CDP Full Corporate Questionnaire

An Overview

Page 3 of 29 @cdp | www.cdp.net

Contents

CDP Full Corporate Questionnaire.......................................................................................................................... 1

Version ............................................................................................................................ 2

Contents........................................................................................................................................................................ 3

Overview of the full corporate questionnaire ...................................................................................................... 4

Full corporate questionnaire structure.......................................................................................................... 4

Full and SME questionnaires........................................................................................................................... 5

Environmental issues in CDP’s full corporate questionnaire .................................................... 6

Climate Change .................................................................................................................................................. 6

Forests ................................................................................................................................................................. 6

Water Security .................................................................................................................................................... 7

Plastics................................................................................................................................................................. 7

Biodiversity .......................................................................................................................................................... 8

CDP questionnaire sectors ................................................................................................10

Sector approach............................................................................................................................................... 10

Sector-specific content................................................................................................................................... 11

Connection to other frameworks ........................................................................................21

IFRS S2 (ISSB) climate standard .................................................................................................................. 21

Task Force on Climate-related Financial Disclosures (TCFD) ............................................................... 21

Task Force on Nature-related Financial Disclosures (TNFD)................................................................. 22

European Sustainability Reporting Standards (ESRS) ............................................................................. 22

Accountability Framework initiative (AFi) .................................................................................................. 22

Global Reporting Initiative (GRI) ................................................................................................................... 22

Ellen MacArthur Foundation Global Commitment.................................................................................... 23

Preparing your CDP response ............................................................................................24

CDP disclosure cycle 2024 ............................................................................................................................ 24

CDP disclosure support materials ............................................................................................................... 24

Important notes for completing your CDP response ............................................................................... 26

Providing feedback to CDP ............................................................................................................................ 29

Page 4 of 29 @cdp | www.cdp.net

Overview of the full corporate questionnaire

CDP’s questionnaires evolve annually to drive corporate ambition further, and support companies and

financial markets to transition in line with a 1.5°C, deforestation-free, water-secure world. CDP collects

environmental data from the world’s largest organizations on behalf of over 700 institutional capital

markets signatories with a combined US$142 trillion in assets, and 330+ major purchasers with over

US$6.4 trillion in procurement spend. Since its launch in 2002, CDP has helped thousands of companies

to measure their environmental impacts, set ambitious targets, and demonstrate progress for key

stakeholders.

In 2024, the CDP corporate questionnaires on climate change, forests, and water security have been

integrated into one corporate questionnaire. Through this questionnaire, organizations can provide data

on multiple environmental issues in a single disclosure, encouraging more holistic and balanced

reporting. The CDP full corporate questionnaire follows the latest science, aligns with new high-quality

disclosure frameworks and standards, and includes incremental changes to the datapoints from CDP’s

previous climate change, forests, and water security questionnaires.

Full corporate questionnaire structure

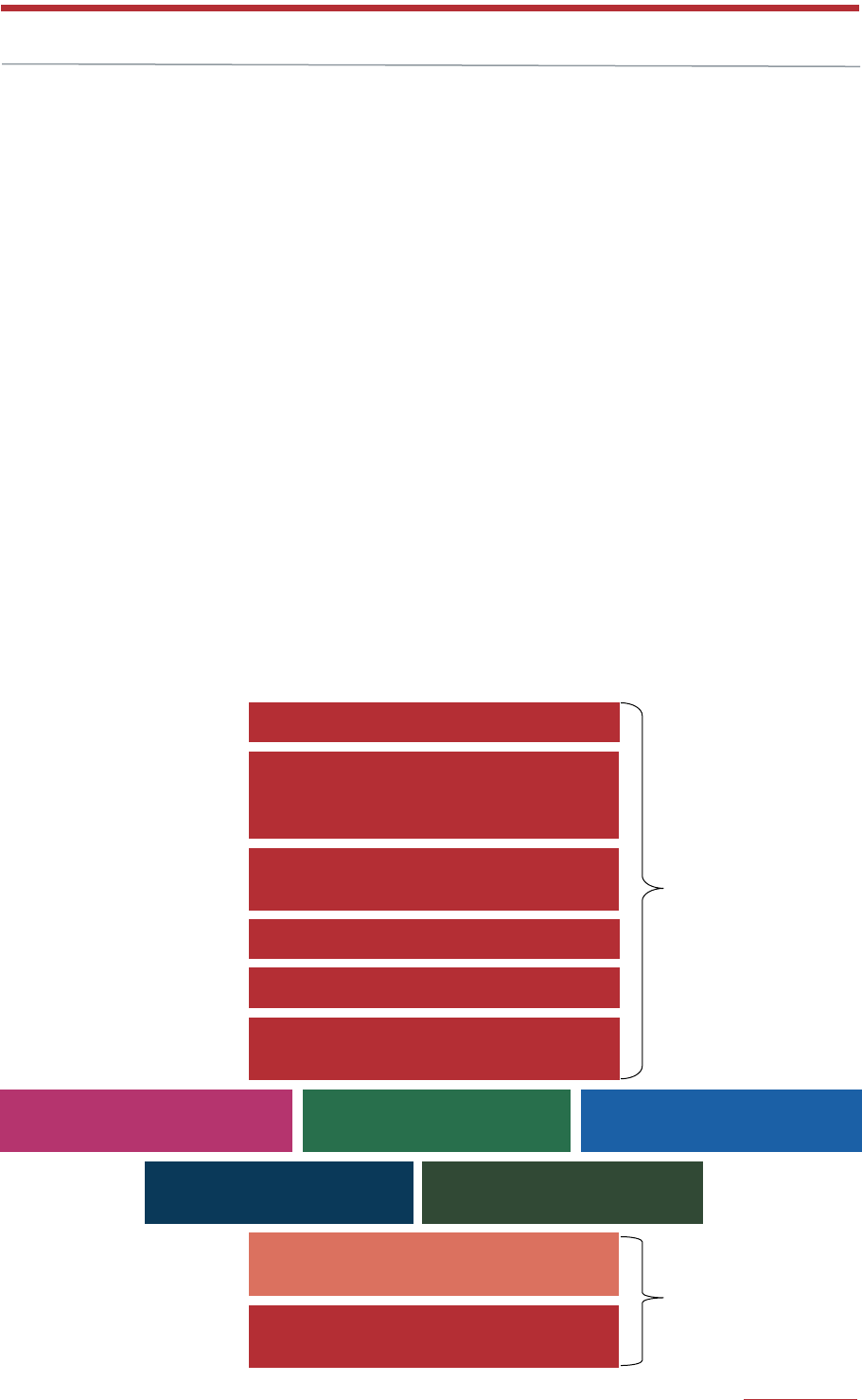

There are 13 modules in the full corporate questionnaire. Modules 1 to 6, and 13 are integrated, which

means that questions in these modules cover more than one environmental issue area. Conversely,

modules 7-11 relate to ‘Environmental Performance’ and each module is specific to an environmental

issue area. Organizations in the financial services sector will be presented with module 12, which is an

integrated, sector-specific ‘Environmental Performance’ module.

All disclosers will be presented with datapoints on climate change, as well as supplementary datapoints

on plastics and biodiversity. Datapoints on forests and water security will only be presented if a

discloser has been requested or has opted in to reporting on these environmental issues.

