1

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

T

he Financial Accounting Standards Board (FASB)

has traditionally encouraged entities to report

major classes of gross cash receipts and gross cash

payments and their arithmetic sum—the net

cash flow from operating activities (the direct

method, DM). Very few financial statement preparers, how-

ever, adhere to the guidance because the indirect method

(IM) continues to be the most favored presentation method

for preparers of cash flow statements (Accounting Standards

Codification

®

230-10-45-25).

In 1987, the FASB published Statement of Financial

Accounting Standards 95 (SFAS 95), “Statement of Cash

Flows,” which set the stage for the statement of cash flows as

we know it today. Over the Statement’s 29-year history, rule-

making bodies made two noteworthy attempts to require the

DM, and another attempt is probably on the horizon. The

first attempt occurred when the Statement was released. The

second attempt occurred in 2008 when the FASB and the

International Accounting Standards Board (IASB) issued a

joint discussion paper titled “Preliminary Views on Financial

Statement Presentation.” The discussion paper proposed,

among other things, a mandate for the DM. As part of an

overall tightening of the cash flow activity classification rules,

attempts continued in 2014 and 2015.

In this article, we provide a history of the cash flow state-

The Statement of Cash Flows

and the Direct Method of

Presentation

EXECUTIVE SUMMARY

Which method of presentation is

better for the cash flow statement:

the direct method (DM) or the indirect

method (IM)? The issue is still being

discussed.

By Nathan H. Jeppson, Ph.D., CPA; John A. Ruddy, CPA, CFA; and David F. Salerno, Ph.D., CPA

2

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

ment, followed by an analysis of the public’s response

to the most recent attempt to mandate the direct

method. Then we describe the FASB’s current ongoing

efforts regarding the direct method, and we close with

an analysis of which method is preferable.

HISTORY AND TIMELINE OF THE STATEMENT

OF CASH FLOWS

Prior to the release of SFAS 95, Accounting Principles

Board Opinion 19 (APB 19), “Reporting Changes in

Financial Position,” allowed the reporting of cash flows,

but it was not a requirement. SFAS 95 established

the current rules for the statement of cash flows—

classifying cash flows into operating, investing, or

financing activities.

The guidance of SFAS 95 allowed a choice of either

the DM or IM of presentation for cash flows from oper-

ating activities. Although SFAS 95 did not require the

DM, it encouraged the DM in lieu of the IM. The

FASB passed SFAS 95 by a four-to-three vote with two

of the three dissenting members concerned that the

statement would have reduced usefulness by not re-

quiring the DM. Specifically, they argued that using the

IM would fail to “provide relevant information about

the cash receipts and cash payments of an enterprise

during a period.” Providing relevant information about

a business entity’s cash flows was the stated overall pur-

pose of SFAS 95.

Ever since SFAS 95 was issued, it has become clear

that businesses have largely disregarded the FASB’s en-

couragement to use the DM. The FASB and the IASB

said they issued the discussion paper in response to

users’ concerns that “existing requirements permit too

many alternative types of presentation and information

in financial statements is highly aggregated and incon-

sistently presented, making it difficult to fully under-

stand the relationship between the financial statements

and the financial results of an entity.” The discussion

paper raised the issue of making the DM mandatory

and contained guidance concerning a detailed reconcili-

ation of cash flows to comprehensive income.

Recent Attempts to Mandate the Direct Method

The most significant attempt to mandate the direct

method began in 2001, when the FASB and the IASB

separately initiated projects to review the presentation

of each financial statement. As part of the international

accounting standards convergence, the Boards agreed to

consider two independent projects in 2004. The rule-

making bodies agreed the projects would have three

distinct phases:

l Phase A would outline the required financial state-

ments and the required reporting periods.

l Phase B would consider details of financial statement

presentation, including whether the DM would be

used for the presentation of cash flows from operating

activities.

l Phase C would consider the required information and

presentation required for interim financial statement

information.

