HB-1-3555

(03-09-16) SPECIAL PN 12-1

Revised (04-01-24) PN 609

CHAPTER 12: PROPERTY AND APPRAISAL

REQUIREMENTS

12.1 INTRODUCTION

Lenders must ensure the property to be purchased is eligible for the Single Family

Housing Guaranteed Loan Program (SFHGLP). The Agency’s minimum property

requirements serve to protect the borrower’s interest, minimize the lender’s loss, and

reduce the potential risk to the government in the event of liquidation. It is the lender’s

responsibility to ensure that the property meets the Agency’s standards.

SECTION 1: UNDERWRITING THE PROPERTY [7 CFR 3555.201]

12.2 OVERVIEW

The lender must ensure the subject property meets the Agency’s site guidelines. In

particular, sites must be located in eligible rural areas; meet community standards

regarding utilities, including water and wastewater systems; meet street and road access

and maintenance requirements; and contain other amenities essential to the continued

marketability of the home. This section addresses each of these standards.

12.3 RURAL AREA DESIGNATION [7 CFR 3555.201(a)]

Only loans secured by properties located in areas designated by the Agency as rural

are eligible to receive a loan guarantee. This section discusses rural areas designations,

how lenders are notified of changes in rural area designations and clarifies rare situations

in which loans for properties in areas no longer designated as rural may receive a loan

guarantee.

A. Rural Area Definition

An area’s rural designation is determined by the Agency and may be changed as a

result of periodic review or after the decennial census of population. The Agency

conducts reviews every five years to identify areas that no longer qualify as rural. In areas

experiencing rapid growth, and in eligible communities within Metropolitan Statistical

Areas (MSAs), reviews take place every three years. Public notification will be given at

least 30 days before the date of the final determination in order to give interested parties

an adequate chance to comment. Refer to section 3550.10 of 7 CFR 3550 and HB-1-3550

Chapter 5, for additional information regarding rural area designations.

HB-1-3555

Paragraph 12.3 Rural Area Designation

12-2

In general, rural areas are defined as:

•

Open country that is not part of, or associated with, an urban area;

•

Any town, village, city, or place, including the immediately adjacent densely

settled area, which is not part of, or associated with, an urban area, and which:

o Is rural in character with a population of less than 10,000; or

o Is not contained within an MSA and has a population above 10,000 but below

20,000 and has a serious lack of mortgage credit for lower and moderate-

income families, as determined by the Secretary of Agriculture and the

Secretary of Housing and Urban Development. Any area classified as “rural”

or a “rural area” prior to October 1, 1990, and determined not to be “rural” or

a “rural area” as a result of data received from or after the 1990, 2000, 2010,

or 2020 decennial census, and any area deemed to be a “rural area” any time

during the period beginning January 1, 2000, and ending December 31, 2020,

shall continue to be so classified until the receipt of data from the decennial

census in the year 2030 if such area has a population in excess of 10,000 but

not in excess of 35,000, is rural in character, and has a serious lack of

mortgage credit for lower and moderate-income families.

• Two or more towns, villages, cities, or places that are contiguous may be

considered separately for a rural designation if they are not otherwise associated

with each other, and their densely settled areas are not contiguous.