The journey through CDP’s full corporate questionnaire includes the following:

Integrated modules

Sector-specific FS module

Integrated modules

Module 1: Introduction

Module 2: Identification, assessment, and

management of dependencies, impacts,

risks, and opportunities

Module 4: Governance

Module 5: Business strategy

Module 6: Environmental performance –

Consolidation approach

Module 7: Environmental

performance – Climate change

Module 8: Environmental

performance – Forests

Module 9: Environmental

performance – Water security

Module 10: Environmental

performance – Plastics

Module 11: Environmental

performance – Biodiversity

Module 12: Environmental performance –

Financial Services approach

Module 13: Further information

& Sign off

Module 3: Disclosure of

risks and opportunities

Page 5 of 29 @cdp | www.cdp.net

Full and SME corporate questionnaires

CDP recognizes that Small and Medium Enterprises (SMEs) may have different reporting capabilities

and requirements compared to larger organizations. For this reason, CDP has two corporate

questionnaires: the full questionnaire and the SME questionnaire.

The full corporate questionnaire is suitable for large organizations and includes sector-specific

datapoints. Meanwhile, the SME questionnaire is tailored to the needs of SMEs and contains fewer and

simplified datapoints. Only organizations that meet CDP’s SME eligibility thresholds will have the option

to complete the SME questionnaire.

Note that this document provides an overview of the full corporate questionnaire only. You can find

more information on the SME questionnaire on the CDP website.

Eligibility to complete the SME questionnaire

Organizations with a headcount of less than 500 total employees and annual revenue less than

US$50 million are eligible and recommended to complete the SME questionnaire.

Organizations with a headcount of less than 500 total employees and revenue between

US$50M – US$250M, as well as organizations with a headcount of 500 – 1,000 total employees

and annual revenue less than US$250 million are eligible to complete the SME questionnaire

but are recommended to complete the full corporate questionnaire.

Organizations with a headcount of more than 1,000 total employees or annual revenue of more

than US$250 million are not eligible to complete the SME questionnaire and can only complete

the full corporate questionnaire.

Page 6 of 29 @cdp | www.cdp.net

Environmental issues in CDP’s full corporate questionnaire

Addressing the climate crisis cannot be achieved without simultaneously addressing the nature crisis.

Carbon emissions and climate change are only part of the challenge. At least US$44 trillion in economic

value is generated through the exploitation of natural resources every year – and losses to nature

continue at unprecedented rates.

To put protecting climate and nature at the heart of corporate strategy, CDP’s full corporate

questionnaire challenges organizations to take more effective action across a wide spectrum of

environmental issues. It encourages CDP disclosers and data users to assess and manage

environmental dependencies, impacts, risks, and opportunities as an interrelated challenge.

Note: ‘environmental issues’ refers to an organization’s dependencies, impacts, risks, and opportunities

related to the environmental issue areas covered in CDP’s corporate questionnaire i.e., climate change,

forests, water, biodiversity and/or plastics.

Climate Change

Improving corporate awareness through measurement and disclosure is essential to the effective

management of climate change risk. CDP’s datapoints on climate change have been evolving over time

in line with the latest climate science and global policy development. The 2015 Paris Agreement was a

tipping point in the global approach to climate change. By agreeing to limit global temperature rises to

well below 2°C and pursue efforts to limit warming to under 1.5°C, governments have committed to a

transition to a net-zero carbon economy. This transition will create winners and losers within and across

business sectors, as the manifestation of climate-related opportunities and risks accelerates in both

size and scope. ‘Business as usual’ will not be a good indicator of how companies will perform.

In its first two decades, CDP’s climate change datapoints focused on raising ambition and providing

data to improve governance and decision-making. But time is fast running out to prevent catastrophic

climate change, and an irreversible loss of nature and habitats. There is now an urgent need to ensure

that stated intentions are accompanied by concrete plans, with transition metrics, and evidence of

progress against agreed targets. Accountability is needed to raise the bar to align with halving

emissions, shifting towards nature positivity by 2030, and achieving net-zero emissions and full nature

recovery by 2050.

In line with CDP’s 2021-2025 strategy, climate change questions and their scoring will be evolving to

further encourage and support organizations to set targets and create tangible climate transition plans,

as well as to measure their performance against them. For this reason, from 2024 onwards, all

organizations disclosing via CDP will be requested to report climate-related data.

Nonetheless, carbon emissions are only one part of the challenge. The climate and nature crises need

to be addressed simultaneously, including by conserving, protecting, and restoring ecosystems,

adopting more sustainable forestry and water use practices, and ensuring a circular economy.

Forests

Deforestation and forest degradation account for approximately 15% of the world's greenhouse gas

emissions. Stopping deforestation and the conversion of other natural ecosystems is vital to

significantly reducing greenhouse gas emissions and the loss of natural capital. Global demand for

agricultural commodities is the primary driver of deforestation and ecosystem conversion, as timber is

extracted unsustainably, and land is cleared for agricultural production. This represents major risks to

businesses, as agricultural commodities associated with high levels of deforestation are the building

blocks of millions of products traded globally, and thus feature in the value chains of many

organizations.

Page 7 of 29 @cdp | www.cdp.net

CDP’s forests questions focus on how organizations produce and source four key commodities: timber,

cattle products, soy, and palm oil. In addition, organizations may report on how they produce and source

rubber, cocoa, and coffee. Eliminating deforestation and conversion of other ecosystems linked to the

production and sourcing of these commodities is critical to meet near-term climate and nature targets

as well as complying with emerging regulatory requirements.

CDP’s forests-related datapoints provide data users and disclosers with important information about

how organizations are progressing towards key targets of eliminating deforestation and conversion.

Organizations can disclose comprehensively on the proportion of their commodity volumes that are

deforestation- and conversion-free (DCF) through standardized metrics developed by the

Accountability Framework initiative (AFi). These metrics are contextualized and complimented by

datapoints on sourcing areas and traceability, methods used to progress volumes to DCF, engagement

with supplier and smallholders, restoration and conservation projects, and adoption of landscape

approaches to achieve sustainable land use at scale.

Water Security

Through transparency and accountability, the CDP questionnaire drives organizations and financial

markets to decouple growth from depletion of freshwater resources and allocate capital towards a

water secure economy to achieve the Sustainable Development Goals. Specifically, the CDP

questionnaire collects information for capital markets actors, customers, and policy makers on an

organization’s management, governance, and use of water resources. The water security program has

grown significantly since it was established in 2010, in terms of the numbers of organizations

disclosing water-related data, the value of associated assets, and the number of investors and

customers requesting the data. CDP now holds the world’s largest corporate water dataset, with more

organizations reporting on water than ever before.

CDP water security datapoints provide data users and disclosers with an insight on current and future

water-related dependencies, impacts, risks, and opportunities. They also present a journey to water

stewardship and water security by assisting organizations to progress the maturity of their water

management and corporate reporting, as well as enabling benchmarking against leading practice.

Collecting and disclosing information on management and governance of water-related dependencies,

impacts, risks, and opportunities, as well as the integration of water into long term strategic objectives,

provides data for decision making and catalyzes corporate action.

Water accounting

To progress water security for all and to minimize water-related risks, organizations must eliminate any

detrimental impact on water ecosystems and resources. Risk exposure occurs as water flows into and

out of an organization’s boundaries, so CDP collects information to determine how well an organization

understands this flow. Organizations are encouraged to account for all their interaction with water, and

to minimize that interaction (e.g., through reduced withdrawals, efficiency improvements, or by

changing their business activities). This means that CDP seeks more nuanced information than

volumetric reductions in freshwater removal or consumption. Most important is that organizations have

robust monitoring and accounting in place for all aspects of their corporate hydrology, and that they

demonstrate an understanding of their dependencies and impacts on water.

