Basic Spending Guidelines

by

Fund Source

April 29, 2021

2

East Carolina University

Basic Spending Guidelines by Fund Source

Table of Contents

April 29, 2021

Introduction ................................................................................................................................ 3

All Sources of Funds ................................................................................................................... 3

Appearance and Reasonableness Tests .................................................................................... 3

Exceptions and Interpretations................................................................................................ 3

Department Head Responsibilities........................................................................................... 3

Payments and Reimbursements to Employees ......................................................................... 4

Travel Reimbursements ........................................................................................................... 4

Moving Expenses .................................................................................................................... 5

Sponsorships ........................................................................................................................... 5

Fund Codes ............................................................................................................................. 6

Organization Codes ................................................................................................................. 6

Expenditure Account Codes.................................................................................................... 6

Program (Purpose) Code Attributes ........................................................................................ 6

Funding Sources .......................................................................................................................... 6

State Budget Codes - General Operating Funds........................................................................... 6

Unallowable Purchases from State Budget Codes .................................................................... 6

State Appropriated Carryforward Funds ...................................................................................... 8

Overhead Receipts Trust Funds .................................................................................................. 8

Auxiliary and Institutional Trust Funds ....................................................................................... 9

Receipts from Vending Facilities Trust Funds ............................................................................. 9

Grants and Contracts Trust Funds ............................................................................................ 10

Residual Funds Related to Grants and Contracts ....................................................................... 11

Gift and Endowment Income Trust Funds ............................................................................... 11

Endowment Principal Funds ..................................................................................................... 11

Patent Royalty Trust Funds ....................................................................................................... 11

ECU Physicians Trust Funds..................................................................................................... 11

ECU School of Dental Medicine (SoDM) Trust Funds ............................................................. 12

Agency Trust Funds .................................................................................................................. 12

Foundation Funds ..................................................................................................................... 12

Discretionary Trust Funds ......................................................................................................... 12

Employee Achievement or Recognition Awards and Retirement Gifts .................................. 13

Restaurant Charges ................................................................................................................ 13

Contributions and Donations ................................................................................................ 13

Additional Information.............................................................................................................. 14

Expediting Fee for H-1B Visa Forms (Form I-907) ............................................................... 14

Contact Information for Questions ....................................................................................... 14

Resources .................................................................................................................................. 14

Appendix................................................................................................................................... 15

Appendix A: Quick Reference Guide of Spending Rules by Fund Source............................. 15

3

East Carolina University

Basic Spending Guidelines by Fund Source

April 29, 2021

Introduction

The University has a wide variety of sources of funds, each of which has its own spending

characteristics. No set of guidelines can be written that addresses every possible expenditure

decision which may arise. These guidelines provide some basic standards, instructions and

precedents to guide an employee in making wise spending decisions. They are provided to ensure

that faculty/staff can carry out the University’s mission effectively, while ensuring that fiscally wise,

politically sound, and legal spending practices are followed. At all times, employees are required to

follow basic purchasing guidelines for the procurement of goods and services.

----------------------

All Sources of Funds

Appearance and Reasonableness Tests

For all potential expenditures from all sources of funds, the “appearance test” should be used, i.e.,

how would this purchase look to external constituents if placed on the front page of a newspaper.

Another test that is useful is to ask the question, “Is this expenditure necessary for a faculty/staff

member to do his/her job or for the University to carry on its normal business?” The use of these

tests should help to guide faculty/staff members in their decision-making. At all times, faculty/staff

are expected to manage funds wisely.

Exceptions and Interpretations

If a case occurs in which an individual believes an exception should be made to the guidelines,

he/she should request from their division business officer that an individual determination be made

on a particular item. The division business officer or designee will work with the University

Controller to determine the latitude available on the request, the University business purpose of

the request, and other options which may be available.

Department Head Responsibilities

The department head (individual responsible for the funds in a fund/org, including the principal

investigator for a research project) has the responsibility to ensure that proper documentation

procedures are followed for funds/orgs that he/she controls and that only authorized expenditures

are charged. Furthermore, the department head is responsible for ensuring that any funds/orgs

which he/she may control are reviewed at least monthly and any errors found are corrected.

