1

For the discussion of market activity in this chapter, commercial real estate refers to office, retail, and industrial

properties.

Chapter 3

Commercial Real Estate

Commercial Real Estate

and the Banking Crises

and the Banking Crises

of the 1980s

of the 1980s

and Early 1990s

and Early 1990s

Introduction

In the era of federal deposit insurance, the 1980s and early 1990s were unique periods

for the commercial banking industry: both the number of banks that failed and the volume

of losses they suffered were unprecedented. Behind bankings problems lay large-scale

changes in the economic and regulatory environment. In addition, banks greatly increased

their exposure to commercial real estate markets during this era, only to have those markets

develop substantial problems.

1

The demand for commercial real estate projects boomed during the early 1980s and

reached a speculative pitch in many markets. Real estate financing by commercial banks

and other institutions grew to meet the demand, because deregulation and other factors had

created an environment in which commercial real estate lending was lucrative for lenders,

especially with its large up-front fees. As a consequence, after 1980 commercial banks dra-

matically increased the volume of such credits.

But historically the commercial real estate industry had been cyclical, and that, com-

bined with the banks aggressive lending, made it likely that lenders would eventually suf-

fer financial losses when markets turned. When the bust did arrive in the late 1980s and

continued into the early 1990s, the banking industry recorded heavy losses, many banks

failed, and the bank insurance fund suffered accordingly. Compounding the magnitude of

these losses was the fact that many banking organizations active in real estate lending had

weakened their underwriting standards on commercial loan contracts during the 1980s.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

138 History of the EightiesLessons for the Future

2

However, while not involved in direct equity investing, banks own and manage substantial amounts of commercial real es-

tate acquired through loan foreclosures.

This chapter presents an account of the boom and bust in commercial real estate mar-

kets in the 1980s and highlights the role commercial banks played in this process. The first

two sections discuss the risks associated with commercial real estate investments and the

ways in which tax-law changes during the 1980s influenced the climate for commercial real

estate investing. (The appendix to the chapter illustrates how specific tax-law changes af-

fected the viability of commercial real estate investments.) The third section surveys trends

in supply, demand, and asset prices during the boom and bust. The following section high-

lights the involvement of commercial banks in the commercial lending boom, and is fol-

lowed by a section on the changing underwriting standards and another on the changing

appraisal policies of lenders during this period (an account of the reforms subsequently en-

acted is also included). The final section discusses the relationship between bank failures

and losses on commercial real estate.

Risks Inherent in Commercial Real Estate Markets

Investments in commercial real estate (for example, office buildings, retail centers,

and industrial facilities)at any stage of the development processhave traditionally been

quite risky. Real estate markets as a whole are traditionally cyclical, so that even the most

well-conceived and soundly underwritten commercial real estate project can become trou-

bled during the periodic overbuilding cycles that characterize these markets. For this rea-

son, historically federal bank regulators have supervised the terms of loans made to

commercial real estate ventures and have prohibited federally chartered banks from invest-

ing directly in such ventures.

2

The riskiness of investments in commercial real estate has a number of aspects. First,

the demand for commercial real estate is affected not only by local economic factors and re-

gional developments but also by national economic trends. This is because firms seeking

commercial floor space typically can choose between a number of locations in different

parts of the country. Thus, the developer of an industrial park in New Jersey, for example,

would have to be concerned not only about how both existing and future developments in

that state might affect demand for the project but also about how market conditions in com-

peting locationsfor example, Florida or Texasmight affect the northeastern developers

ability to attract and keep tenants.

Another factor complicating investments in commercial real estate is that information

about specific projects and markets is often difficult to obtain. These are not highly orga-

nized markets, so data on market developments cannot be easily gathered. Moreover, many

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 139

transactions are private, and the major terms of the investments may not be available to the

public. (Construction costs, for example, are a private matter between the developer and the

contractor.) In addition, widespread statistical data are not available on transaction prices as

they are for single-family structures, so gauging selling prices or rental income is diffi-

cultand even if the statistical data were available, it would be difficult to account for the

many complex financing techniques (such as tenant improvements and rent discounting)

involved in commercial sales and rents.

Other risks are also associated with the financing aspects of most commercial real es-

tate investments, which adds to the volatility of the markets and the prices of commercial

properties. Most real estate projects are highly leveragedthat is, they are funded primar-

ily by debt as opposed to equity capital by the investor. The effect that leverage has on both

the borrowers and lenders risk helps add to the volatility of the commercial real estate

markets. Generally, leveraged investments will be highly sensitive to changes in interest

rates and overall credit conditions. For this reason, the prices of commercial real estate can

decline precipitously during periods of rising interest rates, and vice versa.

Risk in commercial real estate also derives from government tax and other policies.

Since World War II, depreciation allowances and tax rates have changed periodically, and

these changes have affected the demand for and the profitability of real estate investments.

During the 1980s, changes in the federal tax code were important factors influencing both

the boom and to some extent the bust conditions in commercial markets (tax issues are dis-

cussed in the next section). In addition, federal mandates requiring cleanup of existing en-

vironmental hazards may impose unforeseen costs on investors. Changes in state and local

laws governing environmental restrictions on new construction may add unexpected costs

to a project, or may even bar its intended use. Similarly, an unanticipated zoning change can

have a positive or negative effect on the prospects of an investment.

Also contributing to the challenges of these investments is the nature of the produc-

tion process itself when construction lending is involved. Real estate construction projects,

and especially large commercial development projects, typically have long gestation peri-

ods, and these are superimposed on the traditional cyclicality of the economy and of real es-

tate markets. Thus, the economic prospects for a real estate construction project can change

considerably between inception and completion.

Other risks associated with commercial real estate investing are related to macroeco-

nomic changes in the economy. The value of commercial property is highly sensitive to

changes in the availability of credit. When financial institutions cut back or restrict funding

for these types of investments over the business cycle, prices of existing properties can fluc-

tuate widely and the volume of new investments can be severely affected. In part, this pro-

duces the well-known feast-or-famine cycle in commercial real estate markets. An extreme

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

140 History of the EightiesLessons for the Future

3

The dramatic reduction in bank lending in the early 1990s for the purchase and development of commercial real estate was

brought on by many factors, including the 199091 national recession, the closing of insolvent thrift institutions, the im-

plementation of new risk-based capital standards for commercial banks, and the generally closer supervision of financial in-

stitutions after passage of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989. These issues are

discussed below.

4

Investments in residential real estate are also affected by federal tax laws, but this chapter focuses primarily on investments

in commercial real estate properties.

example of this scenario is the credit crunch in the early 1990s, which diminished access

to credit and restricted demand for commercial real estate investments across the nation,

thereby eliminating some potential investors from the market. Consequently, during this pe-

riod the demand for and prices of commercial real estate declined significantly.

3

Finally, the structure of most commercial loans involves unique risks for the lender.

Commercial loans are complex legal documents that usually have nonrecourse provisions

prohibiting lenders from satisfying losses from other borrower assets. Nonrecourse provi-

sions provide borrowers with extra bargaining power to force lenders to accept modifica-

tions in the event of problems. Moreover, commercial borrowers are usually sophisticated

and possess the resources to contest lender actions. Furthermore, in the event of foreclosure,

banks often have little specialized in-house expertise for dealing with the unique problems

of commercial REO (foreclosed real estate) sale and management. All of these factors can

make investing in commercial real estate projects a risky business for all parties involved in

the transaction.

The Effect of Major Tax Legislation

Two major pieces of tax legislationthe Economic Recovery Tax Act of 1981

(ERTA) and the Tax Reform Act of 1986had unusually strong effects on commercial real

estate markets during the 1980s.

4

ERTA included several provisions that improved the rate

of return on commercial real estate and increased demand for these investments. Five years

later, the Tax Reform Act repealed many of these same benefits. (A numerical example of

the effect that both sets of tax-law changes had on commercial real estate investment returns

is presented in the appendix to this chapter.) Among ERTAs most important provisions

were a lowering of ordinary income tax rates (the rate for the highest earners, for example,

fell from 70 percent to 50 percent) and a lowering of the capital gains tax rate from 28 per-

cent to 20 percent. However, what distinguished this tax act from earlier ones was the

change in depreciation rules for commercial real estate. Specifically, an Accelerated Cost

Recovery System (ACRS) was introduced. ACRS allowed investors in commercial prop-

erty to depreciate a building over 15 yearsa period considerably shorter than its economic

life. Under earlier tax legislation, 40 years was the standard. Moreover, this new cost re-

covery system also permitted the use of a 175 percent declining-balance method rather than

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 141

5

According to data from the National Council of Real Estate Investment Fiduciaries and the Frank Russell Company (these

two groups together produced the Russell-NCREIF report), returns on the office properties owned by institutional investors

in the late 1970s and early 1980s averaged 21.9 percent; returns on warehouse/industrial and retail properties were 16.5 per-

cent and 11.7 percent, respectively. In 1995 the Russell-NCREIF Report ceased publication.

6

CB Commercial Torto/Wheaton Research.

simple, straight-line depreciation, and thereby increased, or accelerated, the tax deductions

available in the early years of a propertys holding period. These new provisions had the ef-

fect of increasing the after-tax return on commercial real estate investments relative to other

classes of assets. This was accomplished by deferring taxes and later, upon sale of the prop-

erty, recapturing much of the earlier depreciation at a lower tax rate than the rate that had

applied to the previous depreciation deductions. These provisions were a major reason for

the accelerated production cycle of commercial real estate during the first half of the 1980s.

The Tax Reform Act of 1986 further lowered all marginal tax rates, including the rate

for the highest earners (from 50 percent to 38.5 percent), but it countered that change by

eliminating not only the ACRS but also the ability of taxpayers to offset other income with

tax losses from passive investments in commercial real estate. Deductions and losses

from one business or rental activity had generally been allowed to offset income from other

business activities and investments. After 1986, losses from passive activities (generally de-

fined as those activities in which the taxpayer does not materially participate, and any rental

activity) were allowed to offset only income from other passive activities, and credits from

passive activities were applicable only to the tax attributable to income from such activities.

The consequences of these provisions was to dampen the demand for commercial real es-

tate investments during the late 1980s and early 1990s, and the dampening of demand

helped soften real estate prices.

