1 | P a g e

Contract Costing

PRACTICAL QUESTION WILL APPEAR FROM THIS TOPIC. 100% CHANCES.

Students can call me at 8860828731 for any query at the time of lecture. I will be available at that

time.

2 | P a g e

Day - 1

3 | P a g e

Introduction to Contract Costing

There are two parties in a contract: Contractor and the Contractee. Contractee is the person who

grants the contract to the contractor and contractor is the person who executes the contract.

4 | P a g e

One more party is there called certifier/evaluator/engineer. Now what is the role of the certifier/

evaluator/engineer? Actually, contractee gives money to the contractor on the basis of the work

completed. Suppose, contract price is Rs. 10,00,000 and contractor says to the contractee that 40%

work is completed and give me Rs. 4,00,000 i.e. 40% of the contract price. Now, what if the work

completed is not 40% or if the work completed is 40%? In such a case after taking money the

contractor may leave the work in between. Now the certifier/evaluator/engineer (from the side of the

contractee) comes in the picture. Contractee sends the certifier/evaluator/engineer to the site and

certifier/evaluator/engineer gives a certificate for the completed work. On the basis of this certificate

only the contractee gives money to the contractor. Also, the contractee does not give the full money to

the contractor, because if he does so, then contractor may leave the work in between. So the

contractee retains some money which is called the Retention Money. Now, if the

certifier/evaluator/engineer gives a certificate of 25% work completed then the value of the work

certified will be Rs. 2,50,000 (Rs. 10,00,000 25%). Now the contractor is eligible to get Rs. 2,50,000.

But the contractee gives only Rs. 2,00,000 to the contractor, then Rs. 50,000 will be the retention

money. This retention money is the 20% of the work certified (Rs. 50,000 / 2,50,000 100). Any work

which is completed but not certified by the certifier/evaluator/engineer is called the work not

certified. Also the expenses incurred after obtaining the certificate for the completion of work will

form part of the work not certified.

In order to prepare the contract account, first of all learn/cram the format of the contract account.

It’s like a mini profit and loss account. Its prepared on the basis of two principles—debit what

comes in and credit what goes out, and debit all expenses and losses and credit all incomes and gains.

Further, while preparing the contract account one must keep in mind the principle of normality

also. All the abnormal losses and abnormal incomes shall be excluded from the contract account. For

example, if there is any loss on sales of plant/machinery/material then obviously it’s already

included/debited in/to the contract account, so the amount of such loss shall be credited to the

contract account. Likewise, if there is any profit on sales of plant/machinery/material then obviously

it’s already included/credited in/to the contract account so the amount of such loss shall be debited to

the contract account.

In case of expenses are being incurred then such expenses shall be debited to the contract account

on accrual basis. Outstanding expenses shall be added to the concerned expense and prepaid expenses

shall be subtracted.

In case of material is being used for the contract then such amount shall be debited. In case of

outgoing material the amount shall be credited using the principle of real accounts. At the time of

completion of the contract material is returned to the stores and it’s written on the credit side.

Sometimes the material consumed is calculated (or given) in the question, then such material

5 | P a g e

consumed shall be debited. In such a case all other transactions related to the material are not be

recorded in the contract account. Even profit/loss on sales of material or loss due to fire, rain, theft,

etc. are not be recorded.

Note: Material Consumed = Opening Material + Material Purchased + Material Received from

Stores + Material Transferred from Other Contracts – Material Returned to Stores – Material

Sold (Cost) – Material Transferred to Other Contracts – Material in Hand or Material at Site

In case of plant and machinery is being used for the contract then cost of this shall be debited. In

case of outgoing plant and machinery the amount is to be credited using the principle of real accounts.

Record cost of the plant on the debit side and WDV (cost less depreciation) on the credit side. All the

outgoing plant and machineries shall be credited with the WDV i.e. cost less depreciation.

If the rate of depreciation is given per annum, then depreciation shall be calculated on the basis of

time but if per annum is not mentioned with the rate then depreciation shall be calculated for whole of

the year ignoring the time factor even though the plant was used for less than a year.

At the time of completion of the contract we return the plant to the stores and it’s WDV (cost less

depreciation) is recorded on the credit side.

There is another method under which we do not record the cost on the debit side and WDV on the

credit side. In this method we only record the depreciation of the plant on the debit side. The

depreciation of all the plants (whether outgoing or balance of the plant at the end of the year) shall be

recorded on the debit side. In this method all other transactions related to the plant are not recorded

in the contract account. Even profit/loss on sales of plant or loss due to fire, rain, theft, etc. is not

recorded.

In case of the completion of the contract we write down the contract price on the credit side of the

contract account and the journal is:

Contractee Account Dr. -----

To Contract Account -----

Note: We do not record the Work Certified or Work Not Certified in the year of completion on

the credit side.

In case of the completion of the contract, if the debit side is more than the credit side, then loss will

be there on the contract and the journal is:

Profit and Loss Account Dr. -----

To Contract Account -----

In case of the completion of the contract, if the credit side is more than the debit side then profit

will be there on the contract and the journal entry is:

Contract Account Dr. -----

6 | P a g e

To Profit and Loss Account -----

In case the contract is incomplete then:

1. First of all write down the amount of the Work Certified and Work Not Certified under the

heading Work-in-Progress (see the format) on the credit side of the contract account (as given

in the format).

2. If debit side is more than the credit side, then loss will be there and such loss shall be credited

to the contract account. Journal entry is:

Profit and Loss Account Dr. -----

To Contract Account -----

3. If credit side is more than the debit side, then profit is there. But this total profit cannot be

assumed actual profit because the contract is incomplete. Such profit is called Notional Profit

and then bifurcated in to two parts. One part is transferred to the profit and loss account (How

much amount shall be transferred to the profit and loss account? There are certain rules for

this and discussed below the format of the contract account) and the remaining part is

transferred to the work in progress account (also called reserve). Why to take only a part of the

Notional Profit to the profit and loss account? It’s because of the Principle of the Conservatism

or Principle of Prudence. However, the true profit can be calculated only at the completion of

the contract. But if we calculate the profit only at the completion of the contract then for a

company engaged in the business of taking contracts, profits will be very high in the year in

which too many contracts are being completed and profits may be very low or sometime NIL in

the year in which a few contracts are being completed or no contracts are being completed.

Thus the calculation of the profit only at the time of completion of the contract puts the uneven

burden on the profit and loss account. By calculating notional profit and then bifurcation of it in

two parts puts the even burden on the profit and loss account and also helps the contractor to

follow the principle of conservatism/prudence.

