2023 Dividend Scale

Key points & frequently asked questions

Key points

•

Dividends are based on the performance of participating policies, including investment returns, mortality, persistency

and expenses, among other factors and are therefore not guaranteed.

See questions Q, Q and Q for additional details.

•

Despite the recent increase in investment rates, the sustained low interest rate environment over the past several years continues to

contribute to the low dividend scale interest rates across the industry. Any investment rate increase will not have an immediate impact

on dividends due to the portfolio method used. Dividend scale interest rates should not be confused with internal rates of return or

conventional interest rates.

See question questions Q5 and Q for additional details.

•

The decrease in the 2023 projected dividend payout is driven by the drop in dividend scales for some open and closed block policies.

See question Q for additional details.

•

Dividends are not guaranteed and will change from year to year.

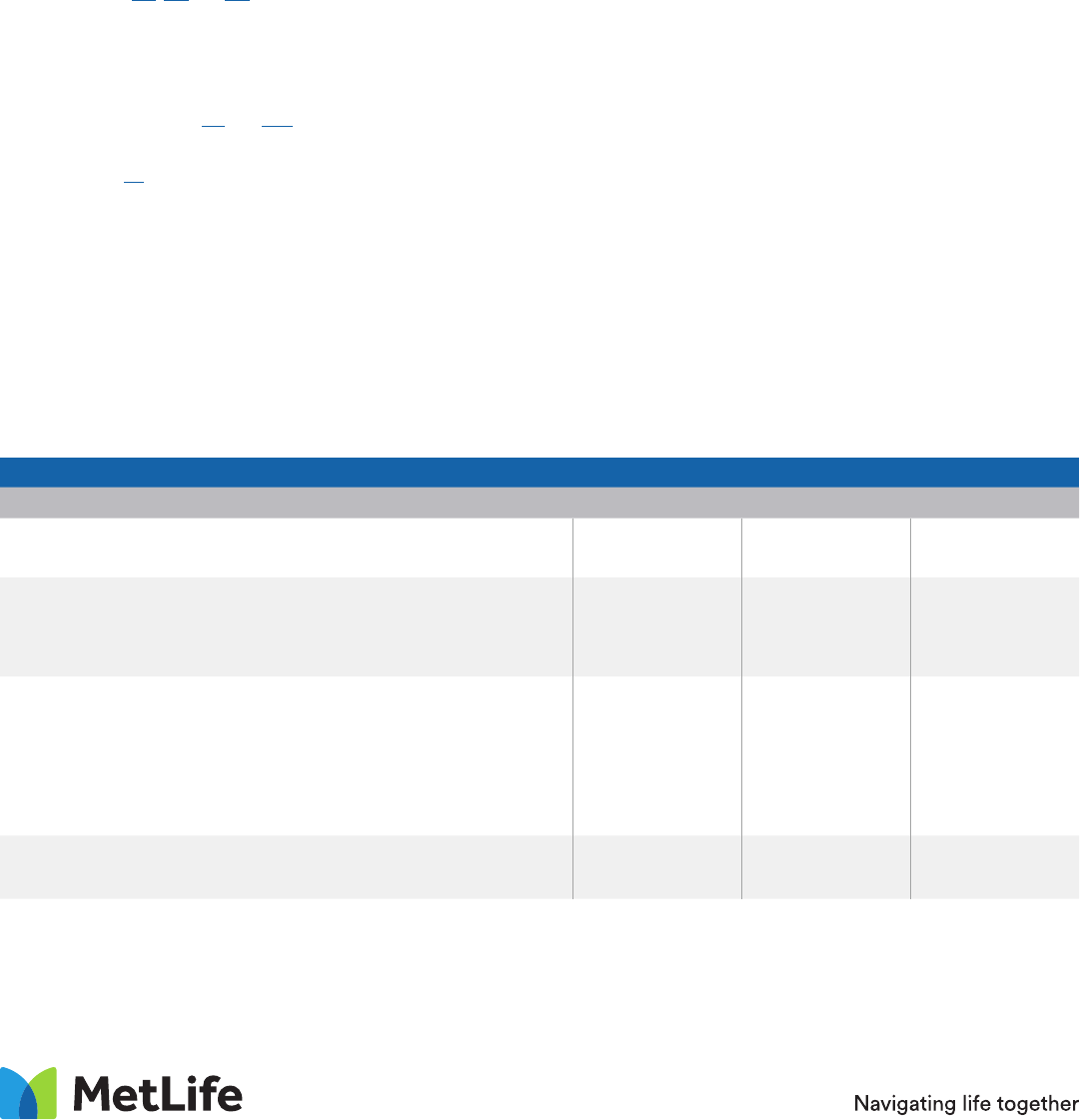

Dividend scale

Q. What are the 2023 dividend scale interest rates?

A. MetLife

1

expects to pay a total of approximately $530 million in dividends to eligible life insurance policyholders in 2023. The sustained

