!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

1000 series

The Standards of Practice covering 1000 Series, Office of Fiscal Services, are

still in review — with the exception of the SPs governing the Student Activities

Fund, represented by the 1500 series.

In the meantime, this document provides relevant guidance for policies and

regulations impacting Fiscal Services.

Please note that the linked materials include relevant Board of Education

policies, although some policies and numbers may have changed as a result of

the Board's update of its policies.

OFFICE OF FISCAL SERVICES

Standard Practices Series 1000

PAGES

SP 1000: Office of Fiscal Services; Overview of 1

SP 1101: Position Control Procedures—Non-WSF Programs 3

SP 1102: FMS Reports; School/Offices 4

SP 1103: FMS Reports; Monitoring by Program Managers 10

SP 1104: FMS Processing Schedule 13

SP 1105: FMS Corrections to Accounting Codes and/or Amounts 14

SP 1106: Revenue/Cash Receipt Collections 16

SP 1120: Non-Appropriated Local School Fund; Description of and Chart 22

of Accounts and General Purpose

SP 1121: Non-Appropriated Local School Fund; Administrator’s Checklist/ 25

Internal Controls

SP 1122: Non-Appropriated Local School Fund; Preparation for Financial Audit 26

SP 1123: Non-Appropriated Local School Fund; Collection and Deposit 28

Procedures

SP 1124: Non-Appropriated Local School Fund Bank Reconciliations; 31

Procedures for

SP 1125: Non-Appropriated Local School Fund; Expenditure of Funds 34

SP 1126: Non-Appropriated Local School Fund; Investing Idle Cash 36

SP 1127: Non-Appropriated Local School Fund; Financial Reporting 38

Requirements

SP 1128: Non-Appropriated Local School Fund; School Clubs 40

SP 1129: Non-Appropriated Local School Fund; Field Trips 41

SP 1130: Non-Appropriated Local School Fund; Gifts, Grants and 43

Requests (Donations)

SP 1131: Non-Appropriated Local School Fund; Fundraising Activities 44

SP 1132: Non-Appropriated Local School Fund: School Stores, Sale 46

of PE/School Uniforms

SP 1133: Non-Appropriated Local School Fund; Independent Organizations 47

(PTSA, PTA, Boosters, etc.)

PAGES

SP 1134: Non-Appropriated Local School Fund: Bank Account Set Up 49

and Maintenance

SP 1135: Non-Appropriated Local School Fund; Processing Invoices 50

for Payment

SP 1136: Non-Appropriated Local School Fund; Refund and Reimbursements 52

SP 1200: Payroll Calculations for Salaried

Employees—Ten (10) 53

Month Employees

SP 1201: Payroll Calculations for Salaried Employees—Twelve (12) 56

Month Employees

SP 1202: Casual Employees; Casual Payroll System; Processing 59

SP 1203: Teacher Substitute Employee Automated System (TSEAS); 61

Processing

SP 1205: Individual Time Sheet; Form D-55 63

SP 1206: Employee Organizational Timesheet; Form D-56 64

SP 1207: Notification of Temporary Assignment (Form SF-10) 65

SP 1208: Request for Overtime; Form BP-2 65

SP 1209: Claim for Lost Check/Non-Received Check; Procedures for 66

SP 1209.1: Claim for Escheated Check/Voided Check 67

SP 1210: Wage and Tax Statement (Form W-2); Request for Duplicate 68

SP 1211: Tax Withholding Exemption Changes (Federal W-4, State HW-4) 69

SP 1212: Salary Assignment/Cancellation Form D-60 for Bank Assignment (BA) 70

SP 1213: Salary Assignment/Cancellation Form D-60 for Credit Union Deduction 72

SP 1214: Savings Bond Authorization (State Accounting Form D-68) 74

SP 1235: Change of Leave Code Request (Form BLA-01) 75

SP 1240: Payment Processing; Introduction 77

SP 1241: Payment Processing: Supporting Documentation Required 78

SP 1242: Credit

Memos; Definitions and Procedures 79

SP 1243: Approval to Pay (ATP) Types; Descriptions 80

SP 1244: Direct Payments; Supplemental, Split, Advance, and Employee 82

Reimbursements

SP 1245: Blanket Purchase Orders; Guidelines 83

PAGES

SP 1246: Petty Cash Replenishment; Procedures 84

SP 1247: Monitoring Status of Payments; Procedure 85

SP 1248: Interest Charges on Late Payments; Procedures 86

SP 1249: Contract Payments; Required Documents 88

SP 1250: Procurement Card; Overview 89

SP 1251: Procurement Card Purchasing and Payment Process 91

SP 1252: Procurement Card Controls 93

SP 1253: Procurement Card Change of Accounting Codes 94

SP 1254: Procurement Card Reports 95

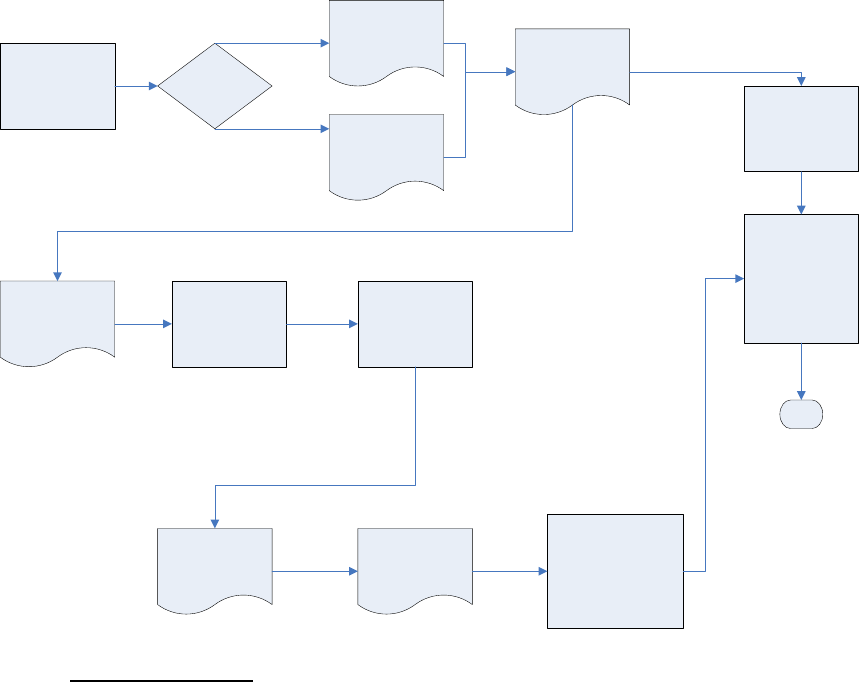

SP 1261: Inter/Intra-Island Travel Procedures 96

SP 1262: Inter/Intra Island Travel Procedural Flow 99

SP 1263: Inter/Intra Island Travel Frequently Asked Questions 103

SP 1264: Out-of-State Travel Policies 106

SP 1265: Out-of-State Travel Procedures 109

SP 1266: Out-of-State Travel

Required Supporting Documents 114

SP 1267 Out-of-State Travel Completed Report 119

SP 1268: Out-of-State Travel Procedural Flow 121

SP 1270: Automobile Allowances 125

SP 1280: Inter/Intra Island Travel Policies 127

SP 1281: Decaling; Guidelines for 130

SP 1282: Annual Physical Inventory Verification—Reports and Deadlines 131

SP 1284: Disposal of Property—Procedures and Process Flowchart 133

SP 1286: Transfers of State Property 138

SP 1287: Off-Site Use of Property Form 140

SP 1288:

Motor Vehicles—Registration, Junking and Other Procedures 141

SP 1289: Inventory Forms 144

SP 1301: Local School Account Audits (Non-Appropriated); Description of 145

SP 1310: Procurement of Goods 147

SP 1320: Procurement and Contracting for Construction 152

SP 1330: Procurement of Services 152

SP 1340: Procurement of Professional Services 158

SP 1350: Procurement of Health and Human Services 160

PAGES

SP 1370: 162

SP 1602:

SP 1603:

SP 1604:

SP 1605:

Risk Management Services

Budget Branch Introduc

tion

Operating Budget Preparation Process

Budget Execution Process

Budget Policies of the Board of Education; Compliance With

SP 1611: Budg

et, Weighted Student Formula 189

SP 1622: Budget Request Database; Instructions for 192

SP 1623: Budget Execution; Introduction to Procedures and Manuals 195

SP 1623.1: Budget Allocation Process; Description of 196

SP 1623.2: Financial Systems; Description of 199

SP 1623.3: Expenditure Plans; Description of Process 203

SP 1623.4: Budget—Carryover Funds; Guidelines and Procedures for 205

SP 1623.5: Deficit Spending: Prohibition and Procedures for Clearing 208

SP 1623.6 School-Based Budgeting: Teacher Participation 210

SP 1624: Federal Budget Execution Procedures; Introduction to 211

SP 1624.1: Federal Fund Allocation Process 212

SP 1624.2: Federal Fund Allocations; Description of Flexibility 214

SP 1624.3 Federal Fund Position; Process for Creating 215

SP 1624.4: Federally Funded Personnel; Description of Actual Payroll Costs 219

SP 1624.5: Federal Fund Fringe Benefit Costs; Actual vs Estimated 220

SP 1624.6: Federal Fund Lapse Date 221

SP 1624.7: Federal Fund Carryover Allocation Year 222

SP 1625: Selling

EDN 100 Categorical Positions 223

SP 1626: Budget: Chapter 42F, HRS; Guidelines and Procedures 225

SP 1627: Unbudgeted Needs; Procedure to Request 228

SP 1629: Budget; Buying or Selling Indexed Complex Area Allocation 230

Positions

180

181

185

187

PAGES

SP

1631: Internal Financial Controls; Description of 234

SP 1633: Position Control Procedures for WSF Positions 235

SP 1634: Fiscal Implementation of Approved Reorganizations 237

1

SP 1000: Office of Fiscal Services; Overview of

1. Purpose

To provide an overview of this SP Manual.

2. Effective

Immediately.

3. Applies to

Users of SPs (teachers, administrators, personnel in the Office of Fiscal Services, and

other DOE employees).

4. Mission

Personnel in the Office of Fiscal Services will provide “customer service”-oriented

financial expertise and timely, accurate information to internal and external customers in

order to ensure transparency, sound fiscal management, and accountability at all levels

of the DOE—from the schools to the state office.

5. Vision

The Office of Fiscal Services personnel will be exemplary stewards of all our resources

to earn and maintain the public trust for effective use of state and federal taxpayer funds

and donor resources to improve student achievement.

6. “Our Pledge”

We will process financial transactions with accuracy, integrity, and sense of urgency

to meet our customers’ needs.

We will report timely, accurate results to our stakeholders.

We will conduct our business ethically and be responsible for our actions and

behavior, with respect for each other and all stakeholders.

We will be technologically proficient and seek ways to continually improve our

processes and methods of conducting business to create a productive and efficient

work environment.

We will partner with our internal and external customers to add value through

financial analyses and pro-active solutions rather than just being the “accounting

police.”

We will strive to make the DOE the preferred-employer department within state

government by providing opportunities for career development, a challenging work

environment, and a safe workplace that result in employee satisfaction and well

being.

7. Organization

A. The Office of Fiscal Services is led by an Assistant Superintendent, who also

serves as the DOE’s Chief Financial Officer (CFO). The Office includes the

Administrative Services Branch (including accounting, vendor payment, payroll,

inventory, and school support services), the Budget Branch (including budget

preparation and budget execution), the Procurement & Contracts Branch, and

the Internal Audit Section. See Reference (i), Organization of Office of Fiscal

Services

2

B. Budget Branch: The Budget Branch prepares and executes the DOE’s

operating budget. It consists of two sections:

1) Budget Preparation Section – Administers the preparation,

development and documentation of the DOE’s biennial and supplemental

operating budgets.

2) Budget Execution Section – Administers the implementation of the

DOE’s operating budget, monitors adherence to policies and procedures,

and makes adjustments to meet anticipated needs or restrictions.

C. Procurement and Contracts Branch: The Procurement and Contracts Branch

provides procurement and contract guidance and assistance to personnel in all

levels of the DOE regarding the procurement of goods and supplies, professional

services, construction-related services, and health and human services. The

Branch drafts contract agreements, reviews non-standard internal/external

agreements, and coordinates the approval of these agreements with the attorney

general’s office. This Branch consists of two sections:

1) Procurement Section – Provides departmental procurement direction,

oversight and expertise in compliance with the procurement code.

2) School-Based Behavioral Health Services Section – Performs

management support and fiscal support services to the Complex Areas in

the delivery of school-based behavioral health services to children eligible

for such services through IDEIA and Section 504.

D. Administrative Services Branch: The Administrative Services Branch provides

accounting, payroll, vendor payment, fixed-assets inventory, and business-

related operational support in the public school system. The Administrative

Branch consists of three sections:

1) Accounting Section – Administers and accounts for all funds,

expenditures, and financial commitments incurred by the DOE through a

centralized accounting system, in conformance with the state

comptroller’s rules and regulations;

2) Operations Section – Administers and performs the DOE’s payroll, vendor

payment, and inventory functions; and

3) School Support Section – Supports and assists the schools, complex

areas, and state offices in business-related matters.

E. Internal Audit Section: The Internal Audit section conducts examinations and

evaluations of the DOE’s fiscal activities and coordinates all external and internal

audits. The internal auditor provides information as to the adequacy and

effectiveness of the DOE’s system of internal controls. In addition, the Internal

Auditor serves as the Superintendent’s liaison with external CPA firm auditors

and audit sections of other governmental agencies (federal and state).

8. SP Maintenance Responsibility

The Assistant Superintendent/Chief Financial Officer in the Office of Fiscal Services is

responsible for maintenance, administration, and questions regarding this SP.

The Frequently Asked Questions (FAQ) page for this SP may provide standard

responses to common questions. Please review this resource before inquiring via

telephone.

3

9. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

(a) Frequently Asked Questions (FAQ) for SP 1000

(b) OFS Organization Chart

(c) OFS Functional Statement

SP 1101: Position Control Procedures

Non-WSF Programs

1. Purpose

To ensure that the number of positions established does not exceed the number of

authorized positions for each Program ID.

2. Effective

Immediately.

3. Applies to

Assistant Superintendents, Directors in the Superintendent’s Office, Complex Area

Superintendents.

4. Authorized Positions

A. Authorization of positions funded by non-WSF Program IDs is the legislative

appropriations act.

B. Adjustments to positions (such as adding a temporary position by moving

Character “A1” or “B” funds to Character “A”) can be made if approved in writing

by the Superintendent or designee per HRS, Section 302A-1116. Such

authorization is only valid until June 30

th

of the fiscal year in which the approval

was obtained.

C. If a temporary position, created with the approval of the Superintendent or

designee, is to be extended to the following fiscal year, the approval must be

obtained in writing before the new fiscal year.

5. Position Control for Certificated Positions Funded by Non-WSF Programs

A. For position control issues related to certificated positions, please contact OHR.

6. Position Control for Classified/SSP Positions Funded by Non-WSF Programs

A. The Legislative Appropriations Act sets the ceiling for permanent and temporary

full time equivalent (FTE) positions for each Program ID. The allocation of

positions for the upcoming fiscal year is reflected in each Program ID’s initial

allocation document which is issued around summer by the Budget Execution

Section.

B. Programs may request to establish new positions up to the allocation ceiling by

submitting DOE-v1a forms to the Budget Preparation Section.

C. A program must obtain the Superintendent’s or designee’s approval in writing to

establish a temporary position(s) that is in excess of the allocation ceiling. After

the approval is obtained, the program may submit a DOE-v1a form to the Budget

Preparation Section to establish a new position, attaching a copy of the approval

document(s) to the DOE-v1a. If a transfer of funds between Characters (i.e.

4

moving funds from Character B to Character A) is required to fund the new

temporary position the school or office must initiate a request to transfer funds to

be approved by the Superintendent or designee. After approval is granted, the

Budget Execution section will generate a subsequent allocation notice

documenting the transfer of funds.

D. A program may establish a position with a different occupational group code than

what that position was allocated as. However, approval of the Superintendent

may be required if this change will also mean a change in bargaining unit for the

position (i.e. establishing a clerk typist with an FTE that was allocated as a bus

driver), or if a certificated position will be established when a classified/SSP FTE

is allocated. Please consult with OHR if these types of changes will be

requested. If these changes result in changes to the offices’ organizational

charts, the charts must be updated by coordinating with OHR.

E. A DOE-v1 must be submitted to the Budget Preparation Section to make

changes to the Uniform Accounting Code (UAC) for established classified and/or

SSP positions.

F. A DOE-v1 must be submitted to the Budget Preparation Section to abolish an

established classified/SSP position.