7 | P a g e

Day - 2

8 | P a g e

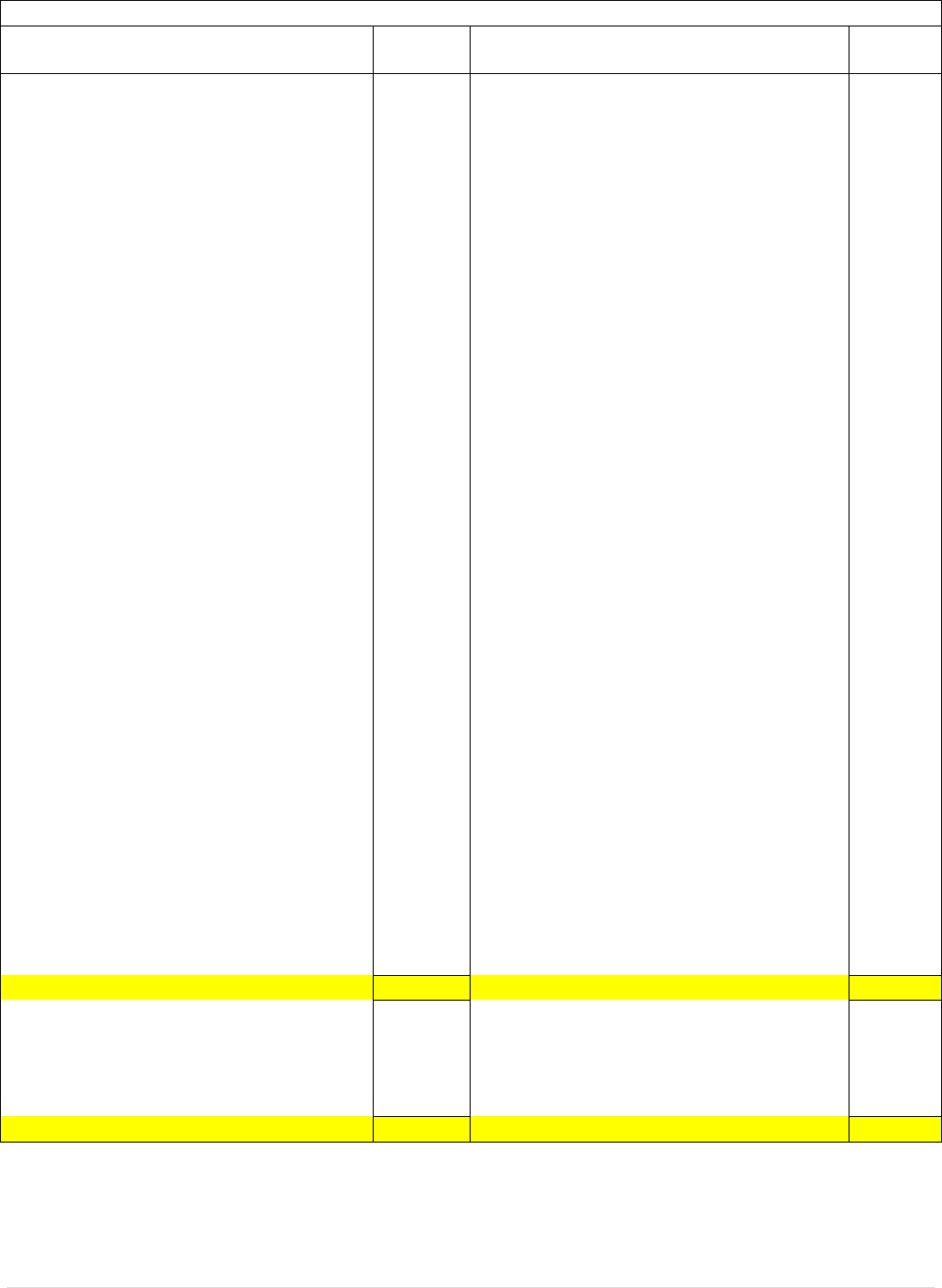

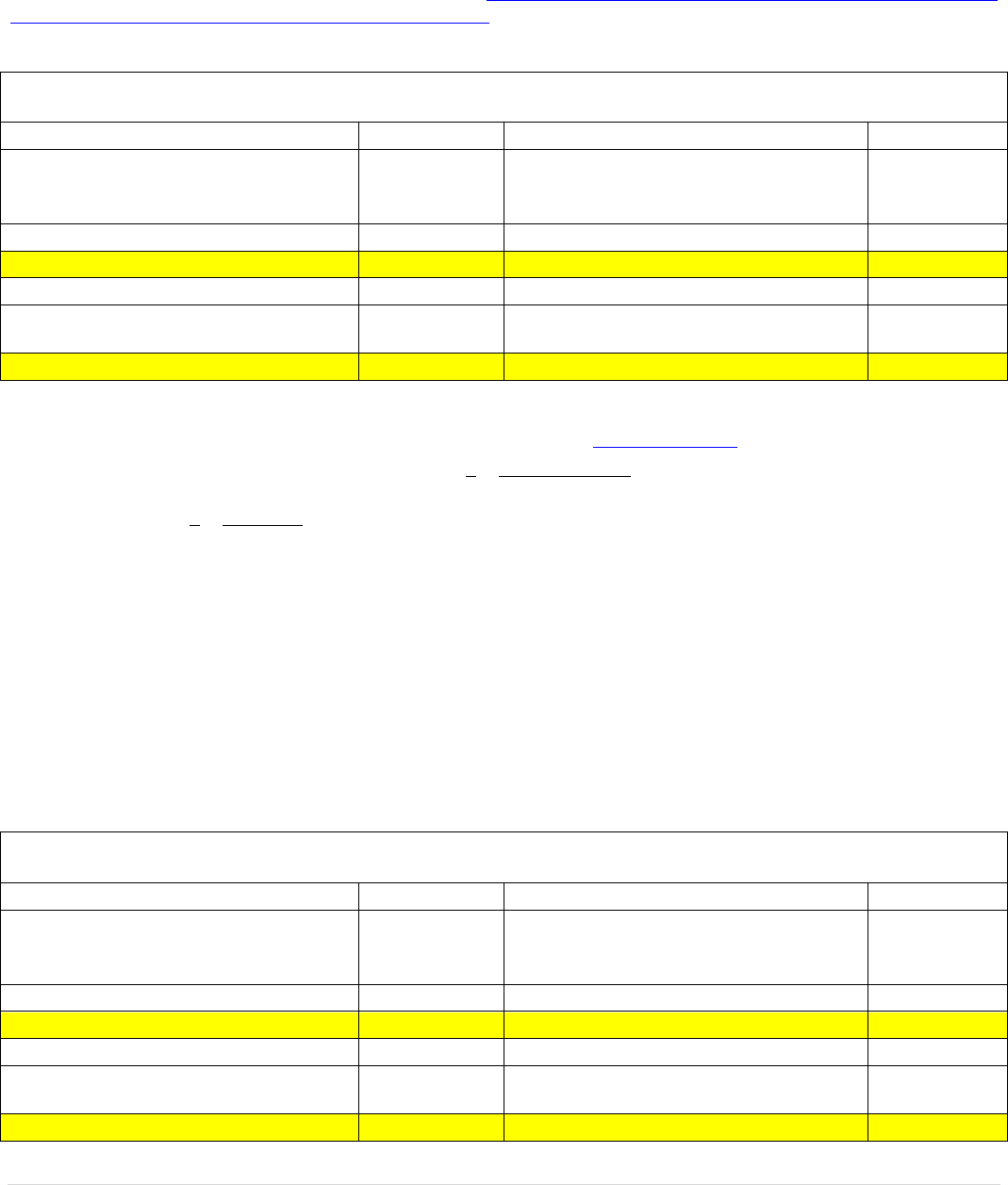

Format of the Contract Account

Performa Contract Account

Particulars

Amount

Rs.

Particulars

Amount

Rs.

To material issued from store

––––

By material at site

––––

To material purchased

––––

By material returned to store

––––

To material transferred from other contracts

––––

By material transferred to other contracts

––––

To material consumed (if given, and in this

case all other items related to material shall be

ignored)

––––

By profit and loss account:

Material/Plant stolen –––

Material/Plant lost due to unforeseen reasons

eg. fire, rain, etc. –––

Loss on sales of material/plant –––

––––

To labour –––

Add: Outstanding labour (–––)

––––

By plant at site (Cost) –––

Less: Depreciation (–––)

––––

To plant issued

To plant purchased

––––

––––

By plant returned to store (Cost) –––

Less: Depreciation (–––)

––––

To plant transferred from other contracts

––––

By plant transferred to other contracts (Cost)

–––

Less: Depreciation (–––)

––––

To sub contract cost

––––

By material/plant sold

––––

To cost of extra work done

To site expenses

––––

––––

By work in progress(In case contract is

incomplete) :

Work certified –––

Work not certified –––

––––

To direct expenses –––

Add: Outstanding expenses (–––)

––––

By CONTRACTEE ACCOUNT (by the amount of

contract price on the completion of contract)

––––

To indirect expenses/overheads –––

Add: Outstanding expenses (–––)

––––

By profit and loss account (if there is loss on

contract either before completion or after

completion)

––––

To profit and loss account:

(Profit on sales of material/plant)

––––

To Contract escalation (Decrease in CP)

––––

By Contract escalation (Increase in CP)

––––

To profit and loss account (if contract is

completed and profit is there)

––––

To profit and loss account (if contract is

completed and loss is there)

––––

To notional profit c/d (if work certified is more

than 25% of the contract price but less than

90% of the contract price)

––––

Total

****

Total

****

To profit and loss account (part of notional

profit if the contract is not completed)*

––––

By notional profit b/d

––––

To work in progress (transferred to reserve

only when the contract is not completed)

––––

Total

****

Total

****

9 | P a g e

Explanation to all the items of the contract account

1. Material

To material issued from store: Any material issued from the store shall be debited to the contract

account because it’s an expense. Apply the principle—Debit all expenses and losses. Further, you can

also apply the principle—Debit what comes in.

To material purchased: Any material purchased shall be debited to the contract account because it’s

an expense. Further, you can also apply the principle—Debit what comes in.

To material transferred from other contracts: Any material transferred from any other contract

shall be debited to the contract account because it’s an expense for this contract. Apply the principle—

Debit all expenses. Further, you can also apply the principle—Debit what comes in.

To material consumed (if given/calculated, then in this case all other items related to material

shall be ignored): Sometimes the material consumed is calculated in the question, then, such

material consumed shall be recorded on the debit side. In such a case all other transactions related to

the material shall not be recorded in the contract account. Even profit/loss on sales of material or loss

due to fire, rain, theft, etc. shall not be recorded.

Note: Material Consumed = Opening Material + Material Purchased + Material Received from

Stores + Material Transferred from Other Contracts – Material Returned to Stores – Material

Sold (Cost) – Material Transferred to Other Contracts – Material in Hand or Material at Site

By material at site: This is the unused material so it shall be credited to the contract account. Apply

the principle—Credit what goes out. We write “By material at site” when the contract is not

completed. In case the contract is competed then we write “By material returned to stores”.

By material returned to store/supplier: This is the unused material so it is returned to the

store/supplier. It shall be credited to the contract account. Apply the principle—Credit what goes out.

Sometimes it’s specifically mentioned that the material is returned though the contract is not

completed, in such a case write “By material returned to store”.

By material transferred to other contracts: If any other contract(s) is/are running short of material

then the material can be transferred to that other contract(s). Because this material is not used for

this contract so we credit this to the contract account and apply the principle—Credit what goes out.

By profit and loss account (Material stolen, Material lost due to unforeseen reasons eg. fire,

rain, etc., Loss on sales of material): The above losses are abnormal in nature. Further, while

preparing the contract account one must keep in mind the principle of normality also, so all the

abnormal losses shall be excluded from the contract account. Credit all these losses and the journal

entry is:

10 | P a g e

Profit and Loss Account Dr. -----

To Contract Account -----

By material sold: Sometimes the material is sold because it’s of no use or not up to the specifications,

etc. Credit the amount of this because this will reduce the cost of the material or we can also say that

it’s outgoing in nature so credit it. Apply the principle—Credit what goes out.

2. To Labour/Wages

It’s an expense so it’s shall be debited to the contract account by applying the principle—Debit all

expenses. Any outstanding amount shall be added and any prepaid amount shall be subtracted.

3. To Plant and Machinery

To plant issued: Cost of any plant issued from the store shall be debited to the contract account

because it’s an expense. Apply the principle—Debit what comes in.

To plant purchased: Cost of any plant purchased shall be debited to the contract account because it’s

an expense. Apply the principle—Debit what comes in.

To Plant transferred from other contracts: Any plant transferred from any other contract shall be

debited to the contract account because it’s an expense for this contract. Apply the principle—Debit

what comes in.

By profit and loss account (Plant stolen, Plant lost due to unforeseen reasons eg. fire, rain, etc.,

Loss on sales of plant): The above losses are abnormal in nature. Further, while preparing the

contract account one must keep in mind the principle of normality also, so all the abnormal losses

shall be excluded from the contract account. Credit all these losses and the journal entry would be:

Profit and Loss Account Dr. -----

To Contract Account -----

By plant at site: This is the remaining plant so it shall be credited to the contract account. Apply the

principle—Credit what goes out. We write “By plant at site” when the contract is not completed. But

it must be noted that only WDV i.e. (Cost – Depreciation) shall be recorded.

By plant returned to store: This is the remaining plant and if not intended for further use then it can

be returned to the store. So it shall be credited to the contract account. Apply the principle—Credit

what goes out. But it must be noted that only WDV i.e. (Cost – Depreciation) shall be recorded.

By plant transferred to other contracts: If any other contract(s) is/are running short of plant then

the plant can be transferred to that other contract(s). Because this plant is not used for this contract

so we credit this to the contract account and apply the principle—Credit what goes out. But it must be

noted that only WDV i.e. (Cost – Depreciation) shall be recorded.

11 | P a g e

By plant sold: Sometimes the plant is sold because it’s of no use or not up to the specifications, etc.

Credit the amount of this because this will reduce the cost of the plant or we can also say that it’s

outgoing in nature so credit it. Apply the principle—Credit what goes out.

Rate of depreciation is important: If the rate of depreciation is given per annum, then depreciation

shall be calculated on the basis of time but if per annum is not mentioned then depreciation shall be

calculated for whole of the year ignoring the time factor even though the plant was used for less than a

year.

In all the cases whenever we are crediting the plant, only WDV shall be credited i.e. Cost –

Depreciation. But if any plant is being returned or transferred at the beginning of the year then

there is no need to write down the WDV i.e. Cost – Depreciation. Mean to say that only cost of the plant

shall be credited if it’s being returned at the beginning of the year. [Sometimes the time of returning

the plant is not given in the question, in such a case you may take an assumption regarding the time.]

There is another method under which we do not record the cost on the debit side and WDV on

the credit side. In this method we only record the depreciation of the plant on the debit side. The

depreciation of all the plants (whether outgoing or balance of the plant at the end of the year) shall be

recorded on the debit side. In this method all other transactions related to the plant are not recorded

in the contract account. Even profit/loss on sales of plant or loss due to fire, rain, theft, etc. is not

recorded.

4. Sub contract cost

The contractor is not able to carry out all task related to the contract on his own. In such a case he can

give sub contract to other persons. e.g. In case of building construction the sub contract can be given

for the wiring, painting, wood work, finishing etc. Any amount incurred for the sub contract shall be

debited as it’s an expense. Apply the principle—Debit all expenses and losses.

