Despite AWP

Inflation Near 10%

CVS Health Kept

Drug Price Growth

Nearly Flat at 0.2%

and Adherence Improved

Drug Trend

Report

2017

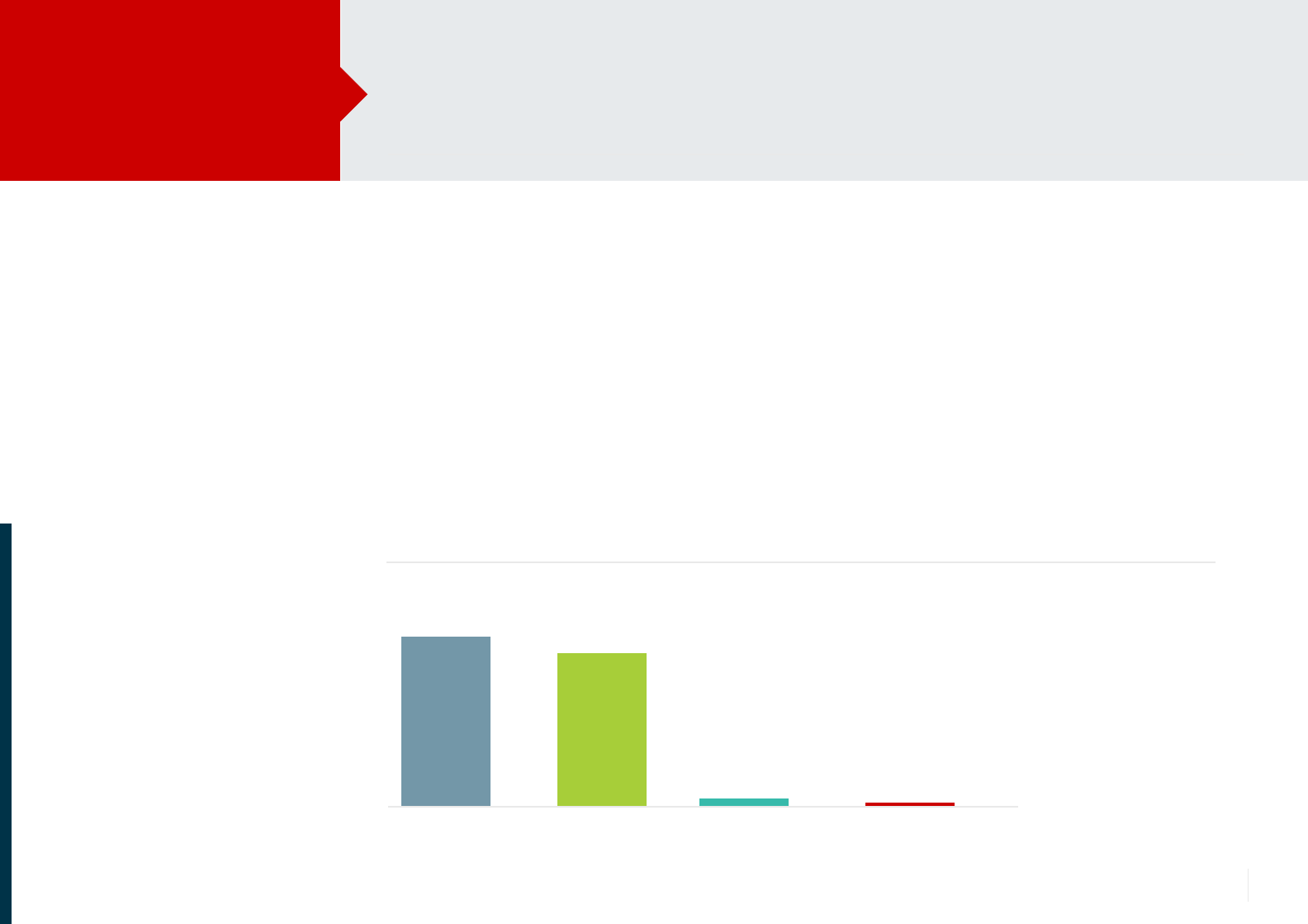

Hyperlipidemia 1.8

Hypertension 1.2

Diabetes 1.2

Out-of-pocket cost

PMPM declined

$11.99

$11.89

2016 2017

In 2018 we are doing even more

to help patients save money.

AWP (Average wholesale price). PMPM (Per member per month).

