CUSTOMS DIRECTIVE

ORIGINATING OFFICE: FO:TP DISTRIBUTION: S-01

CUSTOMS DIRECTIVE NO. 3550-079A

DATE: JUNE 27, 2001

SUPERSEDES: 3550-079, 1/24/01

REVIEW DATE: JUNE 2003

SUBJECT: Ultimate Consignee at time of Entry or Release

1 PURPOSE. To provide guidance on the appropriate identification number to be

provided for the Ultimate Consignee of imported merchandise at the time of entry or

release. The definition of Ultimate Consignee as required at time of entry summary

filing will be addressed in a separate directive (to supersede CD 099 3550-061).

2 POLICY. The references and procedures outlined in this directive will be

followed to ensure consistency and uniformity in data collected.

3 AUTHORITIES/REFERENCES. 19 CFR § 142.3(a)(6), 19 CFR § 24.5,

19 USC Sec. 1484(a)(2), and T. D. 94-39.

4 RESPONSIBILITIES.

4.1 The Directors, Field Operations, Customs Management Centers, are to ensure

implementation of this directive.

4.2 Port Directors will ensure that local procedures accommodate the guidelines

contained in this directive.

4.3 Port Directors will distribute this information through routine trade notification

practices (i.e., information notices, trade notices, etc.).

5 BACKGROUND. Customs has for many years allowed different parties to be

identified as the Ultimate Consignee for shipments of imported merchandise. As a

result, the requirement to identify the Ultimate Consignee at the time of entry or release

has not been uniformly applied to all imported merchandise. In an effort to correct this

situation, the following procedures and requirements will be instituted to ensure

compliance with the required identification of the Ultimate Consignee on formal and

informal entries (both electronic and manual), at the time of entry or release.

6 DEFINITIONS.

6.1 For purposes of this directive, a formal entry is defined as the documentation

required (either electronic or paper) to secure the release of imported merchandise that

is either valued in excess of $2,000, or if valued less than $2,000, would otherwise

require the submission of formal entry documents (e.g., certain quota merchandise).

6.2 For purposes of this directive, an informal entry is defined as the documentation

required (either electronic or paper) to secure the release of imported merchandise that

is either valued less than $2,000, or if valued in excess of $2,000, would otherwise be

released on an informal entry (e.g., personal effects & household goods).

6.3 The Ultimate Consignee at the time of entry or release is defined as the party in

the United States, to whom the overseas shipper sold the imported merchandise. If at

the time of entry or release the imported merchandise has not been sold, then the

Ultimate Consignee at the time of entry or release is defined as the party in the United

States to whom the overseas shipper consigned the imported merchandise. If the

merchandise has not been sold or consigned to a U.S. party at the time of entry or

release, then the Ultimate Consignee at the time of entry or release is defined as the

proprietor of the U.S. premises to which the merchandise is to be delivered.

6.4 For formal entries, the appropriate identification number for the Ultimate

Consignee is defined as an Internal Revenue Service employer identification number, or

a Social Security number. Filing for the appropriate identification number for the

Ultimate Consignee is provided for in 19 CFR § 24.5. Customs assigned numbers are

for non-U.S. entities, and as such, are not acceptable to identify the Ultimate Consignee

on formal entries, except for the following classes of merchandise:

6.4.1 For merchandise which is temporarily imported under the Harmonized Tariff

Schedule (HTS) subheading 9813.00.35 (see below), a nonresident of the United States

may be identified as the Ultimate Consignee.

HTS Subheading 9813.00.35: Automobiles, motorcycles, bicycles, airplanes,

airships, balloons, boats, racing shells and similar vehicles and craft, and the

usual equipment of the foregoing; all the foregoing which are brought temporarily

into the United States by nonresidents for the purpose of taking part in races or

other specific contests.

6.4.2 For merchandise which is temporarily imported under the Harmonized Tariff

Schedule (HTS) subheading 9813.00.50 (see below), a nonresident of the United States

may be identified as the Ultimate Consignee.

HTS Subheading 9813.00.50: Professional equipment, tools of trade, repair

components for equipment or tools admitted under this heading and camping

equipment; all the foregoing imported by or for nonresidents sojourning

temporarily in the United States and for the use of nonresidents.

