Required disclosures appear on page 9

Analyst certification appears on page 11

1177 Avenue of the Americas 5

th

Floor

New York, NY 10036

Phone: 212-297-0001

www.sidoti.com

Yatra Online, Inc. (YTRA) is an online travel agency (OTA) company with a primary

focus on the corporate travel market. Although the shares faced a “one-two punch”

from the cancelled Ebix acquisition and the COVID-19 pandemic, the company remains

a leading OTA in India. In March 2019, Ebix (NASDAQ: EBIX, NC) made an offer to acquire

Yatra, and the companies agreed to the deal on July 17, 2019 for an EV of $337.8 million and

a stock price of about $4.90 per share. On June 5, 2020, Yatra terminated the merger

agreement and filed a lawsuit against Ebix, alleging breaches of the agreement. The end of

the failed Ebix deal coincided with the global response to COVID-19, which dramatically

reduced air travel and cut Yatra’s revenue by nearly 90%. However, as travel in India is

gradually recovering, recent share performance likely reflects an overly pessimistic scenario.

Yatra is India’s second or third largest leisure OTA and the largest corporate travel provider.

Although we think travel could be diminished for a few quarters, India is a high growth market

in both the leisure and business travel categories. With an enterprise value of about $34

million today, we think investors should consider the fundamentals of Yatra’s business.

We think Yatra’s position in the corporate travel market is differentiated and enables a

more efficient acquisition of leisure travelers. Through Yatra’s position as the leading

corporate OTA with a bevy of blue-chip companies signed to multi-year contracts, it already

serves some 15 million people including business travelers and their households. Those

households are likely to represent a significant portion of the rising middle class, putting Yatra

in an advantageous position to efficiently maintain its leisure brand and potentially spend less

to acquire leisure customers. India’s corporate travel market grew 12% annually in recent

years, pre-COVID. Yatra is leveraging its position with corporations by extending additional

services, such as deeply integrating expense reporting and offering its library of 100,000+

hotels, access to bulk discounts on products through Amazon. Yatra’s goal is to reduce

reliance on an unpredictable leisure market.

Yatra’s revenue declined in the quarters pre-COVID when the acquisition by Ebix was

pending, but marketing spending declined substantially and supported two quarters

with positive EBIT, suggesting greater efficiencies. YTRA reported a 26% decline in

revenue from 1Q:F20-3Q:F20 compared to 1Q:F19-3Q:F19, while operating expenses

declined 28% and sales and promotion expenses declined 76% over the same period. In

1Q:F20-3Q:F20, EBIT loss was $7.6 million compared to $26.2 million in the prior year

September

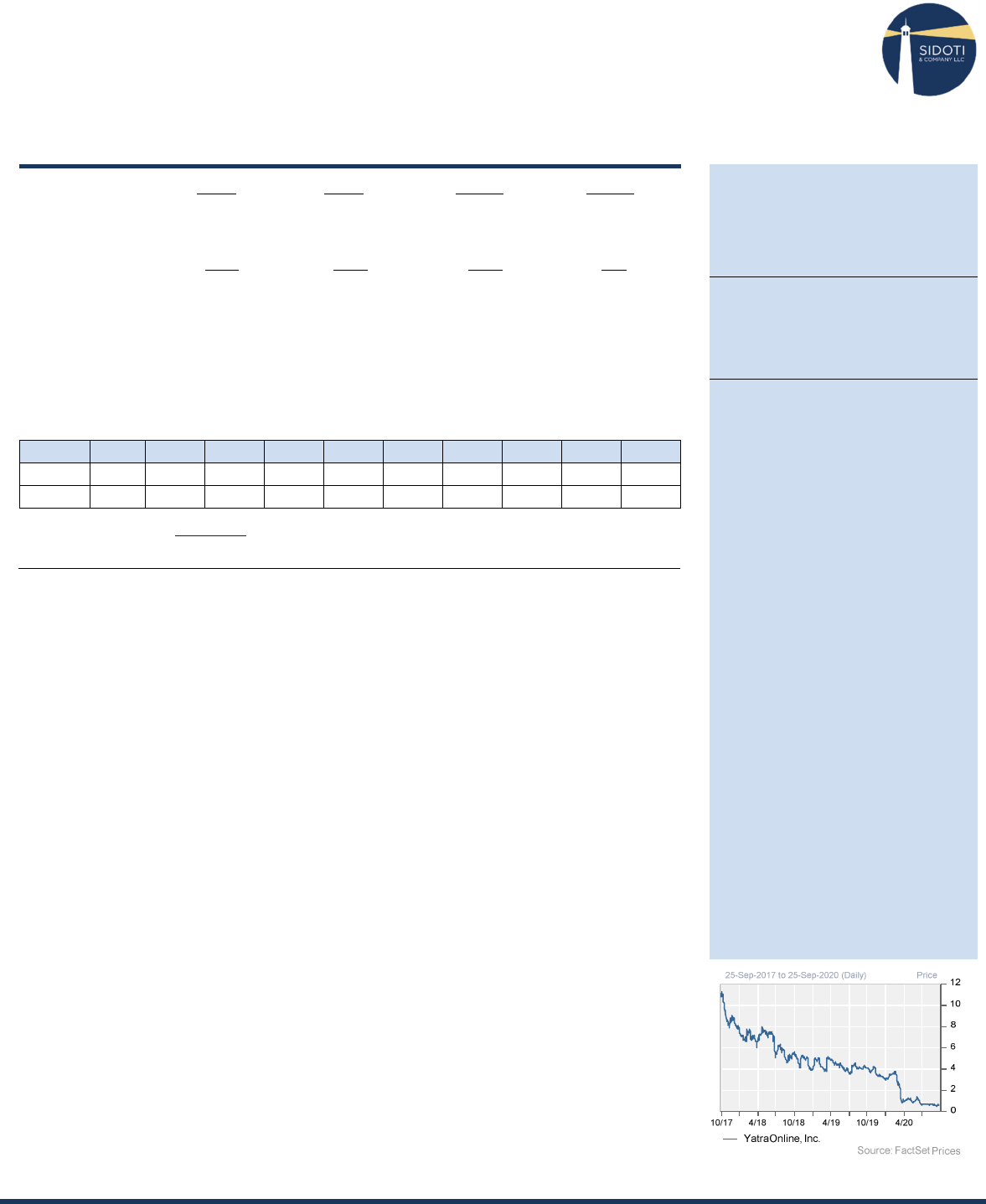

29, 2020 | Company Sponsored Research Report

Sidoti & Company, LLC

Member FINRA & SIPC

Initiation of Coverage

Yatra Online, Inc.

(YTRA)

Initiate Coverage Of Yatra Online, Inc. With A $1.50 Price Target

NR

Price Target: $1.50

Price: $0.70

Risk Rating: H

Matthew Galinko

(212) 894-3338

(mgalinko@sidoti.com)

Key Statistics

Analysts Covering 1

Market Cap (Mil) $40

Enterprise Value* $25

52-Week Range (NASDAQ) 4-1

5-Year EPS CAGR

N/A

Avg. Daily Trading Volume 674,000

Shares Out (Mil) 47.726

Float Shares (Mil) 45.515

Insider Ownership 18%

Institutional Holdings 52%

Annualized Dividend Nil

Dividend Yield N/A

FCF Per Share (F2022E) $0.08

FCF Yield (F2022E) 11.4%

Net Cash Per Share (F2022E) $0.23

Price to Book Value 1.5x

Return on Equity (F2022E)

NM

Total Debt to Capital 25%

Interest Coverage Ratio -12.88

Short Interest % 0.6%

Short Interest Days To Cover 0.7

Russell 2000 1,510

Russell 2000 - Last 12 Months -4.9%

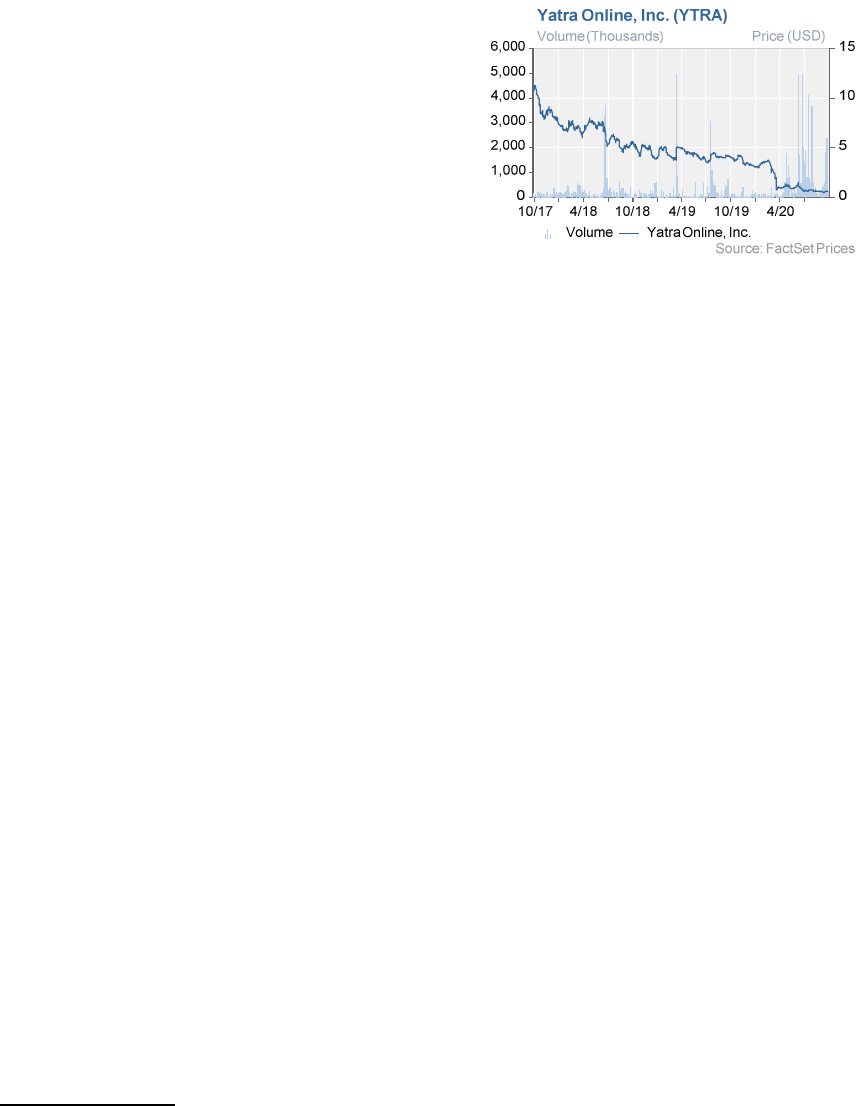

YTRA - Last 12 Months -83.2%

F2019

F2020

F2021E

F2022E

June

($0.23) ($0.13) ($0.13)A ($0.02)

Sep.

