Medium- & Heavy-Duty Vehicles

Market structure, Environmental Impact, and EV Readiness

July 2021

2

Contents

Executive Summary ................................................................................................................................... 4

M/HDV In-Use Fleet: Vehicle Types & Uses ........................................................................................... 8

M/HDV In-Use Fleet: Environmental Impact ........................................................................................ 13

M/HDV EV Market Readiness ................................................................................................................ 16

Policy Implications .................................................................................................................................. 24

Appendix A – Methodology & Data Sources .......................................................................................... 26

Appendix B – Supplemental Information ................................................................................................ 37

References ................................................................................................................................................ 40

3

Acknowledgements

Lead Authors: Dana Lowell and Jane Culkin

This report summarizes an analysis of the U.S. medium and heavy-duty in-use truck fleet to identify the

most common vehicle types/uses, estimate the environmental impact of each, and assess near-term

readiness for greater adoption of electric vehicles based on typical usage patterns and market status. For

this analysis we have included all vehicles with gross vehicle weight rating (GVWR) above 8,500 pounds,

encompassing vehicle classes from Class 2b (8,500 – 10,000 lb GVWR) to Class 8 (>33,000 lb GVWR).

Totaling 22.8 million vehicles that annually travel more than 430 billion miles and consume more than

55 billion gallons of fuel, this is a very diverse group, ranging from heavy-duty pickups and vans to transit

and school buses, freight and work trucks, and tractor-trailers. Most of these vehicles are used

commercially, rather than for personal transportation.

This report was developed by M.J. Bradley & Associates for the Environmental Defense Fund (EDF).

About M.J. Bradley & Associates

MJB&A, an ERM Group company, provides strategic consulting services to address energy and

environmental issues for the private, public, and non-profit sectors. MJB&A creates value and addresses

risks with a comprehensive approach to strategy and implementation, ensuring clients have timely access

to information and the tools to use it to their advantage. Our approach fuses private sector strategy with

public policy in air quality, energy, climate change, environmental markets, energy efficiency, renewable

energy, transportation, and advanced technologies. Our international client base includes electric and

natural gas utilities, major transportation fleet operators, investors, clean technology firms, environmental

groups and government agencies. Our seasoned team brings a multi-sector perspective, informed

expertise, and creative solutions to each client, capitalizing on extensive experience in energy markets,

environmental policy, law, engineering, economics and business. For more information we encourage

you to visit our website, www.mjbradley.com.

© M.J. Bradley & Associates, an ERM Group company, 2021

For questions or comments, please contact:

Dana Lowell

Senior Vice President

M.J. Bradley & Associates, LLC

+1 978 369 5533

This report is available at www.mjbradley.com.

4

Executive Summary

This report summarizes an analysis of the U.S. medium and heavy-duty (M/HD) in-use truck fleet to

identify the most common vehicle types/uses, estimate the environmental impact of each, and assess

readiness for greater adoption of zero emitting technologies over the next decade, based on typical usage

patterns and market status. It is intended to help inform the Environmental Protection Agency’s

deliberations involving future criteria and greenhouse gas emissions standards and policies for medium-

and heavy-duty engines and vehicles.

This analysis focuses on prospects for electric vehicle penetration because all scenarios for avoidance of

detrimental future climate warming point to the need for significant reductions in emissions from the

transportation system, coupled with further decarbonization of the electric sector. Net reductions in

transportation emissions could come from a range of zero-emitting vehicle types including battery-

electric vehicles and hydrogen fuel cell electric vehicles. For this study, MJB&A evaluated the current

state of battery electric vehicles for each M/HDV market segment, to assess prospects for near-term

(through 2025) and medium-term (through 2030) uptake of zero-emission vehicles within each segment.

While fuel cell vehicles could also play a role in transforming the transportation system within this

timeframe, the focus of this report on battery electric vehicles is based on the relatively greater

commercial maturity of this technology in the U.S. market

Also, while comprising less than 10 percent of all vehicles on the road, M/HD trucks account for more

than 60 percent of tailpipe nitrogen oxide (NOx) and particulate (PM) emissions from the onroad fleet

1

;

these emissions contribute to poor air quality in many urban areas, including areas with vulnerable

populations. Deploying zero-emitting vehicles coupled with greater use of renewable electricity will

provide significant public health benefits by reducing urban air pollution. A recent study indicates that

eliminating tailpipe emissions from new medium- and heavy-duty vehicles by 2040 could provide up to

$485 billion in health and environmental benefits as a result of pollution reductions (2020$)

2

.

For this analysis we have included all vehicles with gross vehicle weight rating (GVWR) above 8,500

pounds, encompassing vehicle classes from Class 2b (8,500 – 10,000 lb GVWR) to Class 8 (>33,000 lb

GVWR).

Totaling 22.8 million vehicles that annually travel more than 430 billion miles and consume more than

55 billion gallons of fuel, this is a very diverse group, ranging from heavy-duty pickups and vans to transit

and school buses, freight and work trucks, and tractor-trailers. Most of these vehicles are used

commercially, rather than for personal transportation.

While very diverse, approximately 80 percent of the fleet can be grouped into 17 market segments each

with broadly similar vehicle configuration and usage patterns; these 17 market segments are the focus of

this analysis

3

.

1

Per EPA MOVES model emissions inventory.

2

EDF, Clean Trucks, Clean Air, American Jobs, March 2021; https://www.edf.org/sites/default/files/2021-

03/HD_ZEV_White_Paper.pdf

3

The remaining 20 percent of the fleet encompasses a wider diversity of vehicle types and uses, some of which

includes a relatively small number of vehicles. This includes Fire Trucks, ambulances and other emergency

vehicles, Motor Homes, and trucks used in Forestry and Mining. It also includes vehicles that could not be

classified based on VIN-defined vehicle type or the type of company that registered them. See Appendix A for

more information about how the market segments were determined and number of vehicles in each was estimated.

5

For each market segment the number of vehicles

in the segment was estimated using registration

data collected from all 50 states by IHS Markit

[1]. EPA’s MOtor Vehicle Emissions Simulator

(MOVES3) model [2] was used to estimate the

environmental impact of each market segment –

from both a climate and air quality perspective.

Various resources and considerations were then

used to evaluate prospects for near-term uptake of

battery-electric vehicles within each market

segment, as a proxy for uptake of zero-emission

vehicles more generally.

Each market segment was evaluated based on

four relevant factors that will significantly impact

truck owner decisions about whether to purchase

an electric vehicle: availability of electric models

from major manufacturers (Commercial EV

Market), infrastructure requirements for vehicle

charging (Charging), the ability of current EV

models to meet operating requirements

(Technical Feasibility), and prospects for cost

parity with current diesel and gasoline vehicles

(EV Business case). See the appendix for a full

discussion of the methodology and data sources

used for the EV market readiness analysis.

The analysis finds that there are a large number of

market segments that have favorable ratings

across at least 3 of the 4 relevant factors, which

indicates strong potential for near-term EV

uptake

4

. Representing approximately 66 percent of the current in-use fleet, these market segments include

Heavy-duty Pickups and Vans, Local Delivery and Service Trucks and Vans, Transit and School Buses,

Class 3 - 5 Box Trucks, Class 3 – 7 Stake Trucks, Dump Trucks, and Refuse Haulers. Electrifying these

vehicles would deliver significant public health benefits – including up to 1,500 fewer premature deaths,

1,400 fewer hospital visits, and 890,000 incidents of exacerbated respiratory conditions and lost or

restricted workdays annually. Additional major take-aways from the full analysis are summarized below

and are discussed more fully in the following sections.

4

While not formally evaluated, other zero-emitting technologies such as hydrogen fuel cell electric vehicles could

also play an important role in many market segments.

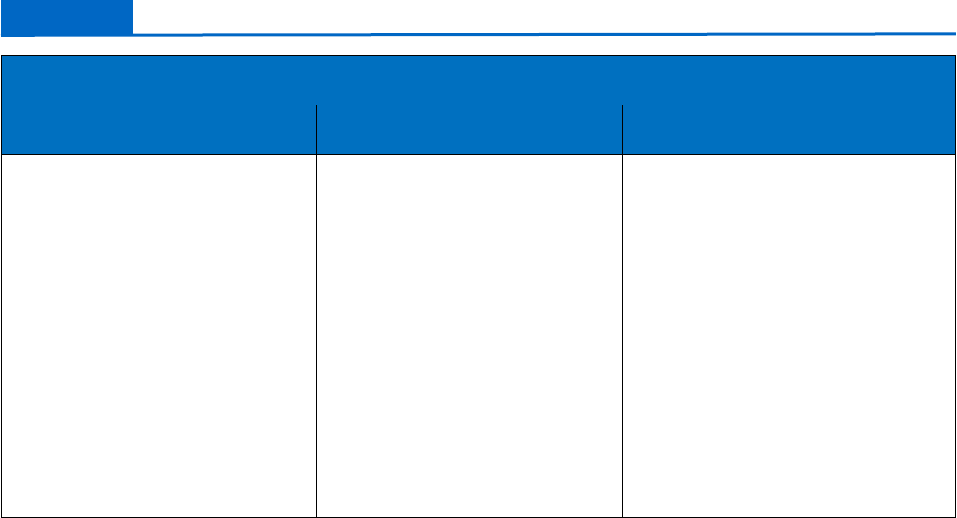

Class 2B

Class 3

Regional Haul Tractor Class 7 - 8

Long Haul Tractor Class 8

Transit Bus Class 8

School Bus Class 7

Shuttle Bus Class 3-5

Delivery Van Class 3-5

Delivery Truck Class 6-7

Service Van Class 3-5

Service Truck Class 6-7

Refuse Hauler Class 8

Box Truck (freight) Class 3-5

Box Truck (freight) Class 6-7

Box Truck (freight) Class 8

Stake Truck (construction) Class 3-5

Stake Truck (construction) Class 6-7

Dump Truck Class 8

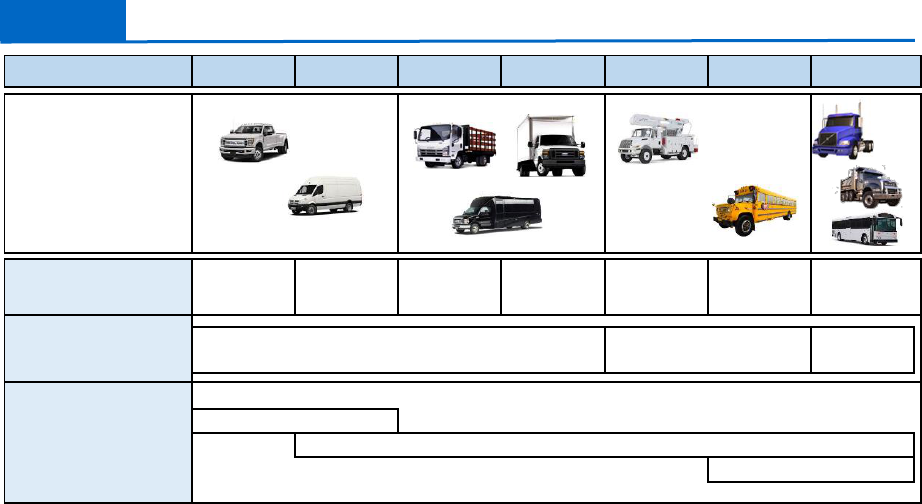

MARKET SEGMENT

Weight

Class

Heavy Duty Pickup & Van

Figure 1

M/HD Market Segments

6

Climate

While less than 15% of vehicles, long- and regional-haul

tractor-trailers have the greatest climate impact - accounting

for 60% of greenhouse gases - due to their high annual

mileage.