Measurements of withdrawal, discharge, and consumption take place as water crosses the reporting

boundary of an organization, at either the corporate level or facility level. This makes the concept of the

reporting boundary at the corporate and facility level central to your CDP response.

You can find more information on water accounting in CDP’s Technical Note on Water Accounting.

Plastics

Plastic pollution and waste harms our ecosystems, economies, and communities. It threatens the

function of the world’s terrestrial, ocean and freshwater ecosystems, which serve as sanctuaries for

biodiversity, vital food sources and major carbon sinks. Despite the globally accepted scale of the

Page 8 of 29 @cdp | www.cdp.net

problem and extent of its impacts, many organizations are yet to have a strong understanding of how

they contribute to the plastics crisis and their exposure to commercial, legal, and reputational risks

across their value chains.

Note that all disclosers responding to CDP’s full corporate questionnaire will be presented with

datapoints on plastics. However, these will be unscored in 2024, and therefore will not impact an

organization’s CDP score. This is in recognition that many organizations are in the early stages of

developing their action, accountability, and reporting on plastics.

On behalf of its data users (capital markets signatories, purchasing companies, and others), CDP is

requesting organizations to report on whether they are currently taking actions to:

reduce plastic usage;

reduce or eliminate virgin content in plastics;

eliminate problematic and unnecessary plastics;

transition to reuse systems;

reduce microplastic emissions; and

increase circularity.

This provides decision makers with clear, comprehensive, and comparable data on the production,

commercialization, usage, and end-of-life management of plastics across the global economy. CDP’s

datapoints on plastics are informed by existing plastics disclosure frameworks, standards, and

guidelines including the Ellen MacArthur Foundation and the UN Environment Programme’s Global

Commitment framework, WWF ReSource Tracker, ESRS and GRI 306: Waste.

As strategies for reducing plastic dependency and increasing circularity mature, CDP will review the

data that organizations are able to provide and collect feedback from our stakeholders on what is most

relevant to driving action and informing decision making.

Biodiversity

In line with its 2021-2025 strategy, CDP has begun to broaden the environmental issues covered in its

questionnaire, with the inclusion of questions on organizations’ approach to addressing and

maintaining biodiversity. These datapoints are material to all sectors and geographies, and responses

will inform future biodiversity metrics, ensuring the relevance and usefulness of biodiversity corporate

reporting to both financial institutions and policy makers.

Note that all disclosers responding to CDP’s full corporate questionnaire will be presented with

datapoints on biodiversity. However, these will be unscored in 2024, and therefore will not impact an

organization’s CDP score.

CDP’s datapoints on biodiversity are aligned with the IUCN’s “Guidelines for planning and monitoring

corporate biodiversity performance” and allow organizations to demonstrate how they:

understand their dependencies, impacts, risks and/or opportunities on biodiversity and identify

where they should concentrate their efforts;

think about their ambitions to mitigate any negative impact on biodiversity and their goals,

objectives, and key strategies;

decide on what indicators and metrics to use to measure the success of their strategies; and

monitor and disclose their success.

The introduction of biodiversity datapoints reflects a growing recognition of the significant risks of

biodiversity loss. In part, these risks stem from the role that biodiversity plays in climate change and

other nature challenges. As highlighted by the Intergovernmental Science-Policy Platform on

Page 9 of 29 @cdp | www.cdp.net

Biodiversity and Ecosystem Services (IPBES) and the Intergovernmental Panel on Climate Change

(IPCC), there are close relationships between biodiversity and GHG emissions, resilience, and

adaptations to the threat of climate change. However, biodiversity loss also represents a real risk in its

own right: biodiversity underpins all of the ecosystem services society ultimately depends on and, unlike

climate change, biodiversity losses are irreversible.

According to the World Economic Forum, at least US$44 trillion of economic value generation – over

half the world’s total GDP – is moderately or highly dependent on biodiversity and its services and, as

a result, exposed to risks from biodiversity loss. The UK Treasury reports that biodiversity losses

threaten to undermine the global economy.

Therefore, it is essential for organizations across all sectors of the economy to demonstrate their

awareness of biodiversity-related dependencies, impacts, risks, and opportunities in their value chain,

and what actions they are taking to mitigate or eliminate any negative effects.

Page 10 of 29 @cdp | www.cdp.net

CDP questionnaire sectors

Sector approach

Organizations in high-impact sectors will be presented with questions specific to that sector in addition

to the general questions. CDP requests additional datapoints from organizations in high-impact sectors

relating to climate change, forests, water security, plastics, and biodiversity.

The sector-specific questions allocated to organizations are defined by CDP's Activity Classification

System (CDP-ACS). This system categorizes organizations by focusing on the activities from which

they derive revenue and associating these with potential effects on their organization regarding climate

change, deforestation, and water security.

An organization may be allocated up to four questionnaire sectors (including ‘General’). However, if an

organization is eligible for CDP scoring, they will only be scored on their primary questionnaire sector.

Note that since the full corporate questionnaire includes sector-specific questions, some question

numbers may not be consecutive, as not all questions are applicable to every organization.

Page 11 of 29 @cdp | www.cdp.net

Sector-specific content

The table below provides sector descriptions and outlines the key sector-specific content for each high-impact sector in CDP’s full corporate questionnaire per

environmental issue area.

Questionnaire

sector

Introduction

Sector-specific content

Climate change

Water security

Agricultural

commodities (AC)

Activities in the agricultural commodities sector include crop farming, fish

& animal farming, and other types of agricultural production, such as for

cotton, sugar, and tea. Other activities can relate to producing raw

materials (crops and/or livestock) that will be used as ingredients in the

manufacturing and packaging of consumer goods by the food, beverage

and tobacco sector. This includes the small-scale production of non-timber

forest products (e.g. rubber, nuts, seeds, etc.).

The agricultural commodities sector is fundamentally dependent on natural

resources, and thus directly affected by climate change. It also accounts

for almost 70% of the world’s water consumption, impacting on and

impacted by water security. With increasingly unpredictable weather

patterns and increasing demand, the agricultural commodities sector is at

high risk.

Regarding climate change, emissions are associated with the entire

agricultural commodities value chain, therefore a whole value chain

approach is advised; including consideration of emissions resulting from

the consumption of products. Water quality is also an important issue for

this sector: excessive or poor application of fertilizers and pesticides can

lead to nitrate and phosphorus run-offs, polluting waterways and

contaminating groundwater.

This CDP sector aligns with the TCFD’s Agriculture, Food, and Forest

Products group.

Climate-related sector-specific

datapoints include:

Land management practices with

climate change

mitigation/adaptation benefits;

Biogenic carbon pertaining to direct

operations;

Commodity-specific emissions

intensity data related to the activities

performed by your organization; and

Scope 1 and Scope 3 emissions

breakdowns by relevant business

activity.

Water-related sector-specific

datapoints include:

Production or sourcing of

agricultural products in

areas of water stress; and

Water intensity of

produced or sourced

agricultural products.

Capital goods

(CG)

The capital goods sector provides products and services to key high

emitting end markets, such as power generation, construction,

transportation, and industry.

It is not an emissions intensive sector from direct emissions (Scope 1) or

indirect emissions from energy use (Scope 2). However, indirect emissions

in the value chain (Scope 3) are key for the sector, with the majority related

to the use of sold products and services. Capital goods producers must

Climate-related sector-specific

datapoints include:

Life cycle emissions assessment of

products and services;

Year-on-year Scope 3 emissions

performance;

No water-related sector-

specific datapoints.

