USAID-Funded Nepal Hydropower Development

Project (NHDP)

November 29, 2018

This document was prepared for the United States Agency for International Development Nepal (USAID/Nepal) by Deloitte

Consulting LLP on Contract No. AID-367-TO-15-00003. The contents are not the responsibility of USAID, and do not

necessarily reflect the views of the United States Government.

Hydropower Financing: Traditional Project Finance,

EPC and EPC-F

Name of Facilitator: Sreeram Pethi

Designation: Senior Financial Advisor

Date: 29 November 2018

Training Objectives

By the end of this session, participants should be able to:

• Growing role of Chinese Infrastructure funding

• Understanding Engineering, Procurement, Construction and Financing (EPC-

F contract)

• EPC vs EPC-F

• EPC –F: Nepal Context

Growing role of Chinese Infrastructure Funding

Introduction

• China is a major funder of developing country infrastructure, lending ~$40

billion annually through policy banks.

• Starting in 2013 China “branded” the program under Belt and Road Initiative

(BRI)

• The BRI consists of two major components:

– Silk Route Economic Belt: overland rail and pipeline connections between

China and Europe via Western China and Central Asia; and

– 21st Century Maritime Silk Road: a seaborne trade route linking China to

Europe via South Asia and the Horn of Africa

• Growing appetite for debt among developing countries driving demand for

additional funds including Chinese financing

– Increased borrowing to bridge budget deficits (Demand side factor)

– Increased Infrastructure spending (Demand side factor)

– Increased appetite for debt of developing countries due to prospect of

higher returns (Supply side factor)

Rising preference for Chinese financing

• Chinese financing is been preferred

– China provides funding in situations where many other traditional

countries are not willing to provide finance

– Chinese government interaction with developing countries does not

prescribe solutions and does not present itself as a expert on developing

countries problems

– China frames its interactions in the context of Infrastructure cooperation

and multilateral engagement with bodies and emphasises its developing

country status

Reasons for increased China lending to developing countries

• Chinese funding provides business opportunities for Chinese contractors

– it creates a situation where countries are getting into debt with China and

China then pays itself through contracting

• Securing resources: China’s financing to in many developing countries is

linked to securing the continent’s natural resources by providing infrastructure

paid for by commodity backed loans

• Enables faster and cheaper transportation of natural resources to the

Chinese economy.

• Better infrastructure in developing countries will facilitate the penetration of

Chinese goods deeper into the continent

• To further its geopolitical control over the continent and pursue strategic

interests. Countries has often consider this as “Debt trap”

• Financing from China opens economies up to Chinese entrepreneurs.

Understanding Engineering, Procurement, Construction

and Financing [EPC-F]

Introduction to EPC-F

• Project financing mechanism in which the EPC contractor also arranges

financing for the project, through tie-ups with financing institutions.

• This model has been implemented for project development, especially in

developing countries.

• It is useful when EPC contractors have better access to low cost financing,

including EXIM financing (In China, Japan, Korea)

• Some examples of proposed EPCF financing in Nepal

– 48.8 MW Khimti -2 hydro power project by Chongqing water Turbine works

– 1200 MW Budhigandaki Hydro electric company by China Gezhouba

Group corporation (Reservoir based project)

