Walgreens Voluntary

Disability Plan for Hourly

Team Members

Summary Plan Description

Prepared by the Walgreen Human

Resources Department for eligible

hourly-paid team members of

Walgreens

TABLE OF CONTENTS

Voluntary Disability Plan Checklist ....................................................................................................................................... 1

Voluntary Disability Plan Resource Guide ............................................................................................................................. 2

Introduction ......................................................................................................................................................................... 3

Eligibility .............................................................................................................................................................................. 3

Enrollment ........................................................................................................................................................................... 3

Plan Options ........................................................................................................................................................................ 4

Plan Costs and Benefits ........................................................................................................................................................ 5

Responsible Parties .............................................................................................................................................................. 5

Plan Features ....................................................................................................................................................................... 5

Deductible Sources of Income .............................................................................................................................................. 6

Definition & Plan Details ...............................................................................................................................................................7

Benefit Maximums ........................................................................................................................................................................8

Benefit Minimums ............................................................................................................................................................... 8

Restrictions Applying to Benefits ......................................................................................................................................... 8

Right to Recover Overpayments ........................................................................................................................................... 8

Recurrent Disabilities ........................................................................................................................................................... 9

Leaves of Absence................................................................................................................................................................ 9

Partial Disability Benefits .................................................................................................................................................... 9

Indexed Monthly Earnings .................................................................................................................................................... 9

Special Return to Work Benefit ...........................................................................................................................................10

Normal Partial Disability Benefits ....................................................................................................................................... 11

Other Benefits .....................................................................................................................................................................11

Filing a Claim .......................................................................................................................................................................12

Procedures for Reviewing Claims .........................................................................................................................................13

Claim Denials ......................................................................................................................................................................13

Appealing a Denied Claim ....................................................................................................................................................14

Prudential’s Review of Appeal.............................................................................................................................................14

Potential Review of Appeal by the Plan Administrator .........................................................................................................14

Notice of Decision on Appeal ...............................................................................................................................................14

General Claims/Appeals Information ...................................................................................................................................15

Plan Limitations ..................................................................................................................................................................15

Pre-existing Conditions ........................................................................................................................................................15

Psychiatric Conditions, Alcohol, Drug, Substance Abuse or Dependency ..............................................................................16

Exclusions and Discontinuation of Benefits ................................................................................................................................ 16

When Coverage Ends...........................................................................................................................................................17

ERISA Rights ........................................................................................................................................................................17

Plan Amendment & Termination Rights ...............................................................................................................................18

Administrative Facts .......................................................................................................................................................... 19

Walgreen Co. (“Walgreens” or the “Company”) is pleased to provide its team members with a comprehensive package of

health and welfare benefit options as described in the Walgreen Health and Welfare Plan (the “Plan”). To assist you in

better understanding the disability benefits available to Walgreens team members covered by the Voluntary Disability

Plan for Hourly Team Members, as in effect as of January 1, 2018 we have prepared this Summary Plan Description

(“SPD”) booklet. The complete Plan includes contracts and agreements with insurance carriers (“Insurer[s]”) and third-

party administrators who provide and administer benefits, this SPD, including any Summary of Material Modifications,

and summary plan descriptions covering other benefits that are not covered by this SPD. You should read the

information provided in this booklet so that you will have a full understanding of the benefits provided and the other

relevant terms and conditions of the Plan. Throughout this document the term “Company” means Walgreen Co. and its

subsidiaries and affiliates whose team members are eligible to participate in the Plan, unless the context is limited to a

particular subsidiary or business unit. See “Administrative Facts” at the end of this booklet for the name of the legal entity

of the Company that is the official plan sponsor of the Plan, and therefore the Company for purposes of formal approvals

and governmental filings.

The benefits of this Plan are governed by the terms of the insurance policy providing the benefits in effect at the time of a

claim. This Summary Plan Description is meant to provide details on the important features of the Plan. Copies of these

Plan documents can be obtained by contacting the Plan Administrator listed at the end of this booklet. In the event of any

discrepancy between this booklet and the provisions of the insurance policies, the provisions of the insurance policies

will govern.

Please understand that the Company reserves the right to amend, modify or terminate this Plan, including any benefits

provided under this Plan or the amount of any required contributions, if any, at any time, and for any reason. You will be

notified of any changes to the Plan within a reasonable amount of time, but not always prior to the time the change goes

into effect. To determine the proper benefits at any given time, it is necessary to consult the Summary Plan Description

booklet, the Plan, and insurance policies that are in effect at the relevant time.

In the event that any term or provision in the SPD is in conflict with any of the terms or provisions of the Plan, the terms

or provisions in the Plan document will govern. The Plan or the Voluntary Disability Plan as used hereinafter refers to

this SPD.

Important Notice

This booklet contains information in English of your Plan rights and benefits under this Plan. If you have difficulty

understanding any part of this booklet, contact the Benefits Support Center at 855-564-6153.

Noticia Importante

Este boletín contiene informacion, escrito en inglés, de sus derechos y beneficios bajo este Plan. Si es difícil comprender

cualquiera parte de este boletín, por favor de ponerse en contacto Benefits Support Center 855-564-6153.

Kung kailangan ninyo ang tulong sa Tagalog tumawag sa Walgreens Human Resources Department at 800-825-5467

如果需要中文的帮助,请拨打这个号码 Walgreens Human Resources Department at 800-825-5467

Dinek'ehgo shika at'ohwol ninisingo, kwiijigo holne' Walgreens Human Resources Department at 800-825-5467

1

Voluntary Disability Plan Checklist

If you need to be off work for an extended period of time due to a disabling condition (illness, injury or pregnancy), you must file a

claim to be considered for a disability benefit under this Plan. Use this checklist as a guide to make sure you take all the necessary

steps for filing a disability claim.

In most cases, you will file a claim for disability benefits under the Walgreens Company-Paid Disability Plan, after a disabling

condition requires you to be off work for more than seven calendar days. If you file a claim for Company-Paid disability benefits, are

approved for benefits, and are nearing the end of the elimination period for benefits under this Plan - the Company-Paid Disability

Plan Administrator, Sedgwick CMS, will forward your disability claim under this Voluntary Disability Plan to the insurance Carrier,

Prudential, for processing.

You may also file a claim directly with Prudential under this Voluntary Disability Plan:

Call Prudential, the voluntary disability insurance carrier, directly at 800-842-1718, between 8 am and 11 pm Eastern Time,

Monday-Friday. You may speak to a trained disability specialist or follow the prompts to record your disability information.

Or, you may log in to www.prudential.com/mybenefits. Click on “Report Time out of Work” and follow the instructions to

complete the Interactive Claimant Submission form.

Please have the following information ready when filing your claim:

o Company name and Control number: Walgreens #42097;

o Your name, address, telephone number, Social Security number, Employee ID number, job title and date of birth;

o Your treating physician's name, telephone number and fax number;

o Your last day worked, first day of absence due to the condition and date you expect to return to work; and

o If your absence is work-related.