Page 12 of 29 @cdp | www.cdp.net

therefore be able to understand their indirect emissions profile and manage

their product-related climate change risks if they are to ensure future

competitive success and be prepared for any product-related regulation.

Investment in research and development of energy efficient low-carbon

products with scope for system-wide change will be also key for the capital

goods sector’s transition to a low-carbon future.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Efficiency metrics for products

and/or services; and

Investments in low-carbon R&D.

Cement (CE)

Activities in the cement sector encompass those associated with concrete

production: from limestone quarrying to concrete end-of-life.

Producing cement is an energy intensive process, with most of the GHG

emissions for cement production originating from the combustion of fossil

fuels for the required heating of key ingredients to about 1450°C in massive

cement kilns. In addition, significant CO2 emissions are released as

process emissions during production. Increasing energy efficiency, fuel

switching, reducing clinker content, and moving to more efficient dry

process kilns with pre-calciner and pre-heating technologies are examples

of ways the cement industry can reduce its emissions.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Climate-related sector-specific

datapoints include:

Emissions intensities of key industry

products;

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

Energy consumption and generation

breakdowns; and

Investments in low-carbon R&D.

No water-related sector-

specific datapoints.

Chemicals (CH)

The chemicals sector is diverse, creating a variety of products such as

commodity chemicals, specialty chemicals, life science products, and

consumer care products.

Most emissions in this sector originate from either fossil fuel combustion

during the production process, or as process chemical emissions. Process

redesign, increased heat production efficiency through cogeneration, and

fuel-switching are examples of ways the chemicals sector can cut

emissions. Depending on feedstocks used, this sector may have significant

upstream emissions, thus feedstock switching from fossil to bio-based

fuels may also reduce significant emissions.

Furthermore, chemical production is frequently water intensive. Water is

used primarily for cooling purposes, but also as a raw material in cleaning

and transport, as a solvent, and as part of final products. Feedstocks,

wastes, or products, and hazardous substances in this sector may pose

particular water pollution risks and a significant threat to water

ecosystems.

Climate-related sector-specific

datapoints include:

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

Scope 3 category 1 emissions by

feedstock;

Energy consumption and generation

breakdowns;

Feedstock consumption;

Emissions intensities of key industry

products;

Production and capacity of key

industry products; and

Investments in low-carbon R&D.

Water-related sector-specific

datapoints include:

Water intensity metrics

Page 13 of 29 @cdp | www.cdp.net

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Coal (CO)

Activities in the coal sector include coal extraction, coal-based fuel

production, and coal-based energy generation.

Coal combustion contributes the largest share of the anthropogenic

greenhouse gas increase in the atmosphere and dominates power

generation globally (IEA, 2017: Tracking Clean Energy Progress). The coal

sector faces increasing regulatory and market pressures in its downstream

use, including competition from natural gas and renewables. As such,

direct and use-phase emissions are strategic risks for coal companies.

Coal mining also depends on and produces large volumes of water, and the

resulting tailings dams are a key environmental risk for this sector requiring

strong management procedures. Tailings dam failures and toxic spills can

lead to long-lasting impacts on human health and downstream riverine

ecosystems. Additionally, coal is one of the most-water intensive methods

of generating electricity.

This CDP sector aligns with the TCFD’s Energy group.

Climate-related sector-specific

datapoints include:

Specific methane reduction targets,

and flaring and methane leak

detection and reduction;

Scope 1 and Scope 2 emissions

breakdown by sector production

activities;

Additional metrics for the coal

industry on coal reserves and

production; and

Investments in low-carbon R&D.

Water-related sector-specific

datapoints include:

Location of and

management procedures

for tailings dams; and

Details on water intensity

metrics for mining and

processing.

Construction (CN)

The construction sector is complex, with different types of companies

operating at different points in the value chain; spanning across design,

materials manufacturing, construction and life cycle maintenance.

Although it is important to draw distinct lines of responsibility for CO2

emissions within the buildings value chain, all of the actors in this sector

need to align their actions if we are to achieve the Paris Agreement goals,

for which the reduction of building-related emissions will play a critical role.

Buildings are currently responsible for 39% of global GHG emissions. The

sizeable part of these emissions is attributable not only to the construction

process itself, but also to materials manufacturing (embodied emissions)

and to operational emissions during the use stage of buildings. With the

present global building floor area set to more than double by 2060, there

will be increased demand for construction materials for new buildings,

extensions, renovations and infrastructure; creating significant and

immediate carbon emissions before a project’s completion.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Climate-related sector-specific

datapoints include:

Assessment of buildings’ life cycle

emissions and embodied carbon

emissions data;

Net zero carbon buildings; and

Investments in low-carbon R&D.

No water-related sector-

specific datapoints.

Page 14 of 29 @cdp | www.cdp.net

Electric utilities

(EU)

Activities in the electric utilities sector include electricity generation,

transmission, distribution, and retailing.

Climate change is a strategic issue for the electric utilities sector, as power

generation is the single largest emitter of CO2, accounting for around 25%

of global emissions (IPCC, 2014: Climate Change 2014: Synthesis Report.

Contribution of Working Groups I, II and III to the Fifth Assessment Report

of the Intergovernmental Panel on Climate Change). With the increasing

commercialization of renewable energy sources and the advent of

decentralized power production, the electric utilities sector has the

potential to undergo a key transition to low-carbon energy sources (IIGCC,

2016: Investor Expectations of Electric Utility Companies: Looking down

the line at carbon asset risk).

Additionally, this sector is heavily dependent on water for cooling; and for

electricity generation itself in the case of hydropower. For this reason,

plants are often located near bodies of water and organizations rely on

access to these resources for the success of their business. Electricity

generation in particular indicates the highest exposure to water-related

dependencies, impacts, risks, and opportunities. The most pressing issues

for the sector relate to the impacts of business activities on the

hydrological cycle and thermal pollution. Specific forms of water pollution

for some fuel types also expose organizations to risks, such as radiation or

hydrocarbon contamination. Robust assessment procedures relating to

water are critical, given the long-term nature of investments in the sector.

This CDP sector aligns with the TCFD’s Energy group.

Climate-related sector-specific

datapoints include:

Methane emissions reduction;

Scope 1 emissions breakdown by

sector production activities;

Power generation capacity;

Global transmission and distribution

business;

CAPEX plans for power generation

and products and services; and

Investments in low-carbon R&D.

Water-related sector-specific

datapoints include:

Organizations are asked

to disclose their

nameplate capacity by

primary power generation

source;

Questions specific for

hydropower operations on

whether they monitor, the

fulfillment of

environmental flows and

the sediment loadings;

and

Water intensity metrics.

Note: Only organizations with

electricity generation activities

will be presented with these

sector-specific questions.

Food, beverage &

tobacco (FB)

This sector can include a broad range of activities from the production of

agricultural products to food retail, and, amongst others, the processing of

raw commodities into ingredients, the manufacturing of packaged

consumer or industrial food, beverage, or tobacco products (including

packaging processes), and the trade and distribution of food products.

Organizations in this sector may also produce their own raw materials, or

source them from the agricultural commodities sector.

This sector inherits climate-related risks from the agricultural activities in

its value chain, including physical risks such as changing weather patterns,

and regulatory risks relating to farm management practices. In addition,

they face other climate-related risks associated with the processing,

manufacture and packaging of food, drinks, and tobacco products, such as

Climate-related sector-specific

datapoints include:

Land management practices with

climate change

mitigation/adaptation benefits;

Biogenic carbon pertaining to direct

operations;

Commodity-specific emissions

intensity data related to the activities

performed by your organization; and

Water-related sector-specific

datapoints include:

Production or sourcing of

agricultural products in

areas of water stress; and

Water intensity of

produced or sourced

agricultural products.