7. SP Maintenance Responsibility

The Budget Director in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

The Frequently Asked Questions (FAQ) reference page for this SP may provide

standard responses to common questions. Please review this resource before inquiring

via telephone.

8. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

(a) HRS, Section 302A-1116, Authority for the DOE to create temporary positions

(b) HRS, Section 37-0074, Authority for the Superintendent to approve transfer of

funds among cost categories (Characters of Expenditure)

SP 1102: FMS Reports; School/Offices

1. Purpose

To describe the purpose of the various FMS reports that are designed to help schools

and offices monitor their accounts.

2. Effective

Immediately.

3. Applies to

All Schools and Offices.

4. Background

Various FMS reports are available to assist schools and offices either in WINFMS, on

the FMS website, or hardcopy. These reports are designed in different formats to

provide users with detailed information based on their needs. WINFMS reports reflect

5

real time balances that are updated as soon as financial adjustments are posted in FMS.

These reports can be printed on demand. FMS website reports are monthly and/or

cumulative that provide financial information through the end of a particular month.

These reports can be found at the FMS website under “DOE School/Office Reports” or

“DOE Grant Managers Reports” and can be searched, viewed on-line, printed, or worked

with in Excel/Word documents. Only payroll reports are provided to schools and offices

in hard copy. This is because they contain confidential personal information.

5. Allotment Reports

Allotment reports are designed to help users monitor their encumbrances, expenditures,

and allotment balances. These reports provide a detailed listing of transactions that

affect the schools or offices available allotment balances. Federal, general, and special

funds have allotment balances that can be found in these reports.

DAFM482 – Allotment Status for all Prog IDs (WINFMS)

This report lists the user’s Program IDs with allotments. Payroll (character 10 and

11) and other (character 20) allotments, expenditures, encumbrances, and available

allotment balances are provided for each Program ID. This report helps users to

monitor their Program IDs and can be used to identify deficits.

DAFM437 – Allotment Status for Specific Prog ID (WINFMS)

This report lists all of the user’s Organization IDs which includes sub-Organization

IDs for a specific Program ID. Payroll (character 10 and 11) and other (character 20)

allotments, expenditures, encumbrances, and available allotment balances are

provided for each Organization ID. This report is categorized by character (10, 11, or

20) and by BFY.

DAFM438 – Allotment Status for Specific Org ID (WINFMS)

This report lists all of the user’s Program IDs for a specific Organization ID which

includes Sub-Organization IDs. Payroll (character 10 and 11) and other (character

20) allotments, expenditures, encumbrances, and available allotment balances are

provided for each Organization ID. This report is categorized by character (10, 11, or

20) and by BFY.

The DAFX4480-A – Allotment Control Status for School Level by Prog ID and

Org ID (DOE School/Office Reports website)

This report provides the same information as the WINFMS DAFM482; however, it is

a monthly versus real time report. This report provides monthly payroll (character 10

and 11) and other (character 20) allotments, expenditures, encumbrances, and

available allotment balances are provided for each Program ID. This report also

helps users to monitor their Program IDs and can be used to identify deficits.

The DAFR4470 – School/Unit Allotment Register (DOE School/Office Reports

website)

This report provides detailed information only for other (character 20) expenditures.

This report combines the allotments, encumbrances, payments, and direct payments

onto one report to show the calculation of the available allotment balance for an

Organization ID/Program ID account. The Approval to Pay (ATP) report number and

the check number for a specific purchase order payment can also be found on this

report. This report is divided into current year and prior year. The current year

6

report shows encumbrances, payments, and direct payments that were created

during the current fiscal year. The prior year report shows encumbrances,

payments, and direct payments that were created during the current fiscal year for

carryover Program IDs. This report also shows payments for purchase orders or

contracts that were encumbered and still outstanding as of the end of the prior fiscal

year.

6. Cash Reports

Cash reports are designed to help users monitor their encumbrances, expenditures, and

cash balances. These reports provide a detailed listing of transactions that affect the

schools or offices available cash balances. Special and trust funds have cash balances

that can be found in these reports.

The DAFM484 – Cash Status for all Prog IDs (WINFMS)

This report provides summary information for the user’s Program IDs with cash

balances. Payroll (character 10 and 11) and other (character 20) allotments,

expenditures, encumbrances, and available cash balances are provided for each

Program ID. This report helps users to monitor their Program IDs and can be used

to identify deficits.

The DAFMR451 – School/Unit Cash Control Register (DOE School/Office

Reports website)

This report provides detailed information on a monthly basis as compared to the

WINFMS DAFM484 which is a real time report. Payroll (character 10 and 11) and

other (character 20) allotments, expenditures, encumbrances, and available cash

balances are provided for each Program ID. This report also helps users to monitor

their Program IDs and can be used to identify deficits.

7. Expenditure Reports

Expenditure reports are designed to help users monitor their expenditures by Object

code. These reports provide a detailed listing of expenditures and encumbrances that

affect the available allotment balances for schools or offices. Federal, general, special,

and trust funds have allotment balances for Characters 11 and 20 that can be found in

these reports. These reports show expenditures for salaries. For general funds, the

salary allotments are in the central salary account, so school reports do not include

allotments for character 10. Therefore, although the reports appear to show a deficit for

Object codes in character 10, the Allotment Status reports should be used to monitor for

deficits. The receipts for special and trust funds are not shown on these reports,

therefore the Cash Control reports should be used to monitor for deficits in special and

trust funds.

The DAFR 385A – Expenditure Status by Program – School View by Program

ID (DOE School/Office Reports website)

This report provides the schools or offices with encumbrances, expenditures, and

allotment balances by object code for each Program ID. The schools or offices can

refer to this report when planning for the expenditures for the following fiscal year. .

The DAFR 385B – Expenditure Status for Program Managers (DOE Grant

Managers Reports website)

7

This report helps program managers monitor their program(s). This report provides

financial information for all of the schools that received funding for a particular

program. It also helps to ensure that the funds are being expended appropriately

and supports the various objectives of the program. The financial information on this

report is sorted by grant #, BFY, fund, appropriation, and Program ID which is then

sorted by school(s) within each district. The expenditures for each school are

categorized by payroll (character 10 and 11) and other (character 20) object codes.

8. Payroll Reports

Payroll reports are designed to help users monitor expenditures that are not posted to

central salary. These reports provide payroll expenditure information for federal,

general, special, and trust funds on a monthly or cumulative basis.

DAFMZ032 – Payroll Detail Transaction Report (Hardcopy)

This report is a monthly, non-cumulative report that provides payroll detail for

programs not charged to central salary. Character 10 (salaried payroll) and/or

character 11 (hourly payroll) expenditures are listed with payroll date, last four digits

of the social security number, payroll number, and Batch ID. Expenditures are

categorized by Program ID first and then object code. This report is only available to

schools and offices in hard copy because of the sensitive nature of its contents.

Besides payroll expenditures, this report also shows payroll adjustments that have

been processed through an FMS-AC4.

DAFR 385B – Expenditure Status for Program Managers (DOE School/Office

Reports website)

This can be used to provide this information, but it will be categorized by character

10 and 11 object codes. Also, this report does not provide the sensitive type of

information that can be found on the DAFMZ032. This report is available on a

monthly basis and can be found at the FMS website under “DOE Grant Managers

Report.”

9. Adjustments

The reports that include journal voucher (JV) and other adjustments are designed to help

users view the adjustments that have been made to their accounts. These reports

provide adjustment information for federal, general, special, and trust funds on a monthly

or cumulative basis.

Most Current AC4 Report (DOE School/Office Reports website)

This report lists all FMS-AC4 adjustments that have been processed by the

Accounting Section, Information System Services Branch, or mass JVs (i.e.

automated General Fund Carryover Program). This report is organized by district

office, Organization ID, BFY, fund, appropriation, and Program ID.

DAFMZ011 – JV/Adjustment List (DOE School/Office Reports website)

This report provides a detailed listing of the JVs entered by the Accounting Section

and other adjustments (cash, allotment, etc.) entered by the schools and offices

during the fiscal year.

8

10. FMS Web Report Tools

The FMS website reports usually consist of an index frame on the left and a report data

frame on the right. To search the index frame you must click within the index frame

first. In Internet Explorer press Ctrl-F or select Edit from the menu and then Find. Type

in the text you are looking for and then click on the "Find Next" button. The text in the

index frame will be highlighted if it is found. Click on the found text to be taken to your

section of the report.

