CEMEX, S.A.B. DE C.V.

Separate Financial Statements

December 31, 2022, 2021 and 2020

(With Independent Auditor’s Report Thereon)

INDEX TO THE PARENT COMPANY-ONLY FINANCIAL STATEMENTS

CEMEX, S.A.B. de C.V. (Parent Com

p

an

y

-Onl

y

):

Statements of Operations for the years ended December 31, 2022, 2021 and 2020 .......................................................................................... 1

Statements of Comprehensive Income (Loss) for the years ended December 31, 2022, 2021 and 2020 .......................................................... 2

Statements of Financial Position as of December 31, 2022 and 2021 ............................................................................................................... 3

Statements of Cash Flows for the years ended Decembe

r

31, 2022, 2021 and 2020 ........................................................................................ 4

Statements of Changes in Stockholders’ Equity for the years ended December 31, 2022, 2021 and 2020 ....................................................... 5

Notes to the Financial Statements ..................................................................................................................................................................... 6

Independent Auditors’ Report – KPMG Cárdenas Dosal, S.C. ......................................................................................................................... 40

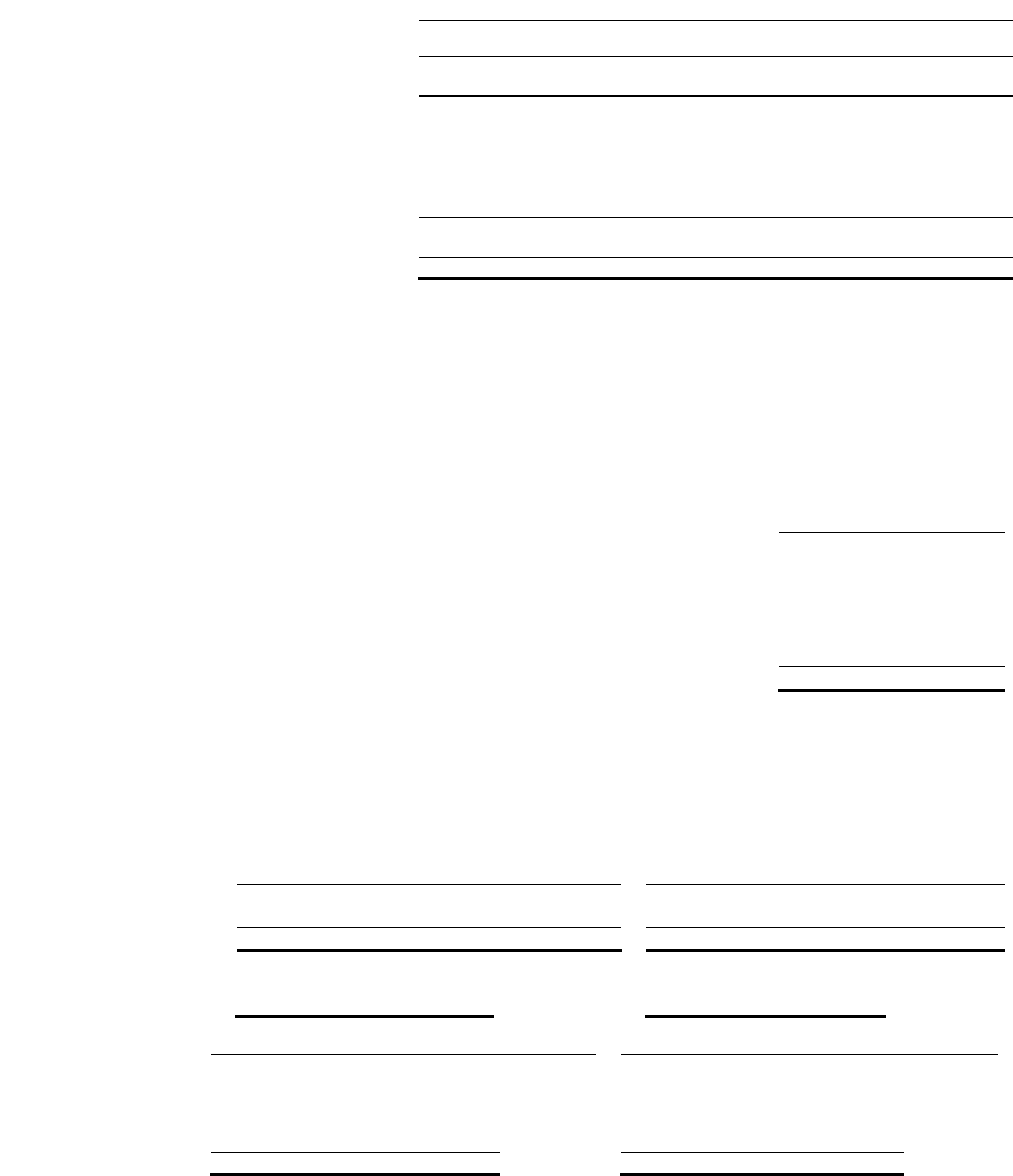

1

CEMEX, S.A.B. de C.V. (PARENT COMPANY-ONLY)

Statements of Operations

(Millions of Pesos)

For the years ended December 31,

Notes

2022 2021 2020

Revenues ....................................................................................................

3.14

,

4

$ 88,866 79,989 59,610

Cost of sales ...............................................................................................

3.15, 5

(

59,077

)

(

51,880

)

(

28,101

)

Gross profit ............................................................................................................

29,789 28,109 31,509

O

p

eratin

g

ex

p

enses ...................................................................................

3.15, 6

(

18,040

)

(

13,857

)

(

19,024

)

Operating earnings before other income (expenses), net ................................

11,749 14,252 12,485

Other income

(

ex

p

enses

)

, net ....................................................................

7

(

921

)

4,287

(

714

)

Operating earnings ..............................................................................................

10,828 18,539 11,771

Financial ex

p

ense .......................................................................................

.

8.1, 18

(

9,319

)

(

13,180

)

(

14,230

)

Financial income and other items, net. .......................................................

.

8.2

2,545 5,084 3,766

Forei

g

n exchan

g

e results ............................................................................

.

(

439

)

2,441

(

3,904

)

Share of

p

rofit of e

q

uit

y

accounted investees .............................................

.

14

12,577 2,028 (29,748)

Net income (loss) before income tax ....................................................................

.

16,192 14,912 (32,345)

Income tax ..................................................................................................

21

1,149 272 (217)

NET INCOME (LOSS) .............................................................................................

$ 17,341 15,184 (32,562)

The accompanying notes are part of these Parent Company-only financial statements.