Finally, the department head is responsible for ensuring all trust funds maintain a positive or zero

cash balance.

The department head may delegate authority to approve and sign direct payment forms, budget

4

forms, position change forms, pre-travel and post-travel forms and/or journal entry forms for

funds/orgs by the proper completion of a Delegation of Authority Form located in Pirate Port

.

The naming of a delegate does not relieve the department head of the ultimate fiscal responsibility

and accountability of funds under his/her control.

Payments and Reimbursements to Employees

Regardless of funding source, payments to employees are limited to authorized reimbursements,

authorized awards (see page 13) or authorized salaries. Payments to employees for compensation

for work must follow guidelines published by ECU Human Resources and must be initiated

through the payroll system.

According to IRS regulations, the University must have an “Accountable Plan” for reimbursing

employees for business related expenses on a tax-free basis. This “Plan” must apply to all funding

sources. Expenses must have a business purpose and must be reported within a reasonable period

of time. IRS requires that any payments made to employees NOT in compliance with this policy

be treated as supplemental wages and subjected to income tax withholding and payment of social

security, Medicare, and FUTA taxes.

Reimbursements for items such as supplies, travel, or meals to an employee must be for a valid

business purpose and must be approved by an individual at a higher level of authority in the

employee’s reporting structure. Employees must use the Chrome River Reimbursement System.

(See the Chrome River Website for additional information.) The purchase of items for personal

use is prohibited regardless of funding source. Any non-travel purchases should normally be made

with prior planning and through one of the following preferred purchasing methods: ProCard, on-

line orders for office supplies from contract vendor(s) as designated by Materials Management,

PORT purchase requisitions/orders (including campus storerooms), or blanket order. Note that

all purchases using grant funds must comply with regulations from the granting agency and/or in

the contract. Any purchases utilizing foundation and institutional trust funds must comply with

any restrictions applicable to the particular fund. For purchases that cannot be processed by one

of the preferred purchasing methods listed above, the Direct Payment Form may be used for

reimbursement. Utilization of the Direct Payment Form should be infrequent and only when other

disbursement methodologies are not available. Any such approved reimbursement must be

documented appropriately for the expenditure. An original, detailed, itemized receipt is the

preferred documentation for reimbursement requests. Reimbursement should be requested within

30 days of the date on which the expense was incurred.

Travel Reimbursements

Comprehensive travel reimbursement procedures may be found in the Travel Procedures Manual.

This manual includes requirements and procedures for reimbursement of costs for conferences,

training sessions and management retreats even when travel is not involved. Chrome River,

accessed through Pirate Port, must be used to request and document all authorizations to travel

[regardless of the method of payment (ProCard, reimbursement, direct payment, etc.)].

The University’s travel policies and procedures are based on the State Budget Manual, section 5,

which sets forth travel policies and regulations relative to securing authorization and

reimbursement of expenditures for official state travel. The administration and control of travel is

5

in accordance with the provisions of General Statutes (G.S.) 138-5, 138-6, and 138-7

.

All University travel is contingent upon availability of funds. The travel policies and procedures as

stated in the State Budget Manual apply to all University funds deposited with the State Treasurer,

whether derived from state appropriations or non-state funds (e.g., Institutional Trust Funds,

Contracts and Grants funds, and receipt supported programs/activities).

Moving Expenses – New and/or Existing Employees

The hiring approval process may include payment of reasonable moving/relocation expenses in

accordance with the University’s Policy on Non-Salary and Deferred Compensation for Employees

Exempt from the State Human Resources Act. When authorized, moving expenses for new and/or

existing employees may be paid and should be carefully documented. The following criteria must

be met.

• A change of residence is deemed to be in the best interests of the University when such a

change is required as a result of a promotion within the University or by a change in

assignment involving the transfer of the employee for the advantage and convenience of

the University, or if authorized by the Chancellor or designee, a new hire that is considered

in the best interests of the University.

• Move is accomplished within 90 days. The department head or designee may approve an

extension of an additional 90 days.

• For an existing employee, the new duty station is 50 miles or more from either the

employee’s existing (or prior) duty station or residence, whichever is closer to the new duty

station.

• For new hires, 50 miles or more from their existing residence.