By October 2008, the joint project titled Financial

Statement Presentation had progressed to the point

where the FASB and the IASB were ready to receive

preparer and user feedback. They issued the document

“Preliminary Views on Financial Statement

Presentation.” From October 2008 to April 2009, they

solicited feedback regarding the proposed changes to fi-

nancial statements (see Figure 1 for a statement of cash

flow event timeline). While the document proposed

changes in format and presentation for all four basic fi-

nancial statements, a substantial amount of responses

addressed using the DM in the presentation of cash

flows. During the feedback period, the Boards received

229 comment letters. Additionally, they received nine

unsolicited comment letters prior to the comment pe-

riod and one comment letter after the comment period.

In the next section we analyze the responses to provide

a deeper understanding of the IM popularity and argu-

ments in favor of the DM.

The Financial Statement Presentation project was

put on hold in October 2010, but subsequent develop-

ments indicate the statement of cash flows will likely

undergo future revisions. In April 2014, the FASB

launched a project aimed at clarifying certain existing

principles on statement of cash flows with the objective

of increasing “consistency in the classification of cash

inflows and outflows as operating, investing, or financ-

ing.”

1

In April 2015, the Board issued an exposure draft

that would require not-for-profit entities to use the

3

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

direct method of cash flow presentation. We discuss this

in detail in the section “Current Developments and

Ongoing Efforts to Mandate.”

As we describe next, the FASB has indicated the

mandatory use of the direct method is still preferred for

business enterprises.

2

Discussion of the Public’s Response to

Mandating the Direct Method

The most recent justification for mandating the DM

comes from the objectives of the discussion paper pro-

posals, which state that financial reports should contain

three features:

l Cohesiveness, which the FASB and the IASB defined

as the ability to clearly see the relationship between

items across all the financial statements;

l Disaggregation of information, which only allows

combining account balances for presentation if the

items are economically similar; and

l Presentation of information such that it allows users

to assess the firm’s liquidity and financial flexibility.

The Boards believed the DM was superior to the IM

in possessing these features.

Letters in response to the discussion paper provide

opinions of interested parties. We reviewed the 229

comment letters, but 32 letters did not address the pre-

sentation or format of the cash flow statement. Of the

197 that did address the cash flow statement, four did

not discuss the debate regarding the direct vs. the indi-

rect format, and 13 letters did not express a format

preference.