B. Notification of Rural Area Designation

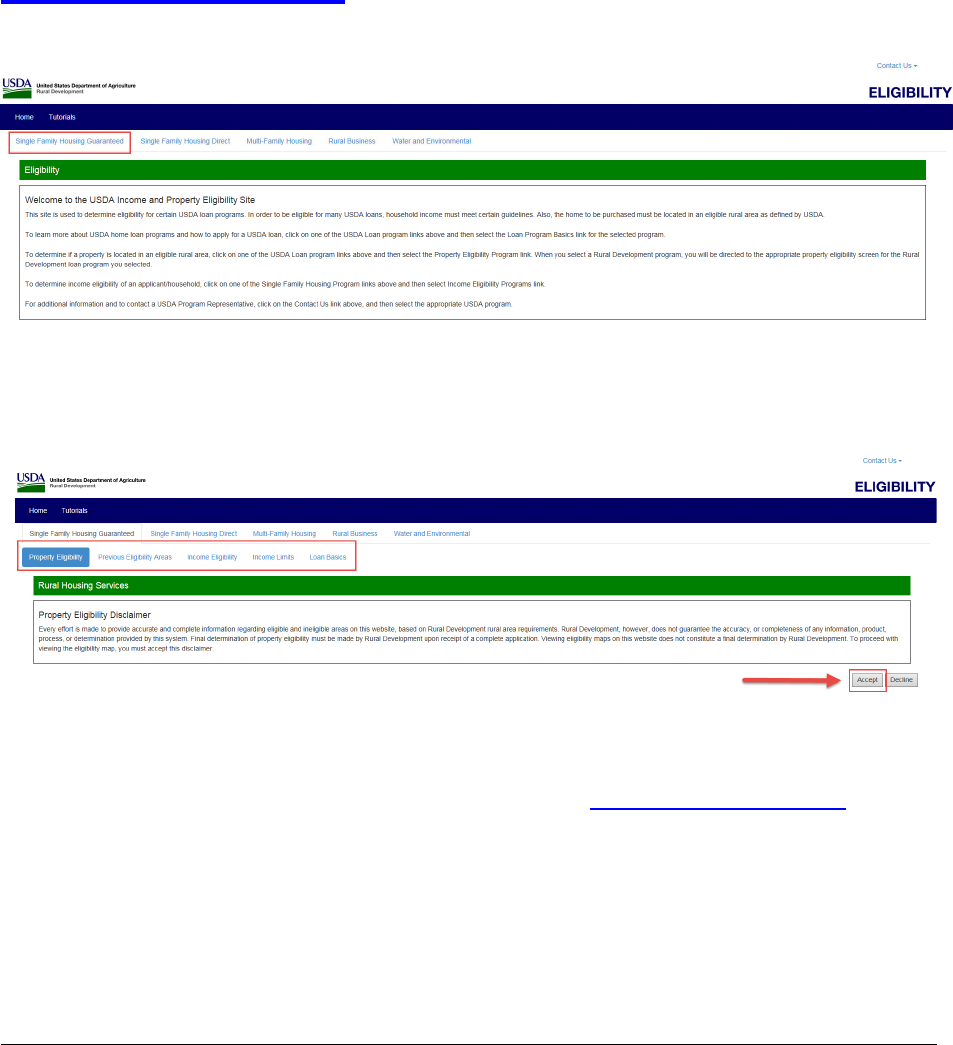

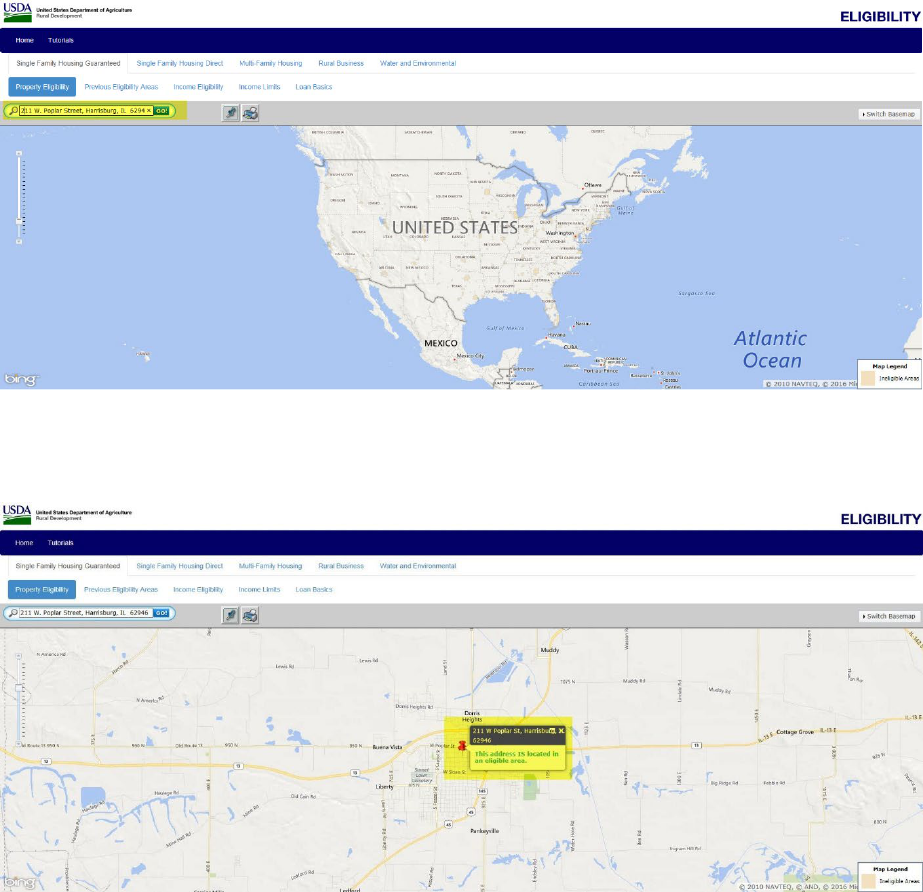

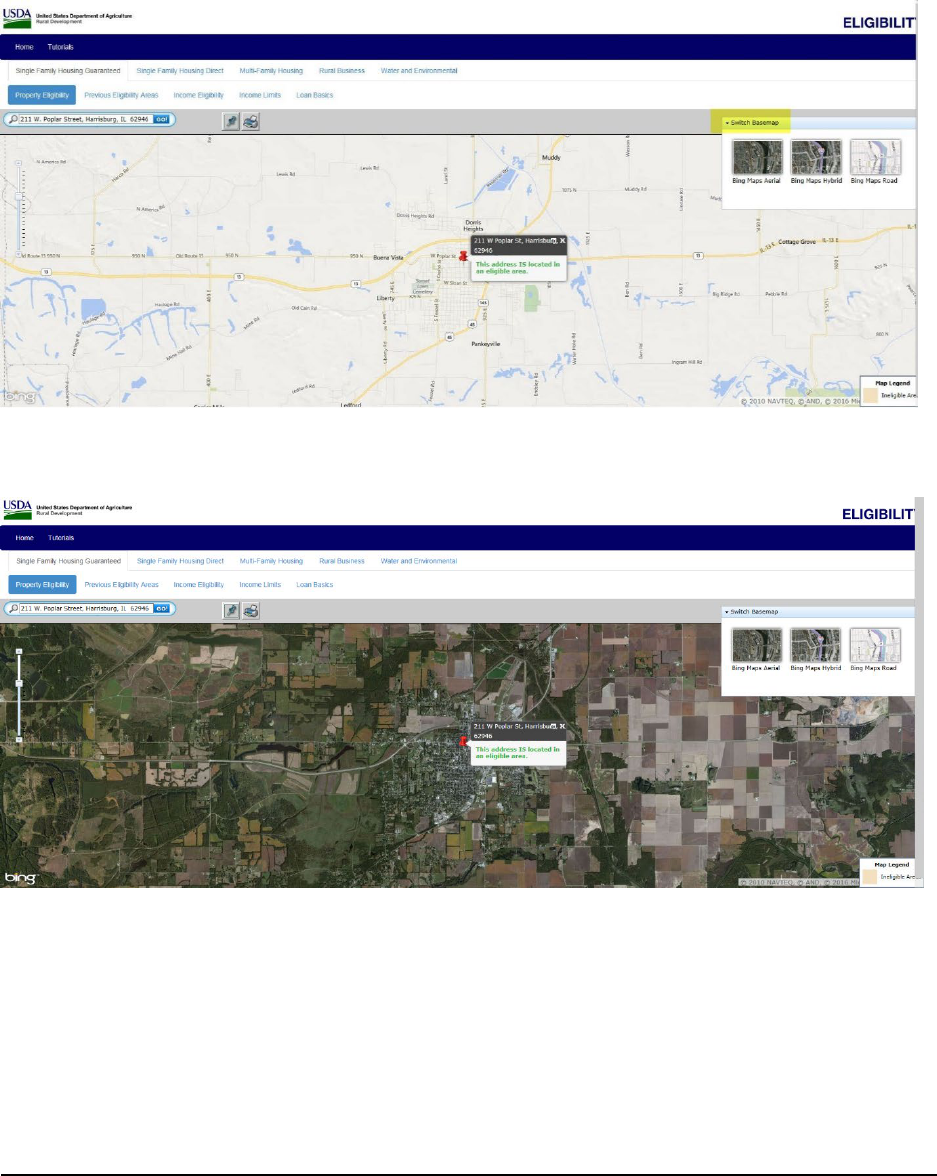

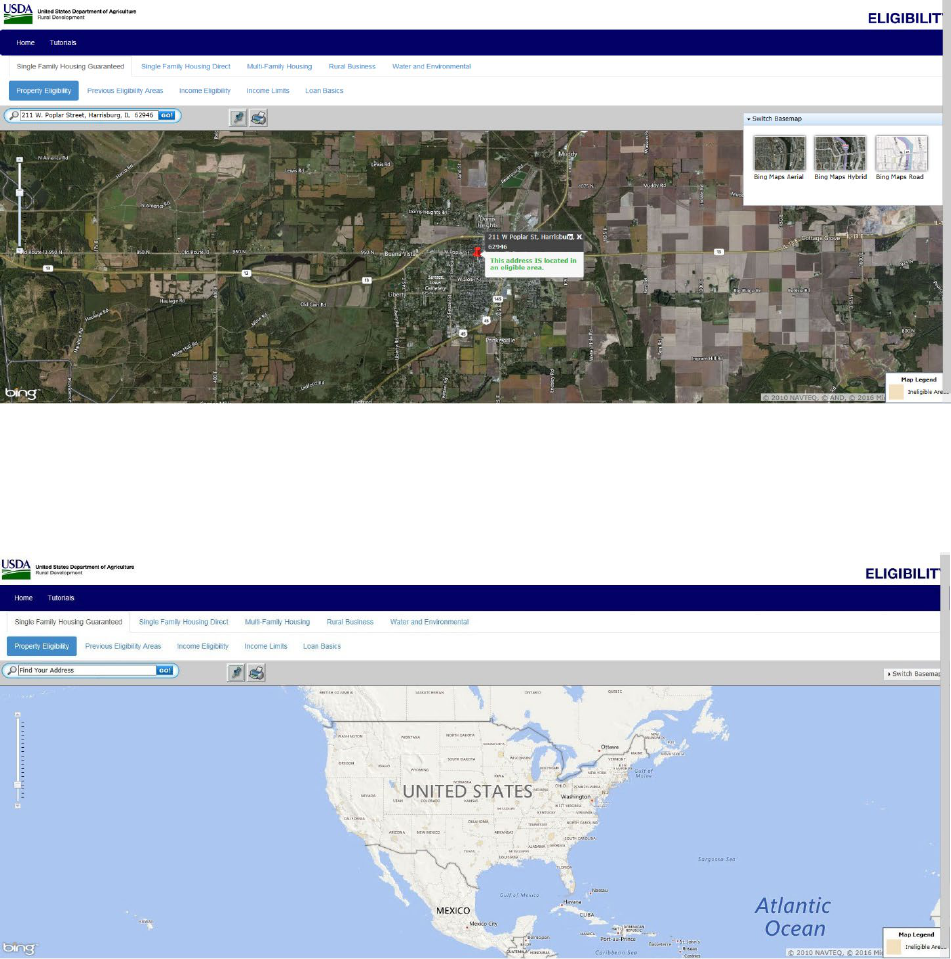

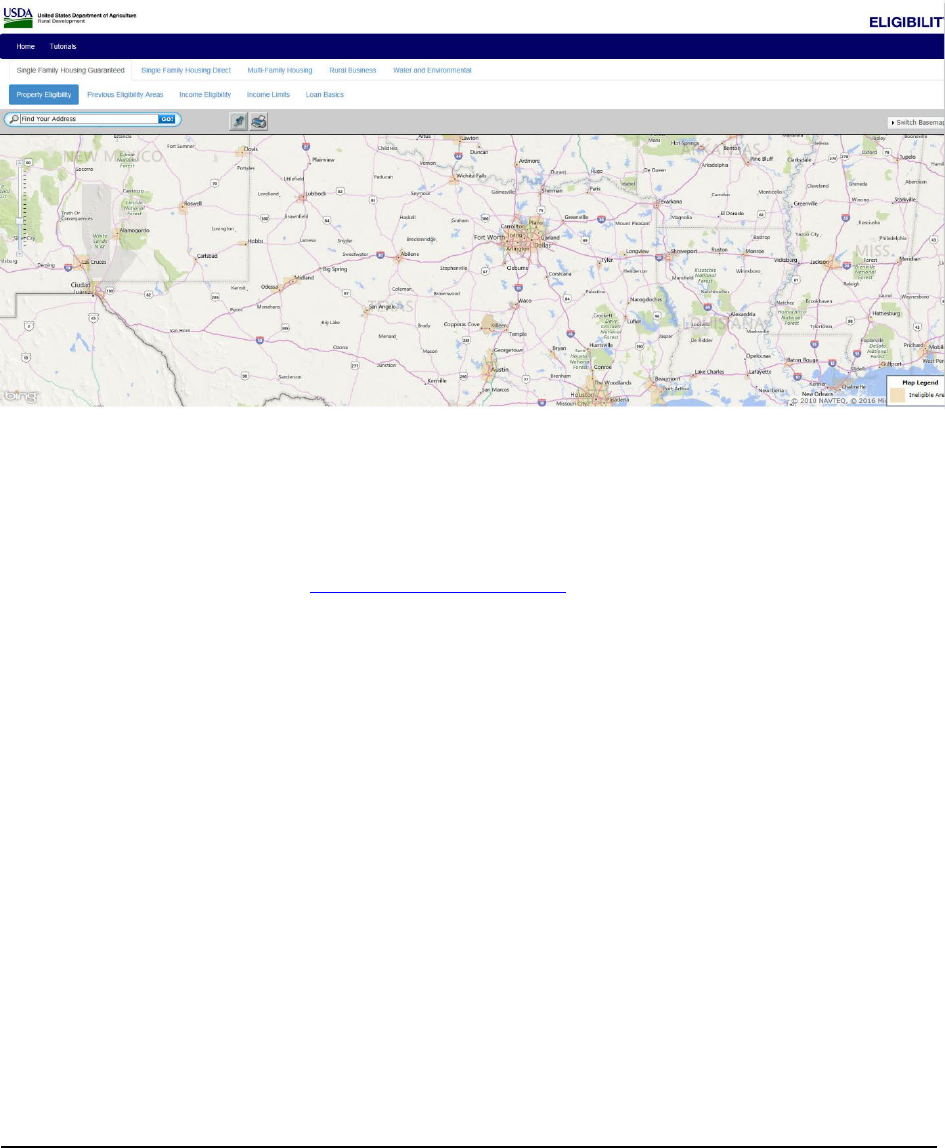

The public website noted below provides an automated system to allow users to enter

addresses and determine property eligibility. Users who utilize the public website will

receive one of three property eligibility decisions when an actual address is entered –

“Eligible,” “Ineligible,” or “Unable to Determine.” In areas not clearly delineated, users

will receive an “Unable to Determine.” With this type of determination, the lender must

confirm with Agency staff the property is located in a rural area and eligible for a

guarantee prior to requesting an appraisal.

USDA Rural Development Property and Income Eligibility Website:

https://eligibility.sc.egov.usda.gov.

Attachment 12-A of this Chapter provides guidance on utilizing the public website to

determine eligible rural areas.

HB-1-3555

Paragraph 12.3 Rural Area Designation

(03-09-16) SPECIAL PN 12-3

Revised (04-01-24) PN 609

C. Making Loans in Areas Changed to Non-rural

If an area’s designation changes from rural to non-rural, loans that meet the following

criteria may be approved in that area:

• Purchase transactions are eligible if the following requirements are met:

o The application is dated and received by the lender prior to the area

designation change;

o The Loan Estimate was issued within three days of the application date;

o The purchase contract is ratified prior to the date of the area designation

change; and

o The applicant and property meet all other loan eligibility requirements.