low interest rate environment from past years continues to affect our investment experience and has adversely impacted the dividends

for our products. During 2022, interest rates began to rise but it will take time for the increasing rate environment to offset the years

of low returns in order to have an impact on our portfolio returns. Nevertheless, MetLife’s disciplined approach to managing risk

and making sound financial decisions enables us to continue our long history of providing these payments to our participating life

insurance policyholders.

Life | Whole

Dividend Scale Interest Rates

2022 2023 Change

Metropolitan Life Insurance Company

•

MetLife Promise Whole Life

SM

products in NY 4.25% 4.00% -0.25%

Open block of business policies, excluding the MetLife Promise

Whole Life products:

•

MetLife Whole Life 2008

•

1980 CSO inforce policies

4.05%

3.80%

4.05%

3.80%

0.00%

0.00%

Closed block of business policies:

•

For ordinary policies issued in 1982 and later

•

For ordinary policies issued before 1982

•

For industrial policies, which were only issued before 1965

•

For policies originally issued by New England Mutual Life

Insurance Company before the merger with Metropolitan

Life Insurance Company

2

4.35%

4.00–4.35%

5.85%

5.25%

3.85%

3.50–3.85%

5.85%

4.75%

-0.50%

-0.50%

0.00%

-0.50%

Metropolitan Tower Life Insurance Company

•

For inforce whole life policies 4.25% 4.00% -0.25%

FOR PRODUCER USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

1. “MetLife” consists of Metropolitan Life Insurance Company and Metropolitan Tower Life Insurance Company, all of which are wholly owned subsidiaries of MetLife, Inc.

This amount is expected to be declared by the boards of directors of the issuing companies in February 2023.

2. These rates are based on a gross dividend scale rate, all other products shown are based on a net dividend scale rate.

Q. Did anything other than interest rates change in the 2023 dividend scale?

A. Yes.

Improvements in the mortality experience for some MetLife Whole Life dividend classes were reflected in the 2023 dividend scale.

Q. Why did MetLife change only some of its 2023 dividend scale interest rates?

A. MetLife remains strong and well positioned to provide the protection that our customers have come to expect. There are numerous

blocks of policies, like the closed block established at the time of demutualization, that are backed by separate assets.

Each block’s assets are managed separately, causing them to have slightly different performance over time, which results in different

dividend scale interest rates. For more information on how the dividend scale interest rate is calculated, please see Q5.

