508-12/15/22-mh

November 9, 2022 - Draft (6.0)

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

UNITED STATES

POSTAL REGULATORY COMMISSION

Washington, D.C. 20268-0001

FORM 10-K

þ

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2022

or

¨

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number N/A

UNITED STATES POSTAL SERVICE

(Exact name of registrant as specified in its charter)

Washington, D.C. 41-0760000

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

475 L'Enfant Plaza, S.W.

Washington, DC 20260

(202) 268-2000

(Address and telephone number, including area code, of registrant's principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Not applicable

Trading Symbol(s)

Not applicable

Name of each exchange on which registered

Not applicable

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes þ No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act

of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes ¨ No ¨ Not Applicable þ

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was

required to submit such files). Yes ¨ No ¨ Not Applicable þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and

"emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ¨

Smaller reporting company ¨ Emerging growth company ¨ Not Applicable þ

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its

internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting

firm that prepared or issued its audit report. þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨No þ

Documents incorporated by reference: None

2022 Report on Form 10-K United States Postal Service

TABLE OF CONTENTS

UNITED STATES POSTAL SERVICE

Page

Glossary of Acronyms

2

Cautionary Statements

4

Part I.

ITEM 1. Business 4

ITEM 1A. Risk Factors 10

ITEM 1B. Unresolved Staff Comments 16

ITEM 2. Properties 16

ITEM 3. Legal Proceedings 16

ITEM 4. Mine Safety Disclosures 16

Part II.

Market for Registrant's Common Equity, Related Stockholder Matters, and

ITEM 5. 16

Issuer Purchases of Equity Securities

Management's Discussion and Analysis of Financial Condition and Results of

Operations

16

ITEM 7.

ITEM 7A. Quantitative and Qualitative Disclosures About Market Risk 42

ITEM 8. Financial Statements and Supplementary Data 43

Changes in and Disagreements with Accountants on Accounting and Financial

ITEM 9. 69

Disclosure

ITEM 9A. Controls and Procedures 69

ITEM 9B. Other Information 73

ITEM 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections

73

Part III.

ITEM 10. Governors, Executive Officers, and Corporate Governance 73

ITEM 11. Executive Compensation 76

Security Ownership of Certain Beneficial Owners and Management and

ITEM 12. 87

Related Stockholder Matters

ITEM 13. Certain Relationships and Related Transactions, and Governor Independence 87

ITEM 14. Principal Accountant Fees and Services 88

Part IV.

ITEM 15. Exhibits and Financial Statement Schedules 89

ITEM 16. Form 10-K Summary 89

Signatures 90

Exhibits 92

GLOSSARY OF ACRONYMS AND DEFINED TERMS

The following are definitions of some of the terms or acronyms that may be used throughout this report:

Term or Acronym Definition

Annual Report Annual report on Form 10-K

AFL-CIO American Federation of Labor and Congress of Industrial Organizations

APWU American Postal Workers Union, AFL-CIO

ASC Accounting Standards Codification

ASU Accounting Standards Update

Board Board of Governors of the United States Postal Service

Board of Actuaries Board of Actuaries of the Civil Service Retirement System

CARES Act

Coronavirus Aid, Relief, and Economic Security Act, enacted as Public Law 116-136

CEO Chief Executive Officer

CFO Chief Financial Officer

COLA(s) Cost-of-living adjustment(s)

COR House Committee on Oversight and Reform

COVID-19 Coronavirus

CPI Consumer Price Index

CPI-U Consumer Price Index for All Urban Consumers

CPI-W Consumer Price Index for Urban Wage Earners and Clerical Workers

CSRDF Civil Service Retirement and Disability Fund

CSRS Civil Service Retirement System

DOL U.S. Department of Labor

DPMG Deputy Postmaster General

EEOC U.S. Equal Employment Opportunity Commission

EIS Environmental Impact Statement

Exchange Act

Securities and Exchange Act of 1934, enacted as Public Law 73-291

FASB Financial Accounting Standards Board

FECA Federal Employees' Compensation Act

FEGLI Federal Employees Group Life Insurance

FEHB Federal Employees Health Benefits

FERS Federal Employees Retirement System

FERS-FRAE Federal Employees Retirement System-Further Revised Annuity Employees

FERS-RAE Federal Employees Retirement System-Revised Annuity Employees

FFB Federal Financing Bank

GAAP Generally accepted accounting principles in the U.S.

HHS U.S. Department of Health and Human Services

House U.S. House

IRA Inflation Reduction Act of 2022, enacted as Public Law 117-169

MRA Minimum retirement age

NALC National Association of Letter Carriers, AFL-CIO

NGDV Next Generation Delivery Vehicle

2022 Report on Form 10-K United States Postal Service 2

NPMHU National Postal Mail Handlers Union, AFL-CIO

NRLCA National Rural Letter Carriers Association

NRP National Reassessment Process

OFO Office of Federal Operations

OPM U.S. Office of Personnel Management

OWCP Office of Workers' Compensation Programs

PAEA Postal Accountability and Enhancement Act, enacted as Public Law 109-435

PFP Pay-For-Performance

PMG Postmaster General

PRA Postal Reorganization Act, enacted as Public Law 91-375

PRC Postal Regulatory Commission

President U.S. President

PSHB Postal Service Health Benefits

PSRA Postal Service Reform Act of 2022, enacted as Public Law 117-108

PSRHBF Postal Service Retiree Health Benefits Fund

RFA Revenue Forgone Reform Act, enacted as Public Law 103-123

SEC U.S. Securities and Exchange Commission

Senate U.S. Senate

SFFAS Statement of Federal Financial Accounting Standards

TSP Thrift Savings Plan

U.S. United States

U.S.C. U.S. Code

USPS U.S. Postal Service

VP Vice President

2022 Report on Form 10-K United States Postal Service 3

CAUTIONARY STATEMENTS

This report contains forward-looking statements representing our best estimates of known and anticipated

trends believed relevant to future operations as of the date of this report. Statements other than those of current

or historical fact, and all statements accompanied by words such as "may," "will," "could," "expect," "believe,"

"plan," "estimate," "project," or other similar terminology, are intended to be forward-looking statements.

Forward-looking statements involve risks and uncertainties, many of which we cannot control or influence, that

could cause actual results to differ significantly from current estimates. Important factors that could cause actual

results to differ materially from those anticipated in our forward-looking statements include, but are not limited

to, those described under Part I., Item 1A. Risk Factors.

We have no obligation to publicly update or revise any forward-looking statements, whether as a result of new

information, future events, or any other reason.

PART I

ITEM 1. BUSINESS

In accordance with the provisions of the PRA, the United States Postal Service ("Postal Service," "USPS," "we,"

"our," and "us") began operations on July 1, 1971, succeeding the cabinet-level Post Office Department

established in 1792. The PRA enacted our status as an "independent establishment of the executive branch of

the Government of the United States" with the mandate to offer a "fundamental service" to the nation "at fair and

reasonable rates." Our governing statute is codified in Title 39 of the U.S. Code. We generally do not receive tax

dollars for operating expenses and rely solely on the sale of our products and services to fund our operations.

We report our performance as a single business and one reporting segment.

As used herein, all references to years in this report, unless otherwise stated, refer to fiscal years beginning

October 1 and ending September 30. All references to quarters, unless otherwise stated, refer to fiscal quarters.

We serve the American people in all areas of our nation, and through the universal service mission, bind our

nation together by maintaining and operating our unique, vital, and resilient infrastructure. We operate and

manage an extensive and integrated retail, processing, distribution, transportation, and delivery network

throughout the U.S., including its possessions and territories. We retain the largest physical and logistical

infrastructure of any non-military government institution, providing an indispensable foundation supporting an

ever-changing and evolving nationwide communication network. As such, we continue to support and expand

the nation’s physical infrastructure and are fundamental to our nation’s growth and prosperity.

We play a vital role as a driver of commerce and as a provider of delivery services that connect Americans to

one another and to every residential and business address, reliably, affordably, and securely. We serve both

consumer and commercial customers in the communications, distribution and delivery, advertising, and retail

markets throughout the nation and the world. As a result, we maintain a diverse customer base and are not

dependent upon a single customer or small group of customers. No single customer represented more than

10% of operating revenue for the years ended September 30, 2022, 2021, and 2020.

STRATEGY

To provide reliable, efficient, trusted, and affordable universal delivery service, we have established the

following four strategic areas of focus:

• Deliver a World-Class Customer Experience;

• Equip, Empower, Connect, and Engage Employees;

• Innovate Faster to Deliver Value; and

• Invest in our Future Platforms.

2022 Report on Form 10-K United States Postal Service 4

In March 2021, we published our vision and ten-year plan to achieve service excellence and financial stability

entitled Delivering for America (https://about.usps.com/what/strategic-plans/deliveringfor-america/assets/

USPS_Delivering-For-America.pdf).

Our comprehensive plan delivers:

• A modernized Postal Service capable of providing world class service reliability at affordable prices;

• Maintenance of universal six-day mail delivery and expanded seven-day package delivery;

• Workforce stability and investment strategies that empower, equip, and engage each employee and put

them in the best possible position to succeed;

• Innovation that grows revenue and meets changing marketplace needs; and

• Financial sustainability to fund our universal service mission.

Our plan’s strategies for revenue growth, cost savings, and investment, combined with administrative actions,

will enable us to operate in a financially self-sustaining manner while fulfilling our universal service mission.

During 2022 and 2021, we have advanced key elements of our plan, but the plan must be implemented timely

and in full to meet our financial targets. In March 2022, we published our year one progress report detailing the

advances that have been made (https://about.usps.com/what/strategic-plans/delivering-for-america/assets/

usps-dfa-one-year-report.pdf).