• Existing conditional commitments that have been issued will be honored provided

the commitment was issued prior to the area designation change;

• Existing direct and guaranteed loans that meet all requirements, as outlined in

Chapter 6, remain eligible for refinance transactions;

• REO property sold from Agency inventory remain eligible for purchase

transactions;

• SFHGLP REO property sales and transfers with assumption may be processed in

areas that have changed to non-rural; and

• A supplemental loan may be made in conjunction with a transfer and assumption

of a guaranteed loan.

12.4 SITE REQUIREMENTS [7 CFR 3555.201(b)]

A qualified property must be predominately residential in use, character, and design.

Sites must be developed in accordance with any standards imposed by a State or local

government. Therefore, the lender must verify that the following requirements are met at

the time of application.

HB-1-3555

Paragraph 12.4 Site Requirements

12-4

•

Site size. There is no specific limitation to the size/acreage of the site. The

appraiser must provide an explanation in the addendum of the appraisal to explain

adjustments to comparable properties, how the subject compares to other single

family sites in the area, etc.

•

Income-Producing Buildings. The property must not include buildings

principally used for income-producing purposes. Barns, silos, commercial

greenhouses, or livestock facilities used primarily for the production of

agricultural, farming, or commercial enterprise are ineligible. However, barns,

silos, livestock facilities, or greenhouses no longer in use for a commercial

operation, which will be used for storage, do not render the property ineligible.

Outbuildings such as storage sheds and non-commercial workshops are permitted

if they are not used primarily for an income producing, agricultural, farming, or

commercial enterprise. A minimal income-producing activity, such as maintaining

a garden that generates a small amount of additional income, does not violate this

requirement. Home-based operations such as childcare, product sales, or craft

production that do not require specific commercial real estate features are not

restricted.

•

Accessory Dwelling Unit. An Accessory Dwelling Unit (ADU) refers to a

habitable living unit, within, or detached from a single family dwelling, which

together constitute a single interest in real estate. The presence of a single ADU

does not automatically render the property ineligible. Design features such as

converted portions of existing homes that include a kitchenette or additional

attached living area (e.g., bedroom and/or bathroom) without a separate address or

independent utilities (e.g., water, gas, electricity) are not restricted, provided they

function in support of only the household members. ADUs which function in

support of the household members, such as multigenerational households are

consistent with the objective of this program, however those designed to create a

potential rental income stream are not. The appraiser will determine if the ADU

represents a second single family housing dwelling unit. The appraiser must

document the highest and best use considering all property characteristics,

including the status of the utilities if they are separate, when making this

determination. The appraiser will include their evaluation in the site analysis and

highest and best use section of the appraisal report, as applicable.

•

Income-Producing Land. The site must not have income-producing land that

will be used principally for income producing purposes. Vacant land or properties

used primarily for agricultural, farming, or commercial enterprise are ineligible. A

residential site that houses a minimal income producing feature such as a

windmill, billboard, cell phone tower, etc. located on the property, does not render

the site income producing. These features are typically maintained with a legal

HB-1-3555

Paragraph 12.4 Site Requirements

(03-09-16) SPECIAL PN 12-5

Revised (04-01-24) PN 609

agreement and generate a minimal amount of additional income. The lender will

review the available documentation and income received in accordance with the

requirements in Chapter 9 for the purpose of calculating annual household

income, as applicable.

•

Multiple Parcels. The lender will ensure the mortgage provides a valid first lien

covering each parcel. Each parcel must be conveyed in its entirety and have the

same basic zoning. The entire property will contain only one dwelling but may

have non-residential, non-income producing buildings, such as a garage. An

improvement that has been built across lot lines is acceptable. For example, a

home built across both parcels where the lot line runs under the home. Parcels

divided by a road, that would otherwise be contiguous, are acceptable.

•

Properties with Solar Panels. Dwellings with solar panels are not considered an

income producing property. If the property owner (seller) is the owner of the solar

panels and the solar panels will be included as part of the purchase transaction,

then standard eligibility requirements apply (i.e. appraisal, insurance, and title). If

the solar panels are subject to a lease agreement, power purchase agreement

(PPA), or similar type of agreement, the following requirements apply:

o Leases and contracts will vary by company and should be considered on a

case by case basis to ensure all terms/regulations are met.

o First lien position, by the lender, should be protected and maintained.

o The property should maintain access to an alternative source of electric/gas

power that meets community standards.

o The energy company or lessee should not block any foreclosure or servicing

actions.

o If an agreement for an energy system lease or PPA could cause restriction

upon transfer of the house, the property is subject to impermissible legal

restrictions and is generally ineligible for the guaranteed loan.

o The lease agreement or PPA should indicate that any damage that occurs as a

result of installation, malfunction, manufacturing defect, or the removal of the

solar panels is the responsibility of the owner of the equipment and the owner

is obligated to repair the damage and return the improvements to their original

or prior condition.

o The lease agreement, PPA, or other agreement should indicate that the owner

HB-1-3555

Paragraph 12.4 Site Requirements

12-6

of the solar panels cannot be a loss payee on the homeowner’s insurance

policy.

o If a lease includes payment for equipment, it should be considered a debt and

included in the total debt ratio. See Chapter 11 for additional guidance.

o Leased solar panels are considered personal property and are not included in

the appraised value.

o Properties with Property Assessed Clean Energy (PACE) loans or assessments

are ineligible for a SFHGLP loan.

•

Site Specifications. The site must be contiguous to, and have direct access from a

street, road, or driveway. Streets and roads must be hard surfaced, or all weather

surfaced, with public access or permanent recorded easements.

•

Utilities. The site must be supported by adequate utilities and water and

wastewater disposal systems.

•

Zoning. The property must comply with applicable zoning requirements and

restrictions. If an existing property does not comply with all current zoning

ordinances but it is accepted by the local zoning authority, the appraiser must

report the property as legal non-conforming. The appraisal must reflect any

adverse effect of the legal nonconforming use on the value and marketability of

the property.

SECTION 2: APPRAISALS [7 CFR 3555.107(d)]

12.5 RESIDENTIAL APPRAISAL REPORTS

Approved lenders must ensure appraisals are completed by a qualified appraiser that

is independent and objective. Approved lenders are responsible to review all appraisals

for integrity, accuracy, and thoroughness, prior to submission of a complete loan

application package to USDA. The lender may pass the cost of the appraisal on to the

borrower. The appraisal must have been completed within 180 days of loan closing.

Appraisals that are older than 180 days prior to loan closing are eligible for an appraisal

update as indicated in this Chapter.

A. Qualified Appraiser

Approved lenders must select qualified and competent appraisers that are properly

licensed or certified, as appropriate, in the State in which the property is located. The

appraiser must comply with the current edition of the Uniform Standards of Professional

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

(03-09-16) SPECIAL PN 12-7

Revised (04-01-24) PN 609

Appraisal Practice (USPAP). Lenders may verify that an appraiser is licensed or

certified by checking the Appraisal Subcommittee website found at: https://www.asc.gov

B. Appraisal Report

All appraisals must comply with the reporting requirements of USPAP available at

www.appraisalfoundation.org. All appraisal reports must meet the Uniform Appraisal

Dataset (UAD) requirements set forth by Fannie Mae and Freddie Mac. To read

definitions of condition and quality ratings, refer to the Fannie Mae and Freddie Mac

Uniform Appraisal Dataset Specification Version 3.6, located online at:

https://singlefamily.fanniemae.com/delivering/uniform-mortgage-data-program/uniform-

appraisal-dataset.

The appraiser will determine the appropriate appraisal form for the subject property.

Appraisers must utilize appraisal forms acceptable to Fannie Mae, Freddie Mac, HUD, or

VA. Applicable forms may include:

• Uniform Residential Appraisal Report (Fannie Mae Form 1004/Freddie Mac

Form 70) for one-unit single family dwellings;

• Manufactured Home Appraisal Report and addendum (Fannie Mae Form

1004C/Freddie Mac Form 70B) for all manufactured homes;

• Individual Condominium Unit Appraisal Report (Fannie Mae Form 1073/Freddie

Mac Form 465) for all individual condominium units.

Appraisal considerations:

• Appraiser/client confidentiality under USPAP Ethics Rules does not permit the

appraiser to discuss the appraisal with anyone other than the client, without the

client’s permission. It is recommended, but not required, that USDA/RD be

identified as an intended user with the lender in the appraisal report obtained.

• The market or sales comparison approach is required in all cases. No less than

three comparable sales will be used unless the appraiser provides documentation

that such comparable sales are not available. The appraiser must use their

knowledge of the area and apply good judgment in the selection of comparable

sales that are the best indicators of value for the subject property.

• The appraiser will determine if the cost approach is required. For example, the

property is unique, or has specialized improvements, or is new manufactured

housing, or if the client requests the cost approach to be completed, then the

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

12-8

appraiser will identify the source of the cost estimates and will comment on the

methodology used to estimate depreciation, effective age and remaining economic

life.

• The income approach is only required if the appraiser determines that it is

necessary to develop credible assignment results.

• An appraisal prepared for REO purposes, loan servicing consideration, or any

other purpose other than the guaranteed purchase or refinance transaction is

ineligible to be used in the origination of a guaranteed loan. A new appraisal with

the intent to arrive at an opinion of value for a purchase transaction must be

obtained.

Photographs. Photographs in the appraisal report must be in color and be clear and

descriptive to identify the property’s condition and quality. Photographs must clearly

represent the improvements, any physical deterioration of the property, amenities,

conditions and external influences that may have a material effect on the market value or

marketability of the subject property. Lenders will upload the appraisal report at the

Application Documents page in the Agency’s automated underwriting system, GUS, by

selecting 10002 Appraisal Report and uploading as an individual document. An appraisal

report with interior and exterior inspection of the subject property must include at least

the following:

• A front view of the subject property;

• A rear view of the subject property;

• A street scene identifying the location of the subject property and showing

neighboring improvements;

• The kitchen, main living area, bathrooms, bedrooms;

• Any other rooms representing overall condition, recent updates, such as

restoration, remodeling and renovation;

• Basements, including all finished and unfinished rooms

• Attic and/or crawl space when it can be safely accessed without disturbing or

moving items that obstruct access or visibility;

• Comparable sales, listings, and/or pending sales utilized in the valuation analysis

must include at least a front view of each comparable utilized;

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

(03-09-16) SPECIAL PN 12-9

Revised (04-01-24) PN 609

• The HUD Data Plate and the HUD Certification Label(s) for manufactured homes; and

• Condominium projects should include additional photographs of the common

areas and shared amenities.

