Background

The Federal Reserve promotes a safe, sound, and efficient banking system that supports the U.S.

economy through its supervision and regulation of domestic and foreign banks.

As part of its supervision efforts, the Federal Reserve conducts annually a supervisory stress test.

The stress test assesses how large banks are likely to perform under hypothetical economic

conditions.

1

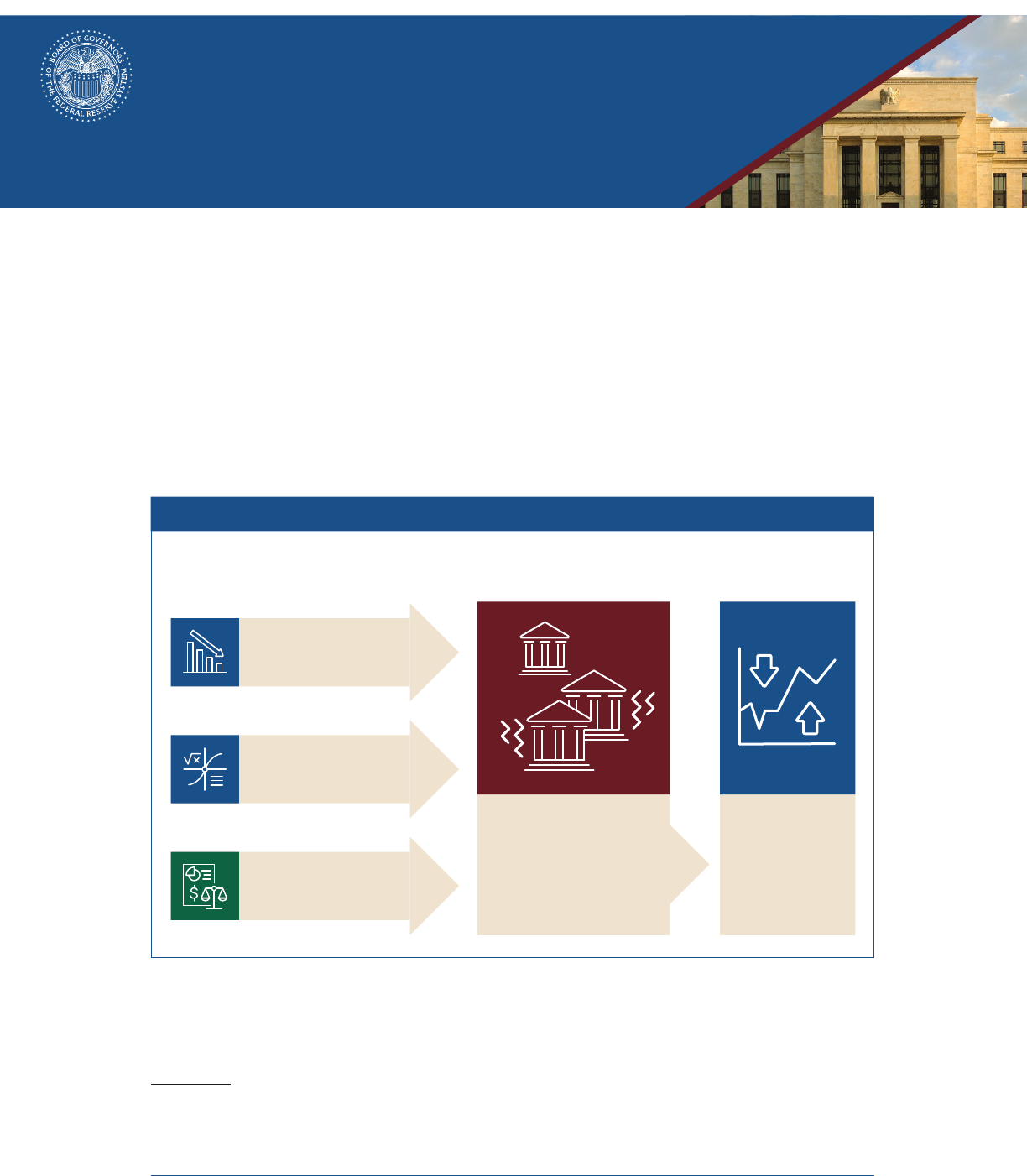

Figure 1 summarizes the stress test cycle.

1

U.S. bank holding companies (BHCs), covered savings and loan holding companies (SLHCs), and intermediate holding

companies of foreign banking organizations (IHCs) with $100 billion or more in assets are subject to the Federal Reserve

Board’s supervisory stress test rules (12 C.F.R. pt. 238, subpt. O; 12 C.F.R. pt. 252, subpt. E) and capital planning

requirements (12 C.F.R. § 225.8; 12 C.F.R. pt. 238, subpt. S).

Figure 1. How stress testing works for large banks

The Federal Reserve conducts stress tests to ensure that large banks are sufficiently capitalized and able to lend to

households and businesses even in a severe recession. The stress tests evaluate the financial resilience of banks by

estimating losses, revenues, expenses, and resulting capital levels under hypothetical economic conditions.

