Chapter 8 IRC SECTION 401(h) RETIREE MEDICAL BENEFITS

By Jay Jensen, Abba Rabbani

Cafeteria Plan Technical Advisors

and Jim Holland (Reviewer)

EMPLOYEE PLANS

TECHNICAL

With Ede Olsen

TE/GE Actuary

IRC SECTION 401(H) RETIREE MEDICAL BENEFITS.................................................................. 147

I. INTRODUCTION................................................................................................................................ 508

II. OBJECTIVES..................................................................................................................................... 509

III. BACKGROUND ............................................................................................................................... 510

IV. FINANCIAL ACCOUNTING AND REPORTING....................................................................... 510

IV(

A). AICPA STATEMENT OF POSITION (SOP) 99-2 ........................................................................... 511

IV(

B). STATEMENT OF FINANCIAL ACCOUNTING STANDARD (SFAS) 132............................................ 511

V. HOW DO YOU IDENTIFY A SECTION 401(H) RETIREE MEDICAL ACCOUNT ............... 511

VI. WHAT SHOULD YOU REVIEW ON A DETERMINATION LETTER APPLICATION ...... 512

VI(

A). SECTION 401(H) IS A QUALIFICATION PROVISION ...................................................................... 513

VI(

B). REVENUE PROCEDURE 2000-6.................................................................................................... 514

VI(

C). SUBORDINATION LIMITATION..................................................................................................... 514

VI(

D). SEPARATE ACCOUNTS ................................................................................................................ 520

VI(

E). REASONABLE AND ASCERTAINABLE BENEFITS........................................................................... 520

VI(

F). NO DIVERSION OR REVERSION.................................................................................................... 521

VI(

G). KEY EMPLOYEE ACCOUNTS ....................................................................................................... 521

VI(

H). EMPLOYEE OR EMPLOYER CONTRIBUTIONS ............................................................................... 522

VI(

I). CAVEATS ..................................................................................................................................... 522

VI(

J). SECTION 420 TRANSFERS............................................................................................................ 524

VII. DEDUCTIONS FOR WELFARE BENEFITS EXCLUSIVE OF SECTION 401(H) ............... 524

VII(

A). DEDUCTION WITHOUT THE USE OF A TRUST............................................................................. 524

VII(

B). FUNDING WELFARE BENEFIT OBLIGATIONS.............................................................................. 525

VII(

C). DEDUCTION USING A VEBA TRUST.......................................................................................... 526

VIII WHAT SHOULD YOU REVIEW DURING AN EXAMINATION........................................... 526

VIII(

A). SECTION 162 DEDUCTION PROVISIONS APPLICABLE TO SECTION 404..................................... 527

VIII(

B). SECTION 404 DEDUCTION PROVISIONS FOR SECTION 401(H)................................................... 527

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

VIII(C). SECTION 404(A)(7) APPLICABILITY ......................................................................................... 529

VIII(D). SECTION 263A UNIFORM CAPITALIZATION ............................................................................. 530

IX. OTHER EXAMINATION ISSUES................................................................................................. 531

IX(A). SUBORDINATION LIMITATION..................................................................................................... 531

IX(B). KEY EMPLOYEE ACCOUNTS........................................................................................................ 534

IX(C). SECTION 415 CONSIDERATIONS.................................................................................................. 534

IX(D). SECTION 420 CONSIDERATIONS.................................................................................................. 536

APPENDIX A: REV. PROC. 2000-6 SECTION 401(H) RULING SECTIONS AND CHECKLIST

.................................................................................................................................................................... 537

APPENDIX/CHECKLIST..................................................................................................................... 539

APPENDIX B: REV. PROC. 2000-6 SECTION 420 RULING SECTIONS AND CHECKLIST.... 541

SECTION 16, OF REVENUE PROCEDURE 2000-6, PROVIDES THE FOLLOWING:......................................... 541

APPENDIX/CHECKLIST..................................................................................................................... 543

APPENDIX C: SAMPLE INFORMATION DOCUMENT REQUEST............................................. 547

APPENDIX D: CAFETERIA PLAN TECHNICAL ADVISOR TEAM............................................ 548

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

I. Introduction

Section 401(h) of the Code permits a pension or annuity plan to provide

for payment of benefits for sickness, accident, hospitalization and medical

expenses for retired employees, their spouses and dependents. In order

for the pension or annuity plan to meet the provisions of section 401(h),

such medical benefits must be subordinate to pension benefits and must

be established and maintained in a separate account.

Medical benefits provided in a pension plan are considered ancillary

benefits. Some of the special requirements discussed herein are

variations on the "incidental benefit" rules that have always been a

concern for qualified pension plans. Thus, the contribution limitation

described in section 401(h) is referred to as the "subordination limit," since

its purpose is to insure that medical contributions are subordinate to the

contributions for pension benefits. Failure to meet such requirements is a

qualification issue for the pension plan of which the section 401(h) medical

account is a part.

Anecdotal evidence suggests that employers sparingly utilized section

401(h) accounts prior to the 1990’s. Employers primarily established

voluntary employee beneficiary associations (VEBA’s), as described in

section 501(c)(9) of the Code, to fund and deduct contributions to provide

post-retirement benefits including retiree health and life insurance.

Currently, many employers use both a VEBA and section 401(h) account

to fund and deduct these benefits. Utilizing a section 401(h) account in

conjunction with a VEBA permits employers to fund and deduct a greater

amount of contributions than either arrangement would individually

provide.

The importance of funding benefits in trusts such as VEBA trusts and

section 401(h) accounts within a pension trust was heightened by the

issuance of Statement of Financial Accounting Standard (SFAS) 106

which addresses employers’ accounting for post-retirement benefits other

than pensions. This Statement, issued in December of 1990, became

mandatory for most employers for fiscal years beginning after December

15, 1992. SFAS 106 requires most employers to accrue the expected

cost of post-retirement benefits other than pensions during the years that

an employee renders services rather than on a pay-as-you-go basis.

SFAS 106 requires the current recognition of the future expense for

financial accounting purposes, but does not require the actual funding of

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

benefits. Expense recognition by the employer creates an unfunded

liability on the employer’s balance sheet.

Although SFAS 106 does not address the tax deduction allowable to the

employer, this Statement may have an indirect effect on the amounts

claimed as a deduction by giving employers an incentive to prefund larger

amounts of post-retirement health and life insurance benefits than

employers may have in the absence of the book accrual requirement.

This effect may occur because SFAS 106 permits an employer to offset

the liabilities accrued on its balance sheet for post-retirement benefits by

the amount of any assets that have been set apart from its general assets,

e.g., in a section 401(h) account or a VEBA trust, and dedicated solely to

the payment of those benefits.

The primary guidance with respect to section 401(h) accounts consists of:

• Code Section 401(h) (including corresponding Committee

Reports),

• Code Section 420 (concerning transfer of assets to a 401(h)

account),

• Treasury Regulation 1.401-14 (concerning qualification issues and

the relationship between a pension plan and a section 401(h)

medical account) and

• Treasury Regulation 1.404(a)-3(f) (concerning specific deduction

issues).

Other available documents that may be of interest include IRS private

letter rulings 9834037, issued May 28, 1998; 9709038, issued December

3, 1996 and 9652021, issued September 30, 1996. Of course, private

letter rulings may not be cited by the Service or employers other than the

specific employers who requested the rulings. Throughout this text, other

relevant sources will also be discussed. Currently, case law does not

exist relating to the deduction or qualification provisions of section 401(h)

accounts.

II. Objectives

1. Identify section 401(h) retiree medical accounts.

2. Determine what should be considered when reviewing a determination

letter application.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

3. Determine what should be considered when examining a pension

or annuity plan.

III. Background

Section 401(h) of the Code was established and generally effective for

taxable years beginning in 1963. This section was amended to add

certain provisions effective for contributions made after October 3, 1989.

IV. Financial Accounting and Reporting

As stated above, SFAS 106 originally provided financial accounting and

reporting requirements for postretirement benefit obligations other than

pensions. Additional financial and reporting requirements also apply to

these postretirement benefits and for pension plans that provide these

benefits.

Section 1.401-1(b)(1)(i) of the Income Tax Regulations provides that a plan is

not a pension plan if it provides for the payment of benefits not customarily

included in a pension plan such as layoff benefits or benefits for sickness,

accident, hospitalization, or medical expenses (except medical benefits

described in section 401(h) as defined in paragraph (a) of section 1.401-14).

Section 401(h) of the Code permits a pension or annuity plan to provide for

payment of benefits for sickness, accident, hospitalization and medical expenses

for retired employees, their spouses and dependents.

Accordingly, the exclusive method for providing medical benefits in a pension

plan (or money purchase plan) is by utilizing a section 401(h) account.

Section 1.401-1(b)(1)(ii) of the Income Tax Regulations provides that a profit-

sharing plan within the meaning of section 401 is primarily a plan of deferred

compensation, but the amounts allocated to the account of a participant may be

used to provide for him or his family incidental life or accident or health

insurance.

Thus, a profit-sharing plan may provide for incidental accident or health

insurance benefits. However, a section 401(h) account is not permitted in a

profit-sharing plan. See section 3.02 of Revenue Procedure 2000-6, I.R.B.

2000-1 187, issued on January 02, 2000.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

IV(a). AICPA Statement of Position (SOP) 99-2

AICPA Statement of Position (SOP) 99-2, Accounting for and Reporting of

Postretirement Medical Benefit (401(h)) Features of Defined Benefit

Pension Plans, requires disclosures relating to section 401(h) retiree

medical accounts. This Statement requires disclosures in financial

accounting statements included in Form 5500, Annual Return/Report of

Employee Benefit Plan, filings for plan years beginning after December

15, 1998, with earlier application encouraged. Accounting changes

required on adoption of the SOP should be made retroactively by

restatement of financial statements for prior periods.

This Statement provides for separate financial accounting and reporting

disclosures for defined benefit pension plans and health and welfare

benefit plans containing section 401(h) features.

Defined benefit pension plan financial statements must disclose that

section 401(h) accounts assets are only available to pay retiree health

benefits. Health and welfare benefit plan financial statements must

disclose that retiree health benefits are partially funded through a section

401(h) account of the defined benefit pension plan. For additional

information access www.aicpa.org.

IV(b). Statement of Financial Accounting Standard (SFAS) 132

Statement of Financial Accounting Standards 132 (SFAS), Employers’

Disclosures about Pensions and Other Post Retirement Benefits,

standardizes the disclosure requirements under SFAS 106 and SFAS 87

effective for fiscal years beginning after December 15, 1997.

This statement suggests a parallel format for presentation of information

about pensions and other postretirement benefits in company financial

statements. For additional information access www.fasb.org.

V. How Do You Identify a Section 401(h) Retiree Medical Account

When reviewing a determination letter application or conducting an

examination, the agent should review the defined benefit plan (or money

purchase plan) document for any plan language describing medical

benefits to determine whether the provisions of section 401(h) have been

met. Most plans providing these benefits contain a separate section that

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

is easily recognizable by the incorporation of standard language from

section 401(h) of the Code.

In addition, beginning with 1999 plan years, the agent should inspect Form

5500 for a code for pension benefit features in Box 6a to determine

whether the pension plan contains a section 401(h) account. Pension

plans featuring a section 401(h) account should indicate code 1E in Box

6a.

For plan years beginning before 1999, the agent may issue an information

document request with the following items:

Ø Is the taxpayer funding retiree health benefits through a section 401(h)

account within a qualified pension plan?

Ø If so, what was the date of adoption of the section 401(h) account and what

was the effective date of the account?

If a section 401(h) account is maintained, the agent may use the

information document request in Appendix C in order to request the basic

information for examining this issue.

Another method for identifying a section 401(h) account when conducting

an examination is to review the employer’s ledger accounts for health

benefits. Usually, separate ledger accounts exist for active employee and

retiree health benefits. Separate labels within the retiree health ledger

account may be an indication that the employer is funding retiree health

benefits utilizing a section 401(h) account and/or VEBA trust.

VI. What Should You Review on a Determination Letter

Application

The following items should be considered by the agent reviewing a

determination letter application. The agent should determine whether a

prior determination letter considered plan provisions relating to section

401(h) and determine whether the current plan provisions meet the

requirements of this section. Most plans providing benefits in a section

401(h) account incorporate language verbatim from section 401(h) of the

Code. If the language of the statute is modified, the agent may wish to

consult a TE/GE actuary or request technical advice.

If a prior determination letter approved plan provisions that did not meet

the requirement of section 401(h), the agent should consider sections

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

5.01, 5.02 and 21.05 of Revenue Procedure 2000-6 that provide the

parameters of reliance by employers on determination letters.

In addition, Internal Revenue Manual sections 7717.2(1) and 7717.1(5)

generally provide that a ruling or determination letter found to be in error

or not in accord with the current views of the Service may be modified or

revoked. Modification or revocation may be effected by a notice to the

taxpayer to whom the ruling or determination letter originally was issued,

or by a revenue ruling or other statement published in the Internal

Revenue Bulletin.

Accordingly, the agent should notify the employer or employer’s

representative in writing that the plan should be amended to reflect the

correct language.

VI(a). Section 401(h) is a Qualification Provision

Section 401(a) of the Code provides the requirements for qualification for

deferred compensation plans. Section 401(a)(1) provides that a trust

created or organized in the United States and forming part of a stock

bonus, pension, or profit-sharing plan of an employer for the exclusive

benefit of his employees or their beneficiaries shall constitute a qualified

trust under this section if the contributions are made to the trust by such

employer, or employees, or both, or by another employer who is entitled to

deduct his contributions under section 404(a)(3)(B) (relating to deduction

for contributions to profit-sharing and stock bonus plans), for the purpose

of distributing to such employees or their beneficiaries the corpus and

income of the fund accumulated by the trust in accordance with such plan.

Section 1.401-1(b)(1)(i) of the Income Tax Regulations provides that a

plan is not a pension plan if it provides for the payment of benefits not

customarily included in a pension plan such as layoff benefits or benefits

for sickness, accident, hospitalization, or medical expenses (except

medical benefits described in section 401(h) as defined in paragraph (a) of

section 1.401-14).

Section 401(h) of the Code permits a pension plan to provide for the

payment of benefits for medical expenses of retired employees, their

spouses, and their dependents, but only if certain provisions are met.

These provisions include sections 401(h)(1) through (h)(6) discussed later

in this text.

The Committee Reports for Public Law 87-863 state that under present

law (prior to the enactment of section 401(h)), however, it is impossible for

an employer to fund such (medical) benefits through a qualified plan.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

* * * The present language of section 401 of the Internal Revenue

Code, however, has been interpreted as making a pension plan which

provides other than pension benefits nonqualified, and thus the employer

would lose his deduction for amounts contributed. * * *

A pension plan which provides the benefits described in the new

subsection (section 401(h)) and which otherwise satisfies the

requirements set forth in section 401(a) of the Code will not be considered

as a qualified plan unless it also satisfies the requirements of paragraphs

(1), (2), (3), (4) and (5) of the new subsection. See, H. Rep. No. 2317,

87

th

Congress, 2

nd

Sess. at 1205, 1206, 1207 (1962).

Thus, if a pension plan containing a section 401(h) retiree medical benefits

account fails to meet the provisions of section 401(h) in form or operation,

the pension plan and trust fail to qualify under sections 401(a) or 501(a) of

the Code.

VI(b). Revenue Procedure 2000-6

When reviewing a determination letter application, the agent should review

the cover letter to determine whether the employer or employer’s

representative has requested a ruling on the section 401(h) account

language in accordance with Revenue Procedure 2000-6. Appendix A of

this text contains a checklist agents should utilize when reviewing

determination letter applications. Appendix A also contains the provisions

relating to when rulings will or will not be issued on section 401(h)

accounts within a pension plan. Note that Form 6406 may not be used to

request a determination letter that considers section 401(h).

VI(c). Subordination Limitation

Section 401(h)(1) of the Code provides that medical benefits provided by

the plan must be subordinate to the retirement benefits provided by the

plan.

The Omnibus Reconciliation Act of 1989 (OBRA '89) modified section

401(h) of the Code by adding the following language, "In no event shall

the requirements of paragraph (1) [the subordination requirement] be

treated as met if the aggregate actual contributions for medical benefits,

when added to actual contributions for life insurance protection under the

plan, exceed 25 percent of the total actual contributions to the plan (other

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

than contributions to fund past service credits) after the date on which the

account is established."

Section 1.401-14(c) of the regulations provides the requirements that must

be met for a qualified pension or annuity plan to provide medical benefits

described in section 401(h).

Section 1.401-14(c)(1)(i) of the regulations states, in part, that the medical

benefits described in section 401(h) are considered subordinate to the

retirement benefits if at all times the aggregate of contributions (made

after the date on which the plan first includes such medical benefits) to

provide such medical benefits and any life insurance protection does not

exceed 25 percent of the aggregate contributions (made after such date)

other than contributions to fund past service credits.

Although section 401(h) of the Code was modified by OBRA'89, the

regulations pertaining to section 401(h) of the Code have not been

revised.

Thus, the language regarding the subordination test in section 1.401-

14(c)(1)(i) of the regulations has been supplemented by the statutory

language in section 401(h) added by OBRA ’89.

When reviewing a determination letter application, the agent should

ensure that the plan provisions include the subordination limitation

language added by OBRA’ 89 in accordance with section 401(h)(1) of the

Code.

To better understand the mechanics of the subordination limitation, the

following illustrations are provided.

S

S

I

I

M

M

P

P

L

L

I

I

F

F

I

I

E

E

D

D

I

I

L

L

L

L

U

U

S

S

T

T

R

R

A

A

T

T

I

I

O

O

N

N

O

O

F

F

T

T

H

H

E

E

S

S

U

U

B

B

O

O

R

R

D

D

I

I

N

N

A

A

T

T

I

I

O

O

N

N

L

L

I

I

M

M

I

I

T

T

A

A

T

T

I

I

O

O

N

N

:

:

Section 401(h) Retiree Medical Contribution $ 6 million

Pension Contribution $ 18 million

Total Contribution to Pension Plan Trust

(other than contributions to fund past service credits) $ 24 million

In this example, the limitation under the Code is met since the retire health

contribution does not exceed the 25% threshold. That is, the $6 million

contribution to the section 401(h) account does not exceed 25% the total

$24 million contribution to the trust.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

This calculation is often determined by actuaries on a “1/3” basis in their

actuarial reports. For example, the $6 million contribution to the section

401(h) account does not exceed 1/3 of the $18 million contribution to the

pension portion of the trust.

Thus, the limitation for contributions to the section 401(h) medical account

could not exceed 1/3 of the pension contribution or in a similar manner,

25% of the total contributions to the trust (the pension contributions plus

the section 401(h) contributions). Either form of calculation nets the same

result mathematically. Note that this example does not consider past

service credits or life insurance protection.

Under section 401(h) of the Code, the subordination limitation is premised

on calculating the amount of actual employer pension contributions to the

plan and aggregate actual contributions for medical benefits from the date

the section 401(h) account is established.

The subordination provision is an “aggregate” or cumulative test. Thus, in

each year the subordination limitation is calculated during an examination,

all contributions to the plan since the date of establishment of the section

401(h) account must be considered.

D

D

E

E

T

T

A

A

I

I

L

L

E

E

D

D

I

I

L

L

L

L

U

U

S

S

T

T

R

R

A

A

T

T

I

I

O

O

N

N

O

O

F

F

T

T

H

H

E

E

A

A

G

G

G

G

R

R

E

E

G

G

A

A

T

T

E

E

S

S

U

U

B

B

O

O

R

R

D

D

I

I

N

N

A

A

T

T

I

I

O

O

N

N

L

L

I

I

M

M

I

I

T

T

A

A

T

T

I

I

O

O

N

N

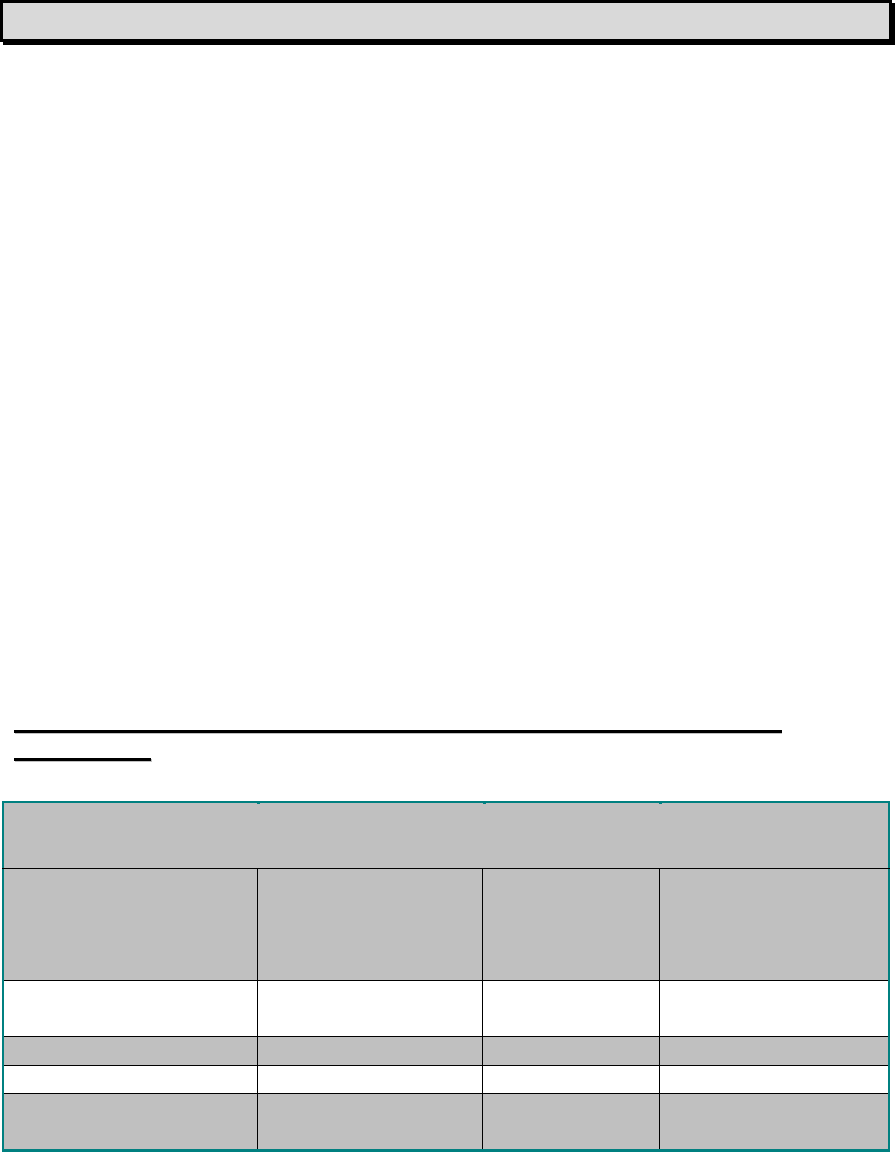

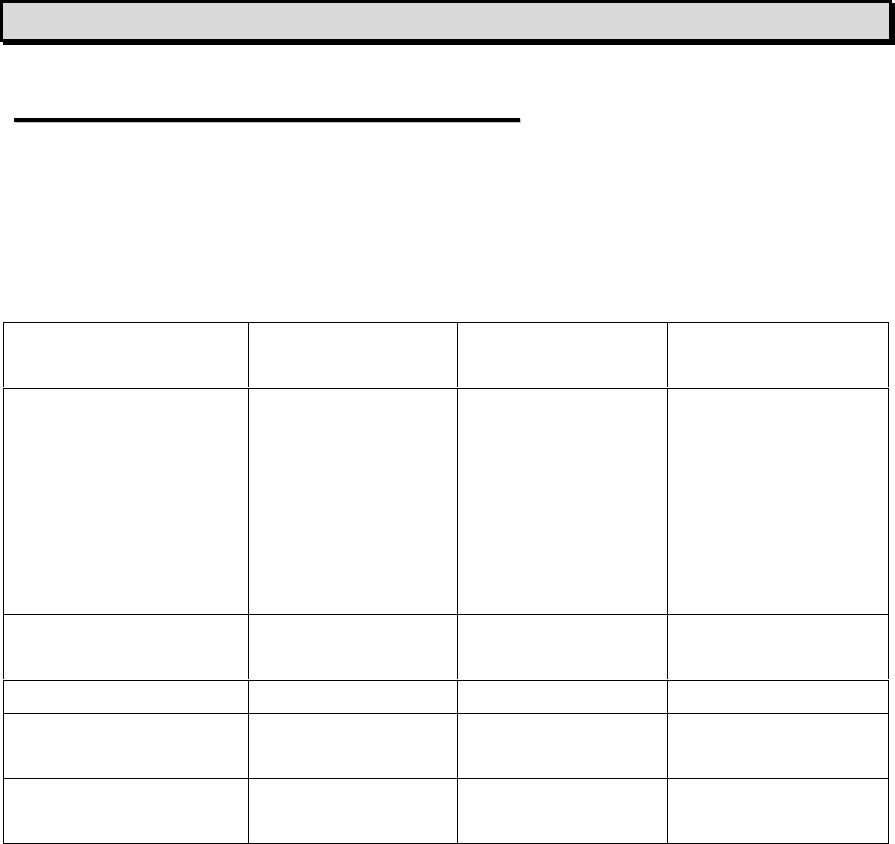

1999 2000 Cumulative

Total

Pension

Contributions (Other

than to fund past

service credits)

$ 20.4 Million $ 16.0 Million $ 36.4 Million

401(h) Account

Contributions $ 2.0 Million $ 6.0 Million $ 8.0 Million

Total Contribution $ 22.4 Million $ 22.0 Million $ 44.4 Million

401(h) as % of Total 8.9 % 27.3 % 18.0 %

Subordination Limit

Test

PASSES for 1999 PASSES for 2000

In the example above, it is assumed that the 401(h) account is established

in 1999 and the relevant contributions are as shown in the table. Since $

2.0 million is less than 25% of $ 22.4 million, the plan meets the

subordination test for 1999. However, since the test is a cumulative test,

even though $ 6.0 million is more than 25% of $ 22.0 million, the plan

meets the subordination test for 2000 on a cumulative basis.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

V

V

I

I

(

(

C

C

)

)

(

(

1

1

)

)

.

.

D

D

A

A

T

T

E

E

O

O

F

F

E

E

S

S

T

T

A

A

B

B

L

L

I

I

S

S

H

H

M

M

E

E

N

N

T

T

The following discusses how the agent should determine the “date of

establishment” during an examination or when reviewing a determination

letter application.

The Committee report for OBRA'89 states "Internal Revenue Service

General Counsel Memorandum 39785 (GCM 39785), issued on April 3,

1989 is rejected to the extent it concludes that contributions to a section

401(h) account may be based on plan costs rather than actual

contributions to the plan. The committee intends that the present-law

rules relating to section 401(h) accounts not be expanded or modified by

the Secretary in a manner that would allow increased contributions to the

section 401(h) account above what is permitted under present law and this

provision."

Accordingly, if the "date of establishment" of a section 401(h) account is

the effective date of the plan amendment adding the 401(h) account, then

the "date of establishment" could be retroactive to a date prior to the date

of adoption of an amendment (such as the first day of the plan year). This

would have the effect of allowing the taxpayer to include contributions

made to the pension plan between the effective date of the account and

the date of adoption of the amendment establishing the account in

satisfying the subordination test.

In changing the law, Congress specifically intended to overturn that

portion of GCM 39785 which had concluded that the subordination test

could be based on "cost" rather than actual contributions. GCM 39785

had allowed a 401(h) account to use pension cost for the entire plan year

in which the amendment to add the 401(h) account was effective. In

amending the law Congress specifically stated that the subordination test

is to be based upon the actual contributions made after the "date of

establishment" of the section 401(h) account.

Thus, the "date of establishment," for purposes of section 401(h), is the

later of the adoption date of the plan amendment adding the 401(h)

account or the effective date of such plan amendment.

Many practitioners and taxpayers misinterpret this Code section and

calculate the contribution limitation under section 401(h) based upon a

retroactive effective date instead of the actual date of adoption.

Retroactive application results in the taxpayer claiming a greater

deduction than entitled to because it is improperly determined based upon

pension contributions made prior to the date of adoption. In addition,

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

utilizing a retroactive effective date may cause the subordination test to be

exceeded in violation of section 401(h)(1).

The following shows the effect on the previous illustration if part of the

$20.4 million pension contribution in 1999 were made prior to the date of

adoption (i.e. "establishment").

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

D

D

A

A

T

T

E

E

O

O

F

F

E

E

S

S

T

T

A

A

B

B

L

L

I

I

S

S

H

H

M

M

E

E

N

N

T

T

I

I

L

L

L

L

U

U

S

S

T

T

R

R

A

A

T

T

I

I

O

O

N

N

:

:

|---------------------------------------------|------------------------|

1/1 10/22 12/31

Improper Retroactive 401(h) Date of

Effective Date Adoption

1999 2000 Cumulative

Total

Pension

Contributions

(Other than to

fund past service

credits) made

after date of

establishment

$ 6.4 Million $ 16.0 Million $ 22.4 Million

401(h) Account

Contributions $ 2.0 Million $ 6.0 Million $ 8.0 Million

Total Contribution $ 8.4 Million $ 22.0 Million $ 30.4 Million

401(h) as % of

Total

23.8 % 27.3 % 26.3 %

Subordination

Limit Test

PASSES for

1999

FAILS for 2000

However, if all or some of the actual contributions were made prior to the

date of establishment of the 401(h) account, then those contributions

would be excluded from the subordination test and the plan could fail to

meet section 401(h)(1).

Note that in situations where the retirement plan is fully funded and the

employer has not made contributions for pension benefits, generally, the

amount of contributions an employer can contribute to the section 401(h)

account is $0 since the subordination limitation would be $0 (25% of

pension contribution). However, the agent should consider the cumulative

application of the subordination limitation when making this determination.

The agent should review the plan document or executed amendment

establishing the Code section 401(h) account to determine the date of

adoption or to determine if the amendment specifies an effective date that

predates the adoption date. Where the plan provisions indicate an

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

improper date of establishment, the agent should consider the introductory

discussion of section VI of this text.

While the agent reviewing a determination letter application would not

have access to the contribution information and would not be able to verify

failure in operation, the examples are included to demonstrate the

implications and importance of proper plan language.

VI(d). Separate Accounts

Section 401(h)(2) provides that a separate account must be established

and maintained.

Section 1.401-14(c)(2) of the regulations provides that section 401(h)

requires that a separate account must be established and maintained

within the pension trust to provide for retiree medical benefits under this

section. This provision requires a separate accounting of the medical

benefits provided within the pension plan.

VI(e). Reasonable and Ascertainable Benefits

Section 401(h)(3) provides that the employer's contribution to such

account must be reasonable and ascertainable.

Section 1.401-14(c)(1)(i) of the regulations provides that a qualified plan

must specify the medical benefits described in section 401(h) which will be

available and must contain provisions for determining the amount which

will be paid.

Section 1.401-14(c)(3) of the regulations provides that section 401(h)

requires that amounts contributed to fund medical benefits therein

described must be reasonable and ascertainable.

Where the plan language provides indications of other sources of payment

for retiree medical benefits, e.g., a VEBA or the general funds of the

employer, the agent should review the plan to determine whether the plan

provisions specify the amounts of benefits, the priority of payment and the

time period with respect to which benefits will be paid from each source.

Where there are other potential sources of payment of medical benefits

such as a welfare benefit fund or the general funds of the employer, the

plan must be specific as to how the benefits payable from the section

401(h) account are coordinated with benefits payable from other sources.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

Without such specificity, a plan participant will not be able to know the

amount of medical benefits which will be paid, and the contributions with

respect to medical benefits payable from the section 401(h) account are

not ascertainable. The plan may not allow for employer discretion in the

timing and amount of benefit payments.

Thus, in accordance with the Code and regulations of this section of the

text, the plan must contain provisions for determining the amount that will

be paid. These requirements will not be satisfied unless the terms of the

plan specify the amount of benefits, the priority of payment from each

source and the time period with respect to which benefits will be paid.

VI(f). No Diversion or Reversion

Section 401(h)(4) provides that all contributions (within the taxable year or

thereafter) to the 401(h) account must be used to pay benefits provided

under the medical plan and must not be diverted to any purpose other

than the providing of such benefits.

Section 401(h)(5) of the Code provides that notwithstanding the provisions

of subsection (a)(2), upon the satisfaction of all liabilities under the plan to

provide such benefits, any amount remaining in such separate account

must, under the terms of the plan, be returned to the employer.

Section 1.401-14(c)(4) of the regulations provides that it must be

impossible at any time prior to satisfaction of all liabilities under the plan

for any part of the corpus or income to be used for or diverted to any

purposes other than providing medical benefits under the account.

Consequently, a plan which, for example, under its terms, permits funds in

the medical account to be used for any retirement benefit provided under

the plan does not satisfy the requirements of section 401(h) and will not

qualify under section 401(a).

VI(g). Key Employee Accounts

Section 401(h)(6) of the Code provides that in the case of an employee

who is a key employee, a separate account is established and maintained

for such benefits payable to such employee (and his spouse and

dependents) and such benefits (to the extent attributable to plan years

beginning after March 31, 1984, for which the employee is a key

employee) are only payable to such employee (and his spouse and

dependents) from such separate account. The term “key employee”

means any employee, who at any time during the plan year or any

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

preceding plan year during which contributions were made on behalf of

such employee, is or was a key employee as defined in section 416(i).

Thus, the agent should review plan provisions to ensure the plan language

reflects section 401(h)(6) where medical benefits are to be provided to key

employees. Where key employees are excluded from eligibility for

medical benefits under the section 401(h) account, the agent should

ensure that the plan provisions specifically provide for this exclusion.

VI(h). Employee or Employer Contributions

Treasury Regulation 1.401-14(b)(3) states that contributions to provide the

medical benefits described in section 401(h) may be made either on a

contributory or non-contributory basis, without regard to whether the

contributions to fund the retirement benefits are made on a similar basis.

Thus, for example, the contributions to fund the medical benefits may be

provided for entirely out of employer contributions even though the

retirement benefits under the plan are determined on the basis of both

employer and employee contributions.

Where the plan is ambiguous as to whether contributions to the section

401(h) account are provided entirely from employer contributions or

whether they will be paid from employer and employee contributions, the

agent should request a clarifying amendment to the plan.

VI(i). Caveats

For determination applications that include a cover letter requesting

consideration of section 401(h) features, these provisions should be

reviewed. A caveat stating that section 401(h) was reviewed in

accordance with the cover letter for the application should be included on

the determination letter in accordance with section 2.04 of Revenue

Procedure 2000-6.

For plans which contain section 401(h) provisions where a ruling was not

requested, the agent should include a caveat stating that the section

401(h) features were not reviewed since the applicant did not request

such review in accordance with section 2.04 of Revenue Procedure 2000-

6.

A caveat such as the following is inappropriate for section 401(h) features

in a pension or annuity plan. This caveat applies only to defined

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

contribution plans that provide for medical or disability benefits as

described in section 1.401-1(b)(1)(ii) of the Income Tax Regulations.

This letter does not express an opinion with respect to whether

(disability benefits or medical care benefits) are acceptable as

accident or health plan benefits, nor does it express an opinion on

the taxability of such benefits under sections 105 or 106.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

VI(j). Section 420 Transfers

Section 420 of the Code permits the transfer of assets in a defined benefit

plan from the defined benefit portion of the plan to a section 401(h)

account within the same pension trust for payment of current retiree

medical benefits.

When reviewing a determination letter application, the agent should review

the cover letter to determine whether the employer or employer’s

representative has requested a ruling on the section 420 plan provisions in

accordance with Revenue Procedure 2000-6. Appendix B of this text

contains a checklist agents should utilize when reviewing these

determination letter applications. Appendix B also contains the provisions

relating to when rulings will or will not be issued on section 420. Note that

Form 6406 may not be used to request a determination letter that

considers section 420.

VII. Deductions for Welfare Benefits Exclusive of Section 401(h)

This section discusses the general concepts applicable to the deduction of

employer contributions when a trust is not utilized or when the employer

establishes a VEBA trust to fund these benefits. Deductions for employer

contributions to a section 401(h) account are discussed in section VIII of

this text.

VII(a). Deduction Without the Use of a Trust

To understand why an employer would consider using a trust to provide

employee benefits, it is helpful to first review the basic mechanics of a

deduction in situations where no funding vehicle is used. An employer’s

deduction for the expense of providing welfare benefits to its employees is

governed by sections 162 and 461 of the Code at the time the employer

pays (or properly accrues) the expense liability. The lead case in this area

is General Dynamics Corporation v. United States, 107 S. Ct. 1732; 481

U.S. 239 (1987). These costs may be paid to the employee, the care

provider, or an insurance company. They may also be paid through a

third party benefit administrator.

In the absence of a trust, employers generally may only deduct amounts

paid for these benefits on a pay-as-you-go basis. In order to prefund and

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

deduct amounts for future benefit obligations, employer contributions must

be funded through a trust.

VII(b). Funding Welfare Benefit Obligations

Employers may decide to fund their obligations to provide employee

welfare benefits through the use of a trust. An irrevocable employee

welfare benefit trust created by an employer can place assets beyond the

reach of the creditors of the employer and can provide employees with

some assurance that assets will be available to pay the promised benefits.

In addition, funding benefits obligations through a trust may provide

employers the opportunity to fund and deduct a greater amount of

contributions to employee welfare benefit plans as permitted by the Code.

Title I of ERISA, Act section 3, defines an “employee welfare benefit plan”

and “welfare plan” as any plan, fund, or program which was heretofore or

is hereafter established or maintained by an employer or by an employee

organization, or by both, to the extent that such plan, fund, or program

was established or is maintained for the purpose of providing for its

participants or their beneficiaries, through the purchase of insurance or

otherwise,

(A) medical, surgical, or hospital care or benefits, or benefits in the event of

sickness, accident, disability, death or unemployment, or vacation benefits,

apprenticeship or other training programs, or day care centers, scholarship

funds, or prepaid legal services, or

(B) any benefit described in section 302(c) of the Labor Management Relations

Act of 1947, 29 USCS section 186(c), (other than pensions on retirement or

death, and insurance to provide such pensions).

Thus, an “employee welfare benefit plan" is a program of benefits provided

to employees. The plan is usually embodied in a written plan document.

Generally, Title I of ERISA requires the employer to prepare a "summary

plan description" explaining the essential features of the plan and to

furnish a copy of this summary plan description to each employee.

The "trust" is the employer’s vehicle for funding its obligation under a plan

or plans. A trust is usually established by a written trust instrument

naming the employer as the settlor of the trust, appointing a trustee, and

describing the powers and duties of the trustee.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

An employer may choose to fund some, or all, of the benefits under its

plan through one or more trusts. A trust may cover more than one plan,

e.g., a medical plan and a disability plan. The trust instrument will set

forth the benefits that the trustee will pay out of the trust fund. The

employer will be responsible for paying other plan benefits, either directly

from the employer’s general accounts or through a different trust.

Within the context of this text, welfare benefits may be funded through

either a VEBA trust or through a section 401(h) account contained within a

section 401(a) pension plan trust (unless paid without the use of a trust).

For a pension trust that contains a section 401(h) account, the trustee files

a Form 5500 information return for the pension trust. In the event the

pension trust is no longer “qualified” under section 401(a) of the Code, the

trustee files Form 1041, U.S. Fiduciary Income Tax Return for the taxable

trust.

VII(c). Deduction Using a VEBA Trust

For a VEBA trust, the trustee files Form 990, Return of Organization

Exempt from Income Tax, for exempt trusts. In the event the trust is no

longer “exempt” from taxes under sections 501(c)(9) and 501(a) of the

Code, the trustee files Form 1041, U.S. Fiduciary Income Tax Return for

the taxable trust.

Deductions for employer contributions to VEBA trusts are governed by

sections 419 and 419A of the Code. In the event contributions to the

VEBA are “overfunded” as determined under these Code sections, the

trust may be required to file Form 990-T, Exempt Organization Business

Income Tax Return. See Employee Plans CPE Technical Topics for 1998

Training 4213-018 (Rev.5/98) for additional information on VEBA

deduction issues. The text may be accessed at

http://ftp.fedworld.gov/pub/irs-utl/lesson5.pdf.

VIII What Should You Review During an Examination

The following sections discuss specific issues to be considered by the

agent when examining a pension plan containing a section 401(h)

account. These sections should be considered in conjunction with the

provisions discussed in section VI of this text in order to determine

whether these provisions qualify under section 401(h) of the Code in

operation.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

VIII(a). Section 162 Deduction Provisions Applicable to Section

404

Deductions for employer contributions to a section 401(h) account are

generally governed by section 404 of the Code which is derived from the

general business deductions permitted under section 162.

Section 162(a) of the Code generally provides a deduction for all ordinary

and necessary expenses paid or incurred during the taxable year in

carrying on any trade or business.

Section 162(o) of the Code provides a cross-reference to section 404 for

deductibility for deferred compensation and other deferred benefits.

Section 1.162-10(a) of the regulations provides that accident or health

benefits which may be deductible under this section are governed by and

deductible under section 404 of the Code if the benefits are provided as

part of a pension or other deferred compensation plan referred to in

section 404(a).

Section 1.404(a)-1(b) of the regulations provides that in order to be

deductible under section 404(a), contributions must be expenses which

would be deductible under section 162 (relating to trade or business

expenses) or 212 (relating to expenses for production of income) if it were

not for the provision in section 404(a) that they are deductible, if at all, only

under section 404(a).

VIII(b). Section 404 Deduction Provisions for Section 401(h)

When examining the deduction of employer contributions to a section

401(h) account within a pension plan, the agent should consult with a

TE/GE actuary in determining the limitation thereunder. The remainder of

this section of the text describes the Code and regulations that apply in

determining the deductible limits for contributions to a section 401(h)

account.

Section 404(a)(1) of the Code limits deductible contributions to one or

more defined benefit pension plans or money purchase pension plans

maintained by an employer which are funded through a trust.

Section 404(a)(2) of the Code limits deductible contributions to one or

more defined benefit pension plans or money purchase pension plans

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

maintained by an employer which are funded through annuity contracts or

annuity contracts and medical benefits as described in section 401(h).

Section 1.404(a)-3(a) of the regulations provides if contributions are paid

by an employer to or under a pension trust or annuity plan for employees

and the general conditions and limitations applicable to deductions for

such contributions are satisfied (see section 1.404(a)-1), the contributions

are deductible under section 404(a)(1) or (2) if the further conditions

provided therein are also satisfied.

Section 1.404(a)-3(a) of the regulations continues by stating that where

medical benefits described in section 401(h) and as defined in paragraph

(a) of section 1.401-14 are provided for retired employees, their spouses,

or their dependents under the plan, deductions on account of such

subordinate benefits are also covered under section 404(a)(1) or (2).

Section 1.404(a)-3(f)(1) of the regulations provides that in determining the

amount which is deductible with respect to contributions to provide

retirement benefits under a plan, amounts contributed for the funding of

medical benefits described in section 401(h) of the Code shall not be

taken into consideration.

Section 1.404(a)-3(f)(2) of the regulations further provides that the

amounts deductible with respect to employer contributions to fund medical

benefits described in section 401(h) shall not exceed the total cost of

providing such benefits. The total cost of providing such benefits shall be

determined in accordance with any generally accepted actuarial method

which is reasonable in view of the provisions and coverage of the plan, the

funding medium, and other applicable considerations. The amount

deductible for any taxable year with respect to such cost shall not exceed

the greater of

(i) an amount determined by distributing the remaining

unfunded costs of past and current service credits as a level

amount, or as a level percentage of compensation, over the

remaining future service of each employee, or

(ii) 10 percent of the cost which would be required to completely

fund or purchase such medical benefits.

In determining the amount deductible, section 1.404(a)-3(f)(2) of the

regulations provides that an employer must apply either

(i) above for all employees or

(ii) (ii) above for all employees.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

Thus, the provisions above apply to limit the deduction of employer

contributions for medical benefits provided through a section 401(h)

account.

The Committee Reports state that the second requirement under section

401(h) is that a separate account must be established. This allocation is

necessary in order to enable the Commissioner of Internal Revenue to

determine whether the actuarial limitations imposed by section 404 of the

Code on deductions claimed for pension contributions are properly

applied. See, H. Rep. No. 2317, 87

th

Congress, 2

nd

Sess. at 1208.

The Committee Reports state that the third requirement is that the

employer’s contribution to fund medical and other benefits must be

reasonable and ascertainable. Thus, it must be possible under the plan to

determine the portion of the employer’s contribution which is made to fund

the pension benefits and the portion of the contribution made under the

plan which is made to fund the medical, etc. benefits. As under existing

law, if any portion of the contribution to provide either pension or medical,

etc. benefits does not meet the ordinary and necessary tests, the

employer will not be permitted to deduct the entire amount of such

contribution under section 404 of the Code. See, H. Rep. No. 2317, 87

th

Congress, 2

nd

Sess. at 1208.

Treasury Regulation 1.404(a)-3(a) detailed above and these Committee

Reports imply a connection between meeting the subordination test of

section 401(h)(1) in operation and deductibility of those contributions

under section 404.

VIII(c). Section 404(a)(7) Applicability

Section 404(a)(7) of the Code applies to limit the amount otherwise

deductible under paragraphs (1), (2) or (3) of section 404(a) for employer

contributions to one or more defined contribution plans and one or more

defined benefit plans. In general, the total amount deductible in a taxable

year under such plans shall not exceed the greater of (i) 25 percent of the

compensation otherwise paid or accrued during the taxable year to the

beneficiaries under such plans, or (ii) the amount of contributions made to

or under the defined benefit plans to the extent such contributions do not

exceed the amount of employer contributions necessary to satisfy the

minimum funding standard provided by section 412 with respect to any

such defined benefit plans.

Under section 401(h) of the Code, a pension plan may provide for the

payment of medical benefits for retired employees, their spouses and

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

dependents, if, among other provisions, a separate account is established

and maintained for such benefits.

Section 1.404(a)-3(f)(1) of the regulations provides that in determining the

amount which is deductible with respect to contributions to provide

retirement benefits under a plan, amounts contributed for the funding of

medical benefits described in section 401(h) of the Code shall not be

taken into consideration.

For deduction purposes, therefore, a pension plan that includes a section

401(h) retiree medical benefits account is treated under the provisions of

the Code and regulations as two separate plans, one providing medical

benefits and the other providing retirement benefits.

While section 404(a)(7) of the Code applies to limit the deductions

otherwise allowed under section 404 for contributions made to fund

retirement benefits, if the contributions are made to provide medical

benefits described in section 401(h) of the Code and are kept in one or

more separate accounts, such contributions will not be subject to the

aggregate deductible limitation under section 404(a)(7) of the Code. The

deductibility of these contributions will be determined in accordance with

the rules and limitations in section 1.404(a)-3(f) of the regulations.

VIII(d). Section 263A Uniform Capitalization

The application of section 263A of the Code to deductions governed by

section 404 are currently being considered by the Section 263A Technical

Advisor and the Cafeteria Plan Technical Advisors.

Section 404 of the Code contains the general limitations on the

deductibility of contributions made to qualified retirement plans. Section

404 similarly applies to contributions made to section 401(h) retiree

medical accounts. Generally, if contributions made for qualified retirement

plans and section 401(h) accounts meet the provisions of section 404 and

the regulations thereunder, they are deductible in their entirety in

accordance with this section.

However, the provisions of section 263A of the Code require that certain

expenses must be capitalized instead of currently expensed and

deducted. Section 263A generally requires the capitalization of otherwise

deductible direct and indirect costs properly allocable to real property and

tangible personal property produced by a taxpayer as well as property

acquired by a taxpayer for resale.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

T

T

H

H

E

E

S

S

E

E

C

C

T

T

I

I

O

O

N

N

2

2

6

6

3

3

A

A

C

C

O

O

S

S

T

T

S

S

A

A

R

R

E

E

C

C

O

O

M

M

P

P

U

U

T

T

E

E

D

D

A

A

S

S

F

F

O

O

L

L

L

L

O

O

W

W

S

S

:

:

Section 471 costs

+ Additional 263A costs

+ Interest capitalized under 263A

Section 263 Costs

========================

Direct and indirect costs are defined in Treas. Reg. 1.263A-1(e). Indirect

costs are defined as all costs other than direct material costs and direct

labor costs. Indirect costs are properly allocable to property produced or

property acquired for resale when the costs directly benefit or are incurred

by reason of the performance of production or resale activities. Indirect

costs as defined in the regulations include employer contributions

for qualified retirement plans, health insurance, life insurance and

other employee welfare and fringe benefits. See Treas. Reg. 1.263A-

1(e)(3)(D).

Any questions relating to the applicability of section 263A to contributions

governed by section 404 may be directed to James Peschl, Section 263A

Technical Advisor, at (763) 549-1020, extension 330 or the Cafeteria Plan

Technical Advisors at the telephone numbers listed in Appendix D.

IX. Other Examination Issues

When examining the subordination limitation of section 401(h), the agent

should also consider section VI(c) of this text in order to determine

whether the qualification provisions of section 401(h) have been met in

operation.

IX(a). Subordination Limitation

The Omnibus Reconciliation Act of 1989 (OBRA'89) modified section

401(h) of the Code by adding the following language, “In no event shall

the requirements of paragraph (1) [(the subordination requirement)] be

treated as met if the aggregate actual contributions for medical benefits,

when added to actual contributions for life insurance protection under the

plan, exceed 25 percent of the total actual contributions to the plan (other

than contributions to fund past service credits) after the date on which the

account is established."

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

If a prior determination letter was issued which approved a retroactive

effect date, or other plan provision defects under section 401(h), the agent

should consider the following.

Sections 5.01, 5.02 and 21.05 of Revenue Procedure 2000-6 provide the

parameters of reliance by employers on determination letters. Section

21.05 states that while a favorable determination letter may serve as a

basis for determining deductions for employer contributions thereunder, it

is not to be taken as an indication that contributions are necessarily

deductible as made. This latter determination can be made only upon an

examination of the employer’s tax return, in accordance with the

limitations, and subject to the conditions of section 404 of the Code.

The determination letter specifically states that it relates to the qualified

status of the plan and refers in a caveat to a section of Publication 794

entitled “Limitations of a Favorable Determination Letter.” Publication 794

is attached to all determination letters. This section provides that, “a

determination letter does not consider whether actuarial assumptions are

reasonable for funding or whether a specific contribution is deductible

(emphasis added).

Internal Revenue Manual sections 7717.2(1) and 7717.1(5) generally

provide that a ruling or determination letter found to be in error or not in

accord with the current views of the Service may be modified or revoked.

Modification or revocation may be effected by a notice to the taxpayer to

whom the ruling or determination letter originally was issued, or by a

Revenue Ruling or other statement published in the Internal Revenue

Bulletin.

Accordingly, the Service should notify the taxpayer that the plan should be

amended prospectively to use a corrected “date of establishment” when

calculating the aggregate subordination limitation under section 401(h)

and the corresponding deduction under section 404 of the Code for

current and subsequent plan years.

During an examination, Form 5701, Notice of Proposed Adjustment,

should be used to formally notify the taxpayer of prospective application.

I

I

X

X

(

(

A

A

)

)

(

(

1

1

)

)

.

.

L

L

I

I

F

F

E

E

I

I

N

N

S

S

U

U

R

R

A

A

N

N

C

C

E

E

P

P

R

R

O

O

T

T

E

E

C

C

T

T

I

I

O

O

N

N

The Omnibus Reconciliation Act of 1989 (OBRA'89) modified section

401(h) of the Code by adding the following language, “In no event shall

the requirements of paragraph (1) [(the subordination requirement)] be

treated as met if the aggregate actual contributions for medical benefits,

when added to actual contributions for life insurance protection under the

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

plan, exceed 25 percent of the total actual contributions to the plan (other

than contributions to fund past service credits) after the date on which the

account is established."

Treas. Reg. 1.401-14(c)(1) provides that life insurance protection includes

any benefit paid under the plan on behalf of an employee-participant as a

result of the employee-participant’s death to the extent such payment

exceeds the amount of the reserve to provide retirement benefits existing

at his death (note that this regulation has not been revised to reflect

OBRA ’89 statutory change which codified the subordination test).

Thus, the section 401(h) subordination limitation is further reduced by any

contributions to the qualified plan for life insurance protection. The term

“life insurance protection” is not further clarified by the Code or

regulations. Therefore, the agent should consult with their TE/GE field

actuary for assistance in determining this component of the subordination

limitation or consider requesting technical advice.

I

I

X

X

(

(

A

A

)

)

(

(

2

2

)

)

.

.

P

P

A

A

S

S

T

T

S

S

E

E

R

R

V

V

I

I

C

C

E

E

C

C

R

R

E

E

D

D

I

I

T

T

S

S

The Omnibus Reconciliation Act of 1989 (OBRA'89) modified section

401(h) of the Code by adding the following language, “In no event shall

the requirements of paragraph (1) [(the subordination requirement)] be

treated as met if the aggregate actual contributions for medical benefits,

when added to actual contributions for life insurance protection under the

plan, exceed 25 percent of the total actual contributions to the plan (other

than contributions to fund past service credits) after the date on which the

account is established."

Thus, the section 401(h) subordination limitation must be based upon

retirement plan contributions other than contributions to fund past service

credits. Often when determining the subordination limitation, taxpayers

improperly use the total amount of pension contributions instead reducing

the amount of pension contributions by the portion of the contribution to

fund “past service credits.”

Note that “contributions to fund past service credits” probably is the same

thing as past service contributions. However, the term “past service

credits” referenced in section 401(h) is not further clarified by the Code or

regulations. Therefore, the agent should consult with their TE/GE field

actuary for assistance in determining the amount the “contributions to fund

past service credits” or consider requesting technical advice.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

IX(b). Key Employee Accounts

Section 401(h)(6) of the Code provides that in the case of an employee

who is a key employee, a separate account is established and maintained

for such benefits payable to such employee (and his spouse and

dependents) and such benefits are only payable to such employee (and

his spouse and dependents) from such separate account. The term “key

employee” means any employee, who at any time during the plan year or

any preceding plan year during which contributions were made on behalf

of such employee, is or was a key employee as defined in section 416(i).

Therefore, the plan should state whether “ key employees” are eligible to

participate. The plan may not provide that the employer has the discretion

to determine at any time whether key employees may participate or

whether only certain key employees may participate.

During an examination, the agent should review plan records to verify that

separate accounts are established or maintained for each of the key

employees and that benefits are only payable to key employees from their

separate account as provided in section 401(h) of the Code.

IX(c). Section 415 Considerations

Section 415 of the Code provides the limitations on benefits and

contributions under qualified plans. Section 415(c) of the Code provides

the limitations on benefits and contributions for defined contribution plans.

Section 415(l) of the Code provides for the treatment of certain medical

benefits under section 415 of the Code. This section provides:

(1) In general. For purposes of this section, contributions allocated to any

individual medical account which is part of a pension or annuity

plan shall be treated as an annual addition to a defined

contribution plan for purposes of subsection (c). Subparagraph (B)

of subsection (c)(1) shall not apply to any amount treated as an

annual addition under the preceding sentence.

(2) Individual medical benefit account. For purposes of paragraph (1),

the term "individual medical benefit account" means any separate

account—

(A) which is established for a participant under a pension or

annuity plan, and

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

(B) from which benefits described in section 401(h) are payable

solely to such participant, his spouse, or his dependents.

Thus, when examining a section 401(h) account and/or a qualified defined

contribution plan, the agent should consider amounts contributed to key

employee accounts in a section 401(h) account when determining whether

the limitations of section 415(c) for the defined contribution plan have

been met.

Similar provisions apply to key employee accounts in a VEBA trust.

Section 419A(d) provides the requirement of separate accounts for post-

retirement medical or life insurance benefits provided to key employees in

a VEBA trust. This section provides:

1 In general. In the case of any employee who is a key employee--

(A) a separate account shall be established for any medical

benefits or life insurance benefits provided with respect to such

employee after retirement, and

(B) medical benefits and life insurance benefits provided with

respect to such employee after retirement may only be paid

from such separate account. The requirements of this

paragraph shall apply to the first taxable year for which a

reserve is taken into account under subsection (c)(2) and to all

subsequent taxable years.

(2) Coordination with section 415. For purposes of section 415, any

amount attributable to medical benefits allocated to an account

established under paragraph (1) shall be treated as an annual

addition to a defined contribution plan for purposes of section

415(c). Subparagraph (B) of section 415(c)(1) shall

not apply to any amount treated as an annual addition under the

preceding sentence.

(3) Key employee. For purposes of this section, the term 'key

employee' means any employee who, at any time during the plan

year or any preceding plan year, is or was a key employee as

defined in section 416(i).

Thus, when examining a VEBA, section 401(h) account and/or a qualified

defined contribution plan, the agent should consider amounts contributed

to key employee accounts in a VEBA and a section 401(h) account when

determining whether the limitations of section 415(c) for the defined

contribution plan have been met.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

While separate accounts are not required for employees who are not key

employees, there is nothing that precludes a plan from establishing

separate accounts under section 401(h) or in a VEBA for each employee.

If that is the case, the agent should consider amounts contributed to each

account when determining whether the limitations of section 415(c) for the

defined contribution plan have been met. Note that in the typical case

separate accounts are not established for employees who are not key

employees.

IX(d). Section 420 Considerations

If the agent encounters any activity involving transfer of assets as

described in section 420 of the Code, the agent should review the

requirements of section VI(i) and Appendix B of this text and should

consult with their TE/GE field actuary for assistance.

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

Appendix A: Rev. Proc. 2000-6 Section 401(h) Ruling Sections

and Checklist

Revenue Procedure 2000-6 sets forth the procedures of the various

offices of the Internal Revenue Service for issuing determination letters on

the qualified status of pension, profit-sharing, stock bonus, annuity, and

employee stock ownership plans (ESOPs) under sections 401, 403(a),

409 and 4975(e)(7) of the Internal Revenue Code of 1986, and the status

for exemption of any related trusts or custodial accounts under section

501(a).

This revenue procedure also contains the provisions to consider when

reviewing a determination letter application where the plan includes

section 401(h) features.

Section 2.04, of Revenue Procedure 2000-6, references changes made

for section 401(h) provisions. This section provides that Section 16 has

been modified to state that a determination letter that considers whether

the requirements of 401(h) are satisfied in a plan will be issued only if the

plan sponsor requests such consideration in a cover letter submitted with

the application and indicates in the cover letter the location of plan

provisions that satisfy the requirements of section 401(h).

Section 3.02, of Revenue Procedure 2000-6, discusses areas in which

determination letters will not be issued. Section (4) applies to

determination letter requests with respect to plans that combine an ESOP

(as defined in section 4975(e)(7) of the Code) with retiree medical benefit

features described in section 401(h) (HSOPs). Otherwise, determinations

will consider section 401(h) in accordance with sections 2.04 and section

16. This section provides the following:

(a) In general, determination letters will not be issued with respect to

plans that combine an ESOP with an HSOP with respect to:

(i) whether the requirements of section 4975(e)(7) are

satisfied;

(ii) whether the requirements of section 401(h) are satisfied; or

(iii) whether the combination of an ESOP with an HSOP in a

plan adversely affects its qualification under section 401(a).

(b) A plan is considered to combine an ESOP with an HSOP if it

EMPLOYEE PLANS CPE TECHNICAL TOPICS FOR 2001

contains ESOP provisions and section 401(h) provisions.

(c) However, an arrangement will not be considered covered by

section 3.02(4) of this revenue procedure if, under the provisions

of the plan, the following conditions are satisfied:

(i) No individual accounts are maintained in the section 401(h)

account (except as required by section 401(h)(6));

(ii) No employer securities are held in the section 401(h)

account;

(iii) The 401(h) account does not contain the proceeds (directly

or otherwise) of an exempt loan as defined in section

54.4975-7(b)(1)(iii) of the Pension Excise Tax Regulations;

and

(iv) The amount of actual contributions to provide section

401(h) benefits (when added to actual contributions for life

insurance protection under the plan) does not exceed 25

percent of the sum of: (1) the amount of cash contributions

actually allocated to participants' accounts in the plan and

(2) the amount of cash contributions used to repay principal

with respect to the exempt loan, both determined on an

aggregate basis since the inception of the section 401(h)

arrangement.

GATT, SBJPA, and TRA '97

Section 16, of Revenue Procedure 2000-6, references the requirements

for section 401(h) and section 420 determination letters. Section 16.01

states that this section provides procedures for requesting determination

letters (i) with respect to whether the requirements of section 401(h) are

satisfied in a plan with retiree medical benefit features and (ii) on plan

language that permits, pursuant to section 420, the transfer of assets in a

defined benefit plan to a health benefit account described in section

401(h).

Section 16.02, of Revenue Procedure, 2000-6, provides the information

required for section 401(h) determinations. This section states that EP

determinations will issue a determination letter that considers whether the