Appraisal transfer. An appraisal ordered by another lender for the applicant can be

transferred to the lender who will complete the purchase transaction. The initial lender

must agree to the transfer of the report. A letter from the initial lender who ordered the

appraisal report must be retained in the permanent loan file as evidence the initial lender

transferred the report to the lender completing the purchase transaction. The receiving

lender must assume full responsibility for the integrity, accuracy and thoroughness of the

appraisal report, including the methods that the original lender used to acquire the

appraisal. The appraisal report must be no older than 180 days at loan closing to be valid.

Appraisal update. The validity period of an appraisal report can be extended only

one time with an Appraisal Update Report. The appraisal may be expired at the time the

appraisal update is requested. However, when the original appraisal is subsequently

updated, the appraisal is valid for no greater than one year from the effective date of the

original appraisal report at loan closing. The purpose of an appraisal update request is to

determine if the property has declined in value since the effective date of the original

appraisal. An update is not eligible to support a higher appraised value of the property.

USPAP considers the term “Appraisal Update” as a business term, but regardless of

the nomenclature used, when a client seeks a more current value or analysis of a property

that was the subject of a prior assignment, this is not an extension of that prior

assignment that was already completed; it is simply a new assignment. Refer to USPAP

Advisory Opinion 3 for additional clarification available at

www.appraisalfoundation.org.

USPAP (Advisory Opinion 3) states that there are three ways that the reporting

requirements can be satisfied for this type of assignment:

1. Provide a new report that contains all the necessary information/analysis to satisfy

the applicable reporting requirements, without incorporation of the prior report by

either attachment or reference.

2. Provide a new report that incorporates by attachment specified

information/analysis from the prior report so that, in combination, the attached

portions and the new information/analysis added satisfies the applicable reporting

requirements.

3. Provide a new report that incorporates by reference specified information/analysis

from the prior report so that, in combination, the referenced portions and the new

information/analysis added satisfies the applicable reporting requirements.

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

12-10

The appraiser may use a pre-printed form or a narrative report to provide the appraisal

update, but whichever reporting format is used, it must be in compliance with USPAP.

Fannie Mae Form 1004D/Freddie Mac Form 442, Appraisal Update and/or

Completion Report, may be utilized by the lender to report the completion of a repair

and/or satisfaction of requirements and conditions noted in the original appraisal report.

Property flipping. It remains the lenders responsibility to ensure any recently sold

property’s value is strongly supported when a significant increase between sales occur.

The lender must perform a thorough review of the appraisal report to validate and support

the property’s value and protect the applicants from possible predatory real estate

lending.

C. Agency Review

The Agency will review appraisals for all guarantee loan requests by completing

Form RD 1922-15, Administrative Appraisal Review. If the Agency reviewer detects

concerns, the appraisal will be referred to an Agency Review Appraiser for a technical

desk or technical field review. Should the Agency licensed appraisers determine the

appraisal is not adequate, the lender will be informed of corrections needed prior to

issuance of the conditional commitment for loan guarantee. The lender will be required to

correct or complete any appraisal returned by the Agency for corrective action. The

lender is responsible to communicate and initiate corrective action with the appraiser.

The corrected appraisal will be subject to the same review process described in this

section. The Agency retains the right to determine an appraiser is ineligible based upon

their failure to comply with requirements of this section. The Agency will notify the

lender when appraisals completed by ineligible appraisers will no longer be accepted for

the SFHGLP.

D. Directors of the Origination and Processing Division Responsibilities

A director of the Origination and Processing Division (OPD) will designate or

delegate authority to the supervisory staff of the unit or other qualified personnel to

conduct administrative appraisal reviews. Technical appraisal reviews must be completed

by an Agency certified or licensed appraiser and need only be licensed or certified in one

State or territory to perform real estate appraisal duties as Federal employees in all states

and territories. Review appraisers must have recent, documented appraisal experience or

other factors which clearly establish their qualifications as a reviewer.

A director of the OPD will determine and establish the training needs for Rural

Development OPD staff completing appraisal reviews. A director of the OPD will also

assure that an adequate number of reviews are being completed.

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

(03-09-16) SPECIAL PN 12-11

Revised (04-01-24) PN 609

E. Types of Agency Reviews

There are three types of reviews for appraisals; “Administrative,” “Technical Desk”

and “Technical Field.” An administrative review will be completed for all transactions

involving the submittal of an appraisal report. A sufficient number of technical desk and

technical field reviews will be completed to ensure the Agency is getting quality

appraisals for the Guaranteed Loan Program. An explanation of the review types are as

follows:

1. Administrative Reviews

Administrative reviews are performed by the Agency loan approval official or

qualified designee on all appraisals prior to issuance of the Conditional Commitment.

This review determines if there are inconsistencies in the appraisal report that may

have to be addressed, or if a technical review should be completed by the Agency

staff appraiser prior to issuance of the Loan Note Guarantee. Indicators that a

technical review may be required will be documented on Form RD 1922-15.

• Administrative reviews are completed by the Agency on Form RD 1922-15.

This form will be signed, dated, and retained in the Agency file for uploading.

This review should be completed prior to issuance of the Conditional

Commitment.

• If there is a deficiency with an appraisal, the loan approval official should

communicate the deficiency to the lender. These deficiencies should include

items that affect loan security, value conclusions, or unacceptable property

conditions.

2. Technical Desk Reviews

A technical desk review is performed to determine whether the appraisal was

complete, was clearly reasoned, and had adequate support for the conclusion of value.

Technical reviews are performed by the Agency Appraiser. Technical reviews

completed by Agency appraisers must follow current USPAP.

• Technical desk reviews may be documented in any format that complies with

USPAP and is acceptable for use by RD. Technical reviews should be selected

in a random method. The percent of files randomly selected will be set by the

direction of the SFHGLD.

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

12-12

A director of the OPD, the Quality Assurance and Lender Oversight Division, or

designated supervisory staff, will coordinate with Program Support Staff (PSS) in

National Headquarters to establish internal management controls and systems to

document and substantiate residential appraisal compliance activities, which will be

evaluated during Internal Control Reviews, Single Family Housing program reviews,

and other similar types of reviews. Technical desk reviews of appraisals received by

the Agency provide a method of internal control by the appraisal review staff and

ensure that appraisals received by the Agency are in compliance with USPAP and

Agency regulations. A Director of the OPD, or designated supervisory staff, will

support completion of technical desk reviews in coordination with PSS to achieve the

appraisal quality control requirements of the Agency.

A technical review may also be requested by OPD staff when problems are

detected on the administrative review that cannot or will not be addressed by the

submitting lender or original appraiser. These problems must be significant and

result in an appraisal which does not support the value conclusion. OPD staff will

document the nature of their concerns on Form RD 1922-15. The appraisal will then

be forwarded to the Appraisal Services Branch for a technical and/or field review

prior to approval of the loan.

3. Technical Field Reviews

Field reviews will involve on-site visits to the subject property and the

comparable properties used in the report. Field reviews are completed by Agency

Appraisal staff on a random, spot-check basis to determine if the appraiser has

followed accepted appraisal techniques and arrived at a logical conclusion.

• USPAP Standard 3 Review is used for technical field reviews. The reviewer

may use any reporting format that complies with USPAP and is acceptable for

use by RD. A director of the OPD, or designated supervisory staff, and the

appraisal review staff are responsible for the administration of residential

appraisal compliance and training. Appropriate actions will be initiated by a

director of the OPD, or designated supervisory staff, and appraisal review

staff to ensure compliance with USPAP and SFHGLP policies governing the

residential appraisal process.

F. Appraisals in Remote Rural Areas, on Tribal Lands, or in Areas Lacking

Market Activity

In remote, rural areas, on Tribal lands, or areas with a lack of market activity, as

identified by the agency, it may be difficult to obtain adequate comparable sales to

appraise a property. When the sales comparison approach cannot be developed for a

credible opinion or conclusions regarding value, the lender’s appraiser may use other

HB-1-3555

Paragraph 12.5 Residential Appraisal Reports

(03-09-16) SPECIAL PN 12-13

Revised (04-01-24) PN 609

methods in compliance with the Uniform Standards of Professional Appraisal Practice

(USPAP) and perform an appraisal without completing the sales comparison approach to

value. Appraisers must explain the exclusion of the sales comparison approach to value

and document their efforts to obtain comparable market data along with an explanation

for any sales data not used. The primary method that the appraiser is relying on should

be summarized to the extent that the user or a review appraiser can understand the

reasoning and support of the valuation and conclusions.

Remote rural areas are identified by the agency and are defined as areas with all the

following characteristics:

• Scattered population;

• Low density of residences;

• Lack of basic shopping facilities;

• Lack of community and public services and facilities; and

• Lack of comparable sales data.

If the appraiser is using the cost approach, external depreciation based on the

remoteness of the site must not be considered; however, factors that impact the site such

as immediate proximity to a feedlot, factory, or other similar considerations should be

included. If the appraiser is using the income approach, they must explain why the

income and expenses used are comparable to the subject property. When a market is

established in these areas, the Agency will again require the sales comparison approach to

be used.

12.6 WATER AND WASTEWATER DISPOSAL SYSTEMS [7 CFR 3555.201]

The site must have acceptable water and wastewater disposal systems to ensure the

property is decent, safe, sanitary, and meets community standards. Public water and

wastewater disposal systems are presumed to meet state and local requirements with no

additional documentation or inspections. Private well and wastewater systems that meet

the requirements in HUD Handbook 4000.1 or meet the requirements of local and/or state

health authority do not require additional inspections other than water purity tests as

discussed in this section. Evidence will be retained in the lender’s permanent loan file.

A. Water

Water systems, for existing or new construction, that require continuous or repetitive

HB-1-3555

Paragraph 12.6 Water and Wastewater Disposal Systems

12-14

treatment to be safe bacterially or chemically may be used if the individual water system,

with purification, meets the requirements of the state department of health or other

comparable reviewing and regulatory authority.