The second most important market segment is heavy-duty

pickups and vans (Class 2b – 3) which account for more

than 20% of GHGs because there are so many of them.

Air Quality

Market segments with the highest relative impact on

urban air quality – NOx and PM emissions relative to

the number of vehicles and miles traveled – include

buses of all types, tractor-trailers, refuse trucks, heavy

freight trucks, and construction trucks

EV Market

The market segments that can be considered fully

mature in 2021 with respect to commercial EV offerings

are transit and school buses.

While most other M/HDV market segments currently

have few commercial EV models from key market

actors, they are seeing rapidly increasing activity from

established players and well-financed start-ups.

Virtually all market segments have the potential to be

fully mature by 2025, with EV models available from multiple companies, including

the majority of major OEMs that currently have 90% market share of the in-use fleet.

A number of companies have near-term plans to launch light-duty electric pickups

and vans (<8,500 lb GVWR), including the market leader Ford. Developments in

this market can help to advance electrification of the heavier Class 2B (8,500 –

10,000 lb GVWR) segment of the M/HD market

Charging

The majority of M/HDVs have relatively modest

charging needs (<20 kW/vehicle) and can do most if not

all charging overnight at their “home base”

Developing additional fueling infrastruture is needed

for wide adoption of zero-emitting long-haul freight

trucks, as those vehicles will require a nation-wide

network of high-power shared (public) chargers (for

battery electric trucks) or hydrogen fuel stations (for fuel

cell electric trucks).

80% of Climate

impact is from

three of the 17

market segments

Air quality impact is

less concentrated

among market

segments than

climate impact

In Most market

segments the EV

market is emerging

with the potential to

be fully

commercially

mature by 2025.

Most M/HD EVs can

be charged

overnight at their

“home base” and

will not need public

chargers

7

$

EV Business

Case

The current cost of M/HD EVs present some challenges

for the business case, but projected cost reductions will

substantially improve EV economics in all market

segments over the next 10 years. Increased EV sales

volumes will accelerate expected cost reductions.

EVs in the majority of market segments have the

potential to achieve life-cycle cost parity with internal

combustion engine vehicles by model year 2025 or

earlier if M/HD battery costs follow a similar trajectory

as battery costs for light-duty EVs.

Policy

Implications

Vehicle segments for near-term ZEV policy focus include

School and Transit buses – mature ZEV market, high urban air quality

impact, high visibility

Urban delivery and service fleets (Class 3 – 5), to include vans and box

trucks of variuous sizes – duty cycle matches EV capability, low charging

barriers, large number of vehicles which can advance techical and

commercial development

Heavy-duty Pickups and Vans (Class 2B) – duty cycle generally matches EV

capability, generally low charging barriers, large number of vehicles which

can advance techical and commercial development

Construction trucks, including Class 3 -7 Stake Trucks, and Dump Trucks –

high urban air quality impact, generally low charging barriers

Refuse Haulers - high urban air quality impact, high visibility

For most Market

Segments the EV

business case

remains

challenging but is

improving rapidly in

a very dynamic

market

8

M/HDV In-Use Fleet: Vehicle Types & Uses

This section discusses the composition of the current M/HD fleet, including the number of vehicles of

each type/use, the percentage of vehicles by fuel type, and manufacturer market shares.

Under EPA’s Phase 2 rules, GHG emissions are regulated both from new engines and from new vehicles

[3]. Engine standards are separated into three categories: those applicable to light-heavy duty engines

(LHD) used in Class 2b – Class 5 trucks, those applicable to medium-heavy duty engines (MHD) used in

Class 6 – 7 trucks, and those applicable to heavy-heavy duty (HHD) engines used in Class 8 trucks.

Vehicle regulations are separated into three vehicle categories: those applicable to Heavy-duty Pickups

and Vans (Class 2b – 3), those applicable to Combination Truck tractors (Class 7 – 8), and those

applicable to all other trucks that are not in either of the first two categories, which are called Vocational

Vehicles. The vocational vehicle category is very diverse, covering vehicles from Class 3 to Class 8 with

a wide range of uses, from freight trucks, to buses, to construction and other work trucks; see Figure 2

Source: U.S. Environmental Protection Agency

Given the diversity of the Vocational Vehicle Category it is further divided by the characteristics of the

duty cycle seen by “typical” vehicles. The defined duty cycles are Urban (low speed, frequent stops),

Regional (higher speeds, less frequent stops) and Mixed Use (a combination of Urban and Regional duty

cycles). Vehicles regulated under the different duty cycles are subject to different regulatory test cycles

that reflect the chosen duty cycle and subsequently have different numerical emission limits.

Manufacturers are allowed to specify the duty cycle used to certify each Vocational Vehicle model.

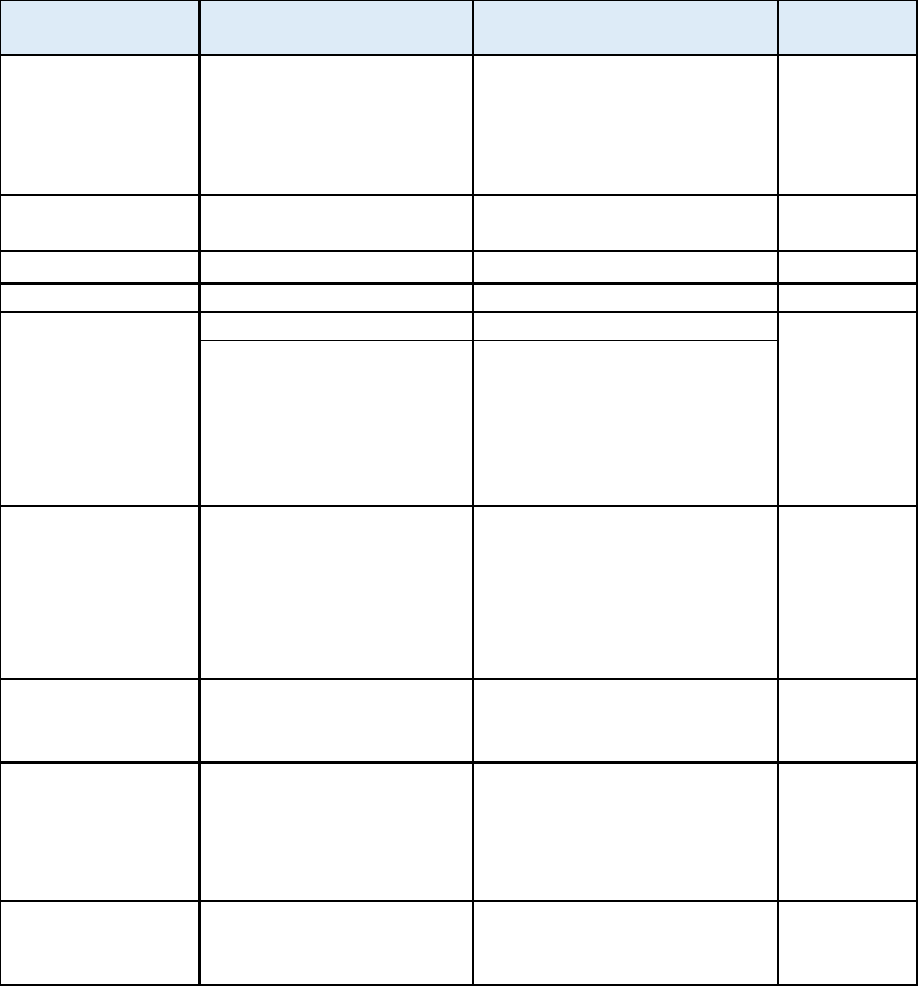

See Figure 3 for a summary of the M/HDV market segments analyzed here, and the estimated number of

in-use vehicles in each. Each market segment is identified by vehicle type and weight class range. Also

included is information on the EPA vehicle and engine regulatory category that the vehicles in the

segment are covered by, for the purposes of regulating new engine and vehicle fuel economy and

greenhouse gas emissions.

Figure 2

Vehicle Weight Classes and EPA Regulatory Categories

Weight Class 2b 3 4 5 6 7 8

GVWR (lb)

8,500 to

10,000

10,001 to

14,000

14,001 to

16,000

16,001 to

19,500

19,501 to

26,000

26,001 to

33,000

>33,000

Engine Regulatory

Category

Heavy Heavy-

Duty

Medium Heavy-duty

Vehicle Regulatory

Category

Heavy Duty Pickup & van

Combination Trucks

Vocational Trucks

Light Heavy-Duty

Example Vehicles

9

For most market segments the estimated number of vehicles shown in Figure 3 is based on an analysis of

state vehicle registration data collected by IHS Markit [1]. For this analysis all in-use vehicles were

categorized based on manufacturer-defined vehicle type

5

and weight class, plus the “registration

vocation” assigned by IHS Markit based on the company that registered each vehicle (i.e. construction,

sanitation, freight, services). The market segmentation summarized in Figure 3 is an organic outcome of

the in-use vehicle analysis, and the market segment names are intended to be illustrative of the vehicle

configuration and use for the majority of vehicles in each segment, based on vehicle configuration and

using company. Within each segment there is some variation in vehicle configuration and daily/annual

usage patterns. See Appendix A for a full discussion of how the in-use vehicle segmentation analysis

summarized in Figure 3 was conducted.

Source: IHS Markit, M.J. Bradley & Associates

5

This information is encoded in the vehicle identification number (VIN) assigned by the original equipment

manufacturer (OEM). Other data encoded in the VIN and included in the IHS Markit database for each vehicle

includes manufacturer name, vehicle model, and weight class.

Figure 3

U.S. In-use Medium- & Heavy-duty Fleet by Market Segment

Engine Vehicle

Class 2B LHD 8,951,335 39.3%

Class 3 LHD 2,330,763 10.2%

Regional Haul Tractor Class 7 - 8 MHD, HHD Combination Trucks 1,094,056 4.8%

Long Haul Tractor Class 8 HHD Combination Trucks 2,057,164 9.0%

Transit Bus Class 8 HHD

Vocational Vehicle

Urban 77,720 0.3%

School Bus Class 7 MHD

Vocational Vehicle

Urban 497,201 2.2%

Shuttle Bus Class 3-5 LHD

Vocational Vehicle

Urban 149,773 0.7%

Delivery Van Class 3-5 LHD

Vocational Vehicle

Urban 500,110 2.2%

Delivery Truck Class 6-7 MHD

Vocational Vehicle

Urban 400,969 1.8%

Service Van Class 3-5 LHD

Vocational Vehicle

Urban 808,802 3.5%

Service Truck Class 6-7 MHD

Vocational Vehicle

Urban 296,999 1.3%

Refuse Hauler Class 8 HHD

Vocational Vehicle

Urban 101,401 0.4%

Box Truck Class 3-5 LHD

Vocational Vehicle

Regional 162,731 0.7%

Box Truck Class 6-7 MHD

Vocational Vehicle

Regional 172,354 0.8%

Box Truck Class 8 HHD

Vocational Vehicle

Regional 153,776 0.7%

Stake Truck Class 3-5 LHD

Vocational Vehicle

Mixed Use 391,348 1.7%

Stake Truck Class 6-7 MHD

Vocational Vehicle

Mixed Use 191,925 0.8%

Dump Truck Class 8 HHD

Vocational Vehicle

Mixed Use 247,475 1.1%

OTHER Class 3 - 8

LHD,MHD,HHD

Vocational Vehicle

Mixed Use 4,216,527 18.5%

22,802,427 100.0%

MARKET SEGMENT

Weight Class

Number

% of Fleet

Estimated In-use Vehicles

EPA Phase 2 Regulatory Category

Heavy Duty Pickup &

Van

HD Pickup & Van

HD Pickup & Van

10

Weight Class 2 (VIN-defined) does not identify the sub-set of vehicles in Class 2b (8,500 – 10,000 lb

GVWR), so the IHS Markit data could not be used to estimate the number of these vehicles in the fleet;

the estimate of Class 2b vehicles in Figure 3 is from EPA’s MOVES3 model [2].