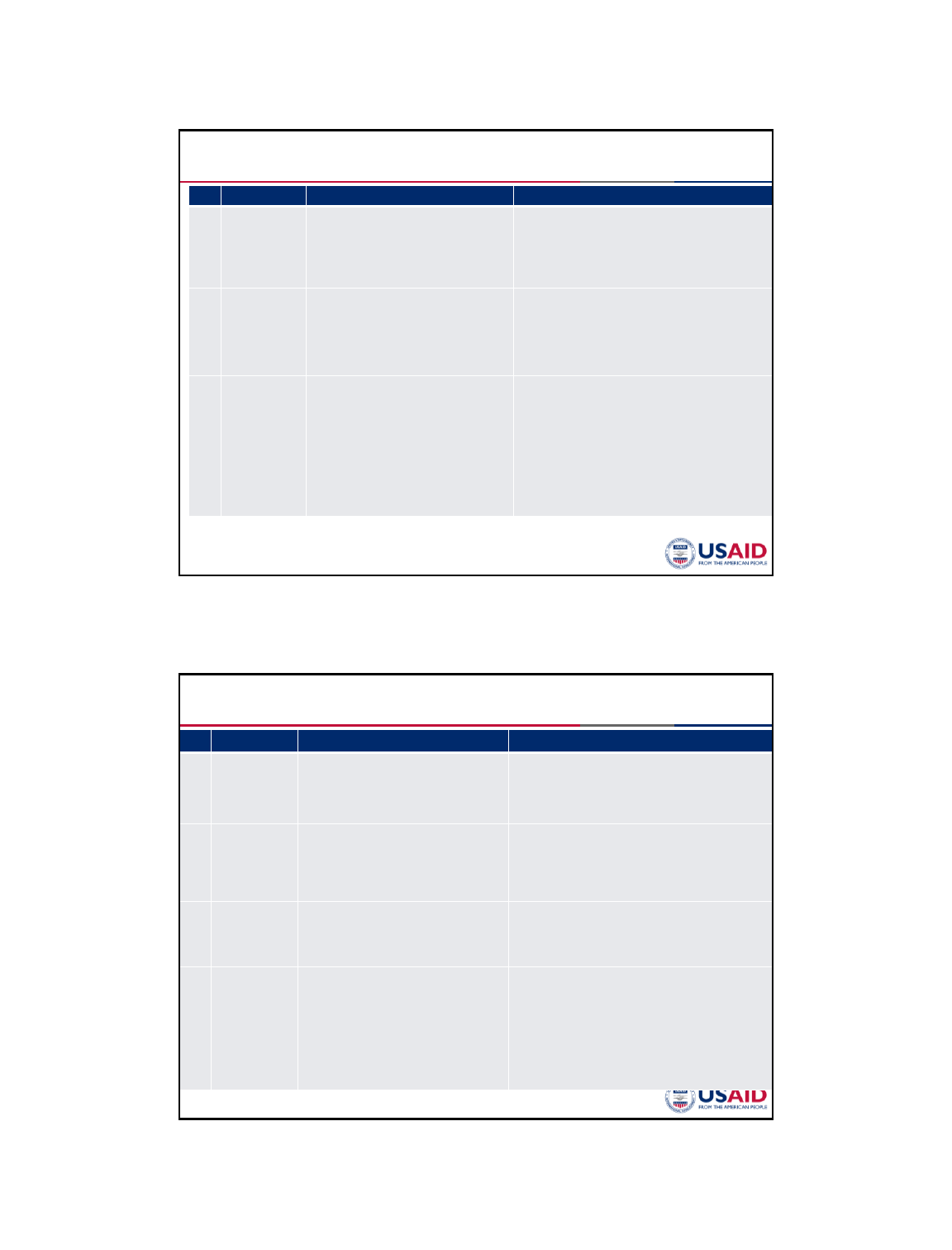

Traditional Project Financing

Parent

Off taker

EPC

Contractor

Lender

Host

country

government

Project

Company

Loan $

Equity

Investment

EPC

Contract

O&M

Contractor

PPA

PDA/IA/PA

O&M

Agreement

Distinguishing Features of Chinese Financing

Resource

Security

Chinese

Content

Government

Involvement

Security and

Credit

Comfort

Typical Chinese EPC-F Funding

Parent

Chinese

Off taker

Chinese

EPC

Contractor

Chinese

Lender

Host

country

government

Project

Company

Loan

$

Equity

Investment

EPC

Contract

O&M

Contractor

PPA

PDA/IA/PA

O&M

Agreement

Chinese

Government

Chinese

Content

Resource

Security

Framework

agreement

Government

Involvement

Chinese

Government

Sovereign

Guarantee

Security and

credit comfort

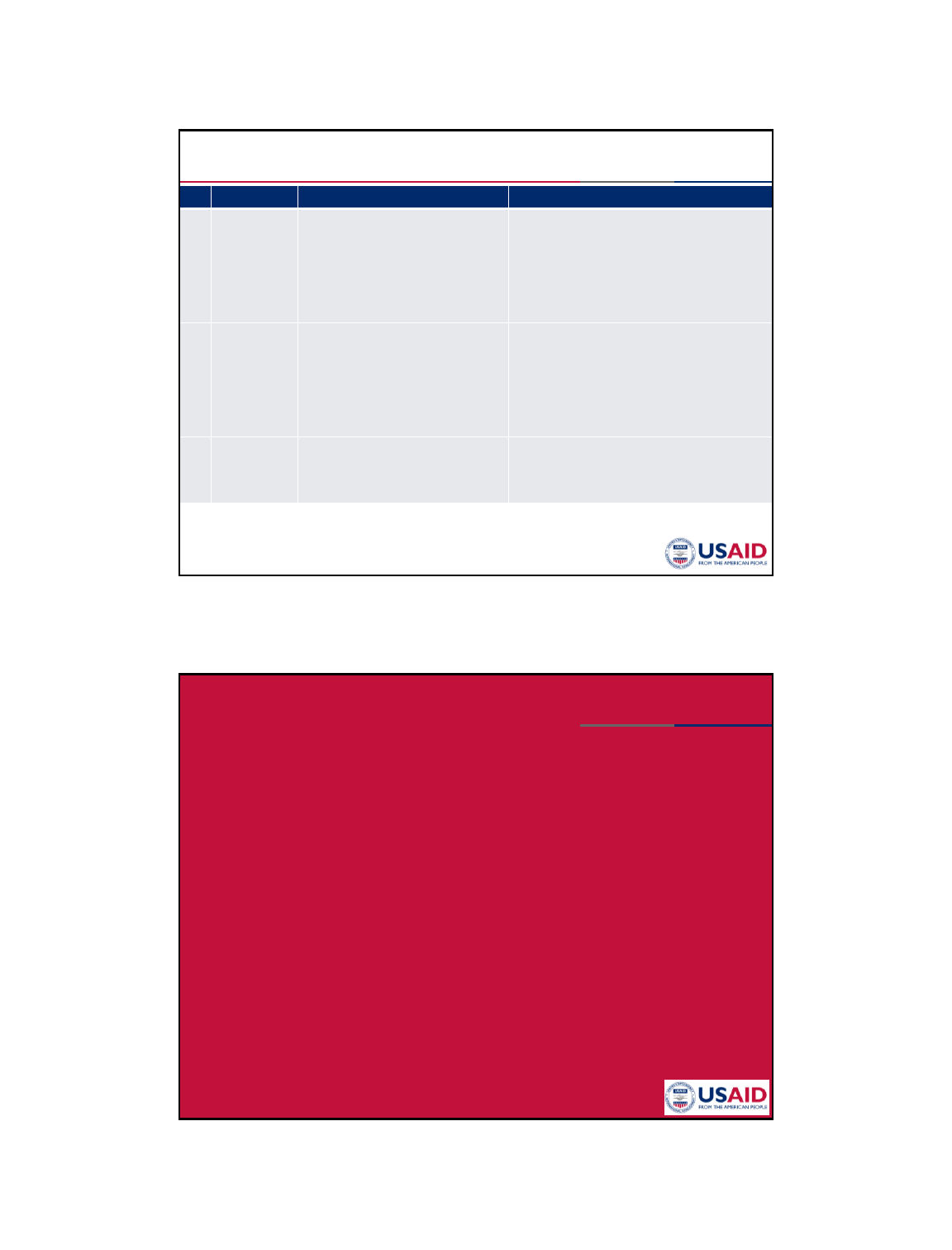

EPC vs. EPC-F

Difference between EPC and EPC-F

S No

Parameter Project Finance Model (EPC) EPCF Model

1

Developer

selection

Developer

for the project is selected by

the

Government

either through Memorandum

of

Understanding

(MoU) or open competitive

bid

process

(QCBS/ least cost, etc.).

The

developer

could be a public sector or

private

sector

company.

The

developer would generally be a public

sector

company/

authority in the host country responsible

for

project

development and sale of electricity.

Government

can

extend same type of concessions/ benefits

made

available

to the private developer under a

concession

agreement

.

2

Project

Financing

The

project financing is the responsibility

of

project

developer which owns the

project

company

and has to mobilize debt and

equity

as

per the requirements of

project.

Government

is expected to provide

sovereign

guarantees

but not mandatory.

The

project financing is generally tied and provided by

a

foreign

country/ National Bank of the foreign

country/

development

agencies affiliated to a foreign country.

Host

Government