5. Cost of extra work done

In case the contractor has carried out any extra work as per the specifications/instructions given by

the contractee then such expense shall be debited. Apply the principle—Debit all expenses and losses.

Later on contractor can recover this amount from the contractee.

6. Site expenses

Any expense incurred on the site shall also be debited. There may be too many expenses under this

head. Apply the principle—Debit all expenses and losses.

12 | P a g e

7. Direct expenses

Any expense of direct nature shall be debited. Apply the principle—Debit all expenses and losses. Any

outstanding amount shall be added and any prepaid amount shall be credited.

8. Indirect expenses

Any expense of indirect nature shall be debited. Apply the principle—Debit all expenses and losses.

Any outstanding amount shall be added and any prepaid amount shall be credited.

9. To profit and loss account (Profit on sales of material/plant)

The above incomes are abnormal in nature. Further, while preparing the contract account one must

keep in mind the principle of normality also, so all the abnormal incomes shall be excluded from the

contract account. Debit all these incomes and the journal entry would be:

Contract Account Dr. -----

To Profit and Loss Account -----

10. To Contract escalation (Decrease in CP)

Sometimes the contract is subject to the escalation/de-escalation. If due to the applicability of the

escalation/de-escalation clause there is decrease in the contract price then such amount shall be

debited to the contract account. The journal entry would be:

Contract Account Dr. -----

To Contractee a/c -----

11. To profit and loss account (if contract is completed and profit is there)

In case of completion of the contract we write down the contract price on the credit side of the

contract account and the journal entry would be:

Contractee Account Dr. -----

To Contract Account -----

Note: We do not record the Work Certified or Work Not Certified on the credit side in the year

of completion.

13 | P a g e

12. To notional profit c/d (if work certified is more than 25% of the contract price but

less than 90% of the contract price) / Profit and loss account (part of notional profit if

the contract is not completed)* / Work in progress (transferred to reserve only when

the contract is not completed) / Work in progress (In case contract is incomplete):

Work certified and Work not certified

In case the contract is incomplete then:

1. First of all write down the amount of the Work Certified and Work Not Certified under the

heading Work-in-Progress (see the format) on the credit side of the contract account (as given

in the format).

2. If debit side is more than the credit side, then loss will be there and such loss shall be credited

to the contract account. Journal entry would be:

Profit and Loss Account Dr. -----

To Contract Account -----

3. If credit side is more than the debit side, then profit is there but this total profit cannot be

assumed actual profit because the contract is incomplete. Such profit is called Notional Profit

and then bifurcated in to two parts. One part is transferred to the profit and loss account (how

much amount shall be transferred to the profit and loss account for this there are certain rules

and discuss later immediately after the format of the contract account) and the remaining is

transferred to the work in progress account (also called reserve). Why to take only a part of the

Notional Profit to the profit and loss account? It’s because of the Principle of the Conservatism

or Principle of Prudence. However, the true profit can be calculated only at the completion of

the contract. And if we calculate the profit only at the completion of the contract then for a

company engaged in the business of taking contracts, profits will be very high in the year in

which too many contracts are being completed and profits may be very low or sometime NIL in

the year in which a few contracts are being completed or no contracts are being completed.

Thus the calculation of the profit only at the time of completion of the contract puts the uneven

burden on the profit and loss account. By calculating notional profit and then bifurcation of it in

two parts puts the even burden on the profit and loss account and also helps the contractor to

follow the principle of conservatism/prudence.

Click to go to the topic.

13. CONTRACTEE ACCOUNT (by the amount of contract price on the completion of

contract)

In case of the completion of the contract we record the contract price on the credit side of the contract

account and the journal entry is:

14 | P a g e

Contractee Account Dr. -----

To Contract Account -----

Note: We do not record the Work Certified or Work Not Certified in the year of completion on

the credit side.

14. Profit and loss account (if there is loss on contract either before completion or after

completion)

In case of the completion of the contract, if the credit side is more than the debit side then profit

will be there on the contract and the journal entry would be:

Contract Account Dr. -----

To Profit and Loss Account -----

In case the contract is incomplete then:

1. First of all write down the amount of the Work Certified and Work Not Certified under the

heading Work-in-Progress (see the format) on the credit side of the contract account (as given

in the format).

2. If debit side is more than the credit side, then loss will be there and such loss shall be credited

to the contract account. Journal entry would be:

Profit and Loss Account Dr. -----

To Contract Account -----

15. Contract escalation (Increase in CP)

Sometimes the contract is subject to the escalation/de-escalation. If due to the applicability of the

escalation/de-escalation clause there is increase in the contract price then such amount shall be

credited to the contract account. The journal entry would be:

Contractee Account Dr. -----

To Contract -----

16. Profit and loss account (if contract is completed and loss is there)

1. First of all write down the amount of the Work Certified and Work Not Certified under the

heading Work-in-Progress (see the format) on the credit side of the contract account (as given

in the format).

2. If debit side is more than the credit side, then loss will be there and such loss shall be credited

to the contract account. Journal entry would be:

Profit and Loss Account Dr. -----

To Contract Account -----

15 | P a g e

17. Notional profit b/d

1. Notional profit is calculated only when the contract is incomplete. Further the value of the

work certified shall be less than ¼

th

of the contract price. Also when value of work certified is

equal to or more than 90% of the contract price or estimated cost is given in the question or in

the question it is given that the contract is near completion, calculate the notional profit and

then estimated profit shall be calculated and the appropriate amount of the estimated profit

shall be transferred to the profit and loss account using any one of the formula given below

(Click here to go to the link).

2. First of all write down the amount of the Work Certified and Work Not Certified under the

heading Work-in-Progress (see the format) on the credit side of the contract account (as given

in the format).

3. If credit side is more than the debit side, then profit is there but this total profit cannot be

assumed actual profit because the contract is incomplete. Such profit (balancing figure) is

called Notional Profit and then it’s bifurcated in two parts. One part is transferred to the profit

and loss account (how much amount shall be transferred to the profit and loss account for this

there are certain rules and discuss later immediately after the format of the contract account)

and the remaining part is transferred to the work in progress account (also called reserve).

Why to take only a part of the Notional Profit to the profit and loss account? It’s because of the

Principle of the Conservatism or Principle of Prudence. However, the true profit can be

calculated only at the completion of the contract. And if we calculate the profit only at the

completion of the contract then for a company engaged in the business of taking contracts,

profits will be very high in the year in which too many contracts are being completed and

profits may be very low or sometime NIL in the year in which a few contracts are being

completed or no contracts are being completed. Thus the calculation of the profit only at the

time of completion of the contract puts the uneven burden on the profit and loss account. By

calculating notional profit and then bifurcation of it in two parts puts the even burden on the

profit and loss account and also helps the contractor to follow the principle of

conservatism/prudence.

Note: Always calculate the notional profit as a balancing figure and the brought down it and

then bifurcate it.

16 | P a g e

* How much of the notional profit should be transferred to Profit and Loss

Account when the contract is incomplete?

(i) When the value of work certified is less than ¼

th

of the contract price:

In this case notional profit shall not be calculated and whole of the balance shall be transferred to the

Work in Progress Account (only in case the total of credit side is more than the debit side).

Profit and Loss Account = NIL

Important Note: In case total of debit side is more than the credit side then the difference shall be

transferred to the Profit and Loss account.

(ii) When value of work certified is equal to or more than ¼

th

of the contract price and

less than ½ of the contract price:

(iii) When value of work certified is equal to or more than ½ of the contract price and

less than 90% of the contract price:

(iv) When value of work certified is equal to or more than 90% of the contract price or

estimated cost is given in the question or in the question it is given that the contract is

near completion:

In this case first of all estimated profit shall be calculated and then the appropriate amount of the

estimated profit shall be transferred to the profit and loss account using any one of the formula given

below.

(v) Amount to be transferred to the work in progress account (reserve)

Amount to be transferred to the work in progress account = Notional Profit – P & L a/c

17 | P a g e

Treatment of Work in Progress in Balance Sheet

Sometimes in the question it is asked to prepare the balance sheet and to show the relevant items in it.

Then the balance sheet shall be prepared as follows:

Balance Sheet as on DD/MM/YEAR

Liabilities

Amount

Assets

Amount

Plant and machinery (Cost –

Depreciation i.e. WDV)

Material in hand

Profit on sales of material/plant

Profit on the contract (before or

after completion)

–––

–––

–––

–––

Work in Progress:

Work Certified –––

Work un–certified –––

Less: Reserve for unrealized profit –––

Less: Cash received from Contractee (–––)

Loss on sales of material/plant

Loss on the contract (before or after completion)

–––

–––

–––

If you are showing relevant items in the balance sheet then obviously total will not tally.

