1

Fiscal Analysis and Forecasting Workshop

Bangkok, Thailand

June 16 – 27, 2014

L1

–

Macroeconomic and Financial

Implications of Fiscal Policy

Mangal Goswami

STISTI

IMF-TAOLAM training activities are supported by funding of the Government of Japan

Introduction: what is fiscal policy?

Fiscal policy is the use of government spending

and taxation to affect the economy (allocation of

resources, production, distribution of income)

Macroeconomic

stability & growth

ObjectivesObjectives

Income

f

2

stability

&

growth

• Revenues

• Expenditures

• Financing

Income

redistribution and

social safety nets

Prov

i

s

i

on o

f

public goods

This training material is the property of the International Monetary Fund and is intended for the use in Institute for Capacity Development (ICD)

and Fiscal Affairs Department (FAD) courses. Any reuse requires the permission of ICD and FAD.

2

Introduction: macro stability & growth

Internal balance: adjust aggregate demand to supply:

Fiscal contraction (spending cuts, tax increases) to slow inflation,

reduce current account deficit

Fiscal expansion (tax cuts, spending increases) to address recession,

help restore demand and achieve potential GDP

External balance: promote sustainable saving / investment

balance and borrow externally on a sustainable way

Economic growth: provide infrastructure, health, education,

implement structural reforms

3

Achieving policy objectives requires coordinating FP with

monetary, exchange rate, and structural policies

Outline

1. Economic effects of fiscal policy

2. Fiscal effects of macroeconomic conditions

3. Optimal fiscal policy for output stabilization

4. Fiscal accounts and fiscal targets

4

3

Part 1

Part

1

Economic Effects

of Fiscal Policy

5

Fiscal policy and GDP

GDP = C + I + G + X - M

Fiscal policy affects GDP:

• Directly through G

• Indirectly through C (taxes, expectations), I (interest rates,

confidence), X and M (demand for imported goods, the

effect of fiscal policy on the exchange rate)

6

Fiscal policy affects C, I, X, and M. There are different

theories on how fiscal policy affects GDP once all the effects

on other variables are considered.

4

Effects on GDP: the Keynesian view (I)

Since Keynes, fiscal policy has been recognized as a useful tool

for affecting aggregate demand (ISLM-BP framework)

i

E

LM

BP

i

0

7

Y

0

IS

Y

Effects on GDP: the Keynesian view (II)

Under Keynesian view, fiscal policy for output

stabilization/control is:

Fixed EX rate Flexible EX rate

High K mobility Very effective Less effective

Low k mobility Less effective Very effective

8

Effectiveness of FP also depends upon:

• Is the economy at full capacity

• Type of budgetary finance – debt or money

• How coordinated are fiscal and monetary policy?

5

Effects on GDP: neo-classical view

The government faces an inter-temporal budget constraint:

11

GT

GT

rr

an increase in spending today (G) requires that the government

lower future spending (G’), or raise future taxes (T’)

Ricardian equivalence proposition:

• rational agents anticipate that a tax cut today will be paid off

in the future:

11

rr

9

• rational agents smooth their consumption and saving now to

pay off future taxes

Under what circumstances fiscal policy retains its effectiveness?

Start with definition of Gross National

Disposable Income (GNDI)

Recall that GDP = C + I + X - M

TR: net transfers (gifts)

TR:

net

transfers

(gifts)

YF: net factor income, labor and capital (receipts

minus payments)

GNDI GDP YF TR

10

Net Factor Net

Income Transfers

GNP GNI

6

Notice the following key macro relationship:

GNDI = C + I + X – M + YF + TRF

or GNDI = C + I + CAB

or CAB = GNDI - C – I

= S - I

11

Policy implications

Domestic

Domestic

I

() 0GNDI C I CAB

Policy Implications

o Domestic demand > income requires external

financing and more external debt

o

If imprudent it may be impossible to finance

I

ncome

Demand

o

If

imprudent

it

may

be

impossible

to

finance

o Reducing current account deficit may require fiscal

tightening and possible exchange rate action

12

7

Decompose GNDI, C and I into private and government

components:

GNDI Y Y

Fiscal policy and the external sector (I)

[][]

[][]

pg

pg

ppp ggg

SS

pp gg

GNDI Y Y

CAB Y C I Y C I

CAB S I S I

13

Private Sector Gap Public Sector Gap =

(Revenue - Expenditure)

Fiscal policy affects the current account through:

o Direct impact through demand

o Impact through the real exchange rate

o Impact on interest rates and country premia

Fiscal policy and the external sector (II)

Expansionary fiscal policy may lead to increase in interest rates,

capital inflows, and appreciation of currency

In general a larger fiscal deficit corresponds to a worse savings

In

general

,

a

larger

fiscal

deficit

corresponds

to

a

worse

savings

—investment balance (weaker current account)

CAB identity is an ex-post identity, behavioral relationships must

to be taken into account:

• reducing transfers that are fully saved leads to a one-to-

one decrease in private savings: the CAB does not improve

ddfdl

14

• re

d

ucing spen

d

ing on

f

oreign goo

d

s causes

l

ower output

contraction than if reducing spending on domestic goods

• a fiscal expansion may crowd out I

p

or increase savings if

the private sector is Ricardian (little evidence of this)

8

Financial consequences of fiscal policy (I)

The macroeconomic consequences of the deficit depends in part

on the way it is financed. There are four forms of financing:

• Borrowing abroad

• Borrowing from the central bank (seignorage)

• Borrowing from the domestic commercial banks

• Borrowing from the domestic nonbank sector

15

Financial consequences of fiscal policy (II)

Borrowing in foreign currency implies, for most developing and

emerging countries, borrowing in foreign currency:

• changes in the exchange rate will affect the value of

external debt in domestic currency

• can cause an initial exchange rate appreciation, reducing

the competitiveness of the tradable sector

• for some countries, concerns about the sustainability of

debt and/or lack of creditworthiness severely limit this

16

debt

and/or

lack

of

creditworthiness

severely

limit

this

source of financing

9

Financial consequences of fiscal policy (III)

Borrowing from the Central Bank entails the sale of bonds to

the Central Bank. Less frequently, the Central Bank allows the

government to hold an overdraft account

government

to

hold

an

overdraft

account

• these loans are often at low interest rates

• it is equivalent to the creation of high powered money,

fueling inflation

• the CB can try to limit credit to the government, but it will

be successful only if it is fully independent

17

be

successful

only

if

it

is

fully

independent

Financial consequences of fiscal policy (IV)

Borrowing from domestic commercial banks: the government

sells bonds of different maturities to the commercial banks at

market interest rates

market

interest

rates

• It does not create high powered money, unless the CB

accommodates the extra demand for credit from

commercial banks by supplying them with additional

reserves (indirect CB financing of deficit)