The Federal Reserve

us

es the results of the

supervisory stress test,

in part, to set capital

requirements for

participating banks

The Federal Reserve develops

stress test scenarios

The Federal Reserve develops

or selects stress test models

Banks submit detailed bank data

Using the scenario data and bank

data as variables in the stress

test models, the

Federal Reserve projects how

banks are likely to perform under

hypothetical economic conditions

Large Bank Capital Requirements

July 2023

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM www.federalreserve.gov

The stress tests ensure that large banks are sufficiently capitalized and able to lend to house-

holds and businesses even in a severe recession. They evaluate the financial resilience of banks

by estimating losses, revenues, expenses, and resulting capital levels under hypothetical eco-

nomic conditions.

As part of this cycle, the Federal Reserve publishes four documents:

•

Stress Test Scenarios describes the hypothetical economic conditions used in the supervisory

stress test. The Stress Test Scenarios document is typically published by mid-February.

•

Supervisory Stress Test Methodology provides details about the models and methodologies used

in the supervisory stress test.

•

Federal Reserve Stress Test Results reports the aggregate and individual bank results of the

supervisory stress test, which assesses whether banks are sufficiently capitalized to absorb

losses during a severe recession. The Federal Reserve Stress Test Results document is typically

published at the end of the second quarter.

•

Large Bank Capital Requirements announces the individual capital requirements for all large

banks, which are partially determined by the results of the supervisory stress test. The Large

Bank Capital Requirements document is typically published during the third quarter.

These publications can be found on the Stress Test Publications page (https://

www.federalreserve.gov/publications/dodd-frank-act-stress-test-publications.htm).

For information on the Federal Reserve’s supervision of large financial institutions, see https://

www.federalreserve.gov/supervisionreg/large-financial-institutions.htm. For information on the Fed-

eral Reserve’s supervision of capital planning processes of banks, see https://

www.federalreserve.gov/supervisionreg/stress-tests-capital-planning.htm.

For more information on how the Federal Reserve Board promotes the safety and soundness of

the banking system, see https://www.federalreserve.gov/supervisionreg.htm.

2 Large Bank Capital Requirements

Capital Requirements

Under the Federal Reserve Board’s capital framework for bank holding companies, covered savings

and loan holding companies, and U.S. intermediate holding companies with $100 billion or more

in total consolidated assets, capital requirements are in part determined by the supervisory stress

test results. Table 1 shows the total common equity tier 1 (CET1) capital ratio requirement for

each large bank, which is made up of several components, including

•

a minimum CET1 capital ratio requirement of 4.5 percent, which is the same for each bank;

•

the stress capital buffer (SCB) requirement, which is determined from the supervisory stress

test results and is at least 2.5 percent;

2

and

•

if applicable, a capital surcharge for global systemically important banks (G-SIBs), which is at

least 1.0 percent.

2

See 12 C.F.R. §§ 225.8(f) and 238.170(f) for rules on the SCB requirement calculation and 2023 Federal Reserve Stress

Test Results (Washington: Board of Governors, June 2023), https://www.federalreserve.gov/publications/files/2023-

dfast-results-20230628.pdf for details on the 2023 supervisory stress test results.

Firms subject to Category IV requirements are generally not required to participate in the supervisory stress test in odd

years. The firms that did not participate in this year’s supervisory stress test have SCB requirements based on 2022

stress test results and that have been adjusted by the Federal Reserve Board pursuant to 12 C.F.R. § 225.8(f)(4) and

