OFFICE OF

INSPECTOR GENERAL

DEPARTMENT OF THE TREASURY

WASHINGTON, D.C. 20220

July 20, 2023

MEMORANDUM FOR JESSICA MILANO, ACTING CHIEF RECOVERY OFFICER,

DEPARTMENT OF THE TREASURY

FROM: Deborah L. Harker /s/

Assistant Inspector General for Audit

SUBJECT: Desk Review of State of Florida’s Use of Coronavirus

Relief Fund Proceeds (OIG-CA-23-029)

Please find the attached desk review memorandum

1

on the State of Florida’s use

of Coronavirus Relief Fund (CRF) proceeds. The CRF is authorized under Title VI of

the Social Security Act, as amended by Title V, Division A of the Coronavirus Aid,

Relief, and Economic Security Act (CARES Act). Under a contract monitored by

our office, Castro & Company, LLC (Castro), a certified independent public

accounting firm, performed the desk review. Castro performed the desk review in

accordance with the Council of the Inspectors General on Integrity and Efficiency

Quality Standards for Federal Offices of Inspector General

standards of

independence, due professional care, and quality assurance.

In its desk review, Castro found that the State of Florida personnel timely

completed the required quarterly Financial Progress Reports (FPR) for Cycles 1

2

through 5.

3

Castro personnel reviewed documentation for a selection of 64

transactions reported in the quarterly reports and found that the State of Florida

personnel could not provide the necessary documentation to support certain

transactions resulting in total unsupported expenditures of $893,154,357.89 (see

attached schedule of monetary benefits).

Castro recommends the Department of the Treasury Office of Inspector General

(OIG) pursue obtaining missing documentation from Florida management and

ensure reporting corrections are made, or whether recoupment of funds is

necessary. Further, based on Florida’s responsiveness to Treasury OIG’s requests

and its ability to provide sufficient documentation, Castro recommends Treasury

OIG determine if a full-scope audit over Florida’s use of its CRF proceeds is

1

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) assigned the Department of

the Treasury Office of Inspector General with responsibility for compliance monitoring and

oversight of the receipt, disbursement, and use of Coronavirus Relief Fund (CRF) payments. The

purpose of the desk review is to perform monitoring procedures of the prime recipient’s receipt,

disbursement, and use of CRF proceeds as reported in the grants portal on a quarterly basis.

2

Calendar quarter ending June 30, 2020.

3

Calendar quarter ending June 30, 2021.

Page 2

feasible. Castro and Treasury OIG personnel met with Florida management to

discuss the questioned costs and reporting issues. Florida Management stated

they are able to support the questioned costs, but would need significantly more

time to collect the support since they utilize a decentralized management

approach and the documentation currently lies with the counties and not the state.

In addition, Florida stated that they have made some corrections to their reporting

in subsequent cycles and would work with Treasury OIG to ensure all corrections

have been made.

In connection with our contract with Castro, we reviewed Castro’s desk review

memorandum and related documentation and inquired of its representatives. Our

review, as differentiated from an audit performed in accordance with generally

accepted government auditing standards, was not intended to enable us to

express an opinion on the State of Florida’s use of the CRF proceeds. Castro is

responsible for the attached desk review memorandum and the conclusions

expressed therein. Our review found no instances in which Castro did not comply,

in all material respects, with the Council of the Inspectors General on Integrity and

Efficiency’s

Quality Standards for Federal Offices of Inspectors General

.

We appreciate the courtesies and cooperation provided to Castro and our staff

during the desk review. If you have any questions or require further information,

please contact me at (202) 486-1420, or a member of your staff may contact Lisa

DeAngelis, Deputy Assistant Inspector General for Audit, at (202) 487-8371.

cc: Michelle A. Dickerman, Deputy Assistant General Counsel, Department of

the Treasury

Victoria Collin, Chief Compliance & Finance Officer, Office of Recovery

Programs, Department of the Treasury

Chris Spencer, Director of Policy and Budget, State of Florida

Christopher Sun, Director of Data and Reporting, Office of Recovery

Programs, Department of the Treasury

Wayne Ference, Partner, Castro & Company, LLC

Page 3

Attachment

Schedule of Monetary Benefits

According to the Code of Federal Regulations,

4

a questioned cost is a cost that is

questioned due to a finding:

(a) which resulted from a violation or possible violation of a statute,

regulation, or the terms and conditions of a Federal award, including for

funds used to match Federal funds;

(b) where the costs, at the time of the review, are not supported by

adequate documentation; or

(c) where the costs incurred appear unreasonable and do not reflect the

actions a prudent person would take in the circumstances.

Questioned costs are to be recorded in the Department of the Treasury’s

(Treasury) Joint Audit Management Enterprise System (JAMES).

5

The amount will

also be included in the Office of Inspector General (OIG) Semiannual Report to

Congress. It is Treasury management's responsibility to report to Congress on the

status of the agreed to recommendations with monetary benefits in accordance

with 5 USC Section 405(b) of the Inspector General Act of 1978.

Recommendation Questioned Costs

Recommendation No. 1 $893,154,357.89

The questioned cost represents amounts provided by Treasury under the

Coronavirus Relief Fund. As discussed in the attached desk review,

$893,154,357.89 is the State of Florida’s expenditures reported in the grant-

reporting portal that lacked supporting documentation.

4

2 CFR § 200.84 – Questioned Cost

5

JAMES is Treasury’s audit recommendation tracking system.

Desk Review of the State of Florida

1

1635 King Street

Alexandria, VA 22314

Phone: 703.229.4440

Fax: 703.859.7603

www.castroco.com

July 20, 2023

OIG-CA-23-029

MEMORANDUM FOR DEBORAH L. HARKER,

ASSISTANT INSPECTOR GENERAL FOR AUDIT

FROM: Wayne Ference

Partner, Castro & Company, LLC

SUBJECT: Desk Review of the State of Florida

On September 2, 2021, we initiated a desk review of the State of Florida’s (Florida)

use of the Coronavirus Relief Fund (CRF) authorized under Title VI of the Social

Security Act, as amended by Title V, Division A of the Coronavirus Aid, Relief, and

Economic Security Act (CARES Act).

1

The objective of our desk review was to

evaluate Florida’s documentation supporting its uses of CRF proceeds as reported

in the GrantSolutions

2

portal and to assess the risk of unallowable use of funds.

The scope of our desk review was limited to obligation and expenditure data for

the period of March 1, 2020 through June 30, 2021 as reported in Cycles 1

3

through 5

4

in the GrantSolutions portal.

As part of our desk review, we performed the following:

1) reviewed Florida’s quarterly Financial Progress Reports (FPR) submitted in

the GrantSolutions portal through June 30, 2021;

2) reviewed the

Department of the

Treasury’s (Treasury) Coronavirus Relief

Fund Guidance

as published in the Federal Register on January 15, 2021;

5

1

P.L. 116-136 (March 27, 2020).

2

GrantSolutions, a grant and program management Federal shared service provider under the

U.S. Department of Health and Human Services, developed a customized and user-friendly

reporting solution to capture the use of CRF payments from recipients.

3

Calendar quarter ending June 30, 2020.

4

Calendar quarter ending June 30, 2021.

5

Coronavirus Relief Fund Guidance as published in the Federal Register (January 15, 2021)

https://home.treasury.gov/system/files/136/CRF-Guidance-Federal-Register_2021-00827.pdf

Desk Review of the State of Florida

2

3) reviewed Treasury Office of Inspector General’s (OIG)

Coronavirus Relief

Fund Frequently Asked Questions Related to Reporting and

Recordkeeping

;

6

4) reviewed Treasury OIG’s monitoring checklists

7

of Florida’s quarterly FPR

submissions for reporting deficiencies;

5) reviewed other audit reports issued, such as Single Audit reports, and

those issued by the Government Accountability Office and other applicable

Federal agency OIGs for internal control or other deficiencies that may

pose risk or impact Florida’s uses of CRF proceeds;

6) reviewed Treasury OIG Office of Investigations (OI), the Council of the

Inspectors General on Integrity and Efficiency Pandemic Response

Accountability Committee (PRAC),

8

and Treasury OIG Office of Counsel

input on issues that may pose risk or impact Florida’s use of CRF proceeds;

7) interviewed key personnel responsible for preparing and certifying

Florida’s GrantSolutions portal quarterly FPR submissions, as well as

officials responsible for obligating and expending CRF proceeds;

8) made a non-statistical selection of Contracts, Grants, Transfers,

9

Direct

Payments, Aggregate Reporting,

10

and Aggregate Payments to Individuals

11

data identified through GrantSolutions reporting; and

9) evaluated documentation and records used to support Florida’s quarterly

FPRs.

6

Department of the Treasury Office of Inspector General

Coronavirus Relief Fund Frequently Asked

Questions Related to Reporting and Recordkeeping

OIG-20-028R; March 2, 2021.

7

The checklists are used by Treasury OIG to monitor the progress of prime recipient reporting in

the GrantSolutions portal. GrantSolutions quarterly submission reviews are designed to identify

material omissions and significant errors, and where necessary, include procedures for notifying

prime recipients of misreported data for timely correction. Treasury OIG follows the

CRF Prime

Recipient Quarterly GrantSolutions Submissions Monitoring and Review Procedures Guide

, OIG-

CA-20-029R to monitor the prime recipients quarterly.

8

Section 15010 of P.L. 116-136 established the Pandemic Response Accountability Committee

within the Council of the Inspectors General on Integrity and Efficiency to promote transparency

and conduct and support oversight of covered funds (see Footnote 18 for a definition of covered

funds) and the coronavirus response to (1) prevent and detect fraud, waste, abuse, and

mismanagement; and (2) mitigate major risks that cut across program and agency boundaries.

9

A transfer to another government entity is a disbursement or payment to a government entity

that is legally distinct from the prime recipient.

10

Recipients are required to report CRF transactions greater than or equal to $50,000 in detail in

the GrantSolutions portal. Transactions less than $50,000 can be reported as an aggregate lump-

sum amount by type (contracts, grants, loans, direct payments, and transfers to other government

entities).

11

Obligations and expenditures for payments made to individuals, regardless of amount, are

required to be reported in the aggregate in the GrantSolutions portal to prevent inappropriate

disclosure of personally identifiable information.

Desk Review of the State of Florida

3

Based on our review of Florida’s documentation supporting the uses of its CRF

proceeds as reported in the GrantSolutions portal, we found that uses of CRF

proceeds for Aggregate Payments to Individuals complied with the CARES Act

and Treasury’s Guidance. However, we determined that the expenditures related

to Contracts greater than or equal to $50,000, Grants greater than or equal to

$50,000, Transfers greater than or equal to $50,000, and Aggregate Reporting less

than $50,000 did not comply with the CARES Act and Treasury’s Guidance. We

also found that Direct Payments greater than or equal to $50,000 complied with

the CARES Act but did not comply with Treasury’s Guidance.

Based on the totality of the work performed, we identified total questioned costs

of $893,154,357.89 consisting of $892,966,838.65 determined through our detailed

transaction testing and $187,519.24, which we did not test in detail but determined

through review of general ledger records compared to amounts reported in

GrantSolutions. We determined that Florida’s risk of unallowable use of funds is

high. Castro recommends Treasury OIG pursue obtaining missing documentation

from Florida management and ensure reporting corrections are made, or whether

recoupment of funds is necessary. Further, based on Florida’s responsiveness to

Treasury OIG’s requests and its ability to provide sufficient documentation, we

recommend Treasury OIG determine if a full-scope audit over Florida’s use of its

CRF proceeds is feasible.

Non-Statistical Transaction Selection Methodology

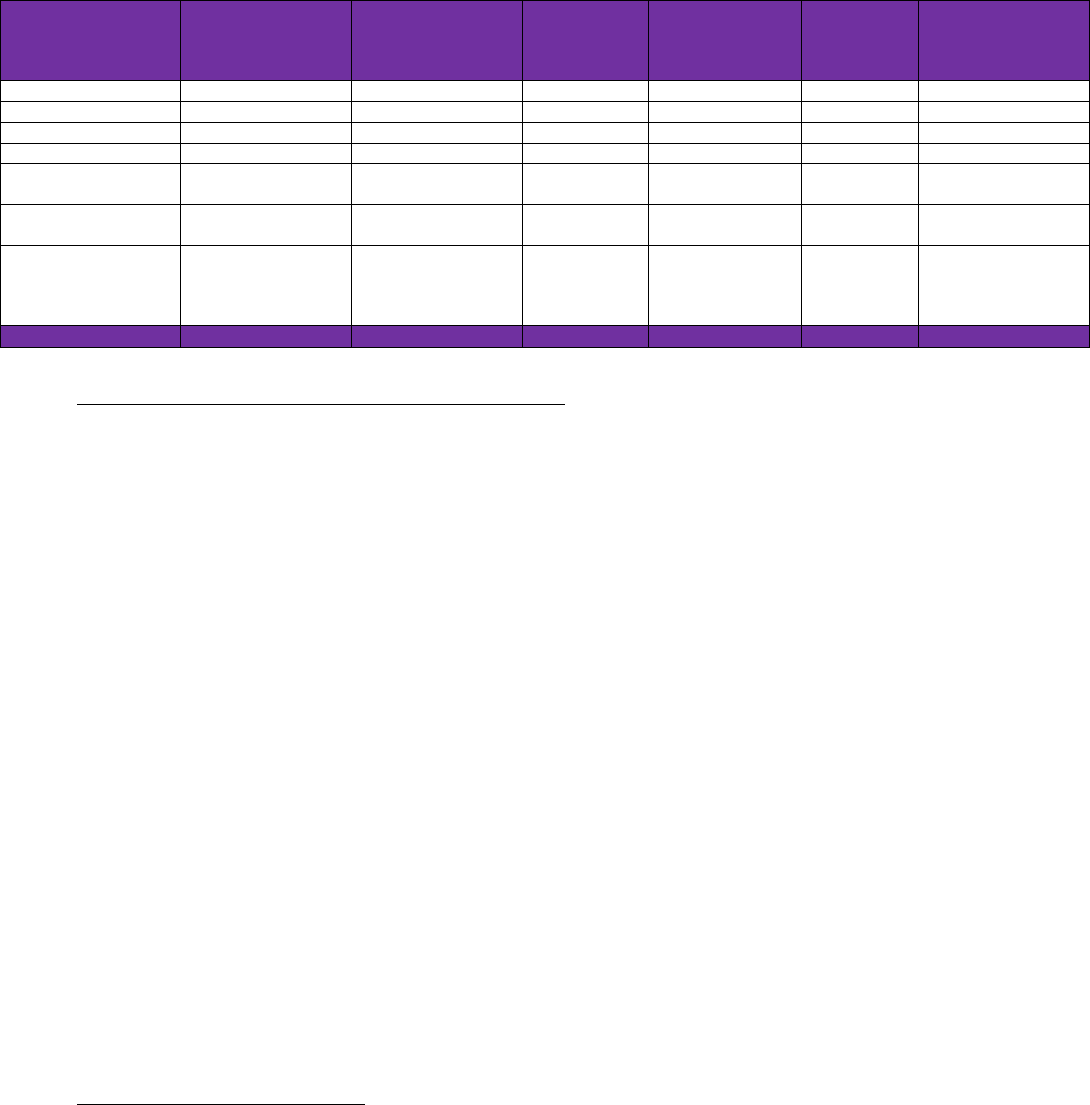

Treasury issued a CRF payment to Florida of $5,855,807,379.80. As of Cycle 5,

12

Florida’s cumulative obligations and expenditures were $5,855,807,379.80 and

$5,813,435,660.79, respectively. Florida’s cumulative obligations and

expenditures, by payment type, as reported in GrantSolutions through Cycle 5 are

summarized below:

Payment Type

Cumulative

Obligations

Cumulative

Expenditures

Contracts >= $50,000

$ 135,879,824.91

$ 134,514,542.52

Grants >= $50,000

$ 1,397,653,855.34

$ 1,356,647,418.72

Loans >= $50,000

$ -

$ -

Transfers >= $50,000

$ 2,368,625,461.00

$ 2,368,625,461.00

Direct Payments >= $50,000

$ 65,983,407.72

$ 65,983,407.72

Aggregate Reporting < $50,000

$ 46,905,800.08

$ 46,905,800.08

Aggregate Payments to Individuals

(In Any Amount)

$ 1,840,759,030.75 $ 1,840,759,030.75

Totals

$ 5,855,807,379.80

$ 5,813,435,660.79

12

Calendar quarter ending June 30, 2021.

Desk Review of the State of Florida

4

Castro made a non-statistical selection of Contracts greater than or equal to

$50,000, Grants greater than or equal to $50,000, Transfers greater than or equal

to $50,000, Direct Payments greater than or equal to $50,000, Aggregate Reporting

less than $50,000, and Aggregate Payments to Individuals. Selections were made

using auditor judgment based on information and risks identified in reviewing

audit reports, the GrantSolutions portal reporting anomalies

13

identified by the

Treasury OIG CRF monitoring team, and review of Florida’s FPR submissions.

Castro noted Florida did not obligate or expend CRF proceeds to Loans greater

than or equal to $50,000; therefore, we did not make a selection of transactions

from this category.

The number of transactions (61) we selected to test were based on Florida’s total

CRF award amount and our overall risk assessment of Florida. To allocate the

number of transactions (61) by payment type (Contracts greater than or equal to

$50,000, Grants greater than or equal to $50,000, Transfers greater than or equal

to $50,000, Direct Payments greater than or equal to $50,000, Aggregate Reporting

less than $50,000, and Aggregate Payments to Individuals), we compared the

payment type dollar amounts as a percentage of cumulative obligations for

Cycle 5.

14

Additionally, Treasury OIG identified four anomalies that consisted of

two outliers

15

and two transactions representing a potential duplicate payment.

Castro determined that out of the two outliers, one outlier was already included

within Castro’s selection for the payment type Grants greater than or equal to

$50,000. The anomalies identified by Treasury OIG resulted in three additional

selections for Castro’s desk review, for a total of 64 transaction selections.

Background

The CARES Act appropriated $150 billion to establish the CRF. Under the CRF,

Treasury made payments for specified uses to States and certain local

governments; the District of Columbia and U.S. Territories, including the

Commonwealth of Puerto Rico, the United States Virgin Islands, Guam, American

Samoa, and the Commonwealth of the Northern Mariana Islands; and Tribal

governments. Treasury issued a CRF payment to Florida for $5,855,807,379.80.

13

Treasury OIG has a pre-defined list of risk indicators that are triggered based on data submitted

by recipients in the FPR submissions that meet certain criteria. Castro reviewed these results

provided by Treasury OIG for Florida.

14

Calendar quarter ending June 30, 2021.

15

Outliers were identified by Treasury OIG personnel. Based on statistical modeling, these

transactions were identified as having a high dollar amount relative to transactions at similar

points in time, with similar award descriptions, and that the same prime recipient disbursed.

Desk Review of the State of Florida

5

The CARES Act stipulates that a recipient may only use the funds to cover costs

that—

(1) are necessary expenditures incurred due to the public health emergency

with respect to the coronavirus disease 2019 (COVID-19);

(2) were not accounted for in the budget most recently approved as of

March 27, 2020; and

(3) were incurred between March 1, 2020 and December 31, 2021.

16

Section 15011 of the CARES Act, requires each covered recipient

17

to submit to

Treasury and the PRAC, no later than 10 days after the end of each calendar

quarter, a report that contains (1) the total amount of large covered funds

18,19

received from Treasury; (2) the amount of large covered funds received that were

expended or obligated for each project or activity; (3) a detailed list of all projects

or activities for which large covered funds were expended or obligated; and (4)

detailed information on any level of sub-contracts or sub-grants awarded by the

covered recipient or its sub-recipients.

The CARES Act assigned Treasury OIG the responsibility for compliance

monitoring and oversight of the receipt, disbursement, and use of CRF proceeds.

Treasury OIG also has authority to recoup funds in the event that it is determined

a recipient failed to comply with requirements of subsection 601(d) of the Social

Security Act, as amended, (42 U.S.C. 801(d)).

Desk Review Results

We reviewed Florida’s quarterly FPR submissions through June 30, 2021, and

determined that Florida submitted all its reports on a timely basis. Based on our

review of Florida’s documentation supporting the uses of its CRF proceeds as

reported in the GrantSolutions portal, we determined that Aggregate Payments to

Individuals transactions selected for detailed review were supported by

16

P.L. 116-260 (December 27, 2020). The period of performance end date of the CRF was extended

through December 31, 2021 by the Consolidated Appropriations Act, 2021. The period of

performance end date for tribal entities was further extended to December 31, 2022 by the State,

Local, Tribal, and Territorial Fiscal Recovery, Infrastructure, and Disaster Relief Flexibility Act,

Division LL of the Consolidated Appropriations Act, 2023, P.L. 117-328, December 29, 2022, 136

Stat. 4459.

17

Section 15011 of P.L. 116-136 defines a covered recipient as any entity that receives large

covered funds and includes any State, the District of Columbia, and any territory or possession of

the United States.

18

Section 15010 of P.L. 116-136 defines covered funds as any funds, including loans, that are made

available in any form to any non-Federal entity, not including an individual, under Public Laws 116-

123, 127, and 136, as well as any other law which primarily makes appropriations for Coronavirus

response and related activities.

19

Section 15011 of P.L. 116-136 defines large covered funds as covered funds that amount to more

than $150,000.

Desk Review of the State of Florida

6

documentation and were allowable expenditures in accordance with the CARES

Act and Treasury’s guidance. We also found that Aggregate Payments to

Individuals and Direct Payments greater than or equal to $50,000 were necessary

expenditures due to the COVID-19 public health emergency, were not accounted

for in the budget most recently approved as of March 27, 2020, and were incurred

during the covered period.

However, we determined that the expenditures related to Contracts greater than

or equal to $50,000, Grants greater than or equal to $50,000, Transfers greater

than or equal to $50,000, and Aggregate Reporting less than $50,000 did not

comply with the CARES Act and Treasury’s Guidance. We also found that Direct

Payments greater than or equal to $50,000 complied with the CARES Act but did

not comply with Treasury’s Guidance. The transactions selected for testing were

not selected statistically, and therefore results cannot be extrapolated to the total

universe of transactions.

The following table includes the total cumulative expenditure population amount

and the cumulative expenditure amount tested. Additionally, this table includes a

summary of Castro’s testing results over expenditure transaction balances. Within

the table below, we have included a summary of unsupported and ineligible

expenditures identified as questioned costs. These expenditures do not comply

with the CARES Act and Treasury’s Guidance. Additionally, in the far-right

column, we have identified the expenditures that Castro tested without exceptions

noted. See Desk Review Results section below this table for a detailed discussion

of questioned costs and other issues identified throughout the course of our desk

review.

Desk Review of the State of Florida

7

Summary of Expenditure Testing and Recommended Results – As of Cycle 5

20

Payment Type

Cumulative

Expenditure

Population Amount

Cumulative

Expenditure Tested

Amount

Unsupported

Reconciling

Items

21

Unsupported

Exception

Ineligible

Exception

Castro Reviewed

Value Without

Exception

(per Support)

Contracts >= $50,000

$ 134,514,542.52

$ 72,604,525.96

$ -

$ 72,604,525.96

$ -

$ -

Grants >= $50,000

$ 1,356,647,418.72

$ 502,722,649.55

$ -

$ 337,242,323.50

$ -

$ 165,480,326.05

Loans >= $50,000

$ -

$ -

$ -

$ -

$ -

$ -

Transfers >= $50,000

$ 2,368,625,461.00

$ 1,465,595,089.00

$ -

$ 481,977,654.00

$ -

$ 983,617,435.00

Direct Payments >=

$50,000

$ 65,983,407.72 $ 981,141.50 $ -

$ - $ -

$ 981,141.50

Aggregate

Reporting < $50,000

$ 46,905,800.08 $ 3,604,632.50 $ 187,519.24 $ 1,142,335.19 $ -

$ 2,462,297.31

Aggregate

Payments to

Individuals (in any

amount)

$ 1,840,759,030.75 $ 1,096,287,986.91 $ -

$ - $ -

$ 1,096,287,986.91

Totals

$ 5,813,435,660.79

$ 3,141,796,025.42

$ 187,519.24

$ 892,966,838.65

$ -

$ 2,248,829,186.77

Contracts Greater Than or Equal to $50,000

Based on the documentation reviewed and entries in GrantSolutions, we

determined Florida’s Contracts greater than or equal to $50,000 did not comply

with the CARES Act and Treasury’s Guidance. We question $72,604,525.96 of

expenditures related to one transaction over which we performed testwork

because of a lack of supporting documentation. For that contract, Castro obtained

and reviewed general ledger (GL) detail files and high-level summaries, which

agreed to the cumulative expenditure amounts reported in GrantSolutions.

However, Florida did not provide any invoice documentation to support the

expenditure amounts. Without detailed invoices, we were unable to assess the

accuracy and eligibility of cumulative expenditures incurred using CRF funding.

Additionally, without invoice expenditure support, we were unable to confirm the

expenditure category and associated project for those related balances.

Florida personnel told us that this contract agreement was for call center support

for Florida’s re-employment assistance program and the claim amount was for

monthly costs that exceeded the Florida Department of Economic Opportunity’s

(DEO) normal operations. Florida stated that the DEO did not keep adequate

records to support the monthly claim amounts that exceeded normal operational

costs, and the DEO was conducting a detailed historical operational cost analysis

and comparison to support their claim amounts. Florida personnel told us that

they intended to work with the DEO to obtain supporting documentation and

20

Calendar quarter ending June 30, 2021.

21

As a result of our reconciliation procedures, we determined that the cumulative expenditures

recorded in GrantSolutions for original transaction amounts prior to sub-selections were

$12,777,942.62 while the expenditures per the general ledger detail were $12,590,423.38, resulting

in a variance of $187,519.24. However, we did not test detailed support for these amounts. As

such, we excluded this balance from the “Cumulative Expenditure Tested Amount” column.

Desk Review of the State of Florida

8

make adjustments at the conclusion of DEO’s analysis. Florida personnel

anticipate reporting these adjustments as a correction in future GrantSolutions

reporting cycles.

Grants Greater Than or Equal to $50,000

Based on the documentation reviewed and entries made in GrantSolutions, we

determined Florida’s Grants greater than or equal to $50,000 did not comply with

the CARES Act and Treasury’s Guidance. We question $337,242,323.50 of

expenditures related to Grants greater than or equal to $50,000 because of a lack

of supporting documentation. We selected 13 transactions over which to perform

testwork, which included 33 sub-selections

22

and we identified $337,242,323.50 in

questioned costs, which we have further disaggregated below.

For 9 out of 33 sub-selections, we identified unsupported expenditure

amounts of $82,592,898.13. Florida provided GL details to support the

transactions, which we were able to agree to our selections without

exception. However, Florida did not provide support for the additional sub-

selections prior to the end of our fieldwork.

For 14 out of 33 sub-selections, we identified unsupported expenditure

amounts of $152,664,054.01. Florida either did not provide a payroll

distribution report or GL, or provided information which did not agree to

our sub-selection. Additionally, Florida did not provide detailed expenditure

support such as vendor invoices.

For 1 out of 33 sub-selections, we identified unsupported expenditure

amounts of $2,804,201. We received the payroll distribution report, but

noted an unsupported expenditure amount labeled “Sheriff and EMS

Payroll Previously submitted” of $2,804,201. We reached out to Florida for a

breakout of this amount; however, Florida did not respond prior to the end

of our fieldwork.

For 2 out of 33 sub-selections, we identified unsupported expenditure

amounts of $6,611,911.37. Castro received partial payroll distribution

reports, but $6,611,911.37 in payroll costs related to another document that

was not provided to Castro.

For 4 out of 33 sub-selections, Florida claimed $92,569,258.99 in

expenditures but provided payroll distribution files totaling $119,245,810.85,

which exceeded claimed expenditures by $26,676,551.86. We reviewed the

payroll distribution report provided by Florida and requested that Florida

provide us with the specific payroll transactions that agreed to amounts

claimed. However, Florida did not respond to our request prior to the end of

22

Due to the voluminous nature of transactions at the original transaction selection level, we

obtained and utilized a GL detail listing to select a sub-selection of transactions needed to test

obligations and expenditures at the detailed transaction level.

Desk Review of the State of Florida

9

our fieldwork. Therefore, we were unable to identify the transactions that

related to this CRF claim and as such, we question $92,569,258.99 in

claimed expenditures.

We do not consider GL detail support provided to be acceptable, as Florida did not

provide us with detailed underlying grant program documentation (e.g., sub-

recipient grant agreements, invoices for goods and supplies purchased, etc.)

needed to verify the expenditures incurred were necessary due to the public

health emergency with respect to COVID-19. Without details of grant program

costs incurred by Florida’s sub-recipients, we were unable to perform a full

assessment to verify the accuracy and eligibility of cumulative expenditures

incurred using CRF funding. Florida did not respond with sufficient supporting

documentation prior to the end of our fieldwork and did not respond to our

requests for both the root cause of missing support and a corrective action plan.

Transfers Greater Than or Equal to $50,000

We determined Florida’s Transfers greater than or equal to $50,000 did not

comply with the CARES Act and Treasury’s Guidance. We question $481,977,654

of expenditures related to Transfers greater than or equal to $50,000 because of a

lack of supporting documentation.

Florida identified a total of $929 million in cumulative obligations of Florida

Education Finance Program (FEFP) funding as necessary to respond to the

pandemic’s impact on K-12 schools. This amount represented three months of

funding granted by Florida, via Executive Order, to 74 different Florida County

Public School Systems, County School Boards, and County School Districts. These

entities were sub-recipients flagged as Special District Governments/ Independent

School Districts by Florida within GrantSolutions. This funding allowed for the

transfer of allocations to school districts to cover the last 3 months of the school

year (April, May, and June of 2020) that were most immediately affected by the

COVID-19 pandemic. We noted that Florida did not calculate these obligation

estimates and allocate these transferred funds based on Treasury’s $500 per full-

time employee (FTE) guidance, as detailed in FAQ #53 of the Federal Register,

Volume 86. Additionally, we determined that Florida made duplicate transfer

payments to each school district, and that the total transfer expenditure claims for

each school exceeded $500 per full time equivalent student. As such, we

determined these expenditures were not subject to Treasury’s administrative

accommodation exempting required documentation, but instead required

underlying expenditure support to evidence compliance with the CARES Act.

As part of our procedures, we selected 21 transactions for testing. We identified

the following exceptions within 7 out of 21 transactions selected for testing, which

Desk Review of the State of Florida

10

consisted of $481,977,654 out of the April, May, and June of 2020 $929 million

transfer allocation amount.

For these samples tested, Florida leveraged its existing FEFP state funding

program as a vehicle to transfer funds to 74 different sub-recipients within the

state on a predetermined allocation basis. Although Florida did provide Castro

with an eligibility justification document with a list of incremental COVID-19 costs

that it intended sub-recipients to use the FEFP transferred CRF claimed funds to

pay for, we reviewed Florida’s FEFP guidance and determined that this statute and

funding guidance was not modified to include CARES Act specific COVID-19

requirements. Additionally, Florida personnel told us that they did not provide any

additional transfer documents to its school districts other than the existing FEFP

statutes and program guidance, which included pre-COVID-19 requirements for

use of funds under the FEFP program. Therefore, we determined that Florida did

not communicate specific COVID-19 eligibility requirements to the school districts

along with these transferred funds.

Further, we requested detailed expenditure documentation from Florida to

support the school district’s actual expenditures incurred using the CRF funds.

Florida personnel told us that they did not require these school districts to retain

detailed expenditure documentation to support costs incurred under this program.

Specifically, school districts were instructed to record CRF funds transferred

through FEFP funds to its general revenue funds, and as such, were not instructed

to create a CRF appropriation code against which to track expenditures incurred

using these transferred CRF funds. Florida personnel told us that it would be

impossible to provide detailed invoices or GL detail files supporting school

districts’ incurred expenditures at the transaction level. Without this GL detail, we

could not make a sub-selection of underlying expenditure transactions incurred by

Florida’s sub-recipients. Additionally, since the sub-recipients did not track actual

expenditures incurred, Castro determined that it would have been difficult, if not

impossible for Florida to perform sufficient sub-recipient monitoring procedures

over these CRF reported expenditure balances.

Florida did provide us with a spreadsheet of its FEFP obligation allocation

calculations, internally generated payment vouchers, and a memo summarizing

Florida’s internal voucher payments to the school districts under the FEFP

program. However, we did not consider this acceptable documentation, as Florida

did not provide detailed underlying expenditure support such as GL detail listings

of school district incurred expenditure amounts, invoices, payroll distribution

reports, and/or timesheets to corroborate the estimated cumulative expenditure

figures reported by Florida in GrantSolutions. As these expenditures were not

subject to Treasury’s administrative accommodation exemption for

documentation, without detailed invoices we were unable to perform a full

Desk Review of the State of Florida

11

assessment needed to verify the accuracy and eligibility of cumulative

expenditures incurred using CRF funding. Therefore, we question expenditures of

$481,977,654 as unsupported.

We determined Florida did not comply with Treasury’s Federal Register Notice

Volume 86, Number 10 FAQ #53. This requirement allowed an administrative

convenience of up to $500 per full time equivalent student but Florida did not

calculate its obligations and distribute transferred funds using this methodology.

In addition to questioned costs of $481,977,654 identified within our testing above,

we determined the full amount of $929 million that Florida transferred to sub-

recipients may be similarly unsupported. If the Treasury OIG determines that a full

scope audit is feasible, we recommend Treasury OIG determine if the full

$929 million claim is similarly unsupported.

Direct Payments Greater Than or Equal to $50,000

We determined Florida’s Direct Payments greater than or equal to $50,000

complied with the CARES Act but did not comply with Treasury’s Guidance. We

selected two transactions to test. For one of these transactions, we selected three

expenditure transactions as sub-selections.

We obtained and reviewed the underlying expenditure support for our sub-

selections and noted that the GrantSolutions balance of $1,871,731.46 consisted of

GL detail of 37 individual transactions (three of which included our sub-

selections), each with their own document number, invoice number, and payment

date. Instead of aggregating these 37 different transactions into one Direct

Payment entry within GrantSolutions, we determined that Florida personnel

should have reported each of these transactions as separate Direct Payment

entries within GrantSolutions with their own cumulative obligation and

expenditure balance and payment date. Therefore, this did not comply with

Treasury OIG’s reporting requirements to individually report direct payment

transactions (for both cumulative expenditure and obligation reported balances).

We determined Florida did not comply with Treasury OIG Guidance OIG-CA-20-

028R,

Department of the Treasury Office of Inspector General Coronavirus Relief

Fund Frequently Asked Questions Related to Reporting and Recordkeeping

(Revised)

, FAQ # 40 because Florida personnel reported transactions in the

aggregate instead of individually in the proper greater than $50,000 payment type

section. We are not questioning these costs as the support for these transactions

was adequate; however, we determined the amount tested was a reporting

misclassification.

Desk Review of the State of Florida

12

Aggregate Reporting Less Than $50,000

We determined Florida’s Aggregate Reporting less than $50,000 payment type did

not comply with the CARES Act and Treasury’s Guidance. We questioned

$1,142,335.19 in expenditures due to a lack of supporting documentation, to

include lack of sufficient eligibility determination responses. Additionally, we

identified misclassification exceptions related to Aggregate Reporting less than

$50,000 that should have been reported as Contracts greater than or equal to

50,000, Direct Payments greater than or equal to 50,000, and/or Transfers greater

than or equal to $50,000. We were unable to determine the correction entry

required due to insufficient obligation support.

We selected one transaction to test; however, due to the volume of expenditures

contained within the transaction, we selected eight sub-selections to obtain

coverage at the transaction level.

We identified unsupported questioned expenditure amounts totaling

$1,142,335.19. We have further disaggregated and detailed these exceptions

below:

For 2 out of 8 sub-selections, we identified unsupported expenditure

amounts of $1,136,250.93. Florida provided us with GL detail files, internally

generated payment vouchers approving amounts for payment, and a high-

level summary of expenditures incurred. We did not consider this to be

sufficient expenditure support, as Florida did not provide us with detailed

expenditure support (such as invoices, payroll distribution reports, and/or

timesheets) needed to corroborate expenditure amounts reported in

GrantSolutions. Without detailed invoices, we were unable to perform a full

assessment needed to verify the accuracy and eligibility of expenditure

amounts incurred using CRF funding.

For 1 out of 8 sub-selections, we identified unsupported expenditure

amounts of $6,084.26. We reviewed expenditure invoice support that we

were able to agree to the amounts reported in GrantSolutions without

exception, but these invoices contained only high-level descriptions of

services incurred which we did not consider sufficient to corroborate that

these expenditure transactions were necessary due to the public health

emergency with respect to COVID-19. Additionally, we requested Florida’s

previous budget to ensure that these expenditures were not previously

budgeted, but Florida did not respond to our request for this supporting

documentation.

We requested missing supporting documentation from Florida personnel on

multiple occasions and granted multiple extensions to our desk review timeline.

Desk Review of the State of Florida

13

Florida personnel told us that the root cause for not providing requested support

for the exceptions was that the review timelines were difficult to meet due to the

voluminous nature of expenditure support, competing financial reporting

requirements, and because Florida did not have the needed documentation

readily available.

For 5 out of 8 sub-selections, we reviewed underlying expenditure support and

determined that each of these transactions exceeded $50,000; therefore, Florida

personnel misclassified these cumulative obligations and expenditures within

GrantSolutions. The result was an overstatement to Aggregate Reporting less

than $50,000. Due to lack of sufficient obligating documentation, we were unable

to determine whether these transactions should have been reported as Contracts

greater than or equal to $50,000, Direct Payments greater than or equal to $50,000,

and/or Transfers greater than or equal to $50,000. Although we do not consider

misclassifications to be questioned costs, we do not consider these misclassified

transaction balances to comply with Treasury’s Guidance as they should have

been reported under a different payment type.

Florida stated that at the transactional level, these orders and subsequent charges

were below $50,000 and therefore reported as Direct Payments in aggregate less

than $50,000. However, it was unable to respond to our requests for detailed

expenditure support. Florida noted that it would review the detailed charges to

verify each charge was below $50,000, and if any of the charges were in excess of

$50,000, then Florida would make an adjustment in future GrantSolutions

submissions.

In addition to our detailed review of transactions in the sub-selections, we

performed data analytic procedures over the expenditures within the GL detail file

provided and found $2,132,953 in additional misclassifications. Florida confirmed

that it would review its transactions to determine if any of the charges were in

excess of $50,000, and if so, Florida told us that it intended to make an adjustment

in future GrantSolutions cycle submissions.

Desk Review of the State of Florida

14

Conclusion

We found that uses of CRF proceeds for Aggregate Payments to Individuals

complied with the CARES Act and Treasury’s Guidance. However, we determined

that the expenditures related to Contracts greater than or equal to $50,000, Grants

greater than or equal to $50,000, Transfers greater than or equal to $50,000, and

Aggregate Reporting less than $50,000 did not comply with the CARES Act and

Treasury’s Guidance. We also found that Direct Payments greater than or equal to

$50,000 complied with the CARES Act but did not comply with Treasury’s

Guidance.

Based on the totality of the work performed, we identified total questioned costs

of $893,154,357.89 consisting of $892,966,838.65 determined through our detailed

transaction testing and $187,519.24, which we did not test in detail but determined

through review of general ledger records compared to amounts reported in

GrantSolutions. We determined that Florida’s risk of unallowable use of funds is

high. Castro recommends Treasury OIG pursue obtaining missing documentation

from Florida management and ensure reporting corrections are made, or whether

recoupment of funds is necessary. Further, based on Florida’s responsiveness to

Treasury OIG’s requests and its ability to provide sufficient documentation, we

recommend Treasury OIG determine if a full-scope audit over Florida’s use of its

CRF proceeds is feasible.

*****

All work completed with this letter complies with the Council of the Inspectors

General on Integrity and Efficiency’s

Quality Standards for Federal Offices of

Inspectors General

, which require that the work adheres to the professional

standards of independence, due professional care, and quality assurance to

ensure the accuracy of the information presented.

23

We appreciate the courtesies

and cooperation provided to our staff during the desk review.

Sincerely,

Wayne Ference

Partner, Castro & Company, LLC

23

https://www.ignet.gov/sites/default/files/files/Silver%20Book%20Revision%20-%208-20-12r.pdf