1. Individual Privately Owned

• Individual water systems are owned and maintained by the homeowner and

subject to compliance with all requirements of the local and/or State Health

Authority codes. Water quality tests are required as follows:

o The water quality of the well must meet the requirements of the state or

local authority. If the state or local authority does not have specific

requirements, the maximum contaminant levels established by the

Environmental Protection Agency (EPA) will apply.

o The local health authority or a state certified laboratory must perform a

water quality analysis. The Safe Water Drinking Act does not apply to

private wells. Contact the EPA’s Safe Drinking Water Hotline at (800)

426-4791 for referral to certified labs and other inquiries.

o The water analysis report must be no greater than 180 days old at loan

closing. If the Agency is aware of any recent environmental impacts that

may render the previous analysis invalid (for example – chemical spills,

natural disasters, etc.) a new report may be required.

• The well location for individual water supply systems must be measured to

establish the distance from the septic system. The separation distance between

the well and septic systems must meet the SF Handbook (HUD Handbook

4000.1) or be found acceptable by the Local and/or State Health Authority.

• Individual water systems/wells should be located on the subject property site.

If located on an adjacent property, evidence of water rights and recorded

maintenance agreement must be retained in the lender’s permanent loan file as

acceptance of the well as the primary source of water.

2. Individual Privately Owned Shared

If the property is served by a shared well or off-site facility, the lender must

ensure the private system will provide a continuous and adequate supply of safe and

potable water. The following requirements must also be met:

HB-1-3555

Paragraph 12.6 Water and Wastewater Disposal Systems

(03-09-16) SPECIAL PN 12-15

Revised (04-01-24) PN 609

•

The well serves properties that cannot feasibly be connected to an acceptable

public or community water supply system. It is the lender’s responsibility to

make this determination.

•

A shared well must have a valve on each dwelling.

•

The water supply is adequate for all families served. A shared well must

service no more than four living units or properties unless approved and

enforced by the local code authority.

• The water quality of the well must meet the requirements of the state or local

authority. If the state or local authority does not have specific requirements,

the maximum contaminant levels established by the Environmental Protection

Agency (EPA) will apply.

•

The well must have an agreement that meets the following requirements:

o Is binding upon all signatory parties and their successors in title;

o Is recorded or will be recorded no later than the closing date; and

o Makes provisions for maintenance and repair of the system and the

sharing of costs to do so. These provisions must include a permanent

easement that allows access for maintenance and repair.

3. Community Owned

If the property is served by a community water system operated by a private

corporation or nonprofit property owner’s association, the lender must ensure the

following conditions are met:

• The system and the water supply meet all applicable federal, state and local

requirements.

• The system has the capacity to provide a sufficient water supply during

periods of peak demand.

• The system is operated under a legally binding agreement that allows

interested third parties to enforce the obligation of the operator to provide

satisfactory service.

HB-1-3555

Paragraph 12.6 Water and Wastewater Disposal Systems

12-16

4. Required Inspections and Documentation

The lender must obtain documentation the water quality meets state and local

standards as discussed in this section. Lenders will retain all documentation in their

permanent loan file. Inspection and documentation requirements are discussed later in

this chapter.

5. Individual Water Systems in Hawaii and the Western Pacific Region

Due to the limited regulation provided by local ordinances and/or regulations of

each jurisdiction in Hawaii and the Western Pacific Region regarding individual

water systems (IWS), including rainwater catchment systems, the Agency has

determined that an IWS is considered an eligible water system if the following

conditions are met:

• The property is located in Hawaii or the Western Pacific Region;

• Property does not have an available affordable connection to a public or

private community water system;

• The alternative water supply system, rainwater catchment system, complies

with and/or is not prohibited by ordinances and/or regulations of the local

jurisdiction in which the property is located;

• Water quality tests are not required if the state or local authority does not have

specific requirements and EPA testing is not available;

• Reliance upon the rainwater catchment system, does not diminish the

marketability or value of the property within its marketplace. The system must

be typical for the area as described by the appraiser; and

• The applicant is required to acknowledge and certify of their responsibility to

maintain the rain catchment system.

HB-1-3555

Paragraph 12.6 Water and Wastewater Disposal Systems

(03-09-16) SPECIAL PN 12-17

Revised (04-01-24) PN 609

B. Wastewater

1. Individual Privately Owned

The lender is required to obtain a septic evaluation. A qualified appraiser who

certifies the property meets required HUD’s Single-Family Housing Policy

Handbook, a government health authority, a licensed septic system professional, or a

qualified home inspector may perform the septic evaluation. The septic evaluation

may require additional inspections as a result of the inspection. The septic system

must be free of observable evidence of failure.

Existing dwellings appraised by a qualified appraiser, who indicates the dwelling

meets the required HUD handbook policy does not require further septic certification;

however, water supply systems must be measured to establish the distance from the

septic system. The separation distance between the well and septic systems must meet

the SF Handbook (HUD Handbook 4000.1) or be found acceptable by the local

and/or State Health Authority.

If the property is served by an individual sewage disposal system, the lender must

ensure the system:

•

Meets any applicable requirements of the state or local health authority with

jurisdiction;

•

Is located entirely on the subject property. If any part of the system is located

on an adjacent property (for example leach lines), evidence such as a

perpetual encroachment easement must be recorded to establish the rights of

the property owner’s permitted use; and

•

Is operating properly and has the capacity to dispose of all domestic wastes in

a manner that will not create a nuisance or endanger public health.

2. Community Owned

If the property is served by a community wastewater system operated by a private

corporation or nonprofit property owner’s association, the lender must ensure that the

system:

•

Meets any applicable requirements of the state or local health authority with

HB-1-3555

Paragraph 12.6 Water and Wastewater Disposal Systems

12-18

jurisdiction;

•

Is licensed, operating properly and has the capacity to dispose of all domestic

wastes in a manner that will not create a nuisance or endanger public health;

and

•

Is subject to a legally binding agreement that allows interested third parties to

enforce the obligation of the operator to provide satisfactory service.

3. Required Inspections and Documentation

The lender must obtain documentation the wastewater system meets state and/or

local standards. Lenders will retain all documentation in their permanent loan file.

Inspection and documentation requirements are discussed later in this chapter.

12.7 STREET ACCESS AND ROAD MAINTENANCE [7 CFR 3555.201]

A. Access

The site must be contiguous to, and have direct access from, a public or private street,

road, or driveway. Private roads or streets are acceptable provided each property has

vehicular or pedestrian access. Private roads or streets must be protected by permanent

recorded easement (non-exclusive and non-revocable easement without trespass from the

property to a public street) or the street must be maintained by a homeowner’s association

(HOA). Shared driveways must also meet these requirements requiring a permanent

recorded easement for ingress and egress. This agreement must be binding to successors

and title. A copy of a title report, retained in the lender’s loan file, may be used to

evidence the easement. Private streets must have a permanently recorded easement or be

owned and maintained by a HOA. All evidence of recorded easements or maintenance

agreements must be reviewed and approved by the approved lender’s underwriter and

documented in the lender’s permanent loan file.

B. Maintenance

Streets and roads must be hard surfaced or all-weather surfaced. An all-weather

surface is a road surface over which emergency and the area’s typical passenger vehicles

can always pass. A publicly maintained road is automatically assumed to meet this

requirement. If a HOA is responsible for maintaining streets and roads, it must meet the

criteria set forth by Fannie Mae, Freddie Mac, the U.S. Department of Housing and

Urban Development (HUD), or U.S. Department of Veterans Affairs (VA).

HB-1-3555

(03-09-16) SPECIAL PN 12-19

Revised (04-01-24) PN 609

SECTION 3: DWELLING REQUIREMENTS [7 CFR 3555.202]

12.8 MODEST HOUSING

There are no maximum mortgage limits for properties financed under the SFHGLP.

Modest housing is defined as a new or existing dwelling that a low- or moderate-income

borrower can afford based on their repayment ability. The property must not be primarily

designed for income producing activity.

12.9 EXISTING AND NEW DWELLINGS

A. Existing Dwellings [7 CFR 3555.202(b)]

The objective of the SFHGLP is to assist eligible rural households in obtaining an

adequate, safe, and sanitary single-family home. Information regarding financing

existing manufactured and modular homes may be found in Chapter 13 of this Handbook.

An existing dwelling may be attached, detached or semi-detached dwellings and must

be inspected to determine the dwelling meets the current minimum property requirements

of the Single Family Housing Policy Handbook (SF Handbook; HUD Handbook 4000.1,

also known as HUD Handbook) or as superseded by HUD. An existing dwelling is

defined as been completed for more than 12 months or has been completed less than 12

months but has been previously occupied.

Qualified appraisers are licensed or certified and can attest the property meets HUD

Handbook standards. It remains the lenders responsibility to determine if the appraiser is

thoroughly familiar with the HUD Handbook. The appraiser may certify the requirements

of the HUD Handbook have been met on page three of the appraisal form in the

“comment” section, or in an addendum to the appraisal.

Appraisers who are unfamiliar with the HUD Handbook standards should not certify

that a property meets those standards and doing so constitutes a misrepresentation. If the

qualified appraiser is unfamiliar with the HUD Handbook standards, the lender should

obtain a home inspection report provided by a home inspector deemed qualified by the

lender. Regardless of whether the appraisal is performed by a qualified appraiser or not,

the appraiser must report all readily observable property deficiencies as well as any

adverse conditions discovered performing the research involved in completing the

appraisal.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-20

Required repairs under the noted handbooks are limited to those repairs necessary to

preserve the continued marketability of the property and to protect the health and safety

of the occupants. A property in which a qualified appraiser indicates is in average or

good condition may be considered in good repair, though repairs may still be required

by the lender. Lenders are responsible for ensuring the following guidelines are met:

• Lenders must encourage applicants to obtain a detailed home inspection of the

property independent of the inspection noted above.

• All repair items required by the appraiser or underwriter must be inspected and

the clearance documented and retained in the lender’s permanent loan file. As

stated in the HUD Handbook, the responsibility for enforcing code rests with the

local municipalities.

• Termite/pest inspections are required if the lender, appraiser, inspector, or State

law requires the inspection to confirm the property is free of active infestation.