The importance of these tax considerations is reflected in the rise and fall of real es-

tate limited partnerships during the 1980s. According to data from the Roulac Group (a real

estate consulting unit of Deloitte & Touche), the market for this investment vehicle had

grown fivefold between 1981 and 1985. After reaching a high point of attracting $16 billion

in new capital in 1985, real estate limited partnership sales fell precipitously over the next

four years, gathering only $1.5 billion in new capital in 1989.

Boom and Bust: Trends in Commercial Real Estate Supply,

Demand, and Asset Prices

As the nations commercial real estate markets entered the 1980s, supply and demand

for commercial real estate were in relative balance and investment returns were attractive.

5

Heavy demand in the late 1970s had absorbed much of the excess space remaining from the

burst in construction activity of the early 1970s and had trimmed vacancy rates in most mar-

kets to below 10 percent.

6

In the late 1970s sharp, unanticipated inflation set off a wave of

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

142 History of the EightiesLessons for the Future

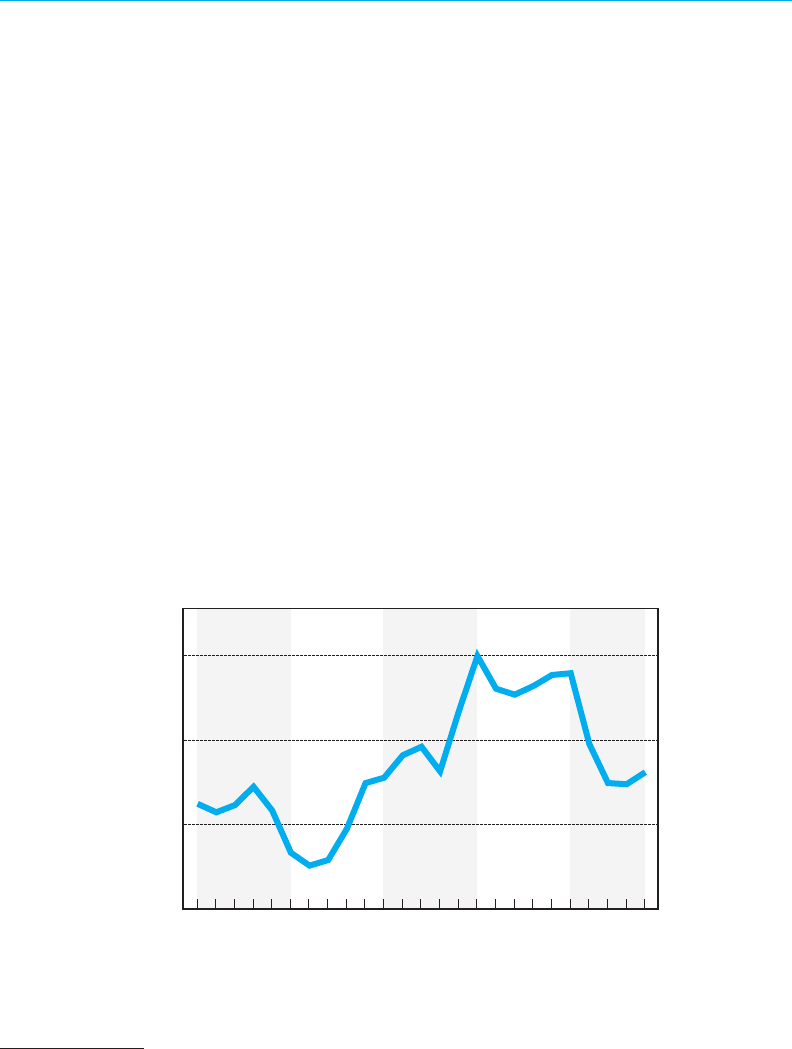

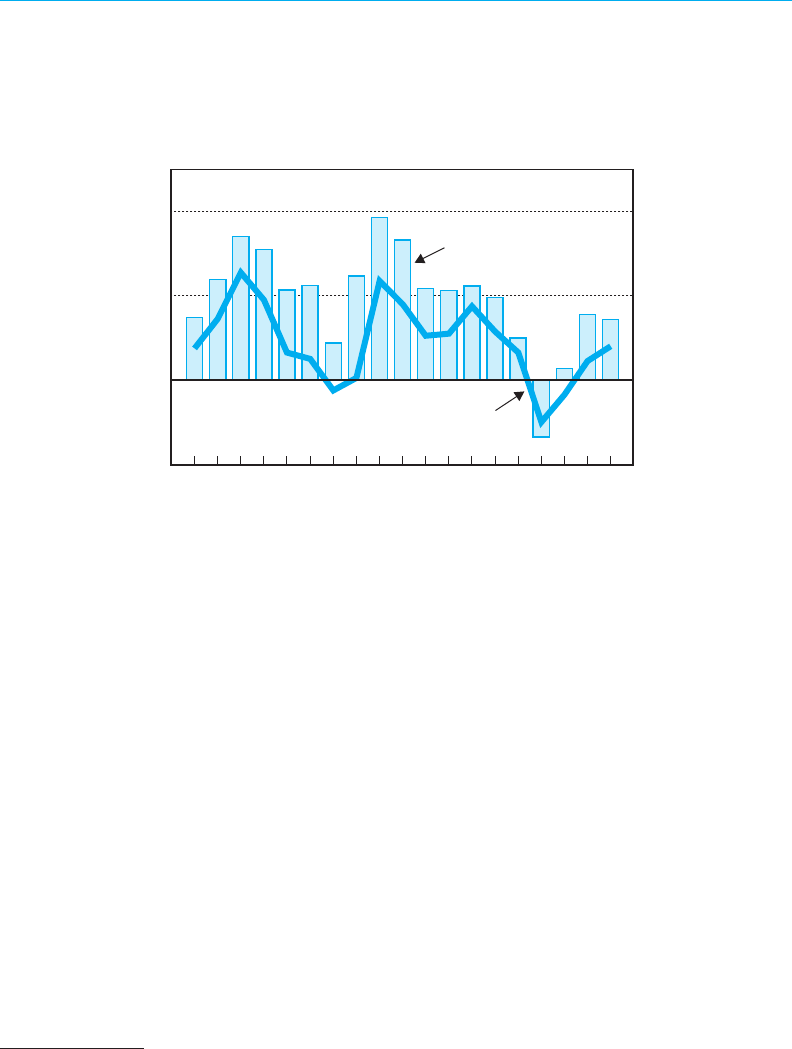

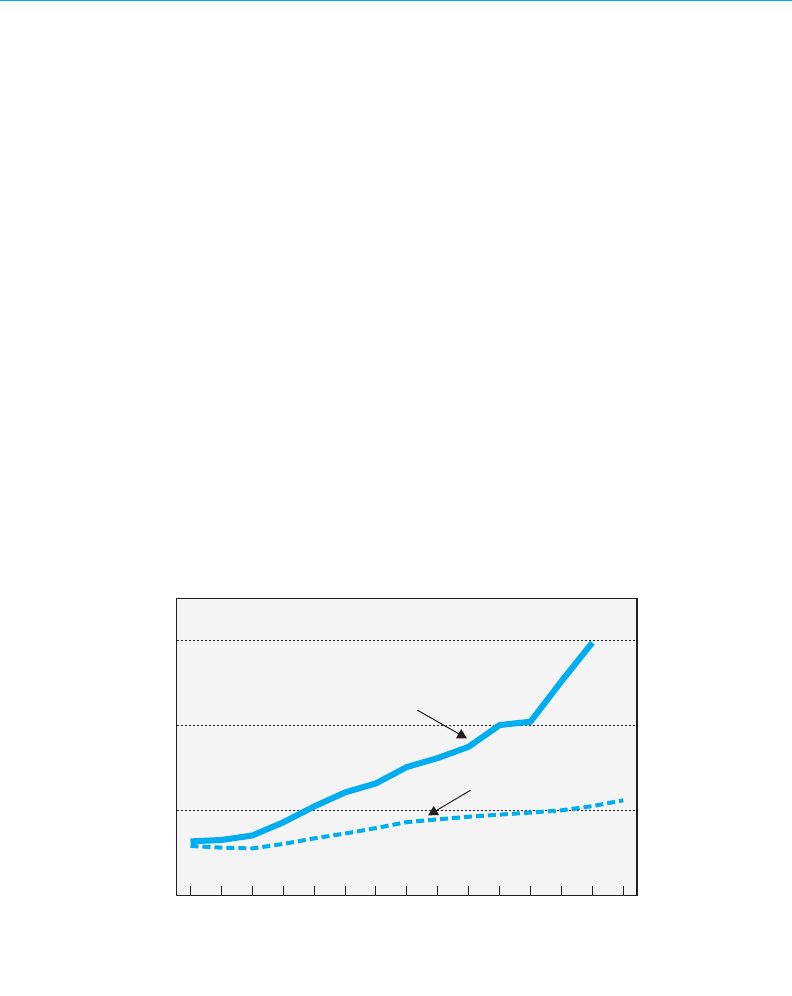

1970 1975 1980 1985 1990 1994

50

75

100

125

$Billions

Source: Current

Construction Reports

U.S. Department of Commerce, Bureau of the Census,

, series C30, monthly.

Note: .“Put in place” refers to the dollar value of new construction completed

Total Nonresidential Construction Put in Place,

1970–1994

(1992Dollars)

Figure 3.1

7

Put in place refers to the dollar value of new construction completed.

speculative demand for real estateand commercial real estate markets experienced an un-

precedented building boom (particularly in the office sector) that lasted in one region of the

country or another throughout the 1980s. From 1980 to 1990, the annual average value of

new nonresidential construction put in place was $108 billion (in 1992 dollars)up from

approximately $71 billion during the period 197579 (see figure 3.1).

7

The boom collapsed

starting in the late 1980s, however, and the decade of the 1980s closed with many markets

across the nation severely depressed, affected by historically high vacancy rates and falling

prices and rents. Construction activity on commercial properties declined to about the lev-

els of the early 1980s.