As shown, as of December 2020 there were an estimated 22.8 million medium- and heavy-duty vehicles

(Class 2b – 8) registered in the U.S. Almost 50% of these vehicles are heavy-duty pickups and vans (Class

2b – 3), 13% are combination trucks (tractor-trailers), and 37 percent are various types of vocational

vehicles. Of the vocational vehicles about 33 percent have a primarily urban duty cycle, 6 percent have

a primarily regional duty cycle, and 61 percent have a mixed duty cycle.

Based on analysis of in-use tractor characteristics, MJB&A estimates that approximately one third of

tractor-trailers are primarily used for local or regional freight hauling (return-to-base) and two thirds are

primarily used to deliver freight across much longer distances, with vehicles not returning to the same

location every day.

6

Some examples of local/regional hauling using tractor trailers include beverage

delivery and shuttles between major regional warehouses or logistics centers.

The market segmentation analysis is most helpful in breaking down the diverse group of vocational

vehicles into different use cases. Almost 9% of vocational vehicles are buses of different types, and

another 11% are construction trucks. Approximately 16% of vocational vehicles are single-unit freight

delivery vans and trucks primarily used for local and regional freight deliveries (return-to-base) and 14%

are vans and single unit trucks used in the delivery of various local services – including by electric and

gas utility companies, telecom companies, and local contractors (plumbers, electrician, landscapers, etc.).

The last category in Figure 2, labeled “other” includes a diverse mix of vocational vehicles, none of which

individually make up more than 0.5% of the fleet. These vehicle types include fire trucks and other

emergency vehicles, motor homes, and mining and forestry trucks. Most of the trucks in this category,

however, are trucks that could not be identified as belonging in one of the other market segments due to

a lack of data – because they were registered to individuals rather than companies (and therefore have no

registration vocation), or because they were registered by companies which could not be easily

categorized by IHS Markit (see the Appendix).

As shown in Figure 3, most of the market segments used to frame this analysis map directly to a single

combination of EPA engine and vehicle regulatory categories – i.e., Transit Bus is HHD/Vocational

Vehicle/Urban Duty Cycle, and Delivery Van is LHD/Vocational Vehicle/Urban Duty Cycle. However,

multiple market segments may map to the same combination of EPA regulatory categories – for example

Delivery Van, Shuttle Bus and Service Van all map to LHD/Vocational Vehicle/Urban Duty Cycle.

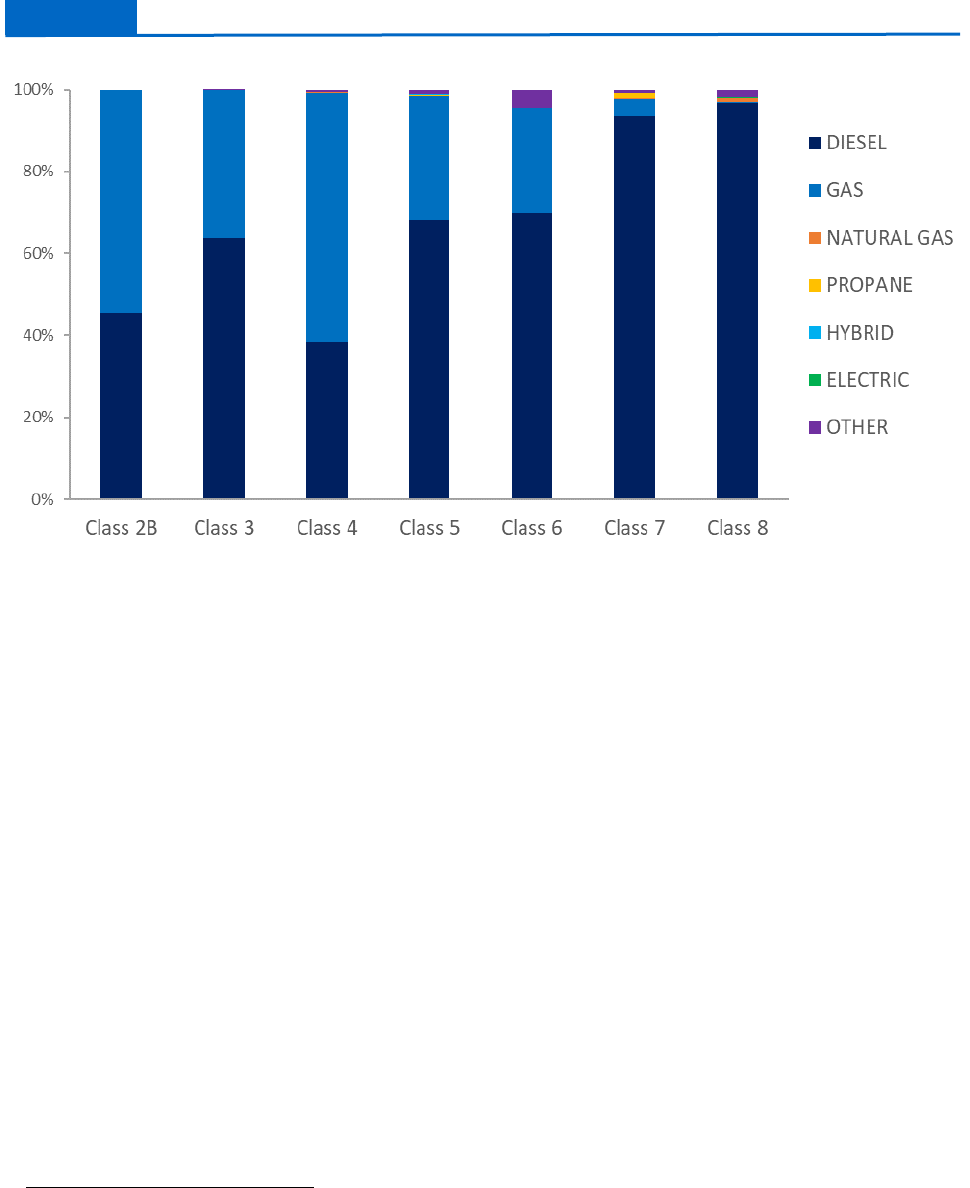

See Figure 4 for a summary of the in-use M/HDV fleet by weight class and fuel type

7

. Today, less than

one percent of the M/HDV fleet are hybrid-electric or battery-electric vehicles and less than 2% are

alternative fuel vehicles (natural gas, propane, other). Over 95% of the largest Class 7 and Class 8 trucks

have diesel engines. A much larger percentage of smaller vehicles have gasoline engines, especially

Class 2B and Class 4 trucks – over 50% of these vehicles have gasoline engines, with most of the rest

diesel.

6

As discussed more fully in Appendix A the estimate of regional versus long-haul tractor trailers is based on

characteristics of vehicles in the registered in-use fleet, including engine displacement, number of driven wheels,

and cab style.

7

Data for Class 3 – 8 in this his figure is based on IHS Markit registration data; the fuel type distribution for Class

2b trucks is based on EPA’s MOVES3 model.

11

Source: IHS Markit

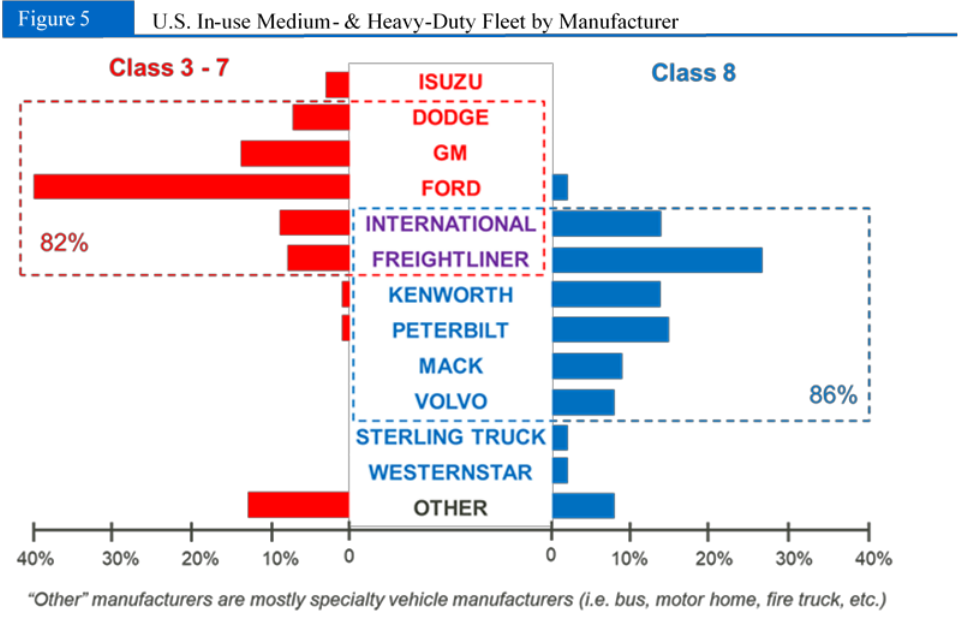

See Figure 5 for a summary of the in-use M/HDV fleet by manufacturer; as shown, 12 companies account

for 90% of the fleet. The remaining 10% of the fleet (“Other” in Figure 5) was primarily produced by

small specialty manufacturers, including those that exclusively make transit buses, fire trucks, and motor

homes.

The twelve primary manufacturers of M/HDV trucks can be divided into three groups – those that

primarily make smaller vehicles (Class 3 – 6), those that almost exclusively make the largest Class 8

trucks, and those that have significant market share across the entire size range. Manufacturing of the

smallest vehicles is dominated by the “big 3” US car companies – Ford, General Motors, and Chrysler

(Dodge)

8

. There are only two companies that have significant market share from Class 4 through Class

8 – International and Freightliner. The companies that primarily produce the largest Class 8 trucks –

most of which are combination truck tractors and construction trucks – include PACCAR (which owns

Kenworth, and Peterbilt), Volvo (Volvo also owns Mack), and Freightliner (which owns Sterling Truck

and Western Star). Note that the manufacturers shown in Figure 5 produce their own engines, but typically

also offer engines from Cummins in many of their models. Cummins is the only large fully independent

engine manufacturer in North America (it produces only engines and not full vehicles)

9

; over the past

three years Cummins has had a 25 percent market share of engines in new Class 3 -8 vehicles, with engine

sales across all weight classes

10

.