Below are brief explanations for the web report tools icons:

- "Work With" Button. This button opens the FMS website report in a separate

window. Inside this window, highlight the section you want to print then select File,

Print. In the Print window click on Selection under the Print Range section then click on

OK.

- “Print” Button. This button allows the schools and offices to print within the report

data frame which will be printed in landscape mode. The right side of the report will not

be cut off and the report headings will be at the top of each page. Each school/office is

contained within a single frame wherever. In some instances, it may be a very large

report, but the print program will let you know how many pages will be printed before

printing.

- “Search” Button. If this is the first time you have tried out the search feature you

will be warned by your browser that a plug-in or ActiveX control has been

requested. You will be taken through a set of dialog boxes asking if it is OK to install the

software from Forest Computer. Then you will be able to type your search criteria in the

"Look for:" box and then click the "Find Now" button.

Additional functions that are available in the "Search Results" window are listed below.

- Flags to select one or more pages for the "Print" or "Work With" operation. If you

click on the "Print" button all of the selected pages will be printed. If you select "Work

With" all of the selected pages will be brought into an edit window. You can then edit

and/or print part or all of the report.

- "Print" and "Work With" buttons operate on selected pages (select them by

clicking on the flag to the left of the page). These buttons will be active as soon as you

click on the flag for one or more pages.

- Dynamically change font size of search results in "List View" or "Browse".

- Select or Deselect all pages

- Page through results or go to first or last page.

- Go forward or backward to each search occurrence within the current page.

9

11. SP Maintenance Responsibility

The Accounting Section in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

The Frequently Asked Questions (FAQ) for this SP may provide standard responses to

common questions. Please review the FAQ section below before inquiring via

telephone.

Frequently Asked Questions (FAQ)

(1) Q: Is there a guide available that provides an overview on how to use the

various FMS reports? If so, where is it located?

A: There is a guide that provides an overview of the FMS reports which is

located on the FMS website (http://fms.k12.hi.us/fmsreportsguide/). This

guide will provide general information for all schools and state offices on

how to use the various FMS reports.

(2) Q: How do I print out an FMS report from WINFMS?

A: There is a guide on the FMS website that provides a walk through on how

to print out FMS reports from WINFMS (http://ists.k12.hi.us/fms2/).

(3) Q: What do I do if there is a payroll deficit in one of the Program IDs?

A: If this is a payroll deficit, you will need to look at the DAFMZ032 (Payroll

Detail Transaction Report) to determine if payroll is being erroneously

charged to this Program ID. Please refer to Section #8 for further

information on how to use this report. Once the error is identified, an

FMS-AC4 with appropriate supporting documentation will need to be

submitted to the Accounting Section to correct the error. Please refer to

the SP on Error Corrections for further information.

(4) Q: When I printed out the DAFM484 (Cash Status) from WINFMS, there is

an expenditure credit for one of the Program IDs. How did this occur and

do I need to correct this?

A: You will need to look at the DAFMR451 (School/Unit Cash Control

Register) for detailed information regarding this Program ID. Please refer

to Section #6 for further information. If the expenditure credit is caused

by an erroneously deposited cash receipt, an FMS-AC4 with appropriate

supporting documentation will need to be submitted to the Accounting

Section. Please refer to the SP on Error Corrections for further

information.

(5) Q: When I printed out the DAFM482 (Allotment Status for all Prog IDs) from

WINFMS, I thought I paid all of the encumbrances for one of the Program

IDs?

A: If there is an encumbrance balance even though you thought that all of it

was paid for, you will need to look at the DAFR4470 (School/Unit

Allotment Register). Please refer to Section #5 for further information.

Once the encumbrances are identified, they will need to either be paid or

liquidated.

(6) Q: How do I print out an FMS report under “DOE School/Office Reports” at

the FMS website?

10

A: You will need to click on the printer icon on the upper left corner of the

FMS report. Then you will be able to print the selected page(s) of the

FMS report that you need to use. Please refer to Section #10 for further

information.

(7) Q: How can I find out if the schools are expending the funds that they have

received?

A: The Grant Manager’s Report (DAFR 385B – Expenditure Status for

Program Managers) provides financial information for all schools

that received funding for a particular program. Please refer to Section #8

for further information.

(8) Q: The DAFMZ032 (Payroll Detail Transaction Report) provides payroll

details on a monthly, non-cumulative basis. Is there a report that

provides cumulative payroll information?

A: The Grant Manager’s Report (DAFR 385B – Expenditure Status for

Program Managers) can provide cumulative payroll expenditures based

on character 10 and 11 object codes. However, this report will not

provide you with specific information that the DAFMZ032 will provide like

the last four digits of the Social Security Number. Please refer to Section

#7 and 8 for further information.

12. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

FMS Reports

a) The FMS reports that are available for schools and offices to use are located on

the FMS website. Please refer to the following link (http://fms-

reports.k12.hi.us/school-reports.htm).

Grant Managers Report

b) The Grant Managers report is located at (http://fms-reports.k12.hi.us/grant-

reports.htm).

FMS Reports Guide

c) The FMS reports guide is located at http://fms.k12.hi.us/fmsreportsguide/.

WINFMS Report Guide

d) The WINFMS reports guide is located at (http://ists.k12.hi.us/fms2/).

SP 1103: FMS Reports; Monitoring by Program

Managers

1. Purpose

To provide helpful tools in monitoring grant awards. This SP is written specifically for

grant awards received from the Federal Government.

2. Effective

Immediately.

11

3. Applies to

Department of Education (DOE) State, Complex Area, and District Program Managers

and Accountants.

4. Background

The Program Manager is responsible in monitoring the overall financial as well as

programmatic requirements of a grant. The funds must be expended in accordance with

approved grant application and budget. Compliance with applicable statutes, provisions,

regulations and guidelines should be strictly enforced. The Financial Management

System (FMS) User Policy and Process Flow Guide is another tool to help program

managers monitor the expenditure of funds.

5. The Grant Award

The grant application and budget, supporting documents and write up submitted in

support of the approved grant application determines how to use the funds.

The grant award notification provides certain requirements including the budget and

performance period when the funds will be used, the authorized amount of the grant,

matching requirements, terms and conditions, and other provisions specified by the

grantor (See Grant Award Notification and explanation of Blocks for more information).

6. Program ID/Grant No/FY

When a new grant is received, a program identification (Program ID) and grant number

with the fiscal year are assigned by Accounting Section (Refer to SP 1101 – FMS

Codes). The Program ID will be used by recipients of the grant to credit allotment and

charge expenditures. The grant number and fiscal year maintains records of all

expenditures, contract encumbrances, claims encumbrances and revenue.

The Program Manager prepares an expenditure plan to distribute the funds to

school/units. This plan is submitted to Budget Office for allocation (Refer to SP 1604 -

Budget Execution Process for more information on this subject). Once the schools/units

receive their allocation, they prepare and enter their own expenditure plans in the budget

system. An interface is done between Budget System and the Financial Management

System (FMS) creating an allocation in the latter.

7. Expenditure Monitoring

Monitoring of expenditures is just as important as obtaining the grant award. The

Program Manager should always be in control of where and when the funds are

expended. Proper monitoring prevents lapsing of funds and ensures appropriate and

timely expenditures of funds that support project objectives.

8. Tools in Monitoring

There are various tools in monitoring expenditures whether hard copy reports, live view

of FMS data or downloads from the internet. Some reports can be viewed or printed on

line by central accountants, user support technicians, complex area program mangers,

and district program managers, to get the most current status of the account.

The following FMS reports are available every month and can be downloaded from the

following FMS website address (Refer to “How to View FMS Reports on the Web

http://fms.k12.hi.us/fmsreports/).

12

http://fms-reports.k12.hi.us/school-reports.htm

a. DAFR385A Expenditure Status By Program – School View by Program

ID – Current and Claims.

b. DAFR4470 School Unit Allotment Register

c. DAFMR451 School Unit Cash Control Register

d. DAFMZ011 Journal Voucher (JV) Adjustment List

e. DAFMC015 Posted Purchase Order Log

http://fms-reports.k12.hi.us/accounting-reports.htm

a. DAFR3811 Expenditure Status by Program ID – District Office View

b. DAFR3831 Expenditure Status by Program ID – Department Wide

View

c. DAFR385B Expenditure Status for Program Managers – Current and

Claims.

d. DAFR385C Expenditure Status for District Program Managers

Helpful hints on how to use the reports are available through this website:

http://fms-reports.k12.hi.us/fmsreportsguide/

9. Perusing the Reports

Negative amounts whether expenditure, encumbrances or account balance should

always raise a red flag when browsing an FMS report. The expenditure or encumbrance

becomes negative when an incorrect credit adjustment is made; a negative account

balance is the result of over-expending the allotment, incorrect charge, or the fund may

still be sitting in the Budget System.