*Percentage point increase in the number of optimally adherent members.

Drug Trend

Report 2017

By the Numbers

2017 Trend: CVS Health 2

•

Increasing price transparency at all points of care

•

Giving members greater access to more affordable options

By keeping drugs

affordable, we also

helped more members

stay on therapy in

key categories*

We helped make

prescriptions

more affordable

for members

<$100 for their

prescriptions

3 of 4

members spent

In 2017, despite

AWP ination ~10%

our strategies kept

drug price growth

nearly flat at 0.2%

9.2%

Traditional

Brands

8.3%

Specialty

Brands

0.4% 0.2%

Generics CVS Health

Drug Price Growth

The health care landscape continues to evolve, but the cost of drugs remains a top concern for payors and

consumers, and an area of focus for the government. At CVS Health, our goal is to ensure that clients and

members are getting the most out of their pharmacy benefit plan and that the cost of a drug is aligned with the

value it delivers in terms of patient outcomes. We leverage competition within drug classes where applicable,

develop innovative strategies to keep prescriptions affordable, and help members be more adherent.

In 2017, CVS Health pharmacy benefit management (PBM) strategies reduced trend for commercial clients to

1.9 percent per member per year (PMPY) the lowest in five years. Despite manufacturer price increases of near

10 percent, CVS Health kept drug price growth at a minimal 0.2 percent. Forty-two percent of our payor

clients spent less on their pharmacy benefit plan in 2017 than they had in 2016.

We also helped members save money and lower out-of-pocket costs. Three out of four members spent less than

$100 out of pocket in 2017, and nearly 90 percent spent less than $300. Monthly cost per member declined

by 10 cents to $11.89. To further enhance affordability and price transparency, we introduced real-time benefits

enabling prescribers to see the member-specific out-of-pocket costs of a prescribed medication as well as the

costs of clinically appropriate alternatives in real-time. This allows them to make more informed prescribing

decisions and offer members medication options that may be more affordable.

Keeping drugs affordable helped improve adherence to the highest level in seven years. With plan designs

that promoted lower-cost options and targeted adherence interventions, we increased the number of

optimally adherent members in key categories like diabetes, hypertension and hyperlipidemia by as much

as 1.8 percentage points. Better adherence can help reduce overall health care costs and improve quality of life.

In 2018, we are doing even more to help keep drugs affordable with our new Saving Patients Money initiative.

Saving Patients Money is designed to help address the high cost of prescription drugs by providing greater

pricing transparency across all points of care, including at the pharmacy, and directly to members.

CVS Health is delivering value for payors and their members with better

outcomes and cost management. It’s part of how we help people on their

path to better health.

It’s All About ValueDrug Trend

Report 2017

2017 Trend: CVS Health 3

AWP Ination Near 10%, But Minimal Drug Price Growth

9.2%

Traditional

Brands

8.3%

Specialty

Brands

0.4% 0.2%

Generics CVS Health

Drug Price Growth

In 2017, we leveraged market competition, maximized use of low-cost generics, and effectively negotiated discounts and rebates,

all of which helped keep drug price growth nearly flat at 0.2 percent for our payor clients. Our strategies helped protect clients

from manufacturer price increases of almost 10 percent. By minimizing cost growth we were also able to reduce overall trend for

clients to 1.9 percent PMPY — the lowest in five years. Forty-two percent of our clients had negative trend; meaning their benefit

plan spent less in 2017 on prescription drugs than they had in 2016.

Many plans adopted generics first strategies or preventive drug lists with $0 copays for generics. Our generic dispensing rate

reached 86.1 percent, and played a significant role in keeping drug price growth down. Brand drugs, both traditional and specialty,

accounted for only 14 percent of prescriptions dispensed, but 69 percent of pharmaceutical spend.

1.7%

Utilization

Growth

+

=

0.2%

CVS Health

Drug Price Growth

1.9%

PMPY 2017

Drug Trend

Minimal drug price

growth helped reduce

trend to the lowest

level in five years.

Low Drug Price Growth and Trend Despite AWP Ination

Prescription drug trend is the measure of growth in

prescription spending per member per month. Trend

calculations take into account the effects of drug price,

drug utilization and the mix of branded versus generic

drugs, as well as the positive effect of negotiated rebates on

overall trend. The 2017 trend cohort represents CVS Health

commercial PBM clients—employers and health plans.

