I further certify that we are engaged in business as a: c Wholesaler c Retailer c Manufacturer c Lessor

of

_____________________________________________________________________________________________________________________

My Nebraska Sales Tax ID Number is 01-_________________________________.

If none, state the reason _____________________________________________________________________________________________________,

or Foreign State Sales Tax Number__________________________________________ State __________________________________________.

for Sales Tax Exemption

13

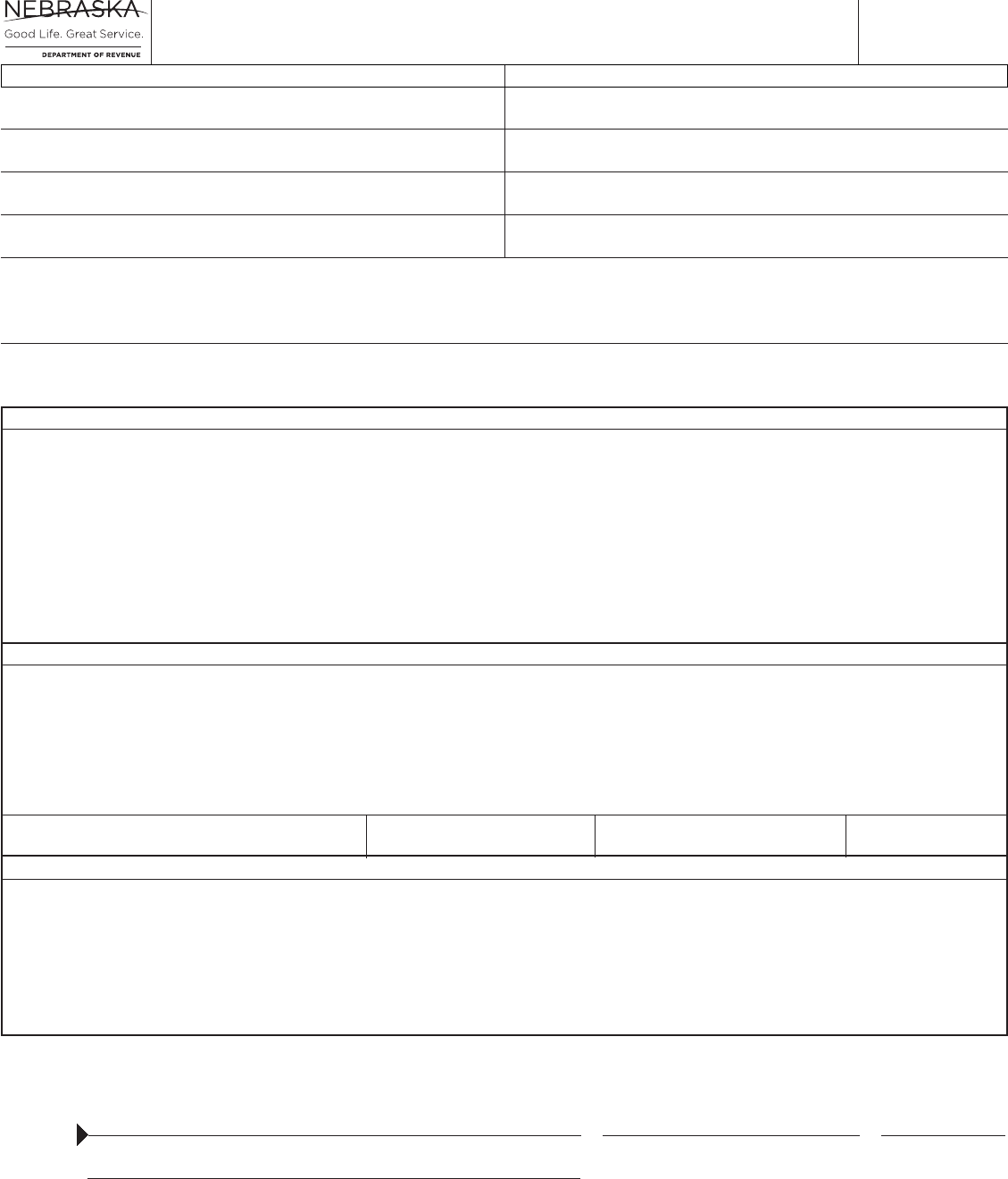

Nebraska Resale or Exempt Sale Certificate

FORM

Name and Mailing Address of Seller

Name

Street or Other Mailing Address

City State Zip Code

Name and Mailing Address of Purchaser

Name

Legal Name

Street or Other Mailing Address

City State Zip Code

Check Type of Certificate

c Single Purchase If single purchase is checked, enter the related invoice or purchase order number ______________________________________.

c Blanket If blanket is checked, this certicate is valid until revoked in writing by the purchaser.

