The Ohio Investment Adviser and

Investment Adviser Representative

Handbook 4.0

REVISED JANUARY 2022

Ohio Department of Commerce, Division of Securities

Licensing Section

Handbook 4.0 replaces Handbook 3.0 dated March 2020

For the most recent version, visit

https://com.ohio.gov/wps/portal/gov/com/divisions-and-

programs/securities

Ohio Investment Adviser Handbook

2

Revised Handbook January 2022

The securities industry is a moving and changing industry. To keep up with new investor

protection challenges, it is imperative that the Division of Securities make amendments

and changes to policy and laws as it pertains to investment advisers. Therefore, as part

of the Division’s continuing outreach and education efforts, the Division is revising the

2020 Handbook. Please refer to Appendix L for specific topics that have changed and a

page locator for those changes. And as always, please feel free to contact our office with

any questions.

The Ohio Department of Commerce

The mission of the Ohio Department of Commerce is to safeguard Ohio’s citizens and

visitors and their property and resources, while ensuring reliable marketplaces conducive

to business growth and prosperity.

The Ohio Division of Securities

The Division of Securities, within the Ohio Department of Commerce, administers and

enforces the Ohio Securities Act. The Division licenses broker-dealers, securities

salespersons, investment advisers, and investment adviser representatives. The Division

also registers securities offered for sale to Ohioans. When Ohio Securities law is violated,

the Division can pursue administrative actions, civil injunctive actions, and criminal

referrals.

Mission: Promoting capital formation while protecting Ohio investors from fraudulent

securities and investment schemes through the sale of properly registered securities by

licensed professionals.

Disclaimer: This compilation of material and information was prepared by the Ohio

Division of Securities to provide general information and assistance regarding the

Division’s oversight of investment advisers and investment adviser representatives in

Ohio. This information is not legal advice and is not a substitute for a thorough review of

the relevant statutory provisions set out in Chapter 1707 of the Ohio Revised Code and

related administrative rules set out in Chapter 1301:6-3 of the Ohio Administrative Code.

Ohio Investment Adviser Handbook

3

Part 1 Table of Contents

Part 2 Introduction .................................................................................................................. 6

Part 3 Licensing – Applications, Renewals, Termination ........................................................ 7

Investment Adviser Licensing ______________________________________________ 7

Are You an Investment Adviser under Ohio Law? _____________________________ 7

How to Form an Investment Adviser Firm in Ohio _____________________________ 8

Investment Adviser Branch Offices ________________________________________ 9

How to Form an Investment Adviser Firm as a Sole Proprietor __________________ 9

The “Good Business Repute” Standard for IAs ______________________________ 11

Application Review Process – Approval or Denial ____________________________ 11

Investment Adviser Representative Licensing ________________________________ 12

Are You an Investment Adviser Representative under Ohio law? ________________ 12

How do I Apply to be an IAR in Ohio? _____________________________________ 13

Fingerprinting Requirement _____________________________________________ 13

Minimum Competency – Series Examinations ______________________________ 14

Minimum Competency – Professional Designations __________________________ 15

IAR Dual Registration _________________________________________________ 15

The “Good Business Repute” Standard for IARs ____________________________ 16

Application Review Process – Approval and Denial __________________________ 16

Renewal and Expiration of a License _______________________________________ 17

How to Terminate a License – Discontinuing Business ________________________ 17

Part 4 Compliance Obligations ..............................................................................................17

Books and Records _____________________________________________________ 17

Financial Records ____________________________________________________ 18

Trading Records _____________________________________________________ 18

Correspondence _____________________________________________________ 19

Advertising Records __________________________________________________ 19

Client Records _______________________________________________________ 20

Suitability/Know Your Client Records _____________________________________ 21

Fiduciary Duty Records ________________________________________________ 21

Trusted Contact ______________________________________________________ 22

Disclosure Records ___________________________________________________ 22

Privacy Policy _______________________________________________________ 22

Compliance Policies and Procedures _____________________________________ 23

Ohio Investment Adviser Handbook

4

Miscellaneous Records ________________________________________________ 23

Retention Period of Books and Records ___________________________________ 24

Electronic Storage ____________________________________________________ 24

Books and Records Should be Current ____________________________________ 24

Financial Records Required to be Kept Quarterly ______________________________ 25

The Brochure Rule – Form ADV (Parts 1 and 2) ______________________________ 25

Form ADV Part 1 _____________________________________________________ 25

Regulatory Assets Under Management (RAUM) _____________________________ 25

Assets Under Advisement ______________________________________________ 26

Third Party Relationships ______________________________________________ 26

Form ADV Parts 2A and 2B _____________________________________________ 27

Material Changes ____________________________________________________ 28

Wrap Fee Program Disclosures _________________________________________ 28

Advertising ___________________________________________________________ 30

Performance Advertising _________________________________________________ 30

Investment Advisory Contracts and Compensation ____________________________ 32

Supervision and Compliance Manual _______________________________________ 33

Compliance Manual ____________________________________________________ 33

Custody ______________________________________________________________ 38

Fees ________________________________________________________________ 40

Wrap Fee Program _____________________________________________________ 41

Fiduciary Standard _____________________________________________________ 42

Mandatory Reporting of Senior Financial Exploitation with Transaction Holds ________ 44

Solicitors and Referral Fees ______________________________________________ 46

Best Execution and Soft Dollars ___________________________________________ 47

Aggregation of Client Orders (Batch Orders) _________________________________ 48

Principal Transactions; Agency Cross Transactions; Cross Trades ____________ 48

Other Disclosure Requirements ________________________________________ 49

Overview of the Anti-Fraud and Conduct Standards ____________________________ 49

Part 5 The Division’s Onsite Examination Program ...............................................................50

Onsite Exams Generally _________________________________________________ 50

Common Deficiencies ___________________________________________________ 52

Part 6 Appendices .................................................................................................................54

Appendix A: Frequently Asked Questions ____________________________________ 54

Appendix B: Common Definitions __________________________________________ 57

Ohio Investment Adviser Handbook

5

Appendix C: Investment Adviser Flowchart __________________________________ 60

Appendix D: Investment Adviser Representative Flowchart ______________________ 64

Appendix E: Pre-Licensing Exam __________________________________________ 67

Appendix F: Determining Regulatory Assets Under Management _________________ 69

Appendix G: Trusted Contact Template _____________________________________ 73

Appendix H: Standing Letters of Authority (SLOAs) ____________________________ 74

Appendix I: Annual Compliance Checklist ___________________________________ 76

Appendix J: NASAA’s State IA Cybersecurity Checklist and Guidance _____________ 78

Appendix K: NASAA’s Confidential Data Inventory Checklist _____________________ 92

Appendix L: Summary of Handbook Changes Since 2020 _______________________ 94

[* * * * *]

Ohio Investment Adviser Handbook

6

Part 2 Introduction

The Ohio Securities Act (the “Act”), set forth in Chapter 1707 of the Ohio Revised Code

(the “ORC”), provides for oversight of investment advisers (“IAs”) and investment adviser

representatives operating in Ohio. This oversight is administered and enforced by the

Division of Securities (the “Division”) pursuant to the Act and the associated rules set forth

in Chapter 1301:6-3 of the Ohio Administrative Code (the “OAC”). Subject to certain

limited exceptions, all investment advisers operating in Ohio must be either licensed by

the Division or in compliance with certain notice filing requirements. Further, subject to

certain limited exceptions, all investment adviser representatives with a place of business

in Ohio must be licensed by the Division. Filings and fees for investment adviser notice

filings or licensure must be submitted electronically through the Investment Adviser

Registration Depository (“IARD”), a nationwide database and filing system maintained by

the Financial Industry Regulatory Authority (“FINRA”) that is available at iard.com. Filings

and fees for investment adviser representative licensure must be submitted electronically

through the Central Registration Depository (“CRD”), the companion FINRA database to

IARD.

Pursuant to the federal National Securities Markets Improvement Act of 1996, as

amended, and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010,

only certain investment advisers are eligible to be registered with the federal Securities

and Exchange Commission (the “SEC”). Generally, there are 11 categories of investment

adviser that are permitted to register with the SEC. The most frequently relied upon

category is for investment advisers with assets under management of $100 million or

more. Subject to certain limited exceptions, investment advisers registered with the SEC

that are operating in Ohio must comply with the Act’s notice filing requirements.

Investment advisers operating in Ohio that are not registered with the SEC must be

licensed by the Division, subject to four limited exceptions.

Similarly, all investment adviser representatives with a place of business in Ohio must be

licensed by the Division, subject to five limited exceptions. The general rule requiring

licensure for investment adviser representatives applies regardless of whether the

investment adviser representative is affiliated with an SEC-registered investment adviser

or a state-licensed investment adviser.

The starting points for consideration of Ohio investment adviser and investment adviser

representative requirements are the definitional sections. “Investment adviser” is defined

in ORC § 1707.01(X). “Investment adviser representative” is defined in

ORC § 1707.01(CC). These definitions track the definitions of these terms contained in

federal law.

If a person meets the definition of investment adviser or investment adviser representative

under Ohio law, the person then must look to the Act’s licensing and notice filing

Ohio Investment Adviser Handbook

7

requirements. ORC § 1707.141 and ORC § 1707.151 set out the licensing and notice

filing requirements for investment advisers, while ORC § 1707.161 sets out the licensing

requirements for investment adviser representatives.