Additional conditions and limitations on moving/relocation expenses may apply. – See State

Budget Manual sections 6.8 and 6.9.

All payments and/or reimbursements for moving expenses are taxable to the employee.

Reimbursements to employees should be coded to account code 61250, processed on a direct

payment form and sent to Accounts Payable. Payments to a vendor via ProCard or PORT should

be coded to 73086. Reimbursements to employees will be paid via payroll and the appropriate

withholdings will be deducted at the time of reimbursement. The value of the payments made to

third parties will be added to employee paychecks as a noncash benefit and withholdings will be

deducted accordingly. The payment amount will determine the number of payrolls the noncash

benefit will be deducted.

Sponsorships

External sponsorships may be allowed from state and/or nonstate funds if there is a clearly written,

documented benefit to the University or to the sponsoring department. For example, the ECU

Regional Development Office sponsors the North Carolina Eastern Region Entrepreneurship

Summit. The Office of Undergraduate Research sponsors the State of North Carolina

Undergraduate Research and Creativity Symposium. Undergraduate students who participate in

this annual event benefit by presenting their own research and observing the presentations of other

6

undergraduates. If a sponsorship is paid from more than one state fund (not fund 111102 or fund

111103), move budgeted funds from one state fund to the other using a BD04. If a sponsorship

is paid from either state fund 111102 or state fund 111103, split-code an invoice or reclassify the

expense. State funds cannot be used to pay for sponsorships to 501(c)3 organizations under any

circumstances.

Fund Codes

The fund code identifies the “owner” of the fund. The University Fund Types Report

lists fund

types and contact information and is located on Financial Services Controller’s Office website.

Organization Codes

The organization code is the designation for departmental subdivisions within the University which

identifies a unit of budgetary responsibility and is used to define “who” spends the money.

Expenditure Account Codes

Expenditure account codes are codes that must be used when processing financial transactions to

identify various classes of expenditures, for example, salaries, travel, supplies, equipment, etc. The

actual codes will provide even more detailed breakdowns of these groupings. This coding scheme

gives the University the ability to create reports that include, or are broken down by, the various

classes of expenditures.

Information regarding expenditure account codes for coding expenditures may be found by logging

into the Banner e~Print System and viewing the account code listing report, FGRACTH (Account

Hierarchy Report).

Program (Purpose) Code Attributes

Program (purpose) codes are codes that help to classify financial activity by its function, for

example, instruction, institutional support, research, or public service. With the exception of a few

grants, these codes should not be used to code a financial transaction but are built into the financial

system for each fund at the time the fund is created. Because of the need to report financial activity

by function, a fund may not be classified into more than one function.

----------------------

Funding Sources

State Budget Codes - General Operating Funds

This group of funds consists of state appropriated funds and receipt supported funds in the state

budget code. The University follows the rules, regulations and guidelines set forth in the Budget

Manual prepared by the Office of State Budget and Management (OSBM).

Unallowable Purchases from State Budget Codes

7

There are some purchases that are specifically not allowable from state funds. Examples include

the following:

• Alcoholic beverages, “setups”, drinks, or food items;

• Contributions and donations;

• Decorations (seasonal or otherwise);

• Excess per diem for meals on travel status;

• Extra insurance for rental cars – see Travel Manual);

• Flower arrangements, cut flowers, works of art, paintings, drawings, pictures, plaques,

plants, etc. Decorative/aesthetic items may be purchased for public areas such as lounges,

hallways, and reception areas.

• Food, coffee, tea, drinks, bottled water, candy, snacks, break refreshments, etc. except for

those provided under University and state travel regulations. The State Budget Manual

gives specific requirements and limitations for internal and external conferences.

• Get well cards, sympathy cards, birthday cards, thank you cards or holiday cards;

• Gifts or items of recognition (regalia, lanyards, cords, ribbons, plaques, awards, prizes)

unless recognizing years of service or items related to the graduation fee;

• Medications (pain relievers, aspirin, etc.), shots, and/or medical supplies for

staff/employees other than as may be required by federal or state regulations or for

emergency first aid.