We analyzed the 180 remaining comment letters that

both discussed the debate between cash flow statement

formats and expressed a preferred cash flow statement

format. We classify the letters by country, business type,

segment classification, and financial statement user

type and provide summary tables that categorize the

23

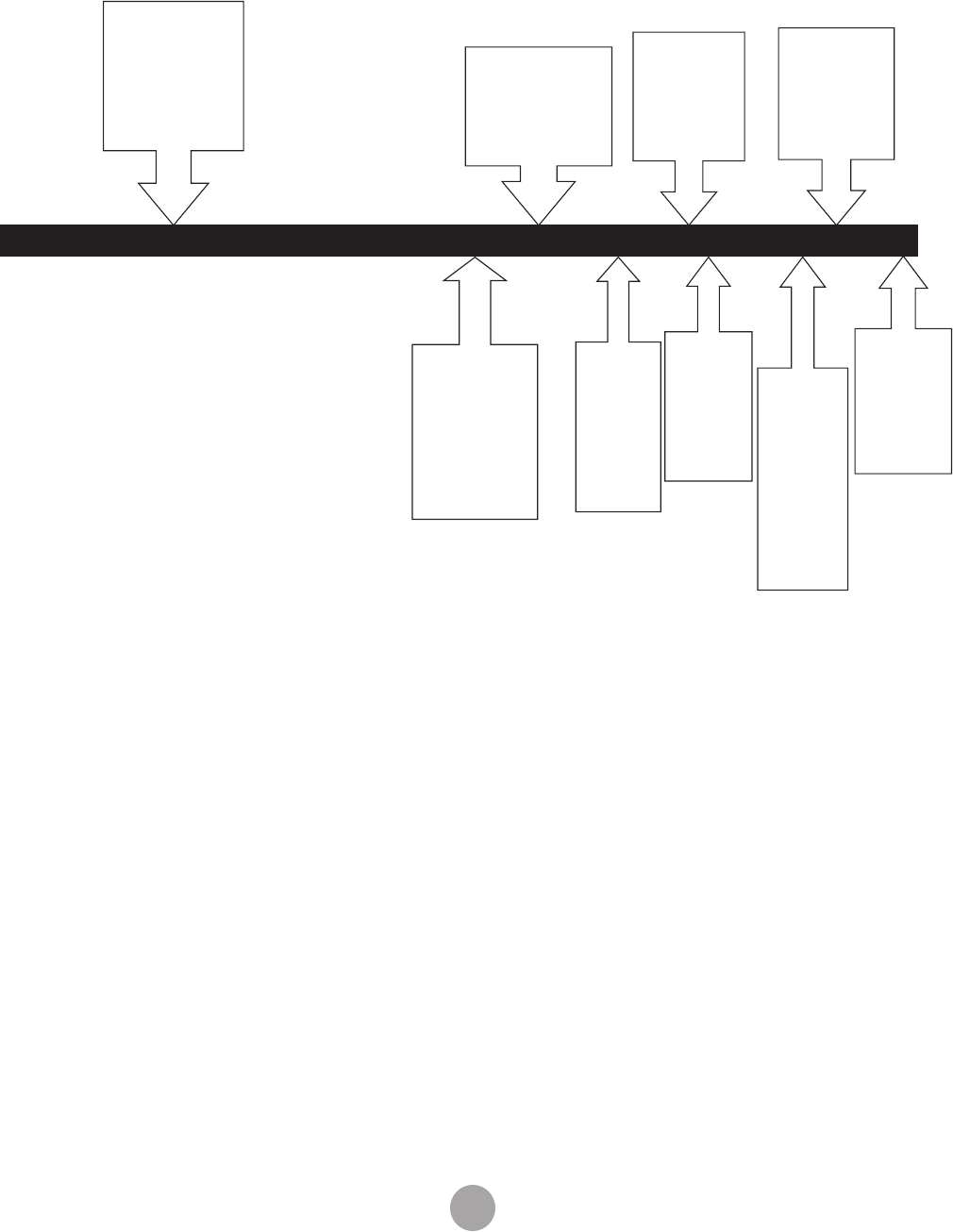

Figure 1: Timeline of Significant Events in Development of Statement of Cash Flows

November 1987:

FASB issues

SFAS 95,

“Statement of

Cash Flows” (now

codified as ASC

Topic 230).

2004: FASB and

IASB agree to

consider financial

statement project

jointly.

July 2010:

FASB issues

staff draft

on financial

statement

presentation.

April 2015:

FASB issues

exposure draft

to require DM

for NFPs.

2001: FASB

and IASB

independently

begin projects

to review

financial

statement

presentation.

October

2008–April

2009: User

feedback

period on

discussion

paper.

October

2010:

Financial

statement

project

put on

hold.

December

2015: FASB

decides to

allow DM

or IM for

NFPs.

April 2014:

FASB

launches

project

to clarify

principles

on the

statement

of cash

flows.

| 1980 | 1985 | 1990 | 1995 | 2000 | 2005 | 2010 | 2015 |

4

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

comment letters and aggregate the results. The remain-

der of this section provides a detailed breakdown of the

180 comment letters and five tables that classify and

summarize the comment letter contents. Tabulating the

data presents the reader with the same information the

FASB received and does not draw any statistical infer-

ences about the opinions of the overall population.