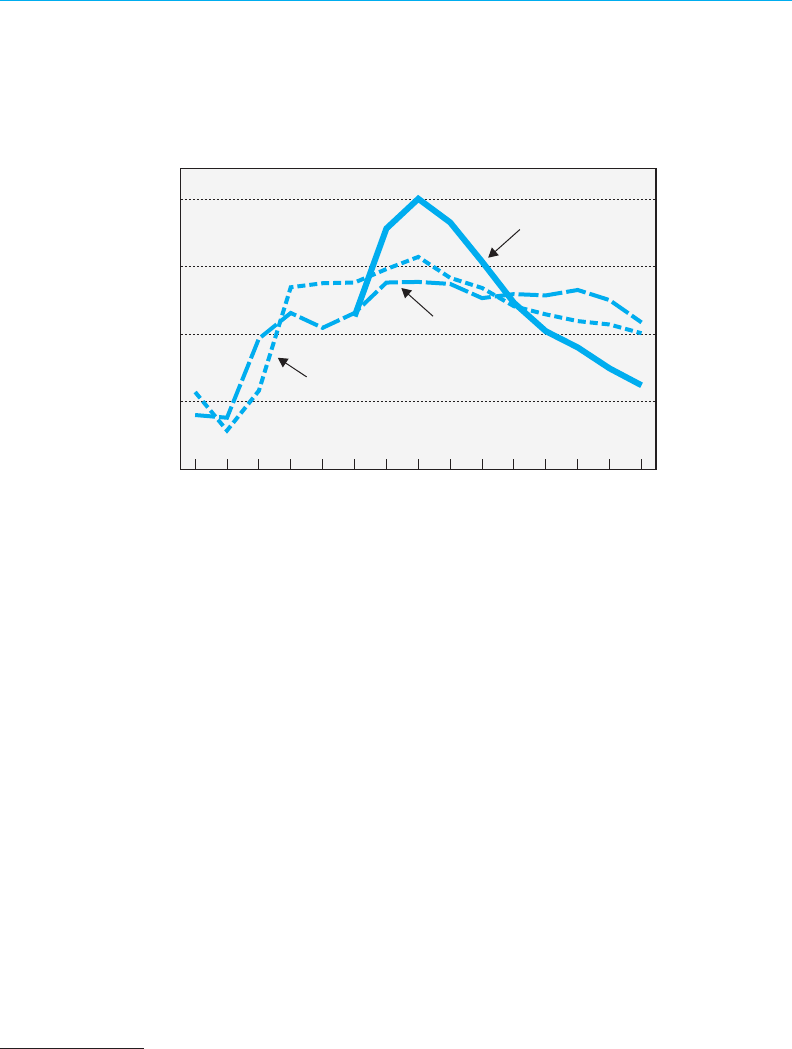

The regions where the boom-and-bust scenario played out included the Southwest,

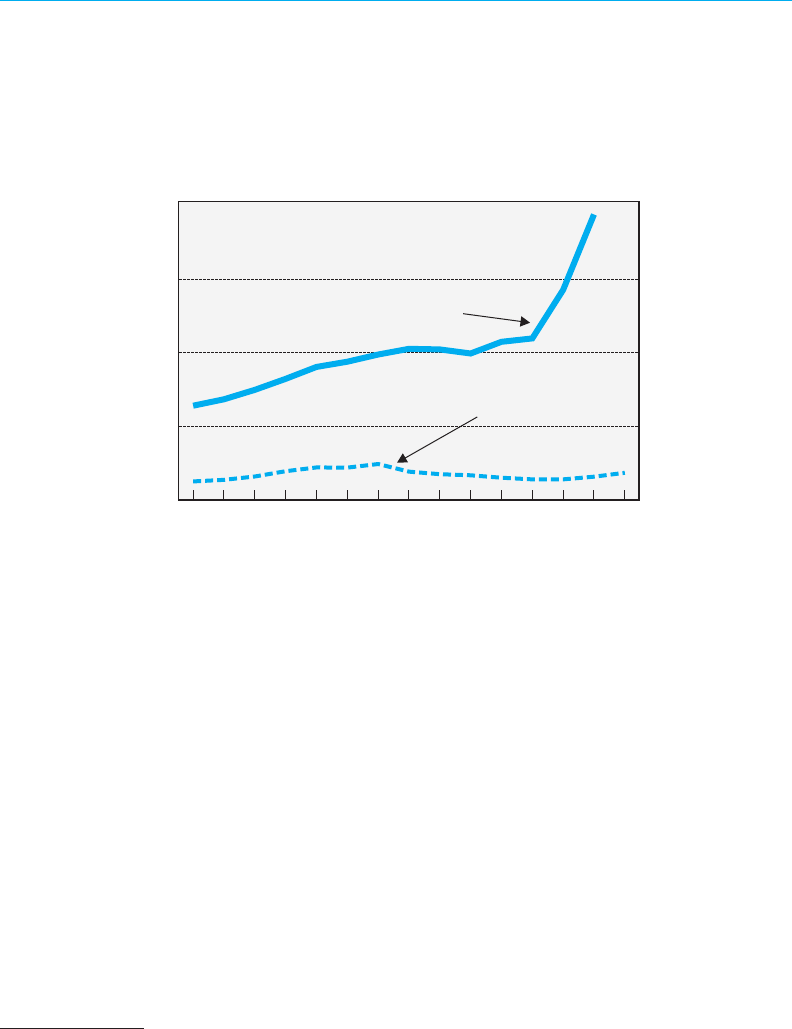

Alaska, Arizona, the Northeast, and California. In Texas, major markets such as Austin,

Dallas, and Houston experienced the building cycle early, spurred in part by robust local

economic growth during the late 1970s and early 1980s which significantly increased office

vacancy rates (see figure 3.2); it was followed by the bust in the late 1980s. More or less si-

multaneously, markets in Louisiana and Oklahoma had similar boom-and-bust experiences,

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 143

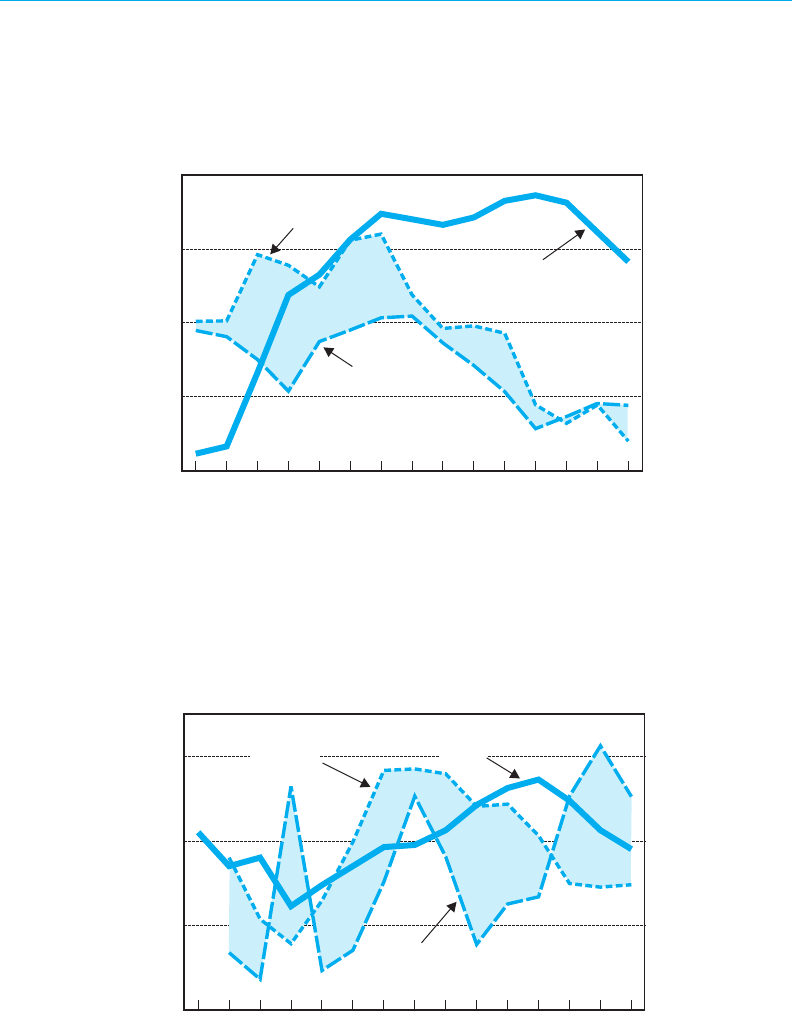

Percent

Source: .CB Commercial/Torto Wheaton Research

Office Vacancy Rates in Major Texas Cities,

1980–1994

Figure 3.2

Note: .Data for Austin are not available before 1985

Austin

Dallas

Houston

1980 1982 1984 1986 1988 1990 1992 1994

0

10

20

30

40

8

Chapters 911 describe the events in the Southwest, the Northeast, and California, respectively.