(0.13) (0.08) (0.09) (0.03)

Dec.

(0.11) (0.01) (0.05) $0.01

Mar. (0.22) (0.08) (0.04) 0.03

EPS (FY)

($0.68) ($0.29) ($0.30) ($0.01)

EPS (Cal.) ($0.44) ($0.35) ($0.08) N/A

P/E (FY)

NM NM

P/E (Cal.)

NM NM

Note: NR = Not Rated. Risk Ratings: H = Highly risky; M = Moderately risky.

Reported results use the exchange rate provided by company;

estimates use a spot rate at the time of publishing. Fiscal year ends March. C2022 estimates N/A until we provide F2023 estimates. We

calculate EV using F2022E projected net cash given our expectation for cash burn. Sum of quarterly EPS may not equal full-year total due to

rounding and/or changes in share count. NC=Not covered by Sidoti & Company, LLC.

Year

F2013

F2014

F2015

F2016

F2017

F2018

F2019

F2020

F2021E

F2022E

Rev.(Mil.)

N/A N/A N/A $125.8 $144.4 $113.8 $128.8 $79.4 $23.1 $55.5

GAAP EPS

N/A N/A N/A ($0.88) ($3.68) ($1.79) ($0.37) ($0.24) ($0.20) ($0.02)

* We use adjusted revenue that normalizes for revenue recognition changes that began in F2018. IFRS financial reporting.

Description: Yatra Online, Inc. (www.yatra.com) is an online travel agency (OTA) focused on India.

Yatra serves the leisure and corporate

travel markets, aggregating airline, hotel, and other travel options, allowing travelers to book through a single site. Headquarters are in

Gurgaon, India.

YATRA ONLINE, INC.

Sidoti & Company, LLC

2

period. YTRA reported an operating profit just prior to the beginning of COVID’s impact with very little promotional spending.

YTRA has made additional cuts due to COVID, and management expects to bring nearly 70% of pre-COVID revenue back at the

reduced spending levels.

The company stemmed its cash burn with cuts before and during the COVID interruption, and after a June secondary

offering, we estimate YTRA has about two years of cash were it to operate at trough revenue levels. YTRA reported

gross cash and term deposits of $48.6 million and net cash of $39.1 million ($0.64 per share) as of the end of 1Q:F21; the cash

balance as of August 31

st

was $33.7 million, including $7.7 million of restricted cash. The company has access to an untapped

credit facility of $8.3 million. YTRA raised approximately $10 million in a June secondary offering. YTRA reported a cash from

operations outflow of $7.3 million in F2020 ($1.5 million excluding working capital), an improvement from $47.7 million ($15.6

million) year over year. Management disclosed a $1.2 million monthly burn rate after the COVID-restructuring.

We initiate coverage of YTRA shares with a highly risky rating and $1.50 price target. OTA peers trade around 3.3x

EV/Sales, compared to Yatra’s 0.5x. We use about a 1.2x EV/Sales multiple applied to our estimate for F2022 revenue, which is

in line with YTRA’s historical 1.2x on a TTM basis. We assume F2022 to be a more normalized period than F2020 and F2021;

the discount to peers reflects the potential for dilution if the recovery is slower. However, if YTRA reaches profitability, drives

revenue growth, and generates sufficient cash flow to support the business, we think the trading multiple should approach the

peer group average. YTRA’s history of losses and the uncertain air travel recovery from COVID informs our risk rating.

Company Overview

Yatra Online is an online travel company founded in 2006

serving the Indian market, with headquarters in Gurgaon,

India. CEO Druv Shringi and CTO Manish Amin were co-

founders of the company and previously worked in

leadership positions at EBookers Group, a U.K. online

travel site founded in 1998.

Yatra’s website and mobile apps offer an integrated

approach to booking travel. Initially focused on air travel,

Yatra now offers hotels, cabs, buses, trains, cruises, and

assembled packages, among others. Yatra reaches

approximately 100,000 hotels in India, which we think is

the largest inventory in the market. The company began

to pursue the corporate travel market in 2013, which in

F2020 accounted for approximately 50% of bookings.

“Yatra” means travel or trip in Hindi, the most commonly

spoken language in India. Travel site visits and travel

bookings by mobile phones overtook computers in 2015,

and this trend is expected to continue. Today, Yatra’s

traffic mix is approximately 83% mobile versus 17% PC.

Yatra’s name may assist with a favorable ranking in the

Google Play store. Pre-COVID, some 60% of India’s

travel market was booked offline.

Ebix offered to acquire Yatra in March 2019, which

resulted in a merger agreement in July 2019. Ebix

apparently struggled to complete certain SEC filings and

later attempted to change the merger agreement; Yatra

left the merger agreement in June 2020 and filed a

lawsuit against Ebix in Delaware after terms of the

agreement were allegedly breached. We think it is

difficult to assess the likelihood that the case results in

awarded damages; we note that representation is on

contingency.

Yatra exited the Ebix merger agreement into the COVID-

19 pandemic that largely eliminated air travel in the worst

of the lockdown and reduced corporate and leisure

willingness to travel for the time being. The result was a

steep decline in Yatra’s June quarter results, with

bookings of -$2.8 million indicating widespread

cancellations and adjusted revenue of $3.1 million,

although we think that is likely to be the trough. As of

August/September, India is gradually opening air capacity

between regions with low infection rates. As more

regions reach acceptable infection rates, air capacity

should continue to grow. Further, with the assumption

that a vaccine will begin to be circulated in early 2021, we

think travel will continue to rebound more rapidly in the

following quarters and YTRA’s revenue should follow a

similar trajectory.

Yatra went public in 2016 through a reverse merger IPO

in a transaction valued around $253 million. The

company held about 2.9 billion Indian rupees ($43 million

at a then 67.944:1 exchange rate) in cash and

equivalents following the listing. YTRA raised $57 million

in a June 2018 secondary and about $12 million in a June

2020 secondary. There are 35 million warrants

outstanding, representing about 17.3 million shares

expiring in December 2021 with an exercise price of

about $26.

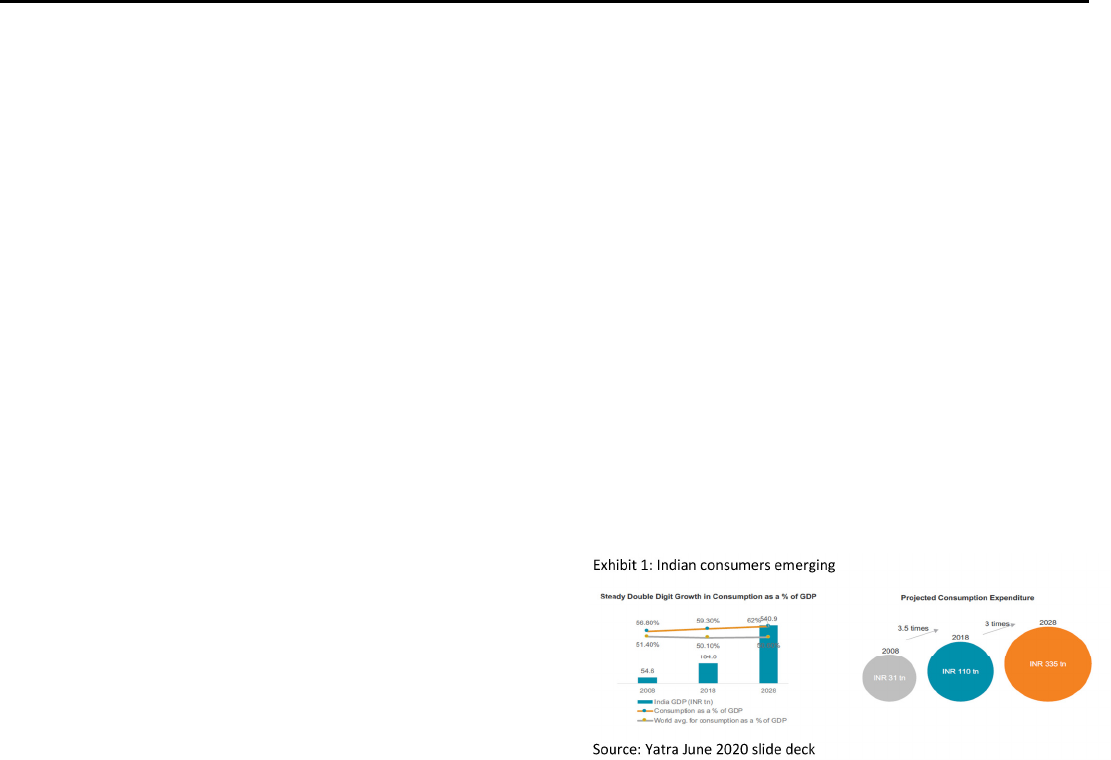

Market Opportunity In Emerging Middle Class

Exhibit 1 shows one of the underpinning elements for an

investment case in Yatra. India’s economy is reaching a

point of development where an emerging middle class

has significant disposable income and spending power.