Finally, investment advisers and investment adviser representatives are subject to certain

anti-fraud and conduct standards. These standards are contained primarily in

ORC § 1707.44(M) and OAC 1301:6-3-15.1 and 1301:6-3-44.

Violations of the Act can result in criminal penalties. ORC § 1707.99 provides that the

penalties for certain violations range from fifth degree to first degree felonies. Violations

can also lead to civil liability. Consequently, the Division urges investment advisers and

investment adviser representatives to take their compliance responsibilities seriously.

To review the full text of references in this Handbook to the ORC or the OAC, please see

the Ohio Revised Code online at codes.ohio.gov/orc, and the Ohio Administrative Code

online at codes.ohio.gov/oac.

Part 3 Licensing – Applications, Renewals, Termination

Investment Adviser Licensing

Are You an Investment Adviser under Ohio Law?

“Investment Adviser” Definition

The Ohio definition of “investment adviser” is set forth in ORC § 1707.01(X) and parallels

the federal definition (see § 202(a)(11) of the Investment Advisers Act of 1940).

In general, an investment adviser is a person who: (1) for compensation; (2) engages in

the business of; (3) advising others as to the value of securities or the advisability of

investing in securities.

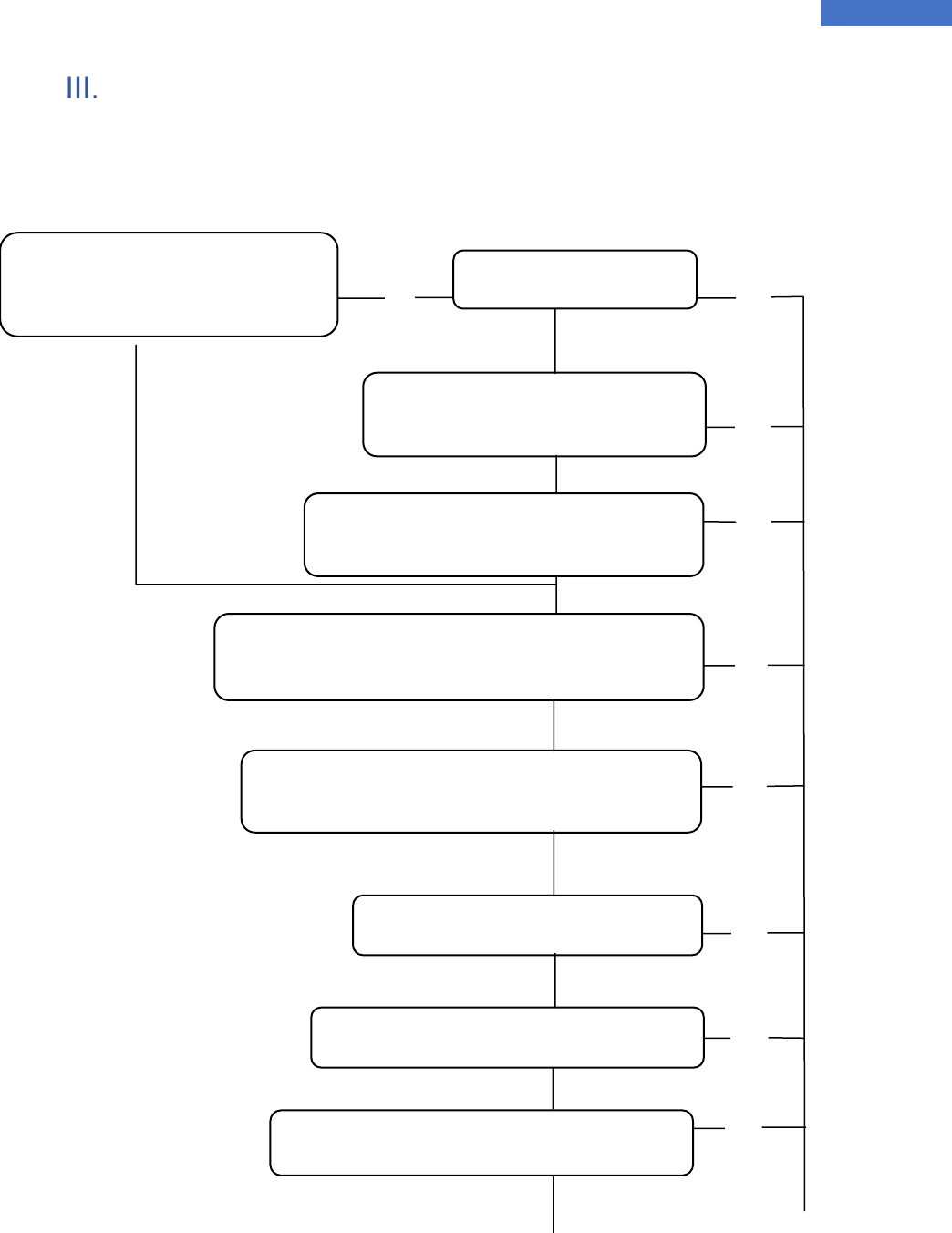

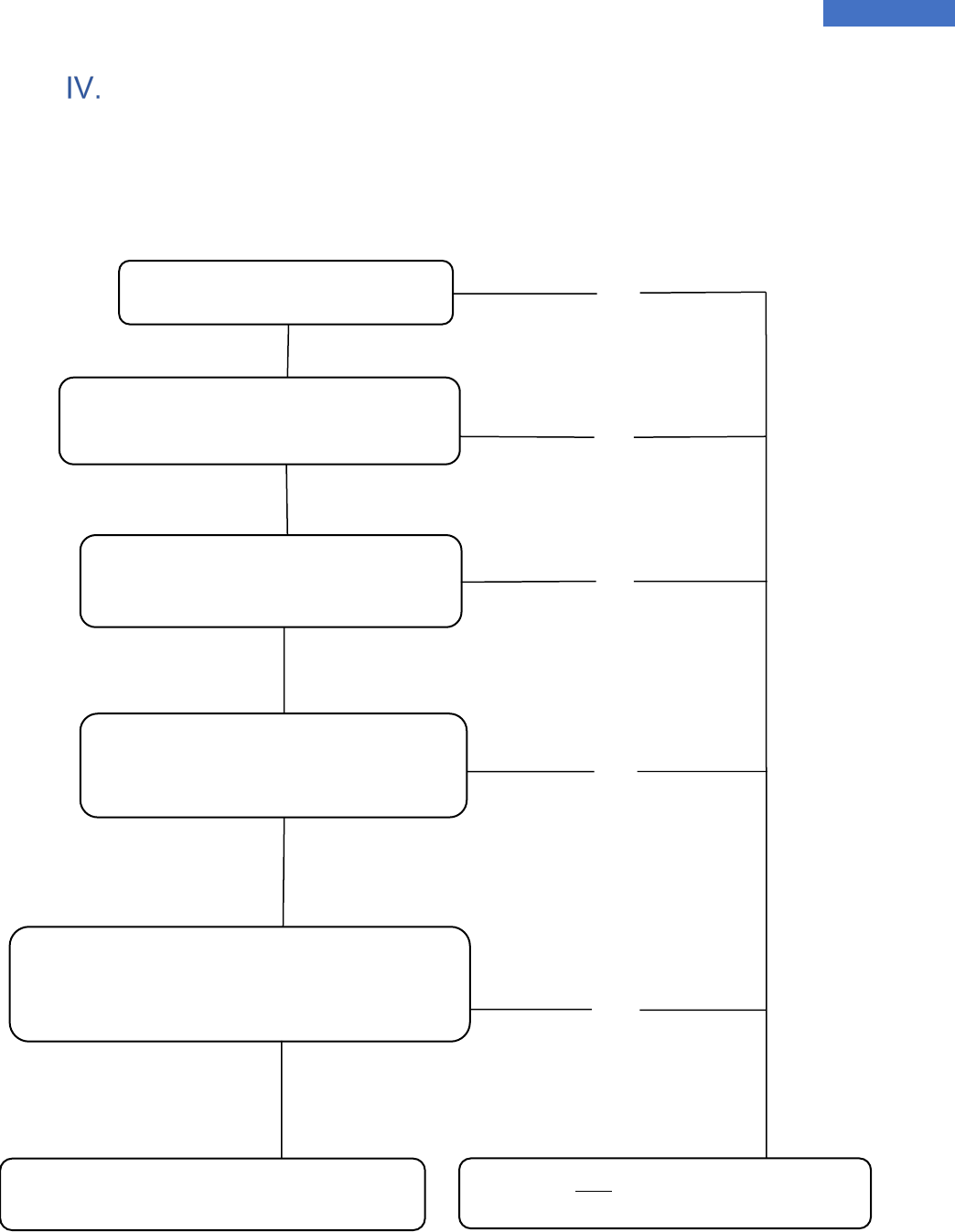

The Investment Adviser Flowchart set forth in Appendix C and accompanying notes

provides a step-by-step guide through the elements of, and exclusions from, the definition

of “investment adviser” under Ohio law.

