Working Paper Series

Assessing the fiscal-monetary

policy mix in the euro area

Krzysztof Bańkowski, Kai Christoffel,

Thomas Faria

Disclaimer: This paper should not be reported as representing the views of the European Central Bank

(ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

No 2623 / December 2021

Abstract

This paper attempts to gauge the effects of various fiscal and monetary policy rules on

macroeconomic outcomes in the euro area. It consists of two major parts – a historical assessment

and an assessment based on an extended scenario until 2030 – and it builds on the ECB-BASE –

a semistructural model for the euro area. The historical analysis (until end-2019, ’pre-pandemic’)

demonstrates that a consistently countercyclical fiscal policy could have created a fiscal buffer

in good economic times and it would have been able to eliminate a large portion of the second

downturn in the euro area. In turn, the post-pandemic simulations until 2030 reveal that certain

combinations of policy rules can be particularly powerful in reaching favourable macroeconomic

outcomes (i.e. recovering pandemic output losses and bringing inflation close to the ECB target).

These consist of expansionary-for-longer fiscal policy, which maintains support for longer than

usually prescribed, and lower-for-longer monetary policy, which keeps the rates lower for longer

than stipulated by a standard reaction function of a central bank. Moreover, we demonstrate

that in the current macroeconomic situation, fiscal and monetary policies reinforce each other

and mutually create space for each other. This provides a strong case for coordination of the

two policies in this situation.

JEL classification: E32, E62, E63

Keywords: Model simulations, Fiscal rules, Monetary policy rules, Joint analysis of fiscal and

monetary policy

ECB Working Paper Series No 2623 / December 2021

1

Non-technical Summary

Fiscal and monetary policy in the euro area exhibited distinct behaviours in the past, especially

amid the euro area sovereign debt crisis when fiscal policy was overall not supportive to growth (i.e.

procyclical). Against this background, this paper attempts to gauge the effects of various fiscal and

monetary policy rules, irrespective of the existing institutional arrangements, on macroeconomic

outcomes under different monetary policy rules. The analysis is conducted through the lens of

counterfactual scenarios using the ECB-BASE model, which is a semi-structural macroeconomic

model of the euro area.

In the model simulations we consider the two following subsamples: the historical pre-pandemic

period up to 2019Q4 and the post-pandemic projection period up to 2030. For the historical period

we mostly investigate whether different fiscal policy behaviour – more aligned with the monetary

policy reaction – would have been able to improve stabilisation of the euro area economy compared

to the realised trajectories. We also carefully look how the efficiency and the cost of the alternative

fiscal policy arrangements depend on the reaction of the central bank. Turning to the post-pandemic

horizon, we note that this period is associated with great macroeconomic challenges such as low

natural interest rate and high government debt. Taking into account this environment, we attempt

to identify constellations of the two policies that would facilitate a strong performance of the euro

area economy going forward.

According to the model simulations for the historical period, consistently countercyclical fiscal

policy significantly improves macroeconomic outcomes. In particular, it creates a buffer in good pre-

crisis times and, subsequently, eliminates a large portion of the second downturn associated with the

euro area sovereign debt crisis. Moreover, it noticeably reduces the negative inflation gap in recent

years. While these benefits are attainable at a manageable cost, as judged by the debt-to-GDP ratio,

they are also conditional on monetary accommodation. Also importantly, the positive outcomes can

only be achieved if the alternative fiscal policy is implementable in the euro area in real time – an

aspect we do not assess in the paper.

Regarding the post-pandemic period, our analysis indicates that the combination of expansionary-

for-longer fiscal policy and low-for-longer monetary policy has a chance to significantly improve

macroeconomic prospects. We define expansionary-for-longer fiscal policy as a policy that is ex-

ECB Working Paper Series No 2623 / December 2021

2

traordinarily cautious to ensure that a recovery is well in place and, as such, it maintains fiscal

support for longer and beyond the closure of the output gap. Low-for-longer monetary policy, in

turn, is defined as a policy that keeps the rates lower for longer compared to what would be sug-

gested by the standard reaction function of a central bank. Concretely, this policy constellation

could recover around 50% of the accumulated output losses that materialised amid the pandemic

and bring inflation into the territory close to the ECB target. While admittedly, this policy course

would require a considerable fiscal expansion and it would lead to a non-negligible increase in gov-

ernment debt the euro area debt-to-GDP ratio would remain still on non-increasing path around

100%, for most policy mixes.

Our analysis also indicates, that at the current juncture fiscal and monetary policy reinforce each

other, pointing to complementarities between the two policies. Fiscal policy stimulates output and

inflation more under the low-for-longer monetary policy rule than under the standard Taylor rule.

In the same vein, the ability of monetary policy to positively influence macroeconomic conditions is

greater when fiscal policy is expansionary-for-longer rather than when fiscal policy behaves as it did

in the past. Another important finding of the model simulations is that both policies create mutual

space for each other. Fiscal policy alleviates the ELB constraint faced by monetary policy, thereby

empowering the central bank. On the other hand, monetary policy limits the cost of fiscal policy

by preserving favourable financing conditions, hence it positively influences the fiscal space. This

provides a strong case for coordination between the two policies at the current juncture.

The stochastic simulations considering uncertainty confirm the findings of the deterministic sim-

ulations. Moreover, these simulations assess the stabilisation properties of fiscal and monetary policy

in an optimistic growth scenario and a pessimistic growth scenario.

1 Introduction

The conduct of fiscal and monetary policy has changed notably in the EMU period. Until the

great financial crisis (GFC) the aggregate variables representing the overall stance of policies (as

depicted by the euro area aggregate government budget balance and the ECB’s short-term interest

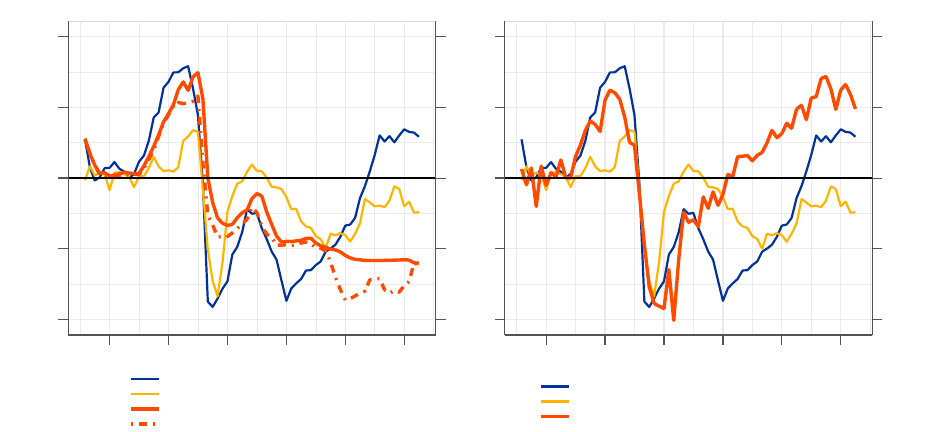

rate) co-moved with the business cycle (see Figure 1, co-movement with the output gap and the

inflation gap). In addition, in the wake of the GFC both policies strongly reacted to the downturn

ECB Working Paper Series No 2623 / December 2021

3

in a countercyclical fashion. Afterwards, however, a notable divergence between fiscal and monetary

policy emerged. While the latter, with the exception of a short tightening episode in 2011, kept

on progressing with an accommodative stance the former was tightening. In essence, fiscal and

monetary policy in the euro area reacted to the second downturn into opposite directions, with fiscal

policy exhibiting a procyclical stance.

Figure 1: Policy reaction over the business cycle in the euro area

-4

-2

0

2

4

-2

0

2

4

6

2004 2007 2010 2013 2016 2019

-4

-2

0

2

4

-7

-5

-3

-1

1

2004 2007 2010 2013 2016 2019

Output Gap (% of Pot. GDP)

Inflation Gap (pp)

Interest Rate (%, rhs)

Shadow Rate (%, rhs)

Output Gap (% of Pot. GDP)

Inflation Gap (pp)

Budget Balance (% of Pot. GDP, rhs)

Sources: Eurosystem and European Commission.

Notes: The inflation gap is calculated as the deviation to the 2% target value. The shadow rate is calculated according

to the methodology of Lemke and Vladu (2017). The potential GDP for the calculation of the output gap and the

budget balance-to-GDP ratio comes from the European Commission (Spring 2021 Economic Forecast) given that the

ECB does not publish potential GDP estimates.

The prevailing policy mix in the euro area since the formation of the EMU relied on monetary

policy as the main macroeconomic stabilisation tool. Fiscal policy instead was supposed to primarily

focus on ensuring debt sustainability and addressing country idiosyncratic shocks mostly by letting

automatic stabilisers operate freely. While the adequacy of this paradigm was largely unchallenged

during the great moderation period, the crisis episodes (i.e. the GFC and the COVID crisis) gave

rise to calls for a reassessment. Addressing these demands requires thorough analysis verifying to

which extent the policy mix in place was supportive to the achievement of the policy targets and

whether potential adjustments to the policy arrangements could improve the economic outcomes in

ECB Working Paper Series No 2623 / December 2021

4

the future.

A remarkable shift in the view on the role of fiscal policy in macroeconomic stabilisation has

materialised already in the aftermath of the GFC. In the policy realm a huge ’multiplier debate’

erupted in 2011 on the effectiveness of fiscal policy after Olivier Blanchard – in his role as chief

economist of the International Monetary Fund – had emphasised that fiscal consolidations may be

self-defeating. The literature rediscovering the role of fiscal policies in macroeconomic stabilisation,

which simply burgeoned since then, pointed out mostly two key points (see Ramey (2019) for a

comprehensive literature survey). First, it underlined that at the lower bound fiscal policy is more

effective than usual (see, e.g. Eggertsson (2011) and Christiano et al. (2011)). Second, it made

clear that fiscal policy might be indispensable for monetary policy to avoid persistent shortfalls of

inflation from its objective at the lower bound (see, e.g. Schmidt (2013) and Corsetti et al. (2019)).

Our paper aims to contribute to this strand of literature by conducting an empirical exercise for the

euro area. While many of the existing studies make use of parsimonious models to highlight key

mechanisms at play our paper aims to conduct the analysis in a realistic data-driven environment

that is closely linked to the prevailing macroeconomic conditions in the euro area (i.e. interest rates

at the ELB, subdued inflation staying persistently below the target and elevated government debt

levels).

This paper attempts to illustrate – through the means of counterfactual scenarios – the im-

plications of different fiscal and monetary policy behaviours, captured by rules, for macroeconomic

outcomes.

1

To this end, we consider the historical pre-pandemic period up to 2019Q4 and a post-

pandemic projection period up to 2030. For the historical period we mostly investigate whether

fiscal policy that avoids procyclicality reduces cyclical fluctuations. As far as the forward-looking

period is concerned, we attempt to identify constellations of policy rules that ensure favourable

macroeconomic outcomes (i.e. no negative output gap and no sizeable inflation shortfalls).

According to the model simulations, consistently countercyclical fiscal policy creates a buffer

in the good pre-GFC times and, subsequently, it has the potential to eliminate a large portion of

the second downturn associated with the euro area sovereign debt crisis. Moreover, it reduces the

1

Fiscal and monetary policy interact in multiple ways. Bassetto and Sargent (2020) emphasise that the separation

between the fiscal and monetary authority tends to be blurred. We maintain a clear separation of monetary and fiscal

authorities and analyse the interactions via the policy rules only.

ECB Working Paper Series No 2623 / December 2021

5

negative inflation gap in recent years without bringing large cost in terms of government debt. These

benefits are conditional on full monetary accommodation.

Regarding the post-pandemic period, our analysis indicate that the combination of an expansionary-

for-longer fiscal policy (i.e. a policy that maintains fiscal support longer beyond the closure of the

standard output gap) and a low-for-longer monetary policy (i.e. a policy that keeps the rates low

for longer compared to a standard Taylor rule) has a chance to significantly improve macroeconomic

prospects. Concretely, this policy constellation recovers around 50% of the accumulated output

losses that materialised amid the pandemic and brings inflation into the territory close to the ECB

target. Reaching such outcomes requires a moderate increase in government debt. Our analysis also

indicates that at the current juncture fiscal and monetary policy reinforce each other and mutually

create space for each other. This provides a strong case for the coordination between the two policies

currently.

