Outbound Planning Into Brazil - U.S. Tax

Considerations - Transnational Tax

Network

November 30, 2017

Jeffrey Rubinger

Bilzin Sumberg LLP

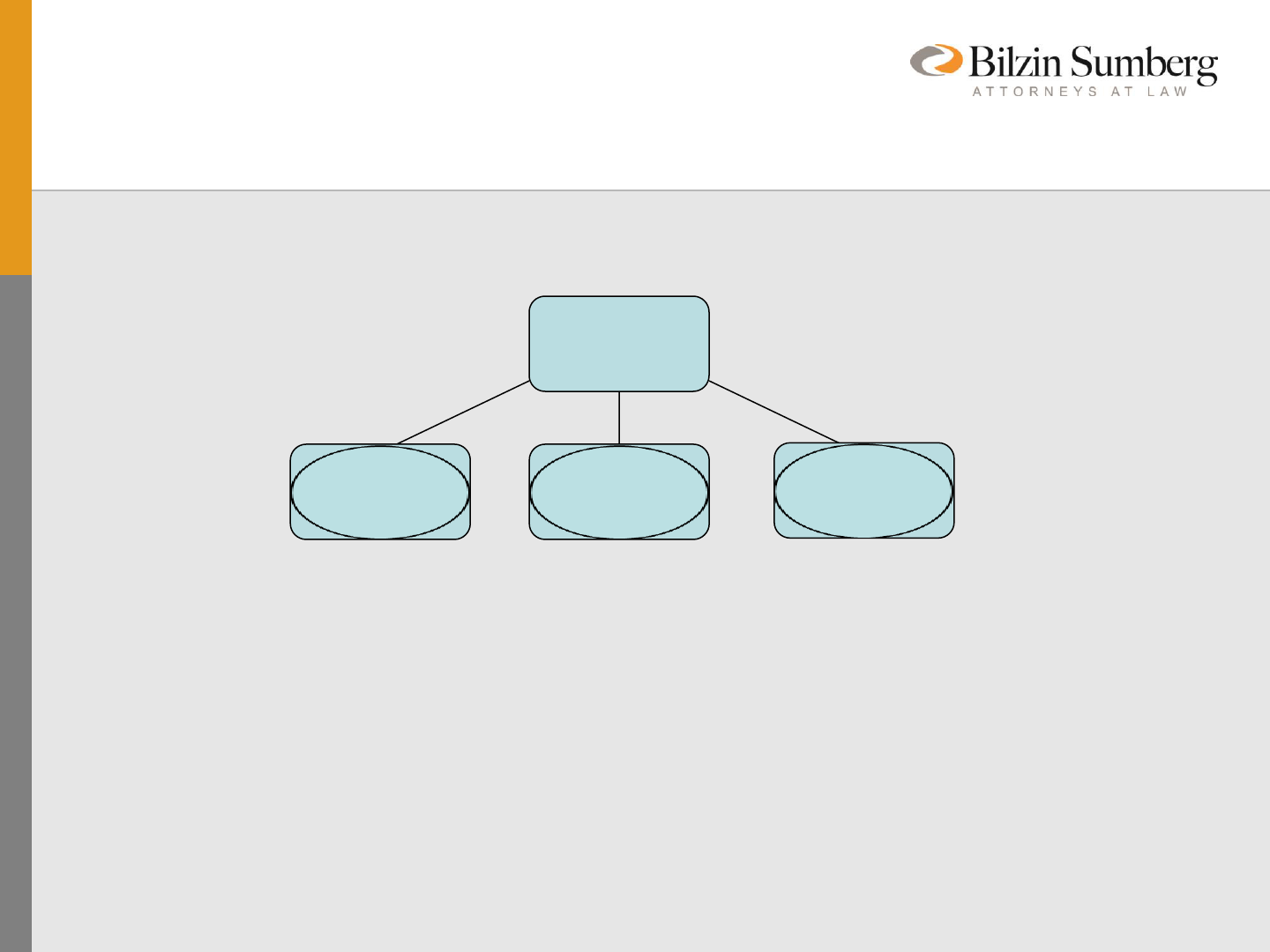

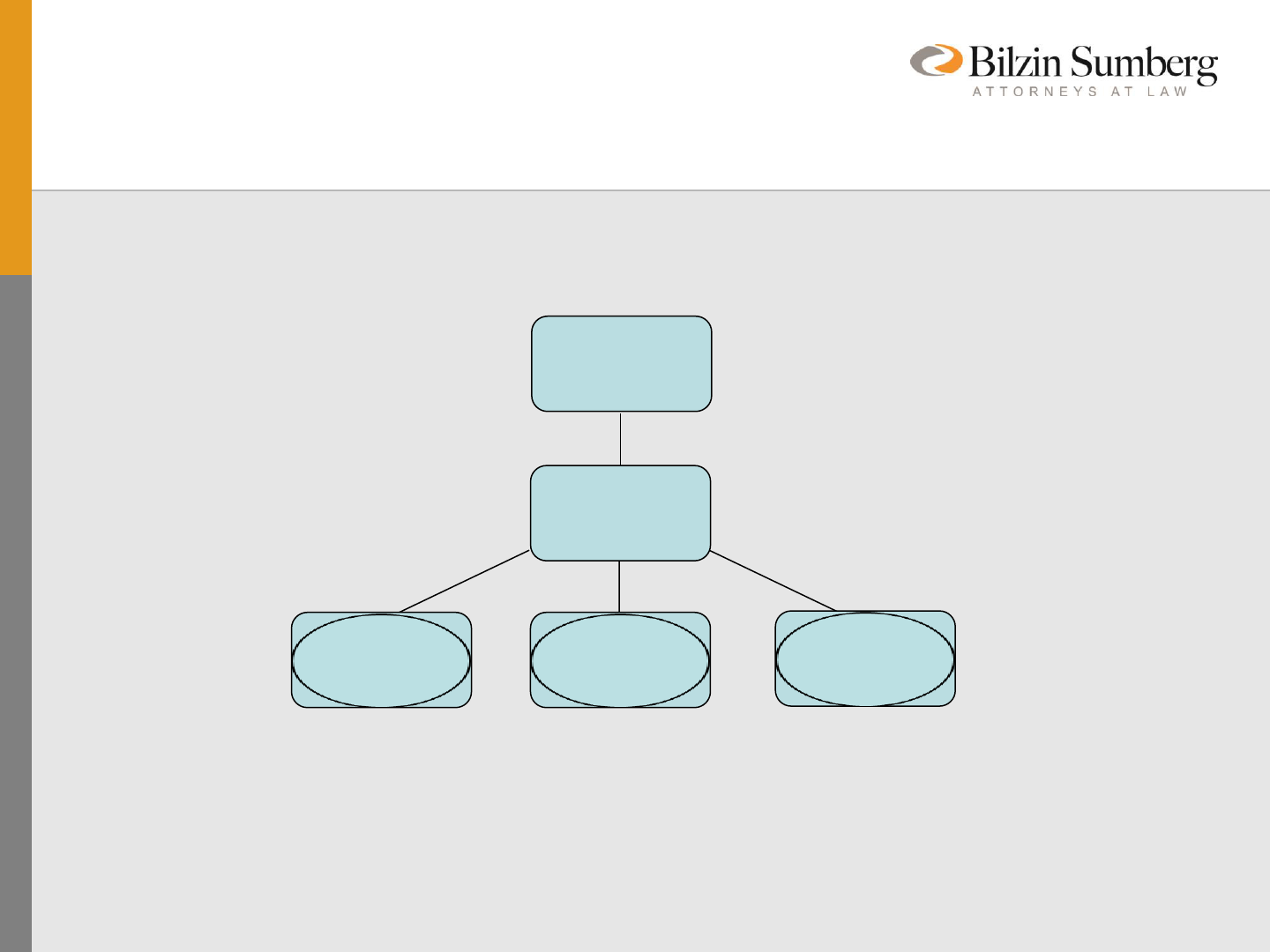

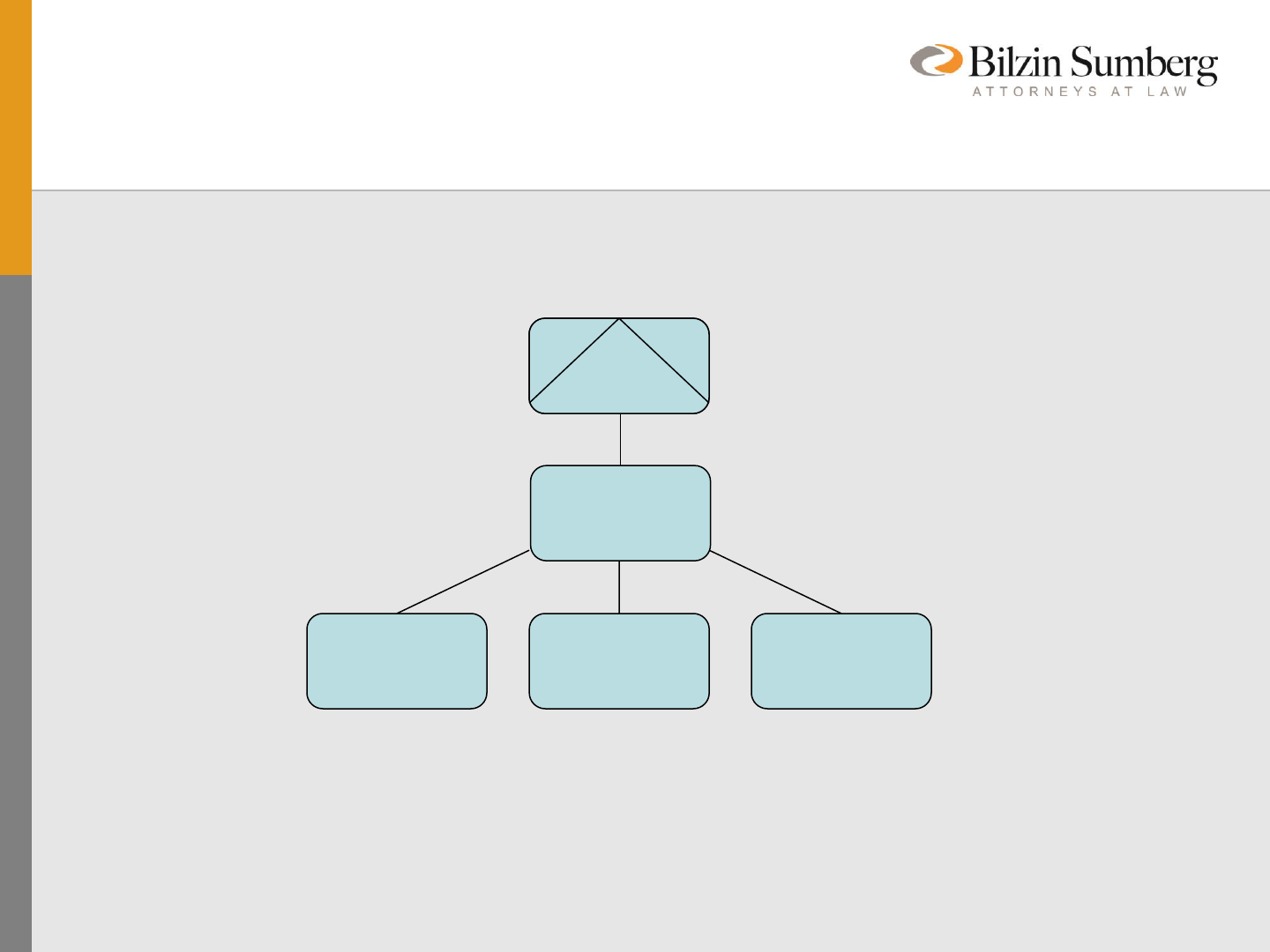

Basic Case - Direct Ownership of

High Tax Latam Subsidiaries

Parent

(US C corp)

100%

Foreign Sub

Colombia

100%

Foreign Sub

Brazil

100%

Foreign Sub

Mexico

Tax Consequences of Structure

• U.S. corporate parent eligible to claim indirect foreign tax credit for corporate

level income paid or incurred in foreign jurisdictions.

• Double tax in the United States (corporate and shareholder level tax).

• Cannot claim indirect foreign taxes for certain foreign taxes such as

Brazilian PIS or COFINS; VAT taxes.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• No treaty based reductions if withholding taxes paid in countries, such as,

Brazil on royalties.

• No ability to defer intergroup payments of interest, dividends, royalties, etc.