GOVERNANCE

The law stipulates an eleven-member Board, which consists of our PMG, our DPMG, and nine independent

Governors. The PMG is appointed by the Governors, and the DPMG is appointed by the Governors and the

PMG. The Governors are appointed by the President with the advice and consent of the Senate. As of the date

of this report, we have a full Board.

SERVICES

We offer two categories of services, which are classified by the PAEA as Market-Dominant and Competitive

"products." However, throughout this report, we use the term "services" for consistency with other descriptions

of services we offer. We fulfill our legal mandate to provide universal services at fair and reasonable prices by

offering a variety of postal services to our many customers. Our Governors approve our prices and fees, subject

to a review process by the PRC.

We provide our services through 31,000 Post Offices, stations, and branches that are managed by the Postal

Service, 2,600 additional Contract Postal Units, Community Post Offices, Village Post Offices, a large network

of commercial outlets, which sell stamps and services on our behalf, and through our website www.usps.com.

Mail deliveries are made to 165 million city, rural, PO Box, and highway delivery points. Our operations are

conducted in the domestic market, although we engage with foreign postal administrations to enable customers

to both send and receive mail and packages internationally. Our international revenue represented 2% of our

operating revenue for the year ended September 30, 2022.

CLASSIFICATION AND PRICING

Periodic reclassification of services from Market-Dominant to Competitive, which requires PRC approval, is

necessary to rationalize service offerings. The additional flexibility provided in Competitive services allows us to

better offer services to meet customer needs, increase our business, and price our services competitively within

the markets in which we operate. Information regarding PRC decisions and pending dockets may be obtained

on the PRC website: www.prc.gov.

Market-Dominant Services

Market-Dominant services account for 58% of our annual operating revenues. Market-Dominant services

include, but are not limited to, First-Class Mail, Marketing Mail, Periodicals, some types of International Mail,

Package Services, and certain other services.

2022 Report on Form 10-K United States Postal Service 5

Price increases for these services are generally subject to a price cap, as determined by the PRC. Prices in

effect until August 29, 2021 were subject to a price cap system based solely on the increase in the CPI-U.

Prices in effect since August 29, 2021 are subject to a price cap system partially based on the increase in the

CPI-U, but also allowing for some additional pricing flexibility and authority, including a density-based rate

authority, retirement-based rate authority, and authority for non-compensatory classes.

Competitive Services

Competitive services, such as Priority Mail, Priority Mail Express, First-Class Package Service, Parcel Select,

Parcel Return Service, and some types of International Mail, have greater pricing flexibility and are not limited

by a price cap. As required by 39 U.S.C. §3633, prices for each Competitive service must cover its attributable

cost as determined using methodologies approved by the PRC, and Competitive services collectively must

contribute an appropriate share (as determined by the PRC) to the institutional costs of the Postal Service. In

general, we attempt to set our prices for Competitive services at rates that maximize revenue and contribution.

SERVICE CATEGORIES

Management uses the following broad service categories to describe and report on our performance:

• First-Class Mail - This category encompasses letters, cards, or large envelopes destined for either

domestic (up to 13 ounces) or international (up to nearly 1 pound) delivery. First-Class Mail letters

include postcards, correspondence, bills or statements of account, and payments.

• Marketing Mail - This category includes advertisements and marketing packages, weighing less than

16 ounces and meeting the criteria of not being required to be mailed using First-Class Mail services

because of the content. Marketing Mail is typically used for direct advertising to multiple delivery

addresses. Every Door Direct Mail enables customers to prepare direct mailings without names and

addresses for distribution to all business and residential customers on individual carrier routes.

• Shipping and Packages - This category includes four sub-categories:

◦ Priority Mail Services - This sub-category includes Priority Mail, which is offered as a service

both within the U.S. and abroad with the domestic, day-specified (non-guaranteed) delivery.

Priority Mail includes basic insurance up to $100 and is required for mailpieces that weigh more

than 13 ounces when the mailpiece contains matter that must be mailed as First-Class Mail.

This sub-category also includes Priority Mail Express, which provides an overnight to 2-day

delivery with money-back guaranteed service including tracking, proof of delivery, and basic

insurance up to $100. Priority Mail Express delivery is offered to most U.S. destinations for

delivery 365 days a year.

◦ Parcel Services - This sub-category includes Parcel Select and Parcel Return services,

including "last-mile" services, and USPS Marketing Mail Parcels, which provide commercial

customers with a means of package shipment.

◦ First-Class Package Services - This sub-category includes First-Class Package Service -

Commercial, a shipping option for high-volume shippers of packages that weigh less than one

pound and First-Class Package Service - Retail, for shipment of boxes, thick envelopes, or

tubes, weighing 13 ounces or less.

◦ Package Services - This sub-category includes merchandise or printed matter, such as library

and media mail, weighing up to 70 pounds, and bound printed matter, weighing up to 15

pounds.

• International Mail - This category offers international mail and shipping services with individual

customer contracts and agreements with foreign postal administrations. Priority Mail Express

International and Priority Mail International services compete in the e-commerce cross-border business.

These services provide an option for our consumer and business customers for much of their shipping

2022 Report on Form 10-K United States Postal Service 6

needs to more than 190 countries. Global Express Guaranteed is the premier international shipping

option that offers delivery to major markets.

• Periodicals - This category encompasses the Periodicals class of mail offered for newspaper,

magazine, and newsletter distribution. Customers must receive prior authorization from us to use this

service.

• Other - This broad category includes PO Box services, money orders, and USPS extra services. PO

Box services provide customers an additional method for mail delivery that is private and convenient.

Money orders offer customers a safe, convenient, and economical method for the remittance of

payments. Money orders are available for amounts up to $1,000, can be purchased and cashed at most

Post Offices, or can be deposited or negotiated at financial institutions. USPS Extra Services offer a

variety of service enhancements that provide security, proof of delivery, or loss recovery. These services

include: Certified Mail, Registered Mail, Signature Confirmation, Adult Signature, and insurance up to

$5,000.

For a discussion of economic and other factors affecting the volume of these services and our actions taken to

address these factors, see Part II., Item 7. Management's Discussion and Analysis of Financial Condition and

Results of Operations, Results of Operations, Operating Revenue and Volume.

SERVICE STANDARDS

We measure our performance by establishing and benchmarking against service standards. A service standard

is the stated delivery goal for a mail class or product. We set service standards so that customers and mailers

can expect consistent and predictable delivery. To improve reliability and enhance efficiency, we may

periodically update service standards through our formal regulatory process and with the advice of the PRC.

COMPETITION

We compete for our business in many different markets. A wide variety of communications media compete for

the same types of transactions and communications that are conducted using our services. These channels

include, but are not limited to, newspapers, telecommunications, television, email, social networking, and

electronic funds transfers. The package and express delivery businesses are highly competitive with both

national and local competitors.

The most significant competitive factor for First-Class Mail is digital communication, including electronic mail, as

well as other digital technologies such as online bill payment and presentment. For Marketing Mail, digital forms

of advertising including digital mobile advertising and social media are the most significant forms of competition.

The primary competitors of our Shipping and Packages services are FedEx Corporation, United Parcel Service,

Inc., and Amazon.com, Inc., as well as other national, regional, and local delivery companies, and

crowdsourced carriers who are testing and implementing "last mile" delivery services. Our Shipping and

Packages business competes based on the breadth of our service network, convenience, reliability and

economy of the service provided.

SEASONALITY

Total revenue and volume for all service categories are historically the highest in the first quarter, which includes

the holiday mailing and shipping season, and lowest in the third and fourth quarters during the spring and the

summer. Marketing Mail benefits from strong political and election mail volumes in election years, especially

during presidential and congressional election cycles.

EMPLOYEES

As one of the largest employers in the U.S., our employees are critical to our success and the fulfillment of our

mission. Our employees are hard-working public servants dedicated to moving the mail and making a difference

2022 Report on Form 10-K United States Postal Service 7

in every community across the country. We are committed to improving the employee experience and we

continue to invest in initiatives that will equip, empower, connect, and engage our employees.

At September 30, 2022, our workforce consisted of 635,250 employees, substantially all of whom reside in the

U.S. We categorize our employees into two primary groups: career and pre-career. Career employees are

considered permanent and are entitled to a full range of benefits (e.g., health and retirement) and privileges,

while pre-career employees do not yet have permanent status and do not receive full employee benefits and

privileges. At September 30, 2022, we had 516,750 career employees and 118,500 pre-career employees.

At September 30, 2022, 92% of our employees are covered by collective bargaining agreements. These

agreements include provisions governing work rules and provide for general wage increases, step increases

and COLAs, which are linked to the CPI-W, as well as provisions that limit our ability to reduce the size of the

labor force and restrict the number of pre-career employees. Our labor force is primarily represented by the

APWU, the NALC, the NPMHU, and the NRLCA.

By law, we must consult with management organizations representing most of our employees not covered by

collective bargaining agreements. These consultations provide non-bargaining unit employees in the field with

an opportunity to participate in the planning, development and implementation of certain programs and policies

that affect them. For additional information on our collective bargaining agreements, see Part II., Item 8.

Financial Statements and Supplementary Data, Notes to Financial Statements, Note 10 - Commitments and

Contingencies.

COMPENSATION AND BENEFITS

We endeavor to enhance our role as a preferred U.S. employer, offering stable jobs with flexible compensation

and benefits packages to attract and retain highly qualified employees. We regularly review our compensation

and benefits offerings to ensure we are meeting the needs of our current and future employees.