We conduct our analysis in a rich macroeconomic environment and our findings illustrate how

conclusions of the academic literature on fiscal policy and its interactions with monetary policy can

be brought closer to policy-making. Most notably, we show that when the interest rate policy is

constrained − until 2024 in our case − fiscal policy becomes an effective tool at the disposal of policy-

makers. While it is necessarily associated with budgetary costs, those are significantly alleviated by

material benefits to both real and nominal developments. This helps to reduce the tension between

the stabilisation needs and fiscal space when debt-to-GDP ratios are high (approaching 100% for

the euro area aggregate in the next years). Moreover and similarly to the literature findings, our

exercise shows that expansionary fiscal policy could support monetary policy. In particular, with

supportive fiscal policy, it would be easier to address the inflation shortfalls persisting in the euro

area rather than with monetary policy tools alone.

Due to the richness of the model specification and the close link to the data, our analysis provides

a higher degree of realism in comparison to existing studies. Notwithstanding this, the modelling

exercise involves several limitations, which should have a bearing on the interpretation of the simula-

tion results. First, the euro area is modelled as a whole, thereby missing country heterogeneity and

other national aspects. This is particularly important because a desirable policy, even if identified,

may not be easily implementable given the incomplete setup of the fiscal architecture of the EMU.

ECB Working Paper Series No 2623 / December 2021

6

Moreover, it is virtually impossible at the aggregate level to reflect fiscal sustainability concerns of

the monetary union as these are driven by single member states. Second, the conducted exercise is

specific to the periods under consideration. For a general ranking of the policy rules, the analysis

should be re-conducted with stochastic simulations around the balanced growth path. Third, the

model does not feature sovereign default and it is therefore not suitable for sovereign stress analysis.

High debt-to-GDP ratios could increase the probability of sovereign stress in euro area Member

States, with a bearing on the cost of refinancing. Fourth, the model is not equipped with a regime

switching to passive monetary policy and active fiscal policy and, as such, is not suitable for study-

ing fiscal dominance. Finally, the lack of model consistent expectations implies that agents in the

economy are not behaving in a Ricardian way. This could lead to an overestimation on the efficacy

of fiscal policy for macroeconomic stabilisation, which is discussed in one of the subsections. In a

related vein, monetary policy cannot rely on the anticipation channel, dampening the efficacy of

monetary policy tools.

The paper is structured as follows. Section 2 describes the model, with a focus on fiscal and

monetary policy rules. Section 3 and 4 contain the historical assessment and the post-pandemic

assessment respectively. Section 5 briefly concludes.

2 Model set-up & specification of the policy rules

The ECB-BASE is a semi-structural macroeconomic model of the euro area, developed for the use

in the macroeconomic projections, as well as for policy simulations (see Angelini et al. (2019) for a

model description). The model features a developed financial block with elaborate monetary policy

channels. Also, the model is characterised by a rich representation of the general government, which

provides for a meaningful role of fiscal policy.

The applied version of the model embeds backward-looking expectations, which tilts the power

from monetary policy to fiscal policy compared to a DSGE model with forward-looking expect-

ations. Backward-looking expectations result in the absence of Ricardian equivalence.

2

In this

context, economic agents do not internalise any future consolidation needs resulting from a fiscal

2

In the situation of economic stress, like during the current COVID crisis, weakening the Ricardian equivalence

may be justified on the grounds that the share of liquidity constrained households is higher than usually.

ECB Working Paper Series No 2623 / December 2021

7

stimulus. Accounting for any anticipated future consolidation would weaken its effects.

3

Similarly,

financial market participants in the model are insensitive to any announced information on the fu-

ture developments in interest rates, or other monetary policy measures known in advance. This

eliminates the power of forward guidance that is present in DSGE models and weakens the potency

of monetary policy make-up rules, which largely work through anticipation channels (see Hebden

et al. (2020) for the analysis of the effects of expectations on monetary policy make-up rules).

The quantitative responses of the ECB-BASE model to macroeconomic shocks are assessed in

Angelini et al. (2019) by benchmarking the model results against comparable models, including

semi-structural and DSGE models. One further reference for assessment can be found in the ’Basic

Model Elasticities’ (BMEs). These BMEs are developed by the National Banks of the Eurosystem

and are used regularly in the forecast exercises. They condense the views of modellers and forecasters

in the Eurosystem on the propagation of macroeconomic shocks.

4

To address a potential criticism

that the model gives too much power to fiscal policy and too little potency to monetary policy we

cross-check the effects fiscal and monetary policy shocks with the BMEs as well. It turns out that

government spending multipliers are broadly consistent with those embedded in the BMEs and the

effects of monetary policy are greater than according to the BMEs.

5

Based on this benchmarking

against reference models, we conclude that the power of the two policies is balanced.

One of the major advantages of the ECB-BASE model is its close link to the current conjunc-

tural developments. The model is firmly anchored not only in the historical data but also in the

Eurosystem projections. In particular, the baseline of the post-pandemic exercise reflects recent

macroeconomic projections.

6

As such, the model takes a comprehensive account of the current

3

The standard RBC/ NK model features infinitely-lived households, whose consumption decisions at any point in

time are based on an intertemporal budget constraint. Ceteris paribus, an increase in government spending lowers

the present value of after-tax income, thus generating a negative wealth effect that induces a cut in consumption.

In this context, standard macroeconomic models feature strong Ricardian effects, which are sometimes at odds with

empirical findings (e.g. Blanchard and Perotti (2002)). Against this background, a vast amount of studies established

models, where the Ricardian effects are weakened (see, for instance, Gali et al. (2007), which added rule-of-thumb

households).

4

The BMEs have been developed in the context of the Eurosystem projections and they summarise the effects of

changes in assumptions (including fiscal and financial assumptions) on macroeconomic variables. They can be inter-

preted as a simplified version of the macroeconomic models used by National Central Banks for economic projections.

As such, they constitute a benchmark for the assessment of fiscal and monetary policy in a macro model. ECB (2016)

provides details on BMEs and their application in the projections.

5

The comparison of policy effects cannot be shown in this paper on account of the fact that the BME elasticities

are not made available to the public.

6

The baseline of the post-pandemic horizon exercise presented in the paper is broadly in line with the December

ECB Working Paper Series No 2623 / December 2021

8

environment with low interest rates, inflation persistently staying well below the target and large

negative output gaps amid the COVID crisis.

2.1 Baseline specification of fiscal and monetary policy

With a view to comprehensively reflecting government accounts, fiscal policy in the ECB-BASE

involves multiple instruments. This applies to both the revenue and spending side of the budget.

Single instruments are in most of the cases modelled with Error Correction Mechanism (ECM)

equations appended with the output gap and deviations of the debt ratio from its target. These two

terms represent the stabilisation and sustainability components of fiscal policy.

In the context of this paper, the three following spending categories are used as primary fiscal

instruments: government transfers, purchases and investment.

7

The choice is motivated by the

observation that the changes in outlays within these items observed in the past were sufficiently large

to influence the evolution of the output gap. This stands in contrast to, for instance, government

compensation which exhibits exceptionally stable dynamics in the data (see Figure A.1 in Appendix).

Moreover, all the three selected categories involve some characteristics of discretionary spending.

Given this we the three fiscal instruments as suitable for macroeconomic stabilisation purposes.

Specifically, the spending instruments considered in this paper evolve in line with Eq. 1. The

formula stipulates that actual spending (g

t

) converges towards its trend and, in addition, responds

to cyclical fluctuations as well as to deviations of the debt-to-GDP ratio from its target.

∆g

t

= α

g

t−1

− g

T

t−1

+ δ∆g

T

t

+

2

X

k=1

ρ

k

∆g

t−k

+ γ

Y

ˆ

Y

t

+ γ

B

B

t

¯

Y

t

P

t

−

¯

b

+ ε

G

t

(1)

where g

t

is log of actual spending, g

T

t

is log of trend spending,

ˆ

Y

t

is the real output gap,

B

t

¯

Y

t

P

t

is

the debt ratio to nominal output,

¯

b is the debt-to-GDP ratio target and ε

G

t

is the residual term.

8

2020 macroeconomic projection (see ECB (2020) for the results), to the extent that macroeconomic variables are

made available to the public. The estimates of potential GDP, which are crucial for the analysis and which are not

published by the ECB, come from the European Commission’s Economic Forecast (Spring 2021).

7

To avoid complexity, we limit our investigation of fiscal rules to the spending side of the budget. In general,

government expenditures are characterised by a higher output multiplier compared to taxes as it affects output more

directly. In this context, government spending may be seen as more suitable for output stabilisation than taxes.

8

Fiscal rules in the ECB-BASE are broadly consistent with those in DSGE models with elaborate fiscal policy (see,

for instance, Coenen et al. (2013)). In addition, the inclusion of trend and lags in the equation ensures a good data

fit.

ECB Working Paper Series No 2623 / December 2021

9

The coefficients entailed in the spending rules are estimated, summarising the average behaviour of

fiscal policy over the entire sample. This also applies to the coefficient on the output gap, which

represents the cyclicality of fiscal policy. Given the contrasting nature of the euro area fiscal policy

(i.e. countercyclical amid the GFC and procyclical thereafter) the estimated coefficients turn out to

be very small (see Table A.1 for exact values). This points to little reaction of fiscal policy to the

cycle on average embedded in the baseline fiscal rules.

Turning to monetary policy, the short-term interest rate follows a standard Taylor rule that

accounts for the ELB. The rule builds upon an empirical version of Taylor (1999), describing the

interest rate setting outside the constrained area.

R

t

= max

h

0.85R

t−1

+ 0.15

r

∗

+ ¯π

t

+

ˆ

Y

t

+ ( ¯π

t

− π

∗

)

, −0.5

i

+ ε

R

t

(2)

where R

t

denotes the nominal short term interest rate, r

∗

is the equilibrium real interest rate, ¯π

t

is

the average annual inflation rate, π

∗

denotes the 2% target, and

ˆ

Y

t

is the output gap.

9

The effective

lower bound is imposed at -50 basis points.

In addition to the standard interest rate rule, the effects of non-standard policies, in particular

asset purchases, are approximated via interest rate add-ons on short-term expectations and long-

term rates. This constitutes an indirect approach to account for the non-negligible effects of APP

and PEPP on the risk premium and on expectations. To this end, the paper takes as given the

existing estimates of the effect of quantitative easing on the yield curve (see Eser et al. (2019)). In

order to include these effects into the simulation a simple rule is specified. This rule defines the

add-ons as a function of the inflation gap, that is only activated if interest rates are in negative

territory (see Eq. 3 and 4).

R

add,ST

t

= 0.99R

add,ST

t

+ 1 [R

t

≤ 0] 0.01 ( ¯π

t

− π

∗

) + ε

R

add,ST

t

(3)

R

add,LT

t

= 0.95R

add,LT

t

+ 1 [R

t

≤ 0] 0.05 ( ¯π

t

− π

∗

) + ε

R

add,LT

t

(4)

9

We base the values for the past unobserved natural rate in the euro area on Holston et al. (2017). Going forward

we assume that the value remains around zero as indicated by some of the estimates in Brand et al. (2018).

ECB Working Paper Series No 2623 / December 2021

10

Subsequently, these values are used to adjust the term premium of the long-term rates and VAR-

based expectation formation through the short-term rate. By incorporating into the analysis the

data on long-term interest rates, forward guidance is partly reflected in the baseline.

10

The analysis in this paper is based on the model under VAR expectations.

11

VAR expectations

assume only limited knowledge of the joint dynamics of the variables and they correspond to the

same restricted information set used in the estimation of the model. Specifically, the VARs share a

core set of macro variables: the policy rate, the GDP deflator, and the output gap. This design can

be interpreted as a limited form of rational expectations. The system of the core VAR variables is

augmented by the specific variable for which expectations are being formed. We label this form as

backward looking expectations because the information set for forming expectations is containing

only contemporaneous and past variables.

More precisely the setup of the VAR used for forming the expectations is:

∆z

t

= Λ

0

(z

t−1

− z

∗

t−1

) +

P

K

k=1

Λ

k

∆z

t−k

(5)

where z

t

is a vector of variables containing inflation, the level of the interest rate and the output gap,

Λ

0

is a matrix containing coefficients that control how the variables respond to the deviation of the

lagged level from the long-term attractors, Λ

k

are matrices that collect autoregressive coefficients for

K lags. There are two different cases how expectations enter into the model. For the price and wage

equations the expectations of the t + h-quarter variable is based on rolling the VAR forward. For

variables inside the PAC specification, the VAR defines the information set to map into the desired

level of the target variable.

12

10

Backward-looking expectations of the model do not allow for analysing the effects of forward guidance in a

commensurate way.

