-1-

©2020 Discover Bank, Member FDIC

CMASECDI063020

This is an example of terms that were available to recent applicants as of 03/31/20.

This Pricing Schedule is part of the Cardmember Agreement.

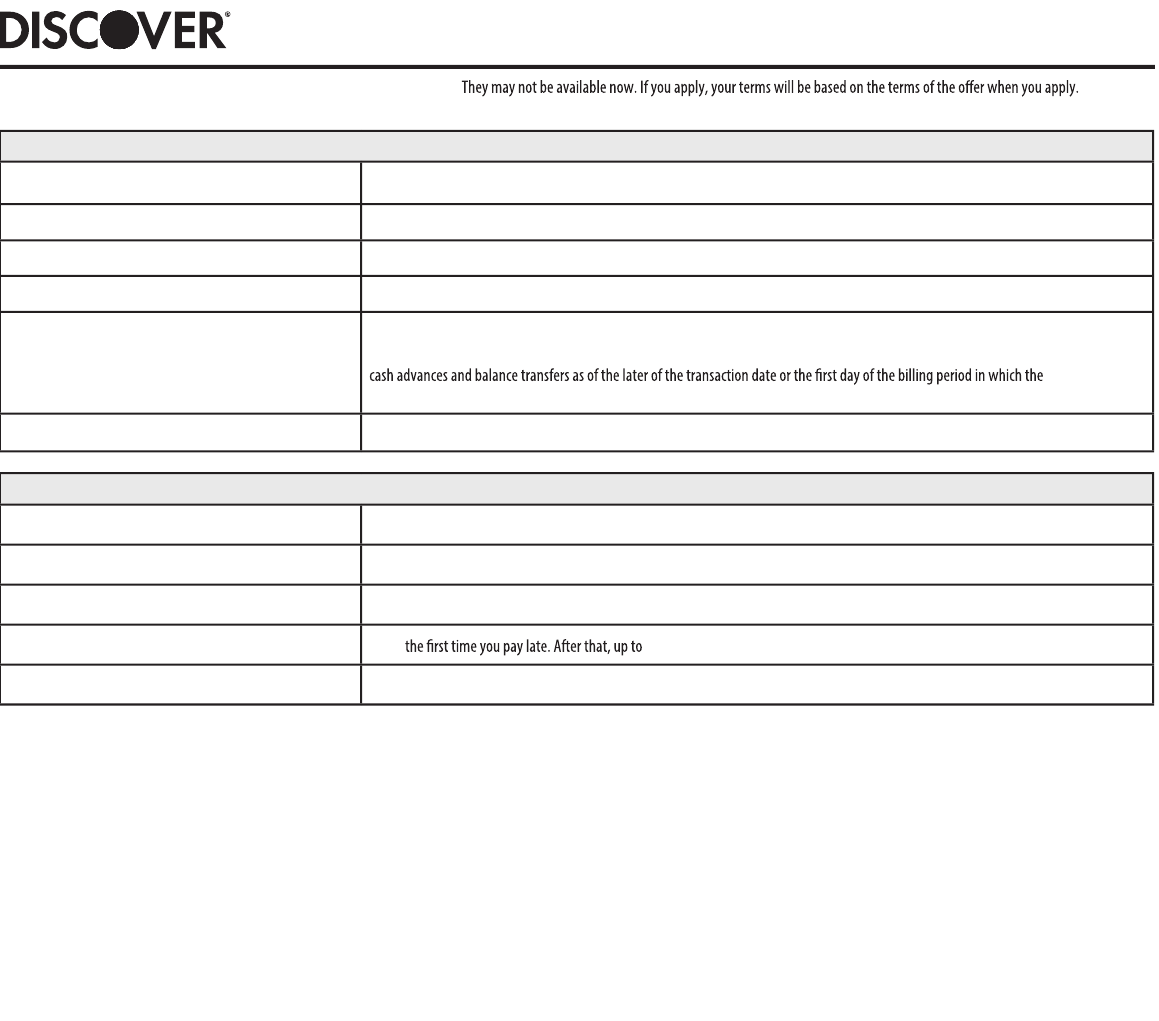

PRICING SCHEDULE

Interest Rates and Interest Charges

Annual Percentage Rate (APR) for Purchases

24.49%. This APR will vary with the market based on the Prime Rate.

1

APR for Balance Transfers

24.49%. This APR will vary with the market based on the Prime Rate.

1

APR for Cash Advances

26.49%. This APR will vary with the market based on the Prime Rate.

1

Penalty APR and When It Applies None

Paying Interest

Your due date is at least 25 days after the close of each billing period (at least 23 days for billing periods that begin in February). We will

not charge you any interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on

transaction

posted to your Account.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $0.50.

Fees

Annual Fee None

Balance Transfer Fee 5% of the amount of each transfer.

Cash Advance Fee Either $10 or 5% of the amount of each cash advance, whichever is greater.

Late Fee None

$39.

Returned Payment Fee

Up to $39.

How We Will Calculate Your Balance: We will use a method called “daily balance (including current transactions)”. See the Cardmember Agreement for details.