For new vehicles registered in the last three years (2018 – 2020) manufacturer market shares are very

similar to those shown in Figure 5 for the full in-use fleet, with the exception that for smaller vehicles

8

Though not included in Figure 3, these companies also dominate manufacturing of Class 2b trucks, which are

primarily heavy-duty pickups and vans, as well as a small number of large SUVs.

9

Detroit Diesel is also an independent engine manufacturer but is a subsidiary of Freightliner.

10

IHS Markit, new Class 3 – 8 vehicle registrations 2018 – 2020.

Figure 4

U.S. In-use Medium- & Heavy-Duty Fleet by Fuel Type

12

(Class 3 - 7) Mercedes and Hino each have about 1.5% market share of recent truck sales, and Sterling

Trucks has less than 1% market share of recent Class 8 truck sales. [4]

Source: IHS Markit

13

M/HDV In-Use Fleet: Environmental Impact

EPA estimates that in 2020 the M/HDV fleet consumed 55.3 billion gallons of fuel and emitted 561

million metric tons (mill MT) of greenhouse gases (GHG), 1.5 million MT of nitrogen oxides (NOx) and

38,000 MT of particulate matter (PM)

11

[2]. Almost 60% of NOx and PM exhaust emissions from the

M/HDV fleet were in urban areas. NOx and PM emissions from the M/HD fleet are currently responsible

for up to 4,550 premature deaths, 4,290 hospital visits, and 2.7 million incidents of exacerbated

respiratory conditions and lost or restricted workdays annually. The monetized cost of these public health

impacts from the M/HD fleet are estimated to exceed $53 billion annually

12

.[5]

In their 2021 Annual Energy Outlook the Energy Information Administration estimates that national

M/HD VMT will grow by 29 percent through 2050

13

, a compound annual average growth rate of 0.75

percent [6]. Projected regional growth rates vary, with higher projected growth in the Southeast and

Mountain West than in most other parts of the country, mirroring projected regional population growth.

Based on EIA VMT growth projections, and current EPA new engine fuel economy and emission

standards, MJB&A estimates that annual M/HDV fuel use and GHG emissions will fall by 18 percent

through 2050 as the fleet turns over to new, more efficient vehicles [7]. Through 2045 annual fleet NOx

and PM exhaust emissions are projected to fall by 43 percent and 72 percent respectively, as the fleet

turns over to new vehicles with engines that meet more stringent emission standards. After 2045 annual

fleet NOx and PM emissions are projected to start rising again due to continued VMT growth.

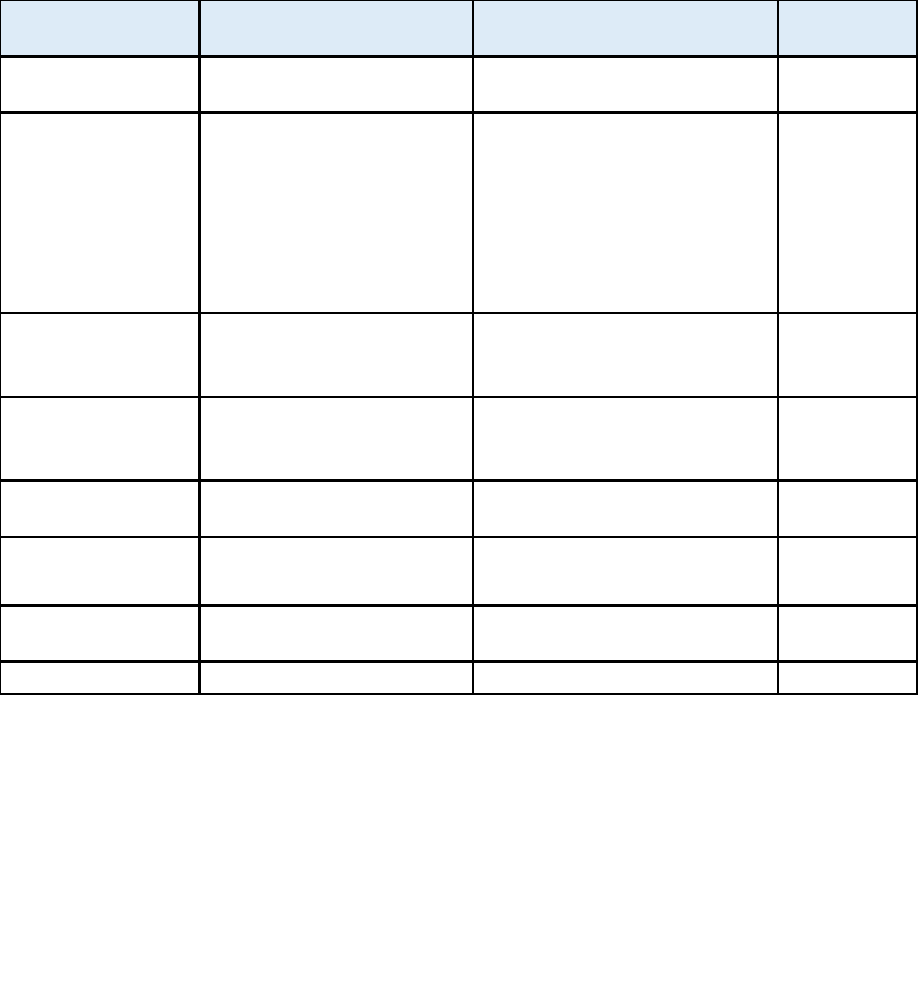

See Figure 6 for a summary of the estimated relative environmental impact of the different M/HDV

market segments in 2020, as a percentage of total M/HD fleet impact. For each segment Figure 6 includes

the estimated percentage of total in-use M/HD vehicles included in the segment, the percentage of total

M/HD fleet miles (VMT) driven by these vehicles, and the percentage of M/HD fleet total GHG, urban

NOx, and urban PM

14

produced by the segment. These estimates were developed by mapping MOVES3

data, delineated by vehicle type and regulatory category, to the vehicle types in each segment. See the

appendix for a full discussion of how this mapping was conducted.

As shown, almost 50% of GHGs from the entire M/HDV fleet are emitted by combination truck tractors

used in long-haul service. This market segment also accounts for over 40% of M/HDV tailpipe NOx

and PM emitted in urban areas. Regional haul tractors account for another 12% of GHGs and a similar

percentage of urban tailpipe NOx and PM emissions. From both a climate and air quality perspective

the third most important market segment is heavy duty pickups and vans, which contribute 16% of GHGs,

17% of tailpipe NOx emissions, and 23% of tailpipe PM emissions from the M/HD fleet. These three

market segments together account for greater than three quarters of the climate and air quality impact of

the M/HDV fleet.

As a group Class 3 – 8 vocational trucks account for 27 percent of fleet VMT, 25 percent of fleet GHGs,

23 percent of urban tailpipe NOx and 26 percent of urban tailpipe PM. Within the vocational vehicle

11

This is estimated direct exhaust emissions of PM with mean aerodynamic diameter less than 2.5 microns

(PM

2.5

). It does not include PM emissions from brake and tire wear, or secondary PM emissions formed in the

atmosphere from exhaust gases such as NOx.

12

This is based on EPA’s Co-Benefits and Risk Assessment (COBRA) screening tool. Values are national

estimates of health impacts due to the contribution of M/HD vehicle exhaust to ambient PM concentrations.

Hospital visits includes hospital admissions and emergency room visits.

13

EIA’s AEO 2021 includes the effects and projected recovery from the COVID-19 pandemic and includes

slower near-term M/HD VMT growth than had been projected by EIA in recent years.

14

Direct exhaust PM, not including secondary PM or PM from brake and tire wear.

14

category approximately 17 percent of urban air quality impact (tailpipe NOx and PM) comes from buses

of different types, 17% comes from construction trucks, 17% comes from single-unit freight trucks

primarily used for local and regional freight deliveries (return-to-base) and 9% comes from vans and

single unit trucks used in the delivery of various local services.

Source: IHS Markit, EPA MOVES3, M.J. Bradley & Associates

For most market segments climate and air quality impact is generally proportional to the miles traveled

by vehicles in the segment (VMT). There are a few segments however, with air quality impact higher

than their proportion of fleet VMT - these segments include both regional and long-haul tractors; transit,

school, and shuttle buses; refuse trucks, the largest (Class 8) freight hauling box trucks, and dump trucks.

It is also worth noting that a long-term trend in the M/HD fleet is the increasing importance of smaller

Class 3 vehicles, most of which are pickup trucks, or are vans and small box trucks used for local services

and deliveries. In 1990 only 7 percent of new M/HD truck sales were Class 3, but by 2000 this had risen

to 20 percent, and since 2010 it has averaged 40 percent; see Appendix B [8]. In 2020 384,000 new Class

Figure 6

U.S. In-use Medium- & Heavy-duty Fleet Environmental Impact by Market Segment

Class 2B 39.2% 22.7% 11.7% 14.6% 18.8%

Class 3 10.2% 6.0% 4.0% 2.8% 4.0%

Regional Haul Tractor Class 7 - 8 4.8% 9.0% 11.9% 12.7% 10.6%

Long Haul Tractor Class 8 9.0% 35.8% 47.8% 46.5% 41.0%

Transit Bus Class 8 0.3% 0.6% 0.7% 0.9% 0.5%

School Bus Class 7 2.2% 1.2% 1.1% 1.3% 1.9%

Shuttle Bus Class 3-5 0.7% 1.0% 1.3% 1.6% 1.9%

Delivery Van Class 3-5 2.2% 1.4% 1.0% 0.7% 1.1%

Delivery Truck Class 6-7 1.8% 2.8% 2.7% 2.2% 2.7%

Service Van Class 3-5 3.5% 2.3% 1.7% 1.2% 1.8%

Service Truck Class 6-7 1.3% 0.8% 0.8% 0.7% 0.8%

Refuse Hauler Class 8 0.4% 0.4% 0.6% 1.0% 1.4%

Box Truck (freight) Class 3-5 0.7% 0.5% 0.3% 0.2% 0.2%

Box Truck (freight) Class 6-7 0.8% 0.6% 0.5% 0.4% 0.5%

Box Truck (freight) Class 8 0.7% 1.8% 1.9% 2.2% 1.7%

Stake Truck (construction) Class 3-5 1.7% 1.0% 0.7% 0.5% 0.8%

Stake Truck (construction) Class 6-7 0.8% 0.5% 0.5% 0.4% 0.5%

Dump Truck Class 8 1.1% 2.3% 2.6% 3.4% 2.8%

OTHER Class 3 - 8 18.5% 9.5% 8.1% 6.6% 7.2%

100% 100% 100% 100% 100%

Heavy Duty Pickup & Van

% of GHG

% Urban

NOx

% Urban

PM

SEGMENT IMPACT

% of

VMT

% of

Fleet

MARKET SEGMENT

Weight

Class

15

3 vehicles were registered, an increase of 42 percent compared to the previous year. By comparison, in

2020 registrations of new Class 4 – 8 trucks were down 19 percent compared to 2019, likely due to the

effects of the COVID 19 pandemic [4].