6.5 For informal entries, the appropriate identification number for the Ultimate

Consignee is defined as an Internal Revenue Service employer identification number, or

a Social Security number. In instances when neither an Internal Revenue Service

employer identification number, nor a Social Security number is available at the time of

entry or release, the appropriate identification number for the Ultimate Consignee on

informal entries may also be defined as any of the following:

6.5.1 The ABI transmission of the name and U.S. address of the party to whom the

overseas shipper either sold or consigned the imported merchandise, or if unknown, the

ABI transmission of the name and U.S. address of the proprietor of the U.S. premises to

which the imported merchandise is to be delivered.

6.5.2 An Internal Revenue Service employer identification number or Social Security

number that identifies the licensed and U.S.-based Customs broker that filed the

informal entry.

6.5.3 An Internal Revenue Service employer identification number or Social Security

number that identifies a U.S.-based Importer of Record that is associated with the

informal entry.

6.5.4 A “blank” Ultimate Consignee field that is either electronically transmitted through

ABI, or manually completed online by Customs. However, the use of the “blank”

Ultimate Consignee field will automatically result in the duplication of the Importer of

Record’s Internal Revenue Service employee identification number, or Social Security

number, in the Ultimate Consignee field. In the case of merchandise that is imported by

a foreign-based Importer of Record, the use of a “blank” Ultimate Consignee field will

result in a foreign-based Ultimate Consignee. A Foreign-based Ultimate Consignee is

only acceptable for informal entries or for such temporary importations that are

described in sections 6.4.1 and 6.4.2 of this directive.

6.5.5 An Internal Revenue Service employer identification number or Social Security

number that identifies a U.S.-based Nominal Consignee, such as a carrier, express

consignment operator, freight forwarder, or consolidator that is associated with the

informal entry.

6.5.6 A Customs-generated identification number that identifies a foreign-based

Ultimate Consignee that is associated with the informal entry. A Foreign-based Ultimate

Consignee is only acceptable for informal entries or for such temporary importations

that are described in sections 6.4.1 and 6.4.2 of this directive.

7 INSTRUCTIONS TO THE TRADE.

7.1 For formal entries, a Customs Broker may not be listed as the Ultimate

Consignee unless they own the merchandise,

or there is no known U.S. buyer and

the

accompanying documentation shows the broker’s premises as the location to which the

merchandise is to be delivered. However, a licensed Customs Broker may be identified

as the Importer of Record on a formal entry, if designated by the owner, purchaser, or

consignee of the merchandise.

7.2 For formal entries, Nominal Consignees (i.e., carrier, express consignment

operators, freight forwarders, or consolidators) may not be identified as the Ultimate

Consignee unless they own the merchandise,

or there is no known U.S. buyer and

the

accompanying documentation shows their premises as the location to which the

merchandise is to be delivered. Nominal Consignees cannot be identified as the

Importer of Record on a formal entry unless they own, or have purchased the imported

merchandise.

7.3 For formal entries, the name of the Ultimate Consignee (not the ID #) must be

provided for duty free merchandise entered on a CF 7523 if it is different from the name

of the Importer of Record.

7.4 For formal entries, the appropriate identification number of the Ultimate

Consignee must be provided for merchandise that is granted immediate delivery on a

CF 3461 ALT.

7.5 Filers must provide the appropriate identification number, name, and U.S. street

address of the Ultimate Consignee on formal entries filed on a CF 3461, or presented

on a CF 7501 for release. The appropriate identification number for the Ultimate

Consignee must reflect the information provided in the supporting documentation. In

the case of a consolidated entry, filers must provide the appropriate identification

number, name, and U.S. street address of the Ultimate Consignee, for each distinct

shipment that is valued in excess of $2,000, or would otherwise require the submission

of formal entry documentation (e.g., certain quota merchandise).

7.6 The Ultimate Consignee at time of release does not necessarily need to match

the Ultimate Consignee provided at time of entry summary processing on a CF 7501.

For example, if the Ultimate Consignee at time of release is unknown, the Filer

will provide the identification number for the U.S. premises to which the merchandise is

to be delivered. When the merchandise is sold or consigned after release but prior to

entry summary filing, the Filer must provide the buyer’s identification number as the

Ultimate Consignee on the entry summary filing.

