Cost basis facts for stock plan participants 1

Don’t overpay your taxes. Learn more

about tax reporting and cost basis facts

for stock plans.

As a participant in your company’s stock plan program and/or employee stock purchase plan

(ESPP), it’s important that you understand the basics of tax reporting on these transactions to avoid

overpayment. You are responsible for accurate tax reporting to the IRS on the sale of all securities

when you le your tax return.

This document reviews all award types. Please click the links below to jump to specic sections that may pertain to your situation:

Cost basis basics >

Cost basis calculations >

Reporting on ISOs, NQs >

Reporting on ESPPs >

Reporting on RSAs, RSUs, PSAs, PSUs >

Cost basis resources >

Please carefully review the information in this document with your tax advisor. If you use TurboTax

®

or other tax software, note that

transactions in your Schwab Equity Award Center

®

account are separate from any other activity in your Schwab brokerage account.

Equity Award Center transactions will not be included in the download into the tax software and must be entered manually.

Why does cost basis matter for stock plan transactions?

Cost basis is used to compute capital gains and losses. You have to determine the correct cost basis on stock plan transactions in order

to accurately le your taxes and avoid being taxed twice on the income portion included in the W-2 your company sends you.

Cost basis for stock

plan transactions

Cost basis is the price paid to acquire shares plus commissions and any fees. Stock plans enable

employers to issue company stock for services rendered. Employers issue company stock as part of

compensation to their employees. As a result, ordinary income (compensation) may be earned as part

of the stock plan transaction.

Ordinary income and capital gains and losses are a factor in determining cost basis when shares

are sold.

The event that triggers the ordinary income varies and is dictated by tax law but can include grant,

vest, or exercise of the award, or purchase of ESPP shares and the subsequent sale or disposition of

those shares. Ordinary income is a factor in determining cost basis when stock plan shares are sold.

About the Internal Revenue Code

Since tax year 2015 regulations and moving forward, regulators have required brokers to report the

award price (i.e., the price at which the award was granted to you).

Brokers are not allowed to adjust the cost basis for shares for which ordinary income has already been

recognized. The responsibility to adjust now falls to you, the participant.

You may need to adjust your cost basis for ordinary income already recognized on Form 8949. We will

explain this in greater detail later in this document.

Cost basis facts for stock plan participants 2

Important items to consider

If you use TurboTax

®

or other tax software, transactions in your Schwab Equity Award Center

®

account cannot be automatically downloaded into the tax software and must be entered manually.

Keeping detailed records of transactions can help you manage your tax obligations. Schwab does not

provide tax advice. Consult a tax advisor to address your specic circumstances.

Depending on your employer’s relationship with Schwab, and the type of award, shares from equity

award transactions may be deposited into your Schwab One

®

brokerage account or directly into your

Equity Award Center account. If you have transactions in your Schwab One brokerage account, you

will receive a 1099 Composite. If you have transactions in your Equity Award Center account, you will

receive a Substitute Form 1099-B.

If you are using a tax software, when you indicate the type of equity award you sold, the software will

prompt you with additional questions to step-up the cost basis to reect ordinary income reported on

your W-2.

What is cost basis?

Original cost basis is the acquisition cost you paid for an investment, plus commissions and any fees.

Adjusted cost basis is the original cost basis plus any adjustments due to the following:

• Stock plan and ESPP transactions

• Corporate actions

• Wash sales

• Amortizations and accretions

• Standardized options

This fact sheet covers cost basis reporting for stock plan transactions and ESPP transactions.

Learn more about cost basis at schwab.com/costbasis by logging in to your account.

What are covered and non-covered securities?

For stock plan awards, covered securities include shares acquired on or after January 1, 2011:

• Upon the exercise of an incentive (ISO) or nonqualied (NQ) stock option

• Upon the purchase of shares through an employee stock purchase plan (ESPP)

Restricted stock units (RSUs), restricted stock awards (RSAs), performance stock units (PSUs), and

performance stock awards (PSAs) are typically non-covered.

For covered securities, Schwab reports cost basis to the IRS. For non-covered securities,

Schwab will not report cost basis to the IRS.

For stock plan participants with retail account transactions, Schwab will provide cost basis for covered

and non-covered securities, as available, on a Form 1099 Composite statement.

For ESPP participants, Schwab provides cost basis information on Substitute Form 1099-B.

Participants with multiple accounts will receive tax forms for each account. Tax forms are sent only if

you had a sale transaction in your account(s).