1

The purchase and balance transfer APR is equal to the Prime Rate plus a margin of 19.74%.

The Cash Advance APR is equal to the Prime Rate plus a margin of 21.74%.

-1-

©2020 Discover Bank, Member FDIC

CMANPRDI033120

06/30/20.

24.99%.

22.99% .

22.99% .

SECURITY AGREEMENT

This is the Security Agreement for your Discover it

®

Secured Credit Card Account (“Account”). The words “you,” “your,” and “yours” mean you and any other person(s) who

are contractually liable under the Cardmember Agreement governing the Account. The words “our,” “us,” and “we” mean Discover Bank. “Business days” are Monday through

Friday, excluding Federal Reserve Bank holidays.

Security Deposit Account

In consideration of and as a condition to our opening the Account for you and other good and valuable consideration, you are providing funds from an account in your name to

serve as security for your Account (“Funds”). We will hold these Funds in an account (“Security Deposit Account”) under our exclusive control. You must maintain this Security

Deposit Account as security for the Account, and you grant us a security interest in the Security Deposit Account. This Security Deposit Account will include any and all future

extensions, renewals, or replacements of the Security Deposit Account. No portion of the Security Deposit Account may be used to secure other loans. The minimum amount

required to be deposited is the amount of your initial Account credit line but will not be less than $200. You may make a transfer to the Security Deposit Account solely for

purposes of funding your required security deposit. The Security Deposit Account will be solely owned by you. Funds in Discover Bank Security Deposit Accounts are insured by the

Federal Deposit Insurance Corporation (“FDIC”) up to the maximum allowable limits. For more detailed information on FDIC coverage, contact the FDIC directly at 1-877-ASKFDIC

(1-877-275-3342), (TDD: 1-800-925-4618) or visit www.fdic.gov. Discover will maintain separate records to account for your Funds.

Withdrawals

You will not be permitted to make withdrawals from the Security Deposit Account. (See Return of Funds Section below for terms and conditions regarding return of the Funds

and closure of your Account.)

Additional Funds

Other than depositing Funds to secure your Account, you will not be permitted to make deposits to the Security Deposit Account.

Security Deposit Account

Statements

You will get a monthly Security Deposit Account statement as part of your Account statement.

Electronic Fund Transfers

to or from your Security

Deposit Account

You may fund your Security Deposit Account with an electronic fund transfer (“Transfer”). If we do not complete a Transfer to your Security Deposit Account on time or in the

correct amount according to our agreement with you, we will be liable for your losses or damages. However, we will not be liable if circumstances beyond our control (such as

fire or flood) prevent the transfer, despite reasonable precautions that we have taken. In case of errors or questions about your funding Transfers call us at 1-800-347-3085 or

write us at P.O. Box 30943, Salt Lake City, UT 84130-0943 as soon as you can, if you think your statement is wrong or if you need more information about a funding Transfer

listed on the statement. We must hear from you no later than 60 days after we sent the FIRST statement on which the problem or error appeared. (1) Tell us your name and

Account number. (2) Describe the error or the Transfer you are unsure about, and explain as clearly as you can why you believe it is an error or why you need more information.

(3) Tell us the dollar amount of the suspected error. If you tell us orally, we may require that you send us your complaint or question in writing within 10 business days. We will

determine whether an error occurred within 10 business days after we hear from you and will correct any error promptly. If we need more time, however, we may take up to 45

days to investigate your complaint or question. If we decide to do this, we will credit your Security Deposit Account within 10 business days for the amount you think is in error (if

applicable), during the time it takes us to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within 10 business days,

we may not credit your Security Deposit Account (if applicable). For errors involving a new Security Deposit Account, we may take up to 90 days to investigate your complaint or

question. For a new Security Deposit Account, we may take up to 20 business days to credit your Security Deposit Account (if applicable) for the amount you think is in error. We

will tell you the results within three business days after completing our investigation. If we decide that there was no error, we will send you a written explanation. You may ask

for copies of the documents that we used in our investigation.

Pledge and Grant of

Security Interest

You understand that granting us a security interest in the Security Deposit Account and the Funds is a necessary condition for opening your Account. As security for the prompt

payment and performance of all your obligations to us arising pursuant to the Account (“Obligations”), you hereby grant a security interest to us in all of your right, title, and

interest in the Security Deposit Account and any and all Funds, including all proceeds of and additions to the Security Deposit Account and the Funds. We may increase or decrease

your Account credit line and no such action shall change the fact that the Security Deposit Account and the Funds are held by us as security for the Obligations. You represent that

there are no current lawsuits or bankruptcy proceedings that might affect our interest in the Security Deposit Account or the Funds. You have not and will not attempt to transfer

or offer any interest in the Security Deposit Account or the Funds to any person other than us. You and we acknowledge that subject to our possession of and security interest in

the Security Deposit Account and the Funds, you retain beneficial ownership of the Security Deposit Account and the Funds for FDIC insurance purposes.