18 | P a g e

Day - 3

19 | P a g e

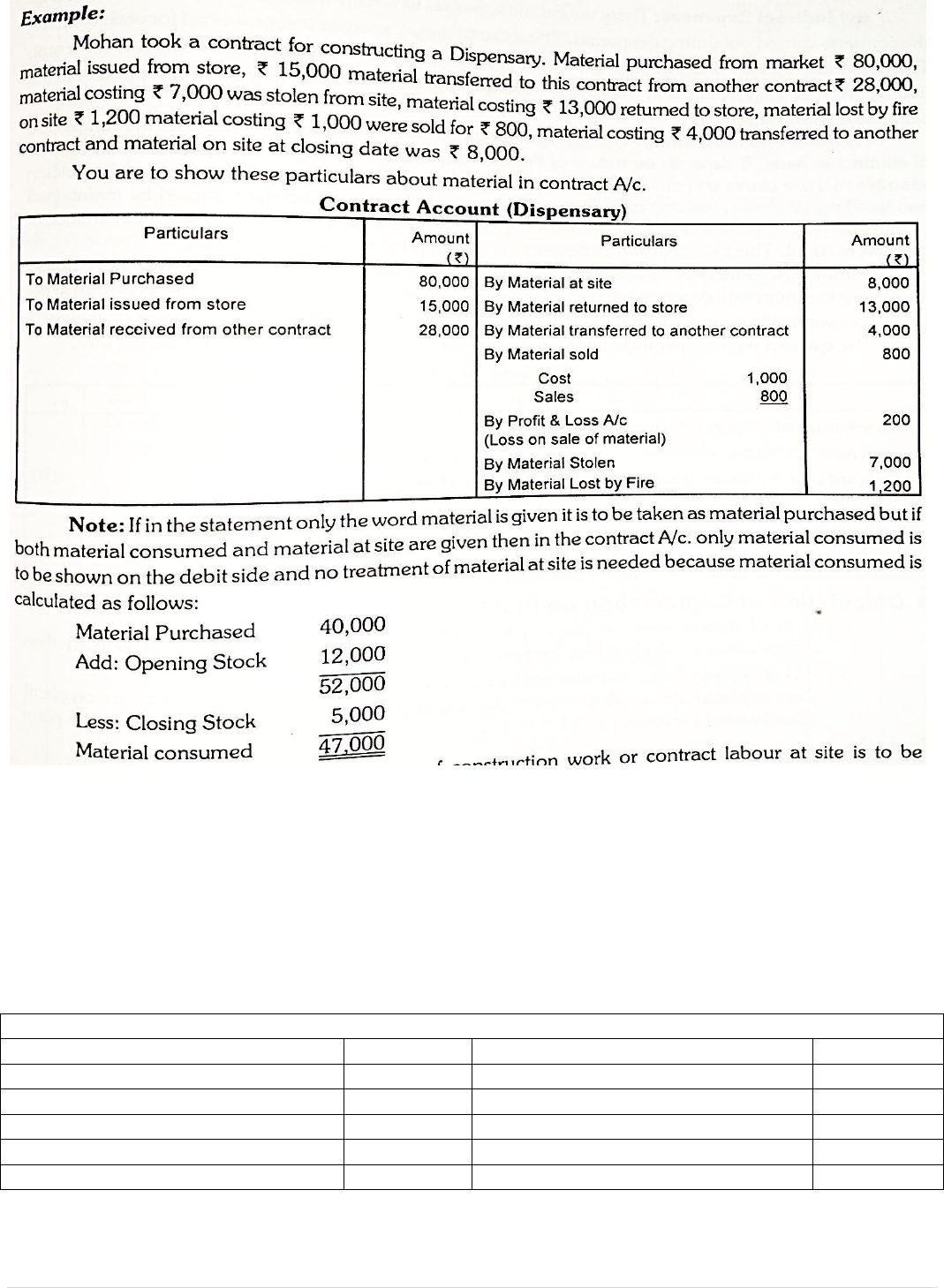

Example 1: Treatment of material

Example 2: Treatment of material

Material purchased Rs. 1,00,000; Opening material Rs. 20,000; Material at site Rs. 30,000; Material costing Rs. 10,000 was

sold for Rs. 12,000; Material costing Rs. 5,000 was sold for Rs. 3,000; Material costing Rs. 4,000 lost by fire. Show the

treatment of the material using both the methods.

Solution:

Method 1

Contract Account

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To opening material

20,000

By material at site

30,000

To material purchased

1,00,000

By material sold

12,000

To P & L a/c (profit on sales of material)

2,000

By material sold

3,000

By P & L a/c (loss on sales of material)

2,000

By P & L a/c (material lost by fire)

4,000

Note: If you calculate the balance of the above contract account then you will get Rs. 71,000 as balancing figure which is

the amount of the material consumed.

20 | P a g e

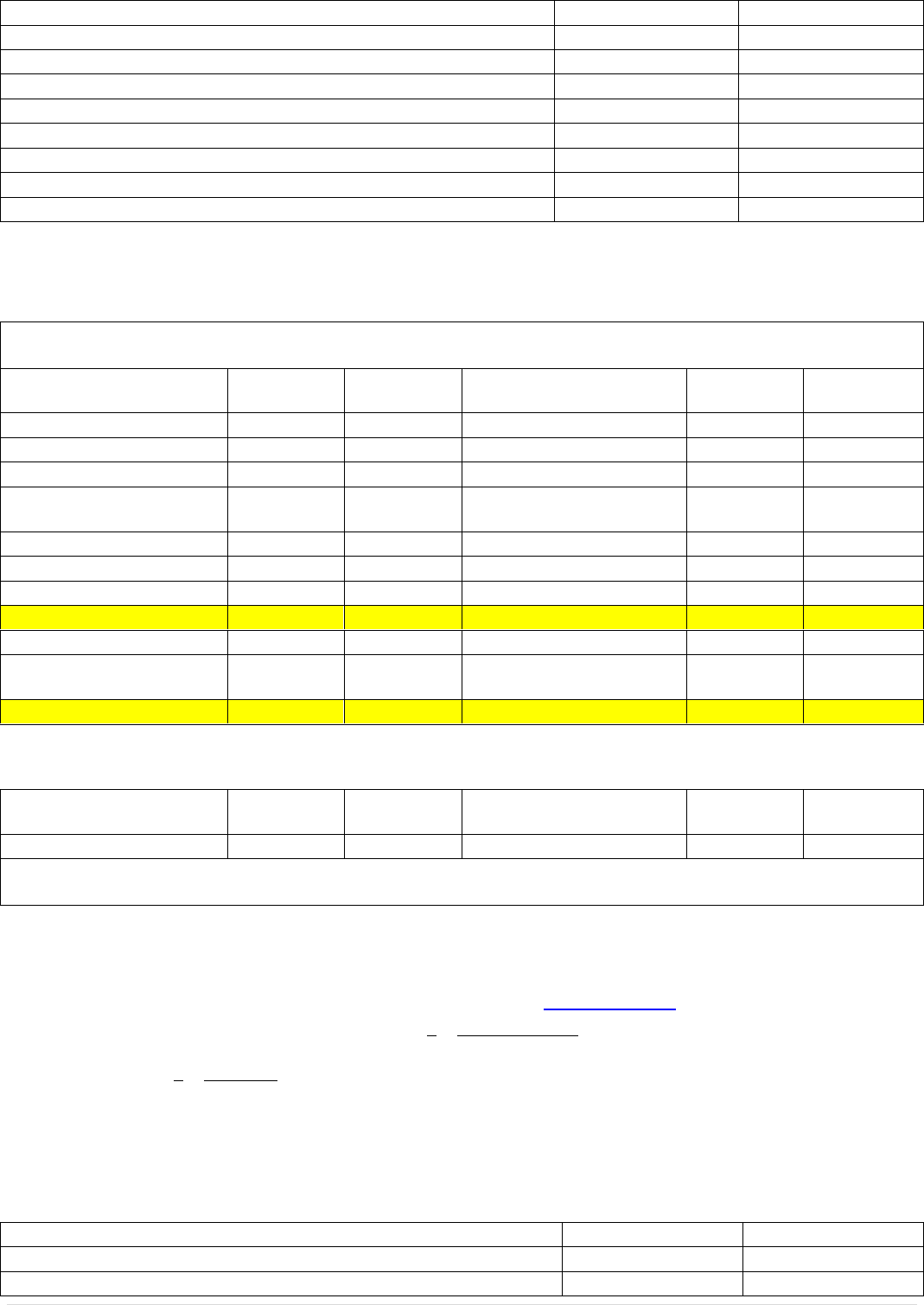

Method 2

Contract Account

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To material consumed

71,000

Material Consumed = Opening Material + Material Purchased –Material at Site – Material Sold (Cost) – Material Sold

(Cost) – Material Lost by Fire (Cost)

=1,00,000 + 20,000 – 30,000 – 10,000 – 5,000 – 4,000 = =71,000

From the above example (example 2) it’s clear that whatever method (Method 1 or Method 2) is used for the

treatment/adjustment of the material the impact/effect on the contract account is same.

Example 3: Treatment of plant & machinery

Dinesh a building contractor started a work from1st January 2010. On 1

st

March 2010 a plant costing Rs. 60,000 was

purchased for the contract. A part of the plant costing Rs. 10,000 was unsuitable and returned to store on 31

st

May 2010.

Plant costing Rs. 6,000 was stolen from the site at the beginning. Plant costing Rs. 20,000 was sold for Rs. 13,000 on 31

st

December 2010. Accounts are closed on 31

st

December every year. Charge depreciation (i) at 10% and (ii) at 10% per

annum and show the treatment in the contract account.

Solution:

Case 1: When depreciation is charged at 10%

Contract Account

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To plant

60,000

By plant returned to store:

Cost Rs. 10,000

Less: Dep. @ 10% (Rs. 1,000)

(Note – 1)

9,000

By P & L a/c (Plant stolen)

6,000

By plant sold

13,000

By P & L a/c (Loss on sales of plant) (Note

-2)

5,000

Plant at site:

Cost Rs. 24,000

Less: Dep. @ 10% (Rs. 2,400)

(Note- 3)

21,600

Note – 1: Calculation on depreciation on plant returned to store (on 31

st

may 2010)

Rs. 10,000 10 / 100 = Rs. 1,000 (Time ignored as per annum is not given with the rate)

Note – 2: Calculation of loss on sales of plant (on 31

st

December 2010)

Rs.

Cost of the plant

20,000

Less: Depreciation @ 10% (time ignored as per annum is not given with the rate)

(2,000)

Written Down Value

18,000

Less: Sales of the Plant

(13,000)

Loss on Sales

5,000

Note – 3: Calculation of plant at site (on 31

st

December 2010)

Rs.

Cost of the plant

60,000

Less: Cost of the plant returned

(10,000)

Less: Cost of the plant stolen

(6,000)

Less: Cost of the plant sold

(20,000)

Cost of the plant at site

24,000

Less: Depreciation @ 10% (time ignored as per annum is not given with the rate)

(2,400)

Value of the plant at site

21,600

21 | P a g e

The above example (Example 3 and Case – 1) can be also be solved by taking the amount of the depreciation only. In such

a case the amount of depreciation shall be debited to the contract account and all other transactions shall be ignored. Let

us calculate the amount of depreciation:

Rs.

Depreciation on plant returned (10,000 10%)

1,000

Depreciation on plant stolen (Not applicable as the plant was stolen and it is abnormal in nature)

0

Depreciation on plant sold (Rs. 20,000 10%)

2,000

Depreciation on plant at site (Rs. 24,000 10%)

2,400

Total depreciation

5,400

Note: If you calculate the balance of the above contract account then you will get Rs. 5,400 as balancing figure which is the

amount of the material consumed.

Case 2: When depreciation is charged at 10% per annum

Contract Account

Particulars

Amount

(Rs.)

Particulars

Amount

(Rs.)

To plant

60,000

By plant returned to store:

Cost Rs. 10,000

Less: Dep. @ 10% (Rs. 250) (Note – 1 )

9,750

By P & L a/c (Plant stolen)

6,000

By plant sold

13,000

By P & L a/c (Loss on sales of plant) (Note -2)

5,333

Plant at site:

Cost Rs. 24,000

Less: Dep. @ 10% (Rs. 2,000) (Note – 2)

22,000

Note – 1: Calculation on depreciation on plant returned to store on 31

st

may 2010

Rs. 10,000 10 / 100 2 Months / 12 Months = Rs. 250

Note – 2: Calculation of loss on sales of plant (on 31

st

December 2010)

Rs.

Cost of the plant

20,000

Less: Depreciation @ 10% for 10 months

(1,667)

Written Down Value

18,333

Less: Sales of the Plant

(13,000)

Loss on Sales

5,333

Note – 3: Calculation of plant at site

Rs.

Cost of the plant

60,000

Less: Cost of the plant returned

(10,000)

Less: Cost of the plant stolen

(6,000)

Less: Cost of the plant sold

(20,000)

Cost of the plant at site

24,000

Less: Depreciation @ 10% for 10 months

(2,000)

Value of the plant at site

22,000

The above example (Example 3 and Case – 2) can be also be solved by taking the amount of the depreciation only. In such

a case the amount of depreciation shall be debited to the contract account and all other transactions shall be ignored. Let

us calculate the amount of depreciation:

Rs.