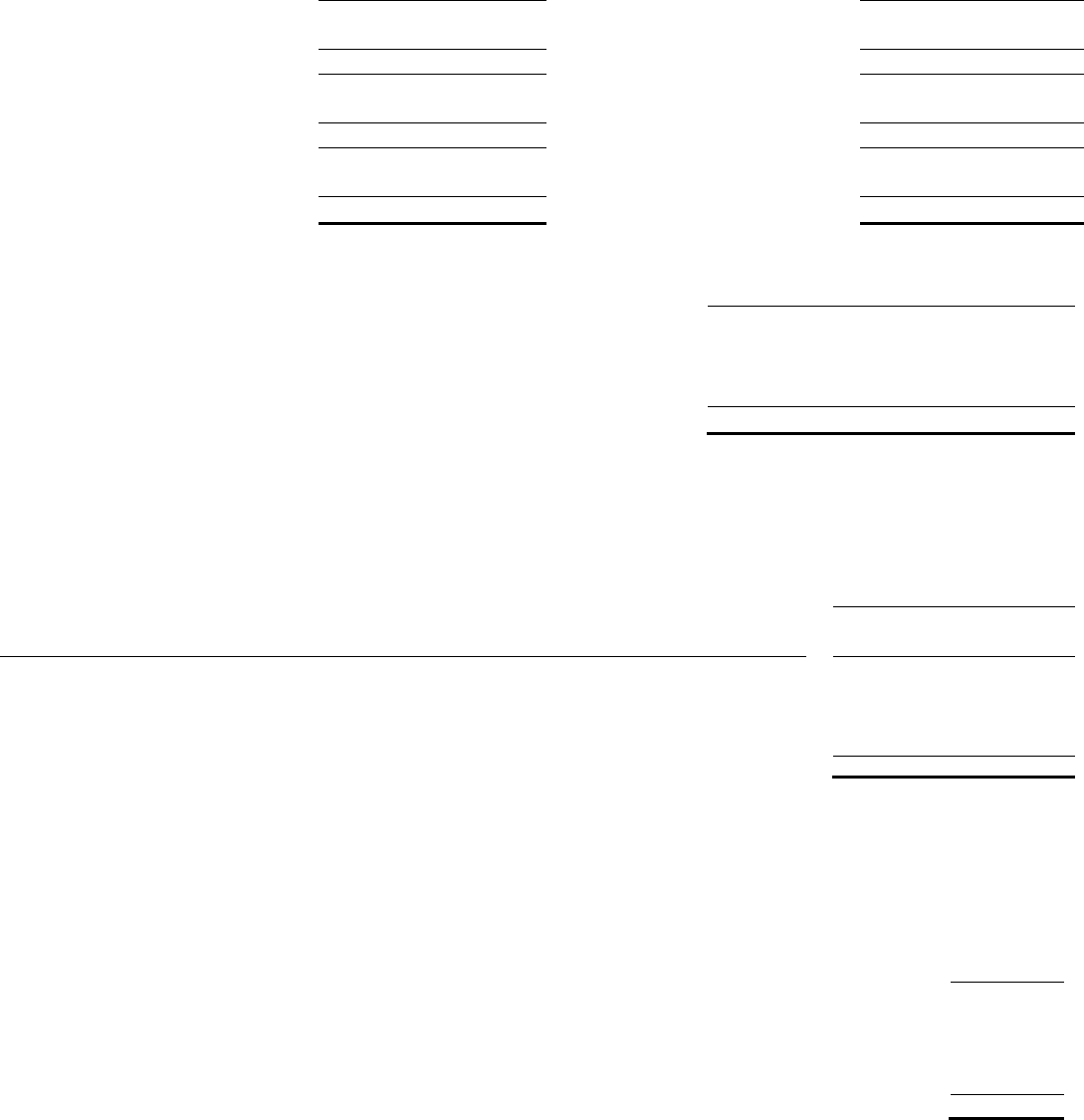

2

CEMEX, S.A.B. de C.V. (PARENT COMPANY-ONLY)

Statements of Comprehensive Income (Loss)

(Millions of Pesos)

For the years ended December 31,

Notes

2022 2021 2020

NET INCOME (LOSS) .........................................................................................

$ 17,341 15,184 (32,562)

Items that will be reclassified subsequently to the statement of operations

Results from derivative financial instruments designated as cash

flow hedges ............................................................................................

18.4

2,105 776 (259)

Items that will not be reclassified subsequently to the statement of operations

Currenc

y

translation effects and results on e

q

uit

y

of subsidia

r

ies ...

3.3

(

12,153

)

3,998 17,537

Results from derivative financial instruments designated as net

investment hed

g

e ......................................................................

18.4

(

561

)

123 1,144

Net actuarial gains (losses) from remeasurements of defined

b

enefit

p

ension

p

lans ................................................................

20

(

33

)

(

9

)

–

Income tax recognized directly in other comprehensive income ......

21.2

519 48 (261)

Total items of other comprehensive (loss) income

for the

p

erio

d

................................................................................

(

10,123

)

4,936 18,161

TOTAL COMPREHENSIVE INCOME (LOSS) ..............................................

.

$ 7,218 20,120 (14,401)

The accompanying notes are part of these Parent Company-only financial statements.

3

CEMEX, S.A.B. de C.V. (PARENT COMPANY-ONLY)

Statements of Financial Position

(Millions of Pesos)

As of December 31,

Notes

2022 2021

ASSETS

CURRENT ASSETS

Cash and cash e

q

uivalents ...................................................................................................................

9

$ 2,652 4,556

Trade accounts receivable, net .............................................................................................................

10

4,243 3,672

Other accounts receivable ....................................................................................................................

11

1,508 1,460

Inventories ...........................................................................................................................................

12

1,121 767

Accounts receivable from related

p

arties .............................................................................................

19.1

2,976 1,688

Other current assets ............................................................................................................................

13

531 430

Total current assets ......................................................................................................................

13,031 12,573

NON-CURRENT ASSETS

E

q

uit

y

accounted investees ..................................................................................................................

14.2

355,529 362,425

Other investments and non-current accounts receivable ......................................................................

15

1,765 1,390

Accounts receivable from relate

d

-

p

arties lon

g

term ............................................................................

19.1

677 1,046

Pro

p

ert

y

, machiner

y

and e

q

ui

p

ment, net and assets for the ri

g

ht-of-use, net .......................................

16 51,399 49,664

Total non-current assets ...............................................................................................................

409,370 414,525

TOTAL ASSETS ..............................................................................................................................................

$ 422,401 427,098

LIABILITIES AND STOCKHOLDERS’ EQUITY

CURRENT LIABILITIES

Other current financial obli

g

ations ......................................................................................................

18.2

$ 2,498 2,542

Trade

p

a

y

ables .................................................................................................................................... 6,963 7,162

Current accounts payable to related parties .........................................................................................

19.1 65,599 59,590

Other current liabilities ........................................................................................................................ 17 9,944 7,354

Total current liabilities .................................................................................................................

85,004 76,648

NON-CURRENT LIABILITIES

Non-current debt ..................................................................................................................................

18.1

128,027 141,592

Other non-current financial obli

g

ations ...............................................................................................

18.2

1,412 1,705

Pensions and other

p

ost-em

p

lo

y

ment benefits .....................................................................................

20

557 119

Non-current accounts

p

a

y

able to related

p

arties .................................................................................. 19.1 59 72

Deferred income tax liabilities .............................................................................................................

21.2 1,668 3,555

Other non-current liabilities .................................................................................................................

901 1,948

Total non-current liabilities .........................................................................................................

132,624 148,991

TOTAL LIABILITIES ....................................................................................................................................

217,628 225,639

STOCKHOLDERS’ EQUITY

Common stock and additional

p

ai

d

-in ca

p

ital .................................................................................. 22.1 105,572 105,572

Other e

q

uit

y

reserves and subordinated notes ..................................................................................

3.13 32,894 46,921

Retained earnin

g

s .............................................................................................................................

22.2

66,307 48,966

TOTAL STOCKHOLDERS’ EQUITY .........................................................................................................

204,773 201,459

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY .....................................................................

$ 422,401 427,098

The accompanying notes are part of these Parent Company-only financial statements.

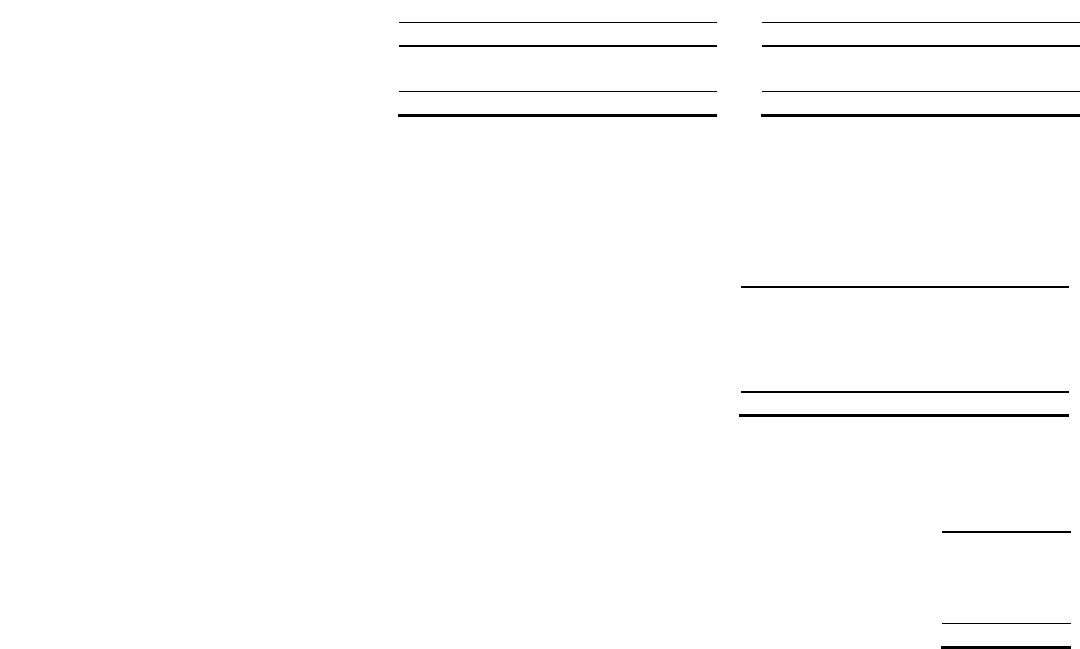

4

CEMEX, S.A.B. de C.V. (PARENT COMPANY-ONLY)

Statements of Cash Flows

(Millions of Pesos)

Years ended December 31,

Notes

2022 2021 2020

OPERATING ACTIVITIES

Net income (loss) .....................................................................................................