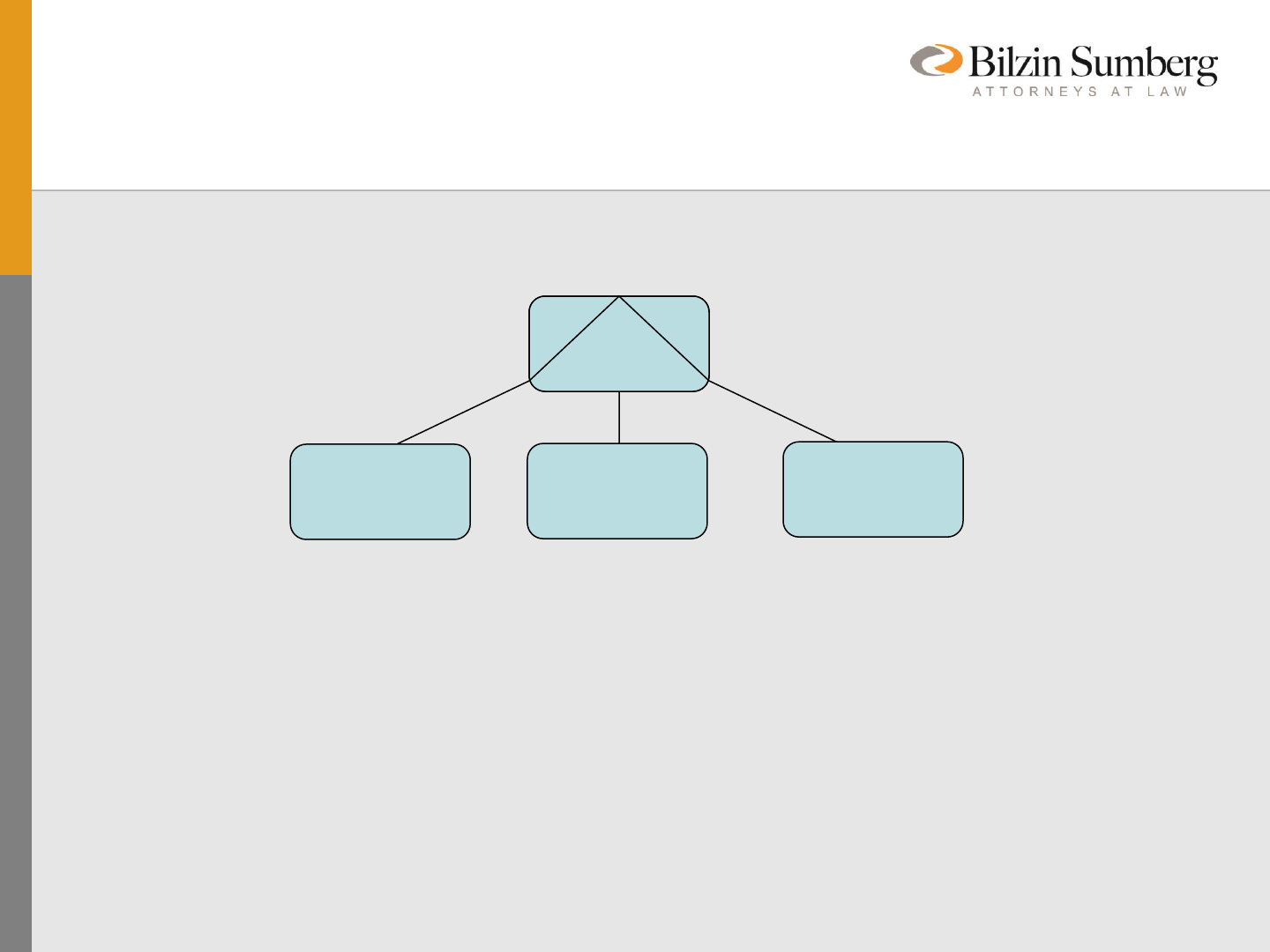

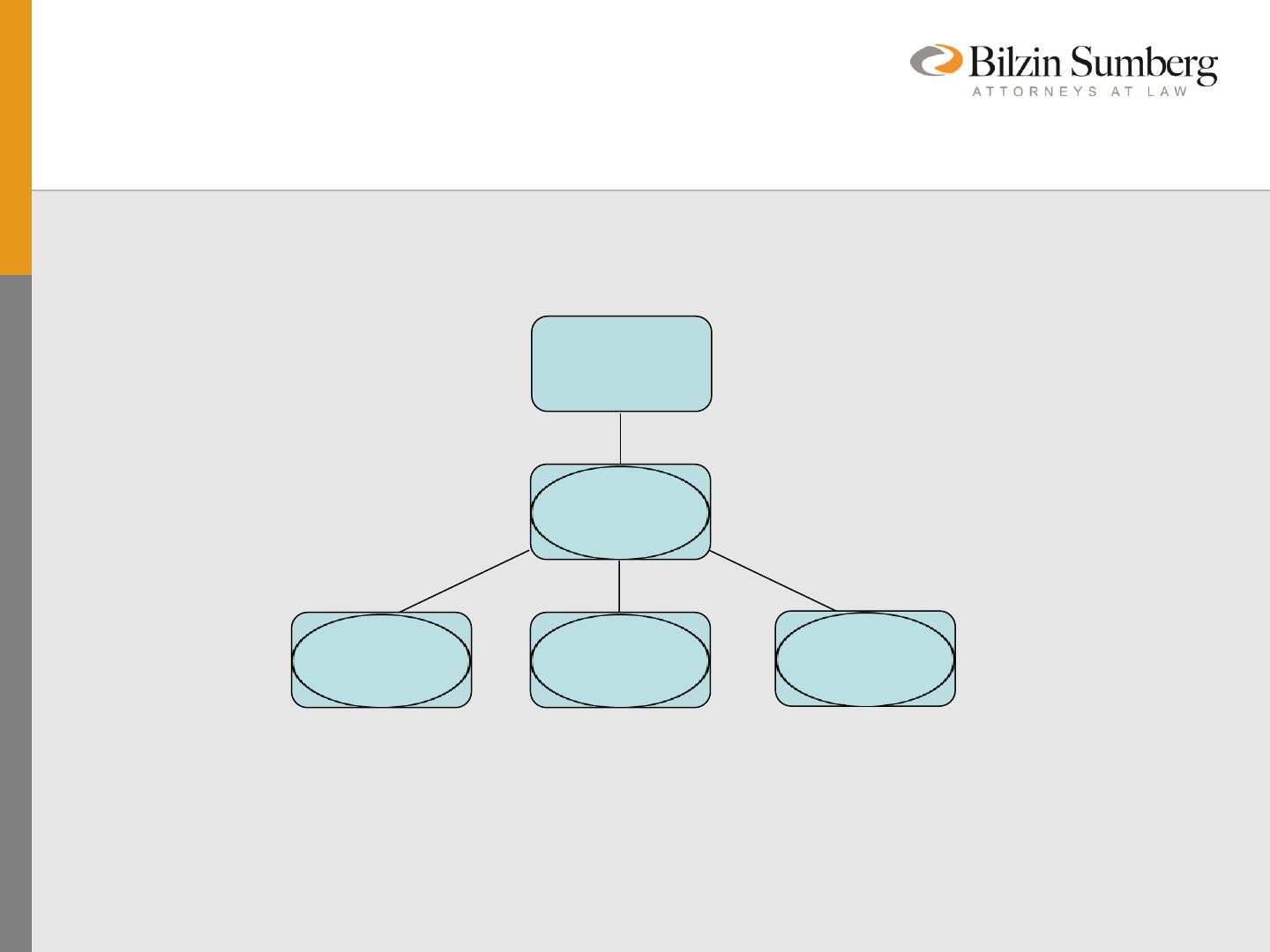

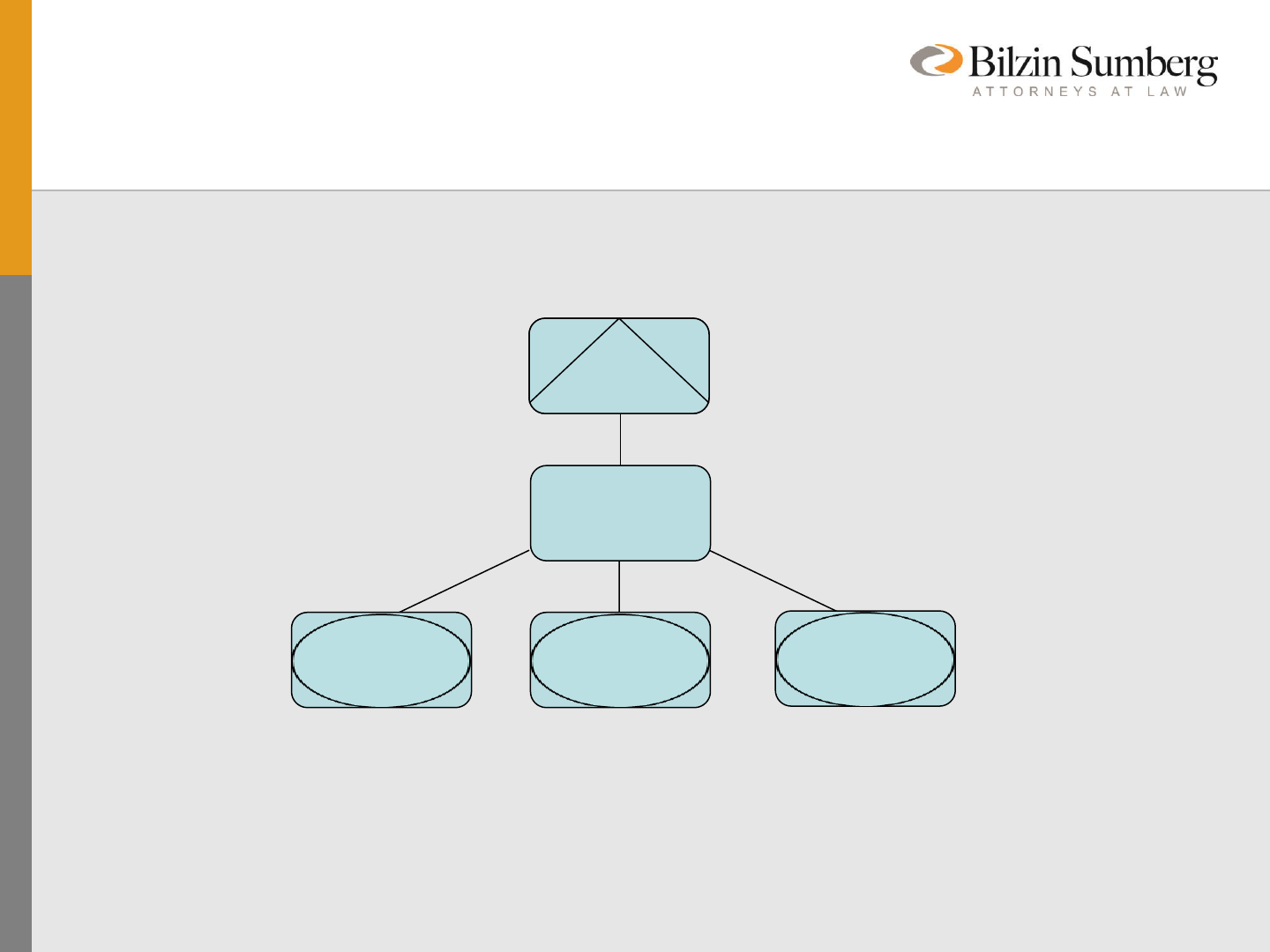

Flow-Through Tax Treatment of

High-Tax Latam Subsidiaries

Parent

(US C corp)

100%

100%

100%

Opco

(Malta)

Foreign

Venezuela

Opco

(Malta)

Foreign

Brazil

Opco

(Malta)

Foreign

Chile

Tax Consequences of Structure

• No ability to defer income

• Can claim direct foreign tax credit for eligible foreign income taxes

paid

• Double tax in the United States (corporate level plus shareholder

dividend)

• Losses flow-through

• But potential loss recapture rules, dual consolidated loss rules,

and overall foreign loss rules.

• No treaty based reductions of withholding for non-treaty subsidiaries.

• No ability to defer intergroup payments

Flow-Through U.S. Parent

Parent

(US C corp)

100%

100%

100%

Foreign

Mexico

Foreign

Brazil

Foreign

Chile

US

Parent

LLC

Tax Consequences of Structure

• U.S. parent cannot claim foreign tax credit for corporate level income paid or

incurred in foreign jurisdictions (can only claim credit for any withholding taxes

incurred).

• But single layer of U.S. income tax.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• No treaty based reductions if withholding taxes paid in countries on dividends.

• U.S. owners eligible to claim qualified dividend treatment on dividends

received from treaty-based subsidiaries, such as Mexico, but not Brazil.

• No ability to defer intergroup payments of interest, dividends, royalties, etc.

Flow-Through U.S. Parent and

High-Tax Latam Subsidiaries

100%

100%

100%

Opco

(Malta)

Foreign

Chile

Opco

(Malta)

Foreign

Mexico

Opco

(Malta)

Foreign

Brazil

US

Parent

LLC

Tax Consequences of Structure

• No ability to defer income

• Can claim direct foreign tax credit for eligible foreign income taxes

paid

• Single layer of U.S. income tax.