Page 15 of 29 @cdp | www.cdp.net

CO

2

emissions from machinery, storage facilities and transportation.

Focusing on the whole value chain to address these risks is highly

important for organizations in this sector.

The agricultural and manufacturing value chains for this sector are also

considered high impact for water. Agricultural production and food

processing are the most significant activities in terms of water-related

dependencies, impacts, risks, and opportunities. Water availability, water

quality, and water pollution due to chemical use and management of

animal wastes are issues that can affect significantly an organization’s

performance.

Note that the manufacturing of personal care and household goods using

agricultural commodities is excluded from CDP’s framing of this sector.

This CDP sector aligns with the TCFD’s Agriculture, Food, and Forest

Products group.

Scope 1 and Scope 3 emissions

breakdowns by relevant business

activity.

Metals & mining

(MM)

This sector represents the first stage of the life cycle of a huge range of

manufactured products, from nuclear reactors to hand cream.

Emissions from this sector occur at mining sites during the combustion of

fossil fuels and the processing of materials necessary to transform the

Earth’s elements into useable industry materials. Metals and mining

organizations can reduce emissions through increased recycling, increased

purchases of renewable and low-carbon electricity, and through generation

at production sites, which may be particularly significant in remote mines

not connected to a power grid. Fuel switching and energy efficiency

improvements are needed at metal processing facilities.

Metals and mining organizations also depend on large volumes of water,

and the resulting tailings dams are a key environmental risk for this sector

requiring strong management procedures. Tailings dam failures and toxic

spills can lead to long-lasting impacts on human health and downstream

riverine ecosystems.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Climate-related sector-specific

datapoints include:

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

Energy consumption and generation

breakdowns;

Production and capacity of key

commodities; and

Investments in low-carbon R&D.

Water-related sector-specific

datapoints include:

Details on water intensity

metrics for mining and

processing; and

Location of and

management procedures

for tailings dams.

Oil & gas (OG)

The main activities of the oil and gas sector are the exploration and

development, production, refining, and the manufacturing and distribution

of petrochemicals.

Climate-related sector-specific

datapoints include:

Water-related sector-specific

datapoints include:

Page 16 of 29 @cdp | www.cdp.net

Climate change is a strategic risk for the oil & gas sector; its operational

and use phase emissions collectively account for half of global CO2

emissions (IIGCC, 2016: Investor Expectations of Oil and Gas Companies:

Transition to a lower carbon future).

Water is also critical to the oil & gas sector. The extraction of hydrocarbons

produces large volumes of water. Smart, safe management of this

produced water is both a business opportunity and a regulatory necessity

(in that water contaminated with hydrocarbons must be properly treated).

In newer exploration and production such as hydraulic fracturing and oil

sands, water is often an essential input for the recovery of the resource.

Downstream operations such as refining and petrochemicals require water

for cooling.

This CDP sector aligns line with the TCFD’s Energy group.

Specific methane reduction targets,

and flaring and methane leak

detection and reduction;

Scope 1 emissions intensities by

hydrocarbon category;

Emissions breakdowns by oil and

gas business divisions, associated

activities, emissions categories, and

methane emissions;

Hydrocarbon reserves, production,

refining, and transportation figures;

Low-carbon investments and capital

flexibility; and

Transfers & sequestration of CO2

emissions.

Total water withdrawals,

discharges and

consumption by business

division (upstream,

downstream and

chemicals); and

Water intensity metrics

Paper & forestry

(PF)

Activities in the paper and forestry sector include the production and/or

sourcing of timber and timber-based products. Note that non-timber forest

products (NTFPs; e.g. rubber, nuts, seeds, etc.) are excluded, as the

production and/or sourcing of these products is generally done at a smaller

scale and consumed in local markets. (Organizations that produce or

source NTFPs are included in our agricultural commodities sector.)

Risks associated with the paper and forestry sector extend across the

whole value chain and arise from a variety of sources. For example,

unsustainable forest management activities, such as illegal logging,

burning or other practices can cause deforestation/forest degradation.

Another potential issue is the sourcing of timber-based products for the

manufacture of wooden goods, paper, and packaging. The use of wood as

biofuel for facility energy use, downstream and upstream transportation

and distribution, and the waste management of plantation/machinery

residues are also all risk factors for the paper and forestry sector. Focusing

on the whole value chain to address these risks is highly important for

organizations in this sector.

This CDP sector aligns with the TCFD’s Agriculture, Food and Forest

Products group.

Climate-related sector-specific

datapoints include:

Land management practices with

climate change

mitigation/adaptation benefits;

Biogenic carbon pertaining to direct

operations;

Commodity-specific emissions

intensity data related to the activities

performed by your organization; and

Scope 1 and 3 emissions

breakdowns by relevant business

activity.

No water-related sector-

specific datapoints.

Real Estate (RE)

The real estate sector is complex, with different types of companies

operating at different points in the value chain; spanning across finance,

design, construction and life cycle maintenance.

Climate-related sector-specific

datapoints include:

No water-related sector-

specific datapoints.

Page 17 of 29 @cdp | www.cdp.net

Although it is important to draw distinct lines of responsibility for CO2

emissions within the buildings value chain, all of the actors in this sector

need to align their actions if we are to achieve the Paris Agreement goals,

for which the reduction of building-related emissions will play a critical role.

Buildings are currently responsible for 39% of global GHG emissions. The

sizeable part of these emissions is attributable not only to the use of built

assets – operational emissions (Scopes 1 and 2), but also to their

construction – embodied emissions (Scope 3). With the present global

building floor area set to more than double by 2060, there will be increased

demand for construction materials for new buildings, extensions,

renovations and infrastructure; creating significant and immediate carbon

emissions before a project’s completion.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Assessment of buildings’ life cycle

emissions and embodied carbon

emissions data;

Net zero carbon buildings; and

Investments in low-carbon R&D.

Steel (ST)

The activities in this sector encompass those associated with the steel

production chain: from quarrying to furnace operations.

Steel production is a highly energy-intensive process as it transforms iron

ore to steel. This transformation requires significant amounts of heat and

coking coal, an emissions-intensive product. Production efficiency is

closely tied to furnace type, so replacing less efficient furnaces with

electric arc furnaces can greatly reduce emissions. However, electric arc

furnaces rely on recycled steel for production, and therefore cannot be

utilized without the more emissions-intensive production routes such as

the blast furnace to transform the iron ore. Attention to feedstocks,

implementing various techniques throughout the production process,

installing technologies at plants, and switching to less emissions-intensive

fuels will lower production emissions in the steel industry. In addition,

recycling steel has, and will continue to, significantly reduce emissions.

This CDP sector aligns with the TCFD’s Materials and Buildings group.

Climate-related sector-specific

datapoints include:

Best available technique

implementation;

Emissions intensities of steel plants;

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

Energy consumption and generation

breakdowns;

Feedstock consumption;

Consumption, production, and

capacity figures by steel plant;

Production and capacity of key

industry products; and

Investments in low-carbon R&D.

No water-related sector-

specific datapoints.

Transport OEMs

(TO)

Transport activity is responsible for almost a quarter of global energy-

related emissions, with total energy use for transport having doubled in the

last 35 years. The transport value chain includes activities such as original

equipment, vehicle parts and engine manufacturers, and service operators.