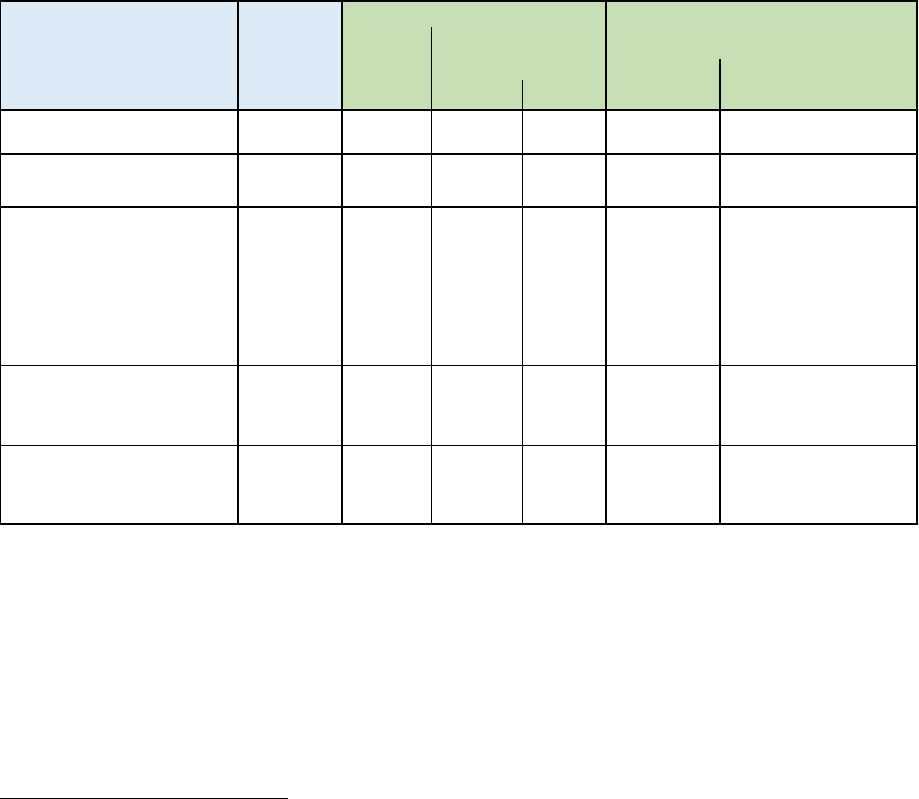

See Figure 7 for a summary of relative market segment impact for Vocational trucks (the market

segments other than Heavy-duty Pickup and Van, and tractors).

Among the Vocational truck market segments, the most impactful are dump trucks, Class 8 box trucks,

Class 6-7 delivery trucks, Class 3 -5 service vans, and school and shuttle buses.

Note that the “other” category at the bottom of Figure 7 includes a wide range of vehicles. As

discussed above, some vehicles in this segment are known specialty vehicles with very low total

numbers in the fleet (i.e. ambulances, forestry trucks) but the majority of vehicles in this segment could

not be fully characterized by type and usage due to a lack of data

15

; it is likely that a significant

percentage of these vehicles actually belong in one of the other market segments.

The analysis summarized in Figure 6 is based on the current 2020 in-use fleet. As described above,

EPA projects that total annual GHG, NOx, and PM emissions from the M/HD fleet (Class 2B-8) will

fall by 2030 due to turnover of the in-use fleet to new, cleaner vehicles. However, estimated reductions

15

This is because they were registered by individuals or by companies that could not be characterized by business

type. See the Appendix for a full discussion of the data and methods used to apportion vehicles to market

segments.

Transit Bus Class 8 0.9% 2.1% 2.9% 3.8% 1.8%

School Bus Class 7 5.9% 4.4% 4.6% 5.6% 7.5%

Shuttle Bus Class 3-5 1.8% 3.8% 5.3% 6.9% 7.5%

Delivery Van Class 3-5 6.0% 5.2% 4.2% 3.2% 4.2%

Delivery Truck Class 6-7 4.8% 10.5% 11.0% 9.6% 10.6%

Service Van Class 3-5 9.7% 8.5% 6.8% 5.1% 6.8%

Service Truck Class 6-7 3.5% 3.1% 3.2% 2.8% 3.1%

Refuse Hauler Class 8 1.2% 1.6% 2.3% 4.4% 5.4%

Box Truck Class 3-5 1.9% 1.7% 1.3% 0.7% 0.9%

Box Truck Class 6-7 2.1% 2.3% 2.2% 1.7% 1.9%

Box Truck Class 8 1.8% 6.7% 7.6% 9.5% 6.5%

Stake Truck Class 3-5 4.7% 3.8% 3.0% 2.3% 3.0%

Stake Truck Class 6-7 2.3% 1.8% 1.9% 1.7% 1.9%

Dump Truck Class 8 3.0% 8.7% 10.6% 14.4% 10.9%

OTHER Class 3 - 8 50.4% 35.8% 33.1% 28.3% 28.1%

RELATIVE SEGMENT IMPACT

% of Fleet

% of

VMT

% of

GHG

% Urban

NOx

% Urban

PM

MARKET

SEGMENT

Weight Class

Figure 7

Market Segment Impacts – not Including Tractors and Heavy-Duty Pickups and Vans

16

in average emissions (g/mi) are generally consistent across different vehicle types, and the relative

environmental impact of the different market segments is expected to remain consistent with the values

in Figure 6, with only minor shifts based on changes in the fleet vehicle mix (see Appendix B). For

example, if the trend of increasing Class 3 vehicle sales continues this would slightly increase the

relative impact of market segments such as Heavy-duty Pickup and Van, Delivery Van and Service

Van.

M/HDV ZEV Market Readiness

In the last two years there has been significant activity in the M/HD ZEV market, with a number of fleets

making commitments to electrification, and vehicle manufacturers introducing prototype vehicles and

pilot fleets, and announcing commercial launch dates [9]. Volvo and Freightliner are operating ZEV

demonstration fleets across the country and have both begun taking commercial orders for their e-models.

Kenworth has developed a prototype Class 6 electric truck and plans to produce up to 100 of them in

2021.

Both Navistar (NEXT) and General Motors (Bright Drop) have launched new business units to focus on

electric mobility solutions, including vehicles, software, and services. Navistar, Volvo, and Freightliner

have all announced major investments to build or upgrade U.S. factories to produce zero emitting

vehicles. Cummins will invest more than $500 million into its Electrified Power technology, and, by

2050, has committed to powering its products using carbon neutral technologies that address air quality.

Ford will soon begin taking pre-orders for an electric version of their Transit commercial van, to be

introduced in Model Year 2022; the electric version of Ford’s F150 pickup – the bestselling vehicle in

the U.S. – will also launch in Model Year 2022

16

.

In addition to these major market players there are several smaller players and start-ups already selling

M/HD ZEVs into the market or planning to launch vehicles in the next three years. These include Lion

Electric, Workhorse, Tesla, Nikola, Rivian, and UK-based Arrival. Roush CleanTech also recently

announced a collaboration with electric bus maker Proterra and Penske Truck Leasing to develop a next

generation all-electric commercial truck build on the Ford F-650 chassis.

Fleets that have already made significant commitments to electrification include Amazon (100,000

electric delivery vans ordered from Rivian), UPS (950 electric trucks ordered from Workhorse and 10,000

electric vans from Arrival), Pride Group (6,400 electric vehicles ordered from Workhorse, Tesla, and

Lion), FedEx (500 electric delivery trucks ordered from Bright Drop), Montgomery Maryland Public

Schools (326 electric school buses from Thomas Built), and PepsiCo (100 electric semi-trucks ordered

from Tesla).

In addition, there are over 2,000 electric transit buses in-service or on order at over 160 U.S. transit

agencies in 45 different states. Agencies that have already made major commitments to electric buses

include Los Angeles Metro and Los Angeles Department of Transportation (369 electric buses), and the

Antelope Valley and Foothill transit systems in California (80+ buses each). Many other private and

public fleets have made public commitments to electrify their entire fleets by 2030 but have yet to order

a significant number of vehicles; see Appendix B [9].

For this analysis MJB&A evaluated the current state of electrification for each M/HDV market segment,

to assess prospects for near-term (through 2025) and medium-term (through 2030) uptake of battery-

1616

Neither the Ford e-Transit or F150 Lightning electric vehicles are expected to initially be available with

GVWR above 8,500 pounds; as such they are “light-duty” vehicles but are prevalent in many commercial fleets.

17

electric vehicles within the segment. This analysis focused on prospects for electric vehicle penetration,

as a proxy for uptake of all zero-emitting technologies, because all scenarios for avoidance of detrimental

future climate warming point to the need for significant pollution reductions from the transportation

system, coupled with further decarbonization of the power sector. In addition, as described above,

medium- and heavy-duty vehicles are a significant source of health harming air pollution, which ZEVs

would likewise help to eliminate.

Each market segment was evaluated based on four relevant factors that will significantly impact truck

owner decisions about whether to purchase an electric vehicle:

• Charging - infrastructure requirements for vehicle charging, including required charging

capacity (kW/vehicle) and location (at vehicle home base or shared public charging)

• Technical Feasibility - the ability of current and future EV models to meet operating

requirements of the segment, primarily based on range per charge compared to typical daily

mileage accumulation,

• Commercial EV Market – current and announced availability of electric models from major

manufacturers in the short (through 2025) and medium (through 2030) term, and

• EV Business Case - prospects for lifetime cost parity with current diesel and gasoline vehicles

in the short (through 2025) and medium (through 2030) term. Potential cost parity was evaluated

based on incremental EV purchase cost – compared to a diesel or gasoline vehicle – compared

to life-time projected discounted fuel cost savings.

See the appendix for a full discussion of the methodology and data sources used to evaluate each of these

metrics for each M/HDV market segment. The results of the analysis are discussed below.