• Multi-year agreements not with original purchase and multi-year agreements where vendor

requires up-front payment for all years;

• Paper products (cups, napkins, plates, utensils, etc.);

• Penalties or late fees; ∗

• Personal clothing items or t-shirts which are not part of required uniforms, safety related,

or required program-related;

• Personalized or personal use items (Kleenex, hand sanitizer or disinfectant wipes (except

in a medical setting or during a pandemic), desk name plates, personal memberships,

wireless routers for home use, etc.). Name badges may be purchased with state funds as

long as the position requires such identification. The badge must be worn during all work

hours.

• Pre-payments;

• Rental fees for non-State owned buildings for retreats, meetings, etc.

• Rental of portable water dispensers, coffee pots, or tablecloths or the purchase of items

related to refreshments;

• Search expenses for travel related to SHRA employees;

• Staff development expenses (Ropes courses, motivational speakers, etc.);

• Student registration fees unless on official state business;

• Window curtains and draperies made of cloth (blinds, shades, etc. may be ordered through

Facilities’ work order system).

∗ Note, travel penalties and charges incurred due to extraordinary circumstances like natural disasters, weather

events, and pandemic events, are permissible.

8

The University may employ a private employment search firm to conduct employment searches

for difficult to fill professional and managerial vacancies. Non-state funds shall be used to pay these

costs to the maximum extent possible. State funds may be used for EHRA positions only when

non-state funds are not available.

State Appropriated Carryforward Funds

State appropriated carryforward funds are State operating funds which have not been expended as

of June 30 of a fiscal year and have been approved to “carry forward” as budget in the next fiscal

year. Expenditures of these funds follow the same guidelines as normal State appropriated

operating funds except that, with the appropriate approvals related to capital improvement budgets,

and inclusion in the budget flexibility plan, funds may be transferred to capital improvement codes

and used for renovation and/or new construction projects. Once transferred to a capital

improvement code, the carryforward funds cannot be transferred back to an operating code.

Overhead Receipts Trust Funds

Expenditures from overhead receipts funds must be related to research unless the receipts are from

a grant that is not research related. Examples include public service or educational grants. In those

cases, the overhead receipts fund expenditures should be related to those purposes. Under no

circumstances may the following costs be charged to Overhead Receipt Funds.

• Alcoholic beverages

• Alumni activities

• Bad debts

• Charitable contributions, donations, gifts

• Commencement and convocation expenses

• Disallowed direct costs

• Entertainment costs

• Fines, penalties, damages, and other settlements

• Fund raising and investment management costs

• Investment costs, borrowed capital, etc.

• Legal costs

• Lobbying costs

• Memberships in country clubs, social or dining clubs and other organizations where

purpose is lobbying

• Organizational costs of establishing a new organization e.g., broker’s fees, incorporation

fees, attorneys, etc.

• Personal use goods or services

• Selling and marketing costs of products or services

• Student activities costs (publications, clubs, athletics, etc.)

• Travel or subsistence or living allowances for Board of Trustees or Board of Governors.

The Office of Research Administration website has a link to Policy, Guidance, and SOPs

with

additional information in the Section 510 Allowable Costs - Cost Principles document. (Note:

9

Security access is required.)

Auxiliary and Institutional Trust Funds

Auxiliary and similar operations include, but are not limited to, the Student Stores, Student Center,

University Dining, Parking and Transportation, Campus Living, Student Health Services,

University Printing and Graphics, and Central Stores. Expenditures from auxiliary funds and other

institutional trust funds must follow the same guidelines used for state funds except when used for

certain program related activities as noted in the fund authority for the respective fund. For

example, student activity funds can pay for student programs including inflatables, bands, and

giveaways. Expenditures must align with the approved fund authority form. No extra benefits,

compensation, food, or any other item which could not be paid from state funds may be provided

to University employees except as noted in sections below. The purchase of alcoholic beverages

from auxiliary funds is prohibited.

Receipts from Vending Facilities Trust Funds

Per North Carolina general statutes [N.C.G.S. 116-2. and N.C.G.S. 111-42(d)], the term “vending

facilities” includes both of the following descriptions:

a. any mechanical or electronic devise dispensing items or something of value or

entertainment or services for a fee, regardless of the method of activation, and regardless

of the means of payment, whether by coin, currency, tokens, or other means; and

b. a snack bar, cafeteria, restaurant, café, concession stand, vending stand, cart services, or

other facilities at which food, drinks, novelties, newspapers, periodicals, confections,

souvenirs, tobacco products or related items are regularly sold.

