NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-1

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

Table of Contents

Section 1. Purpose

Section 2. Scope

Section 3. Authority

Section 4. Exemptions

Section 5. Definitions

Section 6. Duties of Insurers and Producers

Section 7. Producer Training

Section 8. Compliance Mitigation; Penalties; Enforcement

Section 9. Recordkeeping

Section 10. Effective Date

Appendix A. Insurance Agent (Producer) Disclosure For Annuities

Appendix B. Consumer Refusal to Provide Information

Appendix C. Consumer Decision to Purchase an Annuity Not Based on a Recommendation

Section 1. Purpose

A. The purpose of this regulation is to require producers, as defined in this regulation, to act in the best interest

of the consumer when making a recommendation of an annuity and to require insurers to establish and

maintain a system to supervise recommendations so that the insurance needs and financial objectives of

consumers at the time of the transaction are effectively addressed.

B. Nothing herein shall be construed to create or imply a private cause of action for a violation of this regulation

or to subject a producer to civil liability under the best interest standard of care outlined in Section 6 of this

regulation or under standards governing the conduct of a fiduciary or a fiduciary relationship.

Drafting Note: The language of Subsection B comes from the NAIC Unfair Trade Practices Act (#880). If a state has adopted different language, it should

be substituted for Subsection B.

Drafting Note: Section 989J of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank Act”) specifically refers to this

model regulation as the “Suitability in Annuity Transactions Model Regulation” (#275). Section 989J of the Dodd-Frank Act confirmed this exemption of

certain annuities from the Securities Act of 1933 and confirmed state regulatory authority. This regulation is a successor regulation that exceeds the

requirements of the 2010 model regulation.

Section 2. Scope

This regulation shall apply to any sale or recommendation of an annuity.

Section 3. Authority

This regulation is issued under the authority of [insert reference to enabling legislation].

Drafting Note: States may wish to use the Unfair Trade Practices Act (#880) as enabling legislation or may pass a law with specific authority to adopt this

regulation.

Section 4. Exemptions

Unless otherwise specifically included, this regulation shall not apply to transactions involving:

A. Direct response solicitations where there is no recommendation based on information collected from the

consumer pursuant to this regulation;

B. Contracts used to fund:

(1) An employee pension or welfare benefit plan that is covered by the Employee Retirement and

Income Security Act (ERISA);

Suitability in Annuity Transactions Model Regulation

275-2

© 2020 National Association of Insurance Commissioners

(2) A plan described by Sections 401(a), 401(k), 403(b), 408(k) or 408(p) of the Internal Revenue Code

(IRC), as amended, if established or maintained by an employer;

(3) A government or church plan defined in section 414 of the IRC, a government or church welfare

benefit plan, or a deferred compensation plan of a state or local government or tax-exempt

organization under Section 457 of the IRC; or

(4) A nonqualified deferred compensation arrangement established or maintained by an employer or

plan sponsor.

C. Settlements of or assumptions of liabilities associated with personal injury litigation or any dispute or claim

resolution process; or

D. Formal prepaid funeral contracts.

Section 5. Definitions

A. “Annuity” means an annuity that is an insurance product under state law that is individually solicited, whether

the product is classified as an individual or group annuity.

B. “Cash compensation” means any discount, concession, fee, service fee, commission, sales charge, loan,

override, or cash benefit received by a producer in connection with the recommendation or sale of an annuity

from an insurer, intermediary, or directly from the consumer.

C. “Consumer profile information” means information that is reasonably appropriate to determine whether a

recommendation addresses the consumer’s financial situation, insurance needs and financial objectives,

including, at a minimum, the following:

(1) Age;

(2) Annual income;

(3) Financial situation and needs, including debts and other obligations;

(4) Financial experience;

(5) Insurance needs;

(6) Financial objectives;

(7) Intended use of the annuity;

(8) Financial time horizon;

(9) Existing assets or financial products, including investment, annuity and insurance holdings;

(10) Liquidity needs;

(11) Liquid net worth;

(12) Risk tolerance, including but not limited to, willingness to accept non-guaranteed elements in the

annuity;

(13) Financial resources used to fund the annuity; and

(14) Tax status.

D. “Continuing education credit” or “CE credit” means one continuing education credit as defined in [insert

reference in state law or regulations governing producer continuing education course approval].

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-3

E. “Continuing education provider” or “CE provider” means an individual or entity that is approved to offer

continuing education courses pursuant to [insert reference in state law or regulations governing producer

continuing education course approval].

F. “FINRA” means the Financial Industry Regulatory Authority or a succeeding agency.

G. “Insurer” means a company required to be licensed under the laws of this state to provide insurance products,

including annuities.

H. “Intermediary” means an entity contracted directly with an insurer or with another entity contracted with an

insurer to facilitate the sale of the insurer’s annuities by producers.

I. (1) “Material conflict of interest” means a financial interest of the producer in the sale of an annuity

that a reasonable person would expect to influence the impartiality of a recommendation.

(2) “Material conflict of interest” does not include cash compensation or non-cash compensation.

J. “Non-cash compensation” means any form of compensation that is not cash compensation, including, but not

limited to, health insurance, office rent, office support and retirement benefits.

K. “Non-guaranteed elements” means the premiums, credited interest rates (including any bonus), benefits,

values, dividends, non-interest based credits, charges or elements of formulas used to determine any of these,

that are subject to company discretion and are not guaranteed at issue. An element is considered non-

guaranteed if any of the underlying non-guaranteed elements are used in its calculation.

L. “Producer” means a person or entity required to be licensed under the laws of this state to sell, solicit or

negotiate insurance, including annuities. For purposes of this regulation, “producer” includes an insurer

where no producer is involved.

M. (1) “Recommendation” means advice provided by a producer to an individual consumer that was

intended to result or does result in a purchase, an exchange or a replacement of an annuity in

accordance with that advice.

(2) Recommendation does not include general communication to the public, generalized customer

services assistance or administrative support, general educational information and tools,

prospectuses, or other product and sales material.

N. “Replacement” means a transaction in which a new annuity is to be purchased, and it is known or should be

known to the proposing producer, or to the proposing insurer whether or not a producer is involved, that by

reason of the transaction, an existing annuity or other insurance policy has been or is to be any of the

following:

(1) Lapsed, forfeited, surrendered or partially surrendered, assigned to the replacing insurer or otherwise

terminated;

(2) Converted to reduced paid-up insurance, continued as extended term insurance, or otherwise

reduced in value by the use of nonforfeiture benefits or other policy values;

(3) Amended so as to effect either a reduction in benefits or in the term for which coverage would

otherwise remain in force or for which benefits would be paid;

(4) Reissued with any reduction in cash value; or

(5) Used in a financed purchase.

Drafting Note: The definition of “replacement” above is derived from the NAIC Life Insurance and Annuities Replacement Model Regulation (#613). If a

state has a different definition for “replacement,” the state should either insert the text of that definition in place of the definition above or modify the definition

above to provide a cross-reference to the definition of “replacement” that is in state law or regulation.

Suitability in Annuity Transactions Model Regulation

275-4

© 2020 National Association of Insurance Commissioners

O. “SEC” means the United States Securities and Exchange Commission.

Section 6. Duties of Insurers and Producers

A. Best Interest Obligations. A producer, when making a recommendation of an annuity, shall act in the best

interest of the consumer under the circumstances known at the time the recommendation is made, without

placing the producer’s or the insurer’s financial interest ahead of the consumer’s interest. A producer has

acted in the best interest of the consumer if they have satisfied the following obligations regarding care,

disclosure, conflict of interest and documentation:

(1) (a) Care Obligation. The producer, in making a recommendation shall exercise reasonable

diligence, care and skill to:

(i) Know the consumer’s financial situation, insurance needs and financial

objectives;

(ii) Understand the available recommendation options after making a reasonable

inquiry into options available to the producer;

(iii) Have a reasonable basis to believe the recommended option effectively addresses

the consumer’s financial situation, insurance needs and financial objectives over

the life of the product, as evaluated in light of the consumer profile information;

and

(iv) Communicate the basis or bases of the recommendation.