• Commercial banks may be forced to reduce credit to the

18

private sector. This crowding out effect takes place through

interest rate increases

10

Financial consequences of fiscal policy (V)

Borrowing from the domestic non bank sector: The government

sells bonds of different maturities to the private sector at market

interest rates

interest

rates

• It does not create high powered money

• But it puts upward pressure on interest rates and thus

crowds out the private sector

• It can also distort interest rates if the non-bank sector is

required to hold government bonds

19

required

to

hold

government

bonds

Fiscal policy effects on the BOP

Fiscal contractions help reduce the effects of large capital flows on

aggregate demand and the real exchange rate:

B d i t d d it ll l i t t t

•

B

y

d

ampen

i

ng aggrega

t

e

d

eman

d

,

it

a

ll

ows

l

ower

i

n

t

eres

t

ra

t

es

and helps reduce incentives for inflows

• It alleviates the appreciating pressures on the exchange rate

directly (public spending is biased toward non-traded goods)

• It may provide greater scope for a countercyclical fiscal response

to cushion economic activit

y

when the inflows sto

p

20

yp

Typically, fiscal policy in emerging markets receiving capital inflows

is pro-cyclical, because a fast-growing economy generates

revenues that feed higher spending.

11

Effects on inflation and the financial sector

Central bank borrowing: inflationary effects with implications for:

o Current account deficit

o

Depending on fiscal repressions nominal interest rates

o

Depending

on

fiscal

repressions

,

nominal

interest

rates

o Real exchange rate

Commercial bank borrowing: crowds out private borrowing,

raising interest rates (unless central bank accommodates)

Domestic non-bank borrowing: crowds out private borrowing that

could be used to finance investment, less funding available for

lldthihittt

l

oans

l

ea

d

s

t

o

hi

g

h

er

i

n

t

eres

t

ra

t

es

Foreign borrowing: raises foreign debt and may lead to BoP

problems; exch. rt. risk; debt service needs may exert

downward pressure on the exchange rate

21

Financing from monetary sector

Note:

M = NFA + NDA

NDA DC OIN

NDA

=

DC

+

OIN

DC = NCG + CRE (State Ent. & Priv.)

• Fiscal policy determines the government’s demand for bank

financing (NCG), which, in turn, affects total domestic credit

(DC), net domestic assets (NDA), and broad money (M)

i h b d fi i ill i i

• H

i

g

h

er

b

u

d

get

fi

nanc

i

ng w

ill

requ

i

re more money expans

i

on

unless credit to the private sector is less or NFA is lower

(meaning a worse BOP).

22

12

Part 2

Fiscal effects of

macroeconomic

conditions

23

The impact of the macroeconomy on the

fiscal sector

• Government budget reflects changes in the

macroeconomic environment

;

;

• Need to be aware of the current and changing

macroeconomic environment and how it might

affect fiscal outcome;

• May need to change fiscal stance, if so what

should be the appropriate policy;

24

13

Real GDP

• Revenues rise during periods of economic expansion and typically

tax/GDP ratio rises, while the opposite happens during a slowdown

• Higher revenues may trigger higher discretionary expenditures i.e.

induce pro-cyclicality and allocation of expenditures may not be

optimal

• Lower global GDP growth could hurt export growth – both volume

and prices could affect revenues

• Weaker national GDP growth could lead to declining imports and

import tax revenue

25

Real GDP and the budget

During an economic contraction revenues-to-GDP fall and

expenditure-to-GDP increases

26

From: Patrizia Tumbarello, Unit Chief, Pacific Islands Unit, Asia and Pacific Department, IMF: "Fiscal Frameworks

to Support Growth and Macro Stability“, presentation for high-level Conference on Pacific Island Countries

Lifting Potential Growth in the Pacific Islands

14

Inflation

• High commodity prices

o for an oil importer if domestic prices are not

raised, subsidies would increase and/or tax

d

revenues re

d

uce

o Domestic (or international) wheat prices up,

subsidies may increase for consumers

• Higher inflation rate could lead to higher nominal

interest rates

• Higher inflation rate would lead to appreciation of

currenc

y

in real terms and loss of com

p

etitiveness

yp

• Very high inflation could lead to uncertainty, decline

in investments, and thus GDP and revenues

27

Interest rates

• Lower interest rates mean lower interest expenditure

for government

•

Lower interest rates could spur investment and higher

Lower

interest

rates

could

spur

investment

and

higher

GDP growth; also corporate costs decline leading to

higher corporate profits and tax collections

• Low foreign interest rates – search for yield could lead

to capital inflows

• High capital inflows could lead to more liquidity

supporting higher growth as well as lower interest rates

(maybe higher inflation) and higher revenues

Beware of just the opposite! In all of the above cases!

28

15

Exchange rate and external sector

• If the Real Effective Exchange Rate (REER) appreciates,

lose competitiveness lowering GDP:

o Exports decline

o Cheaper imports hurt domestic industry

• High external debt – if exchange rate depreciates or

global interest rates rise, liability increases as do

interest payments; if not rolled over could cause capital

flight and lower growth and revenues

• Capital flows

29

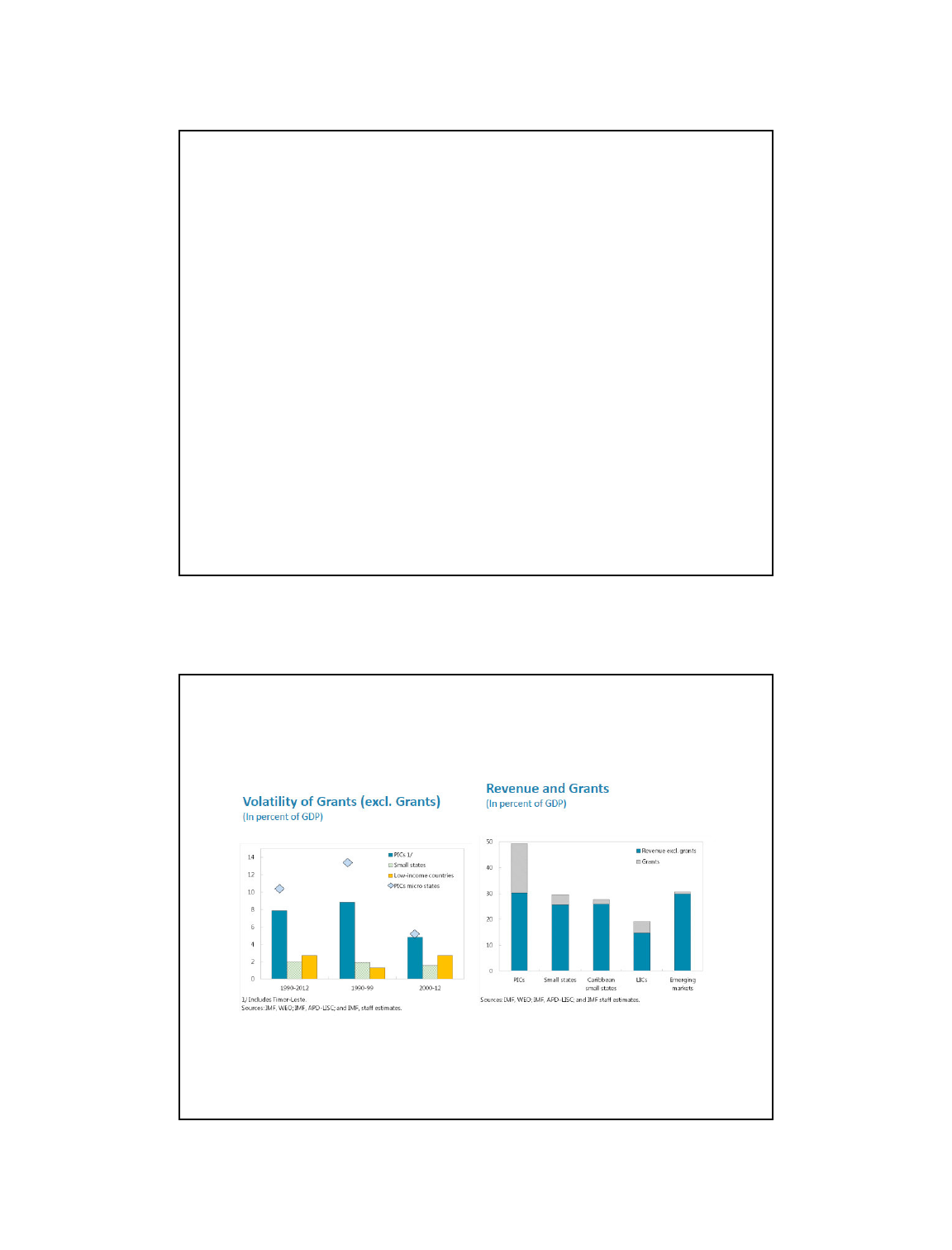

Grants

Grants are an important component of government’s receipts

30

From: Patrizia Tumbarello, Unit Chief, Pacific Islands Unit, Asia and Pacific Department, IMF: "Fiscal Frameworks

to Support Growth and Macro Stability“, presentation for high-level Conference on Pacific Island Countries

Lifting Potential Growth in the Pacific Islands

16

Part 3

Optimal fiscal policy for

output stabilization

31

General questions

• How should fiscal policy respond to fluctuations of output?

• Is fiscal policy effective in smoothing output fluctuations?

• In practice, how does fiscal policy respond to output?

• What level to target for fiscal balances?/ How much fiscal

adjustment (up or down)?

• Shall fiscal rules be used?

32

17

Countercyclical fiscal policy can be an effective

tool for stabilizing the economy

y

p

In a recession the government should stimulate the economy

y

t

CyclicalCyclical

FluctuationsFluctuations

In

a

recession

,

the

government

should

stimulate

the

economy

by increasing spending and/or lowering taxes

In an expansion, the government should avoid the economy

overheating by reducing spending and/or increasing taxes

-33-

Fiscal multipliers

The fiscal multiplier is the ratio of a change in output (∆Y)

to an exogenous change in the fiscal deficit (∆G or -∆T)

o The larger the fiscal multipliers, the more effective

fi l li ld b i t bili i th

fi

sca

l

po

li

cy wou

ld

b

e

i

n s

t

a

bili

z

i

ng

th

e economy

Fiscal multipliers would be larger

, if

Few “leakages” through savings or imports;

The monetary conditions are accommodative (less

crowding-out)

Country

’

s fiscal position after the stimulus is sustainable

Country s

fiscal

position

after

the

stimulus

is

sustainable

-34-

Source: IMF SPN/09/11

18

Effectiveness of fiscal policy (I)

Can fiscal policy help to stabilize short-run fluctuations in the

economy? In theory,

– Yes if fiscal policy mainly has demand effects, i.e., shifts out

aggregate demand during recessions (when individuals or

firms are credit constrained)

– No if fiscal policy mainly has a negative wealth effect on

labor supply and a crowding out effect on private

itt

35

i

nves

t

men

t

Automatic stabilizers and discretionary measures (fiscal stimulus)

help implement counter-cyclical fiscal policies.

Effectiveness of fiscal policy (II)

Automatic stabilizers are revenue or expenditure

provisions that have counter

cyclical impact without need

Automatic stabilizers:

• Allow implementing counter-cyclical fiscal policies

• Dampen business cycles

El

provisions

that

have

counter

-

cyclical

impact

without

need

for policy intervention

36

E

xamp

l

es

• Unemployment insurance

• Price stabilization funds

19

Is the economy at full capacity (employment)?

• FP affects supply and price responses

Effectiveness of fiscal policy (III)

Fixed or flexible exchange rate system?

• Adjustments through reserves or through prices

Is capital fully mobile?

• Capital will respond to changes in interest rates

• Impact on the exchange rate

Type of budgetary finance

–

debt or money

Type

of

budgetary

finance

debt

or

money

How will the private sector respond?

• Crowding-out effect

How coordinated are fiscal and monetary policy?