Interest on Funds

No interest will be paid on the Funds. If we do pay interest in the future, we will add it to the Security Deposit Account.

Application of Funds to

the Account

If you are in default under the Cardmember Agreement or the Account is closed for any reason, you authorize us at any time(s) to withdraw all or any portion of the Funds from

the Security Deposit Account and apply them to reduce your Obligations. Any such application of Funds will not constitute any part of the Minimum Payment Due under the

Cardmember Agreement. You will continue to be responsible for making payments as required under the Cardmember Agreement and for repaying any outstanding Obligations.

Our rights under this Security Agreement are in addition to any others we have under applicable law. We may make settlements or compromises on the Security Deposit Account,

transfer the Security Deposit Account to our name, or exercise ownership rights on the Security Deposit Account. We are not required to notify you of any of the above.

Return of Funds

If we determine that you qualify for return of any Funds from the Security Deposit Account, we will return these Funds to you by a method we deem sufficient. If your Account is

closed, we will return any excess Funds that remain in the Security Deposit Account after repayment of all Obligations. We generally return these excess Funds within ten days

after the end of the second billing period following the time that Funds are initially applied to reduce your Obligations. If we mail a check to you, we will mail it to your mailing

address on file with us for the Security Deposit and Card Accounts. In the event of your death, we will not release Funds on deposit unless all Obligations have been repaid and

all legal documents we require are delivered to us.

Condentiality

We will disclose information to third parties about your Security Deposit Account or any transfers you make: (a) where it is necessary for completing a transfer, or (b) in order to

verify the existence and condition of your Security Deposit Account for a third party, or (c) in order to comply with government agency or court orders, or (d) if you give us your

written permission, or (e) as permitted by the privacy notice we have provided to you.

Legal Proceedings

We may comply with any writ of attachment, adverse claim, garnishment, tax levy, restraining order, subpoena, warrant or other legal proceeding involving your Security Deposit

Account which we believe to be valid. If your Account, your Security Deposit Account, or your Funds become involved or are likely to become involved in a legal proceeding,

you understand that the entire balance of your Funds in the Security Deposit Account may be restricted until the matter has been resolved. Such proceedings are subject to our

security interest. We shall be entitled to rely upon the representations, warranties, and statements made in such legal proceedings. You agree to hold harmless and indemnify us

for any losses, expenses and costs, including reasonable attorneys’ fees, incurred by us as a result of complying with such legal proceedings. In addition to the events of default

set forth in the Cardmember Agreement, you will be in default under the Cardmember Agreement if we are served or become involved with a legal proceeding regarding the

Funds or Security Deposit Account.

Miscellaneous

This Security Agreement and our security interest and rights as pledge hereunder are governed by Delaware law. We may, in our sole discretion, assign the Security

Deposit Account and our rights and obligations under this Security Agreement. If we use an attorney to defend or enforce our rights under this Security Agreement or

to perform any legal services in connection with this Security Agreement, we may charge you our legal costs as permitted by law. This Security Agreement supplements

the Cardmember Agreement. The other terms of the Cardmember Agreement apply to this Security Agreement, and as such disputes regarding the terms of this Security

Agreement are subject to Arbitration as set forth in the Cardmember Agreement. The terms of this Security Agreement shall survive and continue to apply to the

Security Deposit Account following closure of the Account or the Security Deposit Account, and shall be binding on you even if you cancel your Account or do not accept

the Cardmember Agreement as permitted in the Cardmember Agreement. If any part of the Security Agreement is invalid, the rest of the Security Agreement will remain in effect.

-2-

CARDMEMBER AGREEMENT

Thank you for choosing Discover

®

card. This Agreement explains the current terms and conditions of your Account. The enclosed Pricing Schedule is part of this Agreement. Please read this Agreement,

including the Pricing Schedule, carefully. Keep them for your records. Contact us if you have any questions. We have included a “Definitions” section for your reference on page 5.

ACCEPTANCE OF AGREEMENT

You accept this Agreement if you do not cancel your Account within 30 days after receiving a Card. You also accept this Agreement if you or an Authorized User use

the Account. You may, however, reject the “Arbitration of Disputes” section as explained in that section.

CHANGES TO YOUR AGREEMENT

The rates, fees and terms of this Agreement may change from time to time. We may add or delete any term to this Agreement. If required by law, we will give you

advance written notice of the change(s) and a right to reject the change(s). We will not charge any fee or interest charge prohibited by law.

USING YOUR ACCOUNT

Permitted Uses You may use your Account for Purchases, Balance Transfers and Cash Advances. You may not use it for illegal transactions.

Authorized Users You may request additional Cards for Authorized Users to make transactions on your Account. You must notify us if you wish to cancel the authority of an Authorized

User to use your Account. You are responsible for all charges made by your Authorized Users.

Joint Accounts If your Account is a joint Account

• each of you agrees to be liable individually and jointly for the entire amount owed on the Account; and

• any notice we mail to an address provided by either of you for the Account will serve as notice to both of you.

Checks If we provide you with Checks, we will tell you whether we will treat the Check as a Purchase, Balance Transfer or Cash Advance. You may not use these Checks to

pay any amount you owe us.