• Lenders are not required to collect an inspection report to confirm thermal

standards for existing dwellings.

• Lenders must provide applicants with Form HUD-92564-CN, For Your

Protection: Get a Home Inspection, with evidence maintained in the lender’s

permanent loan file.

Lenders are responsible to determine if any repairs will be required to meet HUD

Handbook standards. Lenders are reminded they are responsible for the acts of their

agents, including appraisers. When lending to low- and moderate-income borrowers

under the SFHGLP, lenders are expected to use professional judgment and rely upon

prudent underwriting practices in determining when a property condition requires

additional inspections or repairs.

Conditions that would warrant additional repairs include those that pose a threat to

the safety of the occupants, jeopardize the soundness and structural integrity of the

property, or adversely affect the likelihood of a low- or moderate-income borrower from

becoming a successful homeowner.

HUD Handbooks and forms are located at:

https://hud.gov/program_offices/administration/handbks_forms

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

(03-09-16) SPECIAL PN 12-21

Revised (04-01-24) PN 609

B. New Dwellings [7 CFR 3555.202(a)]

New dwellings must be designed and constructed in accordance with certified plans

and specifications. Evidence of all of the items below must be retained in the lender’s

permanent loan file:

• Certified plans and specifications

• Required construction inspections

• Thermal standards are met

Certifications may be accepted from individuals or organizations trained and

experienced in the compliance, interpretation, or enforcement of the applicable

development standards for drawings and specifications. One year builder warranties are

deemed acceptable to the Agency when the policy is non-refundable or cancellable, the

policy is from an insurance company licensed to do business in the state where the

property is located, and the coverage includes (from effective date) at least one year for

any defects caused by faulty workmanship or defective materials. This section will

provide documentation options necessary to meet each of these requirements for both

stick built and manufactured homes.

Information regarding financing new manufactured and modular homes may be found

in Chapter 13 of this Handbook.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-22

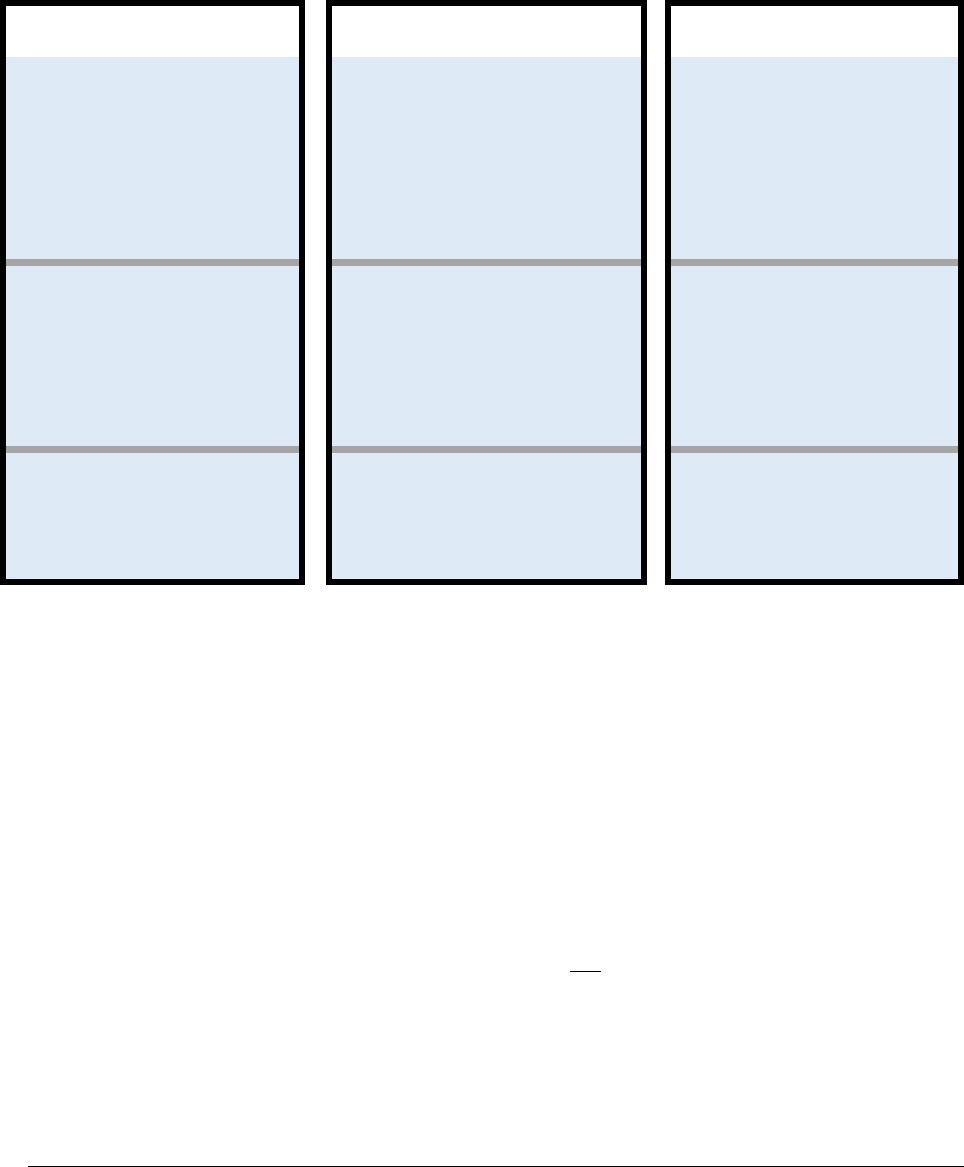

1. Documentation Requirements for New Construction Stick Built Homes:

Evidence of

Certified Plans and Specs

Evidence of

Construction Inspections

Evidence of

Thermal Standards

OPTION 1

Copy of the certification from

a qualified individual or

organization that the reviewed

documents comply with

applicable development

standards; OR

OPTION 1

Certificate of Occupancy issued

by a local jurisdiction showing

that it has performed at least the

3 construction phase inspections,

as identified in Section 12.9(B),

and an acceptable 1 year builder

warranty; OR

OPTION 1

A qualified, registered

architect or a qualified,

registered engineer may

certify confirmation with

IECC standards;

OR

OPTION 2

Certificate of Occupancy

issued by a local jurisdiction;

OR

OPTION 2

Three construction phase

inspections performed at each of

the phases identified in Section

12.9(B), and an acceptable 1

year builder warranty;

OR

OPTION 2

Builder may certify

confirmation with the IECC

standards;

OR

OPTION 3

Building Permit (or equivalent)

issued by local jurisdiction.

OPTION 3

Final inspection and a 10-year

insured builder warranty. Builder

backed 2/10 warranty fulfills the

10-year warranty requirement.

OPTION 3

The final inspection,

or Certificate of

Occupancy issued by

a local jurisdiction.

The lender is responsible for obtaining one form of required evidence from the list of

available source options in each category. This evidence must be kept in the lender's permanent

loan file.

New Construction Certified Plans and Specifications for Stick Built Homes

The lender’s file must contain evidence the plans and specifications comply with all

development standards* applicable to the new construction. Acceptable evidence

includes:

1. Copy of the certification from a qualified individual or organization that the

reviewed documents comply with applicable development standards. Form RD

1924-25 is an acceptable format but may not be required by the Agency for

guaranteed loans.

-OR-

2. Certificate of Occupancy issued by a local jurisdiction.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

(03-09-16) SPECIAL PN 12-23

Revised (04-01-24) PN 609

-OR-

3. Building Permit (or equivalent) issued by local jurisdiction.

The lender may accept certifications from individuals or organizations trained and

experienced in the compliance, interpretation or enforcement of the applicable

development standards* for drawings and specifications. Plan certifiers may be any of

the following:

• Licensed architects;

• Professional engineers;

• Plan reviewers certified by a national model code organization;

• Local building officials authorized to review and approve building plans and

specifications; or

• National codes organizations.

*Applicable development standards. The current International Code Council (ICC)

standards or current state adopted ICC code(s) for residential construction.

Evidence of Construction Inspections for Stick Built Homes

The lender’s file must contain copies of the documents described in one of the

following three options:

1. Certificate of Occupancy issued by a local jurisdiction showing that it has

performed at least 3 construction phase inspections, including inspections noted in

option 2 below and a 1-year builder warranty plan acceptable to Rural

Development.

-OR-

2. Three construction inspections performed when:

•

Footings and foundation are ready to be poured and prior to back-filling;

•

Shell is complete, but plumbing, electrical and mechanical work is still

exposed;

•

Final inspection of completed work prior to occupancy; and

•

A 1-year builder warranty plan acceptable to Rural Development. Builders

may utilize their own warranty form, HUD-92544 or Form RD 1924-19.

Applicants who build their own homes cannot provide a self-warranty.

-OR-

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-24

3. Final inspection and a 10-year insured builder warranty.

• Final Update and/or Completion Report (Fannie Mae Form 1004D/Freddie

Mac Form 442) is acceptable as a final inspection, provided the appraiser is

deemed qualified by the lender.

• Builder backed 2/10 warranty fulfills the 10-year warranty requirement.

Evidence of Thermal Standards for New Construction Stick Built Homes

The lender’s file must contain evidence thermal standards meet or exceed the

International Energy Conservation Code (IECC) in effect at the time of construction.

Evidence of thermal standards are typically included in the plans and specs to which the

dwelling is built.