Three Elements

The three elements are broadly construed. The “compensation” element is satisfied by

the receipt of any economic benefit by the person providing advice. The “engaged in the

business” element is satisfied if any one of the following occurs: (1) the person holds

himself or herself out as an investment adviser or as one who provides investment advice;

(2) the person receives compensation that represents a clearly definable charge for

providing advice about securities; or (3) the person, on anything other than rare, isolated

Ohio Investment Adviser Handbook

8

and non-periodic instances, provides specific investment advice. Finally, as to the third

element, the advice must “pertain to securities.” However, in order to satisfy the “pertain

to securities” element, the advice need not be about specific securities, but rather only

about securities generally as a possible avenue for investment.

Keep in mind that it is not necessary that a person's activities consist solely of investment

advisory services to qualify as an investment adviser. Rather the test is whether any part

of the person's activities meet the three elements of “for compensation,” “engaged in the

business,” and “regarding securities.” For example, a recommendation to sell securities

holdings in order to purchase a particular insurance product may satisfy the definition of

an investment adviser where the insurance sale results in a commission payment.

Exclusions From the Definition of “Investment Adviser”

Ohio Revised Code § 1707.01(X)(2) excludes several classes of persons from the Ohio

definition of investment adviser. These exclusions track the exclusions from the federal

definition of investment adviser. (See §§ 202(a)(11)(A)-(F) of the Investment Advisers Act

of 1940). Whether an exclusion is available depends on all the relevant facts and

circumstances.

How to Form an Investment Adviser Firm in Ohio

If you determine that you meet the definition of an Investment Adviser under Ohio law

and that you are required to be licensed, you need to take steps to become licensed.

• Determine the legal status of your firm. The most common structures are

Corporation, Sole Proprietorship (see the section of this Handbook titled

“Establishing an Investment Adviser Firm as a Sole Proprietor”), Limited

Partnerships, Partnership, and Limited Liability Company. To determine the best

structure for your firm, you should consult with an attorney or accounting

professional for guidance.

• Register your firm with the Ohio Secretary of State’s office and obtain an

Employer Identification Number (EIN) for your firm, if applicable. Helpful sites to

visit are sos.state.oh.us and irs.gov.

• Establish that your firm has a representative that meets minimum

competency requirements and determine if the representative is required to submit

fingerprints. Investment Adviser Representative licensing requirements are

discussed in more detail in the section of this Handbook titled “Investment Adviser

Representative Licensing.”

• Establish an IARD account, through FINRA’s IARD at:

iard.com/accessIARD.asp. This is where a firm applies for licensure and funds the

Ohio Investment Adviser Handbook

9

payments for licensing and future renewals. IARD Gateway Call center

representatives can be reached at (240) 386-4848.

• Applications for licensure must be submitted electronically using the IARD

system. Items to be filed on IARD include Form ADV Parts 1A and 1B, Parts 2A

and 2B, and wrap fee brochure, if applicable. These documents make up your

firm’s application. Form ADV in its entirety as well as the Instructions and Glossary

are available at: sec.gov/about/forms/formadv.pdf.

• Pay the applicable licensing fees for your firm and all IARs as prescribed in

ORC § 1707.17(B).

• Create your firm’s Compliance and Cybersecurity Manuals, policies and

procedures, business continuity plan and investment advisory agreement. These

requirements are discussed in more detail in the section of this Handbook titled

“Compliance Manual.”

• Install your initial recordkeeping procedures, including your accounting

records that you will use for creating the required financial statements. These

requirements are discussed in more detail in the section of this Handbook titled

“Books and Records.”

Once you have filed your initial application material on the IARD, the Division requires a

Pre-Licensing Examination. The exam will require that certain documents be provided.

See Appendix E.

Investment Adviser Branch Offices

If you operate a branch office(s) other than your primary office, you need to register the

branch office with the Division. Each investment adviser must file a Form BR through

IARD to report a “place of business” other than their principal place of business. “Place

of business” is defined in OAC 1301:6-3-01(G) to include two categories of locations. First

is an office at which an investment adviser or investment adviser representative regularly

provides investment advisory services, solicits, meets with, or otherwise communicates

with clients. Second is any other location that is held out to the general public as a location

at which an investment adviser or investment adviser representative provides investment

advisory services, solicits, meets with or otherwise communicates with clients. There is

no filing fee for filing Form BR.

How to Form an Investment Adviser Firm as a Sole

Proprietor

Ohio Revised Code § 1707.151(B) provides that each natural person applicant for an

investment adviser license (i.e., as a sole proprietor) must demonstrate their competence

Ohio Investment Adviser Handbook

10

to engage in the advisory business. A sole proprietor investment adviser is a natural

person who has not created a legal entity to engage in that business. Sole proprietor

investment advisers should keep in mind that, as with firms, they are subject to anti-fraud

and business conduct standards.

In addition, because sole proprietor investment advisers are distinguished from sole

shareholders of corporate investment advisers, sole proprietor investment advisers need

not file a Form U-4 with the Division and need not be licensed as an investment adviser

representative (unless the person also acts as an investment adviser representative for

another investment adviser). However, in addition to submitting Form ADV and a filing

fee through the IARD system, a sole proprietor must also submit a standard impression

sheet for fingerprints provided by the Division if one is not currently on file with the

Division. See the section of this Handbook titled “Fingerprinting Requirement” for more

information.

A sole proprietor investment adviser must also demonstrate “good business repute” (as

discussed in this Handbook under “The Good Business Repute Standard for IAs”) and

minimum competency. Under OAC 1301:6-3-15.1(C), the minimum competency standard

for sole proprietors may be satisfied by:

• Having been licensed as an investment adviser or investment adviser

representative by the division within the two years immediately preceding the

date of the application;

• Achieving a passing score on one of the following exams, or their successor

exams, within two years of the date of filing the application:

o The uniform investment adviser law exam (series 65); or

o The securities industry essentials exam (SIE), the general securities

representative exam (series 7), and the uniform state law exam (series

66);

• By earning and being in good standing with the organization that issued any

of the following credentials:

• Certified Financial Planner awarded by the Certified Financial

Planner Board of Standards, Inc.;

• Chartered Financial Analyst;

• Chartered Financial Consultant;

• Chartered Investment Counselor; or

• Certified Public Accountant with a Personal Financial Specialist

designation.

Important Note: An applicant under this rule will be considered to have met the

examination requirement(s) of this rule if the applicant was licensed or registered as an

Ohio Investment Adviser Handbook

11

investment adviser representative in another United States jurisdiction within the two

years immediately preceding the filing of an application with the division. Also, an

applicant will be considered to have passed the securities industry essentials exam (SIE)

if they currently maintain a non-expired “SIE Credit” issued by the financial industry

regulatory authority. See OAC 1301:6-3-15.1(C)(4) and (5).

An applicant who is not affiliated with a FINRA-registered securities dealer may register

for the Series 65 or Series 66 by submitting to FINRA a completed Form U-10, Uniform

Examination Request for Non-FINRA Candidates. These examinations are administered

by the North American Securities Administrators Association (NASAA). For information

about registration, scheduling, and study guides, visit their website for more information:

nasaa.org.

The “Good Business Repute” Standard for IAs

In addition to the application requirements described above, ORC § 1707.151(E) requires

the Division to make an affirmative finding that an applicant is of “good business repute”

before granting a license. To determine if you meet the “good business repute” standard,

the Division considers the factors set forth in OAC 1301:6-3-19(D), which generally

include whether the applicant has:

• Engaged in fraudulent conduct or been found liable for conduct constituting

incompetence in financial activities;

• Been subject to administrative, civil or other disciplinary action by a regulatory

agency, or failed to fully satisfy any judgment or award;

• Been found guilty of a felony, or of any misdemeanor involving theft, deception,

or moral turpitude; or

• Engaged in any conduct that would reflect on the applicant's reputation for

honesty, integrity, and competence in business and personal dealings.

Application Review Process – Approval or Denial

Failure to answer all questions on the appropriate forms, and failure to provide all required

information will delay the Division’s review of an application. By rule, the Division may

terminate an application with unresolved deficiencies that remains pending for more than

180 days. See OAC 1301:6-3-15.1(L).

Pursuant to ORC § 1707.151(B), the Division may investigate any license applicant and

may require any additional information as it deems necessary in consideration of the

application.

Ohio Investment Adviser Handbook

12

If the Division determines that an applicant lacks good business repute, the Division will

issue to the applicant a notice of intent to deny the application. The applicant must, within

30 days, either withdraw the application or, pursuant to ORC Chapter 119, request an

administrative hearing. Failure to withdraw the application or request a hearing within 30

days will result in the issuance by the Division of a final order to deny the application.