Once you are off work, and you are near the end of the elimination period for benefits under this Voluntary Disability Plan,

Sedgwick will forward your claim information to Prudential Insurance. Prudential will process your claim, and contact you to

verify your benefits.

To process your claim for disability, Prudential needs statements from you, your doctor and Walgreens. When you speak to a

Prudential specialist, they will obtain your information. Prudential will request information from your doctor and from

Walgreens, and a decision will be made after review of all the information.

To get information on your claim status or payments, call 800-842-1718 or log in to www.prudential.com/mybenefits.

You should notify Prudential if you have any updated information on your return to work date, your delivery date or if you’d

like to request any forms.

IMPORTANT INFORMATION FOR RESIDENTS OF CERTAIN STATES: There are state-specific requirements that may change the provisions

under the Coverage(s) described in the Group Insurance Certificate provided by Prudential. If you live in a state that has such

requirements, those requirements will apply to your Coverage(s) and are made a part of your Group Insurance Certificate. Prudential has

a website that describes these state-specific requirements. You may access the website at www.prudential.com/etonline. When you

access the website, you will be asked to enter your state of residence and your Access Code. Your Access Code is 42097.

2

Voluntary Disability Plan for Hourly Team Members

Resource Guide

If you have a question about:

Resource

Contact Info

Filing a disability claim under the company-paid plan

and whether it has been forwarded to the Prudential

Voluntary Disability Plan

Sedgwick CMS Disability Center

877-872-0911

TTY: 901-531-4554

Questions about benefit payments after your

v

oluntary disability claim has been approved

Prudential

800-842-1718

Questions on eligibility for coverage under the

Voluntary

Disability Plan

Walgreens Human Resources

Leave Department

800-825-5467

Survivor benefits

Prudential

800-842-1718

Filing an appeal (following a disability claim denial)

Prudential

800-842-1718

Unpaid leave of absence

Walgreens Human Resources

Leave Department

800-825-5467

Medical benefits and/or COBRA

Benefits Support Center

855-564-6153

3

Introduction

Walgreens provides the Voluntary Disability Plan for

Hourly team Members (the “Plan”) to help protect your

financial security if you are unable to earn a full income

due to a covered injury, pregnancy or sickness. This Plan

provides additional income after company-paid disability

benefits under the Walgreens Company-Paid Disability

Plan are exhausted. Coverage is only available to eligible

Walgreen Co. team members – there is no coverage

option for dependents.

This Voluntary Disability Plan has two available options for

providing financial benefits to a covered team member, in

the event the individual is unable to work due to a

disability. These options both provide a benefit of 60% of

covered pay, as long as you qualify – for up to a two year

or five year period. Effective January 1, 2019, these

options both provide a benefit of 50% of covered pay, as

long as you qualify – for up to a two year or five year

period. Eligible team members may enroll in either the

two year or five year option, and pay for the coverage

through after-tax paycheck deductions.

The Plan is meant to provide a disability benefit to

covered team members, once the Company-Paid Disability

Plan benefit ends. The Plan is coordinated with the

Company-Paid Disability Plan, but these are separate plans

with different rules governing qualification for disability

benefits.

There is a 13-week elimination period before disability

benefits begin under this Plan, but that elimination period

may be reduced, so that benefits under this Voluntary

Disability Plan begin as soon as benefits under the

Company-paid plan end.

The Plan is an insured disability benefits program offered

by the Prudential Insurance Company of America.

Prudential reviews and approves your disability claims and

pays disability benefits. The Benefits Support Center is

also involved in the administration of the Plan, as is

Sedgwick CMS for purposes of coordinating claims under

this Plan and the Company-Paid Disability Plan.

Eligibility

To be eligible for coverage under the Voluntary

Disability

Plan for Hourly Team Members, you must:

■

Be an active employee, working in the United States,

excluding Puerto Rico locations;

■

Be paid on an hourly-basis (excluding hourly-paid

pharmacists or registered nurses and hourly-paid

team members who have a Benefit Indicator (BI) of

20 (Assistant Store Managers), 510 (Coordination

Pay Band Team Members) or 511 (Analysis Pay Band

Team Members, who are eligible under a different

plan);

■

Work an average of 30 or more hours per week for

the most recent 52 weeks (or since your start date if

less than 52 weeks);

■

Have at least 181 days of continuous service; and

■

Be actively at work or on approved paid time off or a

regularly scheduled day off on your initial date of

coverage or when the illness or injury occurs. If you

do not meet this requirement on your date of initial

eligibility or onset of illness or injury, that coverage

will be deferred until you return for one full day.

You are not eligible for coverage if you are:

■

A team member of Healthcare Clinics (HCC)

whose payroll is not processed from Walgreens

payroll system.

■

A team member who is covered by a collective

bargaining agreement, unless that agreement

specifically provides for your right to coverage by

this Plan.

■

On a personal leave of absence when the illness or

injury occurs.

A temporary or seasonal team member.

Enrollment

When to Enroll

Evidence of Insurability

If you meet the eligibility requirements, you can enroll in,

cancel or change coverage in the Plan at any time.

However, any enrollment or increase in coverage at any

time other than within 62 days of initial eligibility is subject

to passing Evidence of Insurability (EOI, or proof of good

health). If your EOI is approved, your new coverage will be

effective on the first day of the month, after EOI is

approved.

How to Enroll

To enroll in the Voluntary Disability Plan, go to Your

Benefits Support Center website at

www.BenefitsSupportCenter.com to apply online, or call

the Benefits Support Center at 855-564-6153. If you enroll

online, you will be linked to the Prudential enrollment

website to answer health questions that will assist

Prudential in determining your Evidence of Insurability (EOI

or proof of good health). You will be notified by Prudential

if additional documents are required (such as physician

statements), along with how and when those documents

should be submitted.

When Coverage Begins

Your new coverage or increase in coverage will be effective

the first day of the month following the date your

4

application is received, reviewed and approved, as long as

you are working on the date your coverage would begin (if

not, coverage is deferred until you return to work for one

full day).

Verifying Coverage

Once your coverage begins, the Company will start after-

tax payroll deductions. It is your responsibility to make

sure your premium is deducted from your paycheck. Your

coverage is not in effect if there are no premium

deductions taken from your paycheck. If your deductions

do not begin within two pay periods from your effective

date of coverage, or if your deduction amount is incorrect,

contact the Benefits Support Center by calling 855-564-

6153 to verify your coverage effective date. Payment of

premiums does not activate coverage for any period

during which you do not meet the actively working

requirement.

Your Insurance Certificate

You can obtain a copy of the insurance certificate for your

coverage on Your Benefits Support Center website

www.BenefitsSupportCenter.com, or by calling the

Benefits Support Center at 855-564-6153 to request a

copy. If there are any discrepancies between the

insurance certificate and this Summary Plan Description,

the terms of the certificate will apply.

Changing Your Coverage

You can change your coverage options, add or cancel

coverage at any time, on Your Benefits Support Center

website www.BenefitsSupportCenter.com, or by calling

the Benefits Support Center at 855-564-6153. Please note

that any new coverage or increase in coverage you elect

more than 62 days after your initial eligibility date is

subject to passing Evidence of Insurability (EOI or proof of

good health). You will be notified by the Benefits Support

Center if additional documents are required (such as

physician statements), along with how and when those

documents should be submitted.