Depreciation on plant returned (10,000 10% per annum 3 Months/ 12 Months )

250

Depreciation on plant stolen (Not applicable as the plant was stolen and it is abnormal in nature)

0

Depreciation on plant sold (Rs. 20,000 10% per annum 10 Months / 12 Months)

1,667

Depreciation on plant at site (Rs. 24,000 10% per annum 10 Months / 12 Months)

2,000

Total depreciation

3,917

Note: If you calculate the balance of the above contract account then you will get Rs. 3,917 as balancing figure which is the

amount of the material consumed.

22 | P a g e

Example 4

The total contract price of a contract is Rs. 20,00,000. On 31

st

march 2017, the value of work certified was Rs. 15,00,000

and the total cost incurred was Rs. 11,00,000. The value of work uncertified was Rs. 50,000. The cash received was Rs.

10,00,000. You are required to determine the amount of the profit to be taken to the P & L a/c and to the work in progress

account (reserve).

Solution:

First of all prepare the contract account and calculate the notional profit. Then using the formula used to calculate the

amount to be transferred to the profit and loss account. (Click here to see the rules for the calculation of amount to be

transferred to the P & L a/c in case of incomplete contracts). It is to be noted that always calculate the notional profit first

of all as a balancing figure and then brought it down and then bifurcate the notional profit in to parts. This is the easiest

approach.

Contract Account

For the year ending 31

st

March 2017

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

11,00,000

By work in progress:

Work certified Rs. 15,00,000

Work not certified Rs. 50,000

15,50,000

To notional profit c/d

4,50,000

Total

15,50,000

Total

15,50,000

To P & L account (Note – 1)

2,00,000

By notional profit b/d

4,50,000

To work in progress a/c (Bal. figure)

(Note – 2)

2,50,000

Total

4,50,000

Total

4,50,000

Note – 1: Percentage of the work certified to the contract price is 75% i.e. Rs. 15,00,000 / Rs. 20,00,000 100. Because the

value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

Note – 2: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 4,50,000 – Rs. 2,00,000 = Rs. 2,50,000

Example 5

The contract price is Rs. 20,00,000. On 31

st

March 2018, 90% of the work had been completed and certified by the

architects. The costs incurred up to 31

st

march, 2018 on this project amounted to Rs. 16,00,000. It was estimated that

another 80,000 would have to be incurred further to complete the project. The contractee paid 75% of the value of the

work certified. Work not certified is Rs. 1,00,000. Find out the profit to be taken to profit and loss account.

Solution:

Contract Account

For the year ending 31

st

March 2018

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

16,00,000

By work in progress:

Work certified Rs. 18,00,000

Work not certified Rs. 1,00,000

19,00,000

To notional profit c/d

3,00,000

Total

19,00,000

Total

19,00,000

To P & L account (Note – 2)

2,16,000

By notional profit b/d

3,00,000

To work in progress a/c (Bal. figure)

(Note – 3)

84,000

Total

3,00,000

Total

3,00,000

23 | P a g e

In this question it’s clearly stated that the 90% of the work has been completed and certified, so the contract is near

completion. So first of all estimate the profit as follows (Click here to see the rules for the calculation of estimated profit

and amount to be transferred to the P & L a/c in case of near completion contracts):

Note – 1: Estimated Profit = Contract Price – Estimated Cost

= Rs. 20,00,000 – (Rs. 16,00,000 already incurred + Rs. 80,000 to be incurred)

= Rs. 3,20,000

Note – 2: Profit to be taken to the P & L a/c (In case the contract is near competion):

Note – 3: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 3,00,000 – Rs. 2,16,000 = Rs. 84,000

Example 6

Following is the information related to the contract account number 101:

Contract price Rs. 6,00,000

Wages Rs. 1,64,000

General expenses Rs. 8,600

Raw materials Rs. 1,20,000

Plant Rs. 20,000

As on date, cash received was Rs. 2,40,000, being 80% of the work certified. The value of materials remaining at site was

Rs. 10,000. Depreciate plant by 10%. Prepare the contract account. (Examination Question)

Solution:

Contract Account

For the year ending 31

st

March 20xx

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To raw material

1,20,000

By work in progress:

Work certified Rs. 3,00,000

(Note – 1)

Work not certified Rs. 0

3,00,000

To wages

1,64,000

By plant at site:

Cost Rs. 20,000

Less: Depreciation (Rs. 2,000)

(Note – 2)

18,000

To general expenses

8,600

By material at site

10,000

To plant (Note – 6)

20,000

To notional profit c/d (Note – 3)

15,400

Total

3,28,000

Total

3,28,000

To P & L a/c (Note – 4)

8,213

By notional profit b/d

15,400

To work in progress a/c (Bal. figure)

(Note – 5)

7,187

Total

15,400

Total

15,400

Note – 1: Cash received is given Rs. 2,40,000 which is 80% of the work certified. So, work certified can be calculated as

follows—

Note – 2: Depreciation has been calculated at 10%. Time factor has been ignored as the per annum is not given with the

rate.

Note – 3: In this question the percentage of the work certified is 50% i.e. Work Certified/Contract Price 100 i.e. Rs.

3,00,000/Rs. 6,00,000100. Further the credit side of the contract is more than the debit side, so notional profit is there.

Then notional profit has been brought down so that it can be bifurcated in two parts.

Note – 4: Percentage of the work certified to the contract price is 50% i.e. Rs. 3,00,000 / Rs. 6,00,000 100. Because the

value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

24 | P a g e

Note – 5: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 15,400 – Rs. 8,213 = Rs. 7,187

Note – 6: Alternatively the depreciation of Rs. 2,000 can be debited and in such a case cost of the plant and the WDV of the

plant shall not be recorded in the contract account.

Example 7

How much profit will be credited to profit and loss account in the following cas:

Contract price Rs. 20,00,000

Cost incurred Rs. 11,20,000

Cash received (90% of work certified) Rs. 10,80,000

Work not certified Rs. 1,20,000 (Examination question)

Solution:

First of all prepare the contract account and calculate the notional profit. Then using the formula used to calculate the

amount to be transferred to the profit and loss account. (Click here to see the rules for the calculation of amount to be

transferred to the P & L a/c in case of incomplete contracts). It is to be noted that always calculate the notional profit first

of all as a balancing figure and then brought it down and then bifurcate the notional profit in to parts. This is the easiest

approach.

Contract Account

For the year ending 31

st

March 2017

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

11,20,000

By work in progress:

Work certified Rs. 12,00,000

(Note – 1)

Work not certified Rs. 1,20,000

13,20,000

To notional profit c/d

2,00,000

Total

13,20,000

Total

13,20,000

To P & L account (Note – 2)

1,20,000

By notional profit b/d

2,00,000

To work in progress a/c (Bal. figure)

(Note – 3)

80,000

Total

2,00,000

Total

2,00,000

Note – 1: Cash received is given Rs. 10,80,000 which is 90% of the work certified. So, work certified can be calculated as

follows—

Note – 2: Percentage of the work certified to the contract price is 60% i.e. Rs. 12,00,000 / Rs. 20,00,000 100. Because the

value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

Note – 3: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 2,00,000 – Rs. 1,20,000 = Rs. 80,000

Example 8 (Illustration Number 7.7 or 8.7 of Maheshwari-Mittal)

Modern construction limited has taken two contracts on 1

st

October 2017. The position of contracts as on 30

th

September

2018 was as follows:

Particulars

Contract – I (Rs.)

Contract – II (Rs.)

Contract price

27,00,000

60,00,000

Materials

5,80,000

10,80,000

25 | P a g e

Wages paid

11,24,000

16,50,000

Other expenses

28,000

60,000

Plant at site (Cost)

1,60,000

3,00,000

Unused material at site

40,000

60,000

Wages payable (outstanding)

36,000

54,000

Other expenses due (outstanding)

4,000

9,000

Work certified

16,00,000

30,00,000

Cash received

12,00,000

22,50,000

Work completed but not yet certified

80,000

90,000

The plant at site is to be depreciated at 10%. Prepare the contract account in respect of each contract showing the notional

profit and also the profit to be transferred to P & L a/c.

Solution

Contract Account

For the year ending on 30

th

September 2018

Particulars

Contract – I

(Rs.)

Contract – II

(Rs.)

Particulars

Contract – I

(Rs.)

Contract – II

(Rs.)

Materials

5,80,000

10,80,000

By work in progress:

Wages paid

11,24,000

16,50,000

Work certified

16,00,000

30,00,000

Wages payable

36,000

54,000

Work not certified

80,000

90,000

Depreciation on plant (Note

– 1)

16,000

30,000

By material at site

40,000

60,000

Other expenses

28,000

60,000

By P & L a/c (Note – 2)

68,000

Other expenses due

4,000

9,000

To notional profit c/d

2,67,000

Total

17,88,000

31,50,000

Total

17,88,000

31,50,000

To P & L a/c (Note – 3)

1,33,500

By notional profit b/d

2,67,000

To work in progress (Note

– 4)

1,33,500

Total

2,67,000

Total

2,67,000

Note – 1: The depreciation has been calculated at 10%. Time factor has been ignored as per annum is not given with the

rate. Further, we have debited the depreciation only and not the cost and WDV of the plant. Alternatively the cost of the

plant can be debited to the contract account and the WDV can be credited as follows:

Particulars

Contract – I

(Rs.)

Contract – II

(Rs.)

Particulars

Contract – I

(Rs.)

Contract – II

(Rs.)

To plant

1,60,000

3,00,000

By plant at site (WDV)

1,44,000

2,7,000

Plant at site for contract – I: Cost – Depreciation @ 10% = Rs. 1,60,000 – 16,000 = Rs. 1,44,000

Plant at site for contract – II: Cost – Depreciation @ 10% = Rs. 3,00,000 – 30,000 = Rs. 2,70,000

Note-2: In case of contract – I the debit side is more than the credit side so loss is there and such loss shall be transferred

to the P & L a/c.

Note – 3: Percentage of the work certified to the contract price is 59.26% i.e. Rs. 16,00,000 / Rs. 27,00,000 100. Because

the value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

Note – 4: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 2,67,000 – Rs. 1,33,500 = Rs. 1,33,500

Example 9 (When the work certified is less than ¼

th

of the contract price)

Particulars

Case – 1 (Rs.)

Case – 2 (Rs.)

Contract price

10,00,000

10,00,000

Work certified

2,40,000

2,40,000

26 | P a g e

Work not certified

10,000

10,000

Cost incurred

2,00,000

2,60,000

Solution:

Case – 1 (When the credit side is more than the debit side)

Contract Account

For the year ending 31

st

March 20xx

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

2,00,000

By work in progress:

Work certified Rs. 2,40,000

Work not certified Rs. 10,000

2,50,000

To work in progress a/c (Note)

50,000

Total

2,50,000

Total

2,50,000

Note: In this case the work certified is 24% of the contract price, so, it’s less than ¼

th

of the contract price. In this case

notional profit shall not be calculated and whole of the balance shall be transferred to the Work in Progress Account (only

in case the total of credit side is more than the debit side).