11

Similarly to the FRB/US model, the ECB-BASE can technically allow for two alternative ways of forming the

expectations of different agents. Specifically, expectations can be either based on projections from an estimated

small-scale auxiliary VAR model (i.e. VAR or limited information expectations) or consistent with a full knowledge

of the dynamics of the model (i.e model-consistent or rational expectations). The latter case assumes that agents

are fully rational and their expectations are based on the solution of the model under the assumption that also the

expected variables follow the internal logic of the model. Rational expectations are sometimes criticised as being overly

optimistic on the assumption that agents have a complete understanding of the economy and base their expectation

on this understanding.

12

Angelini et al. (2019) contains an in-depth description of the expectation formation process in the ECB-BASE.

ECB Working Paper Series No 2623 / December 2021

11

2.2 Alternative fiscal policy and monetary policy rules

We define the rule with the estimated coefficients as the baseline, which turns out to be broadly

neutral (i.e. acyclical) to the cycle. A first counterfactual rule is then defined as a rule that decisively

reacts to real economic developments in a countercyclical fashion. Such a rule has its natural limit,

once the real output gap closure is achieved. After deep recessions with lasting inflation shortfalls,

it might still be warranted to keep fiscal stimulus in place. To address this limitation we introduce

further rules based on an augmented output gap, which deviates from the standard gap only when the

policy rate hits the ZLB. We label rules of this type as expansionary-for-longer fiscal policy because

they provide fiscal support for longer, beyond the point when the output gap closes. Such fiscal

policy rules constitute an analogy to low-for-longer monetary policy rules, which provide monetary

support beyond what is suggested by a standard Taylor rule.

The exact specification of the countercyclical fiscal rules is as follows (see Eq. 6).

∆g

t

= α

g

t−1

− g

T

t−1

+ δ∆g

T

t

+

2

X

k=1

ρ

k

∆g

t−k

+ γ

Y

ˆ

Y

t

+ γ

B

B

t

¯

Y

t

P

t

−

¯

b

+ ε

G

t

(6)

where γ

Y

<< 0. In fact, what makes the countercyclical fiscal rule distinct from an estimated fiscal

rule (see Eq. 1) is the size of the coefficient on the output gap, which in the case of the latter is

close to zero.

13

The first approach to implement expansionary-for-longer fiscal policy is based on the substitution

of the real output gap by the nominal output gap – the nominal approach. This means that the real

output gap is augmented by a price gap, computed as cumulative inflation deviations over time. The

second approach relies on augmenting the standard output gap with past negative output gaps – the

real approach. This implies that policy-makers rather than being concerned only about closing the

contemporanous output gap attempt to also compensate additionally for past output shortfalls.

14

There are multiple reasons for fiscal policy to consider not only the real but also the nominal

13

Given the complexity of the spending rules the interpretation of γ

Y

may not be straight-forward. The value used

in the analysis for government purchases is equal to -0.1 which is a value that ensures a sizeable, albeit still plausible,

fiscal expansion (see Figure 13 for the exact amounts of additional expenditure associated with various scenarios).

The coefficient values for other instruments (i.e. social transfers and government investment) are rescaled accordingly

so that a fiscal expansion is evenly distributed across the three instruments used in the analysis.

14

This might be considered in cases where protracted shortfalls lead to hysteresis or scarring effects which are not

fully reflected in the level of the output gap.

ECB Working Paper Series No 2623 / December 2021

12

developments in policy setting. First, nominal income, and not only real income, is a relevant

variable perceived by economic agents, thereby constituting the basis for their business decision

making. Second, it is nominal income that is relevant for debt sustainability – one of the main

concerns for a fiscal authority. Third, the price dynamics embedded in the nominal concept may

improve the understanding of the current state of the business cycle given material uncertainty about

the unobservable real output gap (see for example Jarociński and Lenza (2018)). Finally, a fiscal

authority responding only to real developments and the monetary authority reacting solely to price

dynamics may result in the divergence of policy courses. The aim to coordinate, will necessarily

involve policy rules based on similar variables (i.e. see, for instance, Bianchi et al. (2020) suggesting

a common strategy for fiscal and monetary policy in the current environment).

Importantly, such a formulation does not call for any shift of responsibility between monetary

and fiscal authorities. With policy rates at the ELB monetary policy may not be able to ensure

adequate dynamics on the nominal side. In such a situation fiscal policy, supported by favourable

financing conditions, remains an effective macroeconomic tool. In a situation characterised by a

closed output gap and still subdued price dynamics, nominal output gap targeting on the fiscal side

could contribute to excess demand and higher prices simultanously. It would deliver some make-up

for the large output losses experienced in the euro area both during the great recession and amid

the COVID crisis.

Turning to the real approach, expansionary-for-longer fiscal policy can also be achieved by con-

sidering past negative real output gaps when the interest rate is at the ZLB. This specification can

be mostly motivated by the desire to recover at least some of the significant output losses that

materialised during severe crises (e.g. amid the GFC or the COVID crisis). Our model baseline

indicates that cumulative output losses with respect to potential GDP are reaching around 15%

of GDP, which is undeniably a sizeable figure (see Figure 5). The case for recovering past output

losses is particularly strong in the presence of hysteresis effects, which stipulates that grave output

shortfalls affect potential GDP.

15

In such an environment, a period of excess demand could help to

address some of these adverse effects, thereby preserving potential capacity of the economy. This

15

Permanent damage to a potential output following a cyclical recession can materialise through a number of

channels such as labour force, capital stock and productivity. Cerra et al. (2020) contains a review of the related

literature.

ECB Working Paper Series No 2623 / December 2021

13

may be the case currently when the COVID crisis brings massive disruptions to economic activity.

16

Formally, the expansionary-for-longer fiscal rules can be described by the following equation

∆g

t

= α

g

t−1

− g

T

t−1

+ δ∆g

T

t

+

2

X

k=1

ρ

k

∆g

t−k

+ γ

Y

ˆ

Y

t

aug,i

+ γ

B

B

t

¯

Y

t

P

t

−

¯

b

+ ε

G

t

(7)

where γ

Y

<< 0 remains like in the countercyclical fiscal rules. The specification of

ˆ

Y

t

aug,i

depends

on whether we consider the nominal (i = nom; see Eq. 8) or the real (i = real; see Eq. 9) approach.

It is crucial to emphasise that the augmenting terms, which cumulate the inflation deviations in

the case of

ˆ

P

t

or output shortfalls in the case of

ˆ

Y

t

add

embed a memory loss (see the details on

Appendix Section B). Varying the degree of it is useful to demonstrate how expansionary-for-longer

fiscal policy gains strength in macroeconomic stabilisation.

17

ˆ

Y

t

aug,nom

=

ˆ

Y

t

+ 1 [R

t

≤ 0]

ˆ

P

t

(8)

ˆ

Y

t

aug,real

=

ˆ

Y

t

+ 1 [R

t

≤ 0]

ˆ

Y

t

add

(9)

Turning to monetary policy, the paper considers three alternative policy rules which embed

various degrees of monetary accommodation. These rules stipulate average inflation targeting with

an averaging windows of different length. As such, the rules take into account the accumulated

inflation deviations over the corresponding time windows. Given the persisting negative inflation

deviations, the rules imply additional monetary accommodation (i.e. keeping rates low for longer)

compared to the standard Taylor rule at the current juncture.

18

For this reason, we label the regimes

implied by these alternative rules as low-for-longer monetary policy.

Concretely, the rules feature inflation gaps based on 2-year, 3-year and 4-year averaging windows.

The specification of the rules is consistent with the study by Arias et al. (2020) prepared for the

16

IMF (2021) points to significant scarring effects to global output in the medium term as a result of the pandemic.

17

Without any memory loss the price gap becomes very large given the persistent inflation shortfalls in recent years.

The large size makes the gap hardly usable as an indicator in a policy rule.

18

The readiness of a policy-maker to cool the economy because of a realised inflation overshooting may be different

from the readiness to stimulate the economy because of realised inflation shortfalls. To reflect this, some studies,

like Arias et al. (2020), consider asymmetric average inflation rules, where the make-up strategy only applies to past

inflation shortfalls. In our analysis this is the case even with the symmetric rules because the inflation have been

recording negative deviations in the data.

ECB Working Paper Series No 2623 / December 2021

14

discussion of the Federal Reserve’s review of monetary policy strategy.

19

Formally the rule for a

T-year average inflation targeting follows Eq. 10 with ¯π

t

(T −year )

being the T-year average inflation.

R

t

= max

h

0.85R

t−1

+ 0.15

r

∗

+ ¯π

t

+

ˆ

Y

t

+ T

¯π

t

(T −year )

− π

∗

, −0.5

i

+ ε

R

t

(10)

2.3 Criteria for assessing the rules

Having specified fiscal and monetary policy rules for the analysis it is equally important to lay out

criteria used for their assessment. By contrast to many papers in the academic literature, we do not

attempt to identify optimal rules for fiscal and monetary policy (see Benigno and Woodford (2003))

for a single economy and Kirsanova et al. (2007) for a monetary union as examples of studies).

Instead, we consider rules that are commonly accepted in the policy-making world and extend them

along several dimensions as explained in Subsection 2.2. The modifications are motivated by the

desire to improve realised or projected macroeconomic outcomes, such as high output volatility or

persisting inflation shortfalls.

In contrast to the existing literature based on parsimonious theoretical models, we do not assess

the rules with a single welfare-based loss function (see the derivation for a simple NK model in Gali

(2015)). ECB-BASE is not rigorously micro-founded and consequently, does not feature an explicit

welfare measure. Specifying a loss function in this context would necessarily require additional

assumptions, such as weighting the typical loss function variables.

20

We focus, instead, on a set of variables that are relevant to policy-makers and will allow them to

judge the rules with a cost-benefit approach. In line with the chosen policy rules, we use output gap

and inflation. In addition to this we analyse the policy variables themselves and variables that are

informative about the cost of stabilisation. For monetary policy, these are the short-term interest

rate and the ZLB duration. For fiscal policy, these are the budget balance-to-GDP ratio and the

government debt-to-GDP ratio. To condense the findings of the simulations we do not only offer

graphical presentation of the above mentioned variables but also summarise them in heat maps for

19

The average inflation targeting rules in Arias et al. (2020) rely on 4-year and 8-year averaging windows. We

consider shorter horizons for the sake of realism.

20

Hauptmeier and Kamps (2020), for instance, in their assessment of selected fiscal rules assume that a fiscal

authority follows a quadratic loss function consisting of the output gap and government debt-to-GDP deviations. The

aggregation of the two terms requires choosing υ parameter (where 0 < υ < 1), which represents the preference of a

fiscal authority to stabilise the business cycle relative to debt sustainability.

ECB Working Paper Series No 2623 / December 2021

15

the post-pandemic scenario (see Figure 11, 12 and 13.)

3 Historical perspective

The analysis of fiscal policy in this section is based on counterfactual scenarios conducted around

the historical sample from 2003 to 2019. Through the lens of the ECB-BASE model we attempt to

illustrate how various fiscal policies affect the business cycle under two different configurations of

monetary policy.

21

The first set of simulations assumes that monetary policy does not react to any

changes brought by the alteration of the fiscal rules and remains the same as observed in the data. In

the second step, the monetary policy reaction becomes endogenous with the central bank following a

standard Taylor rule. Eventually, by turning to stochastic simulations we generalise the illustration

by considering uncertainty. The analysis remains agnostic on whether the fiscal policy implied by

the considered fiscal rules was implementable given past financial and political conditions.