(b) The requirements under Subparagraph (a) of this paragraph include making reasonable

efforts to obtain consumer profile information from the consumer prior to the

recommendation of an annuity.

(c) The requirements under Subparagraph (a) of this paragraph require a producer to consider

the types of products the producer is authorized and licensed to recommend or sell that

address the consumer’s financial situation, insurance needs and financial objectives. This

does not require analysis or consideration of any products outside the authority and license

of the producer or other possible alternative products or strategies available in the market

at the time of the recommendation. Producers shall be held to standards applicable to

producers with similar authority and licensure.

(d) The requirements under this subsection do not create a fiduciary obligation or relationship

and only create a regulatory obligation as established in this regulation.

(e) The consumer profile information, characteristics of the insurer, and product costs, rates,

benefits and features are those factors generally relevant in making a determination

whether an annuity effectively addresses the consumer’s financial situation, insurance

needs and financial objectives, but the level of importance of each factor under the care

obligation of this paragraph may vary depending on the facts and circumstances of a

particular case. However, each factor may not be considered in isolation.

(f) The requirements under Subparagraph (a) of this paragraph include having a reasonable

basis to believe the consumer would benefit from certain features of the annuity, such as

annuitization, death or living benefit or other insurance-related features.

(g) The requirements under Subparagraph (a) of this paragraph apply to the particular annuity

as a whole and the underlying subaccounts to which funds are allocated at the time of

purchase or exchange of an annuity, and riders and similar producer enhancements, if any.

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-5

(h) The requirements under Subparagraph (a) of this paragraph do not mean the annuity with

the lowest one-time or multiple occurrence compensation structure shall necessarily be

recommended.

(i) The requirements under Subparagraph (a) of this paragraph do not mean the producer has

ongoing monitoring obligations under the care obligation under this paragraph, although

such an obligation may be separately owed under the terms of a fiduciary, consulting,

investment advising or financial planning agreement between the consumer and the

producer.

(j) In the case of an exchange or replacement of an annuity, the producer shall consider the

whole transaction, which includes taking into consideration whether:

(i) The consumer will incur a surrender charge, be subject to the commencement of

a new surrender period, lose existing benefits, such as death, living or other

contractual benefits, or be subject to increased fees, investment advisory fees or

charges for riders and similar product enhancements;

(ii) The replacing product would substantially benefit the consumer in comparison to

the replaced product over the life of the product; and

(iii) The consumer has had another annuity exchange or replacement and, in particular,

an exchange or replacement within the preceding 60 months.

(k) Nothing in this regulation should be construed to require a producer to obtain any license

other than a producer license with the appropriate line of authority to sell, solicit or

negotiate insurance in this state, including but not limited to any securities license, in order

to fulfill the duties and obligations contained in this regulation; provided the producer does

not give advice or provide services that are otherwise subject to securities laws or engage

in any other activity requiring other professional licenses.

(2) Disclosure obligation.

(a) Prior to the recommendation or sale of an annuity, the producer shall prominently disclose

to the consumer on a form substantially similar to Appendix A:

(i) A description of the scope and terms of the relationship with the consumer and

the role of the producer in the transaction;

(ii) An affirmative statement on whether the producer is licensed and authorized to

sell the following products:

(I) Fixed annuities;

(II) Fixed indexed annuities;

(III) Variable annuities;

(IV) Life insurance;

(V) Mutual funds;

(VI) Stocks and bonds; and

(VII) Certificates of deposit;

Suitability in Annuity Transactions Model Regulation

275-6

© 2020 National Association of Insurance Commissioners

(iii) An affirmative statement describing the insurers the producer is authorized,

contracted (or appointed), or otherwise able to sell insurance products for, using

the following descriptions:

(I) From one insurer;

(II) From two or more insurers; or

(III) From two or more insurers although primarily contracted with one

insurer.

(iv) A description of the sources and types of cash compensation and non-cash

compensation to be received by the producer, including whether the producer is

to be compensated for the sale of a recommended annuity by commission as part

of premium or other remuneration received from the insurer, intermediary or other

producer or by fee as a result of a contract for advice or consulting services; and

(v) A notice of the consumer’s right to request additional information regarding cash

compensation described in Subparagraph (b) of this paragraph;

Drafting Note: If a state approves forms, a state should add language to Subparagraph (a) reflecting such approvals.

(b) Upon request of the consumer or the consumer’s designated representative, the producer

shall disclose:

(i) A reasonable estimate of the amount of cash compensation to be received by the

producer, which may be stated as a range of amounts or percentages; and

(ii) Whether the cash compensation is a one-time or multiple occurrence amount, and

if a multiple occurrence amount, the frequency and amount of the occurrence,

which may be stated as a range of amounts or percentages; and

(c) Prior to or at the time of the recommendation or sale of an annuity, the producer shall have

a reasonable basis to believe the consumer has been informed of various features of the

annuity, such as the potential surrender period and surrender charge, potential tax penalty

if the consumer sells, exchanges, surrenders or annuitizes the annuity, mortality and

expense fees, investment advisory fees, any annual fees, potential charges for and features

of riders or other options of the annuity, limitations on interest returns, potential changes

in non-guaranteed elements of the annuity, insurance and investment components and

market risk.

Drafting Note: If a state has adopted the NAIC Annuity Disclosure Model Regulation (#245), the state should insert an additional phrase in Subparagraph (c)

above to explain that the requirements of this section are intended to supplement and not replace the disclosure requirements of the NAIC Annuity Disclosure

Model Regulation (#245).

(3) Conflict of interest obligation. A producer shall identify and avoid or reasonably manage and

disclose material conflicts of interest, including material conflicts of interest related to an ownership

interest.

(4) Documentation obligation. A producer shall at the time of recommendation or sale:

(a) Make a written record of any recommendation and the basis for the recommendation

subject to this regulation;

(b) Obtain a consumer signed statement on a form substantially similar to Appendix B

documenting:

(i) A customer’s refusal to provide the consumer profile information, if any; and

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-7

(ii) A customer’s understanding of the ramifications of not providing his or her

consumer profile information or providing insufficient consumer profile

information; and

(c) Obtain a consumer signed statement on a form substantially similar to Appendix C

acknowledging the annuity transaction is not recommended if a customer decides to enter

into an annuity transaction that is not based on the producer’s recommendation.

Drafting Note: If a state approves forms, a state should add language to Subparagraphs (b) and (c) of this paragraph reflecting such approvals.

(5) Application of the best interest obligation. Any requirement applicable to a producer under this

subsection shall apply to every producer who has exercised material control or influence in the

making of a recommendation and has received direct compensation as a result of the

recommendation or sale, regardless of whether the producer has had any direct contact with the

consumer. Activities such as providing or delivering marketing or educational materials, product

wholesaling or other back office product support, and general supervision of a producer do not, in

and of themselves, constitute material control or influence.

B. Transactions not based on a recommendation.

(1) Except as provided under Paragraph (2), a producer shall have no obligation to a consumer under

Subsection A(1) related to any annuity transaction if:

(a) No recommendation is made;

(b) A recommendation was made and was later found to have been prepared based on

materially inaccurate information provided by the consumer;

(c) A consumer refuses to provide relevant consumer profile information and the annuity

transaction is not recommended; or

(d) A consumer decides to enter into an annuity transaction that is not based on a

recommendation of the producer.

(2) An insurer’s issuance of an annuity subject to Paragraph (1) shall be reasonable under all the

circumstances actually known to the insurer at the time the annuity is issued.

C. Supervision system.

(1) Except as permitted under Subsection B, an insurer may not issue an annuity recommended to a

consumer unless there is a reasonable basis to believe the annuity would effectively address the

particular consumer’s financial situation, insurance needs and financial objectives based on the

consumer’s consumer profile information.