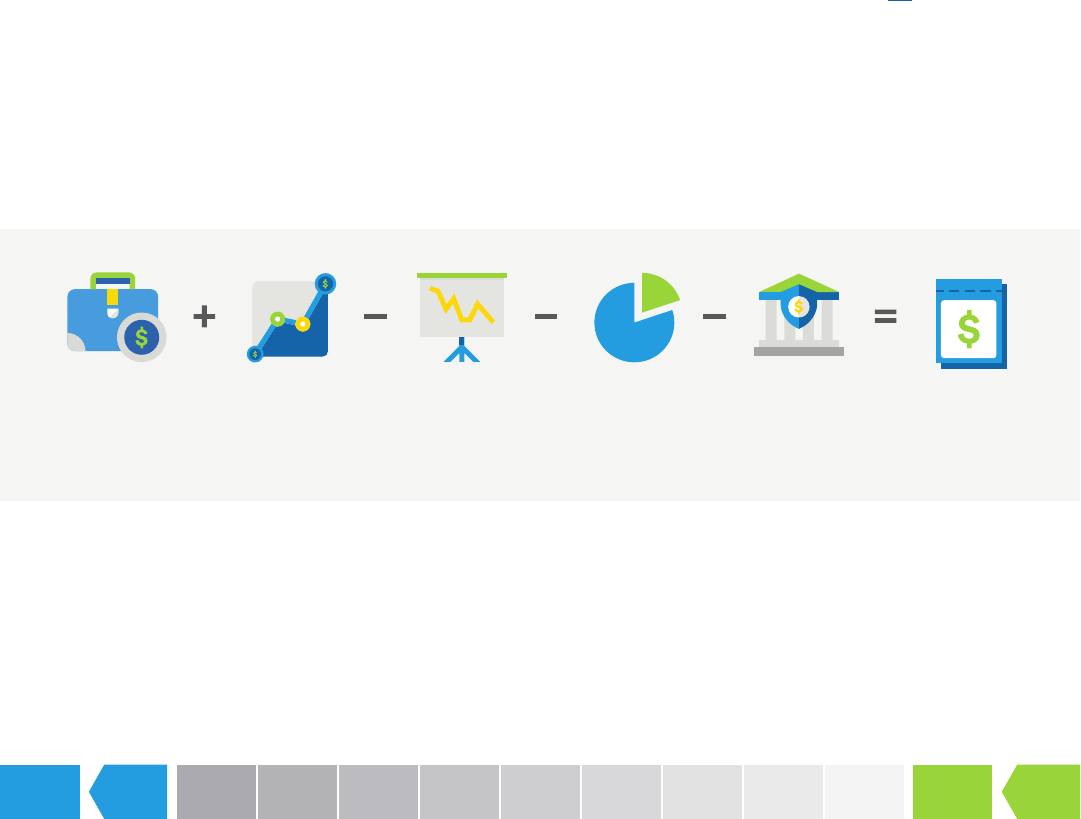

Q. How does MetLife determine if a dividend should be paid?

A. When MetLife sells a specific product, it’s usually grouped together into larger blocks of similar products that are issued by the same

issuing company. Combining similar products allows us more investment flexibility and to manage our risks better. MetLife reviews its

financial performance throughout the year in order to understand how earnings are emerging for our various blocks of business. Several

variables like premium income, investment, mortality charges, etc. are used to determine the amount available for dividends. If a block of

business is performing better than expected and has made a profit, we take those earnings and spread them across all the policies within

the block of business that have contributed to that profit.

MetLife’s dividend scale is set annually based on this formula:

Q. What will happen to the dividend scale in future years?

A. The dividend scale is determined by MetLife each year using factors that can vary over time. As a result, dividends can fluctuate from year

to year and are never guaranteed.

Q. How does MetLife calculate the dividend scale interest rate?

A. MetLife uses the portfolio method to determine the interest rate used in the dividend formula. The portfolio yield (interest rate) is based

on the average yield of all investments within it. As one block of investments matures, it is replaced with a new block of investments

yielding a current market rate. If the new block of investments has a lower yield than the block that matured, then the total average

portfolio yield will decrease, as has been the case in recent years. The overall impact of using the portfolio method is that as rates drop,

the portfolio rate won’t drop as quickly. But, in an environment where rates are increasing, this will also mean that the dividend rate will

not increase as quickly as new business rates do.

Here’s a hypothetical example:

Blocks of investments

5.6% OUT 5.35% 5.1% 4.6% 4.6% 4.25% 4.25% 3.75% 3.75% 3.50% 4.0% IN

10

years old

9

years old

8

years old

7

years old

6

years old

5

years old

4

years old

3

years old

2

years old

1

year old

Replacement

block

FOR PRODUCER USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

*For future claims and expenses.

Premium income Investment Mortality charges Expenses Changes in

reserves*

Amount available

for dividends

Dividends 101

Q. What is a dividend scale?

A. A dividend scale is a figure used by insurance companies to calculate the dividends to be paid for owners of participating policies.

The dividend scale is created as a means to fairly distribute annual dividends. It is reviewed annually to determine the current financial

standing of the insurance company’s different blocks of business. Factors affecting a dividend scale can include changes in interest rates,

expenses, mortality experience, and even taxes.

Q. How are dividends calculated for a policy?

A. The actual dividend credited to a policy is dependent on a number of factors including the product the policyholder purchased,

the issue age of the policyholder, the policyholder’s current age and policy duration, the face amount of the policy, as well as a host

of other categories. For any given dividend scale, rates per thousand of face amount are determined for all the combinations of these

factors. These rates are then used to determine a given policy’s dividend for that scale year.

