PUBLIC SERVICE COMMISSION

OF MARYLAND

TEN-YEAR PLAN

(2011 – 2020)

OF ELECTRIC

COMPANIES

IN MARYLAND

Prepared for the

Maryland Department of Natural Resources

In compliance with Section 7-201

of the Maryland Public Utilities Article

February 2012

State of Maryland

Public Service Commission

Douglas R. M. Nazarian, Chairman

Harold D. Williams, Commissioner

Lawrence Brenner, Commissioner

Kelly Speakes-Backman, Commissioner

W. Kevin Hughes, Commissioner

David J. Collins Gregory V. Carmean H. Robert Erwin

Executive Secretary Executive Director General Counsel

6 St. Paul Street

Baltimore, MD 21202

Tel: (410) 767-8000

www.psc.state.md.us

This report was drafted by the Commission’s Energy Analysis and Planning Division (Crissy Godfrey,

Director), in cooperation with the Engineering Division (Jerry Hughes, Chief Engineer). Electric

companies under the Commission’s jurisdiction provided most of the data in the Appendix.

TABLE OF CONTENTS

I. INTRODUCTION ...............................................................................................................................1

II. MARYLAND UTILITY AND PJM ZONAL LOAD FORECASTS...............................................3

A. Introduction...................................................................................................................................... 3

B. PJM Zonal Forecast.......................................................................................................................... 4

C. Maryland Company Forecasts.......................................................................................................... 5

III. REGIONAL GENERATION AND SUPPLY ADEQUACY IN MARYLAND..............................7

A. Introduction...................................................................................................................................... 7

B. Maryland Generation Profile: Age and Fuel Characteristics........................................................... 9

C. Potential Generation Additions in Maryland.................................................................................. 13

D. CPCN Exemptions for Generation................................................................................................. 15

IV. TRANSMISSION INFRASTRUCTURE: PJM, MARYLAND, AND NATIONAL...................19

A. Introduction.................................................................................................................................... 19

B. Eastern Interconnection Planning Collaborative............................................................................ 19

C. The Regional Transmission Expansion Planning Protocol ............................................................ 20

D. Transmission Congestion in Maryland........................................................................................... 22

E. High Voltage Transmission Lines in PJM ..................................................................................... 24

V. DEMAND RESPONSE AND CONSERVATION AND ENERGY EFFICIENCY....................26

A. Statutory Requirements.................................................................................................................. 26

B. Demand Response Initiatives......................................................................................................... 28

C. Energy Efficiency and Conservation Programs ............................................................................. 34

D. Advanced Metering Infrastructure / Smart Grid ............................................................................ 37

E. Mid-Atlantic Distributed Resources Initiative ............................................................................... 42

VI. ENERGY, THE ENVIRONMENT, AND RENEWABLES...........................................................42

A. The Regional Greenhouse Gas Initiative........................................................................................ 42

B. The Renewable Energy Portfolio Standard Program ..................................................................... 44

C. Solar Power Requirements in Maryland ........................................................................................ 49

VII. ELECTRIC DISTRIBUTION RELIABILITY IN MARYLAND.................................................51

A. Electric Distribution Reliability Reporting, Operation and Maintenance ...................................... 51

B. Distribution Reliability Issues........................................................................................................ 53

C. Managing Distribution Outages ..................................................................................................... 58

D. Distribution Planning Process........................................................................................................ 60

VIII. MARYLAND ELECTRICITY MARKETS....................................................................................63

A. Status of Retail Electric Choice in Maryland................................................................................. 63

B. Standard Offer Service................................................................................................................... 65

IX. REGIONAL ENERGY ISSUES AND EVENTS ............................................................................66

A. Overview of PJM, OPSI, and Reliability First............................................................................... 66

B. PJM Summer Peak Events of 2010 and 2011 ................................................................................ 68

C. PJM’s Reliability Pricing Model.................................................................................................... 69

D. Region-Wide Demand Response in PJM Markets......................................................................... 71

X. PROCEEDINGS BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION.....72

i

APPENDIX

Table A-1: Utilities Providing Retail Electric Service in Maryland................................. 74

Table A-2: Number of Customers by Customer Class as of December 31, 2010............ 75

Table A-3: Typical Monthly Electric Bills in Maryland (Winter 2010)........................... 76

Table A-4(a): System Wide Peak Demand Forecast as of December 31, 2010 (MW) (Net

of DSM Programs).................................................................................................... 77

Table A-4(b): Maryland Peak Demand Forecast as of December 31, 2010 (MW) (Net of

DSM Programs)........................................................................................................ 78

Table A-4(c): System Wide Peak Demand Forecast as of December 31, 2010 (MW)

(Gross of DSM Programs) ........................................................................................ 79

Table A-4(d): Maryland Peak Demand Forecast as of December 31, 2010 (MW) (Gross

of DSM Programs).................................................................................................... 80

Table A-5(a): System Wide Energy Sales Forecast (GWh) (Net of DSM Programs)...... 81

Table A-5(b): Maryland Energy Sales Forecast (GWh) (Net of DSM Programs) ........... 82

Table A-6: Maryland Licensed Electric/Natural Gas Suppliers and Brokers as of

December 1, 2011..................................................................................................... 83

Table A-7: Transmission Enhancements by Service Area ............................................... 89

Table A-8: Renewable Projects Providing Capacity and Energy to Maryland Customers

as of December 31, 2010 .......................................................................................... 94

Table A-9: Power Plants in the PJM Process for New Electric Generating Stations in

Maryland as of December 31, 2010.......................................................................... 95

ii

LIST OF MAPS, FIGURES, TABLES, AND CHARTS

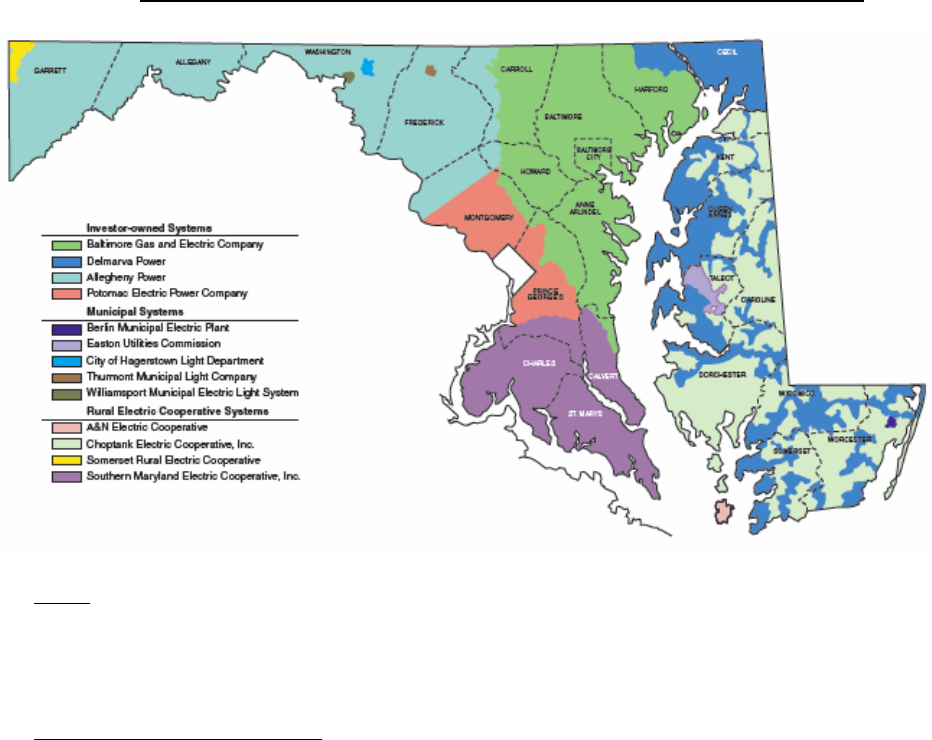

Map I.1: Maryland Utilities and their Service Territories in Maryland............................. 2

Figure II.A.1: PJM Maryland Forecast Zones................................................................... 3

Table II.B.1: Summer Peak Load (MW) Growth Rates .................................................... 4

Table II.B.2: Winter Peak Load (MW) Growth Rates....................................................... 5

Table II.C.1: Comparison of Maryland Peak Demand Forecasts....................................... 6

Table II.C.2: Comparison of Maryland Energy Sales Forecast.......................................... 6

Table III.A.1: State Electricity Imports (Year 2009) (GWh)............................................. 8

Table III.B.1: Maryland Generating Capacity Profile (Year 2010)................................... 9

Table III.B.2: Maryland Electric Power Generation Profile (Year 2009) ....................... 11

Table III.B.3: Generation by Owner, County, and Capacity (Year 2010)....................... 12

Table III.C.1: PJM Transmission Queue Active New Generating Capacity................... 15

Table III.D.1: Construction Approvals for CPCN Exempt Generation........................... 17

Table III.D.2: Number and Capacity in MW of CPCN Exempt Generating Units by

Energy Resource....................................................................................................... 18

Table V.B.1: Utilities’ Incentives to DLC Program Participants .................................... 29

Table V.B.2: Utilities’ Direct Load Program Installations; Program-to-Date as of

December 31, 2010................................................................................................... 30