3

The comment letter analysis results show that, of the

respondents who commented on and expressed a pref-

erence for a particular cash flow statement format, 81%

disapproved of the DM requirement. These results are

in contrast to Wallace, et al., who reported that the ma-

jority (57.2%) of respondents of four key countries

(Australia, New Zealand, the U.K., and the United

States) favored making the DM mandatory.

4

These re-

sults are from an FASB survey in 1987 before SFAS 95

was issued.

Table 1 provides preferences for cash flow formats by

country/region. Of the 180 response letters, 53 were

from the U.S. and 127 (70%) from the remaining coun-

Table 1: Preferences by Country for Method of Presenting Cash Flows

from Operations

Number for Number for

Total Direct Method Indirect Method

Country/Region Respondents Quantity Percent Quantity Percent

Australia 12 5 41.7% 7 58.3%

Austria 1 0 0.0% 1 100.0%

Belgium 3 0 0.0% 3 100.0%

Canada 15 3 20.0% 12 80.0%

Denmark 1 0 0.0% 1 100.0%

Europe 8 0 0.0% 8 100.0%

Finland 1 0 0.0% 1 100.0%

France 8 0 0.0% 8 100.0%

Germany 13 1 7.7% 12 92.3%

Greece 1 0 0.0% 1 100.0%

Hong Kong 1 0 0.0% 1 100.0%

India 1 0 0.0% 1 100.0%

Ireland 3 3 100.0% 0 0.0%

Italy 1 0 0.0% 1 100.0%

Japan 5 0 0.0% 5 100.0%

Malaysia 1 0 0.0% 1 100.0%

Netherlands 4 0 0.0% 4 100.0%

New Zealand 4 3 75.0% 1 25.0%

Pakistan 1 1 100.0% 0 0.0%

Poland 1 1 100.0% 0 0.0%

Scotland 1 0 0.0% 1 100.0%

South Africa 3 2 66.7% 1 33.3%

Spain 1 0 0.0% 1 100.0%

Sweden 2 0 0.0% 2 100.0%

Switzerland 5 0 0.0% 5 100.0%

Taiwan 1 1 100.0% 0 0.0%

U.K. 28 2 7.1% 26 92.9%

U.S. 53 12 22.6% 41 77.4%

Zambia 1 0 0.0% 1 100.0%

Total 180 34 18.9% 146 81.1%

5

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

tries. These responses are consistent with the notion

that strong support exists for the DM in countries

where it has been a required format in the past. For ex-

ample, three of the four respondents in New Zealand

favored the direct cash flow format. In Australia, where

12 respondents expressed a preferred method, 41.7%

favored the direct cash flow format. Table 1 also shows

the preference for countries where the DM has not

been mandated in the past. For example, in the U.K.,

where the direct cash flow format has never been re-

quired, only 7.1% of the 28 respondents were in favor of

mandating direct cash flow disclosures.

Table 2 presents preferences for the two methods by

segment classification. At 92%, respondents from indus-

try are the most supportive of the IM, presumably be-

cause of the ease of compilation since all of these re-

spondents need to make regular cash flow disclosures.

Respondents from public accounting firms and other or-

ganizations had nearly equal support for the DM with

28.6% and 30.4%, respectively.

Table 3 shows the respondents’ preferences catego-

rized as either preparers or users of financial statements.

To make the categorization, we coded public account-

ing firms and industry respondents as preparers and fi-

nancial analysts as users. We classified the remaining re-

sponses as either preparers or users based on whether

they crafted their response letter from the perspective

of a preparer or user. Note that substantially more re-

spondents commented as preparers than as users (153

vs. 27). Less than 16% of the preparers favored the

DM, and 37% of users preferred the DM. Clearly the

IM enjoys favor with both groups as more than 84% of

preparers and 63% of users prefer to use it. As might

be expected, a larger percentage of users (37%) pre-

ferred the DM, reflecting the likelihood that users of

financial statements attach more value to direct cash

flow information.