Unusually big account balances should also be a concern for Program Managers

especially when the grant is nearing the lapse date.

10. Identifying the Problems

The Program Manager identifies the school/unit with deficits by going through the DAFR

385B report. This report provides the grant/fiscal year and Program ID by school/office

and the status of the account. The grant/fiscal year determines when the will grant

lapse, therefore, it is necessary to check where the funds come from. The lapse date

can also be verified per the allocation notice.

The Program Manager should be able to view print the most current allotment status of a

Program ID in FMS. This will facilitate immediate resolution of deficits. The problem

should be relayed to the school/office if it cannot be resolved by the Program Manager.

The school/office will examine the account in deficit and initiate corrective actions. Refer

to SP 1102 – FMS Reports; School/Offices and/or SP 1105 – School/Office/Program

FMS Error Corrections)

Unresolved deficits may result in locking out other school/office from paying bills or

encumbering purchase orders because the grant ceiling may have been overspent.

13

11. SP Maintenance Responsibility

The Accounting Section in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

The Frequently Asked Questions (FAQ) page for this SP may provide standard

responses to common questions. Please review this resource before inquiring via

telephone. See Reference (a) below.

12. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

(a) Frequently Asked Questions (FAQ) for SP 1103.

Q: Who is responsible in correcting an erroneous charge to a school/office?

A: The school/office where the incorrect charge was made should initiate the

correction by completing and submitting the Form AC4 “Request For Change of

Accounting Codes and/or Amounts”

(b) US Education Department General Administrative Regulations (EDGAR)

http://www2.ed.gov/policy/fund/reg/edgarReg/edgar.pdf

(c) FMS User Policy and Process Flow Guide

(d) SP 1101 – FMS Codes

(e) SP 1604 – Budget Execution Process

(f) SP 1102 – FMS Reports; School/Offices

(g) SP 1105 – School/Office/Program FMS Expenditure Error Corrections

Forms

(h) Form AC-4, Request For Change of Accounting and/or Amounts

http://fms.k12.hi.us/forms/fms-ac4/fms-ac4.pdf

SP 1104: FMS Processing Schedule

1. Purpose

To outline the Financial Management System (FMS) and Budget plans and processing

requirements for the end of the current fiscal year and the start of the new school fiscal

year.

2. Effective

Immediately.

3. Applies to

All State, complex area, district offices and schools.

4. Background

The FMS/Budget processing schedule identifies key dates as we close the current fiscal

year and start the new fiscal year.

5. Processing Schedule

The FMS processing schedule can be found on the FMS website (http://fms.k12.hi.us/)

under the FMS Year-End Close Information section.

The FMS/Budget processing schedule establishes the following key deadlines:

14

Planned budget carryovers to become available.

First and last days to post purchase orders, pay purchase orders and make direct

payments using current and carryover funds.

Form FMS AC-4 deadlines for the first and second half of the year.

Form BUD-3 deadlines for Budget System.

Planned carryover transfer program.

When FMS will temporarily close for year-end processing.

Identifies the new purchase order prefixes for the new fiscal year.

Also refer to the following:

SP 1105 – Error Corrections for details and instructions on AC4.

Budget Branch Standard Practices at SP 1600s.

6. SP Maintenance Responsibility

The Accounting Section in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

7. References, Resources, and Forms

FMS processing schedule: http://fms.k12.hi.us

SP 1105: FMS Corrections to Accounting Codes

and/or Amounts

1. Purpose

To provide instructions for requesting corrections or changes related to revenue and

expenditure transactions posted in Financial Management System (FMS).

2. Effective

Immediately.

3. Applies to

All DOE offices and schools.

4. Background

Schools/offices may make corrections/changes to revenue and expenditure transactions

posted in FMS. For example, changes may be made to the following transaction detail:

Organization ID, Program ID, Object Code, Budget Fiscal Year (BFY), Source Code,

and/or Amount. To request this change, schools/offices should complete a Form FMS-

AC4, Request for Change of Accounting Codes and/or Amounts. The FMS-AC4 should

be sent to DOE Accounting Section with appropriate supporting documentation. DOE

Accounting will process the FMS-AC4 by posting a correcting journal voucher (JV) to

FMS.

5. Completing FMS-AC4

The FMS-AC4 and related instructions to complete the Form is provided below at

Section 11 - References, Resources and Forms.

15

A few important notes regarding the FMS-AC4:

Form FMS-AC4s should not be used to clear deficits unless they were caused by

legitimate errors. Examples of legitimate errors include using an erroneous Program

ID to purchase supplies or equipment, or an erroneous Organization ID or Program

ID to incur substitute teacher charges.

Error corrections must be processed timely. Refer to Section 9 below for deadlines.

There is no dollar threshold amount for processing a Form FMS-AC4

Q: Can error corrections be processed for errors that were made in a prior

fiscal year?

A: No. Error corrections need to be corrected in the fiscal year in which the

errors occur. Refer to the Deadlines section below.

Q: Is there a dollar threshold amount for processing FMS-AC4s?

A: No. There is no dollar threshold amount for processing a Form FMS-AC4.

6. Acceptable Supporting Documentation

The type of supporting documentation that should be submitted with the FMS-AC4

depends on the type of correction/change that is being requested, such as follows:

Payroll Expenditures (Character 10):

Payroll Detail Transaction Report (DAFMZ032), or

Principal Report

AND

Form 5, Personal Action Form .

Payroll Expenditures (Character 11):

Payroll Detail Transaction Report (DAFMZ032), or

Principal Report

Non-Payroll Expenditures (Character 20):

Approval To Pay Report (ATP), or

DAFR447, School/Unit Allotment Register, or

ERFPC100-C, P-Card Transactions Posted Report

Revenue Receipts:

Collection Activity Report (CAR), or

Treasury Deposit Receipt (TDR), or

DAFMR451, School/Unit Cash Control Register

Cash Transfer:

DAFMR451, School/Unit Cash Control Register

Formal memo/letter initiating or authorizing the cash transfer and/or calculation of

cash transfer amounts (if applicable)

7. Submission Process

One copy of the FMS-AC4 should be submitted to DOE Accounting Section via intra-

departmental mail. A second copy should be maintained by the school/office as a

suspense copy until the “validated” FMS-AC4 is returned.

16

For rush requests, the FMS-AC4 may be faxed to DOE Accounting Section @ (808)

586-3374. Rush request should be only be used in extreme cases such as to prevent

the lapsing of funds.

**Please do not submit the FMS-AC4 more than once. Submitting duplicate forms

may result in double-postings.

8. Completion Process

After DOE Accounting processes the FMS-AC4, the Accountant will write the DOE

Journal Voucher (JV) number on the bottom of the FMS-AC4, and send a copy of the

processed or “validated” FMS-AC4 back to the school/office.

Schools/offices should review the processed or “validated” FMS-AC4 against what was

posted on FMS to verify the correction/change was posted properly. Schools/offices can

see the FMS-AC4s transactions posted in FMS in the current fiscal year at the “Most

Current AC4 Report” link at the FMS website: http://fms-reports.k12.hi.us/school-

reports.htm.

Schools/offices should keep on file a copy of the processed FMS-AC4 for their records.

9. Deadlines

There are two deadlines during each fiscal year to submit Form FMS-AC4s—the mid-

year close for July – Dec transactions and year-end close for January – June

transactions. For further information regarding the deadlines, please refer to SP 1104 -

FMS Processing Schedule.

**Please be mindful of the deadline schedules. FMS-AC4 corrections/changes

cannot be posted for the period after the deadlines have passed.

10. SP Maintenance Responsibility

The Accounting Section in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

11. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

(a) Form FMS-AC4, Request for Change of Accounting Codes and/or Amount

(b) Instructions for Form FMS-AC4

SP 1106: Revenue/Cash Receipt Collections

1. Purpose

To describe the Department’s revenue/cash receipts processes.

2. Effective

Immediately.

3. Applies to

All State, District and school level personnel responsible for revenue/cash collections.

17

4. Background Information

Revenue/cash receipt collections include any monies collected by a school or office.

Monies collected fall into two major groups.