Documentation of conformance may be met by one of the following options:

1. A qualified, registered architect or a qualified, registered engineer may certify

confirmation with IECC standards; or

2. The builder may certify confirmation with the IECC standards; or

3. The final inspection or Certificate of Occupancy issued by a local jurisdiction

meets this requirement.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

(03-09-16) SPECIAL PN 12-25

Revised (04-01-24) PN 609

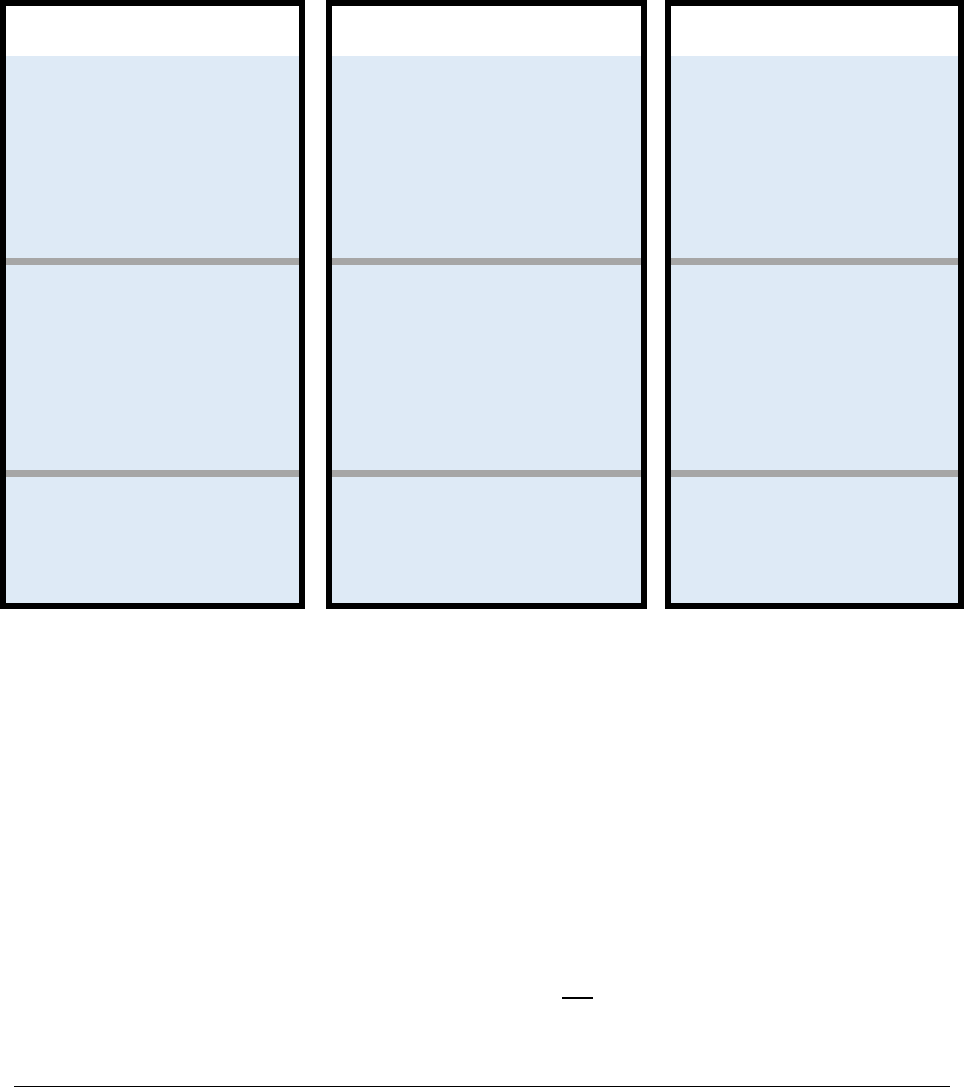

2. Documentation Requirements for New Construction Manufactured Homes:

Evidence of

Certified Plans and Specs

Evidence of

Construction Inspections

Evidence of

Thermal Standards

OPTION 1

Copy of the certification from

a qualified individual or

organization that the reviewed

documents comply with

applicable development

standards; OR

OPTION 1

Certificate of Occupancy issued

by a local jurisdiction showing

that it has performed at least the

footing and final inspections, as

identified in Section 12.9(B),

and an acceptable 1 year builder

warranty; OR

OPTION 1

HUD Data Plate confirmation

with IECC standards;

OR

OPTION 2

Certificate of Occupancy

issued by a local jurisdiction;

OR

OPTION 2

Footing and final inspections

performed by a qualified

inspector as identified in Section

12.9(B), and an acceptable 1

year

builder warranty;

OR

OPTION 2

Builder may certify

confirmation with the IECC

standards;

OR

OPTION 3

Building Permit (or equivalent)

issued by local jurisdiction.

OPTION 3

Final inspection and a 10-year

insured builder warranty. Builder

backed 2/10 warranty fulfills the

10-year warranty requirement.

OPTION 3

The final inspection, or

Certificate of Occupancy

issued by a local jurisdiction.

The lender is responsible for obtaining one form of required evidence from the list of

available source options in each category. This evidence must be kept in the lender's permanent

loan file. Warranty documents for manufactured homes must include the serial number.

New Construction Certified Plans and Specifications for Manufactured Homes

The lender’s file must contain evidence the plans and specifications comply with all

development standards* applicable to the new construction. Acceptable evidence

includes:

1. Copy of the certification from a qualified individual or organization that the

reviewed documents comply with applicable development standards. Form RD

1924-25 is an acceptable format but may not be required by the Agency for

guaranteed loans.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-26

-OR-

2. Certificate of Occupancy issued by a local jurisdiction.

-OR-

3. Building Permit (or equivalent) issued by local jurisdiction.

The lender may accept certifications from individuals or organizations trained and

experienced in the compliance, interpretation or enforcement of the applicable

development standards* for drawings and specifications. Plan certifiers may be any of

the following:

1. Licensed architects;

2. Professional engineers;

3. Plan reviewers certified by a national model code organization;

4. Local building officials authorized to review and approve building plans and

specifications; or

5. National codes organizations.

*Applicable development standards. The current International Code Council (ICC)

standards or current state adopted ICC code(s) for residential construction.

Evidence of Construction Inspections for Manufactured Homes

The lender’s file must contain copies of the documents described in one of the

following three options:

1. Certificate of Occupancy issued by a local jurisdiction showing that it has

performed at least 2 construction phase inspections, which must include the

inspections noted in option 2 below and a 1-year builder warranty plan

acceptable to Rural Development.

-OR-

2. Two construction inspections performed when:

•

Footings and foundation are ready to be poured and prior to back-filling;

•

Final inspection of completed work prior to occupancy; and

•

A 1-year builder warranty plan acceptable to Rural Development. Builders

may utilize their own warranty form, HUD-92544 or Form RD 1924-19.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

(03-09-16) SPECIAL PN 12-27

Revised (04-01-24) PN 609

Applicants who build their own homes cannot provide a self-warranty.

-OR-

3. Final inspection and a 10-year insured builder warranty.

• Final Update and/or Completion Report (Fannie Mae Form 1004D/Freddie

Mac Form 442) is acceptable as a final inspection, provided the appraiser is

deemed qualified by the lender.

• Builder backed 2/10 warranty fulfills the 10-year warranty requirement.

Evidence of Thermal Standards for New Construction Manufactured Homes

The lender’s file must contain evidence thermal standards meet or exceed the

International Energy Conservation Code (IECC) in effect at the time of construction.

Evidence of thermal standards are typically included in the plans and specs to which the

dwelling is built.

Documentation of conformance may be met by one of the following options:

1. A HUD Data Plate confirmation with IECC standards; or

2. The builder may certify confirmation with the IECC standards; or

3. The final inspection or Certificate of Occupancy issued by a local jurisdiction

meets this requirement.

In general, the lender has primary responsibility for all loan origination activities. The

Agency has primary responsibility to review lenders’ actions and monitor participants’

compliance with program requirements. The Agency will not require the lender to

routinely submit documentation maintained in the lender’s file regarding new

construction that is not required to be submitted under program guidelines, such as:

• Copies of plans, drawings, and specifications;

• Certifications regarding the plans, drawings, and specifications. Although lenders

may voluntarily elect to use Form RD 1924-25, this form is not a required form

for the SFHGLP. The certification may be on the plans and drawings, a separate

form, or on any document that conveys the necessary information;

• Building permits;

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-28

• Copies of new construction inspections, including pest and termite inspections

that the lender may opt to collect as part of state laws or investor requirements;

• Occupancy certificates; and

• Copies of construction warranties.

The Agency has the option to request any of these documents in appropriate

situations such as:

• The Agency is performing a processing review of a newly approved lender;

• The Agency is performing a periodic review of the lender’s compliance with

program regulations;

• The Agency believes the lender is not fulfilling the obligations of the Lender

Agreement and/or program guidelines; or

• The Agency is reviewing a loss claim.

New home purchase transactions that cannot meet the minimum required plan

certification, inspections, and warranty document requirements outlined in this paragraph

are limited to a 90 percent loan to value (LTV). The lender may loan the one-time upfront

guarantee fee in addition to the limiting 90 percent LTV.

C. Repair Escrows for Existing and New Dwellings, Post Issuance of the Loan Note

Guarantee [7 CFR 3555.202(c)]

Repair escrows, post issuance of the Loan Note Guarantee, are acceptable provided

the home is habitable, as determined by the lender. All items of new construction or

repairs must be 100 percent (100%) complete in accordance with plans and

specifications, except for minor items not affecting the livability of the structure or that

cannot be completed due to weather conditions. This section does not apply to the Single

Close Combination Construction to Permanent Loans or Rehabilitation or Repair Loans.

The lender assumes responsibility for completion of repairs in accordance with the

conditions set forth in this Section for any repair escrow established. Lenders may utilize

Attachment 12-E, Repair Escrow and Rehabilitation & Repair with Purchase

Comparison, when determining how repairs or rehabilitation may be financed.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

(03-09-16) SPECIAL PN 12-29

Revised (04-01-24) PN 609

Repair items will be required to be completed within 180 days of loan closing. This

period may be extended, at the discretion of the Agency, for homes that need exterior

repairs but are in an area experiencing inclement weather conditions. The maximum

exterior repair escrow period when an extension is granted is limited to 240 days.

Extensions may be granted beyond 180 days for exterior escrows only.

The Agency may issue a Loan Note Guarantee prior to the completion of interior or

exterior repairs provided all the following conditions are met:

•

The incomplete work does not affect the livability of the dwelling, nor the health

or safety of the occupants;

•

A signed contract between the borrower and the contractor is in effect for the

proposed work;

•

The funds to be escrowed are not less than 100 percent of the repair cost contract.

The loan underwriter may determine the escrow amount, which could exceed the

repair cost;

•

The Closing Disclosure reflects the holdback;

•

The development will be complete within 180 days of closing, unless an

extension is granted by the Agency for inclement weather conditions;

•

The escrow account is established in a federally supervised financial institution;

and

•

An inspection report certifying the defect/repair has been properly repaired.