3.1 Fiscal rules with exogenous monetary policy

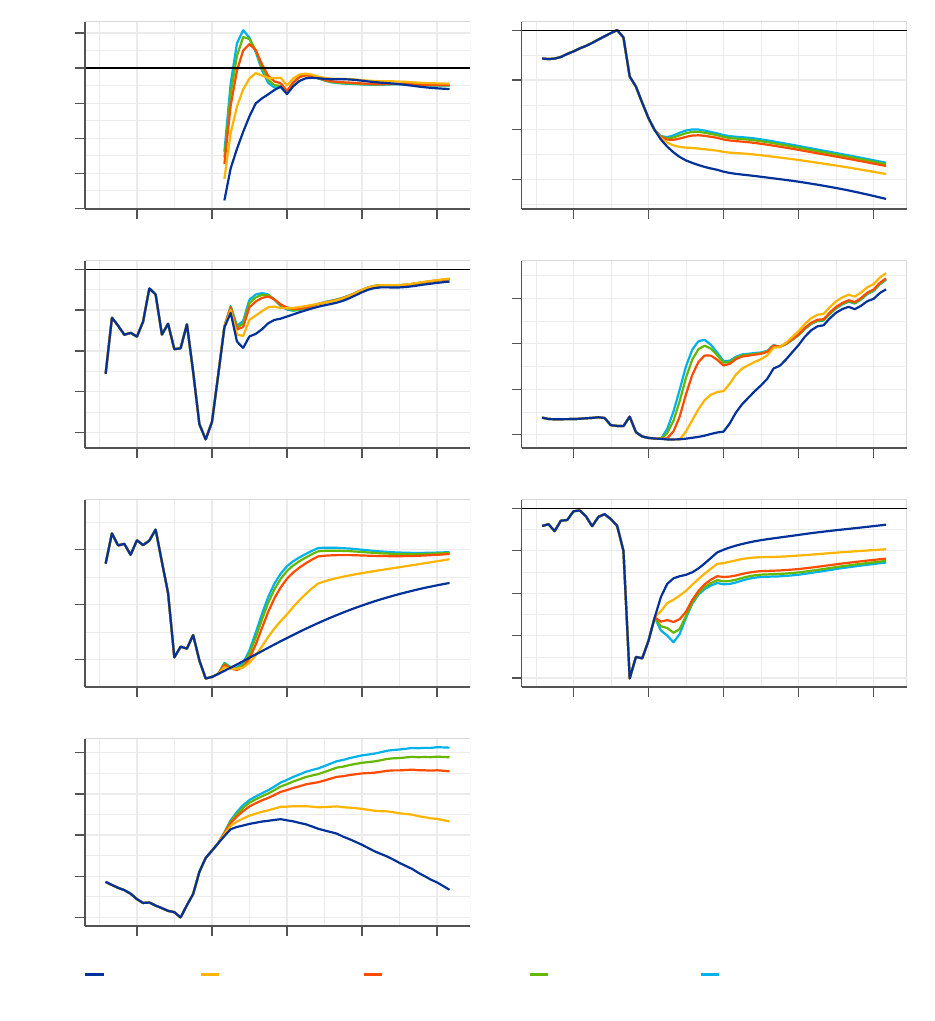

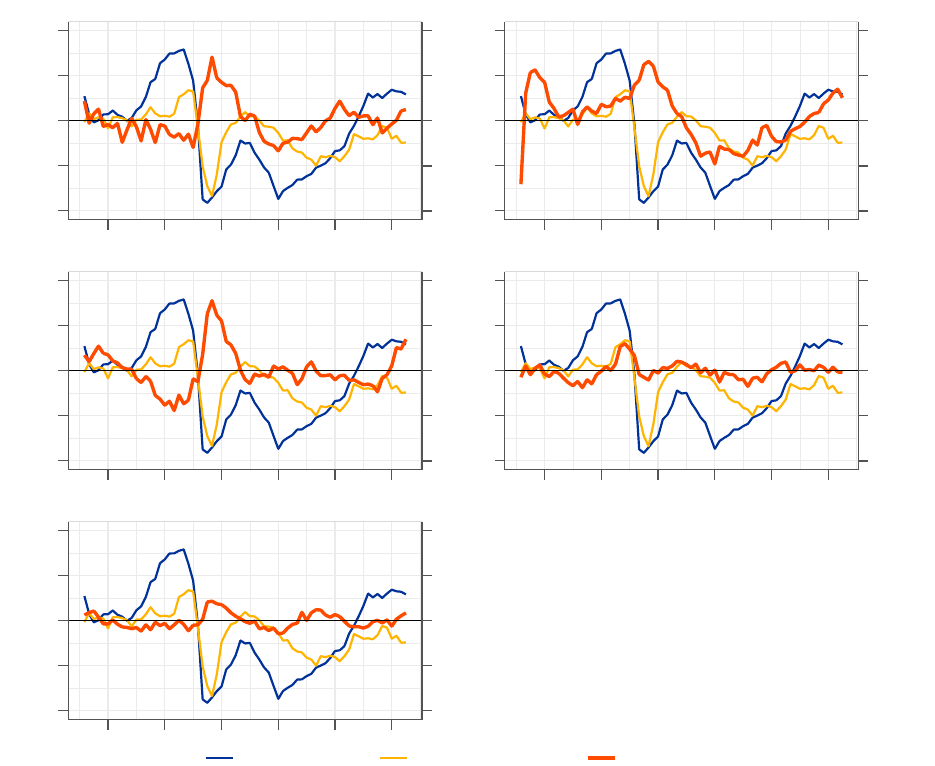

According to the model simulations, the alternative fiscal rules substantially smooth the real out-

put gap and slightly reduce the inflation gap without causing a surge in the government debt. A

systematically countercyclical policy (see Figure 2, Countercyclical rule) reduces the output gap

fluctuations significantly. Initially, the spending retrenchment imposed by the rule during the good

pre-crisis times dampens the positive output gap noticeably. Afterwards, a supportive fiscal policy

that sharply reacts to the downturns facilitates the post-GFC recovery and alleviates the gravity of

the second downturn. While the inflation benefits are non-negligible during the post-GFC period,

the inflation rate still remains far from the target for an extended period of time given the large size

of the recorded shortfalls.

Scenarios with expansionary-for-longer fiscal rules (see Figure 2, Expansionary-for-longer I, II,

III rules) bring additional stimulating effects. The countercyclical fiscal rule that reacts to the

standard output gap stops providing support with the output gap closure in late 2016. This is the

moment when the expansionary-for-longer fiscal policy starts making a sizeable difference providing

21

One crucial assumption underlying the simulations is that all shocks/ residuals in the model remain unchanged

compared to those associated with the realised data.

ECB Working Paper Series No 2623 / December 2021

16

support beyond the output gap closure. Fiscal policy under these rules constitutes an option to

further diminish the accumulated output losses amid the two crisis episodes or to support inflation

dynamics. This, however, requires a prolongation of the fiscal stimulus well beyond the sovereign

debt crisis, which is associated with a considerable overheating of the economy in recent years. In

fact, the implementation of the expansionary-for-longer rules more than overcompensates for the

accumulated output losses towards the end of the sample with inflation still not being firmly on

target.

Judging by the evolution of the debt-to-GDP ratio in the various scenarios, sizeable benefits of

expansionary-for-longer fiscal policy come at only limited cost under the assumption of full monetary

accommodation. Increases in debt as a share of potential GDP associated with the alternative fiscal

policies are small. The investigated fiscal rules first lead to savings prior to the GFC, thereby building

a small fiscal buffer. Afterwards, supportive fiscal policies, even the expansionary-for-longer versions,

yield substantial benefits to both real and nominal sides, which significantly alleviates the cost of the

increased expenditures. With policy rates being unresponsive, monetary policy keeps the servicing

cost of the sovereigns debt low. It also provides an additional accommodation, in the sense of

keeping rates unchanged against the background of higher output and inflation. The findings of

the simulations heavily rely on the assumption that policy-makers know in real time the current

estimates of the output gap and are able to adjust policies accordingly. Given the extent of the

revisions to the output gap, accurate fiscal policy fine-tuning is very difficult in practice.

ECB Working Paper Series No 2623 / December 2021

17

Figure 2: Historical counterfactual simulations of various fiscal rules with exogenous monetary policy

-2

0

2

2003 2006 2009 2012 2015 2018

Output Gap (% of Pot. GDP)

-10

-5

0

5

2003 2006 2009 2012 2015 2018

Cum. Output Loss wrt 02Q1 (% of Pot. GDP)

-1

0

1

2

3

2003 2006 2009 2012 2015 2018

Inflation (%)

0

1

2

3

4

5

2003 2006 2009 2012 2015 2018

Interest Rate (%)

0

1

2

3

4

5

2003 2006 2009 2012 2015 2018

10Y long-term rate (%)

-8

-6

-4

-2

0

2003 2006 2009 2012 2015 2018

Budget Balance (% of Pot.

GDP)

65

70

75

80

85

90

2003 2006 2009 2012 2015 2018

Gov. Debt (% of P

ot. GDP)

Estimated Countercyclical Exp.-for-longer I Exp.-for-longer II Exp.-for-longer III

Sources: ECB-BASE simulations.

Notes: "Estimated" fiscal rule reproduces the observed data. The expansionary-for-longer fiscal rules presented in

the context of the historical exercise are formulated on the basis of the nominal approach. Rules bringing equivalent

outcomes can be devised following the real approach (see the demonstration for the post-pandemic horizon, Subsection

4.2).

ECB Working Paper Series No 2623 / December 2021

18

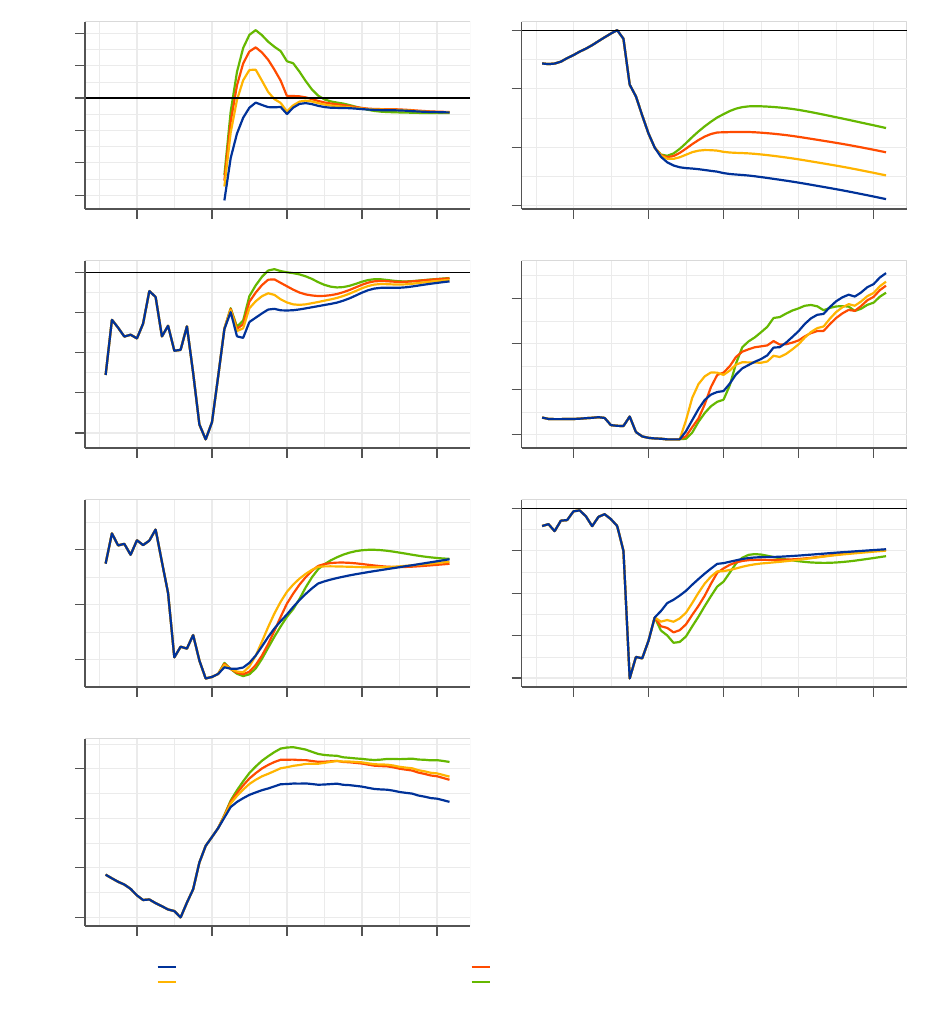

3.2 Fiscal rules with endogenous monetary policy

The sizeable macroeconomic effects of fiscal policy in Subsection 3.1 are conditional on fully accom-

modative monetary policy. The assumption of exogenous monetary policy implies that the central

bank undertakes the same measures as observed in the past irrespective of inflation and output gap

outcomes. Relaxing this assumption, namely that the central bank reacts to more positive macroe-

conomic outcomes brought by an alternative fiscal policy (for instance, by following a Taylor rule)

may be seen as more realistic and it changes the picture materially.

The simulations indicate that for the efficacy of fiscal rules full accommodation of monetary

policy is crucial. In a configuration with endogenous monetary policy, the central bank responds

to the macroeconomic developments according to the Taylor rule. Prior to the GFC, the policy

rate in the simulations remains below the baseline. Subsequently, given the improved economic

conditions, the rate is above baseline and remains there also during the second downturn. The

monetary policy reaction has substantial consequences for the efficacy of the investigated fiscal rules

in our simulations. More concretely, the extent to which fiscal policy reduces output gap fluctuations

is more limited compared to the case with full monetary accommodation (see Figure 3). None of

the fiscal rules eliminates the crisis-related accumulated output losses at the end of the simulation

horizon. Moreover, virtually no gains from the alternative fiscal policy rules are visible for inflation.