Investment Adviser Representative Licensing

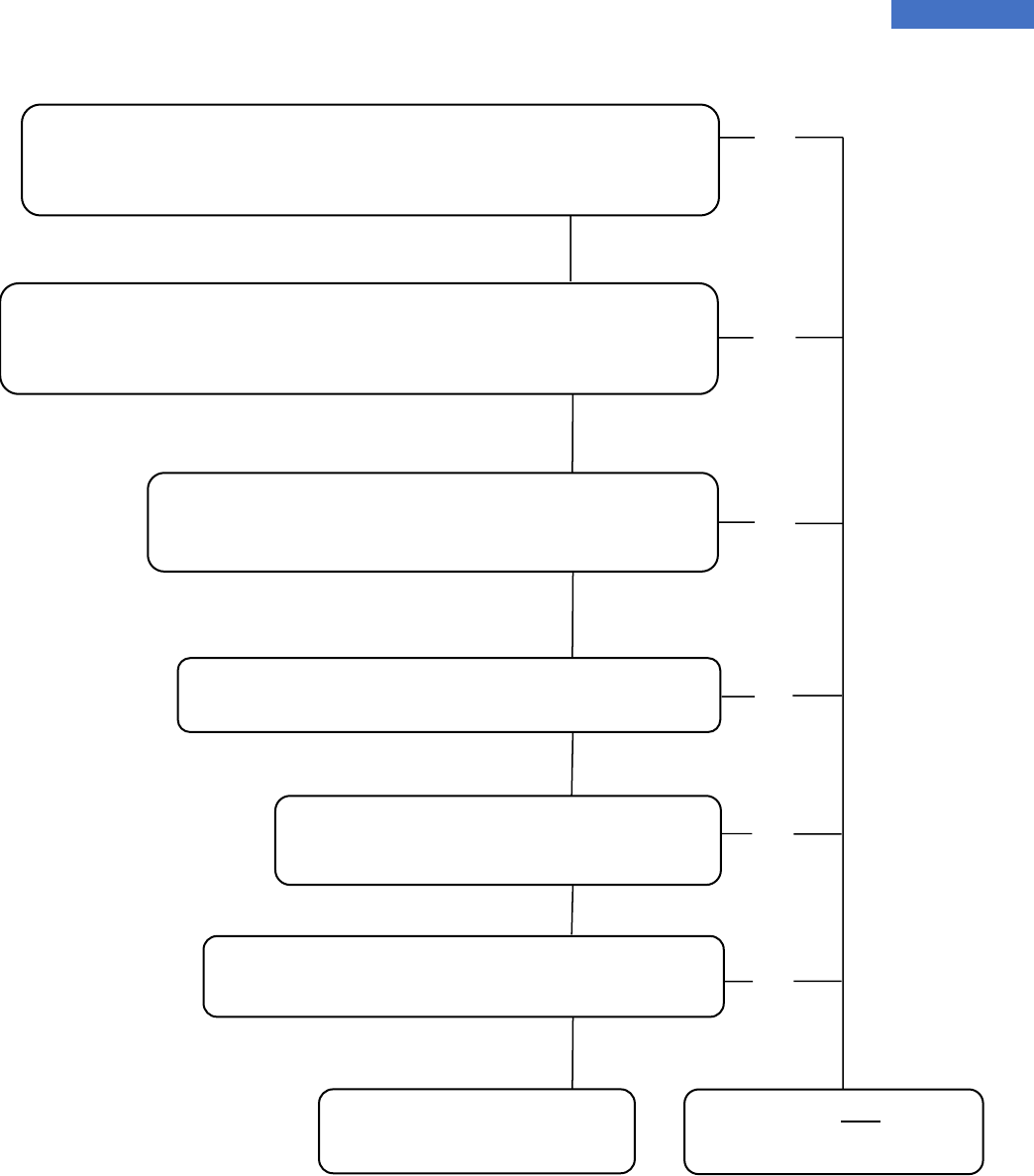

Are You an Investment Adviser Representative under Ohio

law?

The Ohio definition of “investment adviser representative” is set forth in

ORC § 1707.01(CC) and parallels the federal definition (See SEC Rule 203A-3(a)). The

Investment Adviser Representative Flowchart set forth in Appendix D and accompanying

notes provide a step-by-step guide through the elements of this definition.

In general, an investment adviser representative is an individual who gives advice on

behalf of an investment adviser to a certain minimum number of natural person clients

through regular meetings or communications.

• Supervised Person: Specifically, in order to be an investment adviser

representative, the person first must be a “supervised person” as

defined in ORC § 1707.01(DD) and generally means officers, directors and

employees of an investment adviser as well as others who provide advice

on behalf of the investment adviser firm.

• More than five Clients: The supervised person must have more than five

clients who are natural persons other than “excepted persons,” and more

than 10% of the clients must be natural persons other than “excepted

persons.” “Excepted person” is defined in ORC § 1707.01(EE) and

generally means certain wealthy and high net worth individuals.

• Client meetings: The supervised person must on a regular basis solicit,

meet with, or otherwise communicate with clients of the investment adviser.

All three of these elements must be met for a person to qualify as an investment

adviser representative. However, even if a person meets all three of these elements,

ORC § 1707.01(CC)(1)(b) provides that the person is excluded from the definition of

investment adviser representative if the natural person provides advisory services only

by means of written materials or oral statements that do not purport to meet the objectives

or needs of specific individuals or accounts.

Ohio Investment Adviser Handbook

13

How do I Apply to be an IAR in Ohio?

Ohio Revised Code § 1707.161(D)(1) states that an application for an investment adviser

representative license shall consist of the information, materials, and forms specified in

rules adopted by the Division. OAC 1301:6-3-16.1(A) specifies that an application shall

consist of:

• A completed Form U-4 for each individual for whom the applicant

seeks to act as an investment adviser representative;

• The fingerprinting requirement; and

• The license fee prescribed in ORC § 1707.17(B).

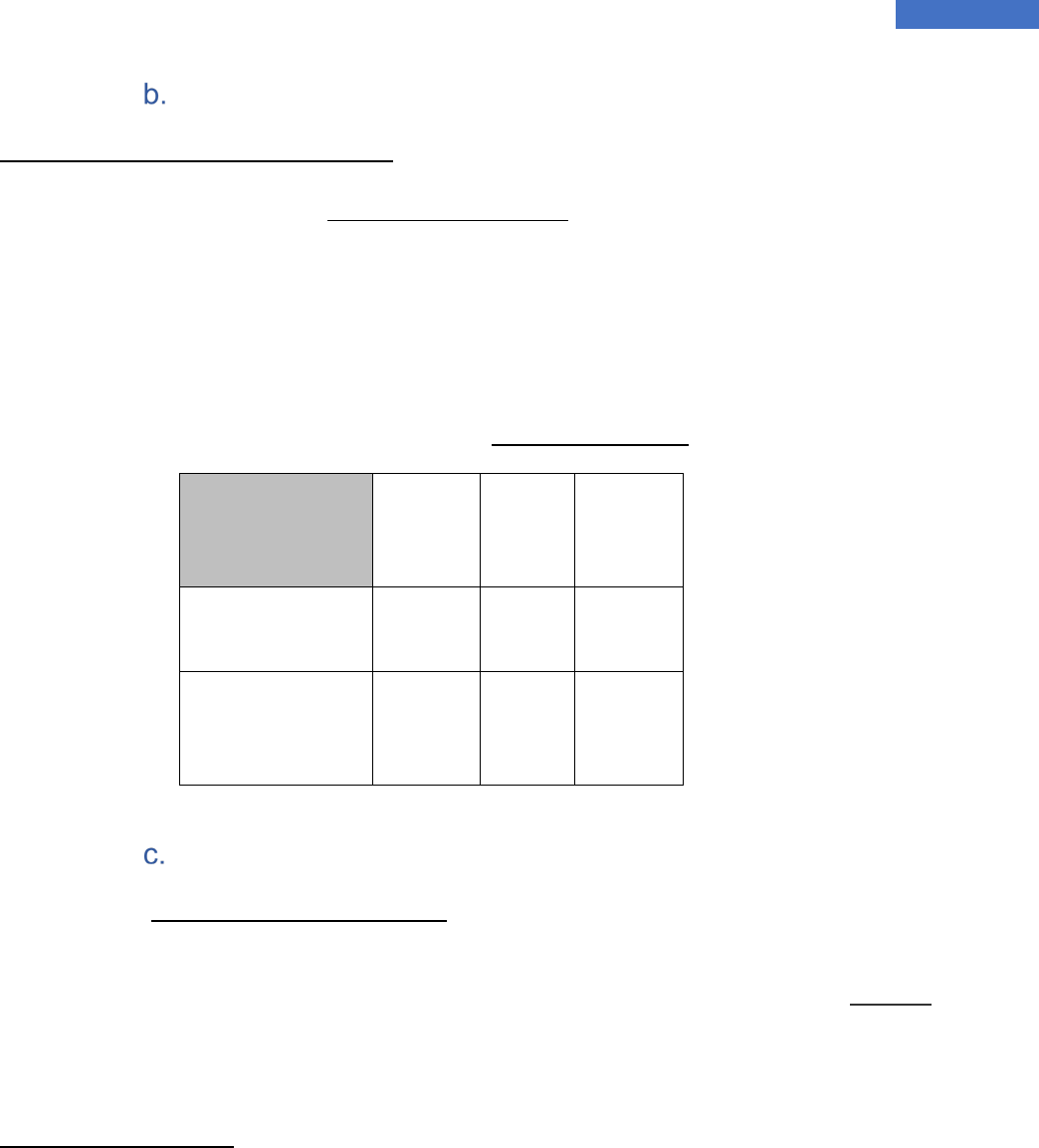

Annual Cost

table

Ohio

Fee

IARD

User

Fee Totals

Investment

Adviser Firm

$100.00 $0.0 $100.00

Investment

Adviser

Representative

$35.00 $15.00 $50.00

Fingerprinting Requirement

(OAC 1301:6-3-16.1(A)(1)(c))

All investment adviser representatives are required to be fingerprinted when applying for

a license. The Division will only waive this requirement if the applicant has a current

approved status by a regulatory authority at the time application for licensure is made with

the division and the applicant has submitted fingerprint impressions to FINRA or CRD in

connection with the approved status.