Regaining Eligibility

If you lose eligibility for this coverage but remain actively

employed or on an approved leave of absence, and then

you later

become eligible, you will regain eligibility for this

Disability Plan. If your break in coverage is less than six

months, your coverage in this Plan will automatically be

reinstated, and paycheck deductions for premiums will

resume. If you believe your coverage should be reinstated,

but you do not see premium deductions from your

paycheck, contact the Benefits Support Center at 855-564-

6153. If your break in coverage is six months or longer,

you must reapply for coverage, and be subject to passing

Evidence of Insurability (EOI or proof of good health) to be

covered by this Plan again.

Plan Options

Voluntary Disability Plan Benefits

Dates of Disability Prior to 1/1/2019

Option

Benefit Amount

Length of Benefit

Payments

2-Year

Option

60% of monthly

earnings

Until no longer disabled or

24 months from the date

of first payment under the

Voluntary Disability Plan

5-Year

Option

60% of monthly

earnings

Until no longer disabled or

60 months from the date

of first payment under the

Voluntary Disability Plan

Voluntary Disability Plan Benefits

Dates of Disability After 1/1/2019

Option

Benefit Amount

Length of Benefit

Payments

2-Year

Option

50% of monthly

earnings

Until no longer disabled or

24 months from the date

of first payment under the

Voluntary Disability Plan

5-Year

Option

50% of monthly

earnings

Until no longer disabled or

60 months from the date

of first payment under the

Voluntary Disability Plan

Monthly Earnings

Your monthly earnings is determined by multiplying your

hourly rate times your 52-week average weekly work hours

(or your average since date of hire, if less than 52 weeks)

multiplying by 52, and dividing by 12. For purposes of

determining both your premiums for coverage and your

disability benefit payments, your monthly earnings is

generally measured as of a set date prior to initial

enrollment, and then is reset annually, with potential

exceptions for certain types of mid-year changes, as

determined by Walgreens.

Prudential will determine monthly earnings based on the

set covered pay amount reported by Walgreens prior to

your date of disability. Monthly earnings includes base pay

for all hours worked (including base pay for any overtime

hours worked for hourly team members) but does not

include income received from commissions, bonuses,

overtime premium pay, any other extra compensation or

income received from sources other than Walgreens.

If you become disabled while you are on a covered leave

5

of absence, monthly earnings will be determined as

described above.

Premiums will most likely change each calendar year,

based on changes to your age and salary and any other

relevant factors.

Plan Costs and Benefits

Once enrolled, team members pay for the cost of coverage

through after-tax payroll deductions. Walgreens does not

pay any portion of the cost for this Voluntary Disability

Plan. If you receive disability benefits from Prudential

through this Plan, no premiums are due while you are

receiving disability payments.

The cost of coverage depends on your age, your monthly

earnings (calculated once per year to determine your

premium and disability benefit amount), and the plan you

choose (2-year or 5-year option). If you continue coverage

from year to year, your premiums will be recalculated each

year, and your new coverage amount will begin on January

1 (based on your new monthly earnings calculation and

age). Your age is calculated as of January 1

st

of the year you

will move into a higher age bracket (so if you move to a

higher age bracket in June, you will pay the higher rate

beginning in January of that year).

The rates for both options are available on the enrollment

site, www.Benefits SupportCenter.com

These rates are subject to change –so you should check

for any updated information before enrolling in this Plan.

Responsible Parties

All benefits under this Plan are paid directly from

the

insurance carrier, The Prudential Insurance Company of

America, and Prudential is directly

responsible for the final

adjudication of your disability

claim under this Plan.

Sedgwick CMS may forward information on your disability

to Prudential, to aid in determining your benefits.

No deductions will be taken for taxes or benefits from any

disability payments received from this Voluntary Disability

Plan.

Plan Features

Elimination Period

The Voluntary Disability Plan is intended to coordinate

with any benefits available through the Walgreens

Company-Paid Disability Plan. In all cases, there is a

Benefit Elimination Period before the Voluntary

Disability Plan will begin payments. This Benefit

Elimination Period is the earlier of the end of your

Company-Paid Disability Plan benefit, or 13 weeks (91

days), per the following chart.

Benefits under the Voluntary Disability Plan may begin

earlier than 13 weeks after the onset of your disability, if

your benefits under the Company-Paid Disability Plan end

sooner than 13 weeks. For example, if you were disabled

for six weeks earlier in the calendar year, and received

five weeks of disability plan benefits from the Company-

Paid Disability Benefit Plan for Hourly-Paid Team

Members, some of your calendar year benefits would be

used. If you were later disabled from a different condition

in the same calendar year, your benefit under the

company-paid plan would only last six weeks, so you would

have a shorter Benefit Elimination period before your

Voluntary Disability Plan benefits would begin.

Dates of Disability Prior to 1/1/2019

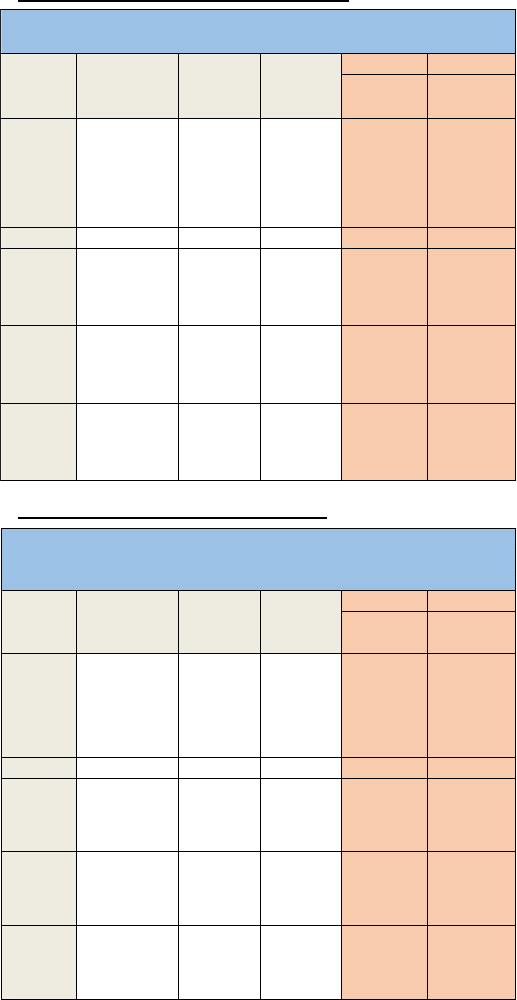

Dates of Disability After 1/1/2019

VOLUNTARY VOLUNTARY

2-Yea r Income

Re pl a ce Pl a n

Option Pays

5-Yea r Income

Re pl a ce Pl a n

Option Pays

1 week

waiting

period

7 day waiting

period (Full pay to

supplement from

PTO, sick or

vacation time, if

available)