Credit Authorizations We may not authorize a transaction for security or other reasons. We will not be liable to you if we decline to authorize a transaction or if anyone refuses your Card,

Check or Account number.

Credit Lines We will tell you what your Account credit line is. You must keep your Account

balance below your Account credit line. If you do not, we may request immediate

payment of the amount by which you exceed it. We may establish a lower credit line

for Cash Advances. We may increase or decrease your Account credit line or your

Cash Advance credit line without notice. We may delay increasing your available

credit by the amount of any payment that we receive for up to 10 business days.

FEES (See your Pricing Schedule for Additional Fees)

Late Fee We will not charge a Late Fee the first time you do not make the Minimum Payment Due by the Payment Due Date. After that, if you do not pay the Minimum Payment

Due by the Payment Due Date, we will charge you a Late Fee. The fee is $28 if you were not charged a Late Fee during any of the prior six billing periods. Otherwise,

the fee is $39. This fee will never exceed the Minimum Payment Due that was due immediately prior to the date on which the fee was assessed.

Returned Payment Fee If you make a payment that is not honored by your financial institution, we will charge you a Returned Payment Fee even if the payment is honored after we re-submit

it. The fee is $28 if you were not charged a Returned Payment Fee during any of the prior six billing periods. Otherwise, the fee is $39. This fee will never exceed the

Minimum Payment Due that was due immediately prior to the date on which the payment was returned to us.

ANNUAL PERCENTAGE RATES (“APRs”) (See your Pricing Schedule for the APRs that apply to your Account)

Variable APRs Your Pricing Schedule may include variable APRs. These APRs are determined by

adding the number of percentage points that we specify to the Prime Rate. Variable

APRs will increase or decrease when the Prime Rate changes. The APR change

will take effect on the first day of the billing period that begins during the

same calendar month that the Prime Rate changes. An increase in the APR will

increase your interest charges and may increase your Minimum Payment Due.

Penalty APR None

MAKING PAYMENTS

Payment Instructions • You must pay in U.S. dollars. Please do not send cash. Sending cash is not

allowed. All checks must be drawn on funds on deposit in the U.S.

• You must pay us for all amounts due on your Account. This includes charges

made by Authorized Users.

• We may refuse to accept a payment in a foreign currency. If we do accept it,

we will charge your Account our cost to convert it to U.S. dollars.

• We can accept late payments, partial payments or payments marked

“ payment in full” or with any other restrictive endorsement without

losing any of our rights under this Agreement.

• We credit your payments in accordance with the terms contained on your

billing statement.

• If you mail your payment to an address other than the address designated on

your billing statement, there may be a delay in processing and crediting the

payment to your Account.

• If a third party makes a payment on your Account and we return all or a part

of such payment, then we may adjust your Account for any amount returned.

We reserve the right to defend ourselves against any demand to return funds

we have received, and may agree to a compromise of the demanded amount

as part of a settlement.

Minimum Payment Due You may pay the entire New Balance shown on your billing statement at any time. Each

billing period you must pay at least the Minimum Payment Due by the Payment Due Date

shown on your billing statement. The Minimum Payment Due will be the greater of:

• $20; or

• Any amount past due plus the greater of:

– 3% of the New Balance shown on your billing statement (excluding any Interest

Charges and Late Fee shown on your billing statement); or

– $15, plus any of the following charges as shown on your billing statement:

fees for any debt protection product that you enrolled in on or after 2/1/2015;

Interest Charges; and Late Fees (not to exceed 4% of the New Balance).

The Minimum Payment Due may also include amounts by which you exceed your

Account credit line. It will never exceed the New Balance. When we calculate

the Minimum Payment Due, we may subtract from the New Balance certain fees

added to your Account during the billing period. The Minimum Payment Due is

rounded up to the nearest dollar.

How We Apply Payments We apply payments and credits at our discretion, including in a manner most

favorable or convenient for us. In all cases, we will apply payments and credits as

required by applicable law.

Each billing period, we will generally apply amounts you pay that exceed the

Minimum Payment Due to balances with higher APRs before balances with lower

APRs as of the date we credit your payment.

-3-

EBZ_20_758807_Ag reementUpdatesF orCFPB Filing_T&Cs_Secured

-4-

INTEREST CHARGES

How We Calculate Interest

Charges—Daily Balance

Method (including current

transactions)

We calculate interest charges each billing period by first figuring the “daily balance”

for each Transaction Category. Transaction Categories include standard Purchases,

standard Cash Advances and different promotional balances, such as Balance Transfers.

How We Figure the Daily Balance for Each Transaction Category

• We start with the beginning balance for each day. The beginning balance for the

first day of the billing period is your balance on the last day of your previous billing period.

• We add any interest charges accrued on the previous day’s daily balance and any

new transactions and fees. We add any new transactions or fees as of the later of

the Transaction Date or the first day of the billing period in which the transaction

or fee posted to your Account.

• We subtract any new credits and payments.