With fiscal support in place the monetary policy rate reaches the ELB significantly later than

in the data (i.e. in late 2017 rather than in mid-2015). In this context, the alternative fiscal rules

create ample room for monetary policy. The expansionary-for-longer fiscal rules start making a

difference only during the last part of the simulation period. This is because the activation of

the augmented gap is conditional on the central bank being at the ZLB (see the explanations in

Subsection 2.2). In this context, there are no substantial changes to government expenditure and

no material implications for economic outcomes compared to the countercyclical rule.

Endogenous monetary policy also affects the size of fiscal cost of the alternative fiscal rules. Prior

to the crisis, interest rates are lower than observed in the data, therefore contributing to the build-up

of a fiscal buffer. Following the GFC this tendency is reverting, however. The less accommodative

stance of monetary policy gradually increases the servicing cost of government debt. This, together

with additional expenditure and limited macroeconomic benefits, brings the debt-to-GDP ratio to

ECB Working Paper Series No 2623 / December 2021

19

levels noticeably exceeding the observed values.

ECB Working Paper Series No 2623 / December 2021

20

Figure 3: Historical counterfactual simulations of various fiscal rules with endogenous monetary

policy following a standard Taylor rule

-2

0

2

2003 2006 2009 2012 2015 2018

Output Gap (% of Pot.

GDP)

-10

-5

0

5

2003 2006 2009 2012 2015 2018

Cum. Output Loss wrt 02Q1 (%

of Pot. GDP)

-1

0

1

2

3

2003 2006 2009 2012 2015 2018

Inflation (%)

-1

0

1

2

3

4

5

2003 2006 2009 2012 2015 2018

Interest Rate (%)

0

1

2

3

4

5

2003 2006 2009 2012 2015 2018

10Y long-term rate (%)

-5.0

-2.5

0.0

2003 2006 2009 2012 2015 2018

Budget Balance (% of Pot. GDP)

70

80

90

100

2003 2006 2009 2012 2015 2018

Gov. Debt (% of Pot. GDP)

Estimated Countercyclical Exp.-for-longer I Exp.-for-longer II Exp.-for-longer III

Sources: ECB-BASE simulations.

Notes: "Estimated" fiscal rule reproduces the observed data. The expansionary-for-longer fiscal rules presented in

the context of the historical exercise are formulated on the basis of the nominal approach. Rules bringing equivalent

outcomes can be devised following the real approach (see the demonstration for the post-pandemic horizon, Subsection

4.2).

ECB Working Paper Series No 2623 / December 2021

21

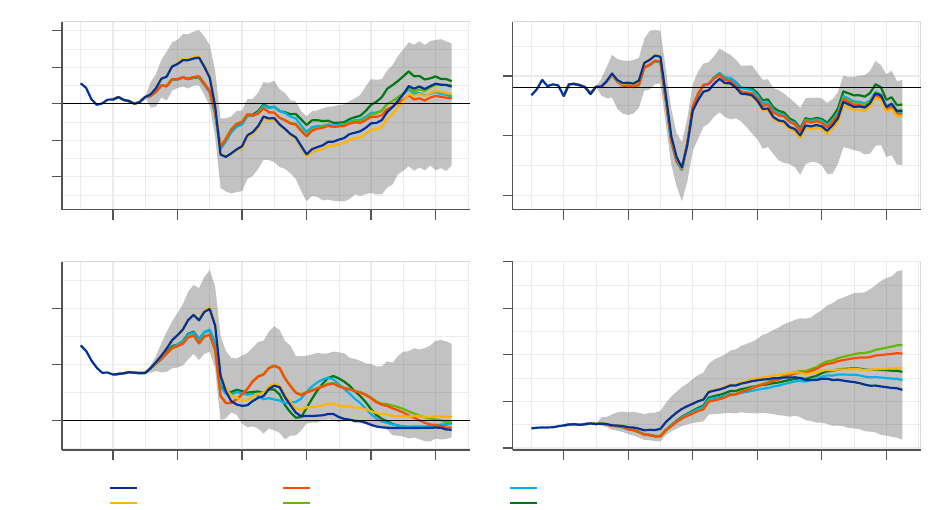

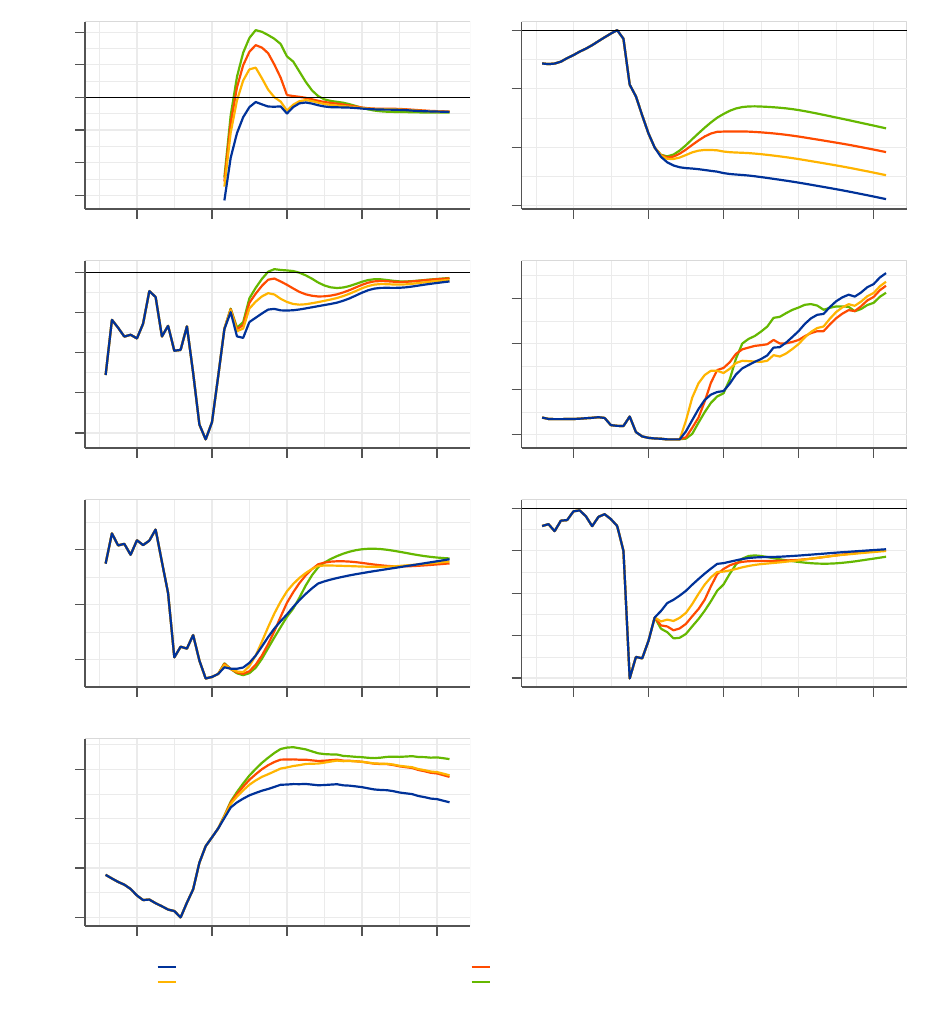

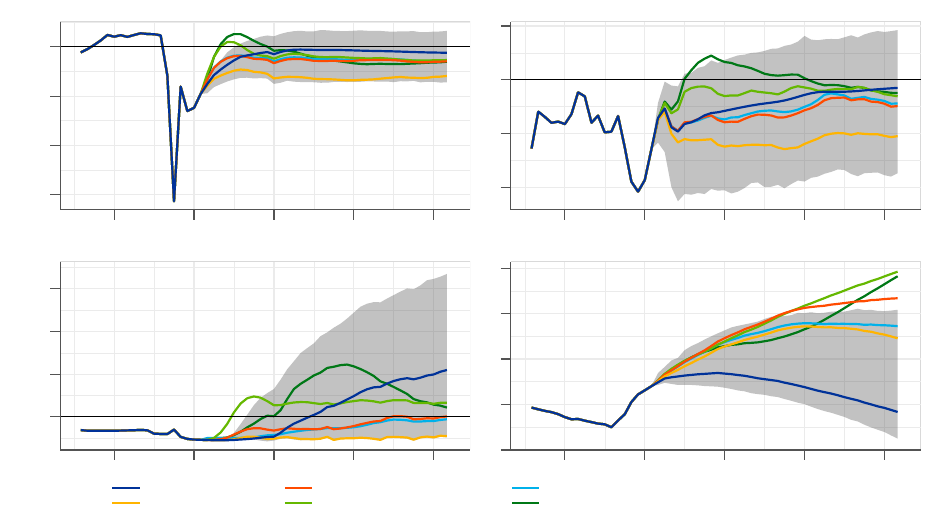

The deterministic simulation presented hitherto evaluate the policy mix in a ceteris paribus

environment assuming that all shocks and residuals remain at the values identified by inverting

the baseline model. One way to evaluate the robustness of the results is to conduct stochastic

simulations. By drawing from model residuals and repeating the simulations multiple times the

analysis incorporates the effects of uncertainty and possible model misspecifications.

22

The depicted

means of the stochastic distributions under the counterfactual policy experiments show a picture

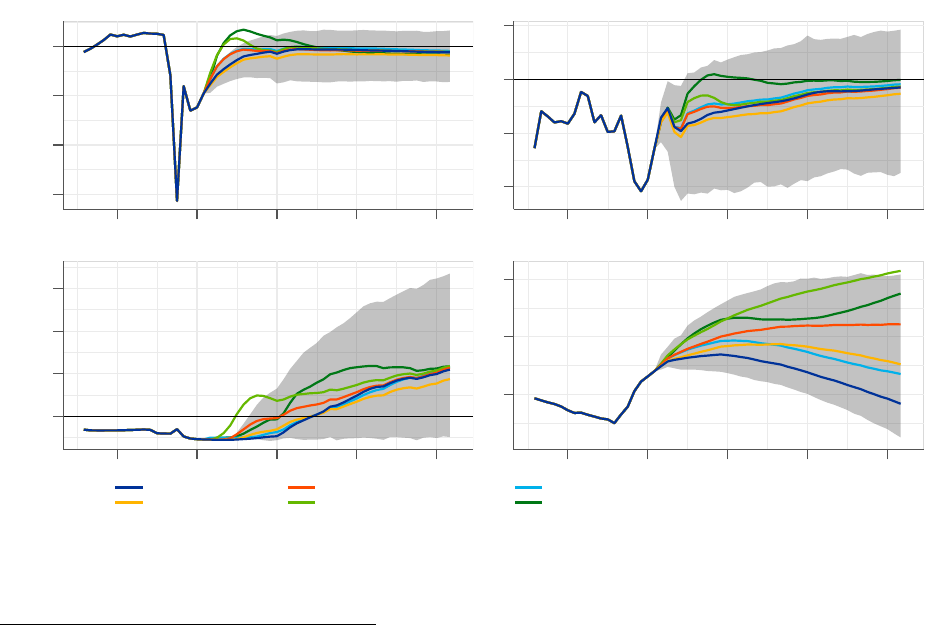

consistent with the counterfactual scenarios described above (see Figure 4; more details on stochastic

simulations, including the occurrences of risk events, is given in Section 4). The differences between

stochastic means across various scenarios very much resemble those of the deterministic simulations.

The property that the means of the stochastic simulations are situated below the deterministic

simulation is due to existence of the ELB. For those paths, where the interest rate is constrained by

the ELB, particularly negative paths for output and inflation are more frequently observed. This

induces a negative bias in the distribution of output and inflation. Non-standard monetary policy

dampens the negative outcomes but it cannot fully compensate for the lack of the interest rate

instrument during ELB episodes. In this environment, alternative fiscal rules improve the outcomes

significantly when it comes to the output gap (see Figure 4, the difference between the blue/ yellow

lines and the other lines) and inflation.

22

The residuals of the equations capture the part of the observed variables that cannot be explained by the structure

of the equations.

ECB Working Paper Series No 2623 / December 2021

22

Figure 4: Stochastic simulations of various fiscal and monetary policy rules

-5.0

-2.5

0.0

2.5

5.0

2004 2007 2010 2013 2016 2019

Output Gap (% of Pot. GDP)

-2.5

0.0

2.5

2004 2007 2010 2013 2016 2019

Inflation (%)

0.0

2.5

5.0

2004 2007 2010 2013 2016 2019

Interest Rate (%)

60

80

100

120

140

2004 2007 2010 2013 2016 2019

Gov. Debt (% of Pot. GDP)

Baseline

TR & Estimated

TR & Countercyclical

TR & Exp.-for-longer II

Low-for-longer II & Coun

tercyclical

Low-for-longer III &

Exp.-for-longer III

Sources: ECB-BASE simulations.