Regarding financial statement users, two financial an-

alyst organizations submitted comment letters worth

noting. The first was from the CFA Institute Centre for

Financial Market Integrity, representing 100,000 ana-

lysts, portfolio managers, financial advisors, and other

Table 2: Preferences by Segment for Method of Presenting Cash Flows

from Operations

Number for Number for

Total Direct Method Indirect Method

Classification Respondents Quantity Percent Quantity Percent

Public accounting firms 42 12 28.6% 30 71.4%

Industry 87 7 8.0% 80 92.0%

Other 46 14 30.4% 32 69.6%

Undisclosed 5 1 20.0% 4 80.0%

Total 180 34 18.9% 146 81.1%

Table 3: Preferences by Role for Method of Presenting Cash Flows

from Operations

Number for Number for

Total Direct Method Indirect Method

Classification Respondents Quantity Percent Quantity Percent

Preparers 153 24 15.7% 129 84.3%

Users 27 10 37.0% 17 63.0%

Total 180 34 18.9% 146 81.1%

6

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

investment professionals in 134 countries. The Institute

indicated strong support for the DM, suggesting it

would improve transparency of operating cash flows and

thus be more useful to analysts and other users. The

letter indicated that the IM makes it more difficult for

investors to perceive any possible earnings manage-

ment. An illustration showed the extent to which Enron

engaged in financial engineering to overstate operating

cash flows and suggested that the company did not ex-

pect investors would notice the diminishing cash flows

under the IM.

The Institute also responded to the allegation that

the transition cost to the DM is prohibitive. It sug-

gested that these costs are notoriously difficult to esti-

mate and that, in the past, preparers have overstated

implementation difficulties associated with proposed

reporting improvements. The comment also addressed

the difference between the indirect-direct method that

involves an accrual-to-cash approach and the direct-

direct approach that captures cash transaction data. It

points out the contradictory and counterintuitive posi-

tions of those opposed to the direct mandate; oppo-

nents agree cash is king yet they support less useful

methods to present cash flows. Although it prefers the

direct-direct method, the Institute indicates concerns

about the indirect-direct method are unwarranted. It ar-

gues that if a company maintains proper accrual records,

adjustments to cash basis will be reliable and useful.

The second notable analyst letter was from the CFA

Society of the UK. The letter represented an unofficial

supplement to the Institute’s letter discussed earlier

and provided survey results from the Society’s mem-

bers. The Society received 351 responses, which consti-

tuted slightly less than 5% of its membership of 8,000

U.K. investment professionals. It reported that a small

majority favors the DM and suggested that the benefits

outweigh the costs. At least 80% of the Society’s mem-

bers, however, stated that the FASB and the IASB

needed to improve the statement’s transparency

through increased note disclosures.

Table 4 compares the responses of a group titled

“banks and financial institutions” (“banks”) to other in-

dustries. Banks submitted 21 comment letters, and

businesses from other industries submitted 159 com-

ment letters. An overwhelming 95.2% of banks pre-

ferred the IM, and 79.2% of businesses from other in-

dustries preferred the IM. Twenty banks preferred the

IM because of its usefulness to users of bank financial

statements. The one bank that preferred the DM com-

mented on its usefulness when reading the financial

statements of other businesses, such as when a bank re-

views a client’s financial statements to decide whether

to make a loan.

Regarding the overall tone of the 21 bank comment

letters, many respondents suggested that the statement

of cash flows (regardless of the method prepared) lacks

the functionality needed for analyzing banking institu-

tions. For example, the banks indicated the statement

does not contain information about a given bank’s liq-

uidity risk exposure. The letters also emphasized that

banks manage cash flows on a comprehensive basis that

does not fit easily into the statement categories.