• We make other adjustments (including those adjustments required in the “Paying

Interest” section).

How We Figure Your Total Interest Charges

• We multiply the daily balance for each Transaction Category by its daily periodic

rate. We do this for each day in the billing period. This gives us the interest charges

for each Transaction Category. To get a daily periodic rate, we divide the APR that

applies to the Transaction Category by 365.

• We add up all the daily interest charges. The sum is the total interest charge for

the billing period.

How We Include Fees

We add Balance Transfer Fees to the applicable Balance Transfer Transaction

Category. We add Cash Advance Fees to the applicable Cash Advance Transaction

Category. We add all other fees to the standard Purchase Transaction Category.

Paying Interest When Interest Charges Begin

We begin to impose interest charges on a transaction, fee or interest charge from

the day we add it to the daily balance. We continue to impose interest charges

until you pay the total amount you owe us. You can avoid paying interest on

Purchases as described below. However, you cannot avoid paying interest on

Balance Transfers or Cash Advances.

How to Avoid Paying Interest on Purchases (“Grace Period”)

If you paid the New Balance on your previous billing statement by the Payment Due

Date shown on that billing statement, we will not impose interest charges on new

Purchases, or any portion of a new Purchase, paid by the Payment Due Date on

your current billing statement. New Purchases are Purchases that first appear on

the current billing statement.

How We Apply Payments May Impact Your Grace Period

If you do not pay your New Balance in full each month, then, depending on the balance

to which we apply your payment, you may not get a grace period on new Purchases.

OTHER IMPORTANT INFORMATION

Default You are in default if:

• you file bankruptcy or another insolvency proceeding is filed by you or against you;

• we have a reasonable belief that you are unable or unwilling to repay your

obligations to us;

• you die or are legally declared incompetent or incapacitated;

• you fail to comply with the terms of this Agreement or any Agreement with us or

an Affiliate, including failing to make a required payment when due, exceeding

your Account credit line or using your Card or Account for an illegal transaction.

If you are in default, we may declare the entire balance of your Account immediately

due and payable without notice.

Collection Costs If we use an attorney to collect your Account, we may charge you our legal costs as permitted by law. These include reasonable attorneys’ fees, court or other collection

costs, and fees and costs of any appeal.

Merchant Disputes If you have a dispute with a merchant, you may request a credit to your Account. If we resolve the dispute in your favor, we will issue a credit to your Account. You assign to

us your claim for the credited amount against the merchant and/or any third party. At our request, you agree to provide this assignment in writing.

Automatic Account

Information Updates

You may set up automatic billing or store your Account information with an Affiliate, merchant, wallet provider, or other third party (“Permitted Party”). If you do, you

authorize us to share your Account information, which may include your rewards account balance, with the Permitted Party, regarding the use of your Account. If your Account

information changes, which may include your billing address, you authorize us to provide this updated information to any such Permitted Party at our discretion. You must

contact the Permitted Party directly or remove your credit card information from the Permitted Party website if you wish to stop automatic billing or Account updates.

Our Privacy Policy We send you our Privacy Policy when you open your Account and annually. Contact

us or visit Discover.com if you would like a copy. Please read it carefully. It summarizes:

• the personal information we collect;

• how we safeguard its confidentiality and security;

• when it may be shared with others; and

• how you can limit our sharing of this information.

Credit Reporting

Agency Information

You authorize us to review your credit, employment, and income for the purpose of

this Account, as well as to consider you for other products and services. We may report

the status and payment history of your Account to credit reporting agencies and other

creditors. We normally report to credit reporting agencies each month.

If you believe that information we reported is inaccurate or incomplete, please write us

at Discover, P.O. Box 30939, Salt Lake City, UT 84130-0939. Please include your name,

address, home phone number and Account number.

Our Communications

with You

You agree that we, our Affiliates, and agents, including service providers (“Authorized

Parties”) may contact you, including calls, text message or email, about any current

or future accounts or applications, with respect to all products you have with us at

any phone number or email (i) you have provided to us, (ii) from which you contacted

us, or (iii) which we obtained and believe we can reach you at, even if your phone

provider may charge you message and data rates for calls or texts. You agree that the

Authorized Parties may record or monitor any calls between you and the Authorized

Parties. You agree to notify us if you change or discontinue using any phone number

you provide. You agree that the Authorized Parties may contact you using an

automatic dialer or pre-recorded voice message. If you no longer wish to be contacted

on your cell phone by an automated dialer or pre-recorded voice message, you must

provide us written notice cancelling your consent at this address: Discover Bank, P.O.

Box 30937, Salt Lake City, UT 84130-0937. The written notice must include: your

name, mailing address, the last four digits of your Account number and the specific

cell phone number(s) for which you would like to cancel your consent to be contacted

by an automated dialer or pre-recorded voice message.

Unauthorized Use You must notify us immediately if:

• your Card is lost or stolen; or

• you believe someone is using your Account or a Card without your permission.

Cancellation of Your Account • You may cancel your Account. You will remain responsible for any amount you

owe us under this Agreement.