7.7 For formal entries, if the required Ultimate Consignee identification number is not

available at the time of release, the ABI filer may use ACS references to locate the

appropriate identification number, but only after having used reasonable care to query

all of their resources. Upon receipt of an ABI transmission of the Ultimate Consignee’s

name and U.S. address, ACS will search for a match and, if available, generate and

supply the Filer with an encrypted version of the Ultimate Consignee’s identification

number to be used in the electronic filing of the entry for release. If a match is not

made, Customs will generate an internal control on the transmitted Consignee’s name

and U.S. address and permit the ABI transmission of the selectivity entry for the

release. However, the Filer is required to obtain the proper identification number for the

filing of the entry summary. The use of the Ultimate Consignee’s name and U.S.

address, in lieu of the Ultimate Consignee’s identification number, is not allowed when

an entry is certified from summary (CF 7501), or if the Filer knows the Ultimate

Consignee’s Internal Revenue Service employer identification number or Social Security

number. The use of the ACS name and address capability will result in the Customs

requirement that paper documentation be presented prior to release.

7.8 For informal entries, if the Ultimate Consignee’s correct Internal Revenue Service

employer identification number or correct Social Security number is not available at the

time of entry or release, an ABI filer may use the name and address capability to obtain

an appropriate identification number for the Ultimate Consignee. If the Ultimate

Consignee’s correct name and U.S. address is not available at the time of entry or

release, the Filer of an informal entry may use any of the options that are specified in

Section 6.5 of this directive to identify the Ultimate Consignee. However, for any ABI

transmission of an informal entry with a “blank” Ultimate Consignee field, the Automated

Commercial System will assume that the Ultimate Consignee and the Importer of

Record are the same party, and will therefore duplicate the Importer of Record

identification number in the Ultimate Consignee field. The use of a “blank” Ultimate

Consignee field is not allowed when an informal entry is certified from summary (CF

7501), or when the merchandise is subject to any requirements imposed by other

Federal agencies of the U.S. Government.

7.9 Filers must provide the name and U.S. street address of the Ultimate Consignee

for informal entries released off the manifest in the express consignment environment,

and for merchandise entered for immediate transportation (CF 7512).

8 EXAMPLES.

8.1 In instances when a U.S. Company places a consolidated order with an overseas

shipper to fill orders placed by the U.S. Company’s individual customers (i.e., direct

sales/just-in-time inventory), the Ultimate Consignee for Customs purposes is the U.S.

Company regardless of whether the imported merchandise will be sent to a distribution

center owned by the U.S. Company or sent directly to the individual customers. This is

because the U.S. Company is the party who purchased the imported merchandise from

the overseas shipper.

8.2 In instances when individual customers place their orders directly with the

overseas shipper and the overseas shipper consolidates the orders and sends one

shipment to a distributor in the U.S. or directly to the individual customers, for Customs

purposes, the Ultimate Consignee is the individual customer. This is because the

individual customer is the party who purchased the imported merchandise from the

overseas shipper.

8.3 In instances when a U.S. Company places an order with a foreign supplier who

in turn places an order with another foreign supplier to be entered into the United States

delivered, duty paid for the account of the U.S. Company, for Customs purposes, the

Ultimate Consignee is the U.S. Company. This is because the U.S. Company is the

party who purchased the imported merchandise from overseas.

8.4 In instances when a U.S. Company places an order with an overseas shipper

and then sells the goods to a second U.S. Company in a domestic transaction prior to

the importation, for Customs purposes, the Ultimate Consignee is the first U.S.

Company. This is because the first U.S. Company is the party who purchased the

imported merchandise from the overseas shipper.

8.5 In instances when an unsold shipment is being imported for and delivered to a

trade show and the importer of record is foreign, for Customs purposes, the Ultimate

Consignee is the proprietor of the trade show location. In other words, since the

merchandise has not been sold or consigned to a U.S. party at the time of entry or

release, the Ultimate Consignee is defined as the proprietor of the U.S. premises to

which the merchandise is to be delivered.

8.6 In instances when entry is made listing one party as the importer of record for a

consolidated shipment, the appropriate identification number for the Ultimate Consignee

must be submitted for each separate and distinct shipment within the consolidated

shipment (See T. D. 94-39 Examples). This is because each shipment has a different

party who purchased the imported merchandise from the overseas shipper.

9 CUSTOMS PROCEDURES.

9.1 If the appropriate identification number for the Ultimate Consignee is not provided

to Customs in a manner consistent with this directive, the entry will not be considered to

be filed in proper form and will be returned to the importer or their agent for correction

prior to Customs processing.