Price is measured as cost per days supply.

2017 Trend: CVS Health 4

Most of our post-rebate trend was driven by growth in utilization, trending at 1.7

percent. Generics played a major role in this utilization growth, helping keep overall as

well as member costs low. Generic utilization grew at 3.6 percent, while utilization of

brands dropped substantially — trending at a negative 9.5 percent.

Affordable generics, along with targeted adherence interventions, also helped increase

the percentage of members who were optimally adherent. Key chronic disease

categories, including hyperlipidemia, hypertension and diabetes, saw adherence

improvements. Preventive drug lists with $0 copays for generics, as well as formulary

strategies and plan designs that promoted the use of generics first, helped drive rapid

member transition to newly launched generics, reducing costs for high-utilization

categories such as antihypertensives and cholesterol-reducing drugs.

Utilization Grew, Adherence Improved

Affordable Generics Also

Helped Promote Adherence*

Hyperlipidemia 1.8

Hypertension 1.2

Diabetes 1.2

Generics Were Top Drivers of Utilization Growth

Ranked in order of contribution to 2017 utilization trend.

rosuvastatin calcium

atorvastatin calcium

ezetimibe

olmesartan medoxomil

metformin HCL

amlodipine besylate

losartan potassium

hyperlipidemia

hyperlipidemia

hyperlipidemia

hypertension

diabetes

hypertension

hypertension

Generic Reference Brand Used in Treating

Crestor

Lipitor

Zetia

Benicar

Glucophage, Glumetza

Norvasc

Cozaar

1

2

3

4

5

6

7

*Percentage point increase in number of optimally

adherent members.

2017 Trend: CVS Health 5

Strategic Management Kept Specialty Drug Price

Growth to 3.7% Despite AWP Ination of 8.3%

Specialty pharmaceuticals have expanded beyond the treatment of small populations and rare conditions to treat

conditions that affect millions of patients. Ongoing growth in utilization and manufacturer-driven price increases

continued to drive rapid growth in specialty spending making these therapies a top payor concern.

In 2017, the AWP inflation rate for specialty drugs was 8.3 percent. However, through effective formulary

strategies, indication- and outcomes-based contracting, and cost-cap based rebates we were able to keep

specialty drug cost growth for payors at just 3.7 percent. The specialty drug pipeline continues to be robust,

fueling further strong growth for years to come. Last year alone, the Food and Drug Administration (FDA) approved

67 new specialty drugs — including five biosimilars — and 69 supplemental specialty indications.

1

Hundreds

more new drugs are in development including therapies for conditions such as eczema, asthma, cancer, and

osteoarthritis. Most, if not all, are expected to carry annual price tags in the tens, if not hundreds, of thousands of

dollars. These new drugs, and supplemental indications for existing therapies, will continue to significantly expand

the population of specialty pharmaceutical users.

With the increase in number of specialty drugs, the growing population of patients on specialty therapies, and

ever-rising prices, careful management is required to help manage utilization of these complex therapies to ensure

that the right patient is receiving the right drug at the right time and that reimbursement is related to the value a

drug delivers. Ensuring high-touch, holistic patient support for optimal adherence, and symptom and co-morbidity

management are also key. Now, more than ever, payors need to have the right strategies in place to ensure

appropriate patient access and utilization.

Growth in appropriate utilization drove most of post-rebate specialty trend.

9.2%

Specialty

Utilization

+

=

3.7%

Drug Price

Growth

12.9%

2017 Specialty

Trend

2017 Trend: CVS Health 6

Market Competition Determines Management Approach

At 1.9 percent, our low 2017 trend reflects a strategic approach to the complex dynamics of the pharmaceutical market. We carefully

evaluate the pharmaceutical landscape to identify competitive therapy classes and compare drug efficacy, to determine appropriate

formulary placement for specific drugs for each condition. This enables us to effectively negotiate rebates and offer competitive

pricing to clients, to help keep overall costs in control.

