ISDA Legal Guidelines for Smart Derivatives Contracts:

Foreign Exchange Derivatives

2

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Contents

Disclaimer .................................................................................................................................. 3

Introduction ................................................................................................................................ 4

The Over-the-Counter FX Market ............................................................................................... 5

Types of FX ............................................................................................................................... 6

Building the foundation for Smart Derivatives Contracts ............................................................11

Constructing Smart Derivatives Contracts for FX ......................................................................16

Valuations and Calculations ......................................................................................................17

Issues for technology developers to consider ............................................................................20

Settlement .................................................................................................................................32

Clearing ....................................................................................................................................37

Reporting ..................................................................................................................................37

Conclusion ................................................................................................................................39

Acknowledgement .....................................................................................................................40

3

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Disclaimer

The purpose of these guidelines is to provide an introduction to foreign exchange derivatives

(“FX”) for readers who are designing and implementing technological solutions for them. The

intention of this paper is not to specify or recommend any particular technological application or

project. Rather, these guidelines intend to provide an overview of the legal and documentary

framework used for FX transactions and to highlight certain issues that developers may wish to

consider. This paper is intended to help developers tailor appropriate technology solutions for the

FX market.

These guidelines discuss a number of legal issues. These discussions are intended to provide

general guidance, not legal advice, and to promote a better understanding of the basic principles

that underpin documentation produced by the International Swaps and Derivatives Association,

Inc. (“ISDA”). In practice, the law relating to derivatives transactions and the legal documentation

that governs them is complex, may change over time due to evolving case law and new

regulations, and may vary substantially from jurisdiction to jurisdiction.

In presenting this material, an assumption is made that certain terms in ISDA documentation

relevant to FX are capable of being (and may currently be) represented in computer code or

performed by or on a technology platform. For example, payment-related provisions that require

one party to pay another an amount that is calculated on the occurrence of a certain event may

be suited to codification or automated processing. This paper also assumes that some provisions

within such ISDA documentation may not be as well suited or efficient to code and will remain as

written in the contract.

These guidelines do not represent an explanation of all relevant issues or considerations in a

particular transaction, technology application or contractual relationship. These guidelines do not

constitute legal advice. Parties should therefore consult with their legal advisors and any other

advisor they deem appropriate prior to using any standard ISDA documentation. ISDA assumes

no responsibility for any use to which any of its documentation or any definition or provision

contained therein may be put.

Unless otherwise defined or the context otherwise requires, capitalized terms used in these

guidelines have the meanings given to them in the relevant ISDA document.

4

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Introduction

Since its foundation in 1985, ISDA has consistently sought to promote efficiencies and cost-

savings through improvements to processes for the settlement and management of lifecycle

events related to a variety of derivatives products. Today, as new technologies are developed and

implemented across the financial markets, the derivatives industry is increasingly seeking to

achieve even greater efficiencies and cost-savings through the deployment of such technologies.

In response, ISDA has published a series of Legal Guidelines for Smart Derivatives Contracts.

The purpose of these guidelines is to support technology developers and other key stakeholders

in the development of smart derivatives contracts by explaining the core principles of ISDA

documentation and raising awareness of the important legal and regulatory issues that developers

and other relevant stakeholders should consider when developing and deploying such solutions

within the derivatives market.

This paper builds upon the ideas examined in ISDA’s previously published papers to focus on the

application of such technology solutions to the FX market. These guidelines will:

• provide high level background on the FX market;

• identify opportunities for the potential application of smart contract technology to FX; and

• highlight important issues for technology developers to consider when designing technology-

enabled solutions for trading and processing FX and associated processes.

The significant size of the FX market and the fact that various aspects and features of FX lend

themselves easily to automation (as described further in this paper) means that there is a

significant opportunity for technology developers to create scalable solutions that can have a

significant impact on the broader derivatives market.

A number of technology-based initiatives working towards greater standardization and automation

of the FX market have already been developed and implemented. These include the electronic

trading and execution of FX and the application of data analytics, including pre-trade transaction

cost analysis.

1

In addition to these existing initiatives, there are opportunities to build further by harnessing new

technologies, such as smart contracts and distributed ledger technology (“DLT”), in order to

provide scalable, cost-efficient and more accurate technology solutions within the FX market.

While the intention of this paper is not to specify or recommend any particular approach or to

address any particular technological application or project, these guidelines seek to ensure that

the design and implementation of new technology solutions are consistent with existing legal and

regulatory standards. These guidelines also highlight areas where further industry collaboration

will be required to identify existing areas of legal and regulatory uncertainty and to develop

solutions.

1

See, e.g., https://www.r3.com/press-media/blockchain-leaders-join-forces-to-tackle-inefficiencies-in-the-global-fx-

market/

5

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

The Over-the-Counter FX Market

This section provides high-level background on the over-the-counter (“OTC”) FX market.

The FX market encompasses a wide variety of products, including FX swaps and FX forwards

(both deliverable and non-deliverable forwards). Fundamental FX elements are also found in

products like cross-currency swaps and cross-currency options (deliverable and non-deliverable).

Payment flows of FX contracts are determined primarily by reference to one or more rates of

exchange between currency pairs specified in the derivative contract. The value of the contract in

this context is often zero on inception, and fluctuates during the life of the transaction, primarily

as a result of movements in the rate of exchange. Payment flows may represent either the

exchange of one or more currencies against one or more other currencies (referred to as

‘deliverable’ or ‘physically-settled’), or settlement in a single currency of the difference in value

between the two or more currencies of the transaction, as determined on the valuation date based

on the rate(s) of exchange for the transaction (referred to as ‘non-deliverable’ or ‘cash settled’).

FX may be used by organizations to hedge their exposures to FX rate fluctuations, for instance,

where a party receives income primarily in one currency, but their expenses are paid in a different

currency. FX may also be used for other reasons, such as for speculative purposes. FX spot

transactions are used to purchase and settle foreign securities. If, for example, a U.S. based firm

that only has a U.S. dollar account wants to purchase a foreign (i.e., non-U.S.) security, that U.S.

firm must purchase the foreign currency in order to pay for the foreign security.

2

The FX market follows the interest rate derivatives (“IRD”) market as the second largest

derivatives product market, by various measures. As of the end of December 2019, the total gross

market value of FX contracts outstanding was approximately $2.2 trillion, which equates to about

19.1% of the gross market value of the OTC derivatives market.

3

The total notional amount of FX

outstanding as at the same time was approximately $92 trillion, corresponding to about 16.5% of

the total notional amount of OTC derivatives then outstanding (see Figure 1).

4

The daily turnover

of FX in April 2019 was $4.6bn, which equates to about 70.7% of the daily turnover of OTC IRDs.

5

2

Here, the FX transactions’ tenor and known currency has to mirror the foreign security, its denomination, and

settlement cycle.

3

https://stats.bis.org/statx/srs/table/d5.1

4

https://stats.bis.org/statx/srs/table/d5.1

5

https://www.bis.org/statistics/rpfx19_ir.htm

6

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Figure 1

Source: Bank for International Settlements semi-annual survey as of December 2019

6

Types of FX

There are different types of FX, including

7

:

• FX spot: A type of transaction that involves the payment of an amount in one currency against

payment of an amount in another currency at an exchange rate specified on the trade date,

for settlement that is typically T+2.

• Deliverable FX forward: A type of transaction that involves the payment of an amount in one

currency against payment of an amount in another currency at an exchange rate specified on

the trade date, for settlement on a specified future date that is beyond the time period typically

applying to spot transactions in the relevant jurisdiction(s) (for example, beyond T+2 business

days in some jurisdictions).

• Non-deliverable FX forward (“NDF”): A type of transaction that involves the payment of an

amount in a single settlement currency where the amount of the payment is determined by

reference to an exchange rate specified on the trade date, for settlement on a specified future

date (beyond the typical settlement cycle for spot transactions). Parties engage in NDF

transactions for a variety of commercial reasons, including in scenarios where at least one of

the currencies (other than the settlement currency) is subject to exchange controls or transfer

restrictions that apply to certain parties.

• FX swap: A type of transaction generally involving the exchange of amounts in two different

currencies on a specified date, or time, followed by reverse exchanges of amounts in the two

6

http://assets.isda.org/media/ce977683/d3c2a494-pdf/

7

It is appreciated that there are different interpretations in the market in relation to each of these types of derivatives

that may be applied in various different contexts. These definitions are intended to be representative examples

only, and are neither exhaustive in nature, nor strict technical definitions in the legal sense.

7

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

currencies at a later date. In each case, the exchange rate and settlement date are specified

on the trade date.

8

• Cross-currency swaps: An IRD type of transaction that, in addition to an exchange of

notional amounts in different currencies at the outset and a reverse exchange at the maturity

of the transaction, provides for periodic exchanges of amounts in each currency based on one

or more fixed and/or floating interest rates.

• Currency option: Under a currency option, the holder or buyer has the right (but not the

obligation) to either make or take delivery of one currency in exchange for taking or making,

respectively, delivery of another currency at a future date. The exchange rate is determined

on the trade date. As for other derivatives, there are a variety of possible option structures,

including deliverable FX and NDFs (i.e., respectively, involving an exchange of the relevant

currencies or settlement in a single currency), as well as structured or more complex options.

• Barrier FX option: A type of option under which the right to exercise the option may arise or

be extinguished, or the terms of which may change in some other pre-defined manner, upon

the occurrence of an event or condition (known as a barrier event) defined by reference to

observed values of one or more exchange rates during the term of the option.

• FX correlation swaps: A type of swap where each party agrees to pay to the other an amount

equal to a specified notional amount multiplied by the difference between a specified level and

the observed correlation between exchange rates for specified currency pairs over a specified

observation period.

• Variance-linked FX transaction: A type of transaction under which a “variance buyer” and a

“variance seller” agree to exchange payments based on the difference between (i) an amount

proportional to the observed level of variance (as defined under the terms of the variance

swap) of the exchange rate for a specified currency pair realized over a stated observation

period and (ii) a fixed amount of variance that is agreed upon at execution.

• Volatility-linked FX transaction: A type of transaction similar to a variance swap, except that

payments under a volatility swap are determined by reference to the observed volatility, rather

than variance, in the relevant exchange rate over the specified observation period.

• FX forward volatility transaction: A type of transaction in which the parties agree on the

trade date to enter into a “straddle” (a combination of a put option and a call option on a

specified currency pair, both of which are purchased by the same party (the option buyer)) on

a specified future date (the “reference date”) with terms that will be based on a volatility level

that is agreed by the parties on the trade date.

It is important to bear in mind that these descriptions of transaction types address the principal

payment flows arising under each transaction type. As a practical matter, except for FX spot

transactions, FX transactions are often not carried out to maturity, or to one or more relevant

8

An “in/out swap” in the CLS system is sometimes considered to be similar to an FX swap, but with a duration less

than one day.

8

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

payment dates, but are instead closed out or novated to another party, in exchange for a mark-

to-market payment.

The intention of parties entering FX transactions is not necessarily to take delivery of the relevant

currencies; instead, many transactions are entered into to gain economic exposure (whether for

hedging or other purposes) to fluctuations in the relevant FX rate during a certain period, after

which the aim is to crystallize or close out that exposure. This can be achieved in a variety of

ways, for example, by agreeing to terminate a transaction at a specified close-out price, or by

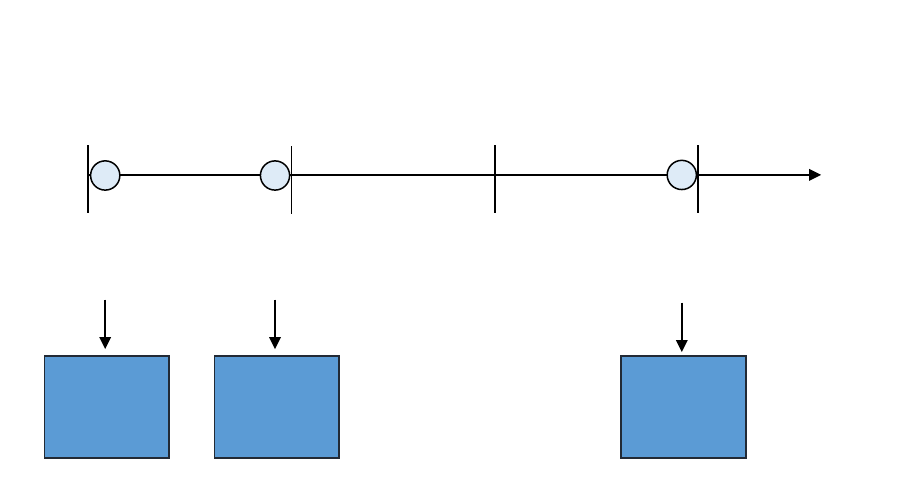

entering into an offsetting trade. We have shown below in Figure 2 one example of two offsetting

FX spot transactions entered into on the same trade date, where the currency fluctuation has

been favourable to Party A, thereby crystalizing a cash payment settled on T+2 (assuming multiple

transaction payment netting applies). It is also possible that the transactions settle gross, although

the economic effect will remain.

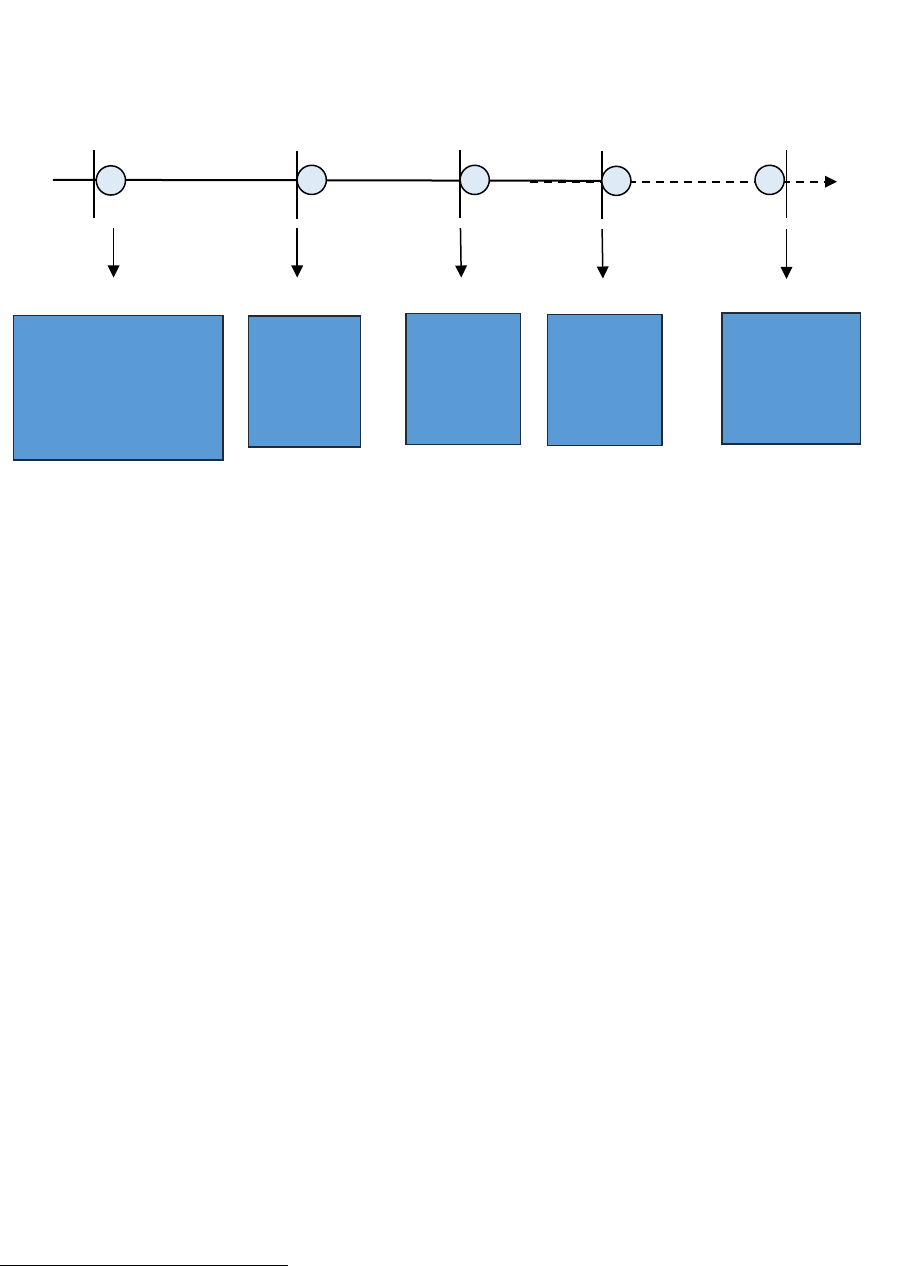

In other circumstances, rollover provisions may be included in an FX transaction (e.g., an FX spot

transaction, swap or FX forward), the effect of which is to replicate the economic effect of

periodically closing out the relevant transaction and then entering into a new transaction. The

effect is a periodic settlement of the transaction, with continuing economic exposure on the terms

agreed unless and until the transaction is otherwise terminated. This is illustrated by Figure 3

below.

Figure 2

Off-setting FX Spot Transactions

T

T+1

Business

Days

Party A

buys

EUR/USD

Party A

receives

EUR (net)

Trade 1

T+2

Trade 2

Party A

sells

EUR/USD

Settlement

9

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Deliverable versus non-deliverable FX

FX can be categorized as either deliverable or non-deliverable. Under a deliverable FX, the

transaction terms provide for an exchange of payments in each of the two currencies on the

settlement date(s).

Under an NDF, by contrast, the transaction terms provide for the payment of a cash settlement

amount in a single settlement currency on the settlement date in lieu of delivery of the notional

amounts of the bought and the sold currency. The cash settlement amount is determined by

multiplying the notional amount for the transaction by a ratio determined by reference to the

exchange rate for the contract and the realised exchange rate (referred to as the “Settlement

Rate”) at the relevant time of valuation. In this way, a single payment in the settlement currency

falls due on the settlement day, payable by one party. Some NDFs provide that each of the bought

and the sold currencies are converted into a third currency that serves as the settlement currency.

Cleared versus uncleared FX

The central clearing of derivatives has generally increased substantially in recent years, largely

as a consequence of policy responses following the global financial crisis. The FX market has,

however, been less affected by the rise of central clearing, as FX are not currently subject to

mandatory clearing in the European Union or United States and, as a consequence, clearing

services have tended to be developed by central clearing counterparties (“CCPs”) only for

voluntary clearing of NDFs. Accordingly, as of the end of December 2019, the notional amount of

foreign exchange contacts with a CCP was approximately 3.7% of the total notional amount of

foreign exchange derivatives then outstanding.

9

By contrast, the share of notional amounts of

9

https://stats.bis.org/statx/srs/table/d5.1

Figure 3

Rolling FX Spot Transaction

T

Business

Days

Party A enters into

a rolling FX spot

to buy EUR/USD

(with a one-day

rollover period)

T+10

Rollover

(new

trade

arises)

Termination

T+1

Rollover

(new

trade

arises)

Party A

receives

EUR

Settlement

Settlement

Rollover

(new

trade

arises)

Settlement

T+2

10

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

cleared IRDs was approximately 76.6% of the total notional amount of IRDs then outstanding, as

at the end of 2019.

10

The legal terms which govern the contracts for non-cleared and cleared derivatives can differ, as

can the processes, valuation, payment and delivery flows. This may give rise to certain additional

issues when considering the use of smart contract technology for other derivatives contracts.

However, this is likely to be less significant in the context of the current FX market, where fewer

derivatives are centrally cleared (as compared with other types of derivatives, notably IRDs or

credit default swaps).

Exchange-traded versus OTC FX

FX can also be traded on specific exchanges (and are therefore referred to as “exchanged-traded

derivatives”) rather than bilaterally between counterparties. Note that a detailed discussion of

exchange-traded derivatives is beyond the scope of these guidelines, though it is possible that

some of the technology solutions applicable to OTC FX could be applied to exchange-traded

derivatives as well.

Market evolution

Markets and market practices are continuously evolving in response to a range of factors,

including client demand. New products are being developed and old products may have certain

terms revised. Developers will therefore need to account for market evolution and to ensure that

technology solutions are capable of adapting to changing market practices.

The OTC FX market in particular is known for its flexibility and frequent innovation. While

benefiting from high levels of standardization, market participants can enter into highly bespoke

FX transactions, with features that allow those participants, for example, to hedge seamlessly the

risk of an equally bespoke cash product, such as a complex loan. While these bespoke

transactions are less common than more standardized products, initiatives to develop smart

derivatives contracts and digitize aspects of the FX market may benefit from taking these more

tailored and flexible transactions into account.

10

https://stats.bis.org/statx/srs/table/d5.1

11

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Building the foundation for Smart Derivatives Contracts

On 28th July, 2020, ISDA and several other trade associations sent a letter to the Financial

Stability Board, IOSCO and the Bank for International Settlements asserting our joint commitment

to defining and promoting the development of a digital future for financial markets.

11

The benefits

of digitization for market participants are clear. Increased and more widespread implementation

of automated, straight-through processing of financial transactions will increase efficiency and

reduce costs for market participants. Digitization will promote the consistent creation, processing

and aggregation of global financial data, bolstering regulatory oversight and compliance. Through

the removal of redundancy and unnecessary complexity, increased digitization and automation

will strengthen the operational resilience of market participants and financial markets

infrastructure, reducing systemic risk and creating a safer and more robust global financial

system.

None of this is possible without industry-led development of essential data standards and the

distribution of these standards in digital formats to allow direct deployment within enhanced,

automated and intelligent processes, systems and technology.

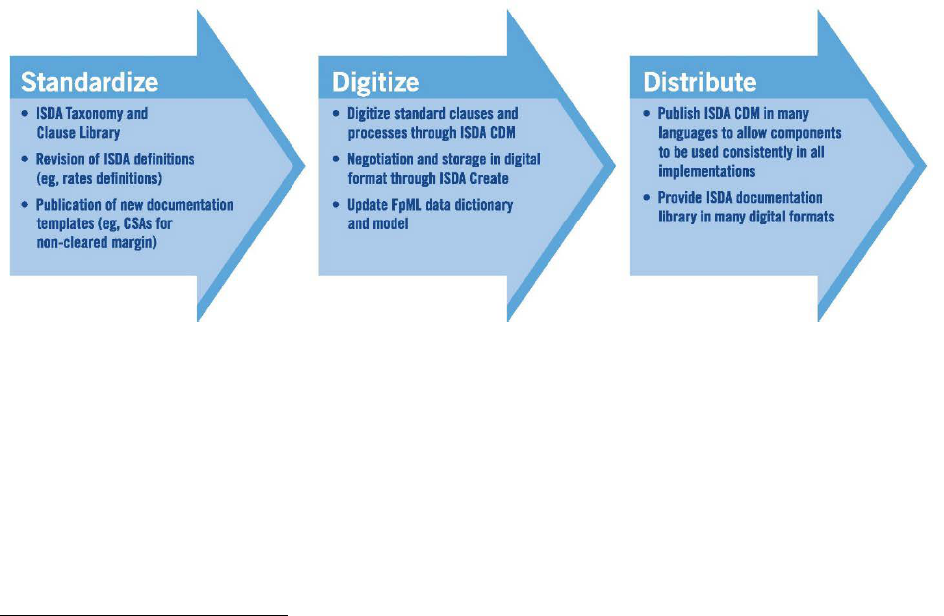

The letter sets out a series of principles and objectives aimed at promoting the development,

distribution and adoption of digital standards within the financial markets, creating the foundation

for transformational change in our industry. These principles and objectives address three key

areas: Standardization, Digitization, and Distribution.

Figure 4: ISDA’s Digitization Initiatives

Standardization

Expanding ISDA’s digital offering across our suite of actively negotiated documentation requires

enhanced standardization of those documents. Firms will always need to negotiate and customize

documentation to address specific commercial, compliance, legal and operational risks. However,

excessive customization can increase complexity and on-boarding times, while providing little or

no commercial or legal benefit. A lack of standardization therefore gives rise to operational

11

https://www.isda.org/a/MGmTE/Digital-Future-for-Financial-Markets-Letter.pdf

12

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

inefficiency, increases risk through unnecessary complexity and creates impediments to

digitization.

In response, ISDA has developed the ISDA Clause Library. The ISDA Clause Library effectively

deconstructs the standard legal document and assigns meaning to the various different

obligations and events expressed within it. Using thousands of agreements and clause samples,

we identified, defined and categorized the most commonly negotiated clauses within the ISDA

Master Agreement and various credit support documents. Having established this framework, we

created standard-form drafting options that are capable of achieving the vast majority of the most

commonly negotiated outcomes within standard-form ISDA documentation. This standard-form

wording is now available for use by market participants in their negotiations.

12

The Clause Library will also be integrated within ISDA Create, ISDA’s digital negotiation and

execution platform, when the ISDA Master Agreement is added to the platform. ISDA Create is

an online solution that allows firms to produce, deliver, negotiate and execute derivatives

documents completely online. The system captures, processes and stores legal data from these

documents in a structured standardized format, which provides users with a complete digital

record, but more importantly, allows easy automated integration with other systems to facilitate

seamless information flows and remove the need for post-execution transfer of data (and the

chance of error during such a data transfer).

FX documentation

The 1998 FX and Currency Option Definitions published by ISDA, Emerging Markets Traders

Association (“EMTA”) and the Foreign Exchange Committee (the “1998 FX Definitions”), as

updated from time to time, provide standard definitions for use by market participants in

documenting privately negotiated FX and currency option transactions. The 1998 FX Definitions

are intended for use in confirmations and allow parties easily to specify standard economic

features of trades and to allocate various risks associated with the occurrence of certain trade

events that are reasonably likely to affect FX and currency options. As for other ISDA definitional

booklets, the 1998 FX Definitions are, therefore, available prior to the point in time at which parties

transact. This may present certain opportunities in the context of technology platforms seeking to

automate or address within the platform the concepts referred to in the 1998 FX Definitions. As

described further in the section below entitled “Issues for technology developers to consider”, this

may present certain challenges, including with regard to the interpretation of the 1998 FX

Definitions, and ensuring consistency where appropriate, both internally to the platform and

across the market.

Standard forms of confirmations have also been published by EMTA and ISDA for NDFs as well

as supplemental provisions to the definitions for specific currencies and FX products, including,

for instance, the Non-Deliverable Cross Currency FX Transactions Supplement published in May

2011, the 2005 Barrier Opinion Supplement, and the September 2019 Averaging Supplement.

These confirmations are generally used when documenting currency transactions involving

certain emerging market currencies and allow parties to allocate risks associated with the

12

The ISDA Clause Library currently covers the ISDA Master Agreement. The Clause Library will be expanded to

cover various ISDA credit support documents in 2021. More information: https://www.isda.org/2020/06/23/isda-

launches-clause-library/

13

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

occurrence of certain trade events that are reasonably likely to occur in a specific country and

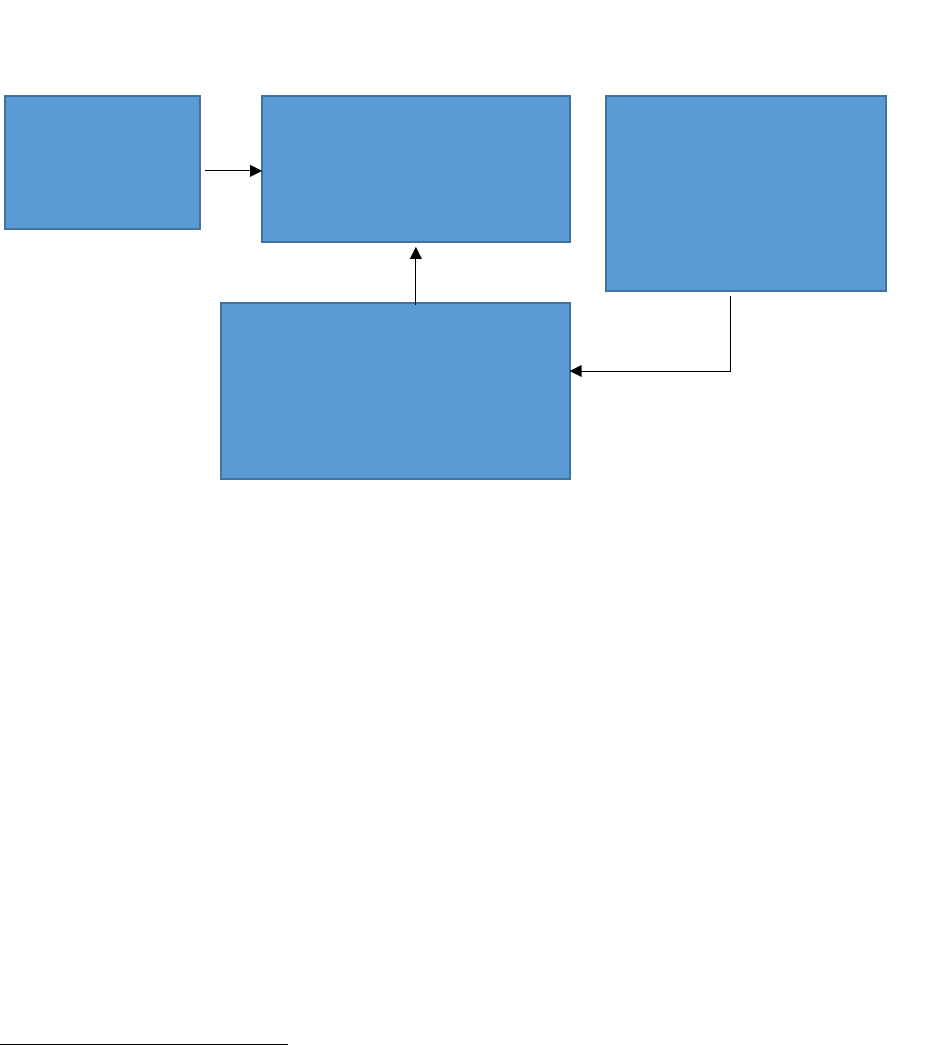

with respect to a related currency pair. We show in Figure 5 how the definitions and supplements

are often applied to a transaction. The ISDA documentation architecture, and considerations in

relation to smart contracts, are also described further in ISDA Legal Guidelines for Smart

Derivative Contracts: Introduction

13

.

The ISDA legal architecture and considerations set out in the ISDA Legal Guidelines for Smart

Derivative Contracts: The ISDA Master Agreement

14

will also be relevant to the FX market. While

the ISDA Master Agreement (and related ISDA published documentation used to document FX,

as described above) is standardized, market participants do negotiate and amend these

documents bilaterally. There are, however, certain amendments that are made, and provisions

added to, ISDA Master Agreements on a relatively regular basis, including, for example, amending

the ISDA Schedule to incorporate FX transactions and currency options within the scope of the

ISDA Master Agreement or adding language relating to the exercise of currency options, netting

of certain offsetting currency option transactions or the payment of currency premium. However,

the exact drafting used by market participants often differs based on differences in drafting style,

rather than commercial intent. As discussed further above, ISDA is engaged in the ISDA Clause

Library Project to encourage the further standardization of derivative transaction terms, including

FX transactions, where appropriate.

The range of documentation available has promoted standardization in the FX market. In this

context, smart contracts offer a viable opportunity to automate many of the processes involved in

the negotiation and documentation of FX. FX confirmations, for instance, which contain the

commercial and economic terms relating to the transaction, may be automated through smart

13

See ISDA, “Legal Guidelines for Smart Derivatives Contracts: Introduction” available at:

https://www.isda.org/a/MhgME/Legal-Guidelines-for-Smart-Derivatives-Contracts-Introduction.pdf

14

See ISDA, “Legal Guidelines for Smart Derivatives Contracts: The ISDA Master Agreement” available at:

https://www.isda.org/a/23iME/Legal-Guidelines-for-Smart-Derivatives-Contracts-ISDA-Master-Agreement.pdf

Credit Support

Documents

Master Agreement

•

1992 Master Agreement

(Multicurrency – Cross border) /

2002 Master Agreement

•

2002 Master Agreement Protocol

Confirmations

•

ISDA Long-form confirmations

•

Short-form confirmations

•

Master Confirmation Agreements

•

EMTA Template Terms

Definitions

•

1998 FX and Currency Option

Definitions

•

2006 Definitions

•

Supplement to 1998 FX and

Currency Option Definitions

FX and Currency Options Documentation Architecture

Figure 5

14

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

contracts. The payment obligations contained within these confirmations could be implemented

as separate pieces of smart contract code. Other obligations related to the economic terms of the

confirmation may also be smart contract coded.

Digitization

ISDA is currently working to provide all of its documentation in digital format. ISDA’s flagship digital

offering is the ISDA Interest Rate Derivatives Definitions, a revised and updated definitions

booklet for use with IRDs. Alongside necessary updates and adjustments to take account of

market evolution and global benchmark reform efforts, a key driver for this project is making the

standardized interest rate definitions more user- and technology-friendly.

15

The ISDA Interest Rate

Derivatives Definitions will be produced in a digital format, allowing for the production and

maintenance of a consolidated and up-to-date view of the definitions, rather than requiring users

to compile paper or pdf copies of the main definitional booklet and up to 70 amending supplements

in order to understand the terms which apply to their trades (as is the case with the current 2006

ISDA Definitions). ISDA will deliver the ISDA Interest Rate Derivatives Definitions through an

online platform, increasing accessibility and incorporating various built-in functionalities and

capabilities, such as hyperlinking and version-control to provide a more user-friendly

experience.

16

Standardization and digitization of documentation is only half the battle. There is also a lack of

common data and process standards, and little alignment between these standards and the

underlying documentation. Firms and infrastructure providers typically use their own unique set

of representations for transaction events and processes. As a result, market infrastructure is

inefficient and expensive.

ISDA supports the development of common, interoperable industry standard models for financial

transactions and processes. The ISDA Common Domain Model (“CDM”) establishes a common,

digital representation of derivatives trade events and actions and creates a common set of

process and data standards that will increase automation and efficiency in the derivatives market.

This model can be easily expanded to cover additional products and contracts as a means of

encouraging further standardization across the financial markets. Indeed, the International

Securities Lending Association (“ISLA”) is currently working to model and code specific securities

financing transaction components for inclusion in the CDM, creating greater alignment between

derivatives and securities lending markets.

17

15

Amongst other things, the following approaches have been adopted:

(i) simplifying and standardizing sentence and paragraph structures (e.g., by making sentences shorter and

splitting detailed paragraphs into multiple limbs);

(ii) streamlining definitions (e.g., by deleting duplicate definitions);

(iii) using formulaic expressions where possible (e.g., in the context of day-count fractions and compounding

provisions); and

(iv) using binary or conditional language that can more easily be understood and converted into code by

technology developers.

16

See ISDA, “Legal Guidelines for Smart Derivatives Contracts: Interest Rate Derivatives” available at:

https://www.isda.org/a/I7XTE/ISDA-Legal-Guidelines-for-Smart-Derivatives-Contracts-IRDs.pdf

17

See https://www.isda.org/2020/07/27/isda-and-isla-agree-to-closer-collaboration-on-digital-initiatives/

15

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Distribution

Critical to the success of these efforts will be the extent to which market participants can easily

access and benefit from these new standards. Fragmented and duplicative distribution of digital

offerings will inevitably result in incompatible platforms and solutions. This will increase

inefficiency and the cost to the market. We will therefore ensure that our standards and the

digitized representation of these standards are made available in a way that promotes

competition, encourages innovation, and facilitates the development of mutualized technology

solutions within our markets.

Refinement and expansion of these models will facilitate greater connectivity between contractual

terms and the processes designed to implement important business and operational functions

deriving from contracts, including netting and collateral enforceability, liquidity, and counterparty

credit-risk. All of this will help move the industry towards more efficient, cost-effective and scalable

payment, settlement, collateral management and regulatory processes, providing a robust

foundation for straight through processing of financial transactions.

These enhanced standards will enable the development and implementation of innovative new

automated and intelligent technology solutions. For example, common, shared representations of

data are required in order for distributed ledger technology to operate effectively. Equally,

platforms such as ISDA Create, which capture structured data at the point of origination, that is,

in legal documentation entered into electronically from the outset, further facilitate convergence

on common standards, and the distribution of standardised data, thereby greatly increasing

efficiency across the industry.

These developments facilitate the development and deployment of common processes across

different market players; taken a stage further, in the case of distributed platforms, they also

facilitate smart contracts to be developed and deployed across the market. The aggregation of

large, structured data sets will also accelerate the use of AI-based technology solutions, with

potential applications across numerous business, risk management and regulatory compliance

functions.

Using these enhanced standards as a foundation, technology developers can then deploy

automated business logic in a way that draws upon the ISDA CDM to facilitate specific

functionality. One straightforward, but compelling, example of the application of smart contract

technology which utilizes the ISDA CDM would be the automation of the calculation and triggering

of the payment of a settlement amount under an FX transaction between two counterparties who

would otherwise rely on their own internal data models and, often, manual processes and

messaging, in order to reconcile and settle the trade.

16

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Constructing Smart Derivatives Contracts for FX

In October 2018, ISDA and King & Wood Mallesons jointly published a white paper entitled “Smart

Derivatives Contracts: From Concept to Construction”.

18

This paper proposed a practical framework for the construction of smart derivatives contracts.

As part of this framework, the paper suggests that a key step toward the construction of a smart

derivatives contract is the selection of those parts of a derivatives contract for which automation

would be:

• Effective, which involves determining which parts of a contract it is possible to automate;

and

• Efficient, which involves determining which of those parts where there is sufficient benefit

in automating.

Effective Automation

In 2017, ISDA and Linklaters jointly published a white paper entitled “Smart Contracts and

Distributed Ledger – A Legal Perspective.”

19

This paper notes that derivatives are fertile territory for the application of smart contracts and DLT

because their main payments and deliveries are typically operational in nature, and thus heavily

dependent on conditional logic. As a result, they are highly suitable to being machine-automated

or analysed in some way. The paper illustrates how these operational provisions can be

expressed in a more technology-friendly form, broken down into components for representation

as functions within the ISDA CDM) and then combined with other functions into templates for use

with particular derivatives products.

20

The Smart Derivatives Contracts: From Concept to Construction paper notes that there are

examples throughout the 2006 ISDA Definitions of such operative clauses, including Section 5.1

which sets out how to determine the fixed amount payable by the fixed rate payer. The paper then

illustrates how this provision can be expressed in a more technology-friendly form, broken down

into components for representation as functions (within the ISDA CDM) and then combined with

other functions into templates for use with particular derivatives products, such as FX.

18

See ISDA’s White paper on “Smart Derivatives Contracts: From Concept to Construction” available at:

https://www.isda.org/a/cHvEE/Smart-Derivatives-Contracts-From-Concept-to-Construction-Oct-2018.pdf

19

See ISDA, Smart Contracts and Distributed Ledger: A Legal Perspective” available at:

https://www.isda.org/a/6EKDE/smart-contracts-and-distributed-ledger-a-legal-perspective.pdf. ISDA, along with

Clifford Chance, R3 and the Singapore Academy of Law published a whitepaper that provides analysis on the legal

issues relating to the use of smart derivatives contracts governed by the laws of Singapore and England and Wales

involving distributed ledger technology (“Private International Law Aspects of Smart Derivatives Contracts Utilizing

DLT”, available at: https://www.isda.org/2020/01/13/private-international-law-aspects-of-smart-derivatives-

contracts-utilizing-distributed-ledger-technology/). Whitepapers considering these issues for contracts governed

by the laws of other jurisdictions are forthcoming.

20

See also ISDA, Legal Guidelines for Smart Derivatives Contracts: Introduction available at:

https://www.isda.org/a/MhgME/Legal-Guidelines-for-Smart-Derivatives-Contracts-Introduction.pdf

17

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Efficient Automation

There are a number of areas within the FX market where greater automation can deliver

considerable efficiency benefits.

There are a number of observed pain points in the current processes associated with FX. These

include:

• repetitive processes that are inefficient and costly;

• challenges with resolving disputes in a timely fashion; and

• slow and ineffective valuations and transfers of payments and assets.

As mentioned above, the operational processes involved in valuing, calculating and settling

payment and delivery obligations are likely to lend themselves well to automation and to deliver

real efficiencies and cost-savings as compared with existing payment infrastructures. These terms

are generally contained in the trade confirmation for the relevant transaction, which sets out the

economic terms thereof and typically incorporates the 1998 FX Definitions.

21

Additionally, the impact of regulatory change on the FX market – particularly with respect to

transaction reporting – has caused firms to implement new or amended processes across the

front-to-back transaction lifecycle in order to ensure ongoing regulatory compliance. There are

opportunities for greater efficiencies and cost-savings in these areas, some of which can be

achieved through greater automation.

These guidelines will discuss each of these areas below, identifying opportunities for greater

automation and highlighting key considerations for technology developers who are creating

responsive technology solutions.

Valuations and Calculations

Calculation of amounts payable on settlement date

A key process in the context of FX is the calculation of the amount which is payable under the FX

transaction. As the calculation is primarily based on currency exchange rates, there is a

compelling use-case for automation, given that the process is easily translatable into code.

FX swap

As noted in Types of FX on pages 6 and 7 above, an FX swap is a derivative transaction that

involves the parties’ exchange of payments in each of the two currencies at the execution of the

swap and on the maturity date, specified in the future at a fixed rate agreed upon on the inception

of the transaction. On the settlement date, each counterparty pays the amount specified as

payable by it in the confirmation to the transaction, based on the foreign exchange rate previously

agreed between the parties in the confirmation.

21

Where provisions do not lend themselves easily to automation, developers may consider adopting a hybrid

approach, which involves integrating smart contract technology with paper-based documentation, until such time

that more sophisticated smart contracts are developed that can cater for more complex provisions.

18

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

FX forward and spot

For FX forwards, as we note above, the exchange of two different currencies occurs on a

settlement date specified in the future at a fixed rate agreed upon on the execution of the

transaction. In the case of an FX spot transaction, one currency is exchanged for another on the

settlement date, typically T+2.

Non-deliverable forwards

As noted above, under an NDF, by contrast, the transaction terms provide for the payment of a

single cash settlement amount on the settlement date in lieu of payment of the notional amounts

of the bought and the sold currency. The economics in a single settlement currency of a cash

settlement transaction are intended to reflect those of deliverable transactions, but without the

exchange of currencies. Cash-settled transactions are often seen in circumstances where non-

deliverable currencies (typically, emerging market currencies) are involved – for example, due to

existing currency exchange controls.

The cash settlement amount is determined by converting the notional amount of one of the

currencies into the other currency at a spot FX rate that is either negotiated as the rate at the

time, observed from a pre-agreed pricing source, or determined using another pre-agreed method

on a date prior to the settlement date, and comparing this with the amount that would have been

payable based on the rate agreed between the parties at the time of trading. A single payment

obligation then arises, in the amount of the difference between the two currency amounts. That

amount is payable by the party owing the excess in the settlement currency on the settlement

date.

Pursuant to the 1998 FX Definitions, the single cash settlement amount is calculated as follows:

Settlement Currency Amount = Notional Amount x (1 – [Forward Rate / Settlement Rate])

where:

“Settlement Currency Amount” is the net cash settlement amount;

“Notional Amount” is the aggregate principal amount in respect of which cash settlement

amount is being calculated;

“Forward Rate” is the currency exchange rate agreed between the parties at the time of

trading, expressed as an amount of one of the currencies that can be purchased for one

unit of the other currency that parties have designated as the “Settlement Currency” in the

confirmation for the FX transaction; and

“Settlement Rate” means, unless specified by the parties in the confirmation, the spot rate

for foreign exchange transactions in the relevant currency pair for value as determined at

the time of settlement on the settlement date (generally by the Calculation Agent (as

defined in paragraph (iii)(a) (Calculation Agent discretion) below)).

19

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

We have considered in Figure 6 below the operation of an FX swap, a deliverable FX forward, an

NDF and an FX spot.

Figure 6

Execution:

Maturity:

##

ISSUER/ COMPANY

NDF: one-way payment

in settlement currency

FX swap, deliverable

forward and spot: parties

exchange Pound Sterling

and U.S. Dollars at

previously agreed rate

SWAP COUNTERPARTY

ISSUER/ COMPANY

FX swap: parties exchange

Pound Sterling and U.S.

Dollars

SWAP COUNTERPARTY

Deliverable forward, NDF

and spot: exchange rate

agreed but no exchange of

currencies

20

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

Issues for technology developers to consider

We have considered below some key issues that technology developers should be mindful of

while designing smart contracts for FX markets. These are not exhaustive of all such

considerations; in particular, as for other derivatives markets, there are a wide variety of product

types traded on the FX markets. There are also a number of existing technologies in the FX

markets that should be considered when considering the development of smart contract solutions.

Ultimately, any DLT or other technology platform in this context will need to take into account

specificities such as these given the commercial context within which it seeks to operate.

(i) Product-related considerations

The focus of automation should not always be on standardization. It is important to have

regard to the broad variety of FX products, and the significant variance in their features.

This is a key factor for developers to bear in mind while designing FX technology platforms.

There are standard FX derivatives, like plain vanilla swaps, as discussed at Types of FX

on pages 6 and 7 above, that are more amenable to automation as compared to bespoke,

exotic or heavily negotiated derivatives. Developers will have to consider how technology

platforms can reflect the variety of FX products that are on offer and ensure that the

platforms are structured carefully to complement each product’s specific features and

related market characteristics.

We consider below some important or common features and examples of FX products to

exemplify this point.

a. Rollover provisions

As noted elsewhere in this paper, rollover provisions are a common feature of the FX

markets, and are intended to replicate the economic effect of periodically closing out

one transaction at the closing rate on the relevant day, and entering into a new

transaction on the same terms. The effect is that there is periodic settlement of the

transaction, but the economic exposure continues until otherwise terminated. Although

there are different ways of achieving this contractually, each with different effects, this

type of “rollover” is frequently automatic, with a periodicity specified contractually,

unless one of the parties exercises a termination right.

Given that these types of provisions are common amongst market participants in the

FX market, and are amenable to automation, technology developers should be mindful

of this feature in the context of FX transactions. In particular, it is important for any FX

smart contracts solution seeking to accommodate such a feature to be sufficiently

flexible to cater for the exercise of discretion, in particular as to whether the rollover

should continue, or whether a termination right should be exercised.

b. Basis risk in hedging

FX is used by a wide variety of market participants for hedging purposes, in particular

to hedge exposure to foreign exchange rate fluctuations where participants realize

income and pay expenses in different currencies. By way of example, a company may

21

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

pay its employees in U.S. Dollars, but have projected earnings in Japanese Yen based

on its product market being Japan. In such a case, the company may wish to hedge

its projected earnings in Japanese Yen against a forward U.S. rate. This allows the

company to manage the risk of unfavourable FX rate movements when effecting a

conversion.

A key concern in the FX market has been to avoid or minimize basis risk which arises

where there are inconsistencies between the FX transaction and related exposure

being hedged (whether a company’s cash flow or a financial instrument, for example),

or which otherwise result in unmatched payment flows. The application of smart

contract technology to the FX market will need to bear in mind this key commercial

purpose in the FX markets and automated processes will need to be developed in a

way which does not give rise to such basis risk and which seeks to minimize it to the

extent practicable.

Basis risk may arise in a number of ways, including where (i) in the context of NDFs,

differences arise between the conversion rate determined under the NDF and the

actual conversion rate, (ii) there is a potential disruption event the published rate may

not be representative of the actual spot rate, (iii) there are differences between any

part of the calculation methodology, (iv) differences arise in the fallbacks which apply

where a calculation cannot be made, or (v) the timings for payments of foreign

exchange amounts differ. Not all instances of basis risk may be relevant in the context

of technology platforms; however, any form of basis risk that is relevant is an important

source of unforeseen FX risks.

A number of the market conventions described in these guidelines for the calculation

of FX amounts (e.g., Business Day Conventions), and the discussion around fallbacks,

apply widely in the financial markets. Consistent implementation of these conventions

in automated systems, or effectively permitting human intervention, is therefore

important to ensure market participants minimize basis risk. As noted elsewhere in this

paper, smart derivative contracts can be designed to, for instance, allow parties to

agree changes or fallbacks outside the smart contract through in-built override

mechanisms which permit manual intervention.

A separate, but related, aspect worth noting in the hedging context is the potential

application of smart contract technology for hedge accounting purposes. Favourable

accounting policies apply to certain types of hedges but identifying qualifying trades

through manual processes can be challenging. Businesses could benefit considerably

from the efficiencies offered by smart contract technology in this respect.

c. Exotic FX options: barrier options

There are many forms of exotic FX options, the features of which may need to be taken

into account in the development of any technology platform. Given that exotic FX

transactions are frequently bespoke, we consider one example, namely barrier

options. Barrier options are a type of option on currencies where, upon the occurrence

of a specific event or condition (known as a barrier event), a right to exercise the

22

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

transaction may arise (or be extinguished) or the underlying terms of the transaction

may be modified in some pre-defined way. A barrier event is typically determined by

reference to some observed event, such as a change in the exchange rate. For

example, the parties may agree that a barrier event will occur when an exchange rate

reaches or passes through a pre-agreed level or price.

A designated party (typically the Calculation Agent) may be designated to determine

when a barrier event has taken place. Smart contracts could be used to automate the

determination as to when a barrier event has occurred. It is worth noting that barrier

events may occur unexpectedly, and it may not always be clear to both parties that a

barrier event has actually occurred.

22

A smart contract solution could address this

asymmetry by monitoring when a potential barrier event has occurred and notifying

the counterparties at the same time.

(ii) Market-wide considerations

a. FX prime brokerage

The FX prime brokerage market presents a good use-case for a scalable application

of smart contract technology.

Use of prime brokerage services is very common in the FX industry, particularly by

hedge funds and commodity trading advisors. Prime brokers effectively act as

intermediaries in the trading and settlement process, offering services such as portfolio

and collateral management, custody, access to liquidity and consolidated settlement,

clearing and reporting processes.

The structure involves clients entering into a ‘prime broker agreement’ with the

intended prime broker, which has various ‘give up agreements’ with executing dealers

in the market. The arrangement allows the client to enter into transactions with the

executing dealers which are then ‘given up’

23

to the prime broker for clearing and

settlement.

As the give-up process involves various steps and a number of different

counterparties, significant operational efficiencies may be realized from the use of

smart contract technology, which can provide seamless end-to-end interoperability

across transactions using integrated, automated systems that foster more effective

and efficient settlement, valuation and ‘give-ups’ across transaction legs. This process

currently involves considerable costs and operational burdens at present, as it is

mainly manual in nature. Use of smart contract technology may therefore also help

reduce the fees and compensation spreads charged by prime brokers who provide

such services.

22

For example, depending on the terms of the transaction and supporting documentation, the determination may be

based upon information available to the Calculation Agent that is not available to the counterparty at the same

time.

23

This precise legal mechanics of the “give up” arrangement may vary depending on the nature and structure of the

arrangements, although the essence of the arrangement is that the prime broker enters into transactions on the

instructions of the client.

23

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

b. Use of Oracles

A key data source for FX is the currency exchange rate that is generally specified by

the parties to the FX transaction in the confirmation. As discussed above, where a

relevant currency exchange rate is unavailable, the 1998 FX Definitions provides

fallbacks.

The use of foreign exchange rates may offer a specific use-case for third-party

oracles

24

or external data sources in the automation process. Smart derivatives

contract models in the context of FX are likely to involve the use of such data providers.

Careful consideration must be given to the choice of such data providers, as a fully

automated process will rely on them for accurate data. Careful consideration should

also be given as to the liability framework in relation to the provision of data and the

role of any oracle, given the increased level of automation expected in this context,

and in particular where that automation involves any straight-through-process or has

a direct impact on the performance of payment or delivery obligations, where

significant risks may arise in the event of data inaccuracies or other failures of a data

provider or oracle.

Therefore, while automation involving oracles could provide significant benefits, a key

issue will be how the relationship between the oracle and the relevant systems should

be managed. An alternative mechanism will likely need to be provided for where there

is an interruption in the feed from the oracle due to, for example, a technology or coding

error (including in relation to reliance on a specified oracle), whether this is a fallback

to manual processes or an alternative screen mechanism. Further, foreign exchange

rates may be adversely affected where there are material changes to the methodology

applied by an administrator of a price source, unannounced government intervention

or other actions of unauthorized third parties. Careful consideration will have to be

given to how such risks can be mitigated and/or resolved subsequently. The extent of

a DLT platform administrators’ powers to modify or replace existing methodology

(including whether this will require participants’ consent) in the event of such

disruptions is another relevant issue that will have to be considered in this context.

It may also be appropriate to consider whether and how these disruptions and other

issues involving oracles and other data providers to the system will interact with the

existing fallbacks in the 1998 FX Definitions and whether new tailored fallbacks may

be required to address novel issues that arise in the context of these new technologies.

24

To execute automatically, smart contracts need to be able to interface with data in the wider world. For example,

a piece of conditional logic that depends on whether a particular stock price has reached a certain level would

require the smart contract to be able to ascertain that stock price. To do this, it can look up the stock price from a

separate data source, typically known in the distributed ledger community as an ‘oracle’.

24

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

c. Interoperability

A smart contract solution may face significant challenges with respect to cross-

jurisdiction interoperability and settlement. While the standardization of FX transaction

documentation promotes interoperability, smart contracts which use a particular

technology must also be interoperable across other technologies. Further, the smart

contract must also be accessible to the wide variety of FX market participants (as well

as infrastructure providers and regulators) and interoperable with the data feeds that

will inform the FX contract.

Standards, accordingly, should be developed to ensure interoperability across different

implementations. ISDA can play a role in unlocking the value of smart contract

technology by encouraging and facilitating the development of such standards.

Developers should also consider how to ensure compliance with standards where they

have already been established, for example, by governments and regulators in various

jurisdictions.

Consideration will also have to be given to the development of appropriate formats

that allow platforms to integrate with firms’ internal systems, including booking and

other related systems (such as collateral and other risk management systems) which

vary from institution to institution. Post-trade process also require appropriate

messaging and data formats capable of standardization across different jurisdictions,

platforms and market participants (including various counterparties, external data

providers, regulators, benchmark administrators, CCPs, other financial market

infrastructures and payment providers). In this context, developers may wish to study

closely how extant technology (such as SWIFT) functions in the market, as well as

which functionalities can be adopted and which ones could be improved, in designing

and developing new technology. In this respect, developers should be mindful that

adoption of these technologies is not universal, so solutions that build upon them may

not be feasibly applied to all market participants.

d. Market Monitoring

The FX industry has implemented the FX Global Code

25

, in response to practices that

have emerged in FX markets. The FX Global Code is a set of principles of good

practice that firms subscribe to, and many of the largest market participants have

signed a statement of commitment to the Code, including in relation to their FX market

activity.

As an example, Principle 10 states that market participants must handle orders fairly,

such as how to fill or partially fill client orders in different situations, and how to make

that transparent to clients.

Developers and market participants may be required to consider whether some of the

Principles of the Code could be implemented in their systems, what the benefits and

25

https://www.globalfxc.org/docs/fx_global.pdf

25

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

trade-offs would be to implement it in this way, and whether a distributed system could

be beneficial.

e. Harmonized interpretations

Industry harmonization leads to greater standardization and predictability in the market

and is a crucial prerequisite to digitization and automation. However, it should also be

acknowledged that market participants have developed firm-specific or proprietary

methods and preferences for various stages of the calculation process (e.g., discount

factors that apply to determine the settlement amounts upon termination) and may see

certain advantages to retaining discretion in this regard. While there is clearly merit in

retaining some element of individual discretion in performing the calculations since it

allows for a more fact-dependent response to a particular event, this also makes it

difficult to implement standardized market-wide approaches in a way that is beneficial

for digitization. Discretion should therefore be maintained for business processes

where users disagree about the right outcomes or methods, to preserve the value of

bespoke negotiated outcomes. The application of smart contract technology to FX

transactions may, therefore, be complicated by the differences in approach to the

calculation process. Nevertheless, where different language is used to describe the

same business process or calculation, this should be standardized where possible to

further promote automation.

f. Consistency across markets

While paragraph (ii)(e) (Harmonized interpretations) above addressed the

considerations involved in standardizing data points, methods and processes within

the FX market, a further point to bear in mind is the need, in some instances, to also

ensure harmonization across markets. There are a number of areas in which, for

instance, IRD and FX markets may wish to maintain consistency (including to assist

in minimizing hedging risk). Examples include, amongst others, harmonized meanings

of Business Days and Business Day Conventions, day count-fractions, benchmark

provisions and fallbacks and the treatment of IRDs in the context of disruption events.

Technology developers ought to bear in mind, therefore, that different types of

derivative products cannot be considered in isolation, as there is a significant amount

of interaction between the different markets (including beyond derivatives markets),

and in particular, between the FX and IRD markets. Conceptual or operational changes

in one market may therefore have a material impact on other markets and market

participants are often heavily focused on such changes, particularly where their

internal systems are built for cross-product usage. Socialization of anticipated changes

on a larger scale would therefore be preferable, and in some cases necessary, in the

context of new technologies. Industry associations like ISDA can play a key role in this

context to coordinate, encourage and facilitate engagement across market

participants.

26

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

(iii) Transaction-specific considerations

a.

Calculation Agent discretion

Consideration will need to be given to the position where there is an issue with the

automated calculation process, including where an unforeseen issue arises – for

example an unplanned bank holiday on which the key market is closed and no

Business Day Convention is specified or deemed to apply, an exchange rate is not

published when expected, or some question of interpretation of the 1998 FX

Definitions arises because of particular circumstances which have not been

encountered previously. It is often the case for an FX transaction that the party

designated as the “Calculation Agent” will step in to help determine the foreign

exchange amount payable in circumstances where there are issues (e.g., if the spot

rate is unavailable, the Calculation Agent may determine the applicable rate acting in

good faith and a commercially reasonable manner). In a recent example, during the

Argentina USD/ARS Exchange Rate Divergence (a term defined in previously used

EMTA template terms that many parties use to document USD/ARS NDFs), parties

found that there was a need for Calculation Agent determination where the Exchange

Rate Divergence occurred beyond the maximum number of days for postponement

specified for the transaction. As a result of the imposition of various capital controls

limiting foreign investors’ access to U.S. Dollars, there was an increasing divergence

between the prevailing Argentine Peso bid and offer rates for certain transactions in

the Buenos Aires marketplace and the settlement rate option of ARS NDF contracts.

Such circumstances requiring intervention outside of usual processes can and do arise

from time to time in highly complex markets.

Separately, one might also find scenarios in which Calculation Agent determinations

are required in the ordinary course of business, as part of its normal contractual

obligations. An example is where the FX contract permits the Calculation Agent to

determine the applicable exchange rate – for instance, by reference to rates

observable in the spot market, rather than rates derived from a rate source. Automation

and digitization will have to accommodate such discretions allowed for Calculation

Agents.

There is a risk of disputes arising in relation to Calculation Agent determinations. Any

application of smart contract technology must also be able to adapt to such dispute

resolution mechanisms (and their outcomes). One way of doing this may be to include

override provisions that will allow divergences from automated processes.

b. Collateralized transactions

Though not unique to FX alone, developers have to be mindful that parties to FX may

be required by regulation, or may prefer for risk management purposes, to collateralize

their outstanding obligations to each other. Developers will therefore be required to

have an understanding of the collateral arrangements and infrastructure relating to the

FX. They will also need to appreciate how calculations of the total amount of collateral

that is required to be transferred from time to time (which will be determined by the

27

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

provisions in the relevant collateral agreement) interacts with, and differs from, the

calculation methodologies in respect of the regularly scheduled payments of the

transaction itself (which are set out in the relevant transaction confirmations), in

conjunction with the relevant ISDA Master Agreement.

Collateral can be used as a method to reduce counterparty risk in transactions.

However, collateral transfers can be subject to rules, such as a minimum transfer

amount, and logic, such as a change in collateral requirements in the event of a

change in credit ratings of the counterparty. Developers may be required to take this

into account. Transaction valuations are also subject to disputes, which can affect

collateral transfers, and this can be another reason to consider the use of an oracle

(see above). The complexity of valuations and collateral transfers generally result in

collateral being transferred once per day. This can create intraday credit risk between

counterparties. A potential benefit of a digitized process is that collateral transfers

could occur more frequently, reducing the systemic risk, and reducing the requirement

for counterparties to post initial margin and independent amounts to one another.

Collateral may need to be transferred or returned as the value of the collateralized

obligations and/or the value of the collateral transferred fluctuates. Developers will

need to provide a mechanism that allows parties to control which obligations they are

seeking to collateralize. It is common for parties to exclude certain transactions from

contributing to the total collateralized exposure under specific collateral arrangements,

either because there is no regulatory requirement to exchange collateral for those

transactions, or the parties otherwise agree that those trades should be excluded

(provided, if there is a regulatory requirement, that they are collateralized under

another collateral arrangement).

In this context, developers should note that certain regulatory requirements for the

exchange of collateral do not apply in the context of certain types of FX, and there are

specific exclusions that may be relevant, depending on the type of transaction and the

jurisdiction in question. In addition, regulations requiring the exchange of collateral

between the parties have resulted in an increase in the use of third-party custodians

and the number and complexity of collateral documents used in a typical trading

relationship.

26

This would need to be considered in any smart derivatives contract

system design.

The mechanism for determining the amount of collateral that needs to be transferred

varies depending on the nature of the margin documentation being used (e.g., the

ISDA Credit Support Agreement governed by New York Law or the ISDA Credit

Support Deed governed by English Law).

26

See ISDA, Legal Guidelines for Smart Derivatives Contracts: Introduction available at:

https://www.isda.org/a/MhgME/Legal-Guidelines-for-Smart-Derivatives-Contracts-Introduction.pdf

28

Copyright © 2020 by the International Swaps and Derivatives Association, Inc.

The considerations that are relevant for collateral arrangements are set out in further

detail in the ISDA Legal Guidelines for Smart Derivative Contracts: Collateral.

27

c. Business Days and Business Day Conventions

Whether a particular day is a “Business Day” (as defined in the 1998 FX Definitions)

is relevant in a number of instances, in relation to the calculation of payments under

an FX transaction. For example, the “Valuation Date”, which is by default the day on

which the spot foreign exchange rate will be determined for the purpose of calculating

the payment(s) owed by one or both of the counterparties to the FX contract, will

generally be specified as a Business Day. The meaning of Business Day in the context

of the Valuation Date is slightly different from that which applies to the Settlement Date

definition. In the case of the Valuation Date, whether there is a Business Day within

the relevant sense broadly depends on whether commercial banks are open on that

day, including to deal in foreign exchange in accordance with the relevant market

practice in the place specified in the confirmation (subject to certain fall-backs). By

contrast, for the purposes of the ‘Settlement Date’ definition, there is a Business Day

broadly if on that day commercial banks effect delivery of the relevant currency in

accordance with the relevant market practice of the place specified in the confirmation

(subject again to fall-backs). It is conceivable, therefore, that there might be a Business

Day for one purpose, but not another – for example, if commercial banks are generally

open for dealings (including FX dealings generally) but are not effecting delivery of

one or more specific currencies relevant to the transaction in question on that day. Any

technological or smart contract implementation seeking to automate payment

processes that rely on the occurrence of a Valuation Date or a Settlement Date would,