• No ability to treat income as qualified dividend income

• Losses flow-through

• But remember potential loss recapture rules, dual consolidated

loss rules, and overall foreign loss rules.

• No treaty based reductions of withholding for non-treaty subsidiaries.

• No ability to defer intergroup payments

Foreign Holding Company

Structure

Parent

(US C corp)

100%

Foreign

Mexico

100%

Foreign

Chile

100%

Foreign

Brazil

Foreign Holdco

Spain

100%

Tax Consequences of Structure

• U.S. corporate parent eligible to claim indirect foreign tax credit for corporate level

income paid or incurred in foreign jurisdictions.

• Cannot claim indirect foreign taxes for certain foreign taxes such as Brazilian

PIS or COFINS.

• Double tax at U.S. corporate level

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• Can claim treaty based reductions with Spanish holding company if withholding

taxes incurred in foreign jurisdictions.

• No qualified dividends for dividends received from Spanish holding company as C

corporations do not qualify for lower rate.

• Can defer intergroup payments of interest, dividends, royalties, etc, so long as

Section 954(c)(6) exists.

• Benefit from bilateral investment protection treaties with Spain (except Brazil)

Foreign Holding Company with

Flow-Through Foreign Subsidiaries

Parent

(US C corp)

100%

100%

100%

Foreign Holdco

Spain

100%

Opco

(Malta)

Foreign

Brazil

Opco

(Malta)

Foreign

Mexico

Opco

(Malta)

Foreign

Colombia

Tax Consequences of Structure

• U.S. corporate parent eligible to claim indirect foreign tax credit for corporate level income

paid or incurred in foreign jurisdictions, even though foreign subsidiaries disregarded

because holding company treated as separate corporation.

• Cannot claim indirect foreign taxes for certain foreign taxes such as Brazilian PIS or

COFINS.

• Double tax at U.S. corporate level

• Income earned in foreign subsidiaries can be deferred from U.S. tax until repatriated.

• Losses do not pass through.

• Can claim treaty based reductions with Spanish holding company if withholding taxes

incurred in foreign jurisdictions.

• No qualified dividends for dividends received from Spanish holding company as C

corporations do not qualify for lower rate.

• Can defer intergroup payments of interest, dividends, royalties, etc, because foreign

subsidiaries are disregarded for subpart F income purposes

• Benefit from bilateral investment protection treaties with Spain (except for Brazil)

Flow-Through Foreign Holding

Company and Foreign Subsidiaries

Parent

(US C corp)

100%

100%

100%

100%

Opco

(Malta)

Foreign

Chile

Opco

(Malta)

Foreign

Brazil

Opco

(Malta)

Foreign

Venezuela

Opco

(Malta)

Foreign

Holdco

Spain

Tax Consequences of Structure

• No ability to defer income

• Can claim direct foreign tax credit for eligible foreign income taxes

paid

• Double tax at U.S. corporate level

• Losses flow-through

• But remember potential loss recapture rules, dual consolidated

loss rules, and overall foreign loss rules.

• Can claim treaty based reductions of withholding taxes incurred in

foreign jurisdictions under treaty with Spain.

• No ability to defer intergroup payments

• Benefit from bilateral investment protection treaties with Spain

(except Brazil)

Flow-Through U.S. Parent with

Foreign Holding Company

100%

Foreign

Brazil

100%

Foreign

Chile

100%

Foreign

Mexico

Foreign Holdco

Spain

100%

Parent

(US C corp)

US

Parent

LLC

Tax Consequences of Structure

• U.S. parent cannot claim foreign tax credit for corporate level income paid or

incurred (as well as foreign withholding taxes paid) in foreign jurisdictions

• But single layer of U.S. income tax.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• Can claim treaty based reductions if withholding taxes paid incurred in foreign

jurisdictions under treaty with Spain.

• U.S. owners eligible to claim qualified dividend treatment on dividends

received from Spanish holding company.

• Can defer intergroup payments of interest, dividends, royalties, etc, so long as

Section 954(c)(6) extended.