• Any joint Accountholder may cancel a joint Account. However, both of you will

remain responsible for paying all amounts owed.

• We may cancel, suspend or not renew your Account at any time without notice.

Purchases and Cash Advances

in Foreign Currencies

If you make a Purchase or Cash Advance in a foreign currency, we will convert

it to U.S. dollars using a rate we choose. This rate will either be a government-

mandated rate, a government-published rate or the interbank exchange rate,

depending on the country and currency in which the transaction is made. We

use the rate in effect on the conversion date for the transaction. This rate may

be different than the rate in effect on the Transaction Date for the transaction.

EBZ_20_758807_Ag reementUpdatesF orCFPB Filing_T&Cs_Secured

-5-

Governing Law This Agreement is governed by applicable federal law and by Delaware law. However, in the event you default and we file a lawsuit to recover funds loaned to

you, the statute of limitations of the state where the lawsuit is filed will apply, without regard to that state’s conflicts of laws principles or its “borrowing statute.”

Severability Except as set forth in the “Arbitration” section, if any part of this Agreement is found to be invalid, the rest of it will still remain in effect.

Enforcing this Agreement We may delay enforcing or not enforce any of our rights under this Agreement without losing or waiving any of them.

Assignment of Account We may sell, assign or transfer your Account or any portion of it without notice to you. You may not sell, assign or transfer your Account without first obtaining our

prior written consent.

MILITARY BORROWERS

Statement of MAPR Federal law provides important protections to members of the Armed Forces and their dependents relating to extensions of consumer credit. In general, the cost

of consumer credit to a member of the Armed Forces and his or her dependent may not exceed an Annual Percentage Rate of 36 percent. This rate must include, as

applicable to the credit transaction or account: (1) the costs associated with credit insurance premiums; (2) fees for ancillary products sold in connection with the

credit transaction; (3) any application fee charged (other than certain application fees for specified credit transactions or accounts); and (4) any participation fee

charged (other than certain participation fees for a credit card account). If you would like more information about whether this section applies to you, please contact

us at 1- 844- DFS- 4MIL (1-844-337-4645) anytime 24/7. If calling outside the U.S. you can contact us at +1-801-451-3730.

Oral Disclosures Before agreeing to this Agreement, in order to hear important disclosures and payment information about this Agreement, please call 1- 844- DFS- 4MIL

(1-844-337-4645) anytime 24/7. If calling outside the U.S. you can contact us at +1-801-451-3730.

CONTACT US

Unless we tell you otherwise, you can notify us:

• by phone at 1-800-347-3085 or

• in writing to Discover, P.O. Box 30943, Salt Lake City, UT 84130-0943.

When writing, please include your name, address, home phone number and

Account number. You must contact us within 15 days after changing your e-mail

address, mailing address or phone number.

DEFINITIONS

“Account” means your Discover card account.

“Afliate” means our parent corporations, subsidiaries and affiliates.

“ Authorized User” means any person you authorize to use your Account or

a Card, whether you notify us or not.

“ Balance Transfer” means a balance transferred from another creditor to

your Account.

“ Card” means any one or more Discover cards issued to you or someone else

with your authorization.

“Cash Advance” means the use of your Account for:

• obtaining cash from participating automated teller machines, financial

institutions or other locations; and

• online gambling, or to purchase lottery tickets, money orders, casino chips, foreign

currency or similar items.

“Check” means any check we send to you to access your Account.

“ Pricing Schedule” means the document entitled, “Pricing Schedule”, which lists

the APRs that apply to your Account and other important information.

“ Prime Rate” means the highest rate of interest listed as the U.S. Prime rate in the

Money Rates section of

The Wall Street Journal

on the last business day of the month.

“ Purchase” means the use of your Account to purchase or lease goods or services

at participating merchants.

“We,” “us” and “our” refer to Discover Bank, the issuer of your Card.

“You,” “your” or “yours” refer to you and any other person(s) who are also

contractually liable under this Agreement.

“Transaction Date” means the date shown on your billing statement for a

transaction or fee.

Agreement to Arbitrate. In the event of a dispute between you

and us arising out of or relating to this Account or the relationships

resulting from this Account or any other dispute between you or

us (“Claim”), either you or we may choose to resolve the Claim by

binding arbitration, as described below, instead of in court. Any

Claim (except for a claim challenging the validity or enforceability

of this arbitration agreement, including the Class Action Waiver)

may be resolved by binding arbitration if either side requests

it. THIS MEANS IF EITHER YOU OR WE CHOOSE ARBITRATION,

NEITHER PARTY SHALL HAVE THE RIGHT TO LITIGATE SUCH

CLAIM IN COURT OR TO HAVE A JURY TRIAL. ALSO DISCOVERY

AND APPEAL RIGHTS ARE LIMITED IN ARBITRATION.

Even if all parties have opted to litigate a Claim in court, you or

we may elect arbitration with respect to any Claim made by a new

party or any new Claims later asserted in that lawsuit.

