agreement on Tariffs and Trade

GDP gross domestic product

GTAP Global Trade Analysis Project

GTAP- ICIO Global Trade Analysis Project- Inter- Country

Input–Output

GVCs global value chains

HHI Herfindahl–Hirschman Index

HP Hodrick–Prescott

HQ headquarters

HS Harmonized System

ICIO inter- country input–output

ICT information and communication technology

IDE- JETRO Institute of Developing Economies- Japan External Trade

Organization

IIO international input–output

IIT intra- industry trade

ILO International Labour Organization

IMF International Monetary Fund

IO input–output

IOT input–output table

IRF impulse response functions

ISIC International Standard Industrial Classification of All

Economic Activities

MNEs multinational enterprises

MRIO multi- region, input–output

NBER National Bureau of Economic Research

NICs newly industrialized countries

NSO national statistical office

Abbreviations and acronyms xiii

OECD Organisation for Economic Co- operation and

Development

OLS ordinary least squares

PPP purchasing power parity

PRC People’s Republic of China

RCA relative comparative advantage

RER real exchange rate

SC supply chain

SCT supply chain trade

SCV supply chain vulnerability

SDR Special Drawing Rights

SITC Standard International Trade Classification

SNA system of national accounts

SOE state owned enterprise

SUT supply and use table

TEC trade by enterprise characteristics

TFP total factor productivity

TiVA OECD- WTO trade in value added database

TOSP tasks, occupations, stages, products

ToT terms of trade

UK United Kingdom

UN United Nations

UNCTAD UN Conference on Trade and Development

UNIDO United Nations Industrial Development Organization

US United States

VA value added

VAR vector autoregressions

WDI World Development Indicators

WIOD World Input–Output Database

WTO World Trade Organization

WTW World Trade Web

ADB recognizes China by the name People’s Republic of China.

1

1. Asia and global production

networks: implications for trade,

incomes and economic vulnerability

Benno Ferrarini and David Hummels

1. INTRODUCTION

Global value chains (GVCs) involve the production of goods and services

through interlinked stages of production scattered across international

borders. The international exchange of intermediate inputs, as opposed to

final consumer goods, is a phenomenon as old as trade itself. What is new

in the global economy is rapid growth in the extent and the complexity of

global value chains. Nowhere in the world is production fragmented quite

as much, or GVCs quite as complex or as fast growing, as in Asia.

As a consequence, there has been a widespread recognition by policy

makers, practitioners and scholars in the field of international economics

that global value chains should figure more prominently in their policies,

advice and research. Early academic work focused primarily on measure-

ment of the extent, geographic orientation, and growth in GVCs (Arndt

and Kierzkowski 2001; Hummels, Ishii and Yi 2001; Grossman and Rossi-

Hansberg 2008; Kimura 2006; Johnson and Noguera 2012). Among inter-

national bodies, the World Trade Organization (WTO) Secretariat launched

its “Made in the World” initiative in 2010, and has collaborated since with

the Organisation for Co- operation and Economic Development (OECD)

to establish a statistical platform (OECD- WTO TiVA) to quantify GVCs

and to increase measurement capacity. Reports have thus proliferated by

international bodies, including the World Bank (Cattaneo et al. 2010),

IDE/JETRO and WTO (2011), OECD (2013), and UNCTAD (2013), and

various think tanks and other bodies, such as the World Economic Forum

(2012) and the Fung Global Institute (Park et al. 2013; Elms and Low 2013).

New measures have opened up insights into the extent and complexity

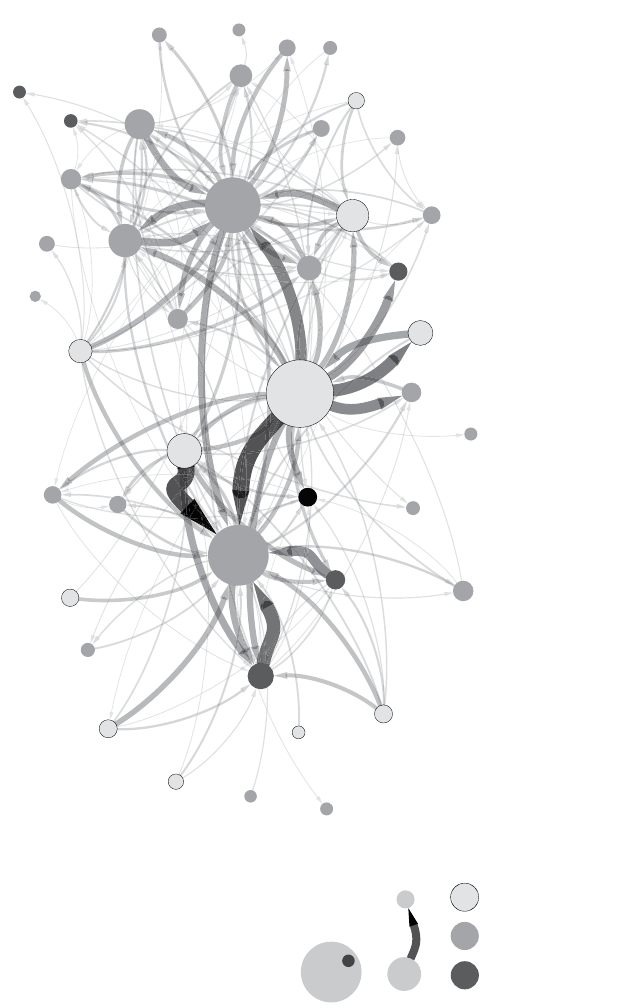

of global production networks. For example, Figure 1.1 shows a network

graph based on the OECD- WTO TIVA indicator of value added embodied

in 2009 gross exports by source country.

1

Three hubs – the United States

2

AUS

KOR

HKG

CHL

PHI

INO

VIE

SAU

NET

RUS

USA

GER

FRA

UKG

LTU

TUR

BEL

JPN

SWI

POR

POL

CZE

LUX

AUT

NOR

SVK

ITA

SPA

HUN

>40%

>60%

>80%

DEN

ISR

SWE

IRE

MEX

CAN

SIN

MAL

BRA

PRC

TAP

IND

FIN

THA

Relative size of countries’ total gross exports

Relative intensity and direction of value added transferred

Domestic value added as share of gross exports

Note: Based on OECD- WTO TiVA database, accessed 5 October 2013.

Source: Authors’ calculations.