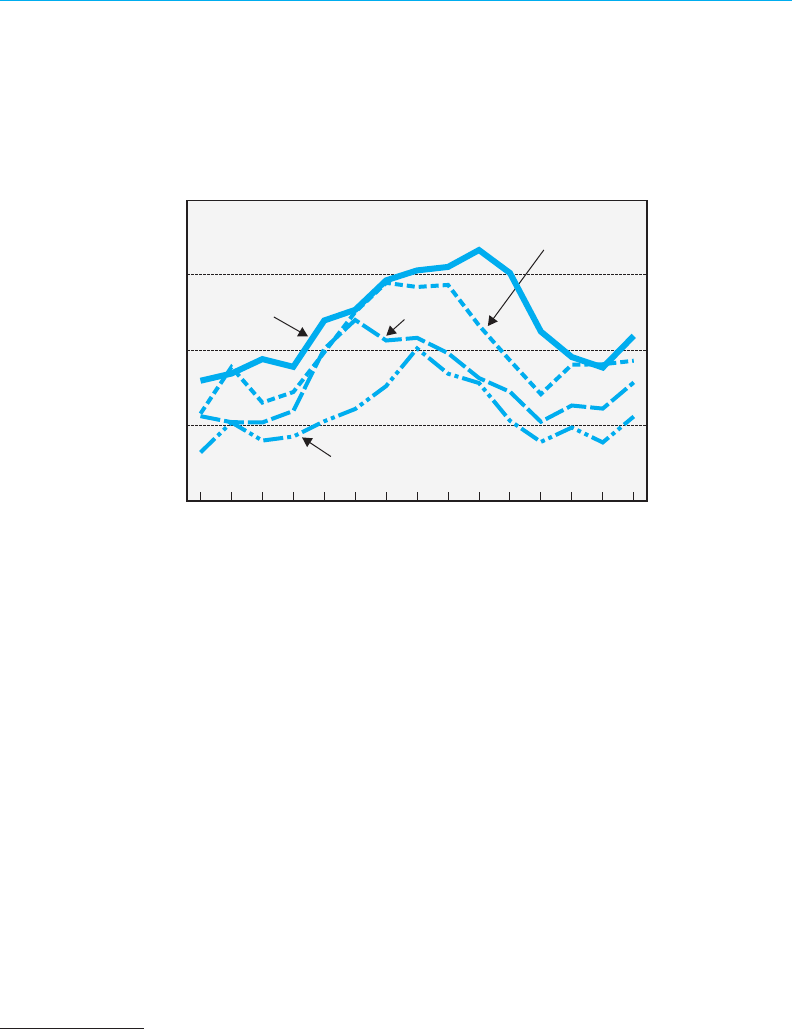

to be followed by Alaska. In Arizona, commercial real estate activity (as measured by the

value of new permits issued) more than doubled between 1983 and 1985, then declined 56

percent during the next six years. In New England and other northeastern states, commer-

cial construction boomed in the mid-1980s. New permit activity was up 100 percent in

Massachusetts between 1983 and 1986, 137 percent in Connecticut between 1983 and

1987, and 87 percent in New Jersey between 1983 and 1989. In all cases, severe overbuild-

ing was followed by high vacancy rates and then by sharp declines in new construction ac-

tivity, as evidenced by the decline in new building permits (see figure 3.3). In California the

value of newly issued commercial permits increased by almost 50 percent from 1983 to

1988 before plunging 31 percent between 1988 and 1991.

8

Although overbuilding and a subsequent run-up in vacancy rates characterized most of

the major commercial property types (office and retail), nationally the office sector was par-

ticularly affected (see figure 3.4). After surging 221 percent between 1977 and 1984, office

construction put in place was pared back somewhat during the second half of the decade be-

fore declining rapidly during the early 1990s. Because the production process is generally

much longer for office buildings than for retail or industrial properties, the adjustment to

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

144 History of the EightiesLessons for the Future

Source: U.S. Department of Commerce, Bureau of the Census, Building Permits

Division.

$Billions

Commercial Real Estate Cycles in Selected States,

1980–1994

(ValueofNewlyIssuedNonresidentialPermits)

Figure 3.3

1980 1982 1984 1986 1988 1990 1992 1994

0

0.75

1.50

2.25

3.00

New Jersey

Massachusetts

Arizona

Connecticut

9

Office employment is defined as the finance, insurance, and real estate sectors as well as office-using services, such as ac-

counting, advertising, personnel services, mailing, and computer processing.

market conditions is correspondingly slower. As a result, the office sector remained out of

balance during the entire decade.

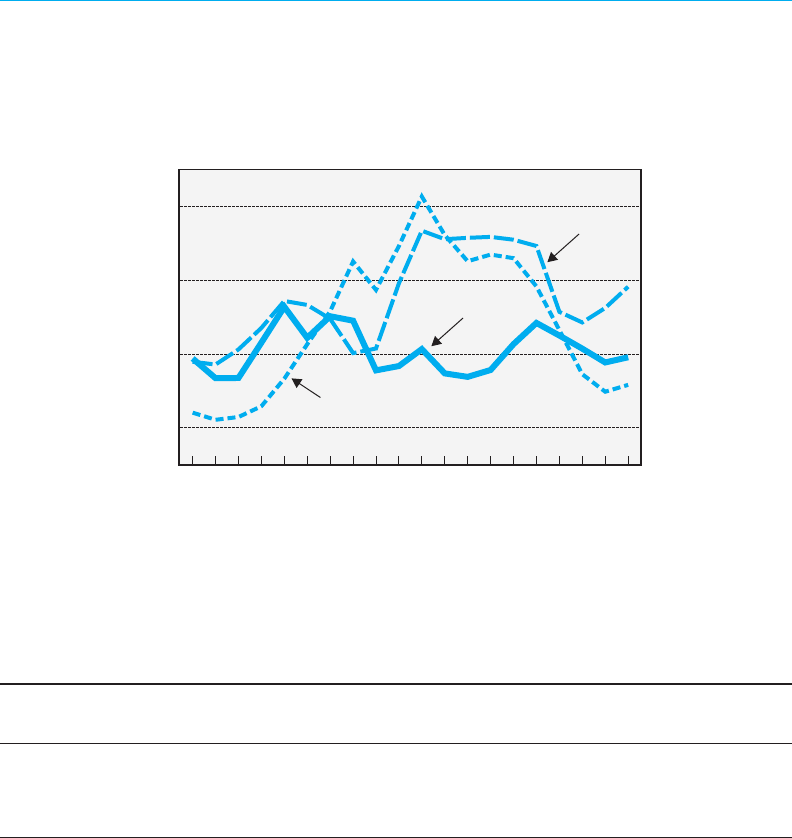

In both dollars and square feet, the magnitude of the 1980s office boom was extraor-

dinary. In dollars, the nationwide upswing in new construction that began in 1977 with $11

billion worth of office construction put in place peaked eight years later with $41 billion

worth of space produced (figure 3.4). In terms of floor space, during the five-year period

197579, in the 31 largest office markets around the country, an annual average of 33.6 mil-

lion square feet per year were completed (see table 3.1). In the next five-year period, com-

pletions of new floor space almost tripled, reaching an annual average of 97.8 million

square feet. From 1985 to 1989, the pace of completions remained at about the same level;

then starting in 1990, it plunged to an average of 28.1 million square feet per year over the

next four years.

The demand for new office space tracked the conditions in the office job market. Dur-

ing the late 1970s, office job growth exceeded 4 percent annually (see figure 3.5).

9

Office

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 145

Source: Current

Construction Reports

U.S. Department of Commerce, Bureau of the Census,

, series C30, monthly.

$Billions

Nonresidential Construction Put in Place,

1975–1994

(1992 Dollars)

Figure 3.4

Other*

Industrial

Office

1975 1980 1985 1990 1994

10

20

30

40

* “Other” includes retail construction.

Table 3.1

Production of New Office Space,

31 Major Markets, 19751994

New Completions* Absorptions

Period (Millions of sq. ft.) (Millions of sq. ft.)

19751979 33.6 44.3

19801984 97.8 64.2

19851989 100.7 73.6

19901994 28.1 33.3

Source: CB Commercial/Torto Wheaton Research.

*Annual average during the period.

Absorptions refers to the net change in occupied space over a defined period.

employment continued to exceed 4 percent annually from 1980 through 1989 with the ex-

ception of the recession-related respite in 1982. As a consequence, the absorption of new

office space increased sharply during most of the decade as well.

However, even though demand as measured by absorption rates increased substan-

tially during the 1980s, it was outpaced by the booming construction (supply) of new office

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

146 History of the EightiesLessons for the Future

Source: CB Commercial/Torto Wheaton Research.

Office and Total Employment Growth,

1976–1994

Figure 3.5

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994

-4

0

4

8

Percentage Change

Office

Employment

Total

Employment

3.0

4.8

6.8

6.2

4.3

4.5

1.8

4.9

7.7

6.7

4.3

4.3

4.5

3.9

2.0

-2.7

0.5

3.1

2.9

10

U.S. Department of Commerce, Bureau of Economic Analysis, Survey of Current Business.

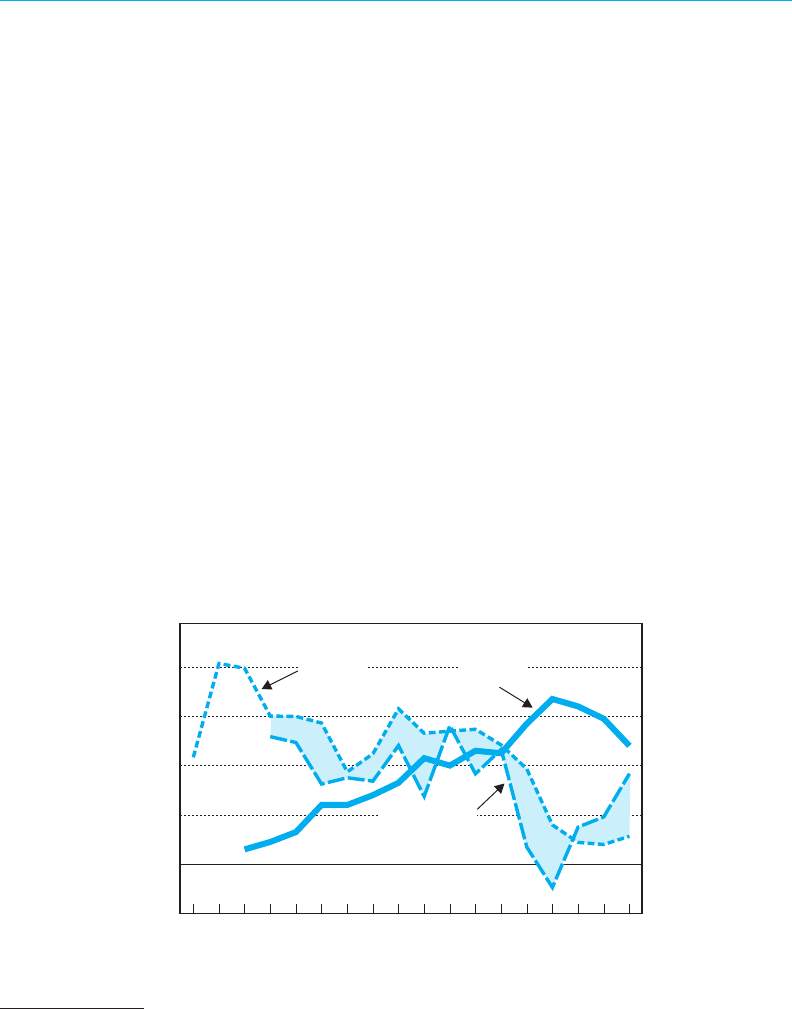

space. In major markets, new completions exceeded absorptions every year from 1980 to

1992 (see figure 3.6). As a result, vacancy rates in major markets rose to unprecedented lev-

els, nearly quadrupling between 1980 and 1991 from 4.9 percent to a peak of 18.9 percent.