UNC Board of Governors Policy 600.5.1

restricts the use of vending receipts. The following uses

of net proceeds from the operations of vending facilities are authorized:

a. Scholarships and other direct student financial aid programs;

b. Debt service on self-liquidating facilities;

c. Any of the following student activities if authorized by the Chancellor:

• Social and recreational activities for students residing in self-supporting Housing &

Residence Life facilities. However, expenditures for these purposes shall not exceed

the amount of total net proceeds derived from vending facilities located in such

facilities;

• Special orientation programs for targeted groups of students (e.g., peer mentor

programs);

• Operating expenses of scholarships and student awards and honors programs; and

• Supplementary student center operating support. However, expenditures for this

purpose shall not exceed the total net proceeds derived from vending facilities

located in such student center facilities.

10

d. Specified use of net proceeds as a condition of certain gifts, grants, or bequests. For

example, a condition of a gift of a vending facility to the University might be that

proceeds are to support some specific segment of the University.

e. Retention to provide for working capital, replacement of facilities and equipment, and other

purposes to support the continuing, orderly operation of the particular self-supporting

service operation.

f. Transfers to other self-supporting student service operations and authorized capital

improvement projects, upon the written recommendation of the University’s Chancellor

and subject to the written, advance approval of the UNC President. [N.C.G.S. 116-36.4]

Grants and Contracts Trust Funds

Grants and contracts must follow all state appropriated funds guidelines, sponsor specific terms,

and conditions noted in the awards documents unless excepted as noted below.

Exceptions to the state funds guidelines must be discussed with/approved by the Vice Chancellor

for Research, Economic Development, and Engagement or the Office of Research Administration

(ORA). An example of an exception would include allowances for food costs for seminars or

workshops associated with the objectives of the award.

Grants and contracts may also be subject to Cost Accounting Standards (CAS) or other

requirements set forth in Title 2 CFR 200 Uniform Administrative Requirements, Cost Principles,

and Audit Requirements for Federal Awards, commonly referred to as Uniform Guidance (UG)

,

or other federal regulations or specific sponsor guidelines. Cost Accounting Standards and UG

are applicable to Federal and Federal flow through awards. In general, ECU adheres to the UG

cost standards on all sponsored programs, regardless of sponsor, unless the sponsor specifically

states costs allowability/restrictions. In these instances, ECU costing guidance applies, meaning

that if the sponsor allows a certain cost, but ECU does not, the ECU policy applies. All Cost

Accounting Standards, UG, and any other sponsor exceptions must be approved by ORA. The

Cost Exception Form is used to seek and approve exceptions to general costing standards.

Sometimes University requirements may be more restrictive than sponsor requirements or sponsor

requirements may be more restrictive than University requirements. In most cases, the most

restrictive policy will apply to a financial transaction. Any exceptions must be approved by ORA.

The Principal Investigator (PI) has the responsibility to monitor the budget, ensure that proper

documentation procedures are followed and that only authorized expenditures are charged to a

sponsored project. The PI is responsible for ensuring that sponsored projects’ funds are reviewed

monthly and any errors found are corrected on a timely basis. While processing of transactional

documents and forms may be delegated within the unit that does not relieve the PI of fiscal

responsibility and accountability for his/her sponsored project funds.

For additional information on sponsored projects spending guidelines, see the ORA website for

the link to Policy, Guidance, and SOPs with additional information in the Section 510 Allowable

Costs - Cost Principles document. (Note: Security access is required.)

11

Residual Funds Related to Grants and Contracts

When the University is authorized by the sponsor to retain unobligated fund balances, expenditures

of remaining balances must be related to research unless the fund balances are from grants and

contracts that are not research related. Examples include public service or educational grants and

contracts. In those cases, the residual fund expenditures should be related to those purposes.

Gift and Endowment Income Trust Funds

Expenditures from gift and endowment income funds must be made prudently with the intent of

the donor in mind and follow the restrictions set by the donor as evidenced in the fund authority.