For Ohio residents, the Division only accepts electronic fingerprints taken via

WebCheck. Below is a website you can use to find a WebCheck location near you:

Ohio Investment Adviser Handbook

14

Ohio Attorney General WebCheck Community Listing

The Division cannot accept fingerprint results directly from the applicant or their

employing firm. Please bring the Division’s address to the facility for the results to be sent

directly to the Division:

Ohio Department of Commerce

Division of Securities

77 South High Street, 22

nd

Floor

Columbus Ohio 43215

For non-Ohio residents needing fingerprints, please contact the Division at (614) 644-

6292, and a Division-specific fingerprint impression card will be forwarded to you.

Minimum Competency – Series Examinations

(OAC 1301:6-3-16.1(B))

As a condition of licensing, every applicant for licensing as an investment adviser

representative shall furnish evidence to the division that they have satisfied one of the

criteria listed in paragraphs (B)(1) to (B)(3) of this rule:

(1) Been licensed as an investment adviser representative by the division within the

two years immediately preceding the date of the application; or

(2) Achieved a passing score on the following exams, or their successor exams,

within two years of the date of filing an application:

(a) The uniform investment adviser law exam (series 65); or

(b) The securities industry essentials exam (SIE), the general securities

representative exam (series 7), and the uniform combined state law exam (series

66);

A WebCheck facility will request the “reason for printing.” Please have the

WebCheck personnel choose “other” and fill in “IAR Registration, pursuant to

OAC 1301:6-3-16.1.” The impressions will be forwarded directly to the Attorney

Generals’ Bureau of Criminal Investigation (“BCI

”) and then be sent to the

Division.

It may be necessary to notify the WebCheck personnel that the

fingerprint results must be sent directly to the Division, not to the adviser/firm to

then route them to the Division. The Division can only accept results if they come

directly from BCI.

Ohio Investment Adviser Handbook

15

An applicant under this rule will be considered to have met the examination requirement

above if the applicant was licensed or registered as an investment adviser representative

in another United States jurisdiction within the two years immediately preceding the filing

of an application with the Division. Further, an applicant will be considered to have passed

the securities industry essentials exam (SIE) referenced in this rule if they currently

maintain a non-expired “SIE Credit” issued by FINRA.

An applicant who is not affiliated with a FINRA-registered securities dealer may register

for the Series 65 or Series 66 by submitting to FINRA a completed Form U-10, Uniform

Examination Request for Non-FINRA Candidates. These examinations are administered

by NASAA (North American Securities Administrators Association). For information about

registration, scheduling, and study guides, visit their website for more information:

nasaa.org.

Minimum Competency – Professional Designations

(OAC 1301:6-3-16.1(B)(3))

As an alternative to the Series Examinations, an applicant can qualify for licensure with

the Division by providing verification that they are in good standing with the organization

that issues credentials for one of the following designations:

• Certified Financial Planner;

• Chartered Financial Analyst;

• Chartered Investment Counselor;

• Chartered Financial Consultant; and

• Certified Public Accountant with a Personal Financial Specialist designation.

IAR Dual Registration

Ohio Revised Code § 1707.161(B)(1) permits an investment adviser representative to be

licensed with up to two (2) investment adviser firms, regardless of whether the two firms

are affiliated.

If the investment adviser representative is licensed with two (2) unaffiliated investment

adviser firms, then they shall do so only after the occurrence of both of the following;

• Being properly licensed, or properly excepted from licensure, as an investment

adviser representative for each of the two investment advisers; and

• Notifying both investment advisers of the dual affiliation via filing of Form U-4 on

the IARD/CRD system and retaining evidence of that notification in his or her

records.

Ohio Investment Adviser Handbook

16

The “Good Business Repute” Standard for IARs

In addition to the application and minimum competency requirements described above,

ORC § 1707.161(E) requires the Division to make an affirmative finding that an applicant

is of “good business repute” before granting a license.

Determining the existence of good business repute. The Division is guided by the

factors set forth in OAC 1301:6-3-19(D), which generally include whether the applicant

has:

• Engaged in fraudulent conduct or been found liable for conduct constituting

incompetence in financial activities;

• Been subject to administrative, civil or other disciplinary action by a regulatory

agency, or failed to fully satisfy any judgment or award;

• Been found guilty of a felony, or of any misdemeanor involving theft, deception

or moral turpitude; or

• Engaged in any conduct that would reflect on the applicant's reputation for

honesty, integrity and competence in business and personal dealings.

If the Division determines that an applicant lacks good business repute, the Division will

issue to the applicant a notice of intent to deny the application. The applicant must,

within 30 days, either withdraw the application or, pursuant to ORC Chapter 119, request

an administrative hearing. Failure to withdraw or request a hearing within 30 days will

result in the issuance by the Division of a final order to deny the application.

Application Review Process – Approval and Denial

Failure to answer all questions on the appropriate forms, and failure to provide all required

information will delay the Division’s review of an application. By rule, the Division may

terminate an application with unresolved deficiencies that remains pending for more than

180 days. See OAC 1301:6-3-16.1(G).

Pursuant to ORC § 1707.161(D), the Division may investigate any applicant and may

require any additional information as it deems necessary in consideration of the

application.

If the Division determines that an applicant lacks good business repute, the Division will

issue to the applicant a notice of intent to deny the application. The applicant must, within

30 days, either withdraw the application or, pursuant to ORC Chapter 119, request an

administrative hearing. Failure to withdraw the application or request a hearing within 30

days will result in the issuance by the Division of a final order to deny the application.

Ohio Investment Adviser Handbook

17

Renewal and Expiration of a License

All investment adviser and investment adviser representative licenses expire on

December 31st each year unless they are renewed through the Web IARD/CRD.

A Preliminary renewal statement is made available to each firm online in Web IARD/CRD

in mid-November each year. The firm’s renewal account must be funded for the entire

preliminary renewal statement amount, regardless of whether there are additions or

deletions in the number of investment adviser representatives, in order for the firm and

their investment adviser representatives to be renewed. Failure to fund the renewal

account with the entire amount of the preliminary renewal account statement will result in

the firm and its investment adviser representatives being terminated. The renewal

account must be funded prior to Web IARD/CRD shutdown in mid to late December.

There are no exceptions in Ohio. You must renew through Web IARD/CRD. Ohio cannot

accept payment directly to the Division.

All licenses not renewed by the deadline will terminate as a matter of law – there are no

grace periods. Investment advisers and investment adviser representatives that “fail to

renew” must re-apply with the Division.

How to Terminate a License – Discontinuing Business

(OAC 1301:6-3-15.1(J))

A notice of withdrawal from licensure shall be filed with the Division via the IARD on Form

ADV-W in accordance with its instructions. The IA should include on Form ADV-W the

address where the books and records will be maintained during such period. Investment

adviser representatives licensed with the terminating firm should have a Form U5 filed on

their behalf.

An investment adviser ceasing to conduct or discontinue business shall arrange for and

be responsible for the preservation of the records in compliance with the OAC for a period

of five years after the firm ceases doing business.

Part 4 Compliance Obligations

Books and Records

(OAC 1301:6-3-15.1(E))

The following books and records must be maintained in true and accurate form by

investment advisers headquartered in Ohio and licensed with the Division.

Ohio Investment Adviser Handbook

18

Financial Records

(OAC 1301:6-3-15.1(E)(1)(a), (b), and (d)–(f))

• Cash receipts and disbursement journals and other records of original entry

forming the basis for entries in any ledger,

• General and auxiliary ledgers reflecting assets, liabilities, reserves, capital, income

and expense accounts,

• All bank statements and bank reconciliations of the adviser,

• All bills or statements (paid or unpaid) relating to the business of the investment

adviser as such,

• All trial balances, quarterly financial statements (which includes balance sheets

and income or profit and loss statements), and internal audit working papers

relating to the investment adviser’s business.

Trading Records

(OAC 1301:6-3-15.1(E)(1)(c) and (h), (E)(2)-(3))

• A memorandum for each order made for the purchase or sale of securities,

including terms, conditions and instructions received from the client, and any

modification or cancellation of the order. The memorandum must identify the

affiliated person who recommended the transaction, the person who placed the

order, the account involved, the date of entry, and the bank, broker or dealer that

executed the order. Orders entered pursuant to discretionary power are to be so

designated.

• A list or record of all accounts in which the adviser has discretionary power as to

funds, securities or transactions.