is responsible for arranging the

counterpart

funding

and for providing sovereign guarantees to

the

project

and lenders.

3

Contractor

selection

There are a number of variations to the

traditional project finance model. Under the

traditional model, the EPC contractor will be

selected by the SPV and subsequently

approved by the lenders prior to financial

close (FC) on the basis of cost, schedule, and

outputs. At a minimum, Lenders’ advisors will

review and approve the final EPC contract

.

The

EPC contractor will be responsible to finance a

large

portion

of the project. The EPC selection criteria

is

determined

on the basis of the availability of finance

which

may

be offered by EPC or available through a

separate

framework/

arrangement. The selection process tends

to

be

restrictive to a particular country or set

of

manufacturers

Difference between EPC and EPC-F

S No

Parameter Project Finance Model (EPC) EPCF Model

4

Off

-taker risk

Developer

needs to factor the off-taker risk

in

the

bid process/ negotiations. The

lenders

tend

to be directly exposed to the off-

taker

risk

and hence do their own due diligence

and

also

require step-in rights for the project

The

off-taker risk is responsibility of the project

company

and

the host government.

5

Project Contract

framework

Concession

Agreement, PPA, TSA.

Lenders

can enter into a separate

agreement

with

Government to safeguard

their

investment

. The lenders to not typically

have

any

financial liabilities to the

government

under

the Lender’s Agreement.

Concession

Agreement (optional), PPA, TSA,

Government

to

Government Agreement.

Government

has to provide sovereign guarantee

to

safeguard

lenders’ interests and provide payment

security

guarantees

on behalf of off-taker, usually

government

owned

entity.

6

Financing

Cost

Directly

related to project risk and

market

rates

. These costs are negotiated

between

the

Lender and the Developer.