This Arbitration Provision does not apply if, on the date you submit

your Application or on the date we seek to invoke our arbitration

provision, you are a member of the Armed Forces or a dependent

of such a member covered by the federal Military Lending Act. If

you would like more information about whether you are covered

by the Military Lending Act, please contact us at 1-844-DFS-4MIL

(1-844-337-4645) or if you are calling from outside the U.S. at

+1-801-451-3730.

CLASS ACTION WAIVER. ARBITRATION MUST BE ON AN

INDIVIDUAL BASIS. THIS MEANS NEITHER YOU NOR WE MAY

JOIN OR CONSOLIDATE CLAIMS IN ARBITRATION BY OR AGAINST

OTHER CARDMEMBERS, OR LITIGATE IN COURT OR ARBITRATE

ANY CLAIMS AS A REPRESENTATIVE OR MEMBER OF A CLASS OR

IN A PRIVATE ATTORNEY GENERAL CAPACITY.

The arbitrator may award injunctive relief only in favor of the

individual party seeking relief and only to the extent necessary

to provide relief warranted by that party’s individual claim. The

arbitrator may not award class, representative or public injunctive

relief. If a court decides that applicable law precludes enforcement

of any of this paragraph’s limitations as to a particular claim

for relief, then after all appeals from that decision have been

exhausted, that claim (and only that claim) must be severed from

the arbitration and may be brought in court. Only a court, and not

an arbitrator, shall determine the validity, scope, and effect of the

Class Action Waiver.

Your Right to Go To Small Claims Court. We will not choose

to arbitrate any individual claim you bring in small claims court or

your state’s equivalent court. However, if such a claim is transferred,

removed or appealed to a different court, we may then choose to

arbitrate.

Governing Law and Rules. This arbitration agreement is governed

by the Federal Arbitration Act (FAA). Arbitration must proceed only

with the American Arbitration Association (AAA) or JAMS. The rules

for the arbitration will be those in this arbitration agreement and the

procedures of the chosen arbitration organization, but the rules in

this arbitration agreement will be followed if there is disagreement

between the agreement and the organization’s procedures. If

the organization’s procedures change after the claim is filed, the

procedures in effect when the claim was filed will apply. For a

copy of each organization’s procedures, to file a claim or for other

information, please contact:

• AAA at 1101 Laurel Oak Rd., Voorhees, NJ 08043, www.adr.org

(phone 1-877-495-4185) or

• JAMS at 620 Eighth Ave., Floor 34, New York, NY 10018,

www.jamsadr.com (phone 1-800-352-5267).

If both AAA and JAMS are completely unavailable, and if you and

we cannot agree on a substitute, then either you or we may request

that a court with jurisdiction appoint a substitute.

Fees and Costs. If you wish to begin arbitration against us but

you cannot afford to pay the organization’s or arbitrator’s costs,

we will advance those costs if you ask us in writing. Any request

like this should be sent to Discover, P.O. Box 30421, Salt Lake City,

UT 84130-0421. If you lose the arbitration, the arbitrator will

decide whether you must reimburse us for money we advanced

for you for the arbitration. If you win the arbitration, we will not

ask for reimbursement of money we advanced. Additionally, if you

win the arbitration, the arbitrator may decide that you are entitled

to be reimbursed your reasonable attorneys’ fees and costs (if

actually paid by you).

Hearings and Decisions. Arbitration hearings will take place in

the federal judicial district where you live. A single arbitrator will

be appointed.

ARBITRATION

EBZ_20_758807_Ag reementUpdatesF orCFPB Filing_T&Cs_Secured

-6-

Your Billing Rights:

Keep This Document For Future Use

This notice tells you about your rights and our responsibilities under the Fair Credit

Billing Act.

What To Do If You Find A Mistake On Your Statement

If you think there is an error on your statement, write to us at:

Discover

PO Box 30421

Salt Lake City, UT 84130-0421.

You may also contact us on the Web: https://discover.com/billingerrornotice

In your letter or on the Web, please give us the following information:

•

Account information:

Your name and account number.

•

Dollar amount:

The dollar amount of the suspected error.

•

Description of problem:

If you think there is an error on your bill, describe what you believe is wrong

and why you believe it is a mistake.

You must contact us:

• Within 60 days after the error appeared on your statement.

• By 5:00 P.M. ET on the date an automated payment is scheduled, if you want to stop payment on the

amount you think is wrong. You must notify us of any potential errors in writing or electronically. You

may call us, but if you do we are not necessarily required to investigate any potential errors and you

may have to pay the amount in question.

What Will Happen After We Receive Your Letter or Web Submission

When we receive your written or electronic notice, we must do two things:

1. Within 30 days of receiving your notice, we must tell you that we received it. We will also tell you if

we have already corrected the error.

2. Within 90 days of receiving your notice, we must either correct the error or explain to you why we

believe the bill is correct.

While we investigate whether or not there has been an error:

• We cannot try to collect the amount in question, or report you as delinquent on that amount.

• The charge in question may continue to appear on your statement.

• While you do not have to pay the amount in question, you are responsible for the remainder of

your balance.

• We can apply any unpaid amount against your credit limit.