CDP’s original equipment manufacturers (OEMs) transport sector includes

industrial producers of transportation vehicles across five transport

Climate-related sector-specific

datapoints include:

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

No water-related sector-

specific datapoints.

Page 18 of 29 @cdp | www.cdp.net

modes: Aviation, Light Duty Vehicles (LDV), Heavy Duty Vehicles (HDV),

Shipping, and Rail; and two transport subjects: freight and passengers.

This CDP sector aligns with the TCFD’s Transportation group.

Activity-based emissions intensities

in Scope 3 category 11: use of sold

products;

Efficiency metrics for products

and/or services;

Implementation metrics for low-

carbon transportation technologies;

and

Investments in low-carbon R&D.

Note that businesses classified as

Transport-OEMs Engine Part

Manufacturers will only be asked to

provide details on investments in low-

carbon R&D.

Transport

services (TS)

Transport activity is responsible for almost a quarter of global energy-

related emissions, with total energy use for transport having doubled in the

last 35 years. The transport value chain includes activities such as original

equipment, vehicle parts and engine manufacturers, and service operators.

CDP’s transport services sector includes operators of vehicles transporting

goods and/or passengers across 5 modes: Aviation, Light Duty Vehicles

(LDV), Heavy Duty Vehicles (HDV), Shipping, and Rail. Between passenger

and freight transport, the key difference with relevance to the CDP

questionnaire is the specific metrics that measure efficiency either by

passenger or by metric ton of goods transported.

This CDP sector (TS) aligns with the TCFD’s Transportation group.

Climate-related sector-specific

datapoints include:

Activity-based accounting of

emissions intensities in Scope 1,

Scope 2 and Scope 3 category 4:

Upstream emissions from

transportation;

Scope 1 and Scope 2 emissions

breakdowns by sector production

activities;

Data coverage and input factors to

calculate emissions intensity of

transport movements per

technology;

Efficiency metrics for products

and/or services; and

Implementation metrics for low-

carbon transportation technologies;

and

Investments in low-carbon R&D.

No water-related sector-

specific datapoints.

Page 19 of 29 @cdp | www.cdp.net

Financial Services (FS)

Activities in the financial services sector include banking, investing (asset management and/or asset

ownership), and insurance underwriting. Most of a financial institution’s climate and nature-related

dependencies, impacts, risks, and opportunities are likely to stem from the financial activities it

undertakes, which are intertwined with the subsequent environmental impacts of that financing. For

financial institutions to be catalysts of the transition, they must understand the commercial risks and

opportunities that they face, along with the environmental impact, and how to act on them.

The recommendations of the TCFD, TNFD, and other key frameworks highlight the important role of the

financial sector as preparers of environmental disclosures. Disclosure by this sector enables capital

markets actors, central banks, regulators/supervisors, and other relevant stakeholders to better

understand both organisational and systemic exposures to environmental risks and opportunities, as

well as how they impact climate change, forests, and water security through activities such as lending,

financial intermediary, investment and/or insurance underwriting.

Organizations in the financial services sector should respond to the CDP questionnaire in the context

of these financing activities, in addition to operational activities where appropriate. They will be

presented with sector-specific questions and modifications to general questions, as well as sector-

specific guidance that clarifies the type of information that banks, asset managers, asset owners, and

insurance companies should consider in their response.

CDP’s financial services questions focus on the following topics:

Identifying, assessing, and managing environmental dependencies, impacts, risks, and

opportunities related to portfolio activities;

Environmental issues covered by the organization’s policy frameworks;

Engagement with clients and investees on environmental topics;

Shareholder voting on environmental issues;

Products and services offered to clients;

Measuring the impact of portfolio activities on the environment;

Financed emissions, in line with the Partnership for Carbon Accounting Financials (PCAF) Global

GHG Accounting and Reporting Standard for the Financial Industry, and additional portfolio

impact metrics;

Portfolio targets related to climate change and other environmental issues.

Organizations with mining projects

The full corporate questionnaire contains additional questions and datapoints on biodiversity for

organizations with mining projects. These datapoints are unscored in 2024. These additional questions

provide information to data users about an organization’s awareness of and management of its

dependencies, impacts, risks, and opportunities related to its involvement in mining projects.

Specifically, “mining projects” refers to the extraction of all types of raw materials such as bauxite,

precious metals, non-ferrous metals (e.g. nickel, zinc, lead, lithium), iron ore, diamonds, coal (thermal

coal, metallurgical coal). Activities relating to the exploration of an area of interest for a mining project,

development to establish permanent access to the ore body and carry out commercial production, and

closure of a mine are also considered to be stages of a mining project.

CDP’s biodiversity questions for organizations with mining projects focus on the following topics:

Organizational activities;

Process for identifying, assessing, and managing dependencies, impacts, risks, and opportunities;

Environmental Impact Assessment (EIA);

Risk disclosure;

Exclusions;

Areas important for biodiversity;

Land resourced and land disturbed;

Page 20 of 29 @cdp | www.cdp.net

Artisanal and small-scale mining (ASM);

Biodiversity action plan;

Impacts on biodiversity;

Strategic business plan;

Biodiversity-related targets;

Mitigation hierarchy;

Additional conservation actions;

Closure and rehabilitation;

Engagement activities.

The option to respond to these is presented to organizations with the following CDP-ACS activities:

Coal extraction & processing, Other non-ferrous metals, Iron & steel, Precious metals, Aluminum, Metal

processing, Copper, Iron ore mining, Precious metals & minerals mining, Bauxite mining, Other non-

ferrous ore mining, Other non-metallic minerals.

Page 21 of 29 @cdp | www.cdp.net

Connection to other frameworks

To support the development of datapoints that are both valuable for organizations and provide

capital markets actors, policy makers, and other data users with meaningful information, CDP

works with a range of leading environmental organizations and standard setters. Through this,

CDP aims to contribute to the harmonization of standards and frameworks which plays an

important role in enhancing data quality and comparability.

Some of the standards and frameworks referenced in CDP’s full questionnaire include:

Accountability Framework initiative (AFi);

CEO Water Mandate;

Ellen MacArthur Foundation Global Commitment;

European Sustainability Reporting Standards (ESRS)

Global Reporting Initiative Standard (GRI);

IFRS S2 (ISSB) climate standard;

RE100;

Task Force on Climate-related Financial Disclosures (TCFD);

Task Force on Nature-related Financial Disclosures (TNFD).

Connections of CDP datapoints to the above frameworks can be viewed in the disclosure portal for

each question.

Furthermore, mapping documents for specific standards and frameworks are also available in

the CDP guidance tool. For additional guidance on standards and frameworks specific to the

Financial Services sector, refer to CDP’s Technical Note: Financial Services Transition Plans and

Net-Zero Commitments.

You can find information below on key standards and frameworks that are referenced in CDP’s

full corporate questionnaire.

IFRS S2 (ISSB) climate standard

CDP is ISSB’s key global climate disclosure partner with 23,000 companies already disclosing in 2023.

The ISSB’s climate standard is the foundational baseline for CDP’s climate disclosure. The 2024 CDP

questionnaire is aligned with IFRS S2 Climate-related Disclosures (IFRS S2). Together with the disclosed

dataset, the questionnaire provides an effective tool to support companies on their path to ISSB

compliance.

The alignment of CDP’s 2024 questionnaire with IFRS S2 will make life easier for companies and

critically accelerate the rapid global uptake of IFRS S2. By disclosing through CDP from June to

September 2024, companies will disclose data directly to their stakeholders and subsequently the wider

global market, including IFRS S2-aligned climate data.