Figure 1.1 Global value chains in 2009

Implications for trade, incomes and economic vulnerability 3

(US), Germany and the People’s Republic of China (PRC) – are seen at the

center of a tightly knit web of value added transfers mainly among regional

economies engaged in split production processes. The US is positioned at

the center of the global supply chains both as the largest gross exporter of

goods and services and as the main exporter of US value added embodied

in other countries’ exports. Germany and the PRC follow in the ranks in

terms of gross (direct) and value added (indirect) exports. Compared to the

US, these economies are positioned further downstream the value chains,

involving a substantial share of value added inflows and outflows.

2

In the

European regional network, horizontal integration prevails, with value

added flowing in both directions among country pairs. Asian production

networks are more hierarchical. At the top, countries such as Japan – and

the US from outside the region – inject value added through the provision

of key components and services to the PRC, the hub downstream, as well

as through Malaysia, Thailand and to a lesser extent the other Association

of Southeast Asian Nations economies as well as India. Other key players,

right at the center of the regional networks, are the Republic of Korea,

Taipei,China, as well as Singapore, each economy exporting high shares of

foreign value added in reflection of their strong GVC involvement.

Baldwin and Forslid (Chapter 10) in this volume provide a deeper

insight into the genesis and development of the Asian production net-

works, drawing on the latest data and insights that have become available

during the past two years, while Escaith (Chapter 9) delves into methodo-

logical issues concerning measuring and mapping of trade associated with

GVCs’ activities.

Proper measurement is an appropriate first step in understanding the

extent of GVCs, but it is only a beginning. What remains is a far harder

task: to understand how GVCs change the nature of global economic

interdependence, and how that in turn changes our understanding of poli-

cies appropriate in this new environment. The chapters in this volume are

focused on this harder task. The authors bring to bear a wide variety of

methodological tools and data, and perspectives ranging from the firm-

level micro economy to the global macro economy to help understand how

GVCs are reshaping interdependence in Asia.

2. ANALYTICAL TOOLS TO ASSESS THE

IMPLICATIONS OF GVCS FOR TRADE,

INCOMES AND ECONOMIC VULNERABILITY

We have two broad themes. We start with a topic of great concern to

scholars and policy makers. Greater integration and interdependence

4 Asia and global production networks

can lead to efficiency gains, but it can also expose national economies to

adverse shocks (natural disasters, political disputes, recessions) elsewhere

in the world. This suggests several important but underexplored questions.

One, to what extent do global value chains serve to transmit and even

magnify shocks across national borders? Two, when a national economy

absorbs the blow from an international shock, what are the most impor-

tant response margins? That is, do firms respond to the failure of a key

supplier or a drop off in foreign demand by shifting to new partners? If

not, do these trade shocks result in large changes in output and employ-

ment, or are they absorbed through changes in factor and product prices?

Of course, shocks need not be abrupt to have important effects at the mac-

roeconomic level. Rebalancing current account surpluses may take years

or decades, and the ways in which rebalancing is absorbed will depend

critically on how nations are linked through GVCs in both consumption

and production.

Our second theme is focused on the evolution of global value chains at

the firm level and how this will affect competitiveness in Asia. Global value

chains allow firms to specialize in stages of production in which they excel,

leaving remaining stages to other firms or other nations. Conceptually this

is a straightforward proposition – applying the principle of comparative

advantage to exchanging stages of production rather than final goods.

What remains unclear are the sources of advantage at the firm level.

Perhaps firm advantages are based on technological sophistication, the

realization of scale economies, arbitrage of policy differentials, or simply,

factor input costs. Also unclear is how firm advantages trade off against

the greater coordination costs of realizing these advantages in a far- flung

“global factory”. Various chapters explore theory and data at the firm

level to understand the evolution of GVCs within and across countries.

2.1 Disaster Impact Assessments with the GTAP Supply Chain Model

Walmsley, Hertel and Hummels (Chapter 2 in this volume) and Hertel,

Hummels and Walmsley (Chapter 3 in this volume) provide a set of tools

for analyzing global value chains in a full general equilibrium context.

Their approach can be thought of as a bridge between two important

literatures related to GVCs: multi- region input–output (MRIO) analysis

and computable general equilibrium (CGE) analysis. In a MRIO analysis

researchers link national input–output tables with trade data to construct

an international, multi- region IO table. Rather than examine total input

usage for each industry, as is the case in national tables, a MRIO provides

information on the source of these inputs. With this disaggregation a

researcher can calculate the share of foreign versus domestic value added

Implications for trade, incomes and economic vulnerability 5

in output and exports for a particular industry, or further break foreign

value added into specific source countries. That is, a MRIO distinguishes

the value of Korean and Chinese steel used in the Japanese automobile

industry, enabling researchers to examine how the Republic of Korea

and the PRC are differentially affected by a shock to Japan. Such tables

provide the basis of most trade in value added statistics and macro level

assessments of global value chains. Additional details on the strengths

and weaknesses of this approach can be found both in Walmsley et al.

(Chapter 2) and in Escaith (Chapter 9).

The challenge for a MRIO comes when a researcher wants to go beyond

a static look at the data and consider changes to the world economy.

That is, a MRIO describes a particular pattern of input–output use that

prevailed at a point in time, but is not well suited to analyzing what will

happen to that pattern should there be a significant shock to an economy.

To answer such questions requires a full computable general equilibrium

model that can track behavioral responses in production, consumption,

and trade.

Walmsley et al. (Chapter 2) provide a detailed discussion of how to

embed MRIO- like data on global value chains into GTAP, a widely used

CGE tool for world trade analysis. The resulting model is called GTAP-

SC (“Supply Chain”). This methodological piece includes a discussion of

the challenges and choices involved in reconciling disparate data sources

on GVCs. The chapter then provides a series of exercises meant to illus-

trate how MRIO and CGE approaches differ when analyzing changes

to global value chains. The authors show that standard MRIO analysis

is actually an extremely restrictive version of a CGE analysis in which

one assumes that output can instantaneously and costlessly adjust to any

shock to the system. The GTAP- SC model allows for much more general

responses, including evaluating how shocks lead to price changes, which

in turn induce substitution in production and consumption, both within

and across countries. The results here are illuminating in themselves,

but readers may find them even more useful as a kind of guidebook to

pursuing their own analysis of GVCs.

Hertel et al. (Chapter 3) employ the GTAP- SC model to evaluate two

major disasters that reduce output and productivity: the first in the elec-

tronics sector in Taipei,China and the second at the Port of Singapore.