• Categories with multiple brand and generic options

• Market competition limits price increases

• Use formulary, preventive drug lists to maximize utilization

of generics

• PBM management helped to improve adherence in these

categories by 1.8 (for antihyperlipidemics) and 1.2 (for

antihypertensives) percentage points

• Account for nearly 70% of cost and all cost and trend growth

• Specialty drugs tend to face less competition in their categories

• Manage formulary and leverage competition to negotiate for lowest-net cost

• For specialty: indication- and outcomes-based contracting, and cost-cap based rebates;

utilization management

• Gross trend for autoimmune was 25.5%

• Adherence improved by 1.2 (for antidiabetics) and 1.9 (for rheumatoid arthritis)

percentage points

Competitive Brand

Categories

Less Competitive

Categories

More Competitive Categories

Antihyperlipidemics

AWP Inflation:

Example Categories:

Antihypertensives Antidiabetics Autoimmune

1.9% 3% 4.9% 11.7%

-25.8%

-11.6%

1.4%

20.3%

Post-Rebate

Trend by

Category

Rebates and

competitive

pricing help

keep overall

costs in control.

.

More Competitive/Less Competitive

2017 Trend: CVS Health 7

Age-adjusted, post-rebate.

CVS Health Managed Formularies: Include Standard with Opt-In to Drug Removals, Advanced Control Formulary, and Template Value Formulary.

Drug Price Declined for Clients Aligned with

Our Formulary Management Strategy

Across our commercial cohort, management strategies helped keep drug price growth to a low 0.2 percent. For clients aligned with

our managed formularies, drug price actually declined — by 0.1 percent — in 2017. Despite greater utilization, these clients had lower

PMPM costs as well as overall trend.

Formulary is one of the most effective means of leveraging market competition and promoting the use of lower-cost options,

including generics. Our management approach includes a strategic assessment of the marketplace, allowing us to evaluate how

products compete in therapeutic categories and where it may be appropriate to remove specific products in categories with multiple

clinical options. This enables us to effectively negotiate rebates and offer competitive pricing to clients. We also continue to develop and

implement more targeted management approaches such as indication-based formularies, in which prices and rebates for a drug are

negotiated based on its effectiveness to treat a specific diagnosis rather than at a therapy class level.

Formulary Strategy Lowers Cost, Improves Utilization

Formularies with

drug removals did

not reduce utilization

but did cause drug

price to decline.

Utilization Trend

1.6% 1.8%

Drug Price Change

2.6% -0.1%

Overall Trend

4.2%

1.7%

2016-2017

Standard Formulary

without Drug Removals

Managed Formularies

with Drug Removals

$104.10

$108.42

$87.43

$88.94

2016 Gross Cost PMPM 2017 Gross Cost PMPM

Standard Formulary

without Drug Removals

Managed Formularies

with Drug Removals

2017 Trend: CVS Health 8

Lower Cost and Trend for Antidiabetics

Diabetes affects a huge portion of the U.S. population, and accounts for substantial health care as well as pharmacy

spend. Effectively managing diabetes with the appropriate medication regimen can help improve outcomes and

lower overall pharmacy as well as health care costs, but managing this complex drug category can be challenging.

Our formulary and utilization management options helped reduce cost for antidiabetic drugs for clients. Trend for the

category fell to just 1.4 percent.

Metformin, a biguanide, is the cornerstone of oral antidiabetic treatment and is available in various forms, as a

generic as well as a branded drug. Prices for both brand drugs and generics vary widely. Our management approach

focuses on encouraging the utilization of the most cost-effective choices, helping reduce cost per day’s supply for

metformin, and for the biguanide class overall.

The U.S. Food and Drug Administration approved the biosimilar Basaglar as safe and effective at improving glycemic

control late in 2015, followed by its launch in late 2016.

2

We were ahead of the industry in adopting Basaglar as the

preferred long-acting insulin, removing the branded products Lantus and Toujeo from our managed formularies.

This helped reduce costs for payors and for members. Preferred formulary placement for drugs with lower member

out-of-pocket costs also helped improve the number of optimally adherent members by 1.2 percentage points.

Higher adherence to diabetes medications can help significantly lower the risk for adverse events, and save money in

avoidable, downstream health care costs.

Reducing Cost Per Days Supply

DRUG TYPE 2016 2017 Decline

Biguanides $1.32 $1.05 -20.5%

Long-Acting Insulin $8.53 $6.51 -23.7%

In 2017, the antidiabetic

category trended at

1.4% PMPY despite

AWP inflation of 4.9%.

What’s more, adherence

increased.

2017 Trend: CVS Health 9

Reducing Trend for Autoimmune Therapies Through Targeted Management

The autoimmune category is one of the fastest growing therapy classes. Many autoimmune drugs — including Humira, the top-selling drug in the U.S., as well as

Enbrel, Stelara, and other specialty medications, rank among the highest cost therapies in the market today.