Where CDP questions are related to requirements of IFRS S2, this is referenced under the ‘Connection

to other frameworks’ section of each question. The mapping table also provides a summary of these

connections between CDP questions and sections of IFRS S2.

Please note that the CDP questionnaire, though aligned with IFRS S2, should not be interpreted as

strictly fulfilling IFRS S2 requirements. Some CDP questions that align with IFRS S2 also ask for

disclosures that go beyond IFRS S2 requirements. The CDP questionnaire and mapping table should

therefore not be taken as alternative text to the IFRS S2 or as modifying IFRS S2 requirements.

Compliance with IFRS S2 requires application of IFRS S1 General Requirements for Disclosure of

Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures in full. IFRS S1

includes the conceptual foundations and general requirements of the IFRS Sustainability Disclosures

Standards.

Page 22 of 29 @cdp | www.cdp.net

Task Force on Climate-related Financial Disclosures (TCFD)

Established by the Financial Stability Board, the TCFD has moved the climate disclosure agenda

forward by emphasizing the link between climate-related risk and financial stability. The Task Force

has recommended that both organizations and capital markets actors disclose information on climate

change. For example, this includes whether organizations are conducting scenario analysis in line with

a 1.5°C pathway and then setting out how climate-related issues affect their strategy and financial

planning.

This amplifies the longstanding call from CDP’s capital markets signatories for organizations to

disclose comprehensive, comparable environmental data in their mainstream reports, driving climate-

related risk management further into the boardroom. CDP’s climate change datapoints have been

aligned with the TCFD recommendations since 2018, prompting organizations to disclose data on how

climate-related issues are addressed in their governance, strategy, risk management, and metrics and

targets. Whilst TCFD adoption remains relevant across the global economy, the taskforce has

disbanded, and its responsibilities have folded into the IFRS Foundation from 2024.

Task Force on Nature-related Financial Disclosures (TNFD)

TNFD’s disclosure recommendations and LEAP framework represent the most comprehensive guide

for organizations looking to assess and respond to their full range of environmental interactions and

serves as an ambitious guide to best practice on environmental assessment and disclosure. In October

2023, CDP announced its intention to align with the TNFD framework. This will ensure that capital

markets actors, purchasers, and policymakers can access nature-related information in a consistent,

comparable, standardized format.

Incorporation of TNFD’s disclosure recommendations into CDP’s disclosure framework will occur in a

phased approach. CDP already has partial alignment – particularly where TNFD parallels the TCFD –

as the TNFD framework is rooted in the TCFD recommendations with which CDP is already aligned,

including datapoints on governance, strategy, risk, and opportunity disclosure.

European Sustainability Reporting Standards (ESRS)

The ESRS will be legally binding under the EU Corporate Sustainability Reporting Directive (CSRD). The

CSRD requires all large companies and all listed companies (with some exceptions) to disclose

information on ESG risks and opportunities, and on the impact of their activities. 50,000 companies are

in scope, including an estimated 10,000 non-EU companies; the applicability of the ESRS to companies’

entire value chains means this regulation will have a vast global reach.

CDP is assessing alignment of the CDP questionnaire with the ESRS from an environmental

perspective.

Accountability Framework initiative (AFi)

CDP is part of AFi’s collaborative effort to help companies fulfill commitments for responsible

agriculture and forestry supply chains. The Accountability Framework provides a set of principles and

guidelines designed to establish common definitions, norms, and best practices to help companies set,

implement, monitor, and report on ethical supply chain commitments as outlined in AFi’s “Core

Principles“ and “Common Methodology”.

CDP has been working in collaboration with AFi to ensure further alignment, so that organizations

disclosing to CDP will also be reporting on the core principles set out in the initiative.

Global Reporting Initiative (GRI)

CDP’s water security datapoints and reporting guidance cover some of the key requirements of

“GRI 303: Water and Effluents 2018”. Organizations using the GRI standards for their corporate

Page 23 of 29 @cdp | www.cdp.net

reporting will find it useful to refer to the “Framework Alignment” tags to see the linkages

between the information required for the GRI 303 standard and that requested for CDP’s

Corporate Questionnaire.

CDP is in the process of assessing the GRI standards with respect to CDP's climate change datapoints,

but the high degree of alignment between GRI 305 and IFRS S2 is likely to be well reflected in the CDP

questionnaire. The ongoing mapping of CDP's key transition plan indicators against GRI 2, GRI 201 and

the draft climate change exposure standard also indicates a high degree of alignment.

Ellen MacArthur Foundation Global Commitment

Launched in October 2018 by the Ellen MacArthur Foundation (EMF) and the UN Environment

Programme, the New Plastics Economy Global Commitment unites businesses, governments, and

other organizations from around the world behind a common vision of a circular economy for plastics,

in which it never becomes waste or pollution. EMF focuses on the production, commercialization and

usage of plastic packaging, which CDP largely captures through our plastics datapoints. CDP is

partnering with EMF to develop plastics datapoints that align with future developments of the EMF

Global Commitment, aiming to allow organizations in the near future to report against the Global

Commitment by disclosing to CDP's full corporate questionnaire.

Page 24 of 29 @cdp | www.cdp.net

Preparing your CDP response

In this section, you can find information on the support materials and options available to organizations,

as well as important notes for completing your disclosure. Review these notes carefully as you prepare

your response, even if you have responded to a CDP questionnaire in previous years.

CDP disclosure cycle 2024

For the latest information on the timeline, please refer to the CDP website.

16 April

CDP Portal opens for requesters

30 April

2024 questionnaires available via CDP website

14 May

CDP Portal opens for disclosers/Requesters can submit lists

4 June

2024 reporting window opens

18 September

Scoring deadline for corporate disclosers

2 October

2024 reporting window closes

CDP disclosure support materials

CDP provides a variety of support materials to help organizations disclosing to our questionnaires.

Before completing the full corporate questionnaire, we strongly recommend you read the Reporting

Guidance, Scoring Introduction, and Scoring Methodology. Also refer to CDP’s Technical Notes and

other guidance materials accessible from CDP’s guidance tool after signing in to the website, and see

the Frequently Asked Questions. If you have any questions that are not answered in the reporting

guidance and the additional resources noted below, please contact your local CDP contact or visit the

CDP Help Center.

Reporting guidance

The reporting guidance includes the following:

Module-level guidance: this guidance provides an overview of general and sector-specific content

for the module, as well as important disclosure notes.

Section-level guidance: for certain modules and sections, this guidance provides an overview of the

section’s content.

Question-level guidance: at the question level, guidance is separated into the following elements to

provide clarity around questions, terminology, and reporting requirements:

• Rationale: provides reasoning behind the inclusion of each question;

• Ambition: outlines the activities, actions, and behaviors that CDP recognizes

organizations should be taking and demonstrating through their disclosure;

• Connections to other frameworks: notes how each question links to relevant standards

and frameworks;

• Requested content: offers guidance on how to respond to the requested datapoints;

• Example responses: for certain questions, this provides an example of a response that

would include all information requested; and

• Explanation of terms: provides detailed definitions for specific terminology;

• Additional information: for certain questions, this provides further contextual information

and sources related to the topics pertinent to a given question.

Glossary: this contains a subset of ‘Explanation of terms’.

Webinars and workshops

CDP hosts live webinars and workshops designed to aid you with environmental reporting.

Visit the workshops and webinars pages of CDP's website for more details.