The model traces through effects on goods and factor markets, focus-

ing on the distribution of effects as a function of GVC linkages to these

sectors. A clear distinction arises between sectors and countries that are

vertically linked to the disrupted area versus sectors and countries that are

substitutes. Vertically linked sectors suffer while substitutes enjoy tremen-

dous growth as they at least temporarily replace the disrupted production.

6 Asia and global production networks

A novel part of the analysis is the ability to evaluate changes that occur at

different time horizons. For example, at very short time horizons, output

quantities may be slow to respond to shocks, so all adjustment must

occur through prices. At medium horizons, some factors of production

(unskilled labor) may be mobile across firms, while others (capital to build

factories) are not, which allows for adjustment to occur through a mix of

price and quantity changes. Similarly, by varying substitution parameters

in the model, the authors can experiment with inputs as vitally necessary

(very difficult to replace), or commodities (easy to replace) to gauge the

resulting impact.

2.2 Natural Disasters Impact Assessment through Regression Analysis

We can think of Hertel et al. (Chapter 3) as a stylized simulation of

what might happen in some future disastrous event, tracing through the

effects on output, trade, employment, wages, and prices. Puzzello and

Raschky (Chapter 4) also examine natural disasters, but they focus on

disasters that have actually occurred and econometrically examine the

linkage between these disasters and trade flows. They draw on a com-

prehensive database of natural disasters (drought, earthquakes, floods,

wind storms) that provides data on the number of persons affected,

numbers killed, and estimated dollar damage for all countries worldwide

during the period 1995–2010. Using this data, they construct measures

of the vulnerability of global value chains to natural disasters. For each

country and industry, these measures capture the proportion of inputs

provided by suppliers struck by at least one large natural disaster in a

given year.

Next, they estimate a regression model that explains a country’s exports

at the industry level as a function of, among other factors, the vulner-

ability to natural disasters of that country- industry’s supply chain. The

causal channel here is straightforward. If an industry relies heavily on

inputs whose supply is disrupted by a disaster, it should raise costs or

lower production for that industry, and this will show up in reduced inter-

national competitiveness and exports. This is not inevitable, of course. It

may be that, while firms purchase inputs from abroad they are not truly

dependent on them. Rather, they may find it relatively easy to switch

away from a disaster- struck supplier to an alternative vendor, with costs,

competitiveness and exports unimpeded.

These authors reveal a set of interesting facts. They find that manu-

facturing products are highly exposed to large natural disasters abroad,

which is consistent with the high incidence of input trade in the manufac-

turing sector. Asia and North America are the regions most vulnerable to

Implications for trade, incomes and economic vulnerability 7

large natural disasters both at home and abroad, both because they are

more disaster prone and because production there is more globalized. The

regression estimates show that higher supply chain vulnerability to large

natural disasters significantly reduces exports, and that the effects are

larger when large disasters happen at home. More complex industries are

little affected by disasters at home, but are affected by disasters abroad.

This is consistent with the idea that firms find it relatively easy to substi-

tute away from affected inputs when they are domestically sourced inputs,

but find it difficult to do the same for imported inputs.

2.3 Impact Assessment of Current Account Rebalancing in Asia

While natural disasters are an excellent laboratory for examining abrupt

changes to GVCs and the world economy, not all shocks are abrupt or

unanticipated. Even slow moving changes can have profound effects if

they fundamentally reorder patterns of production and consumption.

Levchenko and Zhang (Chapter 7) examine one such shock, current

account rebalancing in Asia. A country running a trade surplus is spend-

ing less than the value of its output. Rebalancing – an elimination of the

trade surplus – then by construction increases the country’s total spend-

ing. Classical theory predicts that an elimination of a trade surplus in a

country: (i) increases both relative and real incomes; (ii) appreciates the

real exchange rate; (iii) increases the employment share in the non- traded

sector; and (iv) reduces exports. All of these effects are reversed in the

trade deficit countries as the trade imbalance is eliminated.

While useful starting points, classic theory on rebalancing is based on

stylized small- country or two- country models that are too simplistic to

reliably gauge the magnitudes involved. The real world features many het-

erogeneous countries with highly asymmetric trade relationships between

them. While this distinction is non- existent in two- country models, in the

real world the elimination of the PRC’s trade surplus will likely have a

very different global impact than the elimination of Japan’s trade surplus,

as those two countries occupy different positions in the world trading

system. Since there are differences in the nature and orientation of global

value chains feeding inputs into traded and nontraded sectors, rebalancing

will have differential effects on these suppliers.

Levchenko and Zhang base their analysis on a quantitative Ricardian-

Heckscher–Ohlin framework that features 75 countries (including 14

from developing Asia), 19 tradeable and 1 non- tradeable sector, multiple

factors of production, as well as the full set of cross- sectoral input–output

linkages forming a global supply chain. They begin with a baseline equilib-

rium that matches the observed levels of trade imbalances in each country

8 Asia and global production networks

in 2011, and then compare outcomes to a counterfactual scenario in which

each country is constrained to have balanced trade.

In their sample of 14 developing Asia countries, seven have trade sur-

pluses and seven trade deficits in 2011. Rebalancing leads to the following

effects. The surplus countries experience a large increase in wages relative

to the US, 17.5 percent on average. There is a modest (at the median, 4

percent) increase in the share of labor employed in the non- traded sector

as these countries stop transferring income abroad and instead use it to

purchase domestically produced goods and services. The trade- weighted

real exchange rate (RER) for the surplus countries in developing Asia

appreciates slightly, 1.47 percent on average. While one might expect

larger adjustments given the magnitude of the rebalancing involved, it is

important to keep in mind patterns of trade. Much of these countries’ trade

is with each other, and thus even as they are all appreciating relative to the

US, their trade- weighted appreciation is much smaller. The Republic of

Korea and Taipei,China even experience modest RER depreciations.

The impact of external rebalancing on welfare is much smaller than on

either relative wages or RERs. At the median, these countries experience a

rise in welfare of 0.4 percent, two orders of magnitude less than the average

increase in the relative wage. This is sensible: as these countries’ relative

wages rise dramatically, so do domestic prices. The net impact is positive

(with the sole exception of the Republic of Korea), but much smaller than

the gross changes in either wages or price levels. For countries running

deficits, the adjustments are the opposite of the surplus countries, and

of similar magnitudes, though welfare losses are much more substantial.

Finally, the authors track the changes due to rebalancing through global

value chains. A country’s welfare changes due to global rebalancing are

strongly positively correlated with whether it exports mostly to the deficit

or to surplus countries. Thus, multilateral trade relationships are crucial

for fully understanding the importance of rebalancing.