India and China share a similar population of around 1.4

billion. China’s population is projected to peak in 2030

and India’s in 2060; we think it stands to reason that India

will likely overtake China’s population in the next decade.

YATRA ONLINE, INC.

Sidoti & Company, LLC

3

Both the economies of China and India have undergone

expansion since giving up centralized control, China in

1978 and India in 1990, amid industrialization. India’s

GDP per capita in 2019 was approximately equivalent to

China’s in 2007 adjusting for purchasing power parity

(PPP). China’s GDP per capita adjusted for PPP grew

about 11.6% annually on average from 2007 to 2019.

India’s GDP per capita adjusting for PPP grew 6.6% from

2010 to 2019. Data also shows a steady rise in

consumer spending and disposable income over the last

20 years in both countries; data was sourced from

tradingeconomics.com. FactSet estimates indicate a

return to Real GDP growth of 7.4% in 2021 in India

following the 2020 pandemic impact.

With rising political tension between India and China, and

between the U.S. and China, we think there is likely to be

greater political and economic cooperation between the

U.S. and India over the coming years, which may work to

the benefit of India’s economic growth.

We are not macroeconomists and do not have a nuanced

view or outlook of the Indian economy in the years ahead.

However, we think using China’s development over the

last 20 years as a likely proxy for India’s over the coming

years is a reasonable benchmark. If accurate, we think

India’s middle class will grow dramatically along with

disposable income and demand for luxury items and

experiences.

According to data from Statista.com, air passengers in

China grew by about 16% annually from 2010 through

2019. And according to the International Air Transport

Association (IATA) predicted that India would reach 414

million total air passengers traveling annually by 2037, up

from 158 million in 2017.

Corporate Travel Offers Numerous Growth And

Stability Vectors

Yatra launched a corporate travel strategy in 2013, which

we think was motivated by aggressive marketing by

leisure market competitors and after India’s air travel

market was disrupted by the bankruptcy of a large air

carrier.

By 2019, corporate accounted for approximately half of

Yatra’s bookings and the company claimed several high-

profile customer wins. Contracts typically are for multiple

years and include varying levels of integrations into the

customer’s ERP and other backend systems. Business

rules may be applied to limit corporate travel options to

different roles in the organization. We think the intensity

of integrating YTRA’s technology into customer backend

systems creates stickiness, as work would need to be

replicated if the corporate travel provider were replaced.

Corporate travel typically yields lower commission rates

than leisure travel, but the customer acquisition cost,

which is in the form of an enterprise service contract, is

conceptually amortized over a multi-year contract.

Notably, when the contract is renewed there is no

meaningfully additional or recurring customer acquisition

cost. Customer acquisition in the leisure market is

transactional by contrast. Spending on search engine

marketing is useful for attracting customers actively

searching for travel sites, which usually happens when a

customer plans to book travel. However, leisure travelers

do not tend to be repeat customers, which makes driving

profitable engagements challenging in a highly

competitive market for customer acquisition.

We think that Yatra’s role as a leading travel service

provider to large corporates in India is a strong branding

tool that resonates with the country’s emerging middle

class. Some of the corporate customers allow employees

to accrue points in Yatra’s loyalty program, which are

usable for leisure travel. According to management, the

cost of acquiring a customer through a loyalty program is

half that of search engine marketing. With about 15

million employees, plus household members, represented

in Yatra’s corporate travel business, the potential for

optimized customer acquisition is significant compared to

peers that significantly lag in corporate travel.

Yatra recently announced partnerships that can generate

non-travel booking revenue. In August 2020, YTRA

announced a partnership with Amazon Business. Yatra

will provide its network of hotels (approximately 100,000)

with bulk pricing on Amazon. Amazon’s breadth makes it

a potential “one stop shop” for hospitality customers. We

think Yatra will collect an affiliate fee, essentially a

commission, from sales through the system, that can

traditionally range from 1% to 10% depending on the

product. We think YTRA’s cost for operating this program

is minimal and revenue largely incremental. In July 2020,

Yatra announced a partnership and integration with

Zaggle, an Indian FinTech start-up delivering an expense

reporting solution. Zaggle has approximately 3,500 large

customers. We think it is a lower cost expense reporting

option that may better serve the local market with SaaS

type arrangements, compared to competitors like Concur.

Competition

Yatra’s competition is largely divided by leisure and

corporate travel; we do not know of a competitor that

participates in both markets to the extent of Yatra.

Leisure

MakeMyTrip (NASDAQ: MMYT, NC) is the largest player

in the OTA space, having extended its lead after

acquiring GoIbibo in early 2017. MMYT was founded in

2000 in the U.S., and targets Indians living in the U.S.

seeking travel to India. MMYT went public on NASDAQ

in 2010 and has since completed 11 acquisitions. MMYT

began building a corporate strategy in 2017, and as we

were not able to find an example of the company

discussing corporate in the bookings or revenue mix, we

think MMYT’s corporate business is likely small. At $673

million of adjusted revenue for the year ended March 31,

2019, MMYT generated about 5.7x greater sales than

YTRA prior to COVID. Sales and marketing accounted

for approximately 67% of MMYT’s revenue in F2018,

suggesting aggressive spending on customer acquisition.

We think YTRA’s investment in the corporate market

YATRA ONLINE, INC.

Sidoti & Company, LLC

4

years in advance of MMYT likely provides a significant

advantage in the corporate travel arena.

Bookings Holdings (NASDAQ: BKNG, NC) owns

bookings.com, KAYAK, priceline, agoda, Rentalcars.com,

and OpenTable. These brands are leisure travel focused

and we do not think BKNG has a corporate travel

strategy. BNKG lags MMYT in leisure travel in India.

Expedia Group (NASDAQ: EXPE, NC) operates

Expedia.com, HomeAway, Hotels.com, Hotwire.com,

Orbitz, Travelocity, trivago, Vbro, and CarRentals.com.

The company was founded in 1996 as a division of

Microsoft. The company launched a corporate travel

brand in the U.S. and France, but remains largely

focused on leisure travel.

ClearTrip is a privately held Indian travel company that

has discussed a goal of about $100 million in revenue

from India in F2020. While we think that the majority of

Cleartrip’s revenue is likely leisure, the company also has

a corporate travel strategy; it likely leads Yatra in the

leisure market, making it the second largest leisure OTA

behind MMYT.

Search Engines are an emerging competitor to leisure

OTA. Robust organic traffic is all that is needed, so large

internet search engines can acquire customers and

collect fees for travel bookings at minimal cost. Google

entered the U.S. market in 2011, drawing antitrust

complaints and taking share from market leaders.

Corporate

Carlson Wagonlit Travel, American Express GBT, and

BCD are corporate travel competitors based in the U.S.

and Europe. We think these companies have the ability to

sell global travel services but may not have Yatra’s reach

in India. Thomas Cook India is a multi-service travel

agency with headquarters in Mumbai, India, providing

foreign exchange, leisure bundles, visa and passport

services, among others; this is far from a pure play

corporate travel business.

Terminated Merger Agreement with EBIX

Ebix is an acquisitive public company, attempting over 30

deals since 2010 and completing approximately 5 out of 6

purchases of travel services related companies from

2018-2019. It announced an offer to acquire Yatra in

March 2019, and the companies reached a merger

agreement in July 2019. Yatra shareholders would

receive 0.005 shares of a new class of convertible

preferred stock in Ebix; each preferred share was to be

convertible into 20 shares of Ebix common. At Ebix’s

share price at the time of the deal, it approximated a

$337.8 million enterprise value and $239 million equity

value for Yatra shareholders. The offer represented a

32% premium to Yatra shares.

Yatra terminated the merger agreement with Ebix in June

2020 and filed litigation alleging breach of the agreement.

In a partially redacted legal complaint available for

shareholders on Yatra’s investor relations website, the

company alleges that Ebix was aware of and hid SEC

inquiries into its accounting practices that would preclude

the filing of an S-4 to complete the agreement, from

Yatra. Yatra also alleged that Ebix demanded to

renegotiate the deal after several months but refused to

proceed with good faith toward closing long after the

original merger agreement stipulated.

We do not put an expectation on the outcome of the

lawsuit. However, we do note that the merger agreement

put restrictive covenants on Yatra’s business, during

Ebix’s entrée into the market as a competitor; this is, in

the very least, poor optics.

The COVID Impact And Recovery

COVID-19 continues to challenge India. The government

ordered a 21-day lockdown on March 24, 2020, which

was subsequently extended. The country continues to

progress through a gradual reopening. Air and rail

services were suspended, cutting demand to virtually

nothing in the depth of the lockdown; this was reflected in

YTRA’s 1Q:F21 adjusted revenue of $3.1 million,

compared to $15.5 million sequentially, and $24.8 million

year over year.

Domestic air travel began to resume in July, although it

was limited to regions with lower infection loads.

Management noted approximately 20% of domestic air

travel capacity was back online as of early September.

It is difficult to predict when corporate and leisure travel

will return to prior volumes as there are divergent trends.

It took 22 months for air travel to return to where it was

prior to the 9/11 attacks, but broadband internet was still

in the early days of proliferation and remote work was not

nearly as feasible or accepted. Corporate risk

assessments may take longer to allow business travel to

resume in this era. On the other hand, India’s rapidly

expanding consumer class may opt for leisure travel as

has been the case in other emerging economies.