• For advisers that have custody or possession of client funds or securities, records

must include (a) a journal of purchases, sales, receipts and deliveries of securities,

showing certificate numbers and all other debits and credits to the accounts; (b) a

separate ledger account for each client showing purchases, sales, receipts and

deliveries, showing the date and price for each transaction and all debits and

credits; (c) copies of confirmations of all transactions effected by or for clients’

accounts; (d) a record for each security in which any client has a position, showing

the name of each client having an interest in the security, the amount or interest of

each client, and the location of each such security; and (e) the required

Ohio Investment Adviser Handbook

19

accountant’s certificate verifying client funds and securities in the adviser’s

possession.

• For advisers who render investment advisory or management services to clients,

records with respect to the portfolio being supervised or managed (to the extent

reasonably available or obtainable) must include accurate and current records

showing separately for each client the securities purchased and sold; the date,

amount, and price of each transaction; and for each security in which any client

has a current position, information from which the adviser can promptly furnish the

name of each client and its current amount or interest in the security. Client records

may be maintained using a code instead of the client’s name so long as when

requested the name and other identifying information is promptly provided to the

Division.

Correspondence

(OAC 1301:6-3-15.1(E)(1)(g))

Originals of all written communications received, and copies of all written communications

sent by the investment adviser:

• relating to recommendations or advice given (or proposed to be given);

• relating to receipt, disbursement or delivery of funds or securities; or

• relating to the placing or execution of any order to purchase or sell securities.

Written communications shall include all writings in any form, including but not limited to,

text messages, direct messaging, emails, and email attachments.

The adviser does not need to keep the names and addresses of persons to whom a

publication was sent when it was distributed to more than two persons but must keep with

the copy of the publication a memorandum describing any list to whom the publication

was sent and the source of the list. The adviser does not need to keep unsolicited market

letters or similar communications of general public distribution not prepared by or for the

adviser.

Advertising Records

(OAC 1301:6-3-15.1(E)(1)(k) and (p))

• A copy of any notice, circular, advertisement (as defined in OAC 1301:6-3-

44(A)(2)), newspaper article, investment letter, bulletin or other communication,

including but not limited to, electronic, digital, and internet communications or

postings to internet sites, that the investment adviser circulates or distributes,

Ohio Investment Adviser Handbook

20

directly or indirectly, to two or more persons (other than people connected with

the investment adviser). If the communication recommends the purchase or

sale of a specific security without giving the reasons for the recommendation,

the adviser must keep a memorandum indicating the reasons, and

• All accounts, books, internal working papers, and other records or documents

that support the performance or rate of return calculations for managed

accounts or securities recommendations that are advertised or circulated to ten

or more persons (other than persons connected with the investment adviser).

With respect to performance of managed accounts, it is sufficient to retain the

account statements and related worksheets.

Client Records

(OAC 1301:6-3-15.1(E)(1)(h)-(j), (q)-(r), and (t))

• A list or other records of all accounts in which the investment adviser is vested

with any discretionary power with respect to the funds, securities, or

transactions of any client;

• Originals or copies of all powers of attorney or similar documents from clients

granting the adviser discretionary authority;

• Originals or copies of all written agreements with clients or agreements

otherwise relating to the adviser’s business;

• All current and former client lists, including all contact information in the

adviser’s possession for purposes of communicating with the client, including

address, telephone number, and email address, if applicable;

• All advisory contracts entered into by the adviser or its investment adviser

representatives;

• Originals or copies of all written agreements with clients or agreements

otherwise relating to the adviser’s business; and

• Written information about each investment advisory client and each security

that forms the basis for making any recommendation or providing investment

advice to such client.

As a fiduciary, an adviser must make a reasonable inquiry into the investment objectives,

risk tolerance, liquidity needs, time horizon, and other relevant information necessary to

make recommendations that are in the client’s best interest. All investment advisers must

review their recommendations no less than every three years. This review shall be

Ohio Investment Adviser Handbook

21

conducted more frequently if the client’s circumstances are expected to change or

otherwise indicate a need for more frequent reassessment.

Suitability/Know Your Client Records

(OAC 1301:6-3-15.1(E)(1)(t))

The adviser is required to retain written information about each investment advisory client

and each security that forms the basis for making any recommendation or providing any

investment advice to such client. This information should include all details obtained to

determine a client’s investment objectives, financial needs and any other relevant

information. The information obtained should at the least include income, net worth,

investment objectives, investment experience, the time horizon, liquidity needs and risk

tolerance for each client. This information should be dated and maintained in a manner

for easy access if requested.

In addition, it is recommended that this information be updated at least every three years.

Advisers should review and assess suitability information when there are major changes

in the client’s life (e.g., retirement, job changes, divorce, etc.). The updated information

should be dated and maintained in a manner that is easily accessible and able to be

provided in an orderly manner to examiners or other regulatory agents if requested.

Investment Advisers should also maintain all records documenting the research they

conduct to assess whether a recommended or selected security is suitable for their clients

(also known as, due diligence). This can be written, or maintained in electronic format,

but must comply with all aspects of the record retention rules.

These specific requirements, including how often these records will be updated, should

be made part of the adviser’s compliance manual.

This information is not only required by Ohio’s rules but is deemed a part of the adviser’s

fiduciary duty.

Fiduciary Duty Records

(OAC 1301:6-3-44(E)(1)(f))

Advisers have a fiduciary duty to act in the best interests of clients and to disclose

actual or potential conflicts of interest. Some specific obligations resulting from this

fiduciary duty are:

• A duty to employ reasonable care to avoid misleading clients;

• A duty to have a reasonable independent basis for investment advice;

• A duty to ensure that investment advice is suitable;

Ohio Investment Adviser Handbook

22

• A duty to obtain best execution of client transactions; and

• Borrowing money or securities from a client.

Trusted Contact

The Division strongly encourages that advisers obtain clients’ Trusted Contact

Authorizations as a best practice. This should be separate (although may be similar) to

any Trusted Contact Authorizations executed between the client and third parties (e.g.,

your custodian). A client’s Trusted Contact Authorization may be used if the adviser has

questions or concerns about the client’s health (capacity and well-being) or welfare

(financial exploitation), or if the adviser is unable to contact the client. The adviser would

then be legally permitted to speak with the person(s) listed about the client. The Trusted

Contact Authorization should be signed by the client and updated as needed. While there

is no prescribed format for a Trusted Contact Authorization, advisers may wish to refer to

FINRA’s template while customizing their own. See Appendix G for a sample Trusted

Contact Template.

Disclosure Records

(OAC 1301:6-3-15.1(E)(1)(n))

• A copy of the written disclosure statement, Form ADV Part 2A, 2B, Appendix

1, (and each amendment or revision) made available and a record of the dates

that they were given or offered to each client or prospective client who

subsequently became a client, and

• All written disclosure documents delivered to clients by third-party solicitors

and all written acknowledgments of receipt of such documents received back

from clients.

Privacy Policy

(OAC 1301:6-3-15.1(H))

The investment adviser must deliver upon the investment adviser’s engagement by a

client, and on an annual basis thereafter, a privacy policy to each client that is reasonably

designed to aid in the client’s understanding of how the investment adviser collects and

shares, to the extent permitted by state and federal law, non-public personal information.

The investment adviser must promptly update and deliver to each client an amended

privacy policy if any of the information in the policy becomes inaccurate.

Ohio Investment Adviser Handbook

23

Compliance Policies and Procedures

(OAC 1301:6-3-15.1(E)(1)(w) - (x); and 1301:6-3-44(H))

Advisers are required to maintain compliance policies and procedures, and records of

their annual review of those compliance policies and procedures. Please note that

advisers should maintain copies of the various “versions” of their manual for five years

from the end of the fiscal year that the version was used.

It is advisable to set up routine compliance procedures, including the update of your

compliance manual to stay on top of your requirements. The Division will advise you of

important requirements, including rule/requirement changes, when they occur.

Miscellaneous Records

(OAC 1301:6-3-15.1(E)(1)(l), (s), and (u)-(v))

• A record of every securities transaction (other than in US government

securities) over which the adviser or any of its advisory representative has,

influence or control and in which the adviser or advisory representative has, or

by reason of the transaction acquires, any direct or indirect beneficial

ownership. The record must state the title and amount of securities involved,

the date and nature of the transaction, the price, and the name of the broker,

dealer or bank through whom the transaction was effected.

• A file containing a copy of all written communications received or sent regarding

any complaint, arbitration, civil litigation, unsatisfied judgment, or lien involving

the investment adviser or any investment adviser representative that alleges a

violation of state or federal law, or the rules or codes of ethics of any association

of investment advisers, investment adviser representatives, securities

salespersons or dealers, any professional association granted disciplinary

authority or regulatory authority by any state or federal law, or by a recognized

securities exchange.

• Written physical security and cybersecurity policies and procedures reasonably

designed to ensure the confidentiality, integrity, and availability of physical and

electronic records and information. The policies and procedures must be

tailored to the investment adviser’s business model, considering the size of the

firm, the type(s) of services provided, and the number of locations of the

investment adviser.

• Every investment adviser shall establish, implement, and maintain written

procedures relating to a business continuity and succession plan. The plan

shall be based upon the investment adviser’s business model, including the

Ohio Investment Adviser Handbook

24

size of the firm, type(s) of services provided, and the number of locations of the

investment adviser.

Retention Period of Books and Records

(OAC 1301:6-3-15.1(E)(5))

All books and records required to be made shall be maintained and preserved in an easily

accessible place for a period of not less than five years from the end of the fiscal year

during which the last entry was made on the record. The first two years must be

maintained in an appropriate office of the investment adviser.