2 – 7 Full Pay

8 – 13

50% of Pay

(PTO, sick or

vacation, if

available to

supplement)

14 – 117

50% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

50% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

118 – 273

50% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

Hourly Team Members

Disability Pay Coordination

Effective 1/1/2019

Week of

Disa bili ty

Avail a ble PTO from

Wa l gree ns

Wa l gree ns

Ful l -Pa y

Disa bili ty

Be nefit

Wa l gree ns

Ha lf-Pay

Disa bili ty

Be nefit

VOLUNTARY VOLUNTARY

2-Yea r Income

Re place Plan

Option Pays

5-Yea r Income

Re place Plan

Option Pays

1 week

waiting

period

7 day waiting

period (Full pay to

supplement from

PTO, sick or

vacation time, if

available)

2 – 7 Full Pay

8 – 13

50% of Pay

(PTO, sick or

vacation, if

available to

supplement)

14 – 117

60% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

60% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

118 – 273

60% of Covered

Pay (PTO, sick

or vacation, if

available to

supplment)

Hourly Team Members

Disability Pay Coordination

Week of

Disa bil ity

Avail able PTO from

Wa lgreens

Wa lgreens

Ful l-Pay

Disa bil ity

Be nefit

Wa lgreens

Ha l f-Pay

Disa bil ity

Be nefit

6

Taxes

Because you pay for this benefit with after-tax dollars,

any benefit you receive from this Voluntary Disability

Plan, should you become disabled, is income tax-free.

There will be no deductions for taxes or Walgreen

benefit plan premiums taken from any monthly benefit

payments you receive from Prudential. If you receive

benefits from Prudential through this plan, you should

receive a year end W2 for informational purposes only.

Voluntary Disability Coverage

If you are disabled but not yet receiving benefits from this

Voluntary Disability Plan, because you have not yet met

the elimination period for benefits, you must continue to

pay premiums for this Plan to keep your coverage in force.

If, due to a leave of absence or other circumstances, the

amount of your pay from the Company is not sufficient for

the Company to deduct full premiums for your voluntary

coverage under this Plan, you must contact the Benefits

Support Center at 855-564-6153 to make arrangements to

pay directly for your Plan coverage. If you fail to do so,

your coverage will terminate after a period of 60 days of

unpaid or partial-paid coverage.

Deductible Sources of Income

If you receive disability related benefits from other

sources and/or Social Security disability or retirement-

related income,

your benefits under this Plan will be

reduced, or offset,

by the total amount(s) received from

these sources as

their primary benefit. The “Primary

Offset Benefit” amount

is the total amount you, the

covered team member, receive from

other sources.

Your benefits under this Plan will be reduced by the

amount of benefits you are eligible to receive from other

sources, such as (but not limited to):

Social Security disability and/or retirement

benefits,

Workers' Compensation,

state-mandated or Commonwealth-mandated

disability plans,

any other disability plan to which Walgreens or any

other employer

sponsors or contributes,

disability benefits from any employer-

sponsored retirement or pension plan,

wages received under maritime doctrine of

maintenance, wages and cure,

amounts received from a partnership,

proprietorship or any similar draws, and

Unemployment insurance.

For example, suppose your pre-disability monthly

earnings are $3,000 per month and you receive $500 per

month

from Social Security with an additional Social

Security

dependent benefit amount of $500. Your benefit

from

this Voluntary Disability Plan would be calculated as

follows:

Dates of Disability Prior to 1/1/2019

Base salary $3,000/month

Disability benefit (60%) $1,800/month

Social Security benefit - $1,000/month

Benefit after offset $800/month

Dates of Disability After 1/1/2019

Base salary $3,000/month

Disability benefit (50%) $1,500/month

Social Security benefit - $1,000/month

Benefit after offset $500/month

Any benefit you receive from this Voluntary Disability

Plan

is not taxable to you because you paid the premium

for this benefit with after-tax dollars.

You are required to promptly apply for all other income

benefits for which you are potentially eligible and to

promptly appeal any other income claim denial. If you

fail to do so, your benefits under this Voluntary Disability

Plan will be reduced by the estimated amount of the

Primary Offset Benefit you could have received if your

claim had been approved. Your benefits may be withheld

entirely until you do apply for the offset benefit,

including appeals of these claims. If you receive benefits

under this Voluntary Disability Plan, and are later

awarded benefits from one or

more of the sources

listed, you must reimburse the Plan

for any

overpayment the award causes. Plan benefits may also

be delayed while Primary Offset Benefits are pending.

If you receive other income benefits in a lump sum

instead of in monthly payments, you must provide to

Prudential, satisfactory proof of the

breakdown for the

lump sum amount attributable to lost

income, and the

time period for which the lump sum is

applicable. If you

do not provide this information, your

monthly benefit

will be reduced by an amount equal to

the total lump

sum. In that case, Prudential will withhold your

benefit

each month until the calculated lump sum has

been

exhausted. However, if Prudential is

given proof of the

time period and amount attributable

to lost income, any

appropriate adjustments will be

made.

In the event any benefits eligible as offsets are denied

because a claim was not filed in the required time

frame, benefits from this Voluntary Disability Plan will

be reduced by assuming that plan’s maximum disability

benefit would have been awarded.

7

Definitions & Plan Details

What it means to be disabled

You must be considered “disabled”

to receive Plan benefits.

For purposes of the Voluntary Disability Plan, “Disability” is

defined as follows:

Option 1 (2 Year Plan):

You are disabled when Prudential determines that:

you are unable to perform the material and

substantial duties of your regular occupation due

to your sickness or injury;

you are under the regular care of a doctor; and

you have a 20% or more loss in your monthly

earnings due to that sickness or injury.

Option 2 (5 Year Plan):

Regular Occupation Period. You are disabled when

Prudential determines that:

you are unable to perform the material and

substantial duties of your regular occupation due

to your sickness or injury;

you are under the regular care of a doctor; and

you have a 20% or more loss in your monthly

earnings due to that sickness or injury.

Gainful Occupation Period. After 24 months of

payments, you are disabled when Prudential determines

that due to the same sickness or injury:

you are unable to perform the duties of any

gainful occupation including self-employment,

that is or can be expected to provide you with an

income within 12 months of your return to work

that exceeds 60% of your monthly earnings, for

which you are reasonably fitted by education,

training or experience; and

you are under the regular care of a doctor.

While working during Regular Occupation Period

disability earnings cannot exceed 80% of indexed pre-

disability earnings. During the Gainful Occupation Period

disability earnings cannot exceed 60% of indexed pre-

disability earnings.

Your loss of earnings must be a direct result of your

illness, pregnancy or injury. Economic factors such as, but

not limited to, recession, job obsolescence, pay cuts and

job-sharing will not be considered in determining

whether you meet the loss of earnings test.

For an employee whose occupation requires a license,

"loss of license" or inability to qualify for a license for any

reason does not constitute disability.

You may be required to submit to an independent

medical

examination (IME), sign a written authorization

to release

medical records and furnish medical records. If

you fail to

complete a requested IME, furnish requested

medical

records or provide a written authorization for

release of

medical records, each in a timely fashion,

disability

benefits will cease.