Recent Results

YTRA reports under the International Financial Reporting

Standard (IFRS) and its primary reporting currency is the Indian

Rupee. The company translates results to the US dollar

quarterly at a spot rate on the last day of the quarter; similarly,

full year reporting is translated to USD at the same spot rate as

the fourth quarter. The sum of reported translated quarters may

not be equivalent to the reported full year translation because

they are not calculated at the same translation rate.

We use adjusted revenue in place of IFRS revenue, in line with

YTRA’s reporting, which creates a more apples to apples

comparison to GAAP revenue reporting for travel companies.

Adjusted revenue treats commission from travel packages as

revenue instead of the gross booking, while also adding back

customer acquisition expenses; there is no difference in

earnings calculated using revenue and adjusted revenue.

YTRA’s fiscal year end is March. The company reported

a 1Q:F21 year-over-year revenue decline of 87% and a

sequential revenue decline of 80%, as domestic and

YATRA ONLINE, INC.

Sidoti & Company, LLC

5

global travel was shut down due to the global pandemic.

Total operating expenses declined to $9.1 million from

$18.4 million sequentially and $38.5 million in the prior-

year period. The company reported about $2.2 million in

one-time charges related to the terminated merger

agreement with Ebix. The 1Q:F21 adjusted EBITDA of

($4.1) million compared to ($3.8) million sequentially and

($3.0) million year over year. The severe demand impact

resulting from the pandemic was unusual, but we think

the cost control measures put in place are encouraging.

Earnings Outlook

We translate our estimates to USD uniformly at a spot

rate, and our estimates may be adjusted in subsequent

reports if the exchange rate changes. If we publish a

report after the end of a quarter but before the quarter is

reported, we will freeze the translation rate just for the to

be reported quarter.

For F2021, we anticipate adjusted revenue of $23.1

million, a decline of 71% compared to F2020 owing to the

impact of COVID-19. We expect sequential growth in

adjusted revenue each quarter, with 1Q:F21 the low point

of the year. Management discussed some 20% of

capacity returning to domestic air travel as of early

September and a slower rebound in international air

travel. Business travel is expected to remain muted. We

model operating expenses of $42.9 million, down 60%,

nearly in line with revenue. We project an adjusted

EBITDA of -$6.5 million, which compares to -$1.6 million

in F2020.

For F2022, we estimate adjusted revenue of $55.5

million, up 140% year over year, but still down from $79.4

million in F2020. Note that F2020 results were

diminished by the Ebix merger agreement before COVID-

19 partially impacted 4Q:F20. We model expenses

rebound 58% year over year to $67 million in F2022, but

still down from $106.7 million in F2020 as we expect

Yatra will maintain elements of its leaner operating

structure. We think that as revenue rebounds, the

company will reach positive adjusted EBITDA in 4Q:F21,

maintained throughout F2022, and positive net income for

the full year F2022. A slower recovery in revenue would

likely result in a slower rebound in spending.

Balance Sheet And Cash Flow

YTRA ended 1Q:F21 with $39 million ($0.64 per share) in

cash and equivalents net of debt (about $48.6 million

gross), and the company disclosed $33 million in cash

and equivalents at the end of August 2020 in an early-

September investor presentation; the change was largely

an earn out payment from a prior acquisition. YTRA’s

debt is comprised primarily of invoice discounting,

essentially funding receivables. The company reduced

fixed costs to about $14.4 million annualized ($1.2 million

per month) to preserve liquidity during the pandemic and

established a breakeven level of an estimated $45 million

in annual revenue. We think Yatra will reach breakeven

revenue in 1Q:F22, assuming our estimates and post-

COVID recovery in travel volumes stand.

We model free cash outflow of $6.8 million ($0.12 per

share) in F2021 and free cash flow of $4.8 million ($0.08

per share) in F2022. We model a cash outflow from

financing activities in F2022 results in a $0.2 million

decline in cash and equivalents, but that YTRA will end

F2022 with about $14.7 million ($0.24 per share) in net

cash.

Risks

The COVID-19 pandemic dramatically reduced air travel,

and the recovery timeline is uncertain, particularly as

infections in India continue to grow. Yatra significantly

reduced costs and India has allowed about 20% of domestic

air capacity to date. With vaccines tentatively expected in

early 2021, we think travel will begin to reset to relatively

normal levels by the end of 2021.

The OTA market in India is highly competitive and the

leisure market is prone to disruption. The most notable

recurring cost to an online travel business is customer

acquisition spending. Companies that can direct traffic at

lower costs, such as a search engine, can pose significant

challenges to standalone companies like Yatra.

YTRA has reported years of cash burn and losses.

However, we think the mix shift toward corporate affords the

company a more sustainable customer acquisition model

that yielded a profit just prior to COVID-19 impacting

revenue. Still, if YTRA does not turn the cash flow corner by

the end of F2022, we cannot rule out a dilutive capital raise.

YTRA received a delisting notice from NASDAQ. With

shares trading below $1.00, the company has an initial

period of until January 25, 2021 to regain compliance.

Given the extraordinary circumstances around COVID-19

and the likely business recovery in the coming quarters, we

speculate that leniency may be justified.

Valuation

YTRA stock currently trades around 0.7x F2022E adjusted

revenue and about 0.5x EV/F2022E adjusted revenue,

assuming net cash of $14 million at the end of F2022. The

shares trade around 0.8x the $50 million revenue level

attainable at the current expense level. In other words, we

think as travel returns to new normal levels, post-pandemic,

YTRA has the capacity to handle about $50 million of

revenue at the current reduced spending level. Peers trade

at a median of 2.2x trailing twelve-month revenue, which

captures part of the COVID impact; historically, peers have

traded at a median of about 4.2x EV/TTM revenue and

YTRA stock has traded at 1.2x EV/TTT revenue. Yatra’s

business faced a difficult sequence between restrictions

imposed by the terminated merger agreement with Ebix

followed by the pandemic, which obscured the business’ real

potential for five quarters. With air travel in India beginning

to return, we think YTRA’s business potential and efficiency

in corporate travel will become more apparent to investors.

We apply a multiple of about 1.2x our F2022E revenue to

arrive at a $1.50 price target. We think the multiple fairly

reflects the selected valuation horizon.

YATRA ONLINE, INC.

Sidoti & Company, LLC

6

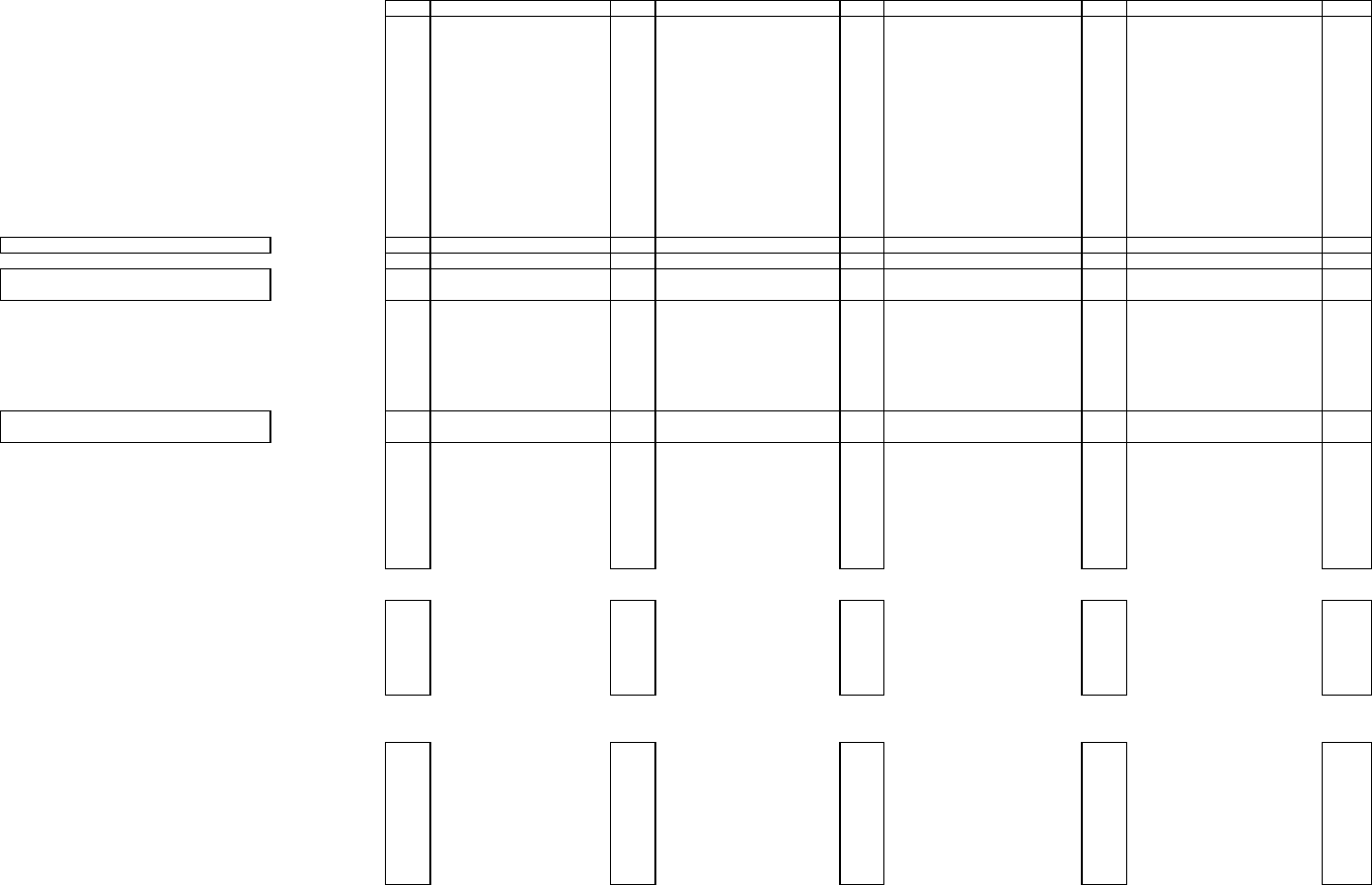

Table 1: Yatra Online Income Statement

($ in millions, except per share data)