Table V.B.3: Direct Load Control Program Bids into PJM BRA (MW) ........................ 30

Table V.B.4: Peak Load Reduction Forecast (MW)........................................................ 34

Table VI.A.1: Annual State CO

2

Allowance Budgets (2009 – 2014).............................. 43

Table VI.B.1: Eligible Tier 1 and Tier 2 Renewable Resources ..................................... 45

Table VI.B.2: Annual RPS Percentage Requirements by Tier........................................ 46

Table VI.B.3: RPS Alternative Compliance Fee Schedule ($/MWh) ............................. 47

Table VI.B.4: RPS Supplier Annual Report Results as of December 31, 2010.............. 48

Chart VI.B.5: Maryland RPS Eligible Capacity by State................................................ 49

Table VIII.A.1: Residential Customers Enrolled in Retail Supply.................................. 64

Table VIII.A.2: Electric Choice Enrollment in Maryland as of September 30, 2011 ..... 65

Table IX.B.1: Summer 2010 and 2011 Coincident Peaks and Zone LMP...................... 69

Table IX.C.1: RPM “Net Load” Price and Cost.............................................................. 71

iii

LIST OF ACRONYMS AND DEFINITIONS USED

ACP Alternative Compliance Penalty

AMI Advanced Metering Infrastructure

ARR Auction Revenue Right

ARRA American Recovery and Reinvestment Act of 2009

BGE Baltimore Gas and Electric Company

BRA Base Residual Auction

C&I Commercial and Industrial

CAIDI Customer Average Interruption Duration Index

CETL Capacity Emergency Transfer Limit

CETO Capacity Emergency Transfer Objective

CIS Customer Information System

CO

2

Carbon Dioxide

CPCN Certificate of Public Convenience and Necessity

CSP Curtailment Service Provider

DLC Direct Load Control

DOE United States Department of Energy

DPL Delmarva Power & Light Company

DR Demand Response or Demand Resource

DSM Demand-Side Management

DY Delivery Year

EDC Electric Distribution Company

EE&C Energy Efficiency and Conservation

EFORd Equivalent Demand Forced Outage Rate

EIA Energy Information Administration

EIPC Eastern Interconnection Planning Collaborative

EISA Energy Independence and Security Act of 2007

EISPC Eastern Interconnection State Planning Council

ELRP Economic Load Response Program

EMAAC Eastern Mid-Atlantic Area Council

EMS Energy Management System

EM&V Evaluation, Measurement, and Verification

EPA United States Environmental Protection Agency

ETR Estimated Time of Restoration

FERC Federal Energy Regulatory Commission

FTR Financial Transmission Right

GATS Generation Attributes Tracking System

GIS Geographic Information System

GW/GWh Gigawatt/Gigawatt-hours

HVAC Heating, Ventilation, and Air Conditioning

HVCS High Volume Call Service

HVDC High Voltage Direct Current

IOU Investor-Owned Utility

IRM Installed Reserve Margin

ISAC Independent State Agency Committee

ISO Independent System Operator

iv

IVR Interactive Voice Response

kV Kilovolt

kW/kWh Kilowatt/Kilowatt-hours

LDA Load Deliverability Area

LMP Locational Marginal Price

LSE Load Serving Entity

MAAC Mid-Atlantic Area Council

MADRI Mid-Atlantic Distributed Resources Initiative

MAPP Mid-Atlantic Power Pathway

MDE Maryland Department of the Environment

MDS Mobile Dispatch System

MEA Maryland Energy Administration

MW/MWh Megawatt/Megawatt-hours

NERC North American Electric Reliability Council

O&M Operation and Maintenance

OATT Open Access Transmission Tariff (PJM)

OMS Outage Management System

OPC Office of People’s Counsel (Maryland)

OPSI Organization of PJM States, Inc.

PATH Potomac-Appalachian Transmission Highline

PE The Potomac Edison Company

Pepco Potomac Electric Power Company

PJM PJM Interconnection, LLC (Pennsylvania-Jersey-

Maryland)

PJM-EIS PJM – Environmental Information Services, Inc

PSC/ MD PSC Maryland Public Service Commission

PTR Peak-Time Rebate

PUA Public Utilities Article, Annotated Code of Maryland

REC Renewable Energy Credit

RFP Request for Proposal

RGGI Regional Greenhouse Gas Initiative

RPM Reliability Pricing Model (PJM)

RPS Renewable Energy Portfolio Standard

RTEP Regional Transmission Expansion Plan

RTO Regional Transmission Organization

SAIDI System Average Interruption Duration Index

SAIFI System Average Interruption Frequency Index

SCADA Supervisory Control and Data Acquisition

SEIF Maryland Strategic Energy Investment Fund

SGIG Smart Grid Investment Grant

SMECO Southern Maryland Electric Cooperative, Inc.

SOS Standard Offer Service

SWMAAC Southwest Mid-Atlantic Area Council

TEAC Transmission Expansion Advisory Committee (PJM)

TrAIL Trans-Allegheny Interstate Line

WMS Work Management System

v

I. INTRODUCTION

Section 7-201 of the Public Utilities Article, Annotated Code of Maryland

(“PUA”), requires the Maryland Public Service Commission (“Commission” or “PSC” or

“MD PSC”) to forward a Ten-Year Plan of Electric Companies in Maryland (“Ten-Year

Plan”) to the Secretary of Natural Resources on an annual basis. This report constitutes

that effort for the 2011 – 2020 timeframe and, with exceptions as noted in the text, the

referenced data and information is as it existed as of December 31, 2010. It is a

compilation of information on long-range plans of Maryland electric utilities. This report

also includes summaries of events that have affected or may affect the electric utility

industry in Maryland in the near future.

A principal focus of the Commission is the reliability of Maryland’s electricity

supply, delivered at reasonable rates. Achieving reliability is a complex undertaking

which requires consideration of factors affecting both supply and demand. To address

these elements the Commission is taking action on several fronts: challenging wholesale

power policies at the Federal Energy Regulatory Commission (“FERC”); working with

the wholesale independent market monitor to effectuate positive market results;

evaluating the need for procuring new generation in the State; directing new utility

investment in demand response programs to reduce peak electricity demand; evaluating

conservation and energy efficiency programs to meet EmPower Maryland peak and

overall energy reductions;

1

and encouraging better use of emergency generation within

the State to promote adequate, economical, and efficient delivery of electricity services.

Section II of this plan addresses the peak demand load forecast for Maryland and

establishes the baseline load requirements for the next ten years. Section III provides

information on generation, including certificates of public convenience and necessity

(“CPCNs”), and forecasts the availability of generation to meet load requirements.

Section IV reviews transmission issues impacting Maryland, including the Department of

Energy’s National Interest Electric Transmission Corridors. Section V addresses the

options of energy efficiency, conservation, and demand response as part of Maryland’s

supply resources, and discusses the effort required to meet EmPower Maryland goals.

Proposals to deploy advanced metering infrastructure also are discussed in this section.

Because environmental issues continue to play an increasingly important role in energy

decisions, Section VI discusses Maryland’s involvement in the Regional Greenhouse Gas

Initiative and other issues involving the impact of renewable generation growth. Section

VII provides information on distribution reliability, the manner in which utilities have

managed outages, and how utilities plan to meet load requirements.

Beginning with Section VIII, we broaden our perspective and review Maryland’s

Electricity Market in general terms and its relation to Commission efforts that are

currently underway or anticipated. Section IX discusses PJM Interconnection, LLC

1

See EmPower Maryland Energy Efficiency Act of 2008, codified within MD. CODE ANN., PUB.

UTIL. § 7-211 (2011) (“EmPower Maryland”).

1

(“PJM”)

2

and the impact that market rule changes have had both regionally and in

Maryland. Section X reviews national issues and the impact generated by FERC rulings

and U.S. Department of Energy actions. Also included in the Ten-Year Plan is an

Appendix that contains a compilation of data provided by Maryland’s utilities

summarizing, among other things, demand and anticipated sales over the next 15 years.

Maryland is geographically divided into thirteen electric utility service territories.

Four of the largest are investor-owned utilities (“IOUs”), four are electric cooperatives

(two of which serve only small areas of Maryland), and five are electric municipal

operations.

3

Table A-1 in the Appendix lists the utilities providing retail electric service

in Maryland and Map I.1 below provides a geographic picture of the utilities’ service

territories.

4

Map I.1: Maryland Utilities and their Service Territories in Maryland

Source: Cumulative Environmental Impact Report 15, MD. DEP’T OF NATURAL RES., Figure 2-12,

http://esm.versar.com/pprp/ceir15/Report_2_3.htm (last updated Feb. 25, 2010).

2

PJM is a regional transmission organization that coordinates the movement of wholesale

electricity in all or parts of 13 states and the District of Columbia.

3

The St. Michaels Utilities Commission service territory was transferred to Choptank Electric

Cooperative, Inc. in October 2006.

4

The Potomac Edison Company no longer uses its “doing business name” of “Allegheny Power”

and any references within the Ten-Year Plan to Allegheny Power should be read as referencing

Potomac Edison.

2

II. MARYLAND UTILITY AND PJM ZONAL LOAD FORECASTS

A. Introduction

The foundation of an analysis for meeting Maryland’s electricity needs starts with

a forecast of the anticipated demand over a relevant planning horizon. The Commission

routinely evaluates forecasts from individual utilities, as well as the PJM forecast, which

provides separate estimates for the transmission zones shown in Figure II.A.1.

Figure II.A.1: PJM Maryland Forecast Zones

Source: PJM Load Forecast Report, PJM PLANNING (Jan. 2011),

http://www.pjm.com/planning/resource-adequacy-planning/~/media/documents/reports/2011-pjm-

load-report.ashx.

PJM sub-regions, known as zones, generally correspond with the IOU service

territories. The PJM zones include adjacent municipal and rural electric cooperatives. The

four IOUs operating in Maryland are Baltimore Gas and Electric Company (“BGE”),

Potomac Electric Power Company (“Pepco”), Delmarva Power & Light Company

(“DPL” or “Delmarva”), and The Potomac Edison Company (“PE”). PJM zones for

three of the four IOUs traverse state bounds and extend into other jurisdictions. Pepco,

DPL, and PE company data are a subset of the PJM zonal data, since PJM’s zonal

forecasts are not limited to Maryland. The BGE zone, alone, resides solely within the

State of Maryland.

PJM operates the wholesale power market that includes the entire mid-Atlantic

region and dispatches power plants to serve load on an economic bid basis, subject to

transmission capacity availability. PJM’s load forecasts drive the need for generation,

3

which impacts electric consumer prices at the retail level. The Commission closely

monitors the development of PJM regional forecasts.

While forecasts can rely on similar economic data, projections of peak demand

and energy usage can vary based upon the underlying assumptions used to generate the

forecasts. In general, the expected growth in peak demand and electricity usage is due

primarily to expected increases in population and economic activity, which have a direct

impact on electricity consumption levels. Key forecast variables include economic and

non-economic variables. Economic variables used in forecast models can include gross

domestic product, employment, energy prices, and population. Non-economic variables

can include weather normalized variables, monthly seasonal variables, ownership of

appliances, and building codes.

B. PJM Zonal Forecast

PJM’s 2011 Load Forecast Report includes long-term forecasts of peak loads and

net energy for the entire wholesale market region and each PJM sub-region (i.e., zone) –

including the four sub-regions in which Maryland resides.

5

The 2011 Load Forecast

Report concludes that the PJM region will, in aggregate, experience higher peak usage in

the summer throughout the forecast period ending 2026.

6

Tables II.B.1 and II.B.2

present comparisons in expected growth for the four PJM zones containing Maryland.

7

The 2011 Load Forecast is compared to the 2009 and 2010 Load Forecasts on a very

broad macro level for the four PJM regions roughly corresponding with the four IOU

service territories that serve Maryland. When compared, the 2011 Load Forecast shows

significant reductions in both Summer and Winter peak demand growth rates from the

previous year’s Load Forecast. The PJM zones containing BGE, DPL, and Pepco

experience their peak demands during the summer while the PJM region containing PE

experiences peak demands in the winter.

8

Table II.B.1: Summer Peak Load (MW) Growth Rates

PJM Zone

2009-2019* 2010-2020** 2011-2021***

PE 1.5% 1.4% 1.0%

BGE 1.8% 1.8% 1.3%

DPL 2.1% 1.4% 1.1%

Pepco 1.2% 1.2% 1.0%

5

PJM Load Analysis Subcommittee, PJM, available at: http://www.pjm.com/committees-and-

groups/subcommittees/las.aspx.

6

PJM Load Forecast Report, PJM, 37 (January 2011), available at:

http://www.pjm.com/committees-and-groups/subcommittees/~/media/documents/reports/2011-

pjm-load-report.ashx. The PJM RTO summer peak is forecasted to be 182,904 MW in 2026, a 15-

year increase of 28,521 MW. Id.

7

For Maryland, the four PJM regions contain all four of the State’s investor-owned utilities, the five

municipal systems, and Maryland’s four rural electric cooperatives. Id.

8

Id.

4

Table II.B.2: Winter Peak Load (MW) Growth Rates

PJM Zone 2009-2019* 2010-2020** 2011-2021***

PE 1.3% 1.3% 1.0%

BGE 1.0% 1.1% 0.8%

DPL 1.5% 1.0% 0.8%

Pepco 1.1% 1.2% 1.0%

Sources: * PJM Load Forecast Report, January 2009, Tables B-1 and B-2.

** PJM Load Forecast Report, January 2010, Tables B-1 and B-2.

***PJM Load Forecast Report, January 2011, Tablets B-1 and B-2.

C. Maryland Company Forecasts

Maryland’s electric utilities annually submit responses to Commission data

requests that include forecasts of peak and annual energy demand. The forecast

information provided by each company is summarized in the Appendices as Tables A-

4(a) – (d) and Tables A-5(a) – (b). Data requests for the current Ten-Year Plan include

responses that expand beyond a ten-year period – from 2011 through 2025. The prior

year’s submissions began and terminated one year earlier, that is, from 2010 through

2024. A comparison of the electric utility submissions for the first and last years of the

forecast period is provided to indicate, on an aggregate basis, current expectations for

peak usage in the State for electricity. The utility forecasts reflect: short-term

recessionary impacts, the utilities’ current expectations with regard to nascent demand-

side management (“DSM”) and energy efficiency programs, and the expected reductions

in energy usage attributable to these programs. Precision and certainty diminish the

longer the time period over which a forecast is generated. Comparisons are first

presented for the State in aggregate for four common future years: 2011, 2016, 2021, and

2024.

9

Additional analysis pertaining to 2011 and the period 2011 through 2021 also are

explored.

Table II.C.1 compares Maryland peak demand forecasts on an aggregate basis and

includes utility-provided estimates of currently-approved DSM and energy efficiency

measures. Actual peak demand in 2011 net of DSM programs compared to the 2010

forecasted peak demand net of DSM programs indicates that peak demand increased by

1.1%. Peak demand forecasts for this Ten-Year Plan period compared to the 2010 – 2019

Ten-Year Plan forecasted peak demand indicate that peak demands are estimated to

increase by 0.7% in 2016, 0.7% in 2021, and 0.8% in 2024.

10

9

Additional data for the 2011 to 2025 period can be located in Tables A-4 and A-5 of this Ten-Year

Plan Appendix. Corresponding data considering the 2010 to 2024 time period can be located in

last year’s Ten-Year Plan Appendix Tables A-5 and A-6.

10

Increases are a comparison strictly to last year’s submissions and not considered on a per capita

basis in keeping with the goals of EmPower Maryland.

5

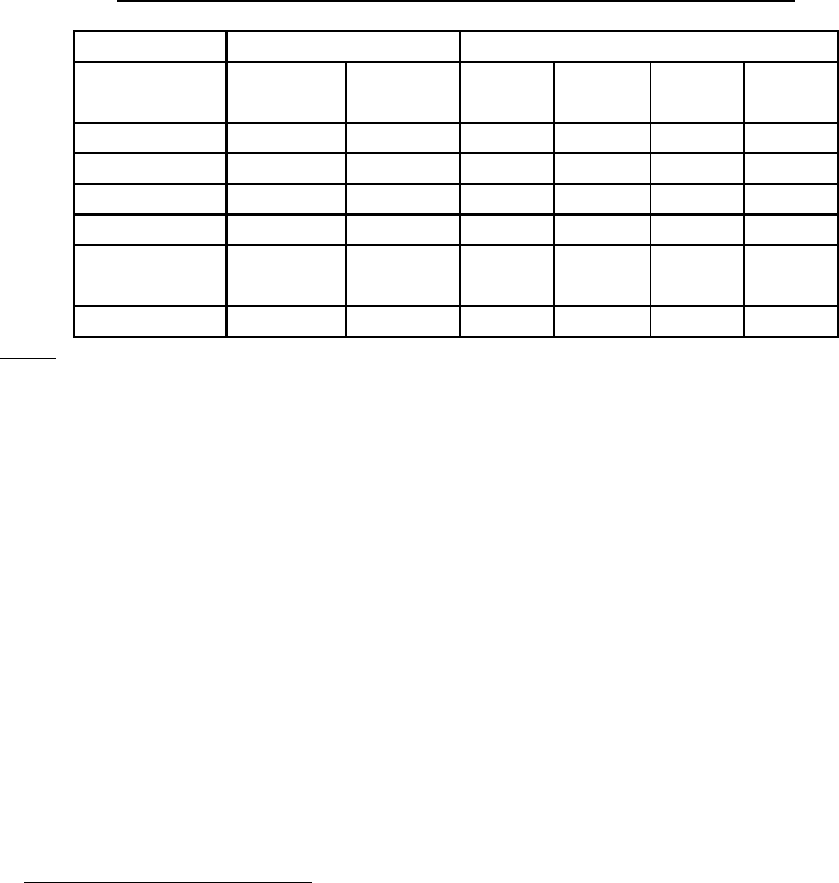

Table II.C.1: Comparison of Maryland Peak Demand Forecasts

(Net of DSM Programs; MW)

2010 - 2019 2011 - 2020

Ten-Year Plan Ten-Year Plan

2011

13,638 13,786 148 1.1

2016

13,812 13,914 102 0.7

2021

14,801 14,900 99 0.7

2024

15,381 15,511 130 0.8

Year Change %

Sources: Ten-Year Plan (2010-2019) of Electric Companies in Maryland, MD PSC,

6 (Aug. 2011), available at: http://webapp.psc.state.md.us/Intranet/Reports/2010-

2019%20Ten%20Year%20Plan.pdf. See Appendix Table A-4(b).

Table II.C.2 compares utility forecasted energy sales within the State of

Maryland. When compared to utility estimates provided last year, the electric utility

forecasts, in aggregate, project additional increases in overall annual electricity sales in

the State. During the timeframe examined, increases in energy usage trend upward

11

between 0.6% and 1.4% when compared to last year’s electric utility submissions.

Table II.C.2: Comparison of Maryland Energy Sales Forecast

(Net of DSM Programs; GWh)

2010 - 2019 2011 - 2020

Ten-Year Plan

(GWh)

Ten-Year Plan

(GWh)

2011

63,651 64,012 361 0.6

2016

66,954 66,887 -67 -0.1

2021

71,111 72,056 945 1.3

2024

73,848 74,865 1,017 1.4

Year Change %

Sources: Ten-Year Plan (2010-2019) of Electric Companies in Maryland, MD PSC,

6 (Aug. 2011), available at: http://webapp.psc.state.md.us/Intranet/Reports/2010-

2019%20Ten%20Year%20Plan.pdf. See Appendix Table A-5(b).

As reflected in Table II.C.1 and Table II.C.2, utility projections of peak demand

and of annual energy sales are currently moving in similar directions: peak demand is

increasing and annual energy sales are increasing when compared to utility estimates

provided last year. Historically, peak demand and annual energy sales have moved in

tandem.

Numerous changes have occurred or have been proposed to PJM demand

response (“DR”) programs recently. These changes include implementing a more

accurate method of measuring and verifying the quantity of demand reductions provided

11

Although the comparison of 2016 forecasted energy sales between the 2010 – 2019 TYP and the

2011 – 2020 TYP indicates a 0.1% reduction, utility data for the 2011 – 2020 TYP reflects an

increase in forecasted State energy sales in the aggregate when compared to the 2010 – 2019 TYP

forecast. See Appendix Table A-5(b).

6

and proposals to significantly expand both the time period and the seasons during which

DR participants must reduce load. The uncertainty associated with such changes leads to

less aggressive projections of future DR participation and DSM impacts.

III. REGIONAL GENERATION AND SUPPLY ADEQUACY IN MARYLAND

A. Introduction

The Commission recognizes that in order to maintain electric system reliability

and an adequate supply of electricity for customers in the future, access to adequate

electric capacity must be available to meet customer demand.

A critical requirement for reliable electric service is an appropriate level of

generation and transmission capacity to meet Maryland consumers’ energy needs. While

reliability needs may be partially met through local demand side management programs

and the import of electricity using high-voltage transmission lines, local generation must

be maintained and is essential to keeping the lights on and the power grid operating

effectively and economically. All load serving entities in the PJM region are required to

ensure they have sufficient capacity contracts to provide reliable electric service during

periods of peak demand. As of 2010, Maryland’s net summer generating capacity was

approximately 12,516 MW.

12

Maryland’s peak demand forecast for 2011 with utility

demand-side management and energy conservation measures is approximately 13,786

MW.

13

According to PJM’s established margin for necessary reserves, an additional

2,137 MW

14

is required and would result in a cumulative estimated reliability

requirement of 15,923 MW. Therefore, 3,407 MWs of estimated capacity in the

transmission system serves to meet Maryland’s requirements during periods of peak

usage in the system.

All major utility systems in the eastern half of the United States and Canada are

interconnected and operate synchronously as part of the Eastern Interconnection. PJM

operates, but does not own, the transmission systems in: (1) Maryland; (2) all or part of

12 other states; and (3) the District of Columbia. With FERC approval, PJM undertakes

this task in order to coordinate the movement of wholesale electricity and provide access

to the transmission grid for utility and non-utility users alike. Within the PJM region,

power plants are dispatched to meet load requirements without regard to operating

company boundaries. Generally, adjacent utility service territories import or export

12

See Tables III.B.1 and III.B.3.

13

See Appendix Table A-4(b).

14

The example uses an installed reserve margin (“IRM”) of 1.155 for 2010/2011, which is

applicable for planning reserves on a regional basis for the entire pool of PJM resources. IRM

establishes a level of installed capacity resources that will provide acceptable reliability levels for

the PJM region – and not on an individual state basis – considering demand forecasts, available

unforced capacity from existing generation, and the probability that a generating unit will not be

available (i.e., Equivalent Demand Forced Outage Rate (“EFORd”)). See PJM, Resource

Adequacy Planning, 2009 PJM Reserve Requirements Study, Table I - 1: Historical RRS

Parameters, 3, available at:

http://www.pjm.com/planning/resource-adequacy-

planning/~/media/documents/reports/2009-pjm-reserve-requirement-study.ashx

.

7

wholesale electricity as needed to reduce the total amount of installed capacity required

by balancing retail load and generation capacity over a regional, diversified system.

Within eastern PJM, the District of Columbia, Maryland, Delaware, New Jersey,

and Virginia continue to be net importers of electricity. Maryland imported about 40

percent of its electricity in 2009.

15

On a percentage basis, Maryland was the fifth largest

electric energy importer in the United States – surpassed by the District of Columbia,

Delaware, and Virginia in the immediate PJM area.

16

Much of the East Coast is

dependent on generation exported from states to the west of the region – many with low-

cost, largely depreciated, coal-fired generation assets. Prominent states within the PJM

region currently exporting more electricity in aggregate than consumed within each state

are Illinois, Indiana, Pennsylvania, and West Virginia.

17

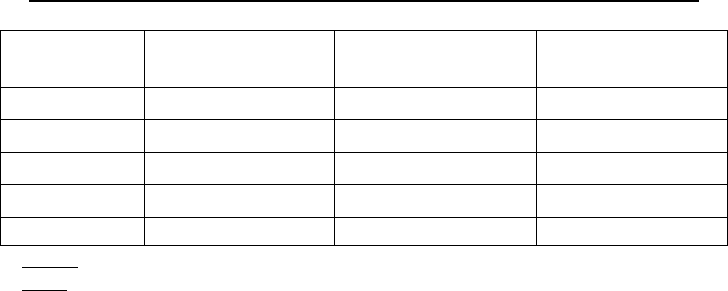

Table III.A.1: State Electricity Imports (Year 2009) (GWh)

State Retail Sales

Losses & Direct

Use

Generation Net Imports

Percent Retail

Sales Imported

DC 12,199 785 35 (12,984) 106%

Delaware 11,258 1,298 4,842 (7,714) 69%

Idaho 22,754 2,635 13,100 (12,333) 54%

Virginia 108,462 8,338 70,082 (46,719) 43%

Maryland 62,589 5,924 43,775 (24,738) 40%

California 259,584 31,858 204,776 (84,137) 32%

New Jersey 75,780 5,630 68,811 (19,598) 26%

Massachusetts 54,359 3,216 38,967 (14,036) 26%

Tennessee 94,650 7,137 79,717 (22,070) 23%

Wisconsin 66,286 5,825 59,959 (12,153) 18%

Minnesota 64,004 6,891 52,492 (10,611) 17%

North Carolina 127,658 11,672 118,407 (20,922) 16%

Louisiana 78,670 24,670 90,994 (12,346) 16%

Ohio 146,300 11,550 136,090 (21,755) 15%

Georgia 130,766 15,814 128,698 (17,881) 14%

Florida 224,750 21,646 217,952 (28,444) 13%

Colorado 51,036 4,345 50,566 (4,815) 9%

Mississippi 46,049 5,563 48,701 (2,911) 6%

New York 140,034 3,026 133,151 (7,606) 5%

Alaska 6,270 770 6,702 (337) 5%

Kentucky 88,809 5,397 90,630 (3,576) 4%

Hawaii 10,126 1,166 11,011 (282) 3%

Michigan 98,121 10,076 101,203 (1,357) 1%

Texas 345,296 54,439 397,168 (2,456) 1%

Source: State Electricity Profiles 2009, U.S. ENERGY INFORMATION ADMINISTRATION, Table 10, (April 15,

2011) available at: http://www.eia.gov/cneaf/electricity/st_profiles/sep2009.pdf.

15

State Electricity Profiles 2009, U.S. ENERGY INFORMATION ADMINISTRATION, Table 10, (April 15,

2011) available at: http://www.eia.gov/cneaf/electricity/st_profiles/sep2009.pdf.

16

Id.

17

Id.

8

B. Maryland Generation Profile: Age and Fuel Characteristics

Most electric generating capacity in Maryland is provided by coal-fired power

plants, which contribute approximately 39 percent of the summer peak capacity available

in-State. The vast majority of the State’s coal-fired generation capacity, approximately

70 percent, is provided by power plants thirty-one or more years old. Approximately 41

percent of all capacity in Maryland burns oil or gas as a fuel source, and the majority of

these facilities are aging. Overall, approximately 67 percent of Maryland generating

capacity has been in operation for over 30 years. As indicated in Table III.B.1, only

about 16 percent of the State’s summer generating capacity has been constructed in the

past 20 years, and only about 7 percent has been constructed in the last 10 years.

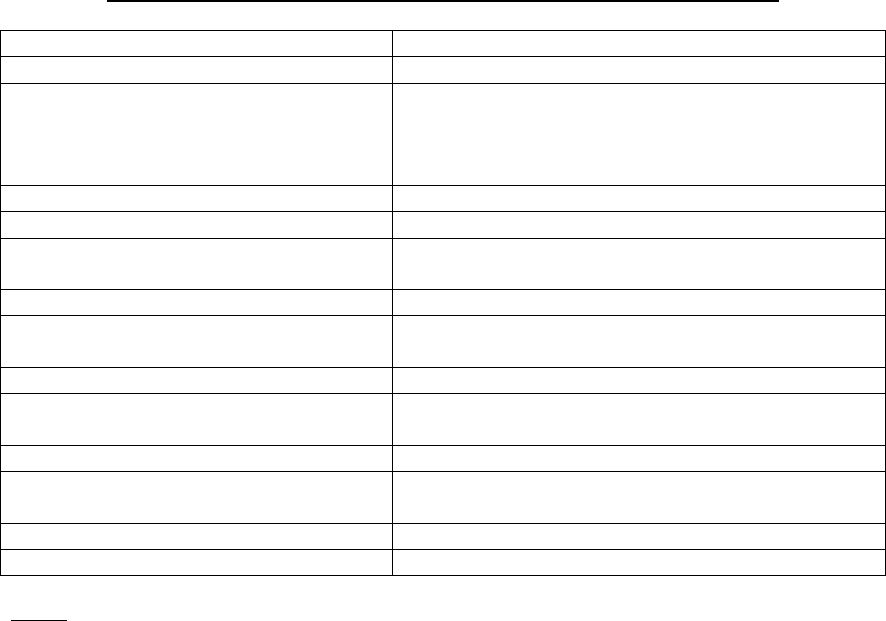

Table III.B.1: Maryland Generating Capacity Profile (Year 2010)

Primar

y

Fuel

Type

Summer

(MW)

Pct. Of

Total

1-10

Years

11-20

Years

21-30

Years

31+

Years

Coal 4886 39.04% 0.0% 16.7% 13.0% 70.3%

Oil & Gas 5126 40.96% 14.2% 21.0% 13.3% 51.5%

Nuclear 1705 13.62% 0.0% 0.0% 0.0% 100.0%

Hydroelectric 590 4.71% 0.0% 0.0% 0.0% 100.0%

Other &

Renewables

209 1.67% 43.9% 25.9% 30.2% 0.0%

TOTAL 12516 100.00% 6.5% 15.6% 11.0% 66.9%

Capacity Age of Plants, by % of Fuel Type

Source: Report EIA-860: “GenY10” Excel, U.S. ENERGY INFORMATION ADMINISTRATION, (Nov. 30, 2011),

available at: http://www.eia.gov/cneaf/electricity/page/eia860.html.

In the past few years several older generating units in the eastern PJM region have

requested deactivation. These older generating units are located in Delaware,

Pennsylvania, New Jersey, Virginia, and the District of Columbia. These older

generation units typically have operated only a limited number of hours each year

recently and generate electricity at relatively high marginal costs. However, the units

also may be helpful in ensuring reliable electric service in the region. PJM undertakes an

analysis to determine the parameters under which units may deactivate or continue to

operate.

18

The following paragraphs summarize the pending deactivations of generating

facilities in the PJM region; several official owner requests for retirement date back to

2007.

In 2007, owners of power plants requested deactivation of units at locations in

D.C.: two Buzzard Point plants with a combined capacity of 240 MW; and two Benning

site power plants, 550 MW. The reliability issues have been identified for all units and

18

Manual M-14D: Generator Operational Requirements, Revision: 17, PJM (effective date Jan. 1,

2010), available at: http://www.pjm.com/~/media/documents/manuals/m14d.ashx.

9

are expected to be resolved to meet the requested deactivation dates.

19

All the units are

scheduled for deactivation on May 31, 2012.

In 2009, owners of power plants requested deactivation of units at three locations

in New Jersey and Pennsylvania: two Cromby units (Pennsylvania) with a combined

capacity of 345 MW; two Eddystone units (Pennsylvania), 588 MW; and two units at the

Kearny (New Jersey) site, 250 MW. On May 31, 2011, one Cromby unit and one

Eddystone unit were deactivated

20

; the remaining four units have requested deactivation

dates between May of 2011 and June of 2012. Reliability impacts were identified with

the Eddystone unit and with the Cromby unit. The requested deactivation date for the

Eddystone unit has been delayed from May 31, 2011 to May 31, 2012, and the requested

deactivation date for the Cromby unit has been delayed from May 31, 2011 to December

31, 2011. Additionally, a reliability analysis remains underway for both Kearny units.

21

In 2010, owners of power plants requested deactivation of five units that remain

pending: one Kearney unit with a capacity of 21 MW; a Cromby Diesel unit, 2.7 MW;

the Ingenco Petersburg plant, 2.9 MW; an Indian River unit, 169.7 MW; and one Sporn

unit, 440 MW. The reliability analysis remains underway for the Kearney unit, with a

projected deactivation timeline reaching into May of 2015. The reliability analyses were

completed for the other four units, and all issues are expected to be resolved to meet the

requested deactivation dates.

22

Depending on the unit, deactivation is projected between

May of 2011 and December of 2013.

In 2011, owners of power plants requested deactivation of nineteen units: two

State Line units with a combined capacity of 515 MW; one Vineland unit, 23 MW; one

Viking Energy unit, 16 MW; five Potomac River units, 482 MW; four Chesapeake units,

576 MW; one Yorktown unit, 159 MW; one Bergen unit, 21 MW; one Burlington unit,

21 MW; one National Park unit, 21 MW; one Mercer unit, 115 MW; and one Sewaren

unit, 111 MW. The reliability analyses remain underway for the majority of the units,

although results are available for both State Line units, the Vineland unit, the Viking

Energy unit, and all five Potomac River units. The reliability issues identified in the

completed analyses are expected to be resolved to meet the requested deactivation

dates.

23

Depending on the unit, deactivation is projected between 2012 and 2015.

Several requests for deactivation were filed in the opening months of 2012. One

noteworthy request is an application submitted on January 26, 2012 by FirstEnergy

19

Pending Deactivation Requests, PJM PLANNING (Feb. 6, 2012), available at:

http://www.pjm.com/planning/generation-retirements/~/media/planning/gen-retire/pending-

deactivation-requests.ashx.

20

PJM Generator Deactivations, PJM PLANNING (Jan. 10, 2012), available at:

http://www.pjm.com/planning/generation-retirements/~/media/planning/gen-retire/generator-

deactivations.ashx.

21

Pending Deactivation Requests, PJM PLANNING (Feb. 6, 2012), available at:

http://www.pjm.com/planning/generation-retirements/~/media/planning/gen-retire/pending-

deactivation-requests.ashx.

22

Id.

23

Id.

10

(formerly Allegheny Power) that references two units located in this State; R. Paul Smith

3 has been in service for 64 years and represents a 28 MW capacity, while R. Paul Smith

4 has been in service for 43 years and represents a capacity of 87 MW. The reliability

analysis is underway, and PJM has listed a projected deactivation date of September 1,

2012 for both R. Paul Smith units.

24

The Maryland generating profile differs considerably from its capacity profile.

Coal and nuclear facilities generate over 88 percent

25

of all electricity produced in

Maryland, even though they represent little more than half of in-State capacity.

26

In

contrast, oil and gas facilities, which tend to operate as mid-merit or peaking units that

come on-line only when needed, generate less than 6 percent of the electricity produced

by in-State resources, while representing approximately 41 percent of in-State capacity.

27

Table III.B.2 summarizes Maryland’s in-State fuel-mix in MWh by generating sources

for 2009. In 2009, Maryland plants produced 43,774,832 MWh of electricity.

Table III.B.2: Maryland Electric Power Generation Profile (Year 2009)

Source MWh

Share

(%)

Coal 24,162,345 55.2

Oil & Gas 2,366,927 5.4

Nuclear 14,550,119 33.2

Hydroelectric 1,888,769 4.3

Other & Renewables 806,671 1.9

Total 43,774,832 100.0

Source: Maryland Electricity Profile, U.S. ENERGY INFORMATION

ADMINISTRATION, Table 5, (April 15, 2011), available at:

http://www.eia.gov/cneaf/electricity/st_profiles/maryland.html.

The total summer capacity of Maryland generators is approximately 12,516

MW,

28

of which approximately 80 percent of the in-State generation capacity is owned

by two companies or their subsidiaries: Constellation Energy Group and GenOn Energy,

Inc. (“GenOn”). Constellation Energy Group owns about 43 percent of this capacity, and

GenOn owns about 37 percent.

29

Nearly two-thirds (65 percent) of the State’s power

plant capacity resides in one of four counties: Prince George’s, 21 percent; Anne

Arundel, 18 percent; Calvert, 14 percent; and Charles, 12 percent. Table III.B.3 lists

Maryland generating units by owner, county, and capacity.

24

Id.

25

See Table III.B.2. In 2009 coal facilities generated 55.2% of Maryland’s electricity and nuclear

facilities generated 33.2%, for a total representative of 88.4% of Maryland’s electric power

generation profile in 2009. Id.

26

See Table III.B.1. Coal facilities represented 39.04% of the in-State capacity in 2010 while

nuclear facilities represented 13.62% of the capacity in 2010. Therefore, coal and nuclear

facilities combined for 52.66% of Maryland’s generating capacity profile in 2010. Id.

27

Id.

28

See Table III.B.3.

29

Id.

11

Table III.B.3: Generation by Owner, County, and Capacity (Year 2010)

Operator/Owner Plant Name County

Name Plate Summer

Pct. Summer

A & N Electric Smith Island

Somerset 1.7 1.6 0.01%

AES Warrior Run AES Warrior Run

Allegany 229 180 1.44%

Allegheny Energy R Paul Smith

Washington 109.5 115 0.92%

American Sugar Domino Sugar

Baltimore City 17.5 17.5 0.14%

Town of Berlin Berlin

Worcester 9 9 0.07%

BP Piney & Deep Creek LLC Deep Creek

Garrett 20 18 0.14%

Calpine Mid-Atlantic Generation LLC Crisfield Somerset 11.6 10.4 0.08%

Constellation Calvert Cliffs Calvert 1828.7 1705

Constellation Brandon Shores Anne Arundel 1370 1273

Constellation C P Crane Baltimore 415.8 399

Constellation Gould Street Baltimore City 103.5 97

Constellation Herbert A Wagner Anne Arundel 1058.5 975.9

Constellation Notch Cliff Baltimore 144 116.7

Constellation Perryman Harford 404.4 353.6

Constellation Philadelphia Baltimore City 82.8 60.9

Constellation Riverside Baltimore 257.2 228

Constellation Westport Baltimore City 121.5 115.8

Constellation Solar Maryland, LLC McCormick & Co. Inc. at Belcamp Hartford 1.4 1.4 0.01%

Covanta Montgomery, Inc. Montgomery County Resource Recovery Montgomery 67.8 54 0.43%

Criterion Power Partners LLC Criterion Wind Project Garrett 70 70 0.56%

Eastern Landfill Gas LLC Eastern Landfill Gas LLC Baltimore 3 3 0.02%

Easton Utilities Comm Easton Talbot 33.6 31.9

Easton Utilities Comm Easton 2 Talbot 38.8 37

Energy Recovery Operations, Inc Harford Waste to Energy Facility Harford 1.2 1.1 0.01%

Exelon Power Conowingo Harford 506.8 572 4.57%

GenOn Chalk Point LLC Chalk Point LLC Prince Georges 2,647 2,347

GenOn Mid-Atlantic LLC Morgantown Generating Plant Charles 1,548 1,477

GenOn Mid-Atlantic LLC Dickerson Montgomery 930 844

Industrial Power Generating Company LLC Wicomico Wicomico 5.4 5.4 0.04%

Maryland Environmental Service Eastern Correctional Institute Somerset 5.8 4.6 0.04%

NAEA Rock Springs LLC NAEA Rock Springs LLC Cecil 772.6 652 5.21%

NewPage Corporation Luke Mill Allegany 65 60 0.48%

NRG Vienna Operations Inc Vienna Operations Dorchester 183 170 1.36%

Panda-Brandywine LP Panda Brandywine LP Prince Georges 288.8 230 1.84%

Power Choice/Pepco Energy Serv NIH Cogeneration Facility Montgomery 22 21.2 0.17%

Prince George's County Brown Station Road Plant I Prince Georges 6.7 5.6 0.04%

RG Steel LLC RG Steel Sparrows Point, LLC Baltimore 120 152.3 1.22%

SCE Engineers Montgomery County Oaks LFGE Plant Montgomery 2.4 2.3 0.02%

Solo Cup Co Solo Cup Co Baltimore 11.2 11.2 0.09%

Trigen Inner Harbor East, LLC Inner Harbor East Heating Baltimore City 2.1 2.1

Trigen-Cinergy Solutions College Park UMCP CHP Plant Prince Georges 27.4 20.8

Wheelabrator Environmental Systems Wheelabrator Baltimore Refuse Baltimore City 64.5 61.3 0.49%

Worcester County Renewable Energy LLC Worcester County Renewable Energy Worcester 2 2 0.02%

13,611.20 12,515.60 100.00%

0.18%

0.55%

Capacity Statistics (MW)

42.55%

37.30%

Source: Report EIA-860: “GenY10” Excel, U.S. ENERGY INFORMATION ADMINISTRATION, (Nov. 30,

2011), available at: http://38.96.246.204/cneaf/electricity/page/eia860.html.

12

C. Potential Generation Additions in Maryland

Siting for central station generation in Maryland continues to be an important

concern. There are reliability, environmental, and competitive issues that must be

resolved when finding an appropriate location for a new generator. Generation is largely

deregulated and currently the responsibility of independent power producers. Generation

companies have proposed various projects, but they are typically either expansions of

existing sites or conjoined locations with other industrial or government facilities.

Without the financial assurances that were typically available through utility ownership,

it has become increasingly difficult for generation companies to secure potential new

sites, long-term sales contracts, and the funding necessary to build new generation.

Other sources of generation have benefited from the Commission’s small

generation interconnection rules. Distributed generation from solar facilities and

combined heat and power installations are examples of small scale generation. Co-

locating smaller generation facilities with other industrial process facilities provides an

alternative to increasing central station generation capacity.

However, regardless of the growth in distributed generation, there will still be a

need for central power stations that can be acceptably developed. Areas in or near the

State that may be considered for new generation include projects in the Atlantic Ocean,

the Nanticoke River area around Vienna on the Lower Eastern Shore, the Calvert Cliffs

area in Southern Maryland, various brownfield sites in the Central Maryland area, and

wind power sites in the mountains of Western Maryland. Upgrades and additions to

existing sites (i.e., brownfield deployment) offer advantages over new, undeveloped

greenfield sites with respect to licensing, transmission facilities, and environmental

concerns.

Although no significant generation has been constructed in Maryland within the

past few years, the Commission has granted both CPCNs and approvals for construction

for those who quality for CPCN exemptions for new generation. Furthermore, no units

have been retired recently. The Commission currently has before it several applications

for construction of new generation and transmission. When and if constructed, these

projects will make available additional electricity for use in Maryland and the PJM

region, and should ease congestion substantially.

In 2009, the Commission initiated a new proceeding (Case No. 9214) to consider

proposals for new electric generation facilities in Maryland. On September 29, 2011, the

Commission issued a Notice of Approval of Request for Proposals for New Generation to

be issued by Maryland Electric Distribution Companies. Attached to that notice was a

Request for Proposals inviting interested persons to submit proposals to the Commission

to construct new generation facilities that would produce and sell electricity to

Maryland’s regulated electric distribution companies. Proposals were due to the

Commission January 20, 2012. Additionally, the Commission set for comment whether

new generation is needed to meet the long-term anticipated demand in Maryland for

13

standard offer service and other electric supply and if so, the quantity of generation

needed. A hearing on the comments was held January 31, 2012.

The status of Commission proceedings covering proposed new electric generator

facilities in Maryland (projects ineligible for CPCN exemptions as discussed in Section

III.D.) that were active cases in late 2009 through 2011, is as follows :

CN9206: A CPCN application from Constellation Power Source Generation Inc.

authorizing the modification of the C.P. Crane generating station for the use of

sub-bituminous coal in Baltimore County. Testimony filed January 13, 2010. In-

service June 9, 2010.

CN9218: A CPCN application from UniStar, LLC authorizing the modification of

the Calvert Cliffs Unit 3 nuclear project for ancillary equipment that will increase

air emissions. In-service April 26, 2010.

CN9199: A CPCN Application from Energy Answers International, Inc. to

construct a 120 MW Generating Facility in Baltimore using processed waste for

fuel. On December 29, 2011, Energy Answers filed a motion to toll its

construction deadline contained in the CPCN.

CN9229: A CPCN Application from Mirant for STAR, a processor for flyash at

the Morgantown Power Plant in Charles County. In-service November 4, 2010.

In addition to the aforementioned CPCN applications, Maryland is experiencing

an uptick in the amount of solar generation capacity both planned and already available to

the State. Section VI.C. details the Commission’s efforts to spur small-scale solar

generator interconnection throughout Maryland. On the utility-scale, plans for new solar

generation also began taking shape in 2011; Case Number 9272 was opened for the

CPCN application of Maryland Solar LLC to construct a 20 MW solar photo-voltaic

generating facility in Hagerstown, Maryland. The Commission granted approval on

October 8, 2011 for construction of the Hagerstown facility in Order No. 84369. Other

notable examples of planned new solar generation include the October 26, 2011

Commission approval for SMECO Solar LLC to construct a Type IV solar generator in

Hughesville.

30

Additionally, on December 14, 2011, the Commission granted approval to

Constellation Solar Holding, LLC to construct a solar photovoltaic generation project

located at Mount St. Mary’s University comprising two solar arrays with capacities of

1.25 MW and 250 kW, respectively.

31

The number of projects for which a transmission interconnection request (capacity

or energy) has been filed with PJM provides an indication of potential generation

capacity additions in Maryland. Table III.C.1 lists the new generation projects located in

Maryland for which a transmission interconnection request has been made to PJM and

that are categorized as under study, under construction, providing partial service, or

30

The Commission granted approval of SMECO Solar LLC’s application for an exemption of the

CPCN requirement. Letter Order, Maillog No. 134380.

31

The Commission granted approval of Constellation Solar Holding, LLC’s application for an

exemption of the CPCN requirement. Letter Order, Maillog No. 135780.

14

currently suspended. The Table demonstrates the diversity of projects being pursued

throughout the State. The vast majority (about 89%) of proposed new generation

capacity would be located within the Southern Maryland Electric Cooperative, Inc.

(“SMECO”) and Pepco service territories, and would use primarily natural gas or nuclear

fuel. Additional generation capacity, especially from renewable sources, has been

proposed for the DPL and PE service territories.

Table III.C.1: PJM Transmission Queue Active New Generating Capacity

BGE

290

DPL

478

PE

259

PEPCO

28

SMECO

-

TOTAL

205

Service

Territory

3,060 - 11,474 2010-2017

- 1,640 1,640 2017

8,520 - 8,548 2012-2017

- - 259 2009-2013

- - 478 2009-2017

259 - 549 2012-2015

Other &

Renewable Total

In-service

DatesNuclearNatural Gas

Plant Capacity (MW) By Fuel

Source

: See Appendix Table A-9.

D. CPCN Exemptions for Generation

Pursuant to Public Utilities Article § 7-207.1, certain power generating stations

are exempt from the requirement to obtain a CPCN, subject to Commission approval,

prior to commencing construction of the generating station. These approvals are

available to generating stations that are designed to provide on-site generated electricity

and that meet the following qualifications:

32

1. The capacity of the generating station does not exceed 70 MW; and

2. The electricity that may be exported for sale from the generating station to

the electric system is sold only on the wholesale market pursuant to an

interconnection, operation, and maintenance agreement with the local

electric company.

33

32

PUA § 1-101(s) defines “On-site generated electricity” as electricity that: (1) is not transmitted or

distributed over an electric company’s transmission or distribution system; or (2) is generated at a

facility owned or operated by an electric customer or operated by a designee of the owner who,

with the other tenants of the facility, consumes at least 80% of the power generated by the facility

each year.

33

The Statute also provides for an exemption from the CPCN process for a generating station that

does not exceed 25 MW if electricity that may be exported for sale from the generating station to

the electric system is sold only on the wholesale market pursuant to an interconnection, operation,

and maintenance agreement with the local electric company, and at least 10% of the electricity

generated at the generating station each year must be consumed on-site. MD. C

ODE ANN., PUB.

UTIL. § 7-207.1 (2011).

15

For wind-powered generating stations with a capacity up to 70 MW, there are two

additional qualifications that must be met in order to be granted approval without

obtaining a CPCN. The first is that the generating station must be land-based; therefore,

any off-shore facility within State waters will be required to obtain a CPCN. The second

qualification is that the Commission must provide an opportunity for public comment at a

public hearing.

The Commission’s PUA § 7-207.1- approved application requires the applicant to

select one of four specific types of generating stations: Type I, Type II, Type III, or Type

IV. With the exception of Type I, all generators are required to obtain an

Interconnection, Operation, and Maintenance Agreement (“Interconnection Agreement”)

with the local Electric Distribution Company (“EDC”). Type I generators must obtain a

letter from the local EDC that states an Interconnection Agreement is not necessary.

A Type I generator is not synchronized with the local electric company’s

transmission and distribution system and will not export electricity to the electric

system.

34

An emergency or back-up generator is the most common Type I generator. A

Type II generator is synchronized with the electric system; however, it will not export

electricity to the electric system. Generators used for peak-load shaving or generators

participating in a demand response program are the most common form of Type II

generators. Type III generators are synchronized with the electric system and export

electricity for sale on the wholesale market. A Type IV generator is a generator that is

synchronized with the electric system, but utilizes the disconnect feature of an inverter to

prevent export of power in the event of a power failure on the utility’s grid.

In order to obtain approval to construct a generator under PUA § 7-207.1, an

applicant must submit a completed application. In addition, the generator will need a

wholesale sales agreement with PJM if the generator is selling electricity on the

wholesale market. It is important to note that the approval does not exempt an applicant

from complying with other regulations or from obtaining all other necessary State and

local permits, such as those required by the Air and Radiation Management

Administration at the Maryland Department of the Environment (“MDE”).

Table III.D.1 provides an overview of the number and capacity of generators that

have applied for PUA § 7-207.1 approvals on an annual basis. The number of

applications has generally been increasing over time, and these generators have a

cumulative generation capacity of over 1,300 MW.

34

PUA § 1-101(h) defines “Electric company,” with certain exclusions, as a person who physically

transmits or distributes electricity in the State to a retail electric customer.

16

Table III.D.1: Construction Approvals for CPCN Exempt Generation

Period Approved Applications No. of Units Total (MW)

Calendar Year 2001 4 7 35.4

Calendar Year 2002 9 26 68.3

Calendar Year 2003 21 29 43.4

Calendar Year 2004 36 58 77.1

Calendar Year 2005 36 70 94.4

Calendar Year 2006 31 55 91.4

Calendar Year 2007 40 62 67.3

Calendar Year 2008 72 130 212.1

Calendar Year 2009 102 153 269.2

Calendar Year 2010 101 152 167.2

Calendar Year 2011 78 138 188.6

Total 530 880 1314.4

Pending 10 16 16.0

Total (Including Pending) 540 896 1330.4

Source: PSC database.

Note

: 2011 data is current as of October 31, 2011. Each application may contain multiple generation units.

Table III.D.2 reflects that fossil fuel generators were 92.6% of the 896 generator

units reported. These fossil fuel generators provided 1070.0 MW (80.4%) of the total

1330.4 MW of generating capacity reported. Oil remained the dominant fuel source for

new generators. Oil-fired generators were 930.1 MW (69.9%) of the total generation

reported. Wind-powered units provided 189.6 MW (14.3%) of total CPCN exempt

capacity. Solar-powered units provided 44.7 MW (3.4%) of total CPCN exempt

capacity.

17

Table III.D.2: Number and Capacity in MW of CPCN Exempt

Generating Units by Energy Resource

Energy Resource

Total

Approved

Percent of

Total

Approved

GENERATOR UNITS

Oil

790 88.2%

Natural Gas

38 4.2%

Fossil

Propane

2 0.2%

Fossil Total 830 92.6%

Biomass

1 0.1%

Digester Gas

3 0.3%

Landfill Gas

3 0.3%

Solar

56 6.3%

Renewable

Wind

3 0.3%

Renewable Total 66 7.4%

Grand Total 896 100.0%

CAPACITY (MW)

Oil

930.1 69.9%

Natural Gas

139.8 10.5%

Fossil

Propane

0.2 0.0%

Fossil Total 1070.0 80.4%

Biomass

19.8 1.5%

Digester Gas

3.2 0.2%

Landfill Gas

3.1 0.2%

Solar

44.7 3.4%

Renewable

Wind

189.6 14.3%

Renewable Total 260.3 19.6%

Grand Total 1330.4 100.0%

Source: PSC database.

Note: Data is current as of November 1, 2011.

18

IV. TRANSMISSION INFRASTRUCTURE: PJM, MARYLAND, AND

NATIONAL

A. Introduction

Transmission facilities in PJM and Maryland have continued to play a key role in

energy supply. With Maryland’s dependence on energy imports, it is necessary that

adequate transmission facilities be available to reliably provide electricity supplies.

While all network systems can experience congestion at times, portions of the Mid-

Atlantic States -- including central Maryland and the Delmarva Peninsula -- have

continued to experience significantly higher levels of congestion than the rest of PJM.

This, in turn, has led to higher energy and capacity costs in portions of Maryland and the

surrounding states since local, but more expensive, generation resources had to be

deployed to meet load. Adequate capacity and reliable supplies of electricity are

continually monitored, managed, and, when necessary, supplemented with additional

infrastructure.

B. Eastern Interconnection Planning Collaborative

During 2011, the Eastern Interconnection Planning Collaborative (“EIPC”)

completed the first phase of its work identifying a broad range of alternative futures to be

analyzed by a production cost model. Eight futures were modeled under varying

assumptions. The futures modeled were:

1. Business as Usual – This Future continues today’s policies.

2. National Carbon Policy/National Implementation – This Future envisions a

national Carbon Emission Mitigation policy to be fulfilled by constructing

no/low carbon – emitting energy generation facilities in the most productive

generation resource areas and building transmission to connect those

generation facilities to customers in the Eastern Interconnection.

3. National Carbon Policy/Regional Implementation – This Future concentrates

on fulfilling a national Carbon Emission Mitigation Policy by constructing

generation and transmission within each region to serve the customers within

that region.

4. High Energy Efficiency/Demand Response/Distributed Generation/Smart

Grid – This Future focuses on developing local programs to avoid the need for

large generation and transmission construction.

5. National RPS/National Implementation – Imposes a 30% Renewable Portfolio

Standard which may be fulfilled by importing renewable from the areas of the

Eastern Interconnection with the highest renewable energy resource potential.

6. National RPS/Regional Implementation – The RPS is assumed to be fulfilled

using renewable energy resource potential within each region of the Eastern

Interconnection.

19

7. Nuclear Resurgence – This Future looks at incenting the construction of

nuclear technologies as an option on other generation technologies.

8. National Carbon Policy/National Implementation with high

Efficiency/Demand Response – This Future combines Future Nos. 2 and 4.

The results from these modeling runs, which include what type of generation is

built, where it will be located, how much is needed, and at what cost, can be found at

www.eipconline.com. Next, EIPC identified three future scenarios for which a complete

transmission build-out will be designed. This exercise will provide an estimate of the

transmission costs associated with each scenario. The results of the transmission build-

out should be available in early 2012.

C. The Regional Transmission Expansion Planning Protocol

Planning the enhancement and expansion of transmission capability on a regional

basis is one of the primary functions of the wholesale market operator, PJM. PJM

implements this function pursuant to the Regional Transmission Expansion Planning

Protocol set forth in Schedule 6 of the PJM Operating Agreement.

PJM annually develops the Regional Transmission Expansion Plan (“RTEP”) to

meet system enhancement requirements for new backbone transmission lines and

interconnection requests for new generation. To establish a starting point for

development, PJM performs a “baseline” analysis of system adequacy and security. The

baseline is used for conducting feasibility studies on behalf of all proposed generation

and transmission projects. Subsequent System Impact Studies for those potentially viable

projects provide recommendations that become part of the RTEP Report.

PJM’s RTEP looks at a 15-year projection of the grid to predict reliability

problems. The system is planned for the probability of loss of load to be one day in ten

years. Single contingency analysis allows for the grid to function with the loss of any

one line. In some cases, double contingency analysis is used. PJM’s 15-year planning

horizon process has predicted that the congestion on the eastern and western interfaces

may cause both load deliverability and generator deliverability issues in central

Maryland.

35

Deliverability issues can be a result of significant load growth and the

retirement of existing generation.

36

Ideally, these problems can be solved with a

combination of new generation, transmission projects, and demand response.

The RTEP process applies reliability criteria over a 15-year horizon to identify

transmission constraints and reliability concerns. PJM uses CETO/CETL

37

analysis to

determine the import capabilities of the transmission system to supply the peak load

requirements for sub-regions within PJM. There are currently 23 sub-regions or load

35

The central Maryland region of the Mid-Atlantic area generally includes northern Virginia and the

Baltimore/Washington region.

36

Generation slated for retirement includes Benning Road, Buzzard Point, Potomac River, and Gude

Landfill in Washington, DC; and Indian River on the Eastern Shore.

37

Capacity Emergency Transfer Objective/ Capacity Emergency Transfer Limit.

20

deliverability areas (“LDAs”) in PJM. The Transmission Expansion Advisory

Committee (“TEAC”) is the primary forum for stakeholders to discuss the RTEP results.

The Commission is an active participant in the RTEP and regularly attends the TEAC

meetings.

1. Baseline Reliability Assessment

PJM establishes a baseline from which the need and responsibility for

transmission system enhancements can be determined. PJM performs a comprehensive

load flow analysis of the ability of the grid to meet reliability standards, taking into

account forecasted loads, imports and exports to neighboring systems, existing generation

and transmission assets, and anticipated new generation and generation retirements. The

baseline reliability assessment identifies areas where the planned system is not in

compliance with standards required by the North American Electric Reliability

Corporation (“NERC”)

38

and the regional reliability councils. The baseline assessment

develops and recommends enhancement plans to achieve compliance.

2. Inter-regional Planning

PJM is engaged in planning processes that address issues of mutual concern to

PJM and neighboring transmission grid systems: the Midwest Independent System

Operator (“ISO”); ISO New England; the New York ISO; the Tennessee Valley

Authority; and the North Carolina Planning Collaborative (added in 2009). The Inter-

regional Planning Stakeholder Advisory Committee facilitates stakeholder review and

input into the Coordinated System Plan. Coordinated regional transmission expansion

planning across seams is expected to reduce congestion on an inter-Regional

Transmission Organization (“RTO”) basis, and enhance the physical and economic

efficiencies of congestion management. Inter-regional ties are a benefit for reliability,

especially when load centers peak at different times (referred to as “load diversity”).

This kind of forum has been important for addressing problems such as loop flows

around Lake Erie.

3. Obligation to Build RTEP Projects

PJM’s Transmission Owners’ Agreement obligates transmission owners to

proceed with building transmission projects that are needed to maintain reliability

38

Since 1968, NERC has been committed to ensuring the reliability of the bulk power system in

North America.

To achieve that goal, NERC develops and enforces reliability standards; assesses

adequacy annually via a 10-year forecast and winter and summer forecasts; monitors the bulk

power system; audits owners, operators, and users for preparedness; and educates, trains, and

certifies industry personnel. NERC is a self-regulatory organization, subject to oversight by

FERC. As of June 18, 2007, FERC granted NERC the legal authority to enforce reliability

standards with all U.S users, owners, and operators of the bulk power system, and made

compliance with those standards mandatory and enforceable. NERC's status as a self-regulatory

organization means that it is a non-government organization which has statutory responsibility to

regulate bulk power system users, owners, and operators through the adoption and enforcement of

standards for fair, ethical, and efficient practices.

21

standards as approved by the PJM Board of Directors. Transmission owners can

voluntarily build these projects, or PJM can file with FERC to request FERC to order the

project to be built. In Maryland, CPCNs are required for transmission lines above 69,000

volts or modifications to existing facilities.

4. PJM’s Authority

FERC approved PJM as an Independent System Operator in 1997. Since that

time, PJM has administered its RTEP as described in Schedule 6 of the Operating

Agreement. PJM has subsequently received authority from FERC for procedures and

rules for transmission expansions needed to enable the interconnection of new and

expanded generation and merchant transmission facilities. PJM has amended the RTEP

to include the development of transmission projects to support competition in wholesale

electric markets, allowing it to justify projects for economic reasons as well as reliability.

PJM received final FERC approval as an RTO in 2002. As an RTO, PJM is the

administrator of the Open Access Transmission Tariff (“OATT”) as approved by FERC.

The OATT is the basis for PJM to collect charges to recover the costs of projects owned,

constructed, or financed by the transmission owners. Transmission owners file rate

schedules with FERC to recover transmission investments made pursuant to the RTEPs

approved by the PJM Board. The OATT enables generation to be sold anywhere in the

system.

D. Transmission Congestion in Maryland

1. PJM’s Definition of Congestion

PJM’s Locational Marginal Pricing (“LMP”) system takes account of congestion

in determining electricity prices. It reflects the value of the energy at the specific location

and time it is delivered. Theoretically, if the lowest-priced electricity could

simultaneously be distributed across the entire 13 states and the District of Columbia

(thereby encompassing the entire PJM wholesale market), prices would be the same

across the entire PJM grid. However, the capital investments that would be required for

such an expansive transmission system would be cost prohibitive. Therefore, more

expensive but advantageously located power plants that generate electricity are required

to meet the demand. As a result, LMPs are higher in the congested areas and lower at the

source of cheaper power. Congestion costs vary significantly during the course of a day,

seasonally, and from year to year. Persistent patterns of high LMPs can indicate future

reliability problems and the need for new generation, new transmission, and/or demand

response.

2. Location of Congestion

In 2010, the PE South interface continued to be the largest contributor to

congestion costs for the third consecutive year. This one constraint’s costs were nearly

22

double the sum of all remaining constraint costs. The PE South interface continues to be

the primary west-to-east transfer constraint.

39

3. Costs of Congestion

Congestion reflects the underlying characteristics of the power system, including

the nature and capability of transmission facilities and the cost and geographical

distribution of generation facilities. Total PJM congestion costs increased by $709.1

million (or 99%) from $719 million in calendar year 2009 to $1,428 billion in calendar

year 2010. Maryland utilities shared in these increased congestion costs.

Zone

2010 Total Annual

Zonal Congestion

Costs ($ million)

40

2009 Total Annual

Zonal Congestion

Costs ($ million)

41

Allegheny Power (Potomac Edison) 282.7 95.3

Baltimore Gas and Electric 91.6 33.5

Delmarva Power 47.2 31.1

Potomac Electric Power 98 58.4

Wholesale prices for electricity are determined in PJM’s Reliability Pricing

Model (“RPM”) Base Residual Auctions (“BRAs”). Blocks of capacity are sold

regionally for future delivery. The data below summarizes the annual capacity price for

Maryland in 2014/2015 compared to the 2013/2014 delivery year.

42

Zone

2014/2015

$/MW-Day

2013/2014

$/MW-Day

Western Maryland (PE) 125.94 27.73

Central Maryland (BGE) 136.50 226.15

Central Maryland (PEPCO) 136.50 247.14

Delmarva (DPL) 136.50 245.00