Cost basis facts for stock plan participants 3

Which values are used

to calculate the cost

basis of various stock

plan transactions?

Ultimately, you need to take into account taxable income and taxes already paid when determining

your nal cost basis. It is extremely important to understand how Schwab reports cost basis to the

IRS and the adjustments to make when completing your tax return.

Consult with a tax advisor to ensure proper reporting at tax time. For more information, log in to

Schwab.com and go to your Equity Awards account. On the Equity Award dashboard, navigate to

the section titled Knowledge Center and select the type of award you have received. Click on the

link to access in-depth premium content. A screen will pop up asking you to click to continue to

myStockOptions.com. The Tax Center will populate once you click the myStockOptions.com link.

The following table can be used as a guide to understand the cost basis price Schwab reports to

the IRS, the cost basis price Schwab provides on our tax reporting documents to you, and which

equity award types require an adjustment to the cost basis reported to the IRS to account for the

income portion.

Cost basis tax reporting by equity award type

Equity award type Cost basis price

Schwab is required to

report to the IRS

Cost basis price

Schwab provides

to participants on

1099-B portion of

tax document

Will I need to adjust

my cost basis on

Form 8949 to account

for ordinary income?

ESPPs: 423

Qualied Plan

Covered: purchase

price

Purchase price Yes, if ordinary income was

reported on your W-2; even if

no W-2 income was reported,

you must still report any

ordinary income.

Incentive Stock Options

(ISOs)

Covered: award price Award price Yes, for stock transactions after

1/1/2015 and if ordinary income

was reported on your W-2

Nonqualied Stock

Options (NQs)

Covered: award price Award price Yes, for stock transactions after

1/1/2015 and if ordinary income

was reported on your W-2

Restricted Stock Awards

(RSAs)

Non-covered: cost basis

not reported to IRS

FMV* You will not need to adjust your

cost basis, but you will need to

use Form 8949 to report cost

basis and the proceeds for these

transactions.

Restricted Stock

Units (RSUs)

Non-covered: cost basis

not reported to IRS

FMV* You will not need to adjust your

cost basis, but you will need to

use Form 8949 to report cost

basis and the proceeds for these

transactions.

Performance Stock

Awards (PSAs)

Non-covered: cost basis

not reported to IRS

FMV* You will not need to adjust your

cost basis, but you will need to

use Form 8949 to report cost

basis and the proceeds for these

transactions.

Performance Stock Units

(PSUs)

Non-covered: cost basis

not reported to IRS

FMV* You will not need to adjust your

cost basis, but you will need to

use Form 8949 to report cost

basis and the proceeds for these

transactions.

*Fair market value (FMV) is dened by the stock plan and/or award agreement and can vary across equity award types. Typically, it

is a value equal to the closing price or the average of the high and low stock prices of company common stock on the date of, or the

date prior to, the taxable event. If this value cannot be determined, the purchase price is typically used.

Cost basis facts for stock plan participants 4

Steps to complete

your taxes for ISOs

and NQs

Step 1: Gather your tax documents and forms.

You will need your 1099 Composite statement (Schwab One

®

brokerage account tax reporting

document) to complete your tax returns for stock plan transactions. In addition, you should review both

your Schwab One brokerage account and your Schwab Equity Awards account for tax information.

Step 2: Locate your cost basis information on your 1099 Composite form.

The information can be found within the 1099-B section and the Realized Gain or (Loss) section of

your 1099 Composite statement. The cost basis price reported to the IRS (i.e., the award price) can

be found under the 1099-B portion, and your adjusted cost basis price or fair market value (FMV)

can be found under the Realized Gain or (Loss) section. It is important to match transactions from

the 1099-B section to the Realized Gain or (Loss) section when completing Form 8949.