At a high level, we typically use the following formula:

Base Dividend = Base Dividend Rate x [Base Face Amount of Insurance/1000]

The dividend paid out may be affected if you have a loan on the policy.

Q. How might a dividend scale change impact a policy?

A. Each dividend is typically set based on assumptions for mortality, interest and expenses for every combination of factors like product,

age, sex, duration, face amount and smoker status. For this reason, each policy may react differently to any given scale change. This

means there’s no easy way to determine the impact on any given policy without looking at that policy in detail. However, there are some

basic concepts that could be helpful.

The younger a policy is in its life cycle (ex. the policy is 10 years old), the more important the mortality component can be within

the dividend calculation. What this means is that if a mortality change is announced, it will likely have a bigger impact to the dividend

for policies that are in their early durations.

The older a policy is in its life cycle (ex. the policy is 30 years old), the more important the investment component can be within the

dividend calculation. What this means is that if the investment component changes, it will likely have a bigger impact to the policy’s

dividend if the policy is older.

Q. Is a Dividend Scale Interest Rate the same as a credited rate on a Universal Life policy?

A. No.

In a Universal Life type policy, the credited rate acts in a manner similar to how an interest rate works for a bank account. Generally

speaking, the rate is applied monthly to the policy’s fund balance less any charges, and then interest is credited to the fund.

For a policy with dividends, the investment component of a dividend is only one of several components. This means that this part of the

dividend only contributes to some of the total dividend. Also, a dividend can be thought of as a return of premium for good experience

in excess of what we thought might happen when we priced a product. For the investment component specifically, we typically look at

the investment earnings in excess of any guarantees we provide for within the guaranteed cash value. This is very different from crediting

interest to a fund balance.

FOR PRODUCER USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

FOR PRODUCER USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Metropolitan Life Insurance Company | 200 Park Avenue | New York, NY 10166

BDWL230912-3 L1122027009[exp1123][All States][DC] © 2022 MetLife Services and Solutions, LLC.

The 2023 dividend scale has received preliminary approval from the boards of directors of the issuing companies. It is expected to receive final

approval in February 2023.

Life insurance policies contain exclusions, limitations and conditions for keeping the policies in force.

Whole Life Insurance Products:

Not A Deposit • Not FDIC-Insured • Not Insured By Any Federal Government Agency • Not Guaranteed By Any Bank Or Credit Union

Policy impact

Q. How can dividends help policyholders?

A. Dividends can be an important product design element in participating policies because they can enhance the overall value of the policy.

Many life insurance contracts allow for a policyholder to use their dividend in a variety of ways. These could include any or all of the

following dividend options:

•

Accelerated payment or premium reduction — dividends are applied toward the payment of the premium and in some instances

may cover the entire annual premium.

•

Additional paid-up insurance or term insurance — dividends are used to purchase additional paid-up life insurance or term

insurance under a rider, increasing the overall death benefit.

•

Paid in cash — a check is sent to the client for the full amount of the dividend.

•

Dividends to accumulate with interest — dividends are left on deposit with MetLife. The total value of the dividends plus interest,

is either added to the death benefit at death or to the cash value at surrender.

•

Repay policy loans — dividends are used to repay loan principal or loan interest.

Tax treatment may vary depending on the option you choose. Consult a tax advisor for details.

Q. How can inforce clients currently on accelerated payment (AP) see how the 2023 dividend scale change impacts their policy?

A. Running inforce illustrations will help clients better understand whether the 2023 dividend scale impacts their policy. Please keep

in mind that illustrations assume that the 2023 dividend scale interest rate will not change for the life of the policy, which is unlikely.

Therefore, it is also advisable to run an illustration at a lower dividend scale interest rate to show how potential future dividend changes

could impact their policy.

Q. Are dividends guaranteed?

A. No.

Neither dividends in general nor the current dividend scale is guaranteed. The assumptions on which the current dividend scale

is based are subject to change by MetLife. Actual results may be more or less favorable.

Illustrations

Q. When will the illustration systems be updated?

A. The illustration software will be updated over the weekend of November 18, 2022 with the new 2023 dividend scale interest rates.

The 2023 dividend scale interest rates are preliminary and are subject to the actions of the Boards of Directors of each company in

February, 2023

New illustration software must be installed as soon as it is received. The use of prior versions after a new version has

been released is prohibited.

For any policy whose scale has changed we recommend that a policyholder request a new illustration.