Office job growth diminished after 1989, as corporate downsizing, mergers, and consolida-

tions became commonplace in the service sector, reducing the demand for office space (fig-

ures 3.5 and 3.6).

Like the office sector, the retail sector also boomed nationwide during the 1980s. Fa-

vorable underlying demographics and economic growth led to gains in retail sales that av-

eraged 6.8 percent per year between 1982 and 1987far above long-run trends.

10

That

growth provided the stimulus for retail development. Other construction activity, which

is dominated by the retail sector, rose sharply during 198485 and then remained steady

during the second half of the 1980s, averaging about $35 billion in construction put in place

annually (figure 3.4). This level was up from an annual average of approximately $24 bil-

lion during the first half of the decade.

Estimates of aggregate supply and demand for retail properties for 56 major markets

across the country are presented in figure 3.7. Between 1984 and 1990, construction of new

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 147

Office Market Conditions, 1980–1994

(31MajorMarkets)

1980 1982 1984 1986 1988 1990 1992 1994

0

40

80

120

160

4

8

12

16

20

Millions of Square Feet Vacancy Rate Percent

Source: CB Commercial/Torto Wheaton Research.

Figure 3.6

Vacancy

Rate

Increase in

Occupied Space

Net New

Supply

Retail Market Conditions, 1980–1994

(56MajorMarkets)

Millions of Square Feet Vacancy Rate Percent

Source: CB Commercial/Torto Wheaton Research.

Figure 3.7

Increase in

Occupied Space

1980 1982 1984 1986 1988 1990 1992 1994

0

40

80

120

0

4

8

12

Net New

Supply

Vacancy

Rate

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

148 History of the EightiesLessons for the Future

11

Commercial activity in the form of hotel/motel construction (not discussed above) was also volatile during this period, trac-

ing a pattern similar to the retail sector, rising 315 percent between 1975 and 1985, leveling off, and declining 64 percent

between 1990 and 1992.

12

For a good discussion of the issues associated with the boom-and-bust conditions of real estate markets during the 1980s,

see Patric H. Hendershott and Edward J. Kane, Causes and Consequences of the 1980s Commercial Construction Boom,

Journal of Applied Corporate Finance (spring 1992): 6170.

13

See, for example, Diana Hancock and J. A. Wilcox, Bank Capital and the Credit Crunch: The Roles of Risk-Weighted and

Unweighted Capital Regulations, AREUEA 22 (January 1993): 5994.

retail space is estimated to have averaged 94.8 million square feet annually in these mar-

kets. During the same period new demand for retail space also increased strongly, averag-

ing 51.6 million square feet, but failed to keep pace with the supply of new product. As a

result, retail vacancy rates are estimated to have risen from 4.9 percent in 1983 to 10.8 per-

cent in 1991. From 1991 to 1994, completions of new retail space fell 28 percent to 64.8

million square feetwell below the demand for new space. As a consequence, retail va-

cancies retreated to 7.6 percent by 1994.

11

Unlike the office and retail sectors of the commercial real estate market, the industrial

real estate sector did not experience a boom during the 1980s (figure 3.4). Industrial con-

struction surged nationwide in the late 1970s, reaching a peak of about $26 billion in 1979

(measured in 1992 dollars). During much of the 1980s activity trended downward before

leveling off in the early 1990s. Because of adjustments in production, the balance between

supply and demand for industrial space in the 1980s was relatively good for several years

during the decade. Nevertheless, as in the other sectors, net new supply still exceeded de-

mand for most of the decade, and vacancy rates rose.

Data on supply and demand conditions in 31 major markets illustrate that pattern (see

figure 3.8). The supply of new industrial floor space peaked in 197879, then trended

downward during the early part of the 1980s before leveling off during the remainder of the

decade. On average, 133 million square feet of new supply came to market each year dur-

ing the decade. At the same time, demand for industrial floor space averaged only 104 mil-

lion square feet annually. As a result, the overall vacancy rate in these 31 major markets rose

from 4.6 percent in 1979 to 10.7 percent in 1991.

Starting in the late 1980s and continuing into the early 1990s, the condition of real es-

tate markets changed dramatically. Boom conditions turned into bust conditions for all

types of commercial properties.

12

A number of factors accounted for this sharp deteriora-

tion. The closing of hundreds of insolvent thrift institutions by the Resolution Trust Corpo-

ration starting in 1989 dried up an important source of financing for real estate ventures. At

the same time, risk-based capital standards were being phased in for the banking industry;

these standards required higher capital levels behind commercial real estate loans and

helped reduce the supply of new loans at that time.

13

Regulatory officials were also sub-

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 149

Industrial Market Conditions, 1977–1994

(31MajorMarkets)

Millions of Square Feet Vacancy Rate Percent

Source: CB Commercial/Torto Wheaton Research.

Figure 3.8

1978 1980 1982 1984 1986 1988 1990 1992 1994

-50

0

50

100

150

200

2

4

6

8

10

12

Increase in

Occupied

Space

Net New

Supply

Vacancy

Rate

14

It is generally recognized that industry-wide underwriting standards for most types of commercial real estate loans declined

during the 1980s and, in the face of mounting real estate losses during the 1990s, were revised upward. These issues are

discussed below.

jecting commercial banks to more frequent examinations and closer supervisory scrutiny,

given passage of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989

(FIRREA) and the increasing number of bank and thrift failures. The national recession of

199091 reduced the demand for commercial space, and the combination of reduced de-

mand and the overbuilding of the 1980s produced significant declines in rents, prices, and

returns for commercial real estate properties. As a consequence, credit quality for outstand-

ing real estate loans on the books of surviving institutions was also declining rapidly. This

induced many real estate lenders to cut back on the origination of new commercial real es-

tate loans and to tighten underwriting standards.

14

Primarily for these reasons, new com-

mercial real estate construction plunged during the 1990s.

In the office sector, new construction activity almost came to a halt. In the 31 major

markets tracked by CB Torto/Wheaton Research, only 1.7 million square feet were com-

pleted in 1994. The pace of both retail and industrial construction similarly slackened, hav-

ing peaked in the mid-1980s. By 1994, completions of new retail space had fallen almost 50

percent (figure 3.7), while construction of new industrial buildings was only a small portion

of its previous peak (figure 3.8). Furthermore, bank lending for construction and land de-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

150 History of the EightiesLessons for the Future

15

National Real Estate Index, Market Monitor (19891994).

16

The Russell-NCREIF Real Estate Performance Report (fourth quarter 1994).

17

Ibid.

velopment, which peaked in 1989 at almost $136 billion, by 1993 fell to a ten-year low of

just over $66 billion.

The drop-off in new construction activity allowed the existing overhang for all types

of commercial properties to be absorbed. By the early 1990s, the demand for commercial

properties exceeded the new supply for the first time since the commercial real estate boom

had begun. Demand has continued to outpace supply since that time, with vacancy rates

falling (figures 3.6, 3.7, and 3.8).

As mentioned above, the overbuilding in the commercial real estate markets during

the 1980s resulted in declining rental rates, falling property values, and decreasing returns

to investors. Although no comprehensive data are available on rents, asset prices, and re-

turns for commercial real estate, the National Real Estate Index (NREI) and the Russell-

NCREIF index provide information on limited sets of commercial properties. As such,

these data may not be representative of the entire market.

According to the NREI, in 51 major metropolitan markets both the mean prices and

rents per square foot and the mean sale prices per square foot of office, industrial, and retail

properties began to slide between mid-1989 and mid-1990. Although all three types of com-

mercial properties experienced declines, the drop in rents and prices was most pronounced

for office properties. For example, from the middle of 1989 through the first quarter of

1994, the average sale price per square foot of commercial office property declined from

$182 to $133, a drop of approximately 27 percent. Office rents declined a more modest 17

percent, from approximately $24 to $20 per square foot.

15

At the same time that rent levels were restrained by rising vacancy rates and leasing

concessions, operating expenses climbed. According to the Russell-NCREIF index, which

tracks prime-quality office properties, between 1982 and 1991 net operating income (NOI)

for these properties declined by an average annual rate of 0.9 percent (the rate was weighted

by the 3.4 percent rate of average annual decline in NOI between 1986 and 1990). In addi-

tion, on the basis of appraisal and sales data, the same properties lost just over 26 percent in

value from 1987 to 1993.

16

Falling NOI and property values resulted in negative overall re-

turns. The NCREIF data show that overall returns on all of these commercial real estate

properties plummeted from a total return of 18.1 percent in 1980 to a negative 6.1 percent

in 1991.

17

Returns continued to be negative or close to zero until 1994.

A 1993 study involving FDIC receivership assets provides additional empirical evi-

dence of the dramatic change in commercial real estate prices during this period. The study

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 151

18

James L. Freund and Steven A. Seelig, Commercial Real-Estate Problems: A Note on Changes in Collateral Values Back-

ing Real-Estate Loans Being Managed by the Federal Deposit Insurance Corporation, FDIC Banking Review 6, no. 1

(spring/summer 1993): 2630.

19

Commercial real estate loans consist of loans for construction and land development, loans secured by nonfarm nonresi-

dential properties, and loans secured by multifamily properties.

analyzed changes in collateral values on a loan-by-loan basis, using data on assets that the

FDICs Division of Liquidation managed after obtaining them from failed banks.

18

Ap-

proximately 224 loans were reviewed from a random sample of 400 loans, evenly distrib-

uted regionally and selected from a population of the approximately 6,000 nonperforming

commercial real estate loans held by the FDIC receiverships as of mid-1992. Because the

loans analyzed were obtained from failed banks, they may not be representative of the

changes in value for the commercial real estate market as a whole during the 1980s.