12 C.F.R. § 238.170(f)(4).

Capital Requirements 3

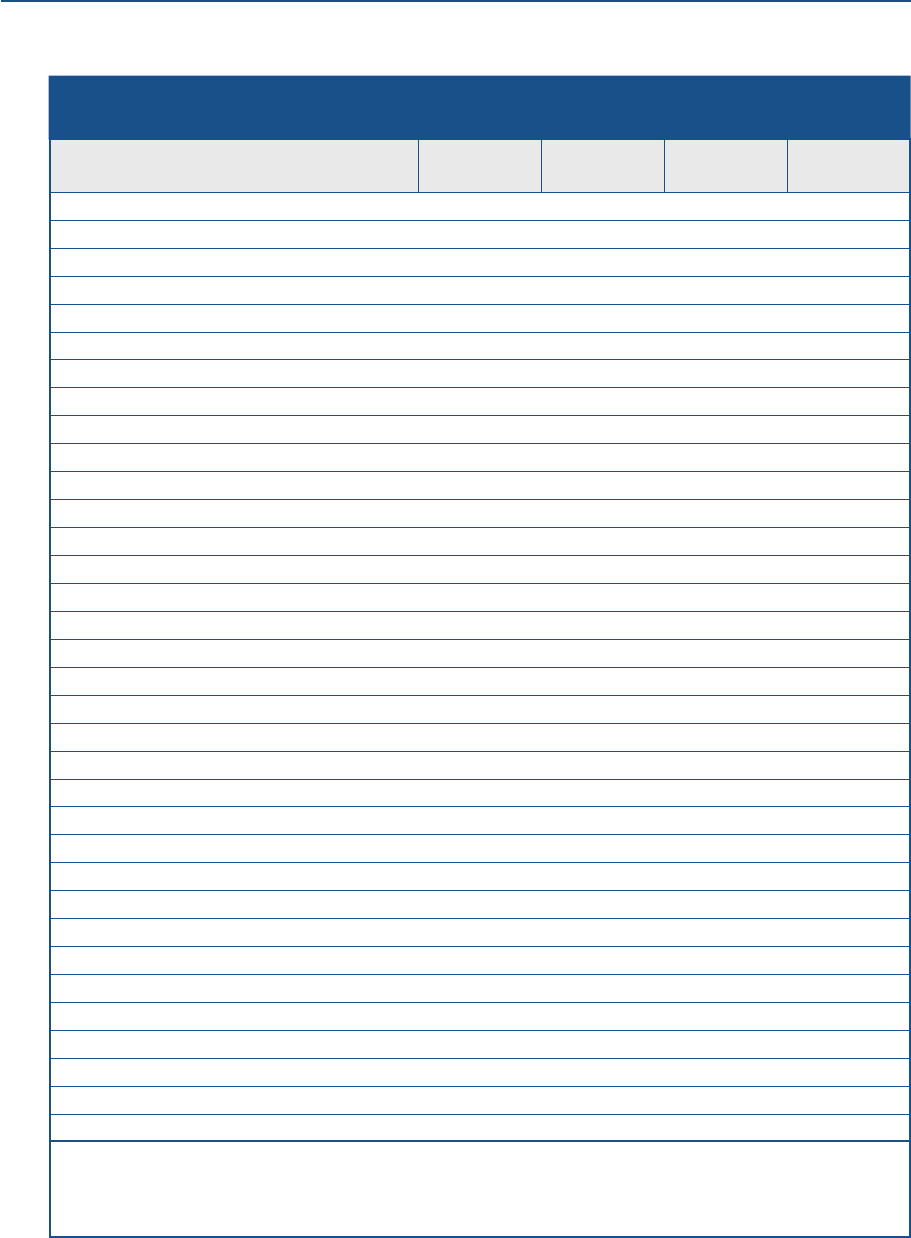

Table 1. Large bank capital requirements, effective October 1, 2023

Percent

Bank

Minimum CET1

capital ratio

Stress capital buffer

requirement

G-SIB surcharge*

CET1 capital

requirement

Ally Financial Inc.

†

4.5 2.5 n/a 7.0

American Express Company

†

4.5 2.5 n/a 7.0

Bank of America Corporation 4.5 2.5 2.5 9.5

The Bank of New York Mellon Corporation 4.5 2.5 1.5 8.5

Barclays US LLC 4.5 4.7 n/a 9.2

BMO Financial Corp. 4.5 3.3 n/a 7.8

BNP Paribas USA, Inc.

†

4.5 4.3 n/a 8.8

Capital One Financial Corporation 4.5 4.8 n/a 9.3

The Charles Schwab Corporation 4.5 2.5 n/a 7.0

Citigroup Inc. 4.5 4.3 3.5 12.3

Citizens Financial Group, Inc. 4.5 4.0 n/a 8.5

Credit Suisse Holdings (USA), Inc. 4.5 7.2 n/a 11.7

DB USA Corporation 4.5 9.3 n/a 13.8

Discover Financial Services

†

4.5 2.5 n/a 7.0

DWS USA Corporation 4.5 5.6 n/a 10.1

Fifth Third Bancorp

†

4.5 2.5 n/a 7.0

The Goldman Sachs Group, Inc. 4.5 5.5 3.0 13.0

HSBC North America Holdings Inc.

†

4.5 6.4 n/a 10.9

Huntington Bancshares Incorporated

†

4.5 3.2 n/a 7.7

JPMorgan Chase & Co. 4.5 2.9 4.0 11.4

KeyCorp

†

4.5 2.5 n/a 7.0

M&T Bank Corporation 4.5 4.0 n/a 8.5

Morgan Stanley 4.5 5.4 3.0 12.9

Northern Trust Corporation 4.5 2.5 n/a

7.0

The PNC Financial Services Group, Inc. 4.5 2.5 n/a 7.0

RBC US Group Holdings LLC 4.5 4.2 n/a 8.7

Regions Financial Corporation

†

4.5 2.5 n/a 7.0

Santander Holdings USA, Inc.

†

4.5 2.5 n/a 7.0

State Street Corporation 4.5 2.5 1.0 8.0

TD Group US Holdings LLC 4.5 2.5 n/a 7.0

Truist Financial Corporation 4.5 2.9 n/a 7.4

U.S. Bancorp 4.5 2.5 n/a 7.0

UBS Americas Holding LLC 4.5 9.1 n/a 13.6

Wells Fargo & Company 4.5 2.9 1.5 8.9

* The global systemically important bank (G-SIB) surcharge is updated annually in the first quarter. The G-SIB surcharge reported in this table

is the G-SIB surcharge in effect as of October 1, 2023.

† Firm did not participate in the 2023 stress test. The SCB requirement is based on 2022 stress test results.

n/a Not applicable.

4 Large Bank Capital Requirements

www.federalreserve.gov

0723