F2018 June Sept Dec Mar F2019 June Sept Dec Mar F2020 JuneA SeptE DecE MarE F2021E JuneE SeptE DecE MarE F2022E

Adjusted revenue $113.8 $29.8 $28.9 $33.5 $35.3 $128.8 $24.8 $21.5 $22.2 $15.5 $79.4 $3.1 $3.2 $7.1 $9.6 $23.1 $11.0 $12.0 $14.4 $18.0 $55.5

Air ticket revenue

77.0

18.3

18.9

20.8

23.6

82.5

16.6

14.6

14.3

10.1

52.5

2.3

2.4

5.1

6.8

16.5

7.5

8.2

9.8

12.3

37.8

Hotel and package revenue 26.1 7.7 5.9 6.9 6.4 27.2 3.4 2.3 3.0 2.2 10.4 0.2 0.5 1.4 2.0 4.1 2.2 2.5 3.0 3.7 11.3

Total revenue 188.1 41.5 28.3 31.7 32.7 135.3 32.7 24.9 27.6 17.0 96.3 2.5 3.8 8.7 11.8 26.9 13.7 14.9 18.0 22.5 69.1

Rendering of services

180.4

39.4

25.1

27.8

28.4

121.7

28.8

21.4

23.4

14.5

83.1

2.2

3.6

8.1

11.0

25.0

12.4

13.5

16.3

20.3

62.5

Other revenue 7.7 2.0 3.3 3.9 4.2 13.6 3.8 3.5 4.2 2.5 13.2 0.3 0.2 0.6 0.7 1.9 1.3 1.3 1.8 2.2 6.5

Other income 1.4 1.2 0.4 1.5 0.7 3.8 0.4 0.7 0.4 0.7 2.1 0.4 0.1 0.1 0.1 0.8 0.1 0.1 0.1 0.1 0.5

Service cost 75.7 23.7 11.7 13.5 12.7 61.9 14.6 9.1 11.3 6.2 38.8 0.0 1.6 3.6 4.8 10.0 5.5 6.0 7.2 9.0 27.7

Personnel expenses 44.6 11.5 9.1 8.5 7.4 36.9 7.4 6.6 6.0 4.8 23.6 2.3 2.7 3.4 4.1 12.5 4.7 4.7 4.7 5.4 19.7

Marketing and sales promotion

63.8

4.2

2.7

2.4

2.3

11.7

1.2

0.7

0.4

0.5

2.6

0.1

0.3

0.3

0.3

1.0

0.4

0.5

0.5

0.5

1.9

Other operating expenses

50.5

11.7

16.2

11.5

17.3

57.5

12.9

10.1

7.3

1.8

30.0

4.7

2.0

2.0

2.0

10.9

2.0

2.7

2.7

3.4

10.8

Depreciation and amortization 6.5 1.9 1.9 2.0 2.5 8.4 2.4 2.4 2.5 2.1 8.8 2.1 2.2 2.2 2.2 8.6 2.0 2.0 2.0 2.0 7.8

Goodwill impairment

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

2.9

2.9

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Total expenses

241.1

53.0

41.6

37.8

42.2

176.4

38.5

28.9

27.5

18.4

106.7

9.1

8.8

11.4

13.4

42.9

14.7

15.9

17.1

20.3

68.0

Income from operations

(51.6)

(10.3)

(12.9)

(4.7)

(8.8)

(37.3)

(5.4)

(3.2)

0.4

(0.7)

(8.3)

(6.2)

(4.8)

(2.6)

(1.5)

(15.2)

(0.8)

(0.9)

1.1

2.3

1.6

Adjusted EBITDA

(29.3)

(5.9)

(3.2)

(2.2)

(6.3)

(17.8)

(3.0)

(0.8)

2.9

(3.8)

(1.6)

(4.1)

(2.6)

(0.4)

0.7

(6.5)

1.3

1.2

3.2

4.4

10.0

Share of loss of joint venture

(0.2)

(0.1)

(0.0)

(0.0)

(0.0)

(0.2)

(0.0)

(0.0)

(0.1)

(0.0)

(0.1)

(0.0)

(0.1)

(0.0)

(0.0)

(0.1)

(0.0)

(0.0)

(0.0)

(0.0)

(0.1)

Finance income

1.4

0.1

0.2

0.2

0.2

0.6

0.4

0.2

0.2

0.1

0.8

0.4

0.0

0.0

0.0

0.4

0.0

0.0

0.0

0.0

0.0

Finance cost (2.4) (0.7) (0.6) (0.9) (1.6) (3.8) (0.7) (0.7) (0.7) (0.6) (2.6) (0.5) (0.5) (0.5) (0.5) (2.1) (0.5) (0.5) (0.5) (0.5) (2.2)

Change in fair value of warrants

(8.7)

6.4

11.6

7.6

(2.0)

24.1

0.7

(1.7)

1.9

(0.8)

0.0

5.3

0.0

0.0

0.0

5.4

0.0

0.0

0.0

0.0

0.0

Income before taxes

(61.4)

(4.5)

(1.8)

2.2

(12.4)

(16.6)

(5.1)

(5.5)

1.7

(2.0)

(10.2)

(1.1)

(5.4)

(3.1)

(2.0)

(11.6)

(1.4)

(1.5)

0.5

1.8

(0.6)

Tax expense (0.9) (0.0) (0.4) (0.2) (0.0) (0.7) (0.2) (0.1) (0.1) (0.5) (0.9) 0.0 (0.1) (0.1) (0.1) (0.4) (0.1) (0.1) (0.1) (0.1) (0.5)

Net income

(62.2)

(4.6)

(2.2)

2.0

(12.4)

(17.3)

(5.3)

(5.7)

1.6

(2.5)

(11.1)

(1.1)

(5.5)

(3.3)

(2.2)

(12.1)

(1.5)

(1.6)

0.4

1.6

(1.2)

Adjusted net income

(37.9)

(8.5)

(6.0)

(5.1)

(10.3)

(30.3)

(6.0)

(3.9)

(0.3)

(3.9)

(13.3)

(6.3)

(5.5)

(3.3)

(2.2)

(17.4)

(1.4)

(1.5)

0.5

1.8

(0.6)

EPS Basic

($1.79)

($0.12)

($0.04)

$0.04

($0.26)

($0.38)

($0.11)

($0.12)

$0.03

($0.05)

($0.24)

($0.02)

($0.09)

($0.05)

($0.04)

($0.20)

($0.02)

($0.03)

$0.01

$0.03

($0.02)

EPS Diluted ($1.79) ($0.12) ($0.04) $0.04 ($0.26) ($0.37) ($0.11) ($0.12) $0.03 ($0.05) ($0.24) ($0.02) ($0.09) ($0.05) ($0.04) ($0.20) ($0.02) ($0.03) $0.01 $0.03 ($0.02)

Adjusted EPS

($1.10)

($0.23)

($0.13)

($0.11)

($0.22)

($0.68)

($0.13)

($0.08)

($0.01)

($0.08)

($0.29)

($0.13)

($0.09)

($0.05)

($0.04)

($0.30)

($0.02)

($0.02)

$0.01

$0.03

($0.01)

Basic shares outstanding 34.3 35.7 45.8 46.2 46.5 43.5 46.5 46.5 46.5 46.5 46.5 47.7 61.0 61.0 61.0 57.7 61.5 61.5 61.5 61.5 61.5

Diluted shares outstanding

34.3

36.4

46.6

47.3

46.5

44.3

46.5

46.5

47.2

46.5

46.5

48.5

61.0

61.0

61.0

57.9

61.5

61.5

61.5

61.5

61.5

% Change (Y-o-Y)

Adjusted revenue

64.8%

17.8%

11.4%

7.0%

10.6%

13.2%

-16.9%

-25.5%

-33.6%

-56.2%

-38.4%

-87.4%

-85.2%

-68.0%

-37.9%

-70.9%

253.1%

277.2%

102.6%

87.3%

140.0%

Air ticket

57.9%

11.4%

3.0%

-3.1%

11.4%

7.2%

-9.2%

-23.0%

-31.2%

-57.3%

-36.4%

-86.5%

-83.7%

-64.5%

-32.8%

-68.5%

230.8%

245.7%

93.6%

81.5%

128.5%

Hotel and package 70.5% 13.7% 20.4% 1.3% -17.3% 4.3% -55.7% -60.2% -56.8% -64.8% -61.7% -95.4% -76.9% -54.8% -9.5% -60.7% 1318.5% 353.8% 117.8% 81.5% 177.1%

Total expenses

60.8%

-14.3%

-13.8%

-40.1%

-39.1%

-26.8%

-27.4%

-30.7%

-27.3%

-56.4%

-39.5%

-76.3%

-69.6%

-58.5%

-27.2%

-59.8%

60.4%

81.3%

49.8%

51.5%

58.3%

EBIT

107.7%

-31.4%

46.3%

-52.7%

-51.3%

-27.8%

-47.5%

-74.9%

-108.7%

-92.1%

-77.8%

14.9%

48.1%

-733.8%

113.3%

83.7%

NM

NM

NM

NM

NM

Adjusted EBITDA 119.8% -37.0% -27.1% -63.5% -34.5% -39.5% -49.8% -74.5% -229.6% -39.7% -90.9% 37.2% 218.9% -114.3% -117.9% 305.8% NM NM NM NM NM