37

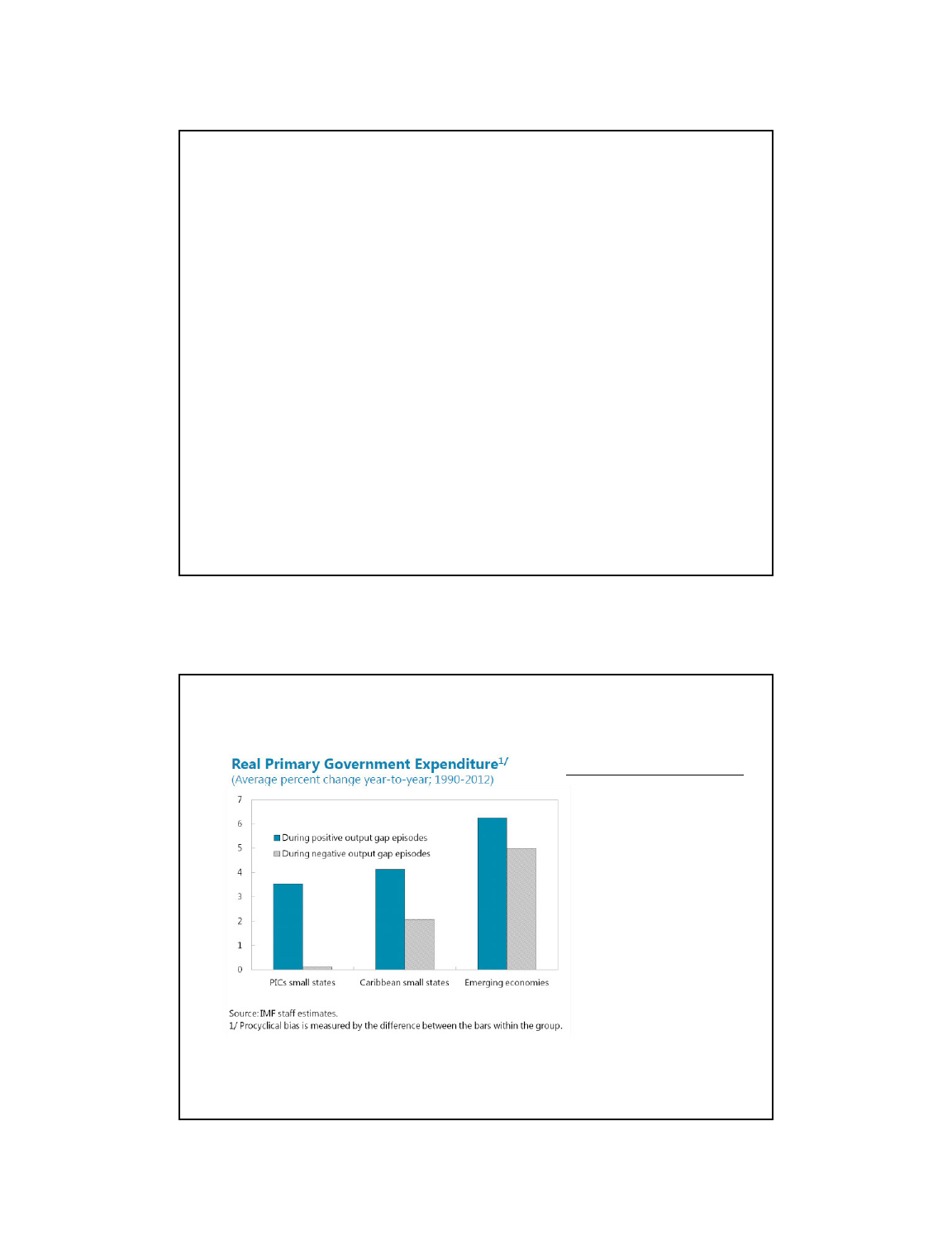

Evidence on procyclical bias

Possible explanations:

• Higher revenues

allow hi

g

her

g

spending: difficult to

resist demands

when times are good

• Lower revenues

force lower spending

when there are

constraints on

38

From: Patrizia Tumbarello, Unit Chief, Pacific Islands Unit, Asia and Pacific Department, IMF: "Fiscal Frameworks

to Support Growth and Macro Stability“, presentation for high-level Conference on Pacific Island Countries

Lifting Potential Growth in the Pacific Islands

constraints

on

financing

20

Policy implications of fiscal policy

• Sound fiscal policy is critical for macroeconomic

management and needs to be coordinated with

dh lf

monetary an

d

exc

h

ange rate po

l

icy

f

or maximum

impact

• Fiscal stimulus is usually expansionary, but it depends

on circumstances

• Fiscal policy affects BOP, monetary policy

• Impact of fiscal policy depends on behavior of private

participants – local and/or foreign

• Note institutional features that can limit impact of fiscal

policy, including globalization

39

Part 4

Fiscal accounts

and fiscal targets

40

21

Fiscal accounts

• Revenues

• Expenditures

• Financing

• Of the

government

• during a period

of time

• Separate sources

of funds that do

not generate debt

/decrease assets

• Separate uses of

funds not directed

• Separate sources

of funds that do

not generate debt

/decrease assets

• Separate uses of

funds not directed

• Define

government

• Define

government

• Flow concept

• Cash in many

cases

• Flow concept

• Cash in many

cases

41

funds

not

directed

to repay debt

funds

not

directed

to repay debt

• Gross vs. net accounting

• Consolidation of accounts

• Gross vs. net accounting

• Consolidation of accounts

Revenues and grants (II)

Revenues are non repayable receipts (i.e. receipts which do not

give rise to an obligation of repayment):

Total Revenues and Grants

Tax revenues

Direct taxes

Taxes on income

Taxes on wealth

Indirect taxes

Taxes on goods and services (VAT, sales tax, turnover)

Taxes on imports

Other tax revenues

Nontax revenue

License, fees, etc.

Central Bank profits

Grants

42

22

Expenditures (I)