The primary purpose of an expenditure must be for the benefit of the University and, therefore,

not for the direct benefit of an employee.

Endowment Principal Funds

Endowment principal funds are funds provided to the University, normally in the form of a trust

or gift, for investment to generate income. The income may be unrestricted or restricted for a

particular purpose.

The request for an endowment fund should include the following:

• Original or copy of the gift agreement, bequest or other gift document;

• Description of the source of funds;

• Purpose of the fund, how the income earned is to be used - in support of what activity or

function;

• Any restrictions on the types of allowable expenditures;

• Name of person authorized to spend endowment income;

• Name of fund.

Expenditures are not allowable against these endowment principal funds. All endowment related

expenditures must be made from endowment spendable funds.

Patent Royalty Trust Funds

Patent royalty funds are royalties derived from licensing of a patent. These funds must be used for

support of research.

ECU Physicians Trust Funds

These funds include fees and other payments for services rendered by professionals under the

University’s approved practice plan. These funds may be utilized to maintain and/or improve the

areas of teaching, research, patient care, public service, and support administration of the practice

plan. Purchased items may fall outside the state funds guidelines for incentive bonuses, food and

beverages for recruitment, Grand Rounds or student and resident events.

12

ECU School of Dental Medicine (SoDM) Trust Funds

These funds include fees and other payments for services rendered by faculty and clinical staff.

These funds may be utilized to maintain and/or improve the areas of teaching, research, patient

care, public service and support administration of the School of Dental Medicine. They also may

be used to purchase items falling outside the state funds guidelines for incentive bonuses, food and

beverages for recruitment, or student and resident events. Also included in the SoDM Trust Funds

are selected student fees which are used for the purposes approved in the University Tuition and

Fee approval process.

Agency Trust Funds

This category includes funds held by the University as fiscal agent for student, faculty, and staff

organizations where it has been deemed in the best interests of the University to provide an

accounting service. These funds do not belong to the University and the University does not

determine what they can be spent for except as follows:

a. The University requires a formal approval process to ensure, to the extent possible, that

funds in these projects are not misused.

b. The funds should not be spent for any purpose which would be detrimental to the image

of the University.

Adequate documentation is required to ensure that an authorized person is initiating an expenditure

request.

Foundation Funds

The University affiliated foundations are legally separate organizations and are not subject to the

University and State spending policies specified in this document. However, all expenditures from

foundation funds must follow restrictions set by the donor and should be supported by appropriate

documentation and approvals. See the ECU Foundation Website

under “Governance Documents”

for the ECU Foundation, Inc. Expenditure Policy. See the ECU Medical & Health Sciences

Foundation Website under “Governance Documents” for the ECU Medical & Health Sciences

Foundation, Inc. Expenditure Policy. For information about the ECU Educational Foundation

(AKA “Pirate Club”) expenditure policy, contact the Athletics Business Office at

athleticsbusiness@ecu.edu.

Discretionary Trust Funds

Discretionary funds are not budgeted for a specific purpose and can be used to meet a broad range

of University needs. The flexibility that is associated with discretionary funds is vitally important to

the University. At the same time expenditures of discretionary funds must be consistent with a

number of general guidelines as set out below.

Each expenditure of discretionary funds must be for a valid University purpose. These expenditures

(whether for meals, travel, lodging, entertainment, official functions, gifts and awards, or

memberships) must follow all University policies that apply to that type of expenditure and must be

accompanied by appropriate documentation including receipt(s), purpose, date, location, and names

of persons involved.

13

The very flexibility associated with discretionary funds means that determining the propriety of

some expenditures will require judgment. In these cases, the prudent person test applies. The

individual making the decision about the expenditure must be comfortable with the prospect that

the specific expenditure would come under the scrutiny of individuals outside the University.

Expenditures that confer a personal benefit upon the individual authorizing the expenditures are

not allowable. Expenditures for items such as employee achievement or recognition awards and

retirement gifts that are authorized by one individual to be received by another are allowable as

discussed below.