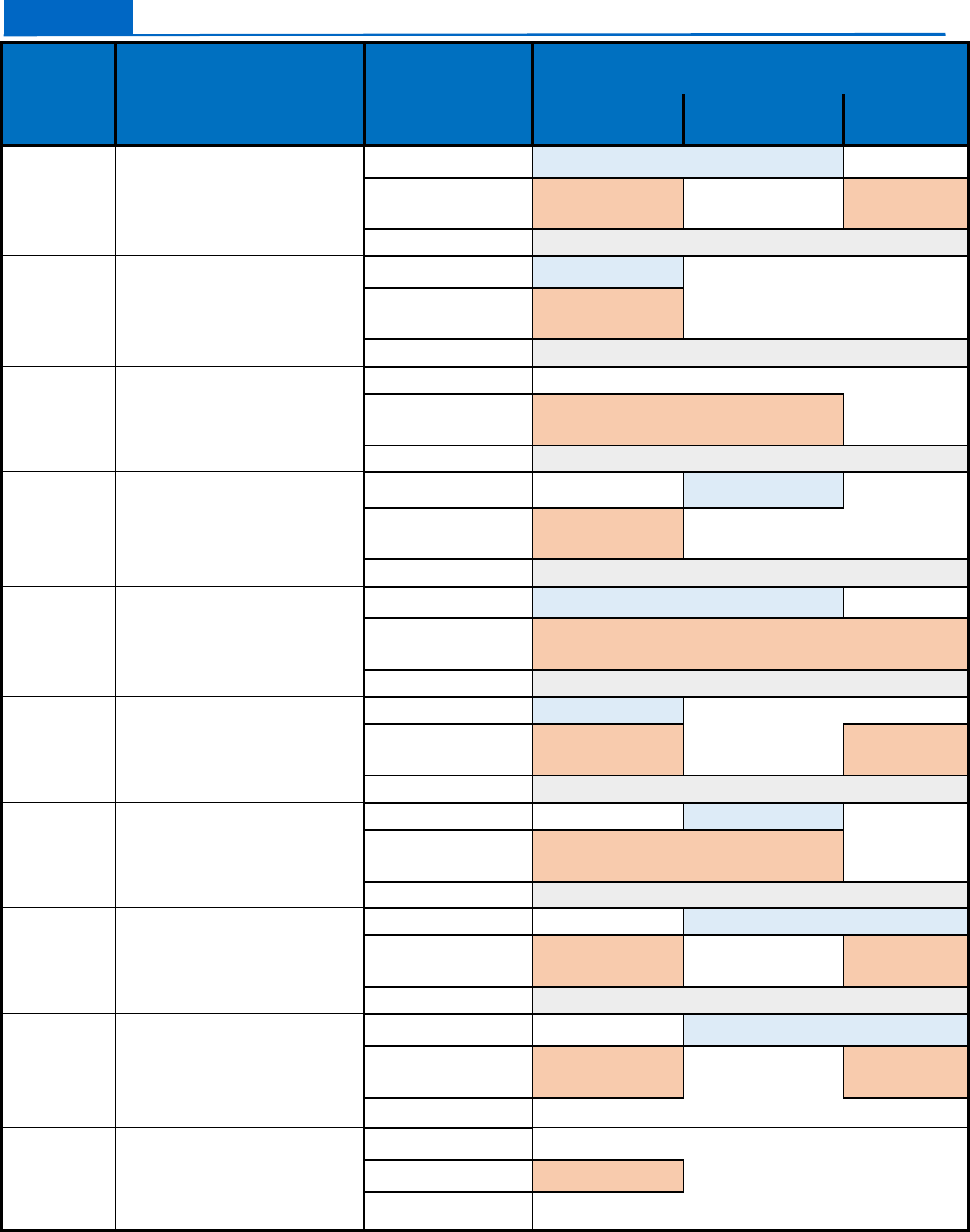

Charging

Charging needs in each market segment were evaluated based on the likely/feasible location of charging

for most vehicles in the segment, and the typical charging capacity required (kW/vehicle). Charging

location is assessed as “Home Base” or “Public”. Home Base charging means that a significant majority

of vehicles in the segment are primarily used during day light hours and return to the same location every

afternoon/evening, allowing for overnight charging at the home base. Public charging means that a

significant percentage of vehicles in the segment are used for long-haul freight operations and do not

routinely return to the same location for overnight parking. These vehicles will need to have access to a

shared (Public) network of chargers.

Required charging capacity for vehicles in each segment was estimated based on typical daily energy use

(kWh/day) and available charging time (hours); estimated daily energy use is based on typical daily usage

patterns (miles driven) and the average energy use (kWh/mi) of vehicles in the segment.

For some market segments required charging capacity is low enough (<19 kW/vehicle) that many

vehicles in the segment can use relatively inexpensive Home Base Level 2 chargers, similar to “home

18

chargers” used with many light-duty EVs

17

. Other market segments will require more expensive Level

3 chargers for home-base charging due to higher typical daily energy needs

18

.

See Figure 8 for a summary of estimated charging needs of vehicles in each market segment; details of

how these charging needs were determined is in the Appendix.

Home Base, Level 2

Home Base, Level 3

Public

• Heavy-duty Pickup & Van

• School Bus

• Delivery Van

• Service Van

• Service Truck

• Box Truck (Class 3 – 5)

• Stake Truck (Class 3 – 5)

• Stake Truck (Class 6 – 7)

• Heavy-duty Pickup

• Regional Haul Tractor

• Transit Bus

• Shuttle Bus

• Delivery Truck

• Refuse Hauler

• Box Truck (Class 6 – 7)

• Box Truck (Class 8)

• Dump Truck

• Long Haul Tractor

• Regional Haul Tractor

• Box Truck (Class 6 – 7)

• Box Truck (Class 8)

As shown in Figure 5, the vehicles in fifteen of the market segments – which include more than 60% of

all vehicles in the M/HDV fleet - will generally be able to use Home Base charging. Of these vehicles

that can use home base charging, for more than 80% of them their charging requirements can likely be

met by an inexpensive Level 2 charger. For these vehicles, charging is not a significant barrier to EV

adoption, either in terms of cost or practicality. Note that the charging needs of many Heavy-duty Pickups

can be met using a Level 2 charger, but for those that regularly tow trailers a Level 3 charger might be

required due to higher daily energy demand.

There is only one market segment – Long Haul Tractor – for which virtually all vehicles will require

access to a public charging network. There are three other market segments – Regional Haul Tractors

and Class 6-7 and Class 8 Box Trucks – for which a large number of vehicles (but not the majority) will

likely require access to a public charging network on a regular basis if not every day (these market

segments are therefore shown in Figure 8 as requiring both Home Base, Level 3 and Public charging).

For these market segments charging requirements are a greater near-term barrier to EV adoption than for

the other segments that can primarily use home base charging

19

. This is primarily because charger

17

Level 2 chargers have 240-volt input voltage and provide alternating current (AC) output to the vehicle; these

chargers typically have a maximum charge rate of 19 kW or less.

18

Level 3 chargers require 480-volt input voltage and deliver direct current (DC) output to the vehicle.

Level 3 chargers can be designed with maximum charge rate between 25 kW and 600 kW.

19

Other zero-emitting technologies – such as hydrogen fuel cell electric vehicles – will also require development

of new public fueling infrastructure to support adoption in these market segments.

Figure 8

Charging Needs by Market Segment

19

siting/availability is outside of the span of control of any individual company or fleet. To keep charging

time low (<2 hr/day/vehicle) public chargers will need to have high charge rates (>500 kW) and will

therefore be expensive. However, they will be a shared resource with one charger able to support 12 –

20 vehicles in the medium and long term, so average charging capacity (kW/vehicle) will be similar to

that required for home base charging of a similar vehicle

20

.

Technical Feasibility

The near-term technical feasibility of electric vehicles in each market segment was evaluated by

comparing the estimated range per charge (miles) of currently available vehicles to average daily usage

(accumulated miles) of vehicles in the segment; see Figure 9 for a summary of this analysis, and Appendix

A for a more detailed discussion of how the analysis was conducted

21

.

Range > Average Daily

Mileage

60% <Range <100%

of Average Daily Mileage

Range < 60%

of Average Daily Mileage

• Heavy-duty Pickup and Van

• Transit Bus

• School Bus

• Delivery Van

• Service Van

• Service Truck

• Refuse Hauler

• Box Truck (Class 3 - 5)

• Box Truck (Class 6 – 7)

• Stake Truck (Class 3– 5)

• Stake Truck (Class 6 – 7)

• Regional Haul Tractor

• Delivery Truck (Class 6 – 7)

• Dump Truck

• Long Haul Tractor

• Shuttle Bus

• Box Truck (Class 8)

As shown, there are 11 market segments, representing 63% of the fleet, for which current commercially

available battery electric models have large enough batteries to power an average day’s driving for

vehicles in the segment; in most cases the range is sufficient to go at least 50% further than the average.

For these market segments, currently available EV models could meet operational needs for the majority

of in-use vehicles in the segment.

20

In the short term when the percentage of in-use vehicles that are electric is low more chargers will likely be

required in order to achieve necessary geographic network coverage.

21

Hydrogen fuel cell electric vehicles do not have the same limitations of on-board energy storage as battery

electric vehicles so “range between fueling events” is generally not a significant barrier to their adoption for any

market segments.

Figure 9

EV Usability by Market Segment

20

Current EV models available for another three market segments, representing an additional 8% of the

fleet, have large enough batteries to cover at least 60% of average daily driving for vehicles in the

segment. For these market segments there will be some individual vehicles for which current EVs can

meet fleet operational needs, while for other vehicles they cannot.

There are only three market segments for which range limits of current commercially available EVs pose

a significant operational challenge – however two of these segments (Long Haul Tractor and Class 8 Box

Truck) also require public charging, which could alleviate some or all the range constraints.

The evaluation summarized in Figure 9 indicates that currently available electric vehicles could replace

diesel and gasoline vehicles for 40 – 60% of the M/HDV fleet while meeting all operational needs.

22

It is

important to note that this estimate is based on current commercially available EVs. Projected

improvements in battery energy density over the next 5 – 7 years should increase vehicle range and

increase the total number of vehicles in the fleet for which EVs can replace diesel and gasoline vehicles

while meeting all operational requirements.

Commercial EV Market

The maturity of the commercial EV Market in each market segment was evaluated based on the number

of electrified models currently available for purchase, and those projected to be available in the next five

years based on announcements already made by manufacturers [10]. Also important is whether the major

full line manufacturers that currently dominate M/HD truck sales (see Figure 5) offer EV models, or

whether they are only offered by small start-up or specialty manufacturers (e.g., ZEV only manufacturers

or retrofitters).

The only market segments that are fully mature in 2020 with respect to EVs are the Transit Bus and

School Bus markets. For both of these vehicle types, EV models are already fully commercially available

from more than one manufacturer that has significant market share in the segment. In the case of Transit

buses every bus manufacturer that sells diesel buses in North America also offers an electric version; in

addition, there are two electric-only manufacturers that have already made a large number of sales.

For other market segments current (2021) commercial EV models are limited and generally produced

only by small start-up manufacturers. However, there is growing and accelerating interest from the 12

major OEMs shown in Figure 5 which account for 90% of the current in-use fleet. Most of these

manufacturers have prototype EV models under development or have in-use pilot or demonstration fleets

under test. Several have announced they will begin limited production or full commercial introduction

of one or more electric models in 2021 or 2022 [11]. The announced model introductions from major

OEMs include vehicles across the M/HD spectrum, from Class 3 vans to Class 6 box and work trucks, to

Class 8 tractors. There are also a number of well-funded start-up companies entering the market

specifically to produce electric trucks – primarily for short- and long-haul freight deliveries.

Several major manufacturers have recently announced plans to introduce light-duty (<8,500 lb GVWR)

electric delivery vans, and two major OEMs and four start-up companies have announced the launch of

light-duty electric pickups in the next three years. No companies have yet announced any plans for

electrification of heavy-duty vehicles in this segment (Class 2b-3), though the announcements from

manufacturers like Ford and Rivian in the light duty truck space may pave the way for manufacturing

opportunities in the heavier duty truck space in the next few years.

22

Hydrogen fuel cell electric vehicles could potentially meet the operational needs of virtually all M/HD vehicles

if supported by depot-based and public hydrogen fueling infrastructure.

21

Figure 10 summarizes the number of companies with at least one EV model in either production (i.e.

currently available for sale in 2021), pre-production (i.e., vehicles with an announced

production/availability date from 2022 - 2025), or concept (i.e., prototypes and/or pilot fleets with no

announced commercial launch date)

23

. In table 10, Company Type “Major OEM” refers to established

players in the U.S. with significant market share of diesel and gasoline vehicles; “EV Manufacturer”

refers to established and start-up companies making only purpose-built EV; and “EV Retrofit” refers to

manufacturers that purchase incomplete vehicles from major OEMs and up-fit them to EV.