Total Expenditures and Net Lending

Current expenditures

Noninterest expenditures

Noninterest

expenditures

Wages and salaries

Goods and services

Transfers

Pensions

Subsidies

Other transfers

I

I

nterest payments

Other current expenditures

Capital expenditures

Net Lending

43

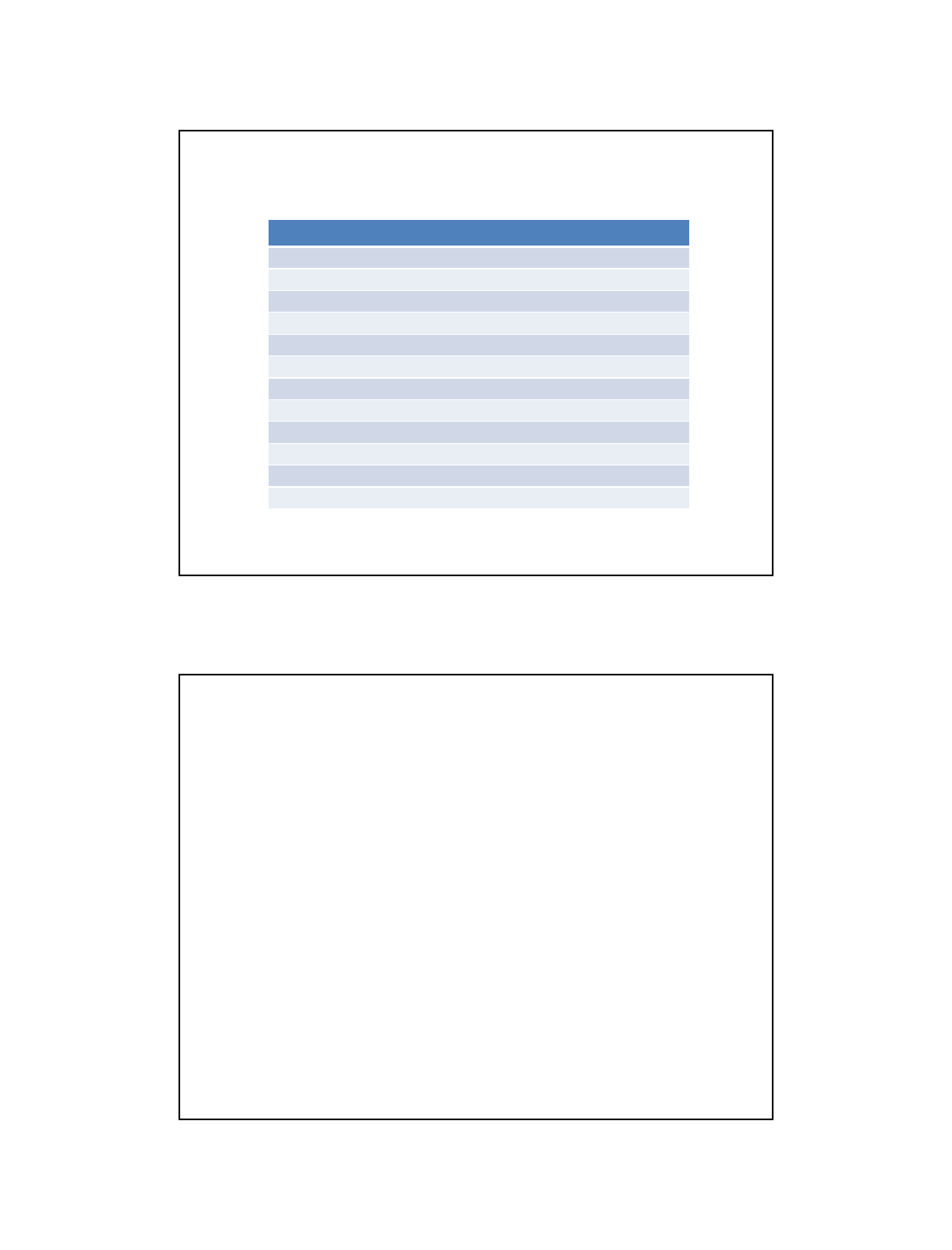

Korea 21.4

Australia 37.1

Some Asian countries: Illustrative shares of

General Government Expenditure to GDP

China 24.9

India 27.3

Indonesia 19.7

Malaysia 29.8

Pakistan 21.5

Philippines 18.8

Thailand 24.7

Laos 22.2

Vietnam 27.7

Source: IMF, October 9, 2013 Fiscal Monitor

44

23

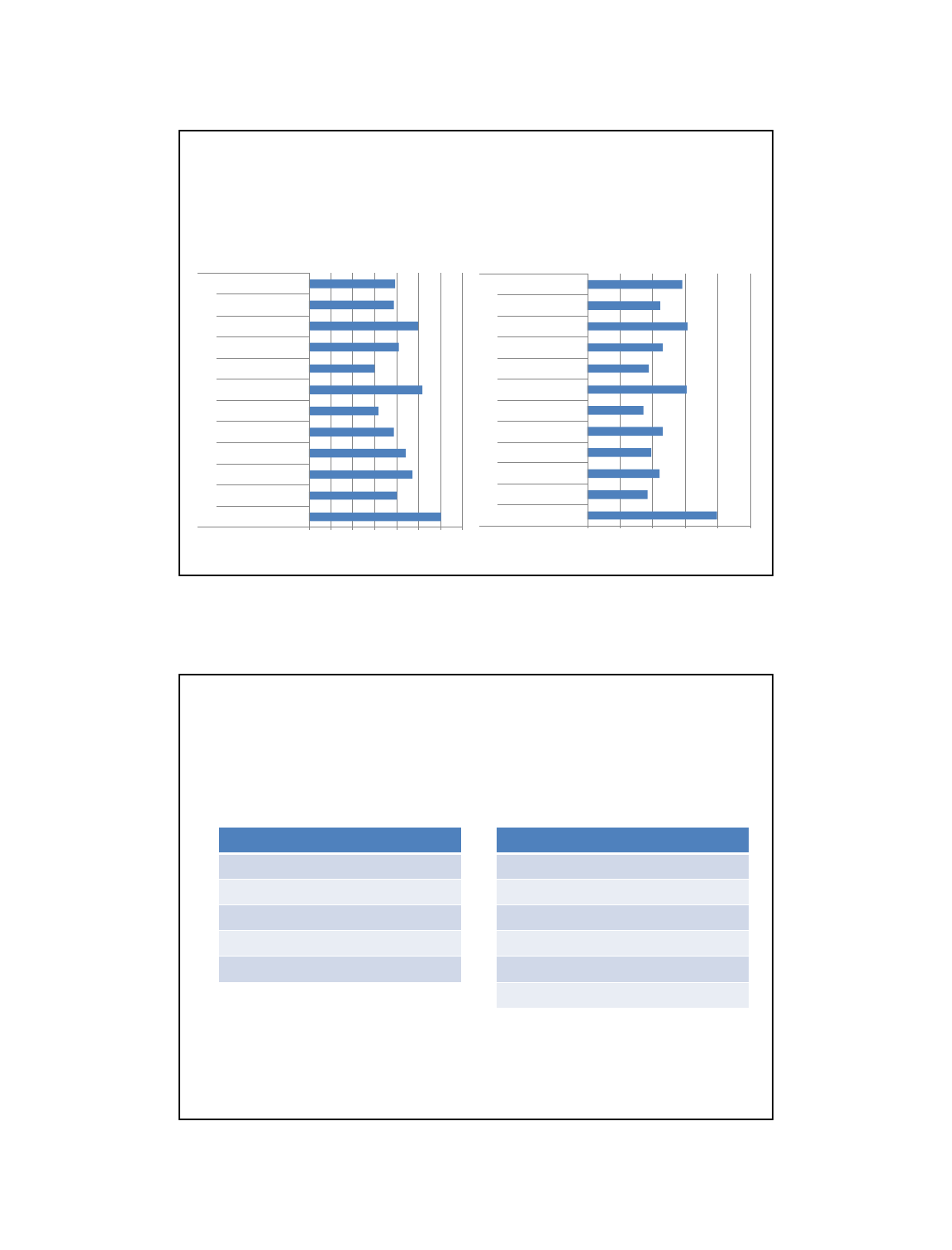

Some Asian countries: government revenues

and expenditures

Government revenues and expenditure as a share of GDP, 2010

Indonesia

Malaysia

Philippines

Thailand

Vietnam

China

India

ment Revenue (% GDP)