Notes: The confidence bands are based on stochastic simulations with the baseline policy rules. The bands are based

on 2.5% and 97.5% percentiles. The alternative rules are presented by the mean of the stochastic simulations to

maintain readability.

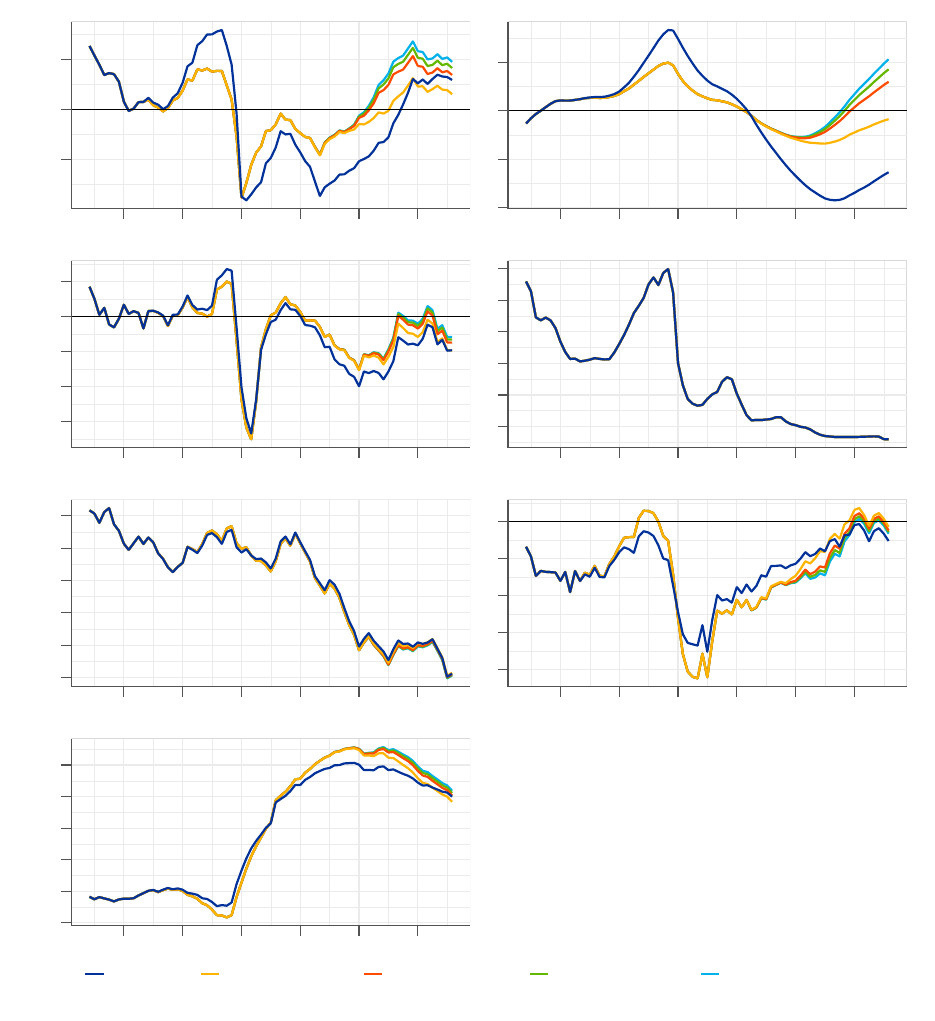

4 Post-pandemic perspective

By conducting simulations over an extended horizon until 2030, we investigate how different con-

figurations of fiscal and monetary policy affect the expected medium-term macroeconomic outlook.

The starting point for the exercise is the construction of a reference baseline with fiscal and monet-

ary policy rules that are consistent with the existing institutional arrangements and the dynamics

observed in the past (i.e. the estimated fiscal rules and the Taylor rule specified in Subsection 2.1).

Subsequently, we vary the rules (for both fiscal and monetary policy) and assess how their different

combinations perform relative to the baseline.

The reference baseline is broadly consistent with the Eurosystem projections (the December 2020

exercise, see ECB (2020) for the results). We complement the set of projected variables published

ECB Working Paper Series No 2623 / December 2021

23

by the ECB, which does not include the potential output, with the potential output of the European

Commission. The projected variables are reproduced by the model until the end of their forecast

horizon (i.e. end-2023 for the Eurosystem and end-2022 for the European Commission). Afterwards

the figures are model-based.

To construct post-2023 baseline we use information contained in the model residuals. Rather

than imposing zero residuals in the calculations the residual in-sample information is considered.

Specifically, it is assumed that residuals consist of a systematic and idiosyncratic component. The

former is derived from an auxiliary state space model and used for the post-2023 simulation (the

appendix of Angelini et al. (2019) contains a description of the methodology). This approach greatly

improves the realism of the medium-term baseline compared to the approach based on zero residuals.

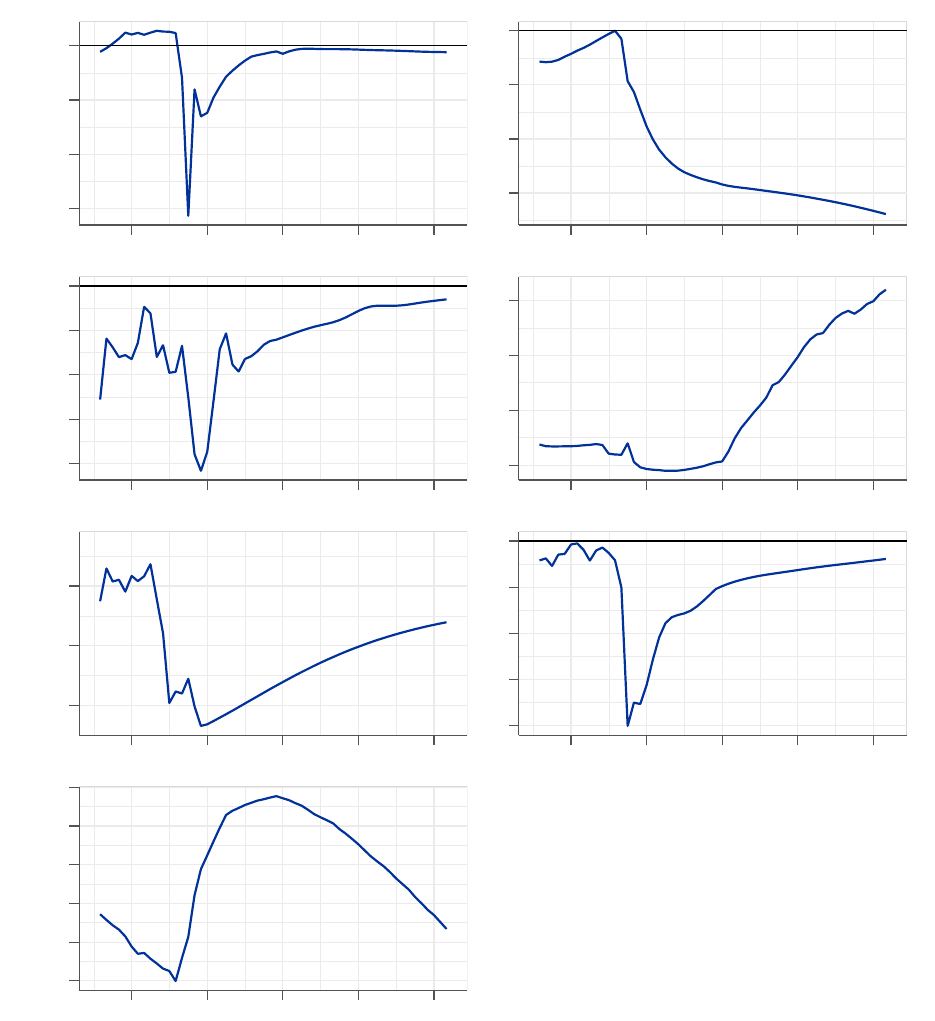

In the baseline the output gap is nearly closed already within the Eurosystem forecast horizon

and remains close to zero thereafter (see Figure 5). The narrowing of the inflation gap with respect

to the 2% target occurs at significantly lower speed in comparison to the closure of the output gap.

The short-term interest rate remains at the ELB until the end of the Eurosystem forecast horizon

and then lifts off following the Taylor rule. Public finances normalise gradually, following the grave

consequences of the COVID crisis. Specifically, the budget balance-to-GDP ratio converges towards

a balanced position and the debt-to-GDP ratio starts falling, albeit from an elevated level.

ECB Working Paper Series No 2623 / December 2021

24

Figure 5: Medium-term reference baseline

-15

-10

-5

0

2018 2021 2024 2027 2030

Output Gap (% of Pot. GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (% of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot.

GDP)

85.0

87.5

90.0

92.5

95.0

97.5

2018 2021 2024 2027 2030

Gov. Debt (% of P

ot. GDP)

Sources: ECB-BASE simulations.

Notes: The baseline presented above is broadly consistent with the Eurosystem projections for the variables that are

made available to the public (see ECB (2020)). The output gap, which is not published, is based on the potential

output of the European Commission (Spring 2021 Economic Forecast). In the post-forecast period the figures are

model-based.

ECB Working Paper Series No 2623 / December 2021

25

4.1 Fiscal and monetary policy rules in isolation

Before analysing combinations of the rules, we look at the effects of fiscal and monetary policy rules

in isolation. This means that a change to fiscal rules and its macroeconomic consequences will be

ignored by monetary policy (i.e. monetary policy is exogenous and kept at its baseline values).

Similarly, when analysing monetary policy rules, we assume no reaction from the side of fiscal policy

(i.e. fiscal policy exogenous). While this set-up is hardly realistic it helps to understand the economic

impact of fiscal and monetary policy alone without mixing the policies and their effects.

Fiscal policy rules can significantly alter the macroeconomic outcomes compared to the baseline.

In particular, a countercyclical fiscal policy stimulates output leading to a very fast output gap

closure and it lifts inflation by a non-negligible margin (see Figure 6). The expansionary-for-longer

fiscal rules bring inflation back to target still within the projection horizon. At the same time, they

significantly reduce the cumulative output gap losses. This involves, however, a sizeable amount

of additional stimulus compared to the baseline as indicated by the deterioration in the budget

balance. Moreover, it also necessitates the tolerance of overheating the euro area economy (output

gap reaching 2% of GDP in the coming years). While the additional stimulus does increase the

debt-to-GDP ratio in a few years’ time it does not raise it in the medium term in 2030.

ECB Working Paper Series No 2623 / December 2021

26

Figure 6: Post-pandemic simulations of various fiscal policy rules in isolation.

-4

-2

0

2

2018 2021 2024 2027 2030

Output Gap (% of Pot. GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (% of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot.

GDP)

85

90

95

100

2018 2021 2024 2027 2030

Gov. Debt (% of P

ot. GDP)

Estimated Countercyclical Exp.-for-longer I Exp.-for-longer II Exp.-for-longer III

Sources: ECB-BASE simulations.

Notes: "Estimated" fiscal rule reproduces the reference baseline presented in Figure 5.

ECB Working Paper Series No 2623 / December 2021

27

Model simulations also reveal that interest rate rules can alter the expected paths for macroeco-

nomic variables, albeit only to a limited extend.

23

Both real output and inflation improve slightly

with more accommodative monetary policy rules (see Figure 7). The reason for limited gains lies in

the limited monetary policy space in the baseline. In this context, the additional rules that we con-

sider make a relatively small difference. The short-term interest rate in the outer years is lower only

by a maximum of around 0.7 percentage point. Furthermore, with backward-looking expectations

in the model there is no expectation channel of monetary policy. In contrast to forward-looking

models, only the realised changes in interest rates matter but not the expected path of interest rates

in the future. In the simulations, the non-standard monetary policy is modelled through add-ons

(see the description in Subsection 2.1) which are kept endogenous. For a complete assessment of the

role of monetary policy, the impact of forward guidance would need to be included.

23

The investigation of monetary policy rules in isolation involves shutting down the reaction of fiscal policy. This

still involves an active fiscal block (i.e. no exogenisation of the entire fiscal block). In particular, changes in tax

bases translate into corresponding changes in tax revenue. Moreover, all fiscal identities, including the budget balance

and debt accumulation remain fully operational. In practice, shutting down the reaction of fiscal policy does not

materially change the outcomes compared to the estimated fiscal rules, which embed very little reaction to the cycle

(as discussed in Subsection 2.1).

ECB Working Paper Series No 2623 / December 2021

28

Figure 7: Post-pandemic simulations of various monetary policy rules in isolation

-3

-2

-1

0

2018 2021 2024 2027 2030

Output Gap (% of Pot. GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (% of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot.