In some cases, you will be required to give Prudential

authorization to obtain additional medical information,

and to provide non-medical information (e.g., copies of

your IRS federal income tax return, W-2s and 1099s) as

part of your proof of claim, or proof of continuing

disability. This proof, provided at your expense, must be

received within 30 days of a request by Prudential.

"Regular care" means:

one personally visits a doctor as frequently as is

medically required, according to generally

accepted medical standards, to effective manage

and treat one’s disabling condition(s); and

one is receiving the most appropriate treatment

and care, which conforms with generally

accepted medical standards, for one’s disabling

condition(s) by a doctor whose specialty or

experience is the most appropriate for one’s

disabling condition(s), according to generally

accepted medical standards.

"Regular occupation" means the occupation you are

routinely performing when your disability begins. Prudential

will look at your occupation as it is normally performed

instead of how the work tasks are performed for a specific

employer or at a specific location.

“Material and substantial duties” means duties that:

are normally required for the performance of your

regular occupation; and

cannot be reasonably omitted or modified.

“Sickness” means any disorder of your body or mind, but

not an injury; pregnancy including abortion, miscarriage

or childbirth. A disability must begin while you are

covered under the plan.

“Injury” means a bodily injury that:

is the direct result of an accident;

is independent of sickness;

occurs while you are covered under the Plan;

and

results in immediate disability. Disability must

begin while you are covered under the Plan.

8

Benefit Maximums

The maximum benefit this plan will pay is $10,000 per

month.

Benefits under this Plan reduce or end if you are

released to return to work on a regular, full-time or

part-time basis, or you are no longer disabled as

defined

by this Plan. This requirement is modified by

the terms of

the Residual Benefit section, discussed

later in this

document.

If you remain disabled as defined by the Plan, benefits

may continue according to the following maximum

benefit period schedule:

2-Year Option

Disability begins at age

Maximum benefit period:

Under age 68

63 or 64

24 months

36 months

Age 68

To age 70

Age 69 or older

12 months

5-Year Option

Maximum benefit period:

Under age 68

63 or 64

24 months

36 months

Age 68

To age 70

Age 69 or older

12 months

Disability begins at age

Maximum benefit period:

Under age 65

63 or 64

60 months

36 months

Age 65 - 68

To age 70

Age 69 or older

12 months

The benefit period may be shorter for certain disabling

conditions. (See the "Plan Limitations" section.)

Benefit Minimums

Should your benefit under this voluntary disability plan

be reduced under the Residual Disability, Return to Work

or Deductible Sources of Income features of the Plan

your actual monthly

benefit from this Plan will be at

least 10%

of your benefit before reductions for other

income,

or $100 (whichever is greater).

For example, if your base rate of pay is $2,000 per

month, your normal disability benefit (60%) is $1,200 per

month, and

you are receiving $1,300 per month from

primary and family Social Security benefits, your

monthly benefit from

this Plan will be calculated as

follows:

Dates of Disability Prior to 1/1/2019

Base salary $2,000/mo

Normal Plan Benefit 60% $1,200/mo

SS Disability Benefit $1,300/mo

Benefit after offset $0

Minimum Plan benefit paid $120/mo*

*The greater of 10% of $1,200 ($120) or $100.

Dates of Disability After 1/1/2019

If your base rate of pay is $2,000 per month, your normal

disability benefit (50%) is $1,000 per month, and

you are

receiving $1,300 per month from primary and family Social

Security benefits, your monthly benefit from

this Plan will

be calculated as follows:

Base salary $2,000/mo

Normal Plan Benefit 50% $1,000/mo

SS Disability Benefit $1,300/mo

Benefit after offset $0

Minimum Plan benefit paid $100/mo*

*The greater of 10% of $1,000 ($100) or $100.

Restrictions Applying to Benefits

In no case will disability benefits be payable after the

earliest of the following events:

you are able to return to work on a regular,

full-

time basis,

you are no longer disabled

as defined by this

Plan,

you are no longer under the regular care of

a

physician,

you fail to furnish proof of continuing

disability

when requested by Prudential,

you do not participate in an approved

rehabilitation program as described in

"Mandatory Rehabilitation Requirements",

or

you die.

Right to Recover Overpayments

The Prudential Insurance Company of America or its

designated

agent has the right to recover from you any

amount

determined to be an overpayment. You have the

obligation to repay Prudential any such amount. Rights

and obligations in this regard are set forth in the

reimbursement agreement you are required to sign

when

you submit a claim for benefits under this Plan. The

agreement confirms you will repay all overpayments and

authorizes Prudential, or its designated agent, to

obtain

any information relating to other income benefits.

An

overpayment occurs when it is determined that the

total

amount paid on your claim is more than the total of

the

benefits due under this Plan.

The overpayment equals the amount paid in excess of

the amount that should have been paid under this Plan.

9

An overpayment also occurs when payment is made

that

should have been made under another group

plan. In

that case, Prudential, or its designated agent,

may

recover the payment from one or more of the

following:

any other organization; or

any person to or for whom payment was

made.

Prudential may recover the overpayment by:

offsetting against any future benefits payable

to

you or your survivors, and/or

demanding an immediate refund of the

overpayment from you, and/or,

taking civil actions to recover any Plan

overpayments.

As part of your

claims/appeals rights described in this

booklet, you have

the right to appeal any overpayment

recovery or

demand.

Recurrent Disabilities

If you return to work after a disability (and are not

eligible for residual disability benefits), meet the Plan's

eligibility requirements, and then become disabled again,

the following rules apply to the way your benefits are

paid.

Your benefit under this Voluntary Disability Plan may be

treated as part of your prior claim, so that you will not

need to complete another elimination period provided:

The recurrent disability occurs within six months of

the end of the prior claim; and

You are continuously insured under this voluntary

disability plan, with paid premiums between the

prior claim and the new disability.

Your new disability will not be considered a

continuation of your original disability if your

new

disability starts more than six months after

your return

to full-time employment, or if you have not been

continuously insured under this Plan. In this

situation,

you must meet the eligibility

requirements for a new

disability, and must meet a new elimination period.

A ”recurrent disability” is defined as a disability which

is:

caused by a worsening in your condition; and

due to the same cause(s) as your prior disability

for which Prudential made a disability payment.

Leaves of Absence

Walgreens policies regarding leaves of absence and

employment status are independent of your rights to

disability benefits under this Plan. The duration of your

disability benefit is based solely on the terms and

conditions of this Plan, while the duration of any leave of

absence (and your continued employment status) is

based on separate policies and legal rules. At the time

your disability leave commences, Walgreens or its

agent,

Sedgwick, will provide you with information regarding

leaves

of absence and employment status.

If you are not receiving paid disability benefits from the

Walgreens Company-Paid Disability Plan for Hourly Team

Members you must apply for an Unpaid Medical Leave of

Absence while you are not working due to disability, to

maintain your employment status with Walgreens.