(2) An insurer shall establish and maintain a supervision system that is reasonably designed to achieve

the insurer’s and its producers’ compliance with this regulation, including, but not limited to, the

following:

(a) The insurer shall establish and maintain reasonable procedures to inform its producers of

the requirements of this regulation and shall incorporate the requirements of this regulation

into relevant producer training manuals;

(b) The insurer shall establish and maintain standards for producer product training and shall

establish and maintain reasonable procedures to require its producers to comply with the

requirements of Section 7 of this regulation;

(c) The insurer shall provide product-specific training and training materials which explain all

material features of its annuity products to its producers;

Suitability in Annuity Transactions Model Regulation

275-8

© 2020 National Association of Insurance Commissioners

(d) The insurer shall establish and maintain procedures for the review of each recommendation

prior to issuance of an annuity that are designed to ensure there is a reasonable basis to

determine that the recommended annuity would effectively address the particular

consumer’s financial situation, insurance needs and financial objectives. Such review

procedures may apply a screening system for the purpose of identifying selected

transactions for additional review and may be accomplished electronically or through other

means including, but not limited to, physical review. Such an electronic or other system

may be designed to require additional review only of those transactions identified for

additional review by the selection criteria;

(e) The insurer shall establish and maintain reasonable procedures to detect recommendations

that are not in compliance with Subsections A, B, D and E. This may include, but is not

limited to, confirmation of the consumer’s consumer profile information, systematic

customer surveys, producer and consumer interviews, confirmation letters, producer

statements or attestations and programs of internal monitoring. Nothing in this

subparagraph prevents an insurer from complying with this subparagraph by applying

sampling procedures, or by confirming the consumer profile information or other required

information under this section after issuance or delivery of the annuity;

(f) The insurer shall establish and maintain reasonable procedures to assess, prior to or upon

issuance or delivery of an annuity, whether a producer has provided to the consumer the

information required to be provided under this section;

(g) The insurer shall establish and maintain reasonable procedures to identify and address

suspicious consumer refusals to provide consumer profile information;

(h) The insurer shall establish and maintain reasonable procedures to identify and eliminate

any sales contests, sales quotas, bonuses, and non-cash compensation that are based on the

sales of specific annuities within a limited period of time. The requirements of this

subparagraph are not intended to prohibit the receipt of health insurance, office rent, office

support, retirement benefits or other employee benefits by employees as long as those

benefits are not based upon the volume of sales of a specific annuity within a limited period

of time; and

Drafting Note: The intent of Subparagraph (h) is to prohibit sales contests, sales quotas, bonuses and non-cash compensation based on the sale of a particular

product within a limited period of time, but not to prohibit general incentives regarding the sales of a company’s products with no emphasis on any particular

product.

(i) The insurer shall annually provide a written report to senior management, including to the

senior manager responsible for audit functions, which details a review, with appropriate

testing, reasonably designed to determine the effectiveness of the supervision system, the

exceptions found, and corrective action taken or recommended, if any.

(3) (a) Nothing in this subsection restricts an insurer from contracting for performance of a

function (including maintenance of procedures) required under this subsection. An insurer

is responsible for taking appropriate corrective action and may be subject to sanctions and

penalties pursuant to Section 8 of this regulation regardless of whether the insurer contracts

for performance of a function and regardless of the insurer’s compliance with

Subparagraph (b) of this paragraph.

(b) An insurer’s supervision system under this subsection shall include supervision of

contractual performance under this subsection. This includes, but is not limited to, the

following:

(i) Monitoring and, as appropriate, conducting audits to assure that the contracted

function is properly performed; and

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-9

(ii) Annually obtaining a certification from a senior manager who has responsibility

for the contracted function that the manager has a reasonable basis to represent,

and does represent, that the function is properly performed.

(4) An insurer is not required to include in its system of supervision:

(a) A producer’s recommendations to consumers of products other than the annuities offered

by the insurer; or

(b) Consideration of or comparison to options available to the producer or compensation

relating to those options other than annuities or other products offered by the insurer.

D. Prohibited Practices. Neither a producer nor an insurer shall dissuade, or attempt to dissuade, a consumer

from:

(1) Truthfully responding to an insurer’s request for confirmation of the consumer profile information;

(2) Filing a complaint; or

(3) Cooperating with the investigation of a complaint.

E. Safe harbor.

(1) Recommendations and sales of annuities made in compliance with comparable standards shall

satisfy the requirements under this regulation. This subsection applies to all recommendations and

sales of annuities made by financial professionals in compliance with business rules, controls and

procedures that satisfy a comparable standard even if such standard would not otherwise apply to

the product or recommendation at issue. However, nothing in this subsection shall limit the

insurance commissioner’s ability to investigate and enforce the provisions of this regulation.

Drafting Note: Non-compliance with comparable standards means that the recommendation or sale is subject to compliance with the requirements of this

regulation.

(2) Nothing in Paragraph (1) shall limit the insurer’s obligation to comply with Section 6C(1) of this

regulation, although the insurer may base its analysis on information received from either the

financial professional or the entity supervising the financial professional.

(3) For paragraph (1) to apply, an insurer shall:

(a) Monitor the relevant conduct of the financial professional seeking to rely on Paragraph (1)

or the entity responsible for supervising the financial professional, such as the financial

professional’s broker-dealer or an investment adviser registered under federal [or state]

securities laws using information collected in the normal course of an insurer’s business;

and

(b) Provide to the entity responsible for supervising the financial professional seeking to rely

on Paragraph (1), such as the financial professional’s broker-dealer or investment adviser

registered under federal [or state] securities laws, information and reports that are

reasonably appropriate to assist such entity to maintain its supervision system.

(4) For purposes of this subsection, “financial professional” means a producer that is regulated and

acting as:

(a) A broker-dealer registered under federal [or state] securities laws or a registered

representative of a broker-dealer;

Suitability in Annuity Transactions Model Regulation

275-10

© 2020 National Association of Insurance Commissioners

(b) An investment adviser registered under federal [or state] securities laws or an investment

adviser representative associated with the federal [or state] registered investment adviser;

or

(c) A plan fiduciary under Section 3(21) of the Employee Retirement Income Security Act of

1974 (ERISA) or fiduciary under Section 4975(e)(3) of the Internal Revenue Code (IRC)

or any amendments or successor statutes thereto.

Drafting Note: The requirement that a producer be “regulated and acting” as a broker-dealer, a registered representative of a broker-dealer, an investment

adviser, an investment adviser representative or a plan fiduciary means that a producer who is not explicitly acting in compliance with the relevant comparable

standards, as specified in Paragraph (4) below, is not eligible for this safe harbor and is subject to compliance with the requirements of this regulation.

(5) For purposes of this subsection, “comparable standards” means:

(a) With respect to broker-dealers and registered representatives of broker-dealers, applicable

SEC and FINRA rules pertaining to best interest obligations and supervision of annuity

recommendations and sales, including, but not limited to, Regulation Best Interest and any

amendments or successor regulations thereto;

(b) With respect to investment advisers registered under federal [or state] securities laws or

investment adviser representatives, the fiduciary duties and all other requirements imposed

on such investment advisers or investment adviser representatives by contract or under the

Investment Advisers Act of 1940 [or applicable state securities law], including but not

limited to, the Form ADV and interpretations; and

Drafting Note: State-registered investment advisers in this safe harbor are included in brackets so that each individual state that implements this model

regulation may determine whether to include the state-regulated investment advisers. Given the varying treatment of annuities, particularly variable annuities,

under state law, the varying structures of state securities and insurance departments, and the varying levels of cooperation between the two agencies, this is a

decision best made in each individual state.

(c) With respect to plan fiduciaries or fiduciaries, means the duties, obligations, prohibitions

and all other requirements attendant to such status under ERISA or the IRC and any

amendments or successor statutes thereto.