Electronic Storage

(OAC 1301:6-3-15.1(E)(7))

The records required to be maintained and preserved may be maintained and preserved

electronically, however the investment adviser must arrange and index the records in a

way that permits easy location, access and retrieval of the record and must be able to

promptly provide legible true and complete copies when requested by the Division. The

Division permits advisers to maintain records exclusively with third parties (e.g., cloud

storage); however, it is the ultimate responsibility of the investment adviser to comply with

all aspects of the record retention rules.

Books and Records Should be Current

Each Investment Adviser licensed with the Division shall make and keep, true, accurate

and current books and records relating to its advisory business. Records must be created

at the time of or in proximity to the entry, action, or occurrence.

As part of the requirement to keep books and records current, all changes to the ADV

must be made promptly. As a reminder:

• Solicitors should always be provided with the most updated version of an

adviser’s Form ADV.

• All referenced links to Form ADV (i.e., on a website or within a publication)

should be to the most updated version.

All links and information provided on an adviser’s website and other social media must

be kept current and all links must be tested for accuracy.

Ohio Investment Adviser Handbook

25

Financial Records Required to be Kept Quarterly

(OAC 1301:6-3-15.1(E)(1))

Investment advisers are required to make and keep accurate and current financial

records. All financial records must be prepared on a quarterly basis. Please refer to the

section of this Handbook titled “Books and Records” for the specific types of records. If

an IA is a sole proprietor, it is recommended that financial records for the

investment adviser be kept separate from the sole proprietor’s personal records. It

is also recommended that financial software be used or that the investment adviser

employ an accountant.

The Brochure Rule – Form ADV (Parts 1 and 2)

(OAC 1301:6-3-15.1(G))

Form ADV Part 1

Part 1 of Form ADV is required to be reviewed and updated within 90 days AFTER the

end of your fiscal year. In addition to your annual updating amendment, you must amend

your Form ADV Part 1, including corresponding sections of Schedules A, B, C, and D, by

filing additional amendments promptly (within 30 calendar days of learning of the

circumstances giving rise to the amendment or update) if:

• Information you provided in response to Items 1, 3, 9 (except 9.A.(2), 9.B.(2),

9.E., and 9.F.), or 11 of Part 1A or Items 1, 2.A. through 2.F., or 2.I. of Part 1B

becomes inaccurate in any way; or

• Information you provided in response to Items 4, 8, or 10 of Part 1A or Item

2.G. of Part 1B becomes materially inaccurate.

• Form ADV Part 1, Item 5(D) and 5(K) were amended in October 2017, and

require additional information to be disclosed.

Regulatory Assets Under Management (RAUM)

Understanding and accurately calculating your firm’s regulatory assets under

management (RAUM) is crucial to making accurate and complete disclosure. As

explained by the instructions to Form ADV Part 1A, Item 5, RAUM includes only the

“securities portfolios” for which you provide “continuous and regular supervisory or

management services” as of the date of Form ADV.

An account is deemed a “securities portfolio” if at least 50% of the total value of the

account is attributable to securities, cash, or cash equivalents (e.g., bank deposits,

Ohio Investment Adviser Handbook

26

certificates of deposit, bankers' acceptances, and similar bank instruments). Assets such

as real estate, fixed indexed annuities, or operating businesses do not meet the definition

of “securities portfolios.” In Re New Line Capital, SEC Proceeding File No. 3-16371

(2015).

You provide “continuous and regular” supervisory or management services to a portfolio

if either (i) you have discretionary authority over and provide ongoing services with

respect to the account, or (ii) you do not have discretionary authority, but you have

ongoing responsibility to make recommendations based on the needs of the client and, if

the client accepts such recommendations, you are responsible for effecting the purchase

or sale. A common example of this scenario is when an adviser reviews a participant’s

401(k) allocations. Only that portion of a securities portfolio that is regularly and

continuously managed should be included. For example, where securities assets are

allocated at the opening of an account, receive only once-quarterly rebalancing, such

assets should not be included among RAUM. In re Retirehub, Inc., SEC Admin Proc, 3-

14666 (2011).

RAUM should be disclosed based on the current market value of the assets determined

within 90 days of filing Form ADV.

Other factors may affect whether your clients’ accounts should be included in your firm’s

RAUM, such as the form of your compensation and the terms of your advisory contract.

You are strongly encouraged to review the entire instructions to Form ADV Part 1A, Item

5, regarding calculating and proper reporting of RAUM.

See Appendix F for an RAUM calculation decision tree.

Assets Under Advisement

Assets under Advisement (AUA) is a non-regulatory term that refers to assets on which

your firm provides advice or consultation but which your firm either does not have

discretionary authority or does not arrange or effectuate the transaction. AUA is distinct

from RAUM and should neither be disclosed as part of RAUM nor used as the basis to

charge an Assets Under Management fee. AUA are permitted to be disclosed, however,

on Form ADV Part 2A as a separate asset figure. If you disclose AUA, then you may be

asked to provide a basis for computing the AUA and a description of the assets

comprising it. Some advisers opt to include AUA to provide prospective clients a more

complete picture of the firm’s responsibilities.

Third Party Relationships

The Division is aware that securities professionals refer clients to other firms for asset

management services. These relationships are sometimes described as solicitor

relationships, subadvisor relationships, third-party money manager relationships, or co-

Ohio Investment Adviser Handbook

27

adviser relationships. Because most of these terms are not defined in the Ohio Securities

Act, we will provide general explanations below. Keep in mind, however, that the terms

“solicitor” and “investment adviser” are defined in the Ohio Securities Act, so regardless

of the terminology used, the Division will look to the licensing and compliance obligations

of your role, as described in your contracts and your regulatory disclosures, to determine

the legal nature of the role.

A solicitor (as defined in by the Act) relationship exists when one refers clients to another

and no longer has any authority in managing or making ongoing decisions on the client

assets, while a referral fee is paid. A co-advisor is generally one who has the authority

and responsibilities to the client, which could mean filling out paperwork, determining

suitability, choosing a model, changing a model, or asset allocation. Co-advisers might or

might not have discretion over the accounts.

Form ADV Parts 2A and 2B

(a/k/a “brochure” or “disclosure document” and “brochure supplement”)

Every investment adviser is required to deliver to each client and prospective client a written

disclosure document, describing the investment adviser's business practices, education,

and business background.

Unless otherwise provided in the OAC, an investment adviser shall follow all current

Instructions to Form ADV issued by the SEC regarding the completion, filing, delivery,

and updating of Form ADV Part 2A (Brochure statement) and Form ADV Part 2B

(Brochure Supplement). A general summary is as follows:

• Provide your Brochure: You must provide a Brochure to each client before or

at the time you enter into an advisory agreement. Evidence of providing the

Brochure is required. This evidence can be in the form of a signed receipt, or

language can be made as part of the client contract.

• Update your Brochure each year you should review your entire brochure and

make necessary changes. The date of the brochure, and the amount of client

assets under management should be updated at this time. In addition, Item 2,

Material Changes, should also be updated by clearly indicating that you are

including only material changes since the last annual update of your brochure.

You must then provide the date of the last annual update of your brochure. If

there are no material changes since your last update, you should state that

there are no material changes. Please note that you must maintain each update

in your files.

• File your Brochure, once it is updated, through the IARD annually within 90

days of the end of your fiscal year. However, if information in your brochure

Ohio Investment Adviser Handbook

28

becomes materially inaccurate, you must update it promptly. According to OAC

1301:6-3-01, the word “promptly” requires licensees to amend or update any

filings within 30 calendar days of learning of facts or circumstances giving rise

to an amendment or update.

• Annual Delivery: Each year you must either deliver within 120 days of your

fiscal year-end your Brochure to each client, that either includes or is

accompanied by a summary of material changes (Item 2), OR you must provide

a summary of material changes and offer your clients the Brochure if they are

interested. If you do not have any material changes: You do not have to

deliver or offer the Brochure to your clients annually.

• Interim Delivery: If any information in response to Item 9 of Part 2A

(disciplinary information) changes, you are required to deliver an interim

amended Brochure Statement to clients. An interim amendment can be in the

form of a document describing the material facts relating to the amended

disciplinary event.

Material Changes

Depending on the facts and circumstances, examples of material changes may include,

but are not limited to:

• Change of address/location or contact information (e.g., phone number or

email address),

• New Owners of Investment Adviser entity,

• Significant change in services offered,

• New potential conflict of interest,

• A new fee schedule,

• Changes in disciplinary history,

• Changes in the custodian or broker used, and/or

• Changes in licensing status with the SEC or state(s).

Wrap Fee Program Disclosures

For advisers offering a wrap fee program, they shall follow all current instructions to Form

ADV issued by the SEC with regards to the completion, filing, delivery, and updating of

Form ADV Part 2A, Appendix 1.