$ 17,341 15,184 (32,562)

Adjustments fo

r

:

De

p

reciation of

p

ro

p

ert

y

, machiner

y

and e

q

ui

p

ment .............................

5, 6, 16

2,373 282 2,397

Share of profit of equity accounted investees ........................................

14

(12,577) (2,028) 29,748

Financial items, net ................................................................................

7,213 5,655 14,368

Income taxes ..........................................................................................

21.1

(1,149) (272) 217

Results from the sale of assets ...............................................................

7

(

1

)

(

50

)

6

Result from sale of emission allowances ...............................................

7

–

(4,210)

–

Chan

g

es in workin

g

ca

p

ital, excludin

g

income taxes ............................

9,578 10,297

(

14,188

)

Cash flow provided (used in) by operating activities .......................................

22,778 24,858 (14)

Financial expense pai

d

...........................................................................

(9,867) (8,255) (12,219)

Income taxes

p

ai

d

..................................................................................

21.1

(

138

)

(

470

)

(

435

)

Net cash flows provided by (used in) operating activities ...............................

12,773 16,133 (12,668)

INVESTING ACTIVITIES

E

q

uit

y

accounted investees .......................................................................

14.2

73

(

262

)

9,172

Proceeds from the sale of emission allowances ........................................

7

826 12,508

–

Purchase of emission allowances ..............................................................

7

(

826

)

(

8,298

)

–

Purchase of property, machinery and equipment ......................................

16

(3,397) (2,529) (2,045)

Non-current leases with related

p

arties .....................................................

(

625

)

–

–

(3,949) 1,419 7,127

FINANCING ACTIVITIES

Issuances of subordinated notes ...............................................................

22.3

– 19,786 –

Coupons paid on subordinated notes .......................................................

22.1

(1,096) (268) –

Non-current related parties, net ................................................................

19.1

925 (995) (35)

Derivative financial instruments ...............................................................

18.4

684 (841) 270

Proceeds from new debt instruments ........................................................

18.1

39,947 84,333 138,921

Debt repayments .......................................................................................

18.1

(47,113) (119,222) (119,600)

Other financial obligations, net .................................................................

18.2

(853) (1,318) (10,718)

Shares repurchase program .......................................................................

22.1

(2,296) – (1,894)

Shares in trust for future deliveries under share-based compensation ......

22.4

(733) – –

Non-current leases paid to related parties .................................................

57 – –

Other financial expenses paid in cash .......................................................

18.1

(250) (280) (274)

Net cash flows (used in) provided by financing activities .............................

(10,728) (18,805) 6,670

Increase

(

decrease

)

in cash and cash e

q

uivalents .................................

(

1,904

)

(

1,253

)

1,129

Cash and cash equivalents at beginning of

p

erio

d

...............................

4,556 5,809 4,680

CASH AND CASH EQUIVALENTS AT END OF PERIOD .......................

9

$ 2,652 4,556 5,809

Changes in working capital, excluding income taxes:

Trade accounts receivable, net ..............................................................

10

$ (571) 517 (323)

Other accounts receivable ......................................................................

11

(

48

)

(

313

)

(

54

)

Inventories .............................................................................................

12

(354) 3,007 (303)

Current related

p

arties, net .....................................................................

19.1

8,160 9,758

(

15,481

)

Trade payables ......................................................................................

(199) (3,648) 1,774

Other current liabilities ..........................................................................

17

2,590 976 199

Changes in working capital, excluding income taxes ......................................

$ 9,578 10,297 (14,188)

The accompanying notes are part of these Parent Company-only financial statements.

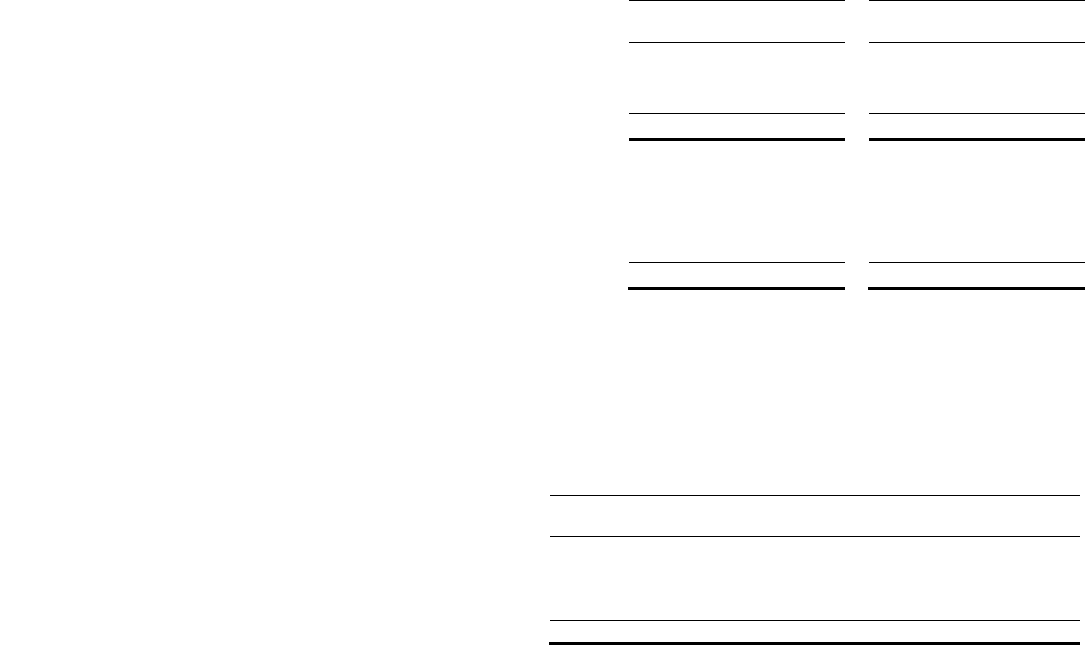

5

CEMEX, S.A.B. de C.V. (PARENT COMPANY-ONLY)

Statements of Changes in Stockholders’ Equity

For the years ended December 31, 2022, 2021 and 2020

(Millions of Pesos)

Notes Common stoc

k

Additional paid-in

ca

p

ital

Other equity Reserves

and subordinated notes Retained earnin

g

s

Total stockholders’

e

q

uit

y

Balance as of December 31, 2019 ........................................................................

$ 4,172 141,925 1,534 28,705 176,336

Comprehensive income (loss), net .........................................................................

– – 18,161 (32,562) (14,401)

Restitution of retained earnings .............................................................................

22.1

– (37,639) – 37,639 –

Share–based compensation ....................................................................................

22.1

– – 563 – 563

Own shares purchased under share repurchase program .......................................

22.1

(5) (986) (903) – (1,894)

Balance as of December 31, 2020 ........................................................................

$

4,167 103,300 19,355 33,782 160,604

Comprehensive income (loss), net .........................................................................

– – 4,936 15,184 20,120

Issuance of subordinated notes ..............................................................................

22.3

– – 19,786 – 19,786

Coupons paid on subordinated notes .....................................................................

22.3

– – (604) – (604)

Share–based compensation ....................................................................................

22.4

– – 1,553 – 1,553

Own shares purchased under share repurchase program .......................................

22.1

(3) (1,892) 1,895 – –

Balance as of December 31, 2021 ........................................................................

$

4,164 101,408 46,921 48,966 201,459

Comprehensive income (loss), net .........................................................................

– – (10,123) 17,341 7,218

Coupons paid on subordinated notes .....................................................................

22.3

– – (1,079) – (1,079)

Share–based compensation ....................................................................................

22.4

– – 895 – 895

Transfer of employees’ rights and obligations ......................................................

2, 20

– – (691) – (691)

Shares in trust for future deliveries under share-based compensation ..................

22.4

– – (733) – (733)

Own shares purchased under share repurchase program .......................................

22.1

– – (2,296) – (2,296)

Balance as of December 31, 2022 ........................................................................