Indonesia

Malaysia

Philippines

Thailand

Vietnam

China

India

e

rnment Expenses (% of GDP)

45

0 5 10 15 20 25 30 35

Japan

Hong Kong SAR

Korea

Singapore

Taiwan Province of China

Govern

0 1020304050

Japan

Hong Kong SAR

Korea

Singapore

Taiwan Province of China

General Gov

e

Source: FAD

Expenditures (II)

Economic classification

Expenditures

Current expenditures

o/w Wages and salaries

o/w Goods and services

Capital expenditures

Functional classification

Expenditures

Education

Defense

Justice

Capital

expenditures

Net lending

…

46

24

Financing

Non repayable receipts: taxes, profits, and grants

Edit

–

E

xpen

dit

ures

Net lending

=

FINANCING:

Domestic borrowing

47

OVERALL

BALANCE

Domestic

borrowing

- Central bank (monetization)

- Bank financing

- Non-bank financing

Foreign borrowing

Privatization receipts

=

The overall balance

Total revenues and grants –

T l di d l di

It reflects the financing needs of the general government, and is

sometimes called the net borrowing requirement

It also indicates the balance between positive contribution of

T

ota

l

expen

di

tures an

d

net

l

en

di

ng =

OVERALL BALANCE

It

also

indicates

the

balance

between

positive

contribution

of

spending vs negative effects of taxes to GDP

It is usually presented in percent of GDP

48

25

Adjusted overall fiscal balance

Overall balance –

Selected items =

It excludes:

- grants

- revenues that are not predictable or out of the government control

(e.g. the oil sector)

ADJUSTED OVERALL BALANCE

- expenditure items that are automatically financed (ex. Spending

financing by grants or “project loans”)

• It allows to measure the balance on items over which the

government has greater control.

49

Targeting the overall balance

Overall balance or adjusted balance if main concern is

containin

g

a

gg

re

g

ate demand

(

inflation and CAD

)

ggg g ( )

Target decided based on broad macroeconomic objectives:

• Objectives for inflation, current account balance, and reserves

• Prospects for external financing, changes in money demand

Financial programming helps us solve for the budget balance

50

Financial

programming

helps

us

solve

for

the

budget

balance

consistent with targets on inflation, the current account and FX

reserves, and credit to the private sector.

26

Targeting financing

Financing requirement if main concern is liquidity crisis

Target decided based on :

• Expected liquidity needs (on a cash basis) both for current

operations but also for debt servicing (including capital)

•

Expected resources (including IMF lending)

51

•

Expected

resources

(including

IMF

lending)

Primary balance

Total revenues and grants –

(Total expenditures and net lending

iitt t)

Measures the effect of current discretionary budgetary policy or

fiscal effort (current interest payments depends on the stock

ofdebt whichdependonpastdeficits)

m

i

nus

i

n

t

eres

t

paymen

t

s

)

=

PRIMARY BALANCE

of

debt

,

which

depend

on

past

deficits)

Shows how recent policies affect government debt.

The debt-stabilizing primary balance is the primary balance

necessary to keep the debt-to-GDP constant

52

27

Targeting the primary balance

Primary balance if main concern is debt sustainability

Target decided based on:

• Estimate of debt stabilizing primary balance

• Primary balance necessary to achieved targeted level of debt

• Fiscal space (the gap between actual debt and “safe” levels of

db h hd d h l f

53

government

d

e

b

t, w

h

ic

h

d

epen

d

on t

h

e qua

l

ity o

f

institutions,

revenue raising ability, the volatility of revenues, and risks

which affect debt sustainability)

Current balance

Current revenues –

Current expenditures =

Used as measure of government savings.

Targeting the current balance can help safeguard investment in

times of fiscal consolidation.

Current

expenditures

=

CURRENT BALANCE

- It does not account that large public investment can lead to large

current expenditures in the future (wages, increase in debt and

interest payments,...).

- It does not compare the social return of investment projects to that of

current expenditures (hiring teachers vs. building schools).

54

28

Targeting the current balance

Current balance to

p

reserve ca

p

ital s

p

endin

g

g

iven

Cu e ba a ce o p ese e cap a spe d g g e

available resources

Target decided based on:

• Available financing (excluding financing in support of capital

55

spending

–

for example, capital grants)

• Macroeconomic considerations (similar to overall balance)

Stock indicators

The most common stock indicators are:

Net financial worth = financial assets minus total liabilities

Net worth = total assets minus total liabilities

Total liabilities (including contingent) to GDP, or to revenues

Other indicators include:

Debt service to GDP, or to revenues

Debt

service

to

GDP,

or

to

revenues

56

29

Targeting debt-to-GDP

Dbt

t

GDP if i t h fi l (b ff )

D

e

b

t-to-

GDP

if

concern

i

s to

h

ave

fi

sca

l

space

(b

u

ff

ers

)

Target decided based on:

• Amount of expected fiscal expansion needed to stabilize the

57

economy to shocks

• Sustainable level of debt

Fiscal stance and fiscal impulse

What is the impact of fiscal policy on domestic demand and

financial resources? How does this change over time?

The cyclically adjusted or the structural balance are used to

define the fiscal stance (deficit = expansionary fiscal policy)

The fiscal stance (expansionary or contractionary)

quantifies the addition or withdrawal of domestic

demand through fiscal policy

58

The fiscal impulse is the change in fiscal stance over time

Is fiscal policy becoming more or less expansionary (or more or

less contractionary) over time?