The results indicate that the average decline in collateral value for the 224 loans re-

viewed was 54 percent. Furthermore, for three-quarters of the loans the 1992 collateral

value was at least 25 percent below the original evaluation; and for almost one-half, the col-

lateral lost at least 50 percent of its former assigned value. In contrast, less than one-tenth

of the collateral had appreciated in value after the loan was originated. As expected, these

losses varied according to region. For example, one-half of the loans reviewed from Con-

necticut lost 63 percent or more of their original valuation, and one-half of the loans from

Texas and Louisiana lost 58 percent or more of their original valuation. Loans from states

affected less severely by commercial real estate problems, such as California and Florida,

lost about 30 percent and 34 percent, respectively, of original appraised value.

The Involvement of Banks

During the 1980s, as the levels of total loans to total assets on the balance sheets of

U.S. commercial banks increased, bank loan portfolios also became relatively riskier.

Banks reallocated resources toward more real estate loans, emphasizing commercial real

estate loans.

19

The increases in total loans, in real estate loans, and in commercial real es-

tate loans eventually had implications for the number of bank failures and the size of losses

to the bank insurance fund.

These trends are presented in table 3.2. Between 1980 and 1990, total loans and leases

increased from 55 to 63 percent of total assetsa record high. Total real estate loans in-

creased sharply as well, going from approximately 18 to over 27 percent of total assets,

whereas total consumer loans grew only slightly, from approximately 10 percent to 11 per-

cent, and total commercial and industrial loans declined, dropping from approximately 20

percent to 17 percent of total assets.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

152 History of the EightiesLessons for the Future

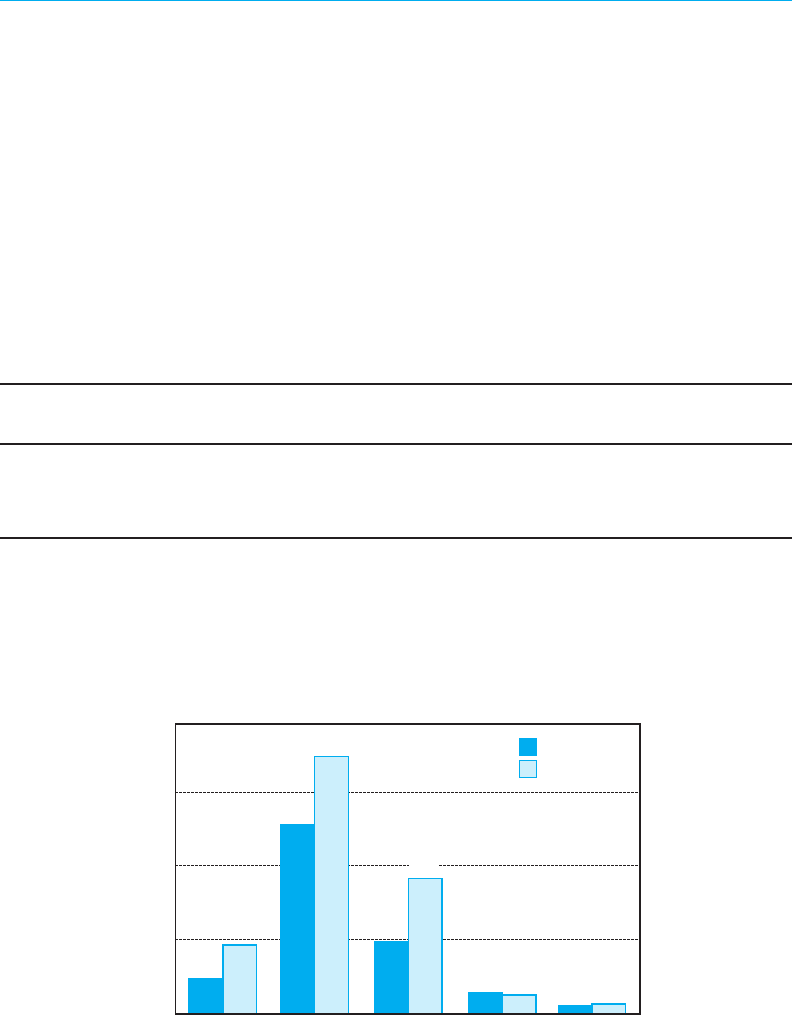

Table 3.2

Major Loan Categories of U.S. Banks as a

Percentage of Total Assets, 1980 and 1990

1980 1990

(Percent) (Percent)

Real estate loans 17.8 27.1

Commercial and industrial loans 19.5 17.1

Consumer loans 9.6 11.3

Total loans and leases 55.4 62.8

1.9

10.2

3.9

1.1

0.4

3.7

13.9

7.3

1.0

0.5

Real Estate Loan Portfolio of U.S. Banks

as a Percentage of Total Assets,

1980 and 1990

Figure 3.9

Percent

1980

1990

0

4

8

12

Construction

and Land

Development

1- to 4-Family

Residential

Properties

Nonfarm

Nonresidential

Properties

Multifamily

Properties

All Other

The changes in the composition of banks real estate loan portfolios over this period

are presented in figure 3.9. Construction and land development loans increased from nearly

2 to 4 percent; loans secured by 1- to 4-family properties rose from 10 to 14 percent of as-

sets; nonfarm nonresidential real estate loans increased from approximately 4 to over 7 per-

cent. Finally, loans originated on multifamily properties were relatively unchanged over the

period. In dollar terms, between year-end 1980 and year-end 1990 total loans and leases

held by banks more than doubled, from $1.0 trillion to $2.1 trillion (not shown). During the

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 153

same period, total real estate lending more than tripled, from $269 billion to $830 billion;

and commercial real estate loans almost quadrupled, from $64 billion to $238 billion.

In the wake of the significant loan-portfolio expansion during the 1980s, the overall

quality of the banks loans deteriorated. Between 1984 and 1991, nonperforming loans rose

from 3.1 percent to 5.2 percent, while net loan charge-offs jumped from 0.7 percent to a

peak of 1.6 percent (see table 3.3). The loss experience with commercial real estate credits,

however, was more pronounced than the loss experience for the overall portfolio. Although

data are not available until 1991, in that year the proportion of commercial real estate loans

that were nonperforming or foreclosed stood at 8.2 percent, and in the following year net

charge-offs for commercial real estate loans peaked at 2.1 percent.

Loan Underwriting Standards

The amount of the commercial real estaterelated losses recorded by the banking in-

dustry was compounded somewhat by the loosening of underwriting standards on commer-

cial loan contracts. It is generally recognized that many banks, under intense competitive

pressure from other banks, thrifts, and other financial institutions, relaxed contract terms

Table 3.3

Real Estate Loan Portfolio Quality,

U.S. Banks, 19841994

Noncurrent Charge-offs on

Commercial Real Commercial Real

Nonperforming Estate Loans/Total Estate Loans/Total

Loans/Total Net Charge-offs/ Commercial Real Commercial Real

Year Loans* Total Loans Estate Loans Estate Loans

1984 3.1% 0.7% NA NA

1985 2.9 0.8 NA NA

1986 3.1 0.9 NA NA

1987 3.7 0.8 NA NA

1988 3.3 0.9 NA NA

1989 3.6 1.1 NA NA

1990 4.8 1.4 NA NA

1991 5.2 1.6 8.2% 2.0%

1992 4.4 1.3 7.0 2.1

1993 2.8 0.8 4.7 1.4

1994 1.8 0.5 1.4 0.8

Note: Data are not available for years before 1984.

*Nonperforming loans include loans 90 days past due, non-accruing loans, and repossessed real estate.

Noncurrent commercial real estate loans include non-accruing loans and repossessed real estate.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

154 History of the EightiesLessons for the Future

20

For a discussion of these issues, see Hendershott and Kane, Causes and Consequences, 6567.

21

From April to June 1995, FDIC staff conducted a series of interviews with regulatory officials from the FDIC, the Federal

Reserve System, the Office of the Comptroller of the Currency, and the Office of Thrift Supervision, some of whom were

located in the six cities listed below and some of whom were senior officials at the agencies headquarters in Washington,

D.C. Also interviewed were commercial bankers in the six locations: Atlanta, Boston, Dallas, Kansas City, New York, and

San Francisco. Altogether approximately 150 regulatory officials and bankers were interviewed for this analysis.

during the 1980s and therefore assumed more credit risk.

20

However, because little empiri-

cal evidence exists to document these trends, the discussion in this section is based primar-

ily upon information gathered directly from interviews with a variety of sources, including

(1) field examiners of the federal bank regulatory agencies who had direct experience re-

viewing real estate loans in the 1980s, (2) other federal bank regulatory staff who tracked

these issues during the period, and (3) commercial bankers who had knowledge of banking

practices during this decade.

21

The heightened competition banks faced during the 1980s was a result of many fac-

tors, including the removal of deposit interest-rate ceilings, which significantly increased

the cost of doing business; the granting of expanded lending and investment powers to thrift

institutions; the increase in the number of newly chartered banks (approximately 2,800 new

charters were granted during the 1980s); pressure from bank stockholders to improve earn-

ings; the large-scale conversion of savings banks from mutual to stock ownership, a con-

version that increased demand for new investments; and the loss of a sizable portion of the

commercial and industrial lending business to the commercial paper market. Under these

circumstances, many banks adopted riskier loan polices in an attempt to increase revenue

and to maintain market share vis-à-vis other lending institutions. Both examiners and com-

mercial bankers themselves who were familiar with the issues of that time suggested that

banks had increasing difficulty coping with the new environment and that many conserva-

tively managed institutions assumed greater risks because of the general belief that if we

dont make the loan, the institution across the street will.

In this environment, commercial real estate lending was attractive to many institu-

tions. These credits brought large up-front fees, which generated immediate income (par-

ticularly from construction loans). Such fee income became essential to many struggling

institutions. The experts who were interviewed observed that as commercial real estate

lending expanded, underwriting standards for the major types of commercial real estate

loans (land, construction, and mortgage) were loosened significantly. The key changes

noted dealt with two fundamental areas of risk control: (1) ensuring that the income gener-

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 155

22

Sound underwriting policies in lending institutions require that borrowers invest some percentage of their own funds into

a project, with the balance being placed by the lender. This standard provision is referred to as the loan-to-value ratio (the

total amount financed by the lender as a percentage of the total investment or value of the collateral). The lower the amount

of borrowers funds as a percentage of the total investment, generally the larger the credit risk for the lending institution.

23

Whether this principal workout provision was more common in the real estate transactions of the 1980s than in other

decades is not known.