Partial Disability Benefits

If your disability is such that you can work — but are not

able to earn more than 80% of your

indexed prior

earnings, as defined below — you may be eligible for a

reduced benefit,

called a Partial Disability Benefit. This

feature

encourages you to return to work when physically

able.

A partial disability is any disability that prevents you

from

performing on a normal full-time basis, one or more

of the

essential duties of your regular occupation, but allows you

to work at your regular or any occupation, on less than a

normal full-time basis. The wages you earn

while on a

partial disability are called your partial

disability wages.

Partial disability benefits are only available from this

Voluntary Disability Plan when you have met all other Plan

requirements.

Indexed Monthly Earnings

In determining your eligibility for a partial benefit

amount, the Plan uses a special definition of your

monthly earnings called indexed monthly earnings.

Indexed monthly earnings means your monthly

earnings as adjusted on each July 1 provided you were

disabled for all of the 12 months before that date.

Your monthly earnings will be adjusted on that date

by the lesser of 10% or the current annual percentage

increase in the Consumer Price Index. Your indexed

monthly earnings may increase or remain the same,

but will never decrease.

The Consumer Price Index (CPI-W) is published by the

U.S. Department of Labor. Prudential reserves the

right to use some other similar measurement if the

Department of Labor changes or stops publishing the

10

CPI–W. Indexing is only used to determine your

percentage of lost earnings while you are disabled

and working.

While working during Regular Occupation period,

disability earnings cannot exceed 80% of indexed

monthly earnings. After the Regular Occupation period,

disability earnings cannot exceed 60% of indexed

monthly earnings.

Special Return-to-Work Benefit

The Special Return-to-Work Benefit is designed to

encourage you to return to work as soon as you are

able.

If you return to work on a partial disability basis,

your payments under this Voluntary Disability Plan will

not be reduced by any earnings you receive provided:

You are within the first 12 months of working

part-time and receiving benefits from this Plan,

and

The total of your disability benefit under this

Plan and your disability earnings do not exceed

100% of your pre-disability earnings.

If you continue to work on a partial disability basis after

the maximum 12 month Return to Work Period, your

benefit under this Plan will be based on a percentage of

your lost income.

For example, suppose you’re covered under the 2-year

option, and your monthly earnings are $3,000 a

month,

and your

partial disability wages are $1,000 a month.

Your

return-to-work benefit would be calculated as

follows:

Dates of Disability Prior to 1/1/2019

Example A

Monthly earnings $3,000/month

Disability normal benefit

(60% of monthly earnings) $1,800/month

Partial disability wages + $1,000/month

Total income from all sources $2,800/month

Return-to-work benefit $1,800/month

In Example A, your return-to-work benefit equals your

disability normal benefit, since your total income

from all

sources ($2,800) does not exceed your monthly earnings

of $3,000.

Example B

If using the same example, your monthly earnings are the

same, but you earn partial disability wages of $2,000 a

month. In this case, your return-to-work benefit would

be

calculated as follows:

Monthly earnings $3,000/month

Disability normal benefit

(60% of monthly earnings) $1,800/month

Partial disability wages + $2,000/month

Total income from all sources $3,800/month

Excess benefit ($3,800-$3,000) $800/month

Return-to-work benefit

($1,800-$800)

$1,000/month

In Example B, the return-to-work benefit is $800 less

than

the disability normal benefit, since your total

income from

all sources cannot be greater than your

monthly earnings

(in this case $3,000).

Dates of Disability After 1/1/2019

Example A

Monthly earnings $3,000/month

Disability normal benefit

(50% of monthly earnings) $1,500/month

Partial disability wages + $1,000/month

Total income from all sources $2,500/month

Return-to-work benefit $1,500/month

In Example A, your return-to-work benefit equals your

disability normal benefit, since your total income

from all

sources ($2,500) does not exceed your monthly earnings

of $3,000.

Example B

If using the same example, your monthly earnings are the

same, but you earn partial disability wages of $2,000 a

month. In this case, your return-to-work benefit would

be

calculated as follows:

Monthly earnings $3,000/month

Disability normal benefit

(50% of monthly earnings) $1,500/month

Partial disability wages + $2,000/month

Total income from all sources $3,500/month

Excess benefit ($3,500-$3,000) $500/month

Return-to-work benefit

($1,500-$500)

$1,000/month

In Example B, the return-to-work benefit is $500 less

than

the disability normal benefit, since your total

income from

all sources cannot be greater than your

monthly earnings

(in this case $3,000).

11

Normal Partial Disability

Benefits

If you are still partially disabled after 12 months of

receiving benefits under this Voluntary Disability Plan,

the Plan will apply a Partial Disability Earnings Test to

determine if your benefits under this plan will be

reduced for any Partial Disability Wages.

2-Year Plan

While receiving benefits under this Plan during

months 12-24, your Plan benefits will be

calculated based on the percentage of income

you are losing due to your disability as long as

your disability wages are between 20% and 80%

of your indexed prior earnings.

5-Year Plan

During months 12-24 of receiving benefits under

this Plan, your Plan benefits will be calculated

based on the percentage of income you are

losing due to your disability as long as your

disability wages are between 20% and 80% of

your indexed prior earnings.

After 24 months of receiving benefits under this

Plan, your Plan benefits will be calculated based

on the percentage of income you are losing due

to your disability as long as your disability wages

are between 20% and 60% of your indexed prior

earnings.

Example C

Suppose you’re enrolled in the 5-year option, and

before you became disabled your monthly earnings

were $3,000 a month and after 24 months of receiving

benefits under this Voluntary Disability Plan, your partial

disability wages

are $1,500/month. Your indexed prior

earnings are

calculated according to the Consumer

Price Index for the

most recent 12-month period (not

to exceed a 10%

maximum change per 12-month

period). Your normal

partial disability benefit amount

would be calculated as

follows:

Dates of Disability Prior to 1/1/2019

Monthly earnings $3,000

Indexed prior earnings $3,200

Indexed benefit @ 60%

$1,920

Partial Disability Wages

$1,500

% of income lost

53%

$3,420

Partial benefit payable

1017.60

$1,700

In this example, the percentage of income lost is

calculated by subtracting your Partial Disability Wages

(1,500) from your indexed prior earnings (3,200) and then

dividing that answer by your indexed prior earnings (3,200).

Your benefit under this Plan would be the percentage of

income lost multiplied by the indexed benefit (1,920 x .53).

Dates of Disability After 1/1/2019

Monthly earnings $3,000

Indexed prior earnings $3,200

Indexed benefit @ 50%

$1,600

Partial Disability Wages

$1,500

% of lost income

53%

$3,100

Partial benefit payable

$848

$1,700

In this example, the percentage of income lost is calculated

by subtracting your Partial Disability Wages (1,500) from

your indexed prior earnings (3,200) and then dividing that

answer by your indexed prior earnings (3,200). Your benefit

under this Plan would be the percentage of income lost

multiplied by the indexed benefit (1,600 x .53).