Non-Appropriated Funds (also known as Local School Funds or “LSF”)

Monies collected from and for students which do not require deposit into the State

Treasury pursuant to HRS section 302A-1130. Examples include: class dues,

student association dues, yearbook, newspaper, school club dues, money-raising

funds, and excursions.

Appropriated Funds

Monies collected for the following:

Central Checking (used for collections of items not falling within the other

appropriated funds categories, such as: use of facilities fees, summer school,

adult education, athletic events, lost textbooks/equipment, returned check fees,

donations)

School Lunch

Student Transportation

A-Plus Program

*This SP 1106 covers appropriated fund collections only. Please refer to SP

1120 for more information on LSF Funds.

5. Billings

Schools and offices are responsible for billing and collecting amounts due from

individuals and organizations which are due to the DOE or State.

DOE Billing Collection Forms

Form 440A, Bill for Lost Textbooks Used for charges/fees related to lost textbooks.

Form 440B, Outstanding School Obligation Used for various charges/fees.

A404, Form 99, Bill for Collection Used to bill external organizations or individuals.

6. Deposits from Schools

Ordering Deposit Slips

Deposit slips for all appropriated fund checking accounts must be ordered through DOE

Accounting. The DOE uses special micro-encoded deposit slips to route deposits to the

appropriate checking account and org code (i.e. school).

IMPORTANT: DO NOT USE PHOTOCOPIES OF DEPOSIT SLIPS TO MAKE BANK

DEPOSITS. BANK SCANNERS ARE UNABLE TO READ THE MICRO-ENCODED

ACCOUNT NUMBERS FROM PHOTOCOPIES. USING PHOTOCOPIES WILL

CAUSE ERRORS AND DELAYS.

Each school is responsible for maintaining a sufficient supply of deposit slips. Re-orders

should be done timely. Orders take a minimum of 10 business days to be received from

18

the day the order is placed. Deposit slip order forms can be found on the FMS website.

Forms should be faxed to DOE Accounting at 586-3374.

Schools should verify all micro-encoded data on the bottom of the deposit slips when

received. The deposit slips should have the org code, bank routing number, and

checking account number. Do not use incorrect deposit slips or make manual

corrections, instead call DOE Accounting at 586-3371.

Checking Accounts

The checking account numbers for the four appropriated fund accounts are:

Central Checking Account #0001-075160

School Lunch Collection Account #0001-063367

Student Transportation Account #0002-374161

A-Plus Program Account #0003-414680

Preparing and Processing Deposit Slips

At least three (3) deposit slips should be prepared for each deposit. One (1) copy

should be retained by the school as a suspense copy until the deposit is validated. The

other two (2) copies should be sent to the bank for validation.

After the bank validates the deposit slips, the bank will retain one copy, and the

remaining copy should be retained by the school. Schools may prepare additional

deposit slips for validation or recordkeeping as necessary.

Deposit Transaction Limits

Schools are limited to ten (10) deposit transactions per day per checking account. Any

deposits above this limit will cause errors and delays.

Other

See Sections 9 – 11 for more information on deposits from Schools.

7. Deposits from Offices

A Treasury Deposit Receipt (“TDR”), SAFORM B-13 4P, should be used by DOE offices

to process revenue/cash collections.

Accessing the TDR

Offices can access the most recent version of the TDR on the State of Hawaii Forms

website: http://www.state.hi.us/forms/, via the “View Internal Forms in the Database” link.

The TDR must be completed on the computer and printed out on specific NCR paper

which can be obtained from DOE Accounting.

Preparing and Processing the TDR

Instructions on how to work with and print out the TDR can be found on the State of

Hawaii Forms website.

19

Instructions on how to complete the TDR are as follows:

FUND

Enter full name of fund type (i.e. “General”, “Special” or “Trust”)

FUND OR

APPROPRIATION

Enter descriptive title of appropriation (i.e. OCISS – Advanced Technology Research)

or school name

DETAIL DATE

Enter current date in following format “XX/XX/XXXX”

SFX

Enter consecutive line number beginning with “01”

TC

Enter transaction code “011” for revenue receipts (i.e. fees, donations, grants, etc.)

Enter transaction code “122” for expenditure reimbursements

F

Enter first letter of the Fund type (i.e. “G”, “S”, “T”)

YR

Enter last two digits of current fiscal year (i.e. “11” for 2011)

APP

Enter three digit appropriation code (refer to FMS website for listing). Appropriation

code should be applicable/related to the program code (PROJECT NUMBER).

D

Enter “E” for Education

SOURCE/OBJECT

Enter four digit source or object code (refer to FMS website for listing).

Revenue receipt transaction code (TC) of “011” should use a source codes.

Expenditure reimbursement transaction code (TC) of “122” should use an object code.

COST CENTER

Enter your three digit org code

PROJECT NUMBER

Enter your five digit program code

PH

Enter two digit District code

AMOUNT

Enter deposit amount

DEPARTMENT

Enter “EDUCATION”

REMARKS

Enter pertinent check information

DEPOSITORY NO.

Do not enter anything. TDR to be validated by Budget & Finance. Validated copy will

be sent to DOE Accounting who will route copy to you.

After completing the TDR, click on the yellow button at the top of the page labeled

“PRINT”, and four (4) copies of the TDR will print. One (1) copy should be retained by

the office as a suspense copy until the deposit is validated. The other three (3) copies

should be sent DOE Accounting with the monies collected.

DOE Accounting will process the deposit and return one (1) copy of the validated TDR to

the office. Please allow 1 week for processing.

Deposit Transaction Limits

Offices are limited to ten (10) deposit transactions per day. Any deposits above this limit

will cause errors and delays.

Wire Transfers

Offices should contact DOE Accounting for instructions on setting up wire transfers for

specific programs.

20

Other

See Sections 9 – 11 for more information on deposits from Offices.

8. Dishonored Checks

Procedures for dishonored checks being deposited in central checking account are as

follows:

DOE Accounting will send the school/office a Dishonored Check Notice with a

copy of the related check.

The school/office should contact the maker of the dishonored check, and request

cash, cashier’s check or money order to replace the dishonored check. The

school/office should also collect a non-refundable service charge of $25.00 for

each dishonored check, as required by State law. This service charge cannot be

waived under any circumstance.

Collections for the dishonored check may be included with the regular deposits.

No separate deposit slip is required.

A separate Collection Activity Report (CAR) will be generated for the debit memo

related to the dishonored check. Refer to Section 10 for further procedures for

CARs.

Schools/offices should consider requiring payments in cash or cashier check for

individuals or organizations with frequent incidents of dishonored checks.

9. Collection Activity Report (CAR)

CARs are generated for any central checking account transaction. No CARs are

generated for school lunch, student transportation, and A-Plus program checking

accounts, as all monies are routed to the respective program IDs automatically.

The CAR allows the schools/offices to designate where collections, refunds, etc. will be

debited and credited to. CARs are uploaded automatically onto the WINFMS website.

CARs should be viewed and released on a regular basis.

There are four (4) types of CARs, as follows:

Cash Receipts (batch number range: 200-209) One Collection Activity Report

(CAR) is generated for each central checking account deposit transaction. The

school/office should input the transaction code, source/object code, and program ID

for each deposit transaction.

Debit Memo (batch number range: 620-625) Debit memos.

Bad Check (batch number range: 640-645) The school/office should adjust the

original CAR by inputting into FMS the appropriate organization ID, program ID,

object/source, the dishonored check amount and the maker’s name.

Credit Memo (batch number range: 720-725).

School/office will adjust the original CAR by inputting into FMS the appropriate

organization ID, program ID, object/source, the dishonored check amount and

the maker’s name.

21

10. Error Corrections

Schools

If a deposit is made in the wrong checking account, schools should call DOE Accounting

to resolve the issue.

If a deposit is made in the central checking but coded incorrectly during the CAR

process, the school should request a correction using Form FMS-AC4, Request for

Change of Accounting Codes and/or Amounts. Refer to SP 1105 – Error Corrections for

more information.

Offices

Corrections to the coding of TDRs should be requested by the office using Form FMS-

AC4, Request for Change of Accounting Codes and/or Amounts. Refer to SP 1105 –

Error Corrections for more information.

11. Write-off of Uncollectible Accounts

Definition of Uncollectible Account

1. The debtor or party causing damage to property, belonging to the State, is no

longer within the jurisdiction of the State;

2. The debtor or party causing damage to property, belonging to the State, cannot

be located;

3. The party causing damage to property, belonging to the State, is unknown or

cannot be identified;

4. The debtor has filed bankruptcy and has listed the State a creditor; or

5. Such other account as may be deemed by the Attorney General to be

uneconomical or impractical to collect.