$

4,164 101,408 32,894 66,307 204,773

The accompanying notes are part of these Parent Company-only financial statements.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

6

1) DESCRIPTION OF BUSINESS

CEMEX, S.A.B. de C.V., originated in 1906, is a publicly traded variable stock corporation (sociedad anónima bursátil de capital variable) organized

under the laws of the United Mexican States, or Mexico, and is the parent company of entities whose main activities are oriented to the construction

industry, through the production, marketing, sale and distribution of cement, ready-mix concrete, aggregates and other construction materials and

services, including urbanization solutions. In addition, CEMEX, S.A.B. de C.V. performs significant business and operational activities in Mexico.

The shares of CEMEX, S.A.B. de C.V. are listed on the Mexican Stock Exchange (“MSE”) as Ordinary Participation Certificates (“CPOs”)

(Certificados de Participación Ordinaria) under the symbol “CEMEXCPO.” Each CPO represents two series “A” shares and one series “B” share of

common stock of CEMEX, S.A.B. de C.V. In addition, CEMEX, S.A.B. de C.V.’s shares are listed on the New York Stock Exchange (“NYSE”) as

American Depositary Shares (“ADSs”) under the symbol “CX.” Each ADS represents ten CPOs.

The terms “CEMEX, S.A.B. de C.V.” and/or the “Parent Company” used in these accompanying notes to the financial statements refer to CEMEX,

S.A.B. de C.V. without its consolidated subsidiaries. The terms the “Company” or “CEMEX” refer to CEMEX, S.A.B. de C.V. together with its

consolidated subsidiaries.

The issuance of these financial statements was authorized by CEMEX, S.A.B. de C.V.´s management on February 16, 2023. These financial statements

will be submitted for approval to the Annual General Ordinary Shareholders' Meeting of CEMEX, S.A.B. de C.V. on March 23, 2023.

2) RELEVANT EVENT DURING THE PERIOD AND AS OF THE ISSUANCE DATE OF THE FINANCIAL STATEMENTS

On January 1, 2022, a group of employees of CEMEX Operaciones México, S.A. de C.V., a subsidiary of CEMEX, S.A.B. de C.V., was transferred to

the Parent Company. Concerning such transfer, CEMEX, S.A.B. de C.V. acquired the rights and obligations related to the employees; additionally,

CEMEX, S.A.B. de C.V. acquired certain assets necessary for the functions of such employees.

Corporate reorganization

On August 1, 2021, CEMEX, S.A.B. de C.V., formalized a corporate reorganization of some operational activities in Mexico ("corporate

reorganization") pursuant to which CEMEX, S.A.B. de C.V. transferred certain activities related to the production of cement, ready-mix concrete, and

aggregates to its subsidiaries CEMEX Operaciones México, S.A. de C.V. and CEMEX Concretos, S.A. de C.V. CEMEX, S.A.B. de C.V. in conjunction

with its subsidiaries CEMEX Concretos, S.A. de C.V. and Proveedora Mexicana de Materiales, S.A. de C.V., continues to carry out activities related

to the commercialization, promotion, and sale of cement and ready-mix concrete products to customers. In addition, on August 1, 2021, CEMEX

Operaciones México, S.A. de C.V., entered into an agreement contract to supply CEMEX, S.A.B. de C.V. of the products, which it will commercialize

following the corporate restructuring. CEMEX, S.A.B. de C.V., recognized assets and liabilities transfer at their book value as it is a transaction between

common control entities. CEMEX, S.A.B. de C.V. accounted for any difference between the price and the book value in stockholders' equity (note

14.1).

3) SIGNIFICANT ACCOUNTING POLICIES

3.1) BASIS OF PRESENTATION AND DISCLOSURE

CEMEX, S.A.B. de C.V.’s financial statements as of December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, were

prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

Separate financial statements

The parent company-only financial statements of CEMEX, S.A.B. de C.V. presented herein constitute the separate financial statements of a parent

company as defined by International Accounting Standard 27 - Separate Financial Statements (“IAS 27”). Separate Financial Statements reflect the

Parent Company’s unconsolidated financial position, financial performance, cash flows and changes in stockholders’ equity as of December 31, 2022

and 2021 and for the years ended December 31, 2022, 2021 and 2020. The consolidated financial statements of CEMEX, S.A.B. de C.V. and its

subsidiaries were issued separately.

Presentation currency and definition of terms

During the reported periods, the presentation currency of the financial statements was the Mexican Peso. When reference is made to Pesos or “$” it

means Mexican Pesos, except when specific reference is made to a different currency. The amounts in the financial statements and the accompanying

notes are stated in millions, except when references are made to earnings per share and/or prices per share. When reference is made to “US$” or

“Dollars,” it means Dollars of the United States of America (“United States”). When reference is made to “€” or “Euros,” it means the currency in

circulation in a significant number of European Union (“EU”) countries. When reference is made to “£” or “Pounds,” it means British Pounds sterling.

Previously reported Peso amounts of prior years are not restated unless the transactions in other currencies are still outstanding, in which case those are

restated using the closing exchange rates as of the reporting date. Amounts reported in Pesos should not be construed as representations that such

amounts, represent those Pesos or Dollars or could be converted into Pesos or Dollars at the rate indicated. As of December 31, 2022 and 2021,

translations of Pesos into Dollars and Dollars into Pesos, were determined for statement of financial position amounts using the closing exchange rate of

$19.50 and $20.50, respectively, and for statements of operations amounts, using the average exchange rates of $20.03, $20.43 and $21.58 Pesos per Dollar

for 2022, 2021 and 2020, respectively. When the amounts between parentheses are the Peso and the Dollar, the amounts were determined by translating

the Euro amount into Dollars using the closing exchange rates at year-end and then translating the Dollars into Pesos as previously described.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

7

Statements of operations

CEMEX, S.A.B. de C.V. includes the line item titled “Operating earnings before other income (expenses), net” considering that it is subtotal relevant

for the determination of CEMEX’s “Operating EBITDA” (Operating earnings before other income (expenses), net plus depreciation and amortization)

as described below in this note. The line item “Other income (expenses), net” consists primarily of revenues and expenses not directly related to

CEMEX, S.A.B. de C.V.’s main activities or which are of a non-recurring nature, including impairment losses of long-lived assets, non-recurring sales

of emission allowances, results on disposal of assets and restructuring costs, among others (note 7). Under IFRS, the inclusion of certain subtotals such

as “Operating earnings before other income (expenses), net” and the display of the statement of operations vary significantly by industry and company

according to specific needs.

Considering that it is a relevant measure used by management to review operating performance and for decision-making purposes, as well as an

indicator used by CEMEX, S.A.B. de C.V.’s creditors of its ability to internally fund capital expenditures and to measure its ability to service or incur

debt under financing agreements, for purposes of note 18, CEMEX, S.A.B. de C.V. presents “Operating EBITDA” (operating earnings before other

income (expenses), net, plus depreciation and amortization). Operating EBITDA is not a measure of financial performance, an alternative to cash flows,

or a measure of liquidity under IFRS. Moreover, Operating EBITDA may not be comparable to other similarly titled measures of other companies.

Statements of cash flows

During 2021, except for the cash and cash equivalents received and disclosed in the statements of cash flows, the effects of the corporate reorganization

as described in note 14.1, did not represent sources or uses of cash in the operating, investing or financing activities. In addition, the statements of cash

flows exclude the following transactions that did not represent sources or uses of cash:

Financing activities:

In 2022, 2021 and 2020, the increases in other financing obligations in connection with lease contracts negotiated during those years for $746, $438 and

$723, respectively (note 18.2).

Investing activities:

In 2022, 2021 and 2020, in connection with the leases negotiated during the year, the increases in assets for the right-of-use related to lease contracts for

$746 (US$38), $438 (US$21) and $723 (US$36), respectively (note 16.2).

Newly issued IFRS adopted in the reported periods

Beginning January 1, 2022, CEMEX, S.A.B. de C.V. adopted prospectively IFRS amendments that did not result in any material impact on its results or

financial position, and which are explained as follows:

Standard Main topic

Amendment to IAS 37, Provisions,

Contingent Liabilities and Contingent

Assets – Onerous Contracts—Cost of

Fulfilling a Contract ..................................

Clarifies that the ‘cost of fulfilling’ a contract comprises the ‘costs that relate directly to the contract.’

Costs that relate directly to a contract can either be incremental costs of fulfilling that contract or an

allocation of other costs that relate directly to fulfilling contracts.

Amendments to IAS 16, Property, Plant and

Equipment –Proceeds before Intended

Use ............................................................

Clarifies the standard to prohibit deducting from the cost of an item of property, plant and equipment

any proceeds from selling items produced while bringing that asset to the location and condition

necessar

y

for it to be ca

p

able of o

p

eratin

g

in the manner intended b

y

mana

g

ement.