After we nish our investigation, one of two things will happen:

• If we made a mistake: You will not have to pay the amount in question or any interest or other fees

related to that amount.

• If we do not believe there was a mistake: You will have to pay the amount in question, along with

applicable interest and fees. We will send you a statement of the amount you owe and the date

payment is due. We may then report you as delinquent if you do not pay the amount we think

you owe.

If you receive our explanation but still believe your bill is wrong, you must write to us (or visit

https://discover.com/billingerrornotice) within 10 days telling us that you still refuse to pay. If you do

so, we cannot report you as delinquent without also reporting that you are questioning your bill. We

must tell you the name of anyone to whom we reported you as delinquent, and we must let those

organizations know when the matter has been settled between us.

If we do not follow all of the rules above, you do not have to pay the first $50 of the amount you

question even if your bill is correct.

Your Rights If You Are Dissatised With Your Credit Card Purchases

If you are dissatisfied with the goods or services that you have purchased with your credit card, and you

have tried in good faith to correct the problem with the merchant, you may have the right not to pay

the remaining amount due on the purchase.

To use this right, all of the following must be true:

1. The purchase must have been made in your home state or within 100 miles of your current mailing

address, and the purchase price must have been more than $50. (Note: Neither of these are

necessary if your purchase was based on an advertisement we mailed to you, or if we own the

company that sold you the goods or services.)

2. You must have used your credit card for the purchase. Purchases made with cash advances from an

ATM or with a check that accesses your credit card account do not qualify.

If all of the criteria above are met and you are still dissatisfied with the purchase, contact us in writing

or electronically at:

Discover

PO Box 30945

Salt Lake City, UT 84130-0945

https://discover.com/billingerrornotice

While we investigate, the same rules apply to the disputed amount as discussed above. After we finish

our investigation, we will tell you our decision. At that point, if we think you owe an amount and you do

not pay, we may report you as delinquent.

The arbitrator must:

• Follow all applicable substantive law, except when contradicted

by the FAA;

• Follow applicable statutes of limitations;

• Honor valid claims of privilege;

• Issue a written decision including the reasons for the award.

The arbitrator’s decision will be final and binding except for any

review allowed by the FAA. However, if more than $100,000

was genuinely in dispute, then either you or we may choose to

appeal to a new panel of three arbitrators. The appellate panel

is completely free to accept or reject the entire original award

or any part of it. The appeal must be filed with the arbitration

organization not later than 30 days after the original award issues.

The appealing party pays all appellate costs unless the appellate

panel determines otherwise as part of its award.

Claim Notice and Special Payment. If you have a Claim, before

initiating an arbitration proceeding, you may give us written notice

of the Claim (“Claim Notice”) at least 30 days before initiating the

arbitration proceeding. The Claim Notice must include your name,

address, and account number and explain in reasonable detail the

nature of the Claim and any supporting facts. Any Claim Notice

shall be sent to us at Discover, P.O. Box 794, Deerfield, IL 60015

(or such other address as we shall subsequently provide to you).

If, and only if, (1) you submit a Claim Notice in accordance with

this agreement on your own behalf (and not on behalf of any

other party); and (2) an arbitrator, after finding in your favor in

any respect on the merits of your claim, issues you an award

that (excluding any arbitration fees or attorneys’ fees and costs

awarded by the arbitrator) is greater than the value of Discover’s

last written settlement offer made before an arbitrator was

selected, then you will be entitled to the amount of the award or

$7,500, whichever is greater. If you are entitled to the $7,500, you

will receive in addition any arbitration fees or attorneys’ fees and

costs awarded by the arbitrator.

Any arbitration award may be enforced (such as through a

judgment) in any court with jurisdiction.

Other Beneciaries of this Provision. In addition to you and

us, the rights and duties described in this arbitration agreement

apply to: our Affiliates and our and their officers, directors and

employees; any third party co-defendant of a claim subject to this

arbitration provision; and all joint Accountholders and Authorized

Users of your Account(s).

Survival of this Provision. This arbitration provision shall survive:

• closing of your Account;

• voluntary payment of your Account or any part of it;

• any legal proceedings to collect money you owe;

• any bankruptcy by you; and

• any sale by us of your Account.

You Have the Right to Reject Arbitration for this Account.

You may reject the arbitration agreement but only if

we receive from you a written notice of rejection within

30 days of your receipt of the Card after your Account is

opened. You must send the notice of rejection to: Discover,

P.O. Box 30938, Salt Lake City, UT 84130-0938. Your rejection

notice must include your name, address, phone number, Account

number and personal signature. No one else may sign the rejection

notice for you. Your rejection notice also must not be sent with

any other correspondence. Rejection of arbitration will not affect

your other rights or responsibilities under this Agreement. If

you reject arbitration, neither you nor we will be subject to the

arbitration provisions for this Account. Rejection of arbitration

for this Account will not constitute rejection of any prior or future

arbitration agreement between you and us.

ARBITRATION

EBZ_20_758807_Ag reementUpdatesF orCFPB Filing_T&Cs_Secured