24

Appraisal policies on commercial properties during the 1980s are discussed in the next section.

ated by a project is sufficient to cover the interest and principal payments on borrowed

funds, and (2) establishing adequate loan-to-value guidelines.

22

Traditionally, decisions to extend loans that are collateralized by commercial real es-

tate property are evaluated by lenders primarily on the borrowers ability to generate earn-

ings from the investment sufficient to cover the existing debt payments. This is a

fundamental tenet of the lending function. As a backup source of security, lenders evaluate

the worth of the investment property as potential collateral to cover the loan value in the case

of default by the borrower. Starting in the late 1970s and continuing for most of the follow-

ing decade, examiners observed that lenders loosened loan terms relating to debt-service

coverage and placed relatively more emphasis on the value of the collateral in making fund-

ing decisions. This change in loan procedures was based primarily on the assumption that

real estate values (collateral values) would continue to rise in the future as they had in the re-

cent past. In this respect, many lenders mistakenly anticipated that the demand for commer-

cial space (office, retail, and industrial) would remain strong and would keep pace with

construction activity. When the real estate markets collapsed starting in the late 1980s, many

lenders discovered that collateral values were often insufficient to cover existing loan losses.

Also with respect to debt-service issues, lenders often liberalized the frequency and

timing of principal payments. In some situations, examiners found credits in which the

lender allowed the principal payments to be renewed repeatedly.

23

Or when interest pay-

ments fell into arrears, the unpaid interest was frequently added back to the unpaid princi-

pal, or capitalized. According to experts, this practice of capitalizing interest payments

had been relatively uncommon before the 1980s.

Examiners also noted important changes in the loan-to-value criteria adopted by

banks during the 1980s. To maintain market share, many banks chose to raise their maxi-

mum loan-to-value ratios, thereby decreasing the amount of borrowers equity at risk and

increasing the risk to the lender. Moreover, appraised property values, which constitute the

denominator in the loan-to-value ratio, frequently provided overly favorable collateral val-

ues and/or were often based on speculative premises.

24

In addition to standards on debt-

service capacity and loan-to-value ratios, other basic underwriting standards were also

relaxed in many regions of the country. For example, secondary repayment sourcesthe re-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

156 History of the EightiesLessons for the Future

course, or the guarantors of the original loan amountoften were not actively scrutinized

by the lender. In contrast, the traditional practice usually involves a detailed analysis of the

recourse partys repayment capacity.

According to examiners and bankers, during the 1980s many banks also abandoned

their traditional reluctance to lend outside their local areas and often became involved in

lending on real estate projects for which they had little or no direct experience. Lenders ei-

ther provided direct funding to out-of-area projects or purchased loan participations from

out-of-area institutions, and often the bank acquiring the loan participation had only a lim-

ited relationship with the out-of-area financial institution. Moreover, in their eagerness to

participate in the burgeoning commercial development market, many institutions became

involved in real estate transactions without having had adequate experience in structuring,

monitoring, or administering specialized commercial real estate credits. As a consequence,

many of these projects later ended up in default.

The Role of Appraisers and Subsequent Reforms

Current federal regulations require that federally insured depository institutions ob-

tain an outside or independent opinion on the collateral value for most real estate loans

before committing funds. The premise underlying the rule is that the real estate appraiser is

the only independent or neutral party involved in the transaction, whereas both bor-

rowers and lenders have vested interests. An experienced appraiser is assumed to bring spe-

cialized knowledge of local real estate markets to the transaction and, if conservative

loan-to-value rules are followed, is expected to serve as a potential check on the amount of

funds being committed to a project. Thus, the appraisal is expected to be an integral part

of the loan decision and to provide another perspective from which to evaluate the viability

of the project.

Evidence about appraisal polices during the 1980s shows that flawed and fraudulent

appraisals were often used by federally insured financial institutions, especially thrift insti-

tutions, and that these practices were associated with most depository-institution failures

during the period.

25

The paragraphs that follow summarize the comments of the bank ex-

25

See Patric H. Hendershott and Edward J. Kane, U.S. Office Market Values during the Past Decade: How Distorted Have

Appraisals Been? Real Estate Economics 23 (1995): 101116. The U.S. House Committee on Government Operations,

which investigated depository institutions appraisal policies during the 1980s and early 1990s, found widespread evidence

of incompetence and fraud associated with appraisal practices, primarily at thrift institutions but to some extent at com-

mercial banks. It was noted in the public record that these appraisal policies caused or were associated with most deposi-

tory-institution failures. As a consequence of the investigations, major reforms in the area of appraisals were enacted in

FIRREA in 1989 (these reforms are discussed below). See the U.S. House Committee on Government Operations, Impact

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 157

aminers and commercial bankers interviewed about the appraisal process during the 1980s

(see footnote 21). They are followed by a brief description of the reforms legislated in 1989.

In the 1980s, appraisals ceased to be as useful a part of the commercial loan process

as they had been in previous years. During the early to middle years of the decade, when

many markets experienced unprecedented boom conditions and both borrowers and

lenders believed the conditions would continue for some time, appraisers generally went

along with the prevailing inflationary expectations and reflected them in their cash-flow

assumptions and analyses. Thus, appraisals often failed to check or slow down the amount

of funds being committed to specific projects.

The quality of appraisals became less rigorous during the 1980s as rapid expansion

in real estate development led to the hiring of many new and inexperienced appraisers. En-

try into the field required few credentials in the form of academic requirements, training,

or on-the-job experience. Thus, many people with only marginal experience in such com-

plex matters were writing opinions on these subjects. In addition, the appraisal industry

was fragmented into numerous associations and membership designations, with no gen-

eral uniformity in performance standards. Finally, real estate appraisers were mostly un-

regulated during the 1980s: state licensing requirements were nearly nonexistent, and the

federal bank regulators provided little oversight of appraisal procedures or practices at in-

sured institutions.

In some instances the ethical standards of the appraisal process were reported to

have been compromised by fraudulent activity. Appraisers would often fail to render un-

biased, independent opinions. And except in the most egregious cases, appraisers were

generally not held accountable for deficient and/or overstated appraisals. The existence of

malpractice and fraud resulted in major reforms in appraisal procedures involving federal

insured institutions in 1989. (See discussion of FIRREA below.)

On the regulatory side, bank examiners had little formal training in evaluating ap-

praisals and were not in a position to challenge their accuracy. Although examiners rou-

tinely reviewed and evaluated credit-file appraisals and periodically questioned them, in

most instances they deferred to the judgment of the qualified appraiser. Moreover, with

the use of increasingly sophisticated discounted-cash-flow models, appraisal reports were

becoming more complicated and thus more difficult for exa

miners to evaluate.

of Faulty and Fraudulent Real Estate Appraisals on Federally Insured Financial Institutions and Regulated Agencies of

the Federal Government: Hearings, 99th Cong., 1st sess., December 11 and 12, 1985; and House Committee on Govern-

ment Operations, Subcommittee on Commerce, Consumer, and Monetary Affairs, Implementation of Title XI, The Ap-

praisal Reform Amendments of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA):

Hearings, 101st Cong., 2d sess., May 17, 1990. See also the House Committee on Government Operations, Status of the

Implementation of Title XI, The Appraisal Reform Amendments of the Financial Institutions Reform, Recovery, and En-

forcement Act of 1989 (FIRREA), 28th report, 101st Cong., 2d sess., November 14, 1990.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

158 History of the EightiesLessons for the Future

26

FDIC Bank Letter 40-87 dated December 14, 1987, details specific guidelines for real estate appraisal policies and review

procedures. These guidelines were adopted jointly by the FDIC, the Federal Reserve Board, and the Office of the Comp-

troller of the Currency. Before 1987 only the Federal Home Loan Bank Board had promulgated regulations regarding ap-

praisal policies, practices, and procedures involving federally insured thrift institutions.

27

The Appraisal Subcommittee consists of officials from the Federal Deposit Insurance Corporation, the Federal Reserve

Board, the National Credit Union Administration, the Office of the Comptroller of the Currency, the Office of Thrift Su-

pervision, and the U.S. Department of Housing and Urban Affairs. The Appraisal Subcommittee is responsible for moni-

toring certification and licensing requirements, banking agency regulations, and appraisal organizations.

28

The Resolution Trust Corporation ceased its activities at year-end 1995.

29

The appraisal foundation is a private sector organization that has established an Appraiser Qualification and Standards

Board. The purpose of the board is to professionalize the appraisal industry and establish coordination between the indus-

try and federal and state officials in developing a national system of qualification and supervision.

30

As stated above, commercial real estate loans are defined as loans for construction and land development, loans secured by

nonfarm, nonresidential properties, and loans on multifamily properties.

In 1987, after Congress investigated the appraisal practices of the 1980s, the federal

bank-regulatory agencies issued interagency guidelines addressing appraisal policies, stan-

dards, and procedures for depository institutions.

26

In 1989, the Financial Institutions Re-

form, Recovery, and Enforcement Act of 1989 (FIRREA) became law, requiring bank

regulatory officials to establish licensing and certification standards for anyone who con-

ducts appraisals for federally insured depositories. Licensing and certification are state

functions that would be overseen by the Appraisal Subcommittee of the Federal Financial

Institutions Examination Council (FFIEC).

27

The legislation assigned four primary responsibilities to the FFIEC Appraisal Sub-

committee: (1) monitoring the adequacy of state requirements for certification and licens-

ing as well as standards of professional conduct; (2) monitoring the regulations of the

banking agencies, the Resolution Trust Corporation,

28

and the National Credit Union Ad-

ministration; (3) monitoring the activities of the appraisal foundation;

29

and (4) maintaining

a national registry of state-certified and licensed appraisers.

Commercial Real Estate Lending and Bank Failures

Many of the banks that failed during the 1980s and early 1990s were active partici-

pants in the regional real estate market booms, particularly the booms in commercial real

estate. The connection between participation in the real estate booms and bank failure can

be seen if one compares the commercial real estate loan concentrations of banks that sub-

sequently failed with those of banks that did not fail.

30

In all years between 1980 and 1993,

the concentrations of commercial real estate loans relative to total assets were higher for

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 159

Percent

Note: Ratios are unweighted averages. Open-bank assistance cases are not

counted as failures.