Along with basic competitive rates, certain employees are also eligible for overtime pay, night shift differential,

and Sunday premium pay. Benefit programs include health, dental, and vision benefits, flexible spending

accounts, paid time off, defined contribution retirement plans, defined benefit retirement plans, and employee

assistance programs, depending on eligibility.

Overall, the total compensation of our median employee was $98,260 during the year ended September 30,

2022. Total compensation for this purpose includes base pay plus other forms of cash compensation, such as

overtime and bonuses, plus any change in pension value.

DIVERSITY AND INCLUSION

We believe diversity means building an inclusive environment that respects the uniqueness of every individual

and encourages the contributions of people from different backgrounds, experiences, and perspectives. We

believe our investment in a strong diversity program creates a positive work environment that recognizes the

contributions of all our employees and provides us with a strategic advantage. As a further commitment to this

investment, in 2021, we established an Executive Diversity Council to advise on diversity, equity, and inclusion

matters, and champion key initiatives to build leadership and organizational capabilities.

We focus on diversity and inclusion in the recruitment, development, and retention of employees. We continue

to be one of the leading employers of historically underrepresented racial groups, women, and veterans, at all

levels of our organization. As of September 30, 2022, historically underrepresented racial groups, women, and

veterans represented 53%, 46%, and 10% of our total workforce, respectively, and 38%, 36%, and 11% of our

senior management, respectively.

EMPLOYEE ENGAGEMENT

We aim to provide employees with an engaged workplace, one in which teams and individuals thrive and

perform at high levels. We use a variety of methods to promote engagement including employee feedback

mechanisms, such as open communication through Next Level Connection conversations, engagement

ambassadors, an annual engagement survey, engagement communications through multiple platforms (e.g.,

social media, videos, newsletters, publications, etc.), engagement action planning, and engagement recognition

2022 Report on Form 10-K United States Postal Service 8

programs. We believe that cultivating an engaged workplace will help us improve both the employee and

customer experience while delivering exceptional business results.

EMPLOYEE DEVELOPMENT

We believe that investing in our employees is a key strategy for individual and organizational success. We

provide a variety of professional development programs, mentoring programs, career development and

succession plans, career conferences, and both in-house and external learning opportunities to meet the

training and development needs of our employees, to fulfill organizational skill requirements, and to provide

individuals with career growth opportunities.

EMPLOYEE SAFETY

Employee safety is a top priority for us, and we strive to provide a workplace that is safe for all employees,

supports disability rights and access, and health management. Prevention is the guiding principle for both

occupational safety and health-related legislation. To avoid accidents and occupational diseases, we have

adopted standard requirements for safety and health protection at the workplace and established compliance

protocols to ensure effective implementation. We promote safety performance using safety programs and safety

leadership recognition, and monitor our performance using key metrics, including a total accident rate.

OVERSIGHT AND REGULATION

As discussed throughout this report, we are subject to oversight by Congress and regulation by the PRC and

certain other government agencies. In addition to Senate confirmation of our Governors, Congress can

influence how we conduct our business and operations through passage of laws. For a discussion of new laws

and regulations that impact us, see Part II., Item 7. Management's Discussion and Analysis of Financial

Condition and Results of Operation, Legislative Update.

REGULATORY MATTERS

We are required to comply with various federal, state, and local laws and regulations concerning numerous

matters, including environmental matters. Except for federal laws specific to the Postal Service, such as the

PRA, the PAEA, and the PSRA, none of these laws have had a material impact on our financial results or

competitive position, or resulted in material capital expenditures. However, the effect of possible future

legislation or regulations on operations cannot be predicted. New laws or regulations, such as the regulation of

greenhouse gas emissions into the environment, may increase our operating costs, including the cost of fuel,

and the potential costs of compliance with any such new laws or regulations.

Our 2022 Annual Sustainability Report is available at about.usps.com/what/corporate-social-responsibility/

sustainability/report/2022/usps-annual-sustainability-report.pdf. This report discusses our sustainability

management approach, including key goals, programs, and metrics used to monitor our compliance and

commitment to sustainability.

REGULATORY REPORTING

We are not a reporting company under the Exchange Act, and are not subject to regulation by the SEC.

However, the PAEA requires us to file with the PRC certain financial reports containing information prescribed

by the SEC under Sections 13 or 15(d) of the Exchange Act. These reports include Annual Reports, Quarterly

Reports, and current reports.

We are also required by law and regulations to disclose operational and financial information beyond what the

law requires of most U.S. government entities and private-sector companies. Pursuant to Title 39 of the U.S.

Code and PRC regulations, we must also file additional information with the PRC, including Cost and Revenue

Analysis reports, Revenue, Pieces, and Weight reports, financial and strategic plans, and the Annual Report to

Congress. These reports can be found online at about.usps.com/what/financials. Requests for copies of our

reports may also be sent to the following address: Corporate Communications, United States Postal Service,

475 L'Enfant Plaza, SW, Washington, DC 20260-3100.

2022 Report on Form 10-K United States Postal Service 9

ITEM 1A. RISK FACTORS

We are subject to various risks and uncertainties that could adversely affect our business, financial condition,

results of operations, and cash flows. In addition to the material risks and uncertainties that are described

below, others that we do not yet know of or that we currently believe are immaterial could arise or become

material and may also impair our business.

OPERATIONAL AND MARKET RISK FACTORS

Our business and results of operations are significantly affected by competition from other companies

in the delivery marketplace, as well as competition from substitute products and digital communication.

If we do not compete effectively, operate efficiently, and increase revenue and contribution from other

sources, this adverse impact of competition may become more substantial over time.

Our marketplace competitors include national, regional, and local providers of package delivery services. Our

competitors have different cost structures and fewer regulatory restrictions than we do, which allows them to

offer differing services and pricing. This may hinder our ability to remain competitive in these service areas. In

addition, some of our competitors have broader access to public capital markets, which allows them greater

freedom in the financing and expansion of their business.

Customer usage of postal services continues to shift to substitute products and digital communication, a trend

that has been further exacerbated by the effects of the pandemic. Despite the sustained effect that the

pandemic has had on customer demand during 2022, the long-term impact that the pandemic may have on

these shifts is still uncertain. First-Class Mail, such as the presentment and payment of bills, has been eroded

by competition from electronic media, driven by some of our major commercial mailers which actively promote

the use of online services. Marketing Mail has experienced declines due to mailers' growing use of digital

advertising, including digital mobile advertising, though this service category has stabilized and has proven to

be a resilient marketing channel. The volume of our Periodicals service continues to decline as consumers

increasingly use electronic media for news and information. Periodical advertising has also experienced a

decline as a result of the move to electronic media.

The Postal Service's Competitive service volumes have historically grown due to significant volume

growth from certain major customers. These customers continue to build the delivery capability that

could enable them to divert volume away from the Postal Service.

Historic growth in our Competitive service volumes has largely been attributable to certain of our largest

customers, a trend that was further accelerated by the pandemic as the nation has increasingly relied on the

safety and convenience of e-commerce. However, during 2022, our Competitive service volumes decreased

compared to the prior year, as the impacts of the pandemic began to abate and certain of our largest customers

returned to building their delivery capability, which enables them to divert volume away from the Postal Service

over time. As these major customers divert significant volume away from the Postal Service, our Competitive

service volumes may continue to decline.

Adverse events may call into question our reputation for quality and reliability or our ability to deliver

the mail and could diminish the value of our brand. This could adversely affect our business operations

and operating revenue.

Our brand, a valuable asset, represents quality and reliable service. We use our brand extensively in sales and

marketing initiatives and exercise care to defend and protect it. Any event, whether real or perceived, that calls

into question our long-term existence, our ability to deliver mail and packages, our quality, or our reliability could

diminish the value of our brand and reputation and could adversely affect our business operations and operating

revenue.

Our need to streamline our operations in response to declining mail volume may result in significant

costs. The measures we are considering may be insufficient to reduce our workforce and physical

infrastructure to a level commensurate with declining mail volume.

Our ongoing reviews of cost-savings opportunities may identify opportunities that impact mail processing

operations or affect lobby hours of retail units, Post Offices, or other facilities. Presently, our regular review of

the carrying value of our assets has not resulted in significant write-downs of our physical assets. However,

2022 Report on Form 10-K United States Postal Service 10

future changes in business strategy, operations, legislation, government regulations, or economic or market

conditions may result in material impairment write-downs of our assets, adversely affecting our business and

financial results.

Our success depends on our ability to remain an employer of choice. Failure to attract and retain

qualified employees could adversely affect our business operations.

As one of the largest employers in the U.S., our people are our greatest asset and our success depends on

investing in their future. Difficulty recruiting, developing, engaging, and retaining our employees, including

successors to members of our senior management, could have an adverse impact on our business.

Furthermore, our pre-career employee positions have historically experienced high turnover rates, which can

lead to increased labor costs for recruiting and hiring. If we fail to strengthen our employee experience, it could

diminish our status as an employer of choice, and have an adverse impact on our business.

We rely on third parties for air transportation to deliver our mail throughout the nation and abroad. A

significant disruption in air transportation service could adversely affect our business and results of

operations.

We do not own or operate aircraft and we rely on third parties for the air transportation service required to

deliver our mail and packages to various destinations within the U.S. and abroad. As such, we are subject to the

risk of these providers' business operations and also to the adoption of regulatory requirements and other

events that affect specific airlines or the airline industry as a whole, which could affect air service or temporarily

ground the fleets of one or more of our providers.

A failure to protect the privacy of customer or employee information could damage our reputation and

result in a loss of business.