3

However, ensuring patients have access to the drugs they

need to effectively manage their condition helps improve health outcomes. Through our formulary and utilization management strategies, we have been able to ensure

appropriate utilization, while minimizing impact to payors’ overall drug spend.

Effectively managing the autoimmune class is complex. Many of these drugs have multiple indications, including rheumatoid arthritis, psoriasis, and Crohn’s disease.

Supplemental indications, as well as the aging of the population, contribute significantly to the ongoing growth in utilization. Given the serious nature of these

conditions, it is difficult — and potentially risky — to switch a patient who may be stable on a particular drug to a different brand or biosimilar. This means payors

continue to bear the burden of high-cost drugs even when more cost-effective alternatives may be available.

Pre-rebate trend for the category was 25.5 percent. Through targeted management, including indication-based pricing and rebates, we have been able to mitigate the

impact on payors, resulting in an overall trend of 20.3 percent, driven mostly by an 11.0 percent utilization increase.

We helped keep drug price growth under control by encouraging the use of generic drugs as first-line therapy through our utilization management programs.

Research has demonstrated that generics can equal biologics in effectiveness. Our indication-based formulary targets specific conditions and drugs for appropriate

management. That is, drugs that have shown particular efficacy for a specific indication receive preferred placement for that indication, thereby increasing competition

in the category.

By taking a strategic and targeted approach, we helped payors manage their spend for this high-impact category while supporting appropriate utilization and helping

improve member outcomes.

2018 Advanced Control Specialty Formulary:

Indication-Based Approach for Autoimmune Category

*After failure of Humira.

Contracting at the

indication level can

increase competitiveness

and add value for payors.

Ankylosing spondylitis

Crohn’s disease

Psoriasis

Psoriatic arthritis

Rheumatoid arthritis

Humira, Simponi*

Condition Formulary Preferred Products

Cosentyx, Enbrel, Humira

Cimzia*, Humira

Humira, Stelara*, Taltz*

Cosentyx, Enbrel, Humira, Otezia

Enbrel, Humira, Kevzara, Orencia

Ulcerative colitis

2017 Trend: CVS Health 10

Right drug the first time

• Management according to NCCN

regimen guideline vs. managing

the drug

• Incorporation of tumor genomics into

decision trees

Rigorous avoidance of waste

• Split lls for orals

• Partial vials for infused medications

• Site of care management

• Precise claims management

$8M Projected Annual Oncology

Savings per 1M Members

Specialty Management: Keeping Pace

with the Complexity of Oncology

Cancer treatment has changed dramatically. Rather than treating colon cancer or breast

cancer, we tailor treatment to the individual’s tumor and stage of disease. We’re at the

point of defining the cellular abnormalities in a tumor and guiding therapy based on those

abnormalities. This “precision medicine” is advancing rapidly. Guidelines from the National

Comprehensive Cancer Network (NCCN), considered the gold standard, change 500

times a year.

4

There are 60,000 different genetic testing products on the market, with 10

new tests added every day.

5

At CVS Specialty, our focus is to provide support to oncologists and patients ensuring

that all patients have the opportunity to receive the most current recommended regimens

as early as possible. Once the appropriate regimen is in place we diligently eliminate

waste, avoid the use of supportive agents where there is little clinical utility, and whenever

possible drive to the lowest-cost site of care.

The Novologix management platform enables these efforts. By analyzing prescribed

regimens across medical and pharmacy benefits we are able to ensure conformance with

NCCN guidelines and drive appropriate conversations with physicians when care is off-

guideline. The platform enables several approaches to limiting waste, from partial fills in

clinical scenarios where 30-day supplies often go unused, to paying for partial vials under

the medical benefit. The platform can help us ensure that any patient with any cancer,

regardless of how rare, has the opportunity to get the best possible care from the start,

no matter where they are being treated.

The Novologix platform will help ensure that any patient,

with any cancer, can receive the best possible care, no

matter where they are being treated.