GDP)

85

90

95

2018 2021 2024 2027 2030

Gov. Debt (% of P

ot. GDP)

TR Low-for-longer I Low-for-longer II Low-for-longer III

Sources: ECB-BASE simulations.

Notes: "TR" monetary rule reproduces the reference baseline presented in Figure 5.

ECB Working Paper Series No 2623 / December 2021

29

4.2 Combinations of fiscal and monetary policy rules

To have a realistic assessment of the effectiveness of the two policies we run simulations under

endogenous fiscal and monetary rules. We start with the analysis of various fiscal rules where the

monetary policy reacts in a usual manner following a standard Taylor rule.

The gains from fiscal policy rules combined with a standard monetary policy reaction, that is not

providing any further accommodation, are limited. While alternative fiscal rules initially provide a

significant boost to real activity and to prices the effect is short-lived (see Figure 8). This is because

the standard Taylor rule promptly reacts to the macroeconomic improvements. As such, the benefits

of fiscal policy are eliminated by an ‘uncooperative’ monetary policy tightening. Furthermore,

interest rate increases lead to a situation in which the governments face higher financing costs, which

gradually propagate into the overall debt servicing cost. This brings detrimental consequences for

the debt-to-GDP ratio and makes the fiscal policy very costly.

ECB Working Paper Series No 2623 / December 2021

30

Figure 8: Post-pandemic simulations of various fiscal rules with endogenous monetary policy follow-

ing the standard Taylor rule

-4

-3

-2

-1

0

1

2018 2021 2024 2027 2030

Output Gap (% of Pot.

GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (%

of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot. GDP)

85

90

95

100

105

2018 2021 2024 2027 2030

Gov. Debt (% of Pot. GDP)

Estimated Countercyclical Exp.-for-longer I Exp.-for-longer II Exp.-for-longer III

Sources: ECB-BASE simulations.

Notes: "Estimated" fiscal rule reproduces the reference baseline presented in Figure 5.

ECB Working Paper Series No 2623 / December 2021

31

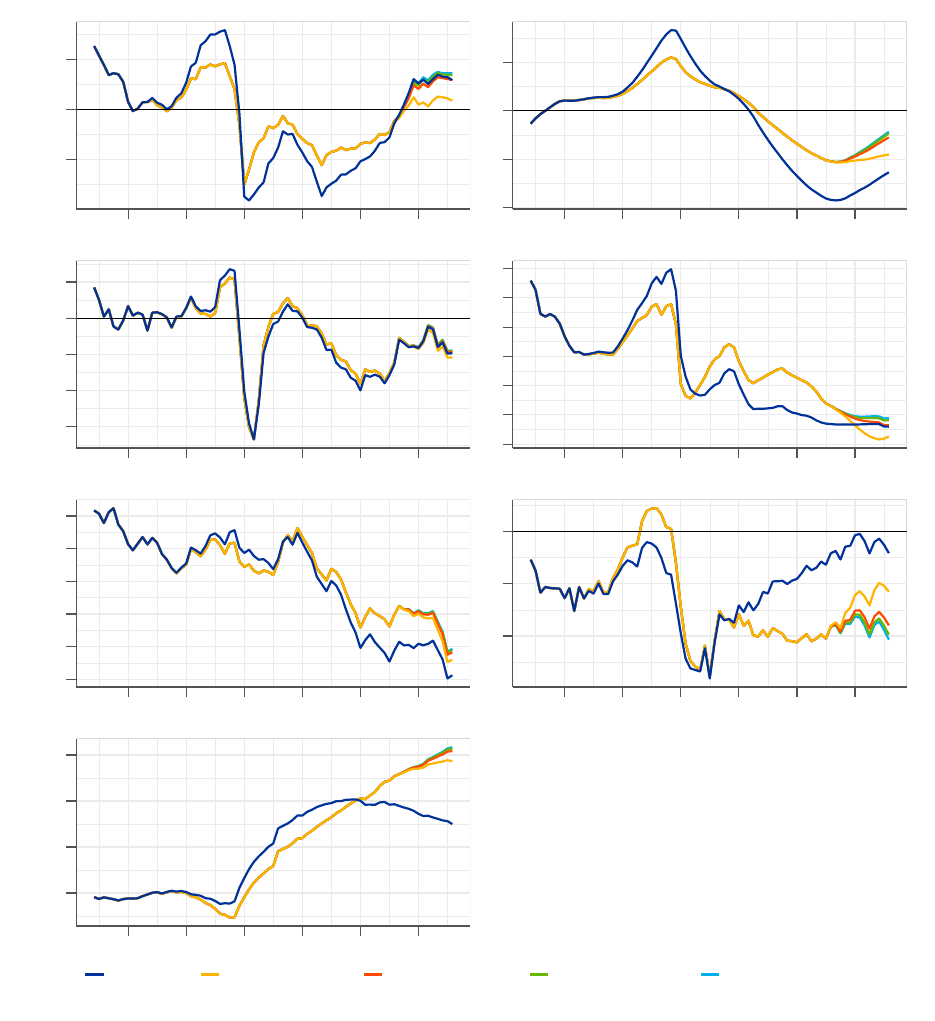

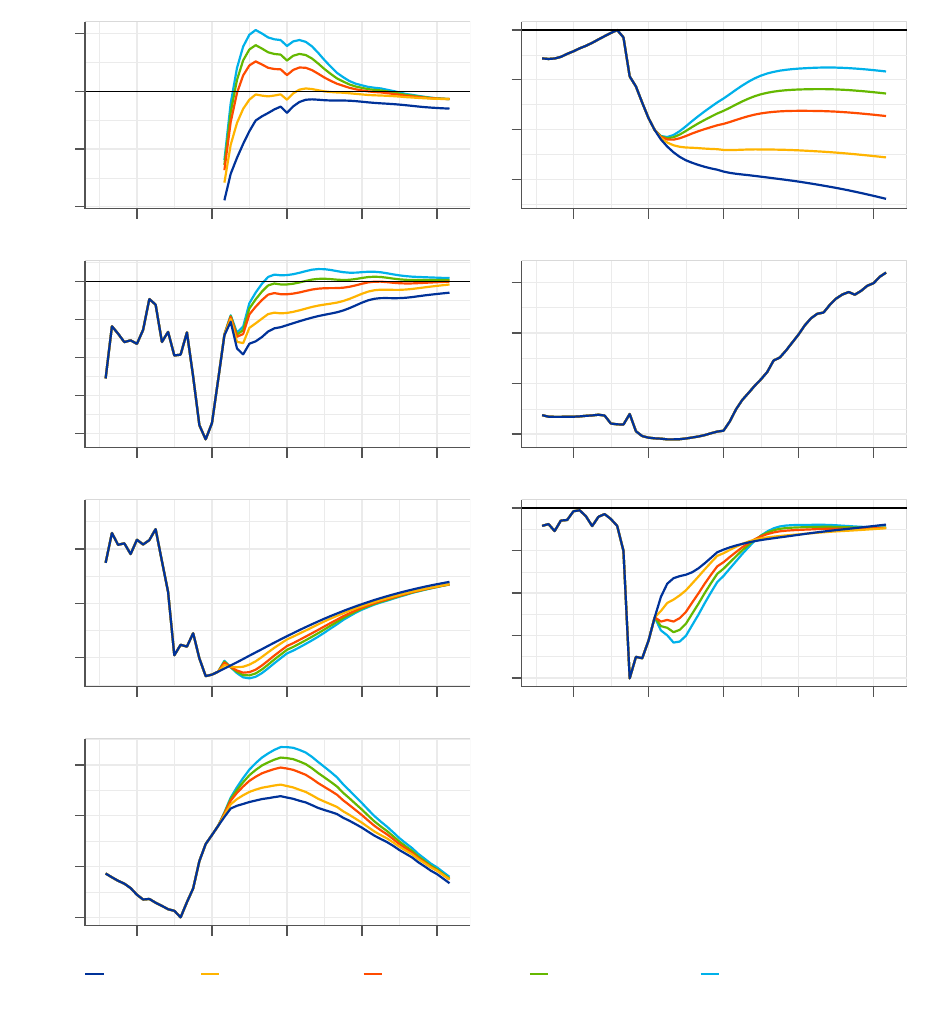

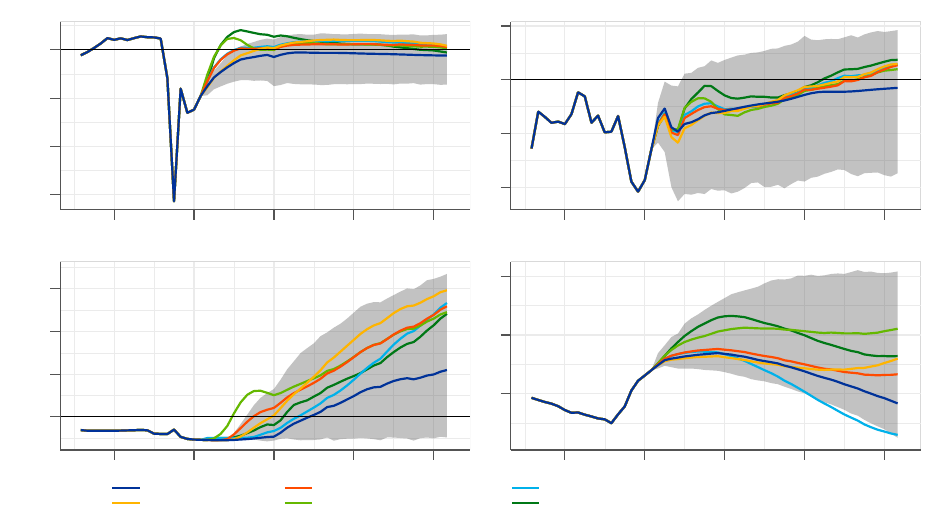

To uncap the potential of fiscal policy, more accommodative monetary policy rules are essential.

With monetary policy still reacting but working in concert with fiscal policy the macroeconomic

benefits are significantly more tangible.

24

Fiscal policy can provide a significant boost to output

and inflation when monetary policy delivers additional accommodation in parallel (see Figure 9 and

10). In our illustration, monetary policy, in contrast to the standard Taylor rule reaction, does

not fight back the benefits of fiscal policy but rather tries to create favourable conditions for it by

lifting the rates only gradually. This makes the macroeconomic gains of fiscal policy sizeable and

long-lasting. However, only with a considerable additional spending and significant overheating of

the economy, a combination of expansionary-for-longer fiscal policy and low-for-longer monetary

policy has a chance to bring inflation close to the 2% target during the simulation horizon. This

scenario halves the output losses accumulated amid the COVID crisis. Also, no sharp monetary

policy tightening means no abrupt increases of the financing cost for the governments. This makes

the application of fiscal policy significantly less costly compared to the situation in which the central

bank strictly follows the standard Taylor rule.