Section 7. Producer Training

A. A producer shall not solicit the sale of an annuity product unless the producer has adequate knowledge of the

product to recommend the annuity and the producer is in compliance with the insurer’s standards for product

training. A producer may rely on insurer-provided product-specific training standards and materials to

comply with this subsection.

B. (1) (a) A producer who engages in the sale of annuity products shall complete a one-time four (4)

credit training course approved by the department of insurance and provided by the

department of insurance-approved education provider.

(b) Producers who hold a life insurance line of authority on the effective date of this regulation

and who desire to sell annuities shall complete the requirements of this subsection within

six (6) months after the effective date of this regulation. Individuals who obtain a life

insurance line of authority on or after the effective date of this regulation may not engage

in the sale of annuities until the annuity training course required under this subsection has

been completed.

(2) The minimum length of the training required under this subsection shall be sufficient to qualify for

at least four (4) CE credits but may be longer.

(3) The training required under this subsection shall include information on the following topics:

(a) The types of annuities and various classifications of annuities;

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-11

(b) Identification of the parties to an annuity;

(c) How product specific annuity contract features affect consumers;

(d) The application of income taxation of qualified and non-qualified annuities;

(e) The primary uses of annuities; and

(f) Appropriate standard of conduct, sales practices, replacement and disclosure requirements.

(4) Providers of courses intended to comply with this subsection shall cover all topics listed in the

prescribed outline and shall not present any marketing information or provide training on sales

techniques or provide specific information about a particular insurer’s products. Additional topics

may be offered in conjunction with and in addition to the required outline.

(5) A provider of an annuity training course intended to comply with this subsection shall register as a

CE provider in this state and comply with the rules and guidelines applicable to producer continuing

education courses as set forth in [insert reference to state law or regulations governing producer

continuing education course approval].

(6) A producer who has completed an annuity training course approved by the department of insurance

prior to [insert effective date of amended regulation] shall, within six (6) months after [insert

effective date of amended regulation], complete either:

(a) A new four (4) credit training course approved by the department of insurance after [insert

effective date of amended regulation]; or

(b) An additional one-time one (1) credit training course approved by the department of

insurance and provided by the department of insurance-approved education provider on

appropriate sales practices, replacement and disclosure requirements under this amended

regulation.

(7) Annuity training courses may be conducted and completed by classroom or self-study methods in

accordance with [insert reference to state law or regulations governing producer continuing

education course approval].

(8) Providers of annuity training shall comply with the reporting requirements and shall issue

certificates of completion in accordance with [insert reference to state law or regulations governing

producer continuing education course approval].

(9) The satisfaction of the training requirements of another state that are substantially similar to the

provisions of this subsection shall be deemed to satisfy the training requirements of this subsection

in this state.

(10) The satisfaction of the components of the training requirements of any course or courses with

components substantially similar to the provisions of this subsection shall be deemed to satisfy the

training requirements of this subsection in this state.

(11) An insurer shall verify that a producer has completed the annuity training course required under this

subsection before allowing the producer to sell an annuity product for that insurer. An insurer may

satisfy its responsibility under this subsection by obtaining certificates of completion of the training

course or obtaining reports provided by commissioner-sponsored database systems or vendors or

from a reasonably reliable commercial database vendor that has a reporting arrangement with

approved insurance education providers.

Suitability in Annuity Transactions Model Regulation

275-12

© 2020 National Association of Insurance Commissioners

Section 8. Compliance Mitigation; Penalties; Enforcement

A. An insurer is responsible for compliance with this regulation. If a violation occurs, either because of the

action or inaction of the insurer or its producer, the commissioner may order:

(1) An insurer to take reasonably appropriate corrective action for any consumer harmed by a failure to

comply with this regulation by the insurer, an entity contracted to perform the insurer’s supervisory

duties or by the producer;

(2) A general agency, independent agency or the producer to take reasonably appropriate corrective

action for any consumer harmed by the producer’s violation of this regulation; and

(3) Appropriate penalties and sanctions.

B. Any applicable penalty under [insert statutory citation] for a violation of this regulation may be reduced or

eliminated [, according to a schedule adopted by the commissioner,] if corrective action for the consumer

was taken promptly after a violation was discovered or the violation was not part of a pattern or practice.

Drafting Note: Subsection B above is intended to be consistent with the commissioner’s discretionary authority to determine the appropriate penalty for a

violation of this regulation. The language of Subsection B is not intended to require that a commissioner impose a penalty on an insurer for a single violation

of this regulation if the commissioner has determined that such a penalty is not appropriate.

Drafting Note: A state that has authority to adopt a schedule of penalties may wish to include the words in brackets. In that case, “shall” should be substituted

for “may” in the same sentence. States should consider inserting a reference to the NAIC Unfair Trade Practices Act (#880) or the state’s statute that authorizes

the commissioner to impose penalties and fines.

C. The authority to enforce compliance with this regulation is vested exclusively with the commissioner.

Section 9. Recordkeeping

A. Insurers, general agents, independent agencies and producers shall maintain or be able to make available to

the commissioner records of the information collected from the consumer, disclosures made to the consumer,

including summaries of oral disclosures, and other information used in making the recommendations that

were the basis for insurance transactions for [insert number] years after the insurance transaction is completed

by the insurer. An insurer is permitted, but shall not be required, to maintain documentation on behalf of a

producer.

Drafting Note: States should review their current record retention laws and specify a time period that is consistent with those laws. For some states this time

period may be five (5) years.

B. Records required to be maintained by this regulation may be maintained in paper, photographic, micro-

process, magnetic, mechanical or electronic media or by any process that accurately reproduces the actual

document.

Drafting Note: This section may be unnecessary in states that have a comprehensive recordkeeping law or regulation.

Section 10. Effective Date

The amendments to this regulation shall take effect [X] months after the date the regulation is adopted or on [insert date],

whichever is later.

________________________________

Chronological Summary of Action (All references are to the Proceedings of the NAIC).

2003 Proc. 3

rd

Quarter 17-18, 24-27, 32, 213 (adopted).

2006 Proc. 2

nd

Quarter 40, 90 (amended).

2010 Proc. 1

st

Quarter Vol. I 105-106, 117, 129-139, 146-159, 313 (amended).

2015 Proc. 1

st

Quarter, Vol. I 117-118, 131-134, 326-335, 431 (amended).

2020 Proc. Spring (amended).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-13

APPENDIX A

INSURANCE AGENT (PRODUCER) DISCLOSURE FOR ANNUITIES

Do Not Sign Unless You Have Read and Understand the Information in this Form

Date: ________________________

INSURANCE AGENT (PRODUCER) INFORMATION (“Me”, “I”, “My”)

First Name: _________________________________________ Last Name: _____________________________________

Business\Agency Name: ___________________________________ Website: ___________________________________

Business Mailing Address:_____________________________________________________________________________

Business Telephone Number: __________________________________________________________________________

Email Address:______________________________________________________________________________________

National Producer Number in [state]:_____________________________________________________________________

CUSTOMER INFORMATION (“You”, “Your”)

First Name: _______________________________________Last Name: ________________________________________

What Types of Products Can I Sell You?

I am licensed to sell annuities to You in accordance with state law.

If I recommend that You buy an annuity, it means I believe

that it effectively meets Your financial situation, insurance needs, and financial objectives. Other financial products, such as

life insurance or stocks, bonds and mutual funds, also may meet Your needs.

I offer the following products:

Fixed or Fixed Indexed Annuities

Variable Annuities

Life Insurance

I need a separate license to provide advice about or to sell non-insurance financial products. I have checked below any non-

insurance financial products that I am licensed and authorized to provide advice about or to sell.

Mutual Funds

Stocks/Bonds

Certificates of Deposits

Whose Annuities Can I Sell to You?