Case – 2 (When the debit side is more than the credit side)

Contract Account

For the year ending 31

st

March 20xx

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

2,60,000

By work in progress:

Work certified Rs. 2,40,000

Work not certified Rs. 10,000

2,50,000

By P & L a/c (Note)

10,000

Total

2,60,000

Total

2,60,000

Note: In this case the work certified is 24% of the contract price, so, it’s less than ¼

th

of the contract price. In this case the

debit side is more than credit side, so loss is there and it shall be transferred to the P & L a/c.

Example 10

Prepare the contract account with the help of following:

Direct material Rs. 28,000

Wages Rs. 22,000

Special plant Rs. 18,000

Stores issued Rs. 9,000

Loose tools Rs. 2,500

Cost of tractor used Rs. 1,20,000

Fuel for tractor Rs. 4,000

Wages of tractor driver Rs. 8,000

The contract was completed in 26 weeks at the end of which plant was returned subject to a depreciation of 20% on the

original cost. The value of loose tools and stores returned were Rs. 500 and Rs. 1,000 respectively. The tractor is subject

to a depreciation of 20% per annum. Provide office overheads at 10% of the works/facotry cost. The contract was agreed

to be performed at a profit of 25% of the total cost.

Solution:

In this some important points are there which are:

1. It’s a cost plus contract. So the contract price shall be calculated by adding the profit of 25% to the total cost.

2. Tractor shall be treated like plant. Either the cost can be debited and WDV can be credited or only the amount of

the depreciation can be debited. Further, the expenses of the tractor like fuel and driver’s wages shall also be

debited.

3. (This contract is completed) In this question office overheads are 10% of the works/factory cost. How can the

works/factory cost be calculated? It’s very easy. First of all prepare the contract account as usual but do not

credit the amount of the contract price. Now calculate the balance of the contract account (debit side will

27 | P a g e

be more than the credit side). This balance is the works/factory cost. Then brought down this balance and

calculate the office overheads at 10% of the works/factory cost. Debit these office overheads and calculate

the total cost. Brought down this total cost and calculate profit at 25% on total cost. Debit this profit. Now

you will get a balancing figure on the credit side which is the contract price.

4. (In case of incomplete contracts) First of all prepare the contract account as usual but do not credit the work

certified and work not certified. Now calculate the balance of the contract account (debit side will be more

than the credit side). This balance is the works/factory cost. Then brought down this balance and

calculate the office overheads at 10% of the works/factory cost. Debit these office overheads and credit

the work certified and work not certified (if these are given). If credit side is more than the debit side then

notional profit is there and then it should be bifurcated in two parts as usual. Transfer one part to the P &

L a/c using the formulae discussed earlier and transfer the balance to the work in progress a/c. But if the

debit side is more than the credit side then there is loss and such loss shall be transferred to the P & L a/c.

Contract Account

For the year ending ……………

Particulars

Amount

(Rs.)

Particulars

Amount

(Rs.)

To direct material

28,000

By plant returned:

Cost Rs. 18,000

Less: Depreciation (Rs. 3,600) (Note – 1)

14,400

To wages

22,000

By stores returned (WDV given)

500

To special plant

18,000

By loose tools returned (WDV given)

1,000

To stores issued

9,000

By tractor returned:

Cost Rs. 1,20,000

Less: Depreciation (Rs. 12,000) (Note – 2)

1,08,000

To loose tools

2,500

To cost of tractor

1,20,000

To fuel for tractor

4,000

Wages of tractor driver

8,000

By works/factory cost c/d

87,600

Total

2,11,50

0

Total

2,11,500

To works/factory cost b/d

87,600

To office overheads (Note – 3)

8,760

By total cost c/d

96,360

Total

96,360

Total

96,360

To total cost b/d

96,360

By contractee account (Balancing figure) (Note – 5)

1,20,450

To profit (Note – 4)

24,090

Total

1,20,45

0

Total

1,20,450

Note – 1: Depreciation on special plant shall be calculated at 20% (ignoring the time factor as per annum is not given with

the rate). Depreciation would be Rs. 3,600 (Rs. 18,000 20 / 100).

Note – 2: depreciation on tractor has been calculated for 26 weeks (on the basis of time as the per annum is given with the

rate). Depreciation would be Rs. 12,000 (Rs. 1,20,000 20 / 100 26 Weeks / 52 Weeks).

Note – 3: Office overheads are 10% of the works cost so the amount would be Rs. 8,760 (Rs. 87,600 i.e. works cost 10 /

100).

Note – 4: Profit is 25% on cost so the amount would be Rs. 24,090 (Rs. 1,20,450 i.e. Total cost 25 / 100).

Note – 5: As this is a cost plus contract. So the contract price has been calculated by adding the profit of 25% to the total

cost (or the balancing figure is the contract price).

28 | P a g e

Day - 4

29 | P a g e

Example 11 (Illustration 7.9 or 8.9 of Maheshwari Mittal)

The Hindutan Construction Company Limited has undertaken the construction of a bridge over the river Yamuna for a

municipal corporation. The value of the contract is Rs. 12,50,000 subject to a retention 0f 20% until one year after the

certified completion of the contract, and final approval of the corporation’s engineer. The following are the details as

shown in the bookson3oth June 2000:

Labour on site Rs. 4,05,000

Material direct to site less returns Rs. 4,20,000

Material received from stores Rs. 81,200

Hire and use of plant – plant upkeep account Rs. 12,100

Direct expenses Rs. 23,000

General overheads allocated to the contract Rs. 37,100

Material in hand on 30

th

June 2000 Rs. 6,300

Wages accrued/outstanding on 30

th

June 2000 Rs. 7,800

Direct expenses accrued/outstanding on 30

th

June 2000 Rs. 1,600

Work not yet certified by the Corporation Engineer Rs. 16,500

Amount certified by the Corporation Engineer Rs. 11,00,000

Cash received on account Rs. 8,80,000

Prepare (a) Contract account; (b) Contractee’s account; and (c) how the relevant items would appear in the Balance Sheet.

Solution:

Contract Account

For the year ending 30

th

June March 2000

Particulars

Amount

(Rs.)

Particulars

Amount (Rs.)

To labour on site Rs. 4,05,000

Add: Outstanding Rs. 7,800

4,12,800

By material in hand

6,300

To material direct to site less returns

4,20000

By work in progress: (Note – 5)

Work certified Rs. 11,00,000

Work not certified Rs. 16,500

11,16,500

To material received from store

81,200

To hire and use of plant – plant upkeep account

12,100

To direct expenses Rs. 23,000

Add: Outstanding Rs. 1,600

24,600

To general overhead allocated to the Contract

37,100

To notional profit c/d (Note – 1)

1,35,000

Total

11,22,8

00

Total

11,22,800

To P & L a/c (Note – 2)

72,000

By notional profit b/d

1,35,000

To work in progress account (Note – 3 and 6)

63,000

Total

1,35,00

0

Total

1,35,000

Contractee Account

For the year ending 30

th

June March 2000

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To balance c/d

8,80,000

By cash account (Note – 4)

8,80,000

Total

8,8,0000

Total

8,80,000

Work in progress Account

For the year ending 30

th

June March 2000

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To contract account (Note – 5)

Work certified Rs. 11,00,000

Work not certified Rs. 16,500

11,16,500

By contract account (transfer to reserve)

(Note – 6)

63,000

By balance c/d

10,53,500

30 | P a g e

Total

11,16,500

Total

11,16,500

Balance sheet as on 30

th

June March 2000

Liabilities

Amount (Rs.)

Assets

Amount (Rs.)

Wages accrued

7,800

Work in progress: (Note – 7)

Work certified Rs. 11,00,000

Add: work not certified Rs. 16,500

Rs. 11,16,500

Less: Transfer to reserve (Rs. 63,000)

Rs. 10,53,500

Less: Cash received (Rs. 8,80,000)

(Note – 8)

1,73,500

Direct expenses accrued

1,600

Material in hand

6,300

Profit and loss a/c

72,000

Total

-NA-

Total

-NA-

Note – 1: The percentage of the work certified to the contract price is 88% and the credit side of the contract side is more

than the debit side so notional profit is there.

Note – 2: Percentage of the work certified to the contract price is 58% i.e. Rs. 11,00,000 / Rs. 12,50,000 100. Because the

value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

Note – 3: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 1,35,000 – Rs. 72,000 = Rs. 63,000

Note – 4: Cash received from the contractree is 80% of the work certified, so it would be Rs. 11,00,000 80 / 100 = Rs.

8,80,000 (it’s already given in the question). Journal entry to receive cash is

Cash a/c Dr. Rs. 8,80,000

To Contractee a/c Rs. 8,80,000

(Being cash received from the contractee)

We have just posted this journal entry in the contractee account. After posting the journal entry calculate the balance of

the contractee account whoch would be Rs. 8,80,000.

Note – 5: The journal entry for the recording of the work in progress account (work certified + work not certified) is:

Work in progress a/c Dr. Rs. 11,16,500

To Contract a/c Rs. 11,16,500

(Being work in progress transferred to the contract account)

Now post this entry in to the contract and work in progress account.

Note – 6: The amount we transfer to the reserve (work in progress account), the journal entry for that is:

To Contract a/c Rs. 63,000

Work in progress a/c Dr. Rs. 63,000

(Being part of the notional profit transferred to the reserve/work in progress account)

Now post this entry in to the contract and work in progress account. Then calculate the balance of the work in progress

account which would be Rs. 10,53,600.

Note – 7: We can also show the balance of the work in progress in the balance sheet as follows:

Balance sheet as on 30

th

June March 2000

Liabilities

Amount (Rs.)

Assets

Amount (Rs.)

Work in progress Rs. 10,53,500

Less: Cash received (Rs. 8,80,000)

1,73,500

Total

-NA-

Total

-NA-

Note – 8: This is the balance of the contractee account. Alternatively this can be shown on the liabilities side.