Commercial Real Estate Loans

as a Percentage of Total Assets,

Failed and Nonfailed Banks, 1980–1994

Figure 3.10

1980 1982 1984 1986 1988 1990 1992 1994

0

10

20

30

* Banks that failed in 1994 did not report year-end financials.

Banks That

Subsequently

Failed*

Banks That

Did Not Fail

banks that subsequently failed than for nonfailed banks. In 1980, commercial real estate

loans of banks that subsequently failed constituted approximately 6 percent of their total as-

sets; in 1993, almost 30 percent (see figure 3.10). Among nonfailed banks, commercial real

estate loans also constituted approximately 6 percent of total assets in 1980, but in 1993 the

figure had risen only to 11 percent. A similar pattern is observed for commercial real estate

loans relative to total real estate loans (see figure 3.11). In 1980, banks that subsequently

failed had 43 percent of their total real estate loan portfolio in commercial real estate loans;

by 1993 this had increased to about 69 percent. In contrast, nonfailed banks were more con-

servatively invested: in 1980, 32 percent of their total real estate loan portfolio was invested

in commercial real estate loans, and by 1993 the percentage was still approximately the

same.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

160 History of the EightiesLessons for the Future

1994

Percent

Commercial Real Estate Loans

as a Percentage of Total Real Estate Loans,

Failed and Nonfailed Banks, 1980–1994

Figure 3.11

1980 1982 1984 1986 1988 1990 1992

30

40

50

60

70

Note: Ratios are unweighted averages. Open-bank assistance cases are not

counted as failures.

* Banks that failed in 1994 did not report year-end financials.

Banks That

Subsequently

Failed*

Banks That

Did Not Fail

31

Nonperforming real estate assets were defined as the sum of real estate loans past due 90 days or more, non-accrual real es-

tate loans, and repossessed real estate (excluding direct investments in real estate).

These exposures to volatile commercial real estate markets contributed to the asset-

quality problems of many banks. Although data on nonperforming commercial real restate

loans were not available before 1991, data on nonperforming real estate assets were avail-

able beginning in 1984. Nonperforming real estate assets of banks that subsequently failed

constituted 34 percent of their nonperforming assets in 1984 but rose to 87 percent by

1993.

31

Nonfailed banks nonperforming real estate assets rose as well but not nearly as

much, from almost 40 percent of total nonperforming assets in 1984 to more than 62 per-

cent by 1993 (see figure 3.12).

Finally, the high concentrations in the volatile commercial real estate market con-

tributed to overall losses. For subsequently failed banks, gross charge-offs on real estate

loans constituted only 8 percent of total charge-offs in 1984 but rose to 43 percent by 1993.

Nonfailed banks real estate charge-offs constituted 12 percent of total charge-offs in 1984

and rose to only approximately 20 percent in 1993 (see figure 3.13). These statistics indi-

cate no bank was totally immune to the real estate market conditions of the period.

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 161

Percent

Nonperforming Real Estate Assets

as a Percentage of Total Nonperforming Assets,

Failed and Nonfailed Banks, 1984–1994

Figure 3.12

1984 1986 1988 1990 1992 1994

30

40

50

60

70

80

90

Note: Ratios are unweighted averages. Open-bank assistance cases are not

counted as failures.

* Banks that failed in 1994 did not report year-end financials.

Banks That

Did Not Fail

Banks That

Subsequently

Failed*

Conclusion

In the early 1980s, a large demand for real estate investments produced a boom in

commercial construction activity. Public policy actions further stimulated the boom: tax

breaks enacted as part of the Economic Recovery Act of 1981 greatly enhanced the after-

tax returns on real estate investment, and the GarnSt Germain Act of 1982 expanded the

nonresidential-lending powers of savings associations.

In pursuit of the construction boom, many banks moved aggressively into commercial

real estate lending. Total real estate loans of banks more than tripled, and commercial real

estate loans nearly quadrupled. Generally, bank underwriting standards were loosened, of-

ten unchecked either by the real estate appraisal system or by supervisory restraints. In ad-

dition, overly optimistic appraisals, together with the relaxation of debt coverage, the

reduction in the maximum loan-to-value ratios, and the loosening of other underwriting

constraints, often meant that borrowers frequently had little or no equity at stake, and in

some cases lenders bore most or all of the risk.

As a result, overbuilding occurred in many markets, and when the bubble burst start-

ing in the late 1980s, real estate values collapsed. At institutions heavily exposed to real es-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

162 History of the EightiesLessons for the Future

Percent

Real Estate Charge-offs as a Percentage of

Total Charge-Offs, Failed and Nonfailed Banks,

1984–1994

Figure 3.13

1984 1986 1988 1990 1992 1994

0

10

20

30

40

50

Note: Ratios are unweighted averages. Open-bank assistance cases are not

counted as failures.

* Banks that failed in 1994 did not report year-end financials.

Banks That

Did Not Fail

Banks That

Subsequently

Failed*

tate lending, loan quality deteriorated significantly. This deterioration eventually caused

many banks to fail. Compared with surviving banks, banks that subsequently failed in the

1980s had higher ratios of (1) commercial real estate loans to total assets, (2) commercial

real estate loans to total real estate loans, (3) noncurrent commercial real estate loans to to-

tal commercial real estate loans, and (4) real estate charge-offs to total charge-offs.

Appendix

Illustration of the Effects of

Illustration of the Effects of

Major T

Major T

ax Legislation

ax Legislation

To illustrate how commercial real estate investment returns were affected by the

changes in tax law during the 1980s (see table 3-A.1), an example is presented here (see

table 3-A.2) that compares the after-tax internal rate of return on a hypothetical income-

producing commercial real estate property acquired in three different years: 1980 (before

passage of the Economic Recovery Tax Act of 1981 [ERTA]); 1982 (after passage of

ERTA); and 1987 (after passage of the Tax Reform Act of 1986).

The example assumes that the real estate investor was in the highest tax bracket and

that 75 percent of the purchase price was financed. The property had a pre-tax operating net

income of $100,000 for the first year (approximately 10 percent of the purchase price), in-

flating at a rate of 5 percent per annum thereafter. The holding period for the property was

seven years. The example also assumes that the investor had other sources of income to

which he or she could apply the tax losses generated by the subject investment.

In this example, the difference in the pre- and post-ERTA after-tax rates of return was

significant (14.1 percent versus 21.5 percent). Much of this difference results from the ag-

gressive depreciation deductions allowable under ERTA in the early years of the propertys

holding period. Specifically, $521,651 in depreciation deductions were taken against tax-

Table 3-A.1

Major Tax Law Provisions Affecting Returns on

Commercial Real Estate Investment

PreEconomic PostEconomic PostTax

Recovery Tax Act Recovery Tax Act Reform Act

of 1981 of 1981 of 1986

Allowable depreciation life,

commercial real estate 40 years 15 years 31.5 years

Allowable depreciation method Straight-line 175% Declining balance Straight-line

Passive losses deductible? Yes Yes No

Max. ordinary income tax rate 70% 50% 38.5%

Capital gains tax rate 28% 20% 28%

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

164 History of the EightiesLessons for the Future

able income over the seven-year holding period (with $272,226 taken in the first three years

alone). At the highest ordinary income tax rate of 50 percent, this allowed for tax deferral

of $260,825. A $161,538 tax loss was generated that was used to offset other taxable in-

come. This benefit far outweighed the $138,215 tax liability for recaptured depreciation

due upon sale of the property.

Table 3-A.2

Hypothetical Investment Illustrating the Economic Effects of Major Tax

Legislation on Commercial Real Estate Investment

PreEconomic PostEconomic PostTax

Recovery Tax Act of Recovery Tax Act of Reform Act of

1981 1981 1986

Initial price of property (loan amt. $820,000) $1,094,745 $1,094,745 $1,094,745

Cumulative net operating income

(before depreciation, debt service, and taxes) 809,342 809,342 809,342

Cumulative depreciation 153,258 521,651 194,621

Cumulative taxable income (loss) (net of

property depreciation and mortgage interest) 45,317 (323,076) 3,954

Cumulative income tax liability (credit) 31,722 (161,538) 1,502

Cumulative after-tax income

(net of annual income taxes and

mortgage payments) 147,550 340,810 177,770

Gross sale proceeds 1,399,916 1,399,916 1,399,916

Gross taxes due upon sale 128,359 199,249 139,941

Ordinary income taxes on excess

accelerated depreciation over straight-line 0 56,475 0

Capital gains taxes on straight-line

depreciation recapture 42,912 81,740 54,494

Capital gains taxes on difference between

property purchase and sale price 85,447 61,034 85,447

Net sale proceeds (net of recapture, taxes,

and loan payoff) 470,872 399,983 459,290

After-tax internal rate of return 14.1% 21.5% 14.5%

Note: The analysis in this table is based on the following assumptions:

1. Real estate investor is in the highest tax bracket; 75 percent of the purchase price is financed.

2. Property has a pre-tax net operating income of $100,000 in the first year, inflating at a rate of 5 percent per annum

thereafter.

3. Property has a seven-year holding period.

4. Investor has other sources of income against which to apply tax losses generated by the property.

Chapter 3 Commercial Real Estate and the Banking Crises

History of the EightiesLessons for the Future 165

These differences are even more stark when we account for the positive time prefer-

ence of money. The $260,825 in cumulative tax savings taken during the life of the project

had a net present value of $188,548 (assuming a discount rate of 10 percent per year). The

net present value of the $138,215 tax liability due at termination of the investment, assum-

ing the same discount rate, was $70,926. Thus, on a discounted basis the investor had to re-

pay only $0.38 for each dollar of taxes deferred under the Accelerated Cost Recovery

System.

In the post-1986 tax regime, the same example shows that the after-tax rate of return

becomes nearly exactly what it had been pre-ERTA (14.1 percent before ERTA, 21.5 per-

cent under ERTA, 14.5 percent post-1986). This happened largely because the accelerated

depreciation methods were eliminated and straight-line was reinstated, with a lengthening

of the depreciable life of commercial real estate from 15 years to 31.5 years. Other signifi-

cant changes were that passive losses could no longer offset nonpassive income, and the

capital gains tax rate increased from 20 percent to 28 percent.