Employee Achievement or Recognition Awards and Retirement Gifts

Awards/Gifts to Employees: Achievement and recognition awards may be purchased for

employees. IRS regulations state that employees may accept gifts not to exceed $25 in value. The

award may not be cash or cash equivalent (a gift certificate, gift card, or prepaid tickets). Any awards

in excess of $25 must be reported to the Payroll Office to be included in the individual's Form

W-2.

Retirement Awards/Gifts: The IRS will allow employee achievement awards that recognize length

of service. The award cannot be cash, or cash equivalent (a gift certificate, gift card, or prepaid

tickets). The value of the gift can be up to $25 for every year of service, not to exceed $400.

IRS guidelines for employee achievement awards that recognize length of service or safety records

state that expenditures:

• Cannot be disguised as wages;

• Must be awarded as part of a meaningful presentation;

• Cannot be cash, cash equivalent (gift certificate, gift card, or prepaid tickets), vacation,

meals, lodging, theatre or sports tickets, or securities.

Non-travel Related Restaurant Charges

There are unique requirements for certain purchases, such as restaurant charges, to be paid from

discretionary funds. While business purpose justification can be provided for working breakfasts,

lunches, and dinners, IRS guidelines allow this type of reimbursement only on an occasional – not

a routine – basis. Restaurant charges may be allowable if documented with an agenda describing

the business purpose of the meeting and a list of attendees. Unless ECU employees are

participating in an internal conference, meals including only ECU employees must be paid for from

personal funds. (Exceptions to this include an occasional holiday or annual event and the case

where an internal candidate has a meal related to the interview/search process.)

In the case of a restaurant that does not provide itemized receipts, the requestor must certify in

writing that no non-food items were purchased regardless of funding source. Grant and/or

contract guidelines and any other fund guidelines all apply.

Contributions and Donations

14

Use of discretionary funds for donations or contributions to non-profit organizations is not

permitted unless a substantial University purpose can be demonstrated and the receipt of the

donation by the organization does not threaten the tax-exempt status of the University or its

foundations. Political contributions are not allowed.

Additional Information

Expediting Fee for H-1B Visa Forms (Form I-907)

Normal processing of an H-1B petition may take between 4-7 months, while paying a premium

processing (expediting) fee will ensure a response within 15 calendar days.

Payments for expediting fees for H-1B Visa Forms may track the salary funding source so long as

the payment is made for a business reason and for the convenience of the University and not for

the employee. Regardless, contracts and grants funds may not be used to pay the fee for any reason.

The expediting fee is considered a business expense and is classified as a recruiting expense and/or

a retention expense. Some examples of appropriate funding sources are as follows:

Salary Source Possible Funding Sources for Expediting Fee

State funds State funds or discretionary funds

Contracts/Grants Discretionary funds

Gift funds Gift funds or discretionary funds

Contact Information for Questions

Questions may be addressed to the appropriate Budget Office as listed in the Funding Source

Contacts located on the Controller’s Office page of the Financial Services website.

Resources

1. East Carolina University Policy Manual

2. North Carolina State Budget Manual

3. UNC System Code and Policy Manual

4. ECU Financial Services Website

5. ECU Materials Management Website

----------------------------------------------------------------------------------------------------