I am authorized to sell:

Annuities from Only One (1) Insurer

Annuities from Two or More Insurers

Annuities from Two or More Insurers

although I primarily sell annuities

from:_________________________

Suitability in Annuity Transactions Model Regulation

275-14

© 2020 National Association of Insurance Commissioners

How I’m Paid for My Work:

It’s important for You to understand how I’m paid for my work. Depending on the particular annuity You purchase, I may be

paid a commission or a fee. Commissions are generally paid to Me by the insurance company while fees are generally paid to

Me by the consumer. If You have questions about how I’m paid, please ask Me.

Depending on the particular annuity You buy, I will or may be paid cash compensation as follows:

Commission, which is usually paid by the insurance company or other sources. If other sources, describe:

__________________.

Fees (such as a fixed amount, an hourly rate, or a percentage of your payment), which are usually paid directly by the

customer.

Other (Describe):_______________________________________________________________________________.

If You have questions about the above compensation I will be paid for this transaction, please ask me.

I may also receive other indirect compensation resulting from this transaction (sometimes called “non-cash” compensation),

such as health or retirement benefits, office rent and support, or other incentives from the insurance company or other sources.

Drafting Note: This disclosure may be adapted to fit the particular business model of the producer. As an example, if the producer only receives commission

or only receives a fee from the consumer, the disclosure may be refined to fit that particular situation. This form is intended to provide an example of how to

communicate producer compensation, but compliance with the regulation may also be achieved with more precise disclosure, including a written consulting,

advising or financial planning agreement.

Drafting Note: The acknowledgement and signature should be in immediate proximity to the disclosure language.

By signing below, You acknowledge that You have read and understand the information provided to You in this document.

________________________________________________

Customer Signature

________________________________________________

Date

________________________________________________

Agent (Producer) Signature

________________________________________________

Date

NAIC Model Laws, Regulations, Guidelines and Other Resources—Spring 2020

© 2020 National Association of Insurance Commissioners 275-15

APPENDIX B

CONSUMER REFUSAL TO PROVIDE INFORMATION

Do Not Sign Unless You Have Read and Understand the Information in this Form

Why are You being given this form?

You’re buying a financial product – an annuity.

To recommend a product that effectively meets Your needs, objectives and situation, the agent, broker, or company needs

information about You, Your financial situation, insurance needs and financial objectives.

If You sign this form, it means You have not given the agent, broker, or company some or all the information needed to

decide if the annuity effectively meets Your needs, objectives and situation. You may lose protections under the Insurance

Code of [this state] if You sign this form or provide inaccurate information.

Statement of Purchaser:

I REFUSE

to provide this information at this time.

I have chosen to provide LIMITED information at this time.

________________________________________________

Customer Signature

________________________________________________

Date

Suitability in Annuity Transactions Model Regulation

275-16

© 2020 National Association of Insurance Commissioners

APPENDIX C

Consumer Decision to Purchase an Annuity NOT Based on a Recommendation

Do Not Sign This Form Unless You Have Read and Understand It.

Why are You being given this form? You are buying a financial product – an annuity.

To recommend a product that effectively meets your needs, objectives and situation, the agent, broker, or company has the

responsibility to learn about You, your financial situation, insurance needs and financial objectives.

If You sign this form, it means You know that you’re buying an annuity that was not recommended.

Statement of Purchaser:

I understand that I am buying an annuity, but the agent, broker or company did not recommend that I buy it. If I buy it

without a recommendation, I understand I may lose protections under the Insurance Code of [this state].

________________________________________________

Customer Signature

________________________________________________

Date

________________________________________________

Agent/Producer Signature

________________________________________________

Date

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

© 2020 National Association of Insurance Commissioners ST-275-1

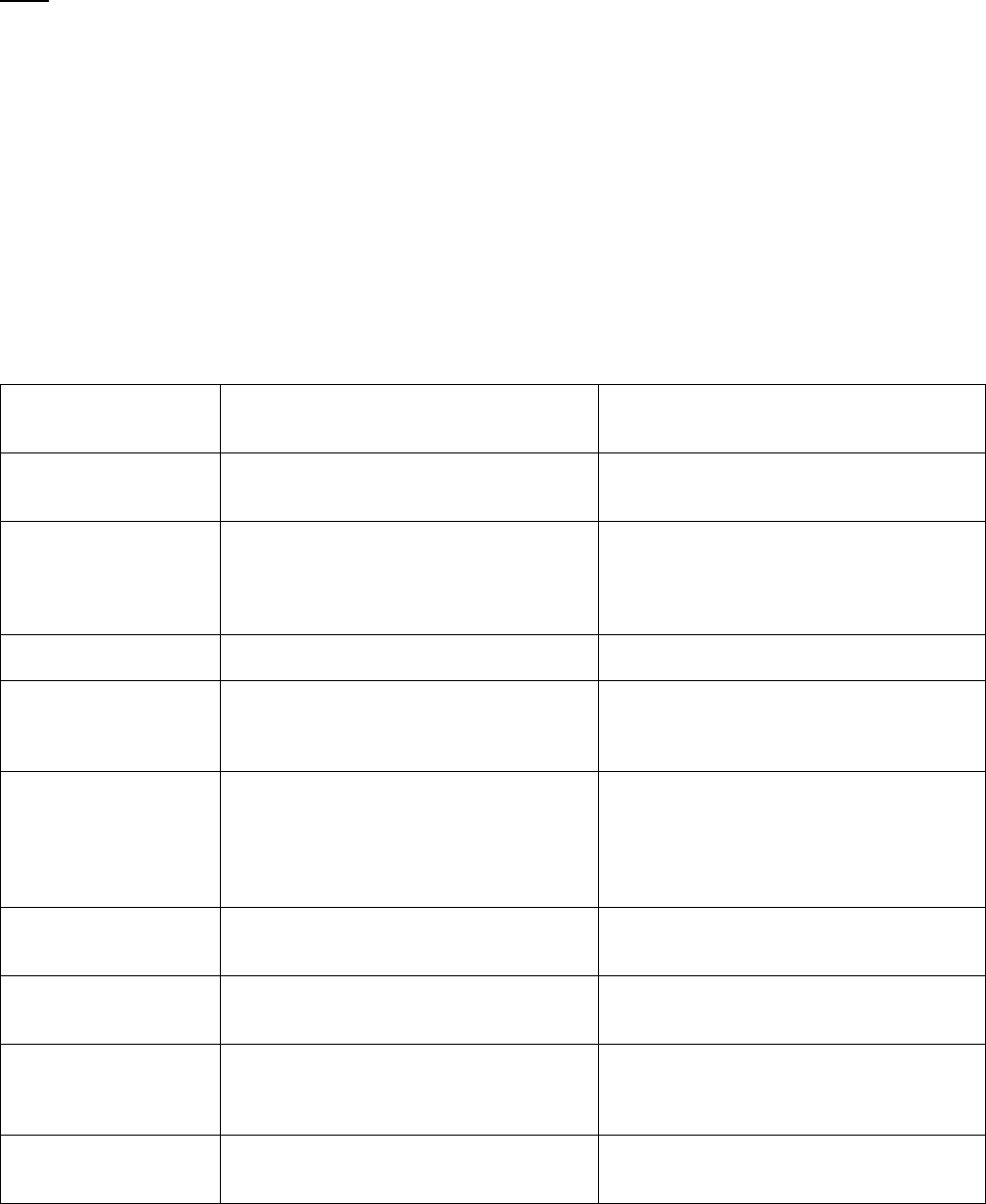

This chart is intended to provide readers with additional information to more easily access state statutes, regulations,

bulletins or administrative rulings related to the NAIC model. Such guidance provides readers with a starting point

from which they may review how each state has addressed the model and the topic being covered. The NAIC Legal

Division has reviewed each state’s activity in this area and has determined whether the citation most appropriately

fits in the Model Adoption column or Related State Activity column based on the definitions listed below. The NAIC’s

interpretation may or may not be shared by the individual states or by interested readers.