% of adjusted revenue

Air

67.7%

61.5%

65.5%

62.1%

66.8%

64.1%

67.2%

67.7%

64.4%

65.1%

66.2%

72.0%

74.5%

71.4%

70.4%

71.5%

67.5%

68.2%

68.2%

68.2%

68.1%

Hotel and package

22.9%

25.9%

20.4%

20.7%

18.0%

21.1%

13.8%

10.9%

13.5%

14.5%

13.1%

5.0%

17.0%

19.0%

21.1%

17.7%

20.2%

20.5%

20.5%

20.5%

20.4%

Service cost 66.6% 79.5% 40.3% 40.2% 36.0% 48.1% 59.0% 42.1% 50.9% 40.0% 48.9% 0.0% 50.0% 50.0% 50.0% 43.1% 50.0% 50.0% 50.0% 50.0% 50.0%

Personnel expenses

39.2%

38.5%

31.5%

25.5%

20.9%

28.6%

30.0%

30.9%

27.1%

31.3%

29.7%

72.6%

85.1%

47.6%

42.3%

54.0%

42.9%

39.5%

32.9%

30.1%

35.4%

Marketing and sales promotion

56.1%

14.0%

9.5%

7.1%

6.5%

9.1%

4.8%

3.0%

1.7%

3.4%

3.3%

2.5%

8.5%

3.8%

3.5%

4.2%

3.7%

3.9%

3.3%

3.0%

3.4%

Other operating expenses 44.4% 39.4% 56.2% 34.2% 48.9% 44.6% 51.9% 46.9% 32.9% 11.7% 37.8% 149.6% 63.8% 28.6% 21.1% 47.1% 18.4% 22.6% 18.8% 18.8% 19.5%

EBIT

5.7%

6.5%

6.6%

5.9%

7.1%

6.5%

9.6%

11.1%

11.1%

13.5%

11.1%

67.5%

67.8%

30.4%

22.4%

37.4%

17.7%

16.3%

13.6%

10.9%

14.1%

Adjusted EBITDA

-25.8%

-20.0%

-11.1%

-6.6%

-17.7%

-13.8%

-12.1%

-3.8%

12.9%

-24.4%

-2.0%

-131.0%

-82.2%

-5.8%

7.0%

-28.3%

11.4%

9.9%

21.9%

24.4%

18.0%

Net margin -54.7% -15.3% -7.6% 5.9% -35.2% -13.4% -21.5% -26.2% 7.1% -16.0% -14.0% -33.6% -172.9% -46.2% -22.7% -52.1% -13.9% -13.4% 2.5% 9.0% -2.1%

Sources: Company reports and Sidoti & Company, LLC estimates

Notes:

1. Yatra provides a courtesy fx translation from INR to USD as of the end of the reported quarter and year. The sum of translated quarters may not equal the translated year, which is how we derive full year results.

2. We will adjust estimate quarters for changes in the fx rate until the final day of an unreported quarter, when we will fix it to the snap rate that day.

3. Adjusted net income removes non-cash and one-time elements, such as stock-based compensation and change in fair value of warrants.

YATRA ONLINE, INC.

Sidoti & Company, LLC

7

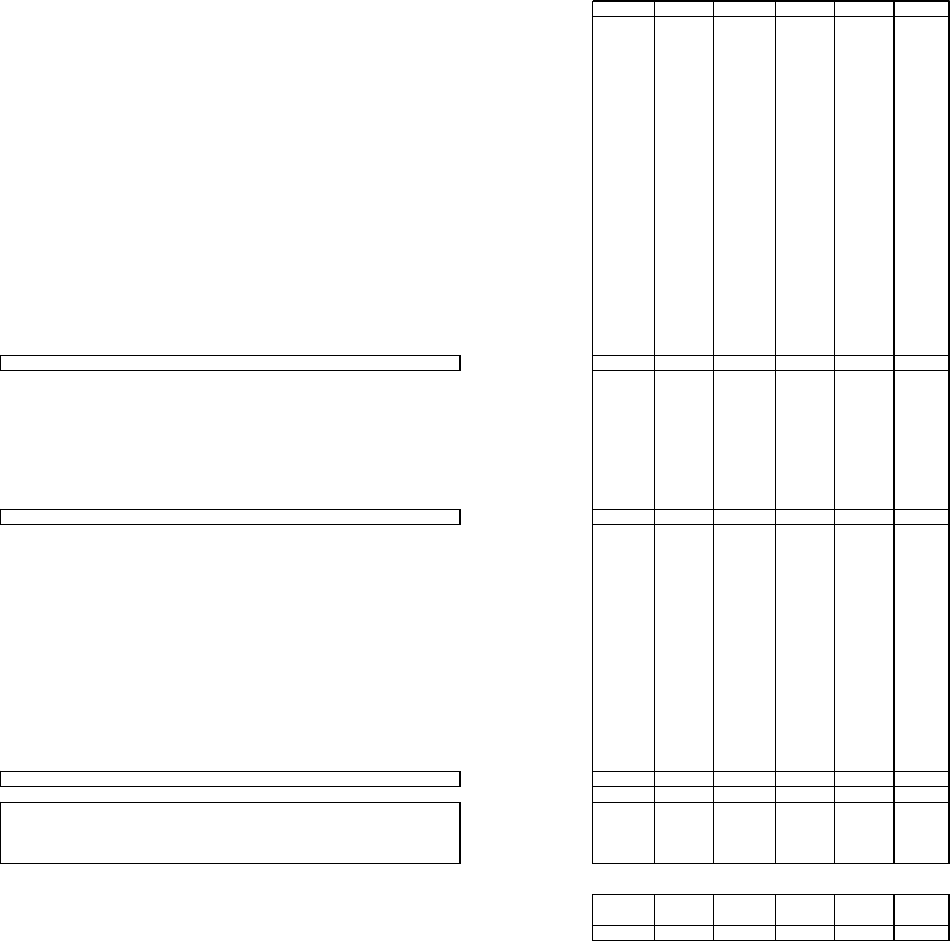

Table 2: Yatra Cash Flow Statement

($ in millions, except per share data)

F2017

F2018

F2019

F2020

F2021E

F2022E

Loss before tax

(91.1)

(61.4)

(16.6)

(10.2)

(11.6)

(0.6)

Depreciation and amortization 4.3 6.5 8.4 8.8 8.6 7.8

Listing and related expenses 62.9 0.0 0.0 0.0 0.0 0.0

Contingent dividend

0.0

(0.0)

0.0

0.0

0.0

0.0

Gain on termination of leases

0.0

0.0

0.0

(0.4)

0.0

0.0

Change in fair value of contingent consideration

0.0

4.5

7.0

(5.2)

0.0

0.0

Finance income (2.1) (1.3) (0.6) (0.4) (0.4) (0.4)

Finance costs 1.8 1.9 2.1 2.2 2.3 2.3

Impairment of goodwill

0.0

0.0

0.0

2.9

0.0

0.0

Unrealized foreign exchange loss/(gain)

0.1

(0.1)

(0.2)

(0.1)

0.0

0.0

Loss/(gain) on disposal of property, plant and equipment

(0.0)

(0.0)

(0.1)

(0.1)

0.0

0.0

Change in fair value of warrants (3.6) 8.7 (24.1) (0.0) (5.4) 0.0

Excess provision written back (0.7) (0.7) (0.5) (0.8) (0.4) (0.4)

Advances/provision written off 0.2 0.2 0.1 0.2 0.1 0.1

Trade and other receivables provision / written-off

1.2

1.8

4.4

1.2

1.4

1.4

Share of loss of a joint venture

0.1

0.2

0.2

0.1

0.0

0.0

Share-based payment expense

9.1

11.2

4.1

0.1

0.1

0.1

Change in working capital (6.8) 14.8 (32.1) (5.8) 1.5 (2.6)

Increase in trade and other receivables (13.7) (12.7) (19.0) 33.0 12.9 (22.2)

Decrease in inventories

(0.0)

(0.1)

0.3

0.0

0.0

0.0

Increase in trade and other payables

7.9

29.2

(13.3)

(38.3)

(11.4)

19.6

Direct taxes paid (net of refunds)

(0.9)

(1.6)

0.0

(0.5)

0.0

0.0

Net cash used in operating activities (24.6) (13.5) (47.7) (7.3) (4.0) 7.6

Acquisition of business

0.0

(5.4)

(3.7)

0.0

(0.7)

0.0

Investment in joint venture

(0.0)

0.0

0.0

(0.0)

0.0

0.0

Purchase of property, plant and equipment

(1.0)

(3.4)

(0.4)

(0.2)

(0.1)

(0.1)

Proceeds from sales of property, plant and equipment 0.0 0.0 0.2 0.3 0.0 0.0

Purchase of in tangible assets (6.3) (5.4) (5.7) (2.7) (2.7) (2.7)

Investment in term deposits (159.0) (80.8) (38.1) (14.5) 0.0 0.0

Proceeds from term deposits

129.4

113.7

38.2

18.3

0.0

0.0

Interest received

0.2

0.1

0.2

0.1

0.1

0.1

Net cash used in investing activities

(36.8)

18.8

(9.4)

1.3

(3.4)

(2.7)

Payment of principal portion of lease liabilities 0.0 0.0 0.0 (0.6) (0.5) (0.5)

Payment of interest portion of lease liabilities

0.0

0.0

0.0

(0.7)

(0.7)

(0.7)

Issuance of shares pursuant to Business Combination

61.3

0.0

0.0

0.0

0.0

0.0

Purchase of own shares

(0.2)

0.0

0.0

0.0

0.0

0.0

Proceeds from issue of share capital 25.9 0.1 51.5 0.0 10.5 0.0

Acquisition by non controlling interest 0.0 0.0 0.0 0.0 0.0 0.0

Transaction with equity shareholders

0.0

(1.7)

0.0

0.0

0.0

0.0

Proceeds from borrowings

0.0

21.5

0.0

0.0

0.0

0.0

Repayment of borrowings

(6.7)

(9.2)

(7.3)

(4.5)

(2.7)