30

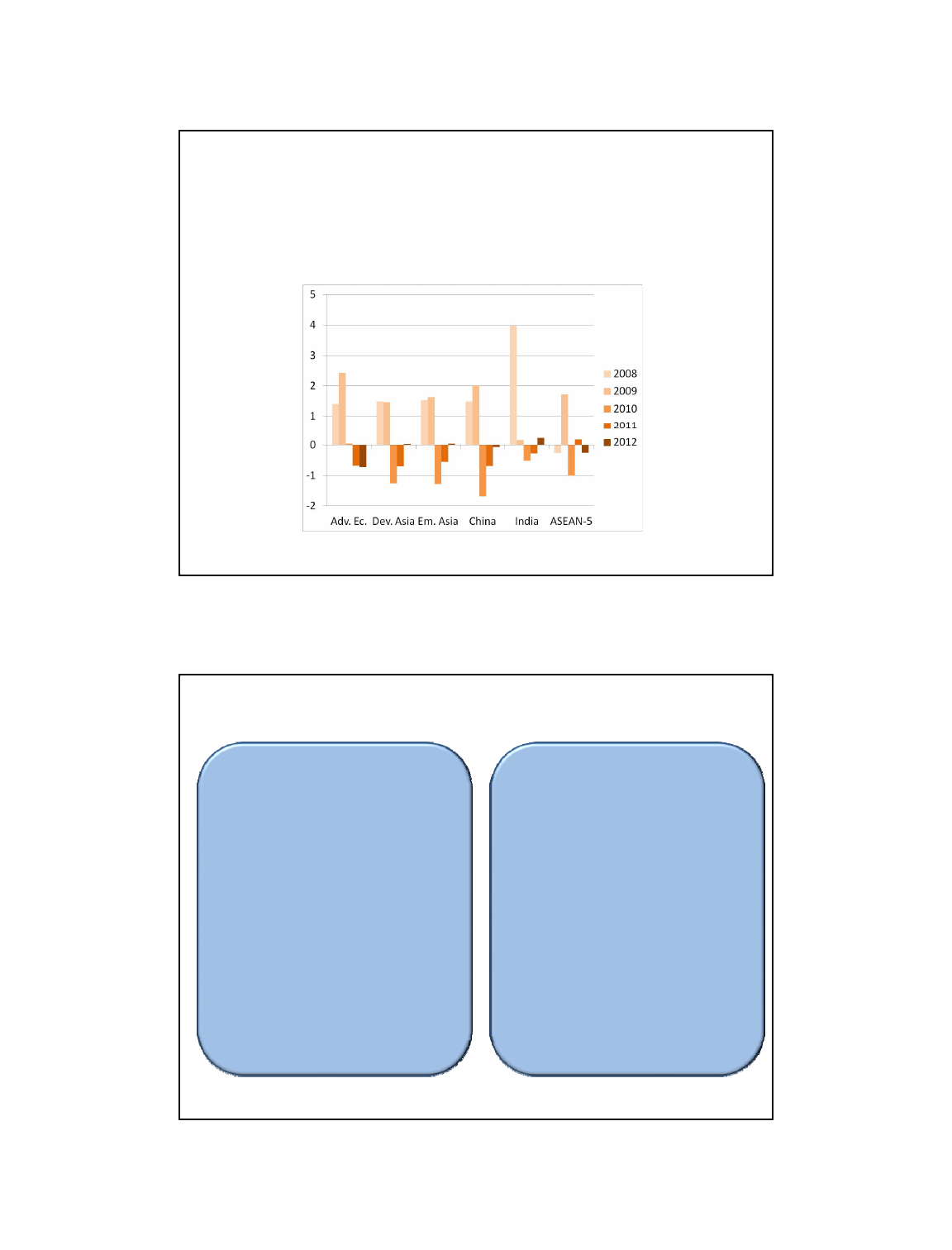

Fiscal impulse in selected countries

In most Asia the withdrawal of fiscal stimulus has not fully

started yet

Fiscal impulse

59

Source: IMF WEO October 2012

Fiscal rules

Pros

• Reduce the deficit bias

Cons

• Lack flexibility

• Reduce tax rate variability

and force expenditure

smoothing

• Support intergenerational

equity

• Substitute for market

• Reduce the quality of fiscal

policy and of policy goals

• Breed nontransparent

accounting practices

• Lacking political

commitment are unlikely

60

discipline

• Build reputation for macro

stability and credibility

commitment

are

unlikely

to be sustained and may

end up undermining policy

credibility.

31

Fiscal Challenges in Emerging and

Developing Economies

• Small tax base;

•

Tax administration system that is unable to fully collect

Tax

administration

system

that

is

unable

to

fully

collect

taxes and other levies;

• Greater vulnerability to external shocks: especially for

governments with sizeable foreign currency denominated

debt;

• Fiscal dominance: high public debt and persistent deficits

also accentuate the links between fiscal and monetary policy

61

Successful fiscal reforms in emerging and

developing economies

• Tax reforms and Expenditure control;

•

Structural and expenditure reforms to boost growth

•

Structural

and

expenditure

reforms

to

boost

growth

;

• Reducing exposure to exchange rate and interest rate

movements;

• Acknowledging contingent liabilities;

• Steps to improve the credibility of fiscal policy;

62

32

Additional Slides:

63

OT14.51 - FAF

Key structural reforms

• Price adjustment and liberalization

o Wage policy, administered prices, etc.