This chart does not constitute a formal legal opinion by the NAIC staff on the provisions of state law and should not

be relied upon as such. Nor does this state page reflect a determination as to whether a state meets any applicable

accreditation standards. Every effort has been made to provide correct and accurate summaries to assist readers in

locating useful information. Readers should consult state law for further details and for the most current information.

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

ST-275-2

© 2020 National Association of Insurance Commissioners

This page is intentionally left blank

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

© 2020 National Association of Insurance Commissioners ST-275-3

KEY:

MODEL ADOPTION: States that have citations identified in this column adopted the most recent version of the NAIC

model in a substantially similar manner. This requires states to adopt the model in its entirety but does allow for variations

in style and format. States that have adopted portions of the current NAIC model will be included in this column with an

explanatory note.

RELATED STATE ACTIVITY: Examples of Related State Activity include but are not limited to: older versions of the

NAIC model, statutes or regulations addressing the same subject matter, or other administrative guidance such as bulletins

and notices. States that have citations identified in this column only (and nothing listed in the Model Adoption column) have

not adopted the most recent version of the NAIC model in a substantially similar manner.

NO CURRENT ACTIVITY: No state activity on the topic as of the date of the most recent update. This includes states that

have repealed legislation as well as states that have never adopted legislation.

*Model Adoption refers to the 2010 version of the model. States that have citations identified in the Model Adoption

column have laws substantially similar to the NAIC’s 2010 version of the model regulation.

NAIC MEMBER

MODEL ADOPTION RELATED STATE ACTIVITY

Alabama

A

LA

.

A

DMIN

.

C

ODE

r. § 482-1-137

(2006/2016) (previous version of model).

Alaska

A

LASKA

A

DMIN

.

C

ODE

tit. 3,

§§

26.770 to

26.789 (2008/2014) (previous version of

model); B

ULLETIN 2008-4 (2008);

BULLETIN 2009-7 (2009).

American Samoa

NO CURRENT ACTIVITY

Arizona

S.B.

1557

(2020).

A

RIZ

.

R

EV

.

S

TAT

.

A

NN

.

§§ 20-1243.01 to

1243.07 (2006/2017) (portions of previous

version of model).

Arkansas

A

RK

.

A

DMIN

.

C

ODE

§§

054.00.82-1

to

054.00.82-10. (2004/2009) (previous version

of model); D

IRECTIVE 2-2006 (2006);

BULLETIN 11-2009 (2009);

B

ULLETIN 5-2010 (2010).

California

C

AL

.

I

NS

.

C

ODE

§§ 10509.910 to 10509.918

(1990/2016) (previous version of model).

Colorado

3

C

OLO

.

C

ODE

R

EGS

.

§

702-4:4-1-11

(2004/2011) (previous version of model).

Connecticut

CONN. AGENCIES REGS. §§ 38a-432A-1 to

38a-432A-8 (2005/2012) (previous version of

model); L

ICENSING BULLETIN L-18 (2012).

Delaware

18 D

EL

.

C

ODE

R

EGS

. § 1214 (2006/2017)

(previous version of model).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

ST-275-4

© 2020 National Association of Insurance Commissioners

NAIC MEMBER

MODEL ADOPTION

RELATED STATE ACTIVITY

District of Columbia

D.C.

M

UN

.

R

EGS

.

tit. 26A, §§ 8400 to 8499

(2010/2011) (previous version of model).

Florida

F

LA

.

S

TAT

. § 627.4554 (2004/2013) (previous

version of model); FLA. ADMIN. CODE ANN.

R. 69B-162.011 (2009/2014) (forms required).

Georgia

G

A

.

C

OMP

.

R.

&

R

EGS

. 120-2-94-.01 to

120-2-94-.10 (2006/2015) (previous version

of model).

Guam

NO CURRENT ACTIVITY

Hawaii

H

AW

.

R

EV

.

S

TAT

.

§§ 431:10D-621 to

431:10D-626 (2008/2012) (previous version

of model); M

EMORANDUM 2011-2 (LC)

(2011).

Idaho

I

DAHO

A

DMIN

.

C

ODE

r. 18.01.09.001 to

18.01.09.025 (2005/2013) (previous version

of model); I

DAHO CODE ANN. § 41-1940

(2005/2008) (portions of previous version of

model and authority to adopt regulation).

Illinois

I

LL

.

A

DMIN

.

C

ODE

tit. 50, §§ 3120.10 to

3120.90 (2007/2011) (previous version of

model).

Indiana

760 I

ND

.

A

DMIN

.

C

ODE

1-72-1 to 1-72-6

(2006/2015) (previous version of model);

IND. CODE §§ 27-4-9-1 to 27-4-9-6

(2005/2007) (limited to seniors);

§ 27-1-15.6-19.5 (2011).

Iowa

I

OWA

A

DMIN

.

C

ODE

r. 191-15.72 to

191.15.78 (2006/2020).

I

OWA

A

DMIN

.

C

ODE

r. 191-15.8 (1963/2009)

(life and annuity sales guidelines); 191-33.3

(1984/1999) (variable life); B

ULLETIN 2007-5

(2007); B

ULLETIN 2009-4 (2009).

Kansas

K

AN

.

A

DMIN

.

R

EGS

. § 40-2-14a (2005/2013)

(previous version of model).

Kentucky

806 KY. ADMIN. REGS. 12:120 (2007/2012);

806 KY. ADMIN. REGS. 9:220 (2011) (previous

version of model).

Louisiana

L

A

.

A

DMIN

.

C

ODE

tit. 37, Pt. XIII §§ 11701 to

11719 (Reg. No. 89) (2006/2019) (portions of

previous version of model).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

© 2020 National Association of Insurance Commissioners ST-275-5

NAIC MEMBER

MODEL ADOPTION

RELATED STATE ACTIVITY

Maine

917

M

E

.

C

ODE

R.

§

02-031

(2007/2015)

(previous version of model); ME. REV. STAT.

ANN. tit. 24-A, § 2517 (1969/2005) (authority

to adopt regulation).

Maryland

M

D

.

C

ODE

R

EGS

. §§ 31.09.12.01 to

31.09.12.11 (2007/2011) (previous version of

model); B

ULLETIN 2011-28 (2011).

Massachusetts

211 M

ASS

.

C

ODE

R

EGS

.

96.01 to 96.10 (2016)

(previous version of model).

Michigan

M

ICH

.

C

OMP

.

L

AWS

A

NN

.

§§ 500.4151 to

500.4165 (2006/2013) (previous version of

model).

Minnesota

M

INN

.

S

TAT

.

A

NN

.

§§ 72A.20 to 72A.2036

(2012/2014) (portions of previous version of

model); §§

60K.46 to 60K.56 (2012/2017)

(portions of previous version of model);

§ 61A.021 (1985) (tying prohibited).

Mississippi

19

M

ISS

.

A

DMIN

.

C

ODE

.

R. Pt. 2, §§

18.01

to

18.11 (2013) (previous version of model);

BULLETIN 2014-7 (2014).

Missouri

MO. CODE REGS. ANN. tit. 20, § 400-5.900

(2017) (previous version of model);

MO. REV. STAT. § 376.671 (2010);

M

O. CODE REGS. ANN. tit. 20, § 400-1.020

(1984/2002); § 700-1.146 (2005/2016).

Montana

M

ONT

.

C

ODE

A

NN

. § 33-20-141;

§§ 33-20-802 to 33-20-807 (2007/2017)

(portions of previous version of model).

Nebraska

NEB. REV. STAT. §§ 44-8101 to 44-8109

(2006/2018) (previous version of model);

BULLETIN CB-128 (2012).

Nevada

N

EV

.

A

DMIN

.

C

ODE

§§

688A.400 to 688A.475

(2005) (previous version of model).;

B

ULLETIN 2006-004 (2006).

New Hampshire

N.H.

C

ODE

A

DMIN

.

R.

A

NN

.

I

NS

.