Section B — Nebraska Exempt Sale Certificate

Section A — Nebraska Resale Certificate

Any purchaser, agent, or other person who completes this certificate for any purchase which is not for resale, lease, or rental in the regular course of the

purchaser’s business, or is not otherwise exempted from sales and use taxes is subject to a penalty of $100 or ten times the tax, whichever amount is larger, for

each instance of presentation and misuse. With regard to a blanket certificate, this penalty applies to each purchase made during the period the blanket certificate

is in effect. Under penalties of law, I declare that I am authorized to sign this certificate, and to the best of my knowledge and belief, it is correct and complete.

sign

here

Authorized Signature Title Date

Section C — For Contractors Only

c As an Option 1 or Option 3 contractor, I hereby certify that the purchase of building materials and xtures from the seller listed above are exempt

from Nebraska sales tax. My Nebraska Sales or Use Tax ID Number is: _____________________________________________________.

c Yes c No

Do not send this certificate to the Nebraska Department of Revenue (DOR). Keep it as part of your records.

Sellers cannot accept incomplete certificates.

The DOR is committed to the fair administration of the Nebraska tax laws. It is unlawful to claim an exemption for purchases of property or

services that are subject to tax. Sellers are encouraged to notify the DOR of any unlawful use of this form.

revenue.nebraska.gov, 800-742-7474 (NE and IA), 402-471-5729

Description of Items Sold

6-134-1970 Rev. 7-2022

Supersedes 6-134-1970 Rev. 3-2018

I hereby certify that the purchase, lease, or rental of ___________________________________________________________from the seller listed above

is exempt from the Nebraska sales tax as a purchase for resale, rental, or lease in the normal course of our business. The property or service will be resold

either in the form or condition in which it was purchased, or as an ingredient or component part of other property or service to be resold.

1. Purchase of building materials or fixtures.

2. Purchases made by an Option 2 contractor under a Purchasing Agent Appointment on behalf of

_________________________

________________________________________.

The basis for this exemption is exemption category ______ (See the list of Exemption Categories and corresponding numbers on reverse side).

If exemption category 2 or 5 is claimed, enter the following information:

Description of Property or Service Purchased Intended Use of Property or Service Purchased

_____________________________________________________________ _______________________________________________________

If exemption category 3 or 4 is claimed, enter your Nebraska Certicate of Exemption State ID number. 05 -______________________________

If exemption category 6 is claimed, the seller must enter the following information and sign this form below:

Date of Seller’s Original Purchase Was tax paid when purchased by seller? Was item depreciable?

I hereby certify that the purchase, lease, or rental by the above purchaser is exempt from the Nebraska sales tax for the following reason:

Check One c Purchase for Resale (Complete Section A.) c Exempt Purchase (Complete Section B.) c Contractor (Complete Section C.)

(exempt entity)

Do not enter your Federal Employer ID Number.

c Yes c No

c

As an Option 2 contractor, I hereby certify that the purchase of building materials and xtures from the seller listed above is exempt from

Nebraska sales tax pursuant to the attached Purchasing Agent Appointment and Delegation of Authority for Sales and Use Tax, Form 17.

Authorized Signature Name (please print)

Description of Property or Service Purchased

RESET FORM

PRINT FORM

Who May Issue a Resale Certificate. Purchasers are to give the seller

a properly completed Form 13, Section A, when making purchases

of property or taxable services that will subsequently be resold in the

purchaser’s normal course of business. The property or services must

be resold in the same form or condition as when purchased, or as an

ingredient or component part of other property that will be resold.

Who May Issue an Exempt Sale Certificate.

Form 13, SectionB,

may be completed and issued by governmental units or organizations

that are exempt from paying Nebraska sales and use taxes. See this

list in the Nebraska Sales Tax Exemptions Chart. Most nonprot

organizations are not exempt from paying sales and use tax. Enter the

appropriate number from “Exemption Categories” (listed below) that

properly reects the basis for your exemption.

For additional information about proper issuance and use of this certicate,

please review Reg-1-013, Sale for Resale – Resale Certicate, and

Reg-1-014, Exempt Sale Certicate.

Contractors. Contractors complete Form 13, Section C, part 1 or part

2 based on the option elected on the Contractor Registration Database.

To make tax-exempt purchases of building materials and xtures,

Option 1 or Option 3 contractors must complete Form 13, SectionC,

Part 1. To make tax-exempt purchases of building materials and xtures

pursuant to a construction project for an exempt governmental unit or

an exempt nonprot organization, Option 2 contractors must complete

Form 13, Section C, Part 2. The contractor must also attach a copy of

a properly completed Purchasing Agent Appointment and Delegation

of Authority for Sales and Use Tax, Form17, to the Form 13, and both

documents must be given to the supplier when purchasing building

materials. See the contractor information guides and Reg-1-017,

Contractors, for additional information. Also, see the Important Note

under “Exemption Categories” number 3.

When and Where to Issue. The Form 13 must be given to the seller

at the time of the purchase to document why sales tax does not apply

to the purchase. The Form 13 must be kept with the seller’s records for

auditpurposes.

Sales Tax Number. A purchaser who is engaged in business as a

wholesaler or manufacturer is not required to provide an ID number

when completing Section A. Out-of-state purchasers may provide their

home state sales tax number. SectionB does not require a Nebraska ID

number when exemption category 1, 2, or 5 is indicated.