Write-off Request

The approval request to write off obligations that have been outstanding for two

consecutive years should identify one of the five definitions (see above box) as a

reason to write-off outstanding obligations as uncollectible.

Review of Write-off Request

Request should be reviewed by the Complex Area Superintendent and the Chief

Financial Officer, and then forwarded to the Attorney General for permission to write-off

the accounts.

Write-off Approval

Once permission from the Attorney General is received, school/office should maintain a

permanent record of the uncollectible accounts that have been written off. Uncollectible

obligations that are written off can be reinstated if the account has become collectible or

the facts presented to the Attorney General were misstated.

12. SP Maintenance Responsibility

The Accounting Section in the Office of Fiscal Services is responsible for maintenance,

administration, and questions regarding this SP.

13. References, Resources, and Forms

(a) Form 440, Outstanding School Obligation

(b) Form A404, Form 99, Bill for Collection

22

http://fms.k12.hi.us/forms/form-99/A404-form-99.pdf

(c) Form FMS-AC4, Request for Change of Accounting Codes and/or Amounts

http://fms.k12.hi.us/forms/fms-ac4/fms-ac4.pdf

(d) Form FMS-C1, Revenue Refund

http://fms.k12.hi.us/forms/fms-c1/fms-c1.pdf

SP 1120: Non-Appropriated Local School Fund;

Description of and Chart of Accounts and

General Purpose

1. Purpose

Provide an overview of the purpose of the Non-Appropriated Local School Fund.

2. Effective

Immediately.

3. Applies to

All schools.

4. Overview Non-Appropriated Local School Fund

The purpose of the Non-Appropriated Local School Fund is to collect and maintain

monies for such purposes as class dues, student association dues, yearbook,

newspaper, school club dues, money-raising funds, excursions, etc., which do not

require deposit into the State Treasury pursuant to Section HRS 302A-1130.

Each school has a Local School Checking Account established with a commercial bank

to maintain these funds. The Principal of the school serves as trustee for the account,

and is directly responsible for the conduct of student financial activities in accordance

with the rules, policies, and procedures set forth by the DOE. Additionally, the students

who have contributed monies for specific purposes should receive direct benefit from

these monies, unless participants have agreed to carry these monies into future years.

(One example is bequeathing a class gift to the school)

The Non-Appropriated Local School Fund uses a cash basis of accounting. In other

words, financial transactions are posted only when money is received or paid by the

school. Additionally the chart of accounts systematically categorizes the listing for all

amounts as follows:

Assets (Control Code)

010 Cash

(Checking account)

030 Investments

(Records investments from idle cash. Only secured investments

are allowed.)

Liabilities (Control Code)

100 School Wide

23

(Accounts in which all students receive benefits such as

newspaper, yearbook, etc.)

300 Revenue Raising

(Accounts of all revenues and expenses for all fundraisers)

400 Student Activity

(Accounts for subgroups within the school such as class or grade

level accounts and clubs)

500 Trust and Agency

(Accounts set up for specific purposes such as field trips,

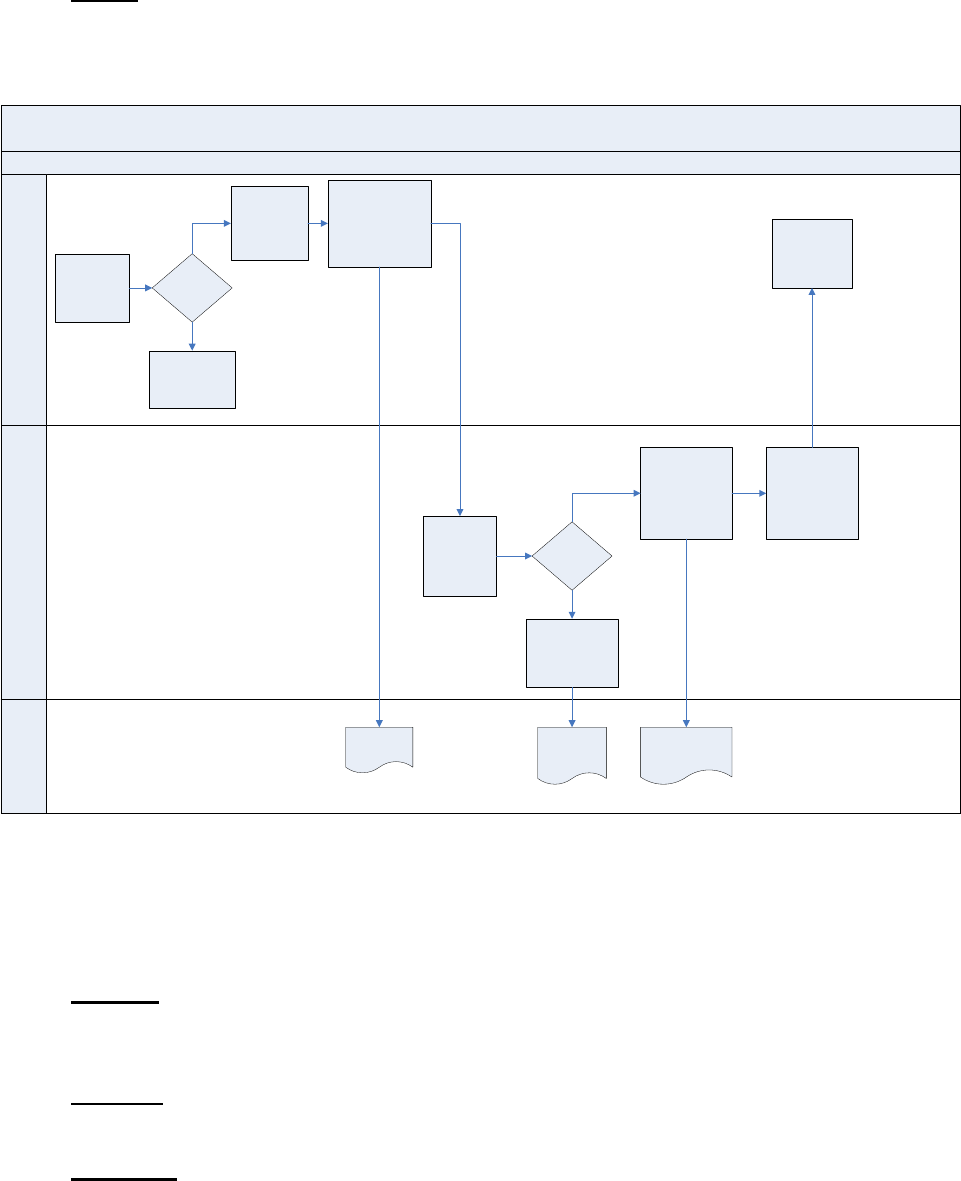

admissions, donations etc.)

5. Description of Asset Accounts

Asset accounts of a school are generally known in commercial accounting as “current

assets”, i.e. cash in bank checking account and investments.

Cash-in-Bank – Checking Account (010): This account records the deposits of

monies and disbursements of the schools non-appropriated local school fund. All

checks drawn are restricted to those properly executed and supported by valid

vouchers. The unexpended balance in the account is reconciled monthly to the

balance shown on the bank statement.

Investments (030): This account is to record investments in savings and

government securities. These investments are to be recorded individually to

provide accountability and control. Schools are authorized to use idle funds for

investment to earn additional income for use by the school for the general welfare

of the school. Refer to SP 1126 for detailed procedures.

6. Description of Liabilities/Fund Accounts

A fund is defined as “a sum of money or other resources set aside for the purpose of

carrying on specific activities or to attain certain objectives”. The financial operations of

the school are therefore, classified by funds. These funds are broken down into groups

of accounts to show in detail the operations of each fund.

School Wide Activities (100): This control account records the financial

transactions of the funds used for administrative and/or educational purposes.

These activities are school-wide in nature.

Following is the list of types of sub-accounts that the schools are authorized to

have:

1) General School

2) Year Book

3) Newspaper

4) Book/School Store

5) Cash overage/shortage

6) Library (not book fair fundraisers)

General School Sub-Account: The General School sub-account is

specifically established for uses directly related to school-wide operations.