9.2 Customs will not issue a Customs-generated identification number to identify the

Ultimate Consignee on formal entries. Since the Ultimate Consignee is a U.S. party, the

“Notification of Importer’s Number or Application for Importer’s Number, or Notice of

Change of Name or Address” (CF 5106) form must provide either an Internal Revenue

Service employer identification number or a Social Security number.

10 MEASURES.

10.1 Directors, Field Operations are to ensure that all ports under their jurisdictions

are in compliance with this directive. An evaluation and audit of each port should be

undertaken to determine the importing community’s compliance with this directive. The

CMC will be responsible for verifying that ports perform audits regarding the data

provided manually and electronically for the Ultimate Consignee. If needed, the CMC

will be responsible for providing analysis support for the port’s audit.

10.2 Port Directors will ensure compliance with this directive by Filers via an audit of

ABI records and paper entry/entry summary records. At a minimum, audits should be

performed to ensure compliance during each self-inspection cycle.

10.3 In cases where the Filer fails to provide, or supplies an identification number for

the Ultimate Consignee, which is inconsistent with the provisions of this directive, the

Importer of Record and Filer will be referred to the Enforcement Evaluation Team or

Broker Compliance Office for appropriate informed or enforced compliance action.

Assistant Commissioner

Office of Field Operations

Attachment

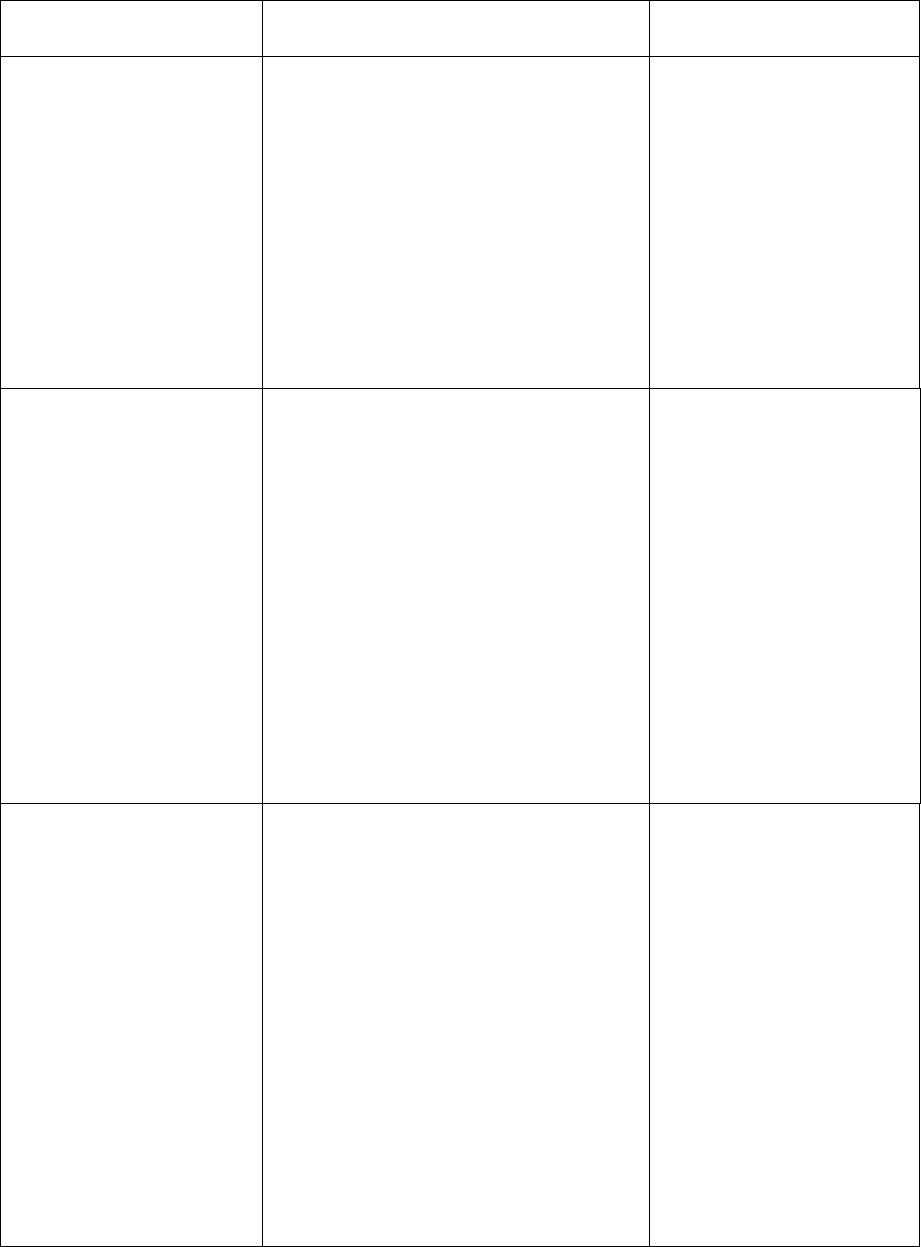

Type of entry at time

of release

Elements required for

Ultimate Consignee

Formal entry

CF 3461/CF7501

All modes of transportation,

including international postal

service

Commercial use & valued over

$2,000

Filers must use the

correct ID #, or an ABI

transmission of the

name and address, if

not certifying from

summary (CF 7501), or

entering merchandise

that is subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

Formal entry with

multiple ultimate

consignees

CF 3461

All modes of transportation

Valued over $2000

Consolidated shipments

consigned to a common carrier,

freight forwarder, freight handler,

or other public service agency for

distribution shall be treated as

one importation.