(2.7)

Repayment of vehicle loan (0.2) (0.3) (0.4) (0.3) (0.3) (0.3)

Repayment from invoice discounting 0.0 0.0 0.0 12.2 0.0 0.0

Repayment of invoice discounting 0.0 0.0 0.0 (8.8) 0.0 0.0

Interest paid on term loan

(0.5)

(1.0)

(1.0)

(0.2)

(0.2)

(0.2)

Interest paid on vehicle loan

(0.1)

(0.1)

(0.1)

(0.0)

0.0

0.0

Interest paid on bank overdraft

(0.2)

(0.6)

(0.8)

(1.2)

(0.7)

(0.7)

Net cash from financing activities 79.3 8.9 42.0 (4.4) 5.5 (5.0)

Net increase (decrease) in cash and equivalents

18.0

14.1

(15.1)

(10.4)

(1.9)

(0.2)

Effect of exchange differences on cash and equivalents

(0.3)

0.2

2.7

0.9

0.0

0.0

Cash and equivalents beginning of year

6.0

23.5

35.6

18.1

8.8

15.2

Cash and equivalents end of year 23.7 37.9 19.7 8.6 15.2 15.0

FCF (Outflow)

(31.9)

(22.4)

(53.8)

(10.2)

(6.8)

4.8

FCF (Outflow) per share

($1.52)

($0.65)

($1.22)

($0.22)

($0.12)

$0.08

INR to USD translation rate 65.1 65.1 69.2 75.4 73.8 73.8

Sources: Company reports and Sidoti & Company, LLC estimates

Notes: Results are translated from Indian Rupee to USD at the rate corresponding to the year.

YATRA ONLINE, INC.

Sidoti & Company, LLC

8

Table 3: Yatra Online Balance Sheet

($ in millions, except per share data)

June

Sept

Dec

F2019

June

Sept

Dec

F2020

JuneA

SeptE

DecE

F2021E

F2022E

Property, plant, and equipment

3.1

2.9

2.7

2.2

1.8

1.5

1.2

0.8

0.7

0.5

0.3

0.1

0.1

Right-of-use assets 0.0 0.0 0.0 0.0 2.4 2.2 8.1 7.1 6.8 6.8 6.8 6.8 6.8

Intangible assets and goodwill 30.9 32.2 32.3 32.3 31.0 29.5 26.6 22.6 21.7 20.4 19.1 17.9 16.1

Prepayments and other assets

0.1

0.1

0.1

0.1

0.1

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Other financial assets

0.8

0.6

0.5

0.4

0.4

0.3

0.3

0.4

0.4

0.4

0.4

0.4

0.4

Term deposits 0.0 0.0 0.0 0.3 0.3 0.3 0.3 0.0 0.0 0.0 0.0 0.0 0.0

Other non financial assets

2.6

2.7

2.7

3.7

3.4

3.5

3.0

3.0

3.0

3.0

3.0

3.0

3.0

Deferred tax asset

1.6

1.4

1.4

1.8

1.7

1.8

1.8

1.2

1.3

1.3

1.3

1.3

1.3

Total non-current assets

39.1

40.1

39.8

40.9

41.2

39.0

41.2

35.2

33.9

32.4

31.0

29.5

27.7

Inventories 0.1 0.2 0.1 0.1 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Trade and other receivables

60.9

69.1

61.7

71.2

69.3

57.2

49.3

31.4

15.8

9.6

14.2

19.2

41.4

Prepayments and other assets

13.5

14.7

11.1

13.0

11.0

11.5

10.4

11.3

9.0

9.0

9.0

9.0

9.0

Income tax receivable 5.2 6.0 6.7 7.2 5.8 6.3 6.1 6.4 5.1 5.1 5.1 5.1 5.1

Other current financial assets 0.6 1.0 4.6 3.4 3.6 4.2 4.2 3.6 1.8 1.8 1.8 1.8 1.8

Other non financial assets

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Term deposits

12.0

14.7

14.8

14.5

15.0

10.0

11.5

10.0

9.4

9.4

9.4

9.4

9.4

Cash and cash equivalents 69.2 56.5 40.0 31.2 15.0 17.8 12.7 18.1 40.3 27.0 20.6 15.2 15.0

Total current assets

161.7

162.1

139.1

140.5

119.8

106.9

94.3

81.0

81.5

62.0

60.2

59.9

81.9

Total assets

200.8

202.2

178.8

181.5

161.0

145.9

135.5

116.2

115.4

94.4

91.2

89.4

109.6

Total shareholders' equity 42.8 43.7 45.7 34.4 28.1 22.2 22.6 20.0 29.8 23.2 19.6 17.0 17.7

Borrowings

3.4

2.1

0.8

0.4

2.4

2.1

7.6

6.4

6.4

6.4

6.4

6.4

6.4

Trade and other payables 0.0 0.0 0.0 0.0 0.0 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4

Deferred tax liability

0.6

0.6

0.6

0.6

0.6

0.6

0.5

0.5

0.5

0.5

0.5

0.5

0.5

Employee benefits

1.0

1.0

1.1

1.2

1.2

1.2

1.0

0.8

0.7

0.7

0.7

0.7

0.7

Deferred revenue

2.7

0.0

0.0

1.4

2.3

1.2

2.5

3.1

3.1

0.5

1.1

1.4

2.7

Other financial liabilities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other non-financial liabilities

0.1

0.1

0.1

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Total non-current liabilities

7.8

3.8

2.6

3.6

6.6

5.3

11.9

11.1

11.0

8.4

9.0

9.4

10.6

Borrowings 12.3 18.0 18.1 16.7 15.1 13.5 17.3 13.8 3.4 3.4 3.4 3.4 3.4

Trade and other payables

68.8

72.7

61.6

76.1

64.0

58.1

44.8

37.9

40.5

28.7

28.5

28.9

45.1

Employee benefits

1.2

1.3

1.5

1.4

1.4

1.4

1.2

1.1

1.0

1.0

1.0

1.0

1.0

Deferred revenue 14.4 14.6 11.5 8.4 5.9 5.4 2.5 1.7 1.9 1.9 1.9 1.9 4.1

Income taxes payable

0.0

0.0

0.0

0.1

0.1

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Other financial liabilities

36.4

32.1

23.4

25.4

24.7

25.5

22.2

17.8

12.8

12.8

12.8

12.8

12.8

Other current liabilities

17.0

16.1

14.6

15.4

15.1

14.5

12.9

12.7

15.0

15.0

15.0

15.0

15.0

Total current liabilities 150.2 154.7 130.6 143.5 126.3 118.4 100.9 85.0 74.6 62.8 62.6 63.0 81.4

Total liabilities

157.9

158.5

133.3

147.1

132.8

123.8

112.8

96.1

85.6

71.2

71.6

72.4

92.0

Total equity and liabilities

200.8

202.2

179.0

181.5

161.0

145.9

135.5

116.2

115.4

94.4

91.2

89.4

109.6

Metrics

Net cash

65.5

51.2

35.9

28.8

12.5

12.1

(0.6)

7.9

40.0

26.7

20.2

14.9

14.7

Net cash per share

$1.41

$1.08

$0.77

$0.65

$0.27

$0.26

($0.01)

$0.17

$0.66

$0.44

$0.33

$0.26

$0.24

LT Debt to Total Capital 7.4% 4.5% 1.8% 1.0% 7.9% 8.7% 25.0% 24.3% 17.6% 21.5% 24.5% 27.2% 26.5%

Return on equity (ttm)

NM

NM

NM

NM

NM

NM

NM

NM

NM

NM

NM

NM

NM

INR to USD translation rate

72.5

69.6

69.2

69.2

70.6

71.4

75.4

75.4

73.8

73.8

73.8

73.8

73.8

Sources: Company reports and Sidoti & Company, LLC estimates

Notes:

1. Yatra provides a courtesy fx translation from INR to USD as of the end of the reported quarter and year. The sum of translated quarters may not equal the translated year, which is how we derive full year results.

Appendix

Required Disclosures

Sidoti & Company, LLC

9

Required Disclosures

Yatra Online, Inc. (YTRA-$0.70) NR Price Target: $1.50 Risk Rating: H

Risks

The COVID-19 pandemic dramatically reduced air travel, and the recovery timeline is uncertain, particularly as infections

in India continue to grow. Yatra significantly reduced costs and India has allowed about 20% of domestic air capacity to date.

With vaccines tentatively expected in early 2021, we think travel will begin to reset to relatively normal levels by the end of 2021.

The OTA market in India is highly competitive and the leisure market is prone to disruption. The most notable recurring

cost to an online travel business is customer acquisition spending. Companies that can direct traffic at lower costs, such as a

search engine, can pose significant challenges to standalone companies like Yatra.

YTRA has reported years of cash burn and losses. However, we think the mix shift toward corporate affords the company a

more sustainable customer acquisition model that yielded a profit just prior to COVID-19 impacting revenue. Still, if YTRA does

not turn the cash flow corner by the end of F2022, we cannot rule out a dilutive capital raise.

YTRA received a delisting notice from NASDAQ. With shares trading below $1.00, the company has an initial period of until

January 25, 2021 to regain compliance. Given the extraordinary circumstances around COVID-19 and the likely business

recovery in the coming quarters, we speculate that leniency may be justified.

Valuation

YTRA stock currently trades around 0.7x F2022E adjusted revenue and about 0.5x EV/F2022E adjusted revenue, assuming net

cash of $14 million at the end of F2022. The shares trade around 0.8x the $50 million revenue level attainable at the current

expense level. In other words, we think as travel returns to new normal levels, post-pandemic, YTRA has the capacity to handle

about $50 million of revenue at the current reduced spending level. Peers trade at a median of 2.2x trailing twelve-month

revenue, which captures part of the COVID impact; historically, peers have traded at a median of about 4.2x EV/TTM revenue

and YTRA stock has traded at 1.2x EV/TTT revenue. Yatra’s business faced a difficult sequence between restrictions imposed

by the terminated merger agreement with Ebix followed by the pandemic, which obscured the business’ real potential for five

quarters. With air travel in India beginning to return, we think YTRA’s business potential and efficiency in corporate travel will

become more apparent to investors. We apply a multiple of about 1.2x our F2022E revenue to arrive at a $1.50 price target. We

think the multiple fairly reflects the selected valuation horizon.