• State enterprise reform, privatization, restructuring

• Policies to promote competition

• Tax, expenditure, and budgetary reforms

o Example: rationalizing social safety nets

• Financial sector reforms

o Developing broader capital markets, related legal

reforms

• External sector reforms

o Trade liberalization, capital account liberalization

db

• More transparency an

d

b

etter governance

o Strengthening public institutions, legal system

64

33

Poverty and social spending

• Avoid perverse

iti k th

Social spending in percent of GDP

i

ncen

ti

ves, ma

k

e sure

th

e

money goes to the real

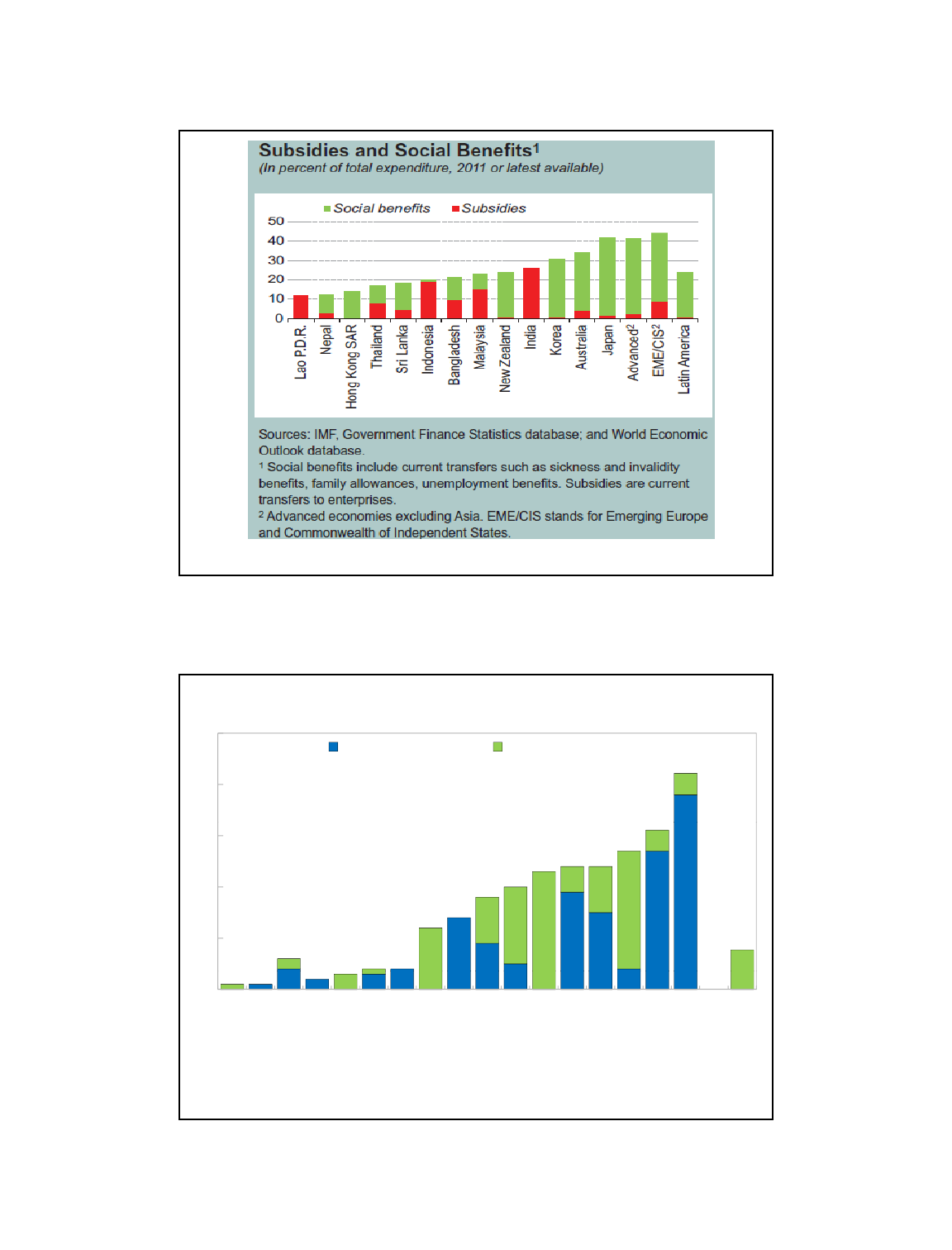

poor

• Phase out generalized

subsidies

• Make use of conditional

-65-

cash transfers

• Review credit guarantee

schemes to limit

distortions

-66-

Source: IMF Asia REO, April 2013, pg. 44

34

-67-

Source: IMF Asia REO, April 2013, pg. 44

4

5

Energy Food and fertilizer

Food and Energy Subsidies

1

2

3

-68-

Source: IMF Asia REO, April 2013, pg. 44

0

Phillippines

Vietanam

Australia

Hong Kong SAR

New Zealand

Mongolia

Taiwan Province of

China

Japan

Nepal

Thailand

India

Korea

Sri Lanka

Bangladesh

China

Malaysia

Indonesia

Advanced economies

35

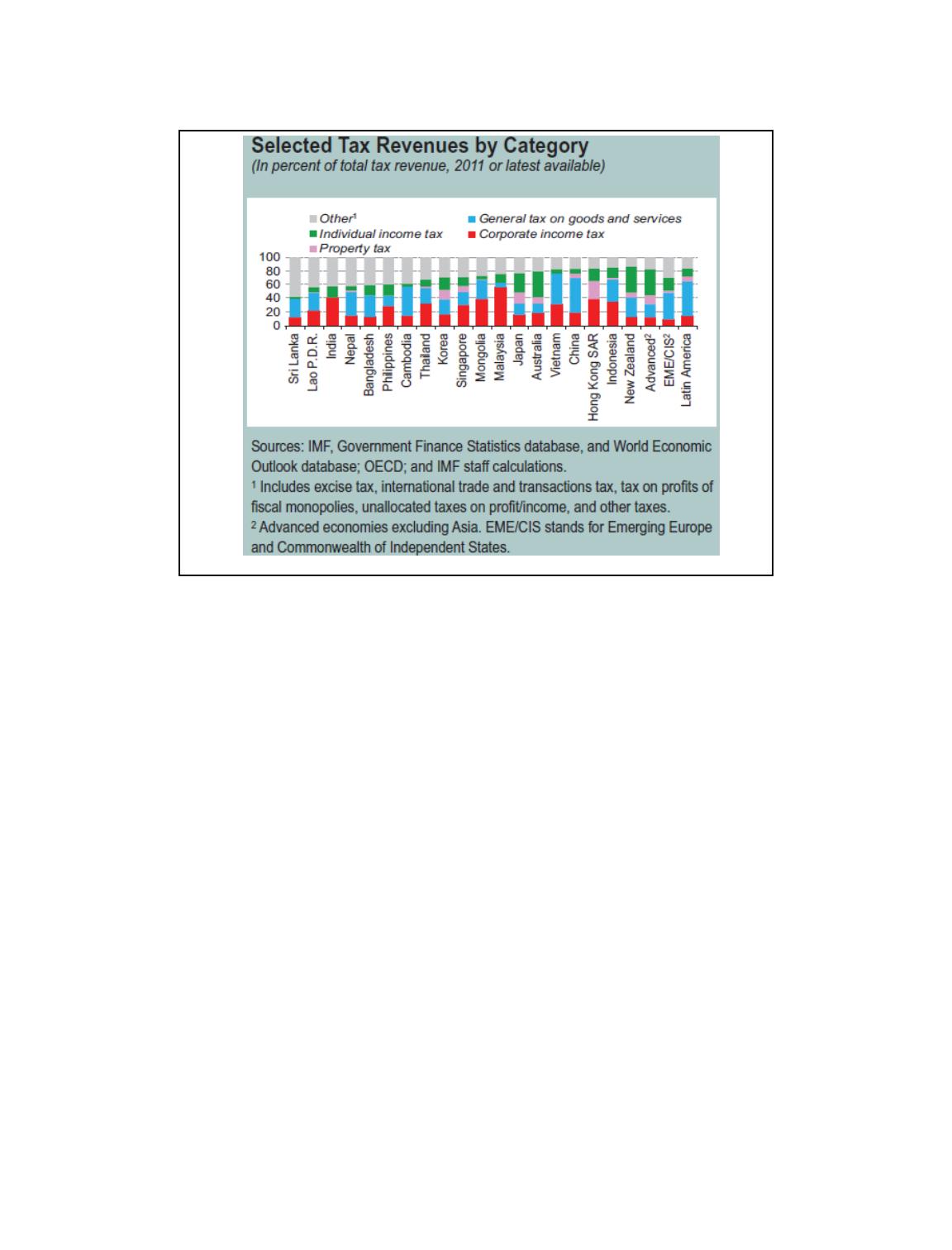

-69-

Source: IMF Asia REO, April 2013, pg. 43