Annual improvements (2018-2020 cycle):

IFRS 1, First-time Adoption of IFRS –

Subsidiary as a First-time Adopte

r

...........

The amendment permits a subsidiary to measure cumulative translation differences using the amounts

reported by its parent, based on the parent’s date of transition to IFRSs.

Annual improvements (2018-2020 cycle):

IFRS 9, Financial Instruments – Fees in

the ‘10 per cent’ Test for Derecognition

of Financial Liabilities ..............................

The amendment clarifies which fees an entity includes when it applies the ‘10 per cent’ test in assessing

whether to derecognize a financial liability. An entity includes only fees paid or received between the

entity (the borrower) and the lender, including fees paid or received by either the entity or the lender on

the other’s behalf.

Amendments to IFRS 3, Business

Combinations – Reference to the

conceptual framewor

k

..............................

Update a reference in IFRS 3 to the Conceptual Framework for Financial Reporting without changing

the accounting requirements for business combinations.

3.2) USE OF ESTIMATES AND CRITICAL ASSUMPTIONS

The preparation of financial statements in accordance with IFRS requires management to make estimates and assumptions that affect the reported

amounts of assets and liabilities, and the disclosure of contingent assets and liabilities at the date of the financial statements, as well as the reported

amounts of revenues and expenses during the period. These assumptions are reviewed on an ongoing basis using available information. Actual results

could differ from these estimates. The items subject to significant estimates and assumptions by management include impairment tests of long-lived

assets, recognition of deferred income tax assets and uncertain tax positions, the measurement of financial instruments at fair value, the assets and

liabilities related to employee benefits, legal proceedings and provisions regarding assets retirements obligations and environmental liabilities.

Significant judgment is required by management to appropriately assess the amounts of these concepts.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

8

3.3) FOREIGN CURRENCY TRANSACTIONS

Transactions denominated in foreign currencies are recorded in the functional currency at the exchange rates prevailing on the dates of their execution.

Monetary assets and liabilities denominated in foreign currencies are translated into the functional currency at the exchange rates prevailing at the

statement of financial position date, and the resulting foreign exchange fluctuations are recognized in earnings, except for exchange fluctuations arising

from: 1) foreign currency indebtedness associated with the acquisition of foreign entities; and 2) fluctuations associated with related parties’ balances

denominated in foreign currency, whose settlement is neither planned nor likely to occur in the foreseeable future and as a result, such balances are of

a permanent investment nature. These fluctuations are recorded against “Other equity reserves,” as part of the foreign currency translation adjustment

(note 3.12) until the disposal of the foreign net investment, at which time, the accumulated amount is recognized through the statement of operations

as part of the gain or loss on disposal.

The financial statements of foreign subsidiaries, as determined using their respective functional currency, are translated to U.S. Dollars and then to

Pesos at the closing exchange rate for the statement of financial position and at the closing exchange rates of each month within the period for the

statement of operations. The functional currency is that in which each consolidated entity primarily generates and expends cash. The corresponding

translation effect is included within “Other equity reserves” and is presented in the statement of other comprehensive income for the period as part of

the foreign currency translation adjustment (note 3.12) until the disposal of the net investment in the foreign subsidiary.

Considering its integrated activities, for purposes of functional currency, CEMEX, S.A.B. de C.V. is considered to have two divisions, one related with

its financial and holding company activities, in which the functional currency is the Dollar for all assets, liabilities and transactions associated with

these activities, and another division related with the CEMEX, S.A.B. de C.V.’s operating activities in Mexico, in which the functional currency is the

Peso for all assets, liabilities and transactions associated with these activities.

The most significant closing exchange rates for the statement of financial position and the approximate average exchange rates (as determined using

the closing exchange rates of each month within the period) for the statement of operations in respect to the primary functional currencies to the Peso

as of December 31, 2022, 2021 and 2020, were as follows:

2022 2021

2020

Currency Closing Average Closing Average Closing Average

Dolla

r

............................

19.50 20.03

20.50 20.43

19.89 21.58

Euros .............................

0.9344 0.9522

0.8789 0.8467

24.3065 24.6985

British Pound Sterlin

g

...

0.8266 0.8139

0.7395 0.7262

27.1981 27.8121

3.4) CASH AND CASH EQUIVALENTS (note 9)

The balance in this caption is comprised of available amounts of cash and cash equivalents, mainly represented by highly liquid short-term investments,

which are readily convertible into known amounts of cash, and which are not subject to significant risks of changes in their values, including overnight

investments, which yield fixed returns and have maturities of less than three months from the investment date. These fixed-income investments are

recorded at cost plus accrued interest. Accrued interest is included in the statement of operations as part of “Financial income and other items, net.”

When applicable, the amount of cash and cash equivalents in the statement of financial position includes restricted cash and investments to the extent

that any restriction will be lifted in less than three months from the reporting date, comprised of deposits in margin accounts that guarantee certain

obligations, except when contracts contain provisions for net settlement, in which case, these restricted amounts of cash and cash equivalents are offset

against the liabilities that CEMEX, S.A.B. de C.V. has with its counterparties. When the restriction period is greater than three months, any restricted

balance of cash and investments is not considered cash equivalents and is included within short-term or long-term “Other accounts receivable,” as

appropriate.

3.5) FINANCIAL INSTRUMENTS

Classification and measurement of financial instruments

The financial assets that meet both of the following conditions and are not designated as at fair value through profit or loss: a) are held within a business

model whose objective is to hold assets to collect contractual cash flows, and b) its contractual terms give rise on specified dates to cash flows that are

solely payments of principal and interest on the principal amount outstanding, are classified as “Held to collect” and measured at amortized cost.

Amortized cost represents the Net Present Value (“NPV”) of the consideration receivable or payable as of the transaction date. This classification of

financial assets comprises the following captions:

Cash and cash equivalents (notes 3.4 and 9).

Trade receivables, other current accounts receivable and other current assets (notes 10, 11 and 13). Due to their short-term nature, CEMEX, S.A.B.

de C.V. initially recognizes these assets at the original invoiced or transaction amount less expected credit losses, as explained below.

Trade receivables sold under securitization programs, in which certain residual interest and continued involvement in the trade receivables sold is

maintained in the case of failure to collect, do not qualify for derecognition and are maintained in the statement of financial position (notes 10 and

18.2).

Investments and non-current accounts receivable (note 15). Subsequent changes in effects from amortized cost are recognized in statement of

operations as part of “Financial income and other items, net.”

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

9

Classification and measurement of financial instruments - continued

Certain strategic investments are measured at fair value through other comprehensive income within “Other equity reserves” (notes 3.12 and 15).

CEMEX, S.A.B. de C.V. does not maintain financial assets “Held to collect and sell” whose business model has the objective of collecting contractual

cash flows and then selling those financial assets.

The financial assets that are not classified as “Held to collect” or that do not have strategic characteristics fall into the residual category of held at fair

value through the statement of operations as part of “Financial income and other items, net,” (notes 8.2 and 15).

Debt instruments and other financial obligations are classified as “Loans” and measured at amortized cost (notes 18.1 and 18.2). Interest accrued on

financial instruments is recognized within “Other current liabilities” against financial expense. During the reported periods, CEMEX, S.A.B. de C.V.

did not have financial liabilities voluntarily recognized at fair value or associated with fair value hedge strategies with derivative financial instruments.

Derivative financial instruments are recognized as assets or liabilities in the statement of financial position at their estimated fair values, and the changes

in such fair values are recognized in the statement of operations within “Financial income and other items, net” for the period in which they occur,

except in the case of hedging instruments as described below (notes 8.2 and 18.4).

Impairment of financial assets

Impairment losses of financial assets, including trade accounts receivable, are recognized using the Expected Credit Loss model (“ECL”) for the entire

lifetime of such financial assets on initial recognition, and at each subsequent reporting period, even in the absence of a credit event or if a loss has not

yet been incurred, considering for their measurement past events and current conditions, as well as reasonable and supportable forecasts affecting

collectability. For purposes of the ECL model of trade accounts receivable, CEMEX, S.A.B. de C.V. segments its accounts receivable in a matrix by

type of client or homogeneous credit risk and days past due and determines for each segment an average rate of ECL, considering actual credit loss

experience generally over the last 12 months and analyses of future delinquency, which is applied to the balance of the accounts receivable. The average

ECL rate increases in each segment of days past due until the rate is 100% for the segment of 365 days or more past due.