Sidoti & Company. Sidoti & Company, LLC is a licensed broker/dealer, and publishes research reports about some of the

securities it follows. All research published by Sidoti & Company, LLC is based on public information, or on information from the

company discussed in the report that that company is required to promptly make public . This report was prepared for market

professionals and institutional investor customers. Market professionals and institutional investors should consider this report as

only one factor in making their investment decisions. This report is for information purposes only and is not intended as an offer

to sell or a solicitation to buy securities. This research report is not a substitute for the exercise of your independent judgment.

Appendix

Sidoti & Company, LLC

10

Information contained herein is based on sources we believe to be reliable but we do not guarantee their accuracy. The stock

rating on this report reflects the analyst’s recommendation based on a 12-month period. It should be presumed that the analyst

who authored this report has had discussions with the subject company to ensure factual accuracy prior to publication.

Sidoti does NOT own securities of the issuers described herein, and Sidoti does not make a market in any securities. Sidoti does

not engage in, or receive compensation from, any investment banking or corporate finance-related activities with the company

discussed in the report. Sidoti’s contracts with issuers protect Sidoti’s full editorial control of all research, timing of release of

reports, and release from liability for negative reports. To ensure further independence, the company discussed in the report has

agreed to a minimum coverage term of one Initiation Report and three Update Reports, which that company cannot unilaterally

terminate earlier. Sidoti & Company, LLC takes steps to ensure analyst independence including setting fees in advance and

utilizing analysts who must abide by the CFA Institute Code of Ethics and Standards of Professional Conduct. Each Sidoti &

Company, LLC analyst has full discretion on the rating and revenue target based on his or her own due diligence. Analysts are

paid in part based on overall profitability of Sidoti & Company, LLC. Such profitability is derived from a variety of sources and

includes payments received from issuers of securities covered by Sidoti & Company, LLC for services described below. No part

of analyst compensation was, or will be, directly or indirectly, related to the specific recommendations or views expressed in any

report or article. All issuers to be considered for research obtain the approval of a stock selection committee comprised of the

Director of Research, the Chief Compliance Officer, and an independent outside person for screening applicants.

Sidoti Company Sponsored Research Rating System The Sidoti & Company, LLC Company Sponsored Research rating

system consists of “Moderately Risky” (M) and “Highly Risky” (H) ratings. “Moderately Risky” suggests companies, that while still

subject to relatively high price volatility, are characterized by more stable and predictable cash flow, a more established operating

history, and an operating environment that is somewhat less competitive with a potential for loss of principal. “Highly Risky”

suggests high risk equities of companies with a short or unprofitable operating history, limited or less predictable revenues, very

high risk associated with success, significant financial or legal issues, or a substantial risk/loss of principal. As of 09/29/20,

Company Sponsored Research provides research on 23 companies, of which 18 (78%) are rated Moderately Risky and 5 (21%)

are rated Highly Risky. Earnings targets and opinions concerning the composition of market sectors included in this report

reflect analyst judgments as of this date and are subject to change without notice. A risk to our earnings targets is that the

analyst’s estimates or forecasts may not be met. This report contains forward-looking statements, which involve risks and

uncertainties. Actual results may differ significantly from such forward-looking statements. Factors that may cause such

differences include, but are not limited to, those discussed in the “Risk Factors” section in the issuer’s SEC filings available in

electronic format through SEC Edgar filings at www.sec.gov.

Every company in the Microcap sector bears certain inherent risks and Sidoti & Company, LLC will not provide any company

subject to those risks with a rating below moderate because stock in the Microcap segment of the market have many risks that

are not as prevalent in Large-Cap, Blue Chips, or even Small-Cap stocks. Often it is these risks that cause Microcap stocks to

trade at discounts to their peers. The most common of these risks is liquidity risk, which is typically caused by small trading floats

and very low trading volume which can lead to large spreads and high volatility in stock price. In addition, Microcaps tend to have

significant company specific risks that contribute to lower valuations. Investors need to be aware of the higher probability of

financial default and higher degree of financial distress inherent in the Microcap segment of the market.

Sidoti & Company policy is to update research reports as and when the Research Analyst and Research Management deem

appropriate, based on developments with the issuer, the sector, or the market that may have a material impact on the research

views or opinions stated therein. In addition, certain Research publications are intended to be updated on a regular periodic basis

(weekly/monthly/quarterly/annual) and will ordinarily be updated with that frequency, unless the Research Analyst and Research

Management determine that a different publication schedule is appropriate based on current conditions.

Sidoti & Company Research does not provide individually tailored investment advice. Sidoti & Company Research has been

prepared without regard to the circumstances and objectives of those who receive it. Sidoti & Company recommends that

investors independently evaluate particular investments and strategies, and encourages investors to seek the advice of a

financial adviser. The appropriateness of an investment or strategy will depend on an investor's circumstances and objectives.

The securities, instruments, or strategies discussed in Sidoti & Company Research may not be suitable for all investors, and

certain investors may not be eligible to purchase or participate in some or all of them. Sidoti & Company Research is not an offer

to buy or sell or the solicitation of an offer to buy or sell any security/instrument or to participate in any particular trading strategy.

The value of and income from your investments may vary because of changes in interest rates, foreign exchange rates, default

rates, prepayment rates, securities/instruments prices, market indexes, operational or financial conditions of companies or other

factors. There may be time limitations on the exercise of options or other rights in securities/instruments transactions. Past

performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that

may not be realized. If provided, and unless otherwise stated, the closing price on the cover page is that of the primary exchange

for the subject company's securities/instruments.

These opinions may not fit to your financial status, risk and return preferences. For this reason, to make an investment decision

by relying solely to this information stated here may not bring about outcomes that fit your expectations. The trademarks and

service marks contained in Sidoti & Company Research are the property of their respective owners. Third-party data providers

make no warranties or representations relating to the accuracy, completeness, or timeliness of the data they provide and shall not

have liability for any damages relating to such data.

Appendix

Sidoti & Company, LLC

11

Investors should consider Sidoti & Company Research as only a single factor in making their investment decision. For valuation

methodology and risks associated with any recommendation, rating or price target referenced in this research report, please

contact the Client Support Team as follows: US/Canada +1 212-453-7000. Alternatively you may contact your investment

representative or Sidoti & Company Research at 1177 Avenue of the Americas, (Attention: Director of Research), New York, NY

10036 USA.

Compensation. Sidoti & Company, LLC received a flat fee of $40,000, renewable annually from the company discussed in this

report for the creation and dissemination of an Initiation Report and three Update Reports, including this report. The purpose of

the fee is to subsidize the high costs of research and monitoring. Sidoti holds a conference twice a year and charges a fee of

$5,000 per conference for presenting companies. Sidoti does not currently have a current investment banking services

relationship with the company discussed in this report, or contemporaneously with any other companies discussed in other

(Sidoti) Company Sponsored Research reports. Sidoti has not received investment banking income from the company discussed

in the report in the past 12 months, and does not expect to receive investment banking income from the company discussed in

the report in the next 12 months. Of securities rated in other Sidoti Company Sponsored Research reports, Sidoti has received

investment banking income from 0 companies (0%) in the past 12 months. Investment banking services, as defined under FINRA

Rule 2241, include, among other things, acting as an underwriter in, or as a member of the selling group in, a securities

underwriting. Sidoti’s role in any issuer’s investment banking transaction can be viewed in that issuer’s filings at www.sec.gov.

Sidoti has non-research employees who will seek compensation for brokerage commission revenue in connection with market

trading the securities of this company. Sidoti & Company, LLC has received compensation for non-investment banking services

on the Small-Cap Universe, and expects to receive additional compensation for non-investment banking services on the Small-

Cap Universe, paid by issuers of securities covered by Sidoti & Company, LLC analysts. These non-investment banking services

include investor relations services and software, financial database analysis, advertising services, brokerage services, advisory

services, investment research, investment management, non-deal road shows, and attendance fees for conferences sponsored

or co-sponsored by Sidoti & Company, LLC.

Sidoti Analysts. Sidoti policy does not allow an analyst or a member of their household (i) to own, trade, or have any beneficial

interest in any securities of any company that analyst covers, or (ii) serve as an officer or director of a covered company. Sidoti

employees, including research analysts, receive compensation that is based in part upon the overall performance of the firm,

including revenues generated by Sidoti’s investment banking and brokerage activities, but compensation is not directly related to

investment banking or brokerage revenues.

Sidoti maintains and enforces written policies and procedures reasonably designed to prevent any controlling persons, officers (or

persons performing similar functions), or employees of Sidoti from influencing the activities of research analysts and the content

of research reports prepared by the research analyst. Sidoti research analysts seek to have management of their covered

companies meet with investors during non-deal road shows. Analysts’ compensation may be related to their success in

scheduling non-deal road shows. This approach could be viewed as presenting potential conflicts of interest.

Reprints of Sidoti & Company, LLC reports are prohibited without permission. Additional information is available upon request.

For any further questions, please contact the Chief Compliance Officer at Sidoti.

Analyst Certification. Matthew Galinko certifies that this report accurately reflects his/her personal views about the subject

securities and issuers and that none of the research analyst's compensation was, is or will be, directly or indirectly, related to the

analyst's specific recommendations or views contained in this research report

Source

Key Statistics data is sourced from FactSet Research Systems