Fully Completed Resale or Exempt Sale Certificate. A fully

completed resale or exempt sale certicate is proof for the retailer

that the sale was for resale or is exempt. For a resale certicate to be

fully completed, it must include: (1) identication of the purchaser

and seller, type of business engaged in by the purchaser; (2) sales tax

permit number; (3) signature of an authorized person; and (4) the date

of issuance.

For an exempt sale certicate to be fully completed, it must include:

(1) identication of purchaser and seller; (2) a statement that the certicate

is for a single purchase or is a blanket certicate covering future sales;

(3) a statement of the basis for exemption, including the type of activity

engaged in by the purchaser; (4) signature of an authorized person; and

(5) the date of issuance.

Penalties. Any purchaser who gives a Form 13 to a seller for any

purchase which is other than for resale, lease, or rental in the normal

course of the purchaser’s business, or is not otherwise exempted from

sales and use tax under the Nebraska Revenue Act, is subject to a

penalty of $100 or ten times the tax, whichever is greater, for each

instance of presentation and misuse. In addition, any purchaser, or their

agent, who fraudulently signs a Form 13 may be found guilty of a Class

IV misdemeanor.

Exemption Categories

(Insert appropriate number from the list below in Section B)

1. Governmental units, identied in Neb. Rev. Stat. §§ 77-2704.15,

Reg-1-072, United States Government and Federal Corporations,

and Reg-1-093, Governmental Units. Governmental units are not

assigned exemption numbers.

Instructions

Sales to the U.S. government, its agencies, instrumentalities, and

corporations wholly owned by the U.S. government are exempt

from sales tax. However, sales to institutions chartered or created

under federal authority, but which are not directly operated and

controlled by the U.S. government for the benet of the public,

generally aretaxable.

Purchases by governmental units that are not exempt from Nebraska

sales and use taxes include, but are not limited to: governmental units

of other states or countries; sanitary and improvement districts;

rural water districts; railroad transportation safety districts; and

county historicalsocieties.

2.

Purchases when the intended use renders it exempt. See Nebraska

Sales Tax Exemptions Chart.

3.

Purchases made by organizations that have been issued a Nebraska

Exempt Organization Certificate of Exemption (Certificate of

Exemption). Reg-1-090, Nonprofit Organizations; Reg-1-091,

Religious Organizations; and Reg-1-092, Educational Institutions,

identify these organizations. These organizations are issued a

Certicate of Exemption with a state ID number which must be

entered in Section B of Form 13.

Important Note: Nonprofit educational institutions must be

accredited regionally or nationally and have their primary campus

in Nebraska to be exempt from sales and use tax. Also nonprot

organizations providing any of the types of health care or services

that qualify to be exempt must be licensed or certified by the

Nebraska Department of Health and Human Services (DHHS)

to be exempt from sales and use taxes. There is no sales and use

tax exemption prior to these entities being accredited, licensed,

or certied. They CANNOT issue either a Resale or Exempt Sale

Certicate, Form 13, or a Purchasing Agent Appointment, Form17,

to any retailer or contractor relating to purchases of building

materials for construction or repair projects performed prior to

being accredited, licensed, or certied. After an entity becomes

accredited, licensed, or certied upon completion of the construction

project, it may submit a Nebraska Exemption Application for Sales

and Use Tax, Form 4.

Nonprofit health care organizations that hold a Certificate of

Exemption are exempt for purchases for use at their facility, or

portion of the facility, covered by the license issued under the

Nebraska Health Care Facility Licensure Act. Only specic types

of health care facilities and activities are exempt. Purchases of items

for use at facilities that are not covered under the license, or for any

other activities that are not specically exempt, are taxable. The

exemption is not for the entire organization that offers different

levels of health care or other activities, but is limited to the specic

type of health care that is exempt. Purchases for non-exempt types

of health care are taxable.

4.

Purchases of motor vehicles, trailers, semitrailers, watercraft,

and aircraft used predominately as common or contract carrier

vehicles; accessories that physically become part of the common or

contract carrier vehicle; and repair and replacement parts for these

vehicles. The exemption ID number must be entered in Section B

of the Form 13. An individual or business that has been issued a

common or contract carrier certicate of exemption may only use it

to purchase those items described above prior to the expiration date

on the certicate. The certicate of exemption expires every 5 years.

(See Nebraska Common or Contract Carrier Information Guide).

5.

Purchases of manufacturing machinery and equipment made by a

person engaged in the business of manufacturing, including repair

and replacement parts or accessories, for use in manufacturing.

6.

Occasional sales of used business or farm machinery or equipment

productively used by the seller as a depreciable capital asset for more

than one year in his or her business. The seller must have previously

paid tax on the item being sold. The seller must complete, sign, and

give the Exempt Sale Certicate to the purchaser. (See Reg-1-022,

Occasional Sales). The Form 13 must be kept with the purchaser’s

records for audit purposes.