Costs incurred in the issuance of debt or borrowings

Direct costs incurred in debt issuances or borrowings, as well as debt refinancing or non-substantial modifications to debt agreements that did not

represent an extinguishment of debt by considering that the holders and the relevant economic terms of the new instrument are not substantially different

to the replaced instrument, adjust the carrying amount of the related debt and are amortized as interest expense as part of the effective interest rate of

each instrument over its maturity. These costs include commissions and professional fees. Costs incurred in the extinguishment of debt, as well as debt

refinancing or modifications to debt agreements, when the new instrument is substantially different from the old instrument according to a qualitative

and quantitative analysis, are recognized in the statement of operations as incurred.

Leases (notes 3.8, 16 and 18.2)

At the inception of a contract, CEMEX, S.A.B. de C.V. assesses whether a contract is, or contains, a lease. A contract is, or contains, a lease if at

inception of the contract, conveys the right to control the use of an identified asset for a period in exchange for consideration, based on IFRS 16, Leases

(“IFRS 16”). to assess whether a contract conveys the right to control the use of an identified asset.

Pursuant to IFRS 16, leases are recognized as financial liabilities against assets for the right-of-use, measured at their commencement date as the net

present value (“NPV”) of the future contractual fixed payments, using the interest rate implicit in the lease or, if that rate cannot be readily determined,

CEMEX, S.A.B. de C.V.’s incremental borrowing rate. CEMEX, S.A.B. de C.V. determines its incremental borrowing rate by obtaining interest rates

from its external financing sources and makes certain adjustments to reflect the term of the lease, the type of the asset leased and the economic

environment in which the asset is leased.

CEMEX, S.A.B. de C.V. does not separate the non-lease component from the lease component included in the same contract. Lease payments included

in the measurement of the lease liability comprise contractual rental fixed payments, less incentives, fixed payments of non-lease components and the

value of a purchase option, to the extent that option is highly probable to be exercised or is considered a bargain purchase option. Interest incurred

under the financial obligations related to lease contracts is recognized as part of the “Financial expense” line item in the statement of operations.

At commencement date or upon modification of a contract that contains a lease component, CEMEX, S.A.B. de C.V. allocates the consideration in the

contract to each lease component based on their relative stand-alone prices. CEMEX, S.A.B. de C.V. applies the recognition exception for lease terms

of 12 months or less and contracts of low-value assets and recognizes the lease payment of these leases as rental expense in the statement of operations

over the lease term. CEMEX, S.A.B. de C.V. defined the lease contracts related to office and computer equipment as low-value assets.

The lease liability is measured at amortized cost using the effective interest method as payments are incurred and is remeasured when: a) there is a

change in future lease payments arising from a change in an index or rate, b) if there is a change in the amount expected to be payable under a residual

guarantee, c) if the Parent Company changes its assessment of whether it will exercise a purchase, extension or termination option, or d) if there is a

revised in-substance fixed lease payment. When the lease liability is remeasured, an adjustment is made to the carrying amount of the asset for the

right-of-use or is recognized within “Financial income and other items, net” if such asset has been reduced to zero.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

10

Hedging instruments

(note 18.4)

A hedging relationship is established to the extent the entity considers, based on the analysis of the overall characteristics of the hedging and hedged

items, that the hedge will be highly effective in the future and the hedge relationship at inception is aligned with the entity’s reported risk management

strategy (note 18.4). The accounting categories of hedging instruments are: a) cash flow hedge, b) fair value hedge of an asset or forecasted transaction,

and c) hedge of a net investment in a subsidiary.

In cash flow hedges, the effective portion of changes in fair value of derivative instruments are recognized in stockholders’ equity within other equity

reserves and are reclassified to earnings as the interest expense of the related debt is accrued, in the case of interest rate swaps, or when the underlying

products are consumed in the case of contracts on the price of raw materials and commodities. In hedges of the net investment in foreign subsidiaries,

changes in fair value are recognized in stockholders’ equity as part of the foreign currency translation gains and losses within other equity reserves

(note 3.5), whose reversal to earnings would take place upon disposal of the foreign investment. During the reported periods, CEMEX, S.A.B. de C.V.

did not have derivatives designated as fair value hedges. Derivative instruments are negotiated with institutions with significant financial capacity;

therefore, CEMEX, S.A.B. de C.V. believes the risk of non-performance of the obligations agreed to by such counterparties to be minimal.

Embedded derivative financial instruments

CEMEX, S.A.B. de C.V. reviews its contracts to identify the existence of embedded derivatives. Identified embedded derivatives are analyzed to

determine if they need to be separated from the host contract and recognized in the statement of financial position as assets or liabilities, applying the

same valuation rules used for other derivative instruments.

Put options granted for the purchase of non-controlling interests

Under IFRS 9, represent agreements by means of which a non-controlling interest has the right to sell, at a future date using a predefined price formula

or at fair market value, its shares in a consolidated subsidiary. When the obligation should be settled in cash or through the delivery of another financial

asset, an entity should recognize a liability for the NPV of the redemption amount as of the reporting date against the controlling interest within

stockholders’ equity. A liability is not recognized under these agreements when the redemption amount is determined at fair market value at the exercise

date and the entity has the election to settle using its own shares. As of December 31, 2022 and 2021, CEMEX, S.A.B. de C.V. did not have written

put options.

Fair value measurements

(note 18.3)

Under IFRS, fair value represents an “Exit Value” which is the price that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date, considering the counterparty’s credit risk in the valuation. The concept of Exit Value

is premised on the existence of a market and market participants for the specific asset or liability. When there are no market and/or market participants

willing to make a market, IFRS establishes a fair value hierarchy that gives the highest priority to unadjusted quoted prices in active markets for

identical assets or liabilities (Level 1 measurements) and the lowest priority to measurements involving significant unobservable inputs (Level 3

measurements).

The three levels of the fair value hierarchy are as follows:

Level 1.- represent quoted prices (unadjusted) in active markets for identical assets or liabilities that CEMEX, S.A.B. de C.V. can access at the

measurement date. A quote price in an active market provides the most reliable evidence of fair value and is used without adjustment to measure

fair value whenever available.

Level 2.- are inputs other than quoted prices in active markets that are observable for the asset or liability, either directly or indirectly, and are used

mainly to determine the fair value of securities, investments or loans that are not actively traded. Level 2 inputs included equity prices, certain

interest rates and yield curves, implied volatility and credit spreads, among others, as well as inputs extrapolated from other observable inputs. In

the absence of Level 1 inputs, CEMEX, S.A.B. de C.V. determined fair values by iteration of the applicable Level 2 inputs, the number of securities

and/or the other relevant terms of the contract, as applicable.

Level 3.- inputs are unobservable inputs for the asset or liability. CEMEX, S.A.B. de C.V. used unobservable inputs to determine fair values, to the

extent there are no Level 1 or Level 2 inputs, in valuation models such as Black-Scholes, binomial, discounted cash flows or multiples of Operating

EBITDA, including risk assumptions consistent with what market participants would use to arrive at fair value.

3.6) INVENTORIES

(note 12)

Inventories are valued using the lower of cost or net realizable value. The cost of inventories is based on weighted average cost formula and includes

expenditures incurred in acquiring the inventories, production or conversion costs and other costs incurred in bringing them to their existing location

and condition. CEMEX, S.A.B. de C.V. analyzes its inventory balances to determine if, because of internal events, such as physical damage, or external

events, such as technological changes or market conditions, certain portions of such balances have become obsolete or impaired. When an impairment

situation arises, the inventory balance is adjusted to its net realizable value. In such cases, these adjustments are recognized against the results of the

period. Advances to suppliers of inventory are presented as part of other current assets.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

11

Inventories – continued

In connection with the corporate reorganization (notes 2 and 14.1), commencing August 2021, CEMEX, S.A.B. de C.V., purchases its merchandise in

a form of ready for sale. In connection with purchasing merchandise ready to be sold, CEMEX, S.A.B. de C.V., acquires such merchandise mainly

with related parties (note 19). CEMEX, S.A.B. de C.V. reports its inventories at the acquisition cost.

3.7) EQUITY ACCOUNTED INVESTEES (note 14.2)

Investments in controlled entities and in entities over which CEMEX, S.A.B. de C.V. exercises significant influence, which are not classified as available

for sale, are measured using the equity method.