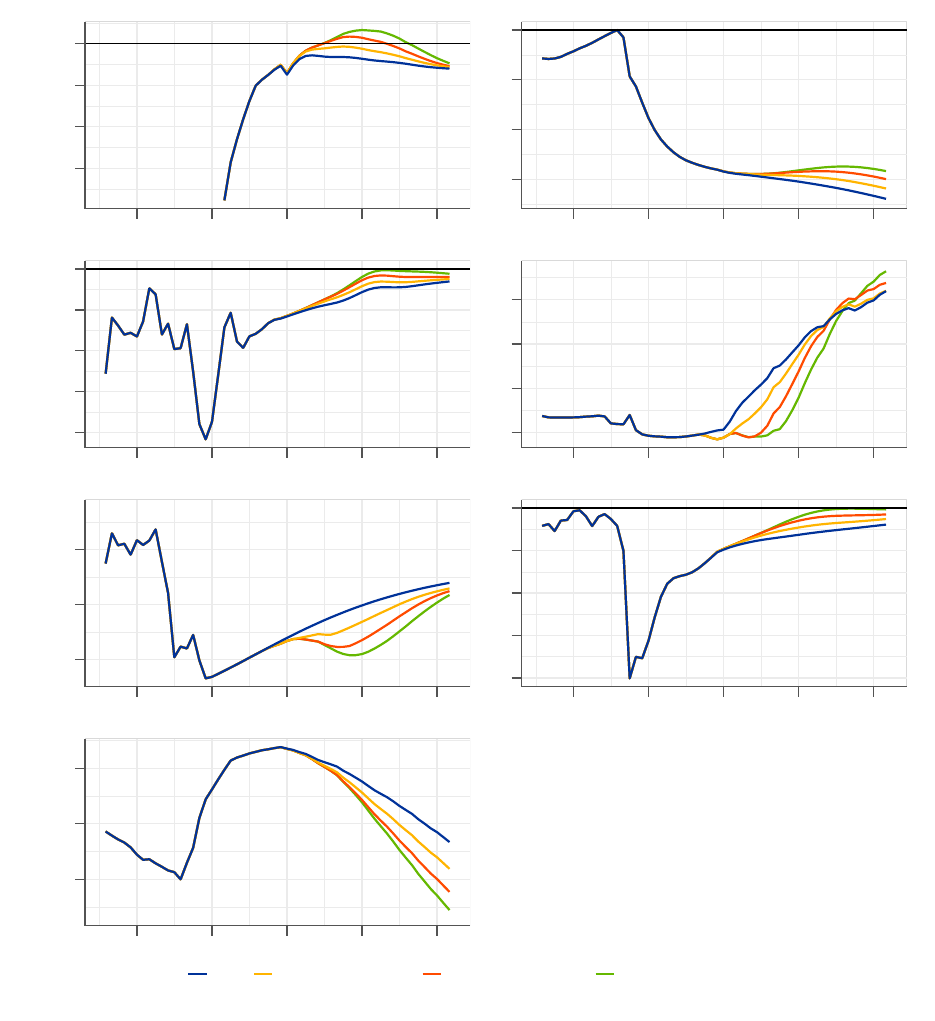

Both formulations of expansionary-for-longer fiscal policy (i.e nominal and real approach) bring

virtually the same macroeconomic outcomes (compare Figure 9 and Figure 10). In this context, a

fiscal authority does not need to choose between the two specifications. Rather it needs to make a

choice how to communicate an expansionary-for-longer fiscal policy. The nominal-based specification

explicitly acknowledges the role of fiscal policy in reaching the inflation target at the time when the

central bank is constrained. The real-based specification emphasises the objective to recover some of

the output losses. At the current juncture both aims coincide and require the same course of fiscal

policy.

24

The lack of any monetary policy reaction could be interpreted as a case of subordination of monetary policy to

the needs of fiscal policy or fiscal dominance. In the analysis we do not consider this theoretical constellation as it

remains at odds with the prevailing institutional arrangement.

ECB Working Paper Series No 2623 / December 2021

32

Figure 9: Post-pandemic simulations of fiscal and monetary policy rules working in concert

(expansionary-for-longer fiscal policy specified following the nominal approach)

-3

-2

-1

0

1

2

2018 2021 2024 2027 2030

Output Gap (% of Pot.

GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (%

of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot. GDP)

85

90

95

100

2018 2021 2024 2027 2030

Gov. Debt (% of Pot. GDP)

TR & Countercyclical

Low-for-longer I & Exp.-for-longer

I

Low-for-longer II & Exp.-for-longer II

Low-for-longer III &

Exp.-for-longer III

Sources: ECB-BASE simulations.

ECB Working Paper Series No 2623 / December 2021

33

Figure 10: Post-pandemic simulations of fiscal and monetary policy combinations working in concert

(expansionary-for-longer fiscal policy specified following the real approach)

-3

-2

-1

0

1

2

2018 2021 2024 2027 2030

Output Gap (% of Pot.

GDP)

-15

-10

-5

0

2018 2021 2024 2027 2030

Cum. Output Loss wrt 19Q4 (%

of Pot. GDP)

0.0

0.5

1.0

1.5

2.0

2018 2021 2024 2027 2030

Inflation (%)

-0.5

0.0

0.5

1.0

2018 2021 2024 2027 2030

Interest Rate (%)

0.0

0.5

1.0

2018 2021 2024 2027 2030

10Y long-term rate (%)

-10.0

-7.5

-5.0

-2.5

0.0

2018 2021 2024 2027 2030

Budget Balance (% of Pot. GDP)

85

90

95

100

2018 2021 2024 2027 2030

Gov. Debt (% of Pot. GDP)

TR & Countercyclical

Low-for-longer I & Exp.-for-longer

I

Low-for-longer II & Exp.-for-longer II

Low-for-longer III &

Exp.-for-longer III

Sources: ECB-BASE simulations.

ECB Working Paper Series No 2623 / December 2021

34

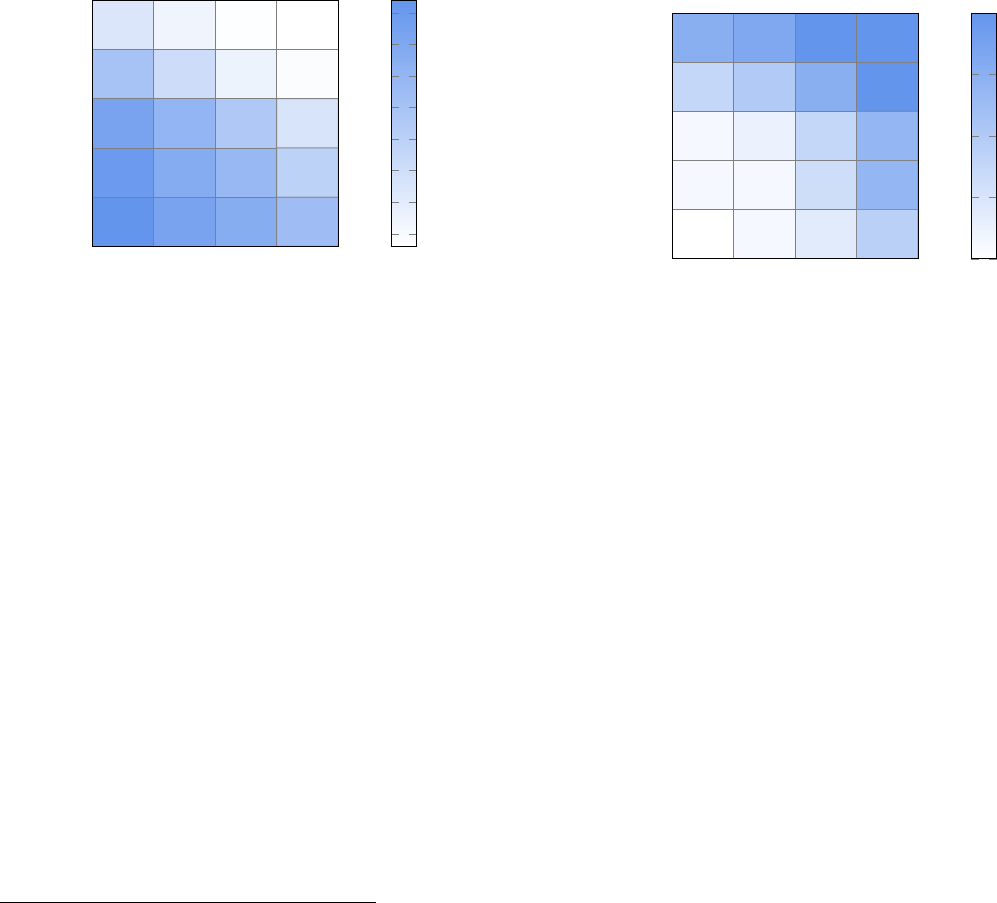

Figure 11: The effects of various combinations of fiscal and monetary rules on output gap and

inflation

(a) Output gap

(% of GDP, 2021q3-25q4 average)

TR

Lo

w-for-longer I

Lo

w-for-longer I

I

Low-for-longer I

II

Estimated

Countercyclical

Exp.-for-longer I

Exp.-for-longer II

Exp.-for-longer III

−1.06 −1 −0.98 −0.98

−0.58 −0.49 −0.43 −0.41

−0.32 −0.14

0.13 0.32

−0.27 −0.06

0.27 0.61

−0.23

0.01 0.36 0.78

Monetary Policy

Fiscal Policy

−1

−0.6

−0.2

0.2

0.6

(b) Inflation

(%, 2021q3-25q4 average)

TR

Lo

w-for-longer I

Low-for-longer II

Lo

w-for-longer III

Estimated

Countercyclical

Exp.-for-longer I

Exp.-for-longer II

Exp.-for-longer III

1.37 1.38 1.39 1.39

1.48 1.51 1.52 1.53

1.53 1.58 1.65 1.7

1.54 1.59 1.68 1.77

1.54 1.61 1.7 1.8

Monetary Policy

Fiscal Policy

1.4

1.5

1.6

1.7

1.8

Sources: ECB-BASE simulations.

Notes: The intersection of the estimated fiscal rule (Estimated) and the Taylor monetary policy rule (TR) corres-

ponds to the baseline. Comparing the outcomes to the baseline is a way to assess the effectiveness of various policy

constellations.

A more detailed look at all simulation scenarios reveals that monetary policy uncaps the potential

of fiscal policy. The more accommodative monetary policy is, the higher are the output gains

associated with fiscal rules (see Figure 11, subfigure (a), vertical gains are bigger for Expansionary-

for-longer III scenario compared to TR scenario). The positive average output gap of 0.8% of GDP

associated with the most favourable policies compares to -1.1% of GDP in the baseline and implies

around 8% of additional output by end-2025. This addresses the large cumulative output losses that

arose amid the COVID crisis. Similarly, inflation benefits most from the alternative fiscal rules under

the most accommodative monetary policy arrangement (see Figure 11, subfigure (b)). Concretely,

while the average inflation can benefit from the most expansionary-for-longer fiscal policy by less

than 0.2 percentage points under the Taylor rule arrangement the gains exceed 0.4 percentage points

under the most accommodative low-for-longer monetary policy. With this outcome the inflation

reaches 1.8% on average, which is closest to the target among all constellations we consider in our

analysis.

ECB Working Paper Series No 2623 / December 2021

35

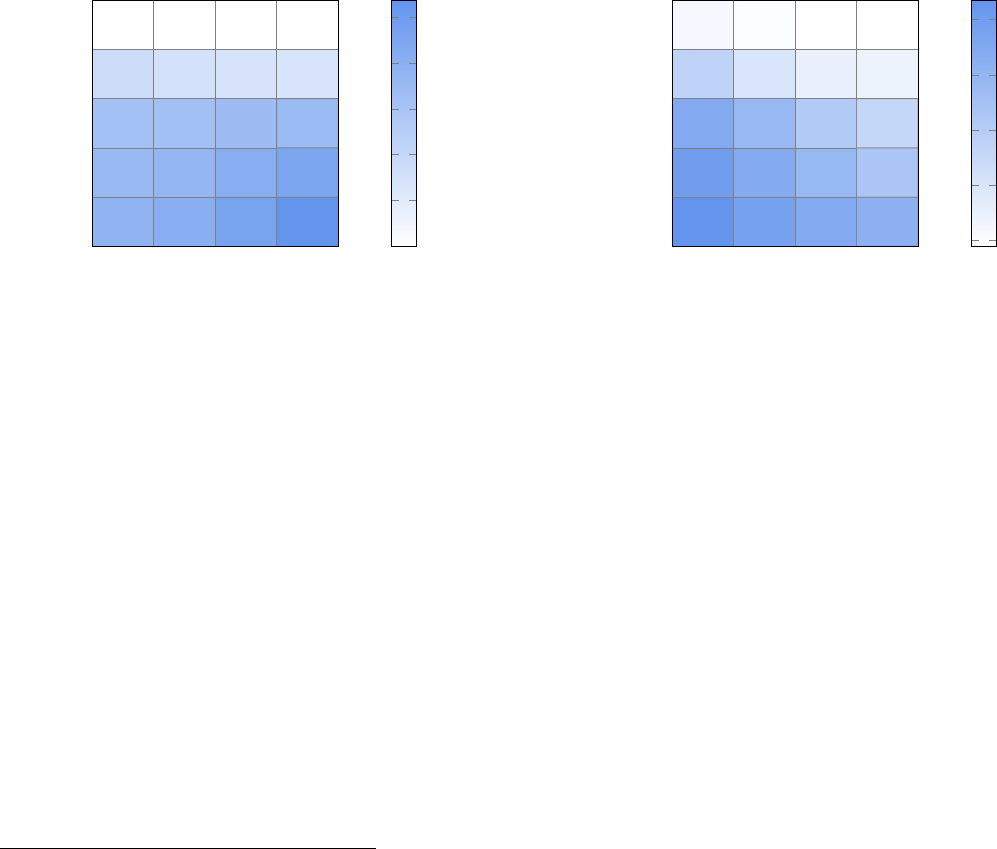

It is not only that monetary policy uncaps the potential of fiscal policy but also fiscal policy

makes monetary policy more powerful. While the potency of monetary policy in the absence of

expansionary-for-longer fiscal policies is relatively limited (see Figure 11, subfigures (a) and (b)