For each consignee,

Filers must use the

correct ID #, or if

unavailable, may use

an ABI transmission of

the name and address

when not certifying

from summary (CF

7501), or entering

merchandise that is

subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

Immediate delivery

CF 3461 ALT

Arrival from contiguous country

Meets immediate delivery

requirements

Commercial use of any value

For formal immediate

deliveries, Filers must

use the correct ID #, or

if unavailable, may use

an ABI transmission of

the name and address

when not certifying

from summary (CF

7501), or entering

merchandise that is

subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

For informal immediate

deliveries, Filers must

use the correct ID #, or

if unavailable, may use

an ABI transmission of

the name and address

or any other option

specified in Section 6.5

of this directive, when

not certifying from

summary, or entering

merchandise that is

subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

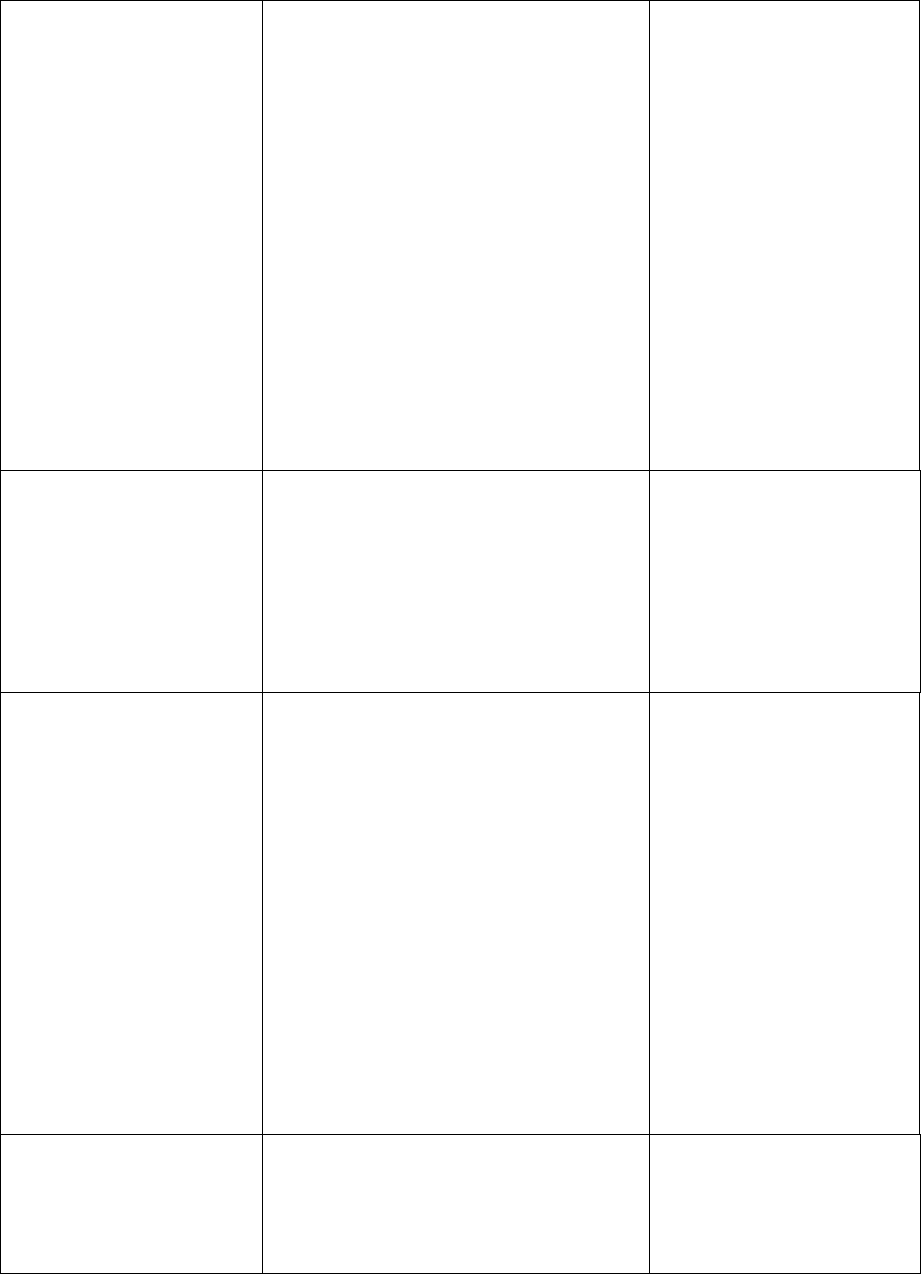

BRASS Repetitive, low risk, and high

volume importations from a

contiguous country

Entry or Immediate Delivery

Participation approved prior to

arrival

None.

Informal entry

CF 3461/CF7501

All modes of transportation

For personal use

Valued under $2,000

Filers must use the

correct ID #, or if

unavailable, may use

an ABI transmission of

the name and address

or any other option

specified in Section 6.5

of this directive, when

not certifying from

summary, or entering

merchandise that is

subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

Informal entry with

multiple ultimate

consignees

CF 3461

All modes of transportation

Valued under $2000

Consolidated shipments

consigned to a common carrier,

freight forwarder, freight handler,

For each consignee,

Filers must use the

correct ID #, or if

unavailable, may use

an ABI transmission of

or other public service agency for

distribution shall be treated as

one importation.