2017 Trend: CVS Health 11

Members who spent over $1,000 were more likely to use specialty drugs

or be in high deductible health plans

88% of Members Spent Less Than

$300 Out-of-Pocket

Prescription affordability is an important issue for consumers, and for our nation, but data indicates that high

out-of-pocket costs affect relatively few members. Among our commercial clients, average member out-of-pocket

(OOP) cost declined in 2017. Primary credit for the decline goes to the increasing utilization of generics, spurred by

formulary and plan designs as well as preventive drug lists with $0 copays for generics.

Across our commercial trend cohort, 88 percent of members spent less than $300 out-of-pocket. Only 2.7 percent

spent over $1,000. These higher cost members tended to be older, use specialty drugs or were enrolled in high

deductible health plans (HDHPs). About 20 percent of our cohort members were in HDHPs, but they comprised 30

percent of those spending $1,000 or more.

Over a quarter of the money members spent went to two categories. Antidiabetics accounted for 14.7 percent of

member spend. Autoimmune agents, including specialty drugs such as Humira and Enbrel, accounted for 11.4 percent

of the cohort’s out-of-pocket expense.

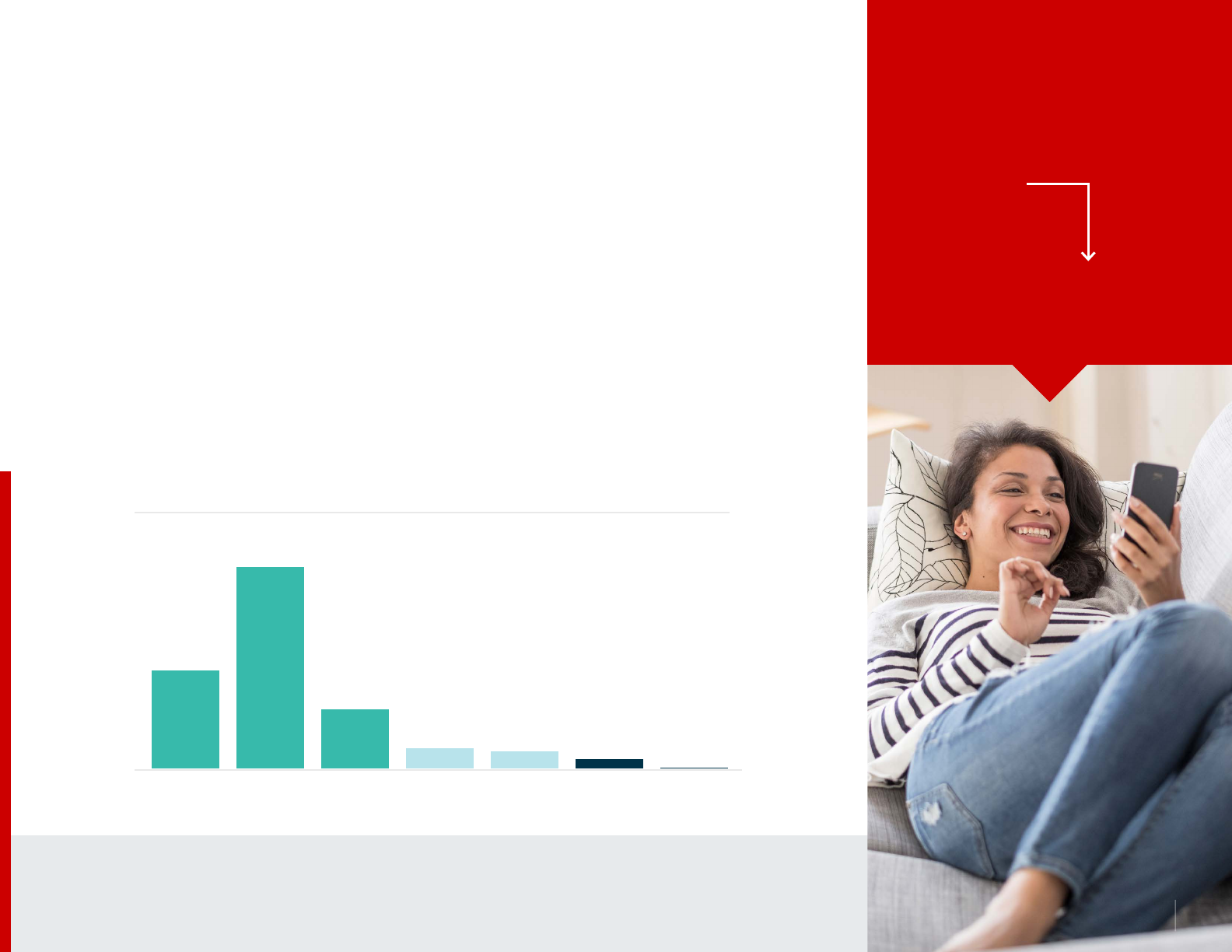

Nearly 3 out of 4 Members Spent Less than $100 in 2017

49.4%

14.6%

5%

4.3%

2.4%

0.3%

24%

W/O Claims $0 – $100 $100 – $299 $500 – $999 $1000 – $3000 >$3000$300 – $499

This analysis is based on commercial member OOP spend and percentages are based on average eligible members in 2017.