305.01

to

305.08 (2009/2014) (previous version of

model); B

ULLETIN 14-036-AB (2014) (training

requirement).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

ST-275-6

© 2020 National Association of Insurance Commissioners

NAIC MEMBER

MODEL ADOPTION

RELATED STATE ACTIVITY

New Jersey

N.J. A

DMIN

.

C

ODE

§§ 11:4-59A.1 to

11:4-59A.6 (2013) (previous version of

model); N.J.

STAT. ANN. § 17B:25-20

(1981/2005) (limits maturity dates and

surrender charges for annuities sold to

seniors); §§ 17B:25-34 to 17B:25-42 (2008);

B

ULLETIN 2009-12 (2009).

New Mexico

NO CURRENT ACTIVITY

New York

N.Y. C

OMP

.

C

ODES

R.

&

R

EGS

.

tit. 11,

§§ 224.0 to 224.9 (2011/2018) (previous

version of model); N.Y. C

OMP. CODES R. &

REGS. tit. 11, §§ 225.0 to 225.3 (2013)

(senior-specific certifications).

North Carolina

N.C. GEN. STAT. §§ 58-60-150 to 58-60-180

(2007/2009) (previous version of model);

11 N.C. ADMIN. CODE 12.0420 (1976/1992)

(submit suitability form).

North Dakota

N.D.

C

ENT

.

C

ODE

§§ 26.1-34.2-01 to

26.1-34.2-05 (2007/2011) (previous version of

model); N.D.

ADMIN. CODE §§ 45-02-02-14

(1984/2001) (recommendations to consumers

over age 65); § 45-04-04-07 (1984).

Northern Marianas

NO CURRENT ACTIVITY

Ohio

O

HIO

A

DMIN

.

C

ODE

3901-6-13 (2010).

Oklahoma

O

KLA

.

A

DMIN

.

C

ODE

§§ 365:25-17-1 to

365:25-17-9 (2005/2007) (portions of

previous version of model);

BULLETIN 1-12-2012 (2012) (training

requirement).

Oregon

O

R

.

A

DMIN

.

R. 836-080-0170 to

836-080-0193 (2011) (previous version of

model).

Pennsylvania

40 P

A

.

C

ONS

.

S

TAT

.

§§ 627-1 to 627-8

(2010/2018) (previous version of model).

Puerto Rico

NO CURRENT ACTIVITY

Rhode Island

230-20 R.I.

C

ODE

R. §§ 25-1.1 to 25-1.10

(2011/2018) (previous version of model);

BULLETIN 2011-2 (2011) (training

requirement).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

© 2020 National Association of Insurance Commissioners ST-275-7

NAIC MEMBER

MODEL ADOPTION

RELATED STATE ACTIVITY

South Carolina

S.C.

C

ODE

A

NN

.

R

EGS

.

69-29

(2011)

(previous

version of model).

South Dakota

S.D.

C

ODIFIED

L

AWS

.

§§ 58-33A-13 to

58-33A-27 (2008/2012) (previous version of

model); S.D.

ADMIN. R. § 58-28-33 (2003);

B

ULLETIN 2008-5 (2008).

Tennessee

T

ENN

.

C

OMP

.

R.

&

R

EGS

. §§ 0780-01-86-.01

to 0780-1-86-.09 (2008/2015) (previous

version of model); B

ULLETIN 5-22-2013

(2013).

Texas

T

EX

.

I

NS

.

C

ODE

A

NN

. §§ 1115.001 to

1115.102 (2007/2011) (previous version of

model).

Utah

U

TAH

A

DMIN

.

C

ODE

R590-230 (2004/2012)

(previous version of model).

Vermont

NO CURRENT ACTIVITY

Virgin Islands

NO CURRENT ACTIVITY

Virginia

14

V

A

.

A

DMIN

.

C

ODE

§§ 5-45-10 to 5-45-50

(2017) (previous version of model).

Washington

W

ASH

.

A

DMIN

.

C

ODE

§

284-17-265

(2012)

(portions of previous version of model);

§ 284-23-390 (2012) (portions of previous

version of model); W

ASH. REV. CODE § 48.23

(2009) (previous version of model).

West Virginia

W.

V

A

.

C

ODE

R.

§§

114-11B-1

to 114-11B-8

(2008/2011) (previous version of model).

Wisconsin

W

IS

.

S

TAT

. § 628.347 (2004/2015) (previous

version of model).

Wyoming

W

YO

.

A

DMIN

.

C

ODE

044.0002.64 §§ 1 to 9

(2014/2018) (previous version of model).

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2020

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

ST-275-8

© 2020 National Association of Insurance Commissioners

This page is intentionally left blank

NAIC Model Laws, Regulations, Guidelines and Other Resources—January 2011

SUITABILITY IN ANNUITY TRANSACTIONS

MODEL REGULATION

Proceedings Citations

Cited to the Proceedings of the NAIC

© 2011 National Association of Insurance Commissioners PC-275-1

In 2000, the NAIC adopted a white paper recommending the establishment of suitability standards for life insurance and

annuities. Shortly thereafter a working group was appointed to draft standards. The purpose of the model act and regulation

developed by that working group was to regulate the activities of insurers and producers who made recommendations to

consumers to purchase certain life insurance and annuity products to ensure that insurers and producers made suitable

recommendations based on relevant information obtained from the persons who purchased life insurance and annuity

products. 2003 Proc. 3

rd

Quarter 27.

A model act and regulation were adopted by the working group and forwarded to the parent committee. Because of the lack

of support for a wide-reaching suitability standard, and because none had existed before in most states, the parent committee

recommended a narrow model that addressed the area of most concern to regulators—the sale of annuities to seniors. A new

model was drafted in early 2003 and comments solicited. Associations, consumer groups and others participated. The process

resulted in a new model that was adopted by the NAIC membership. 2003 Proc. 3

rd

Quarter 28.

A commissioner proposed amending the Life Insurance and Annuities (A) Committee charges to include reviewing and

changing the Senior Protection in Annuity Transactions Model Regulation to address the suitability issue with regards to all

annuity transactions. 2006 Proc. 1

st

Quarter 38.

The Life Insurance and Annuities (A) Committee adopted revisions to this model. A commissioner stated that he had urged

reopening the Senior Protection in Annuity Transactions Model Regulation to expand the model’s suitability protections to

consumers of all ages, not just those 65 years of age or older. Since the model’s adoption in 2003, there was an increasing

number of complaints from those under 65. Committee members expressed support for the proposed revisions particularly in

light of proposed legislation being considered by the California Legislature, Senate Bill 192. 2006 Proc. 1

st

Quarter 322.

The joint Executive Committee/Plenary adopted the proposed revisions to the Senior Protection in Annuity Transactions

Model Regulation. The revisions expand the model’s protections to all consumers, not just those 65 years of age or older.

Since the model’s adoption in 2003, there had been an increasing number of complaints from those under 65. 2006 Proc. 2

nd

Quarter 39.

The Suitability of Annuity Sales Working Group discussed the guidelines that they believed should be part of the revisions.

2008 Proc. 3

rd

Quarter 6-49 to 6-51.

The Working Group discussed a draft of the proposed revisions to the model. Regulators discussed how California had not

adopted the current model because of its concerns with its delegation and other provisions. The Working Group discussed

priorities for revising the model and held a panel discussion on the proposed revisions. 2008 Proc. 4

th

Quarter 6-9 to 6-11.

The Life Insurance and Annuities (A) Committee discussed options as whether to amend the existing Suitability in Annuity

Transactions Model Regulation. 2009 Proc. 2

nd

Quarter 6-4.

The Working Group discussed several issues related to revising the scope of this model as well as issues that needed to be

addressed. 2009 Proc. 2

nd

Quarter 6-29 to 6-30.

The Life Insurance and Annuities (A) Committee decided to affirmatively pursue revising the model regulation rather than

continuing to discuss the issue of developing a model bulletin. 2009 Proc. 3

rd

Quarter 6-4.