the name and address

or any other option

specified in Section 6.5

of this directive, when

not certifying from

summary, or entering

merchandise that is

subject to any

requirements imposed

by other Federal

agencies of the U.S.

Government.

Informal mail entry

CF 3419A, CF 368

and/or CF 7501

International postal service

Valued under $2,000

Not Quota

Not restricted or prohibited

None. No ID # is

required to process this

form.

Informal Mail entry

under pass free

exemption

International postal service

Valued under $200

Gift sent to person other than

purchaser

None. No ID # is

required to process a

mail entry under $200.

Customs Declaration

CF 6059B

Air passenger arrivals from

foreign

None. No ID # is

required to process this

form.

FTZ entry CF 214 All modes of transportation

Commercial merchandise

None. No ID # is

required to process this

form.

Carnet International Customs document

replaces usual Customs

documentation for temporary

importations – valid for one year

None. No ID # is

required to process this

form.

CF 368 Customs

receipt

All modes of transportation

Merchandise for personal use

arriving in cargo or accompanying

international passenger that is

Valued under $2000

None. No ID # is

required to process this

form.

Duty free entry

CF 7523

All modes of transportation

Duty and tax free merchandise

Not restricted or prohibited

Commercial use under $2000

Non-commercial of any value

Written name and

address.

Entry for immediate

transportation

CF 7512

All modes of transportation Written name and

address.

“Release off the Valued under $200 Written name and

manifest”

Section 321

address.

Consolidated informal

entry

CF 3461/CF 7501

Express consignment

environment

Valued from $200 - $2000

Written name and

address.

Oral entry declaration

paid via PC Cash

register

Non-commercial merchandise

accompanying arriving

international passenger

Valued under $2000

None. No ID # is

required to process an

oral baggage

declaration.