• Benefit from bilateral investment protection treaties with Spain (except Brazil)

Flow-Through U.S. Parent and Foreign

Subsidiaries with Foreign Holding

Company

100%

100%

100%

Foreign Holdco

Spain

100%

Parent

(US C corp)

US

Parent

LLC

Opco

(Malta)

Foreign

Chile

Opco

(Malta)

Foreign

Mexico

Opco

(Malta)

Foreign

Brazil

Tax Consequences of Structure

• U.S. parent cannot claim foreign tax credit for corporate level income paid or

incurred (as well as foreign withholding taxes paid) in foreign jurisdictions

• But single layer of U.S. income tax.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• Can claim treaty based reductions with Spanish holding company if

withholding taxes incurred in foreign jurisdictions.

• U.S. owners eligible to claim qualified dividend treatment on dividends

received from Spanish holding company.

• Can defer intergroup payments of interest, dividends, royalties, etc, because

foreign subsidiaries are disregarded for subpart F income purposes

• Benefit from bilateral investment protection treaties with Spain (except for

Brazil)

Complete Flow-Through Holding

Company Structure

100%

100%

100%

100%

Parent

(US C corp)

US

Parent

LLC

Opco

(Malta)

Foreign

Chile

Opco

(Malta)

Foreign

Brazil

Opco

(Malta)

Foreign

Mexico

Opco

(Malta)

Foreign

Holdco

Spain

Tax Consequences of Structure

• No ability to defer income

• Can claim direct foreign tax credit for eligible foreign income taxes

paid (including withholding taxes)

• Single layer of U.S. income tax.

• No ability to treat income as qualified dividend income

• Losses flow-through

• But remember potential loss recapture rules, dual consolidated

loss rules, and overall foreign loss rules.

• Can claim treaty based reductions with Spanish holding company if

withholding taxes incurred in foreign jurisdictions

• No ability to defer intergroup payments

• Benefit from bilateral investment protection treaties with Spain

(except Brazil)

Flow-Through U.S. Parent and

Foreign Holding Company

100%

Foreign

Mexico

100%

Foreign

Chile

100%

Foreign

Brazil

100%

Parent

(US C corp)

US

Parent

LLC

Opco

(Malta)

Foreign

Holdco

Spain

Tax Consequences of Structure

• U.S. parent cannot claim foreign tax credit for corporate level income paid or

incurred in foreign jurisdictions (can only claim credit for any withholding taxes

incurred).

• But single layer of U.S. income tax.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until

repatriated.

• Losses do not pass through.

• Can claim treaty based reductions with Spanish holding company if

withholding taxes incurred in foreign jurisdictions

• No ability to defer intergroup payments

• U.S. owners eligible to claim qualified dividend treatment on dividends paid

from treaty-based subsidiaries, such as Mexico, but not Brazil.

• No ability to defer intergroup payments of interest, dividends, royalties, etc.

• Potentially can convert subpart F income into qualified dividend income with

check-the-box planning

• Benefit from bilateral investment protection treaties with Spain (except for

Brazil)

Use of Foreign Holding Company

with Branch Exemption

Holdco

(Spanish ETVE)

100%

Branch

(e.g., US

LLC/Uruguay/

Irish)

Parent

(US C corp)

US

Parent

LLC

Loans/Licenses/

Services to Subs

Interest/royalties/

service payments

deductible; eligible

for reduced

withholding tax rates

under treaty with

Spain; and exempt

from Tax in Spain

under branch

exemption

Opco

(Malta)

Foreign

Colombia

Opco

(Malta)

Foreign

Brazil

Opco

(Malta)

Foreign

Argentina

Tax Consequences of Structure

• U.S. parent cannot claim foreign tax credit for corporate level income paid or incurred (as

well as foreign withholding taxes paid) in foreign jurisdictions

• But single layer of U.S. income tax.

• Income earned in foreign subsidiaries can be deferred from U.S. tax until repatriated.

• Losses do not pass through.

• Can claim treaty based reductions with Spanish holding company if withholding taxes

incurred in foreign jurisdictions, even though payments made to low-tax branch of

Spanish holding company.

• May not work with Brazil according to Brazil-Spain income tax treaty.

• Can claim deductions for intergroup payments incurred at foreign subsidiary level, even

though receipt of payments will be exempt (or subject to low taxes) at branch level and

Spanish holding company level under branch exemption.

• U.S. owners eligible to claim qualified dividend treatment on dividends received from

Spanish holding company.

• Can defer intergroup payments of interest, dividends, royalties, etc, because foreign

subsidiaries are disregarded for subpart F income purposes

• Benefit from bilateral investment protection treaties with Spain (except for Brazil).