We have invested in technology and employ a variety of technology security initiatives aimed at protecting

organizational information, as well as customer information. As one of the U.S. government entities most trusted

by the nation, protecting the confidentiality of data that we obtain is paramount to us. However, should our

information technology security initiatives not fully insulate us from a security breach or data loss, our reputation

could be damaged, resulting in an adverse effect on our operations and financial results. Moreover, unlike other

non-governmental entities in our industry, we must abide by the Privacy Act of 1974, which restricts how we can

collect, use, maintain, and disseminate personally identifiable information and prescribes civil remedies for non-

compliance.

We rely extensively on computer systems and technology to manage the delivery of mail, process

transactions, summarize results, and manage our business, the failure or disruption of which could

adversely affect our business operations and financial results. We also face cybersecurity threats which

may result in breaches of systems containing confidential or sensitive information, and/or our inability

to operate systems necessary for conducting certain operations.

Our operational and administrative information systems are among the largest and most complex systems

maintained by any organization in the world. Any disruption to our infrastructure, including those impacting

computer systems that facilitate mail handling and delivery and customer-utilized websites, or to the

infrastructure of our service providers, could adversely impact customer service, mail volume, and revenue, and

result in significant increased costs. Any significant systems failure could cause delays in the processing and

delivery of mail or result in the inability to process operational and financial data. Such disruptions could impair

our reputation for reliable service, which would also adversely affect results of operations.

We also depend on and interact with third-party technology and systems. These may include service

organizations that we use for our metered postage revenue and other services, and we often are reliant on

certain information from these third parties to record such revenue. Like us, these third parties are subject to

risks imposed by data breaches, cyberattacks, and other events or actions that could damage or disrupt their

networks or systems, or otherwise affect our financial reporting.

Reports of cyber incidents affecting national security, intellectual property, and individuals have been

widespread, with reported incidents involving data loss or theft, economic loss, computer intrusions, and privacy

breaches. The source of such threats is wide-ranging, and because the techniques used by those who

perpetrate cyber incidents are increasingly sophisticated, change frequently, are complex, and are often not

2022 Report on Form 10-K United States Postal Service 11

recognized until launched, we may not be able to fully anticipate threats to our systems and assets, or to

implement effective preventive measures against all cyber threats, despite our best efforts. The ability to

maintain confidentiality, integrity, and availability of information is critical to fulfilling our mission, and system

failures resulting from these threats could damage our reputation, resulting in loss of business and increased

costs.

Due to our recent and projected cash constraints, our operational performance in the future could be at

risk as a result of inadequate capital investment in facilities, delivery vehicles, mail processing

equipment or information technology infrastructure, all of which are essential for our operations.

If our operations do not generate the liquidity we require, we may be forced to reduce, delay, or cancel

investments in technology, facilities, and/or transportation equipment, as we have done in the recent past, while

our competitors and other businesses are pursuing advanced, competing technologies and equipment.

Additionally, our aging facilities, equipment, and transportation fleet could inhibit our ability to be competitive in

the marketplace, deliver a high-quality service and meet the needs of the American public. The changes in the

economic landscape in recent years have increased the importance for us to invest in our operations in order to

remain competitive. Failure to anticipate or react to our competition, market demands, and/or new technology

due to inadequate cash reserves is a significant operational risk. An aging or potentially obsolete infrastructure

could result in a loss of business and increased costs.

FINANCIAL RISK FACTORS

Current and future management actions to generate cash flows by increasing efficiency, reducing costs

and generating additional revenue may not be sufficient to meet all of our financial obligations or to

carry out our strategy.

Our strategies to increase efficiency, to reduce costs by adjusting our processing and delivery networks,

infrastructure, and workforce, and to retain and grow revenue are currently constrained by contractual, statutory,

regulatory, and legislative restrictions. Accordingly, our ability to react quickly to the changing economic climate

and industry conditions is inhibited. We have also proposed administrative changes, such as changes to retiree

benefit funding rules determining how OPM apportions the costs for CSRS benefits for employees and retirees

that worked for both the Post Office Department and the Postal Service. These administrative changes are

needed to provide us with the legal authority to implement additional measures to increase cost savings. While

the enactment of the PSRA is a critical component of improving our financial condition and reduces our short-

term financial obligations, without the successful implementation of management initiatives and the adoption of

additional administrative changes, our ability to generate adequate cash flow is still at risk.

We have a substantial amount of indebtedness.

As of September 30, 2022, we reported outstanding debt obligations to the FFB of $10.0 billion.

As of September 30, 2022, we have an estimated underfunded PSRHBF liability of $23.7 billion, as reported by

OPM, which we will be required to fund in future periods.

As of September 30, 2022, we have estimated underfunded CSRS and FERS liabilities of $43.2 billion and

$32.9 billion, respectively, as reported by OPM, which we will be required to fund in future periods. Of these

amounts, we are currently liable for $10.8 billion and $7.3 billion for CSRS and FERS, respectively, which we

have reported as current liabilities within Retirement Benefits in the accompanying Balance Sheets for the

amounts due and payable for invoiced but unpaid CSRS and FERS contributions.

Our significant indebtedness and unpaid retirement obligations have important consequences. They limit our

flexibility in planning for, or reacting to, changes in the business environment or competition. They place us at a

competitive disadvantage compared to commercial competitors that may have less debt and which have

broader access to public capital markets. They also could require us to dedicate a substantial portion of our

future cash flows from operations to payments on debt and retirement obligations, thus reducing the availability

of cash flows to fund working capital, capital expenditures and other general organizational activities.

2022 Report on Form 10-K United States Postal Service 12

A union contract arrived at either through negotiation or arbitration could have a significant adverse

impact on our future results of operations by impacting our control over wages and benefits and/or by

limiting our ability to manage our workforce effectively.

Our collective bargaining agreements currently in force include provisions for mandatory COLAs, which are

linked to the CPI-W. The actual and projected COLA increases, starting in September 2021, have been larger

than the historical increases over the past decade. We made COLA-based pay adjustments that have increased

our expenses by $1.6 billion in 2022 and are expected to increase our expenses by $1.6 billion in 2023.

Continued impacts to consumer inflation could have a further significant adverse impact on our labor costs. The

agreements also contain provisions that limit our ability to reduce the size of the labor force and employ pre-

career personnel. Reductions in the size and cost of our labor force may be necessary to offset the effects of

declining volume and revenue.

Our ability to negotiate contracts that control labor costs is essential to achieving financial stability. We have no

assurance that we will be able to negotiate contracts in the future with our unions that will result in a cost

structure that is sustainable within current and projected future revenue levels. In addition, if our future

negotiations should fail and involved parties proceed to arbitration, the risk of an adverse outcome exists, as

there is no current statutory mandate requiring an interest arbitrator to consider our financial health in issuing an

award. An unfavorable award in arbitration could have significant adverse consequences on our ability to meet

future financial obligations.

Furthermore, an increase in the CPI-W may not correspond to an equivalent increase in the CPI-U, which

affects the prices of our Market-Dominant services under current law, as the two indexes are calculated

differently. Therefore, we may not be able to increase the prices of our services to keep up with increases in our

wages.

Health and pension benefit expenses are significant to us.

With 516,750 career employees, 499,000 retirees and survivors who receive retirement health benefits, and

702,000 retirees and survivors who receive pension benefits, our expenses relating to employee and pension

benefits are significant. We participate in U.S. government pension and health and benefits programs for

employees and retirees, including the FEHB Program, the CSRS, and the FERS, as required by law or

contractual agreement with our unions. We have no control or influence over the benefits offered by these plans

and are required to make contributions to these plans as specified by law or, in the case of health benefits for

the majority of our current employees, by contractual agreements with our unions. Several factors including

participant mortality rates, returns on investment, and inflation, all of which are outside of our control, could

require us to make significantly higher future contributions to these plans, which would adversely affect our

financial condition and results of operations.

Workers' compensation insurance and claims expenses could have a material adverse effect on our

business, financial condition and results of operations.

Workers' compensation liabilities are established for estimates of cash outlays that we are expected to

ultimately incur on reported claims, as well as estimates of the costs of claims that have been incurred but not

yet reported. Trends in actual experience and management judgments about the present and expected levels of

cost per claim are significant factors in the determination of such accruals. Several other factors which are

beyond our control, such as discount and inflation rates, could cause us to incur higher workers' compensation

expenses.

We believe our estimated liability for such claims is adequate, but if actual experience results in an increase in

the number of claims, and/or severity of claims for which we retain risk, this could cause a material difference

from our estimates and adversely affect our financial condition and results of operations. In addition, our

workers' compensation program is administered for us by the DOL, and as such, we do not have the same level

of control over the execution of the program, including the costs we incur for certain medical and pharmacy

costs, that a private-sector company has with its workers' compensation insurance provider.

2022 Report on Form 10-K United States Postal Service 13

Fuel expenses are a material part of our operating costs. A significant increase in fuel prices could

adversely affect costs and results of operations.

We are exposed to changes in commodity prices, primarily for diesel fuel, unleaded gasoline, and aircraft fuel

for transportation of mail, and natural gas and heating oil for facilities. For the year ended September 30, 2022,

our expenses for fuel represented 4.4% of operating expenses. The price and availability of fuel can be

unpredictable and is beyond our control. Additionally, as we use contracted carriers to transport the mail, we

anticipate that increased operating costs for these independent carriers, including increased costs resulting from

rising fuel prices, will ultimately be passed through to us, which would result in increased costs.

The potential liability associated with existing and future litigation against us could have a material

adverse effect on our business, results of operations, financial condition, and cash flows.

In the normal course of operations, we are subject to threatened and actual legal proceedings from time to time.

Any litigation, regardless of its merits, could result in substantial legal fees and costs incurred by us. Further,

actions that have been or will be brought against us may not be resolved in our favor and, if significant monetary

judgments are rendered, we may not have the ability to pay them. Such disruptions, legal fees, and any losses

resulting from these claims could have a material adverse effect on our business, results of operations, financial

condition, and cash flows.