2.4 Monetary, Exchange Rate Policy and Business Cycle Analysis in

Light of GVCs

Continuing with a macroeconomic focus, Chinn (Chapter 8) offers a

broad look at how GVCs change the measurement and estimation of

key macroeconomic variables and relationships. In a world where all

trade is in final goods and all goods are traded, the real exchange rate

is easily defined and measured as the nominal exchange rate net of the

price level for final goods at home and abroad. In the presence of global

value chains, real exchange rates are conceptually difficult. Chinn reviews

two approaches in the literature, which turn on whether consumers have

Implications for trade, incomes and economic vulnerability 9

preferences over value- added (i.e. consumers care about each stage in

production and so real exchange rates must reflect where each stage took

place), or only over the final good, in which case global value chains only

matter to the extent that multi- stage production reduces the price of that

good. This literature shows that accounting for GVCs gives a picture

of the RER that differs significantly from conventional measures. For

example, using a GVC adjusted RER, the PRC’s effective exchange rate

appreciated 11.4 percentage points more than was implied using conven-

tional measures. These adjusted measures also significantly change our

measurement and interpretation of how the RER affects trade quantities

(i.e. the elasticity of trade with respect to movements in the RER) and

prices (the degree of pass- through).

Chinn next turns to business cycles. A number of researchers have

claimed that deeper integration via global value chains causes a greater

degree of business cycle synchronization. Chinn provides static and

dynamic exercises to examine whether there have been changes in theextent

of synchronization in Asia over time. First, he calculates thecorrelation of

quarterly GDP growth for Asian country pairs over the 1990–1996 and

1999–2012 periods, using a variety of techniques (HP filters, quadratic and

log detrending) to isolate business cycle components. Correlation coeffi-

cients among Asian country pairs rise significantly, especially those pairs

involving the PRC. As an accompanying exercise focused on dynamics,

Chinn estimates a non- structural VAR to evaluate the impulse response of

each country to output gaps in other countries.

Finally, Chinn analyzes whether global value chains alter the conduct

of monetary and exchange rate policy. The starting point is the idea that

policymakers will value a stable exchange rate when there is more produc-

tion sharing, and therefore more commercial transactions whose value will

be made uncertain by a fluctuating exchange rate. Further, if countries

desire to stabilize, do they stabilize against the US dollar or, owing to the

centrality of the PRC in Asian value chains, do they stabilize against the

Chinese yuan (CNY)? Previous work using daily currency movements has

shown that central banks now place more weight on the CNY than they

did prior to 2005. Chinn extends this work to longer horizons, monthly

and quarterly movements, and confirms the primary finding that the CNY

has risen in importance as a nominal anchor for the region’s currencies.

2.5 The Progression of People’s Republic of China’s Trade through GVC

Participation

We turn next to two chapters that are focused on the microeconomics

of global value chains at the firm level. Previous chapters in the volume

10 Asia and global production networks

have employed input–output tables to measure GVCs. This is a standard

approach, which is useful for comparability across countries and over

time, but it fails to capture significant heterogeneity across firms within

industries. An alternative approach is to rely on firm-level data that pro-

vides a highly detailed picture of which firms are deeply integrated into

GVCs, relying on foreign suppliers and selling to foreign customers, and

which are not. Chapters by Swenson (Chapter 6) and Ma and Van Assche

(Chapter 5), make use of Chinese customs data that provides a rich picture

of these transactions, including product and origin country information

for inputs and product and destination detail for exports. These data are

further broken out by “processing firms”, which import inputs free of

charge and sell their products outside the PRC, and “ordinary firms”,

which do not enjoy duty free imports, but can sell output domestically and

abroad.

One of the central questions of development relates to the progression

of countries through a rising level of production sophistication. At the

crudest level this can be characterized as a switch from agriculture to

“light” manufacturing to more complex manufacturing, and the literature

has provided a variety of ways to characterize technological sophistica-

tion. The rise of global value chains upends these traditional distinctions.

While a laptop computer may be a highly complex piece of machinery,

embodying advanced parts and technology, not all stages of its produc-

tion are complex or sophisticated. Some assembly stages may be labor

intensive, produced capably by workers with few skills or training. This

raises the question of whether the apparent rise in the sophistication of

Chinese exports (for example, a switch from textiles and apparel to elec-

tronics) simply captures Chinese participation in the simplest stages of

production.

Swenson (Chapter 6) uses the rich detail in Chinese customs data to

characterize changes in the production stage position of PRC firms. Key

to her analysis are measures of “upstreamness” and “stages” in production

developed by Fally (2012 a, 2012b). Suppose we have a production process

involving 10 sequential steps. A firm that produces the seventh step has six

previous “stages”, and is “upstream” from three subsequent steps. By using

very detailed IO tables to measure how far a production stage is from final

consumption, then matching this data to traded products, Fally is able

to characterize the “upstream” and “stage” measure of a given product.

Taking these measures, Swenson can then characterize where Chinese

firms sit in sequencing based on the inputs they purchase and the outputs

they produce. Over time, a firm can change its position in two ways. For a

given production process it can move closer to the point of final consump-

tion (increasing stages and decreasing upstreamness), or further away. Or

Implications for trade, incomes and economic vulnerability 11

it can switch to a more complex production process involving more steps

(conceivably increasing both stages and upstreamness).

In the aggregate, Swenson finds that Chinese firms have increased

both the stages and upstreamness, consistent with the view that they are

switching to production processes that involve increasingly long produc-

tion chains. Swenson next provides an alternative measure of complexity,

the number of distinct inputs used in production. Based only on a count

of distinct HS6 product lines imported, there is a decline in the number

of inputs. This could reveal falling complexity, or it could reveal a move

along the production chain further from final consumption. For example,

production of a microchip could involve relatively few parts, while

assembly of a laptop computer could involve many parts.

The initial work focuses on aggregate behavior of the Chinese economy

so Swenson next exploits firm-level data. She relates growth in imports and

exports to the position of these products in the value chain as measured by

Fally’s stages/upstreamness variables, while using fixed effects to control

for unobservables. There are striking differences between imports and

exports. Import growth is greater for products that exhibit higher stages

and upstreamness (products with longer chains), while export growth is

smaller for these products. Swenson also explores an alternative way to

see a similar relationship. She focuses on the probability of exit, that is,

identifying products that were imported (or exported) at some point by

a Chinese firm, but then cease to be, as a function of their position in

the value chain. Here the results are mixed and depend highly on goods

type. All in all, this chapter represents a wholly novel way to evaluate the

changing advantages of firms within multi- stage production processes.