Ohio Investment Adviser Handbook

29

• Preparing a Wrap Fee Program Brochure: If you sponsor a wrap fee

program, you must prepare a Wrap Fee Program Brochure. If you sponsor

more than one wrap fee program, you may prepare a single Wrap Fee Program

Brochure describing all the programs or you may prepare separate brochures

for each program. If you provide advisory services outside of a wrap fee

program, you must prepare a separate brochure for those advisory services. If

a wrap fee program that you sponsor has multiple sponsors, and another

sponsor creates and delivers to your wrap fee program clients a brochure that

includes all the required information, you do not have to create or deliver a

separate Wrap Fee Program Brochure.

• Provide your Wrap Fee Program Brochure: You must provide a Wrap Fee

Program Brochure to each client of the wrap fee program before or at the time

the client enters into a wrap fee program contract. Evidence of providing such

is required. This evidence can be in the form of a signed receipt, or language

can be made as part of the client contract.

• Update your Wrap Fee Program Brochure each year at the time you file your

annual updating amendment on the IARD system and otherwise promptly

whenever any information in the Wrap Fee Program Brochure becomes

materially inaccurate.

• File your Wrap Fee Program Brochure through the IARD annually within 90

days of the end of your fiscal year. However, if information in your Wrap Fee

Program Brochure becomes materially inaccurate, you must update it promptly.

According to OAC 1301:6-3-01, the word “promptly” requires licensees to

amend or update any filings within 30 calendar days of learning of facts or

circumstances giving rise to an amendment or update.

• Annual Delivery: Each year you must either deliver within 120 days of your

fiscal year-end your wrap-fee program brochure to each client, that either

includes or is accompanied by a summary of material changes (Item 2), OR

you must provide a summary of material changes and offer your Wrap Fee

Program Brochure.

• Interim Delivery: If any information in response to Item 9 of Part 2A

(disciplinary information) changes, you are required to provide an interim

update of your Wrap Fee Program Brochure to your wrap fee clients. *NOTE:

Technically, an IA with both Wrap Fee and non-Wrap Fee clients will have to

deliver updated Brochures to each type of client.

Ohio Investment Adviser Handbook

30

Advertising

(OAC 1301:6-3-44(A))

Investment advisers and their investment adviser representatives are prohibited from

using any advertisement that contains any untrue statement of a material fact or that is

otherwise misleading. The rule broadly defines “advertisement” to include any notice,

circular, letter or other written communication addressed to more than one person, or any

notice, circular, letter or other written communication or any communication by electronic

means including but not limited to email, the Internet, any social media sites, or other

digital media, which are disseminated to more than one person, or any notice or other

announcement in any publication or by radio or television.

In addition, an advertisement may not:

• Use or refer to testimonials (which include any statement of a client's

experience or endorsement),

• Refer to past, specific recommendations made by the adviser that were

profitable, unless the advertisement sets out a list of all recommendations

made by the adviser within the preceding period of not less than one year, and

complies with other, specified conditions,

• Represent that any graph, chart, formula, or other device can, in and of itself,

be used to determine which securities to buy or sell, or when to buy or sell such

securities, or can assist persons in making those decisions, unless the

advertisement prominently discloses the limitations thereof and the difficulties

regarding its use, or

• Represent that any report, analysis, or other service will be provided without

charge unless the report, analysis or other service will be provided without any

obligation whatsoever.

Performance Advertising

(OAC 1301:6-3-44(A)(1)(b))

Consistent with the position taken by the SEC, the Division takes the position that an

adviser may advertise its past performance (both actual performance and hypothetical or

model results), only if the advertisement meets certain conditions and restrictions. An

advertisement using performance data must disclose all material facts necessary to avoid

any unwarranted inference.

Among other things, an adviser may not advertise its performance data if the adviser:

Ohio Investment Adviser Handbook

31

• Fails to disclose the effect of material market or economic conditions on the

results portrayed (e.g., an advertisement stating that the accounts of the

adviser’s clients appreciated in value 25% without disclosing that the market

generally appreciated 40% during the same period).

• Includes model or actual results that do not reflect the deduction of advisory

fees, brokerage or other commissions, and any other expenses that a client

paid or would have paid.

• Fails to disclose whether and to what extent the results portrayed reflect the

reinvestment of dividends and other earnings.

• Suggests or makes claims about the potential for profit without also disclosing

the possibility of loss.

• Compares model or actual results to an index without disclosing all material

facts relevant to the comparison (e.g., an advertisement that compares model

results to an index without disclosing that the volatility of the index is materially

different from that of the model portfolio).

• Fails to disclose any material conditions, objectives, or investment strategies

used to obtain the results portrayed (e.g., the model portfolio contains equity

stocks that are managed with a view towards capital appreciation).

• Fails to prominently disclose the limitations inherent in model results,

particularly the fact that such results do not represent actual trading and that

they may not reflect the impact that material economic and market factors might

have had on the adviser’s decision-making if the adviser was in fact managing

clients’ money.

• Fails to disclose, if applicable, that the conditions, objectives, or investment

strategies of the model portfolio changed materially during the period of time

portrayed in the advertisement and, if so, the effect of any such change on the

results portrayed.

• Fails to disclose, if applicable, that any of the securities contained in, or the

investment strategies followed with respect to, the model portfolio do not relate,

or only partially relate, to the type of advisory services currently offered by the

adviser (e.g., the model includes some types of securities that the adviser no

longer recommends for its clients).

• Fails to disclose, if applicable, that the adviser’s clients had investment results

materially different from the results portrayed in the model.

Ohio Investment Adviser Handbook

32

• Fails to prominently disclose, if applicable, that the results portrayed relate only

to a select group of the adviser’s clients, the basis on which the selection was

made, and the effect of this practice on the results portrayed, if material.

An adviser must create and retain all documents necessary to substantiate any

performance information contained in advertisements or communications.

Investment Advisory Contracts and Compensation

(OAC 1301:6-3-15.1(I))

• All advisory contracts shall be in writing and signed and dated by the client and

the adviser.

• The contract should clearly state that the contract may not be assigned without

the client’s consent. OAC 1301:6-3-15.1(A)(2) defines “assignment” generally

to include any direct or indirect transfer of an investment advisory contract by

the investment adviser to another adviser, entity, or firm. A transaction that

does not result in a change of actual control or management of the investment

adviser (e.g., a reorganization for purposes of changing an adviser’s state of

incorporation), would not be deemed to be an assignment for these purposes.

• OAC 1301:6-3-15.1(I)(1)(c) provides that if an investment adviser is organized

as a partnership, the advisory contract must provide that the adviser will notify

the client of a change in its partnership makeup.

• OAC 1301:6-3-15.1(I)(1)(d) prohibits the use of mandatory arbitration of

disputes. For advisory contracts that had a mandatory arbitration clause and

were entered into before the rule became effective (prior to September 30,

2021), the adviser must create a new agreement without the arbitration clause.

The new agreement must be signed by the adviser and client. Alternatively, the

adviser can amend the original agreement voiding the mandatory arbitration

clause. The amendment must also be signed by the adviser and client.

Advisory contracts should describe the specific services that the adviser is to provide to

the client. Descriptions such as “investment advisory services” do not provide adequate

detail.

If client fees are pre-paid, the contract should contain a provision for the pro rata refund

of fees if the contract is terminated.

If the adviser has trading authority but does not have discretionary authority, it is

recommended that the adviser contract include language that the adviser cannot trade

without prior approval of the customer.

Ohio Investment Adviser Handbook

33

Ohio Administrative Code 1301:6-3-44(E)(1)(e) makes it unlawful for any investment

adviser to use any condition, stipulation, or provision binding upon any person to waive

compliance within any provision of Chapter 1707 of the ORC or any rule promulgated

thereunder. This includes the use of hedge clauses, or disclaimers absolving the IA from

responsibility or accuracy of the information obtained, which would lead a client to believe

that any rights have been waived.

Supervision and Compliance Manual

(OAC 1301:6-3-15.1 (D))

Every investment adviser licensed by the Division shall reasonably supervise its

investment adviser representatives and other persons employed or associated with the

investment adviser.

Part of the supervision obligation requires the investment adviser to adopt and implement

written policies and procedures reasonably designed to prevent violations by the adviser

and its supervised person of the Ohio Securities Act and the administrative rules

promulgated by the Division. These written policies and procedures are often referred to

as the adviser’s “compliance manual.”

Compliance considerations must be relevant to the operations of the adviser, and not

simply an “off the shelf” version adopted without modifications tailored to the activities of

the adviser.

In connection with adopting and implementing the written compliance program, an adviser

must designate a person, who is a supervised person, as the “Chief Compliance Officer”

(“CCO”) responsible for administering the program.

The CCO should establish procedures for those they supervise to:

• prevent violations from occurring;

• detect violations that have occurred; and

• promptly correct any violations that have occurred.

Compliance Manual

The IA is required to review, no less frequently than annually, the adequacy of the

policies and procedures and their effectiveness. In addition, you are required to

document, in writing, evidence of the annual review, sign and confirm receipt of the policy

by employees.

Ohio Investment Adviser Handbook

34

Advisers licensed with the Division have an obligation to establish, maintain, and enforce

written policies and procedures reasonably designed to prevent and detect any violation

by its investment adviser representatives or other persons, employed by or associated

with, the investment adviser. The Division cannot provide a standard template for a

compliance manual. The following is a sample list of the most common fiduciary and

regulatory obligations of an adviser that should be addressed in the firm’s written