The banks also maintained it would be too costly to

change to the DM. Several banks stated they were un-

aware of any user groups that would prefer banks to use

the DM. Of the banks currently using International

Financial Reporting Standards (IFRS), they preferred

mandating IFRS 7, “Financial Instruments: Disclosures,”

Table 4: Preferences for Financial Classification for Method of

Presenting Cash Flows from Operations

Number for Number for

Total Direct Method Indirect Method

Classification Respondents Quantity Percent Quantity Percent

Banks and financial 21 1 4.8% 20 95.2%

institutions

Other industries 159 33 20.8% 126 79.2%

Total 180 34 18.9% 146 81.1%

7

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

disclosure requirements instead of changing the cash flow

statement format. As a matter of background, IFRS 7 re-

quires two main categories of disclosures: information

about the significance of financial instruments and infor-

mation about the nature and extent of risks arising from

financial instruments.

The bank and financial institutions respondents gen-

erally agreed that although the DM might be relevant

for other industries, it should remain optional for banks,

which is in contrast to prior banker survey results. As

stated in the responses to Exposure Draft #23 for SFAS

95, bankers preferred the DM.

5

They said that the DM

is more useful to financial statement users and suggest

converting from IM data to DM information imposes an

additional cost for users. We found no such preference

by bankers in the recent data.

Table 5 outlines the arguments from respondents

in support of their preferences regarding cash flow

format.

6

As shown in Panel A, of the respondents who

favored the DM format, the most common reason was

that the DM provided useful information (50.0%). The

second most common reason was “cohesiveness and

disaggregation (35.3%),” which was the rationale the

FASB and the IASB cited for undertaking the financial

statement presentation project. Several respondents

stated they believed the benefits outweighed the costs

of DM disclosures (8.8%). Last, the category titled

“Other” includes any remaining reason for support of

the DM.

Panel B of Table 5 shows that cost (61.0%) was the

largest concern to those who responded negatively to

the DM format. Generally, large companies with elabo-

rate structures and complicated enterprise resource

planning (ERP) systems are most affected. Yet only a

limited number of respondents provided a cost estimate

for their implementation and ongoing budget estimate

for DM presentation. To the researchers’ knowledge,

no one has conducted a comprehensive investigation

of the cost/benefit tradeoff of converting to the DM.

7

Intel Corp., however, estimated it would cost more than

Table 5: Arguments Provided by Respondents in Support of Their Preferences

Frequency

a

Percent

Panel A: Reasons for Direct Method of Cash Flow Presentation Taken

f

rom the 34 Letters Written in Support of Direct Cash Flow Format

Direct method provides useful information 17 50.0%

Direct method achieves cohesiveness and disaggregation 12 35.3%

Benefits outweigh costs 3 8.8%

Other 9 26.5%

Panel B: Reasons against Direct Method of Cash Flow Presentation

Taken from the 146 Letters Written in Dissent

Cost concern/costs outweigh benefits 89 61.0%

Not convinced direct method better information 36 24.7%

Indirect method provides useful information 14 9.6%

Management should have the choice 11 7.5%

Statement of cash flows rarely used in decision making 10 6.8%

Direct method too complex to implement/understand 9 6.2%

Does not achieve cohesiveness and disaggregation 4 2.7%

Indirect method connects better to other financial statements 4 2.7%

Other 19 13.0%

a

The sums of the frequencies and percentages do not match the total number

of letters because some respondents provide more than one reason.

8

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

$5 million to implement the DM and another $2 mil-

lion per year post-implementation. Alcoa and Deutsche

Bank estimated implementation would cost between

$20 million and $30 million and in the double-digit mil-

lion euro range ($15+ million), respectively.

The respondents who opposed a DM mandate stated

they did not believe the DM provided more useful in-

formation (24.7%). Some respondents’ explanations did

not appear to consider the financial statement user’s

perspective. For example, 7.5% of respondents stated

management should choose the method. Others said

the DM was too complicated (6.2%) or did not achieve

the cohesiveness and disaggregation (2.7%) goals of the

FASB and the IASB.