2.6 Trade Policy Shocks and Production Relocation by Processing Firms

in the People’s Republic of China

Ma and Van Assche (Chapter 5) also employ the PRC customs data, but

in pursuit of a very different objective. They are interested in how global

value chains allow firms to circumvent trade policy barriers. The authors

begin with a model of heterogeneous firms similar to Melitz (2003), but

introduce two vertical stages of production: headquarters services pro-

duced at home, and manufacturing, which is footloose. The mobility of

manufacturing makes it profitable for some firms to circumvent tariffs and

produce abroad. A key insight is that global value chains increase the elas-

ticity of bilateral exports with respect to tariffs. The reason is that a tariff

hike has two effects. First it raises prices and lowers export sales for firms

who continue to produce at home. Second, it induces a subset of firms to

stop exporting and relocate production to avoid the tariff. Note that while

12 Asia and global production networks

global value chains amplify the effect of the tariff on manufacturing at

home, it dampens the effect on headquarters activities, which continue to

operate and provide services to manufacturing plants abroad. This result

is complementary to recent studies that find offshored assembly activities

are more vulnerable to business cycle shocks than corresponding domestic

activities.

Next, Ma and Van Assche investigate the prediction that vertically spe-

cialized trade is more sensitive to a country- specific tariff hike than exports

that are part of local value chains. They draw on both firm- level (2000–

2006) and provincial level (1997–2009) data from the PRC’s customs sta-

tistics, distinguishing Chinese firms based on customs regimes (processing

and ordinary trade). The processing trade regime is used primarily by

exporting firms in the PRC that are part of a global value chain, while the

ordinary trade regime is used by exporting firms that have more extensive

domestic value chains. Apart from legal treatment, this distinction is clear

in the data: processing exports embody less than half as much domestic

value added than ordinary exports, and foreign- owned firms play a much

more dominant role in the processing trade regime than in the ordinary

trade regime. To measure country- specific trade policy shocks, they use

antidumping cases against the PRC at the HS6 digit level as identified in

the World Bank’s Global Antidumping Database (GAD). Ma and Van

Assche find strong evidence that processing exports are more sensitive

to the imposition of antidumping measures than ordinary exports, and

consistent with the theoretical model, this is mostly due to the extensive

margin effect.

2.7 Measuring Global Value Chains

We conclude with two chapters that address broad conceptual issues high-

lighting the rise and future development of global value chains in Asia.

Escaith (Chapter 9) returns to the issue of measurement of global value

chains, setting in context the varied efforts by researchers and policy

institutes around the world. He strongly advocates for a process of theory

before measurement, or put another way, for researchers to understand

what questions they are trying to answer, and what measurement and data

organization tools are appropriate in that context. He reviews work on

input–output table based approaches, such as those used in the chapters

by Walmsley et al., Puzzello and Raschky, and to some extent in those by

Chinn and by Levchenko and Zhang. While these authors draw on exten-

sive work elsewhere and employ it in varied applications, readers may

find their explanations somewhat terse. Escaith’s chapter provides a more

detailed exegesis, including the economic assumptions implicit in these

Implications for trade, incomes and economic vulnerability 13

calculations. As an example, Chinn describes two methods for calculation

of the real exchange rate in the presence of GVCs, and these approaches

turn on whether consumers have preferences over value added or prefer-

ences over final goods. This is conceptually very close to the problem

described by Escaith in terms of using network theory to understand

GVCs. Can we think of consumers valuing electronic components from

Thailand independently of the way they are integrated into the network of

computer production throughout Asia?

When a methodology becomes dominant, as the MRIO approach has

in measuring GVCs, it can become easy to forget its limitations. Escaith

reminds us of these problems, and then highlights the different sorts of

conceptual questions and problems that can be answered with reference to

firm-level data. This points clearly to the strengths of the data approaches

employed by Swenson and by Ma and Van Assche.

As we noted at the outset of this chapter, the study of global value

chains has progressed beyond infancy but is at best an adolescent litera-

ture. There remain a host of interesting questions about GVCs that are

little understood. Indeed, Escaith’s simple enumeration of “what should

be counted” with respect to GVCs illustrates the fairly limited dimen-

sions of “what has been counted” in the literature extant. Ultimately

Escaith’s chapter provides a useful overview of the work to date, and

a rich outline of work to do for the ambitious researcher or concerned

policy maker.

2.8 The Development and Future of Production Networks in Asia

In a similar vein, Baldwin and Forslid’s Chapter 10 provides a useful over-

view of how global value chains arose in Asia, and where they are going.

They begin with the history, describing globalization as two unbundlings

driven first by lower trade costs (tariffs, transportation costs), and second

by improvements in information and communication technology (ICT).

The first unbundling allowed production and consumption to be sepa-

rated by great distances, but production stages remained bundled locally,

in factories and industrial districts. The ICT revolution unbundled the

factories themselves. They illustrate these facts with a series of data dis-

plays meant to illustrate the sharp changes in trade volumes and patterns

of trade in value added corresponding to the period of the ICT revolution.

These displays also provide a useful set of indicators going forward to

track the extent and growth of GVCs.

The second part of the chapter provides some simple conceptual theory

to help the reader understand driving forces between the second unbun-

dling. The first organizes production into a TOSP (tasks, occupations,

14 Asia and global production networks

stages, and products) hierarchy, where tasks, or the most granular activi-

ties, are bundled in groups to workers of particular occupations, who are

themselves bundled into stages, with these stages ultimately bundled into

products. For a product like a laptop computer, we could separate design,

parts production, assembly, and marketing into four distinct stages. The

design stage could involve occupations like electrical engineers or soft-

ware coders, each of whom has a large set of discrete tasks that must be

completed to design a microchip or the computer’s hardware BIOS.

With this setup in hand, the challenge is to think in terms of the optimal

aggregation of occupations and stages, that is, how many tasks should be

completed by each occupation, and how occupations should be bundled

into a given stage. The ICT revolution lowers the cost of communicating

between disparate stages (making it lower cost to disaggregate occupa-

tions), but it also lowers the marginal benefit of specialization as automa-

tion enables individual workers to master more tasks without the loss of

efficiency. This simple framework helps us to think through the extent of

unbundling, trading off efficiency and coordination costs. A key point

here is that relationships are not monotonic; in other words, the model

reveals tipping points at which offshoring can increase rapidly or even

decrease as costs fall. Further, these costs interact with traditional sources

of comparative advantage that may itself evolve. In short, it is not at

all obvious whether global value chains in Asia will continue to grow in

size and complexity, or whether we have hit a high water mark in their

importance.