15

Appendix

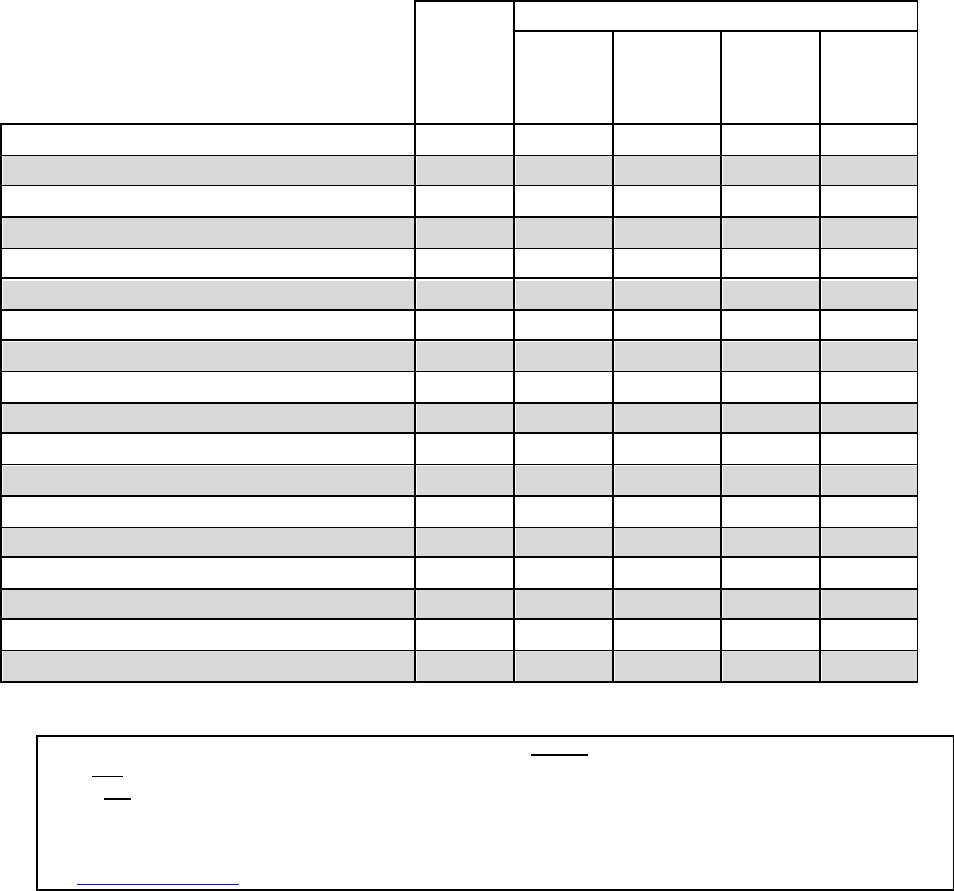

Appendix A: Quick Reference Guide of Spending Rules by Fund Source

State

Funds

Institutional Trust Funds

Contracts Auxiliary & Other Discre-

& Grants Int. Service Inst. Trust tionary

Funds

Funds

Funds

Funds

Moving expenses

Yes

1

No

Yes

1

Yes

1

Yes

1

Travel reimbursements Yes Yes Yes Yes Yes

Membership dues Yes

2

No Yes Yes Yes

Passports & Visas Yes No Yes Yes Yes

Employee awards Yes

3

No Yes Yes Yes

Immigration and Naturalization Service (INS) fees Yes No Yes Yes Yes

Food & Refreshments (non-travel related) No No Yes Yes Yes

Financial aid/scholarships to students

Yes

4

Yes

Yes

Yes

No

Promotional items of nominal value Yes No Yes Yes Yes

Alcoholic beverages & set-ups No No No No Yes

Medications and/or medical supplies for personal use No No No No No

Microwave ovens, refrigerators, coffee pots No No Yes

5

Yes

5

Yes

5

Framed artwork or diplomas No No Yes

5

Yes

5

Yes

5

Party items or decorations

No

No

No

No

Yes

Gifts, flowers/plants, cards No No No No Yes

Personal clothing with University logo No No Yes Yes Yes

Personal clothing No No No No No

Other items for personal use No No No No No

1 Only as allowed by G.S. 138-8 and Section 6.6 and 6.7 of the State Budget Manual.

2 The membership must belong to the “position” and not to the person and/or must have a business purpose such

as a discount for CPE and/or resources available for the member.

3 Only Service Awards.

4 Allowed only in programs approved by the Board of Governors (departments are not authorized to give

scholarships at will).

5 Allowable in common space but not in an individual office.

-

This Quick Reference Guide reflects the rules that generally apply in the majority of situations (80% plus). It is NOT all inclusive.

-

A YES may require: Specific Criteria to be met, adherence to Restrictions, appropriate Documentation, Authorization and Approvals.

-

For NO, authorized exceptions for specific situations may exist.

-

The User of this Quick Reference Guide should always research the Spending Guidelines Document in its entirety, as well as the applicable

policies and procedures, before making a final determination of appropriate spending from the various fund sources.

-

If your research fails to resolve your spending question, please contact the appropriate Budget Office as listed in the

Funding Source Contacts for further discussion and resol ution of your question.