There are currently 30 companies with at least one EV model for sale commercially. An additional nine

companies have announced they will begin production of EV models between 2022 and 2025, including

5 of the 12 OEMs that currently hold 90% of the M/HD market share (Figure 5). Based on existing

manufacturer announcements there will be multiple companies selling EV in virtually all MHD market

segments by 2025, including 58% of the major OEMs.

23

There are also a small number of hydrogen fuel cell vehicle models in-service, under test, and in development

by several manufacturers.

22

Vehicle

Type

Regulatory Category

(Vehicle, Engine)

Company

Type*

Number of Companies with at least one

ZEV Model

Production

Pre-

production

Concept

Transit

Bus

Vocational Urban,

Heavy Heavy-Duty

Engine

Major OEM

4

EV

Manufacturer

4

2

EV Retrofit

3

School Bus

Vocational Urban,

Medium Heavy-Duty

Engine

Major OEM

2

EV

Manufacturer

2

EV Retrofit

2

Coach Bus

Vocational Urban,

Heavy Heavy-Duty

Engine

Major OEM

EV

Manufacturer

3

EV Retrofit

1

Shuttle

Bus

Vocational Urban,

Light Heavy-Duty Engine

Major OEM

5

EV

Manufacturer

2

EV Retrofit

6

Class 2b-3

Heavy Duty Pick-up and

Van/ Vocational Trucks,

Light Heavy-Duty Engine

Major OEM

3

EV

Manufacturer

11

EV Retrofit

4

Class 4

Vocational Trucks,

Light Heavy-Duty Engine

Major OEM

1

EV

Manufacturer

2

4

EV Retrofit

6

Class 5-6

Vocational Trucks,

Light Heavy-Duty

/Medium Heavy-Duty

Engines

Major OEM

3

EV

Manufacturer

7

EV Retrofit

7

Class 7-8

Single

Unit

Combination Trucks,

Medium Heavy Duty

Engine

Major OEM

6

EV

Manufacturer

7

2

EV Retrofit

1

Class 7-8

Tractor

Combination Trucks,

Medium Heavy Duty/

Heavy Heavy-Duty

Engine

Major OEM

9

EV

Manufacturer

3

2

EV Retrofit

Terminal

Tractor

Combination Trucks,

Medium Heavy Duty/

Heavy Heavy-Duty

Engine

Major OEM

EV Only

5

EV Retrofit

Figure 10

Announced and Available M/HD Electric Vehicles

23

EV Business Case

While electric M/HD vehicles are currently more expensive than their diesel counterparts, several studies

have indicated that costs are anticipated to fall dramatically within the next 10 years as manufacturers

introduce more models, and as increased vehicle volumes enable manufacturers to move down the

learning curve in electric vehicle production.

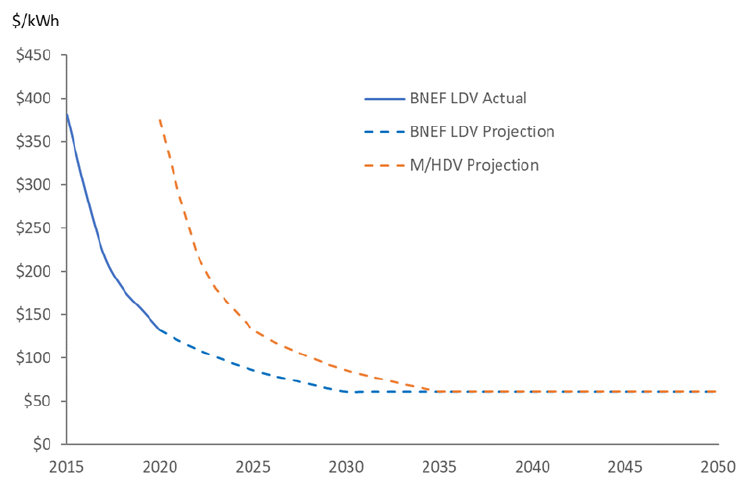

One reason for expected M/HD EV cost reductions are projected continuing reductions in the cost of

batteries, which are a significant contributor to the current increased cost of M/HD EVs compared to

diesel and gasoline vehicles. Light-duty EV battery costs have fallen from over $1,100/kWh in 2010 to

$156/kWh in 2019 [12]. Many analysts are projecting costs will continue to fall, to as low as $61/kWh in

2030; several major car companies have endorsed these estimates [11].

While average battery costs for M/HD EVs have also fallen in the last 10 years they currently remain

higher than costs for light-duty EVs, at approximately $375/kWh [12]; this implies that there is currently

about a 5-year lag between cost reductions for LD EV and M/HD EV batteries. Even if this lag continues,

M/HD EV battery costs should still fall below $90/kWh by 2030 (76% reduction from today). It is likely

that increased production volumes will cause this cost gap to close such that M/HD EV battery costs

could fall below $70/kWh by 2030 (81% reduction). As noted above in Figure 5, the manufacturers that

dominate Class 3 – 7 trucks sales also dominate US car and light truck sales and may therefore be well

positioned to apply to the M/HD segment cost reduction strategies developed for the much higher volume

light-duty segment.

A 2019 study conducted by ICF that evaluated costs of M/HD ZEVs in California estimated that between

2020 and 2030 the purchase cost of most M/HD EVs would fall by almost 50% [13]. ICF assumed that

in 2030 M/HD EV battery costs would average $157/kWh; as such, this study’s conclusions are likely

conservative, and M/HD EV purchase costs will likely fall even further over the next 10 years if the

current trend of LDV battery cost reductions is mirrored in the M/HDV market.

For this study MJB&A used the ICF M/HD EV cost estimates for different vehicle types but adjusted

them downward based on an assumed continued 5-year cost lag between LD EV and M/HD EV battery

costs ($132/kWh in 2025, $86/kWh in 2030). The resulting incremental EV purchase costs were then

compared to an estimate of life-time discounted fuel cost savings for M/HD EVs in each market segment

(compared to equivalent diesel vehicles), to identify when EVs in different market segments might reach

“cost-parity” with diesel vehicles over their lifetime.

24

See Figure 11 for a summary of the analysis. As shown, there are nine market segments – which

account for approximately 72% of the in-use fleet – in which EVs could reach life-time cost parity with

diesel and gasoline vehicles by 2025 based on discounted lifetime fuel savings and projected

incremental purchase costs. EVs in an additional three market segments (4% of the fleet) could reach

cost parity by 2030. Note that neither Transit Buses nor School Buses are shown in Figure 11 due to

significant uncertainty around the ICF future EV cost projections for these two vehicle types. ICF

2030 cost estimates – even when adjusted for lower battery costs – indicate that neither Transit nor

School buses will achieve life cycle cost parity with diesel vehicles by 2030. However, these cost

24

When evaluating the EV Business case this analysis used U.S. average fuel prices (diesel, electricity), as

projected by the Energy Information Administration [6]. Estimated annual fuel cost savings for an EV compared

to a diesel vehicle over the full vehicle life were discounted at a 7% discount rate and compared to the projected

incremental EV purchase cost. The vehicle life used for this calculation varied from 10 years for Class 2b-5

vehicles, to 14 years for Class 6-7 vehicles, and 18 years for Class 8-vehicles.

24

estimates indicate much higher cost reductions by 2030 for electric tractors and Class 8 single unit

trucks than for electric transit and school buses, despite having similar power and energy requirements.

The reason for the difference is not clear. If relative cost reductions for electric transit and school

buses match projected reductions for other Class 8 electric trucks, these market segments could also

achieve life-cycle cost parity with diesel buses by 2030.

Note also that this analysis does not assume any local, state, or federal EV purchase incentives nor does

it take into consideration the potential for more stringent NOx emission standards – currently under

consideration by EPA – to increase purchase costs for new diesel and gasoline vehicles, and thus reduce

net incremental purchase costs for M/HD EVs.

Given significant uncertainties as to future EV incremental purchase costs, the EV-ICE cost parity

projections in Figure 11 are a first order estimate; additional work to refine future EV cost estimates based

on recent and on-going market developments is warranted to refine this preliminary understanding of

how the M/HD EV business case will evolve in the short- and medium-term.

Policy Implications

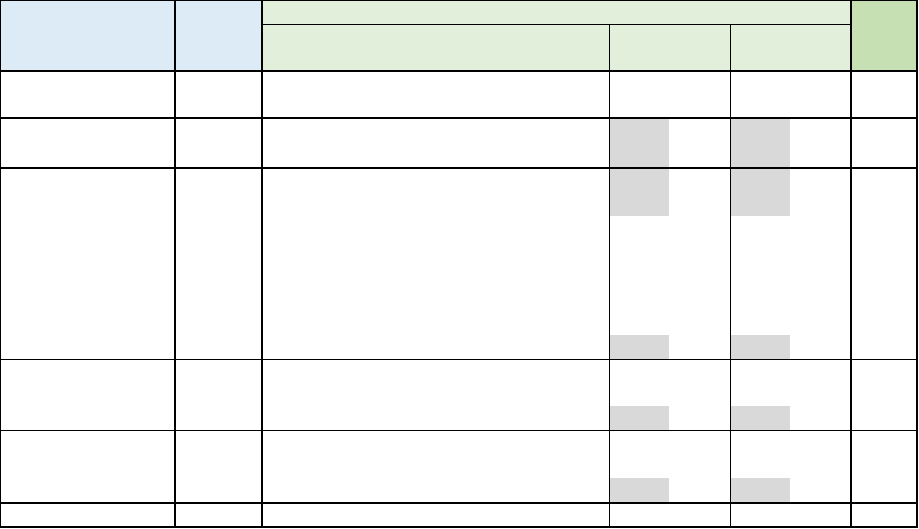

There are a large number of medium- and heavy-duty applications that have favorable ratings for early

deployment of ZEVs in all four categories evaluated (Heavy-duty Pickup and Van, Refuse Hauler,

Delivery Van, and Service Van) or three of four categories (Transit Bus, School Bus, Service Truck

Delivery Truck, Dump Truck, Box Truck (Class 3-5), Stake Truck (Class 3-5) and Stake Truck (Class 6-

7)). Collectively, these segments represent 66 percent of the fleet and account for 28 percent of GHGs,

30 percent of urban NOx and 37 percent of urban PM emitted by the fleet. Eliminating tailpipe pollution

from these vehicles would deliver significant public health benefits – including up to 1,500 fewer

premature deaths, 1,400 fewer hospital visits, and 890,000 incidents of exacerbated respiratory conditions

Projected EV Life-Cycle Cost Parity with Diesel & Gasoline Vehicles

By 2025

By 2030

After 2030

• Heavy-duty Pickup and Van

• Regional Haul Tractor

• Long Haul Tractor

• Delivery Van

• Delivery Truck

• Service Van

• Refuse Hauler

• Box Truck (Class 8)

• Dump Truck

• Shuttle Bus

• Service Truck

• Box Truck (Class 3 - 7)

• Stake Truck (Class 3– 7)

Figure 11

Projected EV -ICE Cost Parity by Market Segment

25

and lost or restricted workdays annually

25

. Together these segments represent a large number of vehicles

which can also advance the technical and commercial development of all M/HDV market segments.

This analysis is based on the current landscape and does not consider future technological improvements

or policy interventions that might further enhance the near-term attractiveness of zero-emitting medium

and heavy-duty vehicles across all applications. For instance, policies could support the development of

high-volume commercial ZEV markets and improving the ZEV value proposition for fleet owners.