We rely on the terms and conditions of our contracts with vendors and customers to deliver our

services. These contracts are renegotiated on a routine and periodic basis. Significant changes in the

costs, pricing or terms associated with these contracts could adversely affect our business.

Some of our suppliers and customers enter into long-term contracts with us to supply goods and services and to

procure our services. These contracts are renegotiated from time to time and, to the extent that contracts are

not renewed or are renewed with terms that may not sufficiently cover our costs or increase our costs, may

have an adverse effect on our business. Certain vendors and customers, including a large courier service for air

transportation, are significant to the delivery of certain services. Our ability to maintain current or improved

contract terms with customers and suppliers is critical to our initiatives to return to financial sustainability.

REGULATORY RISK FACTORS

We are subject to congressional oversight and regulation by the PRC and other government agencies.

We have a wide variety of stakeholders whose interests and needs are sometimes in conflict.

We operate as an independent establishment of the executive branch of the U.S. government and, as a result,

we are subject to a variety of regulations and other limitations applicable to federal agencies. If the U.S.

government curtails its spending due to debt ceiling or other constraints, we may be adversely impacted.

Additionally, as an outgrowth of our unique status as a fundamental service provider to the nation, we attempt to

balance the interests of many parties. Limitations on our ability to take action could adversely affect operating

and financial results.

Existing laws and regulations limit our ability to introduce new products or services, enter new markets,

generate new revenue streams, or manage our cost structure. These laws and regulations may also

prevent us from increasing prices sufficiently or generating sufficient efficiency improvements to offset

increased costs. This would adversely affect our results of operations.

In order to offset declining volume and revenue of mail caused by the changing economy, diversion to electronic

media, and statutorily imposed costs, our ability to sell new products and services in new or existing markets will

be a key factor in improving our financial condition. However, various laws and regulations significantly limit our

ability to enter new markets and/or to provide new services and products, as we are often constrained by

traditional industry definitions.

Without legal or regulatory changes that allow us to introduce new products or services to take advantage of our

assets, including our strong network and "last-mile" capabilities, we may be unable to respond adequately to

consumers' changing needs and expectations. These limitations have the potential to adversely impact our

results of operations and long-term financial viability.

The PAEA subjected our Market-Dominant services to a price cap rigidly tied to the CPI-U, but the PAEA also

required the PRC to review that price-cap system after 10 years and to modify or replace it as necessary to

2022 Report on Form 10-K United States Postal Service 14

allow the achievement of financial stability and other statutory objectives. The PRC concluded during this

mandatory review that the rigid price-cap system prevented us from generating adequate revenues to cover our

costs or produce retained earnings, and adjusted the price-cap formula on a going-forward basis to partly offset

further degradation of our revenue base. However, these adjustments do not allow prices to be reset to a

compensatory level and therefore do not correct for the effects of operating for 14 years under a defective

pricing system. For this reason, the additional pricing authority, while an improvement on the original price-cap

formula, may merely perpetuate annual net losses rather than relieve them, and is only expected to partially

offset the effect of declining mail volume, growing delivery points, and our other increasing costs which are not

best reflected by CPI-U.

A large portion of our cost structure cannot be altered expeditiously, and the number of our delivery points

continues to grow. Because our services are provided primarily through our employees, our costs are heavily

concentrated in wages and employee and retiree benefits. These costs are significantly impacted by wage

inflation, health benefit premium increases, retirement and workers' compensation programs.

We believe that continuing productivity improvements and effective use of our pricing authority will not be

sufficient to address the challenges presented by declining volume and revenue, by the current regulatory price

cap, and by statutorily imposed costs, nor will our efforts to grow operating revenue keep pace with our

increased cost. Further administrative action will be necessary to restore the Postal Service to financial

sustainability.

GENERAL RISK FACTORS

Changes in general economic conditions in the U.S. may adversely affect us.

With our mandate to provide universal postal services to the nation at fair and reasonable prices, we serve

consumer and commercial customers in the U.S., as well as internationally. Our operations are subject to

cyclicality affecting the national economy in general, as well as the local economic environments in which we

operate, which makes us particularly vulnerable to macroeconomic risks. The factors that result in general

macroeconomic changes are beyond our control, and it may be difficult for us to adjust our business model to

mitigate the impact of these factors.

Changes in the basic tenets of macroeconomics – output, unemployment, and inflation – could result in

increased costs due to supply chain disruptions, wage increases, and higher fuel and energy prices. These

changes could also impact the demand for consumer goods and cause a contraction in the retail market,

lowering our volumes, particularly in the Shipping and Packages and Marketing Mail categories.

Consistent with our Delivering for America plan, we have realigned aspects of our organization, including

changes to our workforce and transportation strategy, to best serve the American public and create a high

performing, financially sustainable Postal Service. However, further management initiatives and administrative

changes are still necessary. Changes to macroeconomic conditions could impact our ability to fully implement

our plan in a timely manner and affect our ability to meet the financial targets of revenue growth, cost savings,

and investment associated with the plan.

Rising inflation contributed to an increase in operating expenses during 2022, including higher compensation

expenses, higher retirement benefit expenses, higher transportation expenses, and higher fuel and utility costs.

We expect continued uncertainty in the economy during 2023 and expect the challenges and conditions present

in 2022 to also be present in 2023. Changes in general economic conditions, including further impacts of the

ongoing pandemic, could have an adverse impact on our results of operations and financial position.

Catastrophic events or geopolitical conditions may disrupt our business.

Natural disasters, such as hurricanes, earthquakes, tornadoes, floods, wildfires, and severe winter storms place

our employees in harm's way and make it challenging to deliver mail under these unpredictable and dangerous

conditions. Additionally, shifts in weather patterns caused by climate change could increase the frequency and

intensity of such weather-related natural disaster events. These events may also result in damage to our

facilities, which could have a negative impact on business operations. Furthermore, these events could result in

2022 Report on Form 10-K United States Postal Service 15

adverse economic impacts, including supply chain risks and fuel disruptions. Such disruptions could create

significant additional operating costs in order to maintain continuity in fulfilling our mission.

Geopolitical conflicts and changes, such as the ongoing conflict in Ukraine, pose a risk of general economic

disruption. Such disruptions may cause supply chain disruptions and increase the cost of fuel, utilities, and

transportation, which could have an adverse impact on our business operations and financial results.

The occurrence of regional epidemics or a global pandemic, such as the COVID-19 pandemic, may adversely

affect our operations, financial condition, and results of operations. The COVID-19 pandemic has had severe

and unpredictable impacts on the U.S. and global economy, supply chains, labor markets, and consumer and

commercial behavior. We will continue to be at risk of the adverse impact of another regional epidemic, global

pandemic, or other adverse public health developments in the future.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

We own nearly 8,500 and lease over 23,000 properties (buildings and facilities) ranging in size from 273 square

feet to 32 acres. Our facilities support retail, delivery, mail processing, maintenance, administrative, and support

activities and are located in numerous communities throughout the U.S. and its territories.

ITEM 3. LEGAL PROCEEDINGS

We are subject to legal proceedings and claims that arise in the ordinary course of our business. For further

discussion of the legal proceedings affecting us, see Part II., Item 8. Financial Statements and Supplementary

Data, Notes to Financial Statements, Note 10 - Commitments and Contingencies.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND

ISSUER PURCHASES OF EQUITY SECURITIES

Not applicable. As an "independent establishment of the executive branch of the Government of the United

States" (39 U.S.C. §201), we do not issue equity or other securities.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

Our operating results are presented in accordance with GAAP. As used herein, all references to years in this

report, unless otherwise stated, refer to fiscal years beginning October 1 and ending September 30. All

references to quarters, unless otherwise stated, refer to fiscal quarters.

The following Management's Discussion and Analysis of Financial Condition and Results of Operations should

be read in conjunction with the other sections of this Annual Report, particularly Part I., Item 1. Business, Part I,

Item 1A. Risk Factors, and Part II, Item 8. Financial Statements and Supplementary Data.

2022 Report on Form 10-K United States Postal Service 16

OVERVIEW

With our mandate to provide universal postal services to the nation, we serve consumer and commercial

customers in the U.S., as well as internationally. Our operations include an extensive and integrated retail,

processing, distribution, transportation, and delivery network, and we operate throughout the U.S., including its

possessions and territories. We operate as a single segment and report our performance as a single business.

We continue to implement initiatives that are expected to drive revenue by capitalizing on innovation,

technology, customer and consumer insights, and data management. This includes strengthening the value of

mail through the continued enhancement of Informed Delivery, which enables customers to digitally preview

mail and manage package delivery and adds digital marketing capabilities to the printed mailpiece. We also

recently launched USPS Connect that aims to drive package growth by broadening network access to our next-

day delivery capability for businesses of all sizes. However, legal restrictions on pricing, service diversification,

and operations currently restrict our ability to cover our costs to provide prompt, reliable, and efficient postal

services to the nation.

As an independent establishment of the U.S. government, we have a unique mission to:

• Serve the American people and, through the universal service mission, bind our nation together by

maintaining and operating our unique, vital, and resilient infrastructure;

• Provide trusted, safe, and secure communications and services between the U.S. government and the

American people, businesses, and their customers, and the American people with each other; and

• Serve all areas of our nation, making full use of evolving technologies.

We will carry out this mission by remaining an integral part of the U.S. government and providing all Americans

with universal and open access to our unrivaled delivery and retail network; using technology, innovation and,

where appropriate, private-sector partnerships to meet our customers’ changing needs; operating in a modern,

precise, efficient, and effective manner; and remaining an employer of choice, including attracting and retaining

high-quality employees.