NOTES

1. Figure 1.1 was drawn with the help of Cytoscape, an open- source platform for complex

network analysis and visualization (www.cytoscape.org). The network graph extends

across all country pairs, involving more than 3000 connections. To avoid clutter, only

the top 5 percent are shown on this map. Also omitted from the map are value added

transfers to and from the rest of the world aggregate, as well as self- looping arches in

relation to countries’ domestic value added. Shown are the top 5 percent of value added

flows among country pairs in 2009, connected by arches whose width is proportional

to source countries’ value added embodied in recipient countries’ exports. Individual

economies are shown as nodes whose size relates to the gross value of goods and services

exports. Darker shades denote economies with lower shares of domestic value added in

gross exports, compared to more brightly shaded nodes. The method is described further

in Ferrarini (2013).

2. In fact, exports by the US (89 percent) contain a considerably higher share of domestic

value added compared with that of Germany (73 percent) and the PRC (68 percent).

Implications for trade, incomes and economic vulnerability 15

REFERENCES

Arndt, S.W. and H. Kierzkowski (2001), Fragmentation: New Production Patterns

in the World Economy, Oxford University Press.

Cattaneo, O., G. Gereffi, and C. Staritz (eds) (2010), Global Value Chains in a

Postcrisis World – A Development Perspective, The World Bank, Washington,

DC.

Elms, D.K. and P. Low (eds) (2013), Global Value Chains in a Changing World,

Fung Global Institute, Nanyang Technological University, and World Trade

Organization.

Fally, T. (2012a), ‘Production staging: measurement and facts’, University of

Colorado, Boulder, Manuscript.

Fally, T. (2012b), ‘Data on the fragmentation of production in the U.S.’,

University of Colorado, Boulder, Manuscript.

Ferrarini, B. (2013), ‘Vertical trade maps’, Asian Economic Journal, 105–123.

Grossman, G.M. and R.- H. Esteban (2008), ‘Trading tasks: a simple theory of

offshoring’, American Economic Review, 98, 1978–1997.

Hummels, D., J. Ishii, and K.- M. Yi (2001), ‘The nature and growth of vertical

specialization in world trade’, Journal of International Economics, 54, 75–96.

IDE/JETRO (Institute of Developing Economies/Japan External Trade

Organization and World Trade Organization) (2011), Trade Patterns and Global

Value Chains in East Asia: From Trade in Goods to Trade in Tasks, Geneva:

World Trade Organization.

Johnson, R.C. and G. Noguera (2012), ‘Accounting for intermediates: produc-

tion sharing and trade in value added’, Journal of International Economics, 86,

224–236.

Kimura, F. (2006), ‘International production and distribution networks in East

Asia: eighteen facts, mechanics, and policy implications’, Asian Economic Policy

Review, 1, 326–344.

Melitz, M.J. (2003), ‘The impact of trade on intra-industry reallocations and

aggregate industry productivity’, Econometrica, 71, 1695–1725.

OECD (2013), Interconnected Economies – Benefitting from Global Value Chains,

OECD Publishing.

Park, A., G. Nayyar, and P. Low (eds) (2013), Supply Chain Perspectives and Issues

– A Literature Review, Fung Global Institute and World Trade Organization.

UNCTAD (2013), World Investment Report 2013 – Global Value Chains: Investment

and Trade for Development, Geneva: United Nations.

World Economic Forum (2012), The Shifting Geography of Global Value Chains:

Implications for Developing Countries and Trade Policy, Cologny/Geneva,

Switzerland.

16

2. Developing a GTAP- based multi-

region, input–output framework for

supply chain analysis

Terrie L. Walmsley, Thomas Hertel and

David Hummels*

1. INTRODUCTION

With the global economy increasingly inter- connected through interna-

tional trade in intermediate inputs as well as consumer goods, the demand

for analytical tools that trace out the implications of these linkages has

grown significantly. Examples include studies of international supply

chains and trade in value added (Koopman et al., forthcoming; and

Johnson and Noguera, 2012), virtual water trade (Konar et al., 2013), life

cycle assessment of environmental impacts (Hendrickson et al., 1998), and

greenhouse gas (GHG) emissions associated with global trade flows (Peters

et al., 2011). All of these studies require a global database that traces out

these trade flows between sectors and between producers and consumers

of final goods and services, that is, a multi- region, input–output (MRIO)

database. In response to these demands, several projects have been formed

with the goal of producing new MRIO databases, including EXIOBASE

(Tukker et al., 2009), WIOD (Timmer, 2012), OECD- TiVA (OECD,

2012) and Eora (Lenzen et al., 2013 and Lenzen et al., 2012).

An alternative source of global economic data suitable for MRIO-type

analysis is the Global Trade Analysis Project (GTAP) database

(Narayanan et al., 2012), first released in 1993, which has been updated

and encompasses eight releases covering the period 1990 to 2007; a 2011

update is being prepared. The GTAP database is most commonly used as

the foundation for global computable general equilibrium (CGE) models.

At its core, it is very similar to a MRIO database in that there is an input–

output structure for each country that is linked via trade flows to partner

countries. However, while it contains far more policy detail than a MRIO,

the existing GTAP data contains less import- sourcing detail than is found

in a typical MRIO database. Rather than tracing bilateral trade flows to

Developing a GTAP- based multi- region, input–output framework 17

individual agents (intermediate and final), the existing GTAP database

aggregates these flows at the border. In this chapter we adopt procedures

found in the MRIO literature to disaggregate these flows, thereby creating

a complete MRIO from the GTAP database. The benefit of adapting the

GTAP database is that it offers broad geographical coverage, and has long

term support from a community of researchers and policy makers who

employ and update the data on an ongoing basis.

A MRIO database is most useful if it is integrated with tools that can be

used to understand the evolution of supply chains in response to changes

in technology, final demands, policy and other shocks. That is, global

supply chains represent a complex set of general equilibrium interdepend-

encies between countries that reflect a combination of preferences, tech-

nology, endowments, and policy. Shocks to income or changes in trade

policy, for example, may result in subtle ripple effects throughout supply

chains that are difficult to understand by considering only retrospective

patterns of output and trade, or by fixing relative prices in prospective

analyses. By relaxing these restrictive assumptions, CGE analysis of global

supply chains can be considerably more flexible and powerful.