CURRENT DEVELOPMENTS AND ONGOING

EFFORTS TO MANDATE

The FASB recently again began efforts to require the

DM for business enterprises. As the Figure 1 timeline

shows, two recent developments indicate this is the

case. In April 2014, the Board began a new project ti-

tled Clarifying Certain Existing Principles on

Statement of Cash Flows. The project includes two

main objectives. The first objective is to provide guid-

ance on how to classify particular cash flows that may

contain aspects of more than one category, such as a

cash flow from a derivative instrument that may have

features of both investing and financing activities. The

second objective is to provide classification guidance for

specific transaction types. In the last five years, as many

as 600 companies have had to file restatements because

of cash flow misclassifications.

8

These objectives indi-

cate that the FASB had plans to further develop the

Statement.

Even more recently and more importantly, the Board

initiated a project that seemed to signal a new attempt

to mandate the direct method for business enterprises.

In April 2015, it issued an exposure draft for not-for-

profit organizations titled “Presentation of Financial

Statements of Not-for-Profit Entities.” The Board re-

quested comments on a requirement for not-for-profit

entities to prepare their statements of cash flow using

the DM. In a departure from prior proposed guidance,

including the 2008 discussion paper we discussed, the

proposal did not require entities to simultaneously pre-

pare a separate reconciliation of net income to net cash

flows from operating activities.

To obtain feedback on the proposal, the FASB sur-

veyed 227 members of its Not-For-Profit Resource

Group (NFPRG), which included auditors and prepar-

ers who had specific experience with the DM. The

Board received 91 responses, and the results were con-

sistent with the reported results for the 2008 discussion

paper. While 39% agreed the DM conveyed informa-

tion that provided incremental benefits, 51% did not

believe the incremental benefit outweighed the incre-

mental cost.

Although the 2015 project pertains to not-for-profit

organizations, the FASB may have intended to extend

the not-for-profit DM mandate to for-profit business en-

tities. FASB Vice Chairman James L. Kroeker said, “I’d

challenge you to look at the changes we’re making for

not-for-profits that would eliminate the use of the indi-

rect method of cash flows.” He added, “There’s the

idea that perhaps we would extend that to business en-

terprises as well,” thus indicating that the Board may

make another attempt to mandate the direct method

presentation for business enterprises.

9

Kroeker’s comments also indicated that the mandate

may not require the DM to be accompanied by a recon-

ciliation to net income. In December 2015, however,

the FASB voted four to three to allow not-for-profit en-

tities to use either method in their presentation of cash

flows. They also decided to allow not-for-profit entities

to utilize the direct method without requiring the inclu-

sion of an indirect reconciliation of operating cash flows.

Prior to the decision, the FASB had received mixed

support from respondents to its proposals, with some re-

spondents indicating the direct method should not be

required for not-for-profit entities until it is required for

business entities.

CONSIDER THE POTENTIAL COSTS AND BENEFITS

While it is true that the DM’s straightforward presenta-

tion may be more advantageous to some users, the IM

brings another level of usefulness to the statement. The

reconciliation of accrual basis net income with cash pro-

vided by operating activities offers an initial assessment

of earnings quality by showing the magnitude of accrual

changes employed to arrive at net income each period.

9

M A N A G E M E N T A C C O U N T I N G Q U A R T E R L Y S P R I N G 2 0 1 6 , V O L . 1 7 , N O . 3

Indeed, the level of discretionary accruals and portion

of accruals that result in actual cash flows in a timely

manner are two methods for assessing earnings quality

that are discussed in the academic literature.

1

0

Because companies often manage earnings to meet a

targeted amount of earnings per share with the aggres-

sive use of accruals, persistent increases in current re-

ceivables accompanied by accrual net income similar to

that of the prior period (or close to zero) could indicate

the presence of earnings management. While profes-

sionals can conduct earnings quality assessments by

other means, the cash flow statement prepared using

the IM readily shows the differences in accrual- vs.

cash-basis income and the changes in accruals.

Therefore, in our opinion, eliminating the option for

the IM or allowing the DM without reconciliation to

net income could result in a less useful statement for

some users.