Linked

to MOU/Bilateral Agreement between the

Host

Government

and Government of country extending

the

EPC

tied financing. The expectation is that it would

be

concessional

loan.

7

Loan

terms

Because

project finance is on a non-

recourse

basis,

payment of the loan must be

covered

by

the steam of income generated by

the

SPV

. The lenders must therefore find

their

loan

repayment security in the

project’s

feasibility,

additional security such as

partial

risk

guarantees. Lenders are

mainly

interested

in security through the

loan

repayment

period.

There

is generally a guarantee mechanism for

the

lenders

. The arrangement has to be set out in the

bilateral

agreement

between the two Governments.

Difference between EPC and EPC-F

S No

Parameter Project Finance Model (EPC) EPCF Model

8

Project

cost

The

EPC contracts are fixed price with

limited

scope

for cost and schedule variation.

Project

costs

will be monitored by the lenders and

the

SPV’s

engineers.

The

ability to pass through escalated

costs

are

determined by the regulatory framework.

The

project cost is set by the SPV on the basis of the

EPC

bids

. Pass through of additional costs will be

determined

by

the regulatory framework. In a competitive bid

situation

escalated

costs resulting from geology or hydrology

will

normally

be passed through to end consumers.

9

O&M

performance

O&M

performance parameters are

generally

included

in the PPA; they are also

made

applicable

to the O&M contractor by way

of

the

O&M contract between the SPV and

the

contractor

. Failure to achieve the

required

performance

parameters may result

in

liquidated

damages.

O&M

is the responsibility of the project company and

is

generally

not the responsibility of EPC contract.

10

Conflict

resolution

Usually

by way of independent arbitration

or

mechanism

of the regulator.

Part

of the EPC contract. Needs to be defined to cover

all

penalties

.

EPC-F: Nepal Context

Suitability of EPC-F for various types of projects

Evaluation of EPC-F Proposals: Technical and financial

capability

Technical Capability

Financial Capability

a) Expertise, evidenced by experience,

in managing similar EPC contracts for

HPPs

a) The historical net worth of the

EPC

-F contractor as compared to

project cost

b) Expertise, evidenced by experience,

in providing services under EPC

-F

model

b) Historical average annual turnover

of the EPC

-

F contractor as compared

to project cost

c) Expertise, evidenced by experience,

in managing hydrological risks

c) The EPC

-F contractor’s ability to

provide a bank guarantee in respect

of the construction works

Evaluation of EPC-F Proposals: Commercial Evaluation

Models

Evaluation Criteria

Remarks

Model 1:

EPC + Debt

Financing

Based solely on the EPC costs. The

bidder with lowest EPC costs will have

the highest commercial score

This model is preferred in more mature

financing markets where equity funding is not

a concern and the debt market is more

mature.

Under this Model, negotiations on financing

arrangements are preferred rather than

considering financing costs during the

evaluation

Model 2:

EPC + Debt

Financing

This model considers a combination of

EPC costs and debt financing costs. NPV

of cash flows related to financing of EPC

cost is calculated. The bidder with lowest

NPV will have the highest commercial

score

This model is preferred in developing

countries where debt markets are less mature

and where there may be wide variations in the

availability and cost of debt financing

Model 3:

EPC+ Debt

Financing +

Equity

This model considers a combination of the

EPC cost and the overall financing costs.

The NPV of cash flows related to overall

financing of EPC cost is calculated. The

bidder with lowest NPV will have the

highest commercial score

This model is considered where both equity and debt

financing is a concern and the contractor is

expected to bring in both equity and debt.

Elements of EPC-F Framework for consideration

Key Elements

Remarks

Project Development

Activities including Land

acquisition etc.

Project Development activities to be undertaken by Project sponsor including clearance

land acquisition, R&R, clearance etc.

Project Selection

ROR projects >100 MW to be preferred initially. Other hydro projects including reservoir

based projects to be considered post successful implementation of initial projects

Availability of DPR and

engineering specifications

DPR and engineering specifications must be prepared before the issue of tender for EPC-

F

Bankability of PPA

The project should have a bankable PPA at the time of issue of tender for EPC

-F

Sovereign guarantee

The financing for the project must be backed by sovereign guarantee

Special purpose vehicle

(SPV)

The project must be owned by a separate SPV

Equity infusion by GoN

GoN shall infuse equity equivalent to at least 20

-25% of the project cost.

Handover of project

The project will be handed over to the Project SPV after commissioning and stabilisation,

after satisfactory performance trials have been conducted

Payment to EPC

-F

contractor

Milestone based payments, linked to progress in project construction and commissioning.

Only 10

-15% of the cost should be held back after project handover, for an additional

period of 1

-2 years.

USAID’s NEPAL Hydropower Development Project

Kathmandu, Nepal

THANK YOU!