31 | P a g e

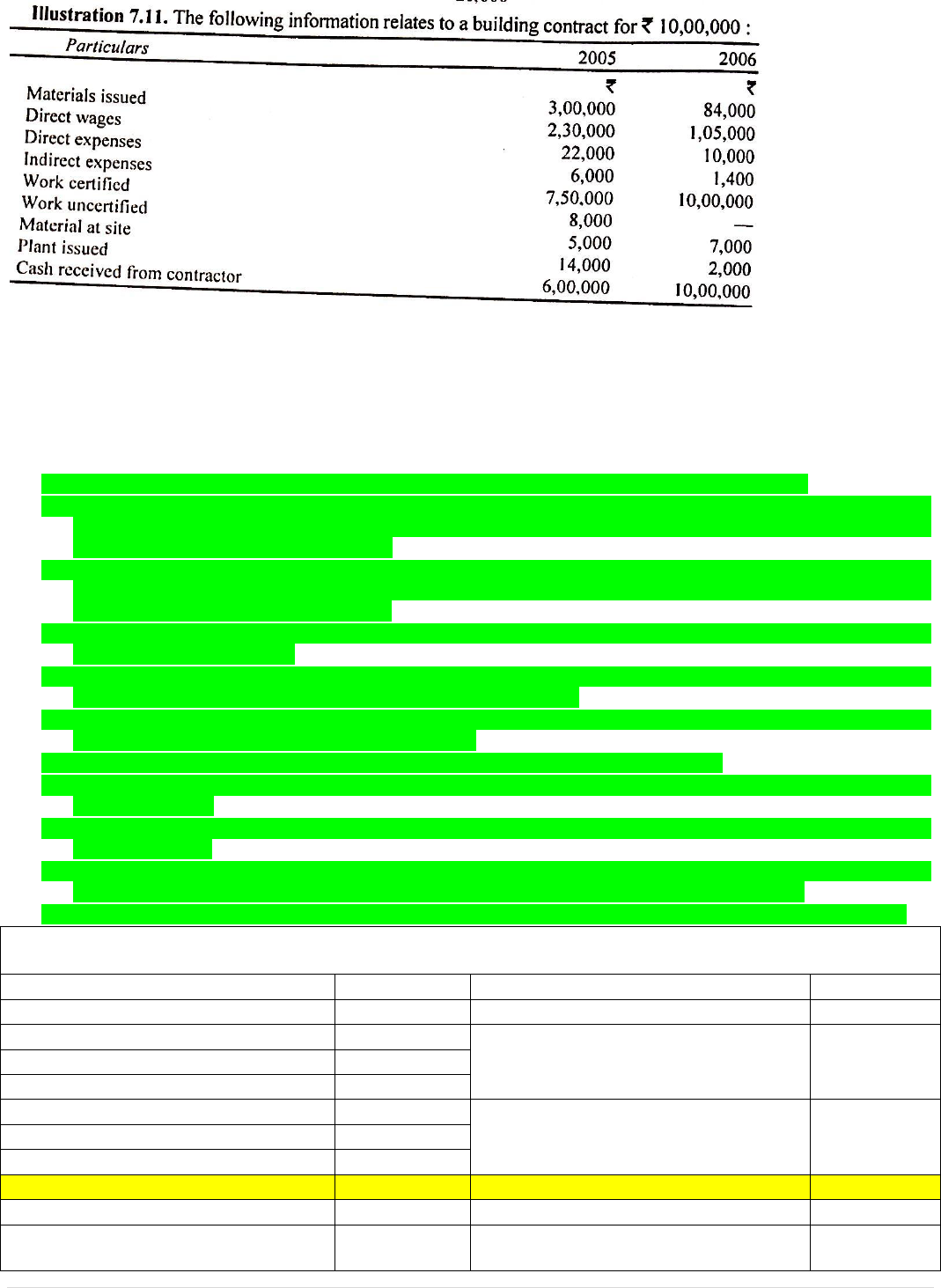

Example 12 (Illustration Number 7.11 or 8.11 of Maheshwari Mittal)

The value of plant at the end of 2005 and 2006 was Rs. 7,000 and Rs. 5,000 respectively. prepare (i) Contract Account, (ii)

Contractee Account for two years 2005 and 2006 taking into consideration such profit for transfer to Profit and Loss

Account as you think proper.

Solution:

When the contract account is to be prepared for more than one year then some important points are to be kept in mind in

such questions which are:

1. Prepare the contract account, work in progress account and the contractee account for every year.

2. The work in progress of 1

st

year shall be transferred to the debit side of the 2

nd

year’s contract account on the first

day of the 2

nd

year. (This process is called passing of the reversing journal as no balance of the work in progress is

maintained on the first day of the 2

nd

year)

3. The work in progress of 2

nd

year shall be transferred to the debit side of the 3

rd

year’s contract account on the first

day of the 3

rd

year. (This process is called passing of the reversing journal as no balance of the work in progress is

maintained on the first day of the 3

rd

year)

4. In the last year i.e. year of completion, there will be no work in progress. In this year we credit the contract

account by the contract price.

5. The plant at site, material at site and prepaid expenses at site at the end of the 1

st

year shall be debited to the 2

nd

year’s contract account at their WDV on the first day of the 2

nd

year.

6. The plant at site, material at site and prepaid expenses at site at the end of the 1

st

year shall be debited to the 3

rd

year’s contract account on the first day of the 3

rd

year.

7. In the last year all unused material and remaining plant shall be returned to the stores.

8. Any outstanding expense at the end of the 1

st

year shall be credited to the 2

nd

year’s contract account on the first

day of the 2

nd

year.

9. Any outstanding expense at the end of the 2

nd

year shall be credited to the 3

rd

year’s contract account on the first

day of the 3

rd

year.

10. Every year (except last year) notional profit shall be calculated and shall be bifurcated in two parts. One part is

transferred to the P & L a/c and remaining portion is transferred to the work in progress account.

11. In the year of completion there will be no notional profit. Any profit or loss shall be transferred to the P & L a/c.

Contract Account

For the year ending 31

st

December2005

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To material issued

3,00,000

By material at site

5,000

To direct wages

2,30,000

By work in progress: (1)

Work certified Rs. 7,50,000

Work not certified Rs. 8,000

7,58,000

To direct expenses

22,000

To indirect expenses

6,000

To plant issued

14,000

By plant at site:

Cost Rs. 14,000

Less: Depreciation (Rs. 7,000)

7,000

To notional profit c/d

1,98,000

Total

7,70,000

Total

7,70,000

To P & L a/c (2) (Note – 1)

1,05,600

By notional profit b/d

1,98,000

To work in progress account (3) (Note –

2)

92,400

32 | P a g e

Total

1,98,000

Total

1,98,000

Contract Account

For the year ending 31

st

December 2006

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To work in progress account (5)

6,65,600

By material at site

7,000

To material at site b/d

5,000

By plant at site:

Cost Rs. 7,000 + Rs. 2,000

Less: Dep. (Rs.4,000)

5,000

To plant at site b/d

7,000

To material issues

84,000

To direct wages

1,05,000

By contractee account (6)

10,00,000

To direct expenses

10,000

To indirect expenses

1,400

To plant issued

2,000

To P & L a/c (7)

1,32,000

Total

10,12,000

Total

10,12,000

Work in progress account

Date

Particulars

Amount

(Rs.)

Date

Particulars

Amount

(Rs.)

31-

12-

2005

To contract account (1)

31-

12-

2005

By contract account (Reserve) (3)

92,400

(Work certified + Work not

certified)

7,58,000

31-

12-

2005

By balance c/d

6,65,600

Total

7,58,000

Total

7,58,000

01-

01-

2006

To balance b/d

6,65,600

01-

01-

2006

By contract account (5)

6,65,600

Total

6,65,600

Total

6,65,600

Contractee account

Date

Particulars

Amount

(Rs.)

Date

Particulars

Amount

(Rs.)

31-

12-

2005

To balance c/d

6,00,000

31-

12-

2005

By cash account (4)

6,00,000

Total

6,00,000

Total

6,00,000

31-

12-

2006

To contract account (6)

10,00,000

01-

01-

2006

To balance b/d

6,00,000

31-

12-

2006

By cash account (Balancing figure) (8)

4,00,000

Total

10,00,000

Total

10,00,000

Journal entries for Work in progress, profit and loss, and cash received from the contractee, etc.

Sr.

No.

Date

Particulars

L.

F.

Amount

(Rs.)

Amount

(Rs.)

1

31-12-2005

Work in progress a/c Dr.

To Contract a/c

7,58,000

7,58,000

Narration: Being work in progress transferred to the contract account.

2

31-12-2005

Contract a/c Dr.

To P & L a/c

1,05,600

1,05,600

Narration: Being notional profit transferred to the profit and loss

account.

33 | P a g e

3

31-12-2005

Contract a/c Dr.

To Work in progress a/c

92,400

92,400

Narration: Being part of notional profit transferred to reserve (work in

progress account)

4

31-12-2005

Cash a/c Dr.

To Contractee a/c

6,00,000

6,00,000

Narration: Being cash received from the contractee.

5

01-01-2006

Contract a/c Dr.

To work in progress a/c

6,65,600

6,65,600

Narration: Being reversing journal passed or Being work in progress on

31

st

December 2005 transferred to the contract account on 1

st

January

2006.

6

31-12-2006

Contractee a/c Dr.

To Contract a/c

10,00,00

0

10,00,00

0

Narration: Being contract completed or Being the contract price

receivable from the contractee.

7

31-12-2006

Contract a/c Dr.

To P & L a/c

1,32,000

1,32,000

Narration: Profit on completion of contract transferred to the profit

and loss account.

8

31-12-2006

Cash a/c Dr.

To Contracteen a/c

4,00,000

4,00,000

Narration: Being the balance amount received from the contractee.

Post all the above entries in the concerned accounts. In case you are not able to understand any posting in any

account then please refer to the above journal entries.

Note – 1: Percentage of the work certified to the contract price is 75% i.e. Rs. 7,50,000 / Rs. 10,00,000 100. Because the

value of work certified is equal to or more than ½ of the contract price but less than 90% of the contract price so profit

(which is to be transferred to the P & L a/c) shall be calculated using the following formula:

Note – 2: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 1,98,0000 – Rs. 1,05,600 = Rs. 92,400

34 | P a g e

Example 13 (Illustration Number 7.12 or 8.12 of Maheshwari Mittal)

Illustration 7.12 or 8.12. Mr. Richardson undertook a contract for Rs. 75,00,000 on an arrangement that 80% of the value

of the work done, as certified by the architects of the contractee should be paid immediately, and the remaining 20% to be

retained until the contract was completed.

In 2004, the amounts expended were: Materials, Rs. 9,60,000, Wages Rs. 8,50,000, Carriage Rs. 30,000, cartage Rs. 5,000,

Sundry Expenses Rs. 35,000. The work certified for Rs. 18,75000 and 80% was paid as agreed.

In 2005, the amounts expended were: Material Rs. 11,00,000, Wages Rs. 11,50,000, Carriage Rs. 1,15,000, Cartage Rs.

10,000, Sundry Expenses Rs. 20,000. Three-fourth of the contract was certified as done by 31

st

December and 80% of this

was received accordingly. The value of the unused stock and work-in-progress uncertified was ascertained at Rs. 1,00,000.

In 2006, the amounts expended were: Materials Rs. 6,30,000, Wages Rs. 8,50,000, Cartage Rs. 30,000, Sundry Expenses Rs.

15,000. The whole contract was completed on 30

th

June.

Show how the contract account, work-in-progress account and the contractee’s account would appear in each of these

years in the books of the contractor assuming that balance due to him was received on completion of the contract. Also

show the relevant items in the Balance Sheet.