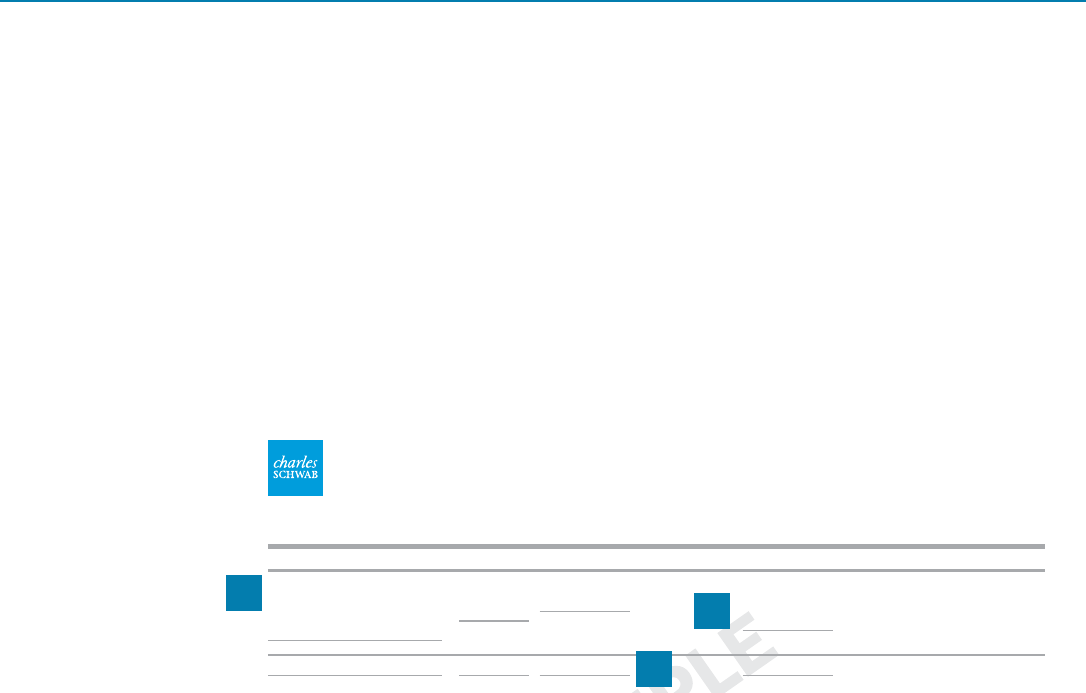

On the sample form below, Schwab has indicated the areas to refer to when completing Form 8949.

Note: Do not use the information in this example. This sample form is not a full 1099 Composite

statement, and Schwab has focused on the areas where stock plan transactions will be displayed

for demonstrative purposes only.

Sample of Form 1099-B

Page 14 of 55

Schwab One® Account of

DANA JONES

JOHN JONES

Account Number

1111-9999

TAX YEAR 2023

FORM 1099 COMPOSITE

Date Prepared: January 11, 2024

©2023 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Taxpayer ID Number: ***-**-0000

FATCA Filing Requirement

Please see the “Notes for Your Form 1099-B” section for additional explanation of this Form 1099-B report.

This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on

you if this income is taxable and the IRS determines that it has not been reported.

Proceeds From Broker Transactions—2023 (continued) Form 1099-B

Department of the Treasury–Internal Revenue Service Copy B for Recipient (OMB No. 1545-0715)

SHORT-TERM TRANSACTIONS FOR WHICH BASIS IS REPORTED TO THE IRS–Report on Form 8949, Part I, with Box A checked.

1a–Description of property

(Example–100sh. XYZ Co.)

CUSIP Number/Symbol **

1b–Date acquired

1c–Date

sold or

disposed

1d–Proceeds

6–Reported to IRS:

Gross proceeds

(except where

indicated)

1e–Cost or

other basis

1f–Accrued

Market Discount

1g–Wash Sale

Loss Disallowed

Realized

Gain or (Loss)

4–Federal income

tax withheld

5,952 SAMPLE CORP

30246XXXX/XXYY

S VARIOUS

04/01/23

$ 101,9 0 2.74

Net proceeds

$ 114,092.06 – –

– –

$ (12,189.32) $ 0.00

300

s

SAMPLE CORP

30246XXXX/XXYY

SS 10/11/23

10/11/23

$ 16,965.80 $ 18,062.05 – –

– –

$ (1,096.25) $ 0.00

Security Subtotal $ 118,868.54 $ 132,154.11 – –

– –

$ (13,285.57) $ 0.00

1,700 SAMPLE MUNI FUND

67062XXXX/ABCXX

S 09/14/23

11/11/23

$ 23,604.95 $ 22,379.62 – –

– –

$ 1,225.33 $ 0.00

Security Subtotal $ 23,604.95 $ 22,379.62 – –

– –

$ 1,225.33 $ 0.00

1,000 CONTINGENT PAYMENT BOND

99999XXXX

S 01/10/23

06/10/23

$ 1,000.00 $ 1,000.00 – –

– –

$ 0.00 $ 0.00

2–Ordinary

X

Security Subtotal $ 1,000.00 $ 1,000.00 – –

– –

$ 0.00 $ 0.00

Total Short-Term (Cost basis is reported to the IRS) $ 152,826.24 $ 165,658.73 $ 200.00

– –

$ (13,032.49) $ 0.00

Section A indicates whether the cost basis for the transaction was reported to the IRS and if the

transaction is a short-term or long-term transaction.