Page 25 of 29 @cdp | www.cdp.net

CDP Reporter Services

The CDP Reporter Services program offers tailored support, enhanced data access and thought

leadership on managing and reporting environmental risk to your business. Access the tools you need

to move from disclosure to leadership on integrating climate, forests management, and water security

into your wider business strategy. For year-round, personalized disclosure support from a dedicated

CDP account manager, a gap analysis of your previous response, final review before submission and

analytics tools to evaluate yourself against peers and understand best practice,

contact reporterservices@cdp.net.

Visit the Reporter Services page of CDP's website for more information.

CDP’s Accredited Solutions Providers

CDP partners with leading environmental service providers that can support organizations throughout

all stages of the measurement, reporting and management of their climate and sustainability data and

impacts. All CDP accredited solutions providers have met specific accreditation criteria. Providers’

expertise covers a wide range of environmental topics, including but not limited to renewable energy

procurement, sustainability strategy, verification, collection, monitoring, and reporting of sustainability,

CSR, and environmental data through integrated sustainability software applications, transition

planning and emissions reduction initiatives. CDP-accredited forests & land and water consultancy

solutions providers support organizations looking to engage with and improve their forest and land,

and water management.

Visit the accredited solutions provider directory to search for the provider best able to support you, or

contact partnerships@cdp.net to find out more.

Page 26 of 29 @cdp | www.cdp.net

Important notes for completing your CDP response

Personal data

It is important that you do not include the name of any individual or any other personal data in your

response. For questions that ask for the positions of staff, out of respect for personal data privacy we

are asking only for the position and not for the individual’s name or any other information relating to

them.

Principles of true and fair reporting

CDP promotes relevant widely accepted reporting principles as adopted by the Greenhouse Gas

Protocol to guide organization’s disclosure and to ensure a true and fair account of their environmental

data.

These principles are as follows:

• Relevance: Ensure the GHG emissions, commodity, and water use inventory appropriately

reflect actual emissions, commodity use, and water use, and serve the decision-making needs

of data users – both internal and external to the organization.

• Completeness: Account for and report on all GHG emission sources, water activities, and

activities with the potential for deforestation risk within the chosen inventory boundary.

Disclose and justify any specific exclusions.

• Consistency: Use consistent methodologies to allow for meaningful comparisons of an

organization’s environmental performance over time. Ensure there is no conflicting information

in your responses, both within a question and across the questionnaire.

• Transparency: Address all relevant issues in a factual and coherent manner, based on a clear

audit trail. Disclose any relevant assumptions and make appropriate references to the

accounting and calculation methodologies and data sources used. Transparently document

any changes to the data, inventory boundary, methods, or any other relevant factors in the time

series.

• Accuracy: Ensure the quantification of GHG emissions, commodity use, and water use is

sufficiently accurate to enable users to make decisions with reasonable assurance as to the

integrity of the reported information.

Information is considered relevant if it contains the detail that users, both internal and external to the

organization, need for their decision-making. When considering what to disclose, identify and report

information that is likely to be of use and benefit to the audience requesting it (in this case the capital

markets community and other data users).

Acronyms

Avoid using bespoke internal acronyms unless required for your organization’s response, in which case

you should provide their meaning to enable correct analysis and scoring.

Blank responses

Leaving a response blank is interpreted as non-disclosure. For numeric fields, values of zero (0) imply

a measurement has been made, and the value is zero (0).

For numeric fields where no measurement has been made, leave the field blank and provide an

explanation in an open text field for that same question, e.g. “Please explain” columns. If there is no

open text field for the question, you may provide an explanation in the 'Further information' field in the

CDP Portal at the end of your disclosure. See CDP’s 2024 Scoring Methodology for more details.

‘Comment’ columns

Some questions include a column labelled as “Comment”. Information provided in these columns will

not be scored.

Page 27 of 29 @cdp | www.cdp.net

Character limits

The character limits noted in the reporting guidance and in the CDP Portal include spaces.

Context and geographic scale

Environmental issues such as deforestation, water security, and biodiversity loss present significant

local challenges. Therefore, they need to be understood and managed at a local level rather than the

corporate level only. For example, it is good practice to consider dependencies, impacts, risks, and

opportunities at least at the country/area level, and specifically at the river basin level when it comes

to water-related issues.

Capital markets actors and other CDP data users are increasingly interested in this type of granularity

when it comes to assessing the nature-related issues within their portfolios. Specifically, data users

wish to assess an organization’s access to granular and location-specific data needed for a robust

assessment and management of nature-related issues across all its operations and locations.

Regarding water security in particular, CDP invites organizations to report their risks at the river basin

level and several questions include a column so that organizations can indicate the location associated

with their data. An organization will not have a comprehensive understanding of its risk exposure and

the most appropriate response unless it is able to take account of local basin context and conditions.

River basin level assessment is particularly relevant to a water stewardship approach to securing water

resources as collaboration with other basin users and external stakeholders is central to understanding

and managing risk.

Copy forward

The ‘copy forward’ functionality will be available in the CDP Portal for organizations that disclosed to

CDP in previous reporting years for certain datapoints. This functionality auto-populates your most

recent answers into your questionnaire where applicable.

Please review the auto-populated answers carefully. It is your responsibility to ensure your answers are

updated for the accuracy and completeness of your response.

Data accuracy

CDP recognizes that there may be uncertainty linked to data – this can arise from data gaps,

assumptions, metering/measurement constraints including equipment accuracy etc. CDP allows

estimated data to be submitted. However, an emphasis is placed on reporting transparently and this

means that an organization should always provide an explanation when its reported data is not accurate

and detail the uncertainty (use the “Please explain” or “Comment” columns provided in the question).

Drop-down options (“Other, please specify”')

Select from the options provided whenever possible, and only select “Other, please specify” when none

of the listed options is appropriate. This greatly assists data analysis. If selecting “Other, please

specify”, you must add a label that describes the option you are providing data for.

'Further information' field

At the end of the questionnaire, there is an opportunity to provide additional information or context that

you feel is relevant to your organization’s response. This field is optional and not scored.

Information specific to your organization

Some questions request information, rationales, case studies, and/or examples specific to the

reporting organization. This level of detail gives data users confidence that the issue at hand has been

thoroughly considered in the context of the responding organization’s own business and not simply

assessed in general terms.

Ensure that you include details specific to your organization, such as references to activities,

programs, products, services, methodologies, or operating locations unique to your

organization’s business or operations. Such explanations should include details that make the

answer true for the responding organization and are distinct from other organizations in the

same industry and/or geography.

Page 28 of 29 @cdp | www.cdp.net

Clear rationales are those which provide logical reasoning for methodologies, descriptions,

decision, and actions.

Case studies are defined as a detailed description of the implementation of a process, strategy,

or decision to a specific situation and/or task. When formulating case studies, responders may

find it helpful to consider a “Situation-Task-Action-Result” (STAR) approach: 1) Situation: what

was the context or background? 2) Task: what needed to be done or what was the problem to

be solved? 3) Action: what was the course of action taken? 4) Result: what was the final

outcome of the course of action?

An example does not need to follow the STAR approach. It can be shorter than a case study

but should include details that are specific to the reporting organization.

For more details, refer to the Scoring introduction on the CDP website.

Mergers and acquisitions (M&As)

All disclosure should be defined by the reporting boundary applicable at the time of the stated reporting

year. Note that for CDP disclosure, organizations are encouraged to align their reporting period and

reporting boundaries with their financial reporting.

Regarding forward-looking disclosure, organizations should include information that was correct at the

time of the stated reporting year (for example, for data points referring to the future or “the next two