RESULTS OF OPERATIONS

SUMMARY

The enactment of the PSRA significantly impacted the results of operations for the year ended September 30,

2022, as it repealed the requirement that we annually prepay future retiree health benefits and canceled all past

due prefunding obligations. These impacts are reflected as a one-time, non-cash benefit of $57.0 billion to net

income for the year ended September 30, 2022.

Rising inflation also had a significant impact on our results of operations. Our Market-Dominant services are

subject to a price cap system that is generally limited by the increase in the CPI-U, with some additional pricing

flexibility and authority granted by the PRC. Our overall revenue grew for the year ended September 30, 2022,

compared to the prior year, largely due to price increases, which are reflective of the inflationary environment.

Despite this increase in revenue, our operating results remain challenged due to rising costs associated with

inflationary pressures. We have experienced higher compensation costs, higher retirement benefit costs, higher

transportation costs, and higher fuel and utility costs as a result of rising inflation.

Pandemic-related pressures on our operations also continue to have a material impact. The operating results

for the year ended September 30, 2022 reflect the sustained effect that the pandemic has had on customer

demand, resulting in lower mail volumes and higher Shipping and Packages volumes than pre-pandemic levels,

as well as pandemic-related inflation contributing to certain higher operating expenses. The operating results for

the year ended September 30, 2022 also reflect increases in certain revenues and expenses associated with

our inter-agency agreement with HHS to distribute COVID-19 tests as described in Part II., Item 8. Financial

Statements and Supplementary Data, Notes to Financial Statements, Note 5 - Related Parties.

Other major factors that impacted our operating results include overall customer demand, the mix of postal

services and the pricing and contribution associated with those services, the volume of mail and packages

2022 Report on Form 10-K United States Postal Service 17

processed through our network, our ability to manage our cost structure in line with the secular declines in the

levels of mail volume, increased competition in the more labor-intensive Shipping and Packages business, and

an increasing number of delivery points.

2022 Compared with 2021

As more fully described below in Operating Revenue and Volume, our operating revenue was $78.5 billion for

the year ended September 30, 2022, an increase of $1.5 billion, or 1.9%, from the prior year, driven by the

impact of price increases and the following changes by service category:

• Marketing Mail revenue increase of $1.4 billion, or 9.7%, compared to the prior year, with a volume

growth of 894 million pieces, or 1.4%, compared to the prior year. Marketing Mail experienced steep

volume declines at the onset of the pandemic, but has been rebounding as the economy continues to

recover. Marketing Mail has generally proven to be a resilient marketing channel, and its value to U.S.

businesses remains strong due to healthy customer returns on investment and better data and

technology integration.

• First-Class Mail revenue increase of $772 million, or 3.3%, compared to the prior year, despite a volume

decline of 1.7 billion pieces, or 3.4%, compared to the prior year, due to on-going migration from mail to

electronic communication and transaction alternatives. First-Class Mail volume remains lower than pre-

pandemic levels and we expect continued secular declines; and

• Other services revenue increase of $485 million, or 12.1%, compared to the prior year, due to non-

postage revenue associated with the COVID-19 test distribution initiative and higher revenue

associated with PO Box services.

These increases in operating revenue were partially offset by the following:

• Shipping and Packages revenue decline of $700 million, or 2.2%, compared to the prior year, on a

volume decline of 399 million pieces, or 5.3%, compared to the prior year. Higher package volumes in

the prior year were due to the pandemic-related surge in e-commerce, which continues to abate as the

economy recovers and market competition intensifies, although such volumes are still higher than pre-

pandemic levels; and

• International Mail revenue decline of $489 million, or 22.2%, compared to the prior year, with a volume

decline of 63 million pieces, or 15.1%, compared to the prior year, as postal administrations have

continued to experience disruptions worldwide, including prolonged delays and temporary suspensions,

as a result of the pandemic and other global economic factors. International Mail has also been

impacted by shifts in global transportation modes to commercial alternatives.

As more fully described below in Operating Expenses, our operating expenses for the year ended

September 30, 2022 decreased $2.3 billion, or 2.8%, compared to the prior year. Operating expenses

decreased due to the following:

• Retiree health benefits expense decrease of $5.1 billion, compared to the prior year. Our Operating

Expenses for the year ended September 30, 2021 included $5.1 billion in retiree health benefits

expense required under the PAEA. As a result of the PSRA, there are no retiree health benefits

expenses for the year ended September 30, 2022; and

• Workers' compensation expense decrease of $1.5 billion, or 265.3%, compared to the prior year, driven

by the impact of actuarial revaluation and changes in discount rates, which are outside of

management’s control.

These decreases were partially offset by the following:

• Compensation and benefits expense increase of $1.4 billion, or 2.9%, from the prior year, primarily due

to contractual wage increases, including the inflationary impacts on related COLA and additional costs

associated with the COVID-19 test distribution, partially offset by a lower number of work hours;

• Retirement benefits expense increase of $986 million, or 13.4%, from the prior year, primarily due to the

inflationary impact on amortization calculations, as determined by OPM, as well as contribution rate

increases for FERS normal costs that are established by OPM;

2022 Report on Form 10-K United States Postal Service 18

• Transportation expense increase of $629 million, or 6.5%, from the prior year, driven by higher average

unit costs per mile, higher average diesel fuel prices, and higher average jet fuel prices; and

• Other operating expenses increase of $1.3 billion, or 13.0%, compared to the same period last year,

driven by higher average fuel prices for delivery vehicles, an increase in supplies and services, and an

increase in rent and utilities for our facilities.

Overall, we reported net income of $56.0 billion for the year ended September 30, 2022, compared to a net loss

of $4.9 billion for the year ended September 30, 2021, primarily due to the one-time, non-cash impact of the

PSRA.

2021 Compared with 2020

For a comparison of our results of operations for the year ended September 30, 2021 to the year ended

September 30, 2020, see Part II., Item 7. Management's Discussion and Analysis of Financial Condition and

Results of Operations of our Form 10-K for the fiscal year ended September 30, 2021, filed with the PRC on

November 10, 2021.

Non-GAAP Measures

In the day-to-day operation of our business, we focus on costs that can be managed in the normal business

operations, such as salaries and transportation. We use various non-GAAP measures to help us better manage

our business. However, these non-GAAP measures should not be considered as a substitute for net income

(loss) and other GAAP reporting measures.

Controllable loss, a non-GAAP measure, is calculated as net income (loss) adjusted for the impact of the PSRA,

workers’ compensation non-cash benefit caused by actuarial revaluation and discount rate changes, expenses

caused by the actuarial revaluation of PSRHBF, and the amortization of the PSRHBF, CSRS, and FERS

unfunded liabilities.

Controllable (loss) income excluding all retiree health benefits expense, a non-GAAP measure, is calculated as

net income (loss) adjusted for the impact of the PSRA, retiree health benefits expense, workers’ compensation

non-cash benefit caused by actuarial revaluation and discount rate changes, and the amortization of the CSRS

and FERS unfunded liabilities.