Specific policy interventions that could address both barriers include low interest loans or tax credits for

ZEV research and development and for development of U.S. manufacturing facilities. Direct ZEV

purchase subsidies for fleets could also significantly strengthen the near-term ZEV business case, which

would advance development of the commercial market by creating more demand from customers.

President Biden has put forward proposals along these lines as part of his American Jobs Plan

26

25

These values are based on the estimated public health impact of the current in-use M/HD fleet in 2020, using

exhaust emissions estimates from MOVES3 and EPA’s CO-Benefits Risk Assessment Health Impacts Screening

and Mapping Tool (COBRA). Annual public health impacts from the entire M/HD fleet, and from this segment of

the fleet, are projected to fall over time as the fleet turns over to newer vehicles with engines that meet more

stringent emission standards. However, electric vehicles have lower annual and life-time public health impact

than even the newest diesel and gasoline vehicles, even after accounting for emissions from generating the

electricity used to charge them.

26

See https://www.whitehouse.gov/briefing-room/statements-releases/2021/05/18/fact-sheet-the-american-jobs-

plan-supercharges-the-future-of-transportation-and-manufacturing

26

Appendix A – Methodology & Data Sources

M/HDV In-Use Fleet: Vehicle Types & Uses

The number of M/HD vehicles in each market segment was estimated using vehicle registration data

collected by IHS Markit [1]. For each registered vehicle IHS uses data encoded in the vehicle

identification number (VIN) to identify vehicle attributes. The VIN-defined attributes used for this

analysis include Gross Vehicle Weight Class, Fuel Type, Vehicle Type, and Manufacturer. In addition,

IHS assigns a Registration Vocation based on the entity that registered the vehicle.

27

Certain VIN-defined vehicle types map directly to the market segments used here – for example PICKUP,

VAN CARGO, BUS SCHOOL, and TRACTOR TRUCK – because they are definitively descriptive of

the final vehicle configuration. Others are more ambiguous and provide little information about the

actual vehicle configuration and use – examples include CAB CHASSIS, STRAIGHT TRUCK, and

INCOMPETE (STRIP CHASSIS).

For this project, assignment of vehicles to each market segment is therefore based on a combination of

VIN-defined Vehicle Type and, if necessary, IHS-defined Registration Vocation and weight class. See

Figure A1, which shows how these attributes were mapped to market segments to estimate the number

of vehicles in each segment. Single unit trucks with indeterminate VIN-defined vehicle type were

assigned to the different market segments based on the type of company that registered them (Registration

Vocation) – as an indication of the vehicle configuration/use based on the work performed by the owning

company.

For example, there are many types of buses in the fleet, but only School Buses are definitively identified

by VIN-defined vehicle type. As shown in Figure A1 the other types of buses in the fleet (Transit, Coach,

Shuttle) were assigned to the bus market segments based on the registering company having Registration

Vocation “Bus Transportation”.

Similarly, Class 3 – 5 single-unit trucks with indeterminate VIN-defined vehicle type were assigned to

the Delivery Van market segment if the registering company had a registration vocation of

Wholesale/Retail, Beverage Processing and Distribution, or Food Processing and Distribution as these

types of companies typically use Class 3-5 vehicles to make local deliveries of the products they

manufacture and sell. In addition, 75% of the vehicles of this type that were registered by companies with

registration vocations characterized as General Freight delivery companies were also put into this market

segment. The remaining 25 percent of Class 3 – 5 vehicles registered by General Freight companies were

classified as small Box Trucks.

Note that Registration Vocation is based on the type of company that registered the vehicle, and is not

directly based on vehicle attributes, so the mapping shown in Figure A1 produced a first order estimate

of market segment population subject to some uncertainty. For example, not all trucks with Registration

Vocation “Sanitation/Refuse” are necessarily refuse-hauling trucks. Similarly, not all vehicles with

Registration Vocation “Wholesale/Retail” are necessarily box trucks used to deliver freight.

27

The IHS VIO database that includes Registration Vocation over-estimates the number of in-use vehicles in

Arizona and California, because these states have non-expiring registrations for some vehicles. MJB&A used IHS

estimated in-use vehicle totals from their statistical database for AZ and CA (which includes scrappage

assumptions) to adjust for this overcount when developing national total estimates presented here. At the national

level the VIO database overcount is approximately 4%.

27

Figure A1 M/HD Vehicle Attribute Mapping to Market Segments

PICKUP

SPORT UTILITY VEHICLE

STEP VAN

VAN CARGO

VAN PASSENGER

GLIDERS

TRACTOR TRUCK

Transit Bus BUS NON SCHOOL ALL

Class 8

2

School Bus BUS SCHOOL ALL Class 7 - 8

BUS NON SCHOOL ALL

CAB CHASSIS

CUTAWAY

INCOMPLETE (STRIP CHASSIS)

INCOMPLETE PICKUP

STRAIGHT TRUCK

UNKNOWN

CAB CHASSIS

CUTAWAY

INCOMPLETE (STRIP CHASSIS)

INCOMPLETE PICKUP

STRAIGHT TRUCK

UNKNOWN

SERVICES

UTILITY SERVICES

UTILITY/HAZARDOUS MATERIAL

GOVERNMENT/MISCELLANEOUS

LANDSCAPING/HORTICULTURE

MARKET SEGMENT

Heavy Duty Pickup &

Van

Class 2b

1

& 3

Class 7 - 8

Class 3 - 5

VIN-Defined Vehicle Type

IHS-Defined Registration Vocation

Weight Classes

BUS TRANSPORTATION

ALL

ALL

Delivery Van

Regional Haul Tractor

& Long Haul Tractor

Shuttle Bus

Delivery Truck

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Service Van

Service Truck

WHOLESALE/RETAIL, BEVERAGE

PROCESSING & DISTRIBUTION,

FOOD PROCESSING &

DISTRIBUTION, and 75% of General

Freight

5

Same registration vocations as

Delivery Van

Class 6 - 7

Class 3 - 5

Same registration vocations as

Service Van

Class 6 -7

Class 3 - 5

28

Figure A1 M/HD Vehicle Attribute Mapping to Market Segments

For Tractor Trucks, the estimated number of vehicles used in long-haul versus regional haul service is

based on supplemental data from IHS which included additional attributes for each registered tractor,

including engine displacement, axle/wheel configuration, and cab style. Using these attributes MJB&A

estimated the number of tractors equipped with day cabs as opposed to sleeper cabs. The estimated

number of regional haul tractors includes 100% of estimated day-cab equipped trucks and 5% of

estimated sleeper-cab equipped trucks. Individual tractors were assumed to have day cabs if:

• Engine displacement is less than 10 liters,

SANITATION/HAZ MATERIAL

SANITATION/REFUSE

CONSTRUCTION

ROAD/HIGHWAY MAINTENANCE

OTHER

All other

3

ALL

4

Class 3 - 8

1

IHS database does not include Class 2b; Class 2b estimate from MOVES model

2

Transit Bus estimate is 69% of total; remainder are estimated to be Coach buses

3

Includes MOTOR HOME and FIRE TRUCK

4

Includes vehicles in weight classes from above registration vocations not otherwise assigned, plus

all vehicles in registration vocations FORESTRY/LUMBER PRODUCTS, MINING/QUARRYING,

AGRICULTURE, MANUFACTURING, EMERGENCY VEHICLES, DEALER, INDIVIDUAL, MISCELLANEOUS, and

UNCLASSIFIED

5

The General Freight category includes registration vocations: GENERAL FREIGHT,

GENERAL FREIGHT/HAZARDOUS MATERIALS, LEASE/FINANCE, LEASE/MANUFACTURER SPONSORED,

and LEASE/RENTAL

IHS-Defined Registration Vocation

Weight Classes

Same vehicle types as delivery

van

Class 3 - 5

Same registration vocation as small

stake trucks

Class 6 - 7

Same registration vocation as stake

trucks

Class 8

Same vehicle types as delivery

van

Refuse Hauler

MARKET SEGMENT

VIN-Defined Vehicle Type

Dump Truck

Stake Truck (large)

Stake Truck (small)

Box Truck (large)

Box Truck (medium)

Box Truck (small)

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Same vehicle types as delivery

van

Class 8

VEHICLE TRANSPORTER, MOVING

AND STORAGE, PETROLEUM,

SPECIALIZED/HEAVY HAULING,

HAZARDOUS MATERIALS,

PETROLEUM/HAZARDOUS

MATERIAL, and 25% of General

Freight

5

Class 3-5

Class 6 - 7

Class 8

Same registration vocations as

other Box Trucks

Same registration vocations as

other Box Trucks

29

• Engine displacement is greater than 10 liters but there are only two driven wheels (4x2 and 6x2

configuration), or

• Engine displacement is greater than 10 liters, and there are more than two driven wheels, but cab

style is any of the following: Low Tilt Cab, High Tilt Cab, Cab Forward, Short Conventional

Cab, Medium Conventional Cab, or Half Cab.

Based on this analysis, 30% of in-use Tractor Trucks are estimated to be used for regional haul operations

and 70% for long-haul operations.

The IHS VIO database cannot be used to estimate the number of Class 2b trucks in the fleet, which are a

subset of VIN-defined Class 2 trucks

28

. To estimate the number of these vehicles, MJB&A used EPA’s

MOVES3 model [2]. The Class 2b estimate includes vehicles identified in MOVES as Source Type

equals “Light Commercial Truck” or “Passenger Truck”, and Registration Class equals “41-LHD2b3”.

Definitive data on the composition of the Class 2b fleet is unavailable but the limited data that is available

indicates that the majority of these vehicles are “heavy duty” pickups and vans, with a small percentage

large SUVs [14]

29

The IHS VIO database also cannot distinguish Transit Buses from other “BUS NON SCHOOL” vehicles

(VIN-defined) or based on registration vocation. The estimated number of vehicles in the Transit Bus

market segment is 69% of registered Class 8 vehicles with vehicle type BUS NON SCHOOL; the other

31% are estimated to be intercity coach buses. These relative percentages of transit and coach buses are

based on vehicle populations reported in the National Transit Database (transit bus) [15], and the ABA

Coach Census (coach bus) [16].

28

VIN-defined Class 2 includes vehicles with GVWR 6,000 – 10,000 lbs. Class 2b includes vehicles with GVWR

8,500 – 10,000 lbs.

29

Class 2B examples for model year 2017 include Chevy Silverado 2500HD; Ford F250, F350 and E350; Ford

Transit; GMC Sierra 2500, and GMC Yukon 2500. Typically, only a portion of total sales of these models would

be Class 2b, with other vehicles of the same model classified as Class 2 or Class 3 depending on actual vehicle

configuration.

30

M/HDV In-Use Fleet: Environmental Impact

To estimate the environmental impact of each market segment, MJB&A calculated total annual fuel use

by the segment (diesel equivalent gallons) using the estimated number of vehicles in the segment, average

fuel economy for vehicles in the segment (MPG), and average annual miles driven per vehicle (VMT).

See Figure A2 for the MPG and VMT assumptions used.

Figure A2 M/HD Vehicle MPG and VMT Assumptions by Market Segment

For each market segment average MPG and average VMT/vehicle was estimated using a number of