The Suitability of Annuity Sales (A) Working Group adopted a draft of revisions to the Suitability in Annuity Transactions

Model Regulation. 2009 Proc. 4

th

Quarter 6-3.

The Life Insurance and Annuities (A) Committee adopted the revisions to the Suitability in Annuity Transactions Model

Regulation. When voting, one state reserved its right to amend the model if it was presented for adoption as a regulation or

law. 2010 Proc. Spring 6-4 to 6-6.

NAIC Model Laws, Regulations, Guidelines and Other Resources—January 2011

SUITABILITY IN ANNUITY TRANSACTIONS

MODEL REGULATION

Proceedings Citations

Cited to the Proceedings of the NAIC

PC-275-2 © 2011 National Association of Insurance Commissioners

The joint Executive Committee/Plenary adopted proposed revisions to the Suitability in Annuity Transactions Model

Regulation. These revisions made three core changes to the model: (1) clarified that the insurer is responsible for compliance

with the model’s requirements even if the insurer contracts with a third party; (2) required a review of all recommended

annuity transactions; and (3) established producer general training and specific-product training requirements. 2010 Proc.

Spring 3-3.

Section 1. Purpose

A. There was some consensus to prepare a draft that started with the National Association of Securities Dealers

(NASD) standards in place for variable products. An interested party said the primary issue was whether incorporation of the

NASD standards meant that regulators were also incorporating the whole supervisory structure of the NASD. 2003 Proc. 2

nd

Quarter 220.

A regulator said the earlier draft prepared by the working group had a checklist of specific items to be reviewed but now that

the standard was more general, he suggested removing the word “minimum” before standards so that the regulation would

just say that it set forth standards and procedures. An interested party said that the wording of Section 1 could imply that

insurers did not have a responsibility if they did not make recommendations and the committee agreed to reword that section

to make this clearer. 2003 Proc. 2

nd

Quarter 217.

To address continuing concerns on the part of interested parties that suitability might be determined based on later

circumstances, the committee added the phrase “at the time of the transaction” to Subsection A. 2003 Proc. 2

nd

Quarter 220.

B. An interested party asked the committee to consider adding specific language in Section 1 about a private cause of

action. Regulators agreed to add a Subsection B referring to a private cause of action. Another regulator said this already

appeared in the Unfair Trade Practices Act and so it was not needed in this regulation. The committee agreed to repeat the

language as it was written in the Unfair Trade Practices Act in this document. The regulator suggested adding a drafting note

that if a state had different language in its Unfair Trade Practices Act, it should use that instead. 2003 Proc. 2

nd

Quarter 217.

Section 2. Scope

Extensive discussion took place on whether the model should cover all recommendations or just recommendations that

resulted in a sale. Ultimately the drafters settled on a focus on recommendations that resulted in sales. They expressed

concern that all recommendations be suitable, but recognized the record-keeping burden that would be imposed by extending

the model to cover all recommendations. 2003 Proc. 3

rd

Quarter 28.

An interested party said the draft was so general in scope that it was confusing. The interested party said that the phrase,

“transaction or a series of transactions” was too broad. If a producer who was not licensed with Company A recommended

that an individual surrender his annuity and buy a Company B product, Company A had no ability to judge the suitability of

that recommendation. A commissioner said that, if a person exchanged an annuity for a universal life insurance policy, the

language recommended by the interested party would be clearer. Another interested party asked if this would cover a

situation when a person surrendered his annuity and bought a mutual fund. The interested party said that, in that case, neither

the securities nor insurance regulators would have jurisdiction when someone surrendered an annuity. 2003 Proc. 3

rd

Quarter 212.

Once the model was narrowed to apply only to sales of annuities to seniors, one new issue was whether the rules should

apply to all transactions involving an annuity, or just a transaction where an annuity was being purchased. The language

settled on referred to a purchase or exchange of an annuity. 2003 Proc. 3

rd

Quarter 28-29.

A commissioner distributed a draft of proposed revisions to the Senior Protection in Annuity Transactions Model Regulation.

The Life Insurance and Annuities (A) Committee voted to expose the draft for comment. The Committee intended to

expedite consideration of these revisions. 2006 Proc. 1

st

Quarter 324.

NAIC Model Laws, Regulations, Guidelines and Other Resources—January 2011

SUITABILITY IN ANNUITY TRANSACTIONS

MODEL REGULATION

Proceedings Citations

Cited to the Proceedings of the NAIC

© 2011 National Association of Insurance Commissioners PC-275-3

Section 3. Authority

There were many controversial items raised during the drafting of the initial model draft. The working group discussed

whether to use the Unfair Trade Practices Act as authority for development of a regulation. Interested parties urged the

working group to develop language specific to suitability of sales. This discussion also extended to whether to require a

pattern of conduct, as in the Unfair Trade Practices Act, or whether a single violation was sufficient to invoke penalties. 2003

Proc. 3

rd

Quarter 28.

Section 4. Exemptions

Once the model was narrowed to apply only to sales of annuities to seniors, many of the issues that previously had been

controversial no longer applied, such as many of the exemptions included in the earlier draft. However one new issue was

whether the rules should apply to all transactions involving an annuity, or just a transaction where an annuity was being

purchased. The language settled on referred to a purchase or exchange of an annuity. 2003 Proc. 3

rd

Quarter 28-29.

The Working Group deleted the exemptions that were in this Section. 2008 Proc. 3

rd

Quarter 6-6.

A. An interested party suggested a number of technical changes to the draft. One suggestion was to add “pursuant to

this regulation” following “based on information collected from the senior consumer” in Section 4A. A regulator said that if

the producer used information he already knew, it would fall outside the scope of the regulation and that was not the drafters’

intent. The interested party responded that the purpose of that language was to reflect the fact that the type of information

gathered from the consumer should be relevant to determining suitability in order to fall under this regulation. Regulators

decided to include the language suggested by the interested party in Section 4A. 2003 Proc. 3

rd

Quarter 213.

The drafting group discussed how the regulation would apply to direct writers. An interested party said that a

recommendation should be based on an exchange of information. Direct writers sent out information with minimal

knowledge of the person receiving it. If the model applied to them, direct writers will have to change the way they did

business. A regulator opined that in direct response solicitations, the advertising just described the product; it does not

“advise.” Another interested party said the earlier draft prepared by the working group exempted direct response if no direct

recommendation was made. An interested party said all advertising could be a recommendation. That is why the words

“specific personalized” needed to be in the draft referring to recommendations. 2003 Proc. 2

nd

Quarter 217.

The Suitability of Annuity Sales (A) Working Group discussed deleting the words “by insurer.” 2009 Proc. 4

th

Quarter 6-7.

The Working Group added the word “insurer” in response to discussions with the Securities and Exchange Commission

(SEC) to clarify what type of direct response solicitation would be exempt from the model’s provisions. 2009 Proc. 4

th

Quarter 6-10.

B. The committee decided to put exemptions in this regulation similar to those that had been in the draft act considered

by the earlier working group. A regulator pointed out that the draft included an exemption for variable annuities, which

should be removed. The committee discussed the various types of contracts included in Subsection B and decided that they

were all appropriate exemptions. A regulator asked why prepaid funeral contracts were being excluded. Another regulator

responded that these were smaller face amount products, not generally in the area of abuses. The drafters considered adding

an exemption for structured settlements. A regulator pointed out that this type of contract did not generally result from a

recommendation by an insurer or producer but agreed that it did not hurt to have the exemption there. Another interested

party requested that the committee consider an exemption for sophisticated purchasers. An interested party said the National

Association of Securities Dealers (NASD) suitability standards did not have an exemption for sophisticated purchasers, for

good reason. The committee declined to add it to this draft. 2003 Proc. 2

nd

Quarter 219.

A regulator expressed concern about deleting the language concerning the exemption for ERISA plans. Another regulator

said that the basis for developing the revisions to the model was due to problems some states had experienced with unsuitable