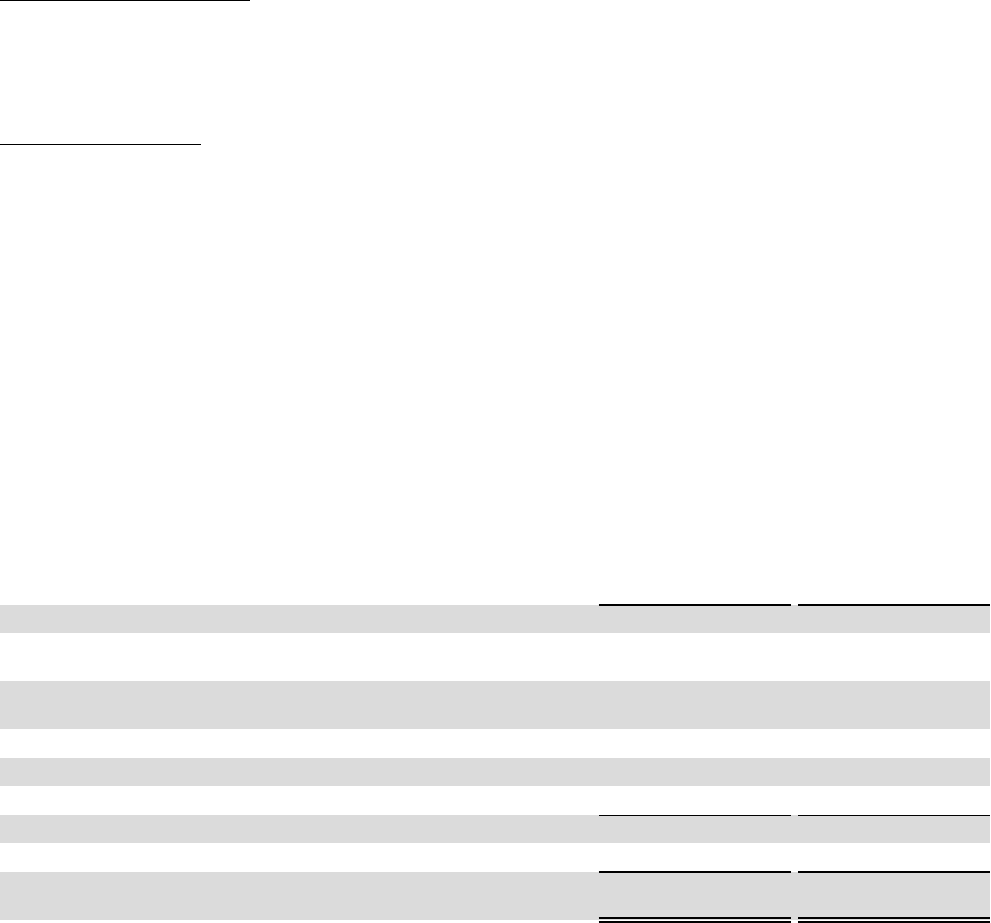

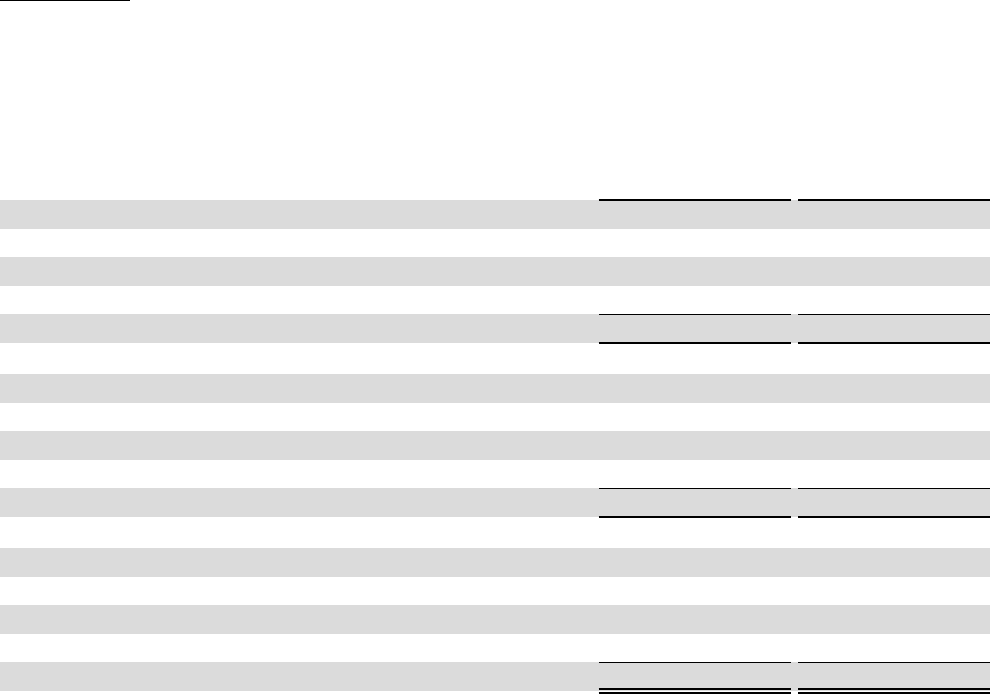

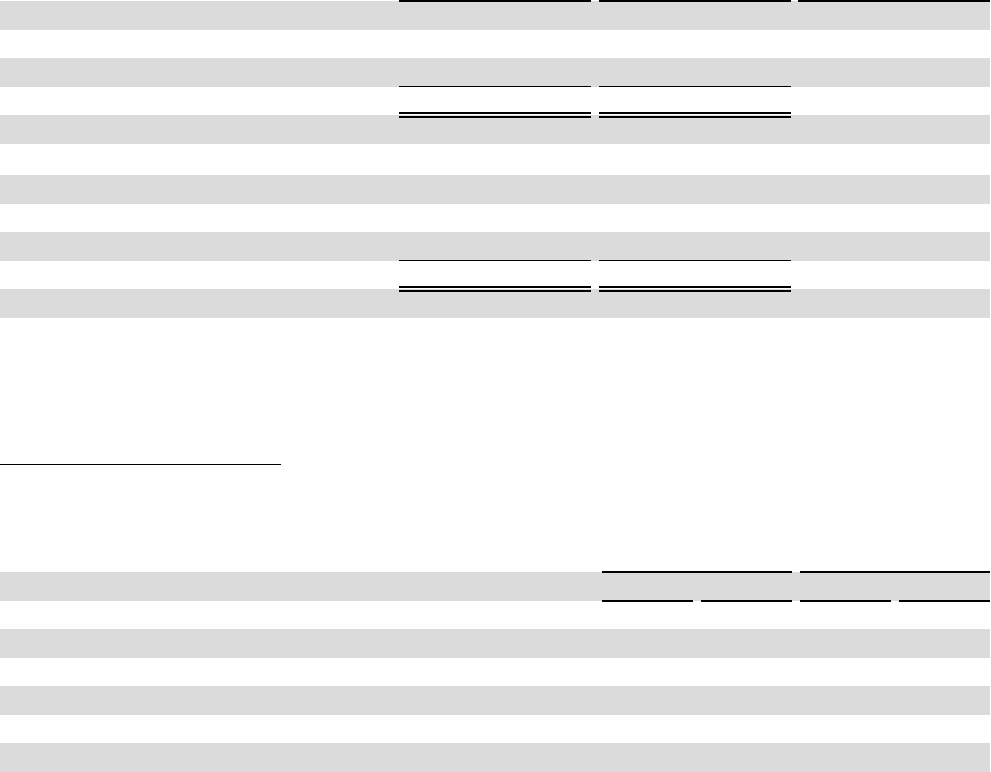

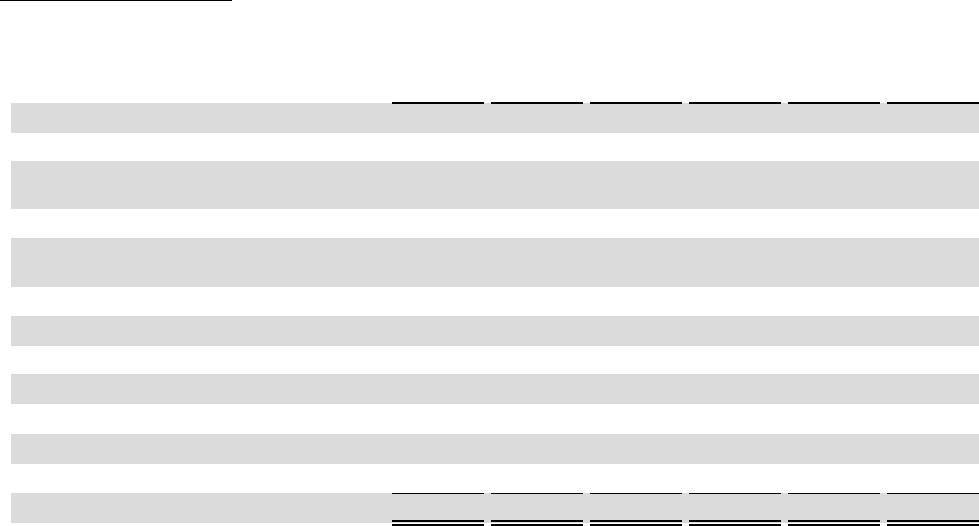

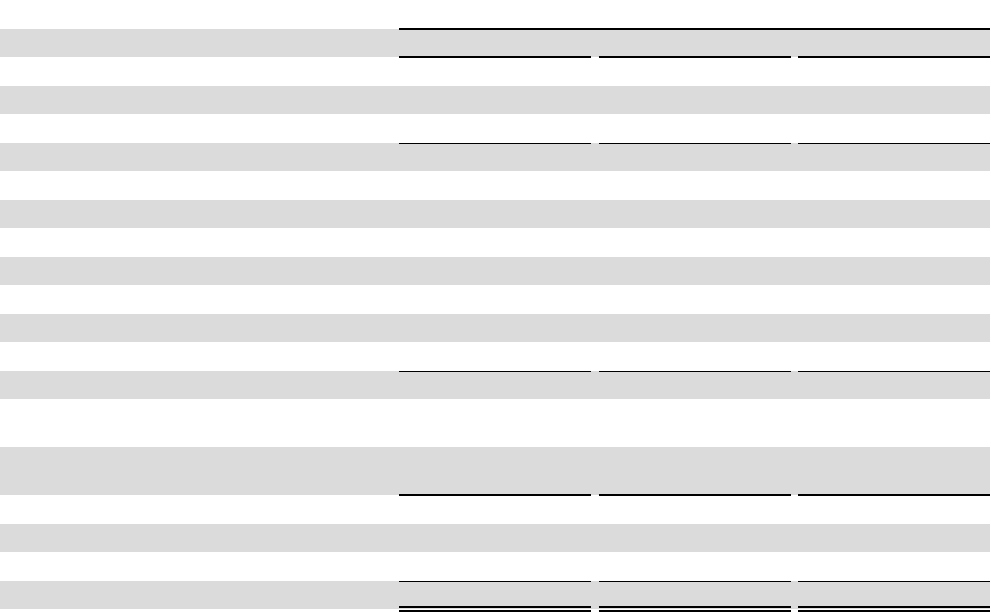

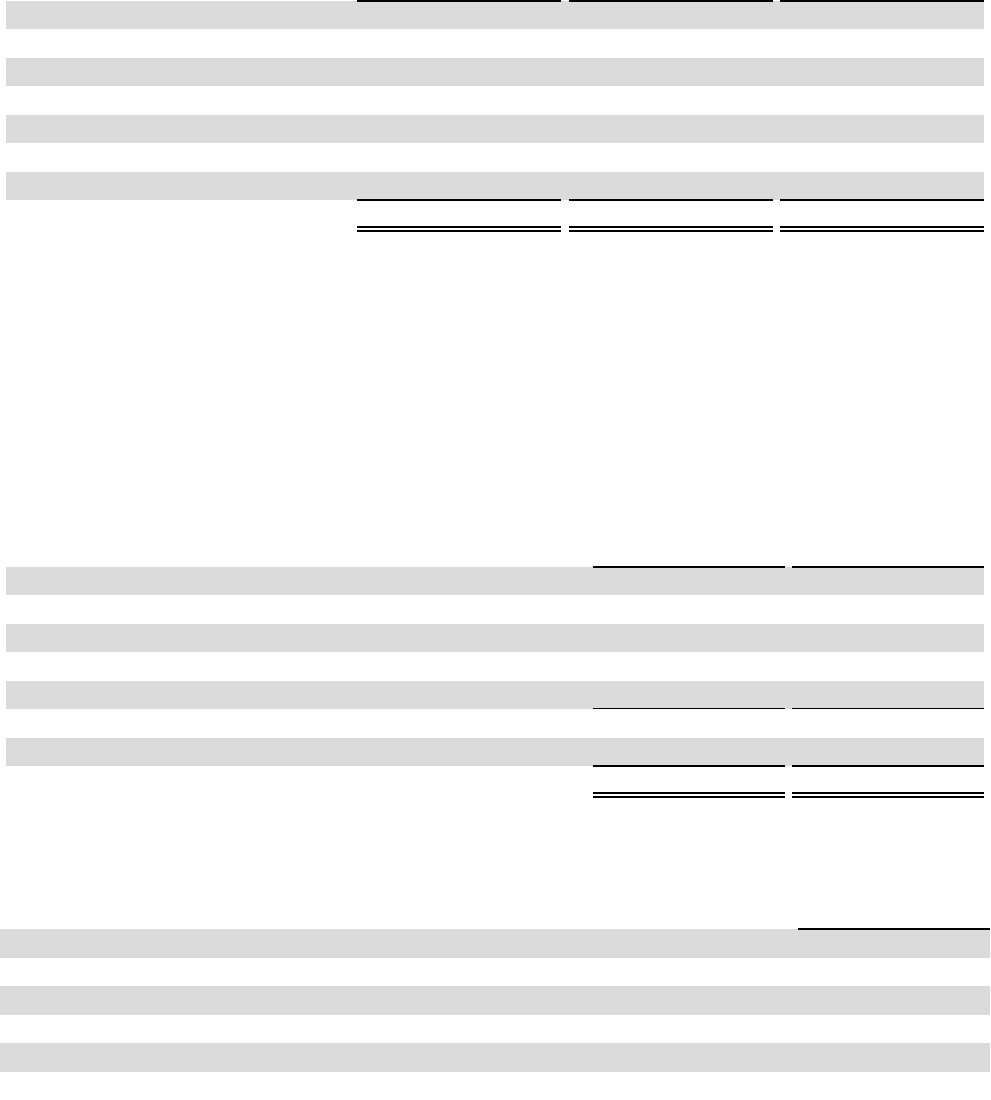

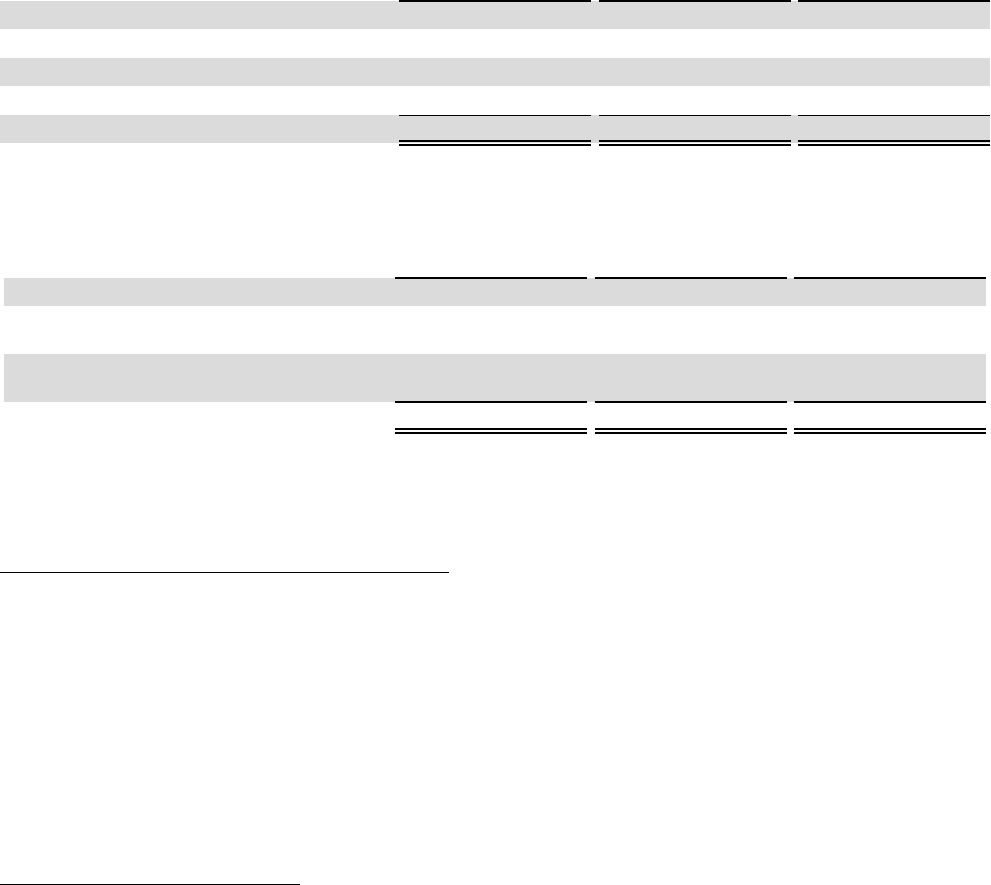

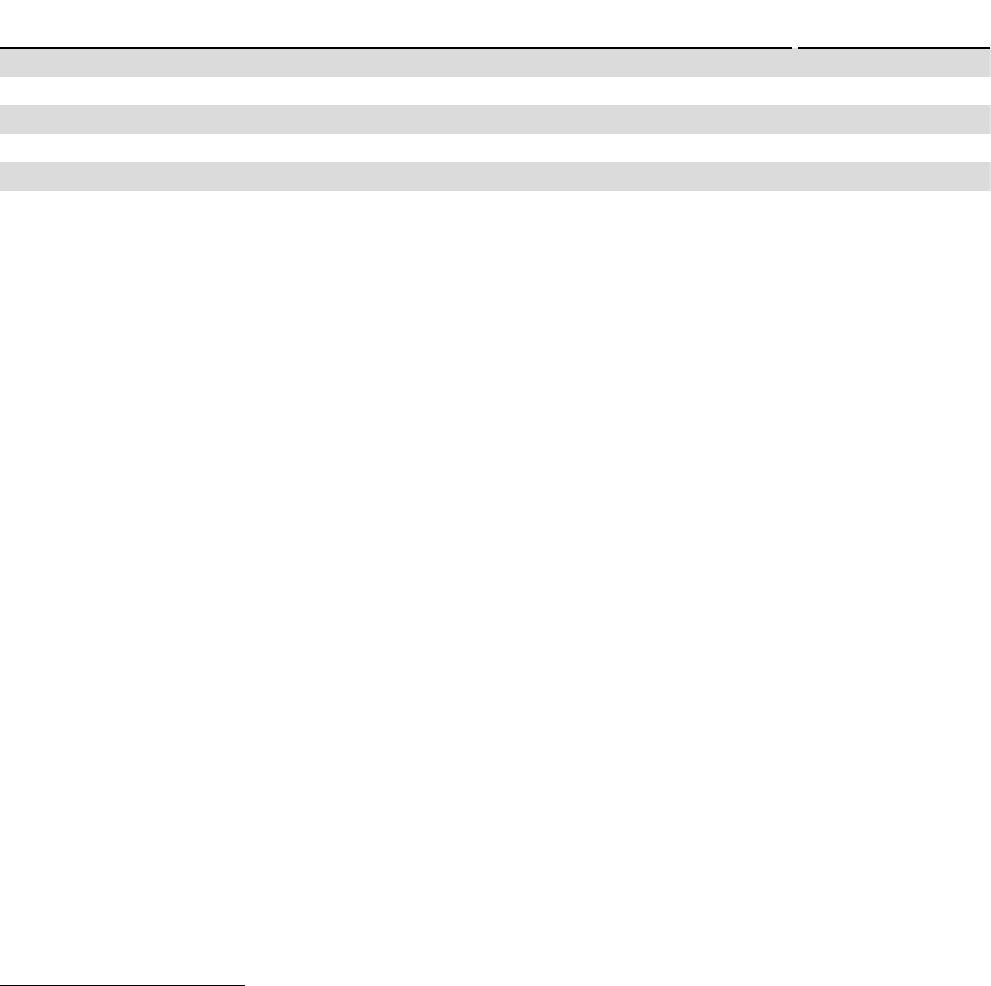

The following table reconciles our GAAP net income (loss) to our non-GAAP financial measures for the years

ended September 30, 2022 and 2021:

(in millions)

2022 2021

Net income (loss)

Impact of Postal Service reform legislation on past-due PSRHBF

obligations

1

PSRHBF amortization and changes in normal costs of

retiree health benefits due to revised actuarial assumptions

2

Workers' compensation non-cash benefit

3

4

CSRS unfunded liability amortization expense

5

FERS unfunded liability amortization expense

Controllable loss

Normal cost of retiree health benefits

6

$

$

56,046

(56,975)

—

(3,454)

2,284

1,626

(473)

—

$

$

(4,930)

—

1,210

(1,925)

1,858

1,401

(2,386)

3,900

Controllable (loss) income excluding all retiree health

benefits expense

$ (473) ( $ 1,514

2022 Report on Form 10-K United States Postal Service 19

Total operating revenue $ 78,507 $ 77,009

1