3.8) PROPERTY, MACHINERY AND EQUIPMENT AND RIGHT OF USE (note 16)

Property, machinery and equipment are recognized at their acquisition or construction cost, as applicable, less accumulated depreciation and

accumulated impairment losses. Depreciation of property, machinery and equipment is recognized as part of cost and operating expenses (notes 5 and

6) and is calculated using the straight-line method over the estimated useful lives of the assets, except for mineral reserves, which are depleted using

the units-of-production method. As of December 31, 2022, the average useful lives by category of property, machinery and equipment, which are

reviewed at each reporting date and adjusted if appropriate, were as follows:

Years

Administrative and industrial buildin

g

s ...................................................................................................................................................... 35

Machinery and equipment in plant .............................................................................................................................................................

25

Ready-mix trucks and motor vehicles ........................................................................................................................................................

10

Office equipment and other assets .............................................................................................................................................................

5

Assets for the right-of-use related to leases are initially measured at cost, comprised by the initial amount of the lease liability adjusted by any payments

made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle, remove or restore the underlying

asset, less any lease incentives received. The asset for the right-of-use is subsequently depreciated using the straight-line method from the

commencement date to the end of the lease term, unless the lease transfers ownership of the underlaying asset to CEMEX, S.A.B. de C.V. by the end

of the lease term or if the cost of the asset for the right-of-use reflects that CEMEX, S.A.B. de C.V. will exercise a purchase option. In that case the

asset for the right-of-use would be depreciated over the useful life of the underlying asset, on the same basis as those of property, machinery and

equipment. In addition, assets for the right-of-use may be reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease

liability.

CEMEX, S.A.B. de C.V. capitalizes, as part of the related cost of property, machinery and equipment, interest expense from existing debt during the

construction or installation period of significant property, machinery and equipment, considering CEMEX, S.A.B. de C.V.’s corporate average interest

rate and the average balance of investments in process for the period.

All waste removal costs or stripping costs incurred in the pre-operative phase of a quarry are recognized as part of its carrying amount. The capitalized

amounts are amortized over the expected useful life of exposed ore body based on the units of production method.

Costs incurred in respect of operating fixed assets that result in future economic benefits, such as an extension in their useful lives, an increase in their

production capacity or in safety, as well as those costs incurred to mitigate or prevent environmental damage, are capitalized as part of the carrying

amount of the related assets. The capitalized costs are depreciated over the remaining useful lives of such fixed assets. Periodic maintenance of fixed

assets is expensed as incurred. Advances to suppliers of fixed assets are presented as part of other non-current accounts receivable.

3.9) IMPAIRMENT OF LONG-LIVED ASSETS (notes 15 and 16)

Property, machinery and equipment, assets for the right-of-use and other investments

These assets are tested for impairment upon the occurrence of internal or external indicators of impairment, such as changes in CEMEX, S.A.B. de

C.V.’s operating business model or in technology that affect the asset, or expectations of lower operating results, to determine whether their carrying

amounts may not be recovered. An impairment loss is recorded in the statement of operations for the period within “Other income (expenses), net” for

the excess of the asset’s carrying amount over its recoverable amount, corresponding to the higher of the fair value less costs to sell the asset, as

generally determined by an external appraiser, and the asset’s value in use, the latter represented by the NPV of estimated cash flows related to the use

and eventual disposal of the asset. The main assumptions utilized to develop estimates of NPV are a discount rate that reflects the risk of the cash flows

associated with the assets and the estimations of generation of future income. Those assumptions are evaluated for reasonableness by comparing such

discount rates to available market information and by comparing to third-party expectations of industry growth, such as governmental agencies or

industry chambers.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

12

Property, machinery and equipment, assets for the right-of-use and other investments – continued

When impairment indicators exist, for each intangible asset, CEMEX, S.A.B. de C.V. determines its projected revenue streams over the estimated

useful life of the asset. To obtain discounted cash flows attributable to each intangible asset, such revenue is adjusted for operating expenses, changes

in working capital and other expenditures, as applicable, and discounted to NPV using the risk adjusted discount rate of return. The most significant

economic assumptions are: a) the useful life of the asset; b) the risk adjusted discount rate of return; c) royalty rates; and d) growth rates. Assumptions

used for these cash flows are consistent with internal forecasts and industry practices. The fair values of these assets are significantly sensitive to

changes in such relevant assumptions. Certain key assumptions are more subjective than others. In respect of trademarks, CEMEX, S.A.B. de C.V.

considers that the most subjective key assumption is the royalty rate. In respect of extraction rights and customer relationships, the most subjective

assumptions are revenue growth rates and estimated useful lives. CEMEX, S.A.B. de C.V. validates its assumptions through benchmarking with

industry practices and the corroboration of third-party valuation advisors. Significant judgment by management is required to appropriately assess the

fair values and values in use of the related assets, as well as to determine the appropriate valuation method and select the significant economic

assumptions.

Equity accounted investees

Equity accounted investees are tested for impairment when required due to significant adverse changes, by determining the recoverable amount of such

investment, which consists of the higher of the investment in subsidiaries and associates’ fair value, less cost to sell and value in use, represented by

the discounted amount of estimated future cash flows to be generated to which those net assets relate. CEMEX, S.A.B. de C.V. initially determines its

discounted cash flows over periods of 5 to 10 years, depending on the economic cycle. If the value in use of the equity accounted investees is lower

than its corresponding carrying amount, the Parent Company determines the fair value of its investment using methodologies generally accepted in the

market to determine the value of entities, such as multiples of Operating EBITDA and by reference to other market transactions. An impairment loss

is recognized within “Other income (expenses), net”, if the recoverable amount is lower than the net book value of the investment.

3.10) PROVISIONS (note 17)

CEMEX, S.A.B. de C.V. recognizes provisions when it has a legal or constructive obligation resulting from past events, whose resolution would require

cash outflows, or the delivery of other resources owned by the Parent Company. As of December 31, 2022 and 2021, some significant proceedings that

gave rise to a portion of the carrying amount of CEMEX, S.A.B. de C.V.’s other current and non-current liabilities and provisions are detailed in note

23.

Considering guidance under IFRS, CEMEX, S.A.B. de C.V. recognizes provisions for levies imposed by governments when the obligating event or

the activity that triggers the payment of the levy has occurred, as defined in the legislation.

Contingencies and commitments (notes 23 and 24)

Obligations or losses related to contingencies are recognized as liabilities in the statement of financial position only when present obligations exist

resulting from past events that are probable to result in an outflow of resources and the amount can be measured reliably. Otherwise, a qualitative

disclosure is included in the notes to the financial statements. The effects of long-term commitments established with third parties, such as supply

contracts with suppliers or customers, are recognized in the financial statements on an incurred or accrued basis, after taking into consideration the

substance of the agreements. Relevant commitments are disclosed in the notes to the financial statements. CEMEX, S.A.B. de C.V. recognizes

contingent revenues, income or assets only when their realization is virtually certain.

3.11) PENSIONS AND OTHER POST-EMPLOYMENT BENEFITS (note 20)

Defined contribution pension plans

The costs of defined contribution pension plans are recognized in the operating results as they are incurred. Liabilities arising from such plans are

settled through cash transfers to the employees’ retirement accounts, without generating future obligations.

Defined benefit pension plans and other post-employment benefits

The costs associated with employees’ benefits for defined benefit pension plans and other post-employment benefits, generally comprised of health

care benefits, life insurance and seniority premiums, granted by CEMEX, S.A.B de C.V and/or pursuant to applicable law, are recognized as services

are rendered by the employees based on actuarial estimations of the benefits’ present value considering the advice of external actuaries. For certain

pension plans, CEMEX, S.A.B de C.V has created irrevocable trust funds to cover future benefit payments (“plan assets”). These plan assets are valued

at their estimated fair value at the statement of financial position date. The actuarial assumptions and accounting policy consider: a) the use of nominal

rates; b) a single rate is used for the determination of the expected return on plan assets and the discount of the benefits obligation to present value; c)

a net interest is recognized on the net defined benefit liability (liability minus plan assets); and d) all actuarial gains and losses for the period, related

to differences between the projected and real actuarial assumptions at the end of the period, as well as the difference between the expected and real

return on plan assets, are recognized as part of “Other items of comprehensive income, net” within stockholders’ equity.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

13

Property, machinery and equipment, assets for the right-of-use and other investments – continued

The service cost, corresponding to the increase in the obligation for additional benefits earned by employees during the period, is recognized within

operating costs and expenses. The net interest cost, resulting from the increase in obligations for changes in NPV and the change during the period in

the estimated fair value of plan assets, is recognized within “Financial income and other items, net.”