As the accounting community struggles to come to

terms with the presentation of cash flows, many respon-

dents state the DM is likely more advantageous for

some users. This is a position that the existing literature

supports, but the consensus favored the IM throughout

the life of the statement. Over the years, opinions re-

mained remarkably consistent. As we described, the

comments from the NFPRG in 2015 are consistent with

those for the 2008 discussion paper and with the 1987

consensus for Exposure Draft #23 issued for SFAS 95 at

the Statement’s inception. The one notable exception is

banks that preferred the DM for SFAS 95 but favor the

IM in the 2008 discussion paper. Over the Statement’s

life, interested parties have indicated that the cost of

switching to the DM is not worth any incremental bene-

fit over the IM that might exist. Because rule makers

have consistently favored mandating the DM, it is likely

that the Statement will undergo a transformation in the

future. The discussion to mandate the DM is almost

certainly going to continue, so accounting and finance

professionals will need to consider the potential costs

and benefits of the DM and IM going forward.

■

Note: On August 18, 2016, the FASB issued ASU

No. 2016-14, “Not-for-Profit Entities (Topic 958):

Presentation of Financial Statements of Not-for-Profit

Entities.” The Board says these new rules complete

Phase I of the project. They continue to allow nonprof-

its to choose either the DM or IM to present operating

cash flows, and they no longer require the inclusion of

an indirect reconciliation of operating cash flows. But

more could happen in other areas.

Nathan H. Jeppson, Ph.D., CPA, is an assistant professor

in the accounting department at Montana State University

at Bozeman. You can reach Nathan at (406) 994-6204 or

John A. Ruddy, CPA, CFA, is an assistant professor in the

finance department at the University of Scranton in

Scranton, Pa. You can reach John at (570) 941-4303 or

David F. Salerno, Ph.D., CPA, is an assistant professor in

the accounting department at the University of Scranton.

You can reach David at (570) 941-4313 or

Endnotes

1 David M. Katz, “FASB Revisits the Cash-Flow Statement,”

CFO, September 30, 2014.

2 Tammy Whitehouse, “FASB Proposal May Foreshadow

Changes to Cash Flow Rules,” Compliance Week, April 24, 2015.

3 It should be noted that the 91 respondents in the 2015 NF-

PRG and the 229 respondents to the 2008 discussion paper

were self-selected participants when they commented. Thus,

similar to prior studies, self-selection bias may exist, so it can-

not be assumed the discussion represents the opinions of all

preparers and users of financial statements.

4 R.S. Olusegun Wallace, Mohammed S.I. Choudhury, and

Maurice Pendlebury, “Cash Flow Statements: An International

Comparison of Regulatory Positions,” The International Journal

of Accounting, Volume 32, Issue 1, January 1997, pp. 1-22.

5 Ibid.

6 While some letter writers only provided one explanation for

their preference, many provided two. No more than two argu-

ments were tallied for each letter.

7 Jeffrey Hales and Steven Orpurt, “A Review of Academic

Research on the Reporting of Cash Flows from Operations,”

Accounting Horizons, September 2013, pp. 539-578.

8 Tammy Whitehouse, “FASB Shifts Gears on Cash-Flow

Classification Issues,” Compliance Week, April 7, 2015.

9 Tammy Whitehouse, “FASB Proposal May Foreshadow

Changes to Cash Flow Rules,” Compliance Week, April 24, 2015.

10 For a discussion of discretionary accruals, see Jennifer Jones,

“Earnings Management During Import Relief Investigations,”

Journal of Accounting Research, Volume 29, Issue 2, Autumn

1991, pp. 193-228; for a discussion of accruals and cash flows,

see Patricia Dechow and Ilia Dichev, “The Quality of Accruals

and Earnings: The Role of Accrual Estimation Errors,” The

Accounting Review, Volume 77, Supplement 2002, pp. 35-59.