Other Benefits

Mandatory Rehabilitation Requirements

Disabled individuals often need to follow a program of

vocational rehabilitation services in order to regain the

ability to work productively. The Prudential Insurance

Company of America will work with you when

appropriate

to develop a work rehabilitation plan. This

will allow you

to return to work on a full- or part-time

basis, in an

occupation for which you are reasonably

qualified, taking

into account your training, education,

experience and

past earnings. This program could

include vocational

training and/or physical therapy. If

you decline to

participate in a Prudential-approved work

rehabilitation plan, you will no longer be eligible for any

benefits from this Plan.

Enhanced Rehabilitation Benefits

While you are receiving benefits under this Plan, and

actively participating in a Prudential approved

rehabilitation program, the Plan will pay enhanced

benefits to you for a maximum of six months. The benefit

enhancement may include:

An additional benefit up to 5% of your monthly

payment. However, the monthly rehabilitation

payment, together with your monthly payment,

will not exceed the maximum monthly payment.

An additional monthly payment up to $500, for

eligible day care expenses for each eligible child.

An additional monthly payment up to $500, for

eligible elder and spouse care expenses for the

care of each eligible family member.

Please contact Prudential at 800-842-1718, for more

information on Rehabilitation Benefits.

12

Survivor Benefit

The Plan will pay a benefit to your eligible survivors if you

die while you are disabled and

receiving voluntary

disability benefits under this Plan at the time of your

death. The

survivor benefit will be paid in a single lump

sum, and

will be equal to three times your most recent

gross

monthly benefit. The benefit is

payable to your

spouse/partner (as defined by Walgreens for its medical

plan qualifications), if living at

the time payment is made.

Otherwise, it is payable by

dividing the benefit amount

equally among your eligible

children. If there is no

eligible survivor, the benefit will be paid to your estate.

Eligible children are your unmarried children, your

eligible spouse/partner's unmarried children, your

unmarried adopted children, and unmarried children

placed for adoption with you prior to legal adoption

being final, and all under age 25.

To file a claim for this benefit, your survivor should

contact Prudential at 800-842-1718.

Please keep this

booklet with your other important

papers so your

beneficiaries will know the correct

procedures to follow.

Filing a Claim

If you file a claim under the Company Paid Disability

Plan for Hourly Team Members through Sedgwick CMS

Disability Claim Center at 877-872-0911 or TTY Line

(Teletypewriter for the hearing

impaired) 901-531-

4554, Sedgwick will forward your claim information to

Prudential, once you are getting close to the end of the

elimination period for benefits under this Plan, so you

may not need to file a separate claim through

Prudential.

If you need to file a claim directly with Prudential for

benefits under this Plan, it's important

to follow the

correct benefit claim procedure.

How to File a Claim

To submit a claim for benefits under this Plan, call

Prudential at 800-842-1718 between 8 am and 11

pm, Eastern Time, Monday – Friday. You can speak

to a trained disability specialist or follow the prompts

to record your disability information. You may also

file a claim online by logging into

www.prudential.com/mybenefits. Click on “Report

Time out of Work” and follow the instructions to

complete the Interactive Claimant Submission form.

You should ensure your claim has been filed with

Prudential within 30 days of the start of your

disability. However, you must give Prudential written

proof of your claim no later than 90 days after your

elimination period ends. If it is not possible to give

proof within 90 days, it must be given no later than 1

year after the time proof is otherwise required except

in the absence of legal capacity.

You should have the following information ready

when you report your claim:

Company Name: Walgreens

Company Control Number: 42097

Your Employee ID or Social Security number

Your address and telephone number

Your date of birth

Your job title

Your doctor’s name, phone number and fax

number

Your last day worked and first day absent due to

the condition

The date you expect to return to work

Whether your absence is work-related.

Prudential will contact you if additional information is

needed.

To process your claim for disability, Prudential will need

a statement from you, your doctor and Walgreens.

When you speak to a Prudential specialist, he or she will

obtain your information. Prudential will then request

the necessary information for your doctor and

Walgreens. A decision will be made after all this

information is reviewed.

Be sure to tell your doctor that he or she will be

contacted by Prudential, to

obtain information

concerning your disability. Your doctor will need

authorization from you to provide Prudential with any

of your medical

information. In most cases, you must

provide each

doctor with a signed authorization to

release medical

information. You may use the

authorization form

provided by the medical provider.

You will also be

required to sign and return an

authorization form for

release of information before any

benefit will be

approved. Prudential will attempt to

work directly with your doctor to obtain the needed

medical history information, but it is your responsibility

to provide these proofs of disability.

If you are unable to personally file your claim, you may

have a friend or relative file it on your behalf, following

the procedures in this section. If you need to designate

someone to authorize the release of any health

information, you will need to appoint a person with

power of attorney to act in your place. This requires a

formal document.

It is your responsibility to pay for any charges by your

medical provider to furnish medical information or

copies of medical records. The company will not

reimburse you or your medical provider for these

13

expenses.

When necessary, Prudential may use the

services of

outside consultants and other sources to aid

in the

evaluation of your disability status. Prudential reserves

the right to determine whether

your disability qualifies

for benefits.

As a condition of receiving benefits, you may be required

to submit to an independent medical examination (IME),

which would be paid for by Prudential. If you do not

complete the requested IME in a timely manner,

disability benefits will cease (or not be approved).

Prudential has the right to request an IME, but is not

obligated to do so.

You should contact Prudential again by phone or online

if:

You have updated information

You are unable to return to work when

planned

You have returned to work or are returning

You want to report your delivery date

You need forms.

If you have questions on the status of your disability

claim or payments, please call Prudential at 800-842-

1718, or log into www.prudential.com/mybenefits.

If you are eligible for state disability

benefits from New

York, Rhode Island, New Jersey,

California or Hawaii,

you are responsible for

filing your separate disability

claim for the

state plan. Upon receipt of the

Explanation of Benefits (EOB) from that plan, you must

provide a copy of the EOB to Prudential before any

voluntary disability benefit payment will be made.

Please Note: If you are eligible for workers' compensation

and/or state disability payments, benefit approval and

payment information for those plans must be submitted

to Prudential in order to receive benefit payments from

this Plan.

Procedures for Reviewing

Claims

The claims procedures described below are prescribed

by

a federal law called the Employee Retirement

Income

Security Act of 1974 (ERISA). The following

disability Claims and Appeals Procedures apply only to

disability claims filed on or after April 1, 2018.

Initial Claims Determinations: All formal benefit claims

under the Plan will be reviewed by Prudential (the

insurance carrier), or any third party engaged by

Prudential for this purpose (collectively, the “Claim

Administrator”), which will make its decision, based

on

the information submitted by you, within 45 days

after

the claim is submitted. By notice to you before this

period ends, the Claim Administrator may extend this

deadline by up to 30 additional days if it determines that

a decision cannot be made during the initial period for

reasons beyond the control of the Plan. An extension

notice will specify the length of the extension and inform

you that a decision cannot be made within the deadline

because of reasons beyond the control of the Claim

Administrator. A second extension of up to an additional

30 days also may be declared. If such an extension is

necessary, the notification will include a description of

the circumstances requiring the extension and an

estimate of the decision date.