The effects from modifications to the pension plans that affect the cost of past services are recognized within operating costs and expenses over the

period in which such modifications become effective to the employees or without delay if changes are effective immediately. Likewise, the effects

from curtailments and/or settlements of obligations occurring during the period, associated with events that significantly reduce the cost of future

services and/or significantly reduce the population subject to pension benefits, respectively, are recognized within operating costs and expenses.

Termination benefits

Termination benefits, not associated with a restructuring event, which mainly represent severance payments by law, are recognized in the operating

results for the period in which they are incurred.

3.12) INCOME TAXES

(note 21)

The effects reflected in the statement of operations for income taxes include the amounts incurred during the period and the amounts of deferred income

taxes, determined according to the income tax law applicable, reflecting uncertainty in income tax treatments, if any. Deferred income taxes represent

the addition of the amounts determined by applying the enacted statutory income tax rate to the total temporary differences resulting from comparing

the book and taxable values of assets and liabilities, considering tax assets such as loss carryforwards and other recoverable taxes, to the extent that it

is probable that future taxable profits will be available against which they can be utilized. The measurement of deferred income taxes at the reporting

period reflects the tax consequences that follow the way in which CEMEX, S.A.B. de C.V. expects to recover or settle the carrying amount of its assets

and liabilities. Deferred income taxes for the period represent the difference between balances of deferred income taxes at the beginning and the end

of the period. According to IFRS, all items charged or credited directly in stockholders’ equity or as part of other comprehensive income or loss for the

period are recognized net of their current and deferred income tax effects. The effect of a change in enacted statutory tax rates is recognized in the

period in which the change is officially enacted.

Deferred tax assets are reviewed at each reporting date and are derecognized when it is not deemed probable that the related tax benefit will be realized,

considering the aggregate amount of self-determined tax loss carryforwards that CEMEX, S.A.B. de C.V. believes will not be rejected by the tax

authorities based on available evidence and the likelihood of recovering them prior to their expiration through an analysis of estimated future taxable

income. If it is probable that the tax authorities would reject a self-determined deferred tax asset, CEMEX, S.A.B. de C.V. would derecognize such asset.

When it is considered that a deferred tax asset will not be recovered before its expiration, CEMEX, S.A.B. de C.V. would not recognize such deferred tax

asset. Both situations would result in additional income tax expense for the period in which such determination is made. To determine whether it is

probable that deferred tax assets will ultimately be recovered, CEMEX, S.A.B. de C.V. takes into consideration all available positive and negative

evidence, including factors such as market conditions, industry analysis, expansion plans, projected taxable income, carryforward periods, current tax

structure, potential changes or adjustments in tax structure, tax planning strategies, future reversals of existing temporary differences. Likewise,

CEMEX, S.A.B. de C.V. analyzes its actual results versus the Parent Company’s estimates, and adjusts, as necessary, its tax asset valuations. If

actual results vary from CEMEX, S.A.B. de C.V.’s estimates, the deferred tax asset and/or valuations may be affected, and necessary adjustments

will be made based on relevant information in CEMEX, S.A.B. de C.V.’s statement of operations for such period.

Based on IFRIC 23, Uncertainty over income tax treatments (“IFRIC 23”), the income tax effects from an uncertain tax position are recognized when it is

probable that the position will be sustained based on its technical merits and assuming that the tax authorities will examine each position and have full

knowledge of all relevant information. For each position probability is considered individually, regardless of its relationship to any other broader tax

settlement. The probability threshold represents a positive assertion by management that CEMEX, S.A.B. de C.V. is entitled to the economic benefits of a

tax position. If a tax position is considered not probable of being sustained, no benefits of the position are recognized. Interest and penalties related to

unrecognized tax benefits are recorded as part of the income tax in the statements of operations.

The effective income tax rate is determined dividing the line item “Income tax” by the line item “Net income before income tax.” This effective tax rate

is further reconciled to CEMEX, S.A.B. de C.V.’s statutory tax rate applicable in Mexico (note 21).

3.13) STOCKHOLDERS’ EQUITY

Common stock and additional paid-in capital (note 22.1)

These items represent the value of stockholders’ contributions, and include increases related to the capitalization of retained earnings and the recognition

of executive compensation programs in CEMEX, S.A.B. de C.V.’s CPOs as well as decreases associated with the restitution of retained earnings.

CEMEX, S.A.B. DE C.V.

Notes to the Parent Company-only Financial Statements

As of December 31, 2022, 2021 and 2020

(Millions of Mexican Pesos)

14

Other equity reserves and subordinated notes

(note 22.3)

Groups the cumulative effects of items and transactions that are, temporarily or permanently, recognized directly to stockholders’ equity, and includes

the comprehensive income, which reflects certain changes in stockholders’ equity that do not result from investments by owners and distributions to

owners.

Beginning in June 2021, this line item includes the balance of subordinated notes with no fixed maturity issued by CEMEX, S.A.B. de C.V. Considering

that CEMEX, S.A.B. de C.V.’s subordinated notes have no fixed maturity date, there is no contractual obligation for CEMEX, S.A.B. de C.V. to deliver

cash or any other financial assets, the payment of principal and interest may be deferred indefinitely at the sole discretion of CEMEX, S.A.B. de C.V.

and specific redemption events are fully under CEMEX, S.A.B. de C.V.’s control, under applicable IFRS, these subordinated notes issued by CEMEX,

S.A.B. de C.V. qualify as equity instruments and are classified within controlling interest stockholders’ equity.

The most significant items within “Other equity reserves and subordinated notes” during the reported periods are as follows:

Items of “Other equity reserves and subordinated notes” included within other comprehensive income (loss):

The effective portion of the valuation and liquidation effects from derivative instruments under cash flow hedging relationships, which are recorded

temporarily in stockholders’ equity (note 3.5);

Changes in fair value of other investments in strategic securities (note 3.5); and

Current and deferred income taxes during the period arising from items whose effects are directly recognized in stockholders’ equity.

Items of “Other equity reserves and subordinated notes” not included in comprehensive income (loss):

Effects attributable to controlling stockholders’ equity for financial instruments issued by consolidated subsidiaries that qualify for accounting

purposes as equity instruments, such as the interest expense paid on perpetual debentures;

The balance of subordinated notes with no fixed maturity and any interest accrued thereof; and

The cancellation of CEMEX, S.A.B. de C.V.’s shares held by consolidated entities.

Retained earnings (note 22.2)

Retained earnings represent the cumulative net results of prior years, net of: a) dividends declared; b) capitalization of retained earnings; c) restitution

of retained earnings when applicable; and d) cumulative effects from adoption of new IFRS.

3.14) REVENUE RECOGNITION (note 4)

Revenue is recognized at a point in time or over time in the amount of the price, before tax on sales, expected to be received for goods and services

supplied because of ordinary activities, as contractual performance obligations are fulfilled, and control of goods and services passes to the customer.

Revenues are decreased by any trade discounts or volume rebates granted to customers. Variable consideration is recognized when it is highly probable

that a significant reversal in the amount of cumulative revenue recognized for the contract will not occur and is measured using the expected value or

the most likely amount method, whichever is expected to better predict the amount based on the terms and conditions of the contract.

Revenue and costs from trading activities, in which CEMEX, S.A.B. de C.V. acquires finished goods from a third party and subsequently sells the

goods to another third-party, are recognized on a gross basis, considering that CEMEX, S.A.B. de C.V. assumes ownership risks on the goods purchased,

not acting as agent or broker.

Commencing August 2021, in connection with the corporate reorganization (notes 2 and 14.1), CEMEX, S.A.B. de C.V., recognizes revenue from

operating leases of some of its property, machinery, and equipment to CEMEX Operaciones México, S.A. de C.V., and CEMEX Concretos, S.A. de

C.V. subsidiaries of the Parent Company.

When revenue is earned over time as contractual performance obligations are satisfied, which is the case of construction contracts, CEMEX, S.A.B. de

C.V. applies the stage of completion method to measure revenue, which represents: a) the proportion that contract costs incurred for work performed

to date bear to the estimated total contract costs; b) the surveys of work performed; or c) the physical proportion of the contract work completed;

whichever better reflects the percentage of completion under the specific circumstances. Revenue related to such construction contracts is recognized

in the period in which the work is performed by reference to the contract’s stage of completion at the end of the period, considering that the following

have been defined: a) each party’s enforceable rights regarding the asset under construction; b) the consideration to be exchanged; c) the manner and

terms of settlement; d) actual costs incurred and contract costs required to complete the asset are effectively controlled; and e) it is probable that the

economic benefits associated with the contract will flow to the entity.