Certification of completion is required to verify the work was completed and

must:

o Be completed by the appraiser;

o State that the improvements were completed in accordance with the

requirements and conditions in the original appraisal report;

o Be accompanied by photographs of the completed improvements; and

o The individual performing the final inspection of the property must sign the

completion report.

HB-1-3555

Paragraph 12.9 Existing and New Dwellings

12-30

The lender is responsible for monitoring the completion of the work and the release of

funds to pay for the work. All documentation supporting the development and

confirmation of the completion will be retained in the lender’s permanent loan file and is

subject to the certification of Form RD 3555-18/18E. Funds that remain in the escrow

account, after the completion of all required repairs, must be utilized for an eligible loan

purpose or applied to the principal balance of the permanent loan. Personal funds of the

borrower utilized to fund the repair escrow (excluding loan funds or a seller concession)

may be returned to the borrower. A seller’s personal funds utilized to fund the repair

escrow (excluding a seller concession as part of the sales contract) may be returned to the

seller.

Escrow completion for interior or exterior repairs on an existing dwelling – without

the assistance of a contractor

When a borrower will complete the planned interior or exterior development on an

existing dwelling without the services of a contractor, the requirement for an executed

contract noted in this section is waived when these three conditions are met:

• The estimated cost to complete the work is not greater than 10 percent of the total

loan amount;

• The escrow amount is less than or equal to $10,000; and

• The lender has determined the borrower has the knowledge, skills and time

necessary to complete the work within the maximum 180-day limit.

All remaining requirements as noted at Paragraph 12.9 C are applicable. The lender is

responsible for monitoring the completion of the work and the release of funds for

payment of the work. All documentation supporting the planned development and

completion will be retained in the lender’s permanent loan file and is subject to the

certification of Form RD 3555-18/18E. Funds remaining in the escrow account upon

completion of the work, that are representative of loan funds or a seller concession, as

part of the sales contract, will be used to reduce the unpaid principal balance of the

mortgage or utilized for an eligible loan purpose. Personal funds of the borrower utilized

to fund the repair escrow (excluding loan funds or a seller concession) may be returned to

the borrower. A seller’s personal funds utilized to fund the repair escrow (excluding a

seller concession as part of the sales contract) may be returned to the seller.

HB-1-3555

(03-09-16) SPECIAL PN 12-31

Revised (04-01-24) PN 609

SECTION 4: ENVIRONMENTAL REQUIREMENTS [7 CFR 3555.5]

12.10 HAZARD IDENTIFICATION

A. Due Diligence

Lenders are required to utilize due diligence regarding potential environmental

hazards to ensure the property is safe, sanitary, and has sufficient value to adequately

secure the loan. The property must be free to the maximum extent possible of any known

hazards that may have adverse effects on the health and safety of the occupants. The

structural soundness of the dwelling must ensure customary use and enjoyment of the

property by the occupants. While the Agency does not specify how the lender’s due

diligence must be conducted, the level of review must be equivalent to the standards

established by Fannie Mae, Freddie Mac, the Federal Housing Authority (FHA), or the

United States Veterans Administration (VA).

Appraisers play an important role in identifying potential environmental hazards by

notifying the lender of concerns identified during their visit to the property. The appraiser

is required to note readily observable conditions. If the lender knows or is informed by

another party of a potential hazard, the information must be disclosed to the appraiser.

Lenders must follow up on all potential environmental hazards identified by an appraiser

to determine the nature and scope of the problem, and the impact the problem is likely to

have on the property’s value. If potential environmental hazards are noted, the lender

must carefully document the suspected problem and the findings of its investigation.

If the lender’s investigation reveals an environmental hazard does exist, the lender

must ensure the hazard is mitigated before requesting the loan guarantee.

B. Flood Hazards

The lender must complete, or arrange for a contractor to complete, FEMA Form FF-

206-FY-21-116, Standard Flood Hazard Determination Form (SFHDF), to determine

whether the dwelling is in a Special Flood Hazard Area (SFHA) in accordance with the

National Flood Insurance Reform Act of 1994.

Existing dwellings located in a SFHA are eligible for the SFHGLP when flood

insurance through FEMA’s National Flood Insurance Program (NFIP) is available for the

community and flood insurance, whether NFIP, “write your own,” or private flood

insurance, is purchased by the borrower. Lenders are required to accept private flood

insurance policies that meet the requirements of 42 U.S.C. 4012a (b)(1)(A) and remain

responsible for ensuring private policies continue to meet this requirement. Insurance

HB-1-3555

Paragraph 12.10 Hazard Identification

12-32

must be obtained as a condition of closing and maintained for the life of the loan for

existing residential structures when any portion of the structure is determined to be in a

SFHA, including decks, carports, etc. However, according to the Homeowner Flood

Insurance Affordability Act (HFIAA) of 2014, flood insurance is not required for any

additional structures that are located on the property but are detached from the primary

residential structure and do not serve as a residence, such as sheds, garages, or other

ancillary structures. Existing dwellings financed through the SFHGLP are not subject to

the requirement within RD Instruction 1970, Subpart F, which requires a search for

practicable off-site alternatives to purchasing an existing dwelling within the SFHA.

New or proposed construction in an SFHA is ineligible for a loan guarantee unless:

•

A final Letter of Map Amendment (LOMA) or final Letter of Map Revision

(LOMR) that removes the property from the SFHA is obtained from FEMA;

•

The lender obtains a FEMA National Flood Insurance Program Elevation

Certificate (FEMA Form FF-206-FY-22-152). The flood elevation certificate

must document that the lowest floor (including the basement) of the residential

building, and all related improvements/equipment essential to the value of the

property, are built at or above the 100-year flood elevation in compliance with

National Flood Insurance Program (NFIP) criteria. The flood elevation certificate

must be prepared by a licensed engineer or surveyor; or

• Documentation is included in the file in accordance with RD Instruction 1970

Subpart F, that there is a demonstrated need for the SFHGLP and there are no

practicable alternatives to new construction within the SFHA that are acceptable

to the applicant(s). Examples include but are not limited to the following: the

entire community is located within the SFHA, there are no comparable homes to

the proposed new dwelling, the existing housing stock is unacceptable to the

applicant, etc.

Note: Part of the site may be in the SFHA without triggering these requirements if no

part of the dwelling is in the SFHA. At the lender’s discretion they may require flood

insurance even if the residential building and related improvements to the property are

not located within the SFHA, but the lender has reason to believe that the building and

related improvements to the property may be vulnerable to damage from flooding.

Existing dwellings and newly constructed dwellings located within the SFHA which

are not served by public sewer systems and have on-site septic or sewage treatment

systems must have a drinking water supply which is protected from cross contamination

from the onsite septic/sewage treatment during flooding. A property serviced by an on-

site septic or sewage treatment system is eligible under this Section, provided one of the

following can be met:

HB-1-3555

Paragraph 12.10 Hazard Identification

(03-09-16) SPECIAL PN 12-33

Revised (04-01-24) PN 609

•

The property is served by a publicly provided water supply.

•

The property is serviced by a private drinking water well/supply with a fitted

sanitary well cap which prevents backflow floodwater from entering the drinking

supply well.

•

The property is served by a private drinking water well/supply whose opening is

located above the base flood elevation of the SFHA. Additional documentation,

such as an elevation certificate, will be required to verify this type of property.

Flood insurance is not required for properties located in unmapped communities.

Since these are often newly developed areas where the potential for flooding is unknown,

lenders have the discretion to require flood coverage as a condition of the loan.

SECTION 5: CONDOMINIUMS [7 CFR 3555.205]

12.11 CONDOMINIUMS AND PLANNED UNIT DEVELOPMENTS

A. General Condominium Project Requirements

Condominium projects typically consist of multi-unit buildings governed by a

Homeowner’s Association (HOA). Each condominium unit is a single family dwelling

that is individually owned, and the common areas such as hallways and recreational

facilities are owned by all the unit owners. Condominium projects may consist of

attached, semi-detached, detached or manufactured housing units.

Lenders may request a Conditional Commitment for Loan Note Guarantee for a

condominium unit if the condominium project:

• Can be approved in accordance with HUD/FHA, VA, Fannie Mae or Freddie

Mac, as applicable; or

• Has been approved or accepted by HUD/FHA, VA, Fannie Mae or Freddie Mac.

HB-1-3555

Paragraph 12.11 Condominiums and Planned Unit Developments

12-34

A Condominium Rider must supplement the Mortgage or Deed of Trust. HOA dues

for dwellings in a condominium project must be included in total debt-to-income. Aside

from the lender certification to Rural Development, all condominium documentation

should remain in the lender’s permanent loan file and should be available upon request.

Full documentation will be requested if the lender fails to certify the condominium unit

meets the requirements of HUD/FHA, VA, Fannie Mae or Freddie Mac project approval

or acceptance.

When there is an indication that a condominium unit or project does not meet the

requirements of HUD/FHA, VA, Fannie Mae or Freddie Mac, the Agency will request

additional documentation from the lender. If the condominium unit or project does not

meet the stated requirements as certified or warranted by the lender, the Agency may

refuse to issue a conditional commitment or loan note guarantee.

1. Ineligible Condominiums

Condominium projects with ineligible characteristics listed under HUD/FHA,

VA, Fannie Mae, or Freddie Mac guidelines are not eligible for guarantee. Lenders

are responsible for verifying eligibility at the time of loan underwriting.

2. Acceptability of a Non-Approved Condominium Project

Lenders who meet the conditional authority and who have staff with knowledge

and expertise in reviewing and approving condominium projects in accordance with

HUD/FHA, VA, Fannie Mae or Freddie Mac, as applicable, may determine the

acceptability of the condominium project. Lenders may refer to HUD/FHA, VA,

Fannie Mae or Freddie Mac for additional guidance in performing their approval

review of the condominium project. Lender representation and certification of project

approval may be accepted as long as the lender meets the self-certification criteria set

forth by HUD/FHA, VA, Fannie Mae or Freddie Mac and is done so consistently with

standards and regulations set forth by each entity. By submitting the request for

Conditional Commitment for Loan Note Guarantee, the lender represents the