Claim Denials

If your claim is denied, the Claim Administrator will send

you a notice that will:

be written in a manner that you should

understand;

include the specific reasons for the adverse

benefit determination;

refer to the provisions of the Plan on which the

determination was based;

describe any additional material or information

necessary to perfect the claim and explain why

the additional material is necessary;

explain the Plan's review procedures including

relevant deadlines;

include a statement of your right to bring a civil

action under ERISA after receiving a final

determination upon appeal. The notice will also

include an explanation of any applicable

contractual limitation period for bringing a civil

action under section 502(a) of ERISA, and a

description of the calendar date on which the

limitations period expires;

identify any internal rule, protocol or

criterion

that was relied on in making the

a d v e r s e

b e n e f i t

determination or, alternatively, a

statement that no such specific rule, guideline,

protocol, standard or criterion exists;

include a language assistance notice in

Chinese, Tagalog, Navajo and Spanish;

if advice is obtained from medical or vocational

experts in connection with an adverse benefit

determination that is inconsistent with its

decision, an explanation as to why the Claims

Administrator disagreed with, or did not

follow, this advice without regard to whether

the advice was relied on in making the

determination; and

an explanation of disagreement with any

14

disability determination made by the Social

Security Administration (SSA), or any view of

health care professionals who are treating

you or vocational experts who are evaluating

your claim to the extent you presented such

determination or views to the Claims

Administrator.

Appealing a Denied Claim

To appeal a claim denial, you must send your written

appeal to

Prudential within 180 days of receiving

notice

of the claim denial. Your appeal should contain:

Your name, control number (42097), and Social

Security number (or claim number)

The reasons that you disagree with the

determination

Medical evidence or information to support

your position such as:

• Copies of therapy treatment notes

• Any additional treatment records from

physicians

• Actual test results (e.g. EMG, MRI)

Your appeal may also contain written

comments,

documents, records and other pertinent

information. You

will be given reasonable access to, and

copies of, all

documents, records and other information

relevant to the

claim. It is essential that you supply all

information or

opinions that you believe may be relevant

to the claim. To

be assured of a proper response to the

appeal, it must be

directed to Prudential Appeals Review Unit at:

Appeals Review Unit

The Prudential Insurance Company of America

Disability Management Services

PO Box 13480

Philadelphia, PA 19176

Phone: (800) 842-1718

Fax: (877) 889-4885

Prudential’s Review of Appeal

The appeal will be conducted by the Prudential Appeals

Review Unit,

and the reviewer will be a named fiduciary

who is neither

the individual nor a subordinate of the

individual who

made the initial denial. This reviewer will

not give

deference to the initial benefit determination

and will

take into account all comments, documents,

records and

other information that you submit relating

to the claim,

without regard to whether the information

was

submitted or considered in the initial benefit

determination.

If the initial denial was based on a medical judgment, the

reviewer will consult with a health care professional who

has appropriate training and experience in the medical

field. This health care professional will not be an

individual

who was consulted in connection with the

initial benefit

determination or the subordinate of any

such individual.

Potential Review of Appeal by

the Plan Administrator

If Prudential determines that the appeal presents

material issues that are outside the expertise or purview

of the Prudential Appeals Review Unit (such as hours

worked, employment status or new or unique procedural

or Plan

interpretation issues), then the decisions will be

subject to further review by the Plan Administrator. You

will be notified if such a further

review will be performed.

Unless you are instructed that

additional information is

needed for this review, you will

not be required to submit

any further information to the Plan Administrator

(although you may do so if you wish).

The Plan

Administrator’s decision will be based on all

information

submitted by you and any other information

that the Plan

Administrator considers relevant.

Notice of Decision on Appeal

Regardless of whether the Plan Administrator gets

involved in the decision, you will be notified of the

benefit determination within 45 days of the receipt of

the appeal. By notice to you before this period ends,

Prudential may extend this deadline by up to 45

additional days if it determines that a decision cannot

be made during the initial period for reasons beyond the

control of the Plan. If any adverse benefit determination

is anticipated during the appeal review, you will be

provided with the new information or rationale sufficiently

in advance of the appeal decision to allow you a

reasonable opportunity to respond. An extension notice

will specify the

length of the extension and inform you

that a decision

cannot be made within the deadline

because of reasons

beyond the control of Prudential.

If the decision on appeal is denied, the Prudential

Appeals Review Unit will provide

you with a notice of

the denial that will:

be written in a manner that you should

understand;

include the specific reasons for the denial;

refer to the provisions of the Plan on which the

determination was based;

inform you that, upon request and free of

charge, you are entitled to reasonable access to

and copies of all documents, records and other

information relevant to your claim;

explain the Plan's claim review procedures

(including relevant time limits) and your right to

bring legal action under ERISA;

15

include an explanation of any applicable

contractual limitation period for bringing a

civil action under section 502(a) of ERISA, and

a description of the calendar date on which

the limitations period expires for filing any

legal action;

identify any internal rule, guideline,

protocol, standard or criterion that was

relied on in making the adverse benefit

determination or, alternatively, a statement

that no such specific rule, guideline,

protocol, standard or criterion exists;;

if the advice of a health care professional or

vocational expert was obtained, identify

such

person or persons;

if advice is obtained from medical or

vocational experts in connection with an

adverse benefit determination that is

inconsistent with the appeal decision, an

explanation as to why the Claims

Administrator disagreed with, or did not

follow, this advice without regard to

whether the advice was relied on in making

the determination;

an explanation of disagreement with any

disability determination made by the SSA,

or any view of health care professionals

who are treating you or vocational experts

who are evaluating your claim to the extent

you presented such determination or views

to the Claims Administrator;

include a language assistance notice in

Chinese, Tagalog, Navajo and Spanish; and

notify you that you can contact the

Department

of Labor to learn about other

voluntary dispute

resolution options.

General Claims/Appeals

Information

Both in the context of initial claims determination and in

the context of reviewing appeals, there may be situations

where Prudential needs additional information from you

before it can

make its determination. If that is the case,

you will be

notified of the specific information that is

needed and/or

any issues that need to be resolved, and

you will be given

a reasonable period of time to supply

the needed

information (generally 30 days). In such

situations, the

deadlines for responding to the claim or

appeal may be

put on hold while the receipt of this

additional

information is pending.

The claims and appeals reviewers described above will

apply their judgment to claims and appeals in a manner

that they deem to be consistent with the Plan and any

rules, regulations or prior interpretations of the Plan.

Those reviewers will

make their decisions in a manner

that they believe will

apply the Plan consistently to

similarly situated

participants.

The authority granted to these claims and appeals

reviewers to construe and interpret the Plan and make

benefit determinations, including claims and

appeals

determinations, shall be exercised by them (or

persons

acting under their supervision) as they deem

appropriate

in their sole discretion. Benefits under this

Plan will be

paid or provided to you only if these reviewers decide in

their discretion that you are entitled to them.

All such

benefit determinations shall be final and binding

on all

persons, except to the limited extent to which the

Prudential

Appeals Review Unit's decisions are subject to

further