Solution:

Self

35 | P a g e

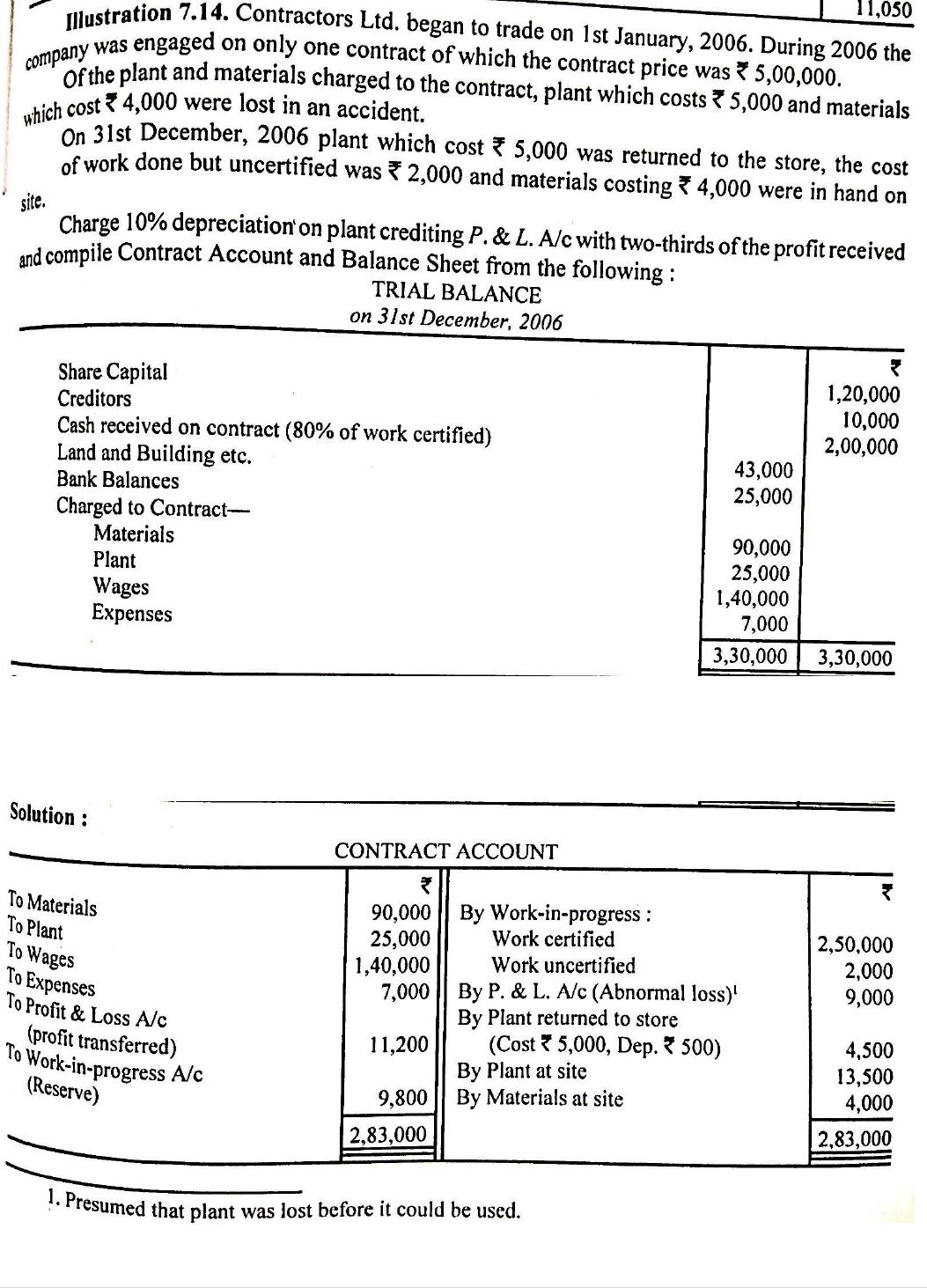

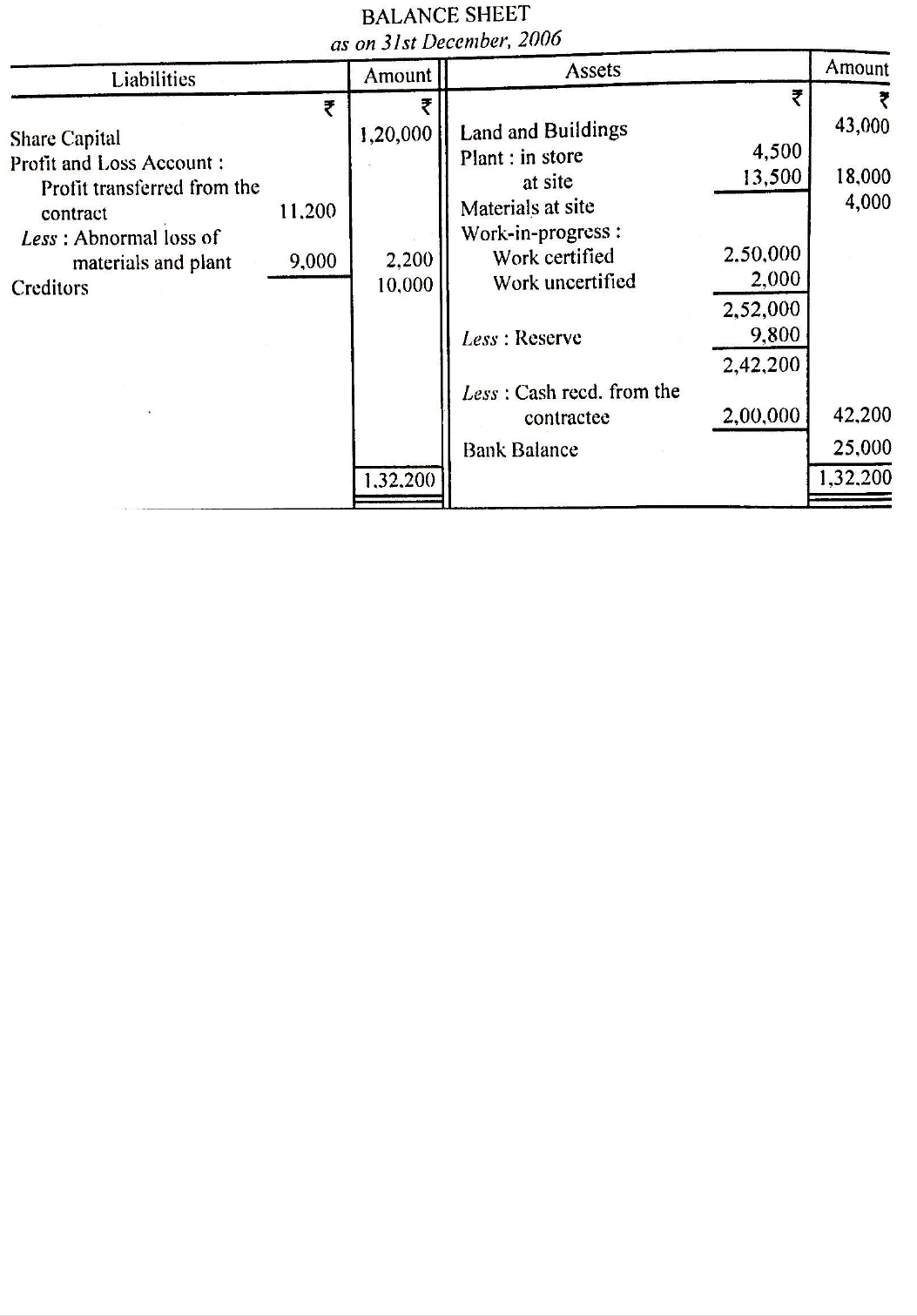

Example 14 (Illustration Number 7.14 or 8.14 of Maheshwari Mittal)

Solution:

When in the question Share capital, other liabilities, cash, etc. are given then total of the balance sheet will match. The only

issue in this question is the preparation of the balance sheet.

36 | P a g e

37 | P a g e

Example 15 (Illustration Number 7.15 or 8.15 of Maheshwari Mittal)

38 | P a g e

Solution:

In this question share capital, other liabilities, cash, etc. are given so the total of the balance sheet will match. The only

issue in this question is the preparation of the balance sheet

39 | P a g e

Example 16

40 | P a g e

Solution:

41 | P a g e

42 | P a g e

43 | P a g e

Example 17

44 | P a g e

Solution:

45 | P a g e

Example 18

46 | P a g e

Solution:

47 | P a g e

Day - 5

48 | P a g e

Example 19 (Illustration Number 7.5 or 8.5 of Maheshwari Mittal)

Contract price is Rs. 50,000. ¾

th

of the work has been approved by the contrractee. The costs incurred so far for contract A

are Rs. 25,000. It is estimated that Rs. 5,000 will be required further to complete the contract. The contractee pays 80% of

the work certified by him. Calculate the figure of profit which you consider reasonable to be taken to the credit of the profit

and loss account.

Solution:

Contract Account

For the year ending ……………

Particulars

Amount (Rs.)

Particulars

Amount (Rs.)

To cost incurred

25,000

By work in progress:

Work certified Rs. 37,500

Work not certified Rs. 0

37,500

To notional profit c/d

12,500

Total

37,500

Total

37,500

To P & L account (Note – 1)

12,000

By notional profit b/d

12,500

To work in progress a/c (Bal. figure)

(Note – 5)

500

Total

4,50,000

Total

4,50,000

Note – 1: Percentage of the work certified to the contract price is ¾

th

. Because the value of work certified is equal to or

more than ½ of the contract price but less than 90% of the contract price so profit (which is to be transferred to the P & L

a/c) shall be calculated using the following formula:

But in this question estimated cost is given though the work certified is not equal to or more than 90% of the contract

price, so profit shall be estimated and the appropriate formula shall be used to calculate the amount which is to be

transferred to the profit and loss account (click here to see the rule).

Note – 2: Estimated Profit = Contract Price – Estimated Cost

= Rs. 50,000 – (Rs. 25,000 already incurred + Rs. 5,000 to be incurred)

= Rs. 20,000

Note – 3: Cash Received =

Note – 4: Work Certified =

Note – 5: Amount which is to be transferred to the work in progress account:

= Notional Profit – Amount transferred to the P & L a/c

= Rs. 12,500 – Rs. 12,000 = Rs. 500

49 | P a g e

Example 20 (Illustration Number 7.6 or 8.6 of Maheshwari Mittal)

Utkal Construction Limited took a contract in 2012 for road construction. The contract orice was Rs. 10,00,000 and it is

estimated that the cost of completion would be Rs. 9,20,000. At the end of 2012, the company has received Rs. 3,60,000

representing 90% of work certified. Work not yet certified was Rs. 10,000.

Expenditure incurred on the contract during 2012 was as follows:

Materials Rs. 50,000; Labour Rs. 3,00,000; Plant Rs. 20,000.

Materials costing Rs. 5,000 were damaged and had to be disposed off for Rs. 1,000. Plant is considered as having

depreciated by 25%.