Out-of-pocket

cost PMPM declined

$11.99

$11.89

2016

2017

2017 Trend: CVS Health 12

CVS Health: Saving Patients Money

In fall 2017, we announced the launch of real-time benefits, giving prescribers transparent access to member-specific

information. In 2018, we are expanding this capability to all points of care with the Savings Patients Money initiative.

During a provider visit: With real-time benefits, all of the information is integrated into the e-prescribing workflow

enabling prescribers to select a clinically appropriate medication that may be more affordable for the member. If the

selected drug has any restrictions, the prescriber can automatically submit an electronic PA (ePA) request, speeding

up the process and helping to avoid a disruption or delay of therapy.

At the pharmacy counter: CVS pharmacists have access to a Rx Savings Finder that lets them quickly and easily

determine the best way members can save money on out-of-pocket costs — with the primary goal of helping find the

lowest cost alternative under their pharmacy benefit. If the member’s prescription is not covered, the pharmacist is

alerted in their workflow and can request a prescription change from the provider at the click of a button.

On the go: Members can also use the Check Drug Cost tool in the CVS Caremark app and on Caremark.com to look

up drug costs, find if there are any lower-cost alternatives available, or learn how they can save by filling a 90-day

prescription rather than a 30-day supply. With this information, they can proactively start a conversation with their

provider or the pharmacist about their prescription options.

Real-time benefits further build on our connections with electronic health records, bringing the system closer to true,

seamless interoperability. It means prescribers, pharmacists and members have transparent access to information at

critical decision points to help members get the medications they need faster and more affordably.

Saving Patients Money at All Points of Care

We’ve made real-time benefit information available to prescribers, CVS pharmacists and to members via the

CVS Caremark app and on Caremark.com. The available information includes:

• Cost of a selected drug based on the member’s plan coverage, deductible, and how much of the deductible

the member has met

• Up to five clinically appropriate, potentially lower-cost therapeutic alternatives, mapped for clinical substitution

and specific to the member’s formulary

• Restrictions on the selected drug such as prior authorization (PA) or step therapy requirement

Today, CVS pharmacists

have access to member-

specific information,

including clinically

appropriate prescription

alternatives, built into

their workflow.

2017 Trend: CVS Health 13

1. New drug count includes new molecular entities, new biologics, biosimilars, new combinations, new formulations, projections by Pipeline Services, data 2017.

2. https://www.mdedge.com/clinicalendocrinologynews/article/105252/diabetes/lantus-competitor-basaglar-wins-fda-approval.

3. https://www.webmd.com/drug-medication/news/20171003/humira-again-top-selling-drug-in-us.

4. https://www.nccn.org/disclosures/transparency.aspx. Accessed February 2, 2018.

5. https://www.concertgenetics.com/resources/current-landscape-of-genetic-testing/. Accessed February 2, 2018.

Trend Methodology

This report provides an overview of performance for CVS Health commercial clients — employers and

health plans. Trend was calculated on a cohort of more than 1,400 clients, covering 24.5 million lives.

The cohort is built only on clients eligible throughout all of 2016 and 2017, removing commercial clients

with eligibility shifts exceeding 20% as well as any clients contractually prohibited from inclusion.

All of the savings and/or trend results discussed in this report will vary for specic populations based on a variety of factors, including demographics, plan design

and programs adopted by the client. Client-specic modeling available upon request.

This document includes references to brand-name prescription drugs that are trademarks of pharmaceutical manufacturers not associated with CVS Health.

Image source: Licensed from Getty Images, 2018.

Data source, unless noted otherwise, CVS Health Enterprise Analytics.

©2018 CVS Health. All rights reserved. 106-45365A 040518

2017 Trend: CVS Health 14