Section B indicates sales proceeds reported to the IRS (proceeds from the transaction,

minus commissions).

Section C indicates cost basis reported to the IRS.

A

B

C

Cost basis facts for stock plan participants 5

Sample of Realized Gain or (Loss) section:

The Realized Gain or (Loss) section of the 1099 Composite statement will contain the FMV you’ll use

on Form 8949 to adjust the cost basis. The adjusted cost basis will include the income portion. This

is extremely important, as the tax on the income portion will be included on your W-2. In the

example form below, Schwab has indicated important areas you’ll need to refer to when completing

your taxes.

Page 36 of 55

Schwab One® Account of

DANA JONES

JOHN JONES

Account Number

1111-9999

TAX YEAR 2023

YEAR-END SUMMARY

Date Prepared: January 11, 2024

©2023 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Please see the “Endnotes for Your Realized Gain or (Loss)” for an explanation of the codes and symbols in this Realized Gain or (Loss) section.

YEAR-END SUMMARY INFORMATION IS NOT PROVIDED TO THE IRS.

The information in this and all subsequent sections is not provided to the IRS by Charles Schwab. It is provided to you as additional tax reporting information you may need to complete your tax return.

Long-Term Realized Gain or (Loss) (continued)

The transactions in this section are not reported on Form 1099-B or to the IRS. Report on Form 8949, Part II, with Box F checked.

Description OR

Option Symbol

CUSIP

Number Quantity/Par

Date

Acquired

Date

Sold Total Proceeds

(–) Cost Basis

Adjusted

(+) Wash Sale

Loss Disallowed

(–) Market Discount

(=) Realized

Gain or (Loss)

Adjusted

SAMPLE COMMON STOCK 03759XXXX 0.25 01/21/21 11/28/22 $ 13.60 $ 12.16 $ 0.00 $ 1.44

Security Subtotal $ 13.60 $ 12.16 $ 0.00 $ 1.44

Total Long-Term (Transactions are not reported on Form 1099-B or to the IRS) $ 13.60 $ 12.16 $ 0.00 $ 1.44

Total Long-Term $ 18,385.15 $

$

18,747.11

18,192.11

i

i

$

$

142.38

0.00

$

$

(1,219.58)

(644.98)

i

bi

Section D indicates the stock option symbol or description.

Section E indicates the adjusted cost basis price (FMV) you will use on Form 8949.

Step 3: Complete your IRS tax forms.

Sample of Form 8949

Please follow the IRS instructions for completing Form 8949 to adjust the cost basis on covered

securities, and then complete Schedule D with the totals from Form 8949.

Form

8949

Department of the Treasury

Internal Revenue Service

Sales and Other Dispositions of Capital Assets

Go to www.irs.gov/Form8949 for instructions and the latest information.

File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2023

Attachment

Sequence No.

12A

Name(s) shown on return Social security number or taxpayer identication number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute

statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported to the IRS by your

broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are generally short-term (see

instructions). For long-term transactions, see page 2.

Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was

reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on

Schedule D, line 1a; you aren’t required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions,

complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will t on this page

for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)

(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn’t reported to the IRS

(C) Short-term transactions not reported to you on Form 1099-B

1

(a)

Description of property

(Example: 100 sh. XYZ Co.)

(b)

Date acquired

(Mo., day, yr.)

(c)

Date sold or

disposed of

(Mo., day, yr.)

(d)

Proceeds

(sales price)

(see instructions)

(e)

Cost or other basis

See the Note below

and see Column (e)

in the separate

instructions.

Adjustment, if any, to gain or loss

If you enter an amount in column (g),

enter a code in column (f).

See the separate instructions.

(f)

Code(s) from

instructions

(g)

Amount of

adjustment

(h)

Gain or (loss)

Subtract column (e)

from column (d) and

combine the result

with column (g).

2

Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract

negative amounts). Enter each total here and include on your

Schedule D, line 1b (if Box A above is checked), line 2 (if Box B

above is checked), or line 3 (if Box C above is checked) . .

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an

adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to gure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions.

Cat. No. 37768Z

Form

8949 (2023)

D

E

Cost basis facts for stock plan participants 6

Steps to complete your

taxes for ESPPs

Employee Stock Purchase Plan (ESPP).

ESPP shares are covered securities as dened by the IRS. Schwab is required to report the purchase

price as the cost basis on ESPP sales; Schwab does not adjust the cost basis price to account for

income that may be reported on the W-2.

ESPPs are complicated. We recommend you work closely with a tax advisor to accurately report

ESPP sales on your tax returns.

Does the cost basis for disqualied and qualied dispositions need to be updated on

Form 8949?

Potentially. Different tax treatments may apply on disqualied and qualied dispositions. We

recommend that you work closely with a tax advisor to assist in completing your tax returns.

How do I know if I have a disqualied or a qualied disposition?

• Disqualied disposition: The sale of ESPP shares within one year of the purchase date and/or

within two years from the grant date (offering date)

• Qualied disposition: The sale of ESPP shares after one year of the purchase date and after two

years of the grant date (offering date)

Step 1: Gather your tax documents and forms.

• Substitute Form 1099-B: ESPP shares are deposited to your Schwab Equity Award Center

®

(EAC) account.

• Form 3922: You may receive this form from your employer, Schwab, or a third party for the year

of purchase.

Tax information is also accessible within your Equity Awards account. To access the Schwab Equity

Award Center, log in to Schwab.com and select your Equity Awards account, and then select History

(for transaction history), or View Equity Details (for current positions).

Step 2: Locate your cost basis information on your Substitute Form 1099-B.

The cost basis will be under the column for Box 1e.

Name:

Name

Recipient Information

Address Line 1

Address Line 2

Taxpayer ID No:

Account Number:

Address:

XXX-XX-XXXX

12345

Federal ID No:

94-1737782

Name:

Address:

Payer Information

(800) 654-2593

STOCK PLAN SVCS

9875 SCHWAB WAY

LONE TREE, CO 80124

CHARLES SCHWAB & CO., INC

Phone #:

Proceeds from Broker Transactions

Department of the Treasury - Internal Revenue Service

(OMB No. 1545-0715)

2

Page

1

of

Box 1a: Description of

property

CUSIP Box 1b: Date

acquired

Box 1d: Proceeds Box 1e: Cost or

other basis

Box 1g: Wash

sale loss

disallowed

Box 5: Noncovered

security

Box 4: Federal

income tax

withheld

Box 14: State name

Box 7: Loss is

not allowed

based on

amount in 1d

Box 1c: Date

sold or

disposed

Box 6: Reported to

IRS: Gross Proceeds

or Net Proceeds

Box 16: State

tax withheld

Box 15: State

identification no.

Box 1f: Accrued

market discount

Box 12: Proceeds

from collectibles

Ordinary

Short-term transaction for which basis is not reported to the IRS; report on Form 8949, Part I, with Box B checked.

1111111

31.0 SHARES OF T EST

3/16/2023

970.11 926.10 X

3/22/2023

GROSS

Copy B for Recipient

1099-B

TAX YEAR: 2023

Step 3: Complete your IRS tax forms.

When reporting the sale of ESPP shares to the IRS, you will complete the following:

• Form 8949: List the details of each ESPP sale on this form. You may need to adjust your cost basis

by completing either the short-term or the long-term section, depending on your particular tax

situation.

• Form Schedule D: List the totals from Form 8949. Enter the totals under either the long-term or

short-term areas of Schedule D.

Cost basis facts for stock plan participants 7

Important wash sales

information

You may notice some changes regarding adjustments on your cost basis related to wash sales. Starting

January 1, 2018, Schwab will no longer be adjusting your transactions to reect wash sales. Any

adjustments made prior to January 1, 2018, will still be provided to you for your reference on your

1099, but beginning January 1, 2018, we will no longer adjust any lots for future wash sales. Please

work with your tax advisor or call our Participant Services for more information on what wash sales

mean for you.

Steps to complete your

taxes for RSAs, RSUs,

PSAs, and PSUs

Note: Schwab will NOT report the cost basis information to the IRS. Schwab provides this information

to you on your copy of your tax form. You are responsible for reporting the cost basis for the sale to the

IRS on Form 8949 and Schedule D. The cost basis is NOT included on the copy Schwab submits to

the IRS.

Step 1: Gather your tax documents and forms.

Depending on your employer’s relationship with Schwab, shares from restricted/performance stock

that has vested may be deposited into your Schwab One

®

brokerage account or directly to your Schwab

Equity Award Center

®

account. You will receive a separate Substitute Form 1099-B for transactions in

your Schwab Equity Award Center account.

You will need your 1099 Composite statement (Schwab One brokerage account tax reporting

document) or your Substitute 1099 statement (if your restricted stock shares are sold from your

EAC account) to complete your tax returns for stock plan transactions.

Step 2: Locate your cost basis information on your Schwab tax form(s).

This information can be found within the 1099-B section of your 1099 Composite statement. For

non-covered securities, the information will be available under the area of the 1099-B that is not

reported to the IRS.

In the sample form below, Schwab has indicated the areas to refer to when completing Form 8949.

Note: Do not use the information in this example. This sample form is not a full 1099 Composite

statement, and Schwab has focused on the areas where stock plan transactions will be displayed

for demonstrative purposes only.

Sample of Form 1099-B

Page 14 of 55

Schwab One® Account of

DANA JONES

JOHN JONES

Account Number

1111-9999

TAX YEAR 2023

FORM 1099 COMPOSITE

Date Prepared: January 11, 2024

©2023 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Taxpayer ID Number: ***-**-0000

FATCA Filing Requirement

Please see the “Notes for Your Form 1099-B” section for additional explanation of this Form 1099-B report.

This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on

you if this income is taxable and the IRS determines that it has not been reported.

Proceeds From Broker Transactions—2023 (continued) Form 1099-B

Department of the Treasury–Internal Revenue Service Copy B for Recipient (OMB No. 1545-0715)

SHORT-TERM TRANSACTIONS FOR WHICH BASIS IS REPORTED TO THE IRS–Report on Form 8949, Part I, with Box A checked.

1a–Description of property

(Example–100sh. XYZ Co.)

CUSIP Number/Symbol **

1b–Date acquired

1c–Date

sold or

disposed

1d–Proceeds

6–Reported to IRS:

Gross proceeds

(except where

indicated)

1e–Cost or

other basis

1f–Accrued

Market Discount

1g–Wash Sale

Loss Disallowed

Realized

Gain or (Loss)

4–Federal income

tax withheld

5,952 SAMPLE CORP

30246XXXX/XXYY

S VARIOUS

04/01/23

$ 101,90 2 .74

Net proceeds

$ 114,092.06 – –

– –

$ (12,189.32) $ 0.00

300

s

SAMPLE CORP

30246XXXX/XXYY

SS 10/11/23

10/11/23

$ 16,965.80 $ 18,062.05 – –

– –

$ (1,096.25) $ 0.00

Security Subtotal $ 118,868.54 $ 132,154.11 – –

– –

$ (13,285.57) $ 0.00

1,700 SAMPLE MUNI FUND

67062XXXX/ABCXX

S 09/14/23

11/11/23

$ 23,604.95 $ 22,379.62 – –

– –

$ 1,225.33 $ 0.00

Security Subtotal $ 23,604.95 $ 22,379.62 – –

– –

$ 1,225.33 $ 0.00

1,000 CONTINGENT PAYMENT BOND

99999XXXX

S 01/10/23

06/10/23

$ 1,000.00 $ 1,000.00 – –

– –

$ 0.00 $ 0.00

2–Ordinary

X

Security Subtotal $ 1,000.00 $ 1,000.00 – –

– –

$ 0.00 $ 0.00

Total Short-Term (Cost basis is reported to the IRS) $ 152,826.24 $ 165,658.73 $ 200.00

– –

$ (13,032.49) $ 0.00

Section A indicates whether the cost basis for the transaction was reported to the IRS and if the

transaction is a short-term or long-term transaction.

Section B indicates sales proceeds reported to the IRS (proceeds from the transaction, minus commissions).

Section C indicates the cost basis (FMV) you’ll use when completing Form 8949. This price was not

reported to the IRS and includes the income portion on your W-2.

Step 3: Complete your IRS tax forms.

When reporting the sale of stock awards to the IRS, you will complete the following:

• Form 8949: List the details of each stock award sale on this form.

• Form Schedule D: List the totals from Form 8949. Enter the totals under either the long-term or

short-term areas of Schedule D.

A

B

C

Sample of Form 8949

Please follow the IRS instructions for completing Form 8949 to adjust the cost basis on non-covered

securities, and then complete Schedule D with the totals from Form 8949.

Form 8949

Department of the Treasury

Internal Revenue Service

Sales and Other Dispositions of Capital Assets

Go to www.irs.gov/Form8949 for instructions and the latest information.

File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2023

Attachment

Sequence No.

12A

Name(s) shown on return Social security number or taxpayer identication number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute

statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported t

o the IRS by your

broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are generally short-term (see

instructions). For long-term transactions, see page 2.

Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was

reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on

Schedule D, line 1a; you aren’t required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions,

complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will t on this page

for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)

(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn’t reported to the IRS

(C) Short-term transactions not reported to you on Form 1099-B

1

(a)

Description of property

(Example: 100 sh. XYZ Co.)

(b)

Date acquired

(Mo., day, yr.)

(c)

Date sold or

disposed of

(Mo., day, yr.)

(d)

Proceeds

(sales price)

(see instructions)

(e)

Cost or other basis

See the Note below

and see Column (e)

in the separate

instructions.

Adjustment, if any, to gain or loss

If you enter an amount in column (g),

enter a code in column (f).

See the separate instructions.

(f)

Code(s) from

instructions

(g)

Amount of

adjustment

(h)

Gain or (loss)

Subtract column (e)

from column (d) and

combine the result

with column (g).

2

Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract

negative amounts). Enter each total here and include on your

Schedule D, line 1b (if Box A above is checked), line 2 (if Box B

above is checked), or line 3 (if Box C above is checked) . .

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an

adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to gure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions.

Cat. No. 37768Z

Form

8949 (2023)

Important items to consider

when completing your taxes

Stock plan transactions for covered securities that resulted in long shares (cash purchase or

sell-to-cover) prior to January 1, 2015, will have an adjusted price used for the cost basis. In

most cases, the cost basis price reported to the IRS will not need to be adjusted.

If cost basis information for stock plan transactions is missing, you can update this information online.

Please take one of the following actions:

• Log in to your Schwab One

®

brokerage account and navigate to the Positions tab. From there,

review the cost basis column. If the word “Missing” appears under this column, you can click it to

update the cost basis information.

• Call Schwab at 1-800-654-2593 to speak with a representative who can walk you through the

steps above.

In some cases, Schwab may not have the cost basis information needed to update the missing

information. Please ensure that you have your cost basis information ready before you call in.

How to view cost basis

information online

From within the Schwab Equity Award Center

®

.

You can view cost basis information online by accessing the Schwab Equity Award Center. Log

in to Schwab.com and select Equity Awards under Accounts. Select View Equity Details

under the Equity Today section (for current positions) or History under the top navigation bar

(for transaction history).

Information used to report cost basis for stock plan and ESPP transactions (such as cost and taxable

compensation) is reected on stock plan activity statements, which are mailed to participants and are

also available online via the Schwab Equity Award Center.

From within a Schwab One brokerage account.

You can view cost basis information (adjusted cost basis) in the History section of your

Schwab One account. Unrealized gain/loss information can be viewed in the Positions section.

Resources

For questions regarding your equity awards, please contact Schwab Stock Plan Services

at 1-800-654-2593.

To learn more about cost basis for non–stock plan awards held at Schwab, visit schwab.com/costbasis,

by logging in to your account.

For general information about stock plan awards, including a glossary of common terms, log in

to Schwab.com and go to your Equity Awards account. On the Equity Award dashboard, navigate

to the section titled Knowledge Center and select the type of award you have received. Click on

the link to access in-depth premium content. A screen will pop up asking you to click to continue to

myStockOptions.com. The Tax Center will populate once you click the myStockOptions.com link.

Stock Plan Services provides equity compensation plan services and other nancial services to corporations and employees through Charles Schwab & Co., Inc. (“Schwab”).

Schwab, a registered broker dealer, offers brokerage and custody services to its customers.

MyStockOptions is not afliated with Charles Schwab & Co., Inc. or its afliates. Schwab is not responsible for the content on their website and does not provide, edit, or

endorse any of the content. MyStockOptions is wholly responsible for the content and features found on their site.

This information is for educational purposes only and is not intended to be a substitute for specic individualized tax, legal, or investment planning advice. Where specic

advice is necessary or appropriate, you should consult with a qualied tax advisor, CPA, Financial Planner, or Investment Manager.

©2024 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

CC7723200 (0224-G1LH) MKT123180OTH-00 (02/24)