In its simplest form, MRIO- based supply chain analysis investigates

the strength of forward and backward linkages from a critical sector or

region to the rest of the global economy. If the Japanese automobile sector

expands by 10 percent, we can use MRIO tools to calculate the quantity of

Korean steel and Thai electronics embodied in a Japanese car, and assume

these sectors expand accordingly. This type of fixed- price, IO- multiplier

analysis relies on some very strong assumptions. In particular, it requires

that there is an infinitely elastic supply of factors available to the economy.

In contrast, CGE analysis would typically take supplies of factors as fixed

and allow prices to adjust and factors to be reallocated across sectors in

order to achieve a new, general equilibrium. That is, an expansion of the

Korean steel sector incurs an opportunity cost in terms of output fore-

gone elsewhere in the Korean economy and the adjustment mechanism is

through changes in factor and commodity prices that cascade throughout

the economy.

We can then think of MRIO supply chain analysis as a special case

of CGE analysis in which there is a perfectly elastic supply of primary

factors that can expand or contract at constant wage and rental rates.

By imposing these factor supply conditions as special restrictions on the

CGE model, we can alternately explore the implications of a given shock

in the presence of MRIO assumptions or in a more general environment in

which these assumptions are relaxed.

Having built a GTAP- based MRIO, this chapter illustrates its use-

fulness through two applications, which have been selected in order to

18 Asia and global production networks

highlight key features of MRIO analysis and extensions thereof. First,

we examine the global labor market implications of economic growth.

We start with a fixed- price IO multiplier model then sequentially relax

the model’s closure assumptions to demonstrate the flexibility of the full

CGE. This application also capitalizes on recent work to disaggregate

labor endowments in GTAP into five occupational categories to under-

stand how economic growth will affect direct and indirect labor market

demands in major Asian markets. We find that the linkages within Asia

and between Asia and the rest of the world make it a true engine for

growth in the world economy. However, sourcing splits are ultimately

endogenous – suggesting that more formal economic modeling is required

to understand how these are likely to evolve.

Our second application highlights both the importance of disaggre-

gating import sources in a MRIO database, and of analyzing them in a

CGE policy setting. Specifically, a key aspect of developing a full MRIO

is attributing import sources for both intermediate and final demands to

individual source countries. For example, it might be that both Thailand

and Japan export large volumes of electronics, but Thailand exports elec-

tronics inputs while Japan exports electronics final goods. To illustrate

this distinction we analyze the effect of eliminating tariffs on imported

intermediates, while leaving tariffs on final goods unchanged. We find

that the additional detail on sourcing can significantly improve our ability

to examine the impact of trade liberalization policies aimed specifically

at firms. Indeed we find that different sourcing shares can affect the size

of the tariff shock and the extent to which other countries gain from

increased exports.

2. BACKGROUND TO MRIO DATABASES

With the increased interest in life cycle and supply chain analyses at the

global or multi- regional level there has been a significant escalation in the

development of databases linking country input–output tables (IOT).

1

Since the motivation behind the development of these datasets is the exami-

nation of supply chains, these databases require information on the value of

imports of commodity

i

by agent (firms, government, households etc), from

source

s,

by region

r.

At this time, however, there is no global source for this

kind of detailed information and data on individual countries (databases

built by IDE- JETRO using industry surveys being the exception). Most of

the global datasets must therefore rely on the proportionality assumption

or the use of the UN Broad Economic Classification (or BEC concordance)

with HS6 COMTRADE data to split imports sources by agent.

Developing a GTAP- based multi- region, input–output framework 19

Table 2.1 can be used to better explain the challenge faced by those

undertaking global MRIO analyses. (The table follows GTAP notational

conventions, since they are widely used and well defined.) In an ideal

world data would be available on the commodity

(

i

)

,

source

(

s

)

,

destina-

tion

(

r

)

,

and agent (

VIFMS

i,j,s,r

:

intermediate firms (1 . . . j),

VIPMS

i,s,r

:

household private consumption,

VIGMS

i,s,r

:

Government consumption

(

G

)

and

VIEMS

i,s,r

:

Investment).

2

Country IO tables or supply and use tables provide the total purchases

of intermediate inputs by firm

j

(

VFM

i,j,r

)

and the total purchases of final

goods by households, government and for investment

(

VPM

i,r

VGM

i,r

and

VEM

i,r

)

,

as well as the value of domestic sales

(

VDM

i,r

)

and the

value of imports

(

VIM

i,r

)

.

Note that the latter are typically not broken

out by source. In some tables there may also be reasonable detail on

the split of intermediate and final purchases into domestically pro-

duced

(

VDFM

i,j,r

,VDPM

i,r

,VDGM

i,r

and

VDEM

i,r

)

and imported items

(

VIFM

i,j,s,r

,VIPM

i,s,r

,VIGM

i,s,r

and

VIEM

i,s,r

)

,

but again, none of these

imports are disaggregated by source country. Rather, imports are simply

aggregated into a single category.

From the United Nations’ COMTRADE database we can obtain

imports

(

VIMS

i,s,r

)

of commodity

(

i

)

by source

(

s

)

and destination

(

r

)

,

but these are not disaggregated by use within the importing country and,

once aggregated, they do not match the data reported in the IO tables.

Two approaches have therefore been used to estimate

VIFMS

i,j,s,r

and

VIPMS

i,s,r

,VIGMS

i,s,r

and

VIEMS

i,s,r

,

thereby constructing an MRIO

database.

Table 2.1 Creating a multi- region input–output database

Sources Intermediate Final Constraints

Sectors 1. . .j Investment Private

Consumption

Government

Consumption

Import

sources 1. . .s

VIFMS

i,j,s,r

VIFMS

i,s,r

VIPMS

i,s,r

VIGMS

i,s,r

VIMS

i,s,r

(COMTRADE)

Domestic r

(IO Data)

VDFM

i,r

VDEM

i,r

VDPM

i,r

VDGM

i,r

VDM

i,r

(IO data)

Constraints

(IO Data)

VFM

i,j,r

VEM

i,r

VPM

i,r

VGM

i,r

Note: COMTRADE = United Nations Commodity Trade Statistics Database; IO =

input–output.

Source: Authors’ calculations.

20 Asia and global production networks

2.1 The Proportionality Method

This is the simplest method, and has therefore been frequently used in the

MRIO literature. It assumes that all uses of a good are sourced in the same

way. That is, if 10 percent of all Chinese imports of electronics come from

Thailand, we assume that the same 10 percent share applies whether they

are used as intermediate inputs, investment, by the government sector or

household final demand, so that:

VIFMS

i,j,s,r

a

s

VIFMS

i,j,s,r

5

VIPMS

i,s,r

a

s

VIPMS

i,s,r

5

VIGMS

i,s,r

a

s

VIGMS

i,s,r

5

VIEMS

i,s,r

a

s

VIEMS

i,s,r

5

VIMS

i,s,r

a

s

VIMS

i,s,r

2.2 The BEC Concordance Method

This method uses the detailed BEC concordances to split commodities at

the HS6 level into intermediate goods, final goods or mixed. Within elec-

tronics, for example, a microchip would likely be classified as an interme-

diate input, while a laptop could be a final good. Using the COMTRADE

HS6 data with source countries disaggregated, in conjunction with these

BEC- derived splits into final, intermediate and mixed, then allows us

to determine the sourcing shares of both intermediate and final goods

independently. If in the trade data Thailand exports microchips and the

People’s Republic of China (PRC) exports laptops, we will obtain differ-

ent sourcing shares for the aggregated category of electronics, even though

we have no independent information on sourcing shares at the HS6 level.

These BEC- influenced sourcing shares for aggregated commodities

are then applied and the data are rebalanced to ensure the adding up

constraints given in Table 2.1. Given the limited information about sourc-

ing in the BEC concordance, this method only provides sourcing shares

for total intermediates (i.e.,

VINMS

i,s,r

5 S

j

VIFMS

i,j,s,r

) and total final

goods

(

VILMS

i,s,r

5

VIPMS

i,s,r

1

VIGMS

i,s,r

1

VIEMS

i,s,r

)

.

3

It does not

distinguish between the sources of, for example, imported steel used in the

motor vehicle industry as opposed to the coal industry for a given desti-

nation country. Nor does it distinguish between the sources of imported

leather for private consumption as opposed to investment or government

uses. To further split these data across intermediate or final uses the

proportionality assumption must be used. Hence:

Developing a GTAP- based multi- region, input–output framework 21

VIFMS

i,j,s,r

a

s

VIFMS

i,j,s,r

5

VINMS

i,s,r

a

s

VINMS

i,s,r

and

VIPMS

i,s,r

a

s

VIPMS

i,s,r

5

VIGMS

i,s,r

a

s

VIGMS

i,s,r

5

VIEMS

i,s,r

a

s

VIEMS

i,s,r

5

VLMS

i,s,r

a

s

VLMS

i,s,r

But

VINMS

i,s,r

a

s

VINMS

i,s,r

≠

VLMS

i,s,r

a

s

VLMS

i,s,r

A number of efforts are currently being undertaken to develop regional

and/or global MRIO datasets. Some of these tables do not yet include the

additional MRIO detail on sourcing by agent, while others have devel-

oped MRIO variants using the proportionality method – for example,

EXIOBASE (Tukker et al., 2009) and various GTAP- based MRIOs

(Andrew and Peters, 2013 and Johnson and Noguera, 2012). The World

Input–Output Database (WIOD) (Timmer, 2012), the TiVA database

(OECD, 2012) and the GTAP- Inter- Country Input–Output (GTAP-

ICIO) (Koopman et al., 2010) are examples of global databases where the

BEC concordance has been used to improve the sourcing splits. Table 2.2

lists some of these projects and the differences in their approaches to the

inclusion of the supply chain detail.

4

Since IO tables are not produced on an annual basis, all of the datasets

discussed above will have had to rely on external data to update the MRIO

to a consistent ‘base year’ and/or ‘fill in’ missing information in the IO

tables to ensure consistency in the data across countries. Another feature

of many of these datasets is the availability of time series. The underlying

idea/assumption behind the updating of these IO tables to a new base year

or the creation of time series data is that it is the IO shares that matter and

that these shares do not change significantly between releases of new IO

tables by statistical agencies. In some cases the producers of these datasets

have chosen to release only those years for which they have IO tables

(e.g., the OECD- WTO TiVA and JETRO databases), while in other cases

constrained optimization techniques have been used to fill in missing years

using the structure given in the IO table for another year as the starting

point and updating it with additional macroeconomic and/or production

data (e.g., WIOD and Eora). In the case of GTAP and EXIOBASE the

data are released for one year (or two in the case of the recent GTAP v.8

22 Asia and global production networks

Table 2.2 Summary of datasets

Database Reference Primary

approach used

to include

supplychain

detail

Balancing

IDE- JETRO

Asian

International

Input–

Output

Tables

Meng et al. (2013) Country foreign

trade data and

imported input

surveys

Manual

identification of

errors/reasons

fordifferences,

followed by

manual

adjustment

OECD- WTO

TiVA

database

OECD (2012) OECD tables

and BEC

concordances

approach

withHS6

tradedata

OECD IO Tables

were adjusted to

ensure balanced

bilateral trade

GTAP

Database

Narayanan et al.

(2012)

Does not include

MRIO detail

Trade data given

priority

GTAP- MRIO Andrew and

Peters (2013)

and Johnson and

Noguera (2012)

Proportional Re- balancing not

required

GTAP- ICIO Koopman et al.

(2010)

BEC

concordance

plus additional

detail on special

processing zones

in People’s

Republic of

China, and

Mexico.

Trade data given

priority

WIOD Timmer (2012) BEC

concordances

approach

withHS6 trade

data

IO/SUT data

given priority. No

balancing undertaken

EXIOBASE Tukker et al.

(2009)

Proportional IOT given priority

but RAS used

torebalance and

ensure non- negative

trade

Developing a GTAP- based multi- region, input–output framework 23

database),

5

however, not all IO tables derive from the base year and hence

they use similar optimization techniques to update the data to the relevant

year.

3. BUILDING A GTAP- BASED MRIO

In this section we describe in detail the process of converting the GTAP

database to a global MRIO by disaggregating imports of commodity

i

from source

s

by region

r

into distinct uses (intermediate versus final). By

going through this process in some detail, we gain better insight into the

alternative approaches currently employed in this literature.

Table 2.2 (continued)

Database Reference Primary

approach used

to include

supplychain

detail

Balancing

EORA Lenzen, Moran

et al. (2013)

and Lenzen,

Kanemoto et al.

(2012)

IO tables

where available

and BEC

concordances

approach with

HS6 trade data

Re- balanced:

preferences are

based on estimated

standard deviations.

In current version

national IO

tables(e.g., IDE/

JETRO) have

highest priority,

COMTRADE the

lowest

Notes: