Financial Statement Analysis (ACCT-UB.0003) Spring 2022

KMC 4-80(11:00 MW), TISC UC-04 (2:00 MW), TISC LC-25 (3:30MW)

Syllabus for Textbook Edition 6

Professor: Christine Cuny

Office: KMC 10-91

E-Mail: ccuny@stern.nyu.edu

Teaching Assistants: Diya Goel ([email protected]); Kayla Han (kh2937@stern.nyu.edu);

Elton Zhu ([email protected])

Zoom Office Hours:* Mondays 12:45pm-1:45pm and Wednesdays 12:45pm-1:45pm and by appointment

Zoom TA Office Hours:* 5:00-6:30pm the night before assignment due dates and by appointment

*Note: If you plan to attend office hours with the professor, please reserve a time slot in advance. You will find a link

to reserve an appointment within each office hour posted in the schedule on Brightspace.

Course Objective:

The objective of this course is to understand how to read, interpret, and analyze financial statements. Throughout the

course, we will use the financial statements of several real companies to illustrate concepts. Specifically, we will:

• Study the interrelationships between financial statement line items

• Use ratio analysis to understand and compare firms

• Understand accounting disclosures

• Use accounting disclosures to adjust financial statements

• Forecast future earnings using accounting disclosures

• Value a firm using forecasts

Prerequisites:

The course assumes you have a solid grasp of general accounting concepts and principles

Course Materials:

• Throughout the course, you will receive three course packets containing lecture slides, in-class exercises,

assignments, and practice exam questions. You will receive four supplements containing select pages from

financial statements for illustrative purposes. All of these materials are available through Brightspace.

• You will need access to Microsoft Excel.

• You will find a financial calculator helpful in the second half of the course. If you plan to go into accounting or

finance, this is a worthwhile investment. The Texas Instruments BA II Plus Financial Calculator sells for roughly

$30 on Amazon: Link.

• The optional textbook for the course is “Financial Statement Analysis & Valuation,” by Easton, McAnally, Som-

mers, and Zhang. The book is currently in its sixth edition, but feel free to use an earlier version. You will

need the textbook to complete the optional practice problems, which are helpful for solidifying concepts and

preparing for exams.

Grading:

Your grade in the course will be determined according to this tentative point distribution:

Exam I 33%

Exam II 33%

Assignments 33%

Exams (66.67%)

There are two exams that are aimed at assessing your grasp of the learning objectives for the course. Exams will be

taken in person during each class meeting time (11am, 2pm, and 3:30pm). Before the exam, I will hold an in-class

review session and a Zoom Q&A session. I do not offer make-up exams.

Assignments (33.33%)

There are six assignments throughout the semester that are aimed at solidifying your understanding of the concepts

covered in class by applying them to the financial statements of Target Corporation. Your five highest scores will be

included in your course grade (I will drop your lowest assignment score). You will have a minimum of a week after we

cover each topic in class to complete the associated assignment. You can work on these assignments individually or

in groups of up to five people (you may hand in one copy per group). To receive credit for the assignments, they need

to be submitted electronically via Brightspace before 5pm New York time on the due date. The solution is posted

at 5pm on the due date of the assignment, therefore I cannot accept late submissions. The assignment due date

schedule is as follows:

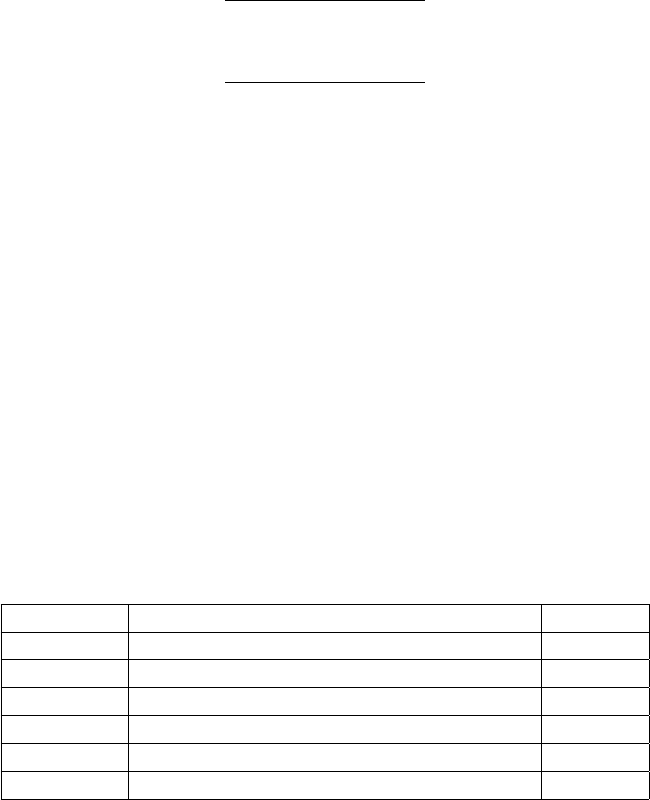

Assignment Topic Due Date

1 Common size & percentage change analysis 2/16

2 Dupont & Penman Profitability Analysis 3/2

3 Risk Analysis 3/23

4 Accounting Analysis 4/13

5 Parsimonious Forecast 4/27

6 Valuation 5/4

Note: The TAs will hold additional office hours the Tuesday before each assignment is due (on Zoom).

Re-Grade Policy:

Grading mistakes happen occasionally. Therefore, you are permitted to submit re-grade requests on exams and as-

signments within one calendar week of the posting of the grades. To have an exam re-graded, you must submit a

short written description of your argument that explains the grading mistake and why you believe you deserve addi-

tional credit. Upon receipt of your written description, I will review the entire exam/assignment for grading accuracy;

therefore your grade may go up or down as a result of the re-grade request.

Additional Information:

Policy on Class Attendance:

I do not take attendance. However, past semesters have shown a strong correlation between class attendance and

overall course performance. The exams are based on our in-class discussions, so participating in class will naturally

correlate with your exam performance. I understand that over the course of 28 sessions, personal, health, and

religious conflicts come up and you may need to miss class. You are welcome to attend an alternative section as long

as there is space in the room. All classes are recorded, so if you cannot attend any of the three sections, I will make

the recording available to you upon request because I want you to have the opportunity to make up the material you

missed on your own. Exercise solutions will also be posted on Brightspace. In the event that the course needs to be

offered entirely online for a particular class meeting, we will meet synchronously at our regularly scheduled class time

using Zoom. Additional details will be emailed to you in the event of a shift to online instruction.

Academic Integrity, General Conduct & Behavior:

The Stern Student Code of Conduct applies to all students enrolled in Stern courses and can be found here. Students

are also expected to maintain and abide by Stern’s Policy in Regard to In-Class Behavior & Expectations (link) and

the NYU Student Conduct Policy (link).

Student Accessibility

If you will require academic accommodation of any kind during this course, you must notify me at the beginning of

the course (or as soon as your need arises) and provide a letter from the Moses Center for Student Accessibility

(212-998-4980, [email protected]) verifying your registration and outlining the accommodations they recommend.

For more information, visit the CSA website.

Student Wellness

These are stressful times. I encourage you to reach out if you need help. The NYU Wellness Exchange offers mental

health support. You can reach them 24/7 at 212-443-9999, or via the “NYU Wellness Exchange” app. There are also

drop in hours and appointments. Find out more here.

Name Pronunciation and Pronouns

NYU Stern students now have the ability to include their pronouns and name pronunciation in Albert. I encourage you

to share your name pronunciation and pronouns this way. Please utilize this link for additional information.

Inclusion Statement

This course strives to support and cultivate diversity of thought, perspectives, and experiences. The intent is to

present materials and activities that will challenge your current perspectives with a goal of understanding how others

might see situations differently. By participating in this course, it is the expectation that everyone commits to making

this an inclusive learning environment for all.

Course Framework:

Specific content and dates are subject to change. The general progression of the course is divided into three sections,

as follows:

1. In this section of the course, you will develop the tools to understand and compare firms. We

will:

• Review basic financial accounting concepts

• Become familiar with the information available to investors and analysts

• Learn where to find information in real 10-Ks

• Learn how to compute various financial ratios

• Understand the value of common-size financial statements in understanding the nature of a firm’s business

• Learn how ratios can be used to identify trends within a company over time and across firms within an industry

• Learn how to use financial ratios to assess a firm’s profitability and risk

• Learn how to interpret financial statement ratios

• Learn how operating and financing activities affect inferences of financial statement ratios

• Learn how to adjust the financial statements to allow for cross-sectional comparison

• Understand the discretion management has in classifying revenues, expenses, gains, and losses on the income

statement and the implications of this discretion

• Learn how to recast financial statements to undo distortions

• Learn the difference between temporary and permanent income

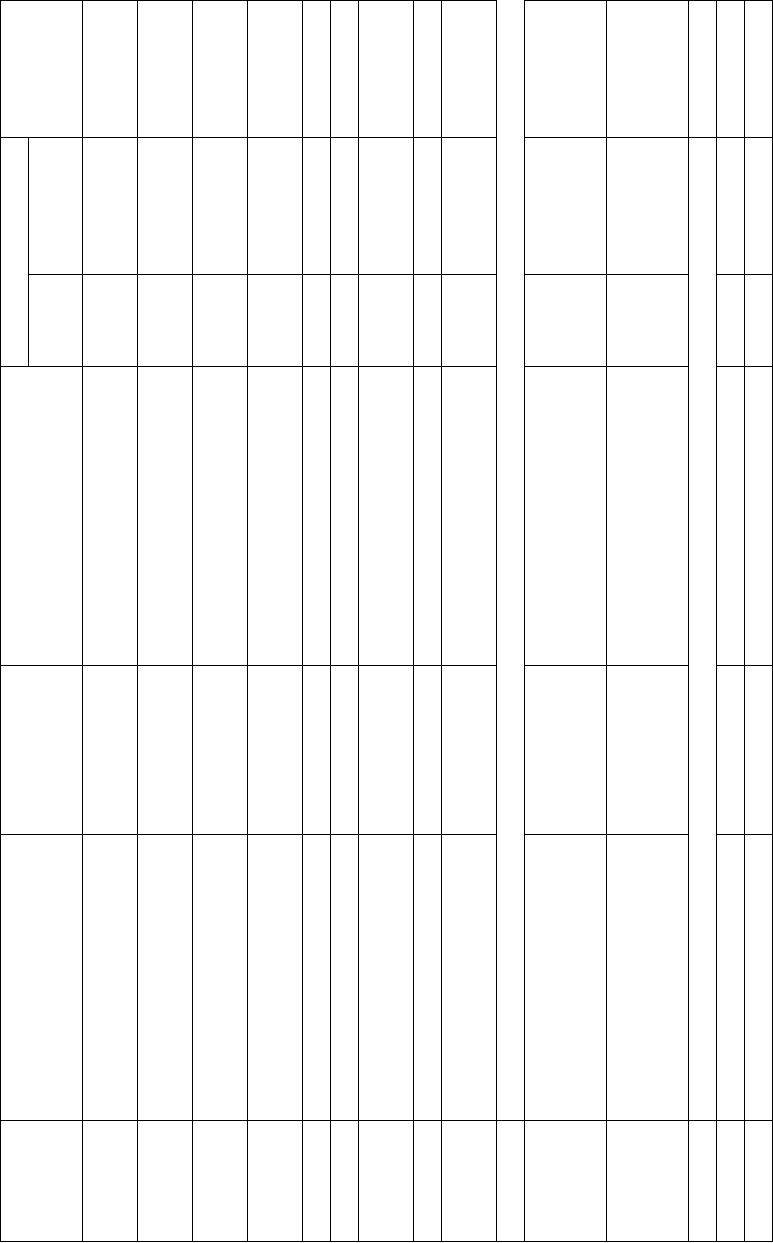

Bring to Class

Before Class After Class Course Assignment

Date Topic Readings 6e Practice Problems 6e Pack Supplement Due

1/24 (Mon) Course Introduction 1-12 to 1-19 1

1/26 (Wed) Accounting Refresh

Skim 2-1 to 2-21 Q1-7, M1-25; E1-35

1 1

Target MD&A Q2-17, M2-23, 28

1/31 (Mon)

Intro to

E2-34, P2-50 1 1

financial statements

2/2 (Wed)

Intro to

1 1

financial statements

2/7 (Mon) Common-size analysis Pepsi MD&A E2-42, 43, 44 1 2

2/9 (Wed) Common-size analysis 1 2

2/14 (Mon) Profitability analysis

1-24 to 1-27 E1-38, 39, 41

1 2

8-26 to 8-27 P1-43, 44, P2-49; M8-31

2/15 (Tue) Assignment 1 TA Office Hours

2/16 (Wed) Profitability analysis

Appendix 3B Q1-19, P1-49, 50, 51, 52, 53

1 2 1

Skim Module 9 M9-20, E9-28, 32, 36

2/21 (Mon) No Class (President’s Day)

2/23 (Wed)

Penman

Module 3

Q3-2, 3, 5, 6, M3-23

1 2Profitability analysis Q3-10, 14, M3-21,E3-37

P3-44, 46, 48, 52

2/28 (Mon) Pro-forma Adjustments

2-12 to 2-15; Q5-9,

1 26-25 to 6-29 Q6-12,

& 5-34 to 5-38 E5-32, P5-39, P5-40

3/1 (Tue) Assignment 2 TA Office Hours

3/2 (Wed) Risk analysis I Module 4 Q4-3, 10, 12, 13, M4-16, 17, 21 1 2 2

3/7 (Mon) Risk analysis II 7-18 to 7-23 E4-22, 26, 28, P4-32 1 2

2. In this section of the course, you will learn how to understand and analyze accounting disclo-

sures. We will:

• Understand how accounting choices affect cross-sectional and time-series variation in financial ratios

• Learn how to identify and evaluate critical accounting policies contained in the footnotes to the financial state-

ments

• Understand the effects of these choices on the historical and future financial statements

• Learn how to adjust the financial statements to allow for cross-sectional comparison

• Learn how changes in the asset and liability valuations on the balance sheet impact the measurement of net

income on the income statement

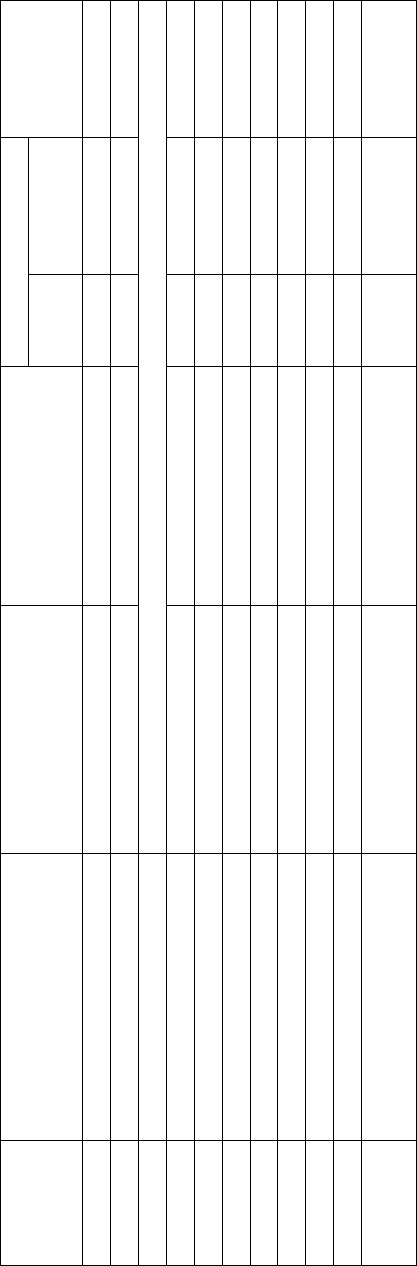

Bring to Class

Before Class After Class Course Assignment

Date Topic Readings 6e Practice Problems 6e Pack Supplement Due

3/7 (Mon) Accounts Receivable I 5-21 to 5-27 Q5-2, M5-18, 19, 20, 21 2 3

3/9 (Wed) Accounts Receivable II HP 10K (Item 1) E5-44, P5-58 2 3

3/14 & 3/16 Spring Break

3/21 (Mon) Fixed Assets I 6-20 to 6-24; 6-31 to 6-33 Q6-7, 8, M6-17, 19 2 3

3/22 (Tue) Assignment 3 TA Office Hours 3

3/23 (Wed) Exam I Review 1 & 2

3/27 (Sun) Optional Q&A Session

3/28 (Mon) Exam I

3/30 (Wed) Fixed Assets II United Tech. 10K (Item 1) E6-32, 36, 37, P6-43, 44 2 3

4/4 (Mon) Present Value Appendix 7A 2 3

4/4 (Mon)

Leases

10-3 to 10-12 Q10-1, 2, 3, M10-14 15

2 3

4/6 (Wed) American 10K (Item 1) E10-28, 30, P10-40

3. In this section of the course, you will learn how to use company disclosures to forecast financial

statements and value a firm. We will:

• Learn how the various financial statement ratios combine to provide a structured framework from which you

can forecast future performance and calibrate its reasonableness

• Understand the importance of sales to forecasting future financial statements

• Learn how to identify the critical forecasting assumptions

• Understand the difference between income flows and cash flows

• Understand equity value is a simple summation of the discounted expected future net distributions of cash to

equity holders

• Understand the assumptions of the discounted cash flow (DCF) valuation method

• Understand the principles behind estimating a terminal value and choosing a discount rate

• Learn some valuation heuristics, or shortcuts, to estimate a company’s value or to compare it to a peer (e.g.,

Price-Earnings ratio, Market-to-Book ratio, and PEG ratio)

• Understand the assumptions behind some common valuation heuristics and how to leverage these heuristics

when performing macro-level analysis of firms

• Learn how to convert analyst forecasts into a simple valuation heuristic

• Understand the intuition supporting the use of the P/E ratio

• Learn how to “anchor” valuation on current earnings

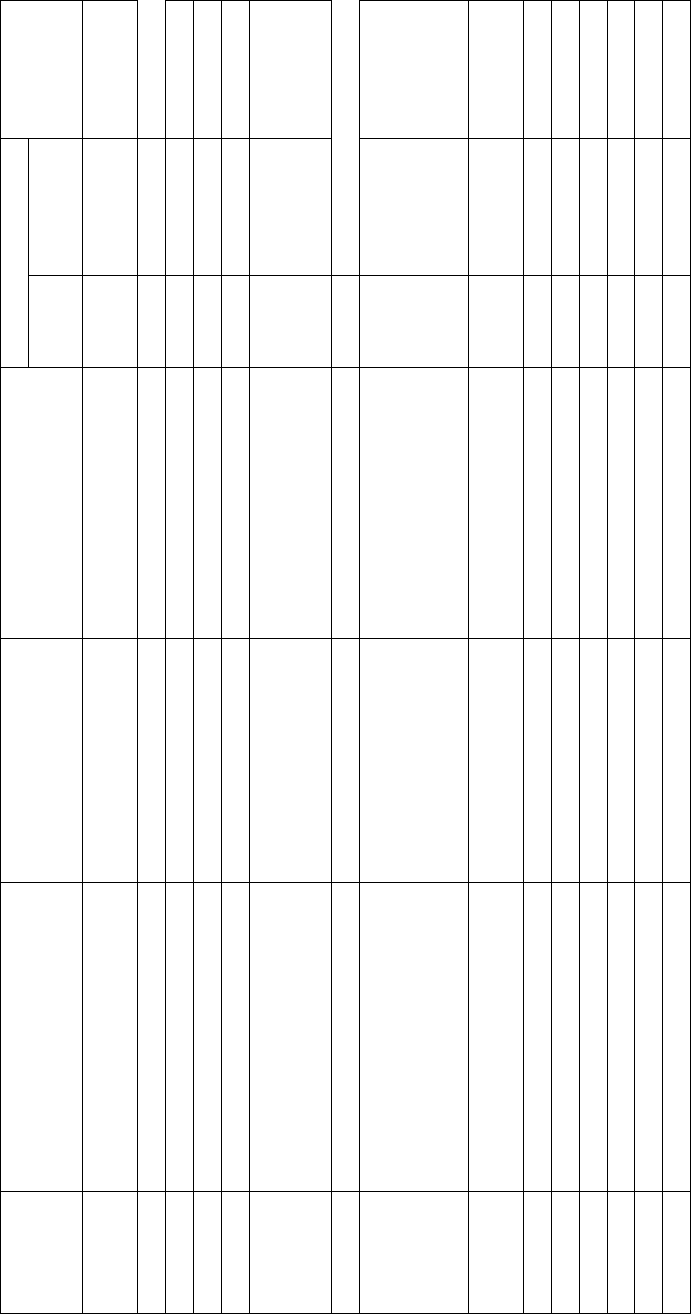

Bring to Class

Before Class After Class Course Assignment

Date Topic Readings 6e Practice Problems 6e Pack Supplement Due

4/11 (Mon) Conference Call

Starbucks Press Release

3 4

Starbucks MD&A

4/12 (Tue) Assignment 4 TA Office Hours

4/13 (Wed) Forecasting Revenues Mod. 11 3 4 4

4/18 (Mon) Forecasting Financial Stmts Appendix 11C Q11-7, M11-11, E11-30 3 4

4/20 (Wed) Forecast Reasonableness 3 4

4/25 (Mon) Cost of Capital

12-10 to 12-17 Q12-3, 6, 7, M12-15, 20,

21, E12-30, 31, 3 4

P12-39, 40

4/24 (Tue) Assignment 5 TA Office Hours

4/27 (Wed)

Discounted Cash Flow

13-4 to 14-14 Q13-3, M13-8, E13-10, 13,

3 4 5

P13-14

Residual Income Model

14-6 to 14-9 Q14-5, M14-10, E14-18, 21,

& Appendix 13B P14-26

5/2 (Mon) Market-Based Valuation

15-3 to 15-11 Q15-1, 2, M15-8, 10, 12, 16,

3 4

E15-23, 24, 27, 33, P15-37

5/3 (Tue) Assignment 6 TA Office Hours

5/4 (Wed) Exam II Review 2 & 3 6

5/9 (Mon) In-class Q&A Session 2 & 3

TBD Exam II @ TBD (11:00 Section)

TBD Exam II @ TBD (2:00 Section)

TBD Exam II @ TBD (3:30 Section)