The sources of revenue for this sub-account are limited to interest income

from investments, closure of inactive accounts of school sponsored

organizations, fundraising and donations specifically designated for the

24

benefit of the entire school, and other sources of revenue designated

specifically for the benefit of the entire school.

Allowable expenditures for general school sub accounts are:

1) Purchasing of materials, supplies, equipment and services that benefit

students and the school.

2) Providing staff and students opportunity to attend workshops.

Revenue Raising (300): This control account is to record the financial

transactions of all money-raising activities of the various organizations authorized

by the principal. The balances (deficits) from each of the money-raising activities

must be transferred to the appropriate organization’s sub-account at the end of

the money raising activity or by year-end, whichever occurs first.

Student Activities (400): This control account is to record the financial

transactions of the student government, class/grade level organizations and

school clubs. Refer to SP 1128 for procedures for school clubs.

The following are a few examples:

1) Student council

2) Grade 4 (not excursion-related)

3) Class of 2020

4) Key Club

5) Drama Club

Expenditure of Monies: Monies derived from dues and money-raising

activities should be expended in such a way to benefit those students

currently in school who have contributed to the accumulation of such money.

(Refer to Administrative Rule, Chapter 32)

Trust and Agency (500): The Trust Fund is used to account for cash or other

resources received and held by the school in the capacity as a trustee or as an

agent. This fund is subject to restrictions and is to be expended or disposed of at

the discretion of the donors or their authorized representatives.

For donations with a donor’s specific intent and purpose, a sub-account must be

established. However, when the designated trustee of the fund is the school’s

principal, revenue raising balances and donations designated for the benefit of

school-wide activities should be deposited into the General School sub-account

(100 series). Also, a copy of the letter or memorandum shall be retained in the

office file. The Agency Fund is used to account for monies held by the school

acting as an agent for individuals and private organizations.

7. SP Maintenance Responsibility

The Accounting Services Branch in the Office of Fiscal Services is responsible for

maintenance, administration, and questions regarding this SP.

8. References, Resources, and Forms

25

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

(a) Hawaii Revised Statutes Section 302A-1130

http://www.capitol.hawaii.gov/hrscurrent/Vol05_Ch0261-

0319/HRS0302A/HRS_0302A-1130.htm

(b) SP 1126 Non-appropriated Local School Fund; Investing Idle Cash

(c) SP 1128 Non-appropriated Local School Fund; School Clubs

(d) SP 1131 Non-appropriated Local School Fund; Fund Raising

SP 1121: Non-Appropriated Local School Fund;

Administrator’s Checklist/Internal Controls

1. Purpose

Provide internal compensating controls for administrators due to the non-segregation of

duties by office staff for the cash receipt and disbursement process.

2. Effective

Immediately.

3. Applies to

All schools.

4. Internal Compensating Controls

Schools are often challenged by insufficient staff to segregate duties for cash control

measures to prevent theft or misappropriation of funds. More specifically, the same

employee may receive cash, record the cash receipt, deposit the receipt, and issue the

check to pay vendors. To ensure accountability, the department has instituted internal

compensating controls to address this situation. The Principal or designee shall provide

for compensating controls at each school or office.

The internal compensating controls are documented on a form called the Non-

Appropriated Local School Fund Administrator’s Checklist. See Form (a) below.

The Checklist includes the following requirements.

A. Quarterly (at least once a quarter), conduct an unannounced cash count of the

Petty Cash Fund.

B. Monthly, conduct a reconciliation of the bank statement’s ending balance, against

the school’s check register ending balance. The Principal needs to initial and

date when this task was performed on the checklist, on the reconciliation form,

and sign and date the bank statement.

C. Monthly, the Principal should perform review of bank statement for unusual

checks or other transactions before giving it to the individual who performs the

bank reconciliation.

D. Monthly, review outstanding checks (defined as more than six months old).

These checks should be cancelled through a journal voucher.

E. Annually, check that cash receipts are reconciled and deposited by the next

business day or next scheduled armored carrier pickup day. Reconciliation of

26

field trip cash receipts however, can be done upon completion of collection.

Cash collected from students for field trips should be secured in the school safe.

F. Annually, check that all journal vouchers have been pre-approved by the

Principal prior to being posted. See Form (b) below.

G. Annually, check that proper documentation (original invoice or receipt) have been

attached to disbursements.

H. The Principal or designee will complete the Non-Appropriated Local School

Fund Administrator’s Checklist to indicate the areas reviewed, the date of the

reviews, discrepancies found and the report should be kept on file for audit

purposes.

It is recommended, at the discretion of the Complex Area Superintendent, that the

complex Administrative Services Assistant or Complex Area Business Manager assist in

this review.

5. SP Maintenance Responsibility

The Accounting Services Branch in the Office of Fiscal Services is responsible for

maintenance, administration, and questions regarding this SP.

6. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

Forms

(a) Non-Appropriated Local School Fund-Administrator’s Check List

(b) Non-Appropriated Local School Fund-Journal Voucher

SP 1122: Non-Appropriated Local School Fund;

Preparation for Financial Audit

1. Purpose

To provide suggestions to schools on how to prepare for a financial audit of the Non-

Appropriated Local School Fund.

2. Effective

Immediately.

3. Applies to

All schools.

4. Preparing for an Audit

The following is a checklist to prepare for a financial audit of the Non-Appropriated Local

School Fund:

A. Check that all expenditures have been pre-approved, signed, and dated by the

Principal through either a Purchase Order Form AC-3, or a Requisition Order.

Auditors will check the date of the invoice or receipt against the date on the

purchase order or requisition form, to determine if prior approval was obtained.

B. Ensure that the Principal’s Financial Report is signed by the Principal and dated.

27

C. Verify that all payments have the proper documentation (original invoices or

Form 99 along with receipts), for payment or reimbursement. Original invoices or

Form 99 should be stamped with Approval of Payment stamp and attached to

the corresponding purchase orders.

D. Ensure that the Monthly Bank Reconciliations and Bank Statements have been

completed, signed, and dated by the Principal and the preparer.

E. Verify that all items on the Administrator’s Checklist have been completed and

documented. This would include unannounced cash counts of the Petty Cash

Fund, checking for timely cash deposits, canceling stale-dated (over six months

old) checks, approval of all journal vouchers, and obtaining proper

documentation for disbursements (original invoices or Form 99 along with

receipts) as noted above. (See SP 1121 for description of Administrator’s

Checklist.)

F. Check that all school-sponsored fundraisers have been approved by the Principal

prior to and after the fundraising activity as noted on the Form 422, Money

Raising Activity. Verify that the form has been reconciled with the amounts

reported in respective Revenue Raising Control Accounts.

G. Verify that all donations have been logged on Form 434, Report of Gifts,

Grants and Bequests, in addition to compliance with the requirement that all

donations $500 or more are accepted by the Superintendent of Education.

Ensure that the Letter of Acknowledgment and supporting documentation are

attached to the Form 434.

H. Match the validated bank deposit slip to the Daily Summary of Collection, and

attach yellow carbon copy of Form WIZ 239 or other documentation, for detailed

information on the deposit.

I. Keep booster club, PTA, PTSA or other independent organization accounts out

of the local school fund. Since they are entities independent of the school, they

must maintain separate bank accounts.

J. Update authorized signatories to the bank, if administrator or office personnel

have changed.

K. Complete the Compliance of Local School Fund Procedures Annual Checklist.

L. Review chart of accounts. All fundraising (300 level) and excursion accounts

should be zero. All class accounts should be closed within 5 years.

M. Verify that fixed asset purchases are included in inventory.

N. School must be in compliance with all other policies and procedures noted in all

SPs and other resources.

5. SP Maintenance Responsibility

The Accounting Services Branch in the Office of Fiscal Services is responsible for

maintenance, administration, and questions regarding this SP.

28

6. References, Resources, and Forms

The following resources may provide access to statutory, policy, and contractual

authorities; and closely related SPs, procedures, and forms.

Forms

(a) Form AC-3, Purchase Order

(b) Form 99, Bill for Collection

(c) Requisition Form

(d) Non-Appropriated Local School Fund-Administrator’s Checklist

(e) Form 422, Money-Raising Activity Form

(f) Form 434, Report of Gifts, Grants and Bequests

(g) Form 239, WIZ Receipt

(h) Daily Summary of Collection

SP 1123: Non-Appropriated Local School Fund;

Collection and Deposit Procedures

1. Purpose

Provide an overview on collection and deposit procedures for the Non-Appropriated

Local